Sign up for webinar email notifications http://bit.ly/MFLN-Notify Provide feedback and earn CEU Credit with one link: We will provide this link at the end of the webinar Welcome to the Military Families Learning Network Webinar This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department of Agriculture, and the Office of Family Policy, Children and Youth, U.S. Department of Defense under Award Numbers 2010-48869-20685 and 2012-48755-20306. Current Personal Finance Issues for Financial Practitioners

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Sign up for webinar email notificationshttp://bit.ly/MFLN-Notify

Provide feedback and earn CEU Credit with one link: We will provide this link at the end of the webinar

Welcome to the Military Families Learning Network

Webinar

This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department of Agriculture, and the Office of Family Policy, Children and Youth, U.S. Department of Defense under Award Numbers 2010-48869-20685 and 2012-48755-20306.

Current Personal Finance Issues for Financial Practitioners

This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department of Agriculture, and the Office of Family Policy, Children and Youth, U.S. Department of Defense under Award Numbers 2010-48869-20685 and 2012-48755-20306.

Research and evidenced-based professional development

through engaged online communities.

eXtension.org/militaryfamilies

Welcome to the Military Families Learning Network

POLL

How would you best describe your current employer?

Connect with the Personal Finance Team

Facebook: PersonalFinance4PFMs

Twitter: #MFLNPF

Additional Resources Available:learn.extension.org/events/1714

Current Personal Finance Issues for Financial

Practitioners

Barbara O’Neill, Ph.D., CFP®, AFC®, CHCRutgers Cooperative Extension

Webinar ObjectivesPresent a 2014 “Financial Year in Review”

•Key findings from 2014 personal finance studies (non-academic)

•Key findings from 2014 government data

•Key 2014 financial events and trends and products

•Key government legislation/policies affecting personal finances

•Implications of 2014 events for financial practitioners

•New or revised financial education resources in 2014

•Preview of expected 2015 personal finance changes

What Do You Think Was the MOST

Significant Personal Finance Event of 2014?

Key Findings From 2014 Personal

Finance Studies (Non-Academic)

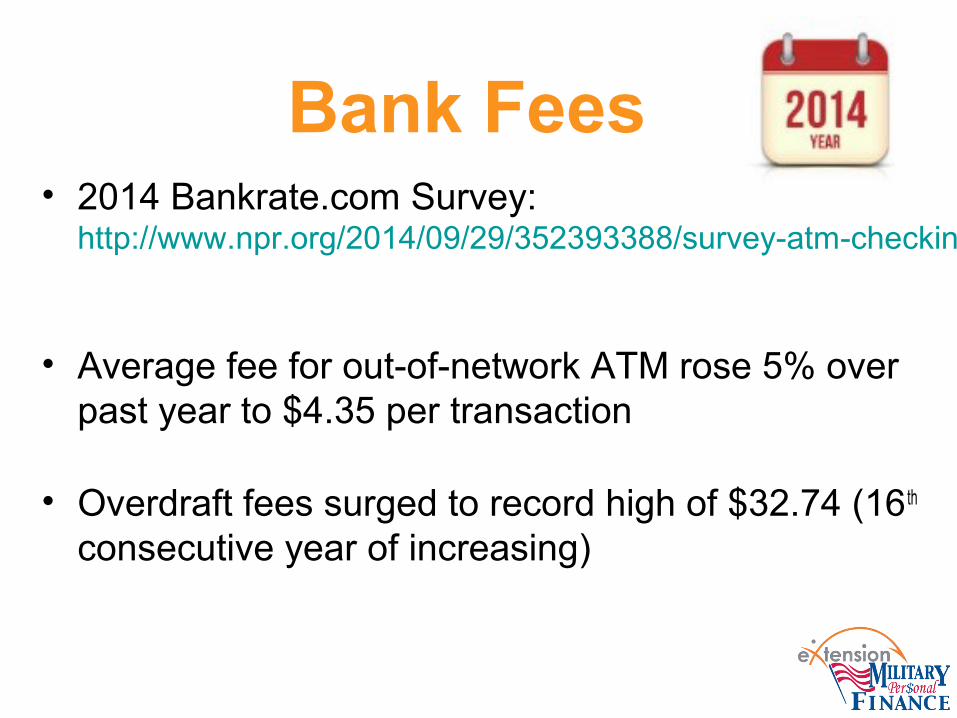

Bank Fees• 2014 Bankrate.com Survey:

http://www.npr.org/2014/09/29/352393388/survey-atm-checking-account-overdraft-fees-surge

• Average fee for out-of-network ATM rose 5% over past year to $4.35 per transaction

• Overdraft fees surged to record high of $32.74 (16 th consecutive year of increasing)

Payday Loans• Pew Charitable Trusts Survey:

http://www.pewtrusts.org/~/media/Assets/2014/10/Payday-Lending-Report/Fraud_and_Abuse_Online_Harmful_Practices_in_Internet_Payday_Lending.pdf

• Online loans much worse than storefront counterparts

• Online payday loans are 1/3 of the market but 90% of complaints

• More abusive tactics than storefront lenders

• More likely to make unauthorized withdrawals from consumer bank accounts

• Claim immunity from individual state laws

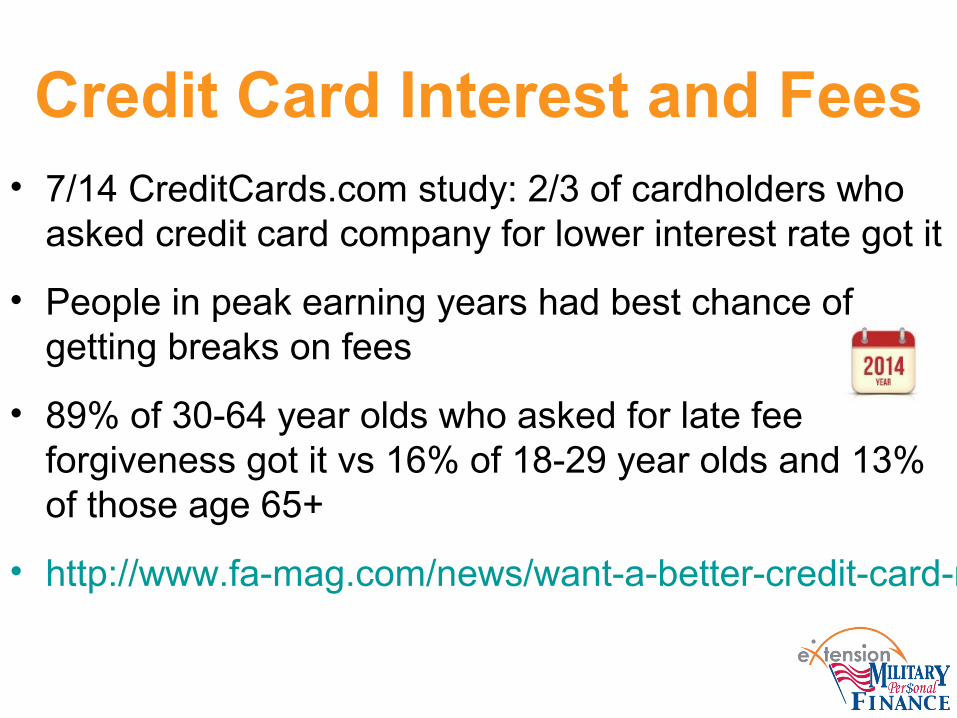

Credit Card Interest and Fees• 7/14 CreditCards.com study: 2/3 of cardholders who

asked credit card company for lower interest rate got it

• People in peak earning years had best chance of getting breaks on fees

• 89% of 30-64 year olds who asked for late fee forgiveness got it vs 16% of 18-29 year olds and 13% of those age 65+

• http://www.fa-mag.com/news/want-a-better-credit-card-rate--just-ask--survey-says-19333.html

Millennial Credit Card Use• Millennials are far more likely than older adults to

make due without credit cards.

• Princeton Survey Research Associates Summer 2014 study: More than 60% of millennials (age 18 to 29) said they did not have a single major credit card vs 35% of adults age 30+

• Reasons cited include CARD Act restrictions on young adults and fear of debt, especially on top of student loans

http://www.nytimes.com/2014/09/10/your-money/the-pros-and-cons-of-avoiding-credit-cards.html

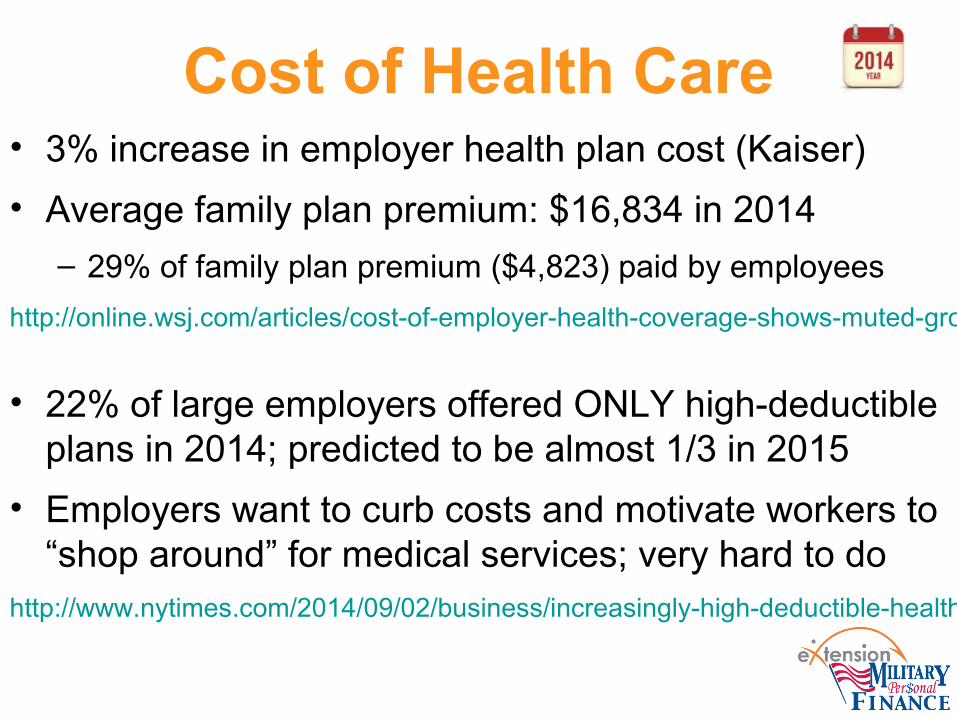

Cost of Health Care• 3% increase in employer health plan cost (Kaiser)

