Credit Risk Analysis in Indian Commercial Banks- An Empirical Investigation Authors: Swaranjeet Arora Assistant Professor (SG), Prestige Institute of Management and Research, Indore, India. Email: [email protected] Abstract Risk exposure in banking system has increased due to fierce competition, changing socio- economic patterns, market flexibility, and increased foreign exchange business and cross border activities. These developments have resulted into various types of banking risks. Credit risk, earlier present in the banking system has also increased and Credit risk analysis has emerged as a big challenge for the Indian commercial banks. This paper attempts to identify the factors that contribute to Credit Risk analysis in Indian banks and to compare Credit Risk analysis practices followed by Indian public and private sector banks, the empirical study has been conducted and views of employees of various banks have been tested using statistical tools. Present study explored the phenomenon from different perspectives and revealed that Credit Worthiness analysis and Collateral requirements are the two important factors for analyzing Credit Risk. From the descriptive and analytical results, it can be concluded that Indian banks efficiently manage credit risk. The results also indicate that there is significant difference between the Indian Public and Private sector banks in Analyzing Credit Risk. Keywords: Risk management; Banks; Credit Risk Introduction “Granting credit involves - accepting risk as well as producing profits” -Bank for international settlements, Basel, Switzerland There has been tremendous transition in the role of bank as a financial intermediary. Before liberalization all the activities of banks were regulated and hence operational environment was not conducive to risk taking. Now, banks have grown from being a financial intermediary into a risk intermediary. Banks are exposed to severe competition and hence are compelled to encounter various types of financial and non-financial risks. Risks and uncertainties form an integral part of banking which by nature entails taking risks. Banks are now required to clearly discriminate avoidable and unavoidable risks and are required to focus on the extent to which such risks can be taken by banks. The banking reforms and policy changes during the years have gradually changed banking landscape and credit market in India. First visible change is that banks are now more customer focused and are providing innovative products at fast pace, Second change is that deregulation has made the banks free to formulate their own schemes and products as per their market segment and risk appetite, redesign business process and lending policies and procedures to meet changing expectations of the customers and the market. Thirdly, introduction of risk management practices and implementation of Basel II recommendations have brought in more professional approach in credit delivery process which is now more risk focused and has made pricing of loan-products dependent on risk perception of the borrower and likely hood of default. Fourth visible change is that banks are moving from so called lazy banking to busy banking by aggressively Asia-Pacific Finance and Accounting Review ISSN 2278-1838: Volume 1, No. 2, Jan - Mar 2013

Credit Risk Analysis

Dec 07, 2015

Credit Risk Analysis in

Indian Commercial Banks

Indian Commercial Banks

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Credit Risk Analysis in Indian Commercial Banks-An Empirical Investigation

Authors:Swaranjeet AroraAssistant Professor (SG), Prestige Institute of Management and Research, Indore, India. Email: [email protected]

AbstractRisk exposure in banking system has increased due to fierce competition, changing socio-

economic patterns, market flexibility, and increased foreign exchange business and cross

border activities. These developments have resulted into various types of banking risks.

Credit risk, earlier present in the banking system has also increased and Credit risk analysis

has emerged as a big challenge for the Indian commercial banks. This paper attempts to

identify the factors that contribute to Credit Risk analysis in Indian banks and to compare

Credit Risk analysis practices followed by Indian public and private sector banks, the

empirical study has been conducted and views of employees of various banks have been

tested using statistical tools. Present study explored the phenomenon from different

perspectives and revealed that Credit Worthiness analysis and Collateral requirements are

the two important factors for analyzing Credit Risk. From the descriptive and analytical

results, it can be concluded that Indian banks efficiently manage credit risk. The results also

indicate that there is significant difference between the Indian Public and Private sector

banks in Analyzing Credit Risk.

Keywords: Risk management; Banks; Credit Risk

Introduction

“Granting credit involves - accepting risk as well as

producing profits”

-Bank for international settlements, Basel, Switzerland

There has been tremendous transition in the role of bank as

a financial intermediary. Before liberalization all the

activities of banks were regulated and hence operational

environment was not conducive to risk taking. Now, banks

have grown from being a financial intermediary into a risk

intermediary. Banks are exposed to severe competition and

hence are compelled to encounter various types of financial

and non-financial risks. Risks and uncertainties form an

integral part of banking which by nature entails taking

risks. Banks are now required to clearly discriminate

avoidable and unavoidable risks and are required to focus

on the extent to which such risks can be taken by banks.

The banking reforms and policy changes during the years

have gradually changed banking landscape and credit

market in India. First visible change is that banks are now

more customer focused and are providing innovative

products at fast pace, Second change is that deregulation

has made the banks free to formulate their own schemes

and products as per their market segment and risk appetite,

redesign business process and lending policies and

procedures to meet changing expectations of the customers

and the market. Thirdly, introduction of risk management

practices and implementation of Basel II recommendations

have brought in more professional approach in credit

delivery process which is now more risk focused and has

made pricing of loan-products dependent on risk

perception of the borrower and likely hood of default.

Fourth visible change is that banks are moving from so

called lazy banking to busy banking by aggressively

Asia-Pacific Finance and Accounting ReviewISSN 2278-1838: Volume 1, No. 2, Jan - Mar 2013

expanding credit to retail, agriculture and small and

medium enterprises. Fifth visible change is that banks are

gradually becoming super market where they will not only

lend but also offer whole gamut of financial products

including third party products so that customer gets

opportunity to select best product at competitive price. All

these changes are on the one hand creating new business

opportunities and on the other hand also creating new

challenges, which banks will have to face boldly and

proactively (Mehrotra, 2005).

