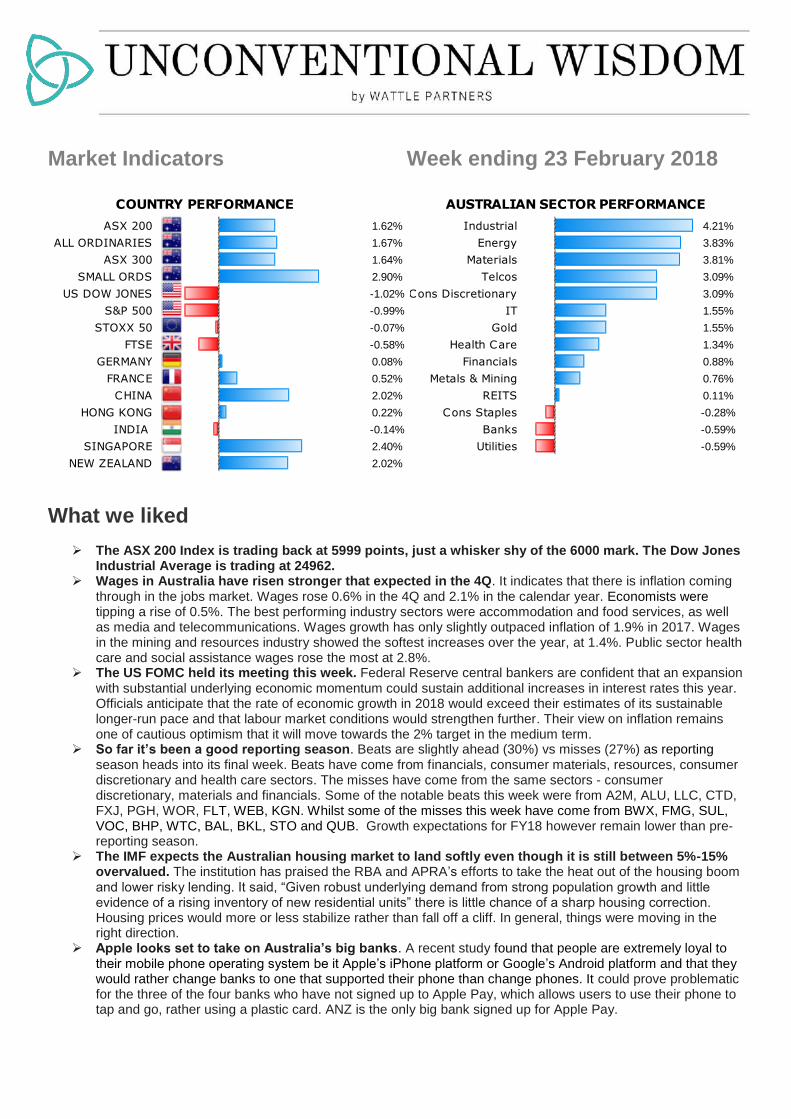

Market Indicators Week ending 23 February 2018 What we liked The ASX 200 Index is trading back at 5999 points, just a whisker shy of the 6000 mark. The Dow Jones Industrial Average is trading at 24962. Wages in Australia have risen stronger that expected in the 4Q. It indicates that there is inflation coming through in the jobs market. Wages rose 0.6% in the 4Q and 2.1% in the calendar year. Economists were tipping a rise of 0.5%. The best performing industry sectors were accommodation and food services, as well as media and telecommunications. Wages growth has only slightly outpaced inflation of 1.9% in 2017. Wages in the mining and resources industry showed the softest increases over the year, at 1.4%. Public sector health care and social assistance wages rose the most at 2.8%. The US FOMC held its meeting this week. Federal Reserve central bankers are confident that an expansion with substantial underlying economic momentum could sustain additional increases in interest rates this year. Officials anticipate that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labour market conditions would strengthen further. Their view on inflation remains one of cautious optimism that it will move towards the 2% target in the medium term. So far it’s been a good reporting season. Beats are slightly ahead (30%) vs misses (27%) as reporting season heads into its final week. Beats have come from financials, consumer materials, resources, consumer discretionary and health care sectors. The misses have come from the same sectors - consumer discretionary, materials and financials. Some of the notable beats this week were from A2M, ALU, LLC, CTD, FXJ, PGH, WOR, FLT, WEB, KGN. Whilst some of the misses this week have come from BWX, FMG, SUL, VOC, BHP, WTC, BAL, BKL, STO and QUB. Growth expectations for FY18 however remain lower than pre- reporting season. The IMF expects the Australian housing market to land softly even though it is still between 5%-15% overvalued. The institution has praised the RBA and APRA’s efforts to take the heat out of the housing boom and lower risky lending. It said, “Given robust underlying demand from strong population growth and little evidence of a rising inventory of new residential units” there is little chance of a sharp housing correction. Housing prices would more or less stabilize rather than fall off a cliff. In general, things were moving in the right direction. Apple looks set to take on Australia’s big banks. A recent study found that people are extremely loyal to their mobile phone operating system be it Apple’s iPhone platform or Google’s Android platform and that they would rather change banks to one that supported their phone than change phones. It could prove problematic for the three of the four banks who have not signed up to Apple Pay, which allows users to use their phone to tap and go, rather using a plastic card. ANZ is the only big bank signed up for Apple Pay. ASX 200 1.62% Industrial 4.21% ALL ORDINARIES 1.67% Energy 3.83% ASX 300 1.64% Materials 3.81% SMALL ORDS 2.90% Telcos 3.09% US DOW JONES -1.02% Cons Discretionary 3.09% S&P 500 -0.99% IT 1.55% STOXX 50 -0.07% Gold 1.55% FTSE -0.58% Health Care 1.34% GERMANY 0.08% Financials 0.88% FRANCE 0.52% Metals & Mining 0.76% CHINA 2.02% REITS 0.11% HONG KONG 0.22% Cons Staples -0.28% INDIA -0.14% Banks -0.59% SINGAPORE 2.40% Utilities -0.59% NEW ZEALAND 2.02% COUNTRY PERFORMANCE AUSTRALIAN SECTOR PERFORMANCE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Market Indicators Week ending 23 February 2018

What we liked

The ASX 200 Index is trading back at 5999 points, just a whisker shy of the 6000 mark. The Dow Jones Industrial Average is trading at 24962.

Wages in Australia have risen stronger that expected in the 4Q. It indicates that there is inflation coming through in the jobs market. Wages rose 0.6% in the 4Q and 2.1% in the calendar year. Economists were tipping a rise of 0.5%. The best performing industry sectors were accommodation and food services, as well as media and telecommunications. Wages growth has only slightly outpaced inflation of 1.9% in 2017. Wages in the mining and resources industry showed the softest increases over the year, at 1.4%. Public sector health care and social assistance wages rose the most at 2.8%.

The US FOMC held its meeting this week. Federal Reserve central bankers are confident that an expansion with substantial underlying economic momentum could sustain additional increases in interest rates this year. Officials anticipate that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labour market conditions would strengthen further. Their view on inflation remains one of cautious optimism that it will move towards the 2% target in the medium term.

So far it’s been a good reporting season. Beats are slightly ahead (30%) vs misses (27%) as reporting season heads into its final week. Beats have come from financials, consumer materials, resources, consumer discretionary and health care sectors. The misses have come from the same sectors - consumer discretionary, materials and financials. Some of the notable beats this week were from A2M, ALU, LLC, CTD, FXJ, PGH, WOR, FLT, WEB, KGN. Whilst some of the misses this week have come from BWX, FMG, SUL, VOC, BHP, WTC, BAL, BKL, STO and QUB. Growth expectations for FY18 however remain lower than pre-reporting season.

The IMF expects the Australian housing market to land softly even though it is still between 5%-15% overvalued. The institution has praised the RBA and APRA’s efforts to take the heat out of the housing boom and lower risky lending. It said, “Given robust underlying demand from strong population growth and little evidence of a rising inventory of new residential units” there is little chance of a sharp housing correction. Housing prices would more or less stabilize rather than fall off a cliff. In general, things were moving in the right direction.

Apple looks set to take on Australia’s big banks. A recent study found that people are extremely loyal to their mobile phone operating system be it Apple’s iPhone platform or Google’s Android platform and that they would rather change banks to one that supported their phone than change phones. It could prove problematic for the three of the four banks who have not signed up to Apple Pay, which allows users to use their phone to tap and go, rather using a plastic card. ANZ is the only big bank signed up for Apple Pay.

ASX 200 1.62% Industrial 4.21%

ALL ORDINARIES 1.67% Energy 3.83%

ASX 300 1.64% Materials 3.81%

SMALL ORDS 2.90% Telcos 3.09%

US DOW JONES -1.02% Cons Discretionary 3.09%

S&P 500 -0.99% IT 1.55%

STOXX 50 -0.07% Gold 1.55%

FTSE -0.58% Health Care 1.34%

GERMANY 0.08% Financials 0.88%

FRANCE 0.52% Metals & Mining 0.76%

CHINA 2.02% REITS 0.11%

HONG KONG 0.22% Cons Staples -0.28%

INDIA -0.14% Banks -0.59%

SINGAPORE 2.40% Utilities -0.59%

NEW ZEALAND 2.02%

COUNTRY PERFORMANCE AUSTRALIAN SECTOR PERFORMANCE

What we didn’t like

The RBA released its monthly minutes from its latest meeting. The central bank said it is keeping an eye

on a large number of interest-only loans that are due to expire between 2018 and 2022. Some of which may not meet the more conservative lending standards currently being imposed. The number stands at around approximately $60bn in interest only loans written at the peak of the property boom that are due to reset in the next four years. Once these expire, they’ll switch to principal and interest repayments as originally contracted. The concern is that some borrowers that do not meet current lending standards for extending their interest-only repayments and will find the higher principal and interest repayments difficult to manage. If they find themselves in hardship, it could cause a knock on effect.

Shareholders of Platinum Asset Management (PTM) were dealt a bit of a blow this week after CEO Kerr Neilson, the legendary investor and founder of PTM decided to step back from the top job and to become an executive director. Shares fell 12% on the day of the announcement. Andrew Clifford, Platinum's chief investment officer, will succeed Mr Neilson from July 1, 2018. Mr Neilson long-term record was outstanding and he has no reason to sell his equity stake in the company. His personal wealth was valued at $1.44bn by Financial Review Rich List 2017.

It’s been a savage week for some market darlings such as BWX and WiseTech Global (WTC) which fell 30% and 23% respectively. It’s concerning when most of the leading brokers had a Buy recommendation on both BWX and WTC days before their announcements. One research note from Goldman Sachs tried to calm investor nerves by saying that they weren’t overly concerned that BWX’s Sukin range was losing steam in China. It instead believes Sukin’s main markets are USA, Canada, and UK and is well-positioned to grow in them. Investors need to be careful with highly pumped up stocks such as both WTC and BWX especially when they don’t deliver better than expected results.

Weak spending and low inflation is bad news for retails who are going through tough times already. Strong competition in the retail sector, has placed downward pressure on the prices of consumer durables and food for some time. The RBA says more of this is expected to persist in the next few years. Low household income growth has constrained consumption and made it tough for some retailers this reporting season.

Economic Insights In this section, we look at the economic news affecting global markets this week. Australia

The RBA released its monthly minutes, no real surprises. It kept the cash rate at 1.5% and has since August 2016. The board is concerned about household consumption but encouraged by retail sales, which rebounded in December. It expects household income growth to rise. The RBA was also cautious about the outlook for wages growth and hours worked. What can be seen is that there is no urgency to tighten rates. The view among most economists is that the RBA will sit on hold for some time yet and are pricing in a rate hike in early 2019.

Construction work done fell 19.4% in the 4Q. There was a large decline in total construction work done. Engineering work done tumbled by 35.4% due to the import of the Prelude & Ichthys FLNG platforms which fell out of the equation. Building work done rose by 0.2% in the 4Q giving a 1.1% annual rise. Residential work

done eased by 1.9 per cent while non‑residential work done lifted by 4.0 per cent in the quarter.

US

US Consumer sentiment rose in February to 99.9 last month. It was the second highest reading since 2004. Analysts had forecast the reading to slip to 95.4.

