1 1 Credit Rating Agencies and developing economies I. Introduction The 21st century has been characterized by a relative scarcity of sovereign defaults and major restructurings, with notable exceptions like Greece and Argentina. Wave after wave of monetary loosening may have helped to keep financing conditions easy and global investors on an increasingly desperate lookout for yield. All too often they found that yield in emerging and developing countries (EMDEs), several of them tapping international capital markets for the first time, especially across the African continent. The pandemic induced global economic crisis has put that period of EMDE funding into question. Private capital flows into the poorest countries dropped sharply. In Sub-Saharan Africa, only the most credit worthy countries can currently access the market. Long-term US-Treasury rates have now begun to inch up, making the mostly USD-denominated debt of frontier markets relatively less attractive. In Africa, 2021 is characterized by relatively few principal repayments. But that will change significantly in 2022 and beyond. The risk of sovereign debt restructurings seems likely to rise. The re-emergence of default risk has directed attention to the institutions that are tasked with predicting and declaring defaults: the international credit rating agencies (CRAs), especially the “Big 3” (S&P Global, Moody’s and Fitch). As far as developing economies are concerned, the rating agencies have gained importance compared to previous cycles of sovereign debt crises, such as the one sweeping across Latin America in the 1980s. Back then only a small number of sovereigns even had a sovereign rating at all. In Sub-Saharan Africa, for example, only South Africa had a rating at the beginning of the century. The CRAs role has expanded significantly since. Rating agencies derive their ratings applying published methodologies. While the methodologies, as well as the ratings differ between the three agencies the main building blocks are the same. They consist of an analysis of (i) institutional and governance quality; (ii) economic growth and resilience; (iii) public finances; (iv) external accounts; and (v) monetary flexibility. The agencies typically create indicative “anchor scores” for each of the five rating factors and then apply a “qualitative” overlay. The credit committee can adjust the indicative scores up or down. The rating, which is always determined by a group of analysts in a credit committee is therefore a mix of objective quantitative and subjective qualitative factors. 1 This Policy Note draws on a forthcoming paper written by Stephany Griffith-Jones and Moritz Kraemer, titled “Credit Rating Agencies and Developing Countries; analysis of the issues and policy suggestions”, written for UNDESA.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

1Credit Rating Agencies and developing economies

I. Introduction The21stcenturyhasbeencharacterizedbyarelativescarcityofsovereigndefaultsandmajorrestructurings,withnotableexceptionslikeGreeceandArgentina.Waveafterwaveofmonetarylooseningmayhavehelpedtokeepfinancingconditionseasyandglobalinvestorsonanincreasinglydesperatelookoutforyield.Alltoooftentheyfoundthatyieldinemerginganddevelopingcountries(EMDEs),severalofthemtappinginternationalcapitalmarketsforthefirsttime,especiallyacrosstheAfricancontinent.ThepandemicinducedglobaleconomiccrisishasputthatperiodofEMDEfundingintoquestion.Privatecapitalflowsintothepoorestcountriesdroppedsharply.InSub-SaharanAfrica,onlythemostcreditworthycountriescancurrentlyaccessthemarket.Long-termUS-Treasuryrateshavenowbeguntoinchup,makingthemostlyUSD-denominateddebtoffrontiermarketsrelativelylessattractive.InAfrica,2021ischaracterizedbyrelativelyfewprincipalrepayments.Butthatwillchangesignificantlyin2022andbeyond.Theriskofsovereigndebtrestructuringsseemslikelytorise.There-emergenceofdefaultriskhasdirectedattentiontotheinstitutionsthataretaskedwithpredictinganddeclaringdefaults:theinternationalcreditratingagencies(CRAs),especiallythe“Big3”(S&PGlobal,Moody’sandFitch).Asfarasdevelopingeconomiesareconcerned,theratingagencieshavegainedimportancecomparedtopreviouscyclesofsovereigndebtcrises,suchastheonesweepingacrossLatinAmericainthe1980s.Backthenonlyasmallnumberofsovereignsevenhadasovereignratingatall.InSub-SaharanAfrica,forexample,onlySouthAfricahadaratingatthebeginningofthecentury.TheCRAsrolehasexpandedsignificantlysince.Ratingagenciesderivetheirratingsapplyingpublishedmethodologies.Whilethemethodologies,aswellastheratingsdifferbetweenthethreeagenciesthemainbuildingblocksarethesame.Theyconsistofananalysisof(i)institutionalandgovernancequality;(ii)economicgrowthandresilience;(iii)publicfinances;(iv)externalaccounts;and(v)monetaryflexibility.Theagenciestypicallycreateindicative“anchorscores”foreachofthefiveratingfactorsandthenapplya“qualitative”overlay.Thecreditcommitteecanadjusttheindicativescoresupordown.Therating,whichisalwaysdeterminedbyagroupofanalystsinacreditcommitteeisthereforeamixofobjectivequantitativeandsubjectivequalitativefactors.

1ThisPolicyNotedrawsonaforthcomingpaperwrittenbyStephanyGriffith-JonesandMoritzKraemer,titled“CreditRatingAgenciesandDevelopingCountries;analysisoftheissuesandpolicysuggestions”,writtenforUNDESA.

2

Ratingagenciesusecomparableratingscaleswith20rungsfromthehighest(AAA)tothelowest(D),withtheuppertenratings(AAAtoBBB-)beingreferredtoasinvestmentgrade,andthelowerhalf(startingfromBB+)asnon-investmentgrade,orspeculativegrade.Thesimilarityoftheratingsmethodologiesappliedhasledtoacomparabilityofoutcomes,especiallyforemergingmarkets.Therewillalwaysberatingsdifferencesfromonecountrytoanother,butonaveragetheagenciesagree.Theaverageratingofthe70EMDEsratedbyeachoftheBig3onJanuary31,2020,beforethepandemicspreadacrosstheglobewasalmostidenticalforthethreefirms,justbelowBBinthenon-investmentgraderange.Oneyearintothepandemic,theaverageEMratinghasfallenbyalittlelessthanone-halfofanotch,againuniformlyacrosstheagencies.ThehistoricallyobservedpatternofS&Pdowngradingfirstandtheothertwoagenciesfollowing,seemstohavebeenbroken.2Theagenciesnowappeartomoveinlockstep.InsectionII,whichfollows,wewillanalyzethemainchallengesposedbycreditratingagencies,especiallyfromadevelopingandemergingeconomiesperspective.SectionIIIwillexplorepossiblepolicysolutionstothosechallenges.

