Credit Suisse 2007 Oil & Gas Conference Marco Mangiagalli CFO London, June 5th, 2007

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Credit Suisse 2007Oil & Gas Conference

Marco MangiagalliCFO

London, June 5th, 2007

2

Eni’s Growth Strategy

E&P:Increase production, replace reserves and build a global LNG position

G&P:Grow internationally and preserve Italian gas business

R&M:Enhance refining profitability and marketing network

Technolo

gy

Op

era

tio

na

l E

ffic

ien

cy

3

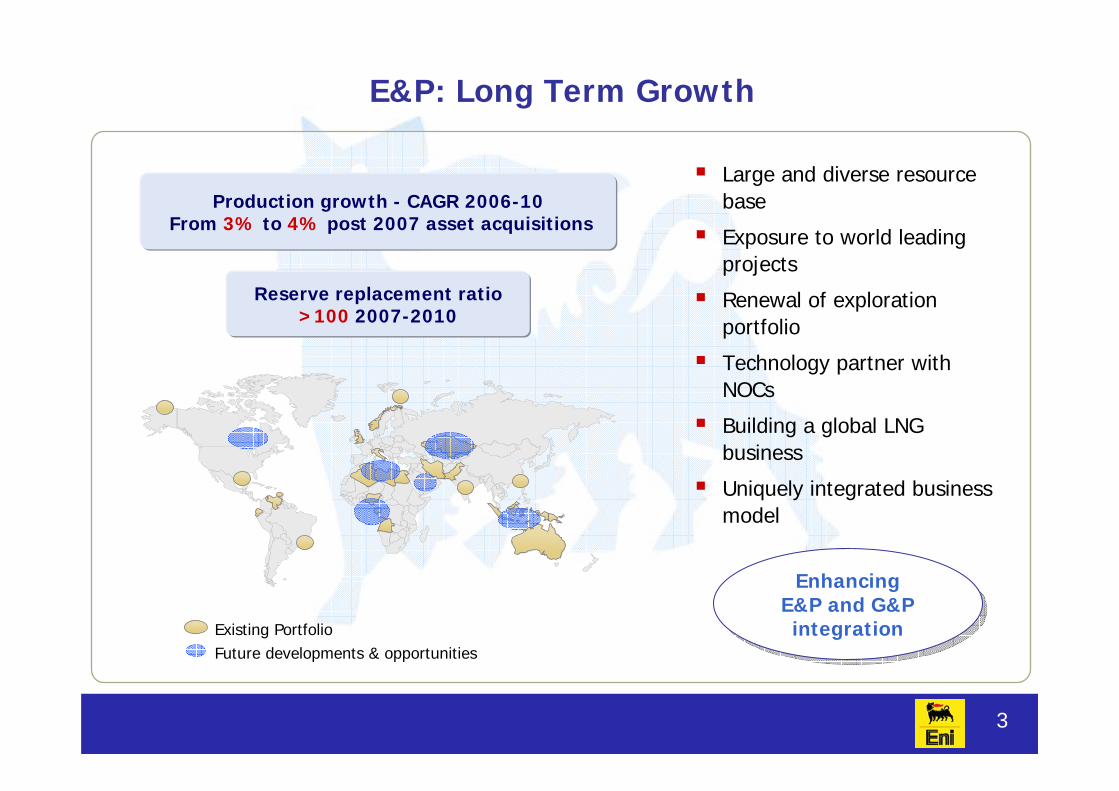

E&P: Long Term Growth

Large and diverse resource base

Exposure to world leadingprojects

Renewal of explorationportfolio

Technology partner withNOCs

Building a global LNG business

Uniquely integrated business model

Existing PortfolioFuture developments & opportunities

Reserve replacement ratio>100 2007-2010

EnhancingE&P and G&P integration

EnhancingE&P and G&P integration

Production growth - CAGR 2006-10From 3% to 4% post 2007 asset acquisitions

4

12.1 10.8 10.0

Proved Reserves and Resources

2005 2006

6.46.87.2

2004

Organic Reserves Replacement2004-06 at 40 $/bl:

106%

65

23

105

38

4091

40.5 58.2 58.9

Proved Reserves(SEC rules)

* Proved + Unproved Reserves + Risked Exploration

Proved Total*Proved+Probable

2006 Total Resources (40$/bl brent)

10.8 >19 >38

>25

Solid Resource Base to SustainLong Term Growth

7.0

Reservesreplacement (%)

Year-end Brent ($/bl)

Life index(year)

Reserves(Billion boe)

all sourcesorganic

12.5

5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2003 2004 2005 2006

Successful Exploration and Portfolio Renewal...

Per year Cumulative

Added Resources(Bln boe)

2.8

• MALI5 blocks onshore

• MOZAMBIQUE1 block offshore

• TIMOR EAST5 blocks offshore

New AreasCore Areas

• NIGERIA1 block offshore

• NORWAY1 licence offshore

• PAKISTAN4 blocks onshore

• USA1 block GoM48 blocks Alaska

• ANGOLA1 block offshore (Bl. 15)

• BRAZIL1 block offshore

• CONGO3 blocks offshore

• EGYPT1 block offshore

• MOROCCO1 block onshore

Resources added per year (2003/06): 700 Mboe

Average ROS SEC 2003-06: ~ 50%

Portfolio renewal: 68% of total acreage in 3 years

High quality portfolio added2003/06 cumulativeproduction

2006 new net acreage:152,000 sqkm, 99% operated

2.4

6

G&P: Robust Cash Generation

Long term contract portfolio, equity gas and LNG

Widespread international infrastructure

Strong position in growing markets

Direct access to customers

Exploit dual offer

Pipeline

Eni markets

LNG ongoing

LNG existing

Pipeline

Eni markets

LNG ongoing

LNG existing

Free Cash Flow:2.1 billion in 2010

CAGR 3% (2006-2010)

7

G&P: Targets

Growth in international sales

58%

97International

sales*

Italy 46%

42%

2006 2010

>105

54%

NewTarget

(bln €)

20102006

Free cash flow

1.92.1

PreviousTarget

2009

1.9**

Maintain strength in domestic

market

Increase operational efficiency

* Including Extra Europe gas sales and E&P equity gas sold in Europe (4 Bcm) ** Normalized to exclude inventory changes and extraordinary commercial credits/debits

50%

2009

>100

50%

PreviousTarget

Gas sales

CAGR 2006-10: ~10%

outside Italy

CAGR 2006-10: ~10%

outside Italy

NewTarget

Potential Upside

2.2

(bcm)

8

Regulated business

International pipelines

Marketing and Power

24%

59% 80%

ItalyInternational

Free Cash Flow Generation Target

2006 2010

Activity

17%20%

50% 50%

2006 2010

1.9*2.1

Billion € Areas

* Normalized to exclude inventory changes and extraordinary commercial credits/debits

9

Increase premium product sales and non-oil activities

Grow sales in Europe

Efficiency programme

Focused investment programme

• Grow refinery throughput• Increase conversion index

Pursue operational efficiency

REFINING

MARKETING

R&M: Improving Profitability

International retail presence Refineries

2010/2006 +40% ebit increaseat 2006 scenario

10

Marketing

Refining

2006 2010

Estimate

Throughput* (Mln ton)

Conversion Index (%)

38.0 40.2 >43.0

41 44

2013

46

Target

57 5861

Improve conversion index and middle distillate yieldIncrease refinery throughputEnhance operational efficiency

Middle Distillate Yield (%)

2006 2010

15.8 17.4

2.5 2.7

Throughput in Europe (Mln lt/ss)Retail sales in Europe (Bln liters)

