“Customer perception about private banks ” Under the supervision of: Submitted by: - Dr. Raghuvir Singh Anuja Agarwal (Director, CIPS) (PGDM-II Sem.) Submitted to: Centurion Institute of Professional Studies, Sector-18, Kumbha marg, Pratap Nagar Jaipur 10, May,2010 ACADEMIC SESSION 2008-10

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

“Customer perception about private banks ”

Under the supervision of: Submitted by: -

Dr. Raghuvir Singh Anuja Agarwal(Director, CIPS) (PGDM-II Sem.)

Submitted to:

Centurion Institute of Professional Studies,Sector-18, Kumbha marg, Pratap Nagar Jaipur

10, May,2010

ACADEMIC SESSION 2008-10

PREFACE

The MBA curriculum is designed in such a way that student can grasp maximum

knowledge and can get practical exposure to the corporate world in minimum possible time.

Business schools of today realize the importance of practical knowledge over the theoretical

base.

The research report is necessary for the partial fulfillment of MBA curriculum and it

provides an opportunity to the researcher in understanding the industry with special emphasis

on the development of skills in analyzing and interpreting practical problems through the

application of management theories and techniques. It is a new platform of learning through

practical experience, which incorporates survey and comparative analysis. It gives the learner

an opportunity to relate the theory with the practice, to test the validity and applicability of

his classroom learning against real life business situations.

The researcher has conducted a research on “Customer perception about private banks”

ACKNOWLEDGEMENT

The research work requires co-operation of many people and this work is no

exception. It is difficult to thank individually all the persons who patronized this work. The

researcher had asked for favors, borrowed ideas, expressions and facts from so many that it

would require one volume to give credit to all. So, the researcher wants to thank all the

patrons of this report

First and foremost, we would like to express our sincere and profound gratitude to

Mrs. Babita Jha (Faculty member of Centurion Institute of Professional Studies, Jaipur),

whose guidance has given a proper shape to this project. This is because of her attitude

towards excellence, and helping nature has been source of constant inspiration. Her

unhitching support during our work is very admirable. She is the true driving force behind

this work throughout, constantly encouraging us to do our best and inspiring us to aim higher.

We will be failing in our duty, if we do not express our thanks to our Parents and

family members for generating Confidence in us right from the commencement of this task to

its accomplishment.

We want to thank our friends who extended their cooperation and were patient at all

stages of our work.

Last but not the least, we are thankful to all respondents, who gave us their precious time and

support to fulfill this task, without their co-operation the study would not have seen the light

of the day.

10, May, 2010 Anuja agrawal

EXECUTIVE SUMMARY.This Project is totally focused on finance of Mutual FundsThis project is made on the topic of Identify and analyze the factors which affects the customer for investing in Reliance mutual funds at the city of Jaipur. This project is totally focused on consumer’s opinion about the investment in mutual funds in the Reliance. For defining the research problem clearly firstly I decided to conduct research in the Reliance mutual funds.For sampling I use Non-Probability sampling technique in which I use Convenience Sampling Method as I did not have sufficient time, money and could not have put lot of efforts sample consist who generally invest in the reliance mutual funds in the city of Jaipur. . Sample is of size of 100. Interrogation through personal interview has been use as a data collection technique and questionnaire is data collection instrument, which is close-ended, after getting these filled form respondents.

CONTENTS

Serial No. Description Page No.

Chapter 1 INTRODUCTION 6-7

Chapter 2 PROFILE OF HDFC 8-9

Chapter 3 PROMOTERS IN HDFC 10-17 Awards Board committee

Chapter 4 Research methodology 18 4.1 Research problem and title of the study 4.2 Objective of the study 4.3 Variables 4.4 Research Design 4.5 Sample Design 4.6 Sample size 4.7 Data collection method 4.8 Data collection instrument Chapter 5 Data tabulation ,analysis and findings. 19-33

Chapter 6 Conclusion 34

Chapter 7 RECOMMENDATIONS 35

Chapter 8 Limitations 36

Chapter 9 Bibliography 37 ANNEXURE-1 Qusetionnaire 38-40

Chapter -1 Introduction

Housing Development Finance Corporation Limited, more popularly known as HDFC Bank Ltd, was established in the year 1994, as a part of the liberalization of the Indian Banking Industry by Reserve Bank of India (RBI). It was one of the first banks to receive an 'in principle' approval from RBI, for setting up a bank in the private sector. The bank was incorporated with the name 'HDFC Bank Limited', with its registered office in Mumbai. The following year, it started its operations as a Scheduled Commercial Bank. Today, the bank boasts of as many as 1412 branches and over 3275 ATMs across India.

AmalgamationsIn 2002, HDFC Bank witnessed its merger with Times Bank Limited (a private sector bank promoted by Bennett, Coleman & Co. / Times Group). With this, HDFC and Times became the first two private banks in the New Generation Private Sector Banks to have gone through a merger. In 2008, RBI approved the amalgamation of Centurion Bank of Punjab with HDFC Bank. With this, the Deposits of the merged entity became Rs. 1,22,000 crore, while the Advances were Rs. 89,000 crore and Balance Sheet size was Rs. 1,63,000 crore.