II. Challenges 1.) Potential bias against EEDEs

Mostofthetimes,ratingsmovegentlyupordownataglacialpace,attimesbrieflyinterruptedbydebtcrisis,eitherinoneorafewcountries,orinmoregeneralizeddebtandfinancialcrises.Ratingagenciesstrivetorate“throughthecycle”,thoughthereisacademicandotherdebateatwhethertheyaresuccessfulinthis(seebelow).Thismeans,thatmostratingschangerelativelyrarely,exceptinmajorcrises,astheyaredesignedtoreflectfundamentalcreditstrengthsandnottheupsanddownsofthecredit,financial,orcommoditymarkets.Therefore,itisusuallydifficulttoassess,whetherratingagenciesfavoronesetofsovereignsoveranother.Todate,however,thefactualevidenceonthishasbeeninconclusive.WepresentsomenewevidencethatmightsupporttheclaimthatCRAshaveaninherentbiasagainstEEDEs.TheCOVID-19crisishasallthehallmarksofapotentialexceptiontothetypicalgradualism:aglobaleconomicshock,thathitsallcountriesonallcontinentssimultaneously,althoughatdifferentintensities.Lookingatthissuddenandbrutalshockwecanassesswhetherratingagenciesdisplaythebiasagainstemerginganddevelopingeconomies.TheeconomicfalloutfromthepandemichasbeenlargerforAEsthanforEMDEs:AccordingtoIMFOctober2020-estimatesAEeconomiescontractedtwiceasfast

2Foranin-depthlead-laganalysisofsovereignratingsseeKraemeretal.(2020)

3

(-4.9%)asEMDEs(-2.4%)lastyear.Similarly,theaggregateAEgovernmentdebtratioincreasedby20percentagepointsto124%ofGDP,versusEMDE’sincreasebyninepercentagepointsto61%ofGDP.Notwithstandingthatbiggershock,betweenJan.31,2020andFeb.28,2021,AEsaccountedforonlysixnotchesofdowngradesbetweentheBig3,against125inEMDEs(seeChart1).Inotherwords,althoughAEsaccountfor29%ofallissuerratingsoftheBig3,lessthan5%ofalldowngradeswereappliedtothem.Ifupgradesduringtheperiodunderinvestigationareincludedinthecount,the“netdowngrades”disappearaltogether.S&PandMoody’sevenhadnetpositive(!)ratingactionsforAEsduringthemostferociouspeacetimerecessioninlivingmemory.

TowardsEMDEs,theratingagenciespandemicresponsehasbeenlesscharitable.Chart2displaystheshareofeachagency’sportfolioofratedsovereignsthatwasdowngradedbyatleastonenotch.SovereignsinSub-SaharanAfrica(41%)andLatinAmericaandtheCaribbean(35%)weremostlikelytobedowngraded,followedbyMiddleEast,NorthAfrica,andCentralAsia(25%)andAsia-Pacific(24%).Non-AECentralandEasternEurope(CEE)includesseveraleconomies,especiallytheEUmembersthatareclosetobeingconsideredAEs.Somearelong-standingmembersoftheOECD.LikeAEs,theCEE

4

region,too,wasalmostentirelyspared:Moody’sloweredTurkey’sratingandFitchdowngradedArmenia.S&Ptooknoactionintheregion.Amongthethreemainplayers,Fitchwasthemostsevereagencyalmosteverywhere,especiallyintheMiddleEastandNorthAfricaregion.S&Pwastheratingsfirmofferingmostforbearanceinallworldregions,exceptinSub-SaharanAfrica,whereitwasthedowngradeleaderbysomedistance,loweringtheratingsof50%ofsovereignsintheregion.Whatexplainstheseinter-regionaldifferences,andespeciallytheratingsstabilityofadvancedeconomies?Onecouldarguethatrich,diversifiedcountriesaremoreresilienttoshocksthanpoorer,morevulnerableeconomies.Thatisundoubtedlytrue.However,itisalsotruethattheshockdeliveredbyCOVID-19wasnotevenlydistributedacrosseconomies.Infact,thehittogrowthandpublicdebtaccumulationhasbeentwiceaslargeforAEsthanforEMDEs,nottomentiontheirsignificantlylargerdeathtolls.Giventhatcontext,itisnotatallclearwhyrichcountries’ratingsremainedlargelyuntouchedevenastheirpoorerpeersweresubjecttomoreextensivedowngrades.Moreanalysisisrequiredtosolvethispuzzle.ThesemoreextensivedowngradesintheEMDEs,especiallyifnotjustifiedfromaneconomicpointofview,canhavenegativeconsequencesontheavailabilityandcostofprivatecapitalflows,andthereforelevelsofinvestment,ofthosecountries,withnegativeeffectsontheirdevelopmentprospects,aswellastheirabilitytomeettheSDGs.

2.) Pro-cyclicality of ratings3

Oneofthekeypurposesofcreditratingagencies(CRAs)istoprovideaccurateanalysisofcountries’long-termsolvency,inwaysthatdonotvarythroughthecycleorevenbetterthatarecounter-cyclical.Thiswouldcontributetomakeinternationalprivatecapitalflows,whichthemselvesareinherentlypro-cyclicallessso.However,concernshavebeenexpressedbybothemerginganddevelopingcountriesthemselves,aswellasevidenceprovidedintheacademicliteraturethatCRAsarethemselvespro-cyclical,andthereforecontributetomakeprivatecapitalflowsMOREandNOTLESSpro-cyclical,thuspossiblyincreasingtheriskoffinancialcrisesoccurringanddeepening.Thus,forexample,Ferri,G.,L.-G.LuiandJ.E.Stiglitz(1999),basedontheireconometricanalysis,concludedthatcreditratingagenciesaggravatedtheEastAsiancrisisbydowngradingmorethanneeded,whichthenincreasedthecostsofborrowingforcountries,afterfailingtopredictthecrisis.Ratingsinthatcasecontributedtocreateaself-fulfillingprophecy.

3WearegratefultoSabrinaAxterforhervaluablecontributiontothissection

5

Indeed,Ferri,LuiandStiglitz,(op.cit.)arguethatbeforetheEastAsiancrisis,theactualratingsassignedtothefourhighgrowthdynamicEastAsianeconomieswereconsistentlyhigherthantheeconomicfundamentalswarranted.Secondly,afterthecrisis,actualratingsdroppedfarmoresharplythantheeconomicfundamentals,asmeasuredbypaperwriters’modelpredicted,suggestingthatratingdowngradeswerelargerthaneconomicfundamentalspredicted.Thiswouldseemtoimplythatbothintimesofboomandcrisis,economicfundamentalsarenotsufficientlyconsideredbyCRAs.TheaboveauthorsaswellasothersemphasizetheroleofprofitandincentivesofCRAsthemselvesinshapingtheirpro-cyclicalbehavior.Thus,CRAsmightbedriventobemoreconservativeduringcrisistoprotecttheirreputationcapital,whichhasbeenunderminedbythecrisis,andarelessconcernedabouttheirreputationcapitalduringeconomicboomandthusmaybemorelenientintheirratingassignments.Bolton,FreixasandShapiro(2012)complementthisbyarguingthatCRAscaninflateratingswheninvestorsbecomemoretrustingandtherearemoreinvestorswillingtoinvestduringboomcyclesand/orwhenCRAreputationcostsarelower.Goodhart(2008)goesfurtherandismorepessimisticashearguesthatproposalstoaddresspro-cyclicalitybymakingcreditratingsonathrough-the-cyclebasiswillnotdomuchsinceduringboomyearsitismorebeneficialforallactorstoadoptapoint-in-timeapproachandcompetitionwillmakethathappen.Interestingly,bothheandBoltonetalareskepticalofthebenefitsofincreasedcompetition,contrarytootheropinion.Ferri,LuiandStiglitz(opcit.),alsosuggesthowCRAscanintroducepro-cyclicalratings:“Iftheratingsgeneratedfromthepaper’sauthorsmodelofeconomicfundamentalsareconsistentlyhigher(orlower)thantheactualratingsassignedforacountry,thentheratingsassignedfromthequalitativejudgementparttendtoundermine(oroverstate)theratingsgeneratedbytheeconomicfundamentalsand,thus,theyclearlyindicatethatratingagenciestendtousetheiridiosyncraticjudgementtomodifytheratingsgeneratedbytheeconomicfundamentals.Indoingso,ratingagenciesmaybehaveinamannerthatmaypotentiallygeneratepro-cyclicalsovereignratings”(347).AnotherimportantpointmadebytheaboveauthorsisthatdowngradesbyCRAs,especiallyifsevere,giveanegativesignalonthecountrythatisexperiencingthedowngradingtomarketparticipants,whichcanalsoaffecttheexchangerate,thestockmarketandthevalueofotherdomesticassetsandthuscanturnintoself-fulfillingprophecy.ItisinterestingthatIMF(2000),alsobasedonempiricalanalysis,basedontheirownmodel,concludesimilarlythat“CRAbehaviorisasymmetricandyield“proofofthepuddingintheeatingresults”:countriesaredowngradedfollowingmajorcrises,possiblybecausetheydonotperformasexpected”.Therefore,thispaperalsoisconcernedaboutCRApro-cyclicalbehavior,andmakessomeinterestingsuggestionsforalternatives,whichwediscussbelow.PretoriusandBotha(2017)carryoutempiricalresearchfor27Africancountriesforthetimeperiodbetween2007and2014.Theyconcludethat:“pro-cyclicality