The minutes from the Federal Reserve’s Jan monetary policy meeting show that that inflation target should be met in 2018. Some officials saw an appreciable risk of inflation lag to target. VIX slightly lower. Gold and stocks higher. The recent strengthening of the US economy increased the likely hood that rates will tick higher this year. Inflation will rise in 2018 and stabilise in the medium term. A couple of officials are concerned about the outlook. Some officials saw an appreciable risk of inflation lag to target. A number of officials raised economic growth forecast based on better data. The tax overhaul might have larger effects as previously thought and there it is important to monitor slope of the yield curve. Finally officials cautioned about market imbalances.

Eurozone

British households are concerned about their finances with most expecting borrowing costs to rise again within six months after the Bank of England propped up rates last November. Markit said its Household Finance Index, a monthly gauge of financial well-being, fell to a seven-month low of 42.2 from 42.9 in January.

The Bank of England could end up raising rates faster than expected if required. Britain is growing slower than developed economies but is benefiting from a global upturn. Unemployment is at a 40-year low which is why the higher rates argument is back on the table.

Market Insights

In this section we look at all the important announcements affecting companies this week.

Brambles (BXB) – Posted its highly antipated HY profit result and there was a lot riding on it following what has

been a tough year. The pallet maker posted an underlying NPAT rise of 1% to US$493.7m which was is line with expectations. It’s NPAT came in at US$447.2m up from US$146.2m. The result was buoyed by a one off-benefit of US$130.1m due to a reduction in the company’s net deferred tax liability in the US.

Santos (STO) – Shares were down after the oil and gas producer posted its interim result. It missed expectations. Underlying profit rose more than five-fold to US$336m but it was lower than a consensus forecast of US$349m. Overall it was a loss of US$360m which was a big reduction from US$1.047bn in 2016. The loss included an impairment charges of US$689m against Gladstone LNG, US$149m against Ande Ande Lumut and US$14m against another asset. Sales rose 21% to US$3.17bn. Despite the miss, the result was a positive result and vast improvement from previous results. It showed a definite turnaround and that the business was tracking along well. Free cash flow was up and net debt was lower. The board decided to pay down debt instead of declare a dividend

Seven West Media (SWM) – Posted a strong profit result, shares closed the day up almost 20% after the company beat profit expectations. It increased its cost cutting plans to $125m which was cheered on by the market although it has suspended dividend due to weaker revenue and rising competition from Nine Entertainment.

Lendlease (LLC) has delivered a 7.8% rise in profit to $425.7m which was a lot higher than an expected $365m. Revenue rose 9.4% to $8.69bn from $7.95bn. It was a strong performance driven by the group's development segment supported by the residential sector. The only laggard was the company’s construction segment which underperformed. Interim distribution 34c. LLC also announced an on market share buyback up to $500m.

GetSwift (GSW) shares came back on line and plummeted by more than 60% after the company confessed that less than half its announced contracts had progressed to a revenue generating stage. According to GetSwift’s website it claimed it had landed deals with big brands such as Pizza Hut, CBA and even Amazon. The Amazon contract cause an 84% share rise and subsequent $100m capital raising. But thanks to the sceptics, its bogus contracts were found out and proven disingenuous. Shares fell another 20% after disgrunted shareholders launched a $300m class action against the company alleging Mr Macdonald and GSW mislead and deceived investors about its contracts.

Woodside Petroleum (WPL) – Has completed its $2.5bn capital raising with $1.57bn coming from institutions and the remaining rights sold in the shortfall bookbuild. The equity raising will fund ExxonMobil’s stake in the Scarborough gas field and other projects.

Vocus Group (VOC) – More bad news. Shares were hit after the company cut its full-year profit guidance due to a rise in subscriber costs in its consumer business and softer than expected energy sign ups. It now expects FY underlying NPAT to come in at $125m-$135m down from $140m-$150m.

Aconex (ACX) – Has posted a solid result. It boosted revenue by 12.8% to $86.9m. Database giant Oracle has made a takeover bid of $1.6bn which its management and board support.

Oil Search (OSH) – Has tripled its dividend on the back of FY profit of US$302.1m. This was up 213% on the back of higher prices and record production. The result was in line with analysts’ expectations with a final dividend of US5.5c.It signalled a proposed LNG expansion that would double gas exports from PNG. It has yet to be approved by the Government.

Lovisa (LOV) – 1H NPAT rise 22.5% pc to $24.8m. The fashion jeweller defied the retal slump and posted a better than expected profit result boosted by its global store expansion program. NPAT rose 22.5% to $24.84m while revenue rose 19% to $118.62m. EBITDA was up 3.2% to $34.7m which fell in line with its guidance for $34.5m-$35m. Interim dividend of 13c.

a2 Milk Company Ltd 36.50% Vocus Group Ltd -14.34%

Altium Ltd 36.27% Blackmores Ltd -13.28%

Seven West Media Ltd 29.59% InvoCare Ltd -12.05%

Nine Entertainment Co Holdings Ltd 26.23% Iress Ltd -13.18%

Webjet Ltd 24.63% Woodside Petroleum Ltd -11.45%

GWA Group Ltd 22.79% Fletcher Building Ltd -8.28%

Corporate Travel Management Ltd 19.55% Domino's Pizza Enterprises Ltd -7.44%

Fairfax Media Ltd 20.49% AGL Energy Ltd -6.98%

NEXTDC Ltd 15.97% Western Areas Ltd -7.34%

Flight Centre Travel Group Ltd 15.40% Orocobre Ltd -4.79%

ASX 200 MOVERS & SHAKERS THIS WEEK

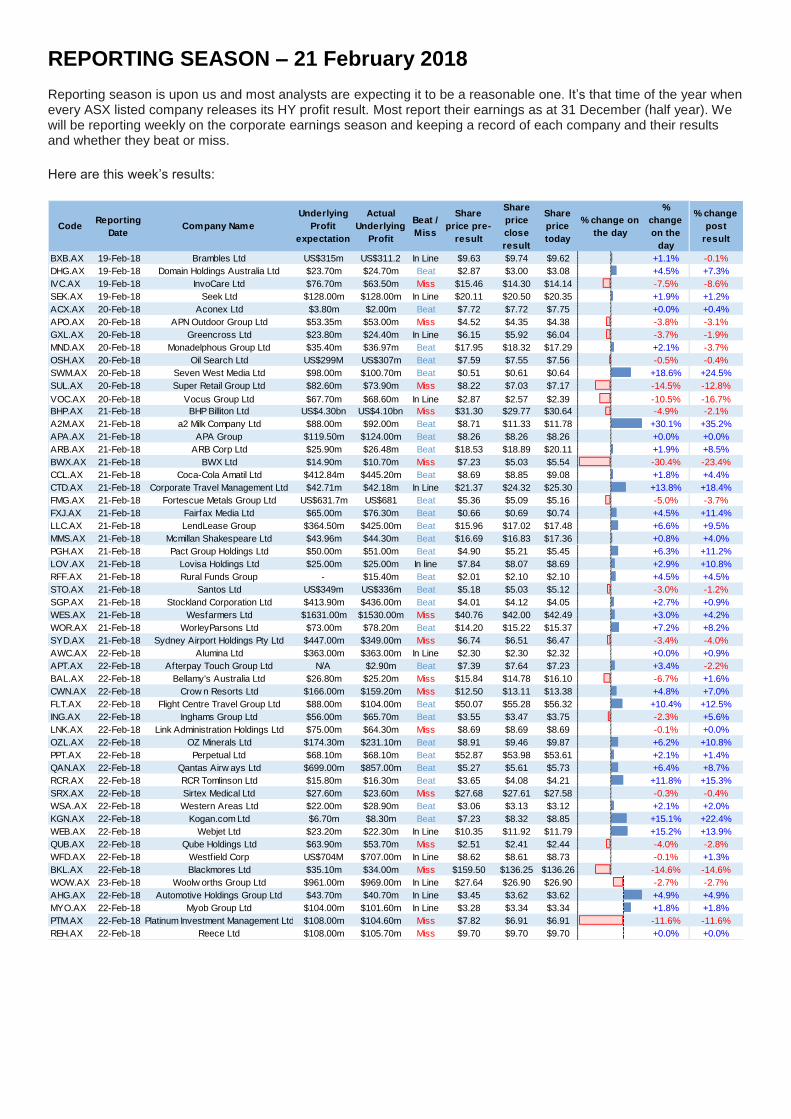

REPORTING SEASON – 21 February 2018

Reporting season is upon us and most analysts are expecting it to be a reasonable one. It’s that time of the year when every ASX listed company releases its HY profit result. Most report their earnings as at 31 December (half year). We will be reporting weekly on the corporate earnings season and keeping a record of each company and their results and whether they beat or miss.

Here are this week’s results:

CodeReporting

DateCompany Name

Underlying

Profit

expectation

Actual

Underlying

Profit

Beat /

Miss

Share

price pre-

result

Share

price

close

result

Share

price

today

% change on

the day

%

change

on the

day

% change

post

result

BXB.AX 19-Feb-18 Brambles Ltd US$315m US$311.2 In Line $9.63 $9.74 $9.62 +1.1% -0.1%

DHG.AX 19-Feb-18 Domain Holdings Australia Ltd $23.70m $24.70m Beat $2.87 $3.00 $3.08 +4.5% +7.3%

IVC.AX 19-Feb-18 InvoCare Ltd $76.70m $63.50m Miss $15.46 $14.30 $14.14 -7.5% -8.6%

SEK.AX 19-Feb-18 Seek Ltd $128.00m $128.00m In Line $20.11 $20.50 $20.35 +1.9% +1.2%

ACX.AX 20-Feb-18 Aconex Ltd $3.80m $2.00m Beat $7.72 $7.72 $7.75 +0.0% +0.4%

APO.AX 20-Feb-18 APN Outdoor Group Ltd $53.35m $53.00m Miss $4.52 $4.35 $4.38 -3.8% -3.1%

GXL.AX 20-Feb-18 Greencross Ltd $23.80m $24.40m In Line $6.15 $5.92 $6.04 -3.7% -1.9%

MND.AX 20-Feb-18 Monadelphous Group Ltd $35.40m $36.97m Beat $17.95 $18.32 $17.29 +2.1% -3.7%

OSH.AX 20-Feb-18 Oil Search Ltd US$299M US$307m Beat $7.59 $7.55 $7.56 -0.5% -0.4%

SWM.AX 20-Feb-18 Seven West Media Ltd $98.00m $100.70m Beat $0.51 $0.61 $0.64 +18.6% +24.5%

SUL.AX 20-Feb-18 Super Retail Group Ltd $82.60m $73.90m Miss $8.22 $7.03 $7.17 -14.5% -12.8%

VOC.AX 20-Feb-18 Vocus Group Ltd $67.70m $68.60m In Line $2.87 $2.57 $2.39 -10.5% -16.7%

BHP.AX 21-Feb-18 BHP Billiton Ltd US$4.30bn US$4.10bn Miss $31.30 $29.77 $30.64 -4.9% -2.1%

A2M.AX 21-Feb-18 a2 Milk Company Ltd $88.00m $92.00m Beat $8.71 $11.33 $11.78 +30.1% +35.2%

APA.AX 21-Feb-18 APA Group $119.50m $124.00m Beat $8.26 $8.26 $8.26 +0.0% +0.0%

ARB.AX 21-Feb-18 ARB Corp Ltd $25.90m $26.48m Beat $18.53 $18.89 $20.11 +1.9% +8.5%

BWX.AX 21-Feb-18 BWX Ltd $14.90m $10.70m Miss $7.23 $5.03 $5.54 -30.4% -23.4%

CCL.AX 21-Feb-18 Coca-Cola Amatil Ltd $412.84m $445.20m Beat $8.69 $8.85 $9.08 +1.8% +4.4%

CTD.AX 21-Feb-18 Corporate Travel Management Ltd $42.71m $42.18m In Line $21.37 $24.32 $25.30 +13.8% +18.4%

FMG.AX 21-Feb-18 Fortescue Metals Group Ltd US$631.7m US$681 Beat $5.36 $5.09 $5.16 -5.0% -3.7%

