Credit card market study Interim findings November 2015 1

Credit card market study Interim findings November 2015 1.

Jan 17, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Credit card market study Interim findings

November 2015

2

The scope

Why we are carrying out a market study:

• To build a sound understanding of the market

• Assess whether it’s working well in the interest of consumers

3

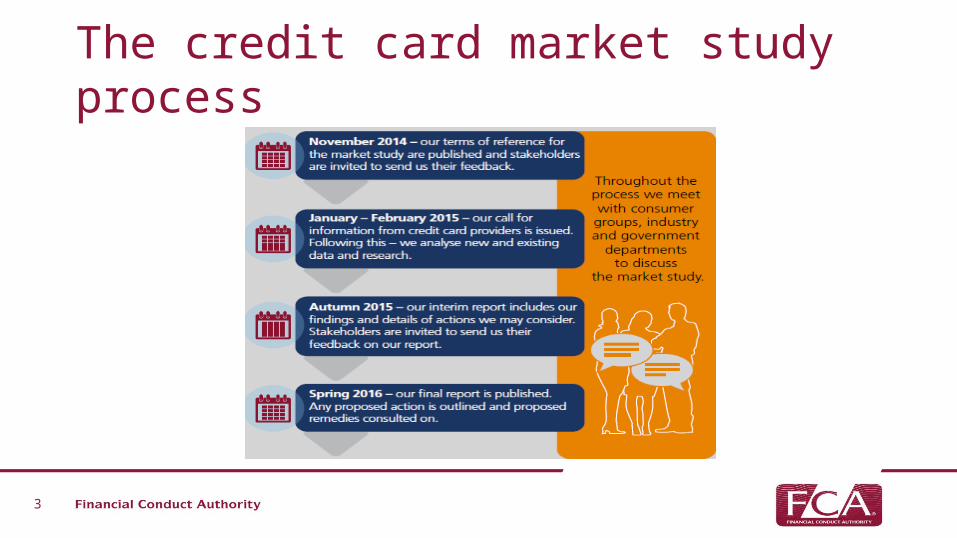

The credit card market study process

4

Three areas of investigation

• The extent to which consumers drive effective competition through shopping around and switching.

• How do firms recover their costs across different cardholder groups and what is the impact of this on the market?

• What is the extent of unaffordable credit card debt?

