49 Comments to the financial statements Consolidated income statement Consolidated balance sheet Consolidated statement of source and application of funds Consolidated off-balance sheet business Notes to the consolidated financial statements Report of the Group’s auditors Income statement (parent company) Balance sheet before allocation of retained earnings (parent company) Notes to the financial statements (parent company) Proposed allocation of retained earnings Report of the statutory auditors 50 52 54 55 56 58 101 102 103 104 108 109 FINANCIAL REPORT

credit swisseAnnual Report Part 2 Financial report 1998 / 1999

Jun 07, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FINANCIAL REPORT

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 49

Comments to the financial statements

Consolidated income statement

Consolidated balance sheet

Consolidated statement of sourceand application of funds

Consolidated off-balance sheet business

Notes to the consolidated financial statements

Report of the Group’s auditors

Income statement (parent company)

Balance sheet before allocation of retained earnings (parent company)

Notes to the financial statements (parent company)

Proposed allocation of retained earnings

Report of the statutory auditors

50

52

54

55

56

58

101

102

103

104

108

109

49

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 50

COMMENTS TO THE FINANCIAL STATEMENTS

Credit Suisse Group’s Annual Report contains two sets of financial statements: the conso-

lidated annual financial statements of Credit Suisse Group at 31 December 1998 and the

annual financial statements of Credit Suisse Group, parent company, for the financial year

ended 31 March 1999. Both sets of statements have been examined by independent auditors.

Their reports are presented on pages 101 and 109.

The consolidated financial statements include Credit Suisse First Boston, Credit Suisse, Neue

Aargauer Bank, the Private Banks, the financial subsidiaries of Credit Suisse Group in

Guernsey, and Winterthur Insurance.

For the banking and financial businesses, the consolidated financial statements were

prepared pursuant to the accounting rules for banks; for the insurance business, the

accounting rules for insurance companies were applied. “Winterthur” Swiss Insurance

Company (Winterthur) is included in the consolidated financial statements using the pooling

of interests method. Significant information about insurance operations is shown separately

in the balance sheet and income statement; figures for previous periods have been adjusted

as prescribed by the pooling of interests method.

The 1998 financial year As of 1 January 1998, the business activities of Bank Leu Ltd

were focused on private banking. Individual and corporate customer relationships were

transferred to the responsibility of Credit Suisse. On 1 June 1998 (legally into force with

retroactive effect on 1 January 1998) Affida Bank, Zurich, was integrated into Bank Leu

Ltd, Zurich, and Bank Heusser, Basle, into Clariden Bank, Zurich. Affida Bank was fully

amalgamated with Bank Leu’s organisation, whilst the former Bank Heusser retained its

structures and operates under the name “Clariden Heusser, Basel”. On 31 July 1998, the

acquisition of the Garantia Group (São Paulo and Nassau) announced in June 1998 was

completed at a price of USD 675 m. In addition, Credit Suisse First Boston acquired two

leading brokerage firms in Australia and New Zealand, First Pacific Group, Sydney, and

First NZ Capital, Wellington. All these acquisitions are included in the consolidated financial

statements of Credit Suisse First Boston as of the acquisition date. Winterthur sold the

majority of its participation in HIH (Australia) in the first half of 1998; CHF 101 m profit was

recorded in extraordinary income. In the second half of 1998 the sale of Winterthur’s active

reinsurance business to PartnerRe was closed; extraordinary income of CHF 442 m was

recorded from this transaction.

In connection with the class action settlement for World War II, in August 1998

Credit Suisse Group and UBS AG reached a comprehensive settlement with the plaintiffs,

and the settlement contracts were signed in February 1999. Credit Suisse Group expects

its portion of the settlement payment to amount to CHF 381 m after tax. This amount is

included under extraordinary expenses in the Credit Suisse Group’s financial statements

and, as announced when the 1998 half-year results were released, it has been offset by

booking the appropriate sum from reserves for general banking risks to extraordinary income.

In addition, in order to create provisions for credit risks, another CHF 552 m of reserves for

general banking risks have been released through extraordinary income.

50

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 51

Total provisions of CHF 1,349 m were set aside in 1996 and 1997 for Credit Suisse

Group’s expected restructuring costs. Costs of CHF 298 m in 1996, CHF 450 m in 1997

and CHF 456 m in 1998 have been charged to these provisions. At the end of 1998, the

balance of the restructuring provision thus stood at CHF 145 m. In 1997, Credit Suisse

First Boston created provisions of CHF 332 m (CHF 237 m after tax) against extraordinary

expenses to cover expected restructuring costs associated with the acquisition of the Euro-

pean investment banking business of BZW. The integration of the business areas acquired

was completed during 1998, with CHF 204 m of the provision used for the purpose. At

Bank Leu, a provision of CHF 115 m (CHF 82 m after tax) was created against extraordin-

ary expenses in 1997 in order to implement the bank’s new organisational structure, which

became effective on 1 January 1998. CHF 12 m of this provision was used for this pur-

pose in 1997, CHF 75 m in 1998. A provision of CHF 375 m (CHF 300 m after tax) was

made for integration and restructuring costs incurred by the insurance business; a balance

of CHF 165 m remained as at 31 December 1998. Overall, the charges to these restructur-

ing provisions in 1998 amounted to CHF 965 m, leaving a total balance of CHF 446 m in

restructuring provisions. An extraordinary provision of CHF 523 m (CHF 453 m for banking

areas, CHF 70 m for insurance) was created in 1997 to cover technology costs, primarily

those associated with the IT changes required to prepare for the year 2000 and the launch

of the euro. Over the course of 1998, CHF 276 m (CHF 241 m for banking and CHF 35 m

for insurance) of this provision was spent accordingly. At the end of 1998, the total balance

of this provision came to CHF 247 m.

Pursuant to Swiss Stock Exchange legislation, the minority interests in Credit Suisse

First Boston, Credit Suisse and Winterthur were acquired in 1998; Credit Suisse Group

now holds 100% of the voting and ownership rights in the two banks and the insurance

company.

As at 31 March 1998, CS Life was transferred from Credit Suisse Group to Winterthur

and subsequently retroactively merged with the latter’s existing life insurance company,

Winterthur Life, as at 1 January 1998.

On 1 January 1999, the method of tax assessment in the Canton of Zurich was

changed to the current-year method. The figure for Swiss taxes in the 1998 income state-

ment thus includes a one-off relief from tax due to the Canton of Zurich amounting to

CHF 118 m.

Subsequent events On 15 February 1999, Credit Suisse Group announced the acquisition

of Warburg Pincus Asset Management Inc., and a stake of 19.9% in Warburg, Pincus & Co.’s

private equity business. Subject to regulatory approval, this transaction is scheduled to close

in June 1999.

Following organisational changes at Credit Suisse First Boston which combine the

Fixed Income division and Credit Suisse Financial Products into a new division, in April

1999 Credit Suisse Group repurchased Swiss Re’s 20% minority position in Credit Suisse

Financial Products.

51

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 52

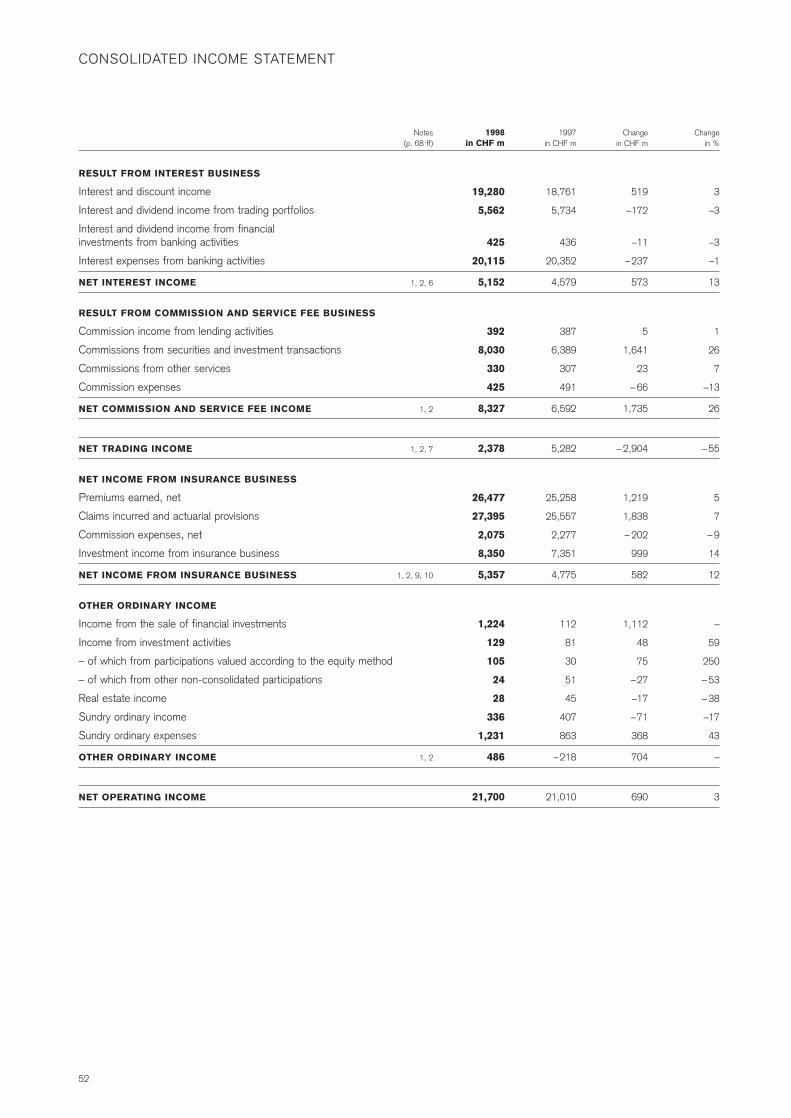

RESULT FROM INTEREST BUSINESS

Interest and discount income

Interest and dividend income from trading portfolios

Interest and dividend income from financial investments from banking activities

Interest expenses from banking activities

NET INTEREST INCOME

RESULT FROM COMMISSION AND SERVICE FEE BUSINESS

Commission income from lending activities

Commissions from securities and investment transactions

Commissions from other services

Commission expenses

NET COMMISSION AND SERVICE FEE INCOME

NET TRADING INCOME

NET INCOME FROM INSURANCE BUSINESS

Premiums earned, net

Claims incurred and actuarial provisions

Commission expenses, net

Investment income from insurance business

NET INCOME FROM INSURANCE BUSINESS

OTHER ORDINARY INCOME

Income from the sale of financial investments

Income from investment activities

– of which from participations valued according to the equity method

– of which from other non-consolidated participations

Real estate income

Sundry ordinary income

Sundry ordinary expenses

OTHER ORDINARY INCOME

NET OPERATING INCOME

Changein %

3

–3

–3

–1

13

1

26

7

–13

26

– 55

5

7

– 9

14

12

–

59

250

– 53

– 38

–17

43

–

3

Changein CHF m

519

–172

–11

–237

573

5

1,641

23

– 66

1,735

– 2,904

1,219

1,838

– 202

999

582

1,112

48

75

–27

–17

–71

368

704

690

1997in CHF m

18,761

5,734

436

20,352

4,579

387

6,389

307

491

6,592

5,282

25,258

25,557

2,277

7,351

4,775

112

81

30

51

45

407

863

–218

21,010

1998in CHF m

19,280

5,562

425

20,115

5,152

392

8,030

330

425

8,327

2,378

26,477

27,395

2,075

8,350

5,357

1,224

129

105

24

28

336

1,231

486

21,700

Notes(p. 68 ff)