Tech-SavvyHDFC Bank has always prided itself on a highly automated environment, be it in terms of information technology or communication systems. All the braches of the bank boast of online connectivity with the other, ensuring speedy funds transfer for the clients. At the same time, the bank's branch network and Automated Teller Machines (ATMs) allow multi-branch access to retail clients. The bank makes use of its up-to-date technology, along with market position and expertise, to create a competitive advantage and build market share.

Capital StructureAt present, HDFC Bank boasts of an authorized capital of Rs 550 crore (Rs5.5 billion), of this the paid-up amount is Rs 424.6 crore (Rs.4.2 billion). In terms of equity share, the HDFC Group holds 19.4%. Foreign Institutional Investors (FIIs) have around 28% of the equity and about 17.6% is held by the ADS Depository (in respect of the bank's American Depository Shares (ADS) Issue). The bank has about 570,000 shareholders. Its shares find a listing on the Stock Exchange, Mumbai and National Stock Exchange, while its American Depository Shares are listed on the New York Stock Exchange (NYSE), under the symbol 'HDB'.

Products & Services

Personal Banking

Savings Accounts Salary Accounts Current Accounts

Fixed Deposits Demat Account Safe Deposit Lockers Loans Credit Cards Debit Cards Prepaid Cards Investments & Insurance Forex Services Payment Services Net Banking Insta Alerts Mobile Banking Insta Query ATM Phone Banking

NRI Banking

Rupee Savings Accounts Rupee Current Accounts Rupee Fixed Deposits Foreign Currency Deposits Accounts for Returning Indians Quick remit (North America, UK, Europe, Southeast Asia) India Link (Middle East, Africa) Cheque LockBox Telegraphic / Wire Transfer Funds Transfer through Cheques / DDs / TCs Mutual Funds Private Banking Portfolio Investment Schemes Loans Payment Services Net Banking Insta Alerts Mobile Banking Insta Query ATM Phone Banking

Chapter-2

HDFC Bank Limited - Company Profile Snapshot

SUPPLEMENTARY ANALYSES REPORTS

FINANCIAL STATEMENT ANALYSIS

FINANCIAL RATIO ANALYSIS

WRIGHT QUALITY ANALYSIS ... and more!

Company Profile:

HDFC Bank Limited

Ticker: 500180Exchanges: OTH BOM2009 Sales: 197,740,000,000

Major Industry: FinancialSub Industry: Commercial

BanksCountry: INDIA

Employees: 37836

Business Description

HDFC Bank Limited. The Group's principal activities are to provide banking and other financial services. The Group operates through four segments: Treasury, Retail Banking, Wholesale Banking and Other Banking Business. The Treasury Services segment consists of net interest earnings on investments portfolio of the bank and gains or losses on investment operations. The Retail Banking segment serves retail customers through a branch network and other delivery channels. This segment raises deposits from customers and makes loans and provides advisory services to customers. The Wholesale Banking segment provides loans and transaction services to corporate and institutional customers. The Other Banking Operations segment provides services relating to credit cards, debit

cards, third party product distribution and primary dealership business and other associated costs.

Chapter 3 Promoter in HDFCHDFC is India's premier housing finance company and enjoys an impeccable track record in India as well as in international markets. Since its inception in 1977, the Corporation has maintained a consistent and healthy growth in its operations to remain the market leader in mortgages. Its outstanding loan portfolio covers well over a million dwelling units. HDFC has developed significant expertise in retail mortgage loans to different market segments and also has a large corporate client base for its housing related credit facilities. With its experience in the financial markets, a strong market reputation, large shareholder base and unique consumer franchise, HDFC was ideally positioned to promote a bank in the Indian environment.

Business focusHDFC Bank's mission is to be a World-Class Indian Bank. The objective is to build sound customer franchises across distinct businesses so as to be the preferred provider of banking services for target retail and wholesale customer segments, and to achieve healthy growth in profitability, consistent with the bank's risk appetite. The bank is committed to maintain the highest level of ethical standards, professional integrity, corporate governance and regulatory compliance. HDFC Bank's business philosophy is based on four core values - Operational Excellence, Customer Focus, Product Leadership and People.

Capital StructureAs on 31st March, 2009 the authorised share capital of HDFC Bank is Rs. 550 crore. The paid-up capital as on the said date is Rs. 425,38,41,090/- ( 42,53,84,109 equity shares of Rs 10/- each). The HDFC Group holds 19.38% of the Bank's equity and about 17.70 % of the equity is held by the ADS Depository (in respect of the bank's American Depository Shares (ADS) Issue). 27.69 % of the equity is held by Foreign Institutional Investors (FIIs) and the Bank has about 5,48,774 shareholders.The shares are listed on the Bombay Stock Exchange Limited and The National Stock Exchange of India Limited. The Bank's American Depository Shares ( ADS ) are listed on the New York Stock Exchange (NYSE) under the symbol 'HDB' and the Bank's Global Depository Receipts (GDRs) are listed on Luxembourg Stock Exchange under ISIN No US40415F2002.