5

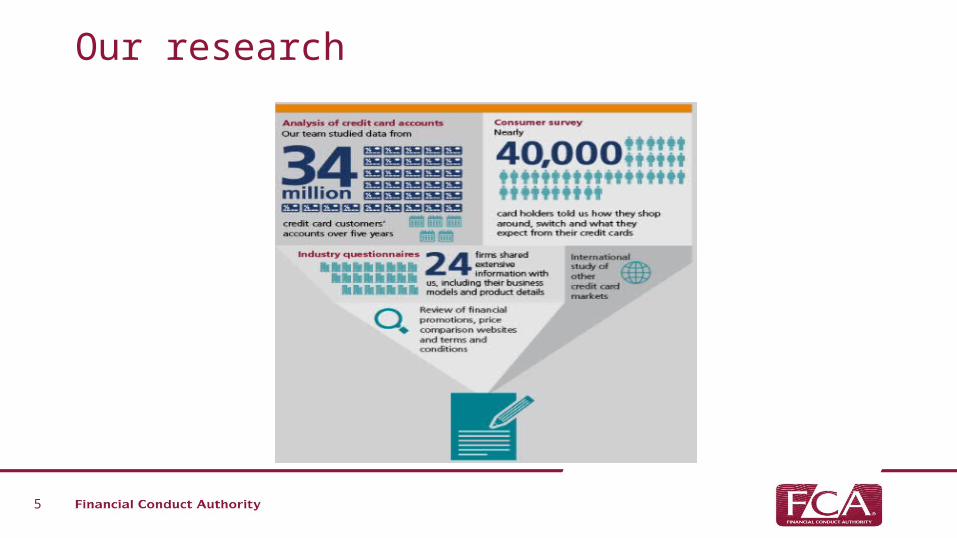

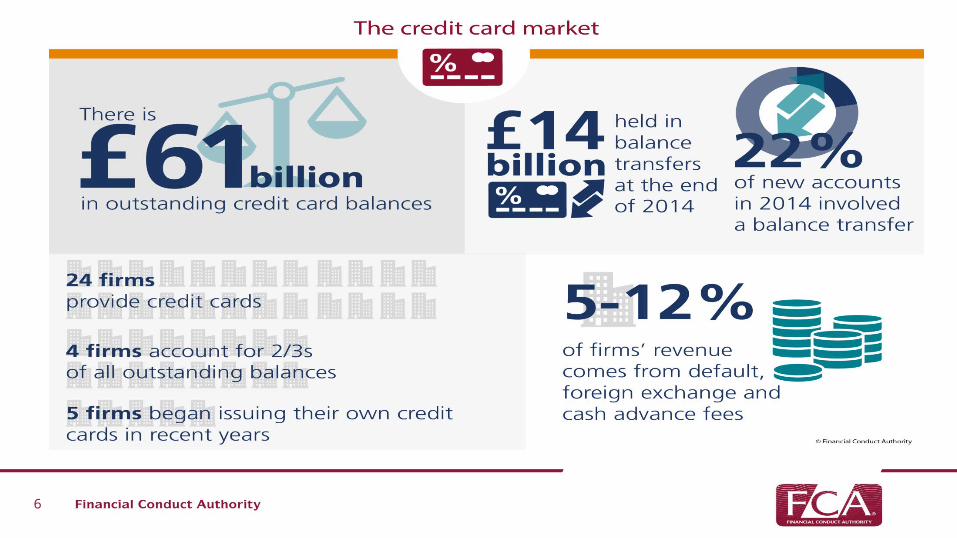

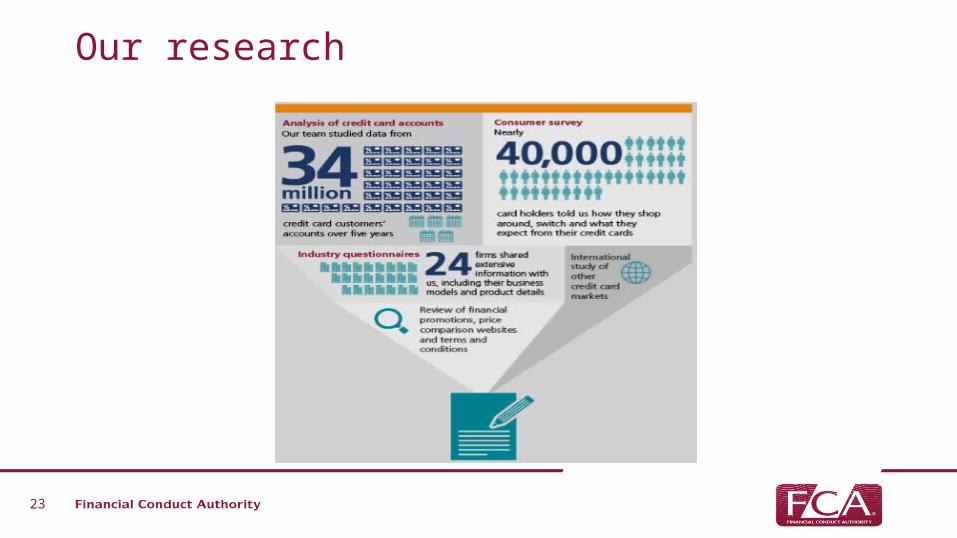

Our research

6

7

8

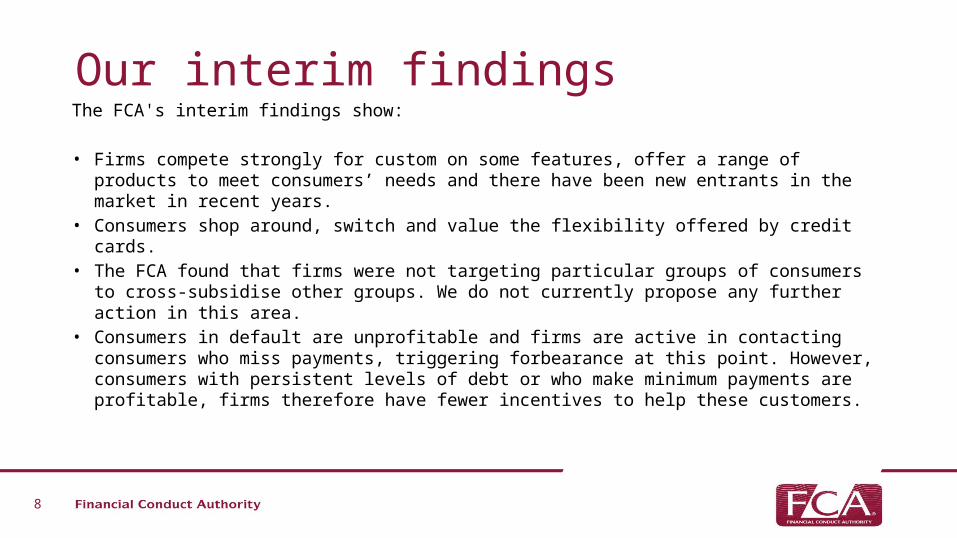

Our interim findingsThe FCA's interim findings show:

• Firms compete strongly for custom on some features, offer a range of products to meet consumers’ needs and there have been new entrants in the market in recent years.

• Consumers shop around, switch and value the flexibility offered by credit cards.

• The FCA found that firms were not targeting particular groups of consumers to cross-subsidise other groups. We do not currently propose any further action in this area.

• Consumers in default are unprofitable and firms are active in contacting consumers who miss payments, triggering forbearance at this point. However, consumers with persistent levels of debt or who make minimum payments are profitable, firms therefore have fewer incentives to help these customers.