• Average family plan premium: $16,834 in 2014

– 29% of family plan premium ($4,823) paid by employees

http://online.wsj.com/articles/cost-of-employer-health-coverage-shows-muted-growth-1410357841

• 22% of large employers offered ONLY high-deductible plans in 2014; predicted to be almost 1/3 in 2015

• Employers want to curb costs and motivate workers to “shop around” for medical services; very hard to do

http://www.nytimes.com/2014/09/02/business/increasingly-high-deductible-health-plans-weigh-down-employees.html?_r=0

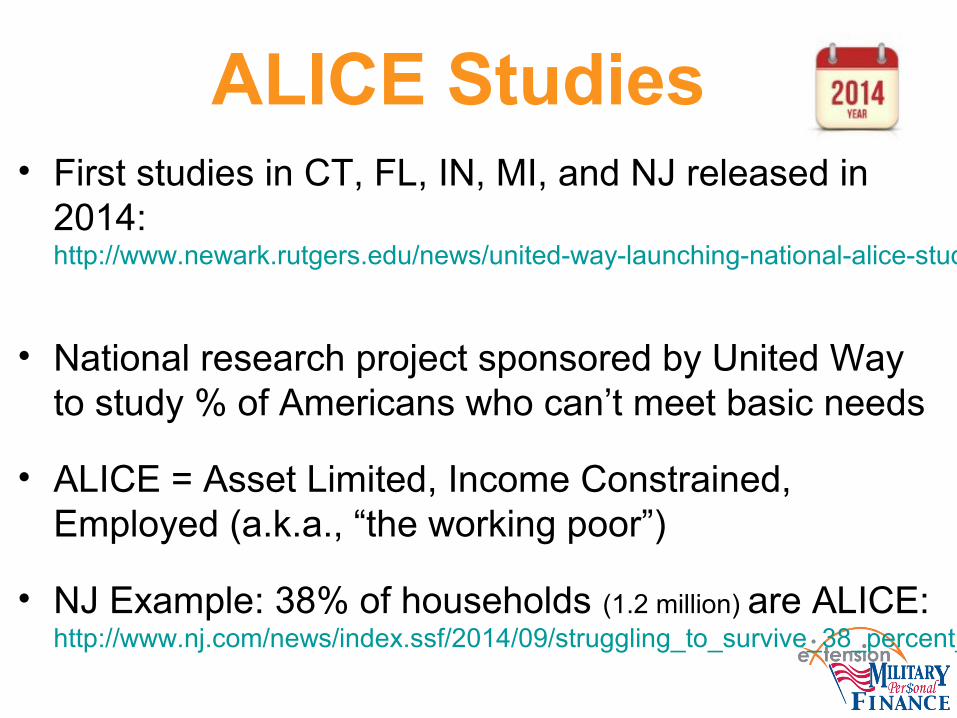

ALICE Studies• First studies in CT, FL, IN, MI, and NJ released in

2014: http://www.newark.rutgers.edu/news/united-way-launching-national-alice-study-rutgers-university-newark-five-states

• National research project sponsored by United Way to study % of Americans who can’t meet basic needs

• ALICE = Asset Limited, Income Constrained, Employed (a.k.a., “the working poor”)

• NJ Example: 38% of households (1.2 million) are ALICE: http://www.nj.com/news/index.ssf/2014/09/struggling_to_survive_38_percent_of_nj_households_cant_meet_basic_needs.html

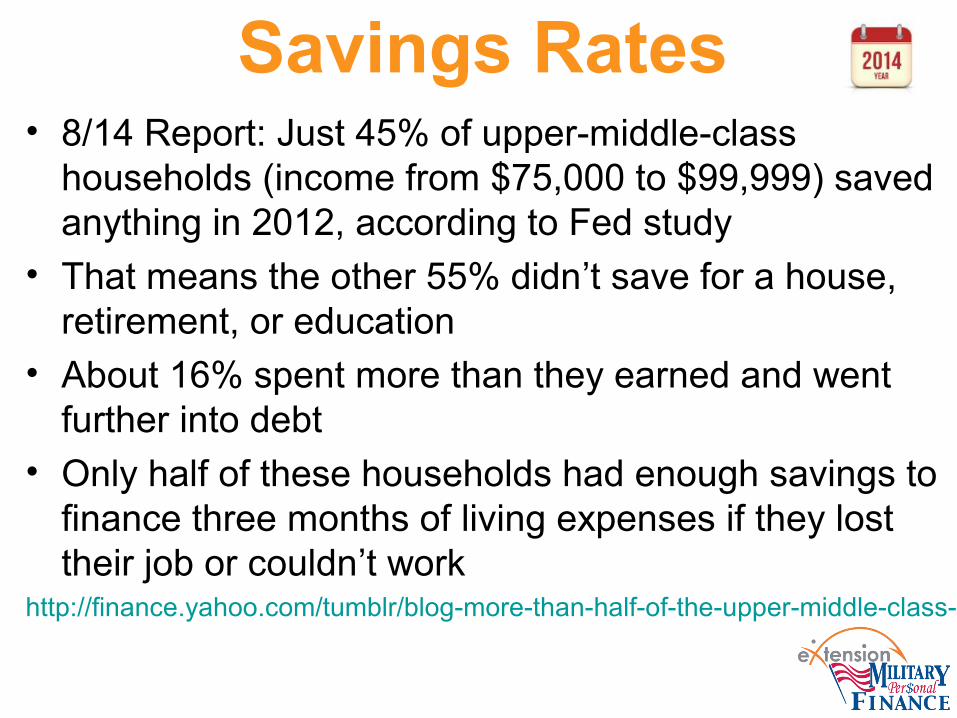

Savings Rates• 8/14 Report: Just 45% of upper-middle-class

households (income from $75,000 to $99,999) saved anything in 2012, according to Fed study

• That means the other 55% didn’t save for a house, retirement, or education

• About 16% spent more than they earned and went further into debt

• Only half of these households had enough savings to finance three months of living expenses if they lost their job or couldn’t work

http://finance.yahoo.com/tumblr/blog-more-than-half-of-the-upper-middle-class-saves-nothing-195411214.html

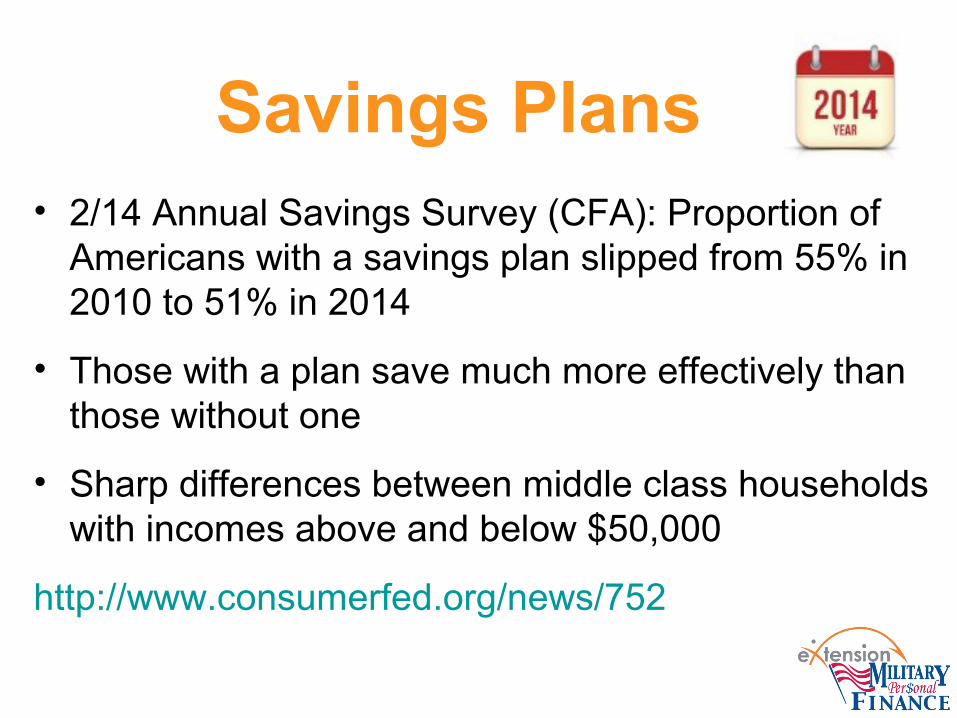

Savings Plans• 2/14 Annual Savings Survey (CFA): Proportion of

Americans with a savings plan slipped from 55% in 2010 to 51% in 2014

• Those with a plan save much more effectively than those without one

• Sharp differences between middle class households with incomes above and below $50,000

http://www.consumerfed.org/news/752

Increased Interest in Prize-Linked Savings

• D2D Fund: 10 weeks, 101 winners, one $25,000 prize: https://www.saveyourrefund.com/home/

