Title Date Lifetime Learning… Building Success… Towards Globalization Derivatives Lifetime Learning… Building Success… Towards Globalization

Course on Derivatives 18-19 Sept 2011.pptx

Dec 10, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TitleDate

Lifetime Learning… Building Success… Towards Globalization

Derivatives

Lifetime Learning… Building Success… Towards Globalization

Learning Outcomes

Introduce risk and the role of derivatives in managing riskDiscuss some of the general terms – such as short/long positions, bid-ask spread – from finance that we need.

Introduce derivative and there major classificationForwardsFuturesOptions

Introduce basic viewpoint needed to analyze these securities

Introduce major traders of these instruments

Applied Finance

Finance is the study of risk.– How to measure it– How to reduce it– How to allocate it

All finance problems ultimately boil down to three main questions:

– What are the cash flows, and when do they occur?– Who gets the cash flows?– What is the appropriate discount rate for those cash flows?

The difficulty, of course, is that normally none of those questions have an easy answer.

Derivatives & Cash Instruments - Basics

• A derivative (or derivative security) is a financial instrument whose value depends upon the value of other, more basic, underlying variables.

• Some common examples include things such as stock options, futures, and forwards.

• It can also extend to something like a reimbursement program for college credit. Consider that if your firm reimburses 100% of costs for an “A”, 75% of costs for a “B”, 50% for a “C” and 0% for anything less. – Your “right” to claim this reimbursement, then is tied to the grade you

earn. The value of that reimbursement plan, therefore, is derived from the grade you earn.

– We also say that the value is contingent upon the grade you earn. Thus, your claim for reimbursement is a “contingent” claim.

– The terms contingent claims and derivatives are used interchangeably• The financial instruments stocks, bonds, commodities and currencies - are

generally referred to as cash instruments (or sometimes, primary instruments). The value of cash instruments is determined directly by markets

Cash Instruments vs Derivatives

• Derivatives are further distinguished from cash instruments in that they are contracts between two or more parties

• These contracts are promises to convey ownership of an asset rather than the asset itself.

• Like other contracts, derivatives represent an agreement between two parties; the terms of the agreement are highly flexible and the contract has a fixed beginning and ending date.

Examples of Derivative Instruments

• A stock option is a derivative that derives its value from the value of a stock. An interest rate swap is a derivative because it derives its value from an interest rate index.

• The asset from which a derivative derives its value is referred to as the underlying asset.

• The price of a derivative rises and falls in accordance with the value of the underlying asset.

Exchange-Traded and OTC Derivatives

• Like their underlying cash instruments, some derivatives are traded on established exchanges (the New York Stock Exchange, the French CAC or the Chicago Board of Trade or the Nasdaq Dubai or SIMEX). These are referred to as exchange-traded derivatives and, generally, they have highly standardized terms and features. The advantage of exchange-traded derivatives is that regulated exchanges provide clearing and regulatory safeguards to investors.

• Many other derivative instruments, including forwards, swaps and exotic derivatives, are traded outside of the formal, established exchanges. These are over-the-counter or OTC-traded derivatives. They can be created by any two counterparties with highly flexible terms and a nearly infinite number of underlying assets or asset combinations. In the OTC derivatives market, large financial institutions serve as derivatives dealers, customizing derivatives for the specific needs of clients.

• Some derivatives are both exchange-traded as well as OTC.

Purposes and Benefits of Derivatives

• Hedging and Leveraging• Price Discovery• Risk Management• They Improve Market Efficiency for the Underlying Asset • Derivatives Also Help Reduce Market Transaction Costs

Hedging and Leveraging

• Investors use derivatives to capture profits resulting from price variations in the underlying investment. Because of this, derivatives are often referred to as leveraged investments. Leverage, can be, both positive and negative, and can be greatly magnified .

• Derivatives are generally used to hedge risk• Derivatives are also attractive to investors because they trade for a

fraction of the price of the underlying asset, enabling investors to control more of an asset for less money.

Criticisms of Derivatives

• When a derivative fails to help investors achieve their objectives, the derivative itself is blamed for the ensuing losses when, in fact, it's often the investor who did not fully understand how it should be used, its inherent risk, etc. Some view derivatives as a form of legalized gambling enabling users to make bets on the market.

• Lifespan - Derivatives are "time-wasting" assets. As each day passes and the expiration date approaches, you lose more and more "time" premium and the option's value decreases.

• Direction and Market Timing - In order to make money with many derivatives, investors must accurately predict the direction in which the market or index will move (up or down) and the minimum magnitude of the move during a set period of time. A mistake here almost guarantees a substantial investment loss.

• Costs - The bid/ask spreads of more common derivatives such as options can be daunting. An option with a bid of 5.25 and an ask of 5.875 means an investor could buy a round lot (100 units) for $587.50 but could only sell them for $525, resulting in an immediate loss of $61.50 before factoring in commissions.

Forward Exchange Contracts

• A Forward Contract is an agreement between a customer and a Bank for the purchase or sale of a specified quantity of one currency in exchange for another and for settlement at a future date at an agreed (fixed ) rate of exchange.

• Forward rates are therefore used to fix an exchange rate now for a future transaction, eliminating the currency exposure.

Characteristics of Forwards

• The settlement price is called the forward rate.Todays price is called the spot rate.

• Normally Forwards are called Purchase contracts or sale Contracts from the Banks point of view. The bank has a long or overbought position when it has contracted a forward purchase.

• The Future settlement date is called the forward value date if it’s a specific date.Such a contract is called an outright forward contract.

• Future settlement or delivery can be on any business day between between two value dates( called a value-date option contract)

• The difference between the spot price and the forward rate is called the swap or a swap difference or the forward premium or discount( depending upon whether the foreign currency is costlier in the forward leg or cheaper)

• Normally Forward contracts are for 12 months.Most liquid contracts are upto 6 months..

Locking in a Rate with a Forward contract

• Forward exchange contracts are used to lock in an exchange rate for a future purchase or sale of foreign currency. If there is an underlying business transaction, a forward contract will eliminate the currency exposure because the rate of exchange of the future transaction is fixed, regardless of the change in spot rate between the contract date and the settlement date.

• No upfront payment is needed.No margins or fees

Examples of Lock-in

• An Emirati Company must pay a German supplier EUR 100000 in three months time. The current spot rate is EUR 1= AED 5.5.Since the Company will have to buy The EUR with AED 550,000.The company has already sold the goods to another Emirati Company for AED 660000 and expects to make a profit of AED 110000.The Company is concerned that AED might weaken against the EUR and erode the profit margin.

• Suppose the spot rate after 3months is EUR1= AED 6.00 It would cost AED 600000 to buy EUR 100000 and the profiit on the transaction would be just AED 60000.

• A forward contract eliminates the risk>If the three months forward rate is 5.475, purchasing EUR 100000 would cost AED 547500. and the Company could secure a profit of AED 112,500.

Pricing of Forwards

• The difference between the Forward rate and the Spot rate is called the swap difference.

• The rates of foreign currencies in the forward value dates can be at a discount or premium to the spot rates.

• The Forward rate differs from spot rate by an amount reflecting the interest rate differential between the two currencies.

Forward Premiums and Discounts

• If the interest rate(on Loans) for A is higher than the interest rate for B, then A would be weaker of the two currencies in the forward market and its forward rate against B would be quoted at a discount to the current spot rate.

• Suppose 1B= 2.00A and one interest rate on loans is B=5% and A=10%. Then A would be 5% cheaper than A in the one year forward .So one year forward rate for B Vs A would be

1B=2.100 A• Suppose rates for quotes as 1A=0.500B then B with a lower

interest rate would be 5% costlier in the forward market. So forward rate of A Vs B would be 1A=0.475 B

Forward Rate is not a predictor

• The Forward rate is not a predictor of the future exchange rate.

• If The spot cable is at GBP1=1.60$ and the one month forward rate is GBP 1=1.5950$ it would be wrong to assume that Dollar spot rate would harden to 1.595$ per GBP over the month. The $0.0050 would represent the value of the difference between the US$ and the GBP interest rates over one-month period.

Other Characteristics of Forward Contracts

• When the amount of payment or reciept is uncertain, forward covers can be partial.

• Forward covers are less liquid for some currencies than others.• The term of the forward contract is related to the term money markets.• Forward Contracts can be value-dated option contracts ie delivery can be

made between two forward dates.• A Company is not exactly certain about the reciept of foreign currency.It

would be anytime in the month of March 2012.The Company could book a contract for delivery between 1st March 2012 to 31st march 2012. Howevery a single rate is quoted. Partail delivery is permitted in the option period.

The Foreign exchange swap market

• Traders use the forward market to take bets on the Interest rate differentials-whether it would widen or narrow.

• They do it through swaps which are a simultaneous purchase and sale of foreign currency or vice-versa.One is a shorter value date and the other a longer value date.

• You could sell the premium currency for the longer date if you expect the premium to narrow Swaps narrow because interest differentials narrow.(receive now and pay later)

• If you expect the swaps to widen then you should buy the premium currency in the forward leg.( pay now and receive later)

Currency Futures

• Currency Futures contract is a legally binding contract to buy or sell a standard quantity of one currency for another

1. At a specified rate of exchange 2.For delivery at a specified time in future.• With currency futures, the underlying financial

instrument is a standard quantity of one currency for a second currency, usually the US$.

Characteristics of Currency Futures

• Only a limited number of currencies are traded on the Futures exchanges and they are mostly the majors.

• The market price at which currency futures are traded is expressed in terms of exchange rates.

• Pricing of Currency Futures is always done with US$ as the variable currency unlike the Foreign exchange markets where the US$ is the variable currency only against GBP, EUR and the Ozzie and the Kiwi.In all other cases the US$ is the base-currency.

• A price movement in the futures market reflects in the Foreign exchange markets.

• Futures have standardized delivery dates• Delivery will be made through specified bank accounts into which

exchanged currencies must be transferred.

Contract Specifications for a Futures Contract

• The content of a futures contract is established by the exchange an dis the same for every user.

• This standardization means that the buyer and seller negotiate only the price, which greatly reduces the time needed to trade a contract.

• Contract specification laid down by the exchange include-• Definition of the underlying, • Nominal amount of contract,• Minimum permissible price movement• Value of minimum price movement• Trading hours• Delivery date• Last trading day of the contract

Contract specifications

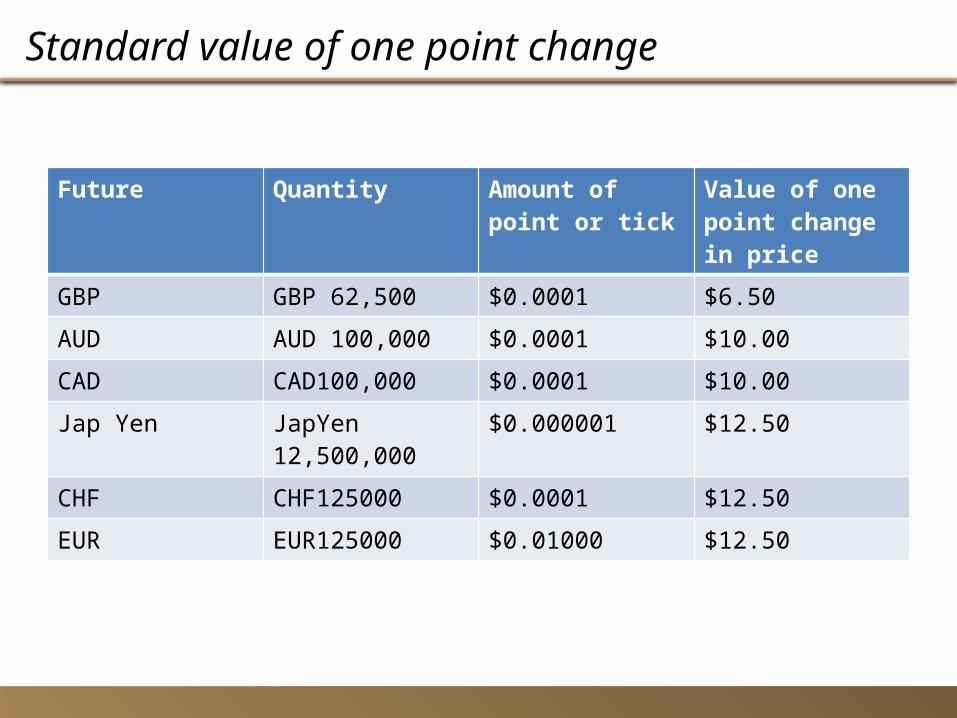

• Standard Contract amounts-GBP62500/-,Ozzie A$100,000/-,C$ 100,000/-,Japyen12,500,000/-Swiss Francs 125000/-, Eur 125000/-.

• To deal in larger amounts multiples of standard amounts are bought or sold.To Buy GBP 500,000 , eight futures contracts of GBP62500 must be bought

• Currency Future Contracts trade for 4 fixed settlement dates in the year.

• On CME the last day of trading is is two business days before the third Wednesday of the delivery month,

• Delivery is the third Wednesday of the delivery month.

Futures Pricing Convention

• Futures are quoted in Dollars per unit of currency.• The USD/CHF foreign exchange market quote

would be 1USD=0.8060 CHF(Swiss Franc)• However in the Futures market the price for

September CHF Future might be 1.2400, which means $1.2400 per CHF .At this price, a seller of the September future would be agreeing to sell CHF125000 to the buyer in exchange for US$155,000(CHF125000x1.2400)

Price Movements in Futures

• The market price could go up from 1.2400 to 1.2500.This rise of $0.0100 per CHF would be a rise of 100 points.

• Another September Future contract at this new price would be an agreement by the seller to sell CHF125000 in exchange for US$156250(125000x1.2500)

• The increase of 100 points in the market price represents an increase of $1250 in the exchange value of CHF125000 for deliver in September

Futures Valuation

• For the seller of September delivery CHF Contract at 1.2400, the increase in market price of 100 points represents a loss of $1250, since he will receive only $155000 for his CHF in September

• For the buyer of the contract, the increase in market price represents a gain of $1250, because he will have to pay only $ 155000

• For the CHF futures contract, every increase in price of one point ($0.0001) represents a gain of $12.50 to the buyer and a loss of $12.50 to the seller. A Fall of one point represents a loss of $12.50 to the buyer and gain to the seller

Standard value of one point change

Future Quantity Amount of point or tick

Value of one point change in price

GBP GBP 62,500 $0.0001 $6.50

AUD AUD 100,000 $0.0001 $10.00

CAD CAD100,000 $0.0001 $10.00

Jap Yen JapYen 12,500,000 $0.000001 $12.50

CHF CHF125000 $0.0001 $12.50

EUR EUR125000 $0.01000 $12.50

Example of Price movements

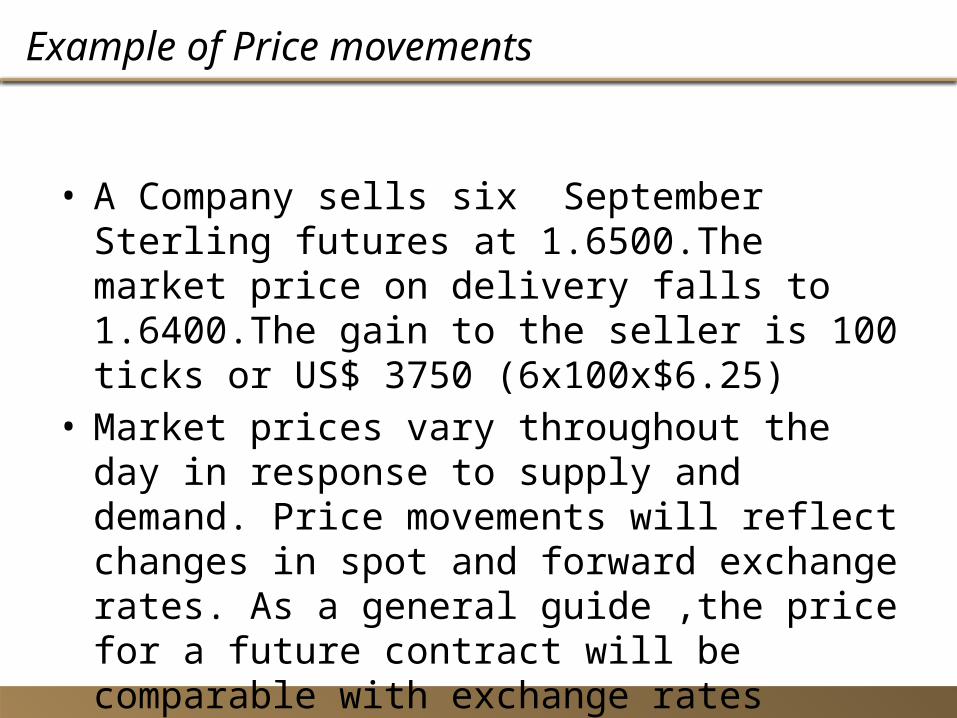

• A Company sells six September Sterling futures at 1.6500.The market price on delivery falls to 1.6400.The gain to the seller is 100 ticks or US$ 3750 (6x100x$6.25)

• Market prices vary throughout the day in response to supply and demand. Price movements will reflect changes in spot and forward exchange rates. As a general guide ,the price for a future contract will be comparable with exchange rates available on forward contracts for the same settlement/Delivery date,

Margin Mechanism

• Each Clearing member firm keeps an account with the Clearing House, and each client keeps an account with its broker.

