INCORPORATION OF COMPANY PRESENTED BY: CA. BHUPESH ANAND FCA, ACMA, FCS, DIP-IFRS ( LONDON) QUALIFIED VALUER, MIND TRAINER

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INCORPORATION OF COMPANY

PRESENTED BY:

CA. BHUPESH ANANDFCA, ACMA, FCS, DIP-IFRS (LONDON)QUALIFIED VALUER, MIND TRAINER

Concept 1Types of Business Entitiesa) A Person can do business as per following forms of organisation namely.

Sole Proprietorship

Partnership

Company

Charitable Organization Contd.

b) Difference between sole proprietorship & Partnership firm.

SOLE-PROPRIETORSHIP

1. No registration required

2. Unlimited liability

3. Used for small business or by professionals

4. No separate legal entity

PARTNERSHIP

1. Registration not compulsory.

2. Two types:a. Limited liabilityb. Unlimited liability

3. Sharing of profits by those agreed upon.

4. Governed by Indian Partnership Act.

Contd.

c) Company- Derived from a LATIN word “COM”=“WITH” or “TOGETHER”; “PANIES= BREAD”

d) Meaning of a Company

“An association of persons who took their meals together”

Legal Formation An Artificial person Has a separate legal entity Has a Perpetual Succession Company seal Common capital with transferable shares Carries limited liability Democratic management

Concept 2Procedure of Formationa) Procedure for Incorporating a Company

STAGE I: PRE REGISTRATION PROCEDURE

Obtain a DIN-Director Identification Number.

DSC-Digital Signature Certificate.

STAGE II: NAME AVAILABILITY

Contd.

STAGE III: DOCUMENTATION

Preparation of Memorandum & Articles of

Association.

Vetting of Memorandum & Articles, Printing,

Stamping & Signing

Contd.

STAGE IV: FILING & REGISTRATIONForm 1 (Declaration)

Form 32 (Details of Directors)

Form 18 (Details of Registered Office of the

company).

Contd.

b) OTHER COMPANY’S

Section 25 Companies.

Companies deemed to be public limited.

Holding and subsidiary companies.

Contd.

Government companies.

Foreign Companies.

One Man Companies.

Private Companies.

Concept 3Meaning of Profit Prior to Incorporation.a) As Incorporation Certificate is the evidence of formation of a company , So Period Prior to Date of

Incorporation in case of conversion of Existing Business to a company is named as Pre- Incorporation Period.

b) Time Period after date of incorporation is named as

post incorporation Period.

Contd.

c) All Profits earned by existing Business (Sole Proprietor/ Partnership Firm) Upto date of incorporation are named as Pre-Incorporation Profits, these profits are non – recurring in nature i.e. capital profits.

d) All profits from date of incorporation Upto end of year are named as post incorporation profits, these

profits are recurring in nature (Revenue Profits).

e) Dividend as per companies Act 2013 can be declared out of Post Incorporation Profits only.

Contd.

Post

Pre

Date of Incorporation From ROC

f) Following is the flow chart for understanding the importance of incorporation certificate.

Concept 4Calculationa) Following steps may be followed for calculation Pre-Incorporation Profits: Step 1- Prepare Trading A/c for whole Accounting year i.e. 12 months in case Gross Profits has not been specified in the question.

Step 2- Calculate Time Ratio & Sales Ratio.

Contd.

Step 3- Profits & Loss A/c should be prepared into separate columns of Pre & Post Incorporation. Following is format for calculating Pre & Post.

Contd.

b) Format of Trading Account To Opening Stock xxx By Sales xxx To Raw Material Purchased xxx By Closing Stock xxx To D. Lab xxx To F. O/h xxx To Gross Profit xxx

(Bal. Fig.)

Contd…

c) Time Ratio

Time Period in Pre- Incorporation Period

Time period in post Incorporation Period

:

Contd.

d) Sales Ratio

Sales in Pre- Incorporation period

Sales in Post Incorporation Period:

Contd.

e) Format of Profi t & loss Accounts

Contd.