6

isconfirmedforFitchandMoody’sintheirassignmentofcreditratingsforAfricansovereigns.ThismeansthatthereisanincreasedprobabilitytoAfricansovereignsofgettingupgradedduringboomphasesanddowngradedduringrecessionphasesbythementionedratingagencies”(546).TheiranalysisofS&Pdidnotgiveclearpro-cyclicalresultsfortheirratings,whichisinterestinginthatthereseemtobedifferentbehavioralpatternsforthedifferentCRAs.BrotoandMolina(2016)notonlyfindevidenceofpro-cyclicalitybutalsofindthatpreviousdowngradeshaveanegativeinfluenceonfutureratingsandthatitisdifficultfordomesticvariablestoaffectthepathofratingsifacountryhasbeendowngraded.Thus,theyconcludethatratingsare“lessinfluencedbyeconomicanddomesticindicatorsinthepost-crisisperiodthaninthepre-crisisperiod”.Thislatterpointmeansthatthetaskforthecountries’policy-makerspost-crisisbecomesharder,especiallyindifficulttimes.Thereareadditionallyseveralotherstudiesthathavereportedthereispro-cyclicalityinratingsofsovereigns,suchasLarrain,ReisenandVonMaltzen(1997)andMasciandaro(2011),whereastherearealsosome,butfewerstudiesthathavenotfoundevidenceofsuchpro-cyclicality,suchasKraemer(2014)andMora(2006),forexample.Inconclusion,mostoftheliteratureprovidesfairlystrongevidencethatCRAstendtobepro-cyclical,thattheirincentivestructureencouragestheirpro-cyclicalityandthatthequalitativeaspectsoftheirriskevaluationseemtobeparticularlypro-cyclical.Wereturntothelatterissueinourproposals.

3.) Governance issues and conflicts in sovereign ratings

Itisimportanttounderstandthattheagenciesaresubjecttoregulationsthattrytoinsulateanalystsdecidingontheratingfromanypressureofcommercialcolleaguesoriginatingbusinessandmanagingclientrelationships.Itappearsthatratingagenciesadheretothosestandardsandthe“Chinesewalls”haveheldupsincetheglobalfinancialcrisis.Atleastthatiswhatthelackofanyviolationspublicizedbyregulatorsseemstosuggest.Evenassumingtheintentofinappropriatebehavior,attemptingtosystematicallyletcommercialinterestdiluteanalyticalindependencewouldputthelucrativebusinessmodelatgraverisk.Ifregulatorsweretoexposesuchmisconduct,thereputationaldamagewouldjustbetoohigh.CRAsfearan“ArthurAndersen”-momentmorethananythingelse.Buttherecanbemoresubtlewaysthatcouldallowapro-AEbiastricklein.The“Big3”areUS-headquartered,profit-maximizingfirms,largelyfundedbytheinstitutionstheyrate.Andtheratingsbusinessisextraordinarilyprofitable.Profitmarginshavesteadilyincreasedandreached60%in2020forMoody’sandS&P,bothpubliclylistedcompanies.Itislittlesurprising,then,thattheirsharepriceshaveaccordinglyrisenbetween3.5-fold(Moody’s)and5-fold(S&P),frompre-GFCpeaks,makingtheirgroupparentcompaniesvaluedat$55billionand$85billion,respectively.Theoligopolisticmarketstructure,wherethreefirmsaccountforover90%ofthemarket,(seechart3below)issomethingtheincumbentswouldliketopreserve.

7

Mostoftheirbusinessisinadvancedeconomies(AEs).RegulatorsinAEsarethemostpowerfulsupervisorsoverseeingtheratingsindustry.ItisinAEs,therefore,wherethemainriskstotheCRA’sbusinessmodelsreside.Forexample,S&P,hadbeensuedbytheU.S.DepartmentofJusticein2013.Althoughsovereignratingswerenottheunderlyingreasonforthecasebroughtagainstit,S&Psaidatthetimeitconsideredthelawsuitas“retaliation”forhavingstrippedtheUSofits‘AAA’-ratingtwoyearsearlier.Thecaseendedwitha$1.5billionsettlementin2015,wipingoutoveroneyearofprofits.NoagencyhassincedowngradedtheUS,notwithstandingthesignificantdeteriorationinpublicfinancesandunprecedentedthreatstogovernancestandardsduringtheincumbencyofthe45thPOTUS.Thereisthereforeanasymmetryofincentivesanddisincentives,asregardswillingnessofCRAStodowngradeAEs,versustheEMDEs,whoseregulatorshavefarless,ifanyinfluenceontheCRAsdecisions.Additionally,mostratingsmanagersandanalystsarecitizensofadvancedeconomies.Andamongthefewwhoarenot,mostofthoseobtainedtheirtertiaryeducationatWesternuniversities.ThishasgivenrisetosuspicionofAnglo-Saxongroupthinkand“homebias”ofCRAs,discriminatinginfavorofAEstothedetrimentofpoorercountries.Or,asGhana’sMinisterofFinance,KenOforo-Atta,moredramaticallyputsit:“AretheratingagenciesbeginningtotipourworldintothefirstcircleofDante’sInferno?”Asoutlinedabove,sovereignratingsareamixtureofobjectivedataanalysisandsubjectivereasoning.Ifanalystsfeelsomepressure,howeversubtle,fromexecutiveswhoaimforeverfasterbusinessexpansion,theymightsubconsciouslybeinclinedtogiveAEsthebenefitofthedoubtintheirqualitativeassessment.Remote,smallerandlesspowerfulnationsmightwellhavebeendowngradedinsimilarcircumstances.CRAmanagementhasofcoursealsotheabilitytopromoteanalystswithareputationfor“generous”ratingrecommendationsincommerciallykeycountriesandblockthepathaheadfor

40

35

16

10

40

33

18

9

MarketshareasestimatedbyEU-regulator(2013and2019in%)

S&P

Moody's

Fitch

Allothers

innerring: 2013outerring:2019

Source:EuropeanSecuritiesandMarketAuthority

8

theirmoreskepticalcolleagues.Suchpatternswillnotescapetheattentionofanalyticalstaffwithprofessionalambitions.Thequalityandimpartialityofratingsrequireanunshakableindependenceofanalystsfromallcommercialconsiderationsorfromfearofcareerrepercussions.Theremayalsobefurtherpersonalconsiderationsofpressuresfromoutsidetheratingsorganization:theknowledgethatratinganalystsofseveralagenciesweretried(andonlyaftermanyyearsacquitted)inanItaliancriminalcourtforratingdowngradesperformedduringtheeurozonecrisismayhaveledsomeanalyststothinktwiceaboutloweringrichcountries’sovereignratings.EMDEgovernmentsandregulatorsdonotdisposeofsimilarpowers.