1, 2, 6

1, 2

1, 2, 7

1, 2, 9, 10

1, 2

CONSOLIDATED INCOME STATEMENT

52

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 53

NET OPERATING INCOME CONTINUED

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

Valuation adjustments, provisions and losses from banking business

DEPRECIATION, VALUATION ADJUSTMENTS, LOSSES

GROUP PROFIT BEFORE EXTRAORDINARY ITEMS AND TAXES

Extraordinary income

Extraordinary expenses

Taxes

GROUP PROFIT

Minority interests

NET PROFIT (AFTER MINORITY INTERESTS)

Changein %

3

7

12

8

– 6

11

21

19

– 28

17

– 84

– 46

435

–28

–

Changein CHF m

690

655

494

1,149

– 459

67

551

618

–1,077

231

– 2,961

– 499

2,614

–57

2,671

1997in CHF m

21,010

9,931

3,979

13,910

7,100

590

2,624

3,214

3,886

1,323

3,534

1,074

601

204

397

1998in CHF m

21,700

10,586

4,473

15,059

6,641

657

3,175

3,832

2,809

1,554

573

575

3,215

147

3,068

Notes(p. 68 ff)

1, 2

1

1, 8

1, 3

1, 4

1, 2

1

53

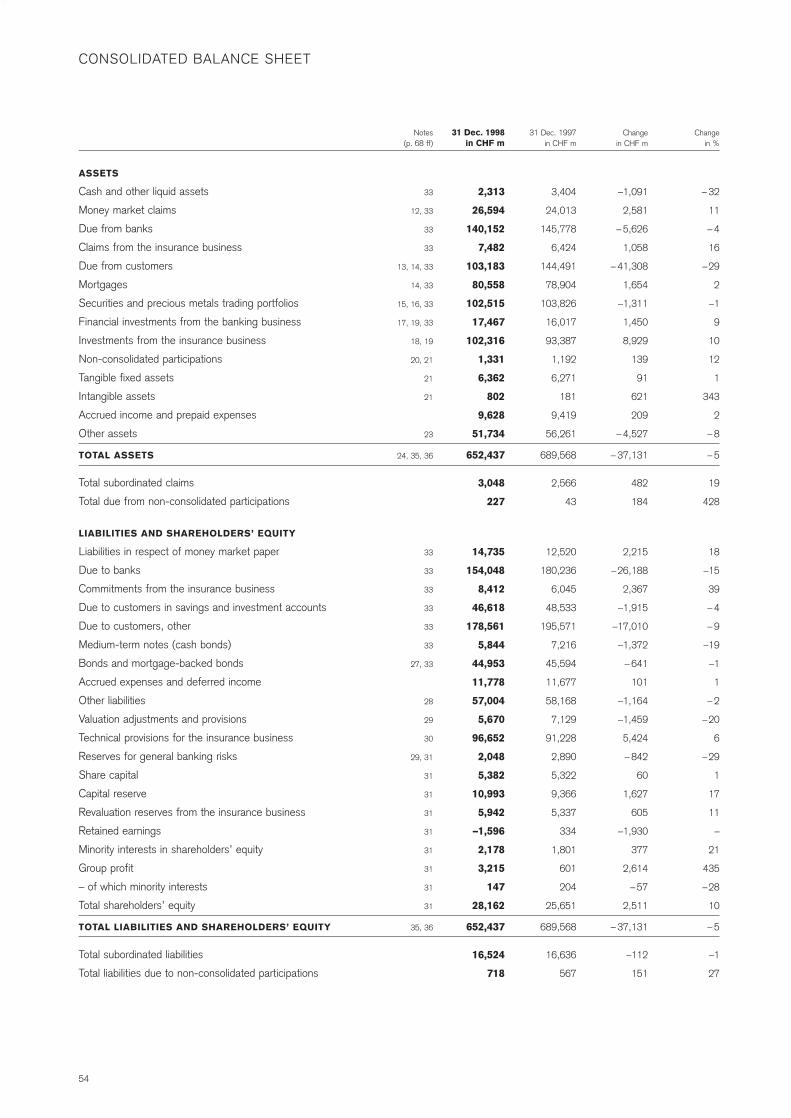

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 54

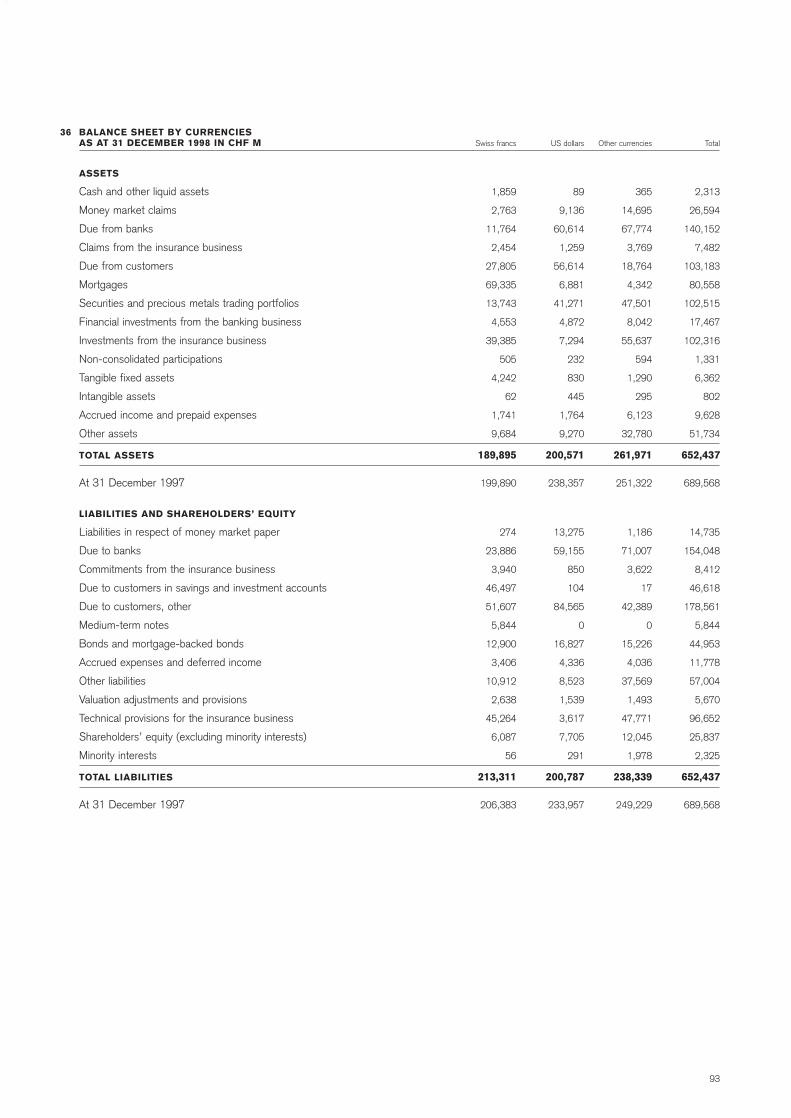

LIABILITIES AND SHAREHOLDERS’ EQUITY

Liabilities in respect of money market paper

Due to banks

Commitments from the insurance business

Due to customers in savings and investment accounts

Due to customers, other

Medium-term notes (cash bonds)

Bonds and mortgage-backed bonds

Accrued expenses and deferred income

Other liabilities

Valuation adjustments and provisions

Technical provisions for the insurance business

Reserves for general banking risks

Share capital

Capital reserve

Revaluation reserves from the insurance business

Retained earnings

Minority interests in shareholders’ equity

Group profit

– of which minority interests

Total shareholders’ equity

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY

Total subordinated liabilities

Total liabilities due to non-consolidated participations

ASSETS

Cash and other liquid assets

Money market claims

Due from banks

Claims from the insurance business

Due from customers

Mortgages

Securities and precious metals trading portfolios

Financial investments from the banking business

Investments from the insurance business

Non-consolidated participations

Tangible fixed assets

Intangible assets

Accrued income and prepaid expenses

Other assets

TOTAL ASSETS

Total subordinated claims

Total due from non-consolidated participations

Notes(p. 68 ff)