Contd..

f)

Contd.

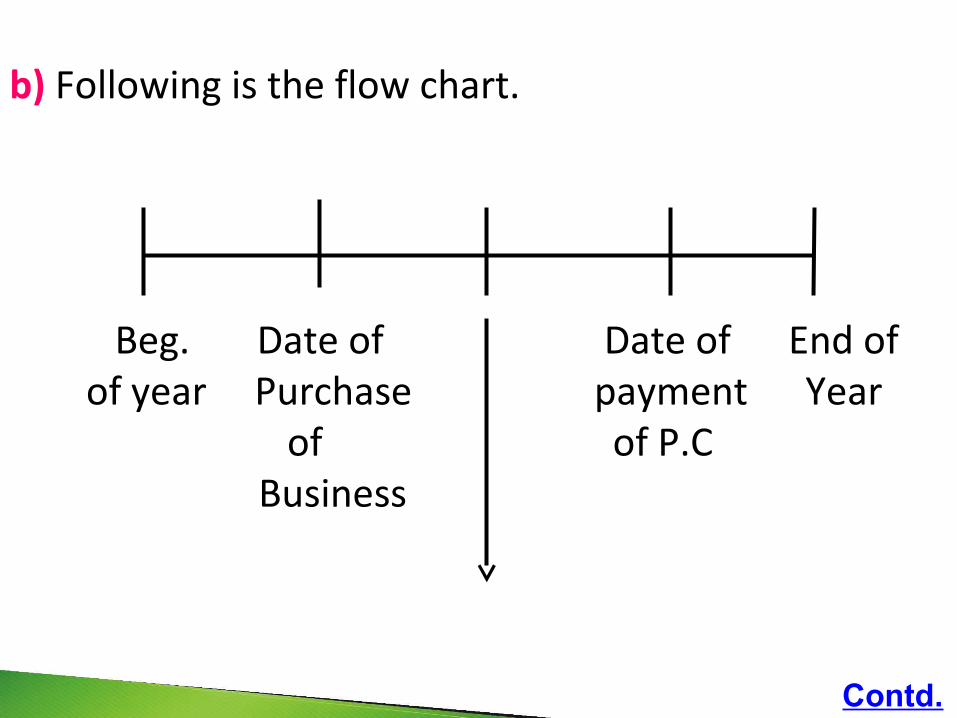

Concept 5Interest to vendors son Purchase Considerationa) Purchase of existing Business has to pay Purchase, in case of any delay in payment of PC, Purchaser has to pay interest to vendors on Purchase Consideration.

Contd.

b) Following is the flow chart.

Beg. Date of Date of End of of year Purchase payment Year of of P.C Business

Contd.

c) Interest paid to Vendors on Purchase Consideration will be divided in new Time Ratio.i.e. Date of Date of Date of Date of Purchase incorporation Incorporation payment of Business to P.C

Concept 6Points to be kept in Minda) In Examination some times, sales Ratio is a difficult task to be calculated so it is better to write all months & then calculate the sales.

b) Preliminary Expenses / Formation Expenses.

i) Those Expenses incurred in relation to formation of a company are named as formation/Preliminary expenses.

Contd.

ii) Preliminary expenses can be written off:- In TO TO In Equal Installments

iii) If Preliminary expenses are to be written off in TOTO then only from capital Profits (Pre- Incorporation Profits)

iv) In case Preliminary expenses are to be written off in parts, then can e written off from post incorporation profits (Revenue Profits)

Related Documents

![[PPT]Auditing Accounts Receivable - Pearson Educationwps.prenhall.com/wps/media/objects/437/448301/ch14.ppt · Web viewTitle Auditing Accounts Receivable Author Prototype Student](https://static.cupdf.com/doc/110x72/5ab7b3757f8b9ad13d8ba788/pptauditing-accounts-receivable-pearson-viewtitle-auditing-accounts-receivable.jpg)