Banking risk results into Expected and Unexpected losses.

Banks rely on their capital as a buffer to absorb such losses.

Chakrabarti and Chawla (2005) suggested that banks must

plough back profit to build profound and solid reserve

base. According to experts banks need to maintain enough

capital for prudential corrective action to prevent any risk

(Bhat 2005). The efficiency of capital plays a major role in

this exercise and banks are advised to adopt risk

management practices. Eichengreen (1999) identifies the

policies of the new international financial architecture as

crisis prevention, crisis prediction and crisis management.

In spite of heavy regulations in the last two decades, many

developed and emerging countries have witnessed severe

banking crises. There is an imperative need to follow

internationally compatible prudential norms relating to

capital structure and supervisory norms. Banks are

required to develop the system which involves minimum

risk exposure.

Credit risk in commercial banks represents the most

important type of risk. Banks bear the credit risk attached to

bank loans and forward contracts. The risk of defaults or

protracted arrears on outstanding loan is termed as credit

risk (Tamimi, H. and Mazrooei, F., 2007). According to the

consultative paper issued by the Basel Committee on

Banking Supervision (1999), for most banks loans are the

largest and most obvious sources of credit risk. Credit Risk

is the potential that a bank borrower or counter party fails

to meet the obligations on agreed terms. It mainly arises

from the potential that a borrower or counterparty will fail

to perform on an obligation. It may arise from either an

inability or an unwillingness to perform in the pre-

committed contracted manner.

Financial markets in developing economies are not sound

and efficient and are predominantly occupied by State-

owned firms. State-owned firms, especially in banking

sector, are commonly found in many developing countries

(La Porta et al. 2002). Banking Policies and Strategies are

formed depending upon type and structure of ownership

of a bank. Organizational culture, attitude and behaviors

also vary according to type of bank ownership i.e. Private-

owned banks and state owned banks. This difference leads

to different levels of risk- taking behavior and banks

performance (Arora, S. and Jain, R.; 2011) and in turn

26

results into varying level of Credit Risk in different types of

banks. This paper is aimed to examine the degree to which

Indian banks analyze Credit Risk and attempts to identify

the factors that contribute to Credit Risk Analysis in

different commercial banks and to compare whether Public

and Private Sector banks efficiently analyze Credit risk.

Various researchers have studied reasons behind bank

problems and identified several factors (Santomero, 1997;

Basel, 1999, Basel, 2004). Bindseil, U. and Papadia, F. (2006)

reviewed the role and effects of the collateral frameworks

which central banks, and in particular the Euro system, use

in conducting temporary monetary policy operations.

They explained the design of such a framework from the

perspective of risk mitigation, which is the purpose of

collateralization. They identified that by means of

appropriate risk mitigation measures, the residual risk on

any potentially eligible asset can be equalized and brought

down to the level consistent with the risk tolerance of the

central bank. Once this result has been achieved, eligibility

decisions should be based on an economic cost-benefit

analysis. They also looked at the effects of the collateral

framework on financial markets, and in particular on

spreads between eligible and ineligible assets.

Gilbert and Wilson (1998) examined the impact of banking

deregulation on the productive efficiency of Korean

private banks during the 1980 and 1994 reporting

productive efficiency improvements following the 1980s

deregulation. A banking crisis can also be initiated by a

high level of unexpected non-performing loans in a bank.

When this information is known by the depositors, they

rush to the bank to get back their deposits before the other

depositors. If markets for liquidity are inefficient because

of market power or information asymmetries, liquidity

problems at healthy banks can turn into solvency

problems. In fact, in this case the bank is forced to sell its

long-term assets below their fair value, see, e.g., Allen and

Gale (1998), Bernanke and Gertler (1989), Donaldson

(1992), Kiyotaki and Moore (1997), and Kwan and Eisenbis

(1997) demonstrate that inefficient banks are more prone to

risk-taking.

Relationship between capital, risk and efficiency varies for

banks with different ownership structures. However, there

is little empirical guidance to suggest whether there are

systematic differences in the relationship between risk

taking, capital strength and efficiency for banks with

different ownership features. Much of the literature on

banking in emerging markets focuses on either the broad

relationship between ownership and financial

performance (e.g., Sarkar, Sarkar and Bhaumik, 1998) or

the agency aspect of ownership, i.e., the impact of

separation between management and ownership on the

Literature Review

Swaranjeet Arora

performance of banks (e.g., Gorton and Schmid, 1999;

Hirshey, 1999).

Previous studies found that foreign-owned banks

outperform domestic-owned banks in developing

countries (Havrylchyk 2003). State-owned banks

underperform domestic-owned banks (Bonin et al. 2003;

Cornett, Guo, Khaksari, and Tehranian 2000). Bonin et al.

(2004) argued that over the second half of the 1990s, foreign

ownership in the banking sectors of transition countries

increased dramatically and the performance of foreign

owned banks were significantly higher than domestically

owned banks and the extent of such foreign ownership

impacted the bank efficiency significantly in eleven

transition countries.

The International Monetary Fund (2000) noted that

subsequent to privatization of banks in Bulgaria, following

the banking-currency crisis of 1996-97, the banking sector

was reluctant to lend in the high-risk environment,

resulting in a ratio of private sector credit to GDP of about

12 percent. This is compared to the optimal value of this

ratio for a country with Bulgaria’s per capita GDP of

around 30 percent. Latin American evidence suggests that

foreign banks are especially risk averse and that significant

market penetration by these banks in a developing

economy context might adversely affect credit disbursal to

small and medium enterprises (Clarke, Cull, D’Amato and

Molinari, 1999; Clarke, Cull, and Peria 2001; Clarke, Cull,

Peria and Sanchez, 2002).