• The accounts are for margin payments and for recording gains or losses on Futures positions.

• The Exchange determines a settlement price at the end of each trading day for each futures contract, which reflects dealt prices towards the close of the days trading

• This price is then used for a process of marking-to-market, whereby daily gain or loss on a Futures position is recorded in each margin account.

• Every buyer or seller of a contract must deposit an initial margin with their broker, who in turn deposits the margin with the exchange clearing house.

• The size of the margin is set by the Exchange and is sufficient to cover the account holder for some loss on his Futures position

Settlement on Delivery Date

• If a currency futures runs to delivery date there will be cash settlement, sometimes called settlement for difference, which is paid by one party to the other through the exchange.

• If A sells sterling futures contract to B (Broker) at $1.6450 to 1GBP and the settlement price is $1.5450, the seller will have made a profit.

• GBP 62500@ 1.6450 = $102812.50• GBP 62500 @ 1.5450 = $ 96562.50• Cash Setllement for difference =$ 6250

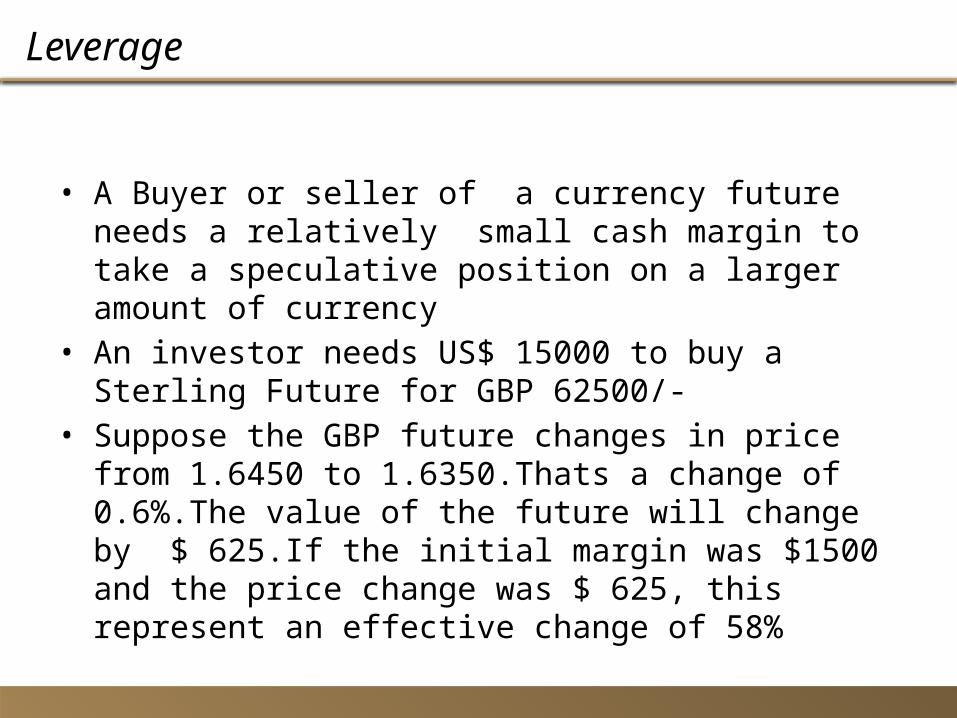

Leverage

• A Buyer or seller of a currency future needs a relatively small cash margin to take a speculative position on a larger amount of currency

• An investor needs US$ 15000 to buy a Sterling Future for GBP 62500/-

• Suppose the GBP future changes in price from 1.6450 to 1.6350.Thats a change of 0.6%.The value of the future will change by $ 625.If the initial margin was $1500 and the price change was $ 625, this represent an effective change of 58%

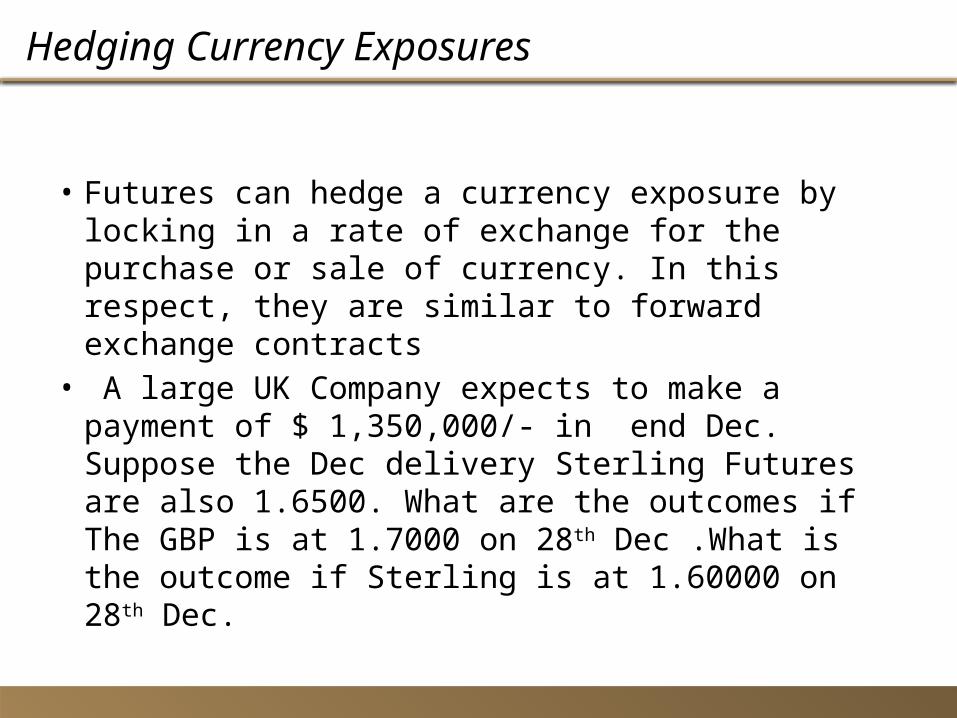

Hedging Currency Exposures

• Futures can hedge a currency exposure by locking in a rate of exchange for the purchase or sale of currency. In this respect, they are similar to forward exchange contracts

• A large UK Company expects to make a payment of $ 1,350,000/- in end Dec. Suppose the Dec delivery Sterling Futures are also 1.6500. What are the outcomes if The GBP is at 1.7000 on 28th Dec .What is the outcome if Sterling is at 1.60000 on 28th Dec.

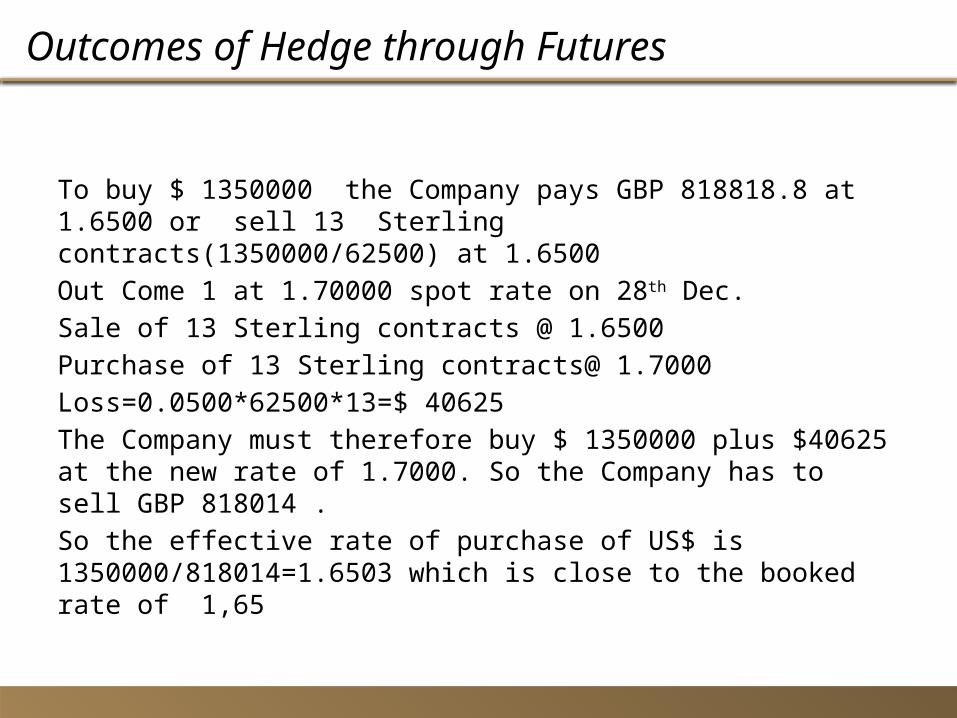

Outcomes of Hedge through Futures

To buy $ 1350000 the Company pays GBP 818818.8 at 1.6500 or sell 13 Sterling contracts(1350000/62500) at 1.6500Out Come 1 at 1.70000 spot rate on 28th Dec.Sale of 13 Sterling contracts @ 1.6500Purchase of 13 Sterling contracts@ 1.7000Loss=0.0500*62500*13=$ 40625The Company must therefore buy $ 1350000 plus $40625 at the new rate of 1.7000. So the Company has to sell GBP 818014 .So the effective rate of purchase of US$ is 1350000/818014=1.6503 which is close to the booked rate of 1,65

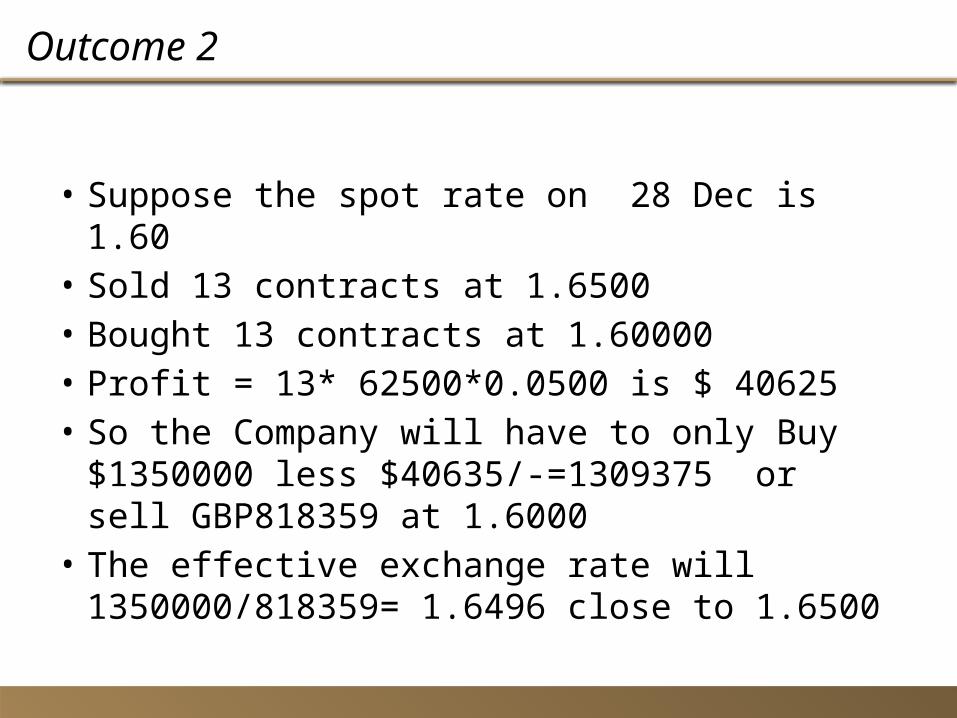

Outcome 2

• Suppose the spot rate on 28 Dec is 1.60• Sold 13 contracts at 1.6500• Bought 13 contracts at 1.60000• Profit = 13* 62500*0.0500 is $ 40625• So the Company will have to only Buy $1350000

less $40635/-=1309375 or sell GBP818359 at 1.6000

• The effective exchange rate will 1350000/818359= 1.6496 close to 1.6500

Futures and Non-Dollar transactions

• When a Company wishes to fix an exchange rate involving two currencies neither of which is the US$ say GBP vs CHF the transaction structure is a bit more complex.

• Suppose an UK Company expects to make a payment in CHF in September and wants to buy CHF with GBP.

• To lock in an exchange rate for CHF vs GBP with Futures, the Company will have to open up two new futures positions( what)?

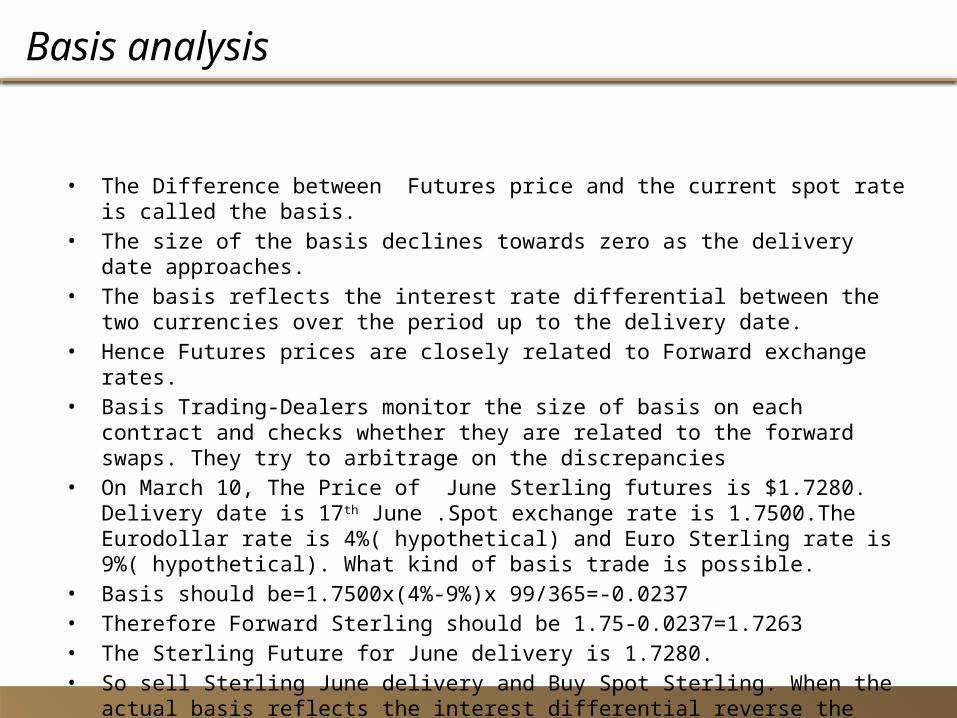

Basis analysis

• The Difference between Futures price and the current spot rate is called the basis.• The size of the basis declines towards zero as the delivery date approaches.• The basis reflects the interest rate differential between the two currencies over the period up

to the delivery date.• Hence Futures prices are closely related to Forward exchange rates.• Basis Trading-Dealers monitor the size of basis on each contract and checks whether they are

related to the forward swaps. They try to arbitrage on the discrepancies• On March 10, The Price of June Sterling futures is $1.7280. Delivery date is 17th June .Spot

exchange rate is 1.7500.The Eurodollar rate is 4%( hypothetical) and Euro Sterling rate is 9%( hypothetical). What kind of basis trade is possible.