Mr. Jagdish Capoor took over as the bank's Chairman in July 2001. Prior to this, Mr. Capoor was a Deputy Governor of the Reserve Bank of India.The Managing Director, Mr. Aditya Puri, has been a professional banker for over 25 years, and before joining HDFC Bank in 1994 was heading Citibank's operations in Malaysia.The Bank's Board of Directors is composed of eminent individuals with a wealth of experience in public policy, administration, industry and commercial banking. Senior executives representing HDFC are also on the Board. Senior banking professionals with substantial experience in India and abroad head various businesses and functions and report to the Managing Director. Given the professional expertise of the management team and the overall focus on recruiting and retaining the best talent in the industry, the bank believes that its people are a significant competitive strength.

Rating

Credit Rating

The Bank has its deposit programs rated by two rating agencies - Credit Analysis & Research Limited (CARE) and Fitch Ratings India Private Limited. The Bank's Fixed Deposit programme has been rated 'CARE AAA (FD)' [Triple A] by CARE, which represents instruments considered to be "of the best quality, carrying negligible investment risk". CARE has also rated the bank's Certificate of Deposit (CD) programme "PR 1+" which represents "superior capacity for repayment of short term promissory obligations". Fitch Ratings India Pvt. Ltd. (100% subsidiary of Fitch Inc.) has assigned the "AAA ( ind )" rating to the Bank's deposit programme, with the outlook on the rating as "stable". This rating indicates "highest credit quality" where "protection factors are very high"The Bank also has its long term unsecured, subordinated (Tier II) Bonds rated by CARE and Fitch Ratings India Private Limited and its Tier I perpetual Bonds and Upper Tier II Bonds rated by CARE and CRISIL Ltd. CARE has assigned the rating of "CARE AAA" for the subordinated Tier II Bonds while Fitch Ratings India Pvt. Ltd. has assigned the rating "AAA (ind)" with the outlook on the rating as "stable". CARE has also assigned "CARE AAA [Triple A]" for the Banks Perpetual bond and Upper Tier II bond issues. CRISIL has assigned the rating "AAA / Stable" for the Bank's Perpetual Debt programme and Upper Tier II Bond issue. In each of the cases referred to above, the ratings awarded were the highest assigned by the rating agency for those instruments.

Corporate Governance RatingThe bank was one of the first four companies, which subjected itself to a Corporate Governance and Value Creation (GVC) rating by the rating agency, The Credit Rating Information Services of India Limited (CRISIL). The rating provides an independent assessment of an entity's current performance and an expectation on its "balanced value creation and corporate governance practices" in future. The bank has been assigned a 'CRISIL GVC Level 1' rating which indicates that the bank's capability with respect to wealth creation for all itsstakeholders while adopting sound corporate governance practices is the highest.

Awards and Achievements - Banking ServicesIt is extremely gratifying that our efforts towards providing customer convenience have been appreciated both nationally and internationally.

Asian Banker Excellence in Retail Financial Services

'Asian Banker Best Retail Bank in India Award 2009 '

2009

Finance Asia Country Awards for Achievement 2008

'Best Bank and Best Cash Management Bank'

CNN-IBN 'Indian of the Year (Business)'

Nasscom IT User Award 2008

'Best IT Adoption in the Banking Sector'

Business India 'Best Bank 2008'

Forbes Asia Fab 50 companies in Asia Pacific

Asian Banker Excellence in Retail Financial Services

Best Retail Bank 2008

Asiamoney Best local Cash Management Bank Award voted by Corporates

Microsoft & Indian Express Group

Security Strategist Award 2008

World Trade Center Award of honour

For outstanding contribution to international trade services.

Business Today-Monitor Group survey

One of India's "Most Innovative Companies"

HDFC Bank began operations in 1995 with a simple mission: to be a "World-class Indian Bank". We realised that only a single-minded focus on product quality and service excellence would help us get there. Today, we are proud to say that we are well on our way towards that goal.

2008

Financial Express-Ernst & Young Award

Best Bank Award in the Private Sector category

Global HR Excellence Awards - Asia Pacific HRM Congress:

'Employer Brand of the Year 2007 -2008' Award - First Runner up, & many more

Business Today 'Best Bank' Award

Dun & Bradstreet – American Express Corporate Best Bank A

Dun & Bradstreet – American Express Corporate Best Bank Award 2007

'Corporate Best Bank' Award

The Bombay Stock Exchange and Nasscom Foundation's Business for Social Responsibility Awards 2007

'Best Corporate Social Responsibility Practice' Award

Outlook Money & NDTV Profit

Best Bank Award in the Private sector category.