Coleman, L. (2007) provided a practical explanation of the

risk taking behavior of finance executives and confirms

that context is more important to decisions than their

content. He also explored reasons for decision makers

facing choices preferring a risky alternative. He finally

identified the risk propensity and quantified it by

respondents’ attitude towards a risky decision, and also

explained decision maker traits using independent

variables. Oldfield and Santomero (1997) investigated risk

management in financial institutions. In this study, they

suggested four steps for active risk management

techniques:

1. The establishment of standards and reports;

2. The imposition of position limits and rules (i.e.

contemporary exposures, credit limits and position

concentration);

3. The creation of self investment guidelines and

strategies; and

4. The alignment of incentive contracts and

compensation (performance-based compensation

contracts).

Scope and Design of the Study

Objectives

The present investigation is based on exploratory research

inquiry and examines the Credit Risk Analysis process in

Public and Private sector banks. It is based on primary data

and compares Credit Risk Analysis process in Indian

Public and Private sector banks of Indore division. The data

was collected from sample of 200 employees of public and

private sector banks of Indore division. 50 respondents

were chosen from each bank viz SBI and Associates; Other

Nationalized Banks; Old Private Sector banks and New

Private Sector Banks. The respondents were selected

through non-probability convenience (judgmental)

sampling method.

As this research has a quantitative base so questionnaire

used in this research is close ended questionnaire. The

research instrument used to collect data was based on

questionnaire developed by Al-Tamimi and Al-Mazrooei

(2007). It included seven close-ended questions based on an

interval scale. Respondents were asked to indicate their

degree of agreement with each of the questions on a five-

point Likert scale. The data were analyzed using window

based Statistical package of the Social Science (SPSS). The

statistical tools used were analysis of variance, Tukey

(HSD) test, Kaiser- Meyer- Olkin (KMO), Bartlett’s test,

Factor Analysis and mean were used to analyze the data.

Questionnaire adopted in this study consisted of seven

questions. As the sample size was 200, item with

correlation value less than 0.1948 should be dropped. All

the items in the study had correlation values more than

0.1948 thus; no item was dropped from the questionnaire.

Reliability of the measures was assessed with the use of

Cronbach’s alpha on all the seven items. Cronbach’s alpha

allows us to measure the reliability of different variables. It

consists of estimates of how much variation in scores of

different variables is attributable to chance or random

errors (Selltiz et al., 1976). As a general rule, a coefficient

greater than or equal to 0.7 is considered acceptable and a

good indication of construct reliability (Nunnally, 1978).

The Cronbach’s alpha for the questionnaire was 0.813.

Hence, it was found reliable for further analysis.

1. To compare whether Public and Private Sector banks

analyze Credit Risk efficiently.

2. To explore the factors contributing to Credit Risk

Analysis in banks.

3. To open up new vistas of research and develop a base

for application of the findings in terms of implications

of the study.

27

Credit Risk Analysis in Indian Commercial Banks-An Empirical Investigation

Hypotheses

Results and Discussion

H : There is no correlation among seven variables in the 01

population under study.

H : There is no significant difference between SBI and 02

Associates, Other Public sector Banks, New Private

Sector Banks and Old Private sector Banks in practice

of Credit Risk Analysis.

H : There is no significant difference between SBI and 03

Associates and Other Public sector Banks in practice

of Credit Risk Analysis.

H : There is no significant difference between SBI and 04

Associates and New Private Sector Banks in practice

of Credit Risk Analysis.

H : There is no significant difference between SBI and 05

Associates and Old Private sector Banks in practice

of Credit Risk Analysis.

H : There is no significant difference between Other 06

Public sector Banks and New Private Sector Banks in

practice of Credit Risk Analysis.

H : There is no significant difference between Other 07

Public sector Banks and Old Private Sector Banks in

practice of Credit Risk Analysis.

H : There is no significant difference between Old 08

private sector banks and New Private Sector Banks

in practice of Credit Risk Analysis.

To test the correlation among all the variables in the

population under study, Kaiser- Meyer- Olkin (KMO)

measure of sampling adequacy and the Bartlett’s test of

sphericity were performed and to test the significance of

variance and understand inter-level difference between

and within group treatments, the data were treated with F-

test analysis.

Results of KMO and Bartlett’s test of sphericity

As indicated in Table-1 the generated score of KMO was

0.676, reasonably supporting the appropriateness of using

factor analysis. The Bartlett’s test of sphericity was highly

significant (p<0.01), rejecting the null hypothesis (H01) that

the seven variables are uncorrelated in the population.

Using Principal components with varimax rotation only

attributes with factor loadings of 0.5 or greater on a factor

were regarded as significant. The factor analysis generated

two factors explaining 72.28% of the variability in the

original data.

