Credit Contracts Credit Contracts Faith Cheok Faith Cheok Consumer Credit Legal Service (WA) Inc Consumer Credit Legal Service (WA) Inc September 2011 September 2011 This presentation is for information This presentation is for information only. You must seek legal advice in only. You must seek legal advice in relation to any particular relation to any particular circumstances. circumstances.

Credit Contracts Faith Cheok Consumer Credit Legal Service (WA) Inc September 2011 This presentation is for information only. You must seek legal advice.

Dec 31, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Credit ContractsCredit Contracts

Faith CheokFaith Cheok

Consumer Credit Legal Service (WA) Consumer Credit Legal Service (WA) IncInc

September 2011September 2011 This presentation is for information only. You This presentation is for information only. You

must seek legal advice in relation to any must seek legal advice in relation to any particular circumstances.particular circumstances.

Vulnerable and Vulnerable and disadvantaged consumersdisadvantaged consumers

Fair relationships with banks Fair relationships with banks & financial institutions& financial institutions

Established February 1991

Case files

Caller help line100 + advice and cases per m

onth

Regulation of CreditRegulation of Credit Credit reform 2010/2011Credit reform 2010/2011

New Regulator – ASICNew Regulator – ASIC

Licensing and compulsory EDRLicensing and compulsory EDR

The The National Consumer Credit Protection Act National Consumer Credit Protection Act 20092009 (and regulations) (“NCCP Act”) commenced 1 (and regulations) (“NCCP Act”) commenced 1 July 2010July 2010

The The National Credit Code National Credit Code (“NCC”)(“NCC”)

- Uniform Consumer Credit Code (“UCCC”) amended - Uniform Consumer Credit Code (“UCCC”) amended & adopted as a schedule to the NCCP Act& adopted as a schedule to the NCCP Act

What loans are covered by What loans are covered by the NCCP and NCC?the NCCP and NCC?

Loans for Loans for personal, domestic, household personal, domestic, household purposes such as home loans, credit cards, purposes such as home loans, credit cards, motor vehicles loans and personal loans motor vehicles loans and personal loans ((same as UCCCsame as UCCC))

Loans for Loans for investment in residential investment in residential property property and re-finances of such loans (and re-finances of such loans (newnew))

Pawnbroking Pawnbroking is only covered by the unjust is only covered by the unjust contract provisionscontract provisions

Australian Credit LicenceAustralian Credit Licence

Who needs a licence?Who needs a licence? Persons who engage in credit activitiesPersons who engage in credit activities Exceptions: credit rep, employee or Exceptions: credit rep, employee or

exemptexempt

Dispute ResolutionDispute Resolution

Each licensee and credit representative Each licensee and credit representative must:must:

Have an IDR procedureHave an IDR procedure Be a member of an EDR scheme - Be a member of an EDR scheme - FOS or FOS or

COSLCOSL

EDREDR

Benefits of EDR for consumersBenefits of EDR for consumers:: FreeFree alternative to court alternative to court NoNo possibility of a possibility of a costscosts order order Accessible – complaints can be made by Accessible – complaints can be made by

unrepresented consumers unrepresented consumers or or lay advocateslay advocates No physical appearance necessary No physical appearance necessary – largely paper – largely paper

& telephone-based& telephone-based EDR possible even after legal proceedings EDR possible even after legal proceedings

commenced unless judgment entered (but COSL commenced unless judgment entered (but COSL possible)possible)

Note limitations of EDRNote limitations of EDR

Responsible LendingResponsible Lending

The NCCP has created RL obligations.The NCCP has created RL obligations. Obligations apply to Obligations apply to brokers and brokers and

lenders lenders (and any (and any other other intermediary intermediary interfacing with the interfacing with the consumer or making lending consumer or making lending decisions).decisions).

They apply to They apply to loans and loans and consumer leasesconsumer leases..

Responsible LendingResponsible Lending

Disclosure:Disclosure: a a Credit Guide Credit Guide about the licensee;about the licensee; Credit service providers Credit service providers (brokers) (brokers)

must provide the consumer with a must provide the consumer with a quotequote prior to providing credit assistanceprior to providing credit assistance

AssessmentAssessment The requirement to assess whether a The requirement to assess whether a

loan is “loan is “not unsuitablenot unsuitable”.”.

Responsible LendingResponsible Lending

Brokers/lenders must not suggest, recommend Brokers/lenders must not suggest, recommend or approve a loan or lease unless they have or approve a loan or lease unless they have conducted the above assessment and conducted the above assessment and concluded that the loan is “concluded that the loan is “not unsuitablenot unsuitable”.”.

