Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Bizsol UPDATE August - 2012

Pranab Mukherjee, the quintessential product of

Indian politics has now become the new tenant of

Raisina Hills earning his well deserved retirement

benefits after more than four decades in politics.

Mukherjee while taking oath of the office of the

President of India was dressed in an impeccable Nehru

jacket casting aside his drab and ill-fitting safari suits.

The sartorial shift was perhaps to signal to the world

that he is now an elder statesman than a mere

politician. Be that as it may, the photo op provided by

the previous incumbent and the new President was

indeed a study in contrast. There have been Presidents

and Presidents in Rashtrapati Bhavan, twelve of them

in all before Pranab Mukherjee - some were garrulous,

some cantankerous and some plainly difficult. But none

a non-entity like Madam Pratibha Patil. She can be a

proud mother who facilitated the process of

establishing her son as an MP and an equally proud

wife who used her influence to clean up the Augean

Stables at Amravati, her home town during her tenure

washing the taint of corruption involving some local co

operative societies and her family. Just as one thought

that we had an eminently forgettable presidential term

for the last five years, here comes the news that

mementos and memorabilia received during her tenure

are being carted away from Delhi to Amravati! She

could definitely be more graceful and spared this

embarrassment to the nation.

The spectre of industrial unrest looms large in the

industrial scene in the country for sure. It may not be

surprising to see the rise of this phenomenon given

the economic and social changes taking place around

us. Whenever there are perceived inequities in the

system there would be backlash in the name of

socialism or communism especially in an environment

where governance has come to a standstill, corruption

rules supreme, the rich has no qualms about obscene

exhibition of their wealth coupled with back-breaking

E D I T O R I A L

inflation. In these days of crony capitalism it is not

surprising that the common man whom the working

class in a way represents rise in revolt. No one justifies

violence as a means to settle any issue; but you cannot

run away from the fact that the disposed has no other

weapon in hand to fight the high and mighty. The irony

that the industrial unrest has happened in a Japanese

firm is not lost on anyone. The Japanese workers are

known to be the most peaceful, productive and

proactive the world over. But then this unrest was

something waiting to happen. At the Manesar plant of

Maruti Suzuk,i when the last strike was broken by the

management by literally and officially bribing the union

leaders, the issue involved was not only of corporate

governance but also about a lack of foresight on the

part of the management. When the union leaders were

paid amounts upwards of forty lakhs to leave there

were no takers to the management posturing that it

was simply a case of a generous compensation for

separation of some recalcitrant workmen. The amount

was obscenely high and the practice was without doubt

reprehensible. Here is the classic case of sacrificing

the long term interest of the company for short term

benefits and now the chickens have come home to

roost. There is also another lesson in all these mess.

Over time industrial relations initiatives have given way

to more fashionable human relations exercises

forgetting the fact that the former is an integral part of

the latter. It is time that the corporates and the institutes

realise that it is far more important to develop healthy

human relations on the shop floor before embarking

on jargon crunching notwithstanding the fact that the

latter looks more fashionable on company brochures.

When Obama hit the campaign trail for his

Presidential elections due in November this year, one

of the first to take him seriously were the Indians. He

criticised India for not being fast enough to usher in

further reforms. The political parties were so incensed

that even the ruling party and opposition came together

to condemn him. It was a display orchestrated

nationalism at its best. He raised just the same issues

and concerns which both the Congress and the BJP

had been raising all along. In fact the only person who

could have taken umbrage, if at all, was Mamta

Banerjee who had been successfully scuttling anything

which the Left would not like even at the cost of national

interest. Sometimes our attitude is so churlish that

2

Bizsol UPDATE August - 2012

i i i

when the Time magazine put Man Mohan Singh on its

cover and called him an under achiever, Outlook

magazine responded by putting Obama on its cover

and called him an under achiever! When would we

grow up?

The big news for us Indians from London

Olympics is that Suresh Kalmadi is not representing

India at the opening ceremony. Thank God that he did

not. I am not prejudging his guilt nor am I prejudiced.

Ethically it is just not right. Kalmadi may say that he

has the right to be there representing Indian Olympic

Association; he may be right legally. What is legally

right need not necessarily be morally right. The

organisers at the London Olympics had to confront

with a similar dilemma when the Chinese and Korean

teams connived to throw away their badminton

matches by playing to lose achieve a better medals

tally. The organisers showed the guts and gumption

to throw out the erring teams. London games would

be remembered more for this act on the part of the

organisers than anything else. In sports you don't

meddle with sportsman spirit, however unfashionable

the concept be. Staying with the London Olympics,

the opening ceremony was indeed a great

organisational feat especially after Beijing Olympics.

There may not be another event like the one we saw

at the opening ceremony at Beijing both in terms of

money spent and the spectacular display by those who

participated. It was simply awesome. If Beijing

Olympics had spectacular electronics London

Olympics had a soul. Indeed, human ingenuity knows

no boundary.

In this busy season of elections and Olympics and

Anna Hazare's periodical ritual fasting, it is easy to

forget the names of two legends who passed away.

One was Rajesh Khanna. When Rajesh Khanna died,

a part of me died. It is not a sentimental eulogy for the

yester year super star. For my generation he was the

hero of our dreams. I still do not know why I feel a

sense of loss, especially since he was around all these

years without affecting your lives in any which way.

One lesson you can cull out from his life is that the tag

of collective worship of celluloid heroes has an expiry

date. Being the first super star he did not know it and

we did not remember it either. The other person who

passed away recently was a man called Gore Vidal.

He may not familiar to many in India; but was feared

and grudgingly respected as an author and critic in

the US. He was perhaps the first acerbic critic who

made irreverence both civil and fashionable. The felicity

with which he wrote and the tongue-in-cheek

comments he produced inspired and chastened at the

same time more than a generation. In fact I am an

abashed admirer of his writing and had always been

amazed by his wit and wisdom.

Even as I am writing this piece Anna Hazare has

announced his intention to enter politics after his latest

round of fast ended in failure. The reactions about his

decision to enter politics are mixed. The experts say it

is not possible to launch an all India political outfit. The

people want a genuine alternative. The sad part is that

Team Anna is entering the political arena with their

reputation in tatters and their credibility at its nadir - a

tragic story of a genuine and timely social movement

about to be hijacked by vested interest groups to

unchartered territories.

Sushil Kumar Shinde is the new Home Minister of the

country. It only means one of the two possibilities. One,

there is an absolute dearth talent in India at ministerial

level. Or it means that servitude to the ruling

dispensation is the only qualification required to occupy

important positions of power in India. Either way it does

not augur well for the country. But then, for our own

safety and security he has to succeed as the Home

Minister. The nation should take a lesson from the

Karnataka Government. Organise mass scale prayers

spending crores of rupees propitiating the Gods to save

us - and Mr. Shinde also in the process.

Thank you

Venkat R. Venkitachalam

3

Bizsol UPDATE August - 2012

CUSTOMS

Anti Dumping

• Antidumping duty imposed vide Notification No.

33/2008-Customs, dated the 11th March, 2008,

on Acetone, originating in, or exported from,

European Union, Chinese Taipei, Singapore,

South Africa and the United States of America,

by one more year, i.e. upto and inclusive of 18th

June, 2013 [Notification No. 37/2012-CUS

(ADD) Dated 19.07.2012]

• Definitive antidumping duty on the imports of

'Grinding media Balls' (excluding Forged Grinding

Media Balls), originating in, or exported from

Thailand and China PR has been imposed for

period of five years [Notification No. 36/2012-

CUS (ADD) Dated 16.07.2012]

• Provisional antidumping duty on imports of vitrified

and porcelain tiles, falling under Chapter 69

originating in or exported from China PR and

United Arab Emirates (UAE) has been imposed.

[Notification No. 35/2012-CUS (ADD) Dated

10.07.2012]

• Definitive anti-dumping duty on import of Soda

ash, originating in or exported from People's

Republic of China, European Union, Kenya, Iran,

Pakistan, Ukraine and United States of America

has been imposed for period of five years.

[Notification No. 34/2012-CUS (ADD) Dated

03.07.2012]

Safeguard Duty

• No new notification!!

Tariff

• The full exemption from customs duty on "Raw

Sugar", "Refined or White Sugar" and "Raw

Sugar" of Chapter Heading 1701 of Customs

Tariff, if imported by a bulk consumer, has been

increased to 10% w.e.f. 13th Jul 2012. Further,

the goods of the Customs Tariff Head 7225 30

90, 7225 40 19, 7225 50 and 7225 99 00 are also

included in the exemption notification 12/

2012CUS dated 17th Mar 2012. Further, the

clause (b) of the proviso to the principal exemption

notification 12/2012CUS dated 17th Mar 2012 has

been omitted. [Notification NO. 45/2012-CUS

Dated 13.07.2012]

• Notification NO. 92/2009-CUS, 93/2009-CUS, 94/

2009-CUS, 95/2009-CUS and 104/2009-CUS all

Dated 11th Sep 2009 have been amended to give

effect of exemptions from Central Excise duty for

clearances against duty credit scrips of FPS, FMS,

Agri. Infrastructure Incentive, VKUG and SHIS.

[Notification NO. 44/2012-CUS Dated 9.7.2012]

Non-Tariff

• Tariff value for Brass Scrap (all grades), Poppy

Seeds, Gold & Silver has been revised.

[Notification No. 66/2012-CUS (N.T.) Dated

31.07.2012, [Notification No. 65/2012-CUS

(N.T.) Dated 26.07.2012 and 58/2012-CUS (N.T.)

Dated 13.07.2012]

• Customs Notification No. 62/1994-Customs (N.T.)

dated the 21st November, 1994, has been

amended to give effect of change of name of

"Dabhol Power Project" as "Ratnagiri Gas and

Power Pvt Ltd (RGPPL)". Furhter, "Unloading of

liquefied natural gas and naptha" has also been

included in the activities to be undertaken at

"Dabhol Port". [Notification 57/2012-CUS (N.T.)

