Full Terms & Conditions of access and use can be found at http://www.tandfonline.com/action/journalInformation?journalCode=mree20 Download by: [University of Florida] Date: 11 January 2018, At: 04:56 Emerging Markets Finance and Trade ISSN: 1540-496X (Print) 1558-0938 (Online) Journal homepage: http://www.tandfonline.com/loi/mree20 Credit Allocation and Firm Productivity under Financial Imperfection: Evidence from Chinese Manufacturing Firms Hua Shang, Teng Zhang & Puman Ouyang To cite this article: Hua Shang, Teng Zhang & Puman Ouyang (2017): Credit Allocation and Firm Productivity under Financial Imperfection: Evidence from Chinese Manufacturing Firms, Emerging Markets Finance and Trade, DOI: 10.1080/1540496X.2017.1410474 To link to this article: https://doi.org/10.1080/1540496X.2017.1410474 Accepted author version posted online: 27 Dec 2017. Submit your article to this journal Article views: 3 View related articles View Crossmark data

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

-

Full Terms & Conditions of access and use can be found athttp://www.tandfonline.com/action/journalInformation?journalCode=mree20

Download by: [University of Florida] Date: 11 January 2018, At: 04:56

Emerging Markets Finance and Trade

ISSN: 1540-496X (Print) 1558-0938 (Online) Journal homepage: http://www.tandfonline.com/loi/mree20

Credit Allocation and Firm Productivity underFinancial Imperfection: Evidence from ChineseManufacturing Firms

Hua Shang, Teng Zhang & Puman Ouyang

To cite this article: Hua Shang, Teng Zhang & Puman Ouyang (2017): Credit Allocation and FirmProductivity under Financial Imperfection: Evidence from Chinese Manufacturing Firms, EmergingMarkets Finance and Trade, DOI: 10.1080/1540496X.2017.1410474

To link to this article: https://doi.org/10.1080/1540496X.2017.1410474

Accepted author version posted online: 27Dec 2017.

Submit your article to this journal

Article views: 3

View related articles

View Crossmark data

http://www.tandfonline.com/action/journalInformation?journalCode=mree20http://www.tandfonline.com/loi/mree20http://www.tandfonline.com/action/showCitFormats?doi=10.1080/1540496X.2017.1410474https://doi.org/10.1080/1540496X.2017.1410474http://www.tandfonline.com/action/authorSubmission?journalCode=mree20&show=instructionshttp://www.tandfonline.com/action/authorSubmission?journalCode=mree20&show=instructionshttp://www.tandfonline.com/doi/mlt/10.1080/1540496X.2017.1410474http://www.tandfonline.com/doi/mlt/10.1080/1540496X.2017.1410474http://crossmark.crossref.org/dialog/?doi=10.1080/1540496X.2017.1410474&domain=pdf&date_stamp=2017-12-27http://crossmark.crossref.org/dialog/?doi=10.1080/1540496X.2017.1410474&domain=pdf&date_stamp=2017-12-27

-

Acce

pted M

anus

cript

1

Credit Allocation and Firm Productivity under Financial

Imperfection: Evidence from Chinese Manufacturing Firms*

Hua SHANG

Research Institution of Economics and Management, Southwestern University of

Finance and Economics, No.55 Guanghuacun Street, Chengdu, Sichuan, China,

610074, Email address: [email protected]

Teng ZHANG**

Corresponding author. School of Securities and Futures, Southwestern University of

Finance and Economics, No.55 Guanghuacun Street, Chengdu, Sichuan, China,

610074, Email address: [email protected]

Puman OUYANG

Research Institution of Economics and Management, Southwestern University of

Finance and Economics, No.55 Guanghuacun Street, Chengdu, Sichuan, China,

610074, Email address: [email protected]

* We would like to thank Xun Zhang, the two anonymous referees and the editor Ali Kutan for their comments and suggestions. All the remaining errors are ours. ** Corresponding author.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

https://crossmark.crossref.org/dialog/?doi=10.1080/1540496X.2017.1410474&domain=pdf&date_stamp=2017-12-24

-

Acce

pted M

anus

cript

2

Abstract: The role of the financial system, especially the credit market, in

productivity enhancement has interested many researchers. However, how credit

allocation affects firms’ productivity in emerging economies remains unanswered.

Using data from the Annual Survey of Industrial Firms (ASIF) during 1999-2007, this

paper examines whether credit allocation impacts Chinese firms’ productivity under

financial imperfection. Our results show that the size of credit market has no influence

on Chinese firms’ total factor productivity (TFP), while allocating more credit to

non-SOEs significantly promotes firm TFP. Our further analysis shows that firms

which are less subsidized, smaller, more external financially dependent, and more

labor intensive are affected more by credit allocation. Since China is the largest

emerging economy, our analysis also sheds light on the development of firms in

emerging economies.

Key words: credit allocation; financial depth; firm TFP; Heterogonous effects

JEL classification: D24; G21; O12

1. Introduction

There is a growing literature investigating the factors leading to the differences of

aggregate total factor productivity (TFP) in each country. Many theories have pointed

out that the differences of the TFP between emerging economies and developed

countries is due to misallocation of resources and financial friction in emerging

economies (Restuccia & Rogerson, 2008; Hsieh & Klenow, 2009; Buera et al., 2009).

Since firms’ TFP is an important element of aggregate TFP, examining how financial

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

3

market impacts firms’ TFP provides the micro sight to very understanding of the

relationship between finance and aggregate TFP. In a market where financial

resources are limited, a better allocation of resources rather than size of the financial

market is expected to promote firms’ TFP. In particular, if credit can be allocated to

firms based on their performances, the firms’ TFP and then the aggregate TFP is

expected to be promoted.

China provides a good case study to investigate the credit allocation and firms’

TFP under financial imperfection. The misallocation of credit has long been a

problem in China. The financial institutions, especially the banks, are used to

distributing disproportionately more credit to poorly performing SOEs (State-owned

enterprises) (Allen et al., 2005; Bai et al., 2006; Cull et al., 2009). The non-SOEs are

lacking of credit due to their short credit history (Stein, 2002) and low chances of

being bailed out by the governments (Brandt & Li, 2003). However, the performance

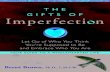

of non-SOEs on average are much better than SOEs. As shown in Fig.1, the average

firm TFP of SOEs is substantially lower than that of non-SOEs during 1999-2007,

indicating that the Chinese SOEs are less productive than non-SOEs. Erosa and

Hidalgo-Cabrillana (2007) point out that financial market imperfection may distort

firms’ selection and discourage firm growth. Therefore, the misallocation of credit

may impede the enhancement of Chinese firms’ TFP on average. This is because the

low-productive SOEs always have better access to external finance regardless of their

performances as credit expands, and they may have no incentive to struggle in

difficult but productivity-improving activities, resulting in a continuing low-level TFP.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

4

On the other hand, the more productive non-SOEs are unlikely to obtain enough

financial support from the credit market. This might hinder their ability to further

improve their TFP.

