1 Customer Lifetime Value (CLV), Customer Equity (CE), and Shareholder Value BA 597: Customer Profitability

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Customer Lifetime Value (CLV),

Customer Equity (CE), and

Shareholder Value

BA 597:

Customer Profitability

2

• To discuss how to calculate customer

lifetime value (CLV)

• To show how it is calculated using actual

data

• To discuss the Tuscan Lifestyles case

results

Today’s Agenda

3

Is CLV better?

Using 54 months of data to predict the next 18

months (for the top 15% of customers)

Selection Metrics

CLV RFM PCV

Avg Revenue 30,427 21,201 21,929

Gross Value 9,184 6,360 6,579

Variable Costs 107 100 95

Net Value 9,077 6,260 6,484

4

Definition:

The sum of calculated cash flows –

discounted using the weighted average

cost of capital (WACC) – of a customer over

his or her entire lifetime with the company.

Customer Lifetime Value

5

Customer Lifetime Value

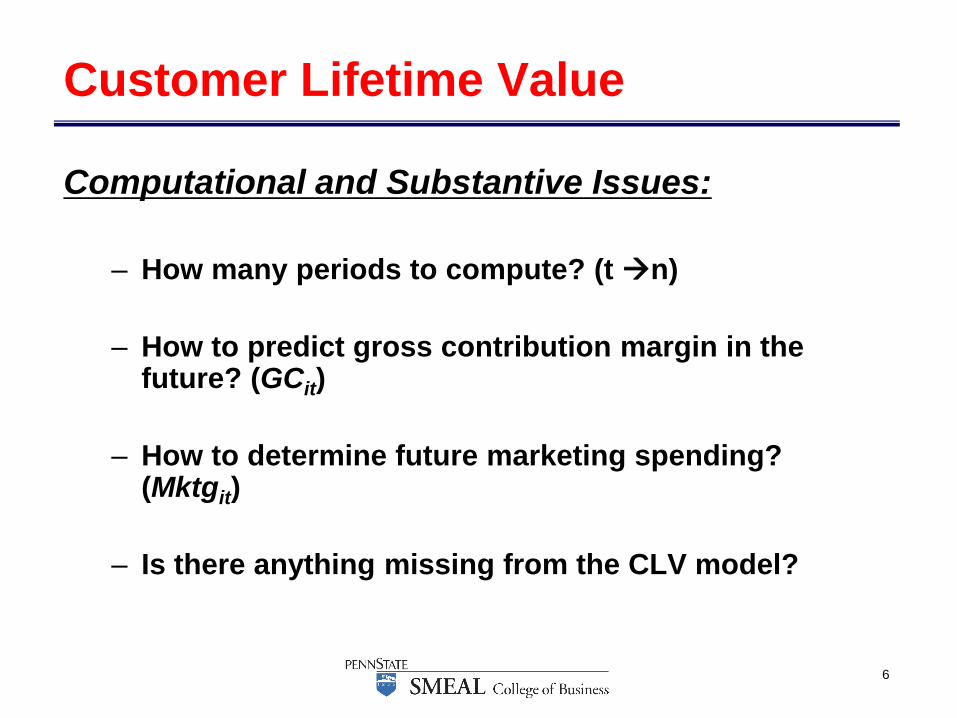

6

Computational and Substantive Issues:

– How many periods to compute? (t n)

– How to predict gross contribution margin in the future? (GCit)

– How to determine future marketing spending? (Mktgit)

– Is there anything missing from the CLV model?

