Creative Resources Leadership Corporate Update February 2017 For personal use only

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Creative Resources Leadership

CorporateUpdate

February2017

For

per

sona

l use

onl

y

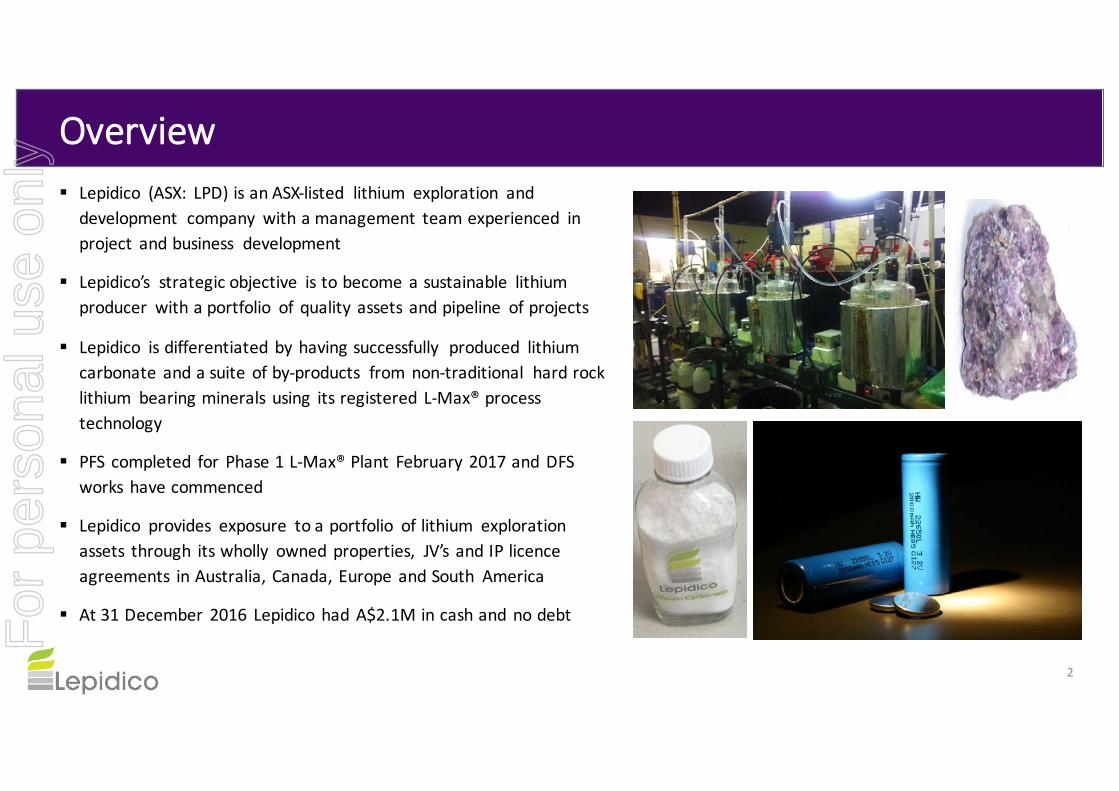

Overview§ Lepidico (ASX: LPD)isanASX-listed lithium exploration and

development company withamanagement teamexperienced inproject andbusiness development

§ Lepidico’s strategicobjective istobecome asustainable lithiumproducer withaportfolio of quality assets andpipeline ofprojects

§ Lepidico isdifferentiatedby havingsuccessfully produced lithiumcarbonate andasuite ofby-products fromnon-traditional hardrocklithium bearingminerals using itsregistered L-Max®processtechnology

§ PFS completed for Phase1L-Max®Plant February 2017andDFSworks havecommenced

§ Lepidico provides exposure toaportfolio oflithium explorationassets through itswholly ownedproperties, JV’s andIPlicenceagreements inAustralia, Canada, Europe andSouth America

§ At31December 2016 Lepidico hadA$2.1Mincashandnodebt

2

For

per

sona

l use

onl

y

Lepidico Strategy&AssetOverviewStrategy:toleverageitsregisteredL-Max®technologytoprocesshigh-quality lithiummicaResourcesviahigh-return,strategicallylocateddevelopmentprojectsthatproducelithiumchemicalsandasuiteofvaluableproducts.