FXJ.AX 21-Feb-18 Fairfax Media Ltd $65.00m $76.30m Beat $0.66 $0.69 $0.74 +4.5% +11.4%

LLC.AX 21-Feb-18 LendLease Group $364.50m $425.00m Beat $15.96 $17.02 $17.48 +6.6% +9.5%

MMS.AX 21-Feb-18 Mcmillan Shakespeare Ltd $43.96m $44.30m Beat $16.69 $16.83 $17.36 +0.8% +4.0%

PGH.AX 21-Feb-18 Pact Group Holdings Ltd $50.00m $51.00m Beat $4.90 $5.21 $5.45 +6.3% +11.2%

LOV.AX 21-Feb-18 Lovisa Holdings Ltd $25.00m $25.00m In line $7.84 $8.07 $8.69 +2.9% +10.8%

RFF.AX 21-Feb-18 Rural Funds Group - $15.40m Beat $2.01 $2.10 $2.10 +4.5% +4.5%

STO.AX 21-Feb-18 Santos Ltd US$349m US$336m Beat $5.18 $5.03 $5.12 -3.0% -1.2%

SGP.AX 21-Feb-18 Stockland Corporation Ltd $413.90m $436.00m Beat $4.01 $4.12 $4.05 +2.7% +0.9%

WES.AX 21-Feb-18 Wesfarmers Ltd $1631.00m $1530.00m Miss $40.76 $42.00 $42.49 +3.0% +4.2%

WOR.AX 21-Feb-18 WorleyParsons Ltd $73.00m $78.20m Beat $14.20 $15.22 $15.37 +7.2% +8.2%

SYD.AX 21-Feb-18 Sydney Airport Holdings Pty Ltd $447.00m $349.00m Miss $6.74 $6.51 $6.47 -3.4% -4.0%

AWC.AX 22-Feb-18 Alumina Ltd $363.00m $363.00m In Line $2.30 $2.30 $2.32 +0.0% +0.9%

APT.AX 22-Feb-18 Afterpay Touch Group Ltd N/A $2.90m Beat $7.39 $7.64 $7.23 +3.4% -2.2%

BAL.AX 22-Feb-18 Bellamy's Australia Ltd $26.80m $25.20m Miss $15.84 $14.78 $16.10 -6.7% +1.6%

CWN.AX 22-Feb-18 Crow n Resorts Ltd $166.00m $159.20m Miss $12.50 $13.11 $13.38 +4.8% +7.0%

FLT.AX 22-Feb-18 Flight Centre Travel Group Ltd $88.00m $104.00m Beat $50.07 $55.28 $56.32 +10.4% +12.5%

ING.AX 22-Feb-18 Inghams Group Ltd $56.00m $65.70m Beat $3.55 $3.47 $3.75 -2.3% +5.6%

LNK.AX 22-Feb-18 Link Administration Holdings Ltd $75.00m $64.30m Miss $8.69 $8.69 $8.69 -0.1% +0.0%

OZL.AX 22-Feb-18 OZ Minerals Ltd $174.30m $231.10m Beat $8.91 $9.46 $9.87 +6.2% +10.8%

PPT.AX 22-Feb-18 Perpetual Ltd $68.10m $68.10m Beat $52.87 $53.98 $53.61 +2.1% +1.4%

QAN.AX 22-Feb-18 Qantas Airw ays Ltd $699.00m $857.00m Beat $5.27 $5.61 $5.73 +6.4% +8.7%

RCR.AX 22-Feb-18 RCR Tomlinson Ltd $15.80m $16.30m Beat $3.65 $4.08 $4.21 +11.8% +15.3%

SRX.AX 22-Feb-18 Sirtex Medical Ltd $27.60m $23.60m Miss $27.68 $27.61 $27.58 -0.3% -0.4%

WSA.AX 22-Feb-18 Western Areas Ltd $22.00m $28.90m Beat $3.06 $3.13 $3.12 +2.1% +2.0%

KGN.AX 22-Feb-18 Kogan.com Ltd $6.70m $8.30m Beat $7.23 $8.32 $8.85 +15.1% +22.4%

WEB.AX 22-Feb-18 Webjet Ltd $23.20m $22.30m In Line $10.35 $11.92 $11.79 +15.2% +13.9%

QUB.AX 22-Feb-18 Qube Holdings Ltd $63.90m $53.70m Miss $2.51 $2.41 $2.44 -4.0% -2.8%

WFD.AX 22-Feb-18 Westfield Corp US$704M $707.00m In Line $8.62 $8.61 $8.73 -0.1% +1.3%

BKL.AX 22-Feb-18 Blackmores Ltd $35.10m $34.00m Miss $159.50 $136.25 $136.26 -14.6% -14.6%

WOW.AX 23-Feb-18 Woolw orths Group Ltd $961.00m $969.00m In Line $27.64 $26.90 $26.90 -2.7% -2.7%

AHG.AX 22-Feb-18 Automotive Holdings Group Ltd $43.70m $40.70m In Line $3.45 $3.62 $3.62 +4.9% +4.9%

MYO.AX 22-Feb-18 Myob Group Ltd $104.00m $101.60m In Line $3.28 $3.34 $3.34 +1.8% +1.8%

PTM.AX 22-Feb-18 Platinum Investment Management Ltd $108.00m $104.60m Miss $7.82 $6.91 $6.91 -11.6% -11.6%

REH.AX 22-Feb-18 Reece Ltd $108.00m $105.70m Miss $9.70 $9.70 $9.70 +0.0% +0.0%

Click here to see result commentary:

c

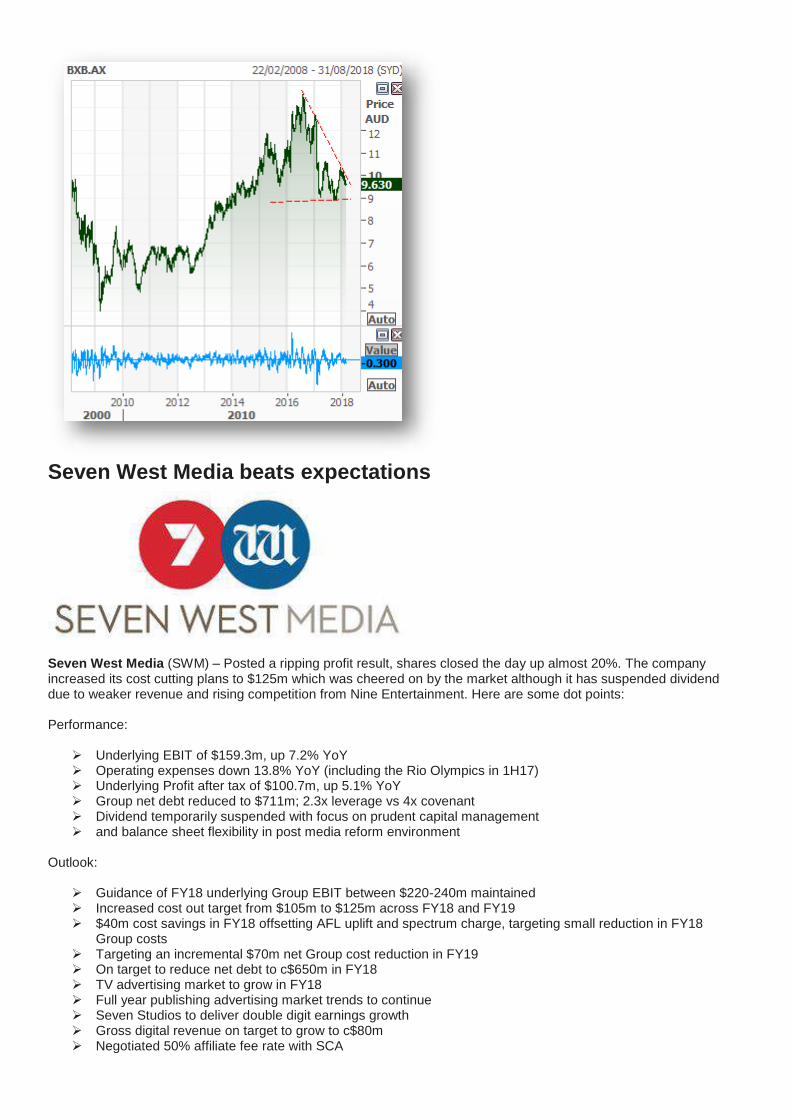

Brambles delivers a pleasing result

Brambles (BXB) – Posted its highly antipated HY profit result and there was a lot riding on it following what has been a tough year. The pallet maker posted an underlying NPAT rise of 1% to US$493.7m which was is line with expectations. It’s NPAT came in at US$447.2m up from US$146.2m. The result was enjoyed a one off-benefit of US$130.1m due to a reduction in the company’s net deferred tax liability in the US. It hasn’t been an easy year for Brambles. Shares were hit hard after it announced a surprise profit warning and writedown as the Amazon effect took its toll. Here are some dot points:

Strong sales revenue performance which was in line with guidance for mid-single digit growth.

Material increase in cash flow from operations which was up US$98.1m.

Interim dividend of 14.5c.

Sale of CHEP Recycled was completed. Proceeds were in line with carrying value and will be reflected in 2H.

Guidance FY18 underlying profit growth will be impacted by 1. The loss of a large Australian RPC contract

and the impact of automotive plant closures of Australian automotive contracts. A loss of US$23m. 2. US$5-

7m investment in BXB Digital is now expected to be US$15-17m. 3. The full year inclusion of losses incurred

in the HFG joint venture.

Unconventional View – Whist the Brambles result was pleasing, we’re not convinced that the company is in the clear yet. Volume growth has returned to the North American business but it’s too early to call this a turnaround story just yet. If you think back, just after BXB posted its profit downgrade, new CEO Graham Chipchase took the reins. He realised that the company’s timber pallets business was at the brink of being disrupted from logistics services offered by global e-commerce group Amazon. This was structural change at its best. To add to it, BXB also faces higher transport costs and higher prices for the timber used in its pallets. The business needs to reinvent or be disrupted. So in the background, Chipchase went on the front foot and started investing in the use of tech, AI and robotics for its logistics. It’s what Amazon have done to build their distributrion network and it’s the right move. It will also help reduce rising costs. Transport and Lumber prices have both risen in the US and Europe. Half of the rising costs are unique to the US business mainly due to its lack of automation. The European business is a lot more advanced and there’s quite a long way to go to automate US. The total cost from inflation rises was US$12m. All in all, we think the result is pleasing but the problem with Brambles is a lot deeper and more concerning. The pallets business is in structural decline. US retailers have stopped collecting goods in their physical stores because consumers have switched to the online phenominom and are ordering goods online via Amazon. This means goods are delivered straight to the consumer by postal vans and parcel couriers cutting out the retailer and the demand for pallets to convey goods to those stores. For Brambles to survive it needs to rethink its business and innovate so that it can adjust to the new competitive pressures. It needs to adopt digital disruption. With the new CEO on board who is more determined than ever to turn the ship around, we think there is potential for BXB to innovate. But it’s too early to see this occuring.

