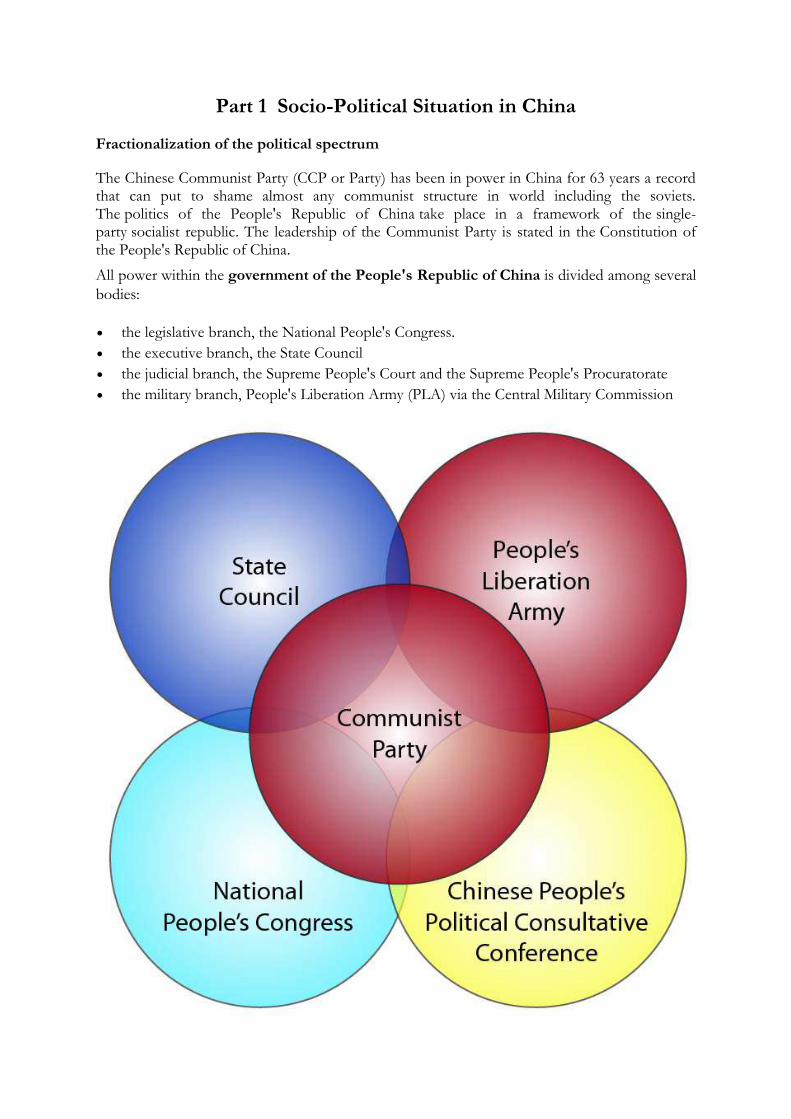

Part 1 Socio-Political Situation in China Fractionalization of the political spectrum The Chinese Communist Party (CCP or Party) has been in power in China for 63 years a record that can put to shame almost any communist structure in world including the soviets. The politics of the People's Republic of China take place in a framework of the single- party socialist republic. The leadership of the Communist Party is stated in the Constitution of the People's Republic of China. All power within the government of the People's Republic of China is divided among several bodies: the legislative branch, the National People's Congress. the executive branch, the State Council the judicial branch, the Supreme People's Court and the Supreme People's Procuratorate the military branch, People's Liberation Army (PLA) via the Central Military Commission

Country Risk Analysis - Pharma firm entering China's market

Oct 24, 2015

A complete, exhaustive exploration of China's socio-political, economic and regulatory environment with respect to FDI in Pharma sector.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Part 1 Socio-Political Situation in China

Fractionalization of the political spectrum

The Chinese Communist Party (CCP or Party) has been in power in China for 63 years a record that can put to shame almost any communist structure in world including the soviets. The politics of the People's Republic of China take place in a framework of the single-party socialist republic. The leadership of the Communist Party is stated in the Constitution of the People's Republic of China.

All power within the government of the People's Republic of China is divided among several

bodies:

the legislative branch, the National People's Congress.

the executive branch, the State Council

the judicial branch, the Supreme People's Court and the Supreme People's Procuratorate

the military branch, People's Liberation Army (PLA) via the Central Military Commission

Most positions of significant power in the state structure and in the military are occupied by members of the Communist Party of China which is controlled by the Politburo Standing Committee of the Communist Party of China, a group of 4 to 9 people, the paramount leader being Xi Jinping. The executive body i.e. the State Council is tasked with running day-to-day affairs of the country. The State Council is the chief authority of the People's Republic of China. It is appointed by the National People's Congress and is chaired by the Premier (Li Keqiang) and includes the heads of each governmental department and agency. Exploring the possibilities of a rift Often sever competition exists among the members of the Communist Party’s Politburo & its Standing Committee - China’s highest decision-making bodies. As part of a trend of very modest political pluralization, moreover, other political actors are increasingly able to influence policy debates. One test of a political system is its ability to manage political transitions. In the run-up to a once in a decade change in the Communist Party’s leadership in November 2012, Communist Party Politburo member and Chongqing Municipality Party Secretary Bo Xilai fell from grace, exposing at least one serious rift in the leadership, raising questions about the tenacity of the one-party command structure opening room for factionalism. Many analysts, both in China and abroad, have questioned the long-term viability of China’s current political system, in which the politburo remains above the constitution, leadership politics is a black box, & right to free speech and association are severely restrained Maintaining domestic stability is one the prime mandates of the 2.5m strong PLA and 800,000 strong police forces. However, the current domestic issues are getting more complex to control:

a) Among the Chinese political system’s governance difficulties is the phenomenon known as “stove-piping,” in which individual ministries and other hierarchies share information up and down the chain of command, but not horizontally with each other.

b) A related governance issue is unproductive competition among official entities. It is not uncommon in China for multiple entities to attempt to assert jurisdiction over the same issue, competing with each other for scarce budget resources, power, and recognition from higher government officials.

c) Although China is effectively a one party state, multiple coalitions, factions, and constituencies exist within the political system. Political mentorship, place of birth, the affiliations of one’s parents, and common educational or work history may lead individuals to form political alliances.

We believe that in the next ten years the Chinese political system may be quite different. There is a chance that the basic game shall change significantly by 2017, and even a chance that there won’t be the same kind of Party Congress by 2022. Instead, we could witness transparent political process, more accountable and representative government, and increasingly democratic elections both within the Party and in the country. And it’s possible that very abrupt (yet largely non-violent) change could happen. Some intellectuals in China argue that cultural change takes 60 years, economic change takes 6 years, but political change takes 6 days, or even a weekend.

Fractionalization by language, race, religion

Today China's population is over 1344 million, the largest of any country in the world. As per

last consensus in 2010, PRC officially recognizes 56 distinct ethnic groups, the largest of which

are Han, who constitute 91.51% of the total population with 8.49% being minorities. The Han

Chinese – the world's largest single ethnic group – outnumber other ethnic groups in every

provincial-level division except Tibet and Xinjiang

The official spoken standard in the People's Republic of China is Putonghua. Its pronunciation is

based on the Beijing dialect of Mandarin, which was traditionally the formal version of the

Mandarin or Chinese language. Mandarin and its various dialects are spoken by more than 70%

of the population.

The Chinese government has implemented state atheism since 1949, making it difficult to

ascertain the data on the religious diversity. Different surveys undertaken over smaller samples

over the years have thrown up divergent results to establish any specific trend. Today, according

to different surveys, Taoism is being practiced by over 30% of the Chinese population while

Buddhism is practiced by between 11 - 18% of the Chinese. Christianity is practiced by 3 - 5%

& Islam by 2% of the population.

Thus religion, race, nor language has any major role to play in igniting any factionalist tensions.

However in light of the recent and rising disparity due to the widening income gap across the

social strata and also the glaring disparity in the economic growth of various parts of the country

may lead to some fractionalization along the regional lines.

