Coupon Trends and Takeaways for 2013 Devora Rogers Senior Director, Retail Marketing Insights

Coupon Trends and Takeaways for 2013 Devora Rogers Senior Director, Retail Marketing Insights.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Coupon Trends and Takeaways for 2013

Devora RogersSenior Director, Retail Marketing Insights

Devora Rogers

• Senior Director, Retail Marketing Insights

• New to Inmar (and North Carolina)

• Previously with IPG Media Lab and Shopper Sciences

• [email protected]• 336.770.3495• Twitter: @devoraerogers

Inmar’s Portfolio of Services

2012 COUPON TRENDSKey Findings

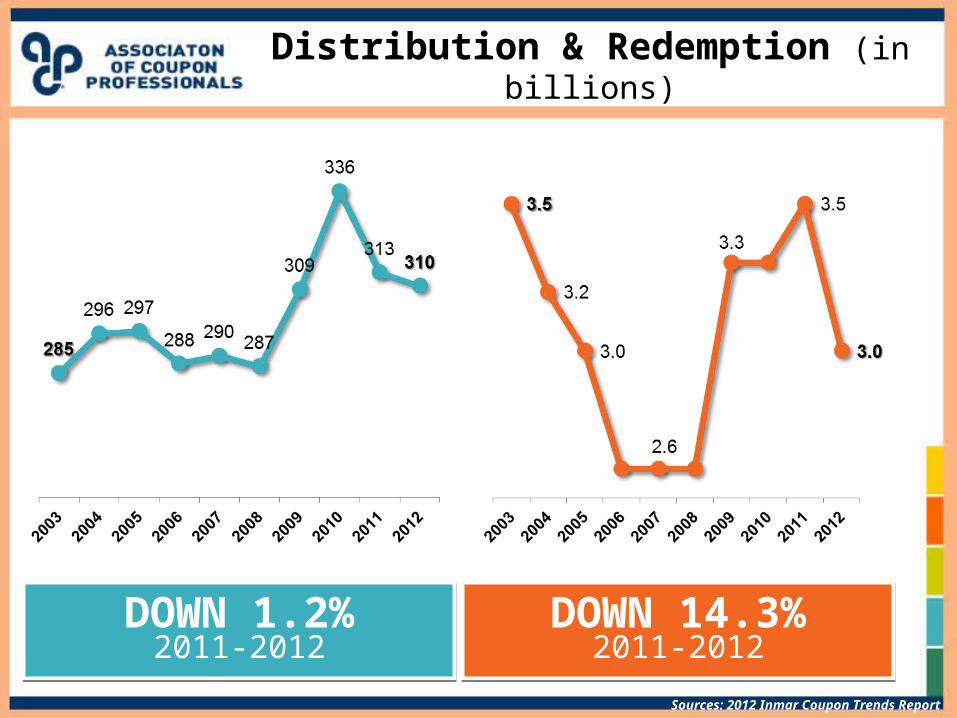

Distribution & Redemption (in billions)

DOWN 1.2%2011-2012

DOWN 1.2%2011-2012

DOWN 14.3%2011-2012

DOWN 14.3%2011-2012

Sources: 2012 Inmar Coupon Trends Report

2012 Distribution

Sources: 2012 Inmar Coupon Trends Report

2012 Redemption

Sources: 2012 Inmar Coupon Trends Report

Redemption Down Across the Board

65.8% of Total

BILLION BILLION

34.2% of Total

Sources: 2012 Inmar Coupon Trends Report

So what’s driving the decline?

Rising pricesRising pricesLow consumer

confidenceLow consumer

confidence

Declining paid Sunday newspaper

subscriptions

Declining paid Sunday newspaper

subscriptions

Sources: 2012 Inmar Coupon Trends Report

Tactics having limited impact on redemption

Distributed:

$1.57 /coupon (-1.3%)

Redeemed:

$1.14 /coupon (+1.8%)

Distributed:

1.49 units/coupon

Redeemed:

1.61 units

Distributed:

2.4 months (-4.0%)

Redeemed:

5.4 months (-7.0%)

Average Face Value

Distributed

Average Face Value

Distributed

Average Purchase Requirement

Distributed

Average Purchase Requirement

Distributed

Average Redemption

Period Distributed

Average Redemption

Period Distributed

Sources: 2012 Inmar Coupon Trends Report

Tactics having limited impact on redemption

34.36%34.36%“I usually won’t use a coupon if I have to purchase multiple items”

37.64%37.64%“There are too

many rules/exclusions

for using coupons”

Sources: 2012 Inmar Coupon Trends Report

New Product Trial Dampening Redemption

Manufacturers Promoting New

Products via FSI in 2012

190190

+9.9% +9.9% over 2011

727727New Product

Event Dates in 2012

+23.2% +23.2% over 2011

9393Categories

Featuring New Product Events

in 2012

+13.4% +13.4% over 2011

“I can’t find coupons for the products I want to buy”52.83%52.83%

Sources:, Marx and 2012 Inmar Shopper Survey

Redemption Period by Method Type

My coupons often expire before I have

the chance to use them.