• 2014 campaign yielded $2,603,019 in savings

• Average amount saved: $890

• Median amount saved: $220

• Created a savings experience that was fun and aspirational

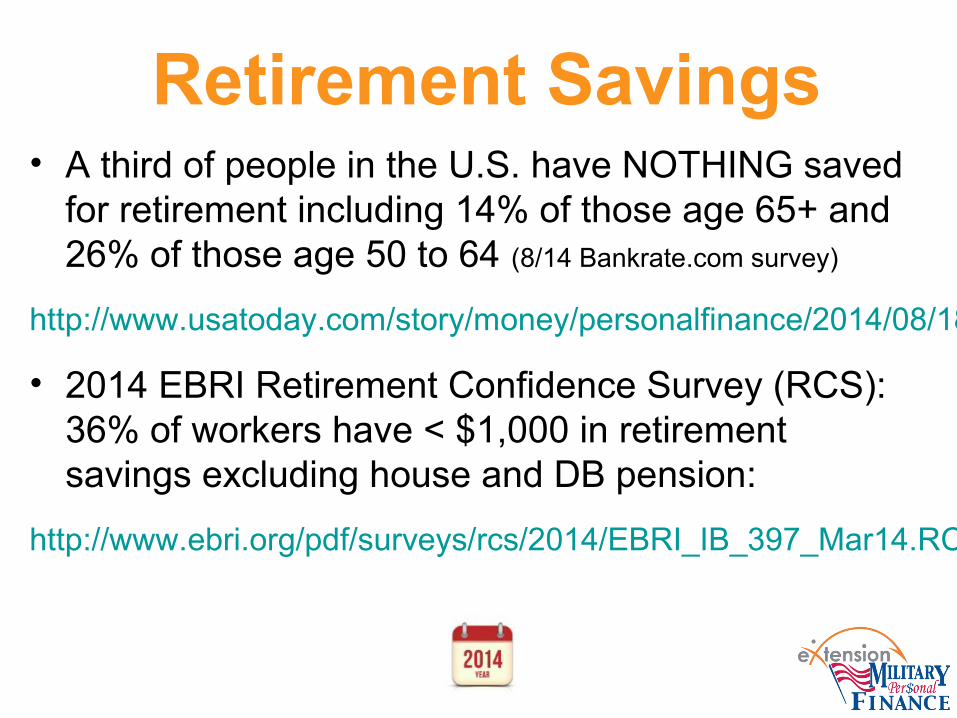

Retirement Savings• A third of people in the U.S. have NOTHING saved

for retirement including 14% of those age 65+ and 26% of those age 50 to 64 (8/14 Bankrate.com survey)

http://www.usatoday.com/story/money/personalfinance/2014/08/18/zero-retirement-savings/14069937/

• 2014 EBRI Retirement Confidence Survey (RCS): 36% of workers have < $1,000 in retirement savings excluding house and DB pension:

http://www.ebri.org/pdf/surveys/rcs/2014/EBRI_IB_397_Mar14.RCS.pdf

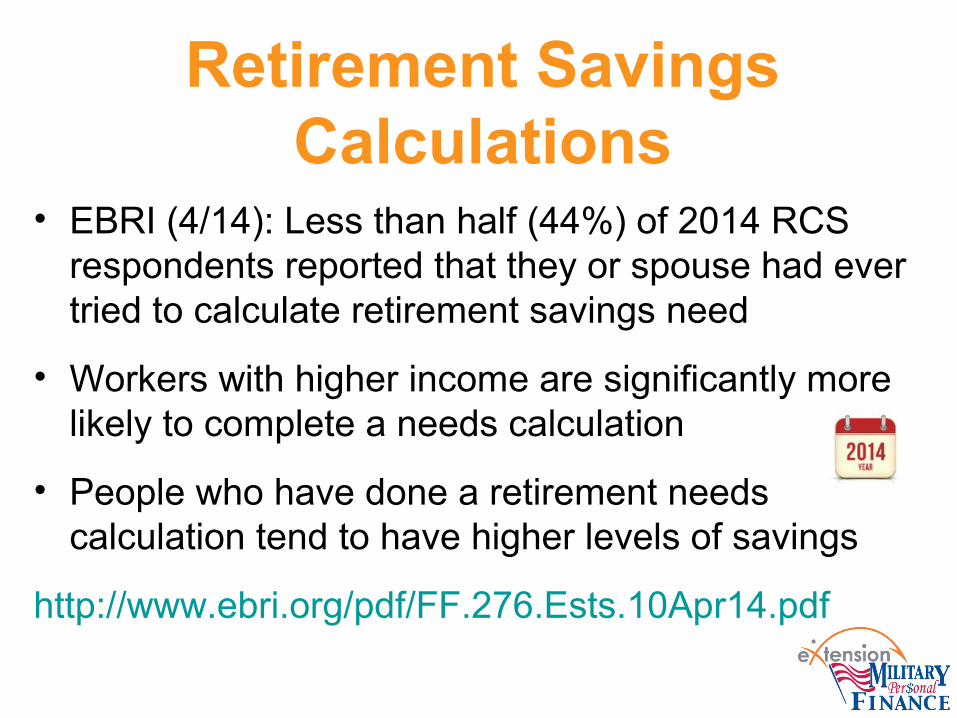

Retirement Savings Calculations

• EBRI (4/14): Less than half (44%) of 2014 RCS respondents reported that they or spouse had ever tried to calculate retirement savings need

• Workers with higher income are significantly more likely to complete a needs calculation

• People who have done a retirement needs calculation tend to have higher levels of savings

http://www.ebri.org/pdf/FF.276.Ests.10Apr14.pdf

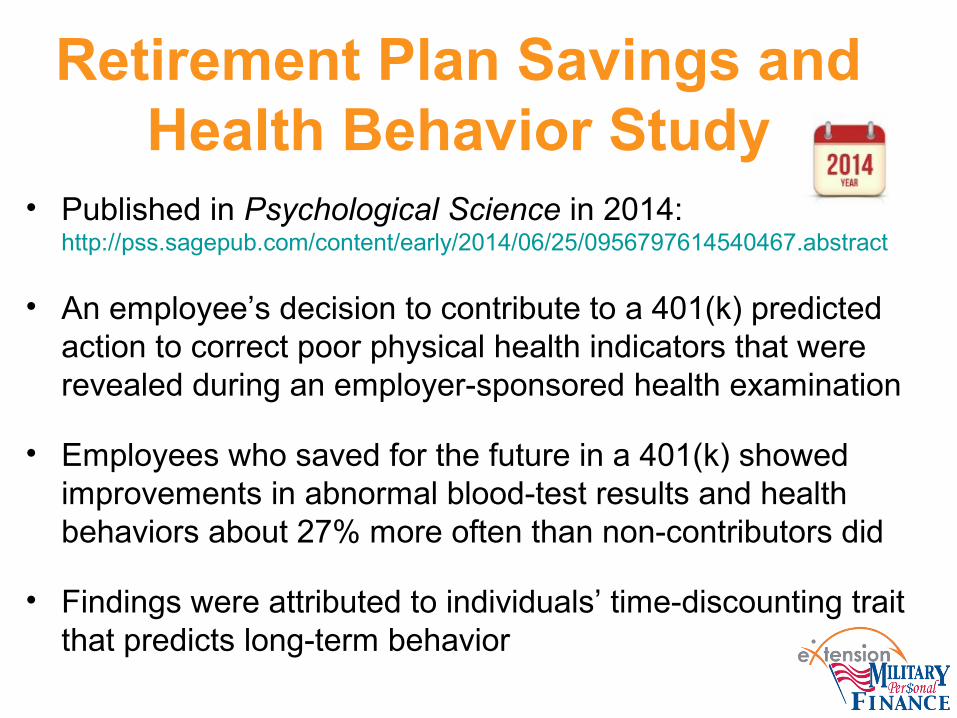

Retirement Plan Savings and Health Behavior Study

• Published in Psychological Science in 2014: http://pss.sagepub.com/content/early/2014/06/25/0956797614540467.abstract

• An employee’s decision to contribute to a 401(k) predicted action to correct poor physical health indicators that were revealed during an employer-sponsored health examination

• Employees who saved for the future in a 401(k) showed improvements in abnormal blood-test results and health behaviors about 27% more often than non-contributors did

• Findings were attributed to individuals’ time-discounting trait that predicts long-term behavior

Retirement Stock Exposure• Kitces & Pfau (4/14 AAII Journal): Allowing equity

exposure to increase in retirement actually improves outcomes

• A portfolio that starts 30% in equities and finishes 70% in equities has 95.1% probability of success over 30-year period

• Recommended framing rising equity glide path to clients as a “bucket strategy”

http://www.aaii.com/journal/article/reduce-stock-exposure-in-retirement-or-gradually-increase-it.touch