Dated 11.07.2012]

Circulars

• Board has given the clarification on the exemption

of the sports utility goods. In this it is clarified that

the sport equipment covered here includes its

spares, accessories and consumables. Hence it

could be concluded that the scope of coverage

4

Bizsol UPDATE August - 2012

of goods under the category 'sports goods, sports

equipment, sports requisites' is comprehensive.

The said exemption entry is subject to specific

conditions such as production of certificate from

specified sports bodies/federations for its usage

in National or International championship or

competition and an undertaking from the importer

that the said goods are required for the intended

purpose of use. There is no distinction between

mandatory or optional accessory for inclusion or

exclusion in the exemption notification. Further

there is no distinction between general purpose

equipment or specialized equipment to the extent

it is a sport equipment for extending the

notification benefit. Apparently it excludes only

those types of equipments which are general

purpose machines. [Circular No. 20 / 2012 -

Customs Dated 27.07.2012.]

• Changes in the Foreign Trade Policy 2009-14

issued vide Annual Supplement dated 5.6.12, are

summarized and highlighted, in the said circular

and same has not been repeated since it was

covered in our earlier Bizsol Update. [Circular

No. 20 / 2012 - Customs Dated 27.07.2012.]

• Mouse pad will not be classified as parts or

accessories of computer mouse falling under

chapter heading 8471 but it will get classified

based on Constituent material, i.e. article of plastic

or article of rubber. [Circular No. 19 / 2012 -

Customs Dated 11.07.2012]

• Professional equipment includes Ambulance,

Sewage Disposal Truck, Refuse Disposal Vehicle

and specified in Circular No. 38/2010-Customs,

dated 27.09.2010 and also includes those which

are pre-designed structurally and pre-fitted with

relevant devices and mechanisms and all are

permitted to import under SFIS scrip. [Circular

No. 18 / 2012 - Customs Dated 05.07.2012]

• Scrips which are issued manually but not

registered with Customs will continued to be

verified by Customs for genuineness of scrips.

[Circular No. 17 / 2012 - Customs Dated

05.07.2012]

Instructions

• No new instructions!!

CENTRAL EXCISE

Tariff

• The goods cleared against a Status Holder

Incentive Scheme duty credit scrip issued for the

exports made during 2009-10 to 2012-13 are

exempted from payment of the Central Excise

duty & Additional Duties of Excise (Goods of

Special Importance) Act, 1957 & Additional Duties

of Excise (Textiles and Textile Articles) Act, 1978,

subject to actual user conditionand fulfillment of

other conditions & procedure mentioned in the

Notification [Notification No. 33/ 2012 - CE dated

9th July, 2012]

• The goods cleared against a VisheshKrishi and

Gram UdyogYojana (Special Agriculture and

Village Industry Scheme) are exempted from

payment of the Central Excise duty & Additional

Duties of Excise (Goods of Special Importance)

Act, 1957 & Additional Duties of Excise (Textiles

and Textile Articles) Act, 1978, subject to

fulfillment of conditions & procedure mentioned

in the Notification. [Notification No. 32/2012 - CE

dated 9th July, 2012]

• The capital goods viz; Cold storage units,

Precooling Units and Mother Storage Units for

Onions. the Pack House equipments notified in

Appendix 37 F of Hand Book of Procedures and

Reefer Van or Containers are exempted from

payment of Central Excise duty & Additional

Duties of Excise (Goods of Special Importance)

Act, 1957 & Additional Duties of Excise (Textiles

and Textile Articles) Act, 1978, when cleared

against Agri. Infrastructure Incentive Scrip, subject

to fulfillment of conditions mentioned therein.

[Notification No. 31/2012 - CE dated 9th July,

2012]

• The goods cleared against a Focus Market

Scheme are exempted from payment of the

Central Excise duty & Additional Duties of Excise

(Goods of Special Importance) Act, 1957 &

Additional Duties of Excise (Textiles and Textile

Articles) Act, 1978, subject to fulfillment of

conditions & procedure mentioned in the

Notification. [Notification No. 30/ 2012 - CE

dated 9th July, 2012]

5

Bizsol UPDATE August - 2012

The above exemptions under duty credit scrips

are subject to following conditions& procedure,

a. that the said scrip is registered with the

Customs authority at the port of registration

(hereinafter referred as the said Customs

authority);

b. that the holder of the scrip, who may either

be the person to whom the scrip was

originally issued or a transferee-holder,

presents the said scrip to the said Customs

authority along with a letter or proforma

invoice from the supplier or manufacturer

indicating details of its jurisdictional Central

Excise Officer (hereinafter referred as the

said Officer) and the description, quantity,

value of the goods to be cleared and the

duties leviable thereon, but for this

exemption;

c. The said Customs authority, taking into

account the debits already made towards

imports under respective Notification and this

exemption, shall debit the duties leviable, but

for this exemption in or on the reverse of the

said scrip and also mentions the necessary

details thereon, updates its own records and

sends written advice of these actions to the

said Officer;

d. At the time of clearance, the above scrip

debited by the Customs authority is

presented to the Jurisdictional Central Excise

Officer of supplier along with an undertaking

by the buyer addressed to the Central Excise

Officer

e. Based on the said written advice and

undertaking, the jurisdictional central excise

Officer will endorse the clearance particulars

and validates, on the reverse of the said

scrip, the details of the duties leviable, but

for this exemption, which were debited by

the said Customs authority, and keeps a

record of such clearances;

f. The manufacturer/supplier retains a copy of

the said scrip, debited by the said Customs

authority and endorsed by the said Officer

and duly attested by the holder of the scrip,

in support of the clearance under this

notification;

g. Holder of the scrip, to whom the goods were

cleared, shall be entitled to avail the

drawback or CENVAT credit of the duties of

excise leviable under the First Schedule and

the Second Schedule to the Central Excise

Tariff Act, 1985 (5 of 1986), section 3 of the

Additional Duties of Excise (Goods of Special

Importance) Act, 1957 (58 of 1957) and

section 3 of the Additional Duties of Excise

(Textiles and Textile Articles) Act, 1978 (40

of 1978), against the amount debited in the

said scrip and validated at the time of

clearance.

Non-Tariff• No new Notification

SERVICE TAX• Service rendered by Directors to the companies

will be covered under the reverse charge. In other

words, the companies will be required to pay

service tax on the director remuneration under

reverse charge on 100% basis [Notification No.

45/2012 - Service Tax dated 7th Aug 12]

• Security service rendered by Individual / HUF /

Partnership to Body Corporate has also been

under Reverse Charge. Further the definition of

Security Service has been added in the service

tax rules. [Notification No. 45 & 46 /2012 -

Service Tax dated 7th Aug 12]

• Services by way of slaughtering of all animals is

now exempted. [Notification No. 44 /2012 -

Service Tax dated 7th Aug 12]

• The services provided by the India Railway for

transportation of passengers in 1st class & AC

coach & goods are exempted from payment of

service tax upto 30.09.2012. [Notification No. 43/

2012-ST dated 02.07.2012]

Circulars

• Clarification on service tax on remittances has

been issued as there is no service tax per se on

the amount of foreign currency remitted to India

from overseas and any fee or conversion charges

are levied for sending such money and the Indian

counterpart bank or financial institution who

charges the foreign bank or any other entity for

the services provided at the receiving end, are

not liable to service tax. [Circular No. 163/14/

2012 dated 10-07-2012]

6

Bizsol UPDATE August - 2012

• Clarification on Point of Taxation Rules

Issue Clarification

Point of taxation and the rate applicable in

respect of continuous supply of services at the

time of change in rates effective from

01.04.2012;

There will be no change in point of taxation for

continuous supply service, The continuous supply of

services was governed by rule 6 until 31.03.2012. The rule

started with the wordings "notwithstanding anything

contained in rules 3, 4 …" Therefore, the point of taxation in

respect of services provided in terms of the said rule on or

before 31.03.2012 would remain unaffected by change in

rates.

Applicability of the revised rule 2A of the Service

Tax (Determination of Value) Rules, 2006 to

ongoing works contracts for determination of

value when the value was being determined

under the erstwhile Works Contract

(Composition Scheme for Payment of Service

Tax) Rules, 2007

The following would be changes in effective rate of tax:-

(i) the change in the portion of total value liable to tax in

respect of works contract other than original works (from @

4.8% earlier to @ 12% on 60% of the total amount charged,

or effectively @ 7.2% now).

(ii) exemption granted to certain works contracts w.e.f. 1st

July 2012 which were earlier taxable.

(iii) taxability of certain works contracts which were hitherto

exempted.

(iv) change in the manner of payment of tax from composition

scheme under the Works Contract (Composition Scheme

for Payment of Service Tax) Rules, 2007 to payment on

actual value under clause (i) of rule 2A of the Service Tax

(Determination of Value) Rules, 2006.

However, the following will not be a change in effective

rate of tax:-

(i) works contracts earlier paying service tax @ 4.8% under

Works Contract (Composition Scheme for Payment of

Service Tax) Rules, 2007 and now required to pay service

tax @12% on 40% of the total amount charged, keeping the

effective rate again at 4.8% (as only the manner of

expression has been altered).

(ii) works contracts which were outside the scope of taxation

(and not merely exempted) but have become now taxable

e.g. construction of residential complex comprising of 2 to

12 residential units, construction of buildings meant for use

by NGOs etc. (Rule 5 of the Point of Taxation Rules, 2011

shall apply to such services.)

Thus the point of taxation for services provided in respect of

taxable works contracts in progress on 01.07.2012 would

need to be determined under rule 4 of the Point of Taxation

Rules unless there is no change in effective rate of tax.