As per BMI’s recent forecast, separatist movements will remain weak, but unrest will

occasionally erupt in the ethnic-minority regions of Tibet and Xinjiang, and related incidents of

terrorist violence elsewhere are possible. There is a small risk that separatism in Xinjiang will

escalate into a full-blown insurgency; a series of security incidents there so far in 2013 have

resulted in numerous deaths. The Tibetan separatist movement could grow more violent when

the exiled Tibetan spiritual leader, the Dalai Lama, dies. As yet, China’s government shows no

signs of moderating its harsh approach to dealing with separatist and ethnic unrest. However,

there are some signs of new policy strategies being discussed in official think-tanks that may

eventually lead to a change.

Restrictive measures to retain power

The Chinese government is famed for using all forms of restrictive practices ranging from

legitimate constitutional provisions to use of force in order to suppress any anti-party

commentary. The PLA is often touted to be the military arm of the CCP. The primary mandate

of the 2.5m-strong PLA along with 800,000 strong police force is to ensure domestic stability i.e

to prevent any social uprising.

In the words of Tanner during his testimony before the U.S.-China Economic and Security Review Commission, that aptly summarizes the popular practices adopted by Chinese Authorities:

“Despite the historic success of Beijing’s 30-year economic growth strategy, the available data from Chinese law enforcement sources indicates that unrest in China has continued rising for nearly two decades with little or no break. The list of government and managerial abuses that spark the great majority of these protests has changed little over the past decade, notwithstanding innumerable directives and laws from Beijing to stanch them. Beijing continues to struggle to find institutional responses that will check these abuses and predations by local officials. But over the past decade it has been far more ambivalent in promoting some of the legal and political institutional reforms first inaugurated in the late 1980s and 1990s that once promised to strengthen citizen access, oversight, and influence. Western analysts would be justified in asking themselves to what extent the promotion of political or legal structural reform can still be described as major priority of the Chinese Communist Party. Shortly after the onset of the 2008 economic crisis, China’s public security forces issued new regulations aimed at forging a more sophisticated response to unrest. As with previous efforts to develop more effective police containment and management of unrest, the question remains whether China’s law enforcement forces can develop the discipline and professionalism to carry out the new strategy—and whether or not local Party authorities will let them.” Besides physical force on the street the Chinese govt. has banned the use of twitter, google, Youtube, FB or any such mass medium of information sharing as part of the internet censorship drive. The govt. employees an army of tech sleuths to constantly monitor and track the web traffic flowing in and out of the country to check for any inflammatory/anti-institution rhetoric. Such heavy restraining measures cast a severe doubt the ability of any multi-national firm to seek

grievance redressal through public campaigns. As the new firms contemplate investing in China,

the informational barriers would have to come down sooner rather than later to ensure a healthy,

conducive environment to carry out their businesses.

Xenophobia, nationalism, corruption

Corruption in China is widespread. The roots of the corruption lie in the extremely bureaucratic

and rigid framework of the Chinese government. Given that everything falls under the aegis of

just one party with minimal counter-vigilance to check existing structures. Given that most

regimes have chosen to bring about only evolutionary changes in the govt. machinery – mal

practices and bribery have now been entrenched into the system. Among its forms are lavish

gifts and expensive meals bestowed on officials by those seeking favors; bribes explicitly

provided in exchange for permits, approvals, and jobs; privileged opportunities offered to

officials or their extended families to acquire corporate shares, stock, and real estate;

embezzlement of state funds; and exemption of friends, relatives, and business associates from

enforcement of laws and regulations. As China’s economy has expanded over the last 30 years,

the scale of corruption has grown dramatically. 2011 report released by China’s central bank

estimated that from the mid-1990s to 2008, corrupt officials who fled overseas took with them

$120 billion in stolen funds.46 Estimates of illicit financial flows out of China are many times

higher. In a 2012 report, Global Financial Integrity, a Washington, DC-based research and

advocacy organization, estimated that total illicit financial flows out of China in the decade from

2001 through 2010 amounted to $2.74 trillion, with $420 billion leaving China illicitly in 2010

alone.47 The international non-governmental organization Transparency International ranks

China 80th on its Corruption Perceptions Index, with the top ranking countries being the least

corrupt. China ranks just below Sri Lanka and above Serbia.

However, given the increased vigilante activism by a more vibrant civil society armed with social

media and other internet based resources, the government has gone into a counter-offensive

crackdown on bribery. The recent Bo-Xilai indiction openly demonstrated the entrenchement of

the endemic. Thus, immediately following his appointment as Communist Party General

Secretary in November 2012, Xi Jinping identified corruption and graft within the Party as

“pressing problems.” He pledged to “work with all comrades in the party, to make sure the party

supervises its own conduct and enforces strict discipline.” Many observers believe, however, that

the Party’s insistence on supervising its own conduct, rather than accepting supervision from

outside, has been part of the reason that corruption has flourished. Critics charge, moreover, that

when the Party’s corruption-fighting agency, the Central Discipline Inspection Commission,

conducts investigations; they are frequently politically motivated, even if they uncover real

wrongdoing. Officials who keep on the right side of their superiors and colleagues may engage in

large-scale corruption, while other officials may be investigated for lesser infractions because

they have fallen afoul of powerful officials.

Media commentators and academics have suggested a variety of measures to tackle corruption,

including allowing the media to play more of a watchdog role and requiring officials to make

their family assets public. So far, neither proposal has advanced significantly. Journalists who

expose wrongdoing do so at their peril. In recent years, however, microbloggers have

successfully exposed a string of corrupt officials. In one high-profile case, microbloggers drew

attention to photographs of a local official showing him wearing at least 11 different luxury

wristwatches on various occasions. Just one of the timepieces was worth more than twice the

man’s annual salary. Going forward, the virtual monitoring done by informed netizens shall play

a decisive role in further governmental reforms.

Managing corruption is a difficult but a mandatory art to be mastered for MNC seeking

successful operations in D&E markets. However, the increasingly complex landscape due the

recent crack-down both by the govt. and also the citizens have alerted the entire country that a

mild revolution is on the anvil.

Social conditions (population density and wealth distribution)

The population density also shows significant diversity with most sparse in the mountainous,

desert, and grassland regions of the northwest and southwest. The Inner Mongolia, Xinjiang,

and Tibet autonomous regions and Qinghai and Gansu provinces comprise 55% of the country's

land area but in 1985 contained only 5.7% of its population. Accordingly the economic disparity

is distributed along the regional lines with wealth being disproportionately held up in wealthy

centres such as Beijing, Guanzhou etc.

Over the last twenty years, China has growth at phenomenal rates raising the per caputa standard

of living but has also widened the gap between the rich and the poor. Results of a wide-ranging

survey of Chinese family wealth and living habits released this week by Peking University show a

wide gap in income between the nation’s top earners and those at the bottom, and a vast

difference between earners in top-tier coastal cities and those in interior provinces. The top 5%

account for 23% of China’s total HHI. The lowest 5 % accounted for just 0.1 % of total income.

Average annual income for a family in 2012 was $2,100. When broken down by geography, the

survey results showed that the average amount in Shanghai, a huge coastal city, was just over

$4,700, while the average in Gansu Province, far from the coast in northwest China, was just

under $2,000. Average family income in urban areas was about $2,600, while it was $1,600 in

rural areas. Ordinary Chinese are increasingly resentful of wealth being accumulated by a select

few — and in particular by people connected to party officials — and government censors often

try to limit discussion in public venues of the personal wealth of the richest Chinese and of the

families of China’s leaders.

The unemployment rate in China estimated to be in the range of 4.4 percent to 9.2 percent. It is

also estimated China’s Gini coefficient to be 0.49 in 2012, less than the 0.51 in 2010. The

Chinese government avoided releasing an official number for several years. Then in January

2013, the head of the National Bureau of Statistics, Ma Jiantang, said the Gini coefficient was

0.474 in 2012, down from a peak of 0.491 in 2008.

Strength of radical left

Though communism has governed China for the last 60 years, the recent & extra-ordinary

growth for the last 2 decades has introduced the Chinese to quasi free-market policies. While the

western media may laud China for its extraordinary economic success, some intellectuals, as well

as former military officials, workers, and farmers have raised serious concerns about the

downside of thirty years of unfettered economic growth. Crony capitalism, the failure to ensure

an adequate social welfare net, and growing environmental challenges are all seen as failures of

the current Chinese political economy.