• Basis should be=1.7500x(4%-9%)x 99/365=-0.0237• Therefore Forward Sterling should be 1.75-0.0237=1.7263• The Sterling Future for June delivery is 1.7280.• So sell Sterling June delivery and Buy Spot Sterling. When the actual basis reflects the

interest differential reverse the position.

Equity Options

Options or Financial Options

• An option is a contract giving the buyer the right, but not the obligation, to buy or sell an underlying asset (a stock or index) at a specific price on or before a certain date (listed options are all for 100 shares of the particular underlying asset).

• An option is a security, just like a stock or bond, and constitutes a binding contract with strictly defined terms and properties.

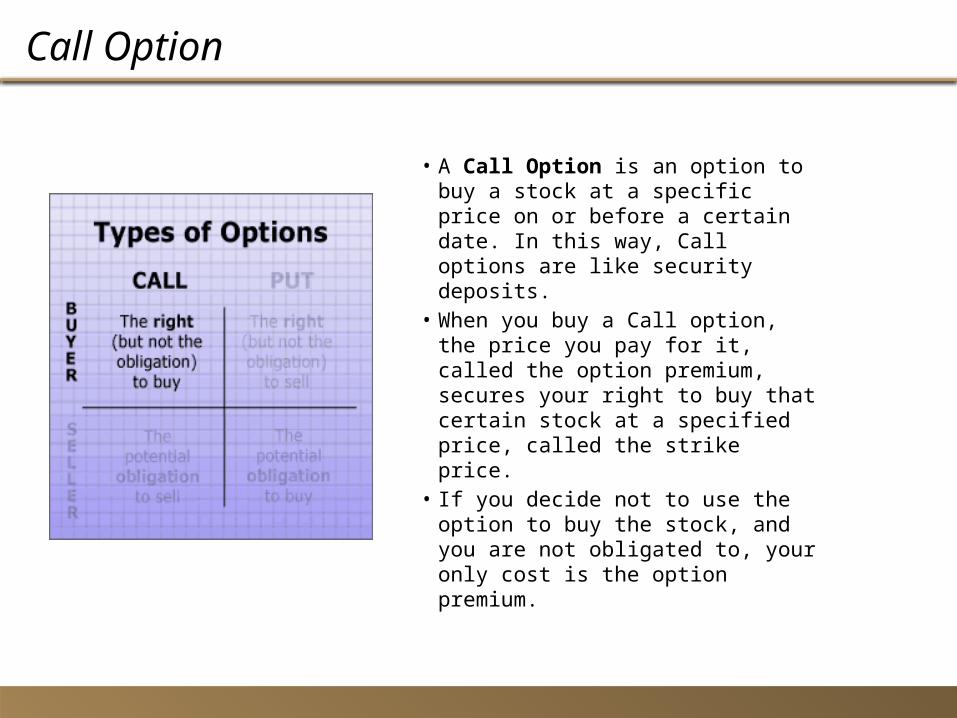

Call Option

• A Call Option is an option to buy a stock at a specific price on or before a certain date. In this way, Call options are like security deposits.

• When you buy a Call option, the price you pay for it, called the option premium, secures your right to buy that certain stock at a specified price, called the strike price.

• If you decide not to use the option to buy the stock, and you are not obligated to, your only cost is the option premium.

Put Option

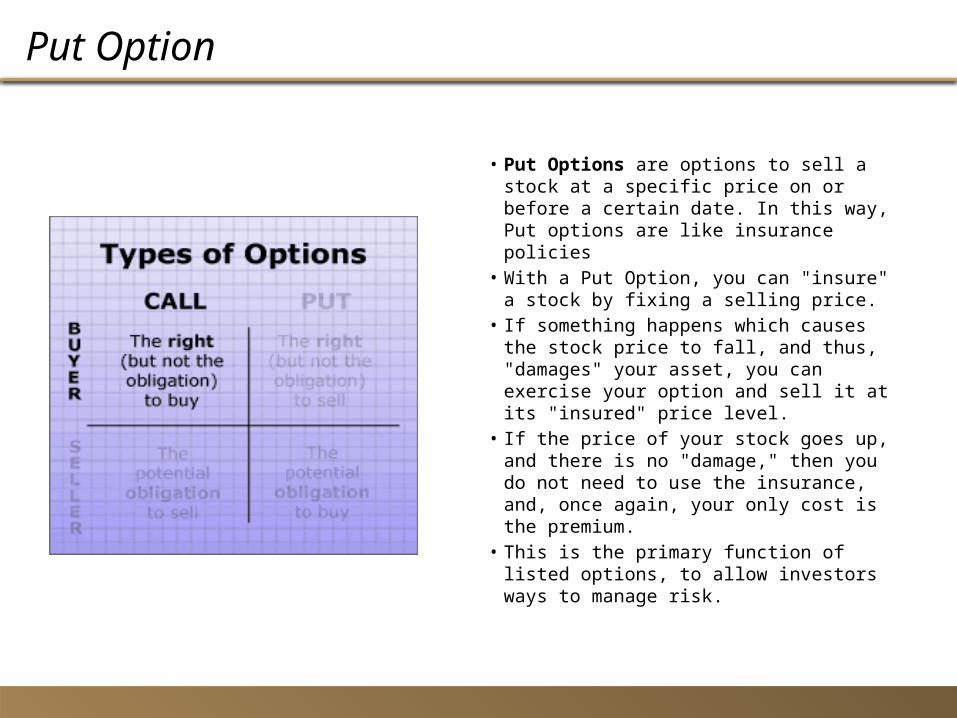

• Put Options are options to sell a stock at a specific price on or before a certain date. In this way, Put options are like insurance policies

• With a Put Option, you can "insure" a stock by fixing a selling price.

• If something happens which causes the stock price to fall, and thus, "damages" your asset, you can exercise your option and sell it at its "insured" price level.

• If the price of your stock goes up, and there is no "damage," then you do not need to use the insurance, and, once again, your only cost is the premium.

• This is the primary function of listed options, to allow investors ways to manage risk.

Option Premium

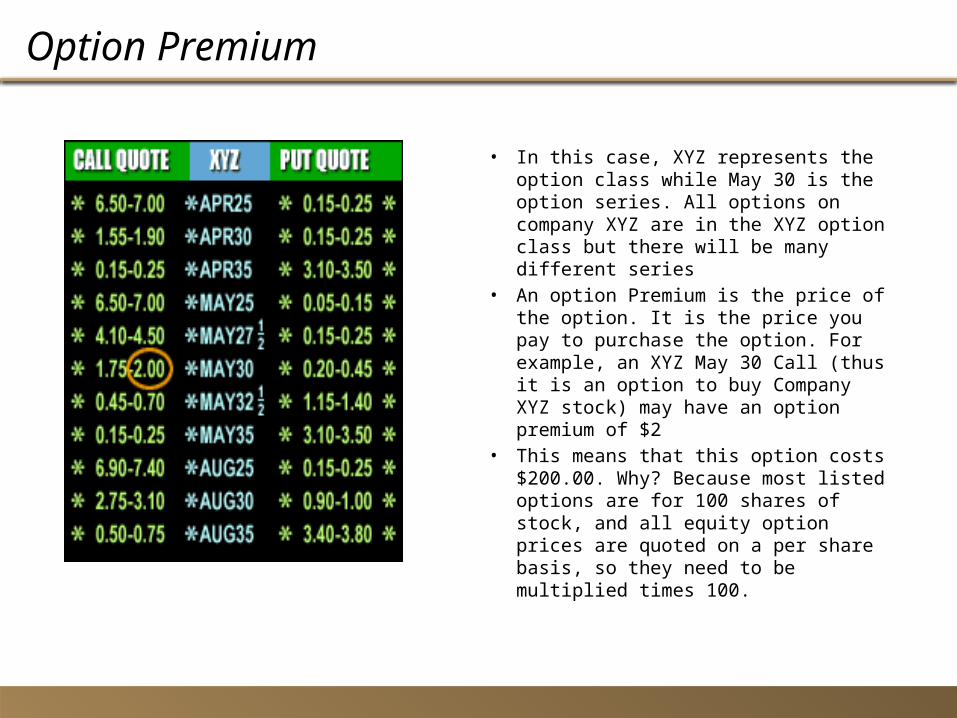

• In this case, XYZ represents the option class while May 30 is the option series. All options on company XYZ are in the XYZ option class but there will be many different series

• An option Premium is the price of the option. It is the price you pay to purchase the option. For example, an XYZ May 30 Call (thus it is an option to buy Company XYZ stock) may have an option premium of $2

• This means that this option costs $200.00. Why? Because most listed options are for 100 shares of stock, and all equity option prices are quoted on a per share basis, so they need to be multiplied times 100.

Strike Price

• The Strike (or Exercise) Price is the price at which the underlying security (in this case, XYZ) can be bought or sold as specified in the option contract.

• For example, with the XYZ May 30 Call, the strike price of 30 means the stock can be bought for $30 per share. Were this the XYZ May 30 Put, it would allow the holder the right to sell the stock at $30 per share.

• The strike price also helps to identify whether an option is In-the-Money, At-the-Money, or Out-of-the-Money when compared to the price of the underlying security..

Expiration Date

• The Expiration Date is the day on which the option is no longer valid and ceases to exist. The expiration date for all listed stock options in the U.S. is the third Friday of the month (except when it falls on a holiday, in which case it is on Thursday).

• For example, the XYZ May 30 Call option will expire on the third Friday of May

Exercise

• People who buy options have a Right, and that is the right to Exercise.

• For a Call Exercise, Call holders may buy stock at the strike price (from the Call seller).

• For a Put Exercise, Put holders may sell stock at the strike price (to the Put seller).

• Neither Call holders nor Put holders are obligated to buy or sell; they simply have the rights to do so, and may choose to Exercise or not to Exercise based upon their own logic.

Obligation

• When an option holder chooses to exercise an option, a process begins to find a writer who is short the same kind of option (i.e., class, strike price and option type). Once found, that writer may be Assigned.

• This means that when buyers exercise, sellers may be chosen to make good on their obligations

• For a Call Assignment, Call writers are required to sell stock at the strike price to the Call holder.

• For a Put Assignment, Put writers are required to buy stock at the strike price from the Put holder.

Types of Options-American or European

• European option: These options give the holder the right, but not the obligation, to buy or sell the underlying instrument only on the expiry date. This means that the option cannot be exercised earlier or during the tenure of the contract. Settlement is based on a particular strike price at expiration.

• American option: These options give the holder the right, but not the obligation, to buy or sell the underlying instrument on or before the expiry date. This means that the option can be exercised early or during the tenure of the contract. Settlement is based on a particular strike price at expiration.

• All exchange traded options are American style• Names have no Geographical significance

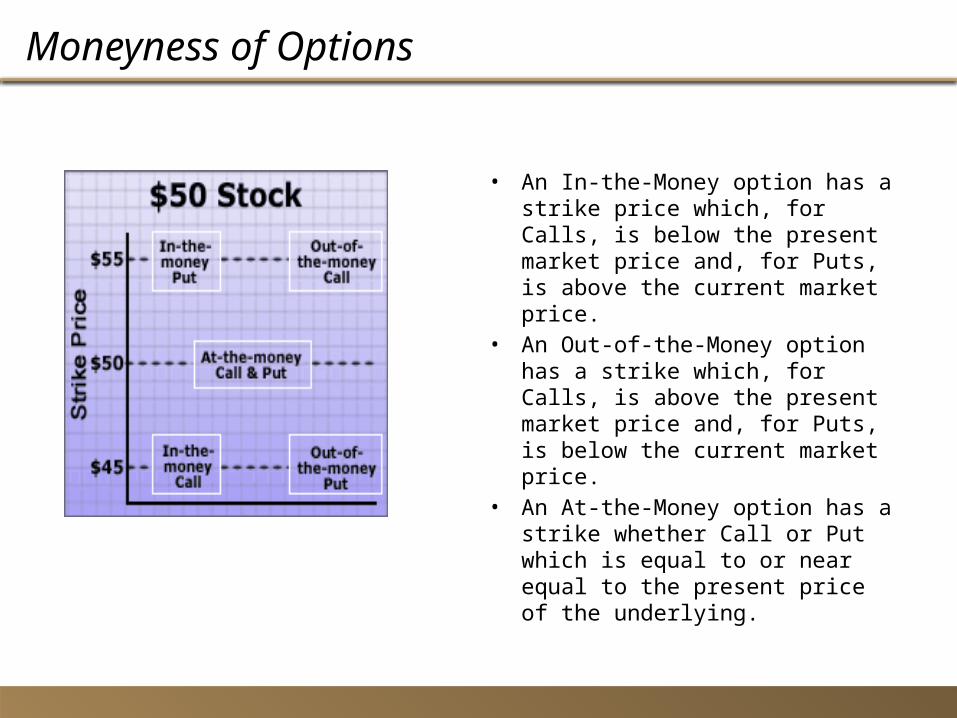

Moneyness of Options

• An In-the-Money option has a strike price which, for Calls, is below the present market price and, for Puts, is above the current market price.

• An Out-of-the-Money option has a strike which, for Calls, is above the present market price and, for Puts, is below the current market price.

• An At-the-Money option has a strike whether Call or Put which is equal to or near equal to the present price of the underlying.

ITM,ATM,OTM

Pricing of Options

• Options are priced using Black-Scholes Model with the following inputs:

• The price of the underlying stock• The strike price of the option• The time until the option expires• The cost of money (interest rates less

dividends if any)• The volatility of the underlying stock

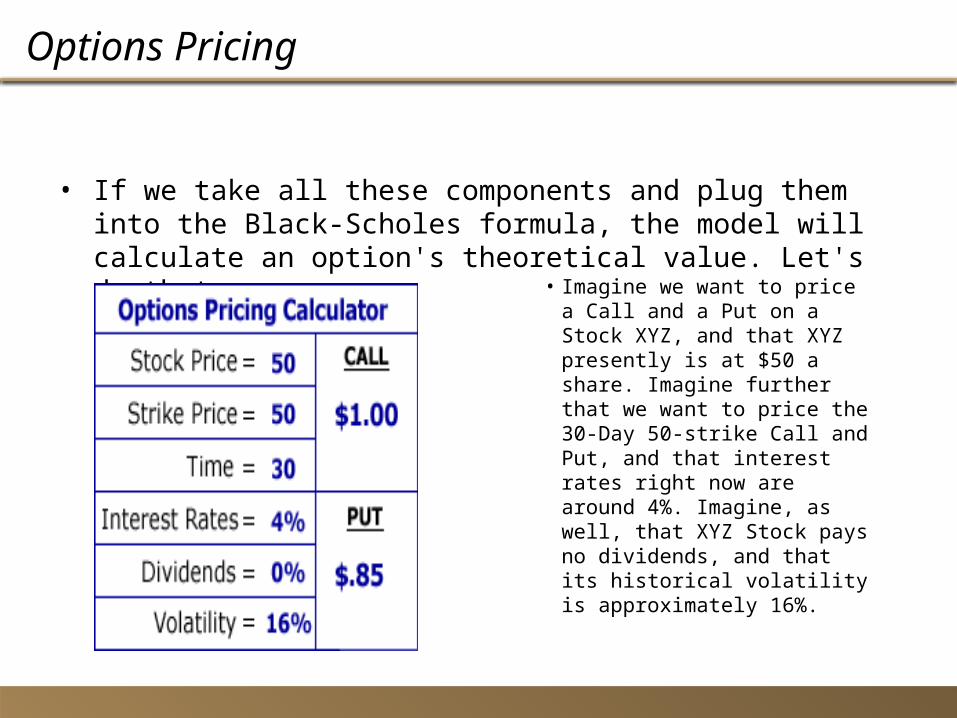

Options Pricing

• If we take all these components and plug them into the Black-Scholes formula, the model will calculate an option's theoretical value. Let's do that now:

• Imagine we want to price a Call and a Put on a Stock XYZ, and that XYZ presently is at $50 a share. Imagine further that we want to price the 30-Day 50-strike Call and Put, and that interest rates right now are around 4%. Imagine, as well, that XYZ Stock pays no dividends, and that its historical volatility is approximately 16%.