9

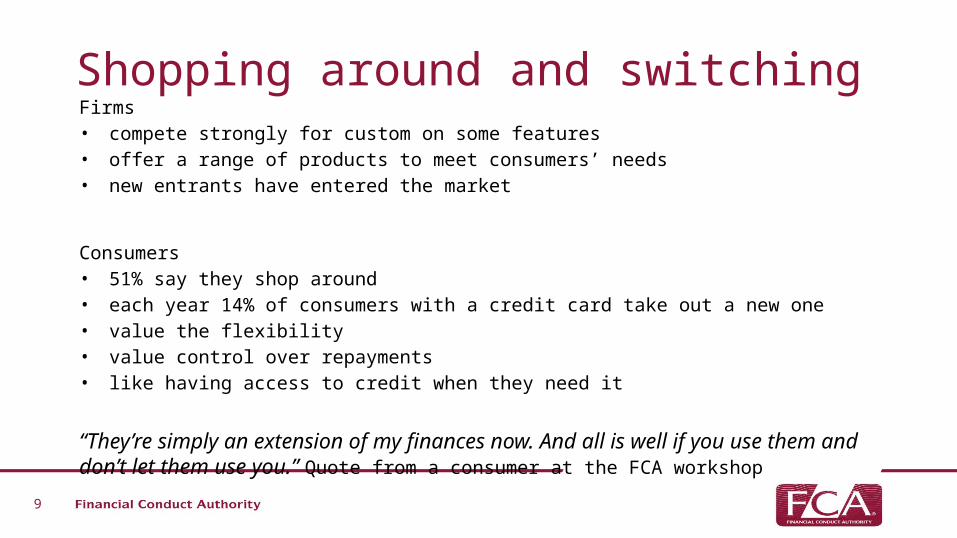

Shopping around and switchingFirms • compete strongly for custom on some features• offer a range of products to meet consumers’ needs • new entrants have entered the market

Consumers • 51% say they shop around• each year 14% of consumers with a credit card take out a new one • value the flexibility• value control over repayments• like having access to credit when they need it

“They’re simply an extension of my finances now. And all is well if you use them and don’t let them use you.” Quote from a consumer at the FCA workshop

10

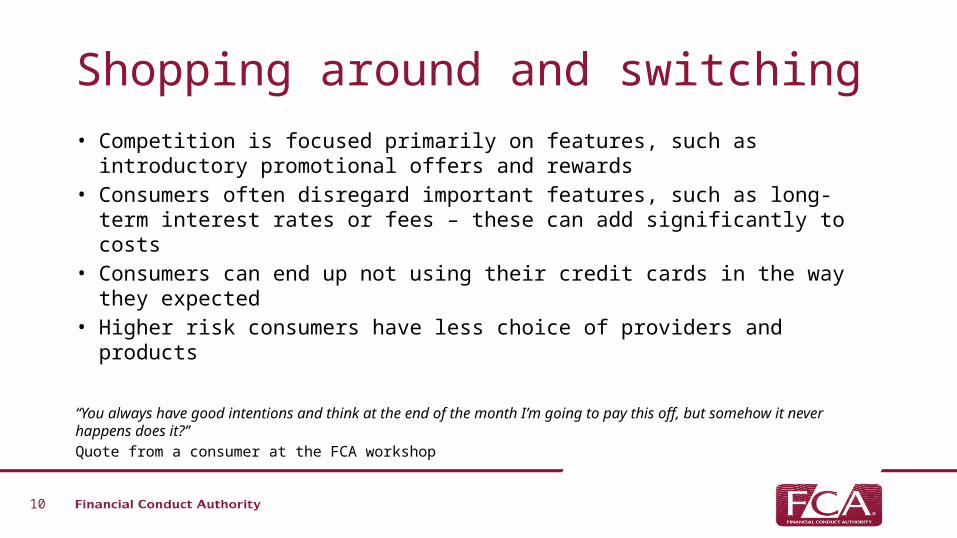

Shopping around and switching• Competition is focused primarily on features, such as

introductory promotional offers and rewards • Consumers often disregard important features, such as long-

term interest rates or fees – these can add significantly to costs• Consumers can end up not using their credit cards in the way

they expected• Higher risk consumers have less choice of providers and

products

“You always have good intentions and think at the end of the month I’m going to pay this off, but somehow it never happens does it?” Quote from a consumer at the FCA workshop

11

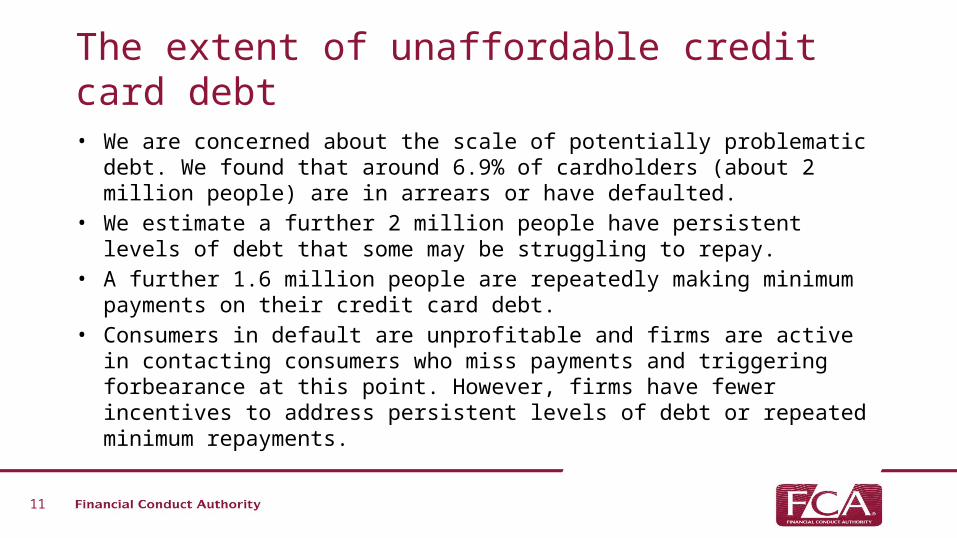

The extent of unaffordable credit card debt• We are concerned about the scale of potentially problematic

debt. We found that around 6.9% of cardholders (about 2 million people) are in arrears or have defaulted.