A loan must be assessed as “unsuitable” if:A loan must be assessed as “unsuitable” if: The consumer will not be able to pay, or not The consumer will not be able to pay, or not

without substantial hardshipwithout substantial hardship; and /or; and /or The loan does not meet the consumer’s The loan does not meet the consumer’s

needs and requirements.needs and requirements.

Responsible LendingResponsible Lending

Lenders and brokers must:Lenders and brokers must: Make Make reasonable enquiriesreasonable enquiries about the about the

borrower’s borrower’s financial circumstancesfinancial circumstances Make Make reasonable enquiriesreasonable enquiries about the about the

borrower’s borrower’s needs and requirementsneeds and requirements Take Take reasonable stepsreasonable steps to to verifyverify the the

above informationabove information

Responsible LendingResponsible Lending

There is a There is a presumptionpresumption that, if the that, if the consumer could consumer could only comply only comply with the with the terms of a loan by terms of a loan by selling their selling their principal residenceprincipal residence, then the , then the consumer could only comply with consumer could only comply with substantial hardshipsubstantial hardship. .

Note:Note: this must be foreseeable at the this must be foreseeable at the time of the assessment, not as a result time of the assessment, not as a result of a later, unplanned occurrence such of a later, unplanned occurrence such as illness or unemployment.as illness or unemployment.

Responsible LendingResponsible Lending

The end to questionable practices?The end to questionable practices? Complaints can plead Complaints can plead bothboth the the

responsible lendingresponsible lending provisions provisions and and unjust contractunjust contract under under section 76 (UCCC s70)section 76 (UCCC s70)

Credit contract - defaultCredit contract - default

A client is in default if they are just 1 A client is in default if they are just 1 day lateday late

CP cannot take any action against CP cannot take any action against the client until a default notice has the client until a default notice has been sentbeen sent

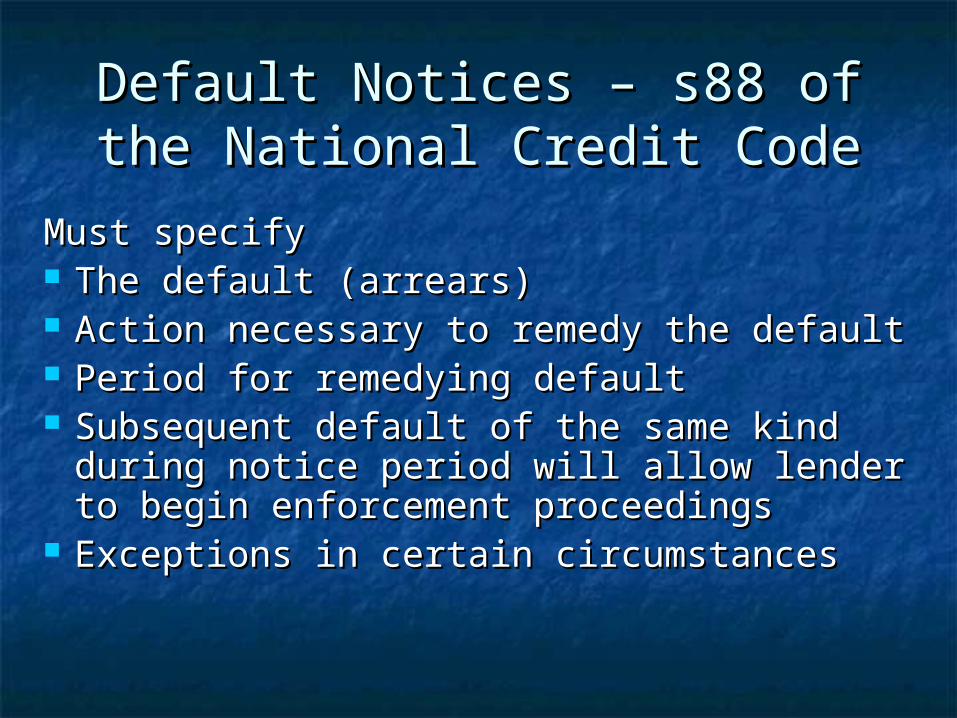

Default Notices – s88 of the Default Notices – s88 of the National Credit CodeNational Credit Code

Must specifyMust specify The default (arrears)The default (arrears) Action necessary to remedy the defaultAction necessary to remedy the default Period for remedying defaultPeriod for remedying default Subsequent default of the same kind Subsequent default of the same kind

during notice period will allow lender during notice period will allow lender to begin enforcement proceedingsto begin enforcement proceedings

Exceptions in certain circumstancesExceptions in certain circumstances

Default - SummaryDefault - Summary

Debtor has 30 days from date of Debtor has 30 days from date of default notice to remedy the default. default notice to remedy the default.