Under the circumstance of financial imperfection in China, we expect that firms’

TFP will be higher in a province with higher proportion of credit to non-SOEs. Since

in current China, the non-SOEs have better performances and are more financially

constraint than SOEs in general, allocating more credit to non-SOEs indicates that the

financial system is evolving towards a well-developed system (Firth et al., 2009; Fan

et al., 2011; Qian & Yeung, 2015; Qian et al., 2015). This is consistent with the

argument of King and Levine (1993a) that if the private sector is more productive

than the public sector, a system allocating a higher proportion of credit to the private

sector is a well-developed system. The finance and growth literature suggests that

macro-level financial environment affect firms’ behavior and outcomes. King and

Levine (1993b) argue that financial system plays an active role in evaluating,

managing and funding firms’ activities that leads to productivity growth. Rajan and

Zingales (1998) show that financial development reduces the moral hazard and

adverse selection problems and thus decreases the costs of external finance to firms.

Amore et al. (2013) and Hsu et al. (2014) find that financial market development and

credit supply affects technology innovation of firms. Krishnan et al. (2015) argue that

credit supply affects small firms’ productivity in US.1 Fig.2 further illustrates the

1 In the finance and growth literature, it is common to analyze how country-level or region-level financial factors affect firms’ behavior. Among the papers we cite, King and Levine (1993b), Rajan and Zingales (1998) and Amore et al. (2013) conduct cross-country analyses and investigate how country-level financial development affects firms’ behavior. Hsu et al. (2014) and Krishnan et al., (2015) analyze how state-level credit supply affects publicly traded

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

5

increasing trend of firm TFP and credit allocation measured by an index constructed

from the ratio of credit to non-SOEs to total credit over time.2 The similar increasing

trend of firm TFP and credit allocation implies that a better credit allocation may help

to improve Chinese firms’ TFP on average. Therefore, it is natural to expect that firms

in a province allocating more credit to non-SOEs would have higher TFP which is the

most popular measure of productivity.

As far as we know, there is no research directly investigating how credit allocation

affects Chinese firms’ TFP. We intend to fill this gap. We also exam the heterogeneous

effects of credit allocation on firms’ TFP across firm and industry characteristics. The

data we mainly rely on is panel data of manufacturing firms obtained from Annual

Survey of Industrial Firms (ASIF) collected by National Bureau of Statistics of China

(NBSC) during 1999-2007.3 The majority of firms in this database are non-listed

firms. The firm-level panel data allows us to control many observed and unobserved

variables, such as firm-, industry-, and province-level variables which influence firms’

TFP. This reduces the potential endogeneity problem caused by omitted variables. In

our estimation, the reverse causality is not a big problem since the independent

variables are lagged by one year.4 Credit allocation in current period is expected to

affect firm performance in next period, while, a shock to firm-level TFP is unlikely to

affect the provincial-level credit allocation in the previous period. We further address

the potential endogeneity concern by controlling additional unobserved variables and manufacturing firms’ innovation and small firms’ productivity in US, respectively. 2 Please refer to Section 3.1 for a detailed description of the index. 3 In Section 3.2 we provide the reason for sample period selection. 4 Since firms’ TFP is an output of firm’s operation, while, credit is an input, it makes more sense that the lagged (beginning-period) credit allocation affects firms’ TFP.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

6

using instrumental variable (IV) method for robustness check. Furthermore, in order

to reduce the measurement errors of firm TFP and make our estimation results more

trustworthy, we adopt the approach of Brandt et al. (2012) to construct the

complementary panel of manufacturing firms and estimate firm-level TFP by using

the Levinsohn and Petrin’s (2003) method.

Our results show that under financial imperfection in China, the size of the credit

market has no significant impact on firm TFP, while allocating more credit to

non-SOEs contributes to the enhancement of firm TFP. Specially, credit allocation

contributes 5.425% to the rise of a Chinese firm’ TFP on average. This finding

suggests that a more efficient credit allocation, rather than simply enlarging the size of

the credit market, is an important way to promote firm TFP in China. Our results also

imply that under financial imperfection, the efficient credit allocation enhances

aggregate TFP in China, which is consistent with the argument in Hsieh and Klenow

(2009) that the aggregate TFP would be boosted if the allocation of resources

becomes better. The results are robust by adopting different methods to cluster

standard errors, using different samples, and addressing the potential endogenous

concerns. Our further investigation indicates that a better credit allocation enhances

TFP more for firms which are less subsidized, smaller, more external financially

dependent, and more labor intensive.

Compared with the previous studies, our contributions are as follows: firstly,

unlike many studies which have documented that the size of financial market plays an

important role in TFP enhancement (Benhabib & Spiegel, 2000; Jeong & Townsend,

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

7

2007), we find that in a country under financial imperfection, credit allocation is more

important than the size of credit market in promoting firms’ TFP. This finding

especially has implications for the development of many emerging economies in

which credit resources are limited. Our results indicate that a better credit allocation

may narrow the difference of emerging economies’ aggregate TFP with that of

developed countries.

Secondly, unlike much empirical research which investigates how finance affects

aggregate TFP (Guillaumont-Jeanneney et al., 2006; Jeong & Townsend, 2007;

Guariglia & Poncet, 2008; Han & Shen, 2015), we exam how credit allocation

impacts firms’ TFP. To the best of our knowledge, the association between firm-level

TFP and credit allocation has never been tested directly before. As we have argued

previously, firms’ activities and then their productivity would be affected by the credit

allocation in their regions. 5 Further, by analyzing firm-level TFP rather than

province-level TFP, we can understand the micro-foundation on how credit allocation

affects TFP through investigating the firm and industry heterogeneous effects.

Firm-level data also allows us to control many observed and unobserved variables and

reduce the endogeneity problem. In general, these cannot be done by using aggregate

TFP (province-level TFP).

Finally, our paper also has important policy implications for China which is going

through the economic transformation. Recently, China is struggling to upgrade its

supply quality since the labor costs are increasing. One primary way to upgrade 5 Please see the third paragraph for the detail.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

8

supply quality is improving firms’ productivity or efficiency (Foster et al., 2008;

Roberts et al., 2012). Therefore our findings indicate that one of the important efforts

of upgrading supply quality could be made through improving the efficiency of credit

allocation.

Our paper is closely related to the papers examining how finance affects

firm-level TFP. Krishnan et al. (2015) study whether and how the access to banking

credit in the state-level influences small firms’ TFP by exploiting a natural experiment

following interstate banking deregulations in the United States. They find that small

firms’ TFP increases after their states implement these deregulations. In addition,

Nucci et al. (2005) and Gatti and Love (2008) find significant impacts of firms’

capital structure and access to credit on their TFP for Italy and Bulgaria, respectively.

Chen and Guariglia (2013) who argue that increase of firms’ cash flow promotes firms’

productivity. Different from these papers, we examine how the credit allocation

impacts Chinese firms’ TFP.

The rest of this paper is organized as follows. Section 2 briefly reviews the

evolution of credit allocation in China. Section 3 demonstrates the methodology and

describes the data. Section 4 presents our main empirical findings and robustness

check. Section 5 discusses the heterogeneous effects of credit allocation on firm TFP.