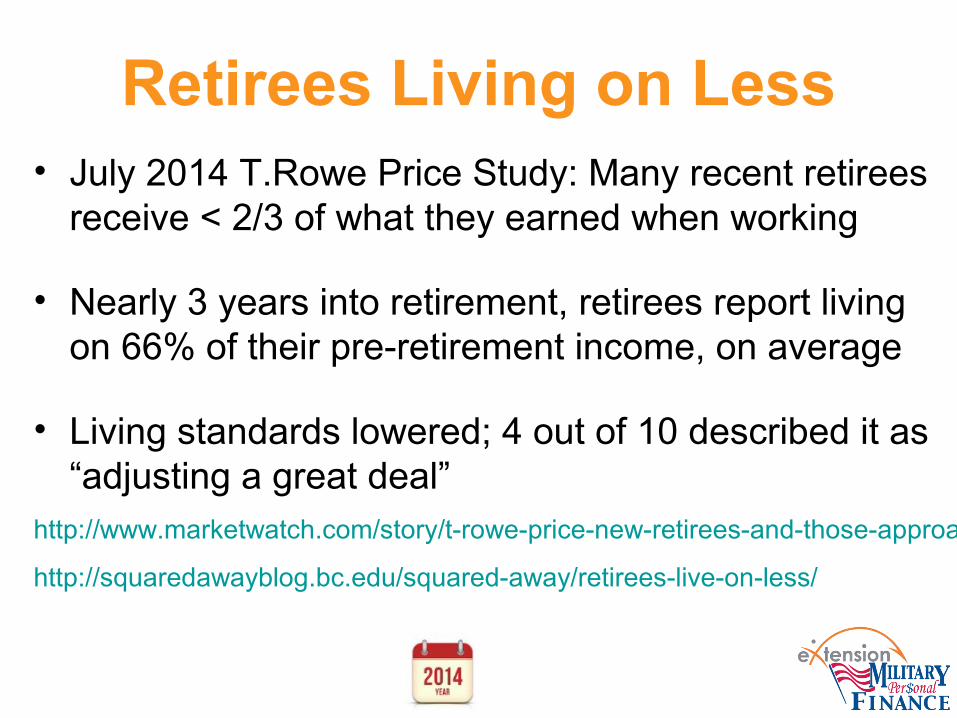

Retirees Living on Less• July 2014 T.Rowe Price Study: Many recent retirees

receive < 2/3 of what they earned when working

• Nearly 3 years into retirement, retirees report living on 66% of their pre-retirement income, on average

• Living standards lowered; 4 out of 10 described it as “adjusting a great deal”

http://www.marketwatch.com/story/t-rowe-price-new-retirees-and-those-approaching-retirement-age-are-faring-well-2014-07-30

http://squaredawayblog.bc.edu/squared-away/retirees-live-on-less/

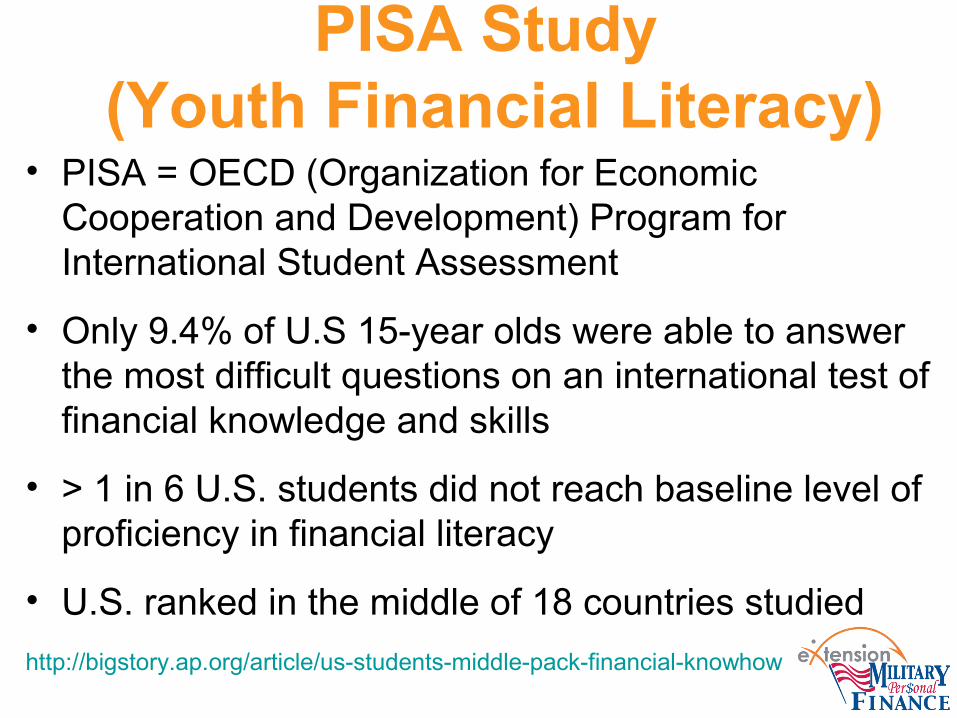

PISA Study (Youth Financial Literacy)

• PISA = OECD (Organization for Economic Cooperation and Development) Program for International Student Assessment

• Only 9.4% of U.S 15-year olds were able to answer the most difficult questions on an international test of financial knowledge and skills

• > 1 in 6 U.S. students did not reach baseline level of proficiency in financial literacy

• U.S. ranked in the middle of 18 countries studied

http://bigstory.ap.org/article/us-students-middle-pack-financial-knowhow

Any Other Interesting 2014 Financial Surveys That You Remember?

Key Findings From 2014 Government

Data

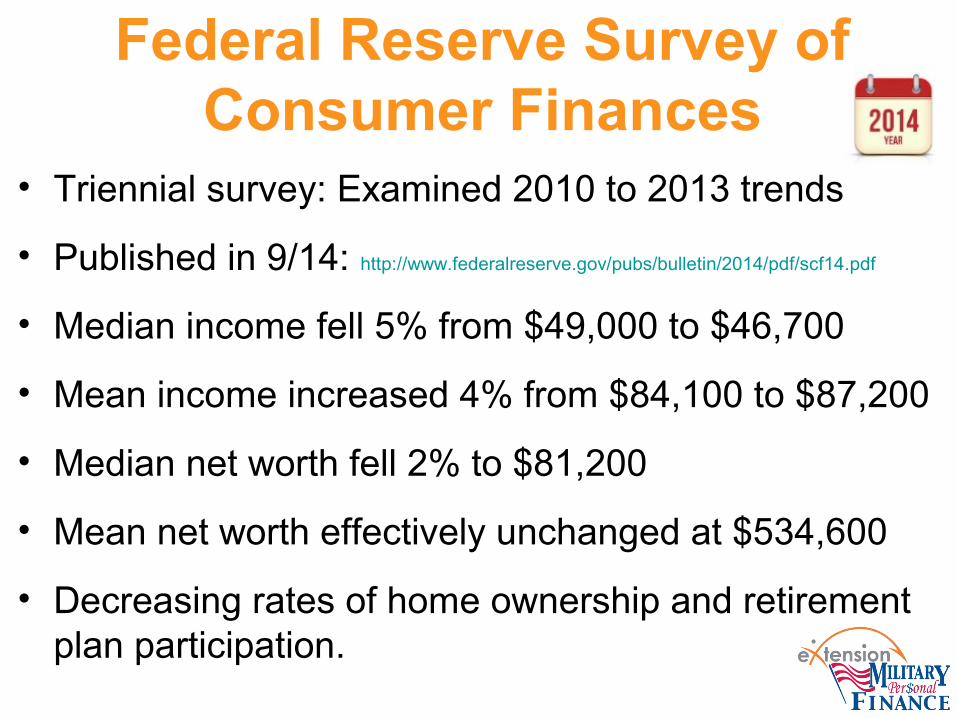

Federal Reserve Survey of Consumer Finances

• Triennial survey: Examined 2010 to 2013 trends

• Published in 9/14: http://www.federalreserve.gov/pubs/bulletin/2014/pdf/scf14.pdf

• Median income fell 5% from $49,000 to $46,700

• Mean income increased 4% from $84,100 to $87,200

• Median net worth fell 2% to $81,200

• Mean net worth effectively unchanged at $534,600

• Decreasing rates of home ownership and retirement plan participation.

Federal Reserve Survey on Economic Well-Being of U.S.

Households (7/14) http://www.federalreserve.gov/econresdata/2013-report-economic-well-being-us-households-201407.pdf

•25% of households “just getting by”; 13% struggling

•31% of people not retired had no savings or pension, including 19% age 55 to 64

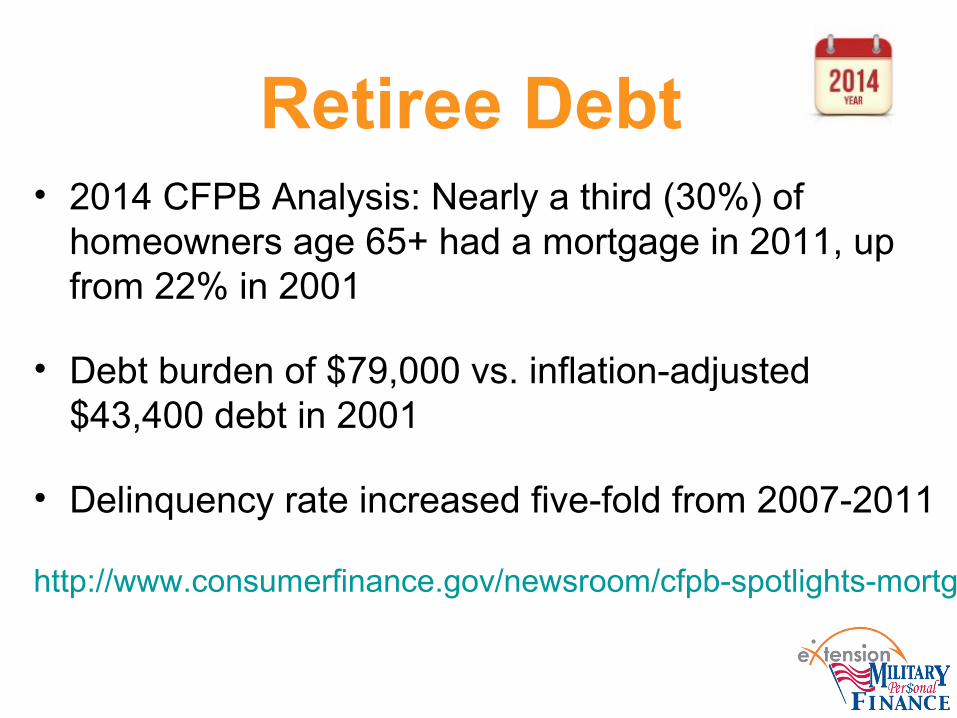

Retiree Debt• 2014 CFPB Analysis: Nearly a third (30%) of

homeowners age 65+ had a mortgage in 2011, up from 22% in 2001

• Debt burden of $79,000 vs. inflation-adjusted $43,400 debt in 2001

• Delinquency rate increased five-fold from 2007-2011

http://www.consumerfinance.gov/newsroom/cfpb-spotlights-mortgage-debt-challenges-faced-by-older-americans/