• We estimate a further 2 million people have persistent levels of debt that some may be struggling to repay.

• A further 1.6 million people are repeatedly making minimum payments on their credit card debt.

• Consumers in default are unprofitable and firms are active in contacting consumers who miss payments and triggering forbearance at this point. However, firms have fewer incentives to address persistent levels of debt or repeated minimum repayments.

12

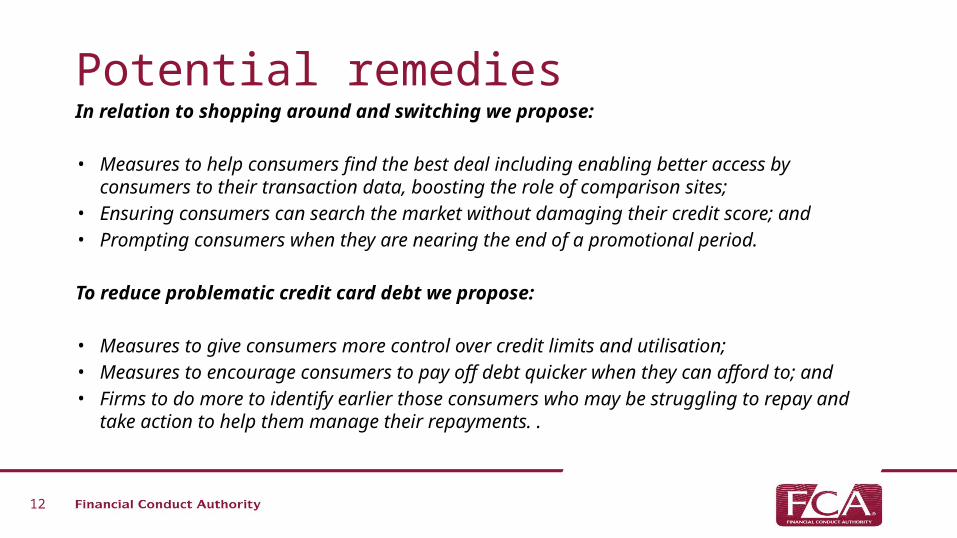

Potential remediesIn relation to shopping around and switching we propose: • Measures to help consumers find the best deal including enabling better access by

consumers to their transaction data, boosting the role of comparison sites; • Ensuring consumers can search the market without damaging their credit score; and• Prompting consumers when they are nearing the end of a promotional period. To reduce problematic credit card debt we propose:

• Measures to give consumers more control over credit limits and utilisation;• Measures to encourage consumers to pay off debt quicker when they can afford to;

and• Firms to do more to identify earlier those consumers who may be struggling to repay

and take action to help them manage their repayments. .

13

Next stepsWe have already engaged with a large number of consumer groups, firms and industry bodies

We want to discuss our interim findings and potential remedies with stakeholders

We plan to publish our final report, including any action we may take, in Spring 2016

Please send your feedback to us by 8 January 2016

14

Any questions?

Quarterly Trade Body Event 5 November 2015

Philip SalterDirector of Retail Lending, Supervision – Retail and Authorisations Division

• Welcome and introduction

• Credit Card Market Study - Brian Corr

• Policy update – Martin Goulden

• Latest Authorisation data – David Fisher

• Supervision – Roma Pearson

• Introduction to the new handbook – Alan Blanchard

• Conclusion and networking lunch

Authorisations Director

Susan de Mont

GI&P Sector Director

Simon Green

Retail Lending Sector Director

Philip Salter

Retail Banking Sector DirectorKarina McTeague

Mortgages & Mutuals HoD

Alison Carpenter

Consumer Credit Supervision HoD

Roma Pearson

Wholesale HoDMark Wilson

Retail HoDMichael Sicsic

Large Retails Banking 2 HoDClare Bolingford

Large Retail Banking 1 HoDJeremy Marsden

Debt, Credit & Regulatory HoD

Nick Mears

Credit HoDDavid Fisher

Debt HoDHilary Bourne

Dual Regulated HoD Lucy Castledine

APPM HoD

Pat Knox

Contact Centre HoDChris Jell

Permissions HoDLucy McClements

Conduct Supervision HoD

David Blunt

Credit Authorisations

Change Director Val Smith

Supervision Retail & Authorisations Director

Jonathan Davidson

SUPVERVISION Retail & Authorisations

Brian Corr Head of Department Competition Division

19

Credit card market study Interim findings

November 2015

20

The scope

Why we are carrying out a market study:

• To build a sound understanding of the market

• Assess whether it’s working well in the interest of consumers

21

The credit card market study process

22

Three areas of investigation

• The extent to which consumers drive effective competition through shopping around and switching.

• How do firms recover their costs across different cardholder groups and what is the impact of this on the market?

• What is the extent of unaffordable credit card debt?

