CREDIBILITY FROM THE EYES OF THE CUSTOMER Michael Round Rational Systems August 11, 1999

CREDIBILITY FROM THE EYES OF THE CUSTOMER Michael Round Rational Systems August 11, 1999.

Dec 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CREDIBILITYFROM THE EYES OF THE CUSTOMER

Michael Round

Rational Systems

August 11, 1999

Rational Systems, formed by Michael Round in 1999, and located in Overland Park, Kansas, specializes in statistical and

actuarial improvement.

For a copy of “Credibility”, please e-mail me at: [email protected]

We are now accepting clients.

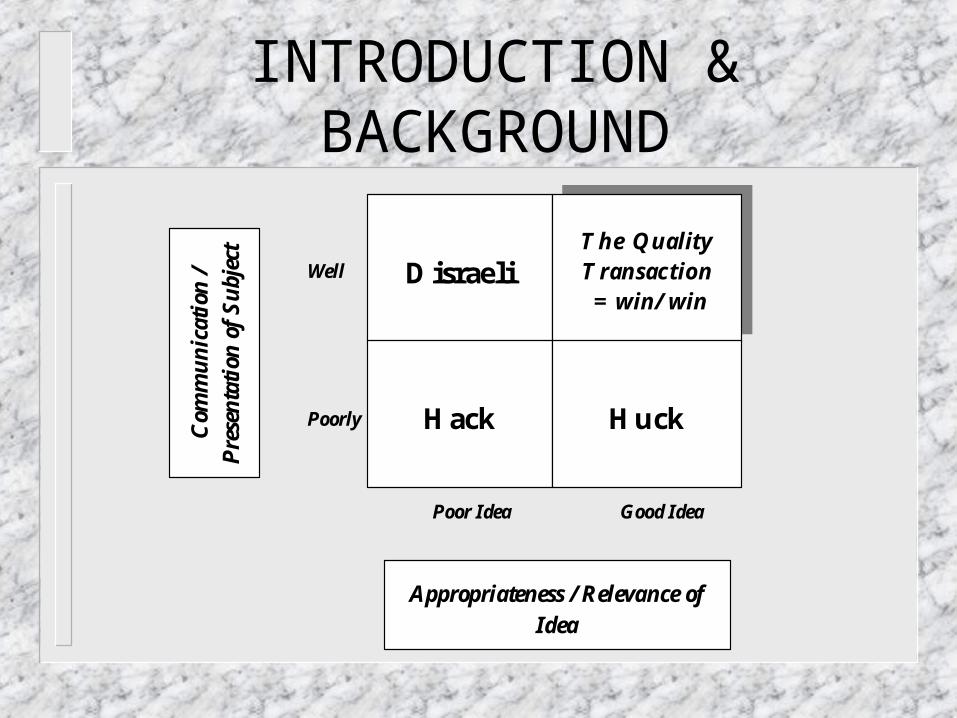

INTRODUCTION & BACKGROUND

BACKGROUND

DISRAELI vs. HUCKLEBERRY FINN

INTRODUCTION & BACKGROUND

Well

Poorly

Poor Idea Good Idea

DisraeliThe Quality Transaction = win/ win

Hack Huck

Com

mu

nic

atio

n /

Pre

sen

tati

on o

f S

ubj

ect

Appropriateness / Relevance of Idea

THE EXISTENCE OF A PROBLEM

CONTEXT: the renewal rating process, the pricing actuary, and the group representative / layperson - all addressing the impending anniversary date of the group.

THE ACTUARIAL POSITION

We want to have a reasonably priced insurance product.

The pricing actuary must take into account claims variability.

Credibility is used in the renewal rating process.