Seven West Media beats expectations

Seven West Media (SWM) – Posted a ripping profit result, shares closed the day up almost 20%. The company increased its cost cutting plans to $125m which was cheered on by the market although it has suspended dividend due to weaker revenue and rising competition from Nine Entertainment. Here are some dot points: Performance:

Underlying EBIT of $159.3m, up 7.2% YoY Operating expenses down 13.8% YoY (including the Rio Olympics in 1H17) Underlying Profit after tax of $100.7m, up 5.1% YoY Group net debt reduced to $711m; 2.3x leverage vs 4x covenant Dividend temporarily suspended with focus on prudent capital management and balance sheet flexibility in post media reform environment

Outlook:

Guidance of FY18 underlying Group EBIT between $220-240m maintained Increased cost out target from $105m to $125m across FY18 and FY19 $40m cost savings in FY18 offsetting AFL uplift and spectrum charge, targeting small reduction in FY18

Group costs Targeting an incremental $70m net Group cost reduction in FY19 On target to reduce net debt to c$650m in FY18 TV advertising market to grow in FY18 Full year publishing advertising market trends to continue Seven Studios to deliver double digit earnings growth Gross digital revenue on target to grow to c$80m Negotiated 50% affiliate fee rate with SCA

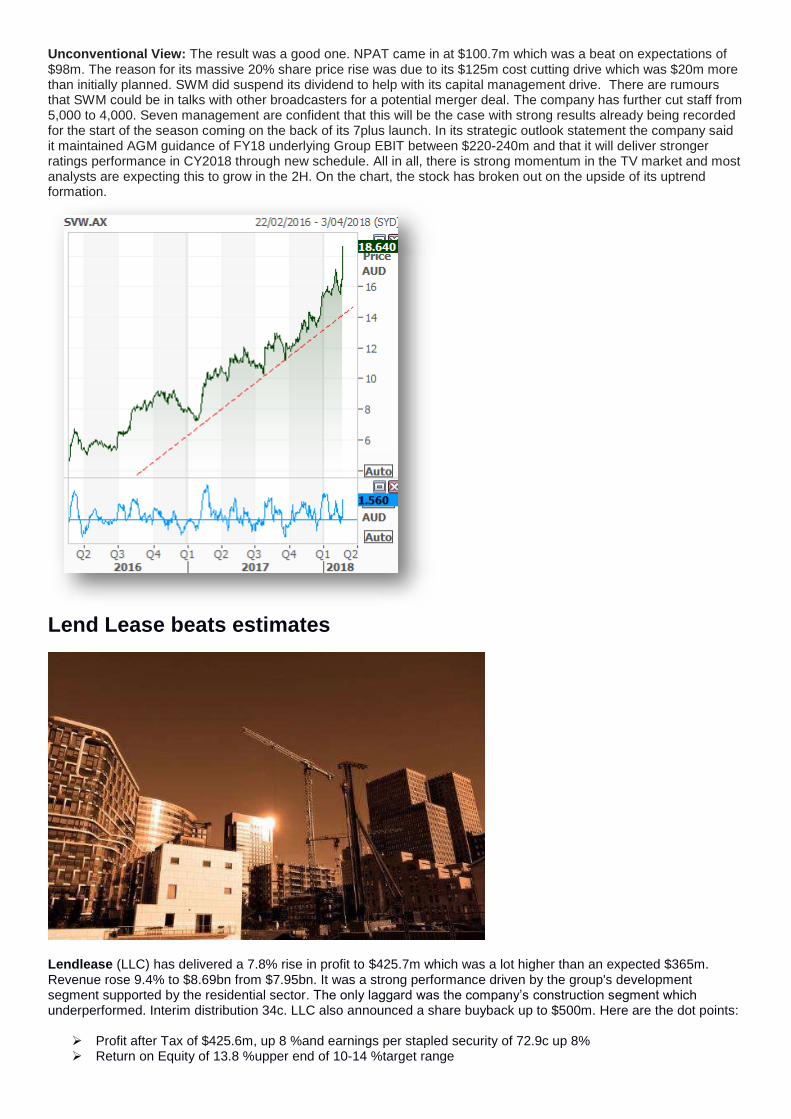

Unconventional View: The result was a good one. NPAT came in at $100.7m which was a beat on expectations of $98m. The reason for its massive 20% share price rise was due to its $125m cost cutting drive which was $20m more than initially planned. SWM did suspend its dividend to help with its capital management drive. There are rumours that SWM could be in talks with other broadcasters for a potential merger deal. The company has further cut staff from 5,000 to 4,000. Seven management are confident that this will be the case with strong results already being recorded for the start of the season coming on the back of its 7plus launch. In its strategic outlook statement the company said it maintained AGM guidance of FY18 underlying Group EBIT between $220-240m and that it will deliver stronger ratings performance in CY2018 through new schedule. All in all, there is strong momentum in the TV market and most analysts are expecting this to grow in the 2H. On the chart, the stock has broken out on the upside of its uptrend formation.

Lend Lease beats estimates

Lendlease (LLC) has delivered a 7.8% rise in profit to $425.7m which was a lot higher than an expected $365m. Revenue rose 9.4% to $8.69bn from $7.95bn. It was a strong performance driven by the group's development segment supported by the residential sector. The only laggard was the company’s construction segment which underperformed. Interim distribution 34c. LLC also announced a share buyback up to $500m. Here are the dot points:

Profit after Tax of $425.6m, up 8 %and earnings per stapled security of 72.9c up 8% Return on Equity of 13.8 %upper end of 10-14 %target range

Net operating and investing cash flow of $825.2m Strong balance sheet with gearing of 1.9 per cent3 and available liquidity of $3.9 billion On-market buyback up to $500m Strong residential completions in apartments and land lots Secured two major urbanisation projects in Europe (estimated end value of $5.4 billion) Introduced capital partner for 25 %of the Retirement Living business at premium to book value Two new asset classes added to the funds management platform Interim distribution of 34 cents per stapled security, up 3%

Unconventional View: Shares in LLC are up 6% on the open. The result was a beat on expectations with an increase in its dividend. All very positive stuff. CEO and MD Steve McCann, said Lendlease delivered resilient earnings for the period with a strong performance from the Development and Investments segments outweighing the underperformance in the Construction segment. LLC has also made substantial progress in implementing its strategic agenda which includes securing two major urbanisation projects, converting opportunities in infrastructure space and creating future growth for the funds platform. Lendlease has an extensive development pipeline of $56.7bn with $40.3bn of urbanisation projects and $16.3bn of Communities and Retirement projects. On the chart, LLC looks to have broken out on the upside of its short term downtrend. This

Santos misses consensus forecasts, shares down

Santos (STO) – Shares are slightly down after the oil and gas producer posted its interim result. It missed expectations. Underlying profit rose more than five-fold to US$336m but it was lower than a consensus forecast of US$349m. Overall it was a loss of US$360m which was a big reduction from US$1.047bn in 2016. The loss included an impairment charges of US$689m against Gladstone LNG, US$149m against Ande Ande Lumut and US$14m against another asset. Sales rose 21% to US$3.17bn. Despite the miss, the result was a positive result and vast improvement from previous results. It showed a definite turnaround and that the business was tracking along well. Free cash flow was up and net debt was lower. The board decided to pay down debt instead of declare a dividend. Here are the results:

Unconventional View: Despite shares being down 2.41% at the time of writing due to the profit miss, we think the overall result was a positive one if we look at the bigger picture. The company held off from paying a dividend and elected to pay down debt. We think this was the right thing to do, even though it may not have impressed shareholders. This was Santos can hit its debt-cutting target well ahead of schedule. That alone, will be a big positive and be welcomed by the market. It also means the company was able to record stronger sales volumes and improved prices. Net debt was cut by another 22% to US$2.73bn following a 26% reduction in debt in 2016. Its target is to hit US$2bn in debt by the end of 2019. Which we think it will do. Overall it was a strong performance, Santos is also looking to reach 2018 production of between 55m to 60mboe even though its output fell 3.4% to 59.5m last year. We might even see Santos declaring a dividend if market conditions are better than expected. There is also the chance that we could see another takeover offer for STO from Harbour Energy. On the chart, Santos is still trending up in the short term and has kept to its support line. It’s a positive indicator.

BHP shares under pressure after the miner missed expectations

BHP shares have fallen close to 5% after it released, what analysts are saying, is a miss on consensus forecasts. Underlying NPAT came in at US$4.10bn up 25% but below a consensus forecast of US$4.30bn. A miss. Here are a few dot points:

Attributable profit of US$2.0bn. Underlying attributable profit of US$4.1bn. Underlying EBITDA of US$11.2bn Free cash flow of US$4.9bn. Negative productivity of US$0.5bn on track for US$2.0bn in gains by end-FY19 Interim dividend US55c up 38%. Net debt fell by US$1bn to US$15.4bn.

BHP also said it will introduce the dividend reinvestment plan option for shareholders.

Unconventional View: Whilst the result was a miss on expectations, overall is was a relatively solid result. There were no real surprises. The numbers were fairly robust and its dividend was a beat on expectations. BHP is on track to reach its debt range of US$10 to US$15 billion before year-end whilst maintaining a strong balance sheet through the commodity price cycle. The free cash flow was impressive. Overall we think BHP is cheap whilst mining and energy activity is picking up. Sure the bottom line numbers were a slight miss, but the sell-off was a little overdone. Analysts are saying the numbers were a miss due to poor numbers at the Broadmeadow and Blackwater coal mines. The result is a good one that included improving financials, reduced debt, good cost control and ongoing capital discipline. Should the iron ore price rally from here on in, it will provide upside surprise to the BHP share price. On the chart – despite today’s fall, BHP is still in a solid uptrend.

A2 Milk delivers a bumper profit & links up with Fonterra

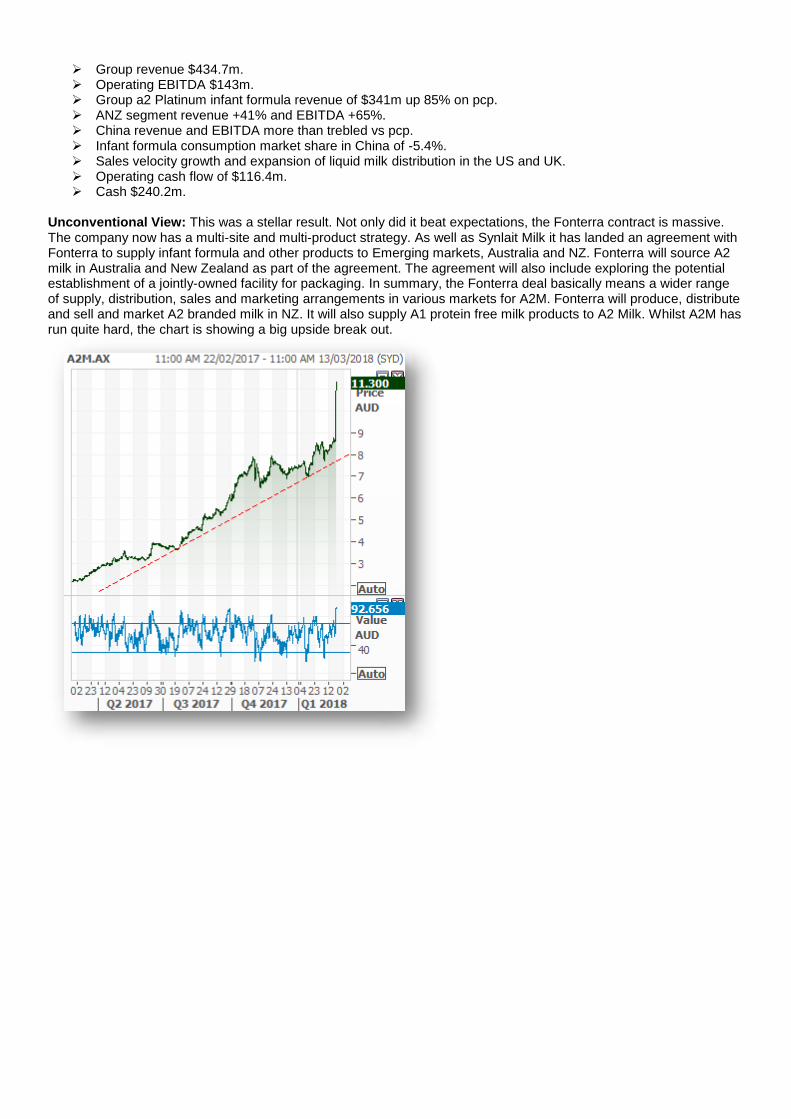

A2 Milk (A2M) – Shares are on a tear today, rising some 30% on a bumper result. We’ve avid supporters of A2M for the past few years, so it’s pleasing to see the company deliver time and time again. Its NPAT came in at $92m which was a beat on an expected $88m. But more importantly, New Zealand dairy giant Fonterra announced a partnership with A2 in a ground breaking deal that will see A2 become more widely available. Fontera will source A2 Milk from Australia and NZ. It provides Fonterrawith access to A2M’s brand strength milk. In return A2M can grow its milk supply through Fonterra’s milk pools using its manufacturing facilities, sales and distribution networks. It’s a win win. The Australian Fonterra will set up an A2 milk pool to service its nutritional product range which is produced from its Darnum factory in Gippsland. Dairy farmers in Australia will now need to supply the special A2 milk sourced from cows that produce only A2 beta casein proteins. Here are the dot points:

Group revenue $434.7m. Operating EBITDA $143m. Group a2 Platinum infant formula revenue of $341m up 85% on pcp. ANZ segment revenue +41% and EBITDA +65%. China revenue and EBITDA more than trebled vs pcp. Infant formula consumption market share in China of -5.4%. Sales velocity growth and expansion of liquid milk distribution in the US and UK. Operating cash flow of $116.4m. Cash $240.2m.