28

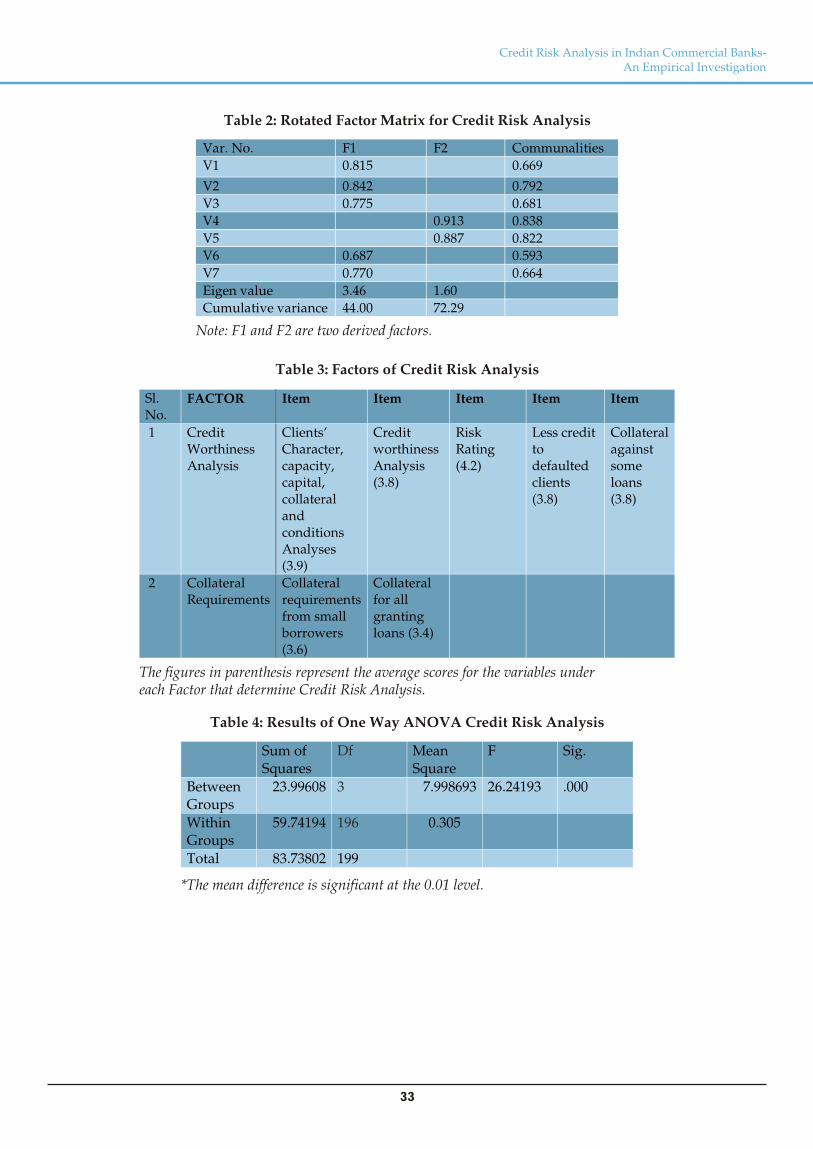

Results of Factor Analysis

Credit worthiness Analysis: It represents specific and

overall analysis of clients in respect of loan granted to them

in order to reduce credit risk. It is measured by items 2, 1, 3,

7 and 6 as identified in table 3. These items are “Before

granting loans your bank undertake a specific analysis

including the client’s characters, capacity, collateral capital

and conditions”, “This bank undertakes a credit

worthiness analysis before granting loans”, “This banks’

borrowers are classified according to a risk factor (risk

rating)”, “The level of credit granted to defaulted clients

must be reduced” and “It is preferable to require collateral

against some loans and not all of them” table 2 display that

Variable 2 is strongest and explains 44.00 per cent variance

and has total factor load of 0.842.

Collateral Requirement: It represents guarantee against

the loan granted so as to reduce credit risk of the bank. It is

measured by items 4 and 5 as identified in table 3. These

items are “It is essential to require sufficient collateral from

the small borrowers” and “This bank’s policy requires

collateral for all granting loans” table 1 display that

variable 4 is strongest and explain 72.28 percent variance

and has total factor load of 0.913.

Results of ANOVA

To test the significance of variance and understand inter-

level difference between and within group treatments, the

data were treated with F-test analysis (Table-4).

H stands rejected02

Credit Risk analysis in SBI and associates, Other Public

sector banks, Old Private sector banks and New Private

sector banks significantly differ in their mean values (F=

26.242 and p< 0.01). Old Private sector banks has highest

mean value of 212, hence have better Credit Risk analysis.

New Private Sector banks with mean value of 199.5, SBI

and associates with mean values of 178.5 and Other Public

sector banks with mean value of 168 represents that Credit

Risk analysis in these banks are comparatively less

effective.