33

12, 33

33

33

13, 14, 33

14, 33

15, 16, 33

17, 19, 33

18, 19

20, 21

21

21

23

24, 35, 36

CONSOLIDATED BALANCE SHEET

31 Dec. 1998in CHF m

2,313

26,594

140,152

7,482

103,183

80,558

102,515

17,467

102,316

1,331

6,362

802

9,628

51,734

652,437

3,048

227

31 Dec. 1997in CHF m

3,404

24,013

145,778

6,424

144,491

78,904

103,826

16,017

93,387

1,192

6,271

181

9,419

56,261

689,568

2,566

43

Changein CHF m

–1,091

2,581

– 5,626

1,058

– 41,308

1,654

–1,311

1,450

8,929

139

91

621

209

– 4,527

– 37,131

482

184

Changein %

– 32

11

– 4

16

–29

2

–1

9

10

12

1

343

2

– 8

– 5

19

428

33

33

33

33

33

33

27, 33

28

29

30

29, 31

31

31

31

31

31

31

31

31

35, 36

14,735

154,048

8,412

46,618

178,561

5,844

44,953

11,778

57,004

5,670

96,652

2,048

5,382

10,993

5,942

–1,596

2,178

3,215

147

28,162

652,437

16,524

718

12,520

180,236

6,045

48,533

195,571

7,216

45,594

11,677

58,168

7,129

91,228

2,890

5,322

9,366

5,337

334

1,801

601

204

25,651

689,568

16,636

567

2,215

–26,188

2,367

–1,915

–17,010

–1,372

– 641

101

–1,164

–1,459

5,424

– 842

60

1,627

605

–1,930

377

2,614

– 57

2,511

– 37,131

–112

151

18

–15

39

– 4

– 9

–19

–1

1

– 2

–20

6

–29

1

17

11

–

21

435

–28

10

– 5

–1

27

54

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 55

FROM OPERATIONS, EQUITY TRANSACTIONS AND INVESTMENTS

OPERATING ACTIVITIES

Net profit for the year

Provisions for credit and other risks

Losses

Provisions for taxes

Depreciation and write-offs

Creation of extraordinary valuation adjustmentsand provisions

Extraordinary income

Valuation of companies valued accordingto the equity method

Accrued income and prepaid expenses

Accrued expenses and deferred income

EQUITY TRANSACTIONS

Share capital

Capital surplus and retained earnings

Dividends paid

Foreign exchange differences

Minority interests

INVESTMENTS IN LONG-TERM ASSETS

Investments in companies

Real estate

Other tangible and intangible fixed assets

FINANCIAL INVESTMENTS, PROVISIONS,OTHER ASSETS AND LIABILITIES

Investments from the banking business

Investments from the insurance business

Valuation adjustments and provisions

Technical provisions 1

Other assets

Other liabilities

FROM OTHER BALANCE SHEET ITEMS

ASSETS

Money market claims

Due from banks

Claims from the insurance business

Due from customers

Mortgages

LIABILITIES

Liabilities in respect of money market paper

Due to banks

Commitments from the insurance business

Due to customers in savings and investment accounts

Due to customers, other

Bonds and medium-term notes

CHANGE IN LIQUID ASSETS

Securities and precious metals trading portfolios

Cash and accounts with central banks

1 In line with insurance practice, the change in the technical provisions is shown as a total amount under changes in provisions affecting the cash flow.

1997Net in/outflow

in CHF m

–24

8,317

1,746

93

–10,180

18,942

–15,833

34,775

18,918

Applicationin CHF m

1,213

30

1,916

1,114

38

1,000

4,436

12,274

1,198

14,642

3,936

23,133

407

2,227

14,336

Sourcein CHF m

601

2,617

133

1,250

617

3,330

2,928

1,436

1,358

104

813

280

7,378

14,992

13,870

1,284

1,033

1,237

29,008

16,549

18,446

472

1998Net

in/outflowin CHF m

1,186

5,917

226

– 874

– 4,083

– 3,588

38,956

– 42,544

– 2,402

Applicationin CHF m

1,488

105

209

1,457

363

1,430

1,450

8,929

3,108

1,164

2,581

1,058

3,265

26,188

1,915

17,010

2,013

1,311

1,091

Sourcein CHF m

3,215

2,584

101

575

681

462

101

60

1,922

64

514

42

5,424

5,144

5,626

40,234

2,215

2,367

CONSOLIDATED STATEMENT OF SOURCE AND APPLICATION OF FUNDS

55

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 56

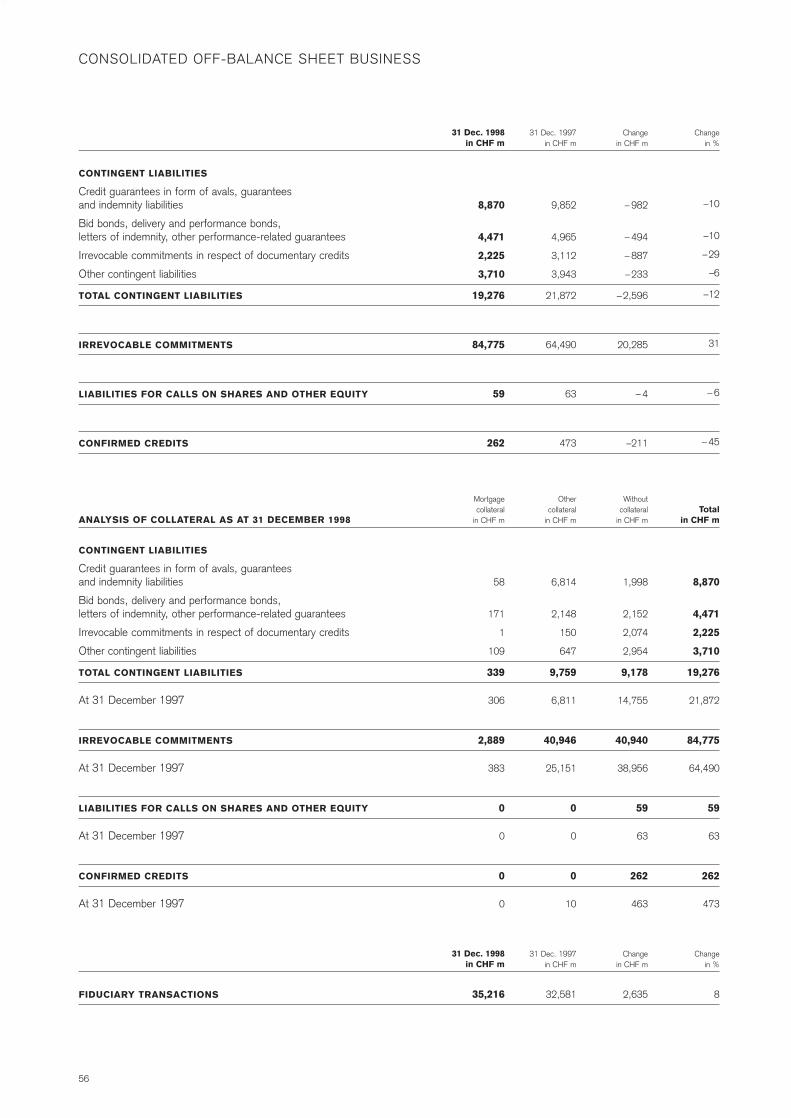

ANALYSIS OF COLLATERAL AS AT 31 DECEMBER 1998

CONTINGENT LIABILITIES

Credit guarantees in form of avals, guarantees and indemnity liabilities

Bid bonds, delivery and performance bonds,letters of indemnity, other performance-related guarantees

Irrevocable commitments in respect of documentary credits

Other contingent liabilities

TOTAL CONTINGENT LIABILITIES

At 31 December 1997

IRREVOCABLE COMMITMENTS

At 31 December 1997

LIABILITIES FOR CALLS ON SHARES AND OTHER EQUITY

At 31 December 1997

CONFIRMED CREDITS

At 31 December 1997

FIDUCIARY TRANSACTIONS

CONTINGENT LIABILITIES

Credit guarantees in form of avals, guarantees and indemnity liabilities

Bid bonds, delivery and performance bonds, letters of indemnity, other performance-related guarantees

Irrevocable commitments in respect of documentary credits

Other contingent liabilities

TOTAL CONTINGENT LIABILITIES

IRREVOCABLE COMMITMENTS

LIABILITIES FOR CALLS ON SHARES AND OTHER EQUITY

CONFIRMED CREDITS

Changein %

–10

–10

–29

–6

–12

31

– 6

– 45

Changein CHF m

– 982

– 494

– 887

–233

–2,596

20,285

– 4

–211

31 Dec. 1997in CHF m

9,852

4,965

3,112

3,943

21,872

64,490

63

473

31 Dec. 1998in CHF m

8,870

4,471

2,225

3,710

19,276

84,775

59

262

CONSOLIDATED OFF-BALANCE SHEET BUSINESS

Total in CHF m

8,870

4,471

2,225

3,710

19,276

21,872

84,775

64,490

59

63

262

473

Changein %

8

Withoutcollateral

in CHF m

1,998

2,152

2,074

2,954

9,178

14,755

40,940

38,956

59

63

262

463

Changein CHF m

2,635

Othercollateral

in CHF m

6,814

2,148

150

647

9,759

6,811

40,946

25,151

0

0

0

10

31 Dec. 1997in CHF m

32,581

Mortgagecollateral

in CHF m

58

171

1

109

339

306

2,889

383

0

0

0

0

31 Dec. 1998in CHF m

35,216

56

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 57

DERIVATIVE INSTRUMENTS

INTEREST RATE PRODUCTS

Forward rate agreements

Swaps

Options bought and sold (OTC)

Forwards

Futures

Options bought and sold (traded)

TOTAL INTEREST RATE PRODUCTS

FOREIGN EXCHANGE PRODUCTS

Forwards1

Swaps 2

Options bought and sold (OTC)

Futures

Options bought and sold (traded)

TOTAL FOREIGN EXCHANGE PRODUCTS

PRECIOUS METALS PRODUCTS

Forwards1

Options bought and sold (OTC)

Futures

Options bought and sold (traded)

TOTAL PRECIOUS METALS PRODUCTS

EQUITY/INDEX-RELATED PRODUCTS

Forwards

Options bought and sold (OTC)

Futures

Options bought and sold (traded)

TOTAL EQUITY/INDEX-RELATED PRODUCTS

OTHER PRODUCTS

Forwards

Options bought and sold (OTC)

Futures

Options bought and sold (traded)

TOTAL OTHER PRODUCTS

TOTAL, GROSS

TOTAL REPLACEMENT VALUESACCORDING TO THE BALANCE SHEET

1 including outstanding spot transactions2 cross-currency interest rate swaps3 positive replacement value after deduction of CHF 4.4 bn (1997: CHF 3.1 bn) of assets pledged as security4 No replacement values are shown for traded derivatives (futures and traded options) subject to daily margining requirements.

