Creating a Bargain Position for India in Hardware Recommendations for Budget 2002-03

Creating a Bargain Position for India in Hardware Recommendations for Budget 2002-03.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Creating a Bargain Position for Indiain Hardware

Recommendations for Budget 2002-03

2

Why Focus on IT Manufacturing & Hardware IT Manufacturing governs and determines the competitive of a nation

IT/Electronics exports account for 47% of S’pore GDP and 65% of Malaysia China’s hardware exports: USD 26 Bn in 2000

Will help build bargain position Shield India from the vulnerability of Sanctions from countries controlling

technology and production

Huge potential for employment generation for unskilled labour Hardware focus essential to remain competitive in software Estimated cumulative hardware requirement by 2008 in the India to meet

software exports target of USD 87 Bn: USD 160 Bn will be a significant drain on forex reserves if everything is imported

The future is in embedded systems and applications - hardware knowledge is critical to build this competence

3

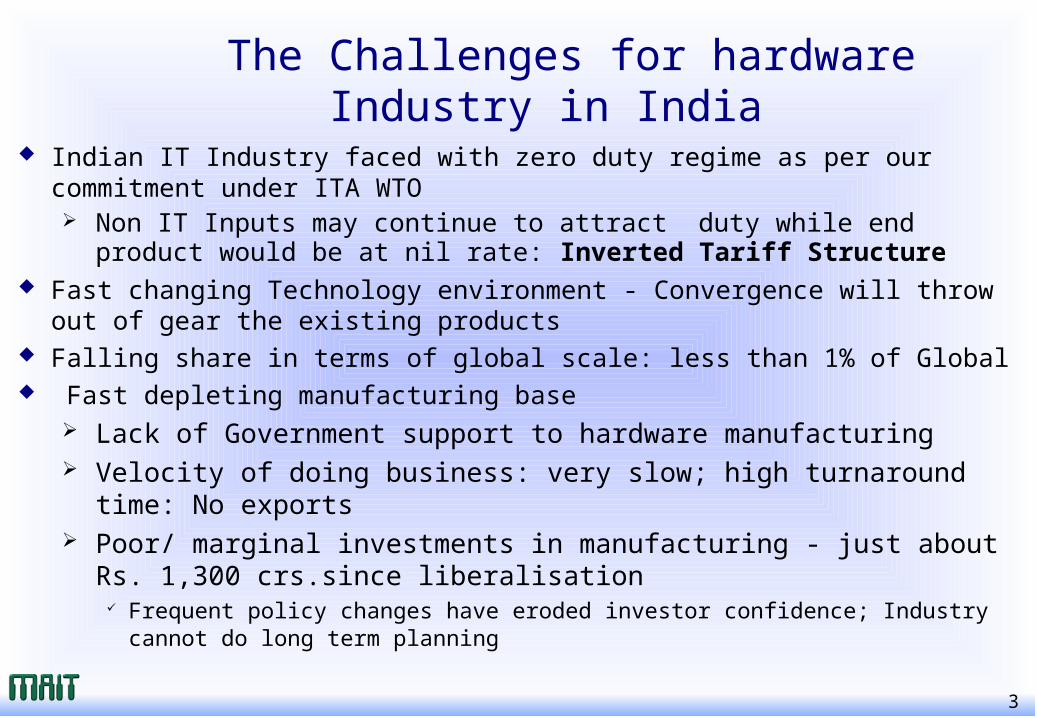

The Challenges for hardware Industry in India

Indian IT Industry faced with zero duty regime as per our commitment under ITA WTO Non IT Inputs may continue to attract duty while end product would be at

nil rate: Inverted Tariff Structure Fast changing Technology environment - Convergence will throw out of gear

the existing products Falling share in terms of global scale: less than 1% of Global Fast depleting manufacturing base

Lack of Government support to hardware manufacturing Velocity of doing business: very slow; high turnaround time: No exports Poor/ marginal investments in manufacturing - just about Rs. 1,300

crs.since liberalisation Frequent policy changes have eroded investor confidence; Industry cannot do long

term planning

4

The Challenges of Globalisation...

India Need to build strategy around technology

Domestic market: increased Grey market and piracy

High price sensitivity of the market coupled with high local taxation

has stymied IT penetration PC penetration in India – 6.2/1000; World average: 26/1000

5

What we aim to achieve: A Bargain position in Hardware

Vibrant manufacturing base for Hardware

Creation of Indian IPR through focus on hardware and firmware

designs and creation of High end technology

Increased IT penetration in the country through ‘affordable IT’

and ‘Killer hardware applications’

6

Strategy for Creating a Bargain position in Hardware

Creating Exponential Demand

Manufacturing- Indigenous Manufacturing

- Indigenous R&D and Designs

- Ancilliarisation

Exports:

- Critical Volumes

- Stream Line Duty Structure

- India Price for Critical Components

- Local content/ local context

- Designing Low cost India PC/ Information Device

- International Market Development

- Easy Financing Options

- Clusterisation: SEZ based model

- Improved Velocity of Business: Simplified Procedures

- Self declaration based clearance

systems

Hardwareand

Embedded

Sustainable

Make IT Happen

Results 2005:

• PC Volumes: 10 Mn

• PC Penetration: 26/1000

• H/W & Design Exports: USD 5 Bn

• Employment: 5 Lakhs

7

What we need from the Ministry of Finance

ITA - WTO implementation: 2005, not 2003 ‘Concomitant’ to the phase out the Government had committed:

Nil customs duty on Capital Goods for Electronics manufacturing Phase out customs duty on all input/raw materials including items

of dual usage: Customs duty on inputs varies from 0% to 35% Reduction in transaction/turn-around time to international levels

for exports and imports

The above is yet to be implemented

Follow India’s commitment to WTO on duty Phase out:

Year 2002-03 2003-04 2004-05 2005-06

Peak Rate 15% 15% 10% 0%

8

S.No. Item HSN Existing Recommended

1. Finished Goods 84.71 15% 15%

2. Parts of 8471(except Populated PCBs)

8473.30 5% Nil

3. Populated PCBs 8473.30 15% 15%

4. Stepper Motors for Printers 8501.10 5% Nil

5. Ink Cartridges, Ribbon Assembly, Ribbon Gear Assembly, Ribbon Gear Carriage for use in Printers for Computers

Ch. 84,96 25% 15%

6. Routers and Modems 85.17.50 15% 15%

7. Set-top boxes 8517.80 25% 15%

8. Parts of Printers for computers 8483 25% Nil

9. Cable Assemblies for Computers and Peripherals

8544.19/ 41/49

35% Nil

10. Key switches for Key-boards 8536.50 15% Nil

What we need from the Ministry of Finance Recommended Duty Structure for 2002- 03

9

Recommendation for rewording/amendment of Customs Notification No. 17/2001 dated 01/03/2001 S.No. 269: Condition No. 7* for stepper motors should be deleted S.No. 233: 8473.30

What we need from the Ministry of Finance

Existing Recommended

Parts (including ink cartridges with Print head assembly and ink spray nozzle) of the machines of heading 84.71, other than Populated Printed Circuit Boards (PPCBs) including motherboards (with or without CPU)

Parts of machines of heading 84.71 with or without Printed Circuit board (including ink cartridges with Print head assembly and ink spray nozzle of inkjet Printers, Toner cartridges of Laser Printers and print head of Dot-matrix/Line printers), other than Populated Printed Circuit Boards (PPCBs) including motherboards (with or without CPU)

*Condition No. 7: If the importer follows the procedure set out in the Customs (Import of goods at concessional rate of Duty for Manufacture of Excisable Goods) Rules, 1996.

10

What we need from the Ministry of Finance Rationalisation of Customs Duty: Correction of inverted tariff structure

Customs duty on all Capital goods for Electronics manufacturing including tools, dyes, moulds etc. should be brought down to nil from existing 25%

Customs duty on input raw materials including dual usage items eg. Steel, Plastics, Chemicals etc. should be reduced to nil as finished goods in most cases are already at nil rate

A list-based exemption or a special scheme for hardware manufacturing may be considered

Uniform Excise duty on all IT products (HSN 8471; 8473.30) at 8% Essential for combating Grey Market: 35% of PC market is grey through

excise and sales tax evasion (Total unorganised market is 53 % of PC market)

Essential to bring down the price of IT products Loss of revenue in initial two years will be more than offset by volumes

generated in the third year

11

Remove 4% Special Additional Duty (SAD) Increase the rate of depreciation on IT products/PC (HSN 8471)

to 100% from existing 60% This will enable Small and Medium Enterprises to invest in IT and stay

competitive Businesses can donate used IT products to schools/colleges as book

value after one year will be nil

What we need from the Ministry of Finance

12

Simplification of procedures for exports and imports Clearance time for imports (from landing to physical clearance)

and exports (from bonded premises to vessel) should be reduced from existing average 7 days to 6 hours

Self declaration based clearance for all IT/electronics products for exports and imports

Customs to work 2 shiftsX365 in at least 4 metros (airports and seaports) and Bangalore, Hyderabad and Goa

Cooling off period of 24 hours to be discontinued for exports6.

What we need from the Ministry of Finance

13

Arrival

No movement to Customs shed (except for random inspection of some shipments)

Received by importer

Arrival process No wait points for goods - ZERO turnaround time for goods clearance!

Update IGM no and other details as available

Audit and closure

Post clearance process As these are post clearance time for these does not impact TAT

Direct removal from aircraft !