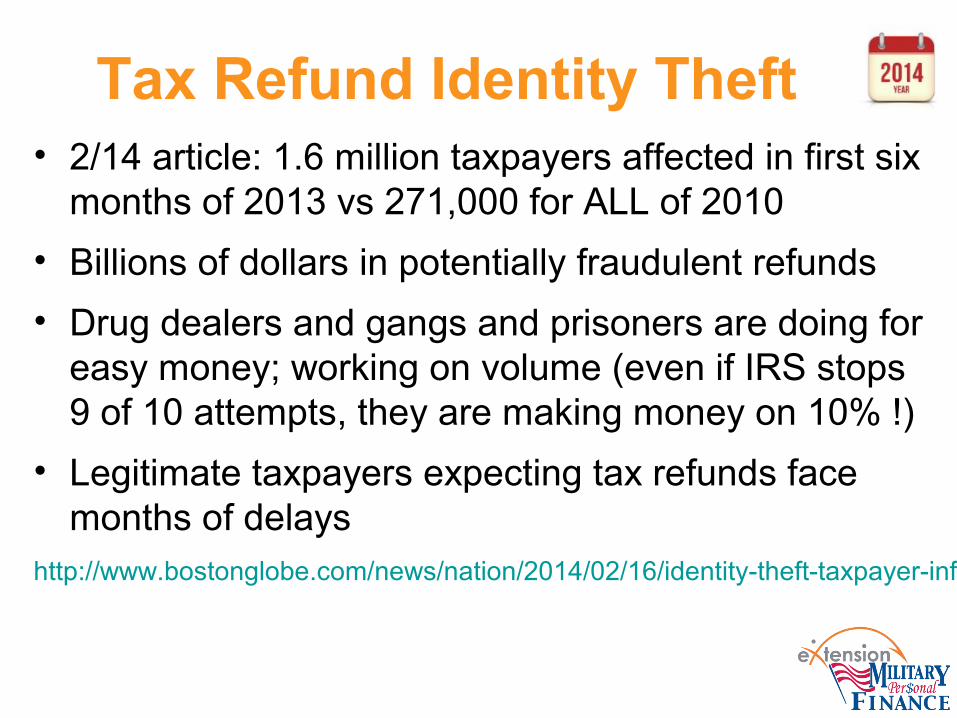

Tax Refund Identity Theft• 2/14 article: 1.6 million taxpayers affected in first six

months of 2013 vs 271,000 for ALL of 2010

• Billions of dollars in potentially fraudulent refunds

• Drug dealers and gangs and prisoners are doing for easy money; working on volume (even if IRS stops 9 of 10 attempts, they are making money on 10% !)

• Legitimate taxpayers expecting tax refunds face months of delays

http://www.bostonglobe.com/news/nation/2014/02/16/identity-theft-taxpayer-information-major-problem-for-irs/7SC0BarZMDvy07bbhDXwvN/story.html

Key 2014 Financial Events and Trends

and Products

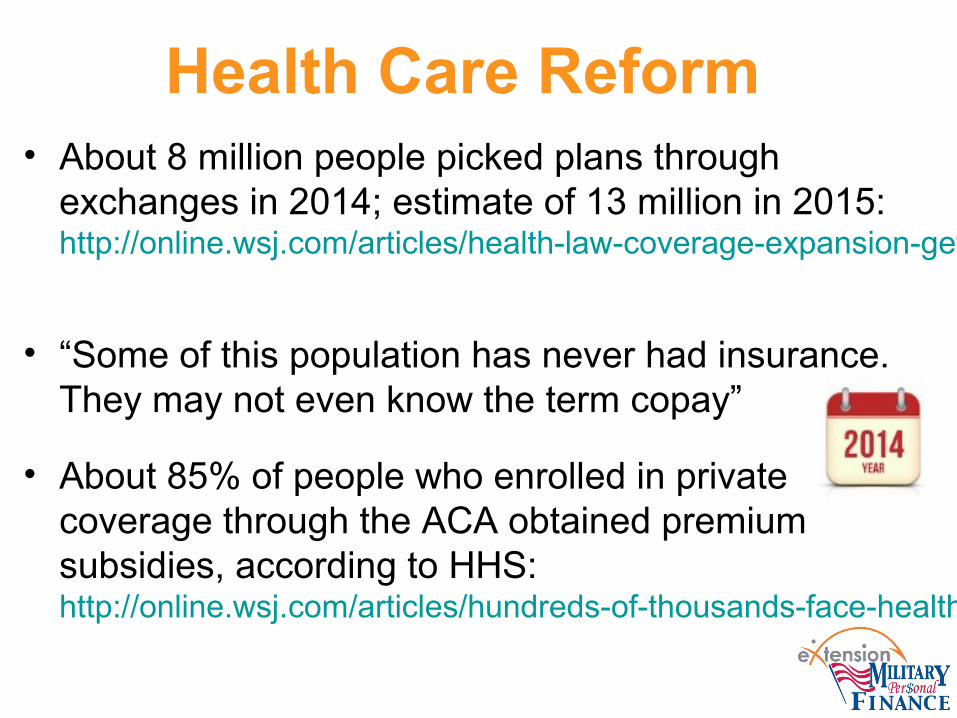

Health Care Reform• About 8 million people picked plans through

exchanges in 2014; estimate of 13 million in 2015: http://online.wsj.com/articles/health-law-coverage-expansion-gets-tougher-1411944893

• “Some of this population has never had insurance. They may not even know the term copay”

• About 85% of people who enrolled in private coverage through the ACA obtained premium subsidies, according to HHS: http://online.wsj.com/articles/hundreds-of-thousands-face-health-law-subsidy-deadline-1412006417

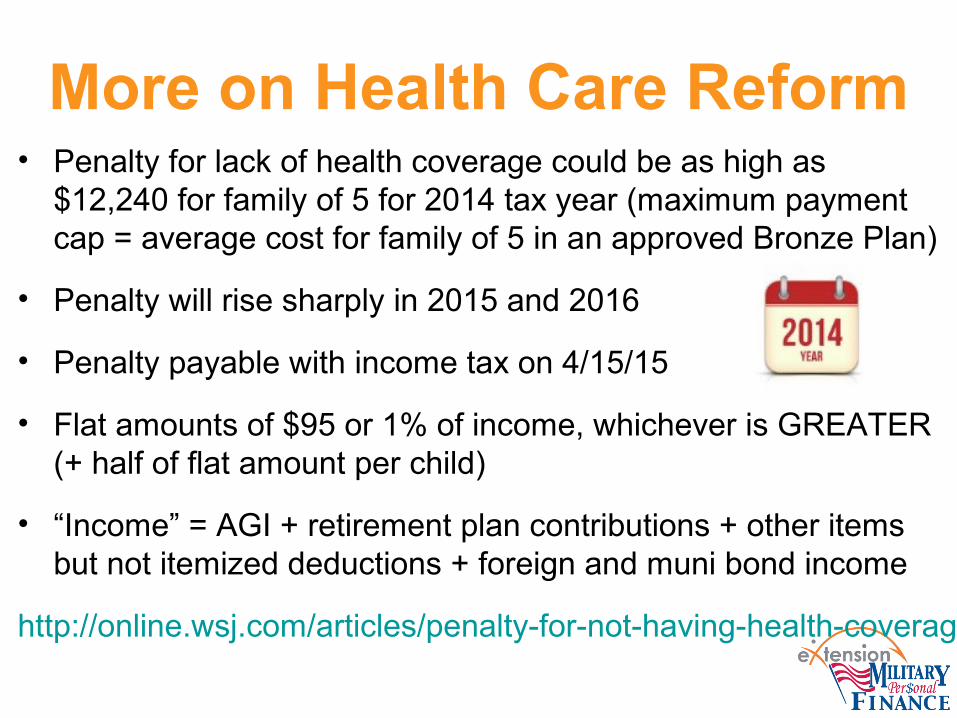

More on Health Care Reform• Penalty for lack of health coverage could be as high as

$12,240 for family of 5 for 2014 tax year (maximum payment cap = average cost for family of 5 in an approved Bronze Plan)

• Penalty will rise sharply in 2015 and 2016

• Penalty payable with income tax on 4/15/15

• Flat amounts of $95 or 1% of income, whichever is GREATER (+ half of flat amount per child)

• “Income” = AGI + retirement plan contributions + other items but not itemized deductions + foreign and muni bond income

http://online.wsj.com/articles/penalty-for-not-having-health-coverage-can-be-thousands-of-dollars-1411748343

More on Health Care Reform

Key dates for health insurance marketplace

•11/15/14- 2/15/15- Open enrollment period for people to apply for, keep, or change coverage