23

Our research

24

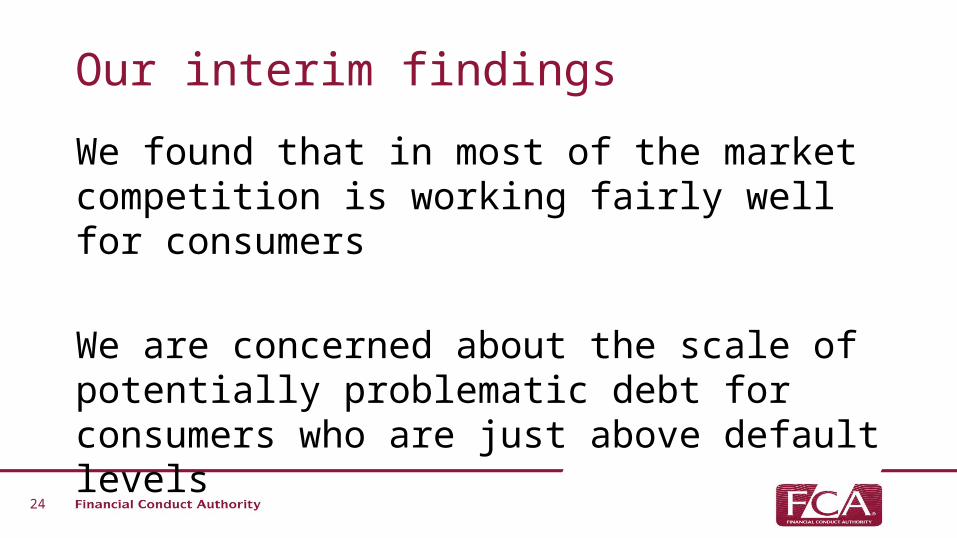

Our interim findings

We found that in most of the market competition is working fairly well for consumers

We are concerned about the scale of potentially problematic debt for consumers who are just above default levels

25

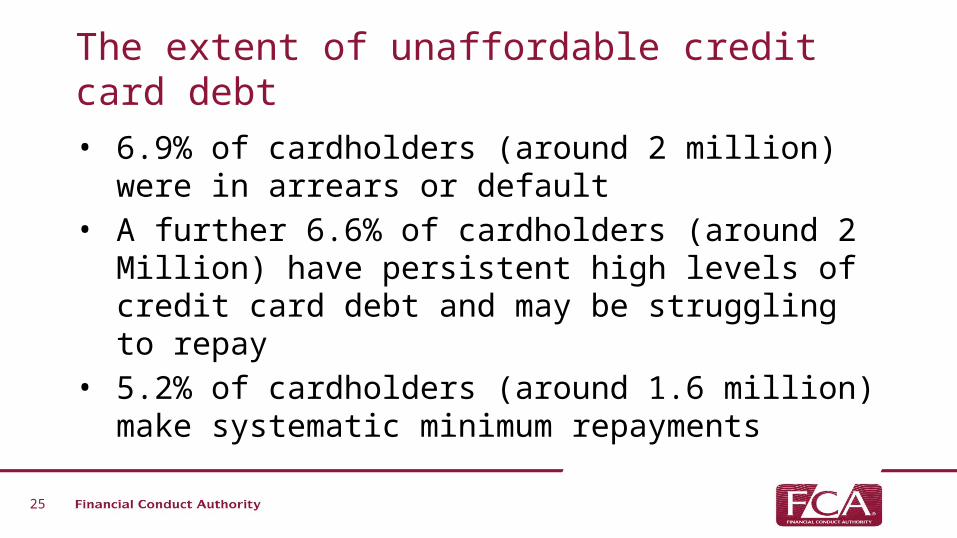

The extent of unaffordable credit card debt• 6.9% of cardholders (around 2 million)

were in arrears or default• A further 6.6% of cardholders (around 2

Million) have persistent high levels of credit card debt and may be struggling to repay

• 5.2% of cardholders (around 1.6 million) make systematic minimum repayments

26

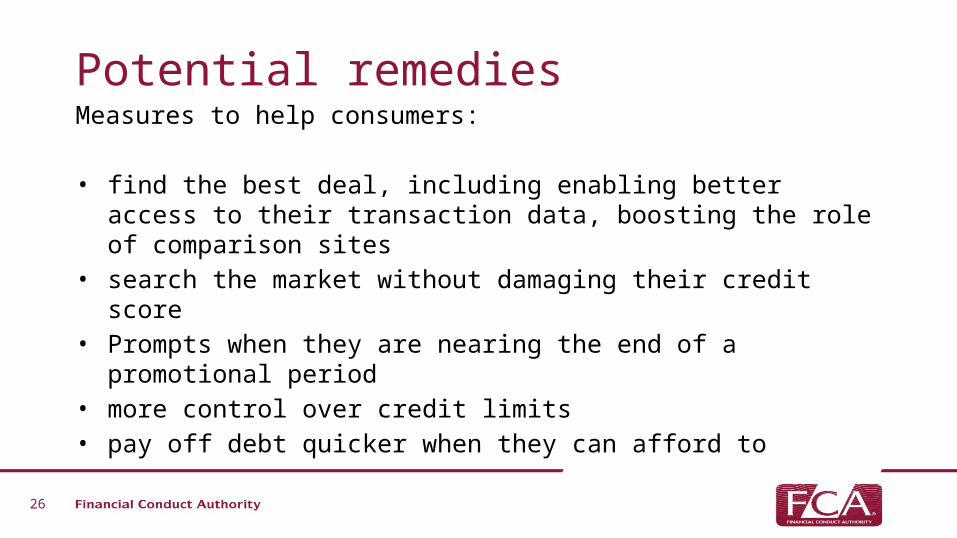

Potential remediesMeasures to help consumers:

• find the best deal, including enabling better access to their transaction data, boosting the role of comparison sites

• search the market without damaging their credit score• Prompts when they are nearing the end of a

promotional period• more control over credit limits• pay off debt quicker when they can afford to

27

Potential remedies

Firms: • to identify earlier, consumers who may be

struggling to repay • take action to help them manage their

repayments

28

Next stepsWe have already engaged with a large number of consumer groups, firms and industry bodies

We want to discuss our interim findings and potential remedies with stakeholders

We plan to publish our final report, including any action we may take, in Spring 2016

Please send your feedback to us by 8 January 2016

29

Any questions?