3

For

per

sona

l use

onl

y

MineralResourceDevelopment

4

SeparationRapids*§ TheSeparationRapidsdeposit isoneofthelargest“complex-type”lithiumpegmatitedepositsintheworld

§ NI43-101PEAcompleted onthePetalite MineralResource

§ Excellent recoveries andhigh-specification, 99.88%batterygradelithiumcarbonateproduced inL-Max® testwork programme

§ OutcroppingLepidolite zonelargelyundrilled – Resource drillingscheduledtocommenceMarch2017 forcompletion inJuneQtr

§ LetterofIntentwithAvalonAdvancedMaterials Inc.(TSX:AVLandOTCQX:AVLNF)foranintegratedLepidoliteminingand lithiumcarbonateproductionpartnership inCanada

Reference: ASXAnnouncement, LithiumAlliance withAvalonAdvancedMaterials Inc,6February 2017

For

per

sona

l use

onl

y

MineralResourceDevelopment

5

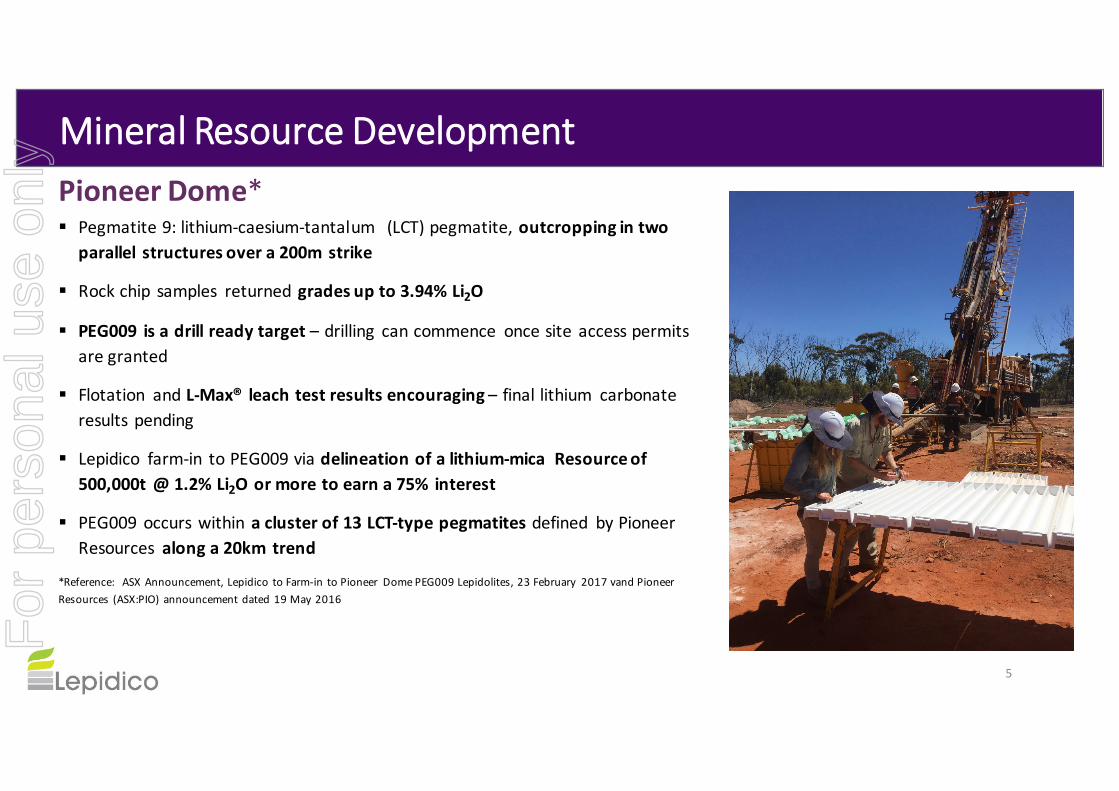

PioneerDome*§ Pegmatite9:lithium-caesium-tantalum (LCT)pegmatite,outcroppingintwo

parallel structuresovera200m strike

§ Rockchip samples returnedgradesupto3.94%Li2O

§ PEG009 isadrillreadytarget– drilling cancommence oncesite accesspermitsaregranted

§ Flotation andL-Max® leachtestresultsencouraging– finallithium carbonateresults pending

§ Lepidico farm-in toPEG009viadelineationofalithium-mica Resourceof500,[email protected]%Li2Oormoretoearna75% interest

§ PEG009occurswithinaclusterof13LCT-typepegmatitesdefined byPioneerResources alonga20km trend

*Reference: ASXAnnouncement, Lepidico toFarm-in toPioneer DomePEG009Lepidolites,23February 2017vand PioneerResources (ASX:PIO)announcementdated19May2016

For

per

sona

l use

onl

y

MineralResourceDevelopment

6

Lemare*§ LemareCentralZone– spodumene pegmatitestrikeof300mand

opentotheNE

§ Drillresults havereturned: [email protected]%Li2O;[email protected]% Li2O;[email protected]% Li2O

§ Newspodumene pegmatiteidentified atLemare SW, 600mstrike,upto4.26%Li2O inrockchipsamples,averagegradeof 2.19%Li2O

§ Lemare claims cover74km2 intheJamesBayregion, 60km fromNemaska, 30kmeastofNemaska Lithium’s Whabouchi deposit

§ Earn-inforuptoa75%interestinLemare fromCritical Elements Corp. Nextdrill phaseC$350k,March2017.