Sources: 2012 Inmar Coupon Trends Report

SHOPPER BEHAVIOR

15

ENTITLEDENABLEDENGAGED

Changing Shopper Sentiment

“If I put in the effort, I can get deals on the brands I buy.”

“If I shop a store a lot, I shouldn’t have to

work for deals I deserve.”

From effort to entitlement

Are shoppers still using coupons?

Compared to 2011, shoppers reported coupon usage in 2012:

In their own words:

YESSources: 2012 Inmar Coupon Trends Report

Shopper Attitudes to Coupons

36%36%I am not sure where to get coupons for the products that I want to buy.

37%37% I wish all coupons were digital.

65%65%Don’t think they should have to work for deals.

66%66%I would use coupons more if they were more available online.

80%80%Using coupons makes me feel smarter.

Sources: 2012 Inmar Coupon Trends Report

“I wish all coupons were digital”“I wish all coupons were digital”19

44%44%HispanicHispanic

35%Non-

Hispanic

Hispanic Shopper Attitudes

The “New Couponer” is Tech Savvy

Goldman Sachs, 2011

of U.S. cell users will have smartphones

By 2015 Coupon methods used (on average)

Smartphone User = 7.12

Non-smartphone User = 5.19

Sources: 2013 Inmar Shopper Behavior Survey

Rise of the Mansumer

86%

44%

40%

Sources: 2012 Inmar Holiday Study, KSDK, Men’s Health, Spike Network’s ‘State of Men’ study

Participation in holiday meal planning

Average Number of Coupon Methods Used

22

6.43Overall

7.1135+

6.00Under 35

6.76Female

5.68Male

7.32Hispanic

6.12Non-

Hispanic

7.49Kids

5.47No kids

THE DISH ON DIGITAL

How Digitally Discovered Coupons are Redeemed

Manifests as a paper coupon Redeems as a paper coupon

Settles as a paper coupon

Retailer Loyalty Program (i.e. eWallet/ Direct-to-Card / Save-to-Card)

Unique Identifier (10-digit mobile)

Loyalty Aggregator (AOL shortcuts, SavingStar, etc.)

“Closed” Retailer Program (Target, Walgreens, Starbucks, etc.)

Never manifests as paperRedemption recorded separately

Text Email Website

Social QR (et al)

Apps

Redeemed like paper Paperlessly redeemed

Digital Stats for 2012

In 2013, the number of retailer storefronts In 2013, the number of retailer storefronts which accept paperless coupons is which accept paperless coupons is expected to grow 50% or more depending expected to grow 50% or more depending on channel. on channel.