Total positive and negative replacement values on traded derivatives amount to CHF 1.4 bn and CHF 2.1 bn respectively.5 of which from the insurance business: positive replacement values CHF 1.3 bn (1997 CHF 0.4 bn), negative replacement values CHF 0.6 bn (1997 CHF 0.2 bn)

31 Dec. 1997Negative gross

replacementvalue

in CHF bn

0.1

38.2

5.0

0.0

–

–

43.3

17.7

10.3

5.7

–

–

33.7

2.0

0.7

–

–

2.7

0.0

10.4

–

–

10.4

0.0

0.0

–

–

0.0

90.1

50.9 5

31 Dec. 1997Positive gross

replacementvalue

in CHF bn

0.3

39.6

5.1

0.0

–

–

45.0

19.2

9.2

5.3

–

–

33.7

1.6

0.5

–

–

2.1

0.1

10.4

–

–

10.5

0.0

0.1

–

–

0.1

91.4

50.2 3, 5

31 Dec. 1997Notionalamount

in CHF bn

193.7

1,551.2

598.3

0.1

420.8

219.0

2,983.1

667.6

216.8

534.2

0.4

0.1

1,419.1

26.3

8.6

1.8

0.0

36.7

2.0

204.4

21.0

63.4

290.8

0.0

3.1

9.5

0.6

13.2

4,742.9

31 Dec. 1998Negative gross

replacementvalue 4

in CHF bn

0.1

60.3

8.8

0.3

–

–

69.5

16.9

11.6

6.1

–

–

34.6

1.1

0.9

–

–

2.0

0.6

14.7

–

–

15.3

0.0

0.1

–

–

0.1

121.5

49.2 5

31 Dec. 1998Positive gross

replacementvalue 4

in CHF bn

0.1

65.3

8.5

0.2

–

–

74.1

14.7

9.3

5.5

–

–

29.5

0.9

0.5

–

–

1.4

0.7

13.8

–

–

14.5

0.0

0.3

–

–

0.3

119.8

43.13, 5

31 Dec. 1998Notionalamount

in CHF bn

152.7

2,383.1

914.1

54.0

539.2

633.8

4,676.9

782.2

247.4

342.3

1.5

0.3

1,373.7

18.8

15.4

0.2

0.4

34.8

8.2

191.4

38.6

63.2

301.4

0.1

4.0

8.5

0.1

12.7

6,399.5

57

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 58

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

GENERAL PRINCIPLES

The Group financial statements have been drawn up based on the accounting rules of

the Implementing Ordinance to the Swiss Federal Law on Banks and Savings Banks of

1 February 1995 and the Federal Banking Commission guidelines of 14 December

1994 (with the amendments of 14 November 1996 and 22 October 1997), supple-

mented by the pooling of interests method and the provisions of the Swiss accounting

and reporting recommendations with respect to insurance companies (FER 14). As

required by the pooling of interests method, the consolidated financial statements of

Credit Suisse Group show the combined results of Credit Suisse Group and Winterthur

as if the merger had been effective for all previous periods shown. In addition, the

consolidation and valuation policies reflect the accounting principles set out in the

Swiss stock exchange listing regulations; they also largely conform to the provisions of

the 4th and 7th EU directives and the EU directive governing the financial statements

of banks. The financial year for the Group ends on 31 December. Group companies

with a different closing date prepare interim financial statements as at 31 December for

consolidation purposes. For subsidiaries acquired after 1 January 1997, goodwill

(the amount paid in excess of the equity acquired when purchasing an interest in a

company) is stated in the balance sheet under “Intangible assets” and amortised over

its estimated useful life (not exceeding 20 years).

SCOPE AND METHOD OF CONSOLIDATION

The assets and liabilities, off-balance sheet transactions and income and expenses

of all the banking, insurance and financial institutions in which Credit Suisse Group

has a direct or an indirect interest of more than 50% as of the balance sheet date are

fully consolidated in the financial statements. For the “Winterthur” Swiss Insurance

Company subgroup, the capital is consolidated according to the pooling of interests

method. For the other Group companies the capital is consolidated according to the

purchase method as of 1 January 1990 (or later, if acquired thereafter). Intercompany

transactions and unrealised gains therefrom are eliminated. Minority interests in share-

holders’ equity and net profit are indicated separately, but are viewed as forming an

integral part of the corporate base. Other companies in which the Group has a stake of

20% or more are accounted for using the equity method. Long-term holdings which are

designated for resale are booked as “Financial investments”. Subsidiaries and long-term

holdings outside the core business, and less significant holdings are not consolidated.

58

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 59

CHANGES TO THE SCOPE OF CONSOLIDATION

The scope of consolidation has undergone the following material changes:

Group division Winterthur Insurance

HIH Winterthur, Sydney

The majority participation in HIH Winterthur of 51.2% was sold mid-1998. The approximately

7% stake still held by the Winterthur Group is included in investments from the insurance

business. HIH Winterthur was deconsolidated retroactively as at 1 January 1998.

Winterthur Reinsurance Corporation of America, New York

Winterthur Life U.S. Holdings, Inc., Wilmington

Winterthur Life Re Insurance Company, Dallas

The investments in the three above mentioned companies were sold as at 1 October

1998. Thus, the income statements of these companies are only included up to

30 September 1998.

Group division Credit Suisse First Boston

Banco di Investimentos Garantia S.A., São Paulo

Garantia Banking Limited, Nassau

For a price of USD 675 m, Credit Suisse First Boston took over 100% of the share

capital of both companies as at 31 July 1998. The companies operate under the name

of Banco de Investimentos Credit Suisse First Boston Garantia S.A. and Credit Suisse

First Boston Garantia Banking Limited respectively.

BZW business areas in the Asian region

In early 1998 selected BZW business areas in Asian investment banking were

acquired. The names of the individual companies are listed in note 37.

FOREIGN CURRENCY TRANSLATIONS

In the annual accounts of the individual Group companies, income and expense items

denominated in foreign currencies are translated into the relevant local reporting curren-

cies on the basis of the exchange rate as of the transaction date. Assets, liabilities and

off-balance sheet items are translated as of the year-end rate. Hedged assets and

liabilities are carried at their forward hedging rates. For the purposes of consolidation,

the balance sheets of foreign Group companies are translated into Swiss francs at the

year-end exchange rate, and their income statements are translated using the average

exchange rate for the financial year. Translation differences are credited or debited to

shareholders’ equity and are shown separately in the statement of shareholders’ equity.

The key foreign exchange rates are listed in the notes to the consolidated financial

statements on page 100.

59

60

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 60

DEVIATIONS FROM THE RELEVANT EU DIRECTIVES

The Swiss accounting rules for banks conform in essence to EU directives and guidelines.

The areas in which Group accounting policies deviate from the accounting principles set

out in the directives of the European Union (4th and 7th EU directives and the EU direc-

tive governing the financial statements of banks) can be summarised as follows:

– The classification criteria used in the balance sheet and the income statement differ

from those set out in the EU directive governing the financial statements of banks.

– The proportions of overall income and expenditure for operations outside Switzerland

are not detailed by geographical location but are provided as combined totals.

– No specific information is given concerning compensation or liabilities towards Members

of the Board of Directors or Members of the Executive Board of Credit Suisse Group.

– Securities and precious metals treated as trading positions are carried at their fair value.

Historical differences between cost and fair value are not disclosed in the notes to the

financial statements.

– Subsidiaries and long-term holdings which are not in the banking, finance or insurance

sectors are not consolidated.

– There is no formal management report on the business year.

The following are significant deviations from the EU directives governing the financial

statements of insurance companies:

– The classification and presentation used in the financial statements have been adjusted

from those set out in the EU directives governing the financial statements of insurance

companies. Winterthur Group publishes an annual report which focuses on the presentation

of the result of the insurance business.

– Unrealised gains on life business investments are taken to revaluation reserves as part

of shareholders’ equity and not to funds for future distribution to shareholders and

policyholders.

GENERAL ACCOUNTING AND VALUATION PRINCIPLES

Recording of business All completed business is recorded in the financial statements

as follows: foreign exchange, money market and precious metal transactions are recorded

on value (settlement) date. Prior to the value date, foreign exchange and precious metal

transactions are recorded as off-balance sheet business. Securities transactions are

recorded on a trade date basis.

Reclassification of prior year figures Certain amounts in the consolidated financial

statements for 1997 have been reclassified to conform to the 1998 presentation. Material

reclassification: In the insurance business, stamp duty is no longer included in “Tax expenses”

but in “Operating expenses” (1997: CHF 132 m) and in “Investment income”

(1997: CHF 44 m).

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 61

Repo business Repurchase and reverse repurchase transactions are shown in the

balance sheet as advances secured by securities or as deposits against which the

bank’s securities are pledged. Depending on the type of counterparty, they are shown

as claims on (“Due from”) or liabilities to (“Due to”) banks or customers. They are carried

in the balance sheet at the amounts at which the securities were initially acquired or

sold as specified by the respective agreements, plus interest accrued to the balance

sheet date.

Transactions involving non-monetary assets Claims and liabilities from lending

and borrowing transactions of non-monetary assets such as money market paper,

precious metals or commodities and those arising from securities lending and borrowing

are marked to market and, depending on the counterparty, are shown as claims on

or liabilities towards banks or customers. Securities positions arising as a result of

securities lending and borrowing are included in the securities and precious metals

trading portfolios.

Cash, bank balances, money market paper and loans Receivables and liabilities

are generally accounted for at nominal value. Money market instruments held for

trading are carried at their fair value. The necessary provisions for recognisable risks

and potential losses are normally deducted from the appropriate asset items in the

balance sheet. Endangered interest and commission income due from customers and

banks are not booked as “Income from interest business”. Instead, they are only included

in the income statement following payment. Provisions for exposures subject to country

risk, default risks and other bank risks are booked to “Valuation adjustments and

provisions”. This position contains no undisclosed reserves.

Leasing All leased items (capital goods, vehicles and real estate) are valued using

the annuity method and are stated as a separate item under lendings. The depreciation

charges contained in the rental income are set off directly against the book values of

the corresponding leased assets, so that only the interest portion of the rental income is

shown in the income statement.

Real estate Real estate is valued at the cost (including capital improvements) less

depreciation over its useful life (40–67 years). No depreciation is charged on land

except where valuation adjustments have been made to allow for a reduction in the

market value.

61

62

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 62

Other tangible fixed assets Other tangible fixed assets such as computers,

machinery, furnishings, vehicles and other equipment, as well as alterations and impro-

vements to rented premises, are depreciated using the straight line method over their

estimated useful life (in general 3–5 years).

Intangible assets The goodwill included in this balance sheet position arises from

the majority holdings acquired from 1 January 1997 in connection with the capital

consolidation. This goodwill is amortised over its estimated useful life (maximum 20 years).

Pension fund As a rule, employees are affiliated to legally autonomous staff pension

funds which are independent of the Group. The requisite contributions are made to the

pension funds and posted under “Personnel expenses”.

Taxes Tax expense is calculated on the basis of the annual results reported in the

individual financial statements of the Group companies. Deferred tax assets and liabili-

ties are established for the expected future tax implications of temporary differences

between the carrying amounts and the tax bases of assets and liabilities. Deferred tax

assets and liabilities calculated at the expected tax rate on the basis of adjustments in

the valuation of assets and liabilities for Group purposes are charged to tax expense

and recorded as other assets or provisions. No provision is made for non-recoverable

withholding taxes on undistributed profits of Group companies nor is a deferred tax

asset recognised arising from tax losses brought forward.