Unconventional View: This was a stellar result. Not only did it beat expectations, the Fonterra contract is massive. The company now has a multi-site and multi-product strategy. As well as Synlait Milk it has landed an agreement with Fonterra to supply infant formula and other products to Emerging markets, Australia and NZ. Fonterra will source A2 milk in Australia and New Zealand as part of the agreement. The agreement will also include exploring the potential establishment of a jointly-owned facility for packaging. In summary, the Fonterra deal basically means a wider range of supply, distribution, sales and marketing arrangements in various markets for A2M. Fonterra will produce, distribute and sell and market A2 branded milk in NZ. It will also supply A1 protein free milk products to A2 Milk. Whilst A2M has run quite hard, the chart is showing a big upside break out.

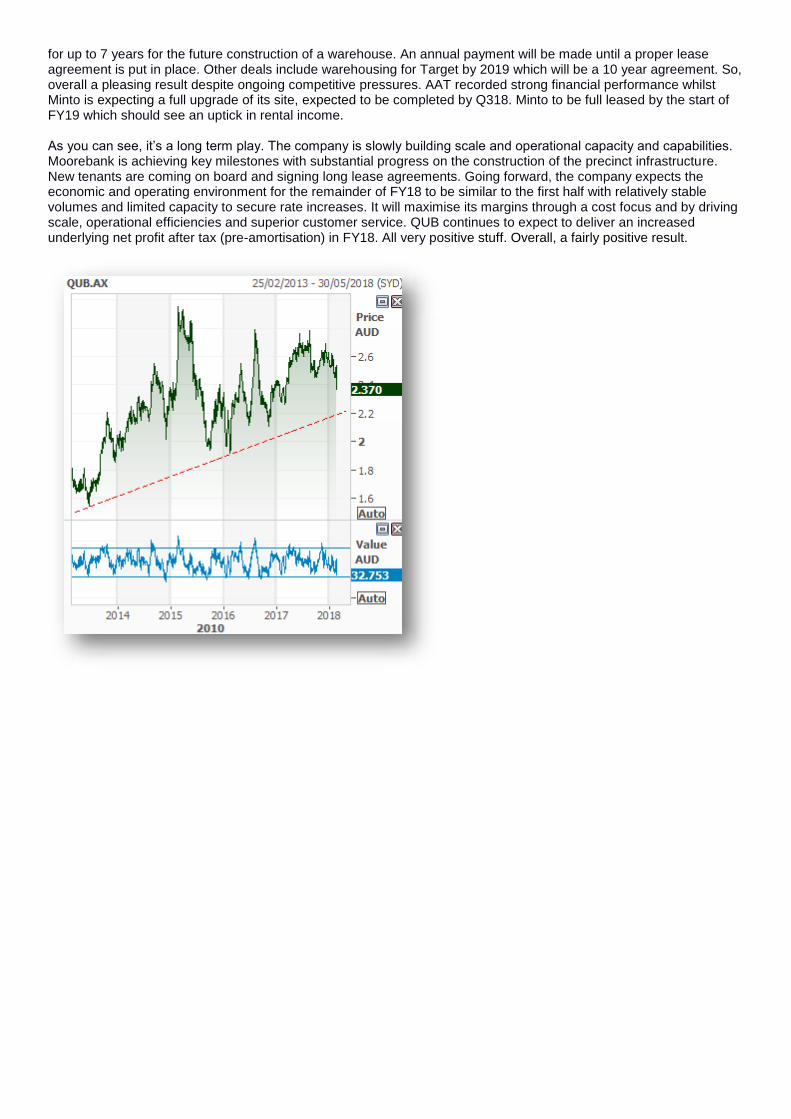

QUBE shares down on earnings miss but lands a second tenant

Qube (QUB) shares are down on the open by about 3%, mainly owing to its earnings miss. The company delivered an underlying NPAT of $61.6m which was below a consensus forecast of $63m. Here are the dot points:

Underlying NPAT of $53.7m ($61.6m NPATA). Statutory NPAT of $45.2m ($53.1m NPATA). Generated strong operating cashflow of $123.9m. Finalised major tenant agreements for Moorebank in the period. Interim dividend maintained at 2.7c fully franked.

Volumes were good across most areas of Qube’s operations including container volumes, vehicle imports, forestry products, bulk commodities and there was also some improvement in oil and gas related activities. Grain volumes were the only area of weakness due to adverse weather conditions. Unconventional View: Qube shares are down on the open, mainly from its earnings miss. It was a little disappointing, but it’s nothing to be to be overly concerned about. The core of the result were solid. It achieved growth in almost all divisions and its earnings were of high quality. The decline in earnings reflects the benefit of a $22.2m contribution from Qube’s Asciano shareholding that was realised in the prior corresponding period. Earnings were also hurt by a $6m impairment in its stake in Prixcar and the dilutionary impact of the $350m capital raising. Reading further into the results uncovered some highlights that the market may have missed. QUB has landed an agreement with its second prospective tenant for its Moorebank hub. The tenant has reserved 150,000 metres of land

for up to 7 years for the future construction of a warehouse. An annual payment will be made until a proper lease agreement is put in place. Other deals include warehousing for Target by 2019 which will be a 10 year agreement. So, overall a pleasing result despite ongoing competitive pressures. AAT recorded strong financial performance whilst Minto is expecting a full upgrade of its site, expected to be completed by Q318. Minto to be full leased by the start of FY19 which should see an uptick in rental income. As you can see, it’s a long term play. The company is slowly building scale and operational capacity and capabilities. Moorebank is achieving key milestones with substantial progress on the construction of the precinct infrastructure. New tenants are coming on board and signing long lease agreements. Going forward, the company expects the economic and operating environment for the remainder of FY18 to be similar to the first half with relatively stable volumes and limited capacity to secure rate increases. It will maximise its margins through a cost focus and by driving scale, operational efficiencies and superior customer service. QUB continues to expect to deliver an increased underlying net profit after tax (pre-amortisation) in FY18. All very positive stuff. Overall, a fairly positive result.

Investing in Robotics – Nanuk Asset Management

By Nanuk Asset Management

Visions of the future often depict a world full of robots – robots that help us around the house, that drive us autonomously and that run entire production lines. For some time now those visions have been coming to life, certainly in factories around the world where automation has revolutionised the production line in an environment that rewards greater efficiency and productivity. While robotics has been a familiar investment theme, there have been many advances in the technologies and applications which have complemented the secular growth and indeed the investment theme associated with robotics.It’s helpful to begin with some context. We think of robots as machines which are programmed to perform a complex series of actions. They can vary dramatically in size and application, they typically operate in an autonomous manner with limited human guidance and they are typically housed in cages for safety reasons. In the current decade we have seen the rise of the collaborative robot, or “cobot”, which is designed to perform specific tasks in physical interaction with humans in a shared workspace. They are typically smaller in size, having built-in sensors which enable them to safely work alongside humans and receive human instruction.

So where does robotics fit in investment-wise?

The Nanuk New World Fund is wholly invested in companies and industries associated with and contributing towards greater environmental sustainability and resource efficiency. The Fund invests globally in companies involved in clean energy, energy efficiency, agriculture, water, waste management, recycling, pollution control and advanced manufacturing and materials. Robotics and automation improve resource efficiency, and fall within the broader theme of Industrial Efficiency. Robotics is a broad space with many interesting areas of development. We have chosen to focus on three core themes. The first is strong structural growth – always a prospective source of investment opportunities. The second is the development of applications beyond the traditional (‘caged’) industrial setting, such as ‘cobots’ – collaborative robots.

The third is the transition of these industrial technologies to consumer products and applications.

Robots are becoming increasingly more common, simply because robotics technology itself is improving rapidly. Key to this growth is the development of artificial intelligence and machine vision, which is allowing machines to navigate independently and adapt to non-standard and changing environments. This moves robots from being limited to a production line and a repeatable action – for instance, attaching a bottle cap – to move around a warehouse for example. In addition to improved use, the cost of components of a robot are rapidly declining. Robotics, like many digital technologies involving software, has benefitted tremendously from Moore’s Law (“the number of transistors on an integrated circuit doubles approximately every two years”). This has led to a massive drop in the cost of computing power and related core components: since 2010 the average robotics sensor cost has dropped by 50%. For context, the cost of lithium-ion batteries has fallen 75% over the same period.

In its Q3 2016 report, the International Federation of Robotics forecast that the number of industrial robots deployed globally will rise to 2.6 million units by 2019, meaning that more than one million units will be added from 2016 to

2019. The sale of traditional industrial robot machines (in units) has grown multiple times in the last decade, with emerging applications such as cobots growing at double digit figures. Teradyne, a company whose primary business is making automatic semiconductor test equipment has seen revenue from its cobot business (it acquired Universal Robotics in 2015) grow 6.5 times over the last four years. This growth has been driven by the improving cost competiveness of cobots vs wage growth in historic manufacturing hubs, particularly China. As cobots become cheaper, they’re gaining market share and this enables a virtuous cycle of increased economies of scale. A great example of a robotics application beyond production lines is in the area of logistics, where deployment has been critical to the rise of ecommerce, allowing denser, more efficient warehousing and expedited order fulfilment. Amazon, for instance now only requires one minute of employee time per order it ships. Amazon and Dematic have bought logistics robot companies over the last few years. Extending the concept further is Ocado, the online supermarket that runs giant automated warehouses that can each support A$2 billion in sales. Ocado’s most advanced and large warehouse operation contains a 3-dimensional grid around which 1000 robots, all controlled by a sophisticated algorithm, select and place items into customers’ shopping baskets. As warehouses become more automated, the idea of a ‘dark warehouse’, where there is no need for lighting because the only workers are robots, comes to mind.

Medical robotics is another key application seeing tremendous growth.

Intuitive Surgical is a US company that pioneered medical robotics in 1995 for minimally invasive surgery. Its main product, the “da Vinci” Surgical System, has been utilised in a variety of surgeries including urology and gynaecology for over three million patients already. The product has been amazingly successful in improving patient outcomes and its market share in its core applications is up to 90%. Although the industry is still quite nascent, new players are joining the medical robotics market such as the joint venture Verb Surgical, a collaboration between Google and Johnson & Johnson. In the consumer market, robotics is becoming more and more common. IRobot’s Roomba robotic vacuum cleaner was once seen as a gimmick for the “tech-obsessed”, but you can now find one in 11 million US households. The robotic vacuum market is growing by 18% p.a., while traditional vacuums are growing at just 5%. Vacuum is far from the only household task amenable to automation: robotic lawnmowers are already available and development on further applications is well underway.

We’re seeing robots move from industrial applications to consumer applications in our homes. We’re seeing strong trend growth at a global level for both these end markets. We’re seeing greater sophistication and application of technologies. And we’re seeing sharp declines in the cost of making robots, leading to rising affordability and a prospective virtuous cycle of increasing demand. In short, they’re cheaper, faster, safer, smarter, more applicable and nimble day by day. This is attractive to us as fundamental investors. Adding to the secular growth story, there is a wide range of companies in which we can invest, some clearly of better quality and value than others. And that’s the investment challenge, to be in the right company in the right area at the right time, to benefit from the robotics thematic as it plays its part in the global transition towards a “new world” of more environmentally sustainable and resource efficient activities in the decades to come.

Nanuk’s investment expertise is focused on industries related to the secular theme of environmental sustainability: a large and increasingly attractive investment universe often overlooked by traditional fund managers. The Fund invests globally in companies involved in clean energy, energy efficiency, agriculture, water, waste management, recycling, pollution control and advanced manufacturing and materials. All of these industries are undergoing significant changes as the world tries to reconcile economic growth with longer term sustainability and are a potentially rich and ongoing source of investment returns.