Volatility

• Volatility is important because it tells the formula how much to expect the stock price to move in a day, a week or a year. It is also important because it is the only unknown input in the pricing model! It is one that you, or the trading floor, or the market, or whoever, must predict!

• The 16% volatility of XYZ stock used here means that, on average, this stock is expected to trade in the range of $42-$58 most of the time or up or down 16%. It may or may not be correct, however, as the volatility increases both the Call and Put prices will increase

• As Volatility increases , so does the option premium

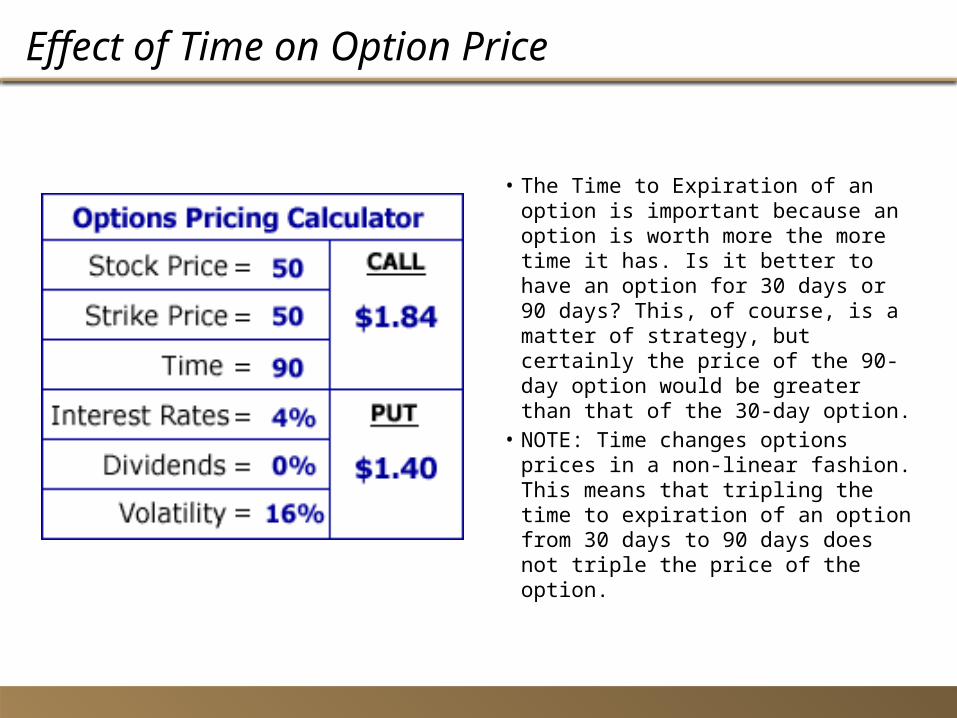

Effect of Time on Option Price

• The Time to Expiration of an option is important because an option is worth more the more time it has. Is it better to have an option for 30 days or 90 days? This, of course, is a matter of strategy, but certainly the price of the 90-day option would be greater than that of the 30-day option.

• NOTE: Time changes options prices in a non-linear fashion. This means that tripling the time to expiration of an option from 30 days to 90 days does not triple the price of the option.

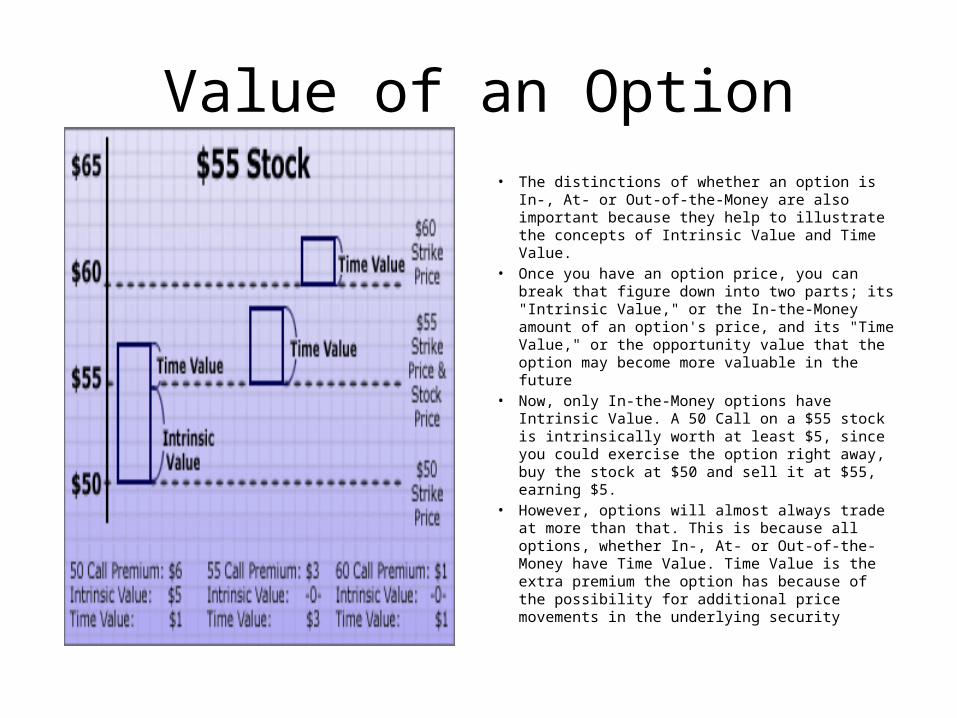

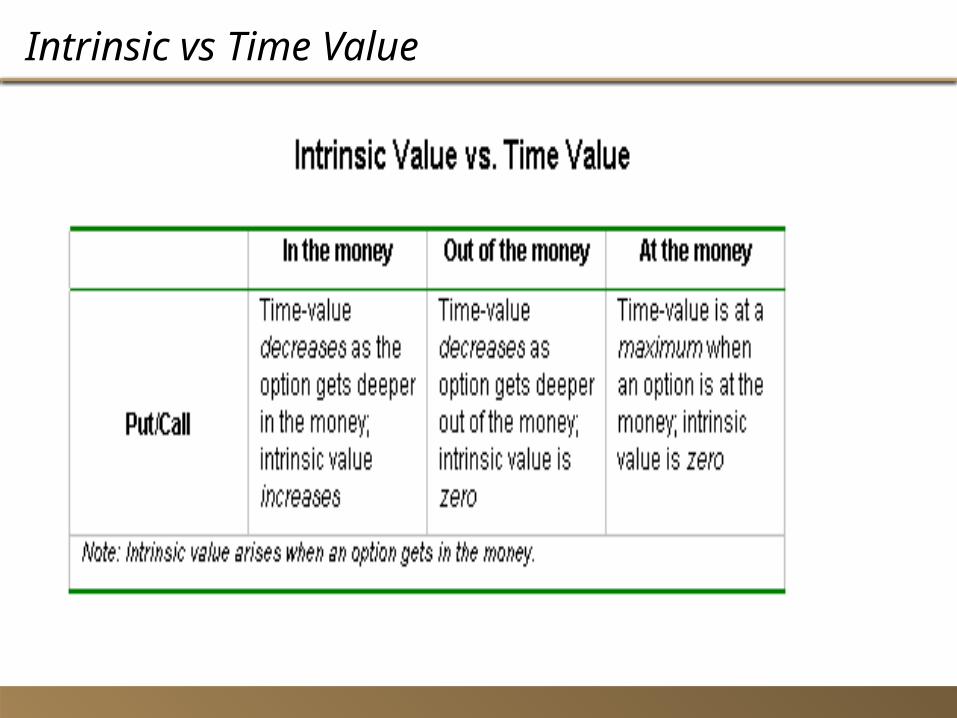

Value of an Option• The distinctions of whether an option is In-, At- or

Out-of-the-Money are also important because they help to illustrate the concepts of Intrinsic Value and Time Value.

• Once you have an option price, you can break that figure down into two parts; its "Intrinsic Value," or the In-the-Money amount of an option's price, and its "Time Value," or the opportunity value that the option may become more valuable in the future

• Now, only In-the-Money options have Intrinsic Value. A 50 Call on a $55 stock is intrinsically worth at least $5, since you could exercise the option right away, buy the stock at $50 and sell it at $55, earning $5.

• However, options will almost always trade at more than that. This is because all options, whether In-, At- or Out-of-the-Money have Time Value. Time Value is the extra premium the option has because of the possibility for additional price movements in the underlying security

Intrinsic Value

• Intrinsic value is the value that any given option would have if it were exercised today. Basically, the intrinsic value is the amount by which the strike price of an option is in the money. It is the portion of an option's price that is not lost due to the passage of time. The following equations can be used to calculate the intrinsic value of a call or put option:

• Call Option Intrinsic Value = Underlying Stock's Current Price – Call Strike Price

• Put Option Intrinsic Value = Put Strike Price – Underlying Stock's Current Price

Time Value of an option

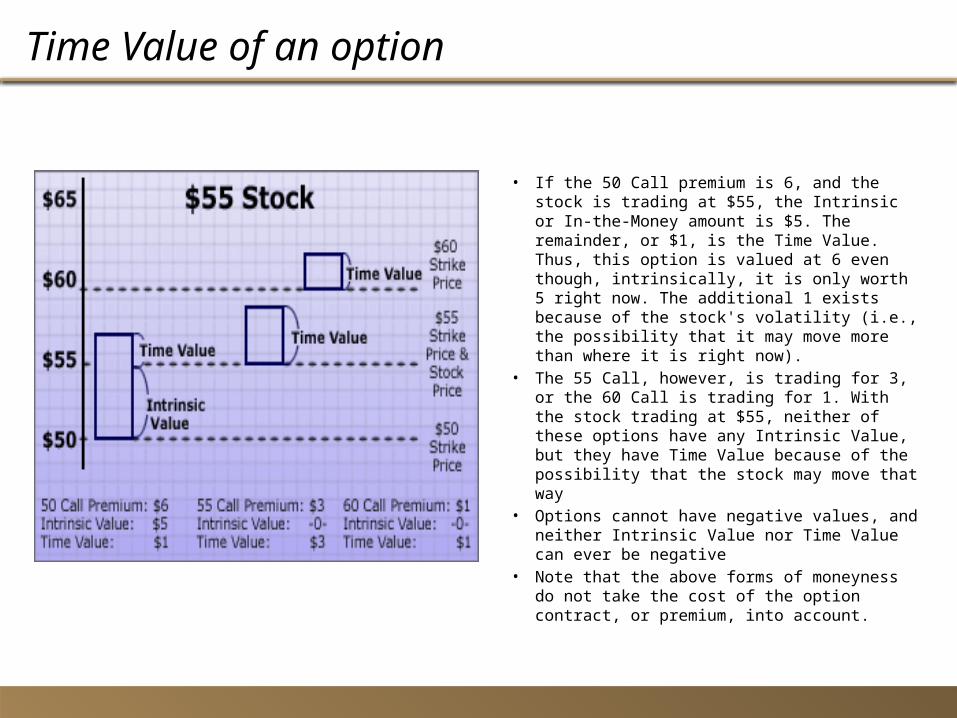

• If the 50 Call premium is 6, and the stock is trading at $55, the Intrinsic or In-the-Money amount is $5. The remainder, or $1, is the Time Value. Thus, this option is valued at 6 even though, intrinsically, it is only worth 5 right now. The additional 1 exists because of the stock's volatility (i.e., the possibility that it may move more than where it is right now).

• The 55 Call, however, is trading for 3, or the 60 Call is trading for 1. With the stock trading at $55, neither of these options have any Intrinsic Value, but they have Time Value because of the possibility that the stock may move that way

• Options cannot have negative values, and neither Intrinsic Value nor Time Value can ever be negative

• Note that the above forms of moneyness do not take the cost of the option contract, or premium, into account.

Intrinsic vs Time Value

Time Decay

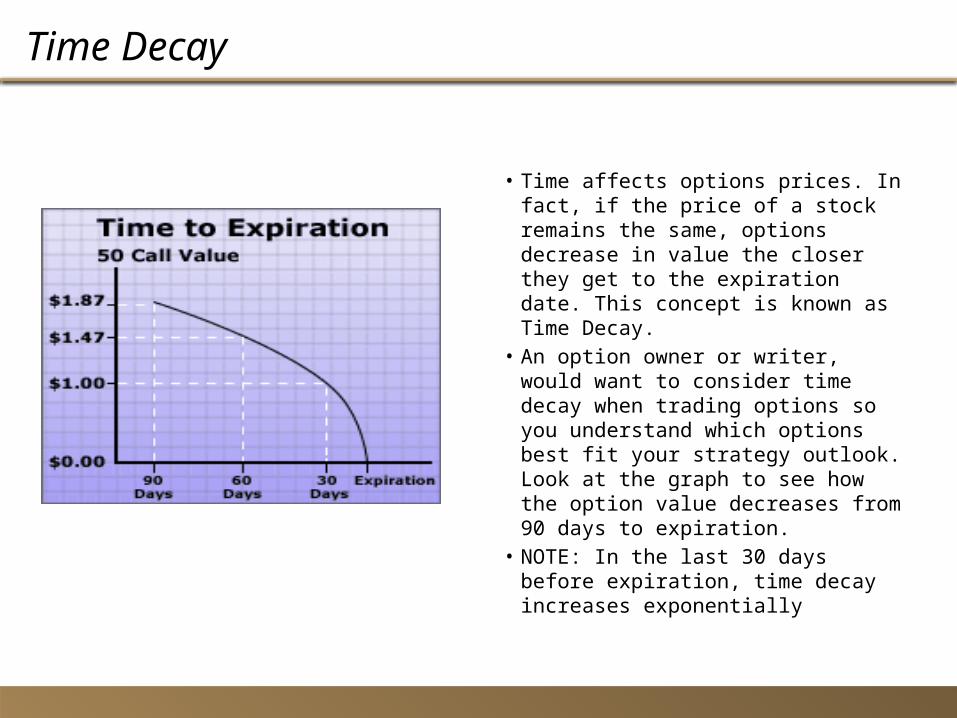

• Time affects options prices. In fact, if the price of a stock remains the same, options decrease in value the closer they get to the expiration date. This concept is known as Time Decay.

• An option owner or writer, would want to consider time decay when trading options so you understand which options best fit your strategy outlook. Look at the graph to see how the option value decreases from 90 days to expiration.

• NOTE: In the last 30 days before expiration, time decay increases exponentially

Volatility

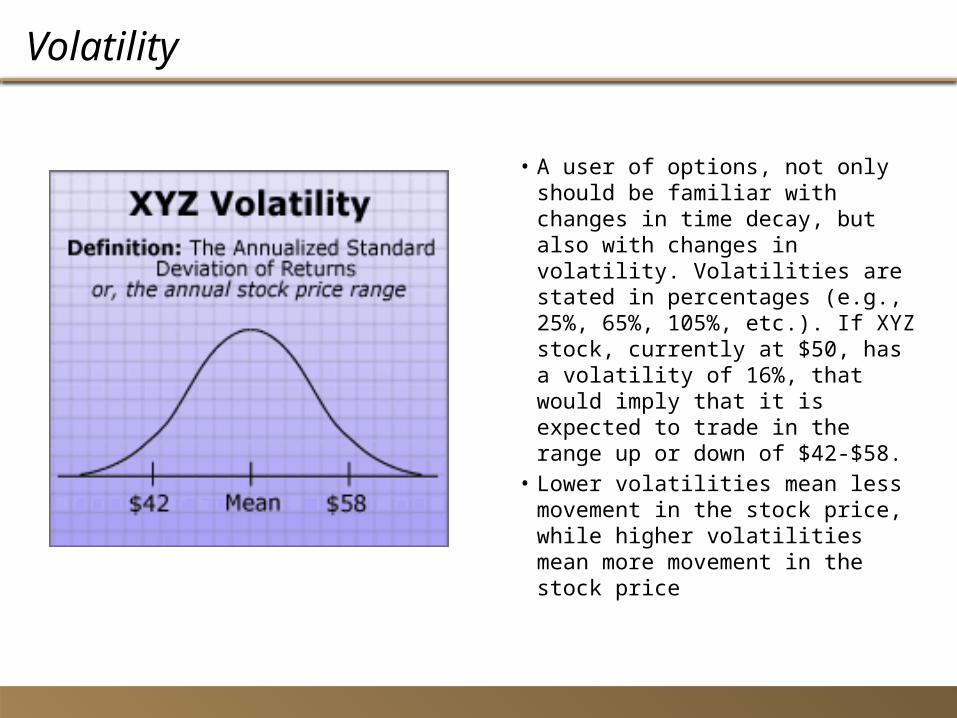

• A user of options, not only should be familiar with changes in time decay, but also with changes in volatility. Volatilities are stated in percentages (e.g., 25%, 65%, 105%, etc.). If XYZ stock, currently at $50, has a volatility of 16%, that would imply that it is expected to trade in the range up or down of $42-$58.