*Reference: ASXAnnouncement,Drilling torecommence at Lemare LithiumProject,16February 2017andtheCompany’sannouncement)dated24November 2016

For

per

sona

l use

onl

y

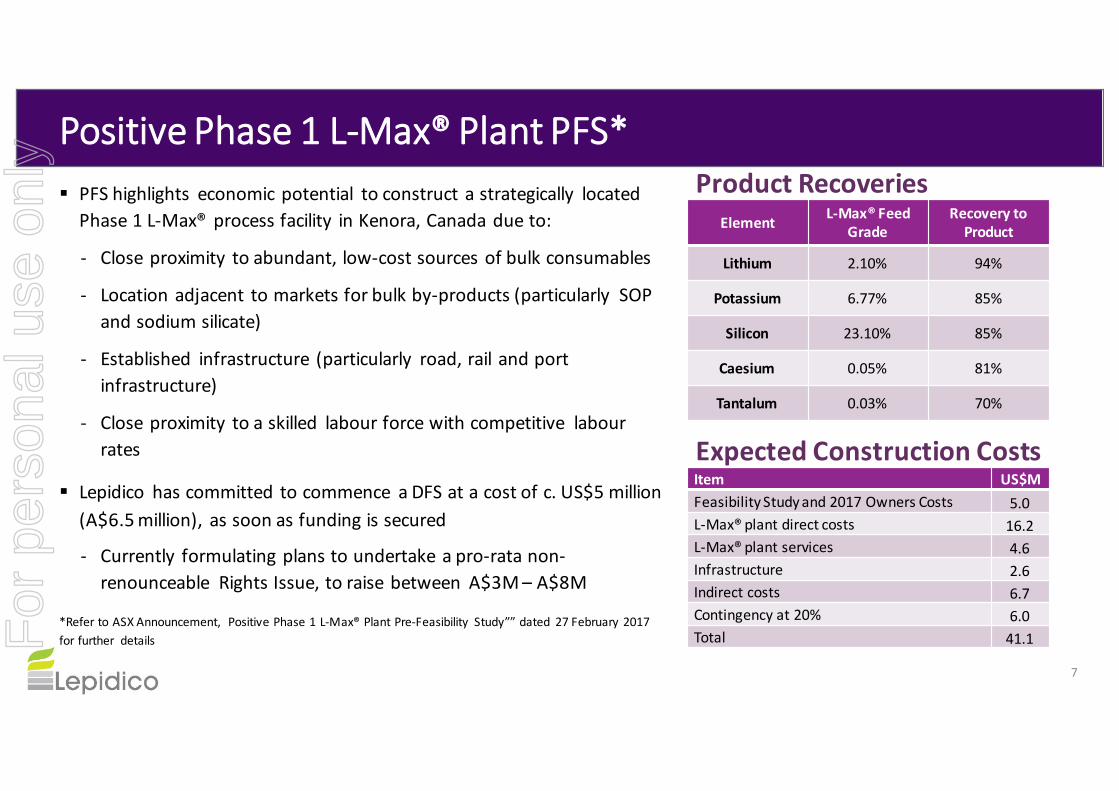

PositivePhase1L-Max®PlantPFS*§ PFShighlights economicpotential toconstructastrategically locatedPhase1L-Max®processfacility inKenora,Canadadueto:

- Closeproximity toabundant,low-costsourcesofbulkconsumables

- Locationadjacent tomarketsforbulkby-products(particularly SOPandsodiumsilicate)

- Established infrastructure (particularly road,railandportinfrastructure)

- Closeproximity toaskilled labourforcewithcompetitive labourrates

§ Lepidico hascommitted tocommence aDFSatacostofc.US$5million(A$6.5million),assoonasfundingissecured

- Currently formulatingplanstoundertakeapro-ratanon-renounceable RightsIssue,toraisebetween A$3M– A$8M

*RefertoASXAnnouncement, PositivePhase1L-Max®PlantPre-Feasibility Study””dated 27February2017forfurther details

7

Element L-Max®FeedGrade

RecoverytoProduct

Lithium 2.10% 94%

Potassium 6.77% 85%

Silicon 23.10% 85%

Caesium 0.05% 81%

Tantalum 0.03% 70%

ProductRecoveries

ExpectedConstructionCostsItem US$MFeasibilityStudyand2017OwnersCosts 5.0L-Max®plantdirectcosts 16.2L-Max®plantservices 4.6Infrastructure 2.6Indirectcosts 6.7Contingencyat20% 6.0Total 41.1F

or p

erso

nal u

se o

nly

Phase1L-Max®PlantProjectProgressingtoDFS§ Keymetrics fortheDFSscope* willbe:

- Plantthroughput rate3.6tphoflithium-mica concentrate(annualised rateof29,000tpa – 91.4%operating time)

- Batterygradelithium carbonate equivalent (LCE)production ofc.3,000tpa

- AverageC1Costs nil tonegativeafterby-products

- AverageC3Costs ofUS$1,000-2,000/t afterby-productcredits including amortisation ofdevelopment capital

- Capex ofUS$40-45M (incl. 20%contingency andUS$5MforDFScosts)

- Valuable suite ofby-products including sulphate ofpotash(SOP), caesium, tantalumconcentrate andsodium silicate

*Theassumptionssetoutaboveandelsewhereinthisannouncementcontainreferencetobroadindicativeplantoperatingparameters(Parameters) forthepurposeoftheDFSwhichhavebeendevelopedthroughscopinglevelworkandsubsequentPFSwork.Fortheavoidanceofdoubt,investorsareadvisedthattheParametersexpectedtobeadoptedfortheDFSdonotconstituteaproductionforecastortargetinrelationtomineralresourcesassociatedwithanyprojectownedbytheCompany.TheCompanywishestoexpresslyclarifythatanyreferencesinthisannouncementorthePFStoannualproductionratesrelatetoscopingandplanningparametersandarenotaproductiontarget.TheCompanycautionsinvestorsagainstusinganystatementsmadeineitherthisannouncementorthePFSwhichmayindicateoramounttothereportingofaproductiontargetorforecastfinancialinformation,asabasisformakinganyinvestmentdecisionsaboutsharesintheCompany.TheprimarypurposeofdisclosingtheDFSParameters istoinformonthescopeofworkforthestudyandprovideanestimateoftheintendedscaleofapotentialfuturePhase1Plant.

8

Item US$/tofConcentrateProcessed(currentprices)

Concentratepurchase 350Concentratetransport 4Inboundconsumableslogistics 144ConsumablesFOB 286Processingcostsother 186Sales,marketing,andoutbound logistics 55Generalandadministration 104TotalUnitCost 1,130

KeyParameter KeyMetric

LithiumCarbonate(>99.5%)Production 3,000tpaSOP(>95%K2SO4)Production 3,000-4,000tpaSodiumSilicate(40wt%solutionatSiO2:Na2Oratioof2.0)Production 40,000-50,000tpa

Caesium(asmetalcontainedinformate)Production 10-100tpaTantaliteCon(30%Ta2O5)Production 20-25tpaLiCarbonate C1costafterby-productscredits <=US$0/tLiCarbonate C3costafterby-productcredits US$1,000-2,000/t

ExpectedOperatingCosts

ProjectPlanningKeyMetrics

For

per

sona

l use

onl

y

PeerAnalysisPhase1L-Max®PlantisFavourablyPlacedontheGlobalCostCurve*

*LithiumCarbonateCostCurve2016co-productbasis(Source:Roskill)

9

For

per

sona

l use

onl

y

TheL-Max® Advantage

ü L-Max®leaches lithium from certainmicasandphosphates withoutroasting– conventional processing ofspodumene requires capitalandenergyintensive roasterstoextractlithium, oftenwithnoby-products

ü L-Max®reagentsandoperation havestraightforwardhealth, safetyandenvironmental characteristics

ü L-Max®utilises common use, inexpensive reagents&isenergyefficient

ü L-Max®is novel bututilises conventional equipment andstraightforwardprocesses – aseries of agitatedtanks, crystallisers andfilters

ü By-products include potassium sulphate fertiliser (SOP), sodium silicate,gypsum andpotentially caesiumandrubidium formates

ü Fastleachkinetics, high recoveries andmoderate process costestimatesmakeforcompelling economics

Elementleachcurves underL-Max®- PFSsample10

Lepidolite

K(Li,Al,Rb)3(Al,Si)4O10(F,OH)2

Zinnwaldite

KLiFeAl(AlSi3)O10(OH,F)2

Ambygonite

(Li,Na)AlPO4(F,OH)

0

20

40

60

80

100

0 2 4 6 8 10 12 14 16 18 20 22 24

Metalex

tractio

n(%)

Time(hrs)

Lithium

Cesium

Potassium

For

per

sona

l use

onl

y

TheL-Max® Process– DemonstrableSuccess

Gypsum

Pending

LepidoliteZinnwaldite Amblygonite 11

Lithium carbonate >99.5%orHydroxide

Sodiumsilicate or‘water-glass’

Potassium sulphate Caesiumformate

Sulphuricacid

Limestone

Benign Residue

Qualitytobedetermined

For

per

sona

l use

onl

y

L-Max®- 100%OwnedbyLepidico

12

§ L-Max®isaproprietary,‘straight-forward’yetnovelhydrometallurgicalprocess

§ L-Max®usescommonindustrialreagentsatatmosphericpressureandmoderatetemperature(c.100oC)