Customer Lifetime Value

7

Customer Lifetime Value

8

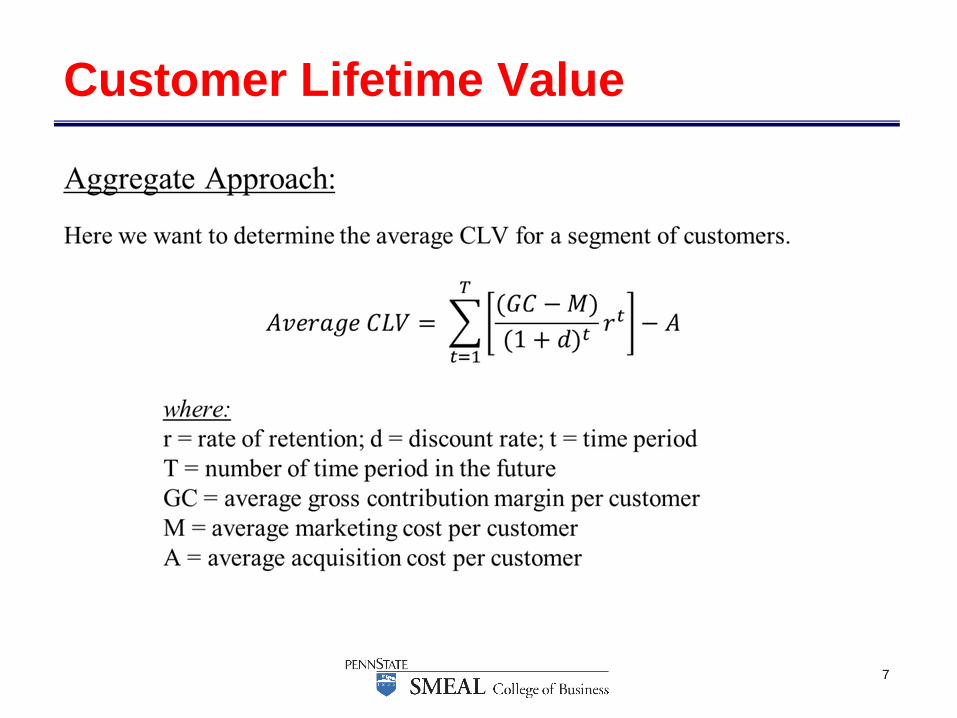

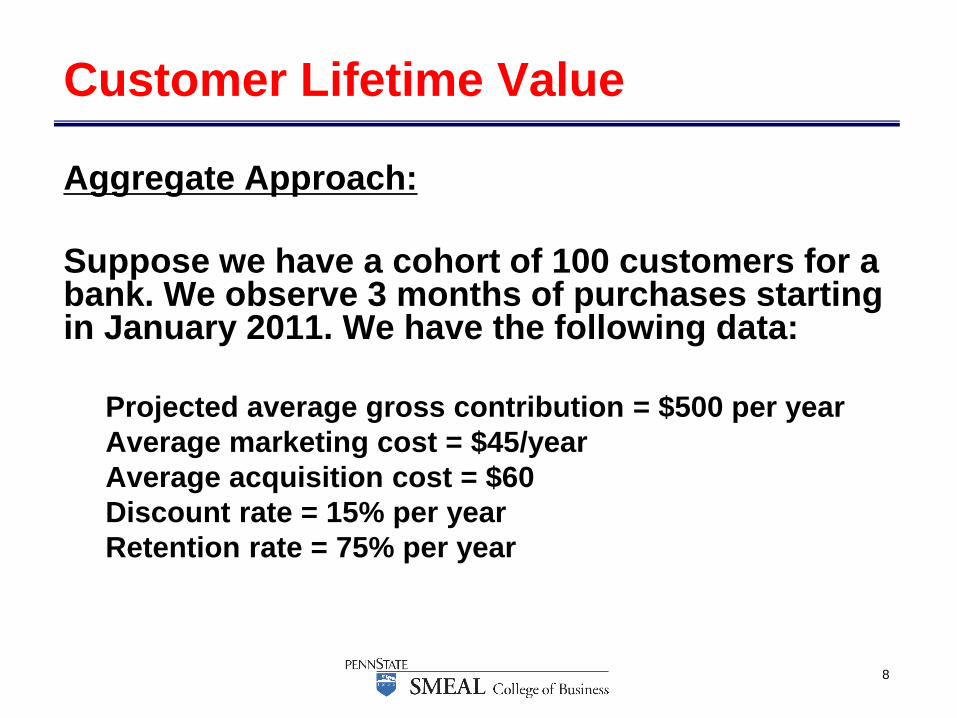

Aggregate Approach:

Suppose we have a cohort of 100 customers for a bank. We observe 3 months of purchases starting in January 2011. We have the following data:

Projected average gross contribution = $500 per year

Average marketing cost = $45/year

Average acquisition cost = $60

Discount rate = 15% per year

Retention rate = 75% per year

Customer Lifetime Value

9

Customer Lifetime Value

10

Customer Lifetime Value

11

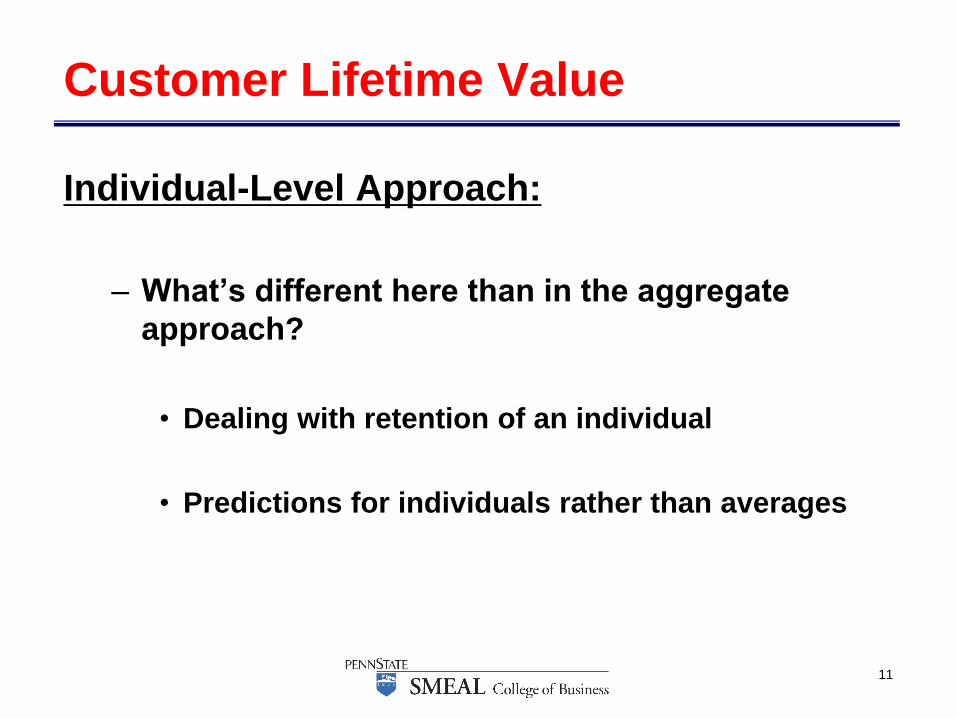

Individual-Level Approach:

– What’s different here than in the aggregate

approach?

• Dealing with retention of an individual

• Predictions for individuals rather than averages

Customer Lifetime Value

12

Dependent Variables of Interest:

– GCit [usually P(Buyit)*E(GCit|Buyit=1)]

– Mktgit [Should we predict it?]

– Ti or P(Aliveit)[Depends on contractual nature]

What are the drivers of each of the three

models?

Customer Lifetime Value

13

P(Aliveit) using Excel (BG/NBD)

Customer Lifetime Value

Required Variables

x The number of transactions by a given customer over all time periods.

Here we assume that it is the sum of the variable Purchase where

customers at most made 1 purchase per quarter.

tx This is the time of the last transaction, i.e. the last quarter where

Purchase = 1.

T The total time between the first purchase and the end of the

observation window, i.e. 12 quarters for all customers.

14

Typical CLV Drivers:

– Exchange Characteristics

– Customer Characteristics

– Product Characteristics

– Firm’s Marketing Actions

Customer Lifetime Value

15

Model Formulation/Data Requirements:

– For prediction you need time dynamics (i.e. DV is in time = t and IVs are in time = t – x)

For example: GCit = f (GCi,t-1, …)

– You need sufficient history to make better future predictions

– You need to select the right model for the DV type(e.g. is the variable continuous, discrete, etc.)