Section 6 concludes.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

9

2. Evolution of credit allocation in China

After several years of China’s Reform and Openness, the financial system is

gradually becoming more developed in order to adapt to the rapid changes in China’s

real economy. One reflection is on the credit allocation, which is becoming more

efficient and effective.

As we know, China’s financial system originates from a mono-bank system in

which the People's Bank of China (PBOC) controlled all banking credit and only

allocated them to SOEs (Chen, 2006). After China’s Reform and Openness in 1978,

the components of China’s economy became diversified, especially due to the rapid

development of non-SOEs. Thus the financial system was forced to adapt to the

development of China’s real economy. The financial system is growing rapidly and

plays a more important role in resource allocation.

Since the late 1980s, various types of financial institutions have been established,

as a result the credit has been extended to more diversified customers. In 1997, the

central government first formally allowed banks to extend loans to the private sector

(Firth et al., 2009), and a bit more credit has been allocated to non-SOEs after that

(Lin, 2011). However, the four state-owned banks which dominate China’s

commercial banking system continue to lend to SOEs only (Guariglia & Poncet,

2008). As a result of that, the more efficient and dynamic non-state sector still has

extremely limited access to banking credit. It is because the central and local

governments issued lending quotas to SOEs which submitted investment plans, while

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

10

the non-SOEs were excluded from those submitting investment plans. This

discrimination against the non-SOEs is from the asymmetric information problems

due to their short credit history (Stein, 2002) and low chances of being bailed out by

the governments (Brandt & Li, 2003).

In 1998, the PBOC reformed the commercial banks’ lending behavior, abolishing

the loan size restrictions on the four state-owned commercial banks. The PBOC’s

regulations of commercial banks also changed from mandatory plans to guiding plans,

and the PBOC required all commercial banks to rank their loans into five categories

according to loan risk from 1998 to 2000. After China’s entry into the World Trade

Organization (WTO) in 2001, the financial system further went through several

reforms, including attracting foreign strategic investors, going public, and

reconstructing themselves. The financial institutions thus became more efficient and

the credit allocation started to become more commercialized. For example, based on

the World Bank survey data from 2002, Firth et al. (2009) show that the state-owned

banks allocating credit to non-state-owned sectors tend to use commercial judgments.

Those reforms by the PBOC also helped China’s financial institutions to avoid severe

impacts from the 2007–2009 global financial crisis.

Recently, the central government has also announced a series of measures to

promote the availability of banking credit to small and medium enterprises (SMEs)

and most of them are non-SOEs. Under the series reforms on financial system, even

though the proportion of lending to non-SOEs has been increased gradually, the

non-SOEs are still financially constrained (Poncet et al., 2010) and the financial

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

11

system is urged to be further improved.

3. Methodology

3.1. Empirical model

As discussed in our Introduction, we identify the effects of credit allocation on

firm TFP using the fixed effects (FE) model by controlling for firm fixed effects. In

addition, to tackle any possible heteroskedasticity and serial correlation problems, we

cluster the standard errors at the industry-province level. Our baseline model is given

by: =∝ + , + ( ), + + + (1) where denotes TFP of firm locating in province in year . In our baseline estimation, besides credit allocation, we also examine how the size of credit

market influences firm TFP as a comparison. Therefore, , represents the financial depth which is a commonly used indicator for the size of credit market, or

credit allocation of province in year − 1. ( ), is a vector of variables including firm, industry, and province characteristics. and are time fixed

effects and firm fixed effects, respectively. is the error term. TFP measurement. In the production function, the residual in the total output

which cannot be explained by the total input is often referred to as TFP. Hence, an

increase in firm TFP represents the technology progress and efficiency improvement

in using resources for a firm. There are mainly three methods to estimate TFP. An

earlier one is the OLS method. However, the OLS estimation approach does not tackle

endogenous problems, such as simultaneity bias and self-selection bias, providing less

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

12

accurate results. The other one is the Olley and Pakes (1996) method, in which a

non-parametrically inverted investment equation is used to instrument productivity

shocks in the production function. This approach does alleviate the simultaneity and

sample selection bias by controlling for firms’ entry and exit. However, the

investment information is often unavailable in most databases. Even though this

information is available, not every firm invests in each year, thus there are many zero

values of the investment variable. To tackle this problem, Levinsohn and Petrin (2003)

develop another method in which intermediates rather than investments are adopted as

the proxy of unobserved productivity shocks. The Levinsohn and Petrin (2003)

method is more feasible than the Olley and Pakes (1996) method, since the

information of intermediates is easier to access than that of investments.

In the present paper, the firm-level investments cannot be observed directly from

our dataset either. Although this variable can be constructed from the capital stock

information (Brandt et al., 2012), lots of missing and non-positive values are

generated, which would make the estimated firm TFP to be untrustworthy. More

importantly, using the computed investments to estimate firm TFP also increases the

measurement errors of estimated TFP. To address those concerns and make our results

more trustworthy, we adopt the Levinsohn and Petrin (2003) method to estimate TFP

for each firm.6 The details of the estimation approach can be found in Levinsohn and

Petrin (2003). It is worthy noting that we estimate firm TFP by allowing each industry

to have a different production function, since there is a large heterogeneity across 6 We use the Levinsohn and Petrin (2003) method to estimate TFP for each firm with revenue, employment, fixed assets, and intermediate inputs.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

13

industries.

Financial depth and credit allocation. Credit market plays a very important role in

supporting non-listed manufacturing firms in China since they mostly rely on credit to

finance their operation. Following the literature, we use the ratio of total credit to

GDP for 31 Chinese provinces to measure local financial depth: Financialdepth = (2) where the variable, “Financial depth”, represents the size of the credit market in

province in year .

We use an index constructed from the ratio of credit allocated to non-SOEs to total

credit for 31 provinces as a proxy for credit allocation. This indicator represents the

allocation of credit between SOEs and non-SOEs. Since non-SOEs in China are in

general more efficient and more credit constrained than SOEs, the increase of this

indicator indicates a better allocation of credit. This is consistent with King and

Levine’s (1993) argument that a financial system which allocates more financial

resources to the private sector is more active in researching firms and managing risks

than that only allocating financial resources to the public sector.

The credit allocation indicator is constructed by Fan et al. (2011), sponsored by the

National Economic Research Institute of China and the China Reform Foundation. It

is a sub-index of the National Economic Research Institute (NERI) index.7 The

original data are from China Banking Yearbooks constructed by China Banking

7 The NERI index describes many aspects of the Chinese economy, including the government, banking market, legal environment, economic structure and trade barrier. Please refer to www.cerdi. org/uploads/sfCmsContent/html/192/Fangang.pdf for description of the data in English.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

14

Association, statistical yearbooks of various provinces, related statistical data on

banking and finance, and surveys on banking and finance on each province. This

measure has been used in many papers (i.e., Qian & Yeung, 2015; Qian et al., 2015).