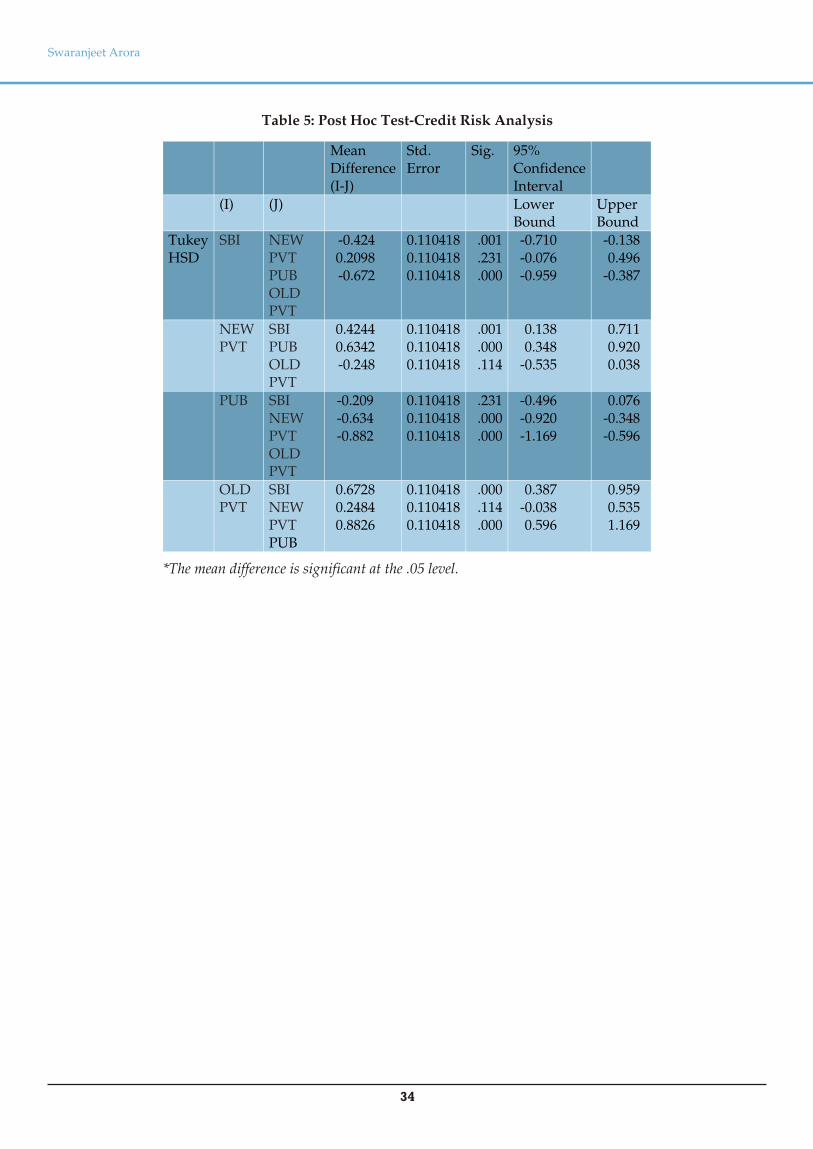

To test the significance of difference between means of each

of the subgroups Tucky test was applied (Table-5)

H stands accepted03

Credit Risk analysis in SBI and associates and Other Public

sector banks do not significantly differ in their mean values

(p> 0.05); this means null hypothesis H cannot be rejected 03

at 5% significance level and it can be inferred that there is no

significant difference between Credit Risk analysis in SBI

and Associates (X =178.5) and Other Public sector Banks (X

=168).

Swaranjeet Arora

H stands rejected04

Credit Risk analysis in New Private Sector Banks and SBI

and associates significantly differ in their mean values

(p<0.05); this means null hypothesis H can be rejected at 04

5% significance level and it can be inferred that Credit Risk

analysis in New Private Sector Banks (X =199.5) is

significantly better then SBI and Associates (X =178.5).

H stands rejected05

Credit Risk analysis in Old Private sector Banks and SBI

and associates significantly differ in their mean values

(p<0.05); this means null hypothesis H can be rejected at 05

5% significance level and it can be inferred that Credit Risk

analysis in Old Private sector Banks (X =212) is significantly

better then SBI and Associates (X =178.5).

H stands rejected06

Credit Risk analysis in New Private sector Banks and Other

Public sector Banks significantly differ in their mean values

(p<0.05); this means null hypothesis H can be rejected at 06

5% significance level and it can be inferred that Credit Risk

analysis in New Private Sector Banks (X=199.5) is

significantly better than Other Public sector Banks (X=168)

H stands rejected07

Credit Risk analysis in Old Private Sector Banks and Other

Public sector Banks significantly differ in their mean values

(p<0.05); this means null hypothesis H can be rejected at 07

5% significance level and it can be inferred that Credit Risk

analysis in Old Private Sector Banks (X = 212) is

significantly better than Other Public sector Banks (X =168)

H stands accepted08

Credit Risk analysis in Old Private Sector Banks and New

Private Sector Banks do not significantly differ in their

mean values (p> 0.05); this means null hypothesis H 08

cannot be rejected at 5% significance level and it can be

inferred that there is no significant difference between

Credit Risk analysis in Old Private Sector Banks (X =212)

and New Private Sector Banks (X =199.5). significantly.

A body of literature on consumer lending has shown that

asymmetric information may prevent the efficient

allocation of lending, resulting in credit rationing (Jaffee

and Russell, 1976; Stiglitz and Weiss, 1981). According to

this literature, because of the existence of informational

asymmetries, lenders fail to observe some relevant

characteristics of potential borrowers and have no way of

learning about them. Were full information available, the

volume and distribution of lending would doubtless be

very different from the outcome under asymmetric

information (deMeza and Webb, 2000). Godlewski (2006)

investigated regulatory and institutional determinants of

credit risk taking and bank's default probability in

emerging market economies. Using a two step logit model

applied to a database of banks from emerging economies,

they confirmed the role of the institutional and regulatory

environment as a source of excess credit risk, which

increases a bank's default risk.

Salas and Saurina (2002) examined credit risk in Spanish

commercial and savings banks; they used panel data to

compare the determinants of problem loans of Spanish

commercial and savings banks in the period 1985-1997,

taking into account both macroeconomic and individual

bank-level variables. The GDP growth rate, firms, family

indebtedness, rapid past credit or branch expansion,

inefficiency, portfolio composition, size, net interest

margin, capital ratio and market power are variables that

explain credit risk. Their findings raise important bank

supervisory policy issues: the use of bank-level variables as

early warning indicators, the advantages of mergers of

banks from different regions, and the role of banking

competition and ownership in determining credit risk.