Increase sales in EuropeImprove retail network economicsEfficiency programme

High turnaround

potential

High turnaround

potential

R&M Targets

(*) Excluding processing for third parties of 1.8 Mln ton/y

11

Disciplined Capex Increase

Billion €

35.2

44.6

36%

16%

48%

Other

PSA

Regulated

2006-2009 E&Pincremental

inflation

AdditionalActivities

2007-2010capex plan

37.1 2.35.2

Strong and selective investment programme 70% of additional capex devoted to grow the businessBalancing risk vs return

1.9

SRG consolidation

and forex

2006-2009pro-forma

€ blnRegulated 2 Refiningupgrading 0.6Saipem new vessels 1.1 29.6

6.7

4.34.0

E&P

G&P

R&MOthers

12

Attractive Dividend & Buy Back

Dividend

2004

0.90

2003

1.10

2005

0.75

€/share

Dividend up 13.6%

Dividendpayment

0.45

0.65

5.7 billion € 2000-YTD (1Q07) share buy back (8.6% of capital)1.7 billion € still availableShare buy back

October 2006: 0.60 € per shareJune 2007: 0.65 € per share

2006 dividend sustainable in the

2007-10 period2006

1.25

0.60

0.65

13

Recent Acquisitions

Core strategic area

Financial discipline

Strong contribution to long term growth

14

The Strategic Rationale

Enter hydrocarbon rich regions and strengthen presence in core areas

Boost growth in the four year plan and beyond - 2006-10 CAGR: 4%

Add valuable resources: over 2 billion boe

Operatorship

Exploration potential

Improve competitive positioning in central Europe

Improve integration with local refining capacity

Strengthen existing marketing network

E&P

R&M

15

New Gulf of Mexico Assets

Miocene

LegacyFields

FrontRunner

Devil TowerThunderhawk

Egom

NeptuneRigel

Main PassNewOrleans

Cash consideration US$ 4,757 bn

Increase materiality in a key area:

- 222 million boe 2P reserves

- from 36 to over 110 kboe/d (effective July 1st 2007)

Strengthen operatorship in the Gulf of Mexico

High exploration potential

EPS and CFPS accretive from 2007

272 Blocks~ 60% operated0.78 Million Net Acres

53 Fields70% of 2P reservesin 8 fields

Production Exploration Core Areas Shelf/StateShelf/State DeepwaterDeepwaterDominion assets

16

Strategic partnership with Gazprom

Access to significant resources: ~ 1.5 billion boe

Sustain production growth in the long term

Leverage on operational skills and technology

Gazprom has an option to acquire a 51% interest within 2 years

If Gazprom exercises its call option:

Eni’s cash consideration: US$ 0.63 bn

Eni’s interest: 30%

Arctic Gas and Urengoil

“SINT” Assets

Moscow

17

Congo Assets

Assets acquisition completed in May

Commercial assets - M’BOUNDI: 43.1%, KOUAKOUALA A: 66.7% KOUAKOUALA B, C, D: 50%

Exploration license - KOUILOU: 48%

Cash consideration: US$ 1.28 bn

2P reserves: 112 Mboe

Acquired assets equity production: 18% CAGR 2007-10

Original Oil in place ~ 1.4 GblOriginal Oil in place ~ 1.4 Gbl

Operatorship

Strengthen materiality in a legacy country

Production growth in medium term

Reserves upside

High exploration potential

18

Other E&P recent acquisitions

Alaska Angola

TAPS

Nikaitchuq

Operatorship and 70% stake in the Nikaitchuq field

2P reserves: 70 Mboe

First oil 2009

13.6% stake in A-LNG

New 5 million-ton LNG plant

Monetize currently untapped reserves

Regasification capacity of 5 bcm/y in Pascagoula

19

Eastern Europe Downstream Activities

102 retail stations in Czech Republic, Slovakia, Hungary

16.11% stake in Czech Refining Company

Enhance Eni’s integrated marketing and refining activities

Increase local refining capacity to 2.6 mln tons per year

Improve network quality: 4.9 mln lt/y throughput per site

Acquired assets

Industrial Rationale

Synergies

EPS accretiveFinancial Impact

Related Documents