These loopholes have now led to the emergence of "the New Left". These scholars are

suspicious of further market reforms and want a stronger state-hand in the market to ensure

social justice.

Some of China's recent reform initiatives, such as the drive to develop a "harmonious society",

derive from an element of the political spectrum that is concerned overwhelmingly with social

justice.

The nature of such a state in the political realm, however, is not as well defined. Scholars

associated with the New Left, such as Professor Wang Shaoguang at the Chinese University of

Hong Kong, express dissatisfaction with Western democracy as it is practiced. Yet they do not

have a clear alternative to propose. They seek a system that is accountable, responsive, and

responsible, but do not know precisely what political institutions will best bring such a system

about.4 In their concern over representative democracy, they pose a challenge to those who seek

more revolutionary reform.

Thus the chances of radicalism being re-introduced remain weak and only a theoretical

possibility. From the stand point of any Pharmaceutical firm planning to engage with China, the

left radicals should not be a major concern area.

Dependence on and/or importance to a hostile major power

The Chinese shares a historic bias against Japan and anti-Japanese sentiment, in particular, has

been a recurring theme among online Chinese nationalists. Periodically, Chinese nationalists use

Internet and the street to contest historical inaccuracies in Japanese textbooks calling for

retribution. Nationalists had also begun with anti-Japanese protests after recent territorial

disputes in the South China Sea, thereby providing the government an impetus to adopt a

tougher stance in its negotiations with Japan.

China’s traditional ties with erstwhile neighbor India has been rocky. While the two nations have

seen phenomenal increase in their mutual trade, the border conflicts have escalated over the

recent period. Repeated violation of border treaties has been observed with both parties

engaging in exchanging gun-fire keeping the foreign embassies busy for both countries. After

much and frantics visits by premiers from both does a peace accord seem to be have reached.

At a global level, China has fancied a head-on tussle with U.S of A. China’s hard-liner stance

with the U.S. on all key strategic issues such as exchange rates to environmental guidelines to

China’s domestic patent rights to the famed conflict over banning Google/FB have meant the

power politics of the world heavy weights is out in the open for everyone to see.

Thus, an American company entering into the Chinese markets may have to be wary of the

potential barriers it may face while it establishes its identity.

Negative influences of regional political forces

China may not have much regional diversity in political opinion given its one-party one

command structure – it is some to some of world’s most engaging separatist movements. The

on-going tiffs over the Mongolia, HK and Taiwan are fairly well documented but it is the far

flung & neglected regions of Tibet and Xinjiang that have seen heavy blood-shed and unrest

over the last few years. Both these regions are home to minority populace and are also equally

distant from main-stream Chinese economic hot-spots.

Also, both regions are fairly rich in term of its natural wealth in minerals and other extractive

materials and thus view the PRC with abundant suspicion of exploitation. The Chinese govt. on

the other hand has not restrained itself in exercising force to exert its control over the regions.

His Holiness Dalai Lama, the “keeper” for Tibet has been forced into political exile in Himachal

Pradesh, India and his well-being decided the future of peace in the region. Xinjiang on the other

hand is another offshoot of the fallen Qing empire inhabitated primarily by the Uighur muslims.

Beijing has used all its military might to stamp down any violence by perpetrators of secessionist

movements.

Societal conflict (demonstrations, strikes or street violence)

Growing disparity between the rich and the poor, opaque political transformations, rampant

corruption at levels of government has created significant resentment among the citizens thus

leading to often violent protests. According to Chinese law enforcement estimates on so-called

“mass incidents”—their official term for a wide variety of group social protest has increased every

year from 1993 to the late 2000s. Numerous police analysts report that official mass incident figures

rose from 74,000 in 2004, to 87,000 in 2005, and to “more than 90,000” in 2006. Official figures for

the year 2007, and at least one analyst asserts that incidents declined slightly that year, though the

number of persons participating “increased dramatically.” Despite Chinese government efforts to

keep protests down in the run-up to the 2008 Olympics, the spring and summer witnessed several

high profile or violent incidents. While the west focused on the March 14 riot in Lhasa, Tibet,

Chinese police were also fixated on major incidents such as those in Weng’an, Guizhou, and

Menglian, Yunnan. Protest numbers apparently spiked with the onset of the financial crisis soon

after the Summer Games, and by the end of 2008, total mass incidents had reportedly risen to

120,000 despite the pre- and post-Olympic security. Nationwide figures for 2009 and 2010 are not

yet available, although local data and reports by some prominent Chinese academics indicate

protests climbed greatly in 2009 in the wake of economic difficulties. Thus, the police and PLA are

finding their hands full trying to suppress a national uprising in the making.

In addition to the mass incidents, the increasing role of the Internet in Chinese political life

poses a significant challenge to the Party’s efforts to constrain political reform. While the

Internet is a important asset critical to the progress of the nation I also possesses significant

threats too. The Internet is, in fact, evolving into a virtual political system in China. The Chinese

people are increasingly using for information, organizing work, and co-ordinating online protests

online. As the blogger Qiu Xuebin writes, "When the interests of the people go unanswered long

term, the people light up in fury like sparks on brushwood. The internet is an exhaust pipe,

already spewing much public indignation. But if the people’s realistic means of making claims are

hindered, in the end we slip out of the make-believe world that is the internet and hit the streets

Instability (non-constitutional changes, assassination, civil war)

CCP maintains water tight control over all aspects of state, judicial or military matters make it to

be the supreme authority in the country. The rule of law is in its weak form in the country.

Scholars who have been privy to various models of government in the west now call upon

institutional reforms that transform the political structure in the country. For e.g. Political activist

and Nobel Peace Prize winner Liu Xiaobo represents the boldest of those who call for such

revolutionary reform with his online human rights manifesto, Charter 08, and his calls for

universal values, direct elections, constitutional democracy, separation of powers, and protection

of private property, among other elements of institutional reform.

Ex premier Wen, a vocal proponent of fundamental reforms, did conduct a small experiment on

political modernization in Shenzhen. The stated goal is strictly in line with the Party’s

constrained vision of political reform: to build a socialist democracy and a rule-of-law system, to

develop a clean, efficient and service-oriented government, and to construct a complete market

system, a socialist advanced culture, and a harmonious society. At the same time, the approach

has some potentially revolutionary reform elements: gradually expanding direct elections,

introducing more candidates than there are positions for heads of districts, and considering

allowing candidates to compete for positions of standing members of district or municipal Party

committees by organizing campaigns within certain boundaries.

Thus success of this reforms remains to seen. But in these trysts with democracy shall lay the

future course of Chinese civilizations that sits on the cusp of a new era.

References (for Part I)

Web Sources

Economic Intelligence Unit Reports

Business Monitor International periodical reports

CFR: Council on Foreign Relations

Online Links

New York Times - 2013/07/20 “Survey in China Shows a Wide Gap in Income”

Forbes.com - 2013/01/20 “The China Miracle: A Rising Wealth Gap”

bbc.co.uk “Xinjiang: China jails 20 for terrorism and separatism”

Wikipedia

Tibetan independence movement

East Turkestan independence movement

List of active separatist movements in Asia

Political Structure in China

Demographics of China

Literature

Elizabeth C. Economy. “Nobel Peace Laureate Liu Xiaobo and the Future of Political Reform in

China”

Murray Scot Tanner. “Unrest In China And The Chinese State’s Institutional Responses”

Susan V. Lawrence & Michael F. Martin. “Understanding China’s Political System”

Tyler Durden. “The Far More Important 'Election' Part 1: China's Political Process”

Part 2 The Economic Risk Rating

The overall aim of the Economic Risk Rating is to provide a means of assessing a country’s

current economic strengths and weaknesses. In general terms where its strengths outweigh its

weaknesses it will present a low economic risk and where its weaknesses outweigh its strengths it

will present a high economic risk.

These strengths and weaknesses are assessed by assigning risk points to a pre-set group of

factors, termed economic risk components. The minimum number of points that can be

assigned to each component is zero, while the maximum number of points depends on the fixed

weight that component is given in the overall economic risk assessment. In every case the lower

the risk point total, the higher the risk, and the higher the risk point total, the lower the risk.