Customer Lifetime Value

16

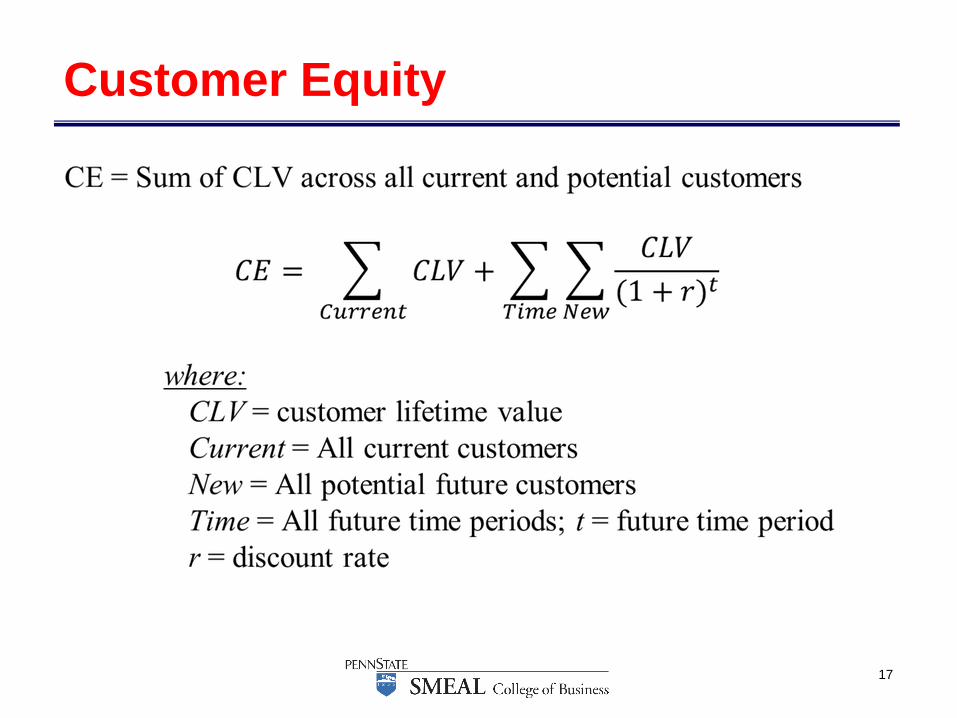

Conceptually, what is it?

– All the discounted profit from current customers

– All the discounted profit from customers

acquired in the future

Customer Equity

17

Customer Equity

18

We know some different techniques for computing the CLV of current customers.

What about future customers?

Computational Issues:

– How many new customers should we expect?

– Does risk matter?

Customer Equity

19

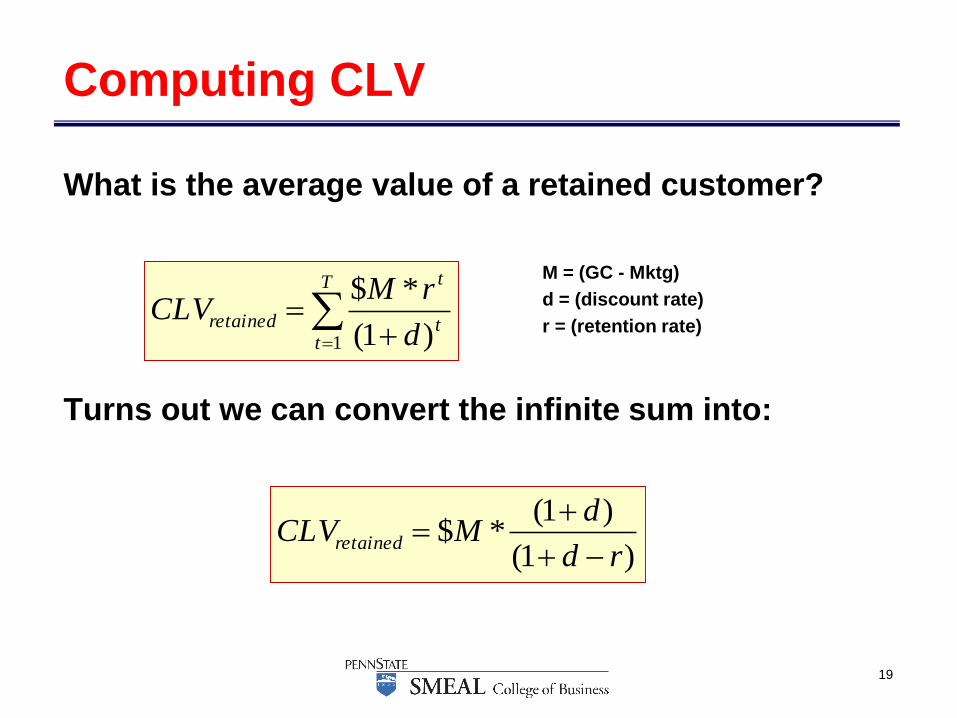

What is the average value of a retained customer?

M = (GC - Mktg)

d = (discount rate)

r = (retention rate)

Turns out we can convert the infinite sum into:

Computing CLV

)1(

)1(*$

rd

dMCLVretained

T

tt

t

retainedd

rMCLV

1 )1(

*$

20

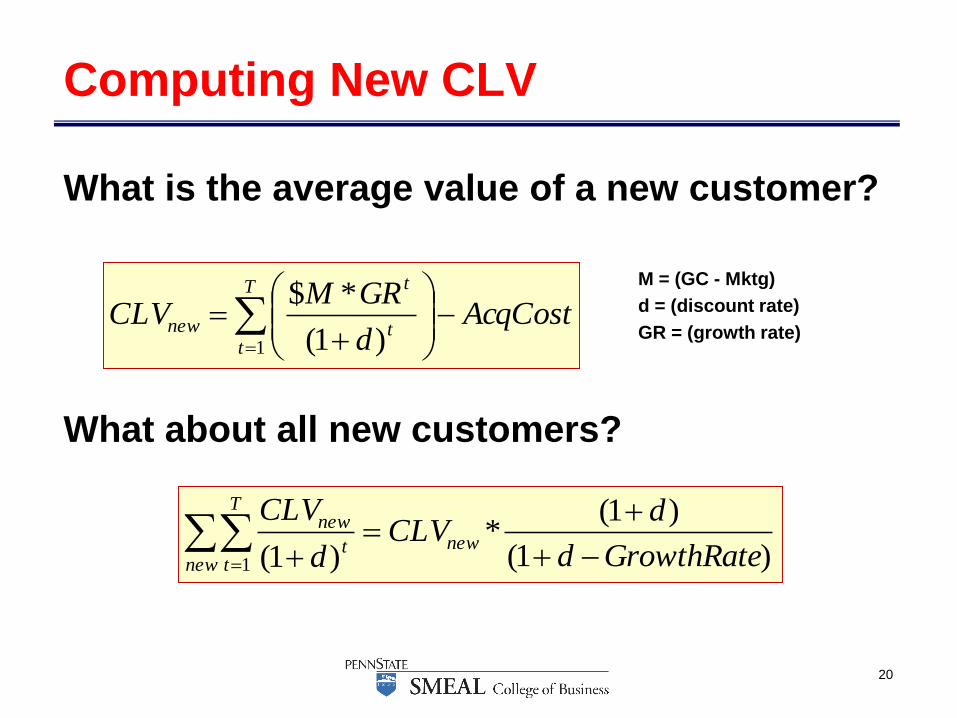

What is the average value of a new customer?

M = (GC - Mktg)

d = (discount rate)

GR = (growth rate)

What about all new customers?

Computing New CLV

AcqCostd

GRMCLV

T

tt

t

new

1 )1(

*$

)1(

)1(*

)1(1 GrowthRated

dCLV

d

CLVnew

new

T

tt

new

21

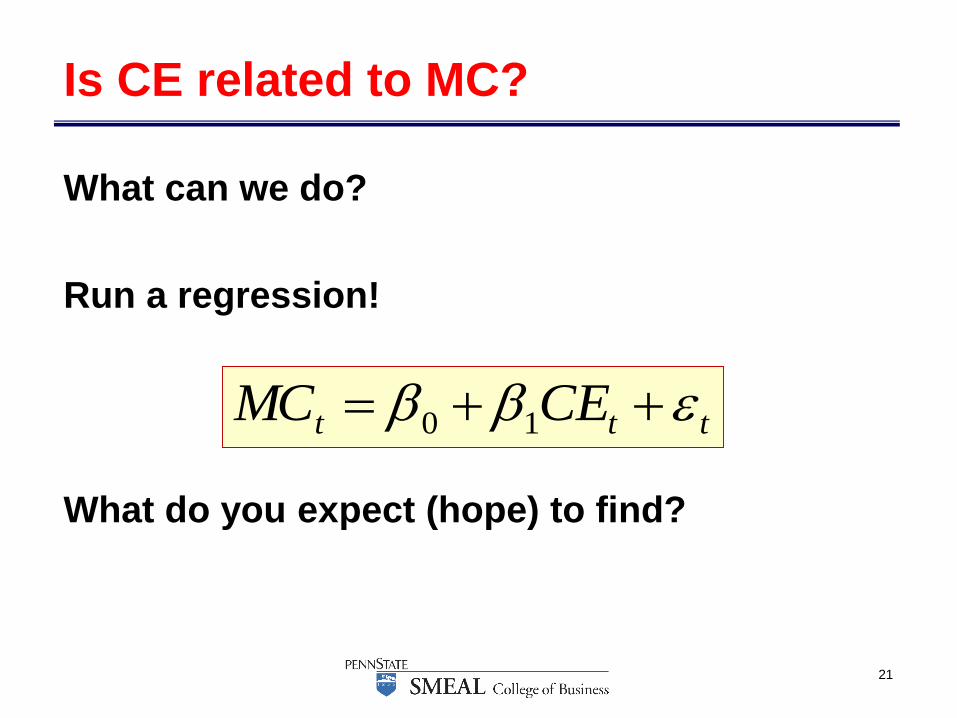

What can we do?

Run a regression!

What do you expect (hope) to find?