The index is constructed by the following method. The base year of the index is

2001. The largest value for the base year is 10 and the lowest is 0. In 2001, the score

for each province can be written as:

= × 10 (3) where is the ratio of credit allocated to non-SOEs to total credit of province p.

and are the smallest and the largest among the 31 provinces,

respectively. For other years except 2001, the score for each province is calculated as: ( ) = ( ) ( )( ) ( ) × 10 (4) where (t) represents the index year, (0) represents the base year 2001. Based on

equations (3) and (4), we can obtain the credit allocation index for each province

during our sample period. And the largest value of the credit allocation index can be

above 10.

Other controls. Besides controlling for the time invariant variables, such as firm

fixed effects , we also control for many time-variant variables at firm, industry, and

province level in order to mitigate omitted variable bias. To capture the difference

between SOEs and non-SOEs, we control a dummy variable for SOEs and treat

non-SOEs as the base group. Similarly, we introduce a dummy variable for exporters

to control the influence of exporting behavior on firm TFP. Since employment and

subsidy revenue may affect firms’ real activities, we also control for employment and

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

15

subsidy ratio in our estimations. In addition, firm TFP may be influenced by the

market structure faced by firms, thus we control for the Herfindahl-Hirschman Index

(HHI) calculated by summing up the square of each firm’s market share at the annual

2-digit industry level. A higher HHI means higher concentration in the industry. We

also control for many variables representing provincial characteristics, including GDP

per capita, human capital and the stock of foreign direct investment (FDI), to isolate

the impact of macro environment on firm TFP. Table 1 lists the definition of main

variables used in this paper.

3.2. Data source

Our empirical analysis mainly relies on the data including information on the

firm-level characteristics, and province-level credit which has been mentioned in

Section 3.1. The firm-level variables are obtained from Annual Survey of Industrial

Firms (ASIF). Since the data of credit allocation of each province is only available

from 1999, and the data of ASIF during 1998-2007 is widely used in the previous

studies due to its stability and accuracy (Brandt et al., 2012; Liu & Qiu, 2016),

therefore in the present paper we set the sample period from 1999 to 2007. The ASIF

is collected by National Bureau of Statistics of China (NBSC), which covers the

annual production information of all SOEs and non-SOEs with sales revenue above 5

million RMB (about USD 650,000). Most firms included in this dataset are non-listed

firms. We use the approach of Brandt et al. (2012) to construct the panel. In this paper,

the industry is identified by the CIC (China Industry Classification) 2-digit industry

code. Since Ouyang et al. (2015) point out that if a firm switches from one industry to

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

16

another or changes its location, its other characteristics may also change. Therefore,

we delete the firms which have changed their industry based on the 2-digit industry

code or have changed provinces during our sample period. Moreover, we delete firms

whose sales revenue are below 5 million RMB, which have fewer than 8 employees,

or which have non-positive total assets in order to mitigate measurement errors. And

then we match the firm-level data with the province-level data. 8 Finally, our

unbalanced panel includes 240,702 firms, which corresponds to 990,387 firm-year

observations, spanning 29 industries and 31 provinces. In addition, we depreciate all

pecuniary variables with 2-digit price deflators constructed by Brandt et al. (2012) in

order to control for the price fluctuation.9 The descriptive statistics of our main

variables are presented in Table 2.

As shown in Table 2, there is a large variation of TFP across firms, implying the

apparent heterogeneity for firms in productivity. There is also a substantial variation

in credit allocation across provinces with standard deviation of 3.16. Moreover, in our

sample, SOEs only account for 10% of the firms, and 29% of firms are exporters.

8 The province-level credit allocation is constructed by Fan et al. (2011), and the province-level financial depth

and control variables are from the China statistical yearbooks in each year. 9 For example, we construct the real capital stock by adopting the approach developed by Brandt et al. (2012), which is used to estimate firm TFP.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

17

4. Results

4.1. The impact of financial depth on firm TFP

Before we investigate the effects of credit allocation on firm TFP, we first check

whether financial depth influences firm TFP based on equation (1). As mentioned

above, we adopt the fixed effects (FE) model that controlling for firm fixed effects to

estimate equation (1). It is worthy noticing that as the firm’s location (by province)

and industry do not change during the sample period, firm fixed effects can also

capture the industry and province fixed effects. The results are reported in Table 3.

In column (1) of Table 3, we test the causal effects of financial depth on firm TFP

without other controls. The coefficient on financial depth is negative and significant at

the 10% level, showing that the increase in size of credit market impedes the

improvement of firm TFP. After introducing micro and macro controls successively in

columns (2) and (3), the coefficients on financial depth turn insignificant, indicating

that, on average, financial depth has no impact on firm TFP. This finding is consistent

with some previous macro-level studies which find that financial depth or the high

level of banking credit in China does not cause a higher growth (i.e., Liang & Teng,

2006).

Why does financial depth not promote the firm TFP? One possibility is that even

though China’s financial system has some improvement during our sample period, the

financial imperfection or the misallocation of financial resources in China is far from

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

18

being eliminated yet. Therefore, it is unlikely for the size of credit market to exert

positive effects on firm TFP yet.

4.2. The impact of credit allocation on firm TFP

We have confirmed that the size of credit market has no contribution to firm TFP

enhancement. How about allocating more credit to the non-SOEs? Fig.2 shows that

credit allocation and firm TFP have a similar increasing trend over time. Therefore we

wonder if allocating more credit to non-SOEs could help to enhance Chinese firms’

TFP. In this subsection, we carry out an investigation based on equation (1) with the

firm-level data.

The regression results regarding the impact of credit allocation on firm TFP are

reported in Table 4. In the first three columns, the coefficients on credit allocation are

positive and significant, showing that on average, the ratio of credit to non-SOEs over

total credit is positively associated with firm TFP. In particular, our results indicates

that when the credit allocation index increases by one standard deviation, the TFP of a

firm increases by 0.9796%.10 Since the average credit allocation in each province

arises about 0.7 every year and the average of a Chinese firm’ TFP increases about

0.04 each year, our results also show that credit allocation contributes 5.425% to the

rise of Chinese firms’ TFP on average during our sample period.11

However, during 1999-2008, many Chinese SOEs are transformed into non-SOEs.

Therefore, one may wonder whether the reduction of the number of SOEs may

contaminate our results. To address this concern, we further introduce non-SOE ratio 10 It is calculated as 3.16*0.0031*100%. 11 This is calculated as 0.0031*0.7/0.04*100%.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

19

measured by the ratio of non-SOEs to total number of firms in a province in column

(4). As shown in column (4), the coefficient of the non-SOE ratio is not significant.

More importantly, the coefficient of credit allocation is similar to that in column (3),

suggesting that the transformation of SOEs in China does not exert significant impact

on our main results.

Table 4 also shows that the coefficients on SOEs in columns (2)-(4) are negative

and significant at the 1% level, again confirming that SOEs perform worse compared

with non-SOEs, on average. Moreover, exporters are more productive than

non-exporters, which is in line with Melitz (2003) that only the more productive

producers can enter into the foreign markets. In addition, firms obtaining more

subsidy from government or having more employees increase their productivity more

than others. For macro controls, firms are more productive in more concentrated

industries. It is because the productivity may be driven by reallocating resources to

more efficient firms through firm turnover or the increase of incumbents’ productivity

in the whole industry. Finally, the human capital and foreign investment of a province

also help to promote firms’ TFP.