The Economic Risk Components

GDP per Head

It is the estimated GDP per head for a given year, converted into US dollars at the average

exchange rate for that year, is expressed as a percentage of the average of the estimated total

GDP of all the countries covered by ICRG.

In world perspective China's performance has been exceptional. In 1300, it was the world's

leading economy in terms of per capita income. It outperformed Europe in levels of technology,

the intensity with which it used its natural resources, and capacity for administering a huge

territorial empire. By 1500, Western Europe had overtaken China in per capita real income,

technological and scientific capacity. From the 1840s to the middle of the twentieth century,

China's performance actually declined in a world where economic progress elsewhere was very

substantial. In the past quarter-century, China has had a rapid growth trajectory-a process of

catch-up which seems likely to continue well into the present century. By 2030 Chinese per

capita income will probably be above the world average, and it will again be the world's biggest

economy as it was from 1300 to 1890.1

Potential Risk: China's GDP per capita doubled to $6,100 from 2009 to 2012. However it does

not mean that this rapid growth has transformed the lives of the Chinese people. According to

Zhuang Jian “The fast-rising yuan value in recent years helped China achieve a higher GDP per

capita in this short span". This means the domestic growth is still not developed in China

For China,

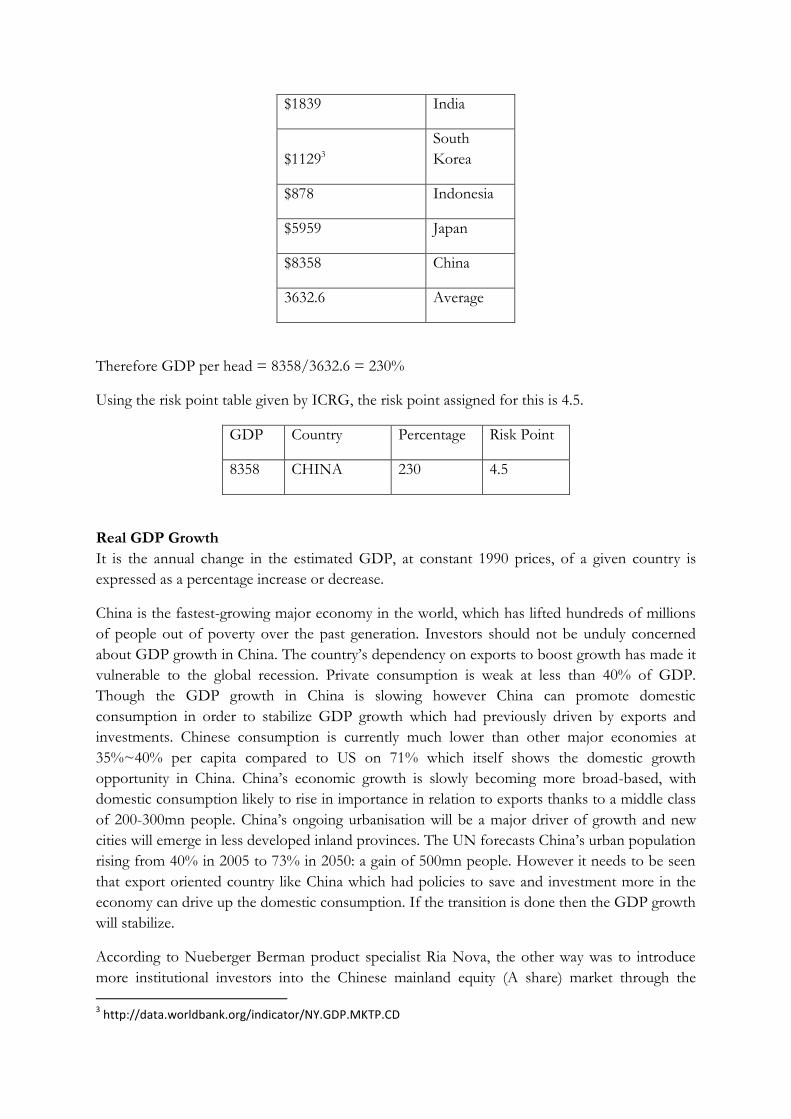

GDP for 2012 is $ 83582

Average of the estimated total GDP of all the countries covered by ICRG is

GDP Per Head

(Billion) Country

1 China in the World Economy 1300 – 2030 by Angus Maddison

2 www.data.eiu.com

$1839 India

$11293

South

Korea

$878 Indonesia

$5959 Japan

$8358 China

3632.6 Average

Therefore GDP per head = 8358/3632.6 = 230%

Using the risk point table given by ICRG, the risk point assigned for this is 4.5.

GDP Country Percentage Risk Point

8358 CHINA 230 4.5

Real GDP Growth

It is the annual change in the estimated GDP, at constant 1990 prices, of a given country is

expressed as a percentage increase or decrease.

China is the fastest-growing major economy in the world, which has lifted hundreds of millions

of people out of poverty over the past generation. Investors should not be unduly concerned

about GDP growth in China. The country’s dependency on exports to boost growth has made it

vulnerable to the global recession. Private consumption is weak at less than 40% of GDP.

Though the GDP growth in China is slowing however China can promote domestic

consumption in order to stabilize GDP growth which had previously driven by exports and

investments. Chinese consumption is currently much lower than other major economies at

35%~40% per capita compared to US on 71% which itself shows the domestic growth

opportunity in China. China’s economic growth is slowly becoming more broad-based, with

domestic consumption likely to rise in importance in relation to exports thanks to a middle class

of 200-300mn people. China’s ongoing urbanisation will be a major driver of growth and new

cities will emerge in less developed inland provinces. The UN forecasts China’s urban population

rising from 40% in 2005 to 73% in 2050: a gain of 500mn people. However it needs to be seen

that export oriented country like China which had policies to save and investment more in the

economy can drive up the domestic consumption. If the transition is done then the GDP growth

will stabilize.

According to Nueberger Berman product specialist Ria Nova, the other way was to introduce

more institutional investors into the Chinese mainland equity (A share) market through the

3 http://data.worldbank.org/indicator/NY.GDP.MKTP.CD

Qualified foreign institutional investors. According to her, returns in this market have dropped

30% or more in the last four years, partly because it is majority-owned by retail investors with a

vigorous trading mentality. The government wants to stabilise returns by giving access to longer-

term participants like insurance companies.

Thus we see that GDP growth in China will not be an issue in the long run if handled with care.

Also the growth rate for real GDP for last 5 years was at an average of 8.86%.

Potential Risk: In Nomura’s baseline scenario, China’s GDP growth slows to 6.7% in the first half

of 2014 and recovers slightly in the second half, bringing next year’s GDP forecast to 6.9%,

China’s slowest since 2008. Both cyclical and structural factors contribute to this slowdown.

Structurally, China’s potential growth is on a downtrend due to a dwindling and aging labour

force and a lack of reform. The government still runs the national and local economies, making

China slow and not very dynamic.4 In a higher risk scenario, GDP growth slows to 5.9% for full-

year 2014 and to 5% in the first half of next year and this could lead to China defaulting on its

loan payments.

For China, the real GDP growth for 2013 is estimated at 7.7%. Therefore using the real GDP

change risk table, the point assigned to China for this indicator is 10.

Annual Inflation Rate

It is the estimated annual inflation rate (the un-weighted average of the Consumer Price Index) is

calculated as a percentage change.

Not only worries over China's slowing growth trajectory may be greater concern but also

inflation could be a concern. Fears of stoking inflationary pressures will inhibit the new

administration from resorting to significant monetary easing. Slowing growth in agriculture

bodes ill both for price stability and Beijing's self-sufficiency goals. Rebalancing is inherently a

long-run process; progress in bringing it about will be slow. However for now inflation is not a

pressing concern. First-quarter results show a rise in CPI of 2.4%, or 1.4pp below that of the

same period in 2012 (and 0.2% below the annual figure for 2012). The only categories which

experienced price rises above the average were food and housing (up by 3.8% and 2.9%).

Producer prices for industrial products fell by 1.7% year-on-year.