•12/15/14- Last date to enroll for new coverage that begins on 1/1/15

https://www.healthcare.gov/blog/key-dates-for-the-health-insurance-marketplace/

• Can enroll anytime if life circumstances change

More on Health Care Reform• Large employer mandate (to provide coverage)

penalties postponed in 2/14 to 2016 (50-99 workers) or 2015 (100 + workers): http://online.wsj.com/news/articles/SB10001424052702304558804579375213074082656

• Insurers and employers will be required to send the IRS files to determine health law compliance in 2016 (for 2015 tax year returns)

• IRS can’t enforce health care penalty with liens but can withhold if from future tax refunds: http://online.wsj.com/articles/penalty-for-not-having-health-coverage-can-be-thousands-of-dollars-1411748343

MyRA Accounts• 2/14 presidential memo instructing U.S. Treasury

Department to create government-backed retirement accounts for LMI Americans lacking employer plans

• Savers invest after-tax dollars and make tax-free withdrawals in retirement

• Roll it over to private sector Roth IRA when balance reaches $15,000

http://www.treasurydirect.gov/readysavegrow/start_saving/retirementaccountfactsheetenglish.pdf

DB Pension Transfers• Insurance companies are taking over pension

responsibilities for large private sector companies (e.g., Motorola to Prudential Insurance in 2014; GM and Verizon previously)

• Companies avoid rising PBGC premiums and risk of having enough assets to cover future obligations

• Employees/retirees no longer have backstop PBGC protection; only state guaranty funds

http://www.bloomberg.com/news/2014-09-25/motorola-solutions-moves-4-2-billion-in-pensions-to-prudential.html

Growth of Inexpensive Financial Advisors

• Example: Vanguard Group: 0.3% annual fee for most clients vs. 1% typically charged by advisory firms

• Other examples: Charles Schwab, Fidelity (0.5% annual fee)

• “Robo-advisor” Examples: Wealthfront, Bettermint that manage investments via unique algorithms for 0.25% fee ($25 per $1,000 invested)

http://www.businessinsider.com/robo-advisors-vs-financial-advisors-2014-7

http://online.wsj.com/articles/the-rise-of-ultracheap-financial-advisers-1411164756

Boomerang Kids• 9/14 MONEY Magazine article: Among adults 40 to

59 with at least one grown child, 73% said they’d helped support an adult child in the prior year

• Nearly a quarter of 25 to 34 year olds are now living with parents or grandparents vs.11% in 1980

• “It’s not at the margins. It’s kind of everybody”

http://time.com/money/page/parents-adult-children-financial-support/

Employment Trends• 62.8% labor force participation rate (8/14) vs. 66%

in 12/07 (start of Great Recession)

• 3.2% difference = 8 million workers

• If “dropouts” were looking for work, unemployment rate would be nearly twice as high

http://online.wsj.com/articles/william-galston-saving-the-vanishing-american-worker-1410908001

Student Loan Defaults• 9/14 Education Department report: drop in Americans

defaulting on student loans

• 13.7% default rate for 2011 those leaving school or graduating in 2011 vs. 14.7% in 2010

• Still, that’s 1 in 7 borrowers!

• Drop attributed to enrollment in income-based repayment plans

http://online.wsj.com/articles/defaults-on-federal-student-loans-decline-1411567201

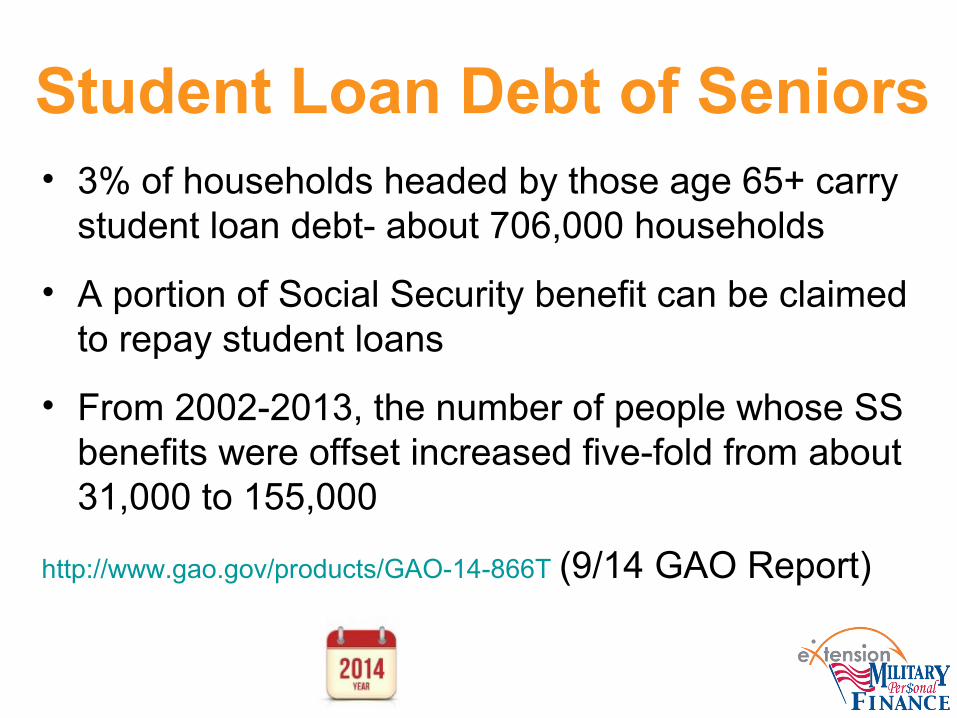

Student Loan Debt of Seniors• 3% of households headed by those age 65+ carry

student loan debt- about 706,000 households

• A portion of Social Security benefit can be claimed to repay student loans

• From 2002-2013, the number of people whose SS benefits were offset increased five-fold from about 31,000 to 155,000

http://www.gao.gov/products/GAO-14-866T (9/14 GAO Report)

Credit Scoring Change• 8/14 Announcement re: FICO credit scores: Fair

Isaac Corp will stop including in FICO score calculations any record of a bill if it has been paid or settled with a collection agency

• They will also give less weight to unpaid medical bills with a collection agency

http://online.wsj.com/news/articles/SB20001424052702304070304580077903072682306

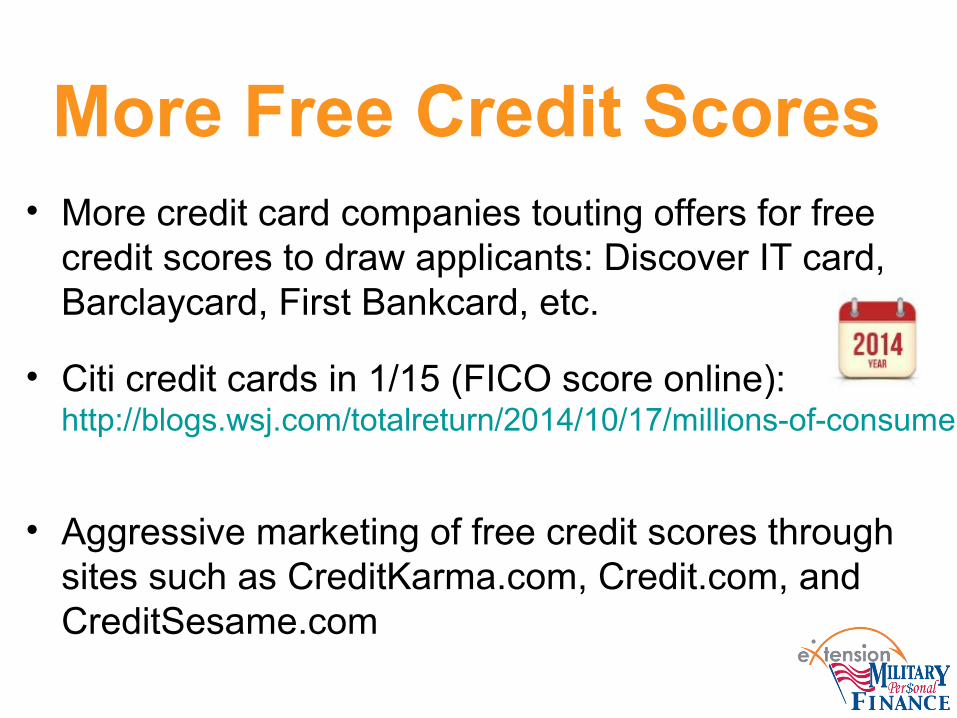

More Free Credit Scores• More credit card companies touting offers for free

credit scores to draw applicants: Discover IT card, Barclaycard, First Bankcard, etc.