§ AninternationalpatentapplicationhasbeenfiledunderthePCTforL-Max®

For

per

sona

l use

onl

y

BusinessModel

OperatingBusiness RoyaltyBusiness

L-Max®processplant(whollyowned/JV)

Integratedwithconcentrator

andmines

Third-partyconcentratefeed

Third-partymineorefeed

L-Max®third-partylicences

13

For

per

sona

l use

onl

y

Opportunities

14

Miningandprocessingsustainablyfor21st centuryproducts

Phase1L-Max®Plantc.3,000tpaLCEH2SO4 ~50,000tpaDFS~US$5MDevelopment~US$35-40M

FullScale1L-Max®[email protected],000tpaLCEH2SO4 ~400,000tpaStudies~US$10MConstruction~$Pending

Phase1L-Max®PlantPFSDFS

Permits&ApprovalsEarlyWorks/FEEDImplementation

Operation

FullScaleL-Max®PlantScopingStudy

PFSDFS

Permits&ApprovalsEarlyWorks/FEEDImplementation

Operation

2017 2018 2019 2020 2021

FID

FID

Mini-plant trial&duediligence

For

per

sona

l use

onl

y

OverviewCapital Structure (ASX:LPD) Directors and Senior Management

Share Price

Description Amount

SharePrice(Close24February2017) 1.5c

Shares O/S(Current) 1.75B

MarketCap(Close 24February2017) $26.3M

Cash(31December2016) $2.1M

Top20Shareholders(31January 2017) 51.5%

Name Title

GaryJohnson Non-ExecutiveChairman

JoeWalsh ManagingDirector

TomDukovcic Executive DirectorExploration

MarkRodda Non-ExecutiveDirector

ShontelNorgate ChiefFinancialOfficer

GavinBecker GMBusinessDevelopment

15

Lithium Carbonate Price

For

per

sona

l use

onl

y

DirectorsandSeniorManagementTeam

16

Mr. Gary JohnsonMAusIMM, MAICD

Chairman

Mr. Tom DukovcicBSc (Hons), MAIG, MAICDDirector Exploration

Mr. Joe WalshBEng, MSc

Managing Director

Mr. Mark RoddaBA, LLB

Non-Executive Director

Mark is a lawyer with 20 years experience in the resources sector including the management of local and international mergers and acquisitions, divestments, exploration and project joint ventures, strategic alliances, corporate and project financing transactions and corporate restructuring initiatives.

Tom is a geologist with over 25 years experience in exploration and development. He has worked in diverse regions throughout Australia, including the Yilgarn, Kimberley, central Australia and northeast Queensland. Tom is a Member of the Australian Institute of Geoscientists and a Member of the Australian Institute of Company Directors.

Joe is a resources industry executive and mining engineer with over 25 years experience working for mining companies and investment banks. Joe also has extensive equity market experience and has been involved with the technical and economic evaluation of many mining assets and companies around the world.

Gary has over 30 years experience in the mining industry as a metallurgist, manager, owner, director and managing director possessing broad technical and practical experience of the workings and strategies required by successful mining companies.

Mr. Gavin BeckerARSM, BSc (Eng), MBA,

FAusIMM, CP(Met), GAICDBusiness Development

Gavin is a metallurgist with 40 years industry experience. During that time he has worked in senior operational, R&D, feasibility study and consulting roles on lead/zinc, gold, uranium, copper and nickel/cobalt/scandium mines and/or projects.

Ms. Shontel NorgateB.Bus

Chief Financial Officer

Shontel is a finance executive with over 20 years commercial experience in the resources industry including debt and equity finance, financial reporting, project management, corporate governance, commercial negotiations and business analysis

For

per

sona

l use

onl

y

InvestorHighlights

CompetitiveAdvantage

§ AfarlesscompetitivelandscapeexistsforLi-micaandLi-phosphateexplorationproperties§ L-Max®isexpectedtohaverelativelycompetitivecapitalintensity

§ By-productpotentialmeansL-Max®shouldhaveacompetitiveoperatingcoststructure

L-Max®

§ Employsconventionalprocessesusingindustrystandardequipment,operatedatambientpressureandmoderatetemperature§ Employscommonuse,inexpensivereagentswithstraightforwardhealth,safetyandenvironmentalcharacteristics

§ Hasanovelflowsheetthatisthesubjectofaninternationalpatentapplication

§ PFSconfirmedviabilityofconstructingastrategicallylocatedPhase1L-Max®PlantatKenora,Canada,processinglithium-micaconcentratespurchasedfromthirdparties

§ DFSworkhascommenced§ Firstproductionprojectedfor2019

ProvenTeam

§ Managementteamexperiencedinnewprocess,projectandbusinessdevelopment§ Astrongindustrytrackrecordthatincludescompanytransformingprojectandtechnologydevelopment