In sum, we find that finance depth cannot promote firm TFP, while allocating

more credit to non-SOEs does enhance firm TFP significantly. It indicates that a better

credit allocation rather than just increasing the size of credit market is an important

way to enhance Chinese firms’ TFP.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

20

4.3. Robustness check

In this section, we will test whether our main results are robust to the specification

of clustering standard errors, different samples, and the potential endogenous

problems.

4.3.1. Cluster standard errors at industry and province level, respectively

In our main analysis we cluster the standard errors at industry-province level,

since the local governments have much discretion in enforcing the industry policy

according to their localities which may generate the substantial variations across

provinces within an industry. Nonetheless, as a robustness check, we recalculate the

standard errors by clustering at industry and province level, respectively, in Table 5.

As shown in Table 5, no matter clustering standard errors at industry or province level,

the significance of financial depth and credit allocation have no essential changes

compared to our previous estimations. This suggests that our findings are robust to the

different specification of clustered standard errors.

4.3.2. Different subsamples

4.3.2.1. The sample without SOEs

Since credit allocation represents the credit allocated to non-SOEs relative to total

credit, non-SOEs are expected to benefit. In our main analysis we utilize the full

sample, including SOEs and non-SOEs, to examine the role of credit allocation on

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

21

firm TFP, which may underestimate the positive effects of credit allocation. To check

this, we re-estimate the relationship between credit allocation and firm TFP by

including non-SOEs only. To be consistent with our previous analysis, in this

sub-section we also re-test the association between financial depth and firm TFP

without SOEs, and to check whether the size of credit market indeed has non-positive

effects on non-SOEs. The results are presented in columns (1) and (2) in Table 6.

Our results show that although the magnitudes of the coefficients (in absolute value)

on the key independent variables become mildly large compared with their

counterparts in Table 3 and Table 4, we continue to find an insignificant impact of

financial depth on firm TFP and a positive and significant effect of credit allocation

on firm TFP.

4.3.2.2. The sample after China’s entry into WTO

As we mentioned in Section 2, after China’s entry into WTO in 2001, the financial

system went through several reforms. Therefore one may wonder whether our earlier

results still hold after this big event. To check this, we only keep the sample after

China’s entry into WTO, and the results are reported in columns (3)-(4) in Table 6. As

shown in these two columns in Table 6, the coefficient on credit allocation becomes

larger. This suggests that after China’s entry into WTO, credit allocation plays a more

important role in firms’ performance improvement.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

22

4.3.2.3. The sample of firms without id change

In our sample, some firms’ id codes change over time. As argued by Brandt et al.

(2012), these changes are often due to restructuring. Since these unusual activities

tend to affect firms’ productivity, one may concern whether our results are driven by

firms’ restructuring. To tackle this problem, we delete the firms with id changes over

our sample period. The results are demonstrated in columns (5) and (6) in Table 6. As

shown in the last two columns of Table 6, the results are consistent with our previous

findings.

4.3.3. Further discussion of the potential endogenous problems

4.3.3.1. IV method

In this subsection, we use the IV method to address the potential endogeneity

problem and further check the robustness of our results. Specifically, we find an IV

for our key explanatory variables to re-estimate model (1). As the increasing

economic intgration in China’s economy, financial sector in each province becomes

closely connected to each other. Thus, financial sector in one location is inevitably

affected by the changes of financial sectors in other locations and it is normally

affected by large economies more. Meanwhile, the behavior of financial sectors in

other locations is not likely to be correlated with unobserved factors which affect the

TFP of local firms. This is because bank branches in China are discouraged from

lending to firms in other provinces to minimize overlapping competition (Qian &

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

23

Yeung, 2015). Therefore, we adopt the GDP-weighted average of size of credit market

of other provinces as the instrument variable (IV) for financial depth. The same

approach is used to construct the IV for credit allocation. Afterwards, we adopt the

extended 2-stage-least-squares (2SLS) method to re-estimate equation (1). The results

are reported in columns (1)-(2) in Table 7.

In each column of columns (1) and (2) in Table 7, the F-test of excluded

instruments in the first-stage has a value substantially higher than the critical value 10

suggested by Staiger and Stock (1997) for the strong instruments, indicating that our

proposed instrument is both relevant and strong. The results show that the magnitudes

of coefficients (in absolute value) on financial depth and credit allocation are

moderately lager than our previous results. However, their significance doesn’t

change, suggesting our main findings are quite robust.

Geographically, the mainland China is divided into 7 regions. 12 Due to

geographical vicinity, the financial environment of the provinces in the same region

may be much more similar to each other than that of the provinces in other regions.

As we have argued before, the behavior of financial sectors in other locations is not

likely to be correlated with unobserved factors which affect the TFP of local firms.13

Therefore, the GDP-weighted average of credit allocation (size of credit market) of

other provinces in the same regions is also a potential instrument for credit allocation

(financial depth). The values of F-test of excluding the instrument are 34.72 for credit

12 The 7 regions are east China, central China, north China, south China, east and north China, west and south China, and west and north China. 13 Please see the first paragraph in Section 4.3.3.1 for the detail.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

24

allocation and 119.03 for financial depth, indicating that these instruments are

statistically valid. The results are presented in columns (3)-(4) in Table 7. Our results

continue to robust.

4.3.3.2. GMM method

Although the endogeneity problem of our key explanatory variables (financial

depth and credit allocation) is not a big issue, one may concern the endogeneity of our

control variables, especially the firm-level controls. For instance, some firm-level

variables (e.g. employment and export behavior) are likely to be highly persistent,

thus the one-year lagged controls may be endogenous. Since it is difficult to find the

external instruments for those controls, one possible way to tackle this concern is

adopting the Generalized Method of Moments (GMM) estimation method with their

2-year lagged values as instruments. To make our estimation more consistent, we also

use the 2-year lagged values of financial depth and credit allocation as instruments for

our key explanatory variables respectively. The regressions estimated by the two-step

efficient GMM method are listed in columns (1)-(2) in Table 8.

As explained above, the F-test of excluded instruments in the first-stage shows that

our proposed instruments are both relevant and strong. And we still find that firm TFP

does not response to financial depth but it is positively influenced by credit allocation.

Those results imply that the potential endogenous problems do not drive our main

findings and if it does, it causes a bias on our estimation downwards at the most since

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

25

the magnitudes of coefficients become larger.

4.3.3.3. Industry-year fixed effects

In our baseline estimations, we tackle the endogenous problems mainly by

controlling for many firm-, industry- and province-level observed time-variant and

unobserved time-invariant factors. In order to further check the robustness of our

results, we include the industry and year fixed effect which captures the time-variant

characteristics of each industry.14 The results are presented in columns (3)-(4) in

Table 8, which are consistent with our earlier results.