4.) Credit ratings and climate risk

AkeyissueisthetimehorizonofsovereignratingsissuedbyCRAs,asthesearerelativelyshort.Thereseemstobeacaseformorelong-termratingstobeissued,alsotomirrorthelengtheningtenorsofgovernmentsecurities(whichhaveevenforsomeemergingeconomiesincluded100-yearbonds)andtotakeaccountoflonger-termfactorsespeciallyclimatechange,butalsodemographicandotherlong-termtrends.ItseemsespeciallyimportantthatCRAsconsiderclimaterisk,includingbothphysicalandtransitionrisk,indeterminingratings.AfailuretocutcarbonemissionscouldcostgovernmentsaroundtheworldhundredsofbillionsofUS$,accordingtoUniversityofCambridgeeconomistswhousedartificialintelligencetoforecastclimatechange’seffectonsovereigncreditratings.Theyestimatethatifemissionscontinueatcurrentlevels,63countrieswillseeratingsdowngradesofmorethanonenotchby2030,andmanymoreduringtherestofthecentury.Importantly,thisfindingappliesforadvancedeconomiesandEMDEsequally.4Thiswouldalsoimplyratingagenciesreflectingsovereigneffortstoincreaseinvestmentinresilienceandadaptationtoclimatechange,whichcouldbepositiveforsomedevelopingandemergingeconomies.Indeed,failingtoinvestinmakingeconomiesandsocietiesmoreclimate-resilientunderminesfuturegrowth,wellbeing,andsovereigncreditworthiness.Suchanapproachcouldleadtodownwardratingpressureforsomesovereigns,whileothersmightbenefit.Forexample,ratingsforsomedevelopingandemergingcountriescouldbelowered,iftheyareparticularlyvulnerabletoclimatechange,orarefossilproducers,andtheirproductionandexportscouldincreasinglybecomestrandedassetsinfutureyears.Nevertheless,ifratingagenciesaretohavealong-termperspective,suchrisksoughttobeincludedmoreexplicitlyinratings.

4https://www.bennettinstitute.cam.ac.uk/media/uploads/files/Rising_Climate_Falling_Ratings_Working_Paper.pdf

9

Inthecaseparticularlyofmajorfossilproducers(seeIEA,2020),butalsoofothercountries,effortsat,andinvestmentin,significantdiversificationofproductiontomorelow-carbonactivities,-bothfordomesticconsumptionandespeciallyforexports-,wouldreducetheproblemofstrandedassets,andshouldthusincreasetheirlong–termcreditratings.Morebroadly,majorinvestmentsmadebydevelopingcountriescontributingtomoredynamic,sustainable,andfairereconomies,andwhichhelpfulfilltheSDGs,shouldbeconsideredpositivelybyratingagencies,astheyarelikelytoincreasecountry’sabilityforfuturerepayment.Indeed,forexample,investmentineducation,healthandsustainableinfrastructure,mayintheshort-termincreaselevelsofpublicdebt,butinthelong-term,ifwellinvested,especiallyinsectorswhichdirectlyorindirectlywillincreasethecapacityoftheeconomytogrow,includingparticularlyintradeables,willthusmakeitmorelikelycountrieswillbeableandwillingtoservicefuturedebt.Animportantexampleoftheimportanceofthelinkbetweensufficientinvestmentinhealthandpandemicpreventionwitheconomicperformanceisprovidedbyinvestment(orlackof)inpandemicpreparationandits’impactoneconomicevolutioninCOVID-19times.ItseemsthatthosecountrieswithbetterresourcedhealthsystemsaswellasbetterpandemicpreparationandresponsehavebeenabletocontroltheCOVIDpandemicbetterandhavethereforeseentheireconomieslessbadlyhit.Thisillustratesthevalueofinvestmentinthesocialsectorsonlong-termevolutionofeconomies.

Indeed,astheUNSecretaryGeneralPolicyBrief(2021)arguesclearly, ,“a more favorable long-term rating might help countries raise long-term capital to invest more effectively in sustainable development”. The availability of ultra long-term ratings, would not just allow a better evaluation of countries ability to service the debt in the long-term, but help enable, in a virtuous circle, higher availability of funds to do such key investment. ItneedstobeconsideredwhetherCRAsshouldalsodosuchultra-long-termratings,orwhetherotherinstitutions,withgreaterfocusandexpertiseonlong-termtrends,wouldbemoreappropriateforthattask.Wereturntotheseissuesbelow(sectionIII.5).

5.) Impact of credit ratings in the DSSI/Common framework context

ShortlyaftertheoutbreakoftheCOVID-19pandemictheG20putinplacetheDebtServiceSuspensionInitiative(DSSI),comingintoeffectinMay2020.UndertheDSSI73oftheworld’spoorestcountriescanapplyfortemporarydebt-servicepaymentrelief(butnotforgiveness)fromitsofficialbilateralcreditors.Thesuspensionistoexpirebymid-2021butmaybeextendedagain.Todate,46countrieshaverequestedDSSIparticipation.Sincecreditratingsspeakonlytomissedpaymentsonnon-officialdebt(e.g.,bondsandcommercialloans),suspendingdebtservicepaymentsisnotadefault.Missingapaymentincommercialdebtwouldbe.TheG20hasencouragedprivatecreditorstoparticipateintheDSSI.Unsurprisingly,eligiblecountrieshavenotrequested