A buy and a sell from reporting season With the bulk of companies having reported we are at the tail end of reporting season. For that reason we thought it would only be fitting to find two stocks that have reported well or have reported not so well. In this article we find one stock that investors should be buying after a positive earnings result and we find one stock investors should sell after a negative result.

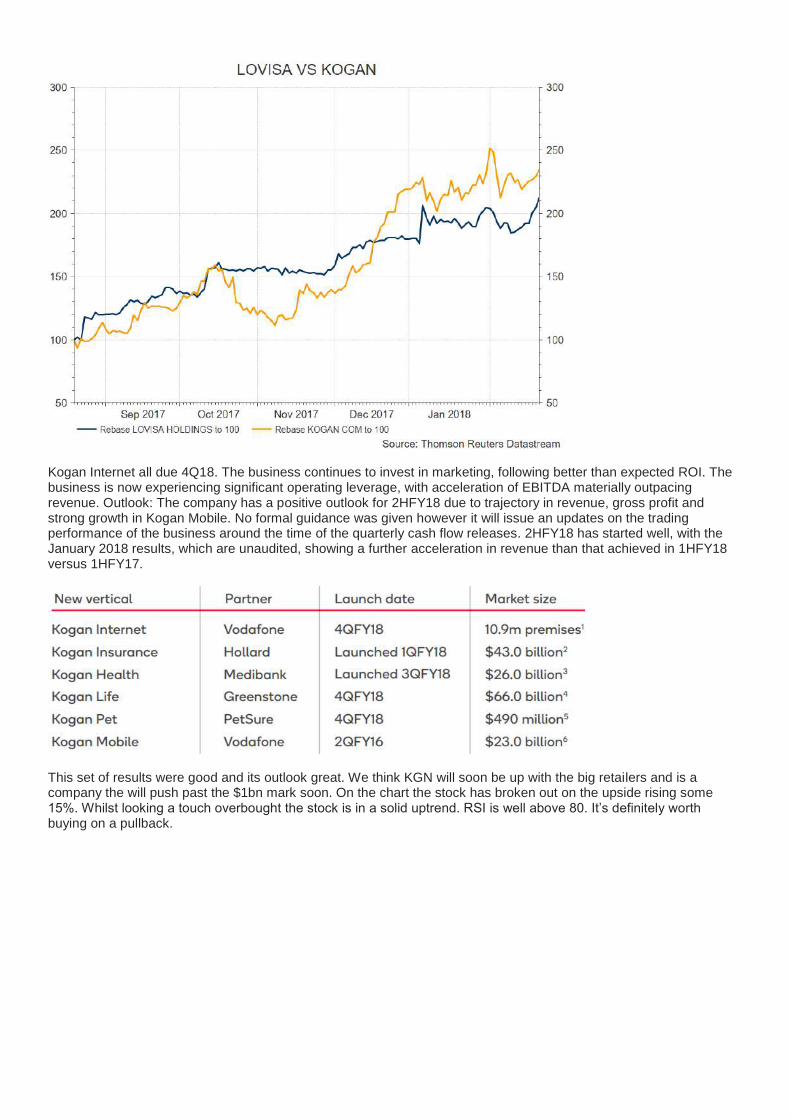

Kogan (KGN) – Ruslan Kogan does it again. Another blistering result that has the stock up 10%. We’ve been avid supporters of Kogan for some time and wrote about the stock back in January last year when it was $1.65. It’s now $8.14. That’s a 393% share price increase. Not bad at all. Back then we said “We like the Kogan business. KGN has $26.5m in the kitty and it’s hitting its prospectus profit forecasts with ease. The chart says Buy. The stock has recently broken out on the upside and has reversal in trend. Traders should looking to buy on this bullish break out.” Here are a few of the dot points:

Trading EBITDA in the first half of FY18 outperformed full year FY17 Pro Forma EBITDA. Revenue of $209.6m, up 45.7% on prior year (1HFY17: $143.9m). 1HFY18 Trading1 EBITDA of $14.1m, up 93.2% on prior year (1HFY17 Pro Forma: $7.3m), reflecting revenue

growth and margin expansion. Trading1 NPAT of $8.1m, up 118.9% on prior year (1HFY17 Pro Forma: $3.7m) and outperformed full year

FY17 Pro Forma NPAT of $7.2m. Statutory NPAT of $8.3m (1HFY17: $1.5m) and outperformed full year FY17 Statutory NPAT of $3.7m. Growth in active customer base to 1,166,000, up 40.5% from 31 December 2016, driven by growth in the

Kogan Brand, New Verticals and strategic marketing initiatives. Gross margin expansion to 19.4% (1HFY17: 18.0%) as a result of rapid growth in New Verticals and

acceleration of the Partner Brands Product Division. Strong balance sheet with net cash of $28.2m, operating cash flow before capital expenditure of $4.6m and

operating cash conversion of 32.6%. Fully franked interim dividend up 76.9% YoY to 6.90c.

So the question is, is Kogan still a buy? Heading into reporting season we had hopes that KGN would beat expectations on the upside. We were proven right this morning after the company beat forecasts. With a market value of close to $800m, the stock is now double the size of Myer (MYR) and closing in on Super Retail Group (SUL). KGN delivered a bumper profit. Underlying NPAT came in at $8.1m up 118.9% and beat a consensus forecast of $6.7m. It’s profit more than doubled after the online retailer added new products and services and attracted new customers. Sales were up 46% to $209.6m also ahead of an expected $206m. It achieved strong growth after the number of online customers rose 40.5% to 1.16 million. It comes at a time when almost every retailer is feeling the Amazon effect. Myer (MYR), Harvey Norman (HVN) and Coles are all facing negative headwinds. KGN has a growing brand and recently launched Kogan Health in February this year. It also plans to launch Kogan Life, Kogan Pet and

Kogan Internet all due 4Q18. The business continues to invest in marketing, following better than expected ROI. The business is now experiencing significant operating leverage, with acceleration of EBITDA materially outpacing revenue. Outlook: The company has a positive outlook for 2HFY18 due to trajectory in revenue, gross profit and strong growth in Kogan Mobile. No formal guidance was given however it will issue an updates on the trading performance of the business around the time of the quarterly cash flow releases. 2HFY18 has started well, with the January 2018 results, which are unaudited, showing a further acceleration in revenue than that achieved in 1HFY18 versus 1HFY17.

This set of results were good and its outlook great. We think KGN will soon be up with the big retailers and is a company the will push past the $1bn mark soon. On the chart the stock has broken out on the upside rising some 15%. Whilst looking a touch overbought the stock is in a solid uptrend. RSI is well above 80. It’s definitely worth buying on a pullback.

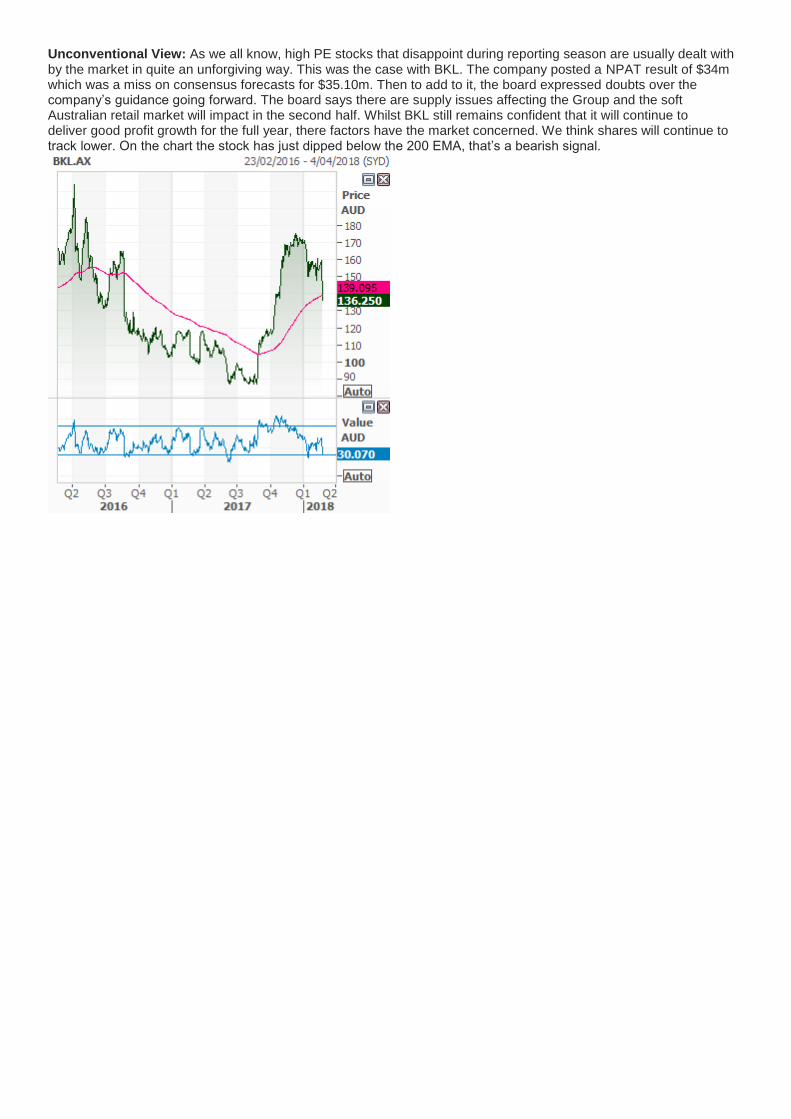

Blackmores (BKL) – We got this one wrong. We were hoping Blackmores would post a stellar result such as its profit of $100m in 2015/16 that came on the back of booming Chinese demand, but things didn’t pan out that way. Instead the company is struggling with supply problems and can’t get its hands on whey protein and fish oil. To make matters worse the Australian retail market has been weak and the Chinese market has become more competitive due to a number of rivals that have entered the space. It’s an oversaturated segment that is now fiercely competitive. Here are a few dot points from the results:

Group net sales of $287m, up 9% compared to previous corresponding period Sales result driven by strong performances from China, BioCeuticals and across Blackmores’ other established Asia markets Net profit after tax of $34m, up 20% compared to previous corresponding period First half dividend of 150 cents per share fully franked, up 15% compared to previous corresponding period Dividend 150c full franked. Blackmores China sales grew by 27% to $74m with record sales from online promotional events including

Singles Day and 12/12. Launched small range of registered products in Vietnam. Gross debt of $100m up $21m compared to June 2017.

Unconventional View: As we all know, high PE stocks that disappoint during reporting season are usually dealt with by the market in quite an unforgiving way. This was the case with BKL. The company posted a NPAT result of $34m which was a miss on consensus forecasts for $35.10m. Then to add to it, the board expressed doubts over the company’s guidance going forward. The board says there are supply issues affecting the Group and the soft Australian retail market will impact in the second half. Whilst BKL still remains confident that it will continue to deliver good profit growth for the full year, there factors have the market concerned. We think shares will continue to track lower. On the chart the stock has just dipped below the 200 EMA, that’s a bearish signal.

New tool for the tool bag!

Retirees have just been given a new tool for their strategy tool bag. The downsizer superannuation contribution (DSC) legislation was passed just before Christmas. The DSC is exactly as the name suggests, the ability for retirees to contribute proceeds to superannuation from selling their home and buying a smaller/cheaper1 one (Downsizing). The new rules allow a fourth way to contribute to superannuation (the other three are concessional, non-concessional and small business) will come into a affect from the 1st of July 2018. The good news is the eligibility for making a DSC is not means tested, nor aged tested. So as long as you are over 65 and have owned your home for more than 10 years you are able to make a contribution of $300,000 each or $600,000 in total. The one-off contribution will not be affected by a person's transfer balance cap, so if you have more than $1.6m you still be eligible for the contribution. It opens up lot of news strategies as previously anyone post 75 was severely disadvantaged as they couldn’t contribute to the most tax effectively entity structure in Australia. Let’s work through a practical example; An Example George and Ruth are both aged 78 and decide to sell their $1.2million home for a townhouse next to the daughters place, worth $600,000. They each already have a pension balance of $1.6m. Meeting the eligibility (see below re the exact eligibility that needs to be met) allows them to make a downsizer contribution of $300,000 each, a total of $600,000. It is irrelevant that George and Ruth don’t satisfy the age and work test for superannuation contributions (these tests don’t apply to DSC’s). It is also irrelevant that they have a superannuation balances in excess if $1.6m (normally superannuation rules stop any contributions to super if you are over $1.6million) even though they are 3 year older than the previous aged cap (75). So George and Ruth are able to sell their home, buy a town house next to their daughter and contribute the remainder (up to $600,000) to superannuation. The Fine Print There is some finer print to the legislation, but essentially it is governed by the following seven conditions:

1. They must be 65 or older at the time the contribution is made. 2. The contribution must be in respect of the proceeds of the sale of a qualifying dwelling in Australia. 3. A 10-year ownership condition must be met.