goal requirements prerequisite

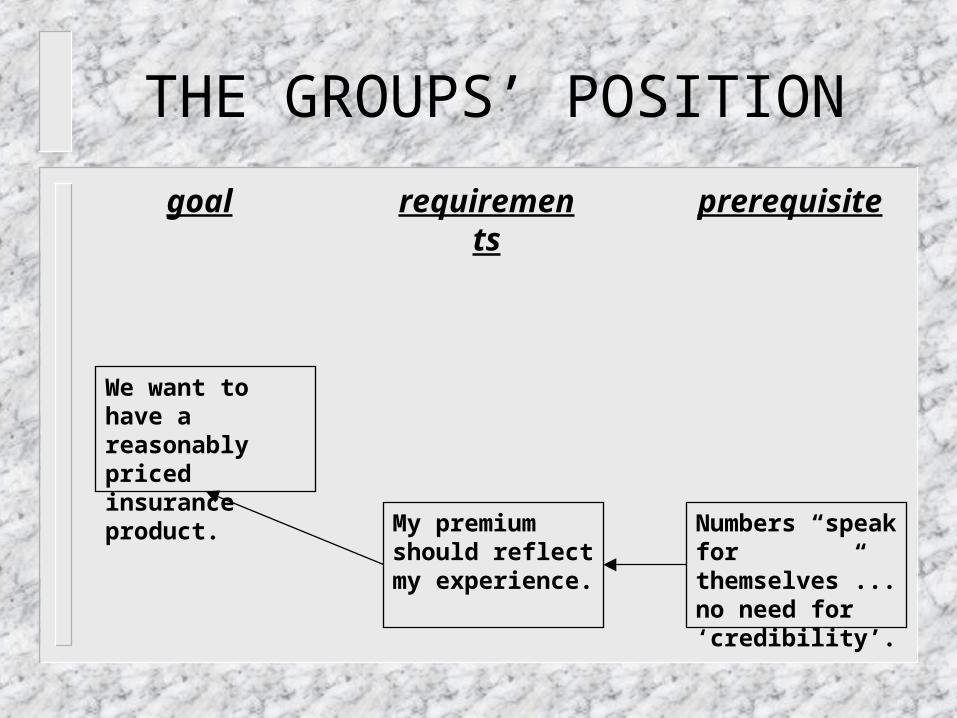

THE GROUPS’ POSITION

We want to have a reasonably priced insurance product.

My premium should reflect my experience.

Numbers “speak for themselves”... no need for ‘credibility’.

goal requirements prerequisite

THE CONFLICT

We want to have a reasonably priced insurance product.

My premium should reflect my experience.

Numbers “speak for themselves”... no need for ‘credibility’.

The pricing actuary must take into account claims variability.

Credibility is used in the renewal rating process.

goal requirements prerequisite

CONFLICT CONSEQUENCES

Numbers “speak for themselves”... no need for ‘credibility’.

Credibility is used in the renewal rating process.

My group has an empirically low loss ratio.

My expectation is a low renewal rate increase.

Credibility may adjust data to an “average renewal rate increase”.

UNDESIREABLE EFFECT

My expectation is a low renewal rate increase.

Credibility may adjust data to an “average renewal rate increase”.

Unhappy, angry, and confused, I go to the market for competing quotes.

THE ROOT CAUSE

At first glance, we might suggest the root cause of the conflict and the inevitable action of the group is:

FAILURE OF THE CLIENT TO UNDERSTAND THAT ADJUSTMENT OF DATA IS NECESSARY IN THE RENEWAL PROCESS . . . After all, the client has the perception:

THE DATA IS WHAT IT IS!!

However ...

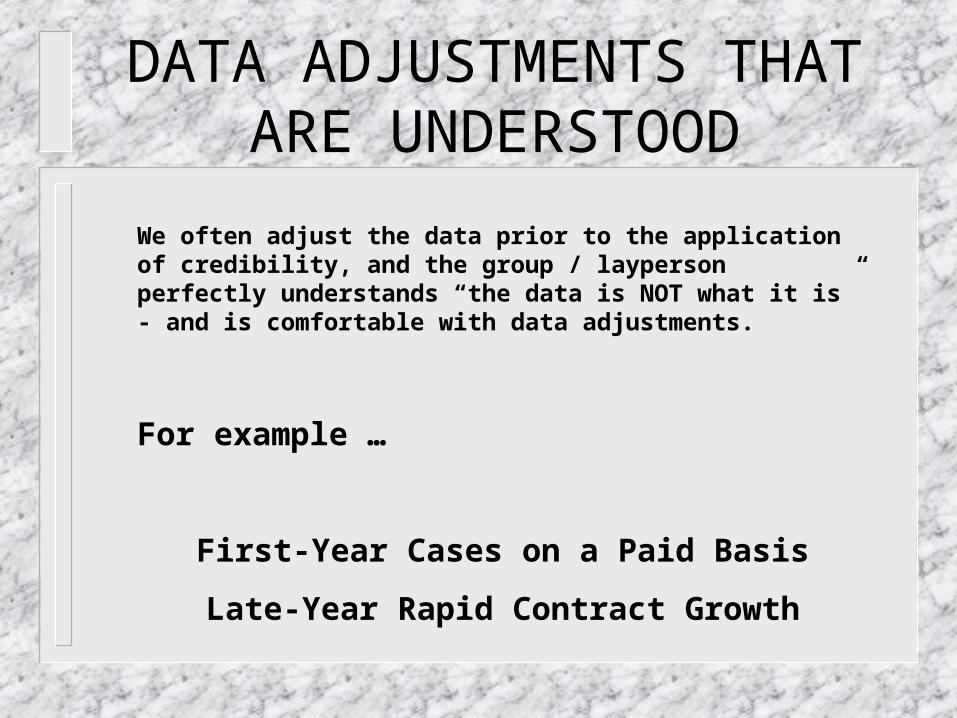

DATA ADJUSTMENTS THAT ARE UNDERSTOOD

We often adjust the data prior to the application of credibility, and the group / layperson perfectly understands “the data is NOT what it is” - and is comfortable with data adjustments.