• Lower volatilities mean less movement in the stock price, while higher volatilities mean more movement in the stock price

Exercise of Options

• Most people believe that 90% of options expire worthless. However, this is untrue. Normally, only about 30% of options expire worthless in each monthly cycle

• Only about 10% of options are exercised during each monthly cycle, usually in the final week before expiration.

• In fact, over 60% of all options are traded out in the marketplace. This means that buyers sell their options in the market, and writers buy their positions back to close

Long and Short Call Positions

• Let's look at a typical long call. Let's say it is 1 MNO May 100 call @ 3; essentially the spot rate for the stock has to rise above $103 ($100 strike price plus $3 premium) to be in the money. In fact, the option begins life at $3 out of the money because of the premium

Short Call

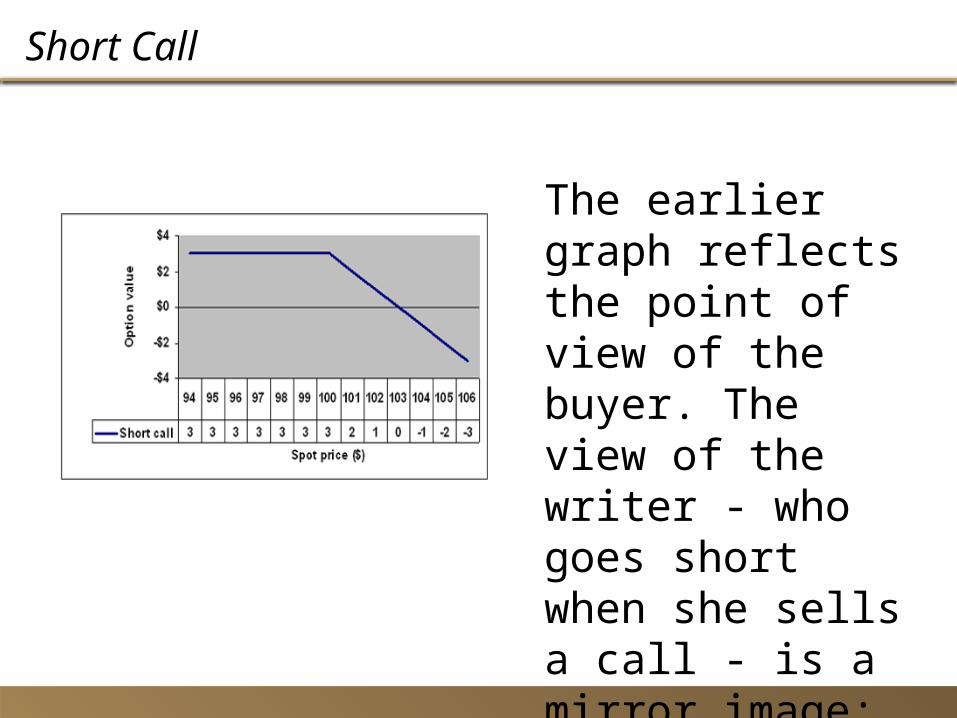

The earlier graph reflects the point of view of the buyer. The view of the writer - who goes short when she sells a call - is a mirror image:

Long and Short Put Positions

• Now let's look at puts. This example is a long put - a put from the perspective of the buyer. Similar to the previous example, let's say it is 1 MNO May 100 put @ 3; so essentially the spot rate for the stock has to sink below $97 ($100 strike price minus $3 premium) to be in the money. It does not matter how far above the strike price the spot price goes; if the option is going to cost the buyer more than the premium, he will simply let it expire unexercised

Short Put Positions

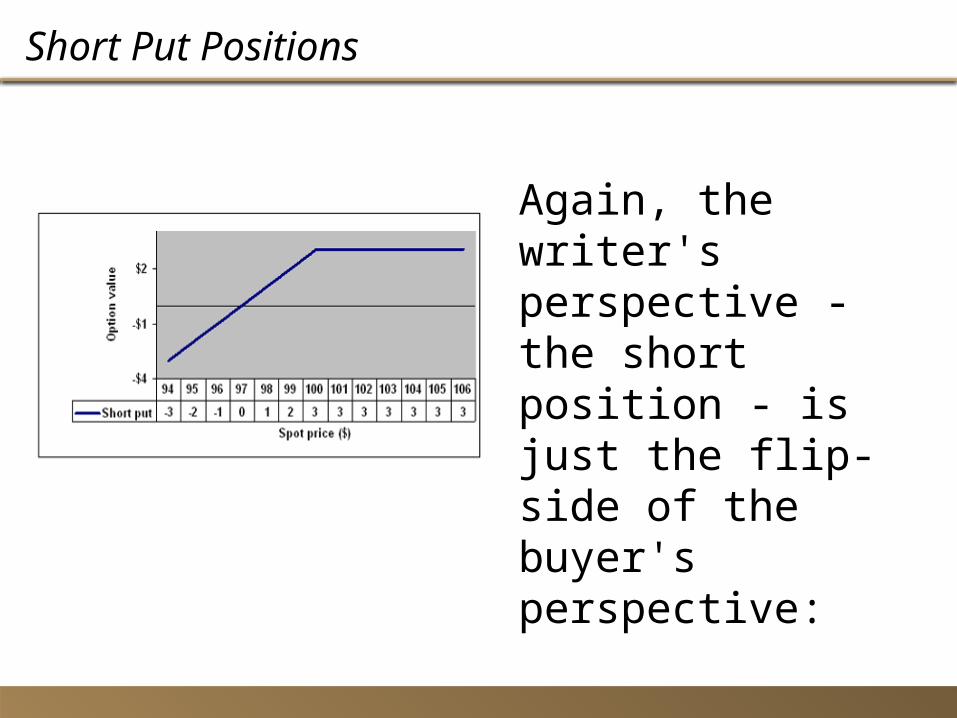

Again, the writer's perspective - the short position - is just the flip-side of the buyer's perspective:

Risk Profile of Buyers and Writers of options

Potential Profit/loss Buyer SellerProfit Unlimited PremiumLoss Premium Unlimited

How does the Option writer cover his risk

• Selling options can be dangerous and care must be exercised. We saw that when options are bought potential gain is unlimited and potential loss is restricted to premiums paid.

• When options are sold the effect is reversed: the potential loss is unlimited and the potential gain is simply premiums received from sale of options.

• How does the writer contain his risk- for that we need to undertsand the “greeks”

Greeks of Options

• When an option reaches maturity, its value is simply determined by the difference between its exercise price and the shares market price(intrinsic value).

• However before maturity its value is dependent upon, the exercise price, current stock price, time to expiry, volatility and risk-free interest rate.,

• Over time, with the exception of exercise price, all the other factors can be expected to change. Each time they change, this will lead to a change in market value of the option. The interactions are represented by the option “Greeks”

• Delta,Gamma,Theta,Vega,Rho(or phi)

Delta

• The relationship between the change in the market value of the option and the change in the share price is given by delta.

• Delta= Change in options market value divided by change in value of shares

• Delta can take any value between 0 and +1 for call options and any value between 0 and -1 for put options

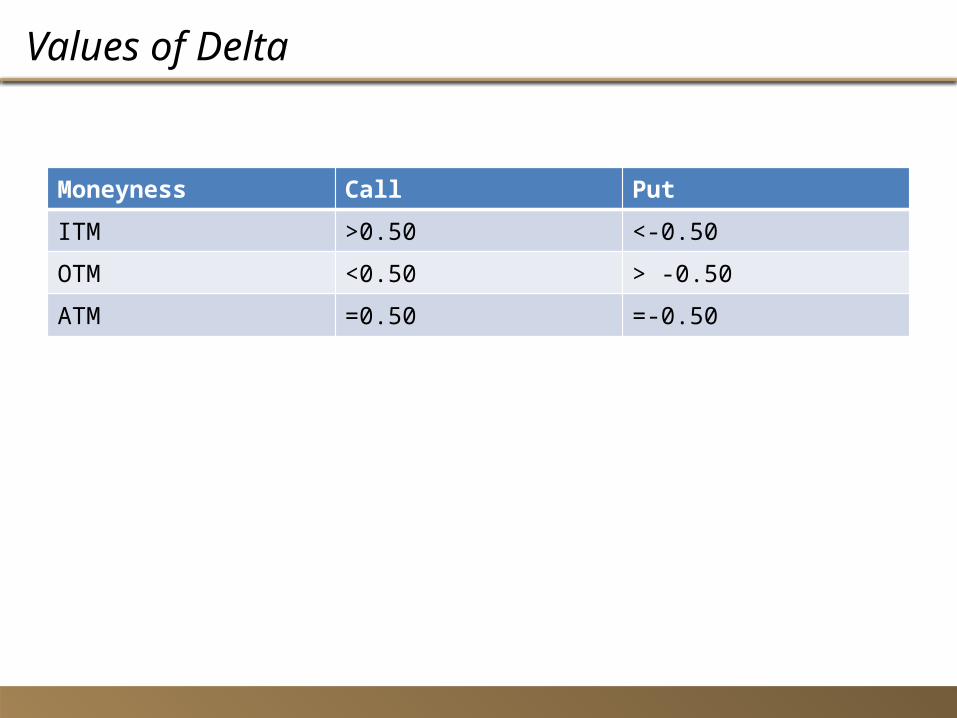

Values of Delta

Moneyness Call Put

ITM >0.50 <-0.50

OTM <0.50 > -0.50

ATM =0.50 =-0.50

Use of Delta

• Suppose call options on Coconut plc. Shares have delta of 0.60 this implies call are in-the-money and a 10p change in the share will lead to a 6p change in value of option.(0.60x10)

• Key interpretation is that it provides the “hedge ratio”.• For a call option writer, the higher the market price of the share, the greater is the

potential loss on the option when the holder exercises• The Hedge Ratio tells the option writer how to hedge (avoid) the risk of this loss by

indicating the number of shares that would have to be held in order to offset any potential loss on the calls.

• In the Coconut Company example if we have sold calls on 1000 shares we would have to buy and hold 1000x0.60 shares or 600 shares, to offset any potential loss on the options.

• If Coconut shares rise by 5p, the value of the calls would increase by 5x0.60 or 3p. And so the writers loss on the 1000 calls would be 1000x0.03= GBP 30 which would be exactly offset by the profit on Coconut shareholding ie 600 sharesx0.05=GBP 30

Share option Trading Strategies

• When investors open a position by buying Calls, they are long those options. When investors open a position by selling Calls, they are short those options.

• To close the positions, the buyer could sell his long Calls back in the marketplace, and the seller could buy the short Calls back in the marketplace

• Put Positions are different from Call positions in that the owner has the right to sell, not buy, the underlying security

• When investors open a position by buying Puts, they are long those options. When investors open a position by selling Puts, they are short those options.

• Once again, if you are long options, you have the right to exercise; if you are short options, you have the obligation of assignment.

• You can, however, always close either position in the marketplace, by simply selling if long and buying back if short

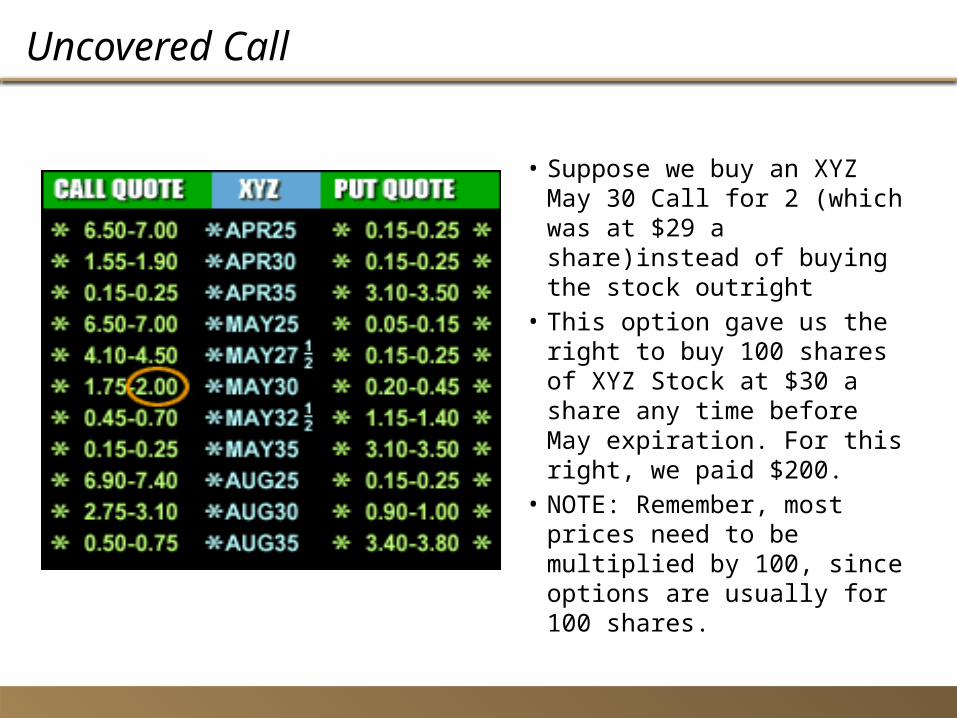

Uncovered Call

• Suppose we buy an XYZ May 30 Call for 2 (which was at $29 a share)instead of buying the stock outright

• This option gave us the right to buy 100 shares of XYZ Stock at $30 a share any time before May expiration. For this right, we paid $200.

• NOTE: Remember, most prices need to be multiplied by 100, since options are usually for 100 shares.

Values of Call

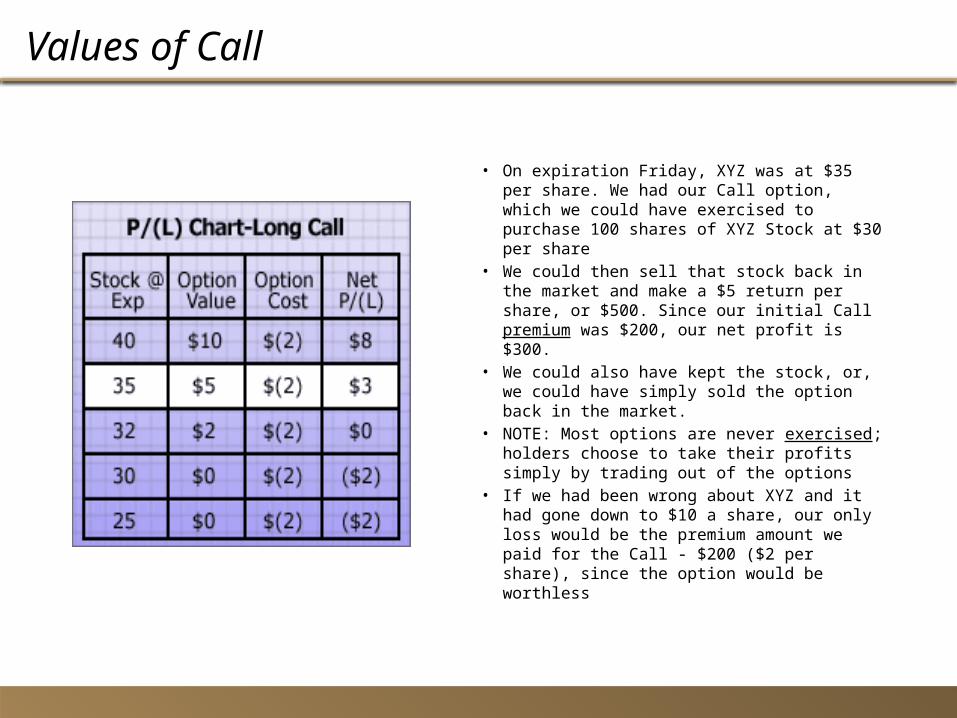

• On expiration Friday, XYZ was at $35 per share. We had our Call option, which we could have exercised to purchase 100 shares of XYZ Stock at $30 per share

• We could then sell that stock back in the market and make a $5 return per share, or $500. Since our initial Call premium was $200, our net profit is $300.