Al-Tamimi (2002) investigated the degree to which the

UAE commercial banks use risks management techniques

in dealing with different types of risk. The study found that

the UAE commercial banks were mainly facing credit risk.

The study also found that inspection by branch managers

and financial statement analysis were the main methods

used in risk identification. The main techniques used in risk

management according to this study were establishing

standards, credit score, credit worthiness analysis, risk

rating and collateral; the study also highlighted the

willingness of the UAE commercial banks to use the most

sophisticated risk management techniques, and

recommended the adoption of a conservative credit policy.

Bindseil, U. and Papadia, F. (2006) reviewed the role and

effects of the collateral frameworks which central banks,

and in particular the Euro system, use in conducting

temporary monetary policy operations. They explained the

design of such a framework from the perspective of risk

mitigation, which is the purpose of collateralization. They

identified that by means of appropriate risk mitigation

measures, the residual risk on any potentially eligible asset

can be equalized and brought down to the level consistent

with the risk tolerance of the central bank. Once this result

has been achieved, eligibility decisions should be based on

an economic cost-benefit analysis. They also looked at the

effects of the collateral framework on financial markets,

and in particular on spreads between eligible and ineligible

assets.

Powell et. al. (2004) analyzed how data in public credit

registries can be used to strengthen bank supervision and

to improve the quality of credit analysis by financial

institutions. The study was performed in central banks of

Argentina, Brazil and Mexico. The results of the empirical

29

Credit Risk Analysis in Indian Commercial Banks-An Empirical Investigation

tests explored that credit analysis enhances credit risk for

capital and provisioning requirements and acts as a check

on a bank’s internal ratings for the Basel II’s internal rating-

based approach. Arora, S.; Chatterjee, A. and Hyde, A.

(2007) analyzed credit risk management system employed

by Public and Private sector banks in India. They found that

Net NPA to Net Advances ratio, Gross NPA to Gross

Advances ratio & Credit Deposit ratio are important

parameters while evaluating Credit risk management

systems of banks. They also found that Credit Risk

management system of banks can be improved if proper

emphasis is given to these parameters.

Jayadev (2006) identified a set of actions to improve the

quality of internal rating models of Indian banks by

analyzing internal credit rating practices of Indian banks.

The survey revealed that the components of internal rating

systems, their architecture, and operation differ

substantially across banks. The range of grades and risks

associated with each grade also varied across the banks

analyzed which implied that lending decisions may vary

across banks. There were differences among the rating

systems of various banks. Arora, S. and Jain, R.(2011)

identified the factors that contribute to Risk Assessment

and Analysis in Indian banks and found that Risk

Measurement and Probability of occurrences were the two

factors for Risk Assessment and Analysis. They also

concluded that Indian banks efficiently assess and analyze

risk in general but there was significant difference between

the public and private sector banks in Risk assessment and

analysis.

Cost of delaying or avoiding proper risk management can

lead to some adverse results, like failure of a bank and

possibly failure of a banking system (Meyer, 2000). Altman

(2002) analyzed that more emphasis is given to new

developments and techniques for analytical treatment of

credit risk management. Information sharing through

credit bureaus is important for a number of reasons: it may

increase the degree of competitiveness within credit

markets, improve efficiency in the allocation of credit, and

increase the volume of lending (Vives, 1990). Credit scoring

is the process of assigning a single quantitative measure or

score to a potential borrower, representing an estimate of

the borrower's future loan performance (Feldman, 1997).

In present study an attempt has been made to cover most of

the aspects of Credit risk Analysis. However, this paper did

not address in detail credit risk practices adopted by Indian

commercial banks. This type of study can be addressed in

future studies as credit risk represents the most challenging

type of risk. Further research can also be done on Basel II

accord and Credit risk management. Finally, the study

could usefully be conducted in another country, using the

Areas for Further Research

30

same methodology. Different and interesting results may

be expected, because credit risk Analysis is affected by

specific factors such as economic conditions, competition

and regulations.

This paper examined Credit Risk analysis system in Public

and Private sector banks of India. Credit risk Analysis is

crucial because no single database typically houses all of

the risk related data and several years of information is

required. The present study has indicated that Credit

Worthiness analysis and Collateral requirements are the

two important factors for analyzing Credit Risk. From the

descriptive and analytical results, it can be concluded that

Indian banks efficiently manage credit risk. The results also

indicate that there is a significant difference between the

Indian Public and Private sector banks in Credit Risk

Analysis. Credit Risk Analysis is better in Old Private

sector banks and New Private Sector banks, as compared to

State Bank of India and its associates and other public

sector banks. This reflects that in order to improve Credit

Risk Analysis system in banks, efforts should be made to

train the employees so as to improve their understanding

of credit risk, proper credit risk identification,

measurement, monitoring and control system should be

implemented throughout the bank and in the process due

emphasis is required to be given to Credit Worthiness

analysis and Collateral requirements.

• A Roadmap for Implementing an Integrated Risk

Management System by Indian Banks by March 2005-

CRISIL (2004). IBA Bulletin special Issue, 26 (1), 37-55.

• Allen, F. and Douglass, G (1998). Optimal Financial Crises.

Journal of Finance, 53 (4), 1245-84.

• Al-Tamimi, H. (2002). Risk management practices: an

empirical analysis of the UAE commercial banks. Finance

India. 16 (3), 1045-57.

• Al-Tamimi, H. and Al-Mazrooei, F. (2007). Banks' Risk

Management: A Comparison Study of UAE National and

Foreign Banks. The Journal of Risk Finance, 8(4), 394 – 409.