Potential Risk: The inflation rate was higher than a median forecast of 2.9% in a Reuter’s poll and

August's 2.6%, but was still below the official target of 3.5% for 2013. If the inflation rate

increases in the coming months, then there will further policy tightening which might affect the

overall growth of the economy.

For China, the annual inflation rate is estimated at 2.6%. Therefore using the annual inflation

risk table, the point assigned to China for this indicator is 9.5.

Budget Balance as a Percentage of GDP

It is the estimated central government budget balance (including grants) for a given year in the

national currency is expressed as a percentage of the estimated GDP for that year in the national

currency.

4 http://www.forbes.com/sites/kenrapoza/2013/07/24/when-china-sneezes-everyone-gets-sick/

China's solid fiscal position is enough to make debt-ridden European and U.S. governments

green with envy. But turning strong public finances into a pro-growth fiscal policy won't be

straightforward. Economists focus on the budget balance – the difference between government

revenue and expenditure – as the main measure of the impact of fiscal policy on growth. In

2012, many expect China's Ministry of Finance to spend more than its income, run a budget

deficit and buoy domestic demand.

However in China, the budget balance doesn't tell the entire story on the government's impact

on growth. An enormous volume of gray revenue raised by local governments isn't included in

the Ministry of Finance's numbers. The most important omission is revenue from land sales –

effectively a tax on real-estate developers and home buyers. Land revenue of 2.9 trillion yuan

($457.3 billion) in 2010 was equal to 7.3% of gross domestic product. What matters for the

overall fiscal position isn't just how much gray revenue is raised but how much is spent.

Whatever be the case, the ministry of finance has to increase the budget deficit to increase

domestic consumption as the export demand is fading due to crisis in Europe and US.

Potential Risk: If the budget balance increases and if the GDP growth decreases, then there is

high chance of default on the loans. If there is a default, then the credit rating will be affected

and thus raising money will be difficult. Companies investing China must look at the growth rate

of Chinese economy before deciding whether to invest or not.

For China, the budget balance as a percentage of GDP is estimated at -2.0%. Therefore using the

budget balance risk table, the point assigned to China for this indicator is 6.5.

Current Account as a Percentage of GDP

It is the estimated balance on the current account of the balance of payments for a given year,

converted into US dollars at the average exchange rate for that year, is expressed as a percentage

of the estimated GDP of the country concerned, converted into US dollars at the average rate of

exchange for the period covered.

In the fourth quarter of 2012, there was a surplus of $65.8 billion in the current account.

According to the calculation of statistics requirements of international balance of payments,

there was a surplus of $107.4 billion in goods trade account in the fourth quarter, a deficit of

$19.6 billion in service trade account, a $21.8 billion deficit in income account and a $100 million

deficit in current transfer account.

In 2012, China had a surplus of $213.8 billion in its current account regarding its international

balance of payments, a deficit of $117.3 billion in the capital and financial account and an

increase of $96.5 in its international reserve assets. Last year, China's current account surplus

increased by 6% year-on-year, the ratio of which to GDP in the same period was 2.6%,

decreasing by 0.2% than that in 2011.

However it was the first time China's balance of payments transferred from "double surpluses"

to surplus in current account and deficit in capital and financial account since the Asian financial

crisis. Thus it also reveals that China has enhanced its ability in balancing its balance of payment

on its own. Also China’s massive trade surplus and huge foreign exchange reserve serves as a

major cushion against external shocks.

Potential Risk: Though China has able to manage the Asian financial crisis as it had double surplus

current account. However now it has reduced its current account and as the export demand is

lessening, the current account surplus may soon be over if domestic demand is not increased. If

the current account surplus goes down, then external shock will start affecting China’s economy.

For China, the current account as a percentage of GDP is estimated at 1.9%. Therefore using the

current account risk table, the point assigned to China for this indicator is 12.5.

Summary: Economic Risk Indicator

Economic Indicator Point

GDP per Head 4.5

Real GDP Growth 10

Annual Inflation Rate 9.5

Budget Balance as a percentage of GDP 6.5

Current Account as a percentage of GDP 12.5

The Financial Risk Rating

The overall aim of the Financial Risk Rating is to provide a means of assessing a country’s ability

to pay its way. In essence, this requires a system of measuring a country’s ability to finance its

official, commercial, and trade debt obligations.

This is done by assigning risk points to a pre-set group of factors, termed financial risk

components. The minimum number of points that can be assigned to each component is zero,

while the maximum number of points depends on the fixed weight that component is given in

the overall financial risk assessment. In every case the lower the risk point total, the higher the

risk, and the higher the risk point total the lower the risk.

Foreign Debt as a Percentage of GDP

It is the estimated gross foreign debt in a given year, converted into US dollars at the average

exchange rate for that year, is expressed as a percentage of the gross domestic product converted

into US dollars at the average exchange rate for that year.

As on 30th September 2013, the amount of debt China owes foreign lenders stood at 771.95

billion U.S. dollars. Of which, 403.31 billion U.S. dollars were international commercial loans

and 59.14 billion U.S. dollars were loans extended by foreign governments and international

financial organizations, according to data released by the State Administration of Foreign

Exchange. Meanwhile, 309.5 billion U.S. dollars were debts stemming from trade loans between

companies, the data showed.

Potential Risk: China has a high component of foreign debt. China economy policy is to borrow

heavily and invest in capacity building projects which return more than the cost of borrowing.

Due to recent crisis in US and Europe where US being one of the major export destinations for

China, export demand has fallen and China is lying with over capacity. If the Chinese are not

able to generate demand for their over-capacity, then growth rate will fall and probability of

default on loans will increase. Though China has state owned assets, land reserves in dealing with

local government debt but they won’t solve the fundamental problem. As long as the debt-

financed investments are not economically viable, there will be an unsustainable increase in debt

and if this continues forever, a debt crisis will take place

The majority or 80.79% of the nation's foreign debt was denominated in the U.S. dollar

Foreign Debt % of GDP = 1 – Public Debt % of GDP = 1 – 16.3% = 83.7%

Therefore using the foreign debt risk table, the point assigned to China for this indicator is 3.5.

Foreign Debt Service as a Percentage of Exports of Goods and Services

The estimated foreign debt service, for a given year, converted into US dollars at the average

exchange rate for that year, is expressed as a percentage of the sum of the estimated total exports

of goods and services for that year, converted into US dollars at the average exchange rate for

that year.

Potential Risk: The amount of debt China owes foreign lenders is approaching the $1 trillion

market. Outstanding short-term foreign debt, due within one year, rose to $565.68 billion from

$540.93 billion at the end of last year however the country has over $3 trillion in cash reserves.

More than enough to service its borrowing or wipe it out entirely and still have a few trillion left

over for a rainy day. Investors have been mildly concerned over China’s debt levels, from federal

to municipal to corporate debt. For the first time ever, a Chinese solar company Suntech Power

defaulted on a $531 million debt. Suntech Power is now in bankruptcy protection.

For China,

Total Exports for the year 2013 is $2224 billion

Total Foreign Debt = 83.7% * 9379 = $7850 billion

Short Term Debt = $565.68 billion (This amount is going to be serviced)

Foreign Debt as a percentage of Export = 565.68/2224 = 25.43%

Therefore using the foreign debt percentage of export risk table, the point assigned to China for

this indicator is 7.

Current Account as a Percentage of Exports of Goods and Services

The balance of the current account of the balance of payments for a given year, converted into

US dollars at the average exchange rate for that year, is expressed as a percentage of the sum of

the estimated total exports of goods and services for that year, converted into US dollars at the

average exchange rate for that year. For China,

Potential Risk: As discussed that export demand is falling and this is hampering the Chinese

economy, the current account surplus will come down. If the indicator falls, it shows that export

is not able to generate enough current account surpluses and China being an export oriented

economy, the GDP of the economy will go down. To counteract the effect of this indicator, the

Chinese government is looking to spur the domestic growth. So this indicator together with

domestic demand can tell us whether the economy will do well in the future or not. If the

current account goes negative, then the government won’t be able to service their foreign debts

through current account which will result in default and credit downgrade.

Total Exports for the year 2013 is $ 2224 billion.

Current Account for the year 2013 is $ 178.20 billion.

Therefore Current account as a percentage of Export = 178.20/2224 = 8.01%

Therefore using the current account as a percentage to export risk table, the point assigned to

China for this indicator is 13.