The Asian Banker Excellence in Retail Financial Services Awards

Best Retail Bank in India

Asian Banker Our Managing Director Aditya Puri wins the Leadership

'Corporate Best Bank' Award

2007

Achievement Award for India

We are aware that all these awards are mere milestones in the continuing, never-ending journey of providing excellent service to our customers. We are confident, however, that with your feedback and support, we will be able to maintain and improve our services

ward 2007

The Board's Committees are as follows:

Audit and Compliance Committee

Compensation Committee

Investors' Grievance (SHARE) Committee

Risk Monitoring Committee

Credit Approval Committee

The Premises Committee

Nomination Committee

Fraud Monitoring Committee

Customer Service Committee

Audit and Compliance Committee

The Audit and Compliance Committee of the Bank is chaired by Mr. Arvind Pande. The other members of the Committee are Mr. Ashim Samanta, Mr. C. M. Vasudev, Mr. Gautam Divan and Dr. Pandit Palande. Dr. Pandit Palande was inducted as member of the Committee w.e.f. May 17, 2007. All the members of the Committee are independent directors and Mr. Gautam Divan is a financial expert.

The Committee met 7 (seven) times during the year.

The terms of reference of the Audit Committee are in accordance with Clause 49 of the Listing Agreement entered into with the Stock Exchanges in India, and inter alia include the following:

Overseeing the Bank's financial reporting process and ensuring correct, adequate

and credible disclosure of financial information.

Recommending appointment and removal of external auditors and fixing of their fees.

Reviewing with management the annual financial statements before submission to the Board with special emphasis on accounting policies and practices, compliance with accounting standards and other legal requirements concerning financial statements.

Reviewing the adequacy of the Audit and Compliance functions, including their policies, procedures, techniques and other regulatory requirements, and

Any other terms of reference as may be included from time to time in clause 49 of the listing agreement.

The Board has also adopted a charter for the audit committee in connection with certain United States regulatory standards as the Bank's securities are also listed on New York Stock Exchange.

Compensation Committee

The Compensation Committee reviews the overall compensation structure and policies of the Bank with a view to attract, retain and motivate employees, consider grant of stock options to employees, reviewing compensation levels of the Bank's employees vis-à-vis other banks and industry in general.

The Bank's compensation policy is to provide a fair and consistent basis for motivating and rewarding employees appropriately according to their job / role size, performance, contribution, skill and competence.

Mr. Jagdish Capoor, Mr. Ashim Samanta, Mr. Gautam Divan and Dr. Pandit Palande are the members of the Committee. Dr. Pandit Palande was inducted as member of the Committee w.e.f. May 17, 2007. The Committee is chaired by Mr. Jagdish Capoor. All members of the Committee other than Mr. Capoor are independent directors.The Committee met 3 (three) times during the year.

Investors' Grievance (SHARE) Committee

The Committee approves and monitors transfer, transmission, splitting and consolidation of shares and bonds and allotment of shares to the employees pursuant to Employees Stock Option Scheme. The Committee also monitors redressal of complaints from shareholders relating to transfer of shares, non-receipt of Annual Report, dividends etc.

The Committee consists of Mr. Jagdish Capoor, Mr. Aditya Puri and Mr. Gautam Divan. The Committee is chaired by Mr. Capoor. The Committee met 11 times during the year. The powers to approve share transfers and dematerialisation requests

have been delegated to executives of the Bank to avoid delays that may arise due to non-availability of the members of the Committee.

As on March 31, 2008, 43 instruments of transfer representing 3871 shares were pending and since then the same have been processed. The details of the transfers are reported to the Board of Directors from time to time.During the year, the Bank received 142 complaints from shareholders, which have been attended to.The Committee met 11 (eleven) times during the year.

Risk Monitoring Committee

The committee has been formed as per the guidelines of Reserve Bank of India on the Asset Liability Management / Risk Management Systems. The Committee develops Bank's credit and market risk policies and procedures, verify adherence to various risk parameters and prudential limits for treasury operations and reviews its risk monitoring system. The committee also ensures that the Bank's credit exposure to any one group or industry does not exceed the internally set limits and that the risk is prudentially diversified.

The Committee consists of Mrs. Renu Karnad, Mr. Aditya Puri and Mr. C. M. Vasudev and is chaired by Mrs. Renu Karnad.

The Committee met 5 (five) times during the year.

Credit Approval Committee

The Credit Approval Committee approves credit exposures, which are beyond the powers delegated to executives of the Bank. This facilitates quick response to the needs of the customers and speedy disbursement of loans. The Committee consists of Mr. Jagdish Capoor, Mr. Aditya Puri, Mr. Keki Mistry and Mr. Gautam Divan. The Committee is chaired by Mr. Capoor.

The Committee met 2 (two) times during the year.

The Premises Committee

The Premises Committee approves purchases and leasing of premises for the use of Bank's branches, back offices, ATMs and residence of executives in accordance with the guidelines laid down by the Board. The committee consists of Mr. Aditya Puri, Mr. Ashim Samanta, Mrs. Renu Karnad and Dr. Pandit Palande. Dr. Pandit Palande was inducted as member of the Committee w.e.f. May 17, 2007. The Committee is chaired by Mrs. Renu Karnad.

The Committee met 4 (four) times during the year.