For example …

First-Year Cases on a Paid Basis

Late-Year Rapid Contract Growth

DATA ADJUSTMENTS THAT ARE UNDERSTOOD

Empirical Data Apples-to-ApplesPaid Paid Paid Paid

Month Premium Claims Premium ClaimsJanuary $10,000 $0 $0 $0February $10,000 $0 $0 $0March $10,000 $0 $0 $0April $10,000 $7,143 $10,000 $7,143May $10,000 $10,000 $10,000 $10,000June $10,000 $14,286 $10,000 $14,286July $10,000 $5,714 $10,000 $5,714August $10,000 $2,857 $10,000 $2,857September $10,000 $3,571 $10,000 $3,571October $10,000 $5,143 $10,000 $5,143

Totals $100,000 $48,714 $70,000 $48,714

Loss Ratio 49% 70%

DATA ADJUSTMENTS THAT ARE UNDERSTOOD

Empirical Data Apples-to-ApplesPaid Paid Paid Paid

Month Contracts Premium Claims Premium ClaimsJanuary 100 $10,000 $7,143 $10,000 $7,143February 100 $10,000 $10,000 $10,000 $10,000March 100 $10,000 $14,286 $10,000 $14,286April 100 $10,000 $5,714 $10,000 $5,714May 100 $10,000 $2,857 $10,000 $2,857June 100 $10,000 $3,571 $10,000 $3,571July 100 $10,000 $5,143 $10,000 $5,143August 200 $20,000 $6,959 $10,000 $6,959September 200 $20,000 $6,933 $10,000 $6,933October 200 $20,000 $6,495 $10,000 $6,495

Totals $130,000 $69,101 $100,000 $69,101

Loss Ratio 53% 69%

THE ROOT PROBLEM

Credibility adjusts data in a numerical “black box”.

The group accepts “data adjustments” they can understand.

The group often does not understand the adjustment of their “good” data when adjusted via credibility.

INJECTION TO SOLVE THE PROBLEM

CREDIBILITY - and what gives rise to its need - ARE INTUITIVELY presented.

The group accepts “data adjustments” they can understand.

The group has an understanding of what has happened to their data - and may not be as dissatisfied with the perceived gap between the “expected” and “actual” renewal rate increase.

THE SOLUTION TO THE PROBLEM

CREDIBILITY seeks to quantify the variability, uncertainty, and predictability of a block of data.

To intuitively present this idea, we need to bridge the gap between our level of knowledge and that of the group representative / lay-person - OR PROVIDE A VISUAL MEANS OF AFFORDING THE LAY-PERSON THE INTUITIVE KNOWLEDGE OF WHAT VARIABILITY IS.

SIMULATION is an excellent mechanism for demonstrating variability and uncertainty at an intuitive level.

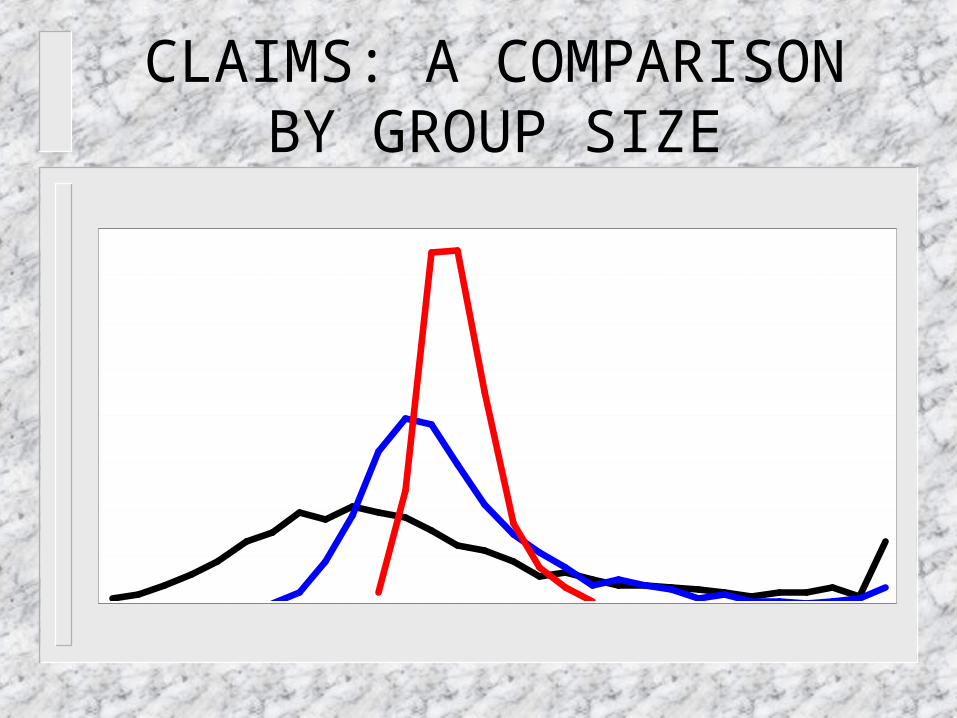

SIMULATING VARIABILITY

IF the essence of credibility is “degree of predictability”, THEN one method of communicating intuitively this concept is a simple simulation probability distribution for three different group sizes:

25 Members

250 Members

2500 Members

A ‘25-MEMBER’ GROUP ...

A ‘250-MEMBER’ GROUP ...

A ‘2500-MEMBER’ GROUP ...

CLAIMS: A COMPARISON BY GROUP SIZE

EXPLAINING CREDIBILITY

IF we have achieved our goal of visually demonstrating the meaning of “variability”, “uncertainty”, and “predictability” [all of which CREDIBILITY is addressing], THEN the group representative / lay-person has some feel why their data is being adjusted.

WHY NOT USE THE SAME SIMULATION PROCESS THAT EXPRESSES VARIABILITY VISUALLY TO TABULATE THE CREDIBILITY FACTORS WE NEED TO ACTUALLY ADJUST THE DATA?

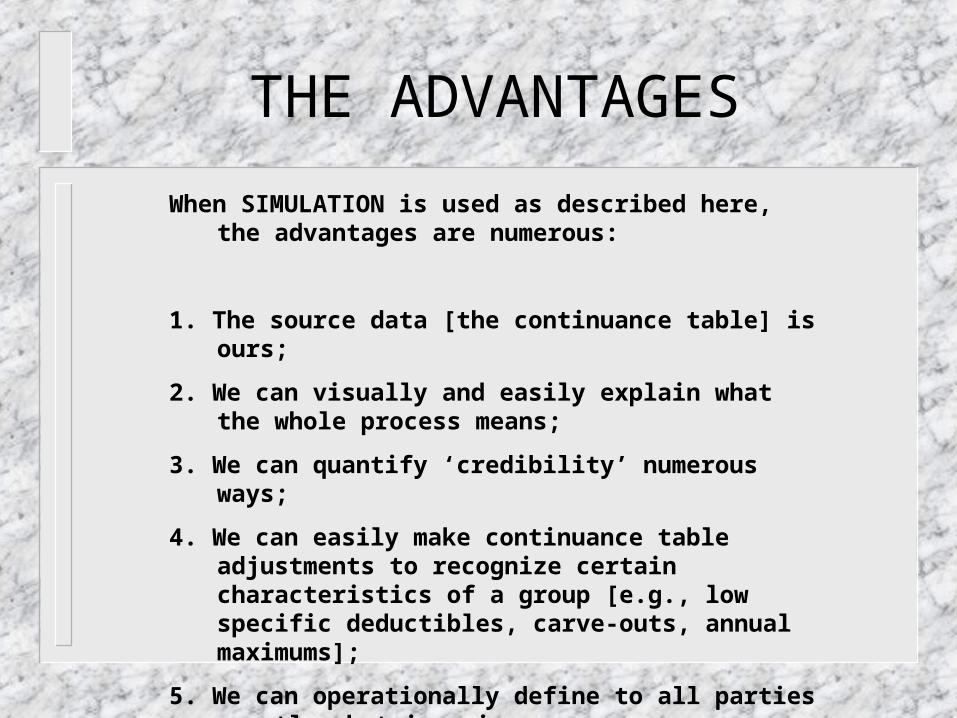

THE ADVANTAGES

When SIMULATION is used as described here, the advantages are numerous:

1. The source data [the continuance table] is ours;

2. We can visually and easily explain what the whole process means;

3. We can quantify ‘credibility’ numerous ways;

4. We can easily make continuance table adjustments to recognize certain characteristics of a group [e.g., low specific deductibles, carve-outs, annual maximums];

5. We can operationally define to all parties exactly what is going on.

TABULATING CREDIBILITY

There are many ways to tabulate credibility when approached from the perspective defined here. The two basic categories are:

1. Percentage of simulations falling within +/- x% of the expected PMPM;

2. Percentage of simulation dollars falling within +/- x% of the total expected dollars.

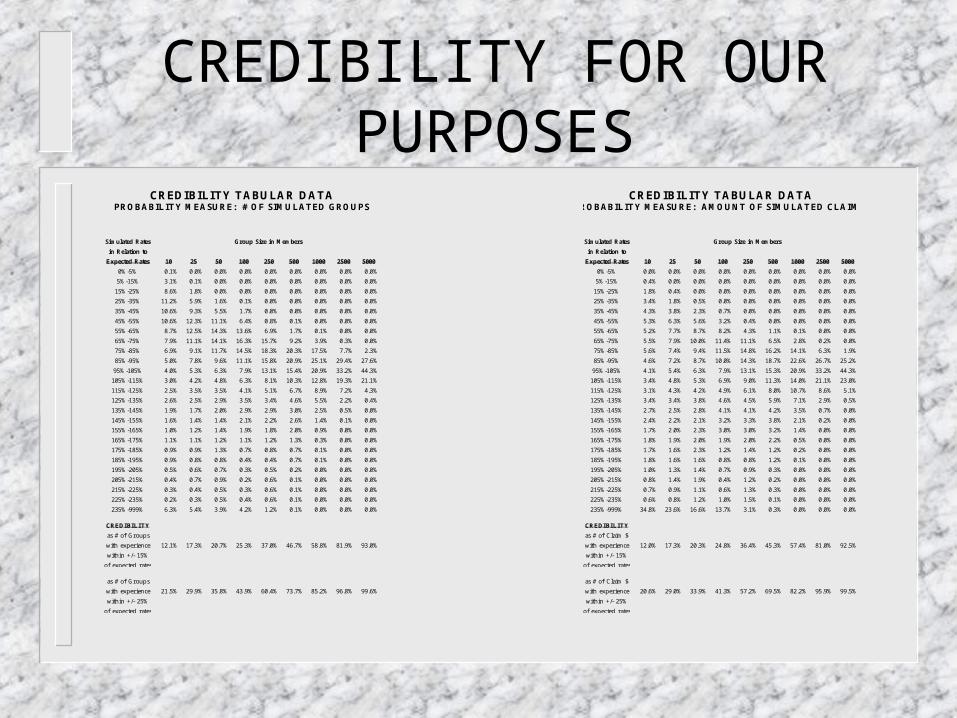

CREDIBILITY FOR OUR PURPOSES

CREDIBILITY TABULAR DATA PROBABILITY MEASURE: # OF SIMULATED GROUPS

Simulated Rates Group Size in Members

in Relation to

Expected Rates 10 25 50 100 250 500 1000 2500 5000

0%-5% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

5%-15% 3.1% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

15%-25% 8.6% 1.8% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

25%-35% 11.2% 5.9% 1.6% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0%

35%-45% 10.6% 9.3% 5.5% 1.7% 0.0% 0.0% 0.0% 0.0% 0.0%

45%-55% 10.6% 12.3% 11.1% 6.4% 0.8% 0.1% 0.0% 0.0% 0.0%

55%-65% 8.7% 12.5% 14.3% 13.6% 6.9% 1.7% 0.1% 0.0% 0.0%

65%-75% 7.9% 11.1% 14.1% 16.3% 15.7% 9.2% 3.9% 0.3% 0.0%

75%-85% 6.9% 9.1% 11.7% 14.5% 18.3% 20.3% 17.5% 7.7% 2.3%

85%-95% 5.0% 7.8% 9.6% 11.1% 15.8% 20.9% 25.1% 29.4% 27.6%

95%-105% 4.0% 5.3% 6.3% 7.9% 13.1% 15.4% 20.9% 33.2% 44.3%

105%-115% 3.0% 4.2% 4.8% 6.3% 8.1% 10.3% 12.8% 19.3% 21.1%

115%-125% 2.5% 3.5% 3.5% 4.1% 5.1% 6.7% 8.9% 7.2% 4.3%

125%-135% 2.6% 2.5% 2.9% 3.5% 3.4% 4.6% 5.5% 2.2% 0.4%

135%-145% 1.9% 1.7% 2.0% 2.9% 2.9% 3.0% 2.5% 0.5% 0.0%

145%-155% 1.6% 1.4% 1.4% 2.1% 2.2% 2.6% 1.4% 0.1% 0.0%

155%-165% 1.0% 1.2% 1.4% 1.9% 1.8% 2.0% 0.9% 0.0% 0.0%

165%-175% 1.1% 1.1% 1.2% 1.1% 1.2% 1.3% 0.3% 0.0% 0.0%

175%-185% 0.9% 0.9% 1.3% 0.7% 0.8% 0.7% 0.1% 0.0% 0.0%

185%-195% 0.9% 0.8% 0.8% 0.4% 0.4% 0.7% 0.1% 0.0% 0.0%

195%-205% 0.5% 0.6% 0.7% 0.3% 0.5% 0.2% 0.0% 0.0% 0.0%