Is CE related to MC?

ttt CEMC 10

22

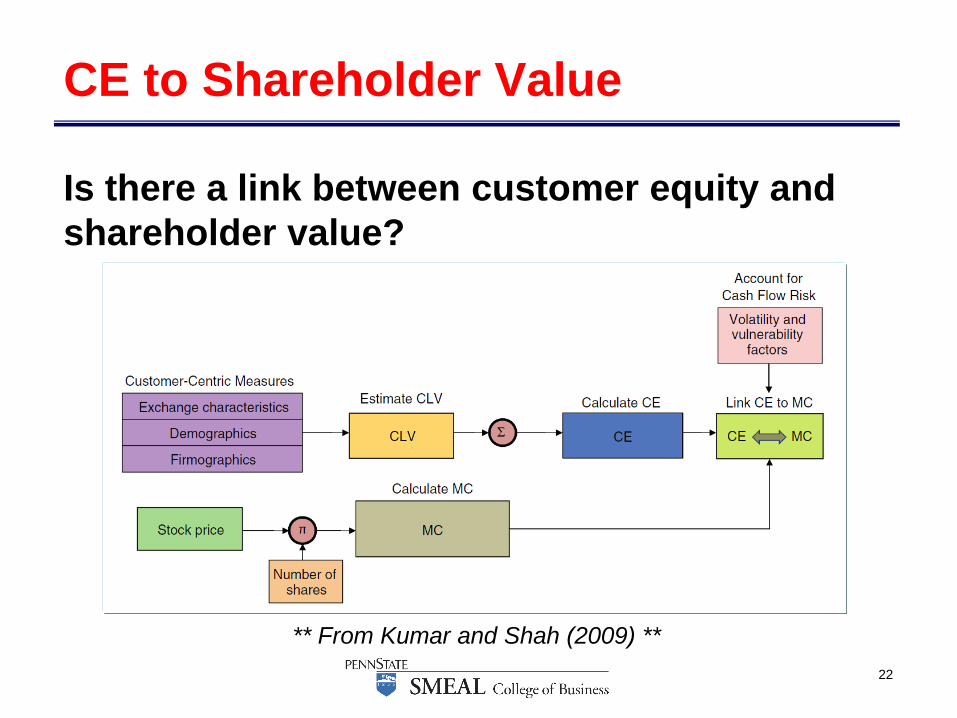

Is there a link between customer equity and

shareholder value?

CE to Shareholder Value

** From Kumar and Shah (2009) **

23

How can we

leverage CRM

strategies to

increase stock

price?

CE to Shareholder Value

** From Kumar and Shah (2009) **

24

What is the

timeline for the

analysis?

CE to Shareholder Value

** From Kumar and Shah (2009) **

25

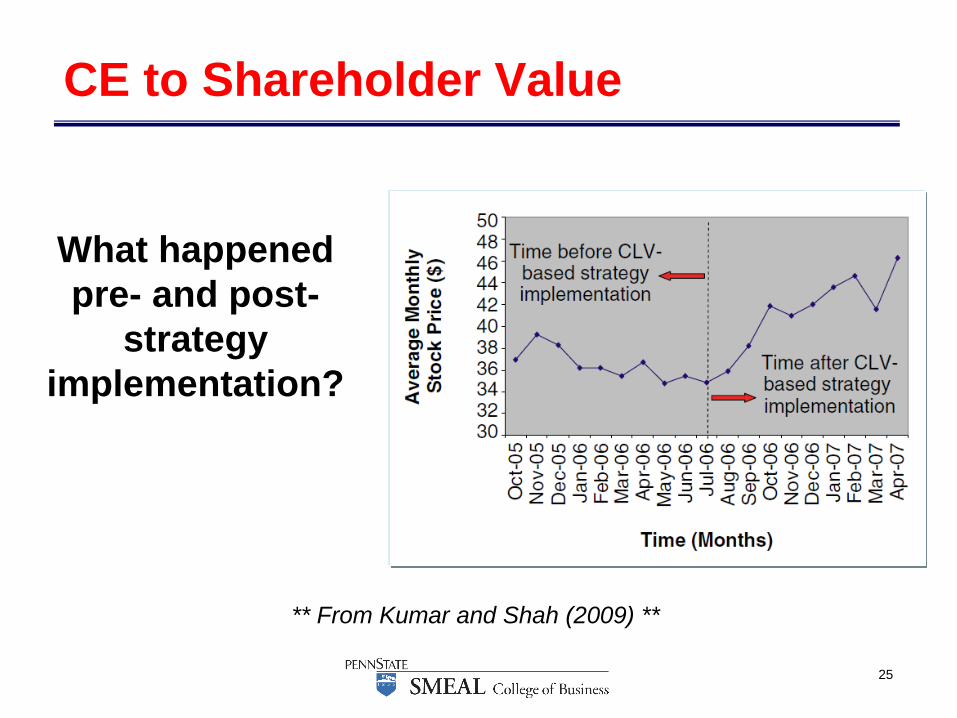

What happened

pre- and post-

strategy

implementation?