250M250MCLIPPEDCLIPPED

27.5M27.5MREDEEMEDREDEEMED

$0.91$0.91AVERAGEAVERAGE

FACE VALUEFACE VALUE11%11%

AVERAGEAVERAGEREDEMPTIONREDEMPTION

RATERATE

Sources: 2012 Inmar Coupon Trends Report

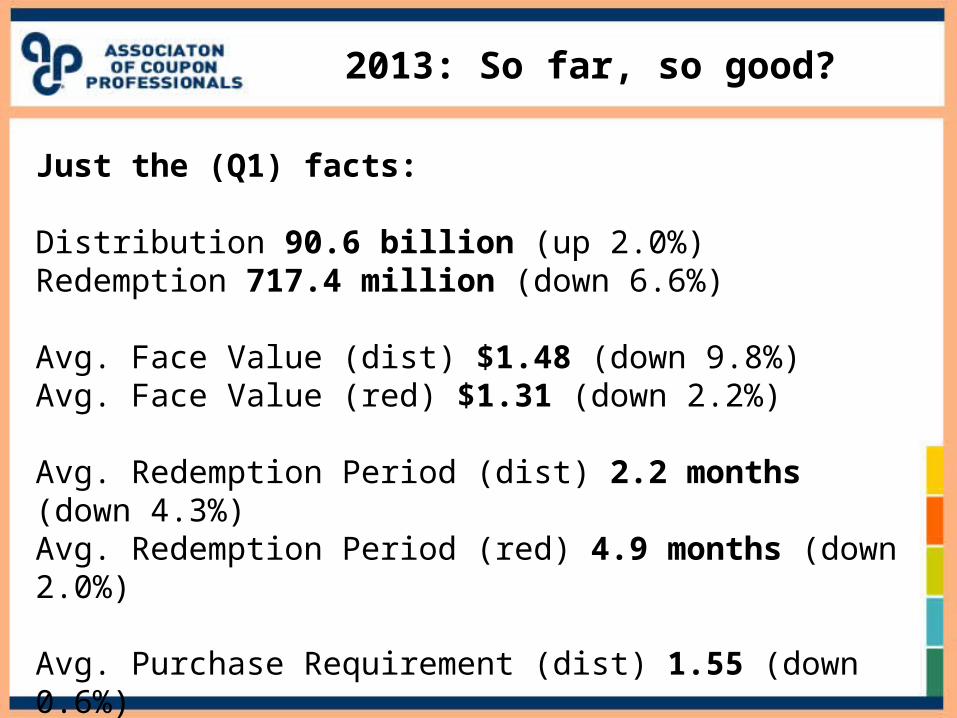

2013: So far, so good?

Q1 2013 (vs. Q1 2012)

Distribution a little better than flat (up 2%)

Redemption continues to slide… (down 6.6%)

…as marketers continue to pull back (face values down, redemption period shortened)

2013: So far, so good?

Just the (Q1) facts:

Distribution 90.6 billion (up 2.0%)Redemption 717.4 million (down 6.6%)

Avg. Face Value (dist) $1.48 (down 9.8%)Avg. Face Value (red) $1.31 (down 2.2%)

Avg. Redemption Period (dist) 2.2 months (down 4.3%)Avg. Redemption Period (red) 4.9 months (down 2.0%)

Avg. Purchase Requirement (dist) 1.55 (down 0.6%)Avg. Purchase Requirement (red) 1.61 (up 1.9%)

Plus ca change…

Q1 2013 (vs. Q1 2012)

Distribution a little better than flat (up 2%)

Redemption continues to slide… (down 6.6%)

…as marketers continue to pull back (face values down, redemption period shortened)

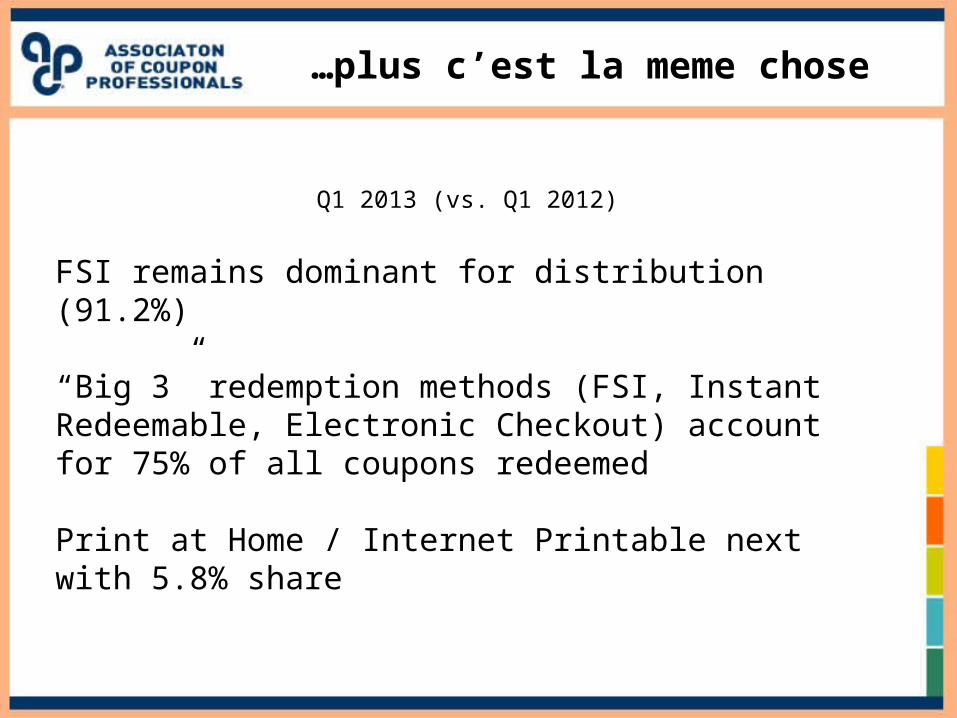

…plus c’est la meme chose

Q1 2013 (vs. Q1 2012)

FSI remains dominant for distribution (91.2%)

“Big 3” redemption methods (FSI, Instant Redeemable, Electronic Checkout) account for 75% of all coupons redeemed

Print at Home / Internet Printable next with 5.8% share

QUESTIONS?Thank you.

Related Documents