• We could also have kept the stock, or, we could have simply sold the option back in the market.

• NOTE: Most options are never exercised; holders choose to take their profits simply by trading out of the options

• If we had been wrong about XYZ and it had gone down to $10 a share, our only loss would be the premium amount we paid for the Call - $200 ($2 per share), since the option would be worthless

Protective Puts

• we had bought some XYZ at a price of $31 a share, and it was trading up at $32 a share.

• But, we were concerned that an adverse market move might have caused our investment in XYZ to lose money, so we bought an XYZ Aug 30 Put for 1.

• This gave us the right to sell our stock at a price of $30 a share in the event it had gone down in value. Since we owned 100 shares, and each option is for 100 shares, we bought one Put, and for this, we paid $100

• We bought the XYZ Aug 30 Put, which gave us the right to sell our stock at $30 a share, no matter how low it went.

Protective Puts(contd.)

• Protective Puts act like an insurance policy on our stock, and protect us against losses below $30 a share.

• If the price remains above $30 need not exercise the Put, since we were the holder and had the choice

• If the Price trades below $30 we can exercise the put and deliver the stock at $30, thus restricting our loss.

Buying a Put Option

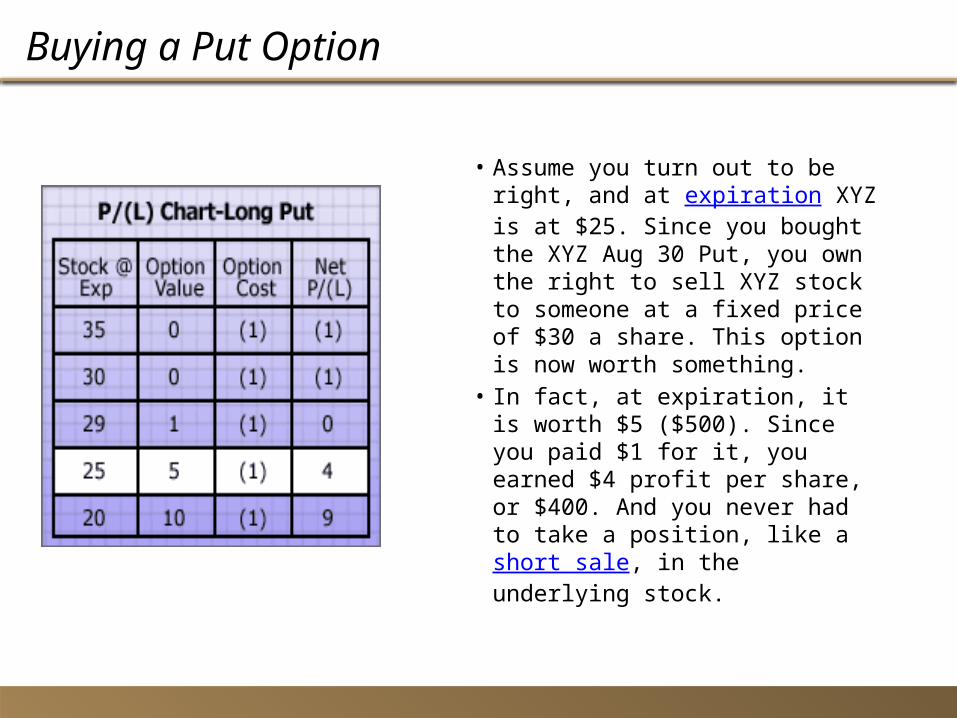

• Assume you turn out to be right, and at expiration XYZ is at $25. Since you bought the XYZ Aug 30 Put, you own the right to sell XYZ stock to someone at a fixed price of $30 a share. This option is now worth something.

• In fact, at expiration, it is worth $5 ($500). Since you paid $1 for it, you earned $4 profit per share, or $400. And you never had to take a position, like a short sale, in the underlying stock.

Short Straddle

WRITE CALL & PUT OPTIONS If you expect the Stock to show very little volatility, it is worthwhile to write a call & put option. ABC stock – has been range bound for the last 3 months. You don’t expect it to move up or down too much. ABC Spot Price $ 25 Premium of 25 Call $ 1.5Premium on 25 Put $ 1.5 Sell $.25 Call and $25 Put Total Premium Received = $.3 . Investor incurs a loss incase price drops below $. 22 or goes up above $. 28 Risky Strategy since profits limited but losses unlimited.

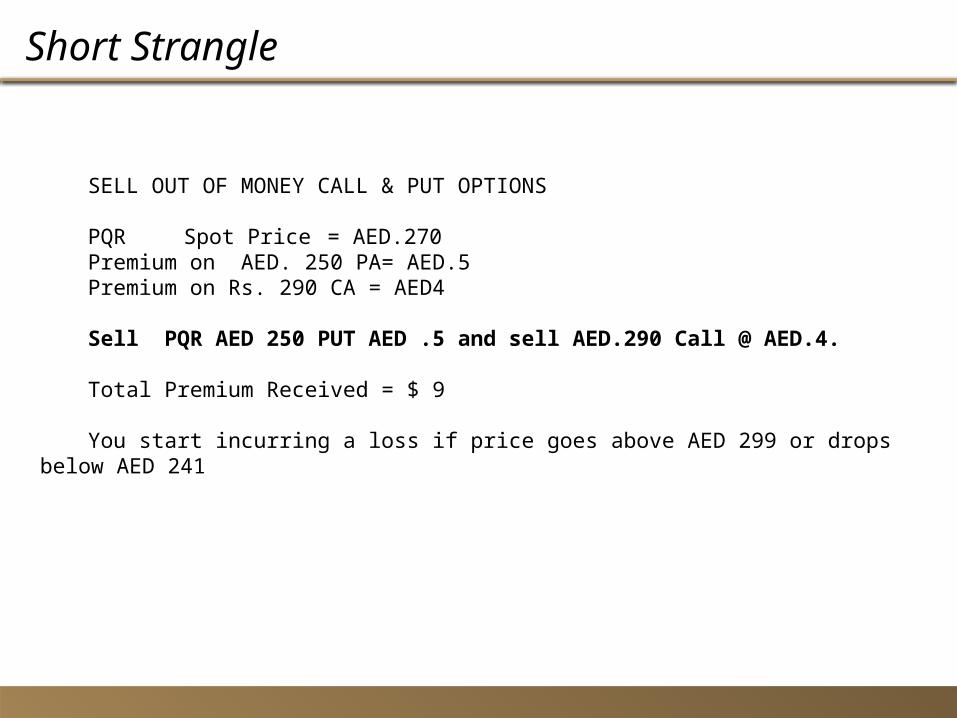

SELL OUT OF MONEY CALL & PUT OPTIONS PQR Spot Price = AED.270Premium on AED. 250 PA= AED.5Premium on Rs. 290 CA = AED4

Sell PQR AED 250 PUT AED .5 and sell AED.290 Call @ AED.4. Total Premium Received = $ 9

You start incurring a loss if price goes above AED 299 or drops below AED 241

Short Strangle

Straddle

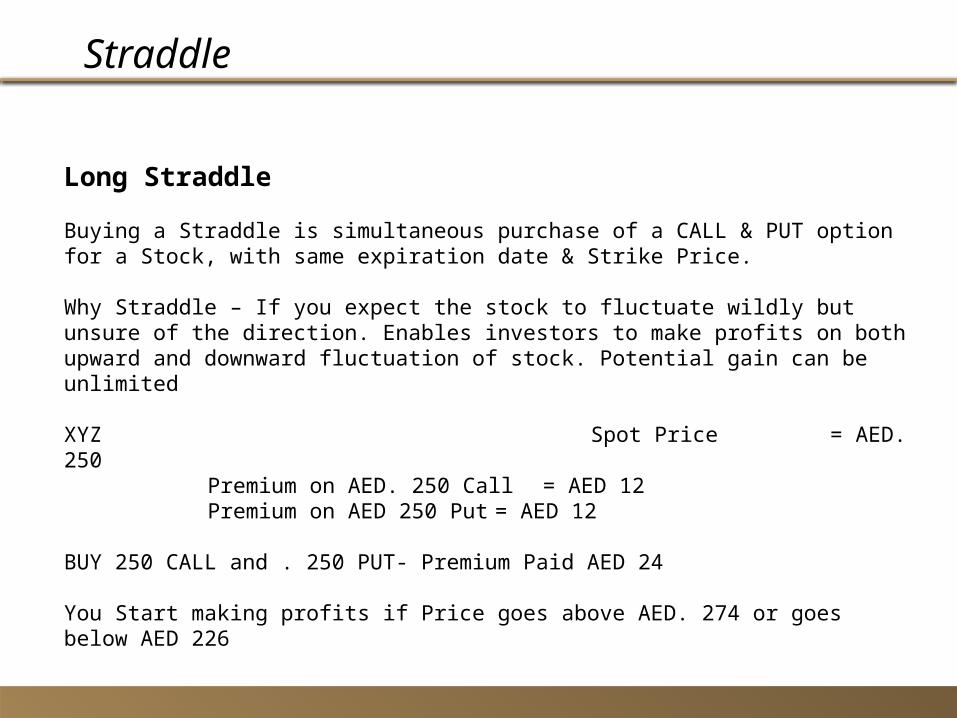

Long Straddle Buying a Straddle is simultaneous purchase of a CALL & PUT option for a Stock, with same expiration date & Strike Price. Why Straddle – If you expect the stock to fluctuate wildly but unsure of the direction. Enables investors to make profits on both upward and downward fluctuation of stock. Potential gain can be unlimited XYZ Spot Price = AED. 250

Premium on AED. 250 Call = AED 12Premium on AED 250 Put = AED 12

BUY 250 CALL and . 250 PUT- Premium Paid AED 24 You Start making profits if Price goes above AED. 274 or goes below AED 226

Strangle

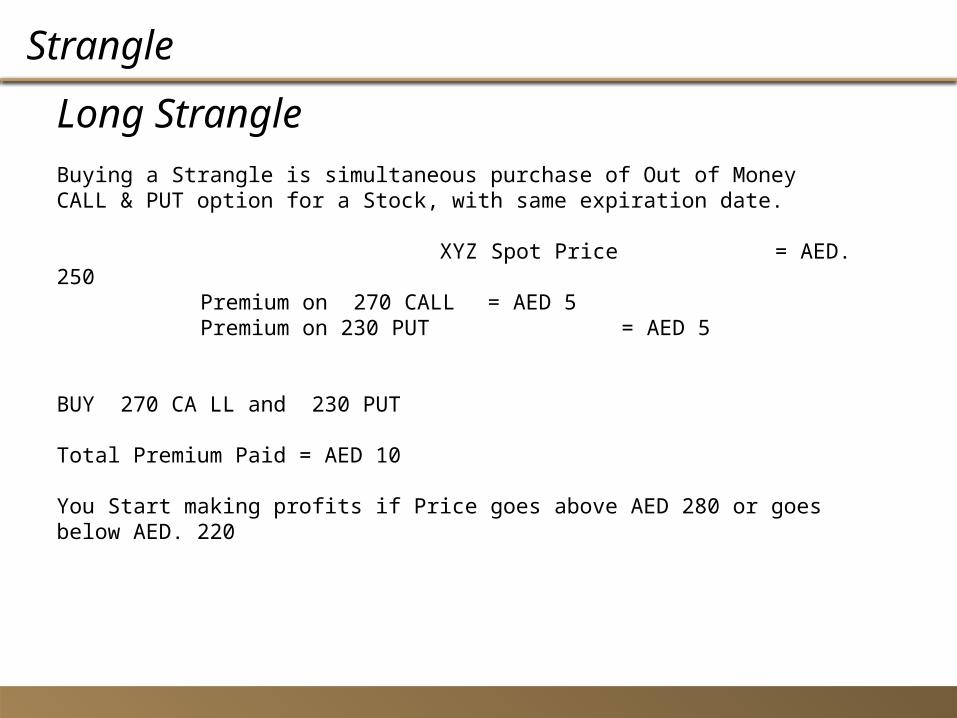

Long Strangle Buying a Strangle is simultaneous purchase of Out of Money CALL & PUT option for a Stock, with same expiration date. XYZ Spot Price = AED. 250

Premium on 270 CALL = AED 5Premium on 230 PUT = AED 5

BUY 270 CA LL and 230 PUT Total Premium Paid = AED 10 You Start making profits if Price goes above AED 280 or goes below AED. 220

Swaps

What are swaps?

• A swap is an agreement between to two parties to exchange payments or income over a period of time

• The swapped payments might be in different currencies(currency swap) or at different rates of interest( interest rate swaps)

• Both Liabilities and assets can be swapped• Asset swaps involve exchange of income on one investment for income in

another• Liability swaps, which are more common, involve an exchange of

payments on one debt(liability) for payments on another.• A currency swap is an agreement to exchange payments in one currency

for payments in another.• Since swaps are derived from underlying transactions in the cash markets

for currency borrowing, they are classed as derivative instruments.

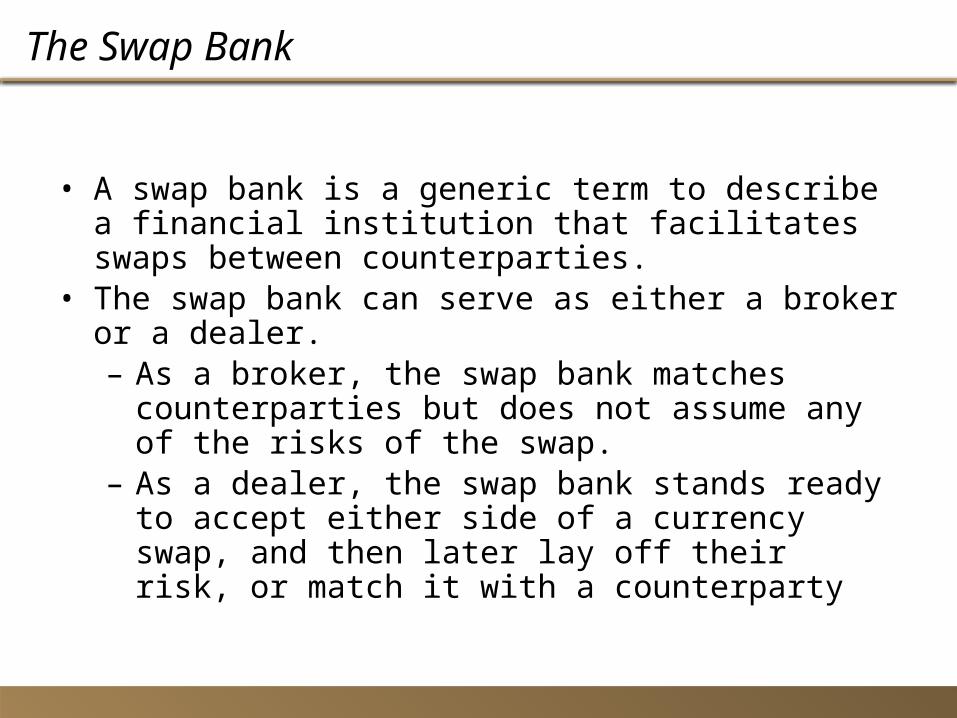

The Swap Bank

• A swap bank is a generic term to describe a financial institution that facilitates swaps between counterparties.

• The swap bank can serve as either a broker or a dealer.– As a broker, the swap bank matches counterparties but

does not assume any of the risks of the swap.– As a dealer, the swap bank stands ready to accept either

side of a currency swap, and then later lay off their risk, or match it with a counterparty

Interest swaps

• Interest rate swaps(IRS) involve periodic payments to settle interest costs on a notional principal.