Claims and liabilities of related companies Claims and liabilities in respect of

related companies towards Group companies which are accounted for using the equity

method are reported in the notes to the consolidated financial statements.

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 63

VALUATION AND ACCOUNTING POLICIES IN RELATION

TO BANK-SPECIFIC POSITIONS

Securities trading portfolio The trading portfolio consists of balances held in

connection with the trading of readily realisable securities, securities acquired as a

result of underwriting activities and holdings of precious metals. Securitised and non-

securitised options are shown under “Other assets”.

Trading balances in bonds, shares and similar securities and precious metal

accounts and holdings are carried at fair value (amount for which an asset could be

exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s-

length transaction) as of the balance sheet date. Profits and losses from the valuation

of the trading portfolio and realised gains and losses on these positions are shown

under “Income from trading”. Interest and dividend income from the trading portfolio is

credited to “Result from interest business”.

Financial investments from the banking business This balance sheet item

comprises securities and precious metal positions purchased as a long-term invest-

ment. It also includes real estate and holdings assumed from the lending business

and designated for resale.

Fixed-interest debt securities which are being held until final maturity are valued

according to the accrual method. In this case, premiums and discounts are accrued or

deferred over the term of the instrument until final maturity in the relevant balance sheet

position. Realised profits or losses which are interest related and which arise from the

early disposal or redemption of the instrument are accrued or deferred over the remain-

ing term of the instrument, i.e. to the original final maturity, and credited to or debited

from “Result from interest business” as appropriate.

Investment holdings of equities and debt securities which are designated for

resale and which do not constitute trading balances are valued according to lower of

cost or market. The notes to the consolidated financial statements include details of

both the cost price and the market value of these holdings.

Capital gains resulting from the sale of financial investments at above the

purchase price are shown under “Income from the sale of financial investments”.

Unrealised losses on equity positions as a result of a decrease in their market value, and

unrealised profits up to the original result of changes in creditworthiness, are accounted

for in the same way as credit business.

Real estate assumed from the lending business and designated for resale is

valued according to lower of cost or market.

63

64

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

03_CSGB_E_Financial Report 1.5.1999 15:36 Uhr Seite 64

Reserves for general banking risks Reserves for general banking risks are precau-

tionary reserves charged to “Extraordinary expenses” to hedge against latent risks in the

bank’s operating activities. Releases are credited to extraordinary income.

Derivatives Forward rate agreements, futures, swaps, options, forward contracts and

other over-the-counter off-balance sheet instruments held for trading purposes are

carried at their fair value and the resulting profits and losses are included in “Net trading

income” in the income statement. The resulting replacement values are included in

“Other assets” or “Other liabilities” as appropriate and are presented net by counterparty

for transactions in those products where the bank has a legal right of set off; otherwise

the replacement values are presented gross by contract.

Hedging transactions are valued using the same procedures as for the underlying

transactions they hedge.

Strategic positions are valued at lower of cost or market. Derivative financial

instruments which are deployed in the context of interest rate risk management are

valued according to the accrual method. The interest component is accrued or deferred

over the term of the instrument according to the annuity method. Realised profits or

losses which are interest related and which arise from the early disposal or redemption

of the instrument are also accrued or deferred over the remaining term of the instru-

ment, i.e. to the original final maturity.

CHANGES TO ACCOUNTING PRINCIPLES

Endangered interest Starting in 1998, the set up and release of provisions for

endangered interest is recorded under “Interest income”. Prior to 1998, provisions set

up for endangered interest overdue for less than 90 days and the reclassification of

provisions for endangered interest, which were no longer necessary from an economic

point of view, were recorded under “Valuation adjustments, provisions and losses”. The

prior year’s financial statements have not been restated. Impact on the 1998 financial

statement:

Net interest income: CHF – 99 m

Valuation adjustments, provisions and losses: CHF – 99 m

FINANCIAL INVESTMENTS

Assets held in the trading book Assets held in the trading book are carried at their

fair values as at the 1998 balance sheet date. Prior to 1998, the trading portfolio was

valued at market value. Assets that were not traded on a recognised stock exchange or

on a representative market were carried at the lower of cost or market value. The prior

year financial statements have not been restated. Impact on the 1997 consolidated

balance sheet and income statement would be:

Valuation adjustments and provisions: CHF – 69 m

Net trading income: CHF 69 m

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 65

YEAR 2000

The challenge faced by financial institutions worldwide as the year 2000 approaches is

substantial. It extends to almost every aspect of daily operations and interaction with the

markets. Credit Suisse Group began work on the year 2000 issue in 1996, utilising a

priority-driven methodology, encompassing inventory and assessment, remediation or

replacement, testing, third-party risk analysis and contingency planning.

Business-critical systems in the banking area are being addressed first, and, having

identified over 1,500 systems that require remediation, 84% were completed and put

back into production by 31 December 1998. Remediation of non-compliant date formats

has been achieved either by expanding the date format to incorporate four-digit years, or

by “windowing” for century determination. To mitigate third-party risks, during 1998 over

7,000 customers and business partners were contacted in relation to their own year 2000

projects. In addition, the Group’s banks have participated in 30 industry tests during

1998 and are committed to taking part in 59 industry tests planned during 1999. However,

with systems of such size and complexity, with multiple interfaces to and high reliance

upon external systems, no guarantee can be given that there will be no adverse effects

from the year 2000 issue. As a consequence, the banks have started a contingency

planning process which includes the formation of management teams to quickly respond

to unexpected events.

The Board of Directors and the Executive Board of Credit Suisse Group are provided

with regular status reports and have given the highest priority to the year 2000 project.

EVENTS SINCE THE BALANCE SHEET DATE

On 15 February 1999 Credit Suisse Group announced that Credit Suisse Asset Management

will acquire Warburg Pincus Asset Management, Inc., a leading US asset manager with

260 employees and USD 22 bn in assets under management, as well as a 19.9% pas-

sive minority equity stake in Warburg, Pincus & Co.’s private equity business. The price

of the asset management transaction was fixed at USD 650 m, including an initial

USD 450 m and an additional USD 200 m earn-out over three years. Subject to

regulatory approval, the agreement is expected to close by mid-1999.

Following the organisational changes at Credit Suisse First Boston which combine the

Fixed Income division and Credit Suisse Financial Products in a new division, in April 1999

Credit Suisse Group repurchased Swiss Re’s 20% minority position in Credit Suisse

Financial Products.

65

66

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 66

VALUATION AND ACCOUNTING POLICIES IN RELATION

TO INSURANCE-SPECIFIC POSITIONS

INVESTMENTS IN RESPECT OF INSURANCE BUSINESS

Real estate Real estate is valued at the market price. The market value of a property

is calculated at its capitalised rental income at the interest rate applied in the country

or market in question. Undeveloped plots of land and buildings under construction are

carried at cost.

Bonds and loans Bonds and loans are valued according to the amortised cost method.

The difference between the purchase price and the redemption value is distributed over

the remaining life so that a constant yield is achieved. The corresponding valuation

adjustment is shown under the position “Net investment income from insurance busi-

ness”. Default risk is accounted for through the use of write-offs. Intercompany trans-

actions and unrealised gains have been eliminated, with the exception of assets booked

as investments from insurance business.

Shares Listed shares are marked to market at year-end. Unlisted shares are valued

at cost. If the yield or intrinsic value is endangered, a valuation adjustment is made.

Derivatives Derivatives and other financial instruments are generally used to hedge

the exposure to changes in the fair value of recognised assets, liabilities and firm

commitments. Any gains and losses are therefore recognised in the income statement

together with the offsetting loss or gain on the hedged item.

Investments for the benefit of life insurance policyholders who bear the

investment risk Investments for the benefit of life insurance policyholders who bear

the investment risk are carried at their market value.

Statement of higher and lower values arising from the uniform valuation of

investments in the Group accounts and revaluation reserves Higher or lower

values arising from the uniform valuation of investments in the Group accounts in com-

parison with the figures contained in the statutory accounts are recorded as follows:

Valuation differences resulting from the revaluation of fixed-interest securities and

mortgages, unlisted shares and non-consolidated long-term holdings are included in the

income statement (under “Net investment income from insurance business”).

In the case of listed shares and real estate, compensated write-offs in respect of the

difference between the balance sheet value in the statutory accounts and the cost value

are stated in the income statement (“Net investment income from insurance business”).

Valuation differences between cost and market values are allocated to shareholders’ equity

(“Revaluation reserves from the insurance business”) directly, without affecting the income

statement, after deferred tax calculated on the basis of a full provision on unrealised gains

for which there is no contractual obligation to pay to policyholders upon realisation.

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 67

Technical provisions The amount of the technical provisions is based on the ex-

pected liabilities due to the insured and the claimants. As a rule, calculations are made

individually, i.e. depending on the insurance contract or claim. Statistical or mathematical

calculation methods are applied if these lead to approximately the same results and if

they conform to the methods approved by the supervisory authorities of the respective

countries. The equalisation reserves legally prescribed and locally created in some

countries are not included in the Group accounts. As a rule, provisions for claims out-

standing are not discounted. Technical provisions for life business are calculated with

regard to local regulations. The surplus due to policyholders is accounted for on the

basis of the resolutions passed by the individual companies as to the distribution of profit.

CHANGES TO ACCOUNTING PRINCIPLES

Equalisation reserves and discount The amounts taken over from the local

accounts in the previous years in order to create equalisation reserves as well as the

discounts made in accordance with local regulations are no longer considered. The

one-time change-over effect has a positive influence on the income statement

amounting to CHF 71.8 m.