7

Bizsol UPDATE August - 2012

Applicability of partial reverse charge provisions

in respect of specified services

It is further clarified that the provisions of partial reverse

charge would also be applicable in respect of such services

where point of taxation is on or after 01.07.2012 under the

applicable rule in respect of the service provider.

[Circular No. 162/13/2012 dated 06-07-2012]

• Accounting Code for payment of service tax under the Negative List approach to taxation of services, with

effect from the first day of July 2012:

Name of ServicesAccounting codes

Tax collection Other Receipts Penalties Deduct refunds

00441089 00441090 00441093 00441094All Taxable

Services

NOTE: (i) service specific accounting codes will also continue to operate, side by side, for accounting of service

tax pertaining to the past period (meaning, for the period prior to 1st July, 2012); (ii) Primary Education Cess on

all taxable services will be booked under 00440298 and Secondary and Higher Education Cess on all taxable

services will be booked under 00440426; (iii) a new sub-head has been created for payment of "penalty"; the

sub-head "other receipts" is meant only for payment of interest etc. leviable on delayed payment of service tax;

(iv) the sub-head "deduct refunds" is not to be used by the assessees, as it is meant for use by the Revenue/

Commissionerates while allowing refund of tax. [Circular No. 161/12/2012 dated 06-07-2012]

FOREIGN TRADE POLICY

Notifications

• Description of ITC HS Codes 2402, 2601,7404, 7802 has been modified as under

Exim Code Item Description (Current) Exim Code Item Description (Amended)

2402 20 Cigarettes, containing tobacco: 2402 20 Cigarettes, containing tobacco:

2402 20 10 Other than filter cigarettes, of length not

exceeding 60 millimetres

2402 20 10 Other than filter cigarettes, of length not

exceeding 65 millimetres

2402 20 20 Other than filter cigarettes, of length

exceeding 60 millimetres but not exceeding

70 millimetres

2402 20 20 Other than filter cigarettes, of length

exceeding 65 millimetres but not exceeding

70 millimetres

2402 20 30 Filter cigarettes of length (including the

length of the filter, the length of filter being

11 millimetres or its actual length, whichever

is more) not exceeding 60 millimetres

2402 20 30 Filter cigarettes of length (including the

length of the filter, the length of filter being

11 millimetres or its actual length, whichever

is more) not exceeding 65 millimetres

2402 20 40 Filter cigarettes of length (including the

length of the filter, the length of filter being

11 millimetres or its actual length, whichever

is more) exceeding 60 millimetres not

exceeding 70 millimetres

2402 20 40 Filter cigarettes of length (including the

length of the filter, the length of filter being

11 millimetres or its actual length, whichever

is more) exceeding 65 millimetres not

exceeding 70 millimetres

8

Bizsol UPDATE August - 2012

Exim Code Item Description (Current) Exim Code Item Description (Amended)

Iron ores and concentrates, other than

roasted iron pyrites:Iron ores and concentrates, other than

roasted iron pyrites:

2601 11 Non-agglomerated: 2601 11 Non-agglomerated:

2601 11 10 Iron ore lumps (60% Fe or more) Iron ore lumps (60% Fe or more)

2601 11 20 Iron ore lumps (below 60% Fe, including

black iron ore containing upto 10% Mn)

2601 11 11 60% Fe or more but below 62% Fe kg. 10%

2601 11 40 Iron ore fines (below 62% Fe) 2601 11 19 65% Fe and above kg. 10%

Current description Amended description

2601 11 30 Iron ore fines (62% Fe or more) 2601 11 12 62% Fe or more but below 65% Fe kg. 10%

2601 11 90 Other 2601 11 21 below 55% Fe kg. 10%

2601 11 50 Iron ore concentrates Iron ore lumps (below 60% Fe, including

black iron ore containing up to 10% Mn)

2601 11 22 55% Fe or more but below 58% Fe kg. 10%

2601 11 29 58% Fe or more but below 60% Fe kg. 10%

Iron ore fines (62% Fe or more)

2601 11 31 62% Fe or more but below 65% Fe kg. 10%

2601 11 39 65% Fe and above kg. 10%

Iron ore Fines (below 62% Fe)

2601 11 41 below 55% Fe kg. 10%

2601 11 42 55% Fe or more but below 58% Fe kg. 10%

2601 11 43 58% Fe or more but below 60% Fe kg. 10%

2601 11 49 60% Fe or more but below 62% Fe kg. 10%

2601 11 50 Iron ore concentrates kg. 10%

2601 11 90 Others kg. 10%

9

Bizsol UPDATE August - 2012

Exim Code Item Description Exim Code Item Description

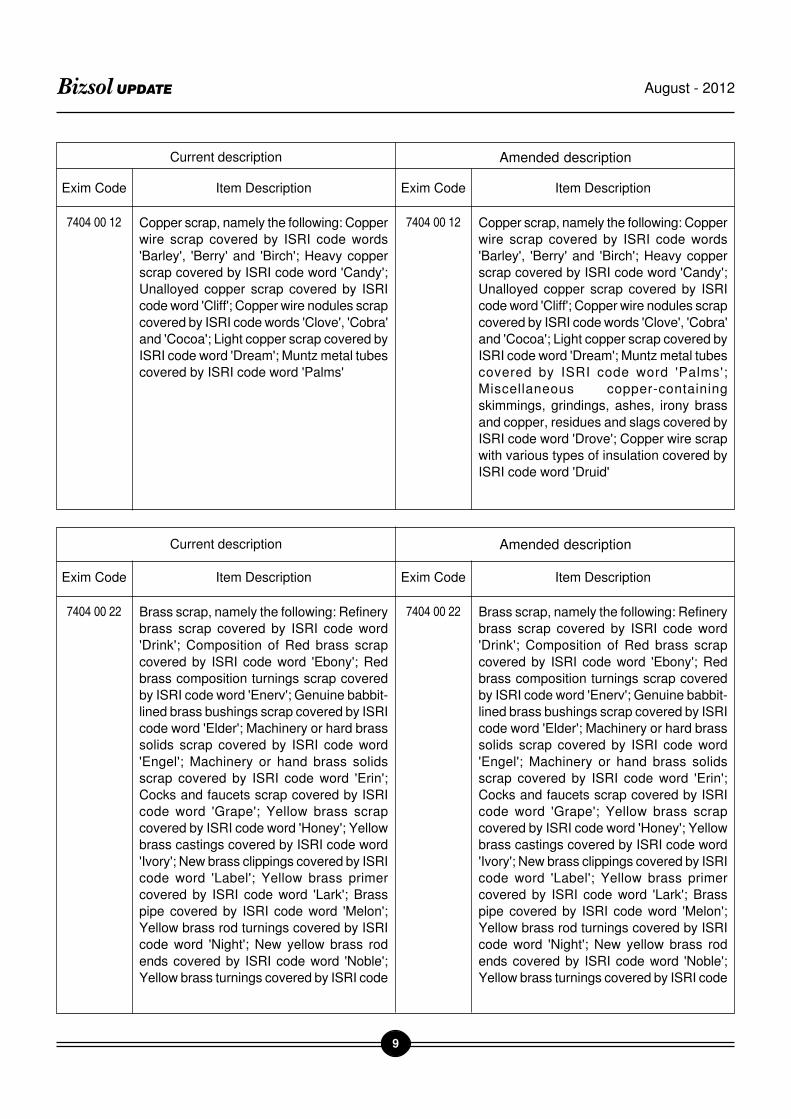

7404 00 12 Copper scrap, namely the following: Copper

wire scrap covered by ISRI code words

'Barley', 'Berry' and 'Birch'; Heavy copper

scrap covered by ISRI code word 'Candy';

Unalloyed copper scrap covered by ISRI

code word 'Cliff'; Copper wire nodules scrap

covered by ISRI code words 'Clove', 'Cobra'

and 'Cocoa'; Light copper scrap covered by

ISRI code word 'Dream'; Muntz metal tubes

covered by ISRI code word 'Palms'

7404 00 12 Copper scrap, namely the following: Copper

wire scrap covered by ISRI code words

'Barley', 'Berry' and 'Birch'; Heavy copper

scrap covered by ISRI code word 'Candy';

Unalloyed copper scrap covered by ISRI

code word 'Cliff'; Copper wire nodules scrap

covered by ISRI code words 'Clove', 'Cobra'

and 'Cocoa'; Light copper scrap covered by

ISRI code word 'Dream'; Muntz metal tubes

covered by ISRI code word 'Palms';

Miscellaneous copper-containing

skimmings, grindings, ashes, irony brass

and copper, residues and slags covered by

ISRI code word 'Drove'; Copper wire scrap

with various types of insulation covered by

ISRI code word 'Druid'

Current description Amended description

Exim Code Item Description Exim Code Item Description

7404 00 22 Brass scrap, namely the following: Refinery

brass scrap covered by ISRI code word

'Drink'; Composition of Red brass scrap

covered by ISRI code word 'Ebony'; Red

brass composition turnings scrap covered

by ISRI code word 'Enerv'; Genuine babbit-

lined brass bushings scrap covered by ISRI

code word 'Elder'; Machinery or hard brass

solids scrap covered by ISRI code word

'Engel'; Machinery or hand brass solids

scrap covered by ISRI code word 'Erin';

Cocks and faucets scrap covered by ISRI

code word 'Grape'; Yellow brass scrap

covered by ISRI code word 'Honey'; Yellow

brass castings covered by ISRI code word

'Ivory'; New brass clippings covered by ISRI

code word 'Label'; Yellow brass primer

covered by ISRI code word 'Lark'; Brass

pipe covered by ISRI code word 'Melon';

Yellow brass rod turnings covered by ISRI

code word 'Night'; New yellow brass rod

ends covered by ISRI code word 'Noble';