• Normally in a plain vanilla IRS, there is an exchange of fixed-rate interest rate for a floating rate interest rate.

• The entity paying fixed- rate is called a fixed rate payer ( and a floating rate receiver)

• The entity paying floating rate is called a floating-rate payer ( and a fixed-rate receiver)

• Fixed interest rates are paid or received and so also in the case of floating rate

• Settlement for interest costs can involve either a two-way exchange of interest payment or a single settlement of the difference between the two amounts.

Currency Swaps

• A plain vanilla currency swap is an agreement between two parties to exchange a quantity of one currency for another .

• There is an exchange of principal at the start of the agreement.(near value-date) at an agreed rate( typically spot rate)

• A re-exchange of the same quantities at the end of the agreement( far-value-date)

• Periodic intermediate payments to settle interest costs in each currency at an agreed interval during the term of the swap.

• The settlements for interest costs can involve either a two-way exchange of interest payments in each currency or a single settlement of the difference between the two amounts in one of the currencies to the swap.

• Currency swaps need not involve an exchange of principal at the near-value-date in which case there is only periodic exchange of interest payments and exchange of principal at the far-value date, with currency amounts exchanged at a rate fixed in the swap agreement.

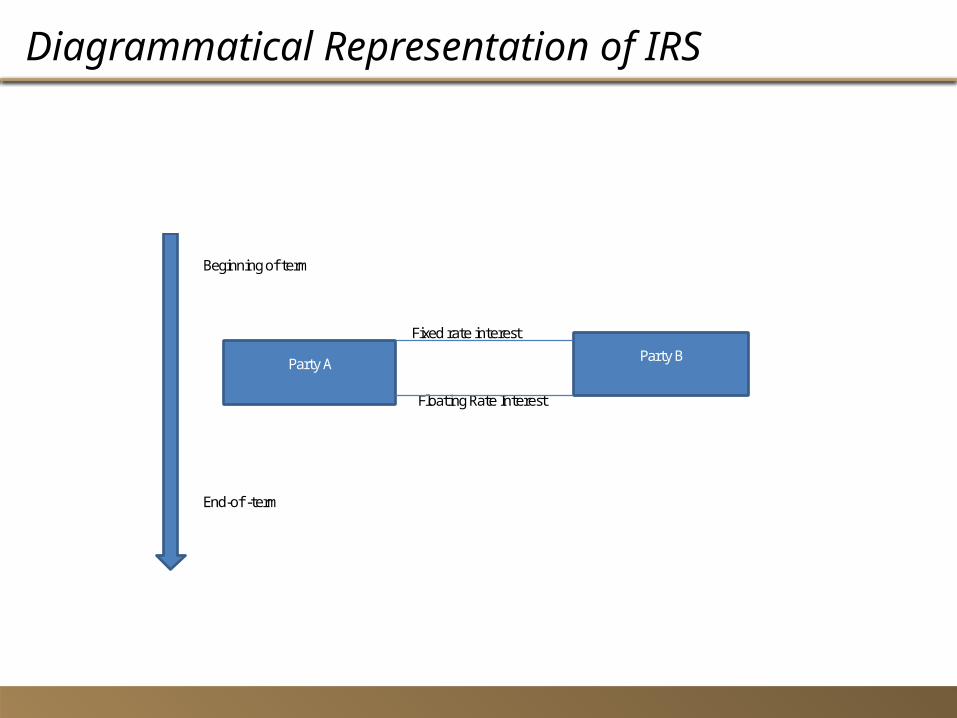

What happens in a IRS ?

• Party A wants to take on the liability of paying fixed rate interest payments in USD for several years on a notional principal

• Party B wants to assume the same amount of liability but as floating-rate USD payments linked to LIBOR for the same period.(It is called floating because LIBOR is repriced every periodically as agreed))

• Party A can borrow floating rate loan and party B can borrow fixed-rate loan separately(separate from swap transaction)

• Under the swap agreement the parties will swap their loan interest payment liabilities. Part A pays fixed rate to B and Party B pays floating rate to A.

• Their payments under the swap are separate and independent of the interest payments they make on their loan liabilities

• The swap enables party A to exchange liability from floating rate to fixed rate and B from Fixed rate to floating.

• Party A pays fixed and receives floating, while B pays floating and receives fixed.

Diagrammatical Representation of IRS

Beginning of term

Fixed rate interest

Floating Rate Interest

End-of -term

Party A Party B

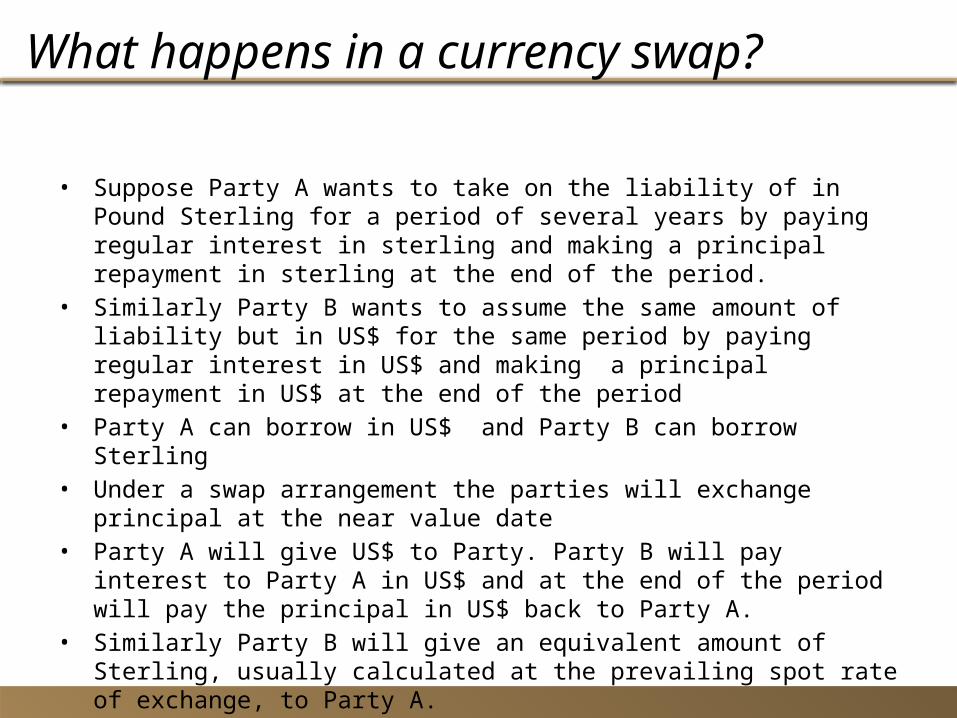

What happens in a currency swap?

• Suppose Party A wants to take on the liability of in Pound Sterling for a period of several years by paying regular interest in sterling and making a principal repayment in sterling at the end of the period.

• Similarly Party B wants to assume the same amount of liability but in US$ for the same period by paying regular interest in US$ and making a principal repayment in US$ at the end of the period

• Party A can borrow in US$ and Party B can borrow Sterling• Under a swap arrangement the parties will exchange principal at the near value

date• Party A will give US$ to Party. Party B will pay interest to Party A in US$ and at the

end of the period will pay the principal in US$ back to Party A.• Similarly Party B will give an equivalent amount of Sterling, usually calculated at

the prevailing spot rate of exchange, to Party A.• Party A will then pay interest in Sterling to Party B, and at the end of the swap

period, will pay back the sterling back to Party B.

Diagrammatic representation of currency swap

Time Party A Party B

Near Value- Date

Exchange of Principal at an agreed rate of exchange

Periodical Intervals

Exchange of Interest payments at previously

agreed rates of payment

Far- value-Date

Re-exchange of Principal at the same

rate of exchange as for the original

exchange at the near-value date

US$ GBP

GBP Interest US$ Interest

GBP US$

The QSD

• The Quality Spread Differential represents the potential gains from the swap that can be shared between the counterparties and the swap bank.

• There is no reason to presume that the gains will be shared equally.

$ €

A $7% €6%

B $8% €5%

QSD 1% – –1% = 2%

The QSD is calculated as the difference between the differences.

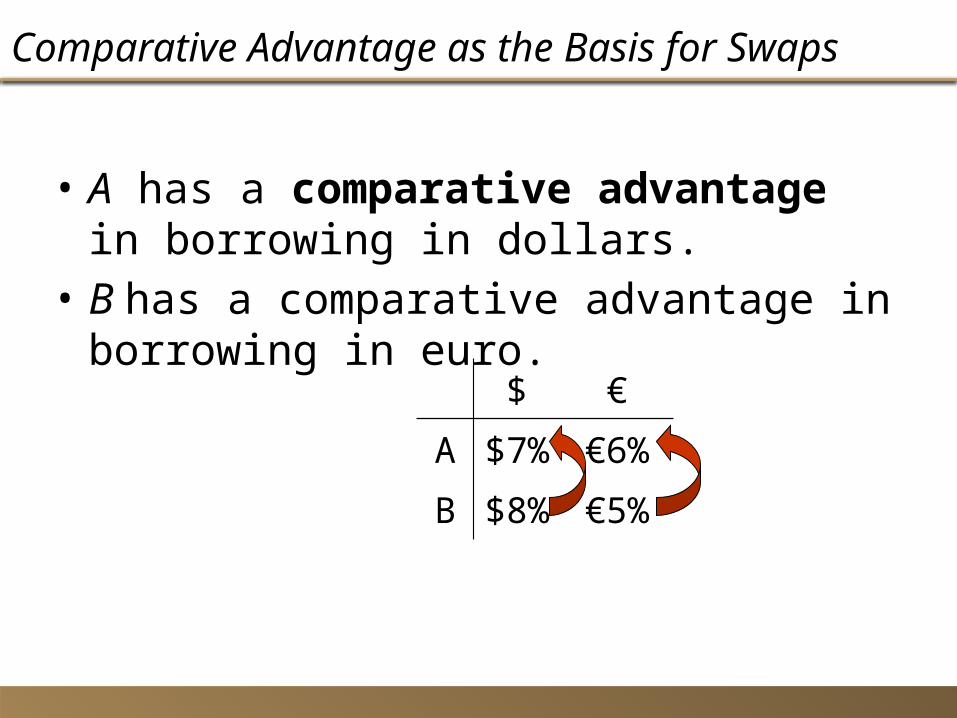

Comparative Advantage as the Basis for Swaps

$ €

A $7%

€6%

B $8%

€5%

• A has a comparative advantage in borrowing in dollars.

• B has a comparative advantage in borrowing in euro.

Variations of Basic Currency and Interest Rate Swaps

Risks of Interest Rate and Currency Swaps

Risks of Interest Rate and Currency Swaps (cont.)

• Credit Risk– This is the major risk faced by a swap dealer—the

risk that a counter party will default on its end of the swap.

• Mismatch Risk– It’s hard to find a counterparty that wants to

borrow the right amount of money for the right amount of time.

• Sovereign Risk– The risk that a country will impose exchange rate

restrictions that will interfere with performance on the swap.

Sample Interest Rate Swap Problem

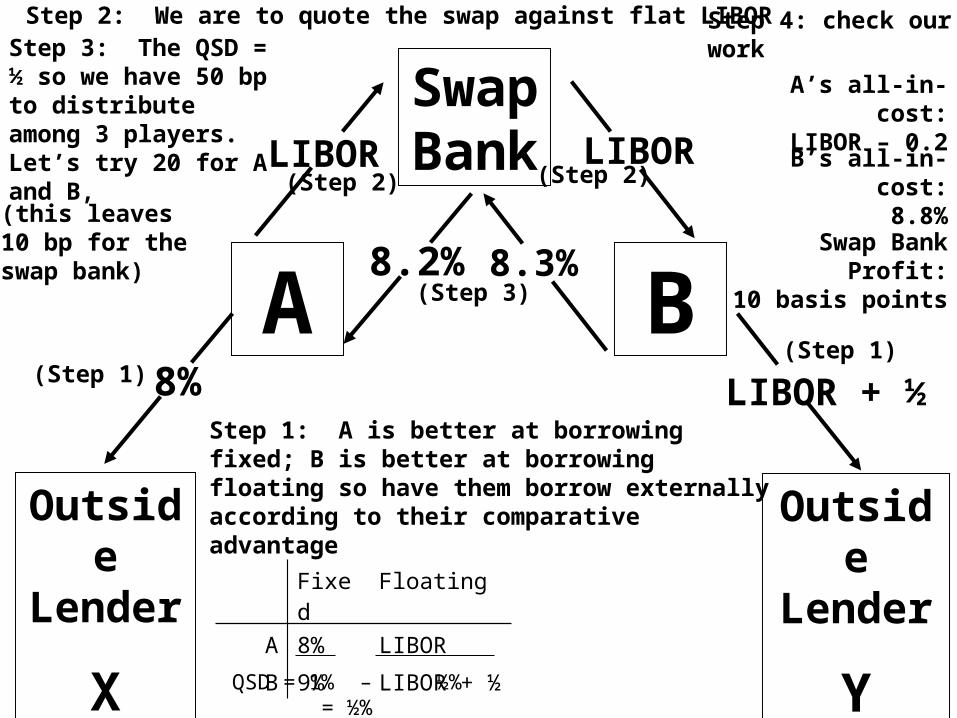

• A is a credit-worthy firm– A can borrow at 8% fixed– A can borrow at flat LIBOR– A prefers to borrow floating

• B is a less-credit-worthy firm– B can borrow at 9% fixed– B can borrow at LIBOR + ½%– B prefers to borrow fixed

• Both firms want a 10-year maturity• Devise a swap that is mutually beneficial for A and B.

• Follow the convention of pricing against “flat” LIBOR.

Fixed Floating

A 8% LIBOR

B 9% LIBOR + ½

A B

Swap

Bank

Outside

Lender

X

Outside

Lender

Y

Fixed Floating

A 8% LIBOR

B 9% LIBOR + ½ QSD = 1% – ½% =

½%

Step 1: A is better at borrowing fixed; B is better at borrowing floating so have them borrow externally according to their comparative advantage

Step 2: We are to quote the swap against flat LIBOR

8%(Step 1)LIBOR + ½

(Step 1)

LIBOR(Step 2)

LIBOR(Step 2)

Step 3: The QSD = ½ so we have 50 bp to distribute among 3 players. Let’s try 20 for A and B, (this leaves 10 bp for the swap bank) 8.2%

(Step 3)8.3%

Step 4: check our work

A’s all-in-cost:LIBOR – 0.2

B’s all-in-cost:8.8%

Swap Bank Profit:

10 basis points

Interest rate Derivatives

• Interest rate forwards• FRAs• Interest rate Futures• Interest rate Options

Forward-Forward Loan

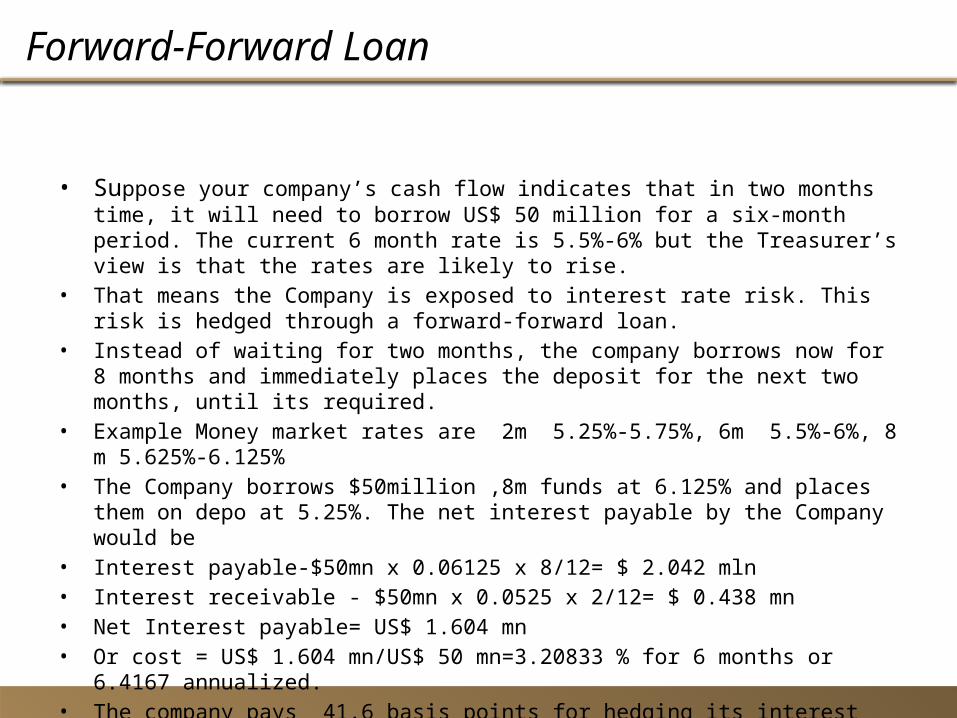

• Suppose your company’s cash flow indicates that in two months time, it will need to borrow US$ 50 million for a six-month period. The current 6 month rate is 5.5%-6% but the Treasurer’s view is that the rates are likely to rise.