10

equaltreatmentfrombondholders,asdebtservicesuspensiononthosesecuritieswillconstituteadefaultundertheratingagencies’definitions.AlthoughmostDSSI-eligiblecountrieshavelostmarketaccessforoveroneyearnow,anyway,thefearofdowngradesstillloomslarge.RatingagencieshavebeencriticizedforsignalingthatratingsparticipatinginDSSIcouldcomeunderdownwardpressure,asparticipationcouldraisetheriskoflossesforinvestorsinthefuture.Infact,therehavenotbeenthatmanyratingactionsexplicitlyreferencingDSSIparticipation.Thiscanbeexplainedbythefactthatpoorcountrieshavemostlyrefrainedfromsolicitingprivatecreditorinvolvement.Forexample,Moody’sputseveralEMDEswithoutstandingEurobondsonreviewforadowngradeonMay28,2020,citingtheG20’scallforprivatesectorinvolvement.Allratings(Pakistan,Coted’Ivoire,Cameroon,Senegal,Ethiopia)werelateraffirmedratherthandowngraded.Moody’shadconcludedthatprivatesectorinvolvementwassufficientlylowsoasnotmeritingadowngrade.Itremainsunclear,however,whyarrivingatthisconclusionwouldhavetakensolongandwhatchangedtheirmind.Bydanglingthe“threat”ofadowngradeinfrontofEMDE’sissuers,Moody’scanbeseenashavingcreatedunnecessarynoiseandfosteringasenseofreluctancetoapplytomechanismdesignedtomakecountries’debtanddebtservicemoresustainable,whichwouldbeimportantforfacilitatingCOVID-19recovery.Ethiopia’sratinghassincebeenloweredanyway,alsobytheotheragencies.ThishasoccurredinthecontextofEthiopiarequesting“treatment”ofitspublicdebtundertheG20CommonFramework(CF).UndertheFramework,whichwasagreedinNovember2020,DSSIeligiblecountriescanrequestamoreprofoundrestructuringofthedebt:debtreductionratherthannet-presentvalueneutralandselectivere-profiling.AconditionforparticipationintheCFis“broadcreditorparticipationincludingtheprivatesector”.ByapplyingforCFdebttreatment,Ethiopiahasthussignaledthatitiswillingtoapproachitsprivatecreditorsfordebtrestructuring.Although,thatrestructuringhasnotyethappened,andmaybeneverwill,ithasobjectivelybecomemorelikely.Andasratingsareverynarrowlydefinedasanassessmentofalikelihoodofdefault(andnothingelse),itishardtofaulttheagenciesoncuttingEthiopia’srating.Distresseddebtrestructuringisadefaultbycapitalmarketconvention.Evenifratingagencieswouldviolatetheircriteriaandnotdeclareadefault,itispossiblethatinvestorswouldbehaveasiftheyhad.Adebtdefaultisahighlyvisibleandwell-understoodeventandwhetheraratingagencycallsitassuchornotmaynotmakeaverylargematerialdifferencetomarketconditions,thoughsomeacademicliteratureprovidesevidencethatdowngradeannouncementsdohaveanimpact,andmaycontributetodeepeningcrisesforexample.ButitremainstruethatgovernmentsinDSSI-eligiblecountriesremainfearfulofthedowngradesthatwillhavetocomeiftheyaskfordebtrenegotiation.Theyshouldnotbe.Proactivelyrestructuringthedebt,evenifitledtoatemporarydeclarationofdefaultbytheagencies,canbebeneficialforhighlyindebted

11

governments.Asexcessleverageisremoved,thegrowthanddevelopmentpotentialwillimprove.Thatshouldmakepoorcountries’sovereigndebtmoreattractiveinvestmentsagain.Inalow-interestworldwhereinvestorsfranticallysearchforyield,adebtwork-outwillquicklyrestoremarketaccess,whichiscurrentlyclosedformostpoorersovereigns.Evenmoresoasinvestors(andratingagencies)willunderstandthattherestructuringwouldnotbetheresultofpoorpolicies,butbadluck,beinghitbyapandemicandglobaleconomiccrisis.Someinvestorsstokethefearofrestructuringandallegedlossofprolongedmarketaccessoutofperceivedself-interest.Butitmaybeanactofself-harminstead:Weknowfromexperiencethatdelaystosovereignrestructuringleadstodeepercrisesindebtorcountries,deeperhaircutsforcreditors,andlongerexclusionfromcapitalmarkets.Procrastinationisalose-loseproposition.

6.) Role of Credit Ratings in financial market regulation

TheratingsbyCRAShaveabroaderindirectimpact,thantheonetheyhavedirectlyonthevolumeandcostofcredit.ThisindirecteffectrelatestotheuseofCRAratingsinseveralaspectsoffinancialregulation.Themostimportantone,whichwewillfocusonhere,istheuseofratingsaspartoftheBasleCapitalAccord,whichregulatesbanklending,nationallyandinternationally;thisisespeciallyimportantfortheirlendingtoemerginganddevelopingeconomies(EEDEs).Therearealsootherregulations,includinginternalones,which,forexample,determineinvestmentpoliciesofinstitutionalinvestors-increasinglyimportantintheirinvestingandlendingtoemerginganddevelopingeconomies,whichwewilldiscussbelow.Afterthe2007/09majorfinancialcrisis,regulatorsagreedthattheuseofCRAratingsinregulationswasnegativebecauseitmade-forexample-theBasleAccordmorepro-cyclicalandthereforecontributedtodeepenthecrisis,andthatthislinkshouldbeeliminatedorreduced;however,unfortunately,thishasnotoccurredtodate.Inbroadterms,thisuseofCRAratingsinBaselregulationisproblematicforthreereasons(Becker,2021).First,theBasleCommitteeforBankSupervision(BCBS)externalizedsub-issues,suchascreditriskmeasurement,thatareoffunctionalimportanceforitsobjectiveofglobalbankingstability.Second,itestablishedaone-sideddependenceonexternalforumssincetheperformanceofbankingregulationisdependentoncreditriskmeasurementbutnotviceversa.Third,theBCBShaslimitedcontrolmechanismstoinfluencegovernanceintheCRAs,leavingthemautonomyforinconsideratebehavior.BaselIIandIIIincludeaweightingsystemthatallowschangeinriskassessment.Thisdynamicriskweightingsystemrequiresconstantupdatesaboutthecurrentprobabilityofdefault(PD)andotherriskparametersofeachfinancialassetinthebank’spossession.SuchdetailedandregularupdatingrequiresspecializedknowledgeandconsiderablecapabilitiesthatlieoutsidetheBCBS’competenceasaperiodiccommitteewithlittleresources.Thelackofcapacitiestogovern

12

riskassessmentitselfcausedtheBCBStohandtheresponsibilityoverthisimportantsub-issuetoCRAs.Thus,theapproach“outsources”theactualassessmentofriskweightsofborrowerstoCRAs.TheseassessmentscanchangeovertimeandaresubjecttotheevaluationoftheCRAs.Hence,theBaselCommitteedecidedtousetheexpertiseofCRAsasprovidersforprobabilityofdefaultestimatesinthestandardizedapproach,whilenotprescribinganydetailedmethodologicalmeansonhowCRAshavetorateassets.TheAccordonlyspecifiessoftcriteriaofwhatpropertiesaCRAmustfulfilltoreceivealicense.Thus,theAccordgaveCRAsmuchdiscretionintheirratingsystem.Akeyproblemisthatwiththis,amultiplicativeaspectisthatBaselIIandIIInotonlyexposedthevalueoffinancialassetstomarketdevelopments,butalsotherelatedriskweights.UnderformerBaselIrules,thepro-cyclicalinfluenceoffairvalueaccountingwerelimitedtotheactualvalueoftheassets,buttheriskweightswerefixedandriskassessmentwouldnothavechangedwiththebusinesscycle.However,theintroductionofdynamicriskweightsandtheimportofriskassessmentfromCRAsinthestandardizedapproachconnectedthepro-cyclicalnatureofbothpolicies,therebymultiplyingtheirpro-cyclicality.Creditratingagencieswereshowninabadlightduringthecreditcrisisof2008/09,mainlyduetoratingsonsecuritizeddebt.However,BaselIIIhasnotoutlawedtheuseofcreditratings.BaselCommitteehadtwoconsultationsforrevisingthecreditriskframework.Inthefirstconsultation,theytriedtodoawaywithcreditratingsforrisk-weightingbutlaterbacktrackedfromtheidea.Inthe2ndconsultationtheyhavegiventheoptionofassigningriskweightsbasedoneithercreditratingsorotherfactorsdependinguponwhetherthejurisdictionallowsuseofcreditratings.Butthatdoesnotstopcertainjurisdictionstonotallowuseofcreditratingsforriskweightingpurpose.Forexample,intheUSyoucannotuseexternalcreditratingsforriskweightingofassets.IntheEU,youcanuseexternalcreditratingstodetermineriskweights,butonlyfromratingagenciesapprovedbyESMAandmeetingcertainstandards(Li,2021).Ratingsandratingchangescancontainvaluablesignalsforitsusers,suchasinvestors.Somesignalsaremuchmorepowerfulthanother.Downgradesofratingsalongtheratingsscalereflecttheassessmentonincrementallyincreasingcreditrisk.Historically,ratingdowngradesatthetopofthescaleincreasedefaultrisklessthanatthelowerendofthespectrum(ofcourse,theoppositeappliesforupgrades).Butthereisnoempiricallydiscerniblecliff,wheredefaultprobabilitieswouldsuddenlychange.Itisasmoothgraduation.Unfortunately,thatisnothowthecapitalmarketsworkandreflectthoseratings.Investorsgenerallysubdividetheratingspectrumintoinvestmentgrade(BBB-orabove)andspeculative(ornon-investmentgrade,BB+orbelow)issuersandinstruments.Avastbodyofinvestmentguidelines,suchasofinstitutional