• Altman, E. (2002). Managing Credit Risk: A Challenge for

the new millennium. Review of Banking, Finance and

Monetary Economics, 31(2), 201-214.

• Arora, S.; Chatterjee, A. and Hyde, A. (2007). Credit Risk

Management in Indian Banks: A Comparative Study.

Sameeksha- Technia journal of Management Studies. 1 (2).

• Arora, S. and Jain R. (2011). Exploring Risk Assessment

and Analysis practices in Indian Commercial Banks. ELK

Asia Pacific Journal of Finance and Risk Management, 2(3),

605-614.

• Bernanke, B. and Mark G (1989). Agency Costs, Net Worth

and Business Fluctuations. American Economic Review, 79

(1), 14-31.

Conclusion

References

Swaranjeet Arora

• Bhat, S (2005), “Capital Adequacy: Regulation and Bank

Evidences” Synthesis- The Journal of BLS Institute of

Management, Ghaziabad, 2(2),18-30.

• Bindseil, U. and Papadia, F. (2006). Credit Risk Mitigation

in Central Bank Operations and Its Effects on Financial

Markets: the Case of the Eurosystem. European Central

bank, occasional paper series no.49.

• BIS, Basel Committee on Banking Supervision (1999), “A

New Capital Adequacy Framework” Bank for International

settlements, Switzerland, CP1

• Bonin (2003). Privatization Matters: Bank Performance in

Transition Countries. Conference on Bank Privatization

World Bank, Washington, D.C. November 20-21.

• Bonin, J.; Hasan, I. and Wachtel, P. (2004). Bank

performance, efficiency, and ownership in transition

countries. Journal of Banking & Finance, 29(1), 31–53.

• Chakrabarti, R and Chawla, G (2005). Bank Efficiency in

India since the reforms - An Assessment. Money and

Finance, 2 (22-23), 31-48.

• Clarke, G.; Cull, R. and Maria S. (2001). Does foreign bank

penetration reduce access to credit in developing countries?

Evidence from asking borrowers, Mimeo, Development

Research Group. The World Bank, Washington, D.C.

• Clarke, G.; Cull, R.; Peria, M. and Sanchez,S. (2002). Bank

lending to small businesses in Latin America: Does bank

origin matter? Mimeo, The World Bank, Washington, D.C.

• Clarke, G.; Cull,R. ; Amato, L. and Molinari, A. (1999). The

effect of foreign entry on Argentina’s domestic banking

sector, Policy Research Working Paper 2158, The World

Bank, Washington, D.C.

• Coleman, L. (2007). Risk and decision making by finance

executives: a survey study. International Journal of

Managerial Finance, 3(1), 108-124.

• Cornett, M.; Guo, M L., Khaksari, S., Tehranian, H. (2000).

Performance differences in privately- owned versus state-

owned banks: an international comparison, Working Paper,

World Bank.

• DeMeza, D. and Webb, D. (2000). Does Credit Rationing

Imply Insufficient Lending? Journal of Public Economics,

78, 215-234.

• Donaldson, G (1992). Costly Liquidation, Interbank Trade,

Bank Runs and Pan-ics. Journal of Financial

Intermediation, 2, 59-82.

• Eichengreen, B. (1999). Towards A New International

Financial Architecture. Institute for International

Economics, Washington, DC.

• Feldman, R. (1997). Small Business Loans, Small Banks,

and a Big Change in Technology Called Credit Scoring.

Federal Reserve Bank of Minneapolis. The Region, 19-25.

• Gilbert, R.A. and Wilson, P.W. (1998). Effects of regulation

on productivity of Korean Banks. Journal of Economics and

Business, 50,133–155.

• Godlewski, C. (2006). Regulatory and Institutional

Determinants of Credit Risk Taking and a Bank's Default in

Emerging Market Economies A Two-Step Approach.

Journal of Emerging Market Finance, sage publications,

5(2), 183-206.

• Gorton, G. and Frank, S. (1999). Corporate governance,

ownership dispersion and efficiency: Empirical.

• Havrylchyk, O. (2003). Efficiency of the Polish Banking

Industry: Foreign versus National Banks, Working Paper,

Department of Economics, European University Viadrina

Frankfurt (Oder), Grobe Scharrnstrabe 59, 15230 Frankfurt

(Oder), Germany.

• Hirshey, Mark (1999). Managerial equity ownership and

bank performance. Economic Letters, 64, 209-13.

International Monetary Fund (2000). Bulgaria: Selection

issues and statistical appendix. IMF Staff Country Report,

00/54.

• Jaffee, Dwight, and T. Russell, (1976). Imperfect

Information and Credit Rationing. The Quarterly Journal of

Economics. 90(4), 651-56.

• Jayadev, M. (2006). Internal Credit Rating Practices of

Indian Banks. Money, Banking and Finance, 41(11).

• Kiyotaki, N. and J. Moore. (1997). Credit Cycles. Journal of

Political Economy, 105 (2), 211-48.

• Kwan, S and Eisenbis, R. (1997). Bank Risk, Capitalisation

and Operating Efficiency. Journal of Financial Services

Research, 12, 117–31.

• La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R. Vishny

(2002). Investor Protection and Corporate Valuation.

Journal of Finance, 57, 1147-1170.

• Lowe, P (2002). Credit risk measurement and procyclicality.

Bank of International settlements - Monetary and Economic

Department, Working Papers (No 116).

• Mehrotra,S. (2005). IBA Bulletin , Indian Bank’s

Association.