§ Significantmilestonesaccomplishedinashortperiodoftime– Lepidicoisjustgettingstarted……

FeedSources

§ Lepidicoisbuildingaportfolioofqualitylithiumassetsaroundtheworld§ InboundenquiriesrevealexplorersthatdiscoverLi-richmicasaredrawntoL-Max®

§ TailingsandwastedumpsrichinLi-micaofferneartermproductionopportunities

17

PathwaytoProduction

For

per

sona

l use

onl

y

LithiumCarbonate/Hydroxide

Supply&MarketBalance“Liisnotrare,justanunderdevelopedmarket”1: depositsclosetoinfrastructure,andofsufficientscaleandqualityforsaleablebatterygradeproductarelesscommon

Committednewsupply: hardrockminedevelopmentswillseenewsourcesoflithiumsupplyfrom2016to2018bringingmarketbacktobalance

Longertermsupplygrowthlesscertain: mostcommentatorsexpectbrineproducerstoincrementallyincreaseoutput tobalancedemand– todatethishasnotbeenthecaseandenvironmental/regulatoryissuesabound

L-Max®willprovideanewsourceoflowcostlithium,frommicas

1DeutcheBank research May2016 18

DBlithiumsupply-demandbalance

DBpriceforecasts(May2016)

For

per

sona

l use

onl

y

LithiumCarbonate/Hydroxide

Usage&DemandSteadygrowth intraditionaluses: fluxes,toughenedglass,medical, andcementandadhesiveadditives

UniquepropertiesforLi-ionbatteries(LIB): Li-ionsmovefromtheanode (-ve carbon)tothecathode(+ve Libased)duringdischargeandbackwhencharging. LIBuseanintercalated lithiumcompoundinthecathode

Stronggrowth inLIBusage: LiCoO1 – highenergydensitybutsafetyrisksifdamaged;LiFePO2/LMO3/NMC4 – longer lifeandsafer;NCA5/LTO6 – moreselective use;andLiS7 – pioneering higherperformance toweight ratio

1LiCoO– Lithium Cobalt Oxide;2LiFePO– Lithium IronPhosphaste; 3LMO– LithiumManganeseOxide;4NMC– (Lithium) Nickel ManganeseCobalt;5NCA– (Lithium) NickelCobalt Aluminum Oxide;6LTO–

Lithium Titanium Oxide;7LiS– Lithium Sulfur;electrolyte – Lisaltinorganicsolvent

19

Batterycostsarefalling

DBGloballithiumdemand forecast

For

per

sona

l use

onl

y

L-Max®:utilises commonuse,inexpensivereagents

L-Max® reagentshavestraightforwardhealth,safetyandenvironmentalcharacteristics

20

Lepidolite Acid consumption (kg/t of mica)

Metal Grade (%) 98% H2SO4 32% HCl 70% HNO3 70% HF

Lithium 2.34 169 385 303 96.3

Rubidium 2.17 12.7 29.0 22.9 7.25

Cesium 0.83 3.12 7.12 5.62 1.78

Potassium 7.65 98.1 224 177 56.0

Aluminum 8.32 462 1054 832 264

Iron 0.36 6.43 14.7 11.6 3.67

Manganese 0.92 16.7 38.2 30.1 9.56

Silicon 27.1 0.00 0.00 0.00 1659

TOTAL (kg/t acid) 768 1,752 1,382 2,098

ACID COST ($/tonne) $100 $150 $250 $800

ACID COST ($/tonne mica) $77 $263 $346 $1,678

Forahostofreasons(including costefficiency, downstream processing simplicity, materialsofconstructin andOH&Sissues)sulphuric acidisclearlyfavouredoverother leachingreagents(such ashydrochloric, nitric andhydrofluoric acids).

For

per

sona

l use

onl

y

SodiumSilicate

8milliontonnes perannumglobalmarketWidecommercialandindustrialapplications,usedin:cement/plaster(reducesporosity),detergents,wastewatertreatment(coagulant),passivefireprotection,textileandlumberprocessing,refractories,andautomobiles/metalrepair

Existingsupply: fromcombiningvariousratiosofsandandsodaashat1,100-1,200oC;Na2CO3 +SiO2 →Na2SiO3 +CO2

Quality: propertiesvarydependingontheSiO2/Na2Oratio;highervalueproductswitharatioof<2.0

L-Max®willprovideanewsourceoflow-costsodiumsilicate:PFStestworkhasproducedsodiumsilicatewitharatioof1.6

SolutionPrice:US$650-700/tex-works1;US$250/tdelivered21SourcePQCorporation website; 2 Lepidico PFSassumption