Net International Liquidity as Months of Import Cover

The total estimated official reserves for a given year, converted into US dollars at the average

exchange rate for that year, including official holdings of gold, converted into US dollars at the

free market price for the period, but excluding the use of IMF credits and the foreign liabilities

of the monetary authorities, is divided by the average monthly merchandise import cost,

converted into US dollars at the average exchange rate for the period.

Potential Risk: The official reserves are used for various purposes like meeting loan obligation.

Also the reserves are increasing because of stable exchange rate maintained by the Central Bank

else appreciation of currency would have happened. If that happens in an export oriented

economy where export demand is low then the growth will be adversely affected and the

reserves will quickly dry up.

Total Import for the 2013 = $1772 billion

Average monthly import = $1772/12 = 148 billion

Official reserves = $3.66 trillion

Therefore Net International Liquidity as Months of Import Cover = 3660/148 = 24

Therefore using the Net International Liquidity as Months of Import Cover, the point assigned

to China for this indicator is 5.

Exchange Rate Stability

The appreciation or depreciation of a currency against the US dollar (against the euro in the case

of the USA) over a calendar year or the most recent 12-month period is calculated as a

percentage change.

China had been fixing its exchange rate at ¥2-US$1 until 1984, when the government changed its

policy and started Yuan depreciation, resulting in a drastic shift from ¥2 per US dollar in January

1984 to ¥8.7 per US dollar in January 1994. During the period from January 1994 to June 2005,

China pegged its currency to the US dollar at around ¥8.4 per US dollar. Around 2005, it started

to appreciate for a while before being re-pegged at around 7.0 in July 2008. World leaders expect

China to take actions by next year to adopt more flexible exchange rates. Facing such a strong

and consistent pressure from the USA along with other developed countries, China promised to

gradually move toward a market-oriented exchange rate, but still infuriates its major trading

partners recently for the pegged regime. Despite a recent halt to the appreciation of the yuan, the

recession is leading to job losses in China’s export sector and thus increasing social instability.

Potential Risk: If appreciation of currency happens then China will lose its competitiveness in

the export market and this will lead to lower growth rate. Till China is not able to spur domestic

demand, China should peg its currency. However this could lead to strain relationship with its

trading partner.

For China, the exchange rate stability is estimated at 6.2%. Therefore using the exchange rate

risk table, the point assigned to China for this indicator is 10.

Summary: Financial Risk Indicator

Economic Indicator Point

Foreign Debt as a Percentage of GDP 3.5

Foreign Debt Service as a Percentage of Exports of Goods and Services

7

Current Account as a Percentage of Exports of Goods and Services

13

Net International Liquidity as Months of Import Cover

5

Exchange Rate Stability 10

Part 3 Legal system in China: Basic structure

The legal system of the People's Republic of China (PRC) is based on the PRC Constitution,

which stipulates that political power is exercised by the people through people’s representation.

This is achieved bottom up, from the local level up to the provincial and national levels. In

practice, policymaking and administration are at times highly centralised and uniform in nature, and

at other times highly decentralised and diverse.5

Legislative function: The National People's Congress (NPC) and its Standing Committee have the

power to pass laws (enact and amend) on behalf of the state.

The Chinese Communist Party: It is technically separate from the government. The Party parallels,

overlaps with and controls the government at all levels. While this achieves a certain high degree of

national uniformity and cohesion, this arrangement tends to set the Party above the government.

Executive function: the State Council of the PRC (State Council) is the highest level of state executive

administration and has the power to enact administrative rules and regulations consistent with law.

The Ministry of Commerce (MOFCOM) is the administrative body that is responsible for approving

foreign investment. The State Administration of Industry and Commerce (SAIC) and Local AIC are

responsible for business registration and other legal/regulatory oversight functions.

Judicial function: the judicial power to apply the law in civil and criminal matters is vested in the

people's courts at various levels – central, provincial and municipal/local. Court cases do not act as

binding precedents.

The Party-controlled central legislative/executive/judicial structure is repeated at lower levels.

Laws and regulations made at lower levels generally only serve to implement central-level

enactments must not conflict with those made at higher levels. It is also important to note that

despite the uniformity attributable to centralisation, there is may be high variation in local practice

and interpretation wherever central policy is silent or unclear.

Direct foreign investment is not permitted across the board in China. It is important to first assess

under what conditions the contemplated activity is open to foreign investment. Investment activities

are classified into 4 broad groups – Permitted, Encouraged, Restricted and Prohibited.

Investment decisions are also largely taken considering the special investment zones available -

national level high-tech industrial development zones; regular economic and technology

development zones; free trade zones; and export processing zones.

Legal & Regulatory system for doing business in China6

5 http://www.out-law.com/en/topics/projects--construction/community-infrastructure1/doing-business-in-

china-part-1---overview/ 6 http://www.sixsmart.com/SSPapers/pmw10.htm

Before entering the Chinese market , the stability of the Chinese government, Chinese laws,

property rights, price controls, and business restrictions need to be analysed. The Chinese

government has in the past strongly controlled prices, markets, products, foreign assets, and

personal assets. However the Chinese government has progressively chosen to open markets to

foreign investors and to create laws and regulations more in line with the WTO guidelines. This

has encouraged more foreign investment in China in recent years.

Building Laws and Regulations for Investment

There is a general understanding that excessive approval delays, personal rivalries, dishonesty,

and graft exist in the mechanism. Other perceived problems are related to leadership succession,

nepotism, favoritism and increased corruption.

The Chinese government has been taking steps to create and enforce a stricter legal system,

support freer commerce, and embrace the global marketplace. The Sino-Foreign Equity Joint

Venture Law was passed in 1979 to build a legal structure governing foreign investment. Since

then, China has continued to build a legal system that will protect both their rights as well as the

rights of their foreign partners

Protection of Private Property Rights

Private firms have been one of the driving forces behind China's rapid economic growth in

recent years. Some systemic problems persist and need to be tackled in order to encourage

additional development; an important one being the need for additional legal protections for

private property rights.

Under the Communist regime, private firms were associated with capitalism. They were typically

forbidden or subjected to various restrictions. However China adopted an open-door strategy in

the 1970s and the situation has since improved. This significant shift in government policy,

however, has yet to be fully reflected in the provisions of Chinese laws. Insufficient protection of

private property rights can otherwise lead to a widespread hesitation to reinvest in the country

and expand businesses.

Protection of Foreign Assets

Since 1979, China has built a legal system that attempts to protect the rights of Chinese citizens

as well as the rights of their foreign partners. New Chinese legislation is regularly introduced in

an attempt to modernize their economic legal structure. China is also expected to increase the

creation and enforcement of laws protecting the property rights of foreign corporations.

However, there is a risk that this may not completely protect foreign assets.

Government Price Controls

The Chinese government retains the capability to impose strict wage-and-price controls, but this

practice in not currently enforced. The majority of prices in China are now dictated by market

rates. China lifted price controls on many items as part of entering the World Trade

Organization. The current policy of relaxed price controls is likely to continue as long as it

benefits the Chinese people.

Corporate Restrictions in China

There are several restrictions for firms operating in China. Certain firms may be blocked from

entering a particular field that is available only to state-owned companies. Certain firms face

difficult rules regarding technology, personnel, and financing. Also, certain firms may be forced

to shoulder an unreasonably large tax burden. Furthermore, financing may hinder access to

funds.

Recently, however, more and more foreign companies are doing business in China. The

government has realized that in addition to reinforcing the protection of property rights,

facilitating competitive and fair market conditions is necessary to allow further development of

the Chinese economy. As a major step in this direction, discriminative measures against foreign

firms are being gradually removed following China's WTO accession

China’s Accession to WTO

China joined the WTO in the process of transition from a planned economy to a ‘socialistic

market economy’. Access to the WTO promotes China’s policy to reform its economy and open

up to world competition. This meant that China was committed to reforming its laws,

regulations, decisions, etc in order to ensure the implementation of the WTO agreements. WTO

focuses on fair trade between members. The fields WTO encompasses have been extended to

investment, services, intellectual property rights and other issues beyond pure trade.