67

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 68

Banking business Insurance business Total1 SPLIT OF INCOME STATEMENT INTO BANKING

AND INSURANCE BUSINESS

Net interest income

Net commission and service fee income

Net trading income

Net income from insurance business

Other ordinary income

NET OPERATING INCOME

Salaries and other compensation

Employee benefits

Other personnel expenses

Personnel expenses

Premises and real estate expenses

Expenses for IT, machinery, furnishing,vehicles and other equipment

Sundry operating expenses

Other operating expenses

Total operating expenses

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

Valuation adjustments, provisions and losses

Total depreciation, valuation adjustments,losses

GROUP PROFIT BEFORE EXTRAORDINARYITEMS AND TAXES

Extraordinary income

Extraordinary expenses

Taxes

GROUP PROFIT

Minority interests

NET PROFIT (AFTER MINORITY INTERESTS)

Expenses due to the handling of both claims and investments are allocated to the income from insurance business.1 personnel expenses CHF 510 m (previous year CHF 573 m)2 other operating expenses CHF 321 m (previous year CHF 312 m)

1997in CHF m

4,579

6,592

5,282

4,775

–218

21,010

8,368

942

621

9,931

773

855

2,351

3,979

13,910

7,100

590

2,624

3,214

3,886

1,323

3,534

1,074

601

204

397

1998in CHF m

5,152

8,327

2,378

5,357

486

21,700

8,919

1,005

662

10,586

885

921

2,667

4,473

15,059

6,641

657

3,175

3,832

2,809

1,554

573

575

3,215

147

3,068

1997in CHF m

0

0

0

4,775 1,2

– 594

4,181

1,401

310

209

1,920 1

242

166

751

1,159 2

3,079

1,102

17

0

17

1,085

0

445

232

408

90

318

1998in CHF m

0

0

0

5,357 1,2

–900

4,457

1,332

325

224

1,881 1

213

137

826

1,176 2

3,057

1,400

90

0

90

1,310

543

0

371

1,482

111

1,371

1997in CHF m

4,579

6,592

5,282

0

376

16,829

6,967

632

412

8,011

531

689

1,600

2,820

10,831

5,998

573

2,624

3,197

2,801

1,323

3,089

842

193

114

79

1998in CHF m

5,152

8,327

2,378

0

1,386

17,243

7,587

680

438

8,705

672

784

1,841

3,297

12,002

5,241

567

3,175

3,742

1,499

1,011

573

204

1,733

36

1,697

68

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 69

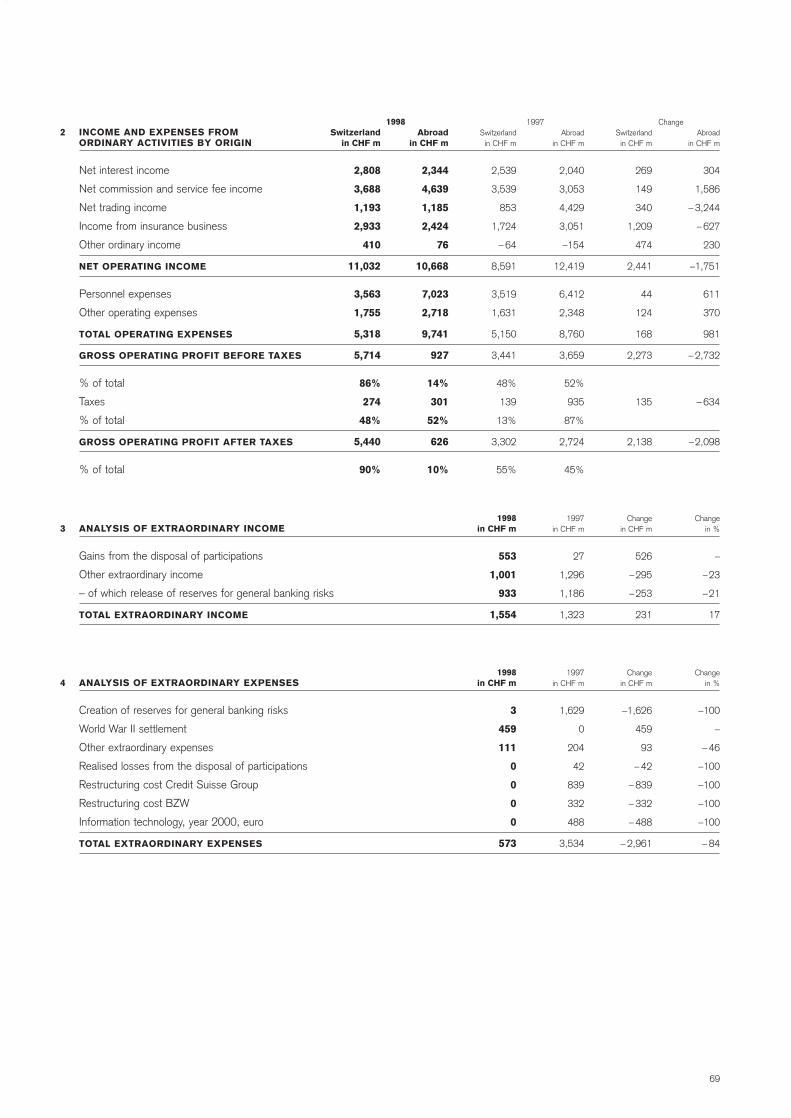

1998 1997 Change2 INCOME AND EXPENSES FROM

ORDINARY ACTIVITIES BY ORIGIN

Net interest income

Net commission and service fee income

Net trading income

Income from insurance business

Other ordinary income

NET OPERATING INCOME

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT BEFORE TAXES

% of total

Taxes

% of total

GROSS OPERATING PROFIT AFTER TAXES

% of total

3 ANALYSIS OF EXTRAORDINARY INCOME

Gains from the disposal of participations

Other extraordinary income

– of which release of reserves for general banking risks

TOTAL EXTRAORDINARY INCOME

4 ANALYSIS OF EXTRAORDINARY EXPENSES

Creation of reserves for general banking risks

World War II settlement

Other extraordinary expenses

Realised losses from the disposal of participations

Restructuring cost Credit Suisse Group

Restructuring cost BZW

Information technology, year 2000, euro

TOTAL EXTRAORDINARY EXPENSES

Abroadin CHF m

304

1,586

– 3,244

– 627

230

–1,751

611

370

981

– 2,732

– 634

–2,098

Changein %

–

–23

–21

17

Changein %

–100

–

– 46

–100

–100

–100

–100

– 84

Switzerlandin CHF m

269

149

340

1,209

474

2,441

44

124

168

2,273

135

2,138

Changein CHF m

526

–295

–253

231

Changein CHF m

–1,626

459

93

– 42

– 839

– 332

– 488

– 2,961

Abroadin CHF m

2,040

3,053

4,429

3,051

–154

12,419

6,412

2,348

8,760

3,659

52%

935

87%

2,724

45%

1997in CHF m

27

1,296

1,186

1,323

1997in CHF m

1,629

0

204

42

839

332

488

3,534

Switzerlandin CHF m

2,539

3,539

853

1,724

– 64

8,591

3,519

1,631

5,150

3,441

48%

139

13%

3,302

55%

1998in CHF m

553

1,001

933

1,554

1998in CHF m

3

459

111

0

0

0

0

573

Abroadin CHF m

2,344

4,639

1,185

2,424

76

10,668

7,023

2,718

9,741

927

14%

301

52%

626

10%

Switzerlandin CHF m

2,808

3,688

1,193

2,933

410

11,032

3,563

1,755

5,318

5,714

86%

274

48%

5,440

90%

69

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 70

5 INCOME STATEMENT OF BANKING BUSINESS

NET INTEREST INCOME

RESULT FROM COMMISSION AND SERVICE FEE ACTIVITIES

Commission income from lending activities

Commissions from securities and investment transactions

Commissions from other services

Commission expenses

NET COMMISSION AND SERVICE FEE INCOME

NET TRADING INCOME

OTHER ORDINARY INCOME

Income from the sale of financial investments

Income from investment activities

– of which from participations valued according to the equity method

– of which from other non-consolidated participations

Real estate income

Sundry ordinary income

Sundry ordinary expenses

OTHER ORDINARY INCOME

NET OPERATING INCOME

Personnel expenses

Other operating expenses

TOTAL OPERATING EXPENSES

GROSS OPERATING PROFIT

Depreciation and write-offs on non-current assets

– of which on real estate

– of which on other tangible and intangible fixed assets

– of which on non-consolidated participations

Valuation adjustments, provisions and losses

DEPRECIATION, VALUATION ADJUSTMENTS, LOSSES

ANNUAL PROFIT BEFORE EXTRAORDINARY ITEMS AND TAXES

Extraordinary income

Extraordinary expenses

Taxes

ANNUAL PROFIT

Minority interests

NET PROFIT (AFTER MINORITY INTERESTS)

Changein %

13

1

26

7

–13

26

– 55

–

65

177

– 59

– 38

14

135

269

2

9

17

11

–13

–1

– 32

6

–

21

17

– 46

– 24

– 81

–76

–

– 68

–

Changesin CHF m

573

5

1,641

23

– 66

1,735

–2,904

1,112

37

53

–16

–17

40

162

1,010

414

694

477

1,171

–757

– 6

– 38

27

5

551

545

–1,302

– 312

–2,516

– 638

1,540

–78

1,618

1997in CHF m

4,579

387

6,389

307

491

6,592

5,282

112

57

30

27

45

282

120

376

16,829

8,011

2,820

10,831

5,998

573

120

453

0

2,624

3,197

2,801

1,323

3,089

842

193

114

79

1998in CHF m

5,152

392

8,030

330

425

8,327

2,378

1,224

94

83

11

28

322

282

1,386

17,243

8,705

3,297

12,002

5,241

567

82

480

5

3,175

3,742

1,499

1,011

573

204

1,733

36

1,697

Notes

6

7

8

70

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 71

6 ANALYSIS OF THE RESULT FROM INTEREST BUSINESS

Interest and discount income

Interest income on claims due from customers

Interest income on claims due from banks

Interest income from money market claims

Credit commissions treated as interest earnings

Interest income from leasing operations

Total interest and discount income

Interest and dividend income from trading portfolios

Interest income

Dividend income

Total interest and dividend income from trading portfolios

Interest and dividend income from financial investments

Interest income

Dividend income

Total interest and dividend income from financial investments

Interest expense

Interest expenses for liabilities due to customers

Interest expenses for liabilities due to banks

Total interest expense

– of which interest expenses for subordinated liabilities

TOTAL INTEREST INCOME

7 ANALYSIS OF TRADING INCOME

Income from securities and commodities trading

Income from foreign exchange and banknote trading

Income from precious metals trading

Income from trading in interest rate instruments

TOTAL TRADING INCOME

8 ANALYSIS OF VALUATION ADJUSTMENTS,PROVISIONS AND LOSSES

For default risks (credit and country risks)