1 Note, the legislation doesn’t actually say you have to buy a new home, so the name is a little miss leading.

4. Any gain or loss on the disposal of the dwelling must have qualified (or would have qualified) for the main residence CGT exemption in whole or part;

5. The contribution must be made within 90 days of the disposal of the dwelling, or such longer time as the commissioner allows.

6. The person must choose to treat the contribution as a downsizer contribution, and notify their superannuation provider, in the approved form, of this choice at the time the contribution is made.

7. The person cannot have had DSCs in relation to an earlier disposal of a main residence. For a property to be classed as a qualified dwelling in Australia, it must have been a fixed structure. Proceeds from the sale of houseboats, caravans, and other forms of mobile homes, even if they were a main residence, do not qualify for a DSC. The 10-year ownership condition is flexible and covers situations where:

One member of a couple may not have been shown on the title of the property sold A property was used for both business and principle place of residence A person has owned a property for less than 10 years as a result of having had a former residence

compulsorily acquired. A very powerful tool that can be used for Good or Evil A word of caution: even though this is a wonderful change in superannuation legislation, it is very powerful tool, especially when you consider your eligibility for the Aged Pension. The problem is simple one, your home value, what-ever it is, is exempt from assessment for the Aged Pension, however superannuation is not. So the amount that you contribute to superannuation will be assessed in the assets test and income test, and could change your eligibility substantially. So as per usual seek some great advice before pulling this one out of your strategy tool bag.

Ferrari Portfolio – We’re selling two stocks and buying two

For our newbie members, just to recap: We introduced the Ferrari Portfolio 9 December 2016. The portfolio was a challenge to turn $100k into enough to buy a Ferrari 246 GT Dino. This classic is around the $400k mark. We set quite a mammoth target and whilst we didn’t quite get there, we did managed to score quite a respectable return of 83.5%. We started off with $100k and we turned that into $183k. Bravo. A quick search on Carsales brought up the Ferrari F430 which retails second hand for around the $180k-$200k mark. Not quite the Dino. That’s ok. For 2018, we’ve decided to change things a bit. Many of the new subscribers that have joined recently we unable to buy shares that and replicate the Ferrari portfolio because many had already run. So what we’re going to do, is reset the portfolio to $100k but still work with the same portfolio.

Here is the portfolio as of the 23 February 2018

Here is our weekly commentary on each stock –

Blackmores (BKL) – SELLING – We are selling Blackmores after a disappointing profit result. The chart isn’t looking good and the stock has breached its stop loss.

Boral (BLD) – Hold A2 Milk (A2M) – SELLING – Taking profits. The stock could rally a lot higher. We’re merely locking in

profits and getting out. No other reason. Costa Group (CGC) – Hold Origin Energy (ORG) – Hold Aristocrat Leisure (ALL) – Hold

Code Description Bought Price Paid Price NowTotal

ReturnStop Loss Holdings Value

BKL Blackmores Ltd 08-Jan-18 $154.33 $136.30 -11.7% $147.90 65 $8,859.50

BLD Boral Ltd 08-Jan-18 $7.68 $7.79 +1.4% $6.63 1300 $10,127.00

A2M a2 Milk Company Ltd 08-Jan-18 $7.01 $11.71 +67.0% $7.19 1425 $16,686.75

CGC Costa Group Holdings Ltd 08-Jan-18 $6.24 $6.10 -2.2% $5.33 1600 $9,760.00

ORG Origin Energy Ltd 08-Jan-18 $9.61 $9.13 -5.0% $7.71 1045 $9,540.85

ALL Aristocrat Leisure Ltd 08-Jan-18 $22.60 $24.41 +8.0% $20.12 445 $10,860.23

LVT Livetiles Ltd 24-Jan-18 $0.52 $0.45 -13.5% $0.48 37100 $16,695.00

EHL Emeco Holdings Ltd 24-Jan-18 $0.28 $0.28 +0.0% $0.24 32855 $9,035.13

LOV Lovisa Holdings Ltd 16-Feb-18 $7.30 $7.30 +0.0% $6.21 1285 $9,380.50

CASH - - - - - -

+0.9% Total $100,944.95

Return 83.5% (2016-2017) Return since inception 9 Dec 2016 Profit / Loss $944.9

Ferrari Portfolio

Totals

LiveTiles – Holding. Despite the stock dropping below its stop loss, we are holding on. The reason was the capital raising.

Emeco Holdings (EHL) – Hold Lovisa - Hold

The sale of BKL and A2M gives a cash balance of $36,061.95.

What we are buying – 2 new stocks that will benefit from earnings surprise next week:

Synlait Milk (SM1) - Is an innovative dairy processing company based in the heart of Canterbury, New Zealand. The company supplies milk to A2 Milk.

Sino Gas & Energy (SEH) -Is an Australian energy company focusing on developing Chinese unconventional gas assets. SEH holds a portfolio of unconventional gas assets in China through Production Sharing Contract (PSCs).

Here is the portfolio up to date:

Subscribers of UWJ – If you have any stock ideas and think they might be suitable for the Ferrari portfolio please email us as with your then at [email protected].

Code Description Bought Price Paid Price NowTotal

ReturnStop Loss Holdings Value

SM1 Synlait Milk Ltd 23-Feb-18 $6.35 $6.35 +0.0% $5.40 2761 $17,530.00

SEH Sino Gas & Energy 23-Feb-18 $0.18 $0.18 +0.0% $0.15 100171 $17,530.00

Code Description Bought Price Paid Price NowTotal

ReturnStop Loss Holdings Value

BLD Boral Ltd 08-Jan-18 $7.68 $7.79 +1.4% $6.63 1300 $10,127.00

CGC Costa Group Holdings Ltd 08-Jan-18 $6.24 $6.17 -1.1% $5.33 1600 $9,872.00

ORG Origin Energy Ltd 08-Jan-18 $9.61 $9.17 -4.6% $7.71 1045 $9,582.65

ALL Aristocrat Leisure Ltd 08-Jan-18 $22.60 $24.49 +8.3% $20.12 445 $10,895.83

LVT Livetiles Ltd 24-Jan-18 $0.52 $0.45 -13.5% $0.48 37100 $16,695.00

EHL Emeco Holdings Ltd 24-Jan-18 $0.28 $0.28 +1.8% $0.24 32855 $9,199.40

LOV Lovisa Holdings Ltd 16-Feb-18 $7.30 $8.42 +15.3% $6.21 1285 $10,819.70

SM1 Synlait Milk Ltd 23-Feb-18 $6.41 $6.36 -0.8% $0.00 2020 $12,847.20

SEH Sino Gas & Energy Holdings Ltd 23-Feb-18 $0.18 $0.18 +0.0% $0.00 73314 $13,196.52

CASH - - - - - -

+3.2% Total $103,235.30

Return 83.5% (2016-2017) Return since inception 9 Dec 2016 Profit / Loss $3,235.3