Changes in the Legal Climate for Foreign Investment after China’s WTO Accession7

i. Fields open to foreign investors have been further extended. For example, there are

351 industries specified as encouraged activities, an increase of 94 items over those

stipulated in the Guidance Catalogue of 2004. Encouraged industries account for 73 per

cent of the list, up from 69 per cent in 2004.

ii. Transparency of foreign investment polices is enhanced. The catalogue therefore

contributes to transparency by clearly indicating the group into which each industry will

fall, thereby clarifying which policies and regulations are relevant to them. This makes the

relevant instruments easy to ascertain and access, so facilitating foreign investment.

iii. Domestic innovation and upgrading of industrial structure are encouraged. In

order to promote domestic innovation and to upgrade the national industrial base,

foreign investment is encouraged in modern agriculture, high‐tech industries, modern

service industries, cutting‐edge manufacturing and infrastructure

iv. Energy‐saving and environmentally‐friendly industries are encouraged. In order to

promote the more effective use of resources, environmental management and sustainable

development, the Guidance Catalogue of 2007 encourages industries in the area of clean

production technology, recycling resources, ecological environment protection and the

comprehensive utilization of resources.

v. Coherent development across regions is encouraged. The eastern and coastal

regions of China were the first areas opened to the world, whereas the western, central

and northeastern regions are relatively underdeveloped. China particularly encourages

investment in underdeveloped regions. The government is determined to improve

7 Bond Law Review, Vol. 20, Issue 1 - January 2008: “The Legal Climate for Foreign Investment in China after its

WTO Accession”

infrastructure significantly, improve the investment climate, allow more market access for

foreign investment and attract expert personnel to western regions.

Establishing a business in China8

Foreign invested enterprises (FIEs) wishing to establish a presence to do business China must

establish one of the several different statutory forms of FIE. In general, only companies with

25% foreign equity or more can be considered as FIEs. Forms of FIE include:

1) “Wholly foreign-owned enterprise (WFOE): a limited liability company 100% owned by one or more

individual or corporate foreign investors. The liability of the investors is limited to their subscribed registered

capital. WFOEs are the most popular form of FIE.

2) “Equity joint venture (EJV): a legal person company invested in together by both foreign and domestic

corporate investors. The equity interests of the investors, and the division of profits, is strictly proportional to

their shares of contributed registered capital.

3) “Cooperative joint venture (CJV): normally established as legal person limited companies, but may also be

established as a non-incorporated contractual cooperation. The liability of the partners in an unincorporated

CJV is unlimited, and investors tend to have greater flexibility. Non-incorporated CJVs are typically only

established for specific limited purposes and activities such as collaboration in natural resources exploration

and venture capital investments.

4) “Foreign invested company limited by shares (FICLS): a joint Chinese and foreign-invested company, hence

a form of joint venture (JV), limited by shares. An investor's liability is limited to its individual

subscription. Companies seeking listing on the Chinese stock market must be in the form of a FICLS. A

WFOE, EJV or CJV may convert to an FICLS in accordance with PRC law.

5) “Holding company and regional headquarters: investors with major operations already in the country may

wish to consider establishing a holding company or a regional headquarters to help consolidate certain group

treasury, support services and trading functions. There are significant minimum investment thresholds, and

operations are limited to holding company functions.”

Key challenges in the business & regulatory environment9

Some recent developments born out of friction between foreign companies and the Chinese

business environment are:

Coca-Cola's failed effort to take over Huiyuan Juice, 2009;

Google's exit from the market amid allegations of government hacking, 2010;

The arrest of Wal-mart employees over mislabeling of pork products, 2011;

Caterpillar's loss of $580 million after acquiring a Chinese construction equipment

company that had fraudulently inflated its revenues;

The bribery case involving GlaxoSmithKline.

According to the annual survey conducted by the American Chamber of Commerce in Shanghai,

the key business challenges in China faced by companies are as shown in the graph below.

8 http://www.out-law.com/en/topics/projects--construction/community-infrastructure1/doing-business-in-

china-part-2---establishing-a-business-in-china/ 9 The American Chamber of Commerce in Shanghai – China Business Report 2012-2013

Rising costs, HR constraints and preference for local firms and resultant competition were stated

by participant companies.

Challenges in business environment

The important regulatory challenges according to the survey are:

Bureaucracy (74%)

Unclear regulatory environment (72%)

Tax administration (66%)

Customs clearance delays (62%)

Customs and trade regulations (61%)

Difficulty enforcing contract terms (61%)

Obtaining required licenses (58%)

Difficulty in litigation (50%)

Domestic protectionism (between provinces) (49%)

Legal restrictions on market access (49%)

Regulatory Challenges

The environment for foreign companies in China has been getting tougher since 2006, when the

nation came to the end of a five-year schedule of market-opening measures it pledged as the

price of admission to the World Trade Organization. Soon after the WTO-mandated reforms

concluded, foreign firms began to complain of an increase in discriminatory practices, more

difficulty in getting licences and approvals, and a generally less friendly attitude from officialdom.

The wordings of the Chinese laws are often ambiguous and hence can be interpreted in many

ways. Laws on trade, intellectual property rights, labor and taxation are often refined which leads

to complexity in interpretation of the laws.

Antitrust laws

China's Anti-Monopoly law was adopted in 2007. Its provisions are partly consistent with

Western economies’ competition policy frameworks, in that they provide for a substantive test of

the impact on competition and consumers of the merger or anti-competitive conduct.

In contrast to the European law, however, the Chinese law leaves significant room for the use of

competition policy to further industrial policy objectives. The Chinese law explicitly allows the

inclusion of ‘economic development’ and ‘national interest’ in the assessment. The Chinese

antitrust law can therefore technically be used to pursue industrial policy objectives and protect

domestic industries.

Ministry of Commerce’s commitment decisions often aim to protect domestic competitors from

the potential increase in the competitiveness of merged companies. Companies are sometimes

prevented from pursuing a certain line of business (like Wal-Mart/NiuHai), or from reducing

their input costs.10

Finding a local partner

Finding a local partner to do business in China is crucial because has China has "gained a

reputation as a place where deals and contracts are often treated more like suggestions than

concrete agreements"11.

Having a Chinese partner does pose some risk. The partner company could infringe the foreign

company's intellectual property, so it's critical to vet potential partners thoroughly before making

any decisions. Ideally, a good partner is an incorporated company that is about the same size as

the entering firm, at least partly Chinese-owned, has a strong network and is well-connected in

the Chinese market. Partnering with massive state-owned enterprises is best avoided, according

to leading law consultants. It is advisable to retain a Chinese lawyer before attempting to enter

the Chinese market, as the paperwork and regulations, while not as opaque as in the past, are still

difficult for a foreigner to navigate.

Due diligence is required to reduce the risk of poor partnering to the entrant's business12. Below

are situations that careful due diligence can help avoid.

Fake companies - A company approaches and offers a big deal with very favourable

margins. This would involve paying a certain amount of “relationship building” fees to

clear the relationship with important local stakeholders. The company disappears soon

after you transmit the money to its account.

Paper tigers - A company promotes itself a leading company in its industry but fails to

present any strong and persuasive evidence to substantiate its claims.

Shell companies - A company with registration information but with no significant assets

or active business records.

Parasite companies – A company relying heavily on its relationship with local

government officials.

Intellectual Property – Infringement & Enforcement13

The legal framework for protecting intellectual property in China is built on three national laws

passed by the National People's Congress (NPC): the Patent Law, the Trademark Law and the

Copyright Law. The framework of regulations, rules, measures and policies have been made by

the NPC Standing Committee, the State Council and various ministries, bureaux and

commissions.

To enforce IPR protection, an administrative system has been established within the

government. To handle cases of infringement of IPRs more efficiently, special intellectual

property courts have been established in some cities and provinces.

10

http://www.voxeu.org/article/chinese-competition-policy 11

http://www.ibtimes.com/how-do-business-china-guide-entrepreneurs-investors-1378695 12

http://www.tradecommissioner.gc.ca/eng/document.jsp?did=132268 13

“Understanding China’s Business Risk Environment”, Marsh Risk Alert, Volume V Issue 3

The enforcement of protection of intellectual property rights is difficult in China. Without

adequate education with regard to IPRs, there is little awareness that infringement is a crime.