Yellow brass turnings covered by ISRI code

7404 00 22 Brass scrap, namely the following: Refinery

brass scrap covered by ISRI code word

'Drink'; Composition of Red brass scrap

covered by ISRI code word 'Ebony'; Red

brass composition turnings scrap covered

by ISRI code word 'Enerv'; Genuine babbit-

lined brass bushings scrap covered by ISRI

code word 'Elder'; Machinery or hard brass

solids scrap covered by ISRI code word

'Engel'; Machinery or hand brass solids

scrap covered by ISRI code word 'Erin';

Cocks and faucets scrap covered by ISRI

code word 'Grape'; Yellow brass scrap

covered by ISRI code word 'Honey'; Yellow

brass castings covered by ISRI code word

'Ivory'; New brass clippings covered by ISRI

code word 'Label'; Yellow brass primer

covered by ISRI code word 'Lark'; Brass

pipe covered by ISRI code word 'Melon';

Yellow brass rod turnings covered by ISRI

code word 'Night'; New yellow brass rod

ends covered by ISRI code word 'Noble';

Yellow brass turnings covered by ISRI code

Current description Amended description

10

Bizsol UPDATE August - 2012

Exim Code Item Description Exim Code Item Description

word 'Nomad'; Mixed unsweated auto

radiators covered by ISRI code word

'Ocean'; Admiralty brass condenser tubes

covered by ISRI code word 'Pales';

Aluminium brass condenser tubes covered

by ISRI code word 'Pallu'; Manganese

bronze solids covered by ISRI code word

'Parch'.

word 'Nomad'; Mixed unsweated auto

radiators covered by ISRI code word

'Ocean'; Admiralty brass condenser tubes

covered by ISRI code word 'Pales';

Aluminium brass condenser tubes covered

by ISRI code word 'Pallu'; Manganese

bronze solids covered by ISRI code word

'Parch'; High Grade-Low Lead Bronze/Brass

Solids covered by ISRI code word 'Eland';

High lead bronze solids and borings covered

by ISRI code word 'Elias'; Clean fired 70/30

brass shell cases free of primers and any

other foreign material covered by ISRI code

word 'Lace'; Clean fired 70/30 brass shell

cases containing the brass primers and

containing no other foreign material covered

by ISRI code word 'Lady'; Clean fired 70/30

brass shells free of bullets, iron and any

other foreign material covered by ISRI code

word 'Lake'; Clean muffled (popped) 70/30

brass shells free of bullets, iron and any

other foreign material covered by ISRI code

word 'Lamb'.

Current description Amended description

Exim Code Item Description Exim Code Item Description

Nickel scrap, namely the following:

New nickel scrap covered by ISRI code

word 'Aroma'; Old nickel scrap covered by

ISRI code word 'Burly'; New cupro nickel

clips and solids covered by ISRI code word

'Dandy'; Cupro nickel solids covered by ISRI

code word 'Daunt'; Soldered cupro-nickel

solids covered by ISRI code word 'Delta';

Cupro nickel spinnings, turnings, borings

covered by ISRI code word 'Decoy';

Miscellaneous nickel copper and nickel

copper iron covered by ISRI code word

'Depth'; New R-monel clippings solids

covered by ISRI code word 'Hitch'; New

mixed monel solids and clippings covered

by ISRI code word 'House'; Old monel sheet

and solids covered by ISRI code word 'Ideal';

k-monel solids covered by ISRI code word

Nickel scrap, namely the following:

New nickel scrap covered by ISRI code word

'Aroma'; Old nickel scrap covered by ISRI

code word 'Burly'; New cupro nickel clips

and solids covered by ISRI code word

'Dandy'; Cupro nickel solids covered by ISRI

code word 'Daunt'; Soldered cupro-nickel

solids covered by ISRI code word 'Delta';

Cupro nickel spinnings, turnings, borings

covered by ISRI code word 'Decoy';

Miscellaneous nickel copper and nickel

copper iron covered by ISRI code word

'Depth'; New R-monel clippings solids

covered by ISRI code word 'Hitch'; New

mixed monel solids and clippings covered

by ISRI code word 'House'; Old monel sheet

and solids covered by ISRI code word 'Ideal';

k-monel solids covered by ISRI code word

Current description Amended description

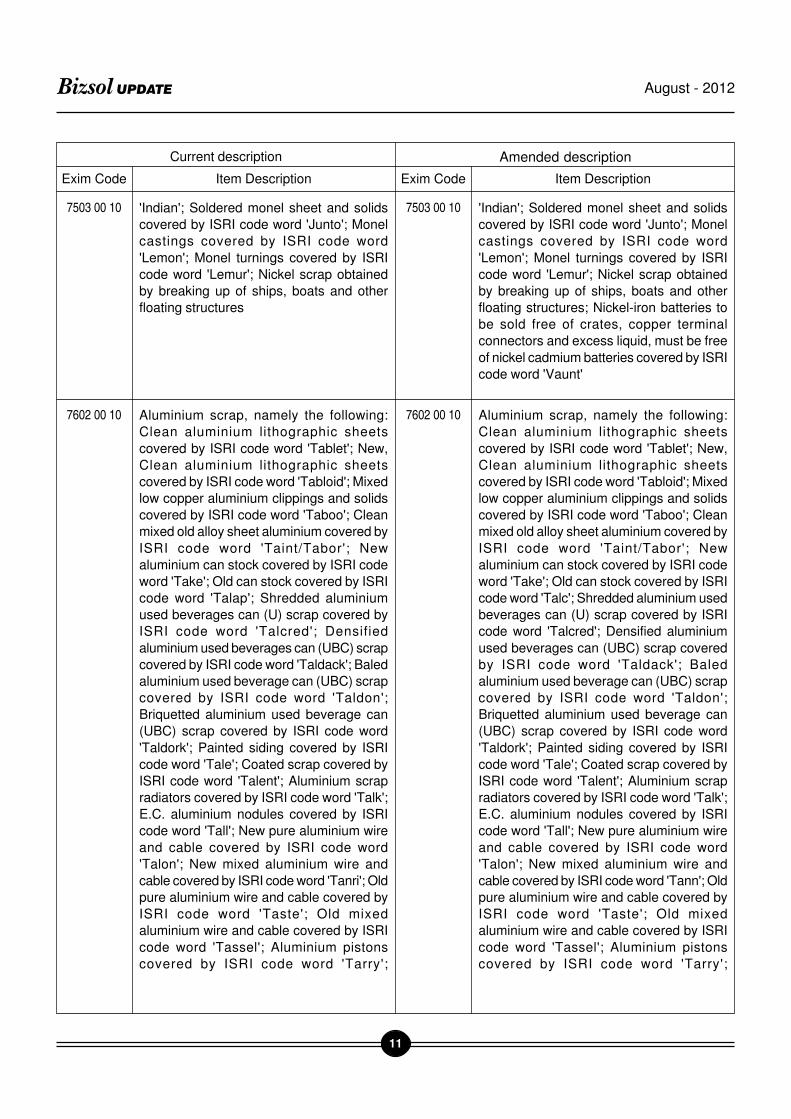

7503 00 10 7503 00 10

11

Bizsol UPDATE August - 2012

Exim Code Item Description Exim Code Item Description

'Indian'; Soldered monel sheet and solids

covered by ISRI code word 'Junto'; Monel

castings covered by ISRI code word

'Lemon'; Monel turnings covered by ISRI

code word 'Lemur'; Nickel scrap obtained

by breaking up of ships, boats and other

floating structures

'Indian'; Soldered monel sheet and solids

covered by ISRI code word 'Junto'; Monel

castings covered by ISRI code word

'Lemon'; Monel turnings covered by ISRI

code word 'Lemur'; Nickel scrap obtained

by breaking up of ships, boats and other

floating structures; Nickel-iron batteries to

be sold free of crates, copper terminal

connectors and excess liquid, must be free

of nickel cadmium batteries covered by ISRI

code word 'Vaunt'

Current description Amended description

7503 00 10

Aluminium scrap, namely the following:

Clean aluminium lithographic sheets

covered by ISRI code word 'Tablet'; New,

Clean aluminium lithographic sheets

covered by ISRI code word 'Tabloid'; Mixed

low copper aluminium clippings and solids

covered by ISRI code word 'Taboo'; Clean

mixed old alloy sheet aluminium covered by

ISRI code word 'Taint/Tabor'; New

aluminium can stock covered by ISRI code

word 'Take'; Old can stock covered by ISRI

code word 'Talap'; Shredded aluminium

used beverages can (U) scrap covered by

ISRI code word 'Talcred'; Densified

aluminium used beverages can (UBC) scrap

covered by ISRI code word 'Taldack'; Baled

aluminium used beverage can (UBC) scrap

covered by ISRI code word 'Taldon';

Briquetted aluminium used beverage can

(UBC) scrap covered by ISRI code word

'Taldork'; Painted siding covered by ISRI

code word 'Tale'; Coated scrap covered by

ISRI code word 'Talent'; Aluminium scrap

radiators covered by ISRI code word 'Talk';

E.C. aluminium nodules covered by ISRI

code word 'Tall'; New pure aluminium wire

and cable covered by ISRI code word

'Talon'; New mixed aluminium wire and

cable covered by ISRI code word 'Tanri'; Old

pure aluminium wire and cable covered by

ISRI code word 'Taste'; Old mixed

aluminium wire and cable covered by ISRI

code word 'Tassel'; Aluminium pistons

covered by ISRI code word 'Tarry';

Aluminium scrap, namely the following:

Clean aluminium lithographic sheets

covered by ISRI code word 'Tablet'; New,

Clean aluminium lithographic sheets

covered by ISRI code word 'Tabloid'; Mixed

low copper aluminium clippings and solids

covered by ISRI code word 'Taboo'; Clean

mixed old alloy sheet aluminium covered by

ISRI code word 'Taint/Tabor'; New

aluminium can stock covered by ISRI code

word 'Take'; Old can stock covered by ISRI

code word 'Talc'; Shredded aluminium used

beverages can (U) scrap covered by ISRI

code word 'Talcred'; Densified aluminium

used beverages can (UBC) scrap covered

by ISRI code word 'Taldack'; Baled

aluminium used beverage can (UBC) scrap

covered by ISRI code word 'Taldon';