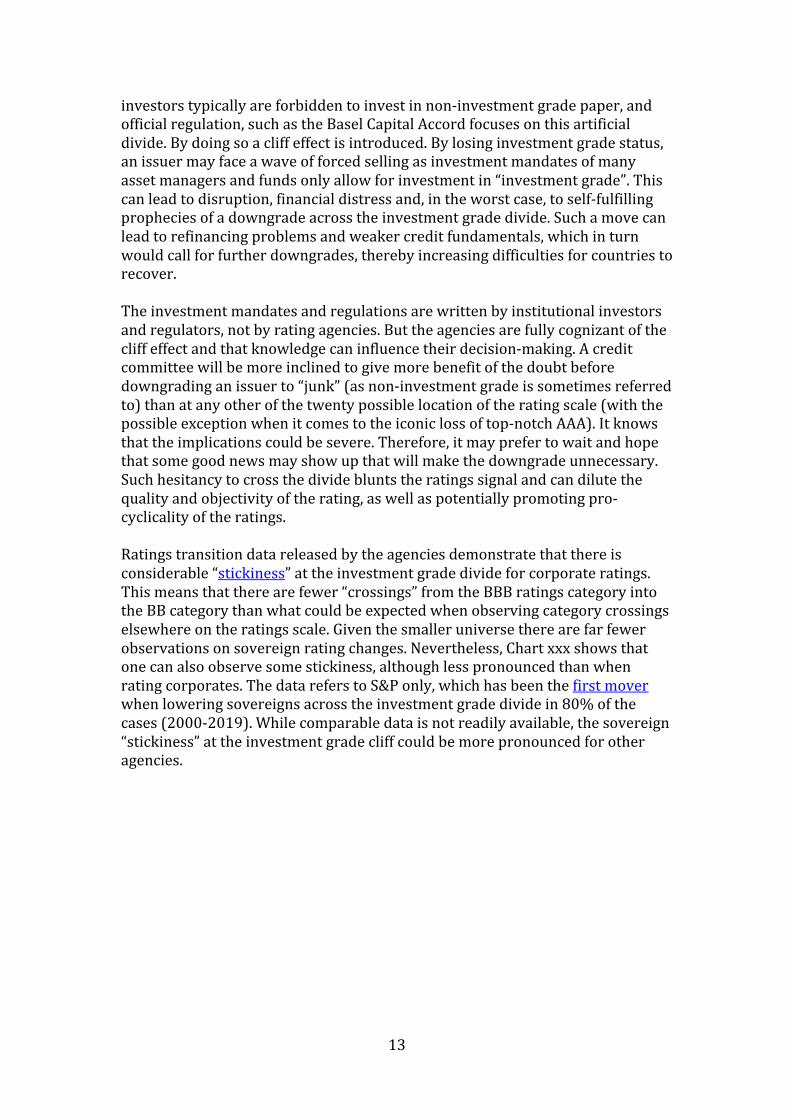

13

investorstypicallyareforbiddentoinvestinnon-investmentgradepaper,andofficialregulation,suchastheBaselCapitalAccordfocusesonthisartificialdivide.Bydoingsoacliffeffectisintroduced.Bylosinginvestmentgradestatus,anissuermayfaceawaveofforcedsellingasinvestmentmandatesofmanyassetmanagersandfundsonlyallowforinvestmentin“investmentgrade”.Thiscanleadtodisruption,financialdistressand,intheworstcase,toself-fulfillingpropheciesofadowngradeacrosstheinvestmentgradedivide.Suchamovecanleadtorefinancingproblemsandweakercreditfundamentals,whichinturnwouldcallforfurtherdowngrades,therebyincreasingdifficultiesforcountriestorecover.Theinvestmentmandatesandregulationsarewrittenbyinstitutionalinvestorsandregulators,notbyratingagencies.Buttheagenciesarefullycognizantofthecliffeffectandthatknowledgecaninfluencetheirdecision-making.Acreditcommitteewillbemoreinclinedtogivemorebenefitofthedoubtbeforedowngradinganissuerto“junk”(asnon-investmentgradeissometimesreferredto)thanatanyotherofthetwentypossiblelocationoftheratingscale(withthepossibleexceptionwhenitcomestotheiconiclossoftop-notchAAA).Itknowsthattheimplicationscouldbesevere.Therefore,itmayprefertowaitandhopethatsomegoodnewsmayshowupthatwillmakethedowngradeunnecessary.Suchhesitancytocrossthedividebluntstheratingssignalandcandilutethequalityandobjectivityoftherating,aswellaspotentiallypromotingpro-cyclicalityoftheratings.Ratingstransitiondatareleasedbytheagenciesdemonstratethatthereisconsiderable“stickiness”attheinvestmentgradedivideforcorporateratings.Thismeansthattherearefewer“crossings”fromtheBBBratingscategoryintotheBBcategorythanwhatcouldbeexpectedwhenobservingcategorycrossingselsewhereontheratingsscale.Giventhesmalleruniversetherearefarfewerobservationsonsovereignratingchanges.Nevertheless,Chartxxxshowsthatonecanalsoobservesomestickiness,althoughlesspronouncedthanwhenratingcorporates.ThedatareferstoS&Ponly,whichhasbeenthefirstmoverwhenloweringsovereignsacrosstheinvestmentgradedividein80%ofthecases(2000-2019).Whilecomparabledataisnotreadilyavailable,thesovereign“stickiness”attheinvestmentgradecliffcouldbemorepronouncedforotheragencies.

14

III. Policy Recommendations 1) Refocus regulatory scrutiny

Regulatorsneedtosharpentheirview.Theregulationoftheratingsindustryhastightenedsignificantly,atleastintheformalsenseintheaftermathoftheglobalfinancialcrisisandthewidelyshareddiscontentabouttheroleplayedbythecreditratingagencies,especiallyinthefieldofratingsub-primemortgagesegment.IntheEU,apan-Europeanregulationandregulator(ESMA)wasintroducedforthefirsttime.Agencieshavebeefeduptheirinternalrulesandcomplianceandqualitycontrolfunctions.Regulatoryfinesbecauseofbreachofregulationsorpoorlymanagedconflictsofinteresthavebeenfewandfarbetween.Inlinewiththeirmandates,regulatorshavebeenfocusingmoreontheformoftheratingsprocessthanonthesubstanceofdecisions.Agencieshaveprovendiligenttoadheretoallformalrulesofengagement,satisfyingregulators.Butasoutlinedabovetheremaybemoresubtlewaysinwhichconflictsofinterestcouldmanifestthemselvesandlead,e.g.,toananalyticallydiscriminatorypracticefavoringtheeconomieswhereagenciesreapmostoftheirprofits.Regulatorsdonotassessthoserisks.Andsinceregulatorsareagentsofadvancedeconomies’governments,theymightbeconflictedthemselvesifaskedtoensurecomparabilityofanalyticaltreatment.ThefactthatthechairoftheEUwatchdoghasreportedlycautionedratingagenciesagainst“quick-firedowngrades”ofsovereignscanberegardedasareflectionofthisinherentconflict,exacerbatingaprivilegedtreatmentofadvancedeconomies.Aglobal“super-regulator”ofCRAswouldbebestplacedtoaddresssuchissues.Theglobalregulator,whereEMDEswouldbeadequatelyrepresented,would

13.1

11.6

13.5

11.4

6.9

11.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

A BBB BB

Stickinessattheinvestmentgradedivide

Sovereigns

Corporates

Shareofissuersdowngradedinto thenextlowercategoryin3years(S&P,1975-2019).