5. Heterogonous effects

Since firms are different in individual characteristics as well as industrial

characteristics, the positive impacts of credit allocation on firm TFP may vary across

firms and industries. For instance, firms more dependent on external finance are

largely affected by credit market development (Cetorelli & Gambera, 2001; Hsu et al.,

2014). It is because credit market development may increase firms’ access to external

finance and reduce their financing costs. Due to the availability of firm-level data, we

can further explore the heterogeneous impacts by introducing the interactions between

credit allocation and the measures of firm as well as industry heterogeneity. The

analysis of heterogeneous impacts helps to show the micro-economic foundations

through which credit allocation generates positive effects on average firm TFP. Next

we will examine whether subsidy to firms, firm size, external financial dependence of

14 Here, we cannot include province and year fixed effect in our estimation, since our key explanatory variables are by province and year.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

26

industries, and labor intensity of industries matter for the relationship between credit

allocation and firm TFP.

5.1. Subsidy

The existing studies have provided evidences that subsidy from governments

plays an important role in firm performance. For example, Hyytinen and Toivanen

(2005) document that the subsidy from government helps firms raising capital from

external sources at lower costs, and thus it disproportionately benefits firms in

industries more dependent on external finance. Bronzini and Piselli (2016) also find

that R&D subsidy program implemented in a region of northern Italy in the early

2000s had a significant impact on firm innovation. Therefore, it is reasonable to

expect that firms obtaining more subsidy from government would be less sensitive to

credit allocation, since the subsidy revenue mitigates their dependence on other

sources of external finance for engaging in TFP-improving activities, such as R&D.

To check this, we introduce an interaction between credit allocation and the firm-level

subsidy from government measured by subsidy ratio to our baseline estimation, and

present the result in column (1) in Table 9.

As shown in column (1) in Table 9, the coefficient on interaction is negative and

significant at the 1% level, suggesting that credit allocation has a smaller impact on

firms with more subsidies, which is consistent with our expectation. This finding

indicates that credit allocation is mainly through improving the productivity of firms

with less government financial support to promote the average TFP of Chinese firms.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

27

5.2. Size

It is widely known that small firms are more financially constrained due to their

more limited access to the credit market (Beck et al., 2005). However, small firms

play an important role in driving China’s rapid economic growth in recent years(Lin

et al., 2015). Therefore, improving TFP of small firms would contribute more on

upgrading the supply quality of total manufacturing and retaining the rapid growth of

China’s economy. Since the majority of small firms are non-SOEs, we expect that the

increase of credit to non-SOEs or credit allocation may disproportionately benefit

those small firms more than the large firms. To see this, we adopt the classification of

firm size from ASIF, which divides firms into three groups: small, medium-sized, and

large firms, according to their sales revenue. In our sample, more than 78% of firms

are small firms, and about 15% of firms are medium-sized firms, while only about 7%

of firms are large firms. We introduce two interactions in our baseline regression: one

is the interaction between credit allocation and a dummy for small firms; the other is

the interaction between credit allocation and a dummy for large firms. The result is

reported in column (2) in Table 9.

In the second column of Table 9, the coefficient on the interaction between credit

allocation and the dummy for small firms is significantly positive, while that on the

interaction between credit allocation and the dummy for large firms is significantly

negative. This result suggests that credit allocation promotes TFP of small firms more

but large firms less, which is in line with our expectation. Our finding implies that

allocating more credit to non-SOEs mainly relaxes the financial constraints of small

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

28

firms which help to increase their TFP, resulting in the enhancement of the average

TFP of Chinese firms.

5.3. External financial dependence

Firms heavily dependent on external finance are supposed to respond more to the

increase of external financial resources, since they have more access to external

finance with low costs, especially for non-SOEs which are hard to get support from

the credit market. Therefore, we further check whether credit allocation impacts more

on firms which heavily depend on external finance.

Here, we adopt the leverage ratio, measured by the total debts to total assets, as a

proxy of external financial dependence. Berman and Héricourt (2010) argue that the

leverage ratio can be interpreted as both a measure of the firms’ lack of collateral and

of the firms’ current demand for borrowing relative to its capacity to borrow. It is

worth noting that unlike in previous subsections, here we cannot directly introduce an

interaction between firm-level leverage ratio and credit allocation to test the

hypothesis due to the potential endogenous concern. For example, managers facing

poor growth opportunities choose high levels of leverage or increases in firms’

leverage may also reflect a response to unobserved variation in investment

opportunities (Desai et al., 2008). To tackle this issue, we construct a measure of

external financial dependence from the leverage ratio at 2-digit industry level

(Manova, 2013). Specifically, we first compute the leverage ratio for each industry.15

15 The measure is averaged over 1999-2007 for the median firm in each industry (Manova, 2013).

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

29

If an industry has leverage ratio above (or below) median level, it is classified as a

high (or low) external financial dependence industry. Firms in an industry with high

external financial dependence are more likely to heavily depend on external finance.

Then we construct a dummy variable for firms in the high financial dependence

industry,16 and introduce an interaction between credit allocation and this dummy in

column (3) in Table 9.

The result in column (3) lends strong support to our prediction that firms in the

industry with high external financial dependence are more affected by credit

allocation. This finding is consistent with the existing studies (Cetorelli & Gambera,

2001; Hsu et al., 2014).

5.4. Labor intensity

Song et al. (2011) develop a model showing that financially constrained firms

with high TFP will specialize in labor-intensive activities. They further show that in

China, where young high-productivity non-SOEs have entered extensively into

labor-intensive sector, while old SOEs continue to dominate capital-intensive sector.

From this perspective, if allocating more credit to non-SOEs, firms in labor-intensive

sector may have more access to financial resources, since more than 90% of

non-SOEs in our sample is in labor-intensive sector. Hence, we expect that firms in

labor-intensive sector respond more to credit allocation than those in capital-intensive

sector.

16 The dummy is equal one if the firm is in an industry with leverage ratio above median level, zero otherwise.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

30

To see this, we divide firms into two types: firms in labor-intensive industries and

those in capital intensive industries. Specifically, we compute the labor-capital ratio

for each industry over 1999-2007,17 if the labor-capital ratio of an industry is above

median level, it is classified as a labor-intensive industry, as a capital-intensive

industry otherwise. Next, we construct a dummy variable for firms in the

labor-intensive industry and introduce the interaction between credit allocation and

this dummy in our baseline estimation.18 The result is reported in column (4) in Table

9.

As shown in the last column of Table 9, the coefficient on the interaction is

positive and significant at 1% level, suggesting that firms in labor-intensive industries

are more sensitive to credit allocation. This finding is in line with Lin et al. (2015)

who argue that labor-intensive industries grow faster than capital-intensive industries

in provinces with more active small banking institutions.

6. Conclusion

In this paper, we have investigated the role of size of credit market and credit

allocation in firm TFP enhancement using firm-level panel data from Chinese

manufacturing firms. Our results show that financial depth or the size of credit market

has no significant effects on firm TFP, while allocating more credit to non-SOEs

contributes to the enhancement of firm TFP. This finding indicates that the

misallocation of financial resources indeed generates productivity loss, and a better

17 The measure is averaged over 1999-2007 for the median firm in each industry. 18 Similar to the analysis of external financial dependence, we cannot introduce an interaction between firm-level labor-capital ratio and credit allocation to our regression directly due to the endogenous concern that financially constrained firms with high TFP will choose to engage in the labor-intensive activities (Song et al., 2011).