Ferrari Portfolio

Totals

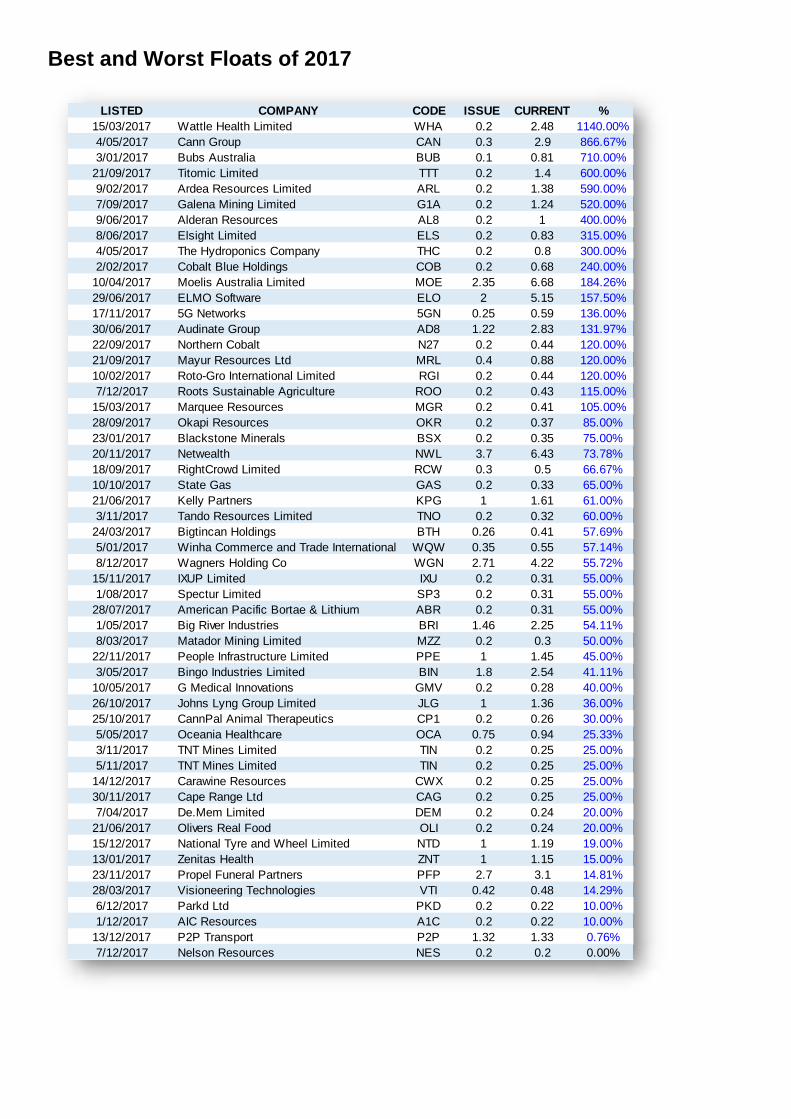

Best and Worst Floats of 2017

LISTED COMPANY CODE ISSUE CURRENT %

15/03/2017 Wattle Health Limited WHA 0.2 2.48 1140.00%

4/05/2017 Cann Group CAN 0.3 2.9 866.67%

3/01/2017 Bubs Australia BUB 0.1 0.81 710.00%

21/09/2017 Titomic Limited TTT 0.2 1.4 600.00%

9/02/2017 Ardea Resources Limited ARL 0.2 1.38 590.00%

7/09/2017 Galena Mining Limited G1A 0.2 1.24 520.00%

9/06/2017 Alderan Resources AL8 0.2 1 400.00%

8/06/2017 Elsight Limited ELS 0.2 0.83 315.00%

4/05/2017 The Hydroponics Company THC 0.2 0.8 300.00%

2/02/2017 Cobalt Blue Holdings COB 0.2 0.68 240.00%

10/04/2017 Moelis Australia Limited MOE 2.35 6.68 184.26%

29/06/2017 ELMO Software ELO 2 5.15 157.50%

17/11/2017 5G Networks 5GN 0.25 0.59 136.00%

30/06/2017 Audinate Group AD8 1.22 2.83 131.97%

22/09/2017 Northern Cobalt N27 0.2 0.44 120.00%

21/09/2017 Mayur Resources Ltd MRL 0.4 0.88 120.00%

10/02/2017 Roto-Gro International Limited RGI 0.2 0.44 120.00%

7/12/2017 Roots Sustainable Agriculture ROO 0.2 0.43 115.00%

15/03/2017 Marquee Resources MGR 0.2 0.41 105.00%

28/09/2017 Okapi Resources OKR 0.2 0.37 85.00%

23/01/2017 Blackstone Minerals BSX 0.2 0.35 75.00%

20/11/2017 Netwealth NWL 3.7 6.43 73.78%

18/09/2017 RightCrowd Limited RCW 0.3 0.5 66.67%

10/10/2017 State Gas GAS 0.2 0.33 65.00%

21/06/2017 Kelly Partners KPG 1 1.61 61.00%

3/11/2017 Tando Resources Limited TNO 0.2 0.32 60.00%

24/03/2017 Bigtincan Holdings BTH 0.26 0.41 57.69%

5/01/2017 Winha Commerce and Trade International LtdWQW 0.35 0.55 57.14%

8/12/2017 Wagners Holding Co WGN 2.71 4.22 55.72%

15/11/2017 IXUP Limited IXU 0.2 0.31 55.00%

1/08/2017 Spectur Limited SP3 0.2 0.31 55.00%

28/07/2017 American Pacific Bortae & Lithium ABR 0.2 0.31 55.00%

1/05/2017 Big River Industries BRI 1.46 2.25 54.11%

8/03/2017 Matador Mining Limited MZZ 0.2 0.3 50.00%

22/11/2017 People Infrastructure Limited PPE 1 1.45 45.00%

3/05/2017 Bingo Industries Limited BIN 1.8 2.54 41.11%

10/05/2017 G Medical Innovations GMV 0.2 0.28 40.00%

26/10/2017 Johns Lyng Group Limited JLG 1 1.36 36.00%

25/10/2017 CannPal Animal Therapeutics CP1 0.2 0.26 30.00%

5/05/2017 Oceania Healthcare OCA 0.75 0.94 25.33%

3/11/2017 TNT Mines Limited TIN 0.2 0.25 25.00%

5/11/2017 TNT Mines Limited TIN 0.2 0.25 25.00%

14/12/2017 Carawine Resources CWX 0.2 0.25 25.00%

30/11/2017 Cape Range Ltd CAG 0.2 0.25 25.00%

7/04/2017 De.Mem Limited DEM 0.2 0.24 20.00%

21/06/2017 Olivers Real Food OLI 0.2 0.24 20.00%

15/12/2017 National Tyre and Wheel Limited NTD 1 1.19 19.00%

13/01/2017 Zenitas Health ZNT 1 1.15 15.00%

23/11/2017 Propel Funeral Partners PFP 2.7 3.1 14.81%

28/03/2017 Visioneering Technologies VTI 0.42 0.48 14.29%

6/12/2017 Parkd Ltd PKD 0.2 0.22 10.00%

1/12/2017 AIC Resources A1C 0.2 0.22 10.00%

13/12/2017 P2P Transport P2P 1.32 1.33 0.76%

7/12/2017 Nelson Resources NES 0.2 0.2 0.00%

LISTED COMPANY CODE ISSUE CURRENT %

1/12/2017 Bojun Agriculture Holdings BJH 0.3 0.3 0.00%

28/02/2017 Eildon Capital Limited EDC 1.06 1.04 -1.89%

4/12/2017 New Energy Solar NEW 1.5 1.43 -4.67%

17/01/2017 eSense-Lab Ltd ESE 0.2 0.19 -5.00%

29/11/2017 Bio-Gene Technology BGT 0.2 0.19 -5.00%

23/11/2017 SelfWealth SWF 0.2 0.19 -5.00%

27/07/2017 Convenience Retail CRR 3 2.72 -9.33%

25/08/2017 Scout Security SCT 0.2 0.18 -10.00%

12/04/2017 URB Investments URB 1.1 0.99 -10.00%

16/11/2017 Domain Holdings DHG 3.5 3.1 -11.43%

22/06/2017 Retech Technology RTE 0.5 0.44 -12.00%

16/08/2017 Pyrolyx AG PLX 1.47 1.29 -12.24%

7/12/2017 Rhythm Biosciences RHY 0.2 0.17 -15.00%

24/02/2017 MetalsTech Limited MTC 0.2 0.17 -15.00%

10/10/2017 Riversgold RGL 0.2 0.17 -15.00%

8/12/2017 Credible Labs CRD 1.21 1.02 -15.70%

4/05/2017 MSL Solutions MPW 0.25 0.2 -20.00%

15/11/2017 Lustrum Minerals LRM 0.2 0.16 -20.00%

15/11/2017 Telix Pharmaceuticals TLX 0.65 0.51 -21.54%

3/07/2017 Eagle Health Holdings EHH 0.4 0.31 -22.50%

23/08/2017 Windlab Limited WND 2 1.52 -24.00%

30/03/2017 I Synergy Group IS3 0.2 0.15 -25.00%

2/08/2017 Nusantara Resources NUS 0.42 0.3 -28.57%

17/10/2017 Bryah Resources BYH 0.2 0.14 -30.00%

11/01/2017 Lifespot Health LSH 0.2 0.14 -30.00%

21/04/2017 Tinybeans Group Pty Ltd TNY 1 0.69 -31.00%

14/12/2017 Engage BDR EN1 0.25 0.17 -32.00%

14/11/2017 Ocean Grown Abalone OGA 0.25 0.17 -32.00%

28/02/2017 Tianmei Beverage Group TB8 0.2 0.13 -35.00%

6/04/2017 Todd River Resources TRT 0.2 0.13 -35.00%

31/10/2017 The GO2 People Limited GO2 0.2 0.12 -40.00%

18/10/2017 Nanollose NC6 0.2 0.12 -40.00%

28/03/2017 Lithium Consolidated LI3 0.2 0.12 -40.00%

19/05/2017 Magmatic Resources MAG 0.2 0.11 -45.00%

19/04/2017 E2 Metals E2M 0.2 0.11 -45.00%

6/01/2017 Skin Elements SKN 0.2 0.1 -50.00%

3/08/2017 Sienna Cancer Diagnostics SDX 0.2 0.1 -50.00%

1/11/2017 Registry Direct Limited RD1 0.2 0.1 -50.00%

7/11/2017 Kore Potash KP2 0.2 0.1 -50.00%

29/09/2017 Doriemus Resources DOR 0.26 0.12 -53.85%

4/01/2017 Asset Owl AO1 0.2 0.09 -55.00%

16/01/2017 Kalamazoo Resources KZR 0.2 0.09 -55.00%

2/05/2017 Mobilicom Limited MOB 0.2 0.08 -60.00%

16/01/2017 Freehill Mining FHS 0.2 0.08 -60.00%

20/01/2017 Davenport Resources Ltd DAV 0.2 0.08 -60.00%

12/09/2017 CropLogic CLI 0.2 0.08 -60.00%

7/02/2017 Velocity Property Group Limited VP7 0.2 0.08 -60.00%

9/03/2017 Jiajiafu Modern Agriculture Limited JJF 0.3 0.11 -63.33%

22/06/2017 Imagion Biosystems IBX 0.2 0.06 -70.00%

28/04/2017 UUV Aquabotix UUV 0.2 0.06 -70.00%

12/01/2017 United Networks UNL 0.2 0.06 -70.00%

17/03/2017 Servtech Global Holdings SVT 0.2 0.02 -90.00%

CHARTS OF THE WEEK – 23 February 2018

The below chart comes from Visual Capitalist. It shows the most valuable brands across the globe. Remarkably Telstra was the most valuable brand in Australia and Amazon the most valuable brand in the US. No surprises there.

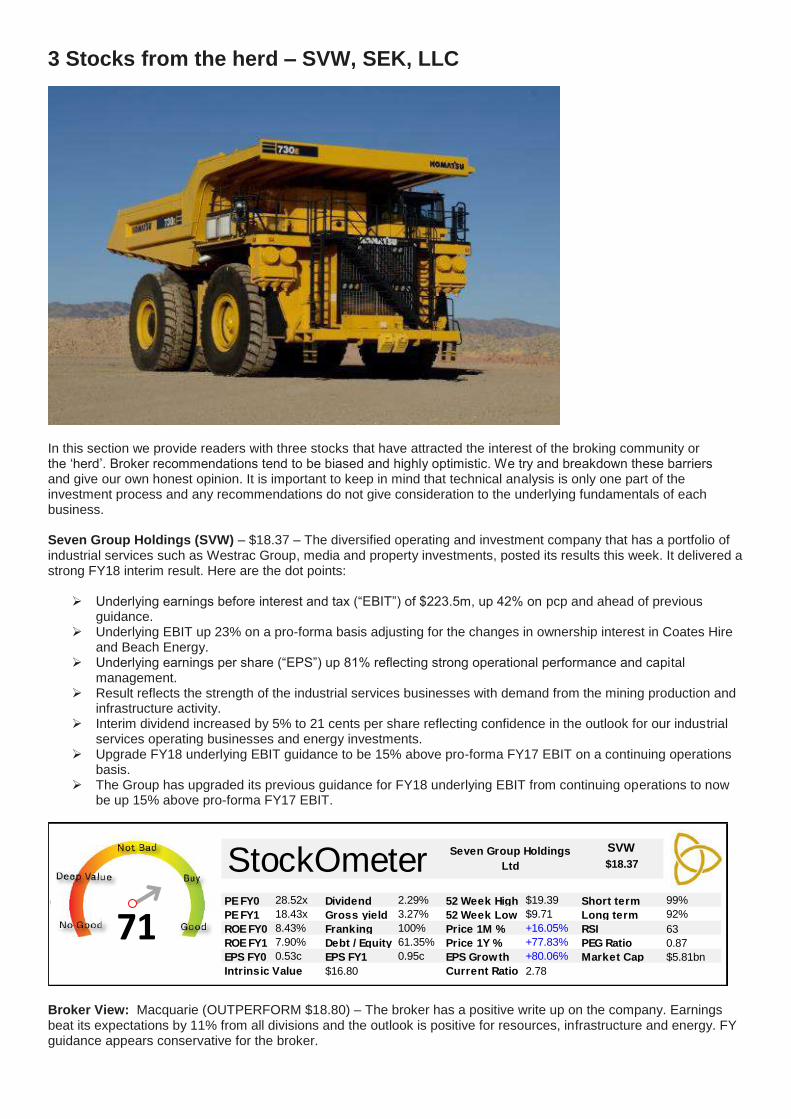

3 Stocks from the herd – SVW, SEK, LLC

In this section we provide readers with three stocks that have attracted the interest of the broking community or the ‘herd’. Broker recommendations tend to be biased and highly optimistic. We try and breakdown these barriers and give our own honest opinion. It is important to keep in mind that technical analysis is only one part of the investment process and any recommendations do not give consideration to the underlying fundamentals of each business. Seven Group Holdings (SVW) – $18.37 – The diversified operating and investment company that has a portfolio of industrial services such as Westrac Group, media and property investments, posted its results this week. It delivered a strong FY18 interim result. Here are the dot points:

Underlying earnings before interest and tax (“EBIT”) of $223.5m, up 42% on pcp and ahead of previous guidance.

Underlying EBIT up 23% on a pro-forma basis adjusting for the changes in ownership interest in Coates Hire and Beach Energy.

Underlying earnings per share (“EPS”) up 81% reflecting strong operational performance and capital management.

Result reflects the strength of the industrial services businesses with demand from the mining production and infrastructure activity.

Interim dividend increased by 5% to 21 cents per share reflecting confidence in the outlook for our industrial services operating businesses and energy investments.

Upgrade FY18 underlying EBIT guidance to be 15% above pro-forma FY17 EBIT on a continuing operations basis.

The Group has upgraded its previous guidance for FY18 underlying EBIT from continuing operations to now be up 15% above pro-forma FY17 EBIT.

Broker View: Macquarie (OUTPERFORM $18.80) – The broker has a positive write up on the company. Earnings beat its expectations by 11% from all divisions and the outlook is positive for resources, infrastructure and energy. FY guidance appears conservative for the broker.

SVW

$18.37

PE FY0 28.52x Dividend 2.29% 52 Week High $19.39 Short term 99%

PE FY1 18.43x Gross yield 3.27% 52 Week Low $9.71 Long term 92%

ROE FY0 8.43% Franking 100% Price 1M % +16.05% RSI 63

ROE FY1 7.90% Debt / Equity 61.35% Price 1Y % +77.83% PEG Ratio 0.87

EPS FY0 0.53c EPS FY1 0.95c EPS Growth +80.06% Market Cap $5.81bn