• Citi credit cards in 1/15 (FICO score online): http://blogs.wsj.com/totalreturn/2014/10/17/millions-of-consumers-to-gain-access-to-credit-scores/

• Aggressive marketing of free credit scores through sites such as CreditKarma.com, Credit.com, and CreditSesame.com

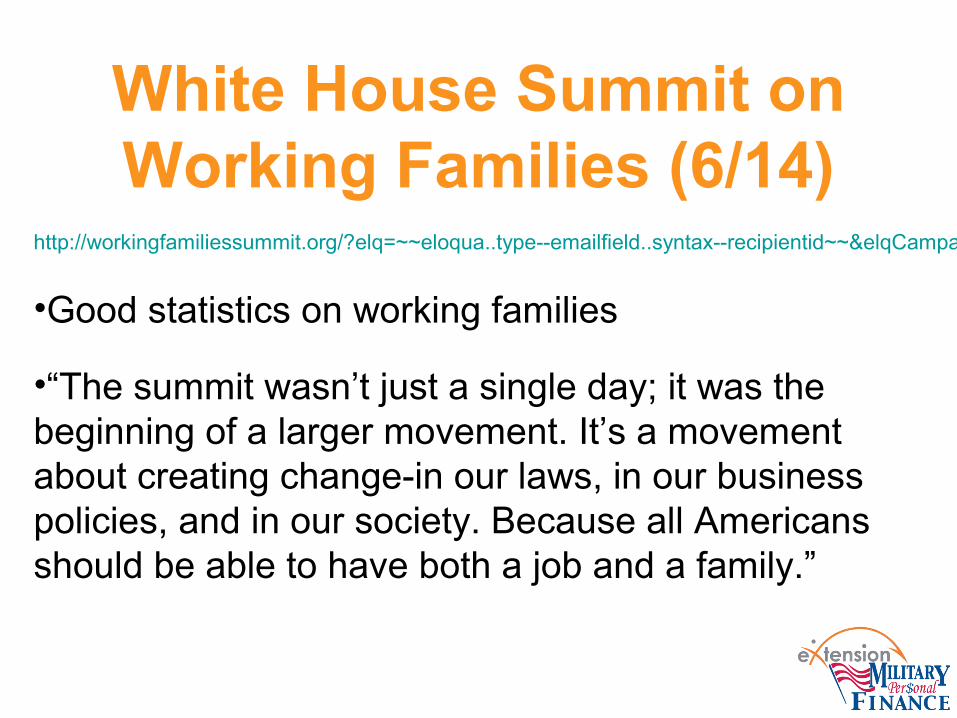

White House Summit on Working Families (6/14)

http://workingfamiliessummit.org/?elq=~~eloqua..type--emailfield..syntax--recipientid~~&elqCampaignId=~~eloqua..type--campaign..campaignid--0..fieldname--id~~

•Good statistics on working families

•“The summit wasn’t just a single day; it was the beginning of a larger movement. It’s a movement about creating change-in our laws, in our business policies, and in our society. Because all Americans should be able to have both a job and a family.”

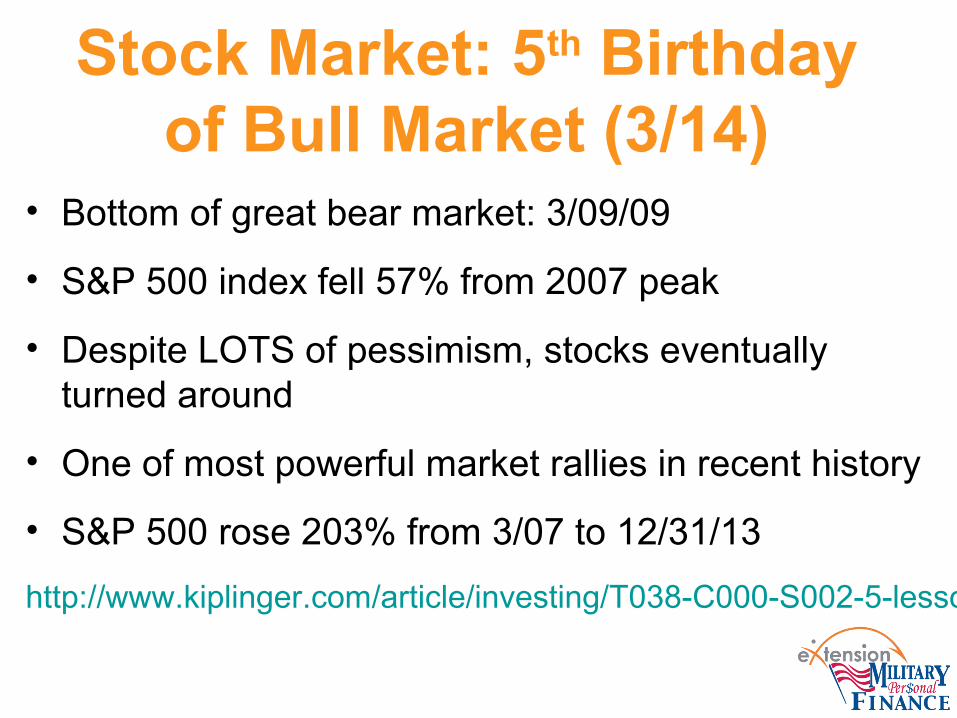

Stock Market: 5th Birthday of Bull Market (3/14)

• Bottom of great bear market: 3/09/09

• S&P 500 index fell 57% from 2007 peak

• Despite LOTS of pessimism, stocks eventually turned around

• One of most powerful market rallies in recent history

• S&P 500 rose 203% from 3/07 to 12/31/13

http://www.kiplinger.com/article/investing/T038-C000-S002-5-lessons-from-this-bull-market.html

Increased Use of ETFs• ETFs have been stealing market share from mutual

funds for past decade

• ETFs have about 11% of assets in “mutual fund space”

• ETFs are winning market share because they are cheaper and more tax-efficient

http://connection.ebscohost.com/c/articles/97363811/mutual-funds-are-dead-here-s-how-adapt

(Journal of Financial Planning, 8/14)

Any Other Interesting 2014 Financial Events, Trends, or Products?

Key Government Legislation and

Policies Affecting Personal Finances

2014 Financial Literacy Legislation

• Prepared by National Conference of State Legislatures

• State-by-state list of legislation introduced or pending in 2014

• http://www.ncsl.org/research/financial-services-and-commerce/financial-literacy-2014-legislation.aspx

Social Security Benefit Estimates

• Agency resumes mailing SS benefit statements

• Once every 5 years for most workers (25, 30, etc.); those not getting benefits and not registered online

• SSA still encouraging online accounts through http://www.ssa.gov/myaccount/

• Expects to mail 48 million statements vs. >14 million online accounts

• SS statement is a valuable retirement planning toolhttp://www.investmentnews.com/article/20140917/BLOG05/140919930/social

-security-resumes-mailing-statements

Reverse Mortgages• As of 1/14, lenders are required to assess the

financial condition of prospective borrowers to determine if their income is sufficient to pay future property taxes and insurance; http://www.onefpa.org/journal/Pages/MAR14-Retirement-Trends,-Current-Monetary-Policy,-and-the-Reverse-Mortgage-Market.aspx

• $625,000 lending limit (amount of home value that can be used to calculate eligible loan amount) for 2014: http://reversemortgagedaily.com/2013/12/06/fha-keeps-reverse-mortgage-loan-limits-unchanged-for-2014/

IRS Policy on Taxation of Bitcoins (3/14)

• Bitcoins are a virtual currency made by computer algorithms and sold in unregulated exchanges

• Operate like currency; pay for goods and services

• IRS will treat Bitcoins as property, not currency

• Wages paid in Bitcoin are subject to withholding

• Bitcoin traders are subject to capital gains taxhttp://www.irs.gov/uac/Newsroom/IRS-Virtual-Currency-Guidance

http://www.usatoday.com/story/money/business/2014/03/25/irs-says-bitcoin-is-property/6873569/

Any Other Interesting 2014 Financial

Legislation or Policies?

Implications of 2014 Events for Financial

Practitioners

Tips for Practitioners• Incorporate 2014 trends and research findings into

outreach efforts

• Correct previous misperceptions and outdated information (i.e., things that you said “Who Knew?” to)

• Make all of your outreach efforts “actionable” (e.g., Web links, application forms, 1:1 counseling sessions)

• Review new (2014) financial education resources

Tips for Clientele• Don’t automatically elect to stay on company plan

through COBRA if unemployed; check out policies available on www.healthcare.gov and online

• Calculate retirement savings need for better planning accuracy and as motivation to save

• Plan for a constrained retirement lifestyle, if needed

• Understand that using an ATM not affiliated with your bank can result in TWO fees: one charged by lender and one charged by owner of ATM

Beware of ATMs Like This

Tips for Clientele• Develop a spending and savings plan for increased

financial discipline and motivation to save

• Understand the financial implications of long-term dependency by adult children

• Negotiate with credit card companies for lower interest and waived fees

• Consider ETFs as an investment vehicle for goals

• Avoid large tax refunds that can be held up by identity theft; adjust W-4 form accordingly

New or Revised Financial Education Resources in 2014

Annual Limits Publication

“The Bible”:

Annual Limits Relating to Financial Planning (College for Financial Planning): http://www.cffpinfo.com/annual-limits/

New and Archived MFLNPF Webinars

Sallie Mae: The College Planning Toolbox

https://www.salliemae.com/plan-for-college/college-planning-toolbox/ •Includes information on grants and loans, scholarship searching, student loan calculators, award letter analyzer (for comparisons), and more

Healthcare.gov

OCC Financial Literacy Resource Directory (4/14)

http://www.occ.gov/topics/community-affairs/resource-directories/financial-literacy/index-financial-literacy.html

Jumpstart Coalition: Making the Case for Financial Literacy- 2014

http://jumpstart.org/assets/files/Making%20the%20Case%202014_2.pdf

•8 pages of current statistics about financial knowledge, attitudes and behaviors

2014 Survey of the States http://www.councilforeconed.org/news-information/survey-of-the-states/

•Tells which states require economic and personal finance education in K-12 schools

Financial Literacy Summit 2014

• Sponsored by Federal Reserve of Chicago and Visa• Archived at

http://www.practicalmoneyskills.com/summit2014/

“Providing Financial Literacy Resources to the Unbanked and Underbanked”

April 2, 2014

COHEAO Financial Literacy Awareness White Paper (3/14)

• Sponsored by the Coalition of Higher Education Assistance Organizations (COHEAO)

http://www.coheao.com/wp-content/uploads/2014/03/2014-COHEAO-Financial-Literacy-Whitepaper.pdf

• Focus on best practices in financial literacy education for college students

• Good resource list with links

Rutgers Cooperative ExtensionPersonal Health and Finance Quizhttp://njaes.rutgers.edu/money/health-finance-quiz/

• Believed to be FIRST combined online health and personal finance behavioral practice assessment tool; IRB approved at Rutgers

• Three distinct uses:

– Stand-alone self-assessment tool for users

– To collect data for ongoing research

– For educators to use for SSHW program evaluation (pre- and post-program score)

Any Other New Financial Education Resources Developed in 2014?