Briquetted aluminium used beverage can

(UBC) scrap covered by ISRI code word

'Taldork'; Painted siding covered by ISRI

code word 'Tale'; Coated scrap covered by

ISRI code word 'Talent'; Aluminium scrap

radiators covered by ISRI code word 'Talk';

E.C. aluminium nodules covered by ISRI

code word 'Tall'; New pure aluminium wire

and cable covered by ISRI code word

'Talon'; New mixed aluminium wire and

cable covered by ISRI code word 'Tann'; Old

pure aluminium wire and cable covered by

ISRI code word 'Taste'; Old mixed

aluminium wire and cable covered by ISRI

code word 'Tassel'; Aluminium pistons

covered by ISRI code word 'Tarry';

7602 00 10 7602 00 10

7503 00 10

12

Bizsol UPDATE August - 2012

Exim Code Item Description Exim Code Item Description

Segregated aluminium borings and turnings

covered by ISRI code word 'Teens'; Mixed

aluminium castings covered by ISRI code

word 'Telic'; Mixed aluminium castings

covered by ISRI code word 'Tense';

Wrecked airplane sheet aluminium covered

by ISRI code word 'Tepid'; New aluminium

foil covered by ISRI code word 'Terse'; Old

aluminium foil covered by ISRI code word

'Testy'; Aluminium grindings covered by

ISRI code word 'Thigh'; Sweated aluminium

covered by ISRI code word 'Throb';

Segregated new aluminium alloy clippings

and solids covered by ISRI code word

'Tooth'; Mixed new aluminium alloy clippings

and solids covered by ISRI code word

'Tough'; Segregated new aluminium

castings, forgings and extrusions covered

by ISRI code word 'Tread'; Aluminium auto

castings covered by ISRI code word 'Trump';

Insulated aluminium wire scrap covered by

ISRI code word 'Twang'; Aluminium airplane

castings covered by ISRI code word 'Twist';

Fragmentizer aluminium scrap (from

automobile shredder) covered by ISRI code

word 'Twitch'

Segregated aluminium borings and turnings

covered by ISRI code word 'Teens'; Mixed

aluminium castings covered by ISRI code

word 'Telic'; Mixed aluminium castings

covered by ISRI code word 'Tense';

Wrecked airplane sheet aluminium covered

by ISRI code word 'Tepid'; New aluminium

foil covered by ISRI code word 'Terse'; New

aluminium foil covered by ISRI code

word 'Tetra'; Old aluminium foil covered

by ISRI code word 'Tesla'; Aluminium

grindings covered by ISRI code word 'Thigh';

Sweated aluminium covered by ISRI code

word 'Throb'; Segregated new aluminium

alloy clippings and solids covered by ISRI

code word 'Tooth'; Mixed new aluminium

alloy clippings and solids covered by ISRI

code word 'Tough'; Segregated new

aluminium castings, forgings and extrusions

covered by ISRI code word 'Tread';

Aluminium auto castings covered by ISRI

code word 'Trump'; Insulated aluminium wire

scrap covered by ISRI code word 'Twang';

Aluminium airplane castings covered by

ISRI code word 'Twist'; Fragmentizer

aluminium scrap (from automobile shredder)

covered by ISRI code word 'Twitch';

Aluminium auto or truck wheels covered

by ISRI code word 'Troma'; Fragmentizer

aluminium scrap from automobile

shredders covered by ISRI code word

'Tweak'; Burnt fragmentizer aluminium

scrap from automobile shredders

covered by ISRI code word 'Twire';

Shredded non-ferrous scrap (predomi-

nantly aluminium) covered by ISRI code

word 'Zorba'; Aluminium drosses,

spatterns, spellings, skimmings and

sweepings covered by ISRI code word

'Thirl'; New production aluminium

extrusions covered by ISRI code word

'Tata'; All aluminium radiators from

automobiles covered by ISRI code word

'Tally'; Aluminium extrusions '10/10'

covered by ISRI code word 'Toto';

Aluminium extrusions dealer grade

covered by the word 'Tutu'.

Current description Amended description

7602 00 10 7602 00 10

13

Bizsol UPDATE August - 2012

Exim Code Item Description Exim Code Item Description

Lead scrap, namely the following: Scrap

lead-soft covered by ISRI code word

'Racks'; Mixed hard or soft scrap lead

covered by ISRI code word 'Radio'; Lead

covered copper cable covered by ISRI code

word 'Relay'; Wheel weights covered by

ISRI code word 'Ropes'; Mixed common

babbit covered by ISRI code word 'Roses'

Lead scrap, namely the following: Scrap

lead-soft covered by ISRI code word

'Racks'; Mixed hard or soft scrap lead

covered by ISRI code word 'Radio'; Lead

covered copper cable covered by ISRI code

word 'Relay'; Wheel weights covered by

ISRI code word 'Ropes'; Mixed common

babbit covered by ISRI code word 'Roses';

Lead battery plates whether automotive,

industrial or mixed covered by ISRI code

word 'Rails'; Scrap drained/dry whole

intact lead covered by ISRI code word

'Rains'; Battery lugs free of scrap lead,

wheel weights, battery plates, rubber or

plastic case material and other foreign

material covered by ISRI code word

'Rakes'; Lead covered copper cable free

of armoured covered cable and foreign

material covered by ISRI code word

'Relay'; Lead dross covered by ISRI code

word 'Rents'; Scrap wet whole intact lead

batteries consisting of SLI (starting,

lighting and ignition), automotive, truck,

8-D and commercial golf cart and marine

type batteries covered by ISRI code word

'Rink'; Scrap industrial intact lead cells

consisting of plates enclosed by some

form of complete plastic case covered

by ISRI code word 'Rono'; Scrap whole

Intact Industrial Lead Batteries

Consisting of bus, diesel, locomotive,

telephone or steel cased batteries

covered by ISRI code word 'Roper'

Current description Amended description

7802 00 10 7802 00 10

• Export of edible oils in branded consumer packs

has been prohibited with immediate effect. Export

of the consignments handed over to the customs

up to 24.00 hrs on 01.08.2012 will be permitted.

[9 (RE-2012) / 2009-2014 dated 1st August

2008]

Public Notices

• Based on requests received from various

stakeholders for extension of the date of

mandatory issuance and transmission of

electronic BRC's on account of lack of readiness,

the existing system of physical BRC issuance from

bank will be continued up to 16.08.2012 for

smooth transition. [PUBLIC NOTICE NO. 08(RE-

2012)/2009-14 dated 6th July 2012]

• Additional quantity of 4,476 MTs of raw sugar is

permitted to be exported to USA under TRQ by

M/s. Indian Sugar Exim Corporation Ltd. This is

in addition to earlier 8,300 MTs allocated. [09(RE-

2012)/ 2009-2014 dated 6th July 2012]

• The requirement of affixing barcodes on

Secondary level and Primary level packaging was

14

Bizsol UPDATE August - 2012

to come into effect from 01.07.2012 and

01.01.2013 respectively. Now this time limit is

being extended by 6 months each. [10(RE-2012)/

2009-2014 dated 11th July 2012]

• One additional branch each at Bengaluru and

Hyderabad has been added for issuing Certificate

of Origin (Non Preferential) of Federation of Indian

Micro and Small & Medium Enterprises. [11(RE

2012)/2009-2014 dated 26th July 2012]

• Following changes have been made in HBoP V1

w.e.f. 5th June 2012 [12(RE 2012)/2009-2014

dated 26th July 2012]/

i Foreign Exchange earnings for Services

provided by Shipping Lines Service

Providers from plying from any country X to

any country Y routes; not touching India at

all will not be eligible for Served from India

Scheme.

i The validity of duty credit scrip issued under

Chapter 3 will be 18 months instead of 24

months.

i Export shipments filed under the Free

Shipping Bill category would require

declaration 'We intend to claim benefits

under Chapter 3.'

i Declaration of Intent will not be required for

export shipments under any of the schemes

of Chapter 4 (including drawback), Chapter

5 or Chapter 6 of FTP.

i Grace period of one month from the date of

decision/ notification/public notice will be

allowed for making the declaration of intent

in case of newly added Focus Product /

Market.

i Tondiarpet (TNPM), Chennai is added as

ICDs and Sea Ports Karaikal (Union territory

of Puducherry)

i Up to 10% of CIF value /duty saved amount

of EPCG authorization can be imported

without enhancement of value of the

authorization. Earlier it was only value.

i In case of Post Export EPCG Scheme, the

importer will require to pay excise duties in

cash.

i In case of post-export EPCG, the scrip will

be issued without considering CVD. In case

the exporter has not availed Cenvat Credit

then subject to certificate issued by

Jurisdictional Central Excise officer towards

non-availment of Cenvat credit. However

such certificate will not be required in case

of the unit is not registered with Central

Excise, or the unit has opted out of Central

Excise net or the end product is not subject

to Central Excise duty

• Description of Sl. No. 23 of General note for fuel

in HBP Vol. II has been amended to harmonize it

with SION C-593, as modified on 02.06.2011.

[13(RE 2012)/2009-2014 dated 30th July 2012]

Policy Circular

• The delay in registration has been condoned in

all cases where

- The vehicles imported prior to 31.08.2006

or

- Where the RTO gives a confirmation that the

imported vehicle is not allowed to be

registered as Tourist Vehicle. [2 (RE-2012)/

2009-14 dated 19th July 2012]

INCOME TAX

Notifications

• The agreement between Government of India and

Jerseyl for exchange of Information and

assistance in collection with respect to taxes

signed at London on 3rd day of November is

brought into force on 8th Day of May, 2012.