205%-215% 0.4% 0.7% 0.9% 0.2% 0.6% 0.1% 0.0% 0.0% 0.0%

215%-225% 0.3% 0.4% 0.5% 0.3% 0.6% 0.1% 0.0% 0.0% 0.0%

225%-235% 0.2% 0.3% 0.5% 0.4% 0.6% 0.1% 0.0% 0.0% 0.0%

235%-999% 6.3% 5.4% 3.9% 4.2% 1.2% 0.1% 0.0% 0.0% 0.0%

CREDIBILITY

as # of Groups

with experience 12.1% 17.3% 20.7% 25.3% 37.0% 46.7% 58.8% 81.9% 93.0%

within +/- 15%

of expected rates

as # of Groups

with experience 21.5% 29.9% 35.8% 43.9% 60.4% 73.7% 85.2% 96.8% 99.6%

within +/- 25%

of expected rates

CREDIBILITY TABULAR DATA PROBABILITY MEASURE: AMOUNT OF SIMULATED CLAIM $

Simulated Rates Group Size in Members

in Relation to

Expected Rates 10 25 50 100 250 500 1000 2500 5000

0%-5% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

5%-15% 0.4% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

15%-25% 1.8% 0.4% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

25%-35% 3.4% 1.8% 0.5% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

35%-45% 4.3% 3.8% 2.3% 0.7% 0.0% 0.0% 0.0% 0.0% 0.0%

45%-55% 5.3% 6.3% 5.6% 3.2% 0.4% 0.0% 0.0% 0.0% 0.0%

55%-65% 5.2% 7.7% 8.7% 8.2% 4.3% 1.1% 0.1% 0.0% 0.0%

65%-75% 5.5% 7.9% 10.0% 11.4% 11.1% 6.5% 2.8% 0.2% 0.0%

75%-85% 5.6% 7.4% 9.4% 11.5% 14.8% 16.2% 14.1% 6.3% 1.9%

85%-95% 4.6% 7.2% 8.7% 10.0% 14.3% 18.7% 22.6% 26.7% 25.2%

95%-105% 4.1% 5.4% 6.3% 7.9% 13.1% 15.3% 20.9% 33.2% 44.3%

105%-115% 3.4% 4.8% 5.3% 6.9% 9.0% 11.3% 14.0% 21.1% 23.0%

115%-125% 3.1% 4.3% 4.2% 4.9% 6.1% 8.0% 10.7% 8.6% 5.1%

125%-135% 3.4% 3.4% 3.8% 4.6% 4.5% 5.9% 7.1% 2.9% 0.5%

135%-145% 2.7% 2.5% 2.8% 4.1% 4.1% 4.2% 3.5% 0.7% 0.0%

145%-155% 2.4% 2.2% 2.1% 3.2% 3.3% 3.8% 2.1% 0.2% 0.0%