• Majnoni,G.; Miller,M. and Powell,A. (2004). Bank Capital

And Loan Loss Reserves Under Basel II: Implications For

Emerging Countries. World Bank Policy Research Working

Paper 3437, Washington, DC.

• Meyer, L. (2000). Why Risk Management Is Important for

Global Financial Institutions” at the Risk Management of

Financial Institutions United Nations Conference Center

Bangkok, Thailand.

• Nunnally, C.J. (1978). Psychometric Theory. McGraw-

Hill, New York, NY.

• Oldfield, G.S. and Santomero, A.M. (1997). Risk

Management in Financial Institutions. Sloan Management

Review, 39(1), 33-46.

• Salas, V. and Saurina, J. (2002). Credit risk in two

institutional regimes: Spanish commercial and savings

banks. The Journal of Financial Services Research, 22 (3),

203-16.

• Sarkar, Jayati, Subrata Sarkar and Sumon K. Bhaumik

(1998). Does ownership always matter? Evidence from the

Indian banking industry? Journal of Comparative

Economics, 26, 262-281.

• Selltiz, C., Wrightsman, L.S. and Cook, W. (1976). Research

Methods in Social Relations. Holt, Rinehart and Winston,

New York, NY.

• Stiglitz, Joseph, and Andrew Weiss (1981). Credit

Rationing in Markets with Imperfect Information.

American Economic Review. 71, 393-410.

31

Credit Risk Analysis in Indian Commercial Banks-An Empirical Investigation

• Vives, Xavier (1990). Banking Competition and European

Integration. CEPR Discussion Papers, 373.

32

• Wesley, D. (1993). Credit Risk Management: Lessons for

Success. Journal of Commercial Lending, 08.

Appendix

Bank’s Risk Management ScaleAuthors-Al-Tamimi and Al-Mazrooei (2007)

InstructionsPlease read the questions carefully and mark (X) at the appropriate place in one of the five columns, as the case may be. The questionnaire is designed to know your opinion in general. Please note it is not to test policies of your banks. There is no right or wrong answer. The data is being collected for purely academic purpose.

General InformationName of the Bank :Name of the employee (optional) :Designation :

STATEMENT Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

1. This bank undertakes a credit

worthiness analysis

before granting loans

2. Before granting loans your bank

undertake a specific

analysis including the client’s characters, capacity,

collateral capital and conditions

3. This banks’ borrowers are classified

according to a risk factor (risk rating)

4. It is essential to require sufficient

collateral from the small borrowers

5. This bank’s policy requires collateral for all granting

loans

6. It is preferable to require collateral against some

loans and not all of them

7. The level

of credit granted to

defaulted clients must be reduced

Table 1: Result of the KMO and Bartlett’s test for Risk Assessment and Analysis

Kaiser-Meyer-Olkin Measure of Sampling Adequacy 0.676

Bartlett’s test of Sphericity

Approx. chi square

728.998

df

21

Sig.

0.000

Swaranjeet Arora

Table 2: Rotated Factor Matrix for Credit Risk Analysis

Var. No. F1 F2 Communalities

V1

0.815

0.669

V2

0.842

0.792

V3

0.775

0.681

V4

0.913

0.838

V5

0.887

0.822

V6

0.687

0.593

V7

0.770

0.664

Eigen value

3.46

1.60

Cumulative variance

44.00

72.29

33

Note: F1 and F2 are two derived factors.

Table 3: Factors of Credit Risk Analysis

Sl. No.

FACTOR Item

Item Item Item Item

1 Credit Worthiness Analysis

Clients’ Character, capacity, capital, collateral

and conditions Analyses (3.9)

Credit worthiness Analysis (3.8)

Risk Rating (4.2)

Less credit to defaulted clients (3.8)

Collateral against some loans (3.8)

2 Collateral Requirements

Collateral requirements from small borrowers (3.6)

Collateral for all granting loans (3.4)

The figures in parenthesis represent the average scores for the variables under each Factor that determine Credit Risk Analysis.

Table 4: Results of One Way ANOVA Credit Risk Analysis

Sum of Squares

Df Mean Square

F Sig.

Between Groups

23.99608

3 7.998693

26.24193

.000

Within Groups

59.74194

196 0.305

Total 83.73802 199

*The mean difference is significant at the 0.01 level.

Credit Risk Analysis in Indian Commercial Banks-An Empirical Investigation

Table 5: Post Hoc Test-Credit Risk Analysis

Mean Difference (I-J)

Std. Error

Sig. 95% Confidence Interval

(I) (J) Lower Bound

Upper Bound

Tukey HSD

SBI NEW PVT PUB OLD PVT

-0.424 0.2098 -0.672

0.1104180.1104180.110418

.001

.231

.000

-0.710 -0.076 -0.959

-0.138 0.496

-0.387

NEW PVT

SBI PUB OLD PVT

0.4244 0.6342 -0.248

0.1104180.1104180.110418

.001

.000

.114

0.138 0.348

-0.535

0.711 0.920 0.038

PUB SBI NEW PVT OLD PVT

-0.209 -0.634 -0.882

0.1104180.1104180.110418

.231

.000

.000

-0.496 -0.920 -1.169

0.076 -0.348 -0.596

OLD PVT

SBI NEW PVT PUB

0.6728 0.2484 0.8826

0.1104180.1104180.110418

.000

.114

.000

0.387 -0.038 0.596

0.959 0.535 1.169

34

*The mean difference is significant at the .05 level.

Swaranjeet Arora

Related Documents