[NOTIFICATION NO. 26/2012 DATED 10/07/

2012]

• An Agreement and the Protocol between the

Government of the Republic of India and the

Government of the Republic of Estonia for the

Avoidance of Double Taxation and the Prevention

of Fiscal Evasion with Respect to Taxes on

Income was signed at Tallinn, Estonia, on 19th

day of September, 2011 was brought into force

on 20th June 2012. [NOTIFICATION NO. 27/2012

DATED 25/07/2012]

• An Agreement and the Protocol between the

Government of the Republic of India and the

15

Bizsol UPDATE August - 2012

Government of the Republic of Lithuania for the

Avoidance of Double Taxation and the Prevention

of Fiscal Evasion with Respect to Taxes on

Income and on Capital (DTAA) was signed at New

Delhi on 26th July, 2011was brought into force

on 10th July, 2012. [NOTIFICATION NO. 28/2012

DATED 25/07/2012]

Circulars

• It has been decided by the board that it will not

be mandatory for agents of non-residents and

private discretionary trust to file return of income

online even if their total income exceeds Ten Lakh

rupees. [CIRCULAR No. 6/2012 dated 03/08/

2012]

• Employees earning only Salary Income and

Interest from Savings bank Account less than

Rs. 10000/- and total income below Rs. 5 Lacs is

exempted from filing Return of Income, [Press

Release No. 402/92/2006-MC (15 of 2012),

dated 20-7-2012]

• Income Tax Department have started two more

tax payer friendly initiatives i.e. Tax R eturn

Preparere will assist assessee in solving their

online filing relating query either online or by

visiting their homes by charging a nominal fee as

prescribed. [Press Release, dated 24-7-2012]

• Individual and HUF having Total income

exceeding Rs. 10 lacs is compulsorily required to

e-file the return. However Digital signature is not

mandatory unless they are filing itr-4 or are

covered u/s 44AB. [PRESS RELEASE No. 402/

92/2006-MC (12 of 2012), dated 2-7-2012]

• Deductors must comply with their obligations to

ensure correct credit to persons from whom

Income Tax is deducted at source, failure of which

may lead to levy of penalty. [Press Release,

dated 10-7-2012]

• An expert committee on GAAR have constituted

to undertake stakeholder consultations and

finalise the guidelines for GAAR. [Press Release,

dated 13-7-2012]

VAT

Notifications

• No new Notifications.

Company Law:

Circulars:

• There will be no additional fees / penalty will be

charged for filing to file Balance Sheet and Profit

& Loss Account in XBRL mode for the financial

year commencing on or after 1.4.2011, upto 15h

November, 2012 or within 30 days from the date

of their AGM, whichever is later. [General

Circular No.16/2012 dated 6th July 2012]

• According to Investor Education & Protection

Fund (uploading of information regarding unpaid

and uncliamed amounts lying with companies)

Rules, 2012 the companies are required to file

the information in form 5 INV before cut-off date.

For the year 2010-11 the companies have to file

this form upto 31st July 2012 or within 90 days

from the date of AGM whichever is later and the

correct excel templete can be filed upto 31st Aug

2012. Further this Form 5 INV is required to file

by companies annually in one Form 5 INV

furnishing information of unpaid / unclaimed

amounts lying with companies as on the date of

AGM. [General Circular No.17/2012 dated 23rd

July 2012]

• As per General Circular No.8/2012 dated 10th

May 2012 it has already been mandated by the

Ministry of Corporate Affairs that all cost auditors

and the concerned companies shall file their Cost

Audit Reports and Compliance Reports for the

year 2011-12 onwards [including the overdue

reports relating to any previous year(s)] only in

the XBRL mode. For this purpose, the applicable

taxonomy, business rules, validation tools, etc.

and also the "Product Group" classification

required for preparing the cost audit reports and

compliance reports as per revised rules are under

preparation and would soon be made available

by the Ministry. Therefore there will be no penalty

charged for the filing of these reports for the year

2011-12(including for pending of previous years

16

Bizsol UPDATE August - 2012

reports) in XBLR mode upto 31st Dec 2012.

[General Circular No.18/2012 dated 26th July

2012]

• The extension for filling fee Form 23B (Information

by Statutory Auditor to the Registrar) without fees

is provided upto 5th Aug 2012. [Genereal

Circular No.19/2012 dated 27th July 2012]

Notifications:

• In supersession of earlier Limited Liability

Partnership(Winding up and Dessolution) Rules,

2010, Central Government makes the revised

rules known as Limited Liability Partnership

(Winding up and Dessolution) Rules, 2012

[Notification dated 10th July 2012]

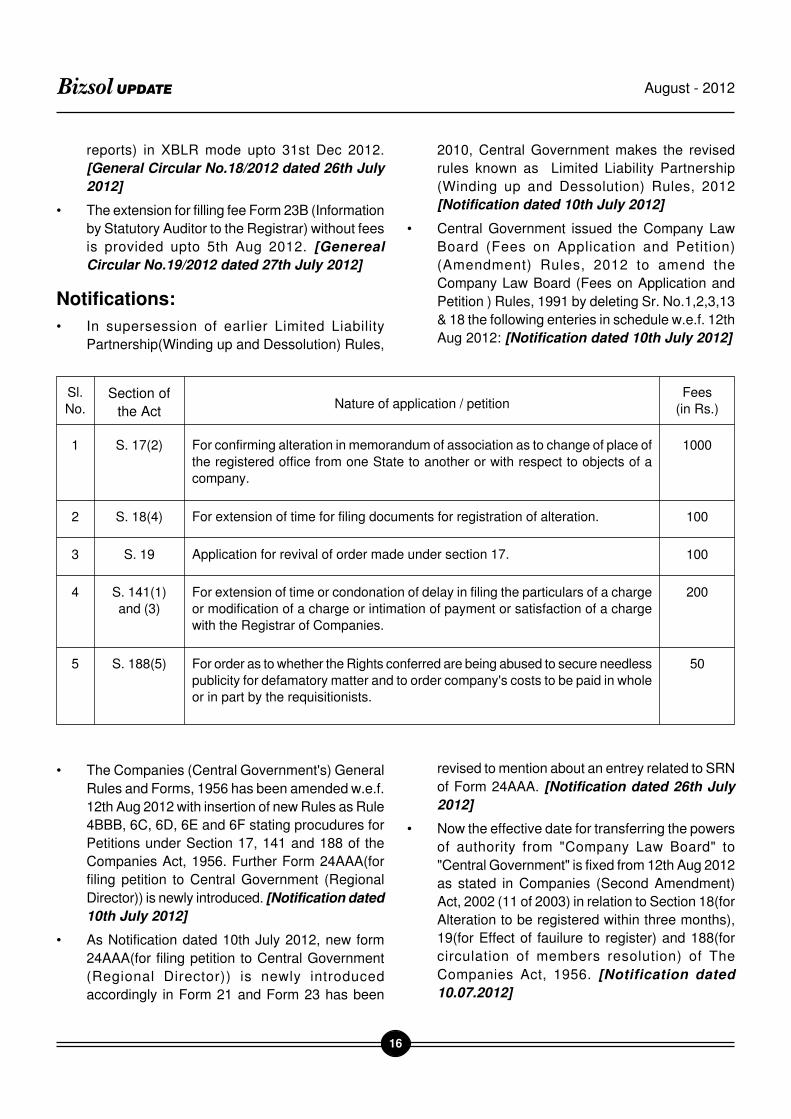

• Central Government issued the Company Law

Board (Fees on Application and Petition)

(Amendment) Rules, 2012 to amend the

Company Law Board (Fees on Application and

Petition ) Rules, 1991 by deleting Sr. No.1,2,3,13

& 18 the following enteries in schedule w.e.f. 12th

Aug 2012: [Notification dated 10th July 2012]

Sl.

No.Section of

the Act

Fees

(in Rs.)Nature of application / petition

1 S. 17(2) 1000For confirming alteration in memorandum of association as to change of place of

the registered office from one State to another or with respect to objects of a

company.

2 S. 18(4) 100For extension of time for filing documents for registration of alteration.

3 S. 19 100Application for revival of order made under section 17.

4 S. 141(1)

and (3)

200For extension of time or condonation of delay in filing the particulars of a charge

or modification of a charge or intimation of payment or satisfaction of a charge

with the Registrar of Companies.

5 S. 188(5) 50For order as to whether the Rights conferred are being abused to secure needless

publicity for defamatory matter and to order company's costs to be paid in whole

or in part by the requisitionists.

• The Companies (Central Government's) General

Rules and Forms, 1956 has been amended w.e.f.