CE to Shareholder Value

** From Kumar and Shah (2009) **

26

How did this

firm compare to

the general

market

performance

during the same

time period?

CE to Shareholder Value

** From Kumar and Shah (2009) **

27

Customer Equity refers to the entire base of

current and future customers from a firm

– Does this sound like a problem from finance?

• We have different cash flows from different

customers over time

• We have to choose which customers to invest in

at each time period

Innovations in Maximizing CE

28

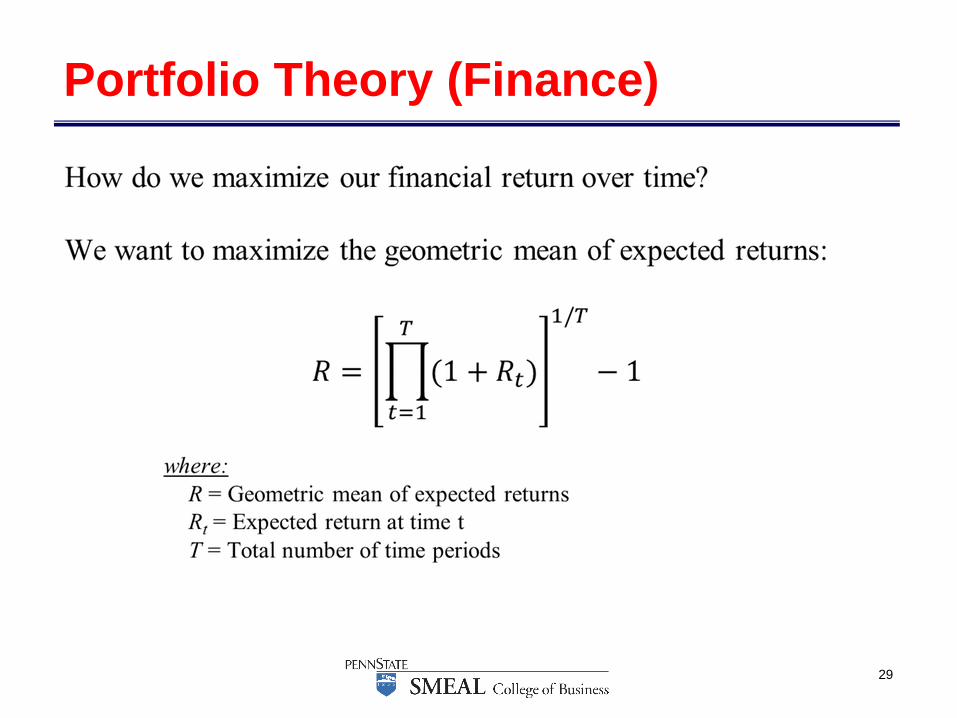

What we know from Finance:

• Markowitz (1952):

– Investors should not try to maximize expected returns.

– Instead, investors should consider maximizing expected return (desirable) and minimizing variance of return (undesirable)

– And, we cannot assume that the law of large numbers will diversify away our risk completely

Portfolio Theory (Finance)

29

Portfolio Theory (Finance)