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

31

credit allocation is one primary way to improve firm performance. We further find

that credit allocation works differently across firms as well as industries. Specifically,

firms having less subsidy from governments, with small size, in industry with high

external financial dependence, and in industry with labor-intensity benefit more from

allocating more credit to non-SOEs.

Nowadays, upgrading the quality of supply has attracted much more attention in

China. Improving firm productivity is seen as an important approach to realize this

goal. Therefore, one most important policy implication of our work is that currently,

allocating more credit to the non-SOEs relative to SOEs can promote Chinese firms’

TFP which helps to improve the supply quality. This is because the Chinese non-SOEs

are more efficient but more financially constrained than SOEs. Credit to non-SOEs

works more efficiently than that to SOEs in enhancing firms’ TFP.

Our work also implies that for emerging economies to grow, one of the most

important things is to allocate credit to the more efficient but financially constrained

sector.

References:

Allen, F., Qian, J., and M. Qian. “Law, finance, and economic growth in China.”

Journal of Financial Economics, 2005, 77: 57-116.

Amore, M. D., Schneider, C., and A. Žaldokas. “Credit supply and corporate innovation.”

Journal of Financial Economics, 2013, 109: 835-855.

Bai, C. E., Lu, J., and Z. Tao. “The multitask theory of state enterprise reform:

Empirical evidence from China.” American Economic Review, 2006, 96:

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

32

353-357.

Benhabib, J., and M. M. Spiegel. “The role of financial development in growth and

investment.” Journal of Economic Growth, 2000, 5: 341-360.

Beck, T., Demirgüç-Kunt, A., and V. Maksimovic. “Financial and legal constraints to

growth: does firm size matter?.” The Journal of Finance, 2005, 60(1): 137-177.

Bronzini, R., and P. Piselli. “The impact of R&D subsidies on firm innovation.”

Research Policy, 2016, 45(2): 442-457.

Berman, N., and J. Héricourt. “Financial factors and the margins of trade: evidence

from cross-country firm-level data.” Journal of Development Economics, 2010,

93(2): 206-217.

Brandt, L., and H. B. Li. “Bank discrimination in transition economies: ideology,

information, or incentives?.” Journal of Comparative Economics, 2003, 31: 387–

413.

Brandt, L., Van Biesebroeck, J., and Y. Zhang. “Creative accounting or creative

destruction? firm-level productivity growth in Chinese manufacturing.” Journal

of Development Economics, 2012, 97(2): 339-351.

Buera, F., Kaboski, J.P., and Y. Shin. “Finance and development: a tale of two sectors.”

American Economic Review, 2009, 101:1964-2002.

Chen, H. “Development of financial intermediation and economic growth: the

Chinese experience.” China Economic Review, 2006, 17: 347–362.

Chen, M., and A. Guariglia. “Internal financial constraints and firm productivity in

China: do liquidity and export behavior make a difference?.” Journal of

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

33

Comparative Economics, 2013, 41(4): 1123-1140.

Cetorelli, N., and M. Gambera. “Banking market structure, financial dependence and

growth: International evidence from industry data.” The Journal of Finance,

2001, 56(2): 617-648.

Cull, R., Xu, L.C., and T. Zhu. “Formal finance and trade credit during China’s

transition.” Journal of Financial Intermediation, 2009, 18: 173-192.

Desai, M. A., Foley, C. F., and K. J. Forbes. “Financial constraints and growth:

Multinational and local firm responses to currency depreciations.” Review of

Financial Studies, 2008, 21(6): 2857-2888.

Erosa, A., and A. Hidalgo-Cabrillana. “On capital market imperfections as a source of

low TFP and economic rents.” Working paper, 2007.

Fan, G., Wang, X., and H. P. Zhu. “NERI index of marketization of China’s provinces.”

Economics Science Press, 2011, Beijing. (in Chinese).

Firth, M., Lin, C., and P. Liu., et al. “Inside the black box: Bank credit allocation in

China’s private sector.” Journal of Banking & Finance, 2009, 33: 1144-1155.

Foster, L., Haltiwanger, J., and C. Syverson. “Reallocation, firm turnover, and

efficiency: Selection on productivity or profitability.” American Economic

Review, 2008, Vol.98, No.1: 394-495.

Gatti, R., and I. Love. “Does access to credit improve productivity? Evidence from

bulgaria1.” Economics of Transition, 2008, 16(3): 445-465.

Guariglia, A., and S. Poncet. “Could financial distortions be no impediment to

economic growth after all? Evidence from China.” Journal of Comparative

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

34

Economics, 2008, 36: 633-657.

Guillaumont-Jeanneney, S., Hua, P., and Z. Liang. “Financial development, economic

efficiency, and productivity growth: Evidence from China.” The Developing

Economies, 2006, 44(1): 27-52.

Han, J., and Y. Shen. “Financial development and total factor productivity growth:

Evidence from China.” Emerging Markets Finance and Trade, 2015, 51(sup1):

S261-S274.

Hsieh, C. T., and P. J. Klenow. “Misallocation and manufacturing TFP in China and

India.” Quarterly Journal of Economics, 2009124 (4): 1403-48.

Hsu, P. H., Tian, X., and Y. Xu. “Financial development and innovation:

Cross-country evidence.” Journal of Financial Economics, 2014, 112(1):

116-135.

Hyytinen, A., and O. Toivanen. “Do financial constraints hold back innovation and

growth?: Evidence on the role of public policy.” Research Policy, 2005, 34(9):

1385-1403.

Jeong, H., and R. M. Townsend. “Sources of TFP growth: occupational choice and

financial deepening.” Economic Theory, 2007, 32(1): 179-221.

King, R.G., and R. Levine. “Finance and growth: Schumpeter might be right.” The

Quarterly Journal of Economics, 1993(a), 108: 717-737.

King, R.G., and R. Levine. “Finance, entrepreneurship and growth.” Journal of

Monetary Economics, 1993(b), 32 (3): 513-542.

Krishnan, K., Nandy, D. K., and M. Puri. “Does financing spur small business

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

35

productivity? Evidence from a natural experiment.” Review of Financial Studies,

2015, 28(6): 1768-1809.

Levinsohn, J., and A. Petrin. “Estimating production functions using inputs to control

for unobservables.” The Review of Economic Studies, 2003, 70(2): 317-341.

Liang, Q., and J. Z. Teng. “Financial development and economic growth: Evidence

from China.” China Economic Review, 2006, 17: 395–411.

Lin, H. D. “Foreign bank entry and firms’ access to bank credit: Evidence from China.”

Journal of Banking & Finance, 2011, 35: 1000–1010.

Lin, J. Y., Sun, X., and H. X. Wu. “Banking structure and industrial growth: Evidence

from China.” Journal of Banking & Finance, 2015, 58: 131-143.

Liu, Q., and L.D. Qiu. “Intermediate input imports and innovations: Evidence from

Chinese firms’ patent filings.” Journal of International Economics, 2016,

103:166-183.