155%-165% 1.7% 2.0% 2.3% 3.0% 3.0% 3.2% 1.4% 0.0% 0.0%

165%-175% 1.8% 1.9% 2.0% 1.9% 2.0% 2.2% 0.5% 0.0% 0.0%

175%-185% 1.7% 1.6% 2.3% 1.2% 1.4% 1.2% 0.2% 0.0% 0.0%

185%-195% 1.8% 1.6% 1.6% 0.8% 0.8% 1.2% 0.1% 0.0% 0.0%

195%-205% 1.0% 1.3% 1.4% 0.7% 0.9% 0.3% 0.0% 0.0% 0.0%

205%-215% 0.8% 1.4% 1.9% 0.4% 1.2% 0.2% 0.0% 0.0% 0.0%

215%-225% 0.7% 0.9% 1.1% 0.6% 1.3% 0.3% 0.0% 0.0% 0.0%

225%-235% 0.6% 0.8% 1.2% 1.0% 1.5% 0.1% 0.0% 0.0% 0.0%

235%-999% 34.8% 23.6% 16.6% 13.7% 3.1% 0.3% 0.0% 0.0% 0.0%

CREDIBILITY

as # of Claim $

with experience 12.0% 17.3% 20.3% 24.8% 36.4% 45.3% 57.4% 81.0% 92.5%

within +/- 15%

of expected rates

as # of Claim $

with experience 20.6% 29.0% 33.9% 41.3% 57.2% 69.5% 82.2% 95.9% 99.5%

within +/- 25%

of expected rates

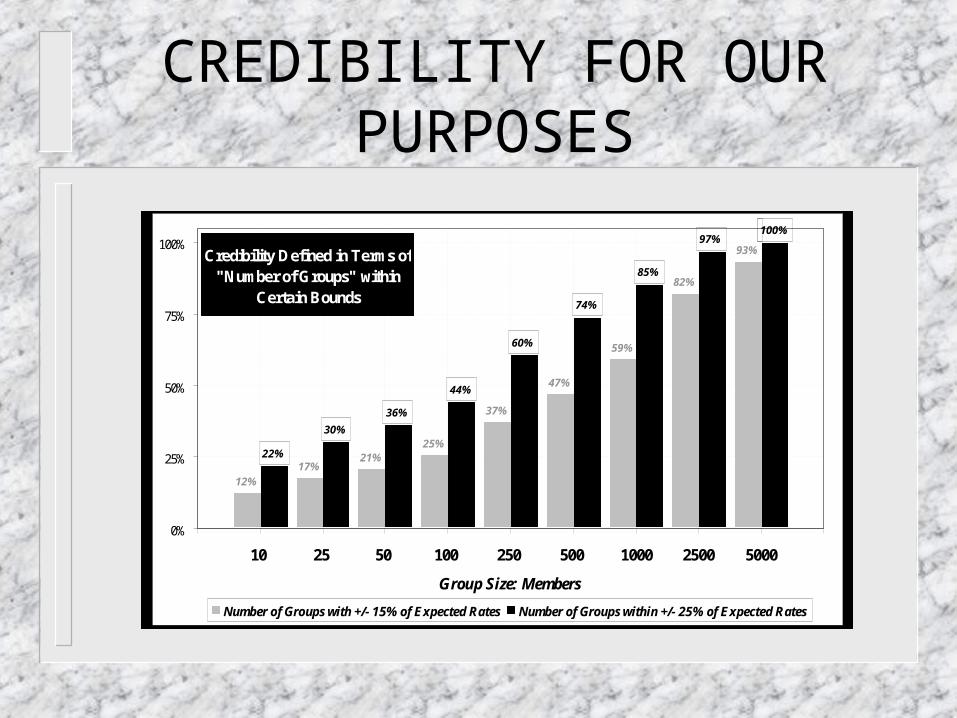

CREDIBILITY FOR OUR PURPOSES

12%17%

21%25%

37%

47%

59%

82%

93%

22%

30%

36%

44%

60%

74%

85%

97%100%

0%

25%

50%

75%

100%

10 25 50 100 250 500 1000 2500 5000

Group Size: Members

Number of Groups with +/- 15% of Expected Rates Number of Groups within +/- 25% of Expected Rates

Credibility Defined in Terms of "Number of Groups" within

Certain Bounds

CREDIBILITY FOR OUR PURPOSES

12%17%

20%25%

36%

45%

57%

81%

93%

21%

29%34%

41%

57%

70%

82%

96%100%

0%

25%

50%

75%

100%

10 25 50 100 250 500 1000 2500 5000

Group Size: Members

Amount of Claim $ with +/- 15% of Expected Rates Amount of Claim $ within +/- 25% of Expected Rates

Credibility Defined in Terms of "Amount of Claim $" within

Certain Bounds

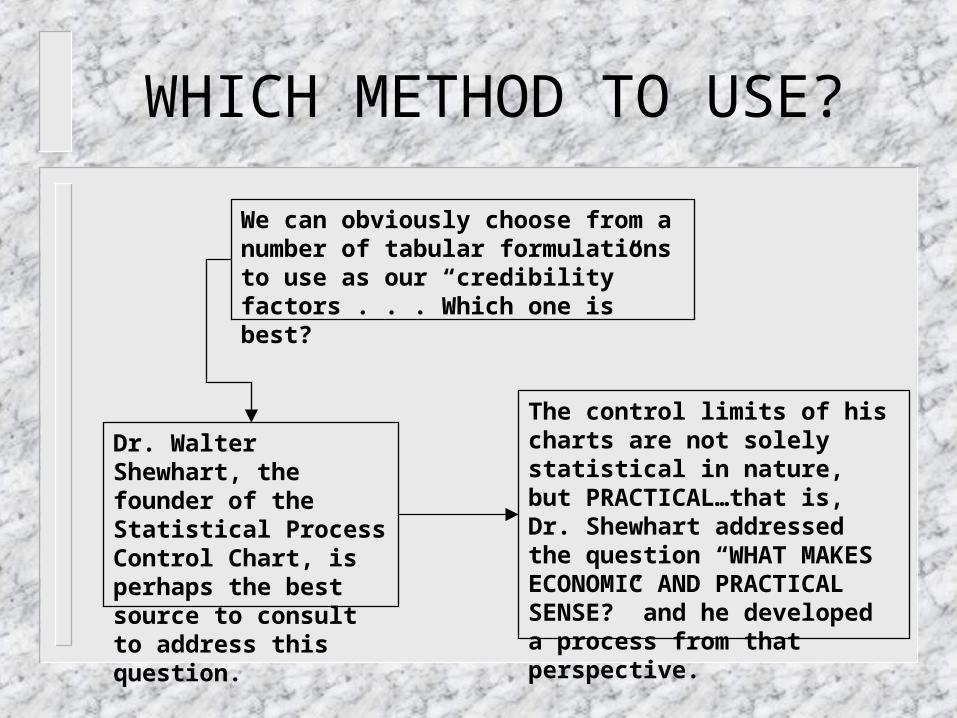

WHICH METHOD TO USE?