Nomination Committee

The Bank has constituted a Nomination Committee for recommending the appointment of independent / non-executive directors on the Board of the Bank. The Nomination Committee scrutinises the nominations for independent / non-executive

directors with reference to their qualifications and experience. For identifying ‘fit and proper' persons, the Committee adopts the following criteria to assess competency of the persons nominated:

Academic qualifications, previous experience, track record, and

Integrity of the candidates.

For assessing the integrity and suitability, features like criminal records, financial position, civil actions undertaken to pursue personal debts, refusal of admission to and expulsion from professional bodies, sanctions applied by regulators or similar bodies and previous questionable business practice are considered.

The members of the Committee are Mr. Arvind Pande, Mr. Ashim Samanta and Dr. Pandit Palande. Dr. Pandit Palande was inducted as member of the Committee w.e.f. May 17, 2007. The Committee is chaired by Mr. Arvind Pande. All the members of the Committee are independent directors. The Committee met 2 (two) times during the year.

Fraud Monitoring Committee

Pursuant to the directions of the Reserve Bank of India, the Bank has constituted a Fraud Monitoring Committee, exclusively dedicated to the monitoring and following up of cases of fraud amounting to Rs.1 crore and above. The objective of this Committee is the effective detection of frauds and immediate reporting thereof to regulatory and enforcement agencies and actions taken against the perpetrators of frauds.

The terms of reference of the Committee are as under:

Identify the systemic lacunae, if any, that facilitated perpetration of the fraud and put in place measures to plug the same.

Identify the reasons for delay in detection, if any, reporting to top management of the Bank and RBI.

Monitor progress of CBI / police investigation and recovery position.

Ensure that staff accountability is examined at all levels in all the cases of frauds and staff side action, if required, is completed quickly without loss of time.

Review the efficacy of the remedial action taken to prevent recurrence of frauds, such as strengthening of internal controls.

Put in place other measures as may be considered relevant to strengthen preventive measures against frauds.

The members of the Committee are Mr. Jagdish Capoor, Mr. Aditya Puri, Mr. Keki Mistry and Mr. Arvind Pande. The Committee is chaired by Mr. Jagdish Capoor. The Committee met 4 (four) times during the year.

Customer Service Committee

The Committee monitors the quality of services rendered to the customers and also ensures implementation of directives received from RBI in this regard. The terms of reference of the Committee are to formulate comprehensive deposit policy incorporating the issues arising out of death of a depositor for operations of his account, the product approval process, the annual survey of depositor satisfaction and the triennial audit of such services. The members of the Committee are Mr. Keki Mistry, Mr. Arvind Pande and Dr. Pandit Palande. Dr. Pandit Palande was inducted as member of the Committee w.e.f. May 17, 2007. The Committee met 4 (four) times during the year.

The Housing Development Finance Corporation Limited (HDFC) was amongst the first to receive an 'in principle' approval from the Reserve Bank of India (RBI) to set up a bank in the private sector, as part of the RBI's liberalisation of the Indian Banking Industry in 1994. The bank was incorporated in August 1994 in the name of 'HDFC Bank Limited', with its registered office in Mumbai, India. HDFC Bank commenced operations as a Scheduled Commercial Bank in January 1995.

Chapter - 4 RESEARCH METHODOLOGY

Research Problem- Identify and analyze the factors which affects the private sector banks .

BROAD AREA: - Finance

Interest Of Area:- HDFC Bank

Objective of the study

To determine the factors which affects private banks. To analyze the factors which affects private sector banks.

Variables Interest Rates New Scheme Lowest account limit Available Loan types Availability of insurance policies Customer Services Credit Card Facility

Research Design

Descriptive(find the associate relationship between variables ) Population:-“ Bank customer accounts"

Sample Design

Non probability with convenience

Sample Size

o 100

Data Collection Method

Interrogation through personal interview.