If they do so, the credit contract is If they do so, the credit contract is reinstated.reinstated.

If they do not remedy the default, CP If they do not remedy the default, CP can initiate enforcement can initiate enforcement proceedings.proceedings.

Repossession of goods Repossession of goods (usually cars)(usually cars)

RestrictionsRestrictions Less than 25% or $10,000.00, Less than 25% or $10,000.00,

whichever is less (s91 NCC)whichever is less (s91 NCC) Consent to enter residential premises Consent to enter residential premises

required (s99 NCC)required (s99 NCC)Options at this StageOptions at this Stage Pay arrears and costs before Pay arrears and costs before

repossessionrepossession Hardship VariationHardship Variation EDR SchemeEDR Scheme Refinance/pay out contractRefinance/pay out contract Voluntarily Surrender Voluntarily Surrender

RepossessionRepossession

CP may repossess goods if CP may repossess goods if default not remedieddefault not remedied

After repossession of goodsAfter repossession of goods

Options at this StageOptions at this Stage Pay arrears and enforcement expenses Pay arrears and enforcement expenses

(goods must be returned)(goods must be returned) Pay out contract (goods must be Pay out contract (goods must be

returned)returned) Nominate purchaserNominate purchaser Hardship VariationHardship Variation EDR SchemeEDR Scheme

See section 102 NCC for required See section 102 NCC for required procedure:procedure:

Within 14 days of repossession CP to Within 14 days of repossession CP to give notice: estimated value of goods, give notice: estimated value of goods, arrears and enforcement expensesarrears and enforcement expenses

Goods not to be sold for 21 daysGoods not to be sold for 21 days If arrears and enforcement expenses If arrears and enforcement expenses

paid up in this 21-day period, CP must paid up in this 21-day period, CP must return goods return goods

Otherwise CP must sell car for the Otherwise CP must sell car for the best price reasonably obtainable as best price reasonably obtainable as soon as reasonably practicable soon as reasonably practicable

Credit Provider must Credit Provider must send a notice send a notice stating:stating:

Amount the vehicle Amount the vehicle was sold forwas sold for

Amount owingAmount owing Proposed recovery Proposed recovery

actionaction

OptionsOptions Check sale price – was it Check sale price – was it

reasonable (s104), check Red reasonable (s104), check Red Book websiteBook website

Shortfall debt – pay in full, Shortfall debt – pay in full, payment arrangement, payment arrangement, bankruptcy etcbankruptcy etc

After Goods are SoldAfter Goods are Sold

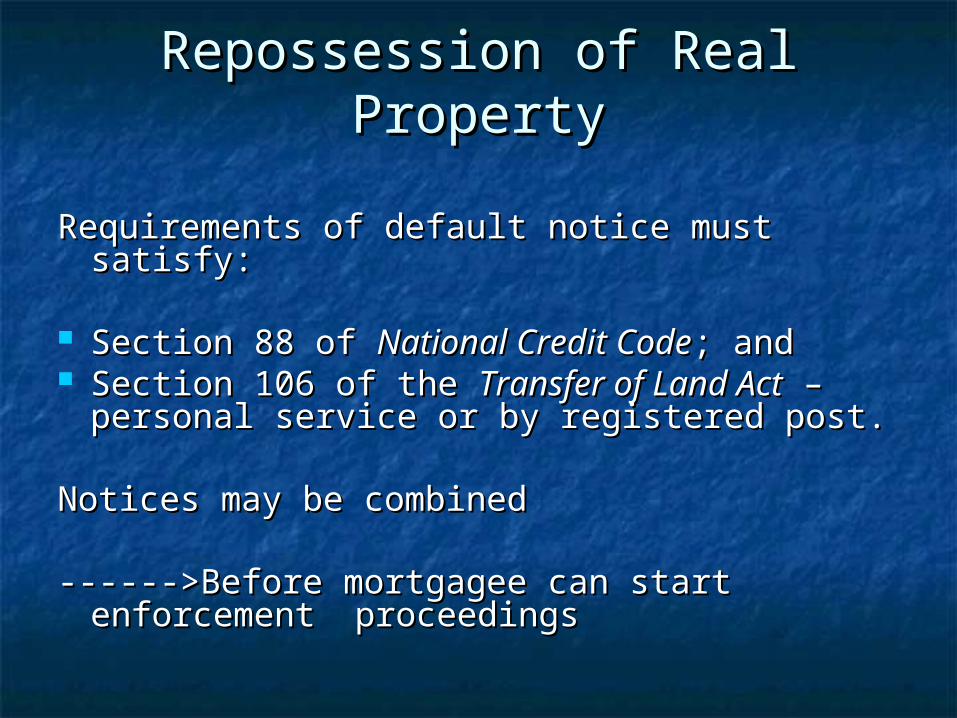

Repossession of Real PropertyRepossession of Real Property

Requirements of default notice must satisfy:Requirements of default notice must satisfy:

Section 88 of Section 88 of National Credit CodeNational Credit Code; and; and Section 106 of the Section 106 of the Transfer of Land ActTransfer of Land Act – –

personal service or by registered post.personal service or by registered post.

Notices may be combinedNotices may be combined

------>Before mortgagee can start ------>Before mortgagee can start enforcement enforcement proceedingsproceedings

Repossession of Real Property Repossession of Real Property (cont’d)(cont’d)

Negotiations?Negotiations? hardship variation per NCC?hardship variation per NCC? Other options –EDR, refinance, sell?Other options –EDR, refinance, sell?

Enforcing the MortgageEnforcing the Mortgage

Ways to enforce:Ways to enforce:

1.1. Request vacant possession (Section Request vacant possession (Section 108 of 108 of Transfer of Land ActTransfer of Land Act); or); or

2.2. Start legal proceedings in the Start legal proceedings in the Supreme Court for possession Supreme Court for possession and/or payment of all monies due.and/or payment of all monies due.

Enforcement methodsEnforcement methods

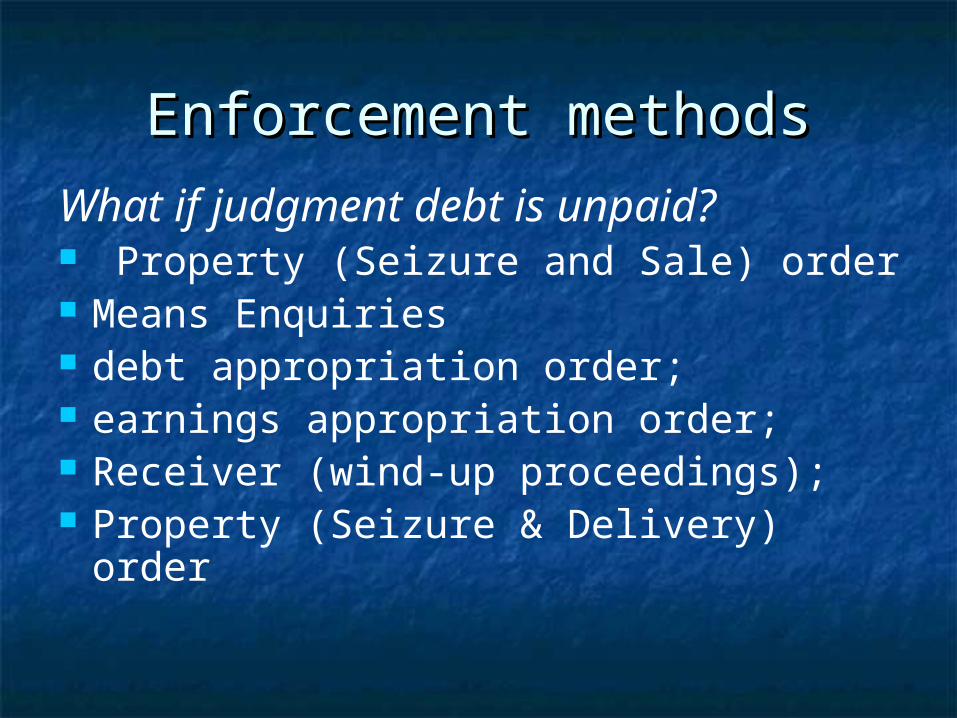

What if judgment debt is unpaid? Property (Seizure and Sale) order Means Enquiries debt appropriation order; earnings appropriation order; Receiver (wind-up proceedings); Property (Seizure & Delivery) order

PSDOPSDO

PSDOsPSDOsProperty Seizure and Delivery Orders

Direct the Sheriff and/or his bailiff delegates to take delivery of property (generally real property) and deliver it to the applicant;

The Enforcement Officer will generally (but is not obliged to) post notice of the intended eviction date;

The Sheriff’s Office manages enforcement of all PSDOs issued out of the Supreme and District Court (usually re default on mortgage repayments)

The Bailiffs manage enforcement of PSDOs issued out of the Magistrates Court (usually re tenants’ default on rental payments)

Related Documents