30

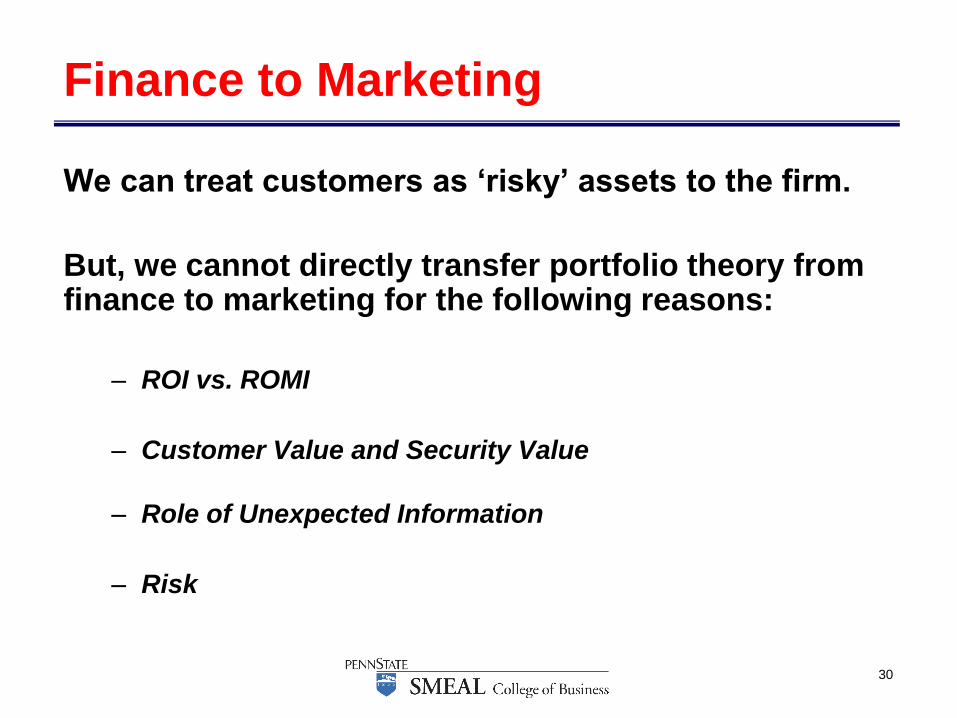

We can treat customers as ‘risky’ assets to the firm.

But, we cannot directly transfer portfolio theory from finance to marketing for the following reasons:

– ROI vs. ROMI

– Customer Value and Security Value

– Role of Unexpected Information

– Risk

Finance to Marketing

31

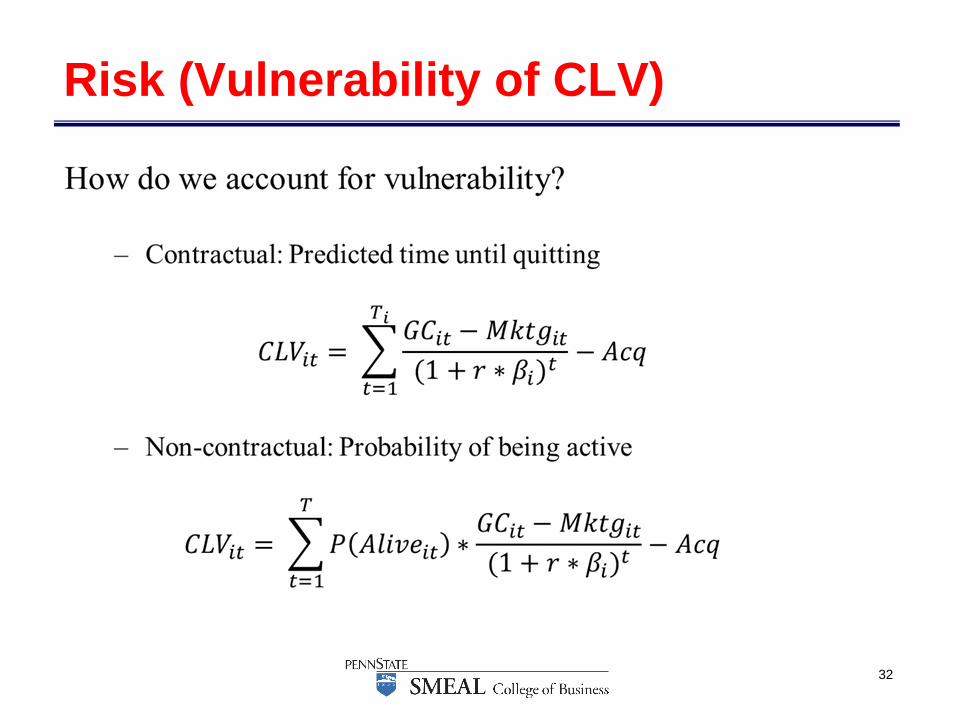

Risk (Volatility of CLV)

32

Risk (Vulnerability of CLV)

33

Questions:

– What is the average CLV (after 5 years) of a

customer whose initial purchase is less than

$50?

– What is the average CLV (after 5 years) of a

customer whose initial purchase is $50 or

greater?

Tuscan Lifestyles

34

Other Questions:

– Based on these CLVs, what marketing plans might be advisable?

– Do you agree with Joan’s assumption that 5 years is a reasonable time horizon?

– Do you have suggestions for other ways to group customers for determining lifetime values?

– What additional information might be helpful for Joan?

Tuscan Lifestyles

35

For Next Class

• Topic:

– Data Mining, Decision Trees, and Data Analysis

– Designing a Loyalty Program

• Reading:

– Applied Logistic Regression

– Assessing a Model’s Performance: Lifts, Gains, and Profits

– The Mismanagement of Customer Loyalty

Related Documents