Manova, K. “Credit constraints, heterogeneous firms, and international trade.” The

Review of Economic Studies, 2013, 80(2): 711-744.

Manova, K., Wei, S. J., and Z. Zhang. “Firm exports and multinational activity under

credit constraints.” Review of Economics and Statistics, 2015, 97(3): 574-588.

Melitz, M. J. “The impact of trade on intra-industry reallocations and aggregate

industry productivity.” Econometrica, 2003, 71(6): 1695-1725.

Nucci, F., Pozzolo, A., and F. Schivardi. “Is firm’s productivity related to its financial

structure? Evidence from microeconomic data.” Rivista di Politica Economica,

2005, 95(1): 269-290.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

36

Olley, G. S., and A. Pakes. “The dynamics of productivity in the telecommunications

equipment industry.” Econometrica, 1996, 64 (6):1263-1297.

Ouyang, P., Zhang, T., and Y. Dong. “Market potential, firm exports and profit: Which

market do the Chinese firms profit from?” China Economic Review, 2015, 34:

94-108.

Poncet, S., Steingress, W., and H.Vandenbussche. “Financial constraints in China: Fir

m-level evidence.” China Economic Review, 2010, 21: 411–422.

Qian, J., Strahan, P. E., and Z. Yang. “The impact of incentives and communication

costs on information production and use: Evidence from bank lending.” Journal

of Finance, 2015 70(4):1457–1493.

Qian, M., and B.Y. Yeung. “Bank financing and corporate governance.” Journal of

Corporate Finance, 2015, 32:258-270.

Rajan, R. G., and L. Zingales. “Financial dependence and growth.” The American

Economic Review, 1998, 88: 559–586.

Restuccia, D., and R. Rogerson. “Policy distortions and aggregate productivity with

heterogeneous establishments.” Review of Economic Dynamics, 2008,

11(4):707-720.

Roberts, M. J., Xu, D. Y., and X. Fan., et al. “A structural model of demand, cost, and

export market selection for Chinese footwear producers.” NBER working paper,

paper series, 2012: 17725.

Stein, J. “Information production and capital allocation: Decentralized versus

hierarchical firms.” Journal of Finance, 2002, 57: 1891-1921.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

37

Staiger, D., and J. H. Stock. “Instrumental variables regression with weak

instruments.” Econometrica, 1997, 65: 557-586.

Song, Z., Storesletten, K., and F. Zilibotti. “Growing like China.” The American

Economic Review, 2011,101(1): 196-233.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

38

Fig. 1. The average firm TFP of SOEs and non-SOEs from 1999 to 2007

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

39

Fig. 2. The average firm TFP and credit allocation from 1999 to 2007

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

40

Table1 Variable definition.

Variable Definition

Dependent variable:

Firm TFP estimated by the Levinsohn and Petrin (2003) method

Independent variables:

Financial depth (total credit/GDP) of each province

Credit allocation index constructed from (credit to non-SOEs/total credit) of each

Control variables:

SOE equals one if a firm is SOE, zero otherwise

Exporter equals one if a firm has exports in the current year, zero otherwise

Employment (log of the number of employees) of each firm

Subsidy ratio (subsidy revenue/total assets) of each firm

HHI (Herfindahl

-Hirschman Index)

= ∑ ( / ) , where denotes firm ’s sales in year , denotes the total sales of each industry in

GDP per capita (log of GDP per capita) of each province

Human capital (college or above graduates/ total population) of each province

FDI (the stock of foreign direct investment/GDP) of each province

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

41

Table 2 Descriptive statistics.

Variable Obs Mean St.dev Min Max

Dependent variable:

Firm TFP 990,387 4.86 2.96 0.13 17.41

Independent variables:

Financial depth 990,387 0.99 0.28 0.56 2.42

Credit allocation 990,387 8.22 3.16 0 14.03

Control variables:

SOE 990,387 0.1 0.3 0 1

Exporter 990,387 0.29 0.45 0 1

Employment 990,387 4.88 1.11 2.08 12.02

Subsidy ratio 990,387 0.002 0.1 0 0.08

HHI (Herfindahl-Hirschman Index) 990,387 0.003 0.004 0.0003 0.04

GDP per capita 990,387 9.59 0.57 7.84 10.87

Human capital 990,387 0.11 0.04 0.01 0.28

FDI 990,387 4.01 2.37 0.06 11.4

Note:Firm TFP is winsorized at the 1% level.

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

42

Table 3 The impact of financial depth on firm TFP.

Dependent variable Firm TFP

(1) (2) (3)

Financial depth -0.0636* -0.0041 -0.0108

(0.0359) (0.0193) (0.0181)

SOE -0.0350*** -0.0321***

(0.0047) (0.0045)

Exporter 0.0251*** 0.0246***

(0.0030) (0.0028)

Employment 0.0650*** 0.0665***

(0.0026) (0.0025)

Subsidy ratio 0.2890*** 0.2700***

(0.0479) (0.0497)

HHI 3.1310**

(1.4300)

GDP per capita 0.0732

(0.0583)

Human capital 0.6840***

(0.1240)

FDI 0.0024*

(0.0014)

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

43

Year fixed effects no yes yes

Firm fixed effects yes yes yes

Constant 4.9200*** 4.5080*** 3.7110***

(0.0357) (0.0278) (0.5570)

Observations 990,387 990,387 990,387

R-squared 0.0010 0.0560 0.0580

Note: As the firm’s location (by province) and industry do not change during the sample period, firm

fixed effects also capture the industry and province fixed effects. Robust standard errors are clustered at

industry-province level. Robust standard errors in parentheses, *** p

-

Acce

pted M

anus

cript

44

Table 4 The impact of credit allocation on firm TFP.

Dependent variable Firm TFP

(1) (2) (3) (4)

Credit allocation 0.0180*** 0.0020** 0.0031*** 0.0031***

(0.0014) (0.0009) (0.0008) (0.0008)

SOE -0.0352*** -0.0322*** -0.0321***

(0.0047) (0.0045) (0.0046)

Exporter 0.0249*** 0.0243*** 0.0243***

(0.0029) (0.0027) (0.0028)

Employment 0.0649*** 0.0664*** 0.0664***

(0.0026) (0.0025) (0.0025)

Subsidy ratio 0.2880*** 0.2670*** 0.2620***

(0.0476) (0.0492) (0.0495)

HHI 3.0780** 3.0840**

(1.4200) (1.4210)

GDP per capita 0.0688 0.0702

(0.0577) (0.0604)

Human capital 0.7260*** 0.7190***

(0.1270) (0.1280)

FDI 0.0028* 0.0028*

(0.0014) (0.0015)

Dow

nloa

ded

by [

Uni

vers

ity o

f Fl

orid

a] a

t 04:

56 1

1 Ja

nuar

y 20

18

-

Acce

pted M

anus

cript

45

Non-SOE ratio 0.0082

(0.0407)

Year fixed effects no yes yes yes

Firm fixed effects yes yes yes yes

Constant 4.7080*** 4.6110*** 3.7750*** 3.7550***

(0.0111) (0.0146) (0.5760) (0.6130)