Data Collection instrument

Questionnaire

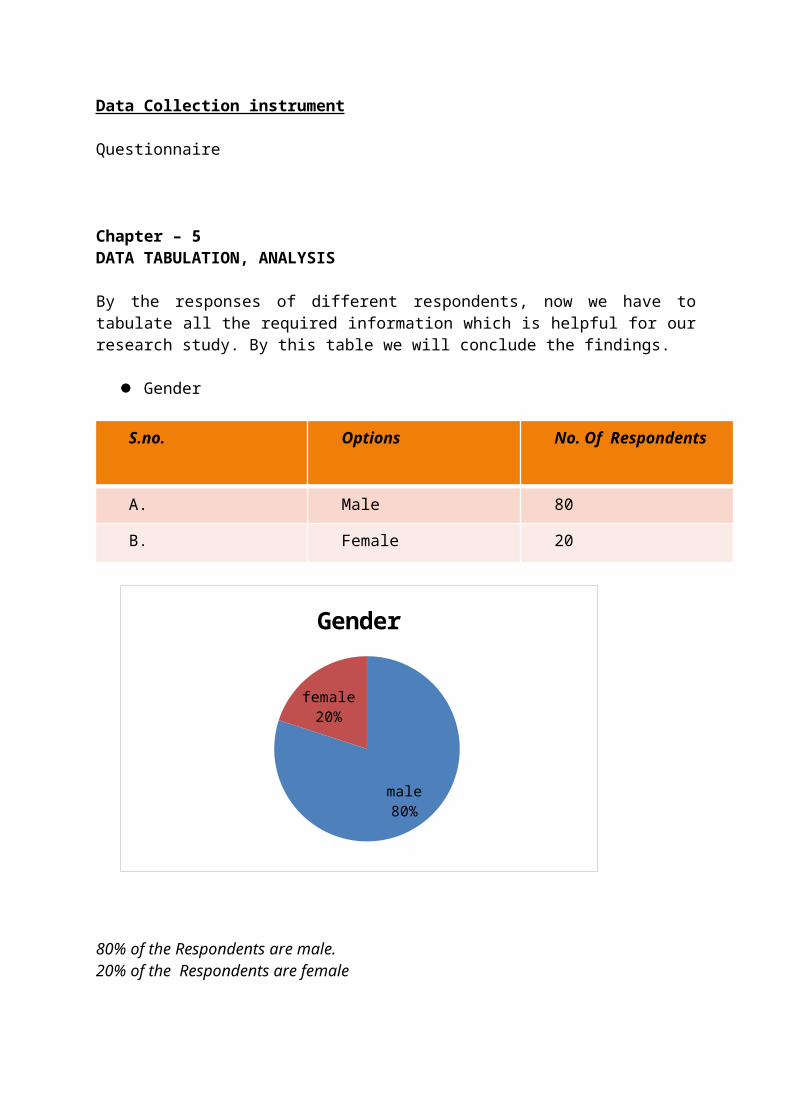

Chapter – 5DATA TABULATION, ANALYSIS

By the responses of different respondents, now we have to tabulate all the required information which is helpful for our research study. By this table we will conclude the findings.

Gender

S.no. Options No. Of Respondents

A. Male 80

B. Female 20

male80%

female20%

Gender

80% of the Respondents are male.20% of the Respondents are female

.

Age . S.no. Options No. Of Respondents

A. Below 20 None

B. 20-30 28

C. 30- 40 42

D. Above 40 30

20-30 28%

30-4042%

above 4030%

None

There are no respondents below 20 years. No. of respondents are 28% under 20-30 years. No. of respondents are 42% under the age of 30-40 years. No. of respondents are 30% above 40 years

Annual Income

S.No Options No. Of Respondents

A. Below 2 lac 39

B. 4-6 lac 15

C. 2-4 lac 21

D. Above 6 25

Below 2 lac39%

4-6 lac15%

2-4 lac21%

Above 6 25%

Annual Income

No. of respondents whose annual income is below Rs. 2 lac is 39% No. of respondents whose annual income is Rs. 4-6 lac is 15% No. of respondents whose annual income is Rs.2- 4 lac is 21% No. of respondents whose annual income is above Rs. 6 lac is 25%

Do you have account in bank?

S.no. Options No. of responedents

A.B.

YesNo

7525

75%

25%

Do you have account in bankYes No

There are 75% of respondents who comes under the category of yes There are 25% of respondents who come under the category of no.

Are this account is beneficial?

S.No. Options No. of respondents

A. Yes 85

B. No 15

Yes85%

No15%

Are this account is benefical

85% respondents are there who come under the category of yes.

!5% respondents are there who come under the category of no.

If yes then what are the reasons?

S.NO. Options No. of respondents

A. Less interest rate None

B. Customer service 72

C. New schemes 12

D. Others 16

Customer 72%

New schems12%

Others16%

none

There are no respondents under the category of less interest rate.72% respondents are come under the category of customer services.12% respondents are come under the category of new schemes.16% respondents are come under the category of others.