Preview of Expected 2015 Personal

Finance Changes

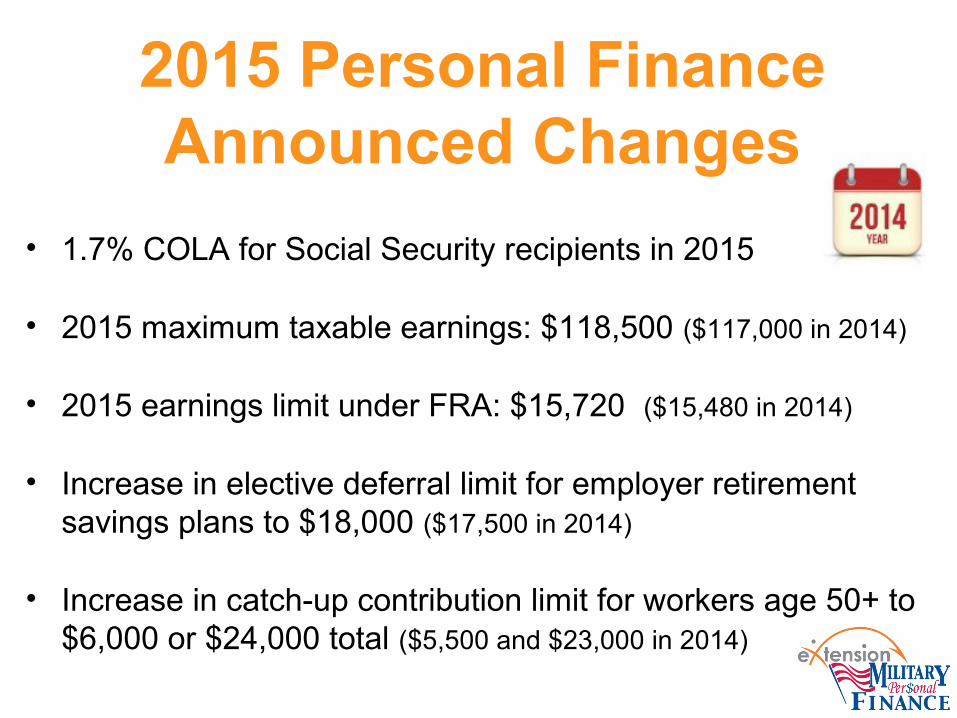

2015 Personal Finance Announced Changes

• 1.7% COLA for Social Security recipients in 2015

• 2015 maximum taxable earnings: $118,500 ($117,000 in 2014)

• 2015 earnings limit under FRA: $15,720 ($15,480 in 2014)

• Increase in elective deferral limit for employer retirement savings plans to $18,000 ($17,500 in 2014)

• Increase in catch-up contribution limit for workers age 50+ to $6,000 or $24,000 total ($5,500 and $23,000 in 2014)

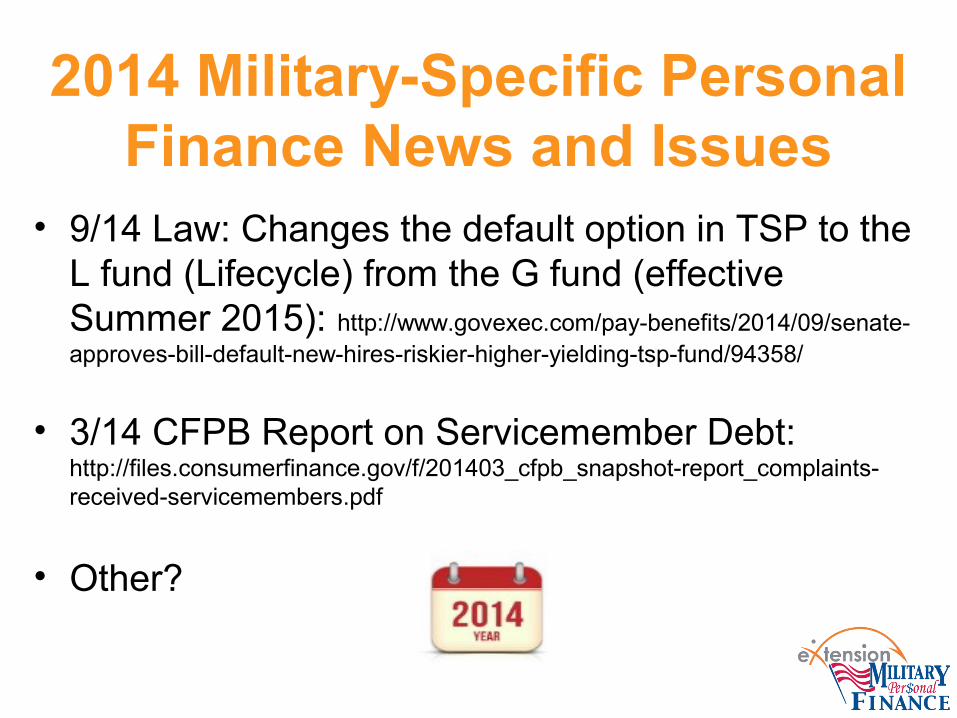

2014 Military-Specific Personal Finance News and Issues

• 9/14 Law: Changes the default option in TSP to the L fund (Lifecycle) from the G fund (effective Summer 2015): http://www.govexec.com/pay-benefits/2014/09/senate-approves-bill-default-new-hires-riskier-higher-yielding-tsp-fund/94358/

• 3/14 CFPB Report on Servicemember Debt: http://files.consumerfinance.gov/f/201403_cfpb_snapshot-report_complaints-received-servicemembers.pdf

• Other?

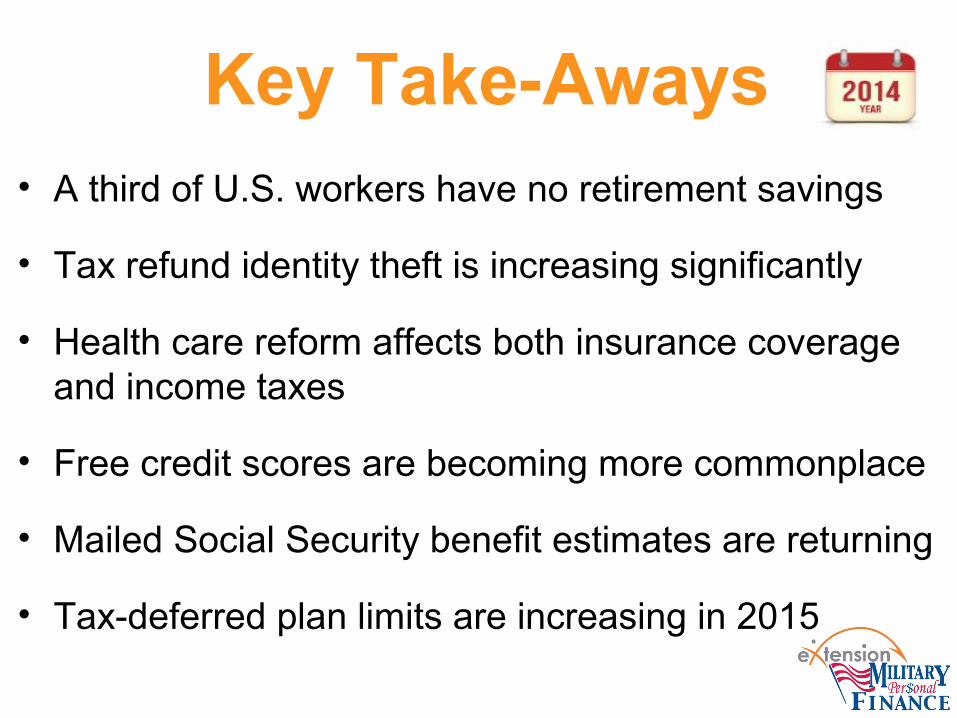

Key Take-Aways• A third of U.S. workers have no retirement savings

• Tax refund identity theft is increasing significantly

• Health care reform affects both insurance coverage and income taxes

• Free credit scores are becoming more commonplace

• Mailed Social Security benefit estimates are returning

• Tax-deferred plan limits are increasing in 2015

Key Take-Away Applications• Encourage people to save something for retirement

• Encourage people to file taxes early and avoid a large tax refund that can be held up by thieves

• Encourage people with ACA health insurance to accurately estimate income for subsidies

• Encourage people to seek out free credit scores

• Encourage people to read SS benefit estimates and get online account at http://www.ssa.gov/myaccount/

• Encourage people to save more for retirement in 2015

Comments? Questions?

Next Personal Finance Webinar

Year End Tax Planning StrategiesTuesday, December 9, 11 a.m. ET

• https://learn.extension.org/events/1675• Speaker: Dr. Barbara O’Neill• 1.5 CEUs for AFC-credentialed participants

Military Families Learning Network

This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department of Agriculture, and the Office of Family Policy, Children and Youth, U.S. Department of Defense under Award Numbers 2010-48869-20685 and 2012-48755-20306.

Family Development Military CaregivingPersonal Finance Network Literacy

Find all upcoming and recorded webinars covering:

http://www.extension.org/62581

Related Documents