21

Source:PQCorporation websiteFor

per

sona

l use

onl

y

Caesium&Rubidium

NicheglobalmarketMainindustrialapplications:caesium (Cs)formate isusedasacompletionfluidinoilwells(c.80%recycled)aswellasinelectricitygeneration,electronics,andchemistry

ExistingCssupply: minedpollucite supplyislimited

Quality: highdensityCsformate brinewithaspecificgravityofc.2.3requiredforoildrilling

L-Max®willprovideanewsourceoflow-costCs&Rb:PFStestworkhasproducedCs/Rb formatewithanSGof2.0

Price:nomarketpricesareavailableforthesealkalimetals.Contractprices1 arestatedasUS$12,000-15,000/tCsmetalcontainedinformate

1Sourceproducer andmarketparticipant22

For

per

sona

l use

onl

y

PotassiumSulphate (SOP)

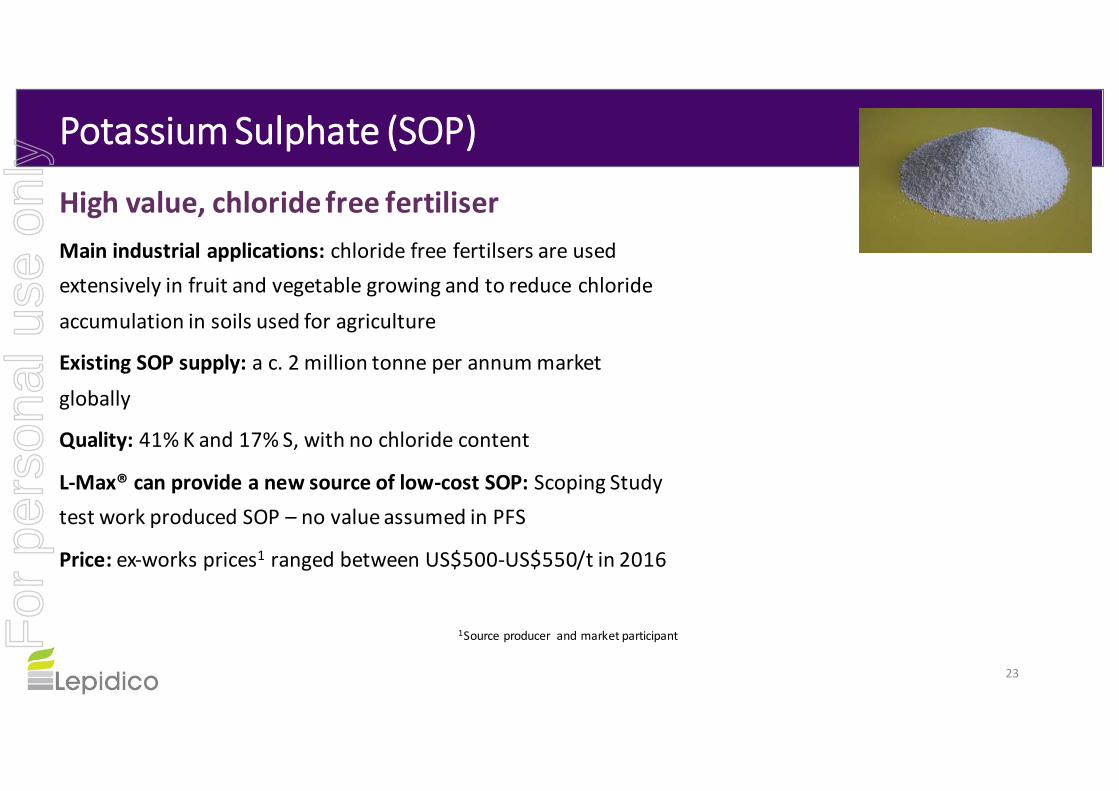

Highvalue,chloridefreefertiliserMainindustrialapplications:chloridefreefertilsers areusedextensivelyinfruitandvegetablegrowingandtoreducechlorideaccumulationinsoilsusedforagriculture

ExistingSOPsupply: ac.2milliontonne perannummarketglobally

Quality: 41%Kand17%S,withnochloridecontent

L-Max®canprovideanewsourceoflow-costSOP:ScopingStudytestworkproducedSOP– novalueassumedinPFS

Price:ex-worksprices1 rangedbetweenUS$500-US$550/tin2016

1Sourceproducer andmarketparticipant

23

For

per

sona

l use

onl

y

Gypsum

CloseproximitytomarketrequiredMainindustrialapplications:fertiliser – softenshardgroundincreasingyieldandreducingwearonmachinery,andasthemainconstituentinmanyformsofplaster,wallboardandchalk

ExistingCaSO4·2H2Osupply: 246milliontonnes globallyin2014fromnumeroussmallscalede-centralised openpitoperationsandrecycling