15

complementtheactivitiesofnationalregulators.Itshouldbespecificallytaskedwithensuringglobalcompatibilityofratings.Itcouldrequireratingagenciestodisclosemoreinformationonhowdecisionshavebeenmade,includingmoremeaningfulminutesofcommittees.Rightnow,thereisacompleteregulatoryvoidtothatregard.Also,theglobalregulatorshouldberequestedtoassesstheadequacyofthequantityandprofessionalqualityofanalyticalstaff.Thisisacomplexundertaking,astheassessmentof“professionalskills”istoalargedegreeasubjectiveone.Butthisisnotthecaseentirely.Theregulatorshouldbeabletotrackmetricsofanalysts’objectiveprofessionalexperience(degrees,yearsofexperience,diversityofexperience)andcareerprogress.Thisshouldcontributetodiscouragingratingsfirmsfrompickingandpromotingwhattheyconsidermoremalleableanalysts.Thequantitymeasureofstaffisimportantasanalyticaloverstretchofanalystsmakesmistakesmorelikely,whichisanotherlessonfromthesubprimecrisis,butalsointhecaseofsovereignratings.

2.) Reducing dependency on credit ratings in regulation

IMF(opcit.)whenstudyingempiricallyhowratingagenciesrespondtoacrisis,concludethatratingagenciesdonotquiteseethroughacrisis.Ratingagencies,moreover,reactstrongerwhenthecrisisisdeeper,andexceedsaminimumthreshold.Onecouldargue,asIMF(opcit.)doesthatbankcapitalrequirementsshouldinsteadbecountercyclical:duringadownturninthebusinesscycle,someofthefactorsforwhichacapitalcushionisneededarematerializingandcapitalshouldbeappliedforthesepurposes.Capitalrequirementscanbesmallerduringdownturnswhenwrite-offsarerelativelyhighbutexpectedtodecline.Consequently,thereisaneedformechanismstodeterminecapitalrequirementsthatsufferlessfrompro-cyclicalityandcontagionsensitivityofratings.Regulatoryinitiativesinthewakeoftheglobalfinancialcrisisaimedatreducingthehardwiringofratingsintoregulation.Sofar,however,littletangibleprogresshasbeenmade.Apossibleinstitutionalsolution,insteadofusingCRAstodeterminecapitalrequirements,inthecontextoftheBaslecapitalaccordcouldincludeforexample:establishmentbybankingsupervisorsofasmallcountrycreditbureauthatdoestheabove,whiletappinginformationfromIFIsandexportcreditagencies.Suchanewinstitutionwouldhavetobeindependent,bothofprivateactorsandgovernmentsinitsdecision-making.Thissolution,orsimilarwouldcutthelinkbetweenCRAratingsandtheBaselCapitalAccord,whichevidencesuggestsincreasespro-cyclicalityinfinancialregulation,insteadofpromotingcounter-cyclicality.Suchasolutioncouldbringaboutthedesiredunlinkingregulatoryrequirementsfromcreditratingsissuedbyprivatefirms.However,it,too,comeswithgovernancechallengesregardingtheinstitutionalandpoliticalindependenceofsuchaninstitution.

16

3.) Reduce cliff effects

Standardsettersacrosstheglobeshouldworktowardssofteningtheinvestmentgradecliffeffect.Theartificialdivisionoftheinvestableuniverseintotwodistinctreservesofinvestmentandspeculativegradeisanoversimplification.Itdoesnotonlynotdojusticetothemuchfinergradationsoftheratingsscale,butalsocreatesself-inflictedrisksforfinancialstability.Whatwasoncedesignedasaneasyshorthandmarketconventionhastakenonasupersizedlifeofitsown.Policymakersshouldtakebackcontrolandreducetheundesirablesideeffectsofthedivide.Anyreformwillhavetoconsiderthatsomedegreeofaggregationofcreditriskswillberequiredforasmoothfunctioningofthecreditandbondmarketsandtoaccommodatethelackofdeeperfinancialeducationofmanyretailinvestors,thataremeanttobeprotectedbysuchclassificationsfromoverlyriskyexposures.Amiddlewaycouldconsistofdividingtheratingsuniverseintohigh-,mid-andlow-graderatings.Ideallytherewouldbesomeoverlapintheratingsscalesothatadowngradedoesnotleadtoacompletelossofonesetofinvestors(whichare,forexamplerestrictedtohighgrade),beforeanothersetofinvestors(mid-grade)comesin.Anoverlapwouldpermitforasmootherentryandexitofinvestorclasseswithdifferentriskappetites.Thedangerofsuddendownwardspiralsfollowingratingactionswouldbereduced.Agenciescouldagaintakeratingactionsinlinewiththewaytheyseecreditrisksevolving.Theynolongerwouldhavetoworryabouthowaratingactionacrossthecurrentlyexistinginvestmentgradedividecouldcreateaviciouscirclebyitselfunderminingthecreditqualityoftheissuerunderconsideration.Removingthecliffwouldenhancethequalityandcomparabilityofratingsignals,whileminimizingstabilityrisks.

4.) Improving transparency of CRA methodologies

Thiscouldbedonebyseparatingmoreexplicitly:a)analysisofsimulationsandstresstests(whilstmakingunderlyingmodelexplicitonwhichbased)andb)morejudgement-based(qualitative)analysis;a)andb)wouldbepublishedseparately,butwithinthesamereport.Thiswouldclarifywhatthejudgementelement,e.g.,ongovernanceandpoliticsofcountry,oftheratingis,asopposedtomorequantitativeevaluationofriskofdefaultis.TheglobalregulatorrecommendedinIII.1shouldberequiredtoopineontherobustnessofratingmethodologiesappliedandthetransparencyinitsworldwideapplication.Currentlynationalregulatorsonlylookatindividualratingactionsinisolationonacase-by-casebasis.Thisexpandedremitmustnotremovetheabilityofratingagenciestodesignandmodifythecriteriaunderwhichtheyassignratings.Thatisoneoftheircoreresponsibilities.Buttheglobal

17

regulatorneedstobeempowered(bothinstitutionallyandprofessionally)toscrutinizeandchallengethemethodologicaldecisionstakenbytheagenciesmoreforcefully.