We can obviously choose from a number of tabular formulations to use as our “credibility” factors . . . Which one is best?

Dr. Walter Shewhart, the founder of the Statistical Process Control Chart, is perhaps the best source to consult to address this question.

The control limits of his charts are not solely statistical in nature, but PRACTICAL…that is, Dr. Shewhart addressed the question “WHAT MAKES ECONOMIC AND PRACTICAL SENSE?” and he developed a process from that perspective.

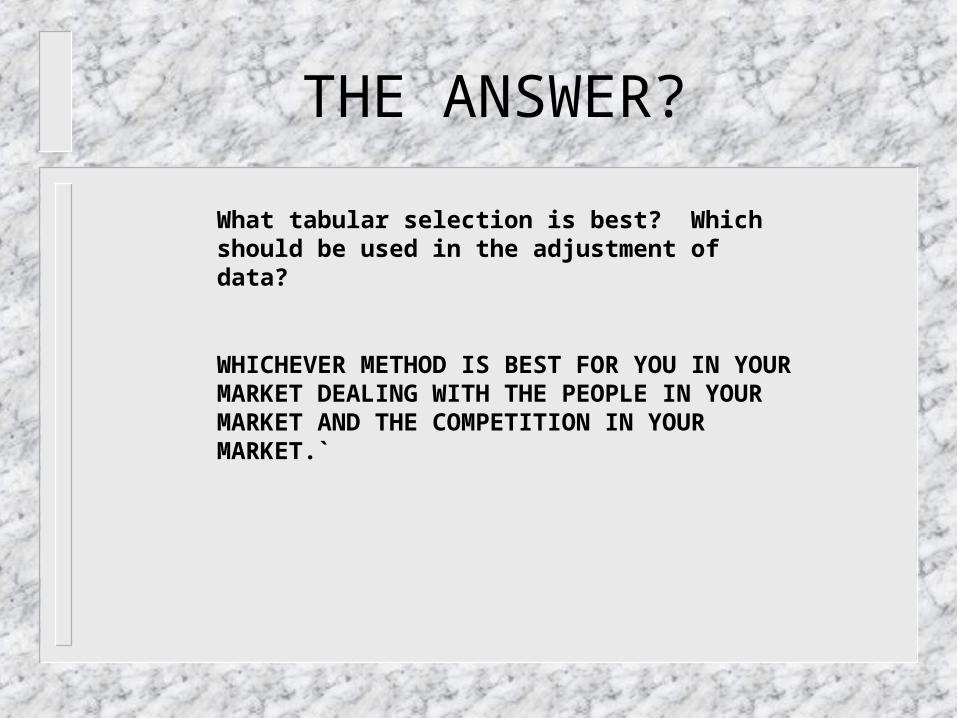

THE ANSWER?

What tabular selection is best? Which should be used in the adjustment of data?

WHICHEVER METHOD IS BEST FOR YOU IN YOUR MARKET DEALING WITH THE PEOPLE IN YOUR MARKET AND THE COMPETITION IN YOUR MARKET.`

CONCLUSION

Have I convinced you there is a problem?

Have I addressed the reason for this problem?

Have I developed the cause of the problem?

Have I solved the problem?

Have I quantified in practical terms what “solution” means?

Have I shown numerous advantages to such a solution, while not introducing negative consequences?

CONCLUSION

Have I convinced you there is a problem?

Have I addressed the reason for this problem?

Have I developed the cause of the problem?

Have I solved the problem?

Have I quantified in practical terms what “solution” means?

Have I shown numerous advantages to such a solution, while not introducing negative consequences?

CONCLUSION

Have I convinced you there is a problem?

Have I addressed the reason for this problem?

Have I developed the cause of the problem?

Have I solved the problem?

Have I quantified in practical terms what “solution” means?

Have I shown numerous advantages to such a solution, while not introducing negative consequences?

CONCLUSION

Have I convinced you there is a problem?

Have I addressed the reason for this problem?

Have I developed the cause of the problem?

Have I solved the problem?

Have I quantified in practical terms what “solution” means?

Have I shown numerous advantages to such a solution, while not introducing negative consequences?

CONCLUSION

Have I convinced you there is a problem?

Have I addressed the reason for this problem?

Have I developed the cause of the problem?

Have I solved the problem?

Have I quantified in practical terms what “solution” means?

Have I shown numerous advantages to such a solution, while not introducing negative consequences?

CONCLUSION

Have I convinced you there is a problem?

Have I addressed the reason for this problem?

Have I developed the cause of the problem?

Have I solved the problem?

Have I quantified in practical terms what “solution” means?

Have I shown numerous advantages to such a solution, while not introducing negative consequences?

Related Documents