• That means the Company is exposed to interest rate risk. This risk is hedged through a forward-forward loan.

• Instead of waiting for two months, the company borrows now for 8 months and immediately places the deposit for the next two months, until its required.

• Example Money market rates are 2m 5.25%-5.75%, 6m 5.5%-6%, 8 m 5.625%-6.125%• The Company borrows $50million ,8m funds at 6.125% and places them on depo at 5.25%.

The net interest payable by the Company would be• Interest payable-$50mn x 0.06125 x 8/12= $ 2.042 mln• Interest receivable - $50mn x 0.0525 x 2/12= $ 0.438 mn• Net Interest payable= US$ 1.604 mn • Or cost = US$ 1.604 mn/US$ 50 mn=3.20833 % for 6 months or 6.4167 annualized.• The company pays 41.6 basis points for hedging its interest rate

FRAs(Forward Rate Agreements)

• Forward-Forward loans are relatively unusual now

• Instead of operating in the loan and depo market, the Company could approach the bank for fixing its 6 months loan rate in two months time.

• This is a Forward rate agreement- a mechanism by which a Company can lock itself into a rate of interest today for a future loan.

How does a FRA operate

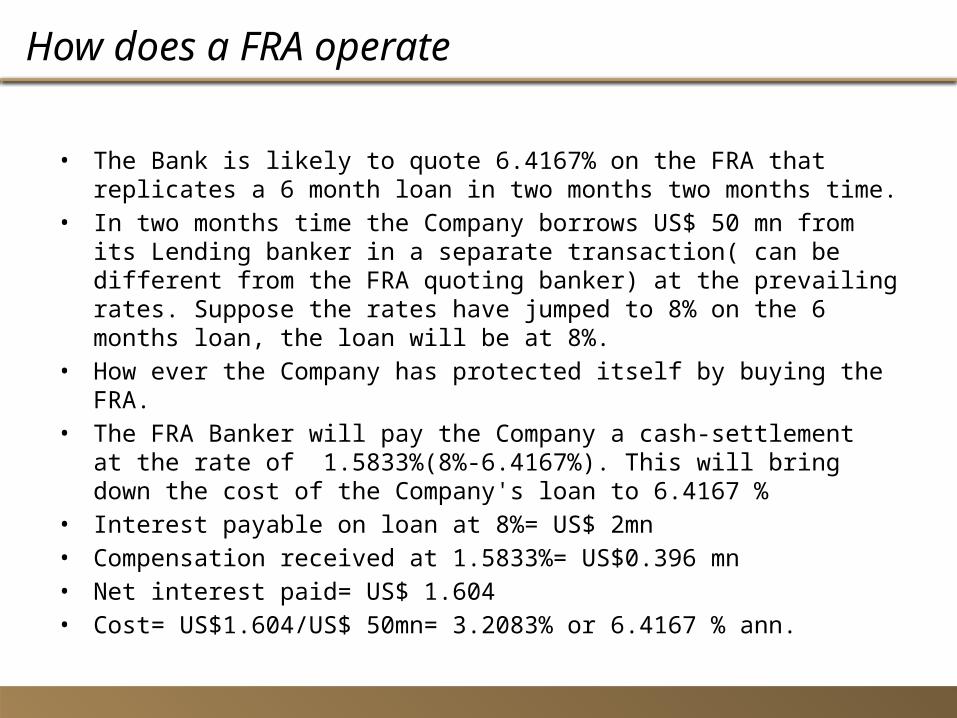

• The Bank is likely to quote 6.4167% on the FRA that replicates a 6 month loan in two months two months time.

• In two months time the Company borrows US$ 50 mn from its Lending banker in a separate transaction( can be different from the FRA quoting banker) at the prevailing rates. Suppose the rates have jumped to 8% on the 6 months loan, the loan will be at 8%.

• How ever the Company has protected itself by buying the FRA.• The FRA Banker will pay the Company a cash-settlement at the rate of

1.5833%(8%-6.4167%). This will bring down the cost of the Company's loan to 6.4167 %

• Interest payable on loan at 8%= US$ 2mn• Compensation received at 1.5833%= US$0.396 mn• Net interest paid= US$ 1.604 • Cost= US$1.604/US$ 50mn= 3.2083% or 6.4167 % ann.

FRA example

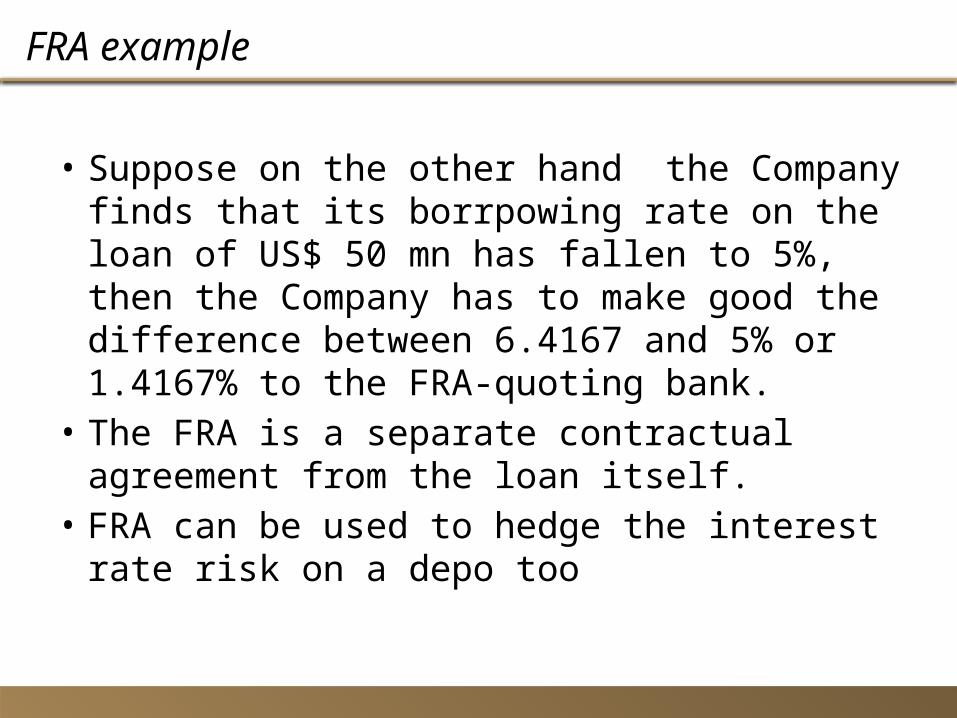

• Suppose on the other hand the Company finds that its borrpowing rate on the loan of US$ 50 mn has fallen to 5%, then the Company has to make good the difference between 6.4167 and 5% or 1.4167% to the FRA-quoting bank.

• The FRA is a separate contractual agreement from the loan itself.

• FRA can be used to hedge the interest rate risk on a depo too

Interest Rate Futures

• Buying an interest rate futures contract allows the buyer of the contract to lock in a future investment rate; not a borrowing rate as many believe. Interest rate futures are based off an underlying security which is a debtobligation and moves in value as interest rates change.

• When interest rates move higher, the buyer of the futures contract will pay the seller in an amount equal to that of the benefit received by investing at a higher rate versus that of the rate specified in the futures contract. Conversely, when interest rates move lower, the seller of the futures contract will compensate the buyer for the lower interest rate at the time of expiration.

• To determine the gain or loss of an interest rate futures contract, an interest rate futures price index was created. When buying, the index can be calculated by subtracting the futures interest rate from 100, or (100 - Futures Interest Rate). As rates fluctuate, so does this price index. As rates increase, the index moves lower and vice versa

Example of Hedging with Interest rate Futures

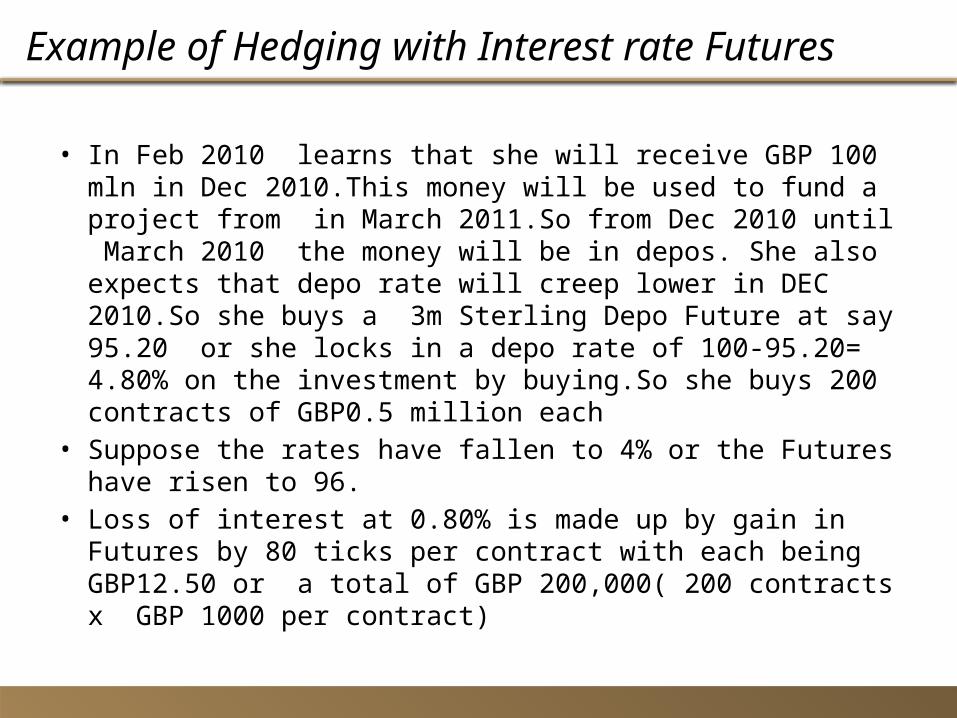

• In Feb 2010 learns that she will receive GBP 100 mln in Dec 2010.This money will be used to fund a project from in March 2011.So from Dec 2010 until March 2010 the money will be in depos. She also expects that depo rate will creep lower in DEC 2010.So she buys a 3m Sterling Depo Future at say 95.20 or she locks in a depo rate of 100-95.20= 4.80% on the investment by buying.So she buys 200 contracts of GBP0.5 million each

• Suppose the rates have fallen to 4% or the Futures have risen to 96.

• Loss of interest at 0.80% is made up by gain in Futures by 80 ticks per contract with each being GBP12.50 or a total of GBP 200,000( 200 contracts x GBP 1000 per contract)

Interest rate Options

• Interest Rate Options are short-term options on short-term interest rates.They are part of the debt options market and include medium term options on short-term interest rates like caps, floors and collars and options on bonds.

• Market for Interest options includes exchange traded contracts and OTC contracts

Single Traded calls and Puts

• Traded interest rate options are individual calls and puts , usually on money-market futures,

• The underlying asset is a US$ 1 million future contract on the 3 months EuroDollar depo.

• Quotations are in terms of an index which quotes as 100 less than the annualized rate.

• The holder of a call options benefits when interest rates fall and index rises

• Holders of put options benefit when rates rise and index falls.• Borrowers are wishing to hedge rising rates are natural holders

of put options; Lenders wishing to lock in a floor rate are natural holders of call options

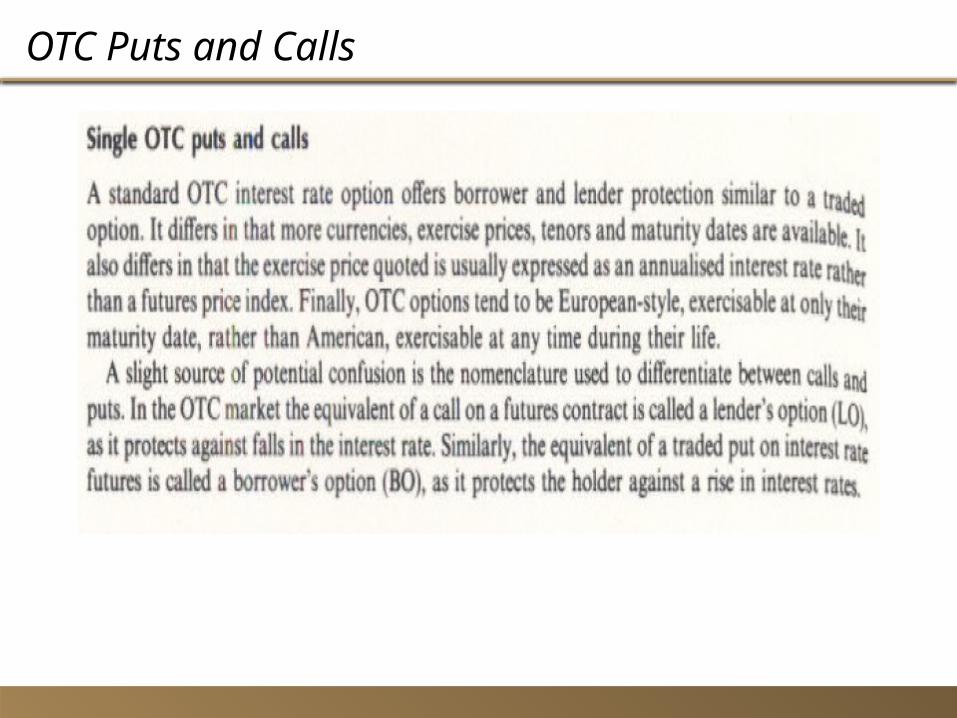

OTC Puts and Calls

Uses of Interest rate instruments

• Capping Liability costs

• A borrower wishing to protect himself against rising interest rates can

• Borrow and lend proceeds• Buy an FRA• Sell Interest rate Futures• Buy Interest rate Puts• Buy an OTC Borrowers Option

• Insuring asset protection( what are the possibilities?)

Interest rate caps

• An interest rate cap is actually a series of European interest call options (called caplets), with a particular interest rate, each of which expire on the date the floating loan rate will be reset.

• At each interest payment date the holder decides whether to exercise or let that particular option expire.

• In an interest rate cap, the seller agrees to compensate the buyer for the amount by which an underlying short-term rate exceeds a specified rate on a series of dates during the life of the contract.

• Interest rate caps are used often by borrowers in order to hedge against floating rate risk.

Interest rate Floors and Collars

• Floors are similar to caps in that they consist of a series of European interest put options (called caplets) with a particular interest rate, each of which expire on the date the floating loan rate will be reset.

• In an interest rate floor, the seller agrees to compensate the buyer for a rate falling below the specified rate during the contract period.

• A collar is a combination of a long (short) cap and short (long) floor, struck at different rates. The difference occurs in that on each date the writer pays the holder if the reference rate drops below the floor. Lenders often use this method to hedge against falling interest rates.

Au Revoir

Related Documents

![NYSUNY 2020 PPT FINAL - SEPT 20 2012.pptx [Read-Only] · ETEC: Creating an Entrepreneurial Ecosystem ... Microsoft PowerPoint - NYSUNY 2020 PPT FINAL - SEPT 20 2012.pptx [Read-Only]](https://static.cupdf.com/doc/110x72/5c31142e09d3f297358bf3da/nysuny-2020-ppt-final-sept-20-2012pptx-read-only-etec-creating-an-entrepreneurial.jpg)