5.) Long-term ratings

Thelong-termcreditratingissuedbytheagenciesaresupposedlycalibratedtoreflectcreditriskupto3to5yearsintothefuturefornoninvestmentgradeissuersanduptotenyearsforinvestmentgrade.Thisisamuchlongerhorizonthatwhatnormallyprevailsinfinancialmarkets.Buttheaspirationaltimehorizonpostulatedbytheagenciesdoesnotchimewithobservablereality.Inthefieldofsovereignratings,theeconomicandfinancialforecastsappliedforthisforward-lookinglong-termratingrarelyextendsbeyondthreeyears.Inotherassetclassesitisless.Itappearsthattheactualratinghorizonismuchshorterandtypicallynotbeyondtwotothreeyears.Atthesametimelonger-termtrends,fromageingsocietiestoclimatechangeareboundtobecomemorebindingcreditrisksforsovereigns.Andsovereignissuershavetakenrecoursetoeverlongertenorsintheirbondissuance,pushingtheyieldcurveinsomecasesoutto50oreven100years.Overthepastdecadeaveragetermtomaturityhasincreasedinmostcountrieswherethecorrespondingdataisavailable.Incombination,thesetrendsmakealonger-termperspectiveofratingsincreasinglyurgent.Ratingagenciesshouldbecompelledtomakemoreexplicitlong-termcreditanalysisorstopratingbondsaboveacertaininitialmaturity,e.g.,10years.Therelativeshort-termperspectiveoftheratingscanbemisleadingwhenratingsareappliedtoratepaymentstreamsdecadesintothefuture.Suchlonger-termratingsshouldexplicitlyreflectplausiblecreditimpactsofclimatechange.AswasshowninsectionII.4,researchhasshownthatlong-termsovereignratingimplicationscanbesubstantial,forrichandpoorcountriesalike.Establishingsuchlonger-termratingswillallowinvestorstogaugetheireffectiveriskexposuremorereliably.Currentlytheyarewithoutanyreliableyardstick.Anadditionalbenefitwouldconsistinincentivizinggovernmentstoengageinlessmyopicpolicies:arobustclimatemitigationpolicy,forexample,couldimproveasovereign’sratingrelativetoitspeers.Rightnow,nosuchincentiveexists.

6.) Alternative ownership models

Callstocreateneworpubliccreditratingagencieshaveresonatedfromdifferentcorners,withparticularstrengthaftercrises,andespeciallyduringtheCOVIDinducedcrisis(Li,opcit;Gosh,2021).Indeed,Gosh(opcit.)hasrecentlyarguedthatthecaseforanindependentpublicratingsagencyhasneverbeenstronger.InitsTradeandDevelopmentReport2020,UnitedNationsConferenceonTradeandDevelopment(UNCTAD)advocatedforaninternationalpubliccreditratingagencytoprovideobjectiveexpert-basedratingsofthecreditworthinessof

18

sovereigns,includingdevelopingcountries.UNCTADhaslongarguedthattheworldneedssuchanindependentpublicratingsagency.SuchapublicCRAagency,whichcouldberegionalorglobal,deservesseriousconsideration,especiallyasacomplementtoexistingprivateCRAs.Afterall,competitioncanintroduceefficiency.Indeed,itispossiblethatthecreationofapublicCRAcouldencourageimprovementsintheefficiencyofprivateCRAs.Furthermore,apublicCRAwouldnothavethetypeoffinancialincentives,whichcouldencourageprivateCRAstobetoolenientinboomyears,asthisismorelikelytoattractclientsfortheirbusiness,whichisanimportantadvantageofpublicCRAs.However,apublicratingagencywouldcomewithpotentiallyitsownsetofconflictsofinterest,whichrequirecarefulmanagementtoallowanalyststooperateatarmslengthfromgovernments’influence,orthatofanyotherpublicbody.Apubliclysponsoredratingagencycouldbefounded,specializingontheverylong-termratings.Thisagencycouldbeusedasabenchmarkthroughwhichtheincumbentagencies’ownlong-termratingscanbeassessed.Theverylong-termnatureoftheratingsmaylessenthepotentialforconflictofinterest,butitdoesnotremoveitcompletely.Stronggovernancestandardswillthereforeberequiredtoensureanarms-lengthrelationshipwithgovernmentsandavoidconflictsofinterest.Analternative,especiallyforissuingultra-longcreditratingssuchasdiscussedabove,couldbeanindependentfoundation-basedmodel,withanot-forprofit-institution,thatwouldhaveitsowngovernance,beingarmslength,bothfromgovernmentsandtheprivatesector,buttrustedbyboth.Initslong-termcreditratings,suchanagencycoulddevelopexpertiseandincorporatelong-termelementssuchascountries’vulnerabilitytoclimatechangeandtheirinvestmenteffortsatadaptationandbuildingresilience;morebroadly,itcouldevaluatetheimpactofcountries’investmentonthefuturegrowthanddevelopmentofthesecountries,whichwillinfluencetheirfutureabilitytoservicedebt,dimensionsnotcurrentlytakenaccountofbyexistingratingagencies.

Bibliography

Becker, Manuel (2021) The unintended consequences of regulatory import: the Basel Accord’s failure during the financial crisis. Journal of European Public Policy, vol 28; issue 2:248-267 Bolton,Patrick,XavierFreixasandJoelShapiro.2012.“TheCreditRatingsGame.”TheJournalofFinance.LXVII(1):85-111.

19

Broto,CarmenandLuisMolina.2016.“SovereignRatingsandtheirAsymmetricResponsetoFundamentals.”JournalofEconomicBehavior&Organization.130:206-224.Ferri,G.,L.-G.LuiandJ.E.Stiglitz.1999.“TheProcyclicalRoleofRatingAgencies:EvidencefromtheEastAsianCrisis.”EconomicNotesbyBancoPaschidiSiena.28(3):335-355.Ghosh,Jayati(2021)“Credit-RatingAgenciesCouldDerailEconomicRecovery”ProjectSyndicate,March2021Goodhart,Charles.2008.“TheRegulatoryResponsetotheFinancialCrisis.”CESIFOWorkingPaperNo2257.InternationalEnergyAssociation(IEA)2020“WorldEnergyOutlook”IMF(2000)BrieucMontfortandChristianMulder“UsingCreditratingsforcapitalregulationonLendingtoEmergingMarketEconomies:PossibleimpactonBaselAccord.WB/00/69Kramer,Moritz(2014)“Standard & Poor's Sovereign Ratings Anchored Expectations In The Depths Of Eurozone Crisis”, June 14, 2014 Larrain,Guillermo,HelmutReisenandJuliavonMaltzan.1997.“EmergingMarketRiskandSovereignCreditRatings.”OECDDevelopmentCentreWorkingPaperNo.124.Paris:OECD.Li,Yuefen(2021)“Theroleofcreditratingagenciesindebtrelief,debtcrisispreventionandhumanrights”February.UnitedNationsHumanRights.OfficeoftheHighCommissioner.A/HRC/46/29Masciandaro,Donato.2011.“WhatifCreditRatingAgenciesWereDowngraded?Ratings,SovereignDebtandFinancialMarketVolatility.”“PaoloBaffi”CentreResearchPaperSeriesNo.2011-107.Mora,Nada.2006.“SovereignCreditRatings:GuiltyBeyondReasonableDoubt?”JournalofBankingandFinance.30:2041-2062.Pretorius,MarindaandIlseBotha.2017.“TheProcyclicalityofAfricanSovereignCreditRatings.”InNicholasTsounisandAspasiaVlachvei(eds.)AdvancedinAppliesEconomicResearch.Springer:Chapter35.537-546.

Related Documents