At end of specified period, file periodic bill of entry with full details, exact duties calculated etc

Actual duty paid as per the periodic bill of entry

Pre-arrival process Carried out in advance, does not impact clearance TAT

Preliminary bill of entry prepared as per pre-alerts

File advance preliminary entry

Pre-deposit of duty of agreed value

System clears most shipments for release on preliminary entry

What we need from the Ministry of Finance Proposed model for Imports clearance:

14

Simplification of procedures for Excise Duty Set the rules for transaction value concept for assessment, as currently

there is tremendous interpretation issues with different authorities. Monthly payment of Excise duty in place of fortnightly payment. No Bond (of exports value) in case the exporter has received advance

payment for exports or has confirmed LC. The bond is not lifted even after the export obligations are met and the

export realization is completed. The Bond is lifted only after the closure of advance licenses.

There should be time limit to close all assessments and appeals say 2 years

There should be settlement commission for excise Follow the Income tax model

What we need from the Ministry of Finance

15

Create Manufacturing Zones: Island of Infrastructure Excellence

Option –I: DTA Scheme: ICT Habitats Permit duty free import of:

Raw materials including dual usage items All Capital goods No restrictions on Sales into DTA or for Exports Nil Corporate tax for 10 years to encourage IT manufacturing Existing units should be allowed to freely convert to new scheme

orOption –II: Modification of EHTP to encourage manufacturing and exports: No NFEP and Export performance (EP) conditions No physical bonding; all clearances on basis of self declaration Unlimited DTA access on payment of full applicable duties

What we need from the Ministry of Finance

16

Encouraging indigenous R&D Corporate Income Tax exemption on royalties from licensing of

Technology and Intellectual Property Amend bilateral treaties for removal of withholding tax on

Technology exports/imports: Germany - 10%; USA-15%; Japan - 20%

popularise products developed in India by exempting them from all local levies

Nil Sales tax (local and Central) on all IT/electronics products for at least two years

Encouraging IT Maintenance industry No Service Tax on AMC (Annual Maintenance Contact)

What we need from the Ministry of Finance

17

Banking and Finance Related: The banking appraisal process should take into account the latest

audited results of the company, whether half year, or quarterly or

yearly along with results of the previous two financial year Currently results of only the last financial year are taken into

consideration.

Margin money paid on LC or BGs should be given the same rate of

interest as that of cash credits operated with the same bank.

Alternatively, the banks can mark a lien to the extent of margins on

the customer’s cash credit accounts.

In cases where importers have to take a constructed bill of entry

from customs; LC opened by the authorized dealer should be

accepted as proof of payment already made against the original Bill

of Entry.

What we need from the Ministry of Finance

18

Improving IT penetration:

Increased Government spend on IT consumption

Government purchase/price preference for IT products

made/assembled in India irrespective of the origin of the company

Ensure Central and State Governments actually spend 3% of

their Budget on IT

Sales of IT products to educational institutions should be exempted

of all local levies

Permit PF loan/withdrawal for purchase of PC (at least one per

individual)

What we need from the Ministry of Finance

19

Create a conducive Investment Climate for IT manufacturing

Permit 100% foreign equity for investment in IT manufacturing

currently limited to designated schemes

Aggressive Industry-Government collaboration to market India

and attract Investment - set annual targets

Permit 100% exports remittance to be banked in foreign currency

What we need from the Ministry of Finance

20

Net Impact: 2005

PC volumes will reach 10 million from current 1.8 million PC penetration will be 26 per 1000 from current 6 per thousand

at par with the existing world average of 26 /1000 Excise Duty and sales tax collection in 2005 will more than offset the

cumulative revenue loss due to nil rate in 20002-03 and 2003-04 The industry will reach a critical mass: entire value chain will flourish

Volumes will lead to ancilliariasation Consumption of basic raw material produced in India will increase Increased employment opportunities for semi-skilled: 5 million new jobs

Confidence of the manufacturing industry will soar - more exports focus: Target USD Bn 5 in hardware and designs

Only bold steps will lead to dramatic results!

21

A High-Tech perspective of a new direction to an old system ……….

Lets MAke IT happen…..

Impact of 8% Excise and Nil Sales Tax Under Current duty structure: Excise Duty: 16%; Sales Tax: 4%

2001-02 2002-03 2003-04 2004-05

PC Volumes (Mn) 2.45 3.18 4.14 5.38

Growth Rate 30% 30% 30% 30%

PC Penetration per 1000 8 11 15 20

PC Price Reduction - 5% 10% 10%

Excise Duty (Rs.Crs.) 513 633 741 866

Sales Tax (Rs. Crs.) 149 184 215 215

2002- 05

Cumulative

2,240

650

2001-02 2002-03 2003-04 2004-05

PC Volumes (Mn) 2.45 3.92 6.27 9.72

Growth Rate 30% 60% 60% 55%

PC Penetration per 1000 8 11.5 17 26

PC Price Reduction - 15% 10% 6%

Excise Duty (Rs.Crs.) 513 611 879 1,227

Sales Tax (Rs. Crs.) 149 Nil Nil 662

2002- 05

Cumulative

2,717 (+21%)

662 (+2%)

Recommended: a) 8% Excise Duty b) Nil Sales Tax for Next 2 years i.e. 2002-04

(Annexure-I )

2,240

650

Related Documents