Quality: lowimpuritiesrequiredforagriculturaluse,buildingmaterialusemoreflexible

L-Max®canprovideanewsourceoflow-costgypsum:ScopingStudytestworkproducedgypsumwithinresidue– novalueassumedinPFS

Price:highlyvariabledependingonimpuritiesandproximitytomarket

24

For

per

sona

l use

onl

y

IndependentViewofL-Max®RoskillWeeklyRound-up– 23January 2017

Lithium:Lepidico producesbatterygradelithiumcarbonateusingtheL-Max®technology

Roskillview:“Lepidicoproducedabatterygradelithiumcarbonateproductgrading99.75%Li2CO3 froma30kgsampleoflepidolite andlithiummicabearingtailings.ThetailingsweregatheredfromanexistingminingoperationandformoneofthreesamplesgatheredatseparatedepositstobeprocessedaspartofaprefeasibilitystudyontheL-Max®plant.Asaresultofthesuccessfulresults,LepidicoexpectstobeginadefinitivefeasibilitystudyoncontinuousL-Max®mini-planttrailsinFebruary2017.

Theproductionofthebatterygradelithiumcarbonateproductfromlepidolite andlithiummicabearingtailingsmaterialrepresentsanattractivepotentialsourceoflithiumchemicalsifprocessingcostsarecomparablewithexistingprimarylithiumproduction. Therecoveryoflithiumcarbonatereportedat91%isalsocomparablewithspodumene processingatChineseconversionplants.Iftest-workontheothersamplesprovessuccessful,thepossibilityofacentralisedplantprocessingtailingsmaterialfrommultiplesourcesimprovesprojectviability.Completionofthepre-feasibilitystudyinQ1-2017anddefinitivefeasibilitystudyscheduledforQ4-2017isawaitedtodeterminehowLepidicoseetheL-Max®plantwouldfittingintothelithiummarket,thoughfirstresultsappearpositive”.

AsubsequentASXannouncement(25January)revealedtestresultsonsecondPFSsamplewithafurtherimprovedproductgrade(99.88%)andoverallrecovery(93%)

25

For

per

sona

l use

onl

y

ImportantNotice

26

ThispresentationhasbeenpreparedbythemanagementofLepidico Ltd(the'Company')forthebenefitofbrokers,analystsandinvestorsandnotasspecificadvicetoanyparticularpartyorperson.

Theinformationisbasedonpubliclyavailableinformation,internallydevelopeddataandotherexternalsources.Noindependentverificationofthosesourceshasbeenundertakenandwhereanyopinionisexpressedinthisdocumentitisbasedontheassumptionsandlimitationsmentionedhereinandisanexpressionofpresentopiniononly.Nowarrantiesorrepresentationscanbemadeastotheorigin,validity,accuracy,completeness,currencyorreliabilityoftheinformation.TheCompanydisclaimsandexcludesallliability(totheextentpermittedby law),forlosses,claims,damages,demands,costsandexpensesofwhatevernaturearisinginanywayoutoforinconnectionwiththeinformation,itsaccuracy,completenessorbyreasonofreliancebyanypersononanyofit.WheretheCompanyexpressesorimpliesanexpectationorbeliefastothesuccessoffutureexplorationandtheeconomicviabilityoffutureprojects,suchexpectationorbeliefisbasedonmanagement’scurrentpredictions,assumptionsandprojections.However,suchforecastsaresubjecttorisks,uncertaintiesandother factorswhichcouldcauseactualresultstodiffermateriallyfromfutureresultsexpressed,projectedorimpliedbysuchforecasts.Suchrisksinclude,butarenotlimitedto,explorationsuccess,commoditypricevolatility,futurechangestomineralresourceestimates,changestoassumptionsforcapitalandoperatingcostsaswellaspoliticalandoperationalrisksandgovernmentalregulationoutcomes.Formoredetailofrisksandotherfactors,refertotheCompany'sotherAustralianSecuritiesExchangeannouncements andfilings.TheCompanydoesnothaveanyobligationtoadviseanypersonifitbecomesawareofanyinaccuracyin,oromissionfrom,anyforecastortoupdatesuchforecast.

CompetentPersonStatementTheinformationinthisreportthatrelatestoExplorationResultsisbasedoninformationcompiledbyMrTomDukovcic,whoisanemployeeoftheCompanyandamemberoftheAustralianInstituteofGeoscientistsandwhohassufficientexperiencerelevanttothestylesof mineralisationandthetypesofdepositunderconsideration,andtotheactivitythathasbeenundertaken,toqualifyasaCompetentPersonasdefinedinthe2012editionofthe“AustralasianCodeforReportingofExplorationResults,MineralResourcesandOreReserves.”MrDukovcicconsentstotheinclusioninthisreportofinformationcompiledbyhimintheformandcontextinwhichitappears.F

or p

erso

nal u

se o

nly

Related Documents