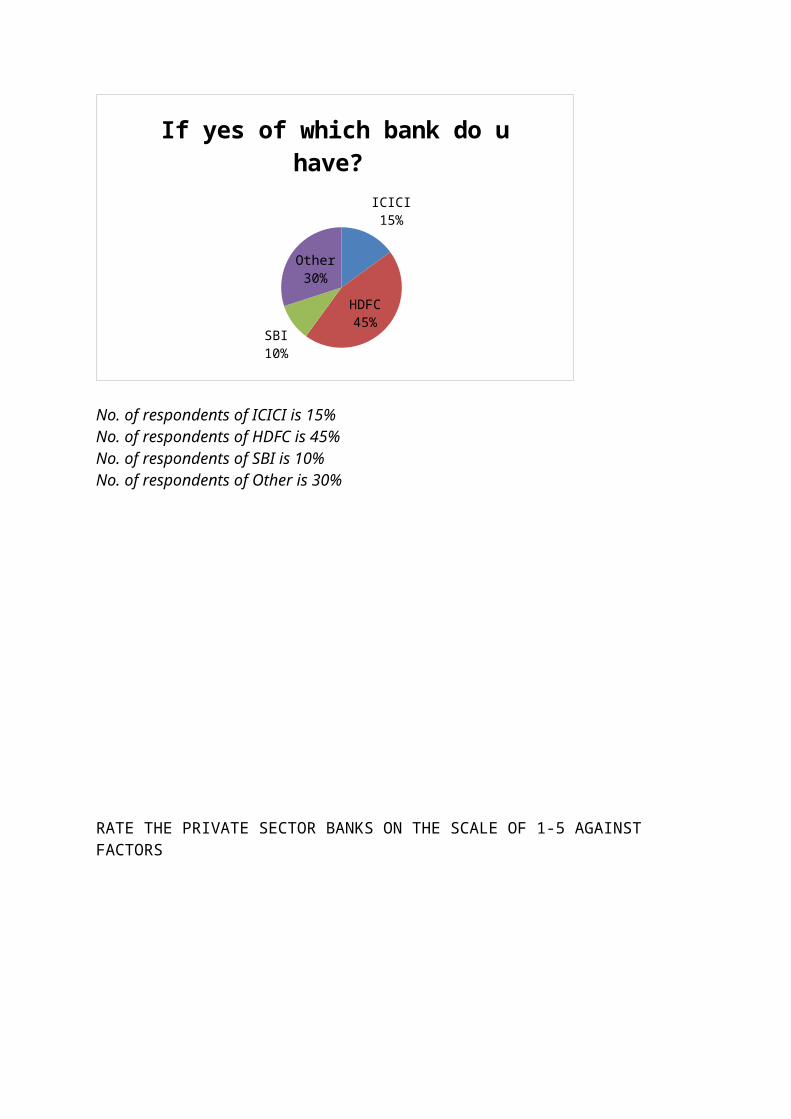

If yes of which bank do you have?

S.no. Options No. of respondents

A. ICICI 15

B. HDFC 45

CD.

SBIOther

1030

ICICI15%

HDFC45%

SBI10%

Other30%

If yes of which bank do u have?

No. of respondents of ICICI is 15%No. of respondents of HDFC is 45%No. of respondents of SBI is 10%No. of respondents of Other is 30%

RATE THE PRIVATE SECTOR BANKS ON THE SCALE OF 1-5 AGAINST FACTORS

MOST INFLUENTIAL

VERY INFLUENTIAL

INFLUENTIAL

LEAST INFLUENTIAL

NOT INFLUENTIAL

INTERST RATE

7 8 15 12 3

16%

18%

33%

27%

7%

INTERST RATE

MOST INFLUENTIAL VERY INFLUENTIAL INFLUENTIAL LEAST INFLUENTIAL NOT INFLUENTIAL

Interpretation:- 15% of the respondents say that interest rate is most influential. 18% of the respondents say that interest rate is very influential. 33% of the respondents say that interest rate is influential. 27% of the respondents say that interest rate is least influential. 7% of the respondents say that interest rate is not influential.

New schemes MOST

INFLUENTIAL

VERY INFLUENTIAL

INFLUENTIAL

LEAST INFLUENTIAL

NOT INFLUENTIAL

NEW SCHEMES

12 7 10 11 5

27%

16%

22%

24%

11%

NEW SCHEMES

MOST INFLUENTIAL VERY INFLUENTIAL INFLUENTIAL LEAST INFLUENTIAL NOT INFLUENTIAL

Interpretation:-27% of respondents say that new schemes is most influential.16% of the respondents say that new schemes is very influential. Most of the people say that still it is not good as well as influential.

MOST INFLUENTIAL

VERY INFLUENTIAL

INFLUENTIAL

LEAST INFLUENTIAL

NOT INFLUENTIAL

LOWEST ACCOUNT LIMIT

13 6 11 10 5

29%

13%

24%

22%

11%

LOWEST ACCOUNT LIMIT

MOST INFLUENTIAL VERY INFLUENTIAL INFLUENTIAL LEAST INFLUENTIAL NOT INFLUENTIAL

Interpretation:- 29% respondents say that this facility is mostly satisfying.13% respondents say that this facility is very satisfying. But the others respondents say that it influential but not so much Influential ,it may be lesser than others.

MOST INFLUENTIAL

VERY INFLUENTIAL

INFLUENTIAL

LEAST INFLUENTIAL

NOT INFLUENTIAL

AVAILABLE LOAN TYPE

7 5 9 11 13

16%

11%

20%24%

29%

AVAILABLE LOAN TYPE

MOST INFLUENTIAL VERY INFLUENTIAL INFLUENTIAL LEAST INFLUENTIAL NOT INFLUENTIAL

Interpretation:-

16% of the respondents say that available loan type is mostly influential. Mostly other respondents say that it is not so much influential as other compared to other variables, but other also is least n influential.