12th Aug 2012 with insertion of new Rules as Rule

4BBB, 6C, 6D, 6E and 6F stating procudures for

Petitions under Section 17, 141 and 188 of the

Companies Act, 1956. Further Form 24AAA(for

filing petition to Central Government (Regional

Director)) is newly introduced. [Notification dated

10th July 2012]

• As Notification dated 10th July 2012, new form

24AAA(for filing petition to Central Government

(Regional Director)) is newly introduced

accordingly in Form 21 and Form 23 has been

revised to mention about an entrey related to SRN

of Form 24AAA. [Notification dated 26th July

2012]

• Now the effective date for transferring the powers

of authority from "Company Law Board" to

"Central Government" is fixed from 12th Aug 2012

as stated in Companies (Second Amendment)

Act, 2002 (11 of 2003) in relation to Section 18(for

Alteration to be registered within three months),

19(for Effect of fauilure to register) and 188(for

circulation of members resolution) of The

Companies Act, 1956. [Notification dated

10.07.2012]

17

Bizsol UPDATE August - 2012

FEMA/RBI

RBI Circulars July-2012

Circular

Number

Date of

IssueDepartment Subject Meant For

RBI/2012-2013/153

A.P.(DIR Series)

Circular No. 11

31.7.2012 Foreign

Exchange

Department

Foreign Exchange Management

Act, 1999 (FEMA) - Com-

pounding of Contraventions

under FEMA, 1999

All Category - I Authorised

Dealer Banks

RBI/2012-2013/152

A. P.(DIR Series)

Circular No. 13

31.7.2012 Foreign

Exchange

Department

Risk Management and Inter Bank

Dealings

All Category - I Authorised

Dealer Banks

RBI/2012-2013/151

A. P.(DIR Series)

Circular No. 12

31.7.2012 Foreign

Exchange

Department

Exchange Earner's Foreign

Currency (EEFC) Account,

Diamond Dollar Account (DDA)

& Resident Foreign Currency

(RFC) Account - Review of

Guidelines

All Category - I Authorised

Dealer Banks

RBI/2012-2013/143

A.P.(DIR Series)

Circular No.10

24.7.2012 Foreign

Exchange

Department

Exim Bank's Line of Credit of

USD 47 million to the

Government of the Federal

Democratic Republic of Ethiopia

All Category - I Authorised

Dealer Banks

RBI/2012-2013/142

A.P. (DIR Series)

Circular No.9

24.7.2012 Foreign

Exchange

Department

Exim Bank's Line of Credit of

USD 250 million to the

Government of Nepal

All Category - I Authorised

Dealer Banks

RBI/2012-2013/135

A.P. (DIR Series)

Circular No. 8

18.7.2012 Foreign

Exchange

Department

Exchange Earner's Foreign

Currency (EEFC) Account

All Authorised Dealer

Category- I Banks

RBI/2012-2013/134

A.P. (DIR Series)

Circular No. 7

16.7.2012 Foreign

Exchange

Department

Scheme for Investment by

Qualified Foreign Investors

(QFIs) in Indian corporate debt

securities

All Category - I- Authorised

Dealer banks

RBI/2012-2013/132

A.P.(DIR Series)

Circular No. 6

13.7.2012 Foreign

Exchange

Department

Deferred Payment Protocols

dated April 30, 1981 and

December 23, 1985 between

Government of India and

erstwhile USSR

All Category - I Authorised

Dealer Banks

RBI/2012-2013/131

DPSS CO

(EPPD) /98/

4.03.01/2012-13

13.7.2012 Department of

Payment and

S e t t l e m e n t

System

National Electronic Funds

Transfer (NEFT) System -

Rationalisation of customer

charges

Chairman and Managing

Director /Chief Executive

Officer of all banks

participating in NEFT

18

Bizsol UPDATE August - 2012

Circular

Number

Date of

IssueDepartment Subject Meant For

RBI/2012-2013/129

A.P. (DIR Series)

Circular No. 5

12.7.2012 Foreign Ex-

change Depart-

ment

Foreign Exchange Management

Act, 1999 - Submission of

Revised A-2 Form

All Authorised Dealers in

Foreign Exchange

RBI/2012-2013/128

A.P. (DIR Series)

Circular No. 4

12.7.2012 Foreign Ex-

change Depart-

ment

Non Resident Deposits -

Comprehensive Single Return

All Authorised Dealers in

Foreign Exchange

RBI/2012-2013/127

F M D . M O A G .

No.70/01.01.01/

2012-13

11.7.2012 Financial Mar-

kets Department

Reverse Repo Window under

Liquidity Adjustment Facility and

Marginal Standing Facility -

Change of Timing

All Scheduled Commercial

Banks (excluding RRBs)

and Primary Dealers

RBI/2012-2013/124

A.P.(DIR Series)

Circular No. 3

11.7.2012 Foreign Ex-

change Depart-

ment

Risk Management and Inter Bank

Dealings

All Authorised Dealer

Category - I Banks

RBI/2012-2013/120

A.P. (DIR Series)

Circular No. 2

6.7.2012 Foreign Excha-

nge Department

Deferred Payment Protocols

dated April 30, 1981 and

December 23, 1985 between

Government of India and

erstwhile USSR

All Category - I Authorised

Dealer Banks

RBI/2012-2013/114

A.P. (DIR Series)

Circular No. 1

5.7.2012 Foreign Excha-

nge Department

Buyback / Prepayment of Foreign

Currency Convertible Bonds

(FCCBs)

All Category-I Authorised

Dealer Banks

RBI/2012-2013/83

DCM (NE) No.G-

1/08.07.18/2012-

13

2.7.2012 Department of

Currency Man-

agement

Master Circular - Facility for

Exchange of Notes and Coins

The Chairman and

Managing Director / The

Chief Executive Officer All

Banks

RBI/2012-2013/82

DGBA.CDD No.

H-8574/13.01.

299/2012-13

2.7.2012 Department of

Government and

Bank Accounts

Master Circular on Nomination

facility in Relief/Savings bonds

The Chairman /Managing

Director Head Office

(Government Accounts

Department) State Bank of

India and Associates All

Nationalized banks

(Excluding Punjab and Sind

Bank & Andhra Bank) Axis

Bank Ltd./ICICI Bank Ltd./

HDFC Bank Ltd./ Stock

Holding Corporation of India

Ltd.(SCHIL)

RBI/2012-2013/81

DGBA.CDD No.

H-8576/13.01.

299/2012-13

2.7.2012 Department of

Government and

Bank Accounts

Master Circular on Appointment

& Delisting of Brokers and

Payment of Brokerage on Relief/

Savings Bonds

The Chairman / Managing

Director Head Office

(Government Accounts

Department) State Bank of

19

Bizsol UPDATE August - 2012

Circular

Number

Date of

IssueDepartment Subject Meant For

India and Associates All

Nationalized banks

(Excluding Punjab and Sind

Bank & Andhra Bank) Axis

Bank Ltd./ICICI Bank Ltd./

HDFC Bank Ltd./ Stock

Holding Corporation of India

Ltd. (SHCIL)

RBI/2012-2013/80

DBS.FrMC.BC.No.1/

23.04.001/2012-

13

2.7.2012 Department of

Banking Super-

vision

Frauds - Classification and

Reporting

The Chairmen & Chief

Executive Officers of all

Scheduled Commercial

Banks (excluding RRBs)

and All India Select

Financial Institutions

RBI/2012-2013/79

DBOD.No.Dir.BC.4/

13.03.00/2012-

13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular- Loans and

Advances - Statutory and Other

Restrictions

All Scheduled Commercial

Banks (excluding RRBs)

RBI/2012-2013/78

DBOD.No.Dir.BC.8/

13.03.00/2012-

13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular of instructions

relating to deposits held in

FCNR(B) Accounts

All Scheduled Commercial

Banks (excluding RRBs)

RBI/2012-2013/77

DBOD.No. BL.

BC. 26 /22.01.

001/2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Section 23 of Banking Regulation

Act, 1949 - Master Circular on

Branch Authorisation

All Commercial Banks

(excluding RRBs)

RBI/2012-2013/76

DBOD. No.Ret.

B C . 2 2 / 1 2 . 0 1 .

001/2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular - Cash Reserve

Ratio (CRR) and Statutory

Liquidity Ratio (SLR)

All Scheduled Commercial

Banks (Excluding Regional

Rural Banks)

RBI/2012-2013/75

DBOD.No.Dir .

BC.1/13.03.00/

2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular on Interest Rates

on Rupee Deposits held in

Domestic, Ordinary Non-

Resident (NRO) and Non-

Resident (External) (NRE)

Accounts

All Scheduled Commercial

Banks (excluding RRBs)

RBI/2012-2013/74

DBOD No.DIR.

B C . 0 6 / 0 4 . 0 2 .

002/2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular - Rupee / Foreign

Currency Export Credit &

Customer Service To Exporters

All Scheduled Commercial

Banks (excluding RRBs)

RBI/2012-2013/73

DBOD. No.DIR.

B C . 0 7 / 0 8 . 1 2 .

001/2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular - Housing

Finance

All Scheduled Commercial

Banks (excluding RRBs)

20

Bizsol UPDATE August - 2012

Circular

Number

Date of

IssueDepartment Subject Meant For

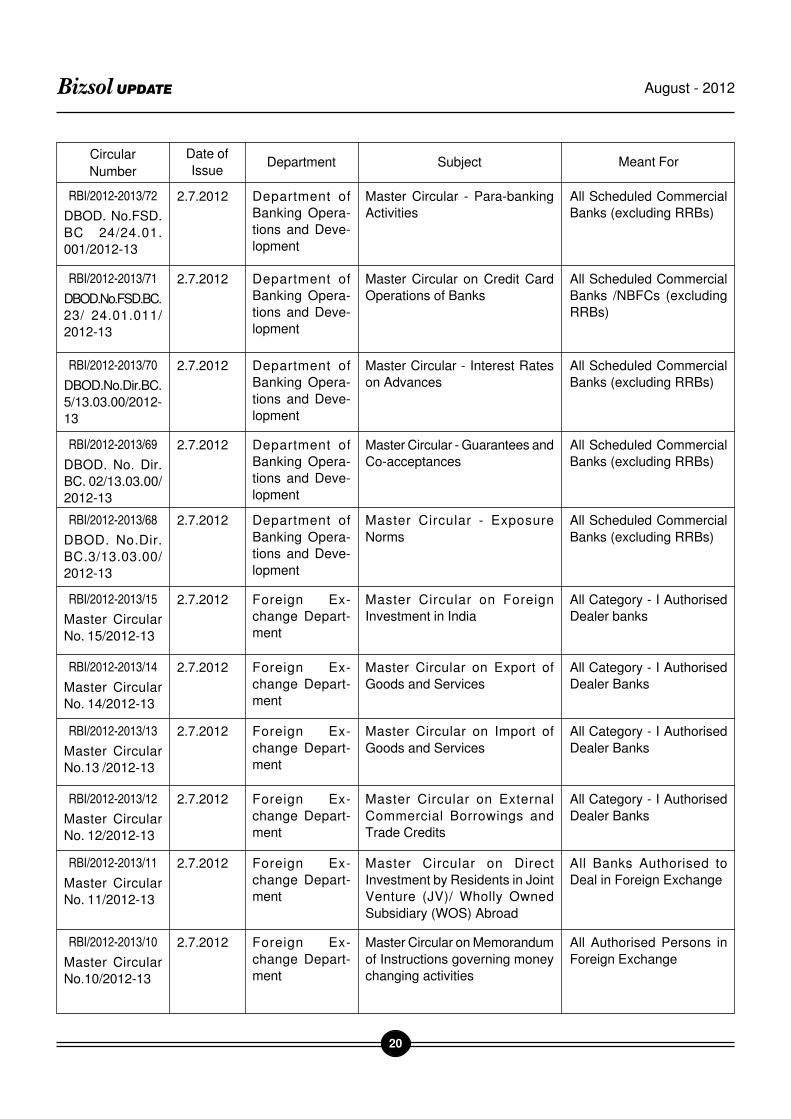

RBI/2012-2013/72

DBOD. No.FSD.