For other business risks

Losses

– of which losses from lending activities

VALUATION ADJUSTMENTS, PROVISIONS AND LOSSES

Changein %

18

–18

26

15

– 3

3

– 8

147

– 3

–7

28

– 3

20

– 31

–1

–14

13

Changein %

– 58

– 86

– 22

–19

– 55

Changein %

18

64

–24

–19

21

Changein CHF m

1,731

–1,464

204

50

–2

519

– 451

279

–172

–28

17

–11

2,414

–2,651

–237

–107

573

Changein CHF m

–1,796

– 874

– 47

–187

–2,904

Changein CHF m

393

190

– 32

–12

551

1997in CHF m

9,634

7,943

775

330

79

18,761

5,544

190

5,734

376

60

436

11,900

8,452

20,352

757

4,579

1997in CHF m

3,085

1,014

210

973

5,282

1997in CHF m

2,193

298

133

64

2,624

1998in CHF m

11,365

6,479

979

380

77

19,280

5,093

469

5,562

348

77

425

14,314

5,801

20,115

650

5,152

1998in CHF m

1,289

140

163

786

2,378

1998in CHF m

2,586

488

101

52

3,175

71

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 72

9 INCOME STATEMENT OF INSURANCE BUSINESS

NON-LIFE BUSINESS

Premiums written

Change in provisions for unearned premiumsand in actuarial provisions (health)

PREMIUMS EARNED

Claims and annuities paid

Change in provision for claims and annuities outstanding

CLAIMS INCURRED

Dividends paid

Change in provision for dividend

DIVIDENDS TO POLICYHOLDERS INCURRED

OPERATING EXPENSES

UNDERWRITING RESULT NON-LIFE

Net investment income

Interest on deposits and bank accounts (incl. exchange rate differences)

Other interest paid

Other income and expenses

PROFIT BEFORE TAX AND MINORITY INTERESTS

LIFE BUSINESS

Premiums written

Change in provisions for unearned premiums

PREMIUMS EARNED

Claims paid

Change in provisions for claims outstanding

CLAIMS INCURRED

CHANGE IN ACTUARIAL PROVISIONS

Bonus allocation

Change in participation fund

ALLOCATION TO PARTICIPATION

OPERATING EXPENSES

Net investment income

Interest on deposits and bank accounts

Interest on bonuses credited to policyholders

Other interest paid

Other income and expenses (incl. exchange rate differences)

PROFIT BEFORE TAX AND MINORITY INTERESTS

Changein %

–10

14

–11

– 9

–37

–12

21

0

14

– 8

0

7

9

38

– 5

18

22

–100

23

16

–

13

27

9

81

18

8

15

75

– 6

60

377

17

Changein CHF m

–1,437

– 57

–1,494

783

451

1,234

– 40

0

– 40

306

6

138

12

–27

10

139

2,602

111

2,713

– 949

141

– 808

–1,958

–121

–169

– 290

– 98

752

89

7

–113

– 230

64

1997in CHF m

13,694

– 397

13,297

– 8,940

–1,214

–10,154

–189

–106

–295

– 4,077

–1,229

2,123

128

–71

–190

761

12,072

–111

11,961

– 6,038

–113

– 6,151

– 7,305

–1,420

–208

–1,628

–1,261

5,006

118

–124

–189

– 61

366

1998in CHF m

12,257

– 454

11,803

– 8,157

–763

– 8,920

–229

–106

– 335

– 3,771

–1,223

2,261

140

– 98

–180

900

14,674

0

14,674

– 6,987

28

– 6,959

– 9,263

–1,541

– 377

–1,918

–1,359

5,758

207

–117

– 302

– 291

430

Notes

10

11

10

11

72

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 73

INCOME STATEMENT OF INSURANCE BUSINESS (continued)

SUMMARY

Profit before tax and minority interests (non-life business)Profit before tax and minority interests (life business)

PROFIT BEFORE TAX, MINORITY INTERESTS, EXTRAORDINARY EXPENSES AND INTEREST ON BONDS

Interest on convertible bonds and warrant issuesExtraordinary expensesIncome from disposal of investments/business areasTax