MOST INFLUENTIAL

VERY INFLUENTIAL

INFLUENTIAL

LEAST INFLUENTIAL

AVAILABILITY OF INSURANCE POLICIES

5 7 9 11

11%

16%

20%24%

29%

AVAILABILITY OF INSURANCE POLICIES

MOST INFLUENTIAL VERY INFLUENTIAL INFLUENTIAL LEAST INFLUENTIAL NOT INFLUENTIAL

Interpretation:- 11% of the respondents say that availability of insurance policies is most influential. 16% of the respondents say that availability of insurance policies is very influential.20% of the respondents say that availability of insurance policies is influential.24% of the respondents say that availability of insurance policies is least influential.29% of the respondents say that availability of insurance policies is not influential.

Customer Services

MOST INFLUENTIAL

VERY INFLUENTIAL

INFLUENTIAL

LEAST INFLUENTIAL

NOT INFLUENTIAL

CUSTOMER SERVICES

9 11 13 7 5

20%

24%

29%

16%

11%

CUSTOMER SERVICES

MOST INFLUENTIAL VERY INFLUENTIAL INFLUENTIAL LEAST INFLUENTIAL NOT INFLUENTIAL

Interpretation:- 20% of the respondents feels that customer services is most influential.But the 29% of the respondents says that customer services is influential but it is low in case of not influential.

MOST INFLUENTIAL

VERY INFLUENTIAL

INFLUENTIAL

LEAST INFLUENTIAL

NOT INFLUENTIAL

CREDIT CARD FACILITY

7 9 5 11 13

16%

20%

11%24%

29%

CREDIT CARD FACILITY

MOST INFLUENTIAL VERY INFLUENTIAL INFLUENTIAL LEAST INFLUENTIAL NOT INFLUENTIAL

Interpretation16% of the respondents say that credit card facility is most influential.20% of the respondents say that credit card facility is very influential.11%of the respondents say that credit card facility is influential.24% of the respondents say that credit card facility is least influential.29% of the respondents say that credit card facility is not influential.

Chapter-6

CONCLUSION

Finally the conclusion which is generalized after the data analysis is that variety of variables

like interest rate, new schemes ,lowest account limit, customer service, availability of loan

type, availability of insurance policies, credit card facility.

The data analysis reveals the fact that the factor which most influential the customers to take

loan from the HDFC bank is lowest account limit, people closely examine this facility after

getting the benefit.

The second most influential factor is new schemes that the reason people prefer to go to

HDFC bank .

Customer service is treated as third most influential ,as good customer service attract

customer towards this bank.

Credit card facility also get good response from customer towards private banks.

Interest rate and availability of insurance policies have got low response from the customers,

this factor can be improved to increase the number of customers to HDFC bank in alwar.

Chapter 7

RECOMMENDATIONS

The data reveals that interest rate n availability of loan should be improved so as to

attract customers.

More credit card facility should be provided so as to given better facility to

customers. More insurance policies should be given to customers.

Chapter 8

LIMITATIONS

CONSTRAINTS WITH THE RESEARCH

The research conducted was limited to Alwar city only.

Due to time constrains more time could not be devoted to individual respondent.

Due to unwillingness of providing any information, the respondents filled the

questionnaire casually which might have affected the consolation.

Non-co-operative behavior of respondent was a big problem in this survey.

Limited knowledge of the researcher in the field of research may lead to

interpretation errors.

The research was based on primary collection of data through Structured Schedule, so

there may be chances of human error and biasness.

Chapter 9

BIBLIOGRAPHY

Kothari C. R. ; Research Methodology; Second Edition; New Age International (p) Limited, publisher; 2004 , pp. (1-229).

Research methodology by Shriendeler and cooper ,Third edition

ANNEXURE-1

“ Analyze consumer perception towards private bank in Alwar.”

QUESTIONNAIRE

Date ……………………………

Name of Respondent………………………..

Gender…………………………………

a. Male……. b. Female…..

Age a. Below 20 b. 20-30 c. 30-40 d. above 40

Qualification a. Graduate b. post –graduate c. Under- graduate d. Other

o Occupation

a. Student b. Professional b. Businessman d. Other

o Annual Income a. Below 2 lac b. 4-6 lac c. 2-4 lac d. above 6

1. Do you have an account in a bank?

a. Yes……… b. no…….

2. If yes, of which bank do you have ?

a. ICICI b. HDFC c. SBI d. other

3. Are this account is beneficial?

a. Yes….. b. no……..

4. If yes then what are the reasons?

(a)less interest rate (b)Customer service (c) New schemes (d) Others

RATE THE PRIVATE SECTOR BANKS ON THE SCALE OF 1-5 AGAINST FACTORS

EFFECT→FACTORS↓

MOST INFLUENTIAL

VERY INFLUENTIAL

INFLUENTIAL LEAST INFLUENTIAL

NOT INFLUENTIAL

INTERST RATE

NEW SCHEMES

LOWEST ACCOUNT LIMIT

AVAILABLE LOAN TYPE

AVAILABILITY OF INSURANCE POLICIES

CUSTOMER SERVICES

CREDIT CARD FACILITY

5) WHAT IS YOUR OVERALL PERCEPTION ABOUT PRIVATE SECTOR BANKS?………………………………………………………………………………………………

Related Documents