BC 24/24.01.

001/2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular - Para-banking

Activities

All Scheduled Commercial

Banks (excluding RRBs)

RBI/2012-2013/71

DBOD.No.FSD.BC.

23/ 24.01.011/

2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular on Credit Card

Operations of Banks

All Scheduled Commercial

Banks /NBFCs (excluding

RRBs)

RBI/2012-2013/70

DBOD.No.Dir.BC.

5/13.03.00/2012-

13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular - Interest Rates

on Advances

All Scheduled Commercial

Banks (excluding RRBs)

RBI/2012-2013/69

DBOD. No. Dir.

BC. 02/13.03.00/

2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular - Guarantees and

Co-acceptances

All Scheduled Commercial

Banks (excluding RRBs)

RBI/2012-2013/68

DBOD. No.Dir.

BC.3/13.03.00/

2012-13

2.7.2012 Department of

Banking Opera-

tions and Deve-

lopment

Master Circular - Exposure

Norms

All Scheduled Commercial

Banks (excluding RRBs)

RBI/2012-2013/15

Master Circular

No. 15/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Foreign

Investment in India

All Category - I Authorised

Dealer banks

RBI/2012-2013/14

Master Circular

No. 14/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Export of

Goods and Services

All Category - I Authorised

Dealer Banks

RBI/2012-2013/13

Master Circular

No.13 /2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Import of

Goods and Services

All Category - I Authorised

Dealer Banks

RBI/2012-2013/12

Master Circular

No. 12/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on External

Commercial Borrowings and

Trade Credits

All Category - I Authorised

Dealer Banks

RBI/2012-2013/11

Master Circular

No. 11/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Direct

Investment by Residents in Joint

Venture (JV)/ Wholly Owned

Subsidiary (WOS) Abroad

All Banks Authorised to

Deal in Foreign Exchange

RBI/2012-2013/10

Master Circular

No.10/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Memorandum

of Instructions governing money

changing activities

All Authorised Persons in

Foreign Exchange

21

Bizsol UPDATE August - 2012

Circular

Number

Date of

IssueDepartment Subject Meant For

RBI/2012-2013/7

Master Circular

No. 7/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Establishment

of Liaison / Branch / Project

Offices in India by Foreign

Entities

All Category - I Authorised

Dealer banks

RBI/2012-2013/6

Master Circular

No. 6/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Miscellaneous

Remittances from India -

Facilities for Residents

All Authorised Persons in

Foreign Exchange

RBI/2012-2013/5

Master Circular

No.5/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Risk

Management and Inter-Bank

Dealings

All Authorised Dealers -

Category I Banks

RBI/2012-2013/4

Master Circular

No.4 /2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Acquisition

and Transfer of Immovable

Property in India by NRIs/PIOs/

Foreign Nationals of Non-Indian

Origin

All Category - I Authorised

Dealer banks

RBI/2012-2013/3

Master Circular

No. 3/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Memorandum

of Instructions for Opening and

Maintenance of Rupee/ Foreign

Currency Vostro Accounts of

Non-resident Exchange Houses

All Authorised Dealer

Category-I Banks

RBI/2012-2013/9

Master Circular

No.9 /2012-13

(Updated as on

January 20, 2012)

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Compounding

of Contraventions under FEMA,

1999

All Authorised Dealer

Category - I banks and

Authorised Banks

RBI/2012-2013/8

Master Circular

No.8/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Remittance

Facilities for Non-Resident

Indians / Persons of Indian Origin

/ Foreign Nationals

All Authorised Dealer

Category - I banks and

Authorised banks

RBI/2012-2013/2

Master Circular

No.2/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Non-Resident

Ordinary Rupee (NRO) Account

All Authorised Dealer

Category - I banks and

Authorised banks

RBI/2012-2013/1

Master Circular

No.1/2012-13

2.7.2012 Foreign Ex-

change Depart-

ment

Master Circular on Money

Transfer Service Scheme

All Authorised Persons,

who are Indian Agents

under the Money Transfer

Service Scheme

22

Bizsol UPDATE August - 2012

CENTRAL EXCISE

v Cenvat credit to the extent the items had been

used purely in erection work, i.e. foundation for

erection of machinery and making supporting

structures for the machinery, or other structures

fixed to earth is correctly disallowed but to the

extent the steel items have been used in

fabrication of identifiable items of machinery,

covered by the definition of capital goods as given

in Rule 2 (a) of Cenvat Credit Rules, the credit

would be admissible - Pre-deposit ordered of Rs.1

Crore: [2012-TIOL-930-CESTAT-DEL]

v SSI Exemption when running unit is

purchased: Running unit purchased with

machineries and dies bearing its brand name,

manufacturing goods out of such dies will

disentitle the new manufacturer from availing the

benefit of SSI notification: [2012-TIOL-923-

CESTAT-MUM]

v No time limit for Rebate claim: Time limit for

claiming rebate prescribed under Notification No.

41/94CE was omitted by subsequent notification

no. 19/2004 CE. Omission was conscious as all

other conditions for obtaining rebate were retained

in the subsequent Notification, even rule 18 did

not prescribe so, hence rebate cannot be rejected

on the ground of limitation. [2012(281) ELT

227(Mad)]

v Interest is payable on differential duty paid

after final assessment - Difference of opinion

resolved in favour of revenue: Goods cleared

to own unit & duty paid on 115% cost of production

and differential duty paid thereafter through

cenvat credit which is available as credit to

another unit. Member (judicial) opined that no

interest is payable on the ground of revenue

neutrality but based on the wording of section

11AB, Member (technical) & 3rd Member decided

the issue in favour of revenue. [2012 (281) ELT

296 (Tri-Ahmd)]

v Interest no payable when Cenvat credit not

utilized: Cenvat Credit availed on inputs used in

exempted product, if reversed without utilization,

there is no liability for interest. As interest is

compensatory in character imposed on assesee

withholding tax as and when due. [2012 (281) ELT

296 (Kar)]

v Reversal of Cenvat credit on inputs contained

in waste destroyed within factory: Revenue

authority cannot call for reversal of credit on inputs

therein on ground that inputs have been removed

as such, Rule 3(5) of CCR, 2004 not applicable.

It is immaterial that assesse had obtained

remission of duty in terms of Rule 21 of Central

Excise Rules, 2002. [2012 (281) ELT 170(Kar)]

v Excise Rules 12AA and 12CC struck down by

Orissa HC: Prior to insertion of clause (xiiia) in

sub section (2) of Section 37 of Central Excise

Act, 1944, ie. before 08.05.2010 the Central

Government had no power to make rule 12CC of

the Central Excise Rules, 2002 or Rule 12AA of

the Central Credit Rules, 2004 and issue

subsequent Notification No. 32/2006-C.E. N.T. dt.

30.12.2006 where certain restriction were

imposed while availing cenvat credit. Hence, it is

held that Rule 12AA and Rule 12CC made in the

year 2006 by the Central Government without any

authority of law which power was vested in them

in the year 2010,therefore, two Rules are

ultravirus the Central Excise Act, 1944 and

Notification No. 32/2006- C.E. N.T. dt. 30.12.2006

issued in pursuance of Rule 12CC and Rule 12AA

is not sustainable in law. [2012(281)E.L.T. 15

(Ori.)]

v Cenvat Credit availed on services used for

traded goods not admissible: Goods containing

Alcohol are not final products since the same are

not excisable goods under the Central Excise Act,

1944. Therefore, the inputs which are used for

manufacture of such goods do not quantify as

inputs and therefore, credit availed on such inputs

is not admissible. Similarly trading activity is

neither an output service not it is final product

hence, assessee is not entitled to avail any cenvat

23

Bizsol UPDATE August - 2012

credit on the services which are used for trading

activity. [2012(281) E.L.T.113(Tri. Mumbai)]

v Assessee can challenge order even when he

paid duty to avoid penalty: Adjudication of

assessment done before coming into force of

Section 11AA of the Central Excise Act, 1944 and

hence, demand of interest under Section 11AA

of the Central Excise Act, 1944 is not sustainable

in this case, as said section has no retrospective

effect. [2012(281)E.L.T. 48 (Mad.)]

v Legal heirs not liable to pay duty due from

deceased: Since, there is no provision in law to

demand from the legal heirs of the deceased due

from assessee, unless they take over and

continue to carry on same business of the

deceased and comply with statutoty

requirements, legal heirs cannot be held liable of

the dues of the deceased. Similarly, on death of

Proprietor and after surrender of central excise

registration of firm his legal heirs cannot use the

unutilised credit. It is not permissible even if the