Strict laws and patents in economies of the West protect domestic and foreign businesses,

whereas in China, the legal system is designed in such a way that gives rise to ambiguity.

“Shanzhai” 14is an integral part of the Chinese tradition promotes individuals sharing what they

create with the society to promote greater harmony. Shanzhai in business today takes the form of

imitation of goods. Hence anything from shoes to cell phones are copied and sold openly in

markets across the country. China today is the world’s largest producer of counterfeit products.

Governments around the world continue to pressure Chinese authorities to do a better job of

enforcing IP laws, and there are signs of progress. In May 2006, President Hu made a speech in

the Political Bureau of the Chinese Communist Party calling for strengthening the country’s IP

system.

Some progress has also been seen in enforcement. In February 2006, the U.S. Department of

Justice obtained a conviction against a U.S. citizen for counterfeiting a popular pharmaceutical.

With the cooperation of Chinese law enforcement, the operation resulted in the seizure in China

of 600,000 labels, 440,000 tablets, and more than 500 pounds of raw pharmaceutical

manufacturing materials.

China’s State Administration of Industry and Commerce (SAIC) is the primary enforcer of IP

regulations. It has the authority to seize counterfeits from markets, warehouses, and factories.

Many companies find it helps to be proactive with the SAIC by using an independent

investigative firm to track counterfeiters, locate the warehouse or the factory where the

counterfeiters are producing the product, and then pass the information on to the SAIC along

with a formal letter of complaint. In theory, the SAIC should then raid the offending site. Brand

owners are well-advised to keep up the pressure on pirates through investigations and raid

actions. They should also practice thorough due diligence on employees and potential business

partners to see if they have a track record of IP theft or are currently involved in counterfeit

activities.

International Disputes Resolution15

China has several institutions for arbitration such as China International Economic and Trade

Arbitration Commission (CIETAC). Only litigations containing an "external element" can be

arbitrated outside China.

Dispute resolution in the commercial area is characterized by: (i) demonstrable overall progress;

(ii) considerable efforts to improve the regulatory framework and respond to investor needs,

14

Jayaraman, Karthik:"Doing business in China: A risk analysis", Journal of Emerging Knowledge on Emerging Markets, Fudan University & The Norwegian School of Management, November 2009 15

"Dispute Resolution in China: Patterns, Causes, and Prognosis": Randall Peerenboom and He Xin - The Foundation for Law, Justice and Society in collaboration with The Centre for Socio-Legal Studies,University of Oxford

thus reducing vertical disputes and tensions between businesses and the state; (iii) a rapid rise in

litigation to resolve horizontal commercial disputes among business operators through the late

1990s followed by relative stability; (iv) improvements in enforcement, particularly in more

developed urban areas; (v) notwithstanding considerable progress, ongoing problems with

litigation, including significant regional differences in the nature of the economy, the nature of

disputes and institutional capacity, and (vi) a renewed emphasis on judicial mediation in response

to ongoing problems

SWOT Analysis of General Business Environment

Strengths

Opening up various sectors of its economy to foreign investment.

China is the top destination for FDI with its vast supply of cheap labour.

Weaknesses

Foreign companies complain about the poor protection of intellectual property in China.

Chinese corporate governance is weak and non-transparent by Western standards.

Choice of right local partner is accompanied by considerable risk for foreign companies.

Opportunities

Urbanisation and infrastructure drive will provide major opportunities for foreign

investment in landlocked provinces as well as the transfer of skills and knowhow.

The Chinese government is giving more protection and encouragement to the private

sector, which is now the most dynamic in the economy and accounts for most of the

country's job growth.

Threats

China's government might block attempts by foreign firms to take over assets of national

importance.

China is experiencing rising labour costs, prompting some investors to turn to cheaper

destinations such as Vietnam.

Pharmaceutical Industry in China – legal & regulatory dimension

The domestic pharmaceutical market in China is highly fragmented. Traditional systems of

medicine have long had a major presence in China. The industry is still small-scale with a

scattered geographical layout, duplicated production processes, and outdated manufacturing

technology and management structures. The Chinese pharmaceutical industry also has a low

market concentration and weak international trading competitiveness, coupled with a lack of

patented domestically-developed pharmaceuticals.

Earlier, the industry had been riddled with problems such as: Poor IP rights protection, non-

transparency for drug approval procedures, ineffective governmental incentives, and poor

corporate support for drug research.

Accession to the WTO has brought a stronger patent system, medical insurance is now more

widespread, and pharmaceutical-related regulations have been tightened. Changes to the

patenting laws in full compliance with the requirement of the Agreement on Trade-Related

Aspects of Intellectual Property Rights (TRIPS Agreement) and the poorly developed

infrastructure of Chinese pharmaceutical R&D have created gaps in the market, which offer a

scope for foreign investments.

SWOT Analysis of the pharmaceuticals industry16

Strengths

Progressive healthcare Reform by Central government

Among the top five drug markets in the world in terms of overall size.

Large pool of highly skilled, low-cost scientists and general labour.

Rising per capita drug expenditure on the back of strong economic growth.

Weaknesses

Highly fragmented market.

Complex and protectionist (biased) drug pricing and reimbursement policy by the

government,

Lack of tight enforcement of domestic patent laws.

General focus on lower-cost pharmaceuticals and production overcapacity.

Government bureaucracy, non-transparency and corruption.

Opportunities

Rapid growth in generic drug sector.

Patented drug sector growth boosted by rising demand for hi-tech treatments.

The fastest growing over-the-counter drugs sector in Asia.

Modernisation of local manufacturing sector

Rising foreign direct investment (FDI) following increased intellectual property rights

Increased tax revenues, allowing the government to expand health insurance coverage.

New and improved drug registration process to place less emphasis on personal

connections.

Increasing research and development capacity.

Part 4 Chinese Pharmaceutical Market17

The Chinese Pharmaceutical market is currently the third greatest pharma market globally, after

the US and Japan, and in 2011 was worth $40 billion. It is forecast to increase dramatically to

$200 billion by 2020 and increase its dominance as a leading player in Asia. As the current third

market leader it is predicted that the Chinese pharma market will be the main competitor of the

US by 2020. The Chinese pharmaceutical market is the main driver of the countries healthcare

industry and in 2011 dominated with almost 90% share. Within the pharmaceutical industry

drugs and active pharmaceuticals (API) are the main revenue generators. Over the Counter

16

Business Monitor International: China – Pharmaceuticals & Healthcare Report, Q4, 2012 17

Deloitte: Opportunities in China's pharmaceuticals market, 2011

(OTC) medicines had a Chinese market figure of $9 billion in 2008 (18% of total market share)

and by 2013 will become the world’s second largest OTC market. In the same year prescription

medicines dominated the market place with 62% share, and traditional Chinese medicine (TCM)

made up almost 20%. Diabetes is one of the most successful therapeutic areas in the Chinese

market and will reach over $2 billion in annual sales in 2019, compared to $700 million in 2009.

Vaccine production is a leading strength in China with the ability to produce almost 1 billion

doses each year according to the State Food and Drug Administration (SFDA). The country has

almost 40 (38 in 2011) companies with vaccine manufacturing capabilities and the vaccine

market was worth an estimated RMB1 billion in 2011. Over 40 different vaccines covering more

than 26 indications are currently being made in China. The main vaccines that are currently

exported are against hepatitis A, influenza and Japanese encephalitis. The oncology market in

China is forecast to grow steadily and reach $2.2 billion by 2017 from $830 million in 2009 with

a CAGR of 12.9%.

Growing and distinctive Chinese pharmaceutical market

1. Pharmaceutical sales grew at a CAGR of 25.9 percent from 2007 through 2010, and are

expected to continue strong but more modest growth from 2010 through 2015, at a

CAGR of 15.5 percent.

2. The aging population will generate higher demand for health care services. Currently, the

elderly population makes up 23 to 40 percent of the prescription drug market and 40 to

50 percent of the over-the-counter (OTC) drug market.

3. Out-of-pocket and private insurance healthcare payments rose steadily from 2007

through 2010, at a CAGR of 13.5 percent and expected to grow at a lower rate of 8.5