ANNUAL PROFIT BEFORE MINORITY INTERESTS

Minority interests

ANNUAL PROFIT AFTER MINORITY INTERESTS

10 ANALYSIS OF DIRECT BUSINESS,GEOGRAPHICAL DISTRIBUTION

Europe

Non-life Life

EUROPE, TOTAL

North America

Non-lifeLife

NORTH AMERICA, TOTAL

Asia-Pacific

Non-lifeLife

ASIA-PACIFIC, TOTAL

Other regions

Non-life Life

OTHER REGIONS, TOTAL

DIRECT BUSINESS, GROSS, TOTAL

Reinsurance assumed, gross

Non-life Life

REINSURANCE ASSUMED, GROSS, TOTAL

TOTAL BUSINESS, GROSS

Reinsurance ceded

Non-lifeLife

REINSURANCE CEDED, TOTAL

Business, net

Non-life Life

TOTAL BUSINESS, NET

Home market Switzerland

Non-life Life

HOME MARKET SWITZERLAND, TOTAL

Changein %

18

17

18

– 52

–

–

60

263

23

331

Changein %

4

25

15

– 6

– 71

– 6

– 86

57

– 81

– 4

0

– 4

7

– 45

– 46

– 45

4

–14

166

– 8

–10

22

5

3

38

27

Changein CHF m

139

64

203

22

445

543

–139

1,074

– 21

1,053

Changein CHF m

385

2,897

3,282

–148

–12

–160

–1,334

31

–1,303

–2

0

–2

1,817

– 586

–218

– 804

1,013

248

– 96

152

–1,437

2,602

1,165

92

2,465

2,557

1997in CHF m

761

366

1 127

– 42

– 445

0

– 232

408

–90

318

1997in CHF m

10,064

11,587

21,651

2,498

17

2,515

1,559

54

1,613

48

0

48

25,827

1,309

472

1,781

27,608

–1,784

– 58

–1,842

13,694

12,072

25,766

2,820

6,489

9,309

1998in CHF m

900430

1,330

–200

543– 371

1,482

–111

1,371

1998in CHF m

10,44914,484

24,933

2,3505

2,355

22585

310

460

46

27,644

723254

977

28,621

–1,536–154

–1,690

12,25714,674

26,931

2,9128,954

11,866

73

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

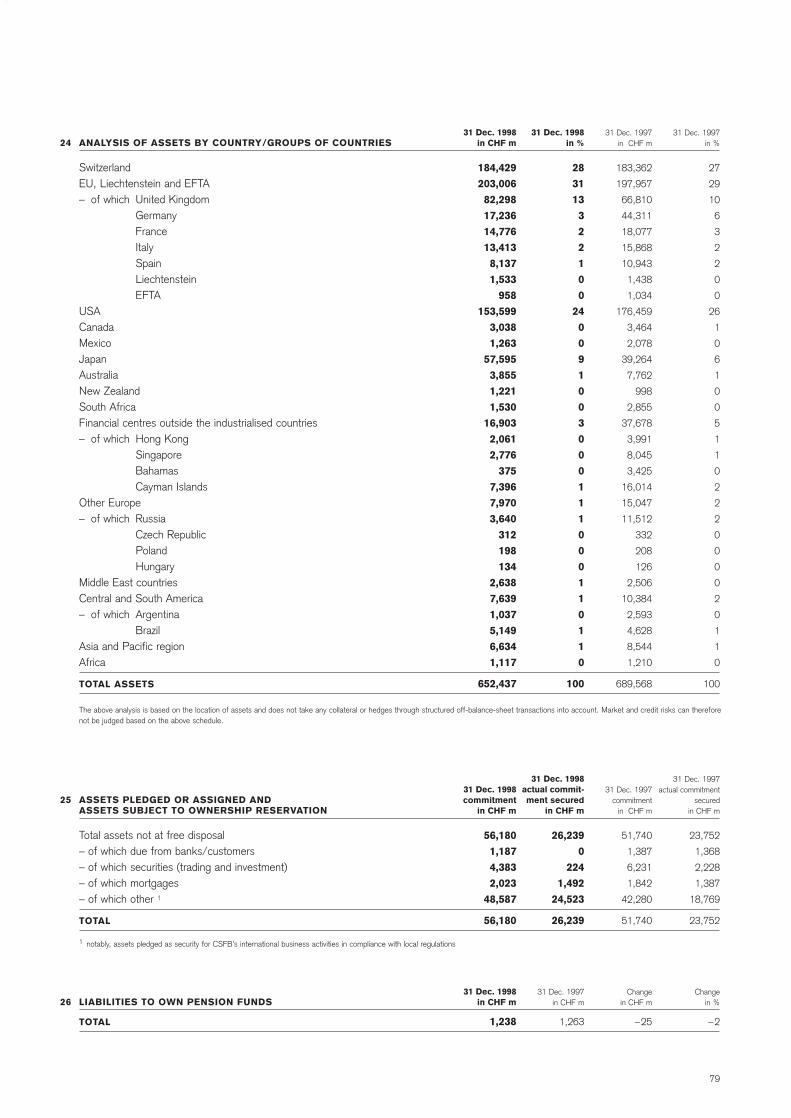

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 74

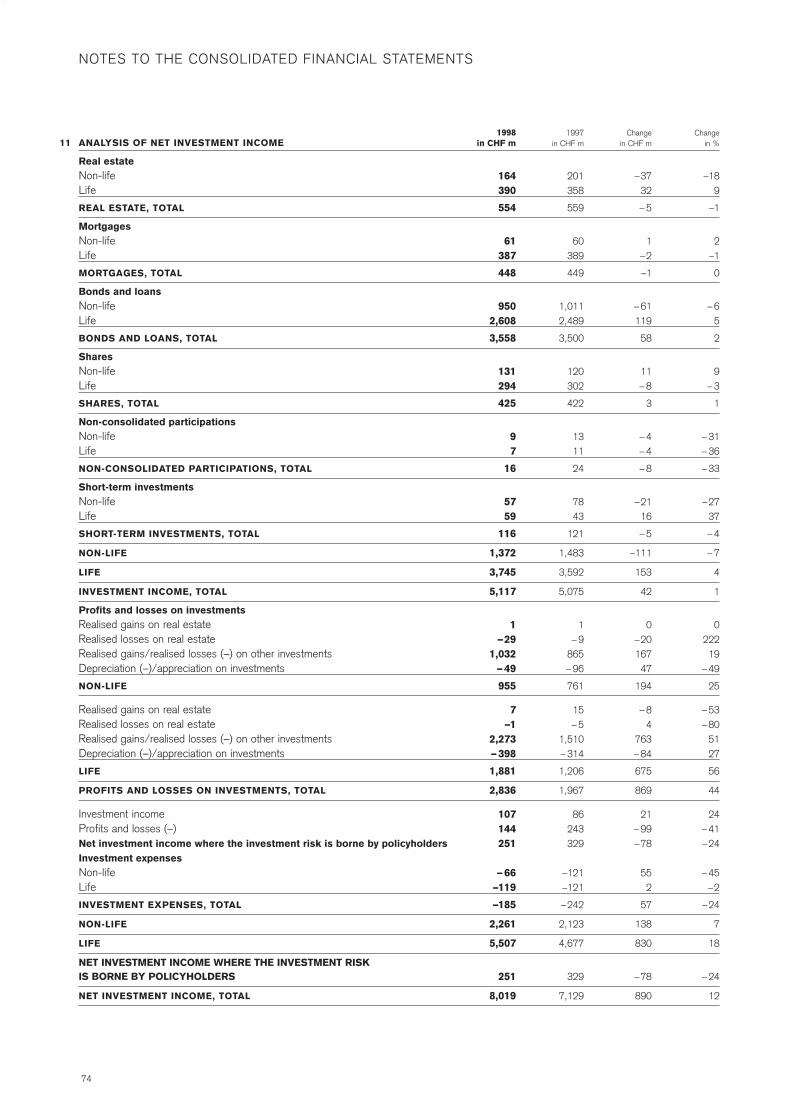

11 ANALYSIS OF NET INVESTMENT INCOME

Real estate Non-lifeLife

REAL ESTATE, TOTAL

MortgagesNon-life Life

MORTGAGES, TOTAL

Bonds and loansNon-life Life

BONDS AND LOANS, TOTAL

SharesNon-life Life

SHARES, TOTAL

Non-consolidated participationsNon-life Life

NON-CONSOLIDATED PARTICIPATIONS, TOTAL

Short-term investmentsNon-life Life

SHORT-TERM INVESTMENTS, TOTAL

NON-LIFE

LIFE

INVESTMENT INCOME, TOTAL

Profits and losses on investmentsRealised gains on real estateRealised losses on real estateRealised gains/realised losses (–) on other investmentsDepreciation (–)/appreciation on investments

NON-LIFE

Realised gains on real estate Realised losses on real estate Realised gains/realised losses (–) on other investmentsDepreciation (–)/appreciation on investments

LIFE

PROFITS AND LOSSES ON INVESTMENTS, TOTAL

Investment incomeProfits and losses (–)Net investment income where the investment risk is borne by policyholdersInvestment expensesNon-life Life

INVESTMENT EXPENSES, TOTAL

NON-LIFE

LIFE

NET INVESTMENT INCOME WHERE THE INVESTMENT RISKIS BORNE BY POLICYHOLDERS

NET INVESTMENT INCOME, TOTAL

Changein %

–189

–1

2–1

0

– 65

2

9– 3

1

– 31– 36

– 33

–2737

– 4

– 7

4

1

022219

– 49

25

– 53– 80

5127

56

44

24– 41–24

– 45–2

–24

7

18

– 24

12

Changein CHF m

–3732

– 5

1–2

–1

– 61119

58

11– 8

3

– 4– 4

– 8

–2116

– 5

–111

153

42

0–2016747

194

– 84

763– 84

675

869

21– 99–78

552

57

138

830

–78

890

1997in CHF m

201358

559

60389

449

1,0112,489

3,500

120302

422

1311

24

7843

121

1,483

3,592

5,075

1– 9

865– 96

761

15– 5

1,510– 314

1,206

1,967

86243329

–121–121

–242

2,123

4,677

329

7,129

1998in CHF m

164390

554

61387

448

9502,608

3,558

131294

425

97

16

5759

116

1,372

3,745

5,117

1–29

1,032– 49

955

7–1

2,273– 398

1,881

2,836

107144251

– 66–119

–185

2,261

5,507

251

8,019

74

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 75

12 MONEY MARKET CLAIMS

Bills of exchange and money market paper rediscountable or pledgeable at central banks

– of which treasury bills

Other bills of exchange and money market paper

TOTAL MONEY MARKET CLAIMS

13 DUE FROM CUSTOMERS FROM FINANCIAL LEASES

Car leasing

Real estate leasing

Leasing of capital goods

TOTAL DUE FROM CUSTOMERS FROM FINANCIAL LEASES

14 ANALYSIS OF LOAN COLLATERAL AT 31 DECEMBER 1998

Due from customers

Mortgages

Residential properties

Business and office properties

Commercial and industrial properties

Other properties

TOTAL LOAN COLLATERAL

At 31 December 1997

15 SECURITIES AND PRECIOUS METALS TRADING PORTFOLIOS

Interest bearing securities and rights

listed on stock exchange

unlisted

– of which own bonds and medium-term notes

Equities

– of which own shares

Precious metals

TOTAL SECURITIES AND PRECIOUS METALS TRADING PORTFOLIOS

– of which securities rediscountable or pledgeable at central banks

Substantial claims and liabilities included in other balance sheet positions.These are valued at fair value and any profit/loss on them is shown under trading income.

Lent trading positions (Due from banks and customers)

Borrowed trading positions (Due to banks and customers)

Positive replacement values of derivative instruments from trading activities (Other assets)

Negative replacement values of derivative instruments from trading activities (Other liabilities)

Changein %

129

340

– 55

11

Changein %

3

3

16

10

Totalin CHF m

103,183

80,558

183,741

223,395

Changein %

– 5

0

–12

–72

8

20

12

–1

– 4

31

20

– 8

–2

Changein CHF m

11,084

12,552

–8,503

2,581

Changein CHF m

9

8

126

143

Without collateral

in CHF m

43,406

43,406

44,171

Changein CHF m

–3,767

129

–3,896

– 852

2,262

393

194

–1,311

–1,322

10,715

6,367

– 4,338

–903

31 Dec. 1997in CHF m

8,585

3,691

15,428

24,013

31 Dec. 1997in CHF m

353

284

777

1,414

Othercollateral

in CHF m

53,581

53,581

92,370

31 Dec. 1997in CHF m

72,597

41,009

31,588

1,185

29,624

1,951

1,605

103,826

29,508

34,244

31,120

51,384

51,316

31 Dec. 1998in CHF m

19,669

16,243

6,925

26,594

31 Dec. 1998in CHF m

362

292

903

1,557

Mortgagecollateral

in CHF m

6,196

80,558

52,912

11,339

9,337

6,970

86,754

86,854

31 Dec. 1998in CHF m

68,830

41,138

27,692

333

31,886

2,344

1,799

102,515

28,186

44,959

37,487

47,046

50,413

75

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

03_CSGB_E_Financial Report 30.4.1999 21:17 Uhr Seite 76

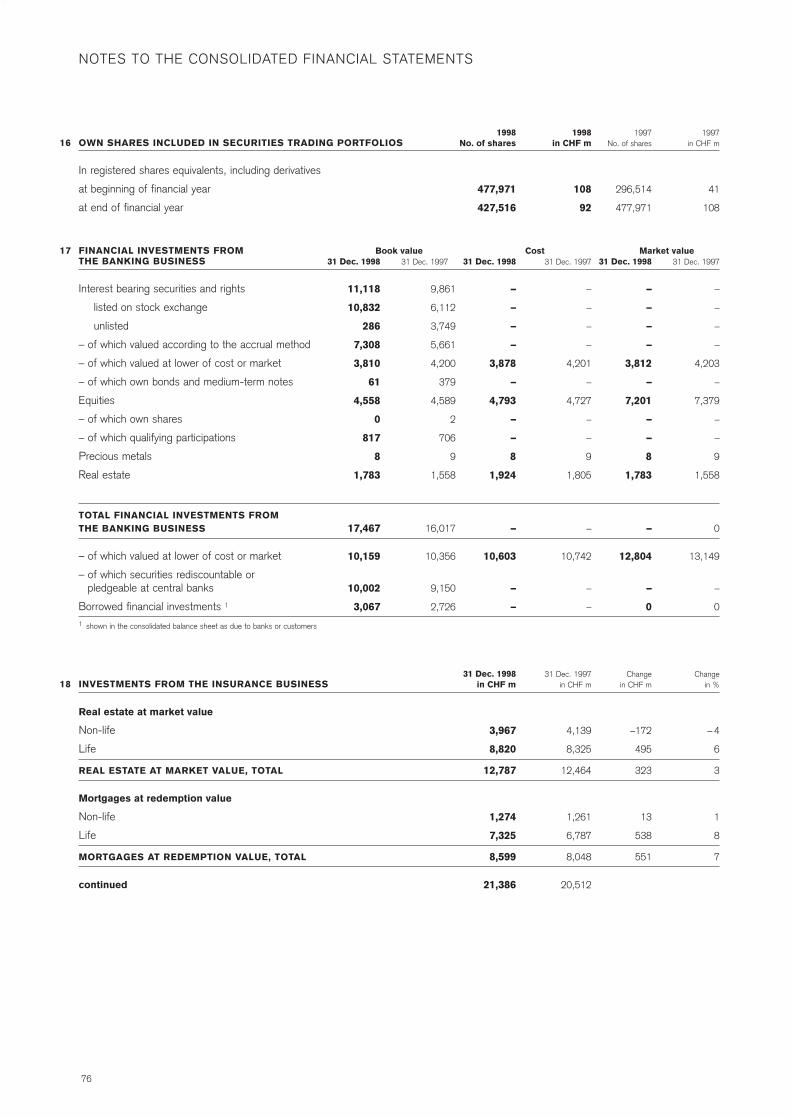

16 OWN SHARES INCLUDED IN SECURITIES TRADING PORTFOLIOS

In registered shares equivalents, including derivatives

at beginning of financial year

at end of financial year

17 FINANCIAL INVESTMENTS FROM Book value Cost Market valueTHE BANKING BUSINESS

Interest bearing securities and rights

listed on stock exchange

unlisted

– of which valued according to the accrual method

– of which valued at lower of cost or market

– of which own bonds and medium-term notes

Equities

– of which own shares

– of which qualifying participations

Precious metals

Real estate

TOTAL FINANCIAL INVESTMENTS FROM THE BANKING BUSINESS

– of which valued at lower of cost or market

– of which securities rediscountable or pledgeable at central banks

Borrowed financial investments 1

1 shown in the consolidated balance sheet as due to banks or customers

18 INVESTMENTS FROM THE INSURANCE BUSINESS

Real estate at market value

Non-life

Life

REAL ESTATE AT MARKET VALUE, TOTAL

Mortgages at redemption value

Non-life

Life

MORTGAGES AT REDEMPTION VALUE, TOTAL

continued

1997in CHF m

41

108

31 Dec. 1997