Martin GouldenConsumer Credit Policy

31

Summary PS15/23 published 28 September – feedback on CP15/6 Further work on credit broking and guarantor lending Round table on creditworthiness – 30 September CP15/30 on 1 October – pension reforms CP15/33 on 28 October – CMA proposals on HCSTC Quarterly consultation in December – to include proposed change on 0% APR

financial promotions (flagged in PS15/23) Review of creditworthiness and quotation searches Review of cold-calling and unsolicited marketing Initial planning for 2019 review of retained CCA provisions

32

PS15/23 – credit brokers Retain PS14/18 rules on disclosure of fees/status Initial impact assessment in April 2015 Minor change to CCR008 reporting requirement Minor changes to other CONC rules Further impact assessment in Q1 2016 Further work on credit broking remuneration including disclosure of

fees/commissions and timing of fees To assess whether there are gaps in current rules that need filling and

whether/what additional rules are required Further consultation in 2016 if needed

33

PS15/23 – lending Guarantor lending – treat guarantor as ‘customer’ for purposes of Principles 6 and 7 and key

CONC rules Scope – borrower and guarantor are both ‘individuals’ Adequate explanations – can be delivered by broker or solicitor as part of independent legal

advice, subject to conditions Creditworthiness – may be different for borrower/guarantor Further work on guarantor lending to assess whether additional rules required (eg post-

contract and approaching guarantor) Further consultation in 2016 if needed Joint borrowers – guidance on explanations/creditworthiness Other proposals – explanations, creditworthiness, enforceability

34

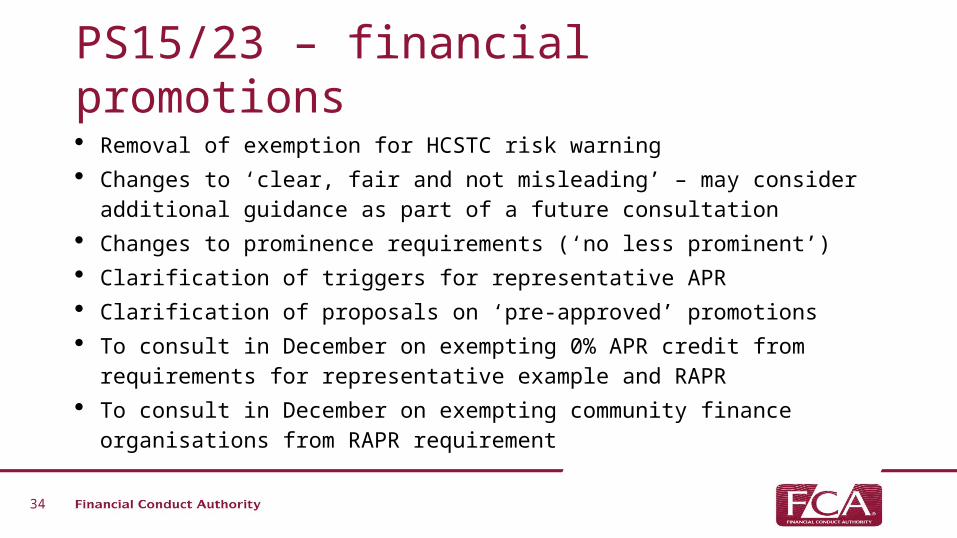

PS15/23 – financial promotions Removal of exemption for HCSTC risk warning Changes to ‘clear, fair and not misleading’ – may consider additional guidance as

part of a future consultation Changes to prominence requirements (‘no less prominent’) Clarification of triggers for representative APR Clarification of proposals on ‘pre-approved’ promotions To consult in December on exempting 0% APR credit from requirements for

representative example and RAPR To consult in December on exempting community finance organisations from RAPR

requirement

35

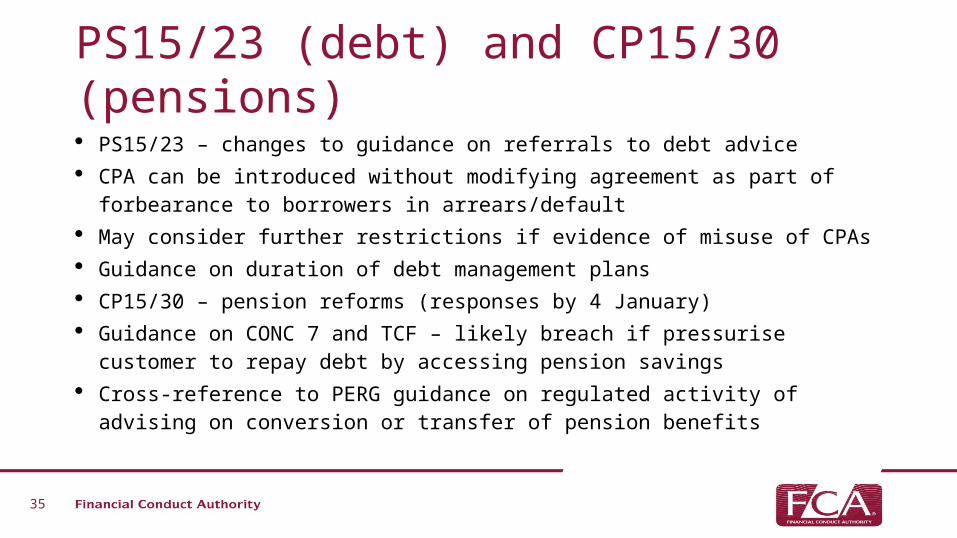

PS15/23 (debt) and CP15/30 (pensions) PS15/23 – changes to guidance on referrals to debt advice CPA can be introduced without modifying agreement as part of forbearance to

borrowers in arrears/default May consider further restrictions if evidence of misuse of CPAs Guidance on duration of debt management plans CP15/30 – pension reforms (responses by 4 January) Guidance on CONC 7 and TCF – likely breach if pressurise customer to repay debt

by accessing pension savings Cross-reference to PERG guidance on regulated activity of advising on conversion

or transfer of pension benefits

36

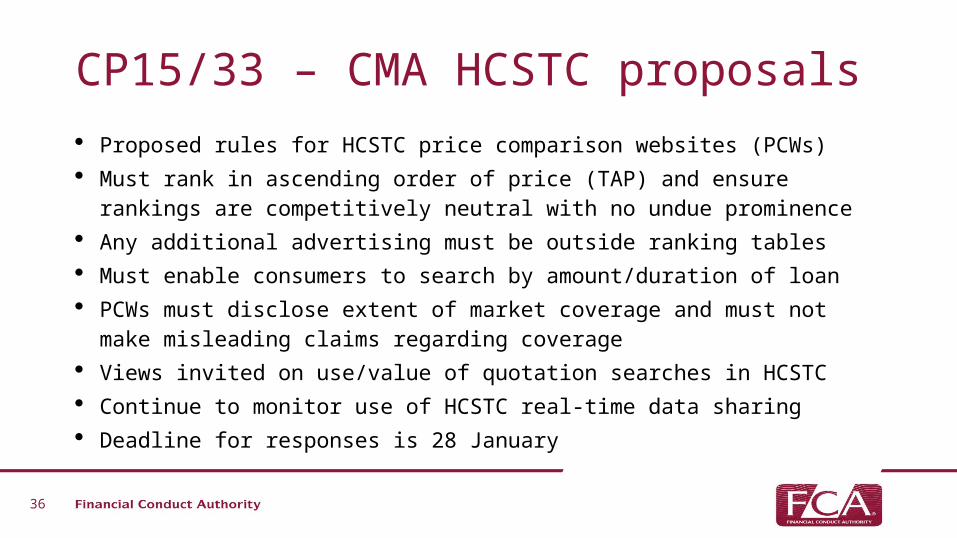

CP15/33 – CMA HCSTC proposals Proposed rules for HCSTC price comparison websites (PCWs) Must rank in ascending order of price (TAP) and ensure rankings are competitively

neutral with no undue prominence Any additional advertising must be outside ranking tables Must enable consumers to search by amount/duration of loan PCWs must disclose extent of market coverage and must not make misleading

claims regarding coverage Views invited on use/value of quotation searches in HCSTC Continue to monitor use of HCSTC real-time data sharing Deadline for responses is 28 January

37

Other policy work Research into how firms assess creditworthiness (including affordability) to inform possible

changes to CONC rules/guidance Firm pilot survey to commence shortly; other work ongoing May supplement ‘common misunderstandings’ document (or issue similar documents in

other areas) Review of repeat and multiple borrowing in HCSTC Further work to promote/facilitate use of quotation searches Possible work on wider issues regarding PCWs in credit markets Review of rules on cold-calling and unsolicited marketing Initial scoping of review of retained CCA provisions (to report to HM Treasury by 1 April

2019) – will engage with stakeholders

David FisherHead of Credit Permissions, Credit Authorisations

40

Authorisations update

Three quarters of eligible firms applied or become appointed representatives

Significant number allowed interim permissions to lapse or cancelled

Application rate from new entrants running at roughly twice expected level

Of applications determined, 94% were authorised

Of remainder, we refused to authorise some but most withdrew

41

Authorisations update

Timescales for determining applications set by FSMA

6 months from application deemed complete – maximum of 12 from receipt

On average, 10 weeks to determine limited permission applications

14 weeks for variation of permissions and 24 for full permissions

Breached statutory deadlines in 13 cases - 0.2% of total

Roma Pearson Head of Department Consumer Credit Supervision

43

Life after Authorisation: what next?

• Supervision is an ongoing process• Key priority: embedding the Principles for

Businesses • Principle 11 considerations:

• Understand your reporting obligations• Remember you must apply for approval or notify us when you make

certain changes• Notify us of significant events

• Stay in touch with consultations and rule changes

44

External engagement

• Trade events• Webinars• “Purple Guide”• Web content

45

Changes to the supervision modelFixed Portfolio

Flexible Portfolio

Named supervisor

Cycle of regular assessments and meetings

Engage with us via the Contact Centre

Ad-hoc interaction

46

Thematic review of staff incentives and remuneration• Phase I - desk-based analysis of information from

c.100 firms. Complete.• Phase II – Visits and more detailed analysis of a

smaller sample. Ongoing through Q1 2016.• We will notify firms as soon as possible if we are

including them in Phase II.• All firms to be visited this year have been notified.• No feedback to firms until mid-2016.

47

Thematic review of early arrears management in unsecured credit• Currently finalising analysis of firm

information• Moving on to review of customer case

files• Expect to visit firms in Q1 2016• Reporting summer 2016

Alan Blanchard Handbook Publisher

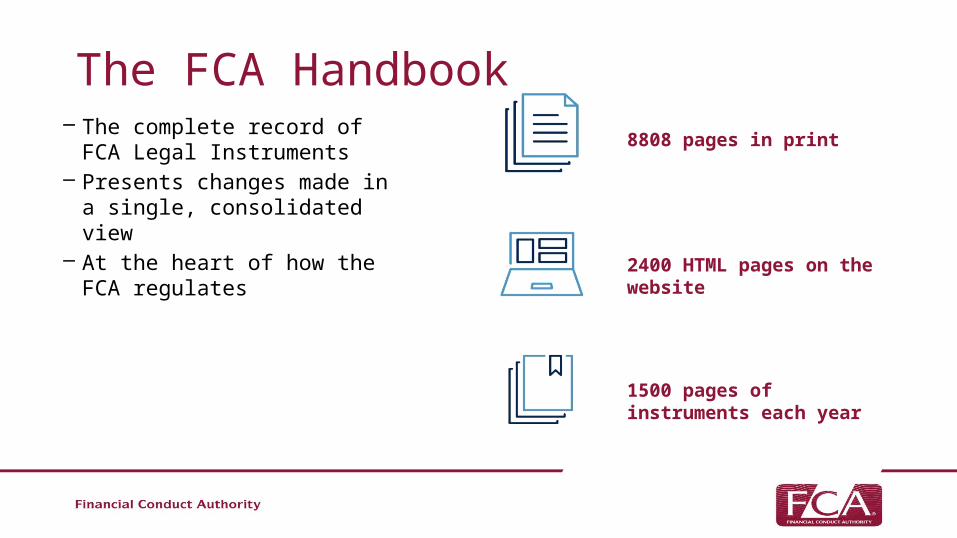

– The complete record of FCA Legal Instruments

– Presents changes made in a single, consolidated view

– At the heart of how the FCA regulates

The FCA Handbook 8808 pages in print

2400 HTML pages on the website

1500 pages of instruments each year

The challenge Glossary

High Level Standards(PRIN, SYSC, COCON, COND, APER, FIT, FINMAR, TC, GEN, FEES)

Definitions for the Handbook

Prudential Standards(GENPRU, BIPRU, IFPRU, MIPRU, IPRU (FSOC), IPRI (INS), IPRU (INV))

Business Standards(COBS, ICOBS, MCOBS, BCOBS, CASS, MAR)

Regulatory Processes(SUP, DEPP)

Redress(DISP, CONRED, COMP)

Specialist Sourcebooks(COLL, CREDS, CONC, FUND, PROF, RCB, REC)

Listing, Prospectus & Disclosure Rules(LR, PR, DR)

This section of the Handbook contains the requirements for all authorised persons (firms) and approved persons, it also contains general interpretive material

Providing prudential and specific notification requirements for the sectors listed for each source book

Day-to-day conduct rules that apply to firms

These modules describe the operations of our supervisory and disciplinary functions, as well as requirements on firms relating to the supervisory function

The modules in Redress outline the processes for handling complaints and compensation

This part of the Handbook indicates to firms in certain sectors how the Handbook applies to their businessRequirements for issuers listed on, or seeking addition to, the Official List of the UK Listing Authority (UKLA), rules that apply to a sponsor and a person applying for approval as a sponsor, as well as prospectus and disclosure document requirements

Handbook Guides(EMPS, OMPS, SERV, BENCH)

Regulatory Guides (COLLG, EG, FC, PERG, RPPD, UNFCOG)

Guides for particular firms, indicating material that applies to them

Guides to particular regulatory topics within the Handbook

Sourcebooks and Manuals“Sourcebooks” cover the commercial activity of firms, providing sources of the FCA’s requirements and guidance. “Manual” covers the relationship between the firm and the FCA, containing processes to be followed.

Who uses the FCA Handbook?

Lawyers Consumers

I’m looking for

something specific to

my firm/market

I want to understand my rights

and protect myself

I want to get a task completed

quickly

I need to submit a complaint

Firms

I need to be

knowledgeable about a product

I have lots of

questions, please help

Compliance Officers

Research process

– Design and navigation – layout and table of contents– Time travel timeline– Favourites– Search with filters– Pop up glossary definitions

Improved functionality

54

Changes

Feedback from users

I look forward to further

developments. All particularly relevant in the context of the

burgeoning RegTech sector

I think the new website is generally much better

than previously

I noticed the Handbook had a fresh

new look and was hugely

easier to navigate

This new handbook

website is a distinct and

major improvement on the former

offering

The new Handbook

website is a welcome sight and looks very

good. Congrats

Excellent! I love it and it looks very good. Well

done!!

Much better

format to navigate

A welcome and refreshing

revision to the way in which the principles and rules are presented.

This will enhance

FCA’s communicati

on and accessibility

A definite improvement on the

previous format, thanks!

… would be great to add a filter at the

top to choose a type of firm, and hide or

grey out non applicable rules and

guidance

56

What’s next?

57

Print version

• Complete reissue• PRA removed• 10,000 pages pre-relaunch• 8,808 pages now• Will grow back:• MiFID• MAR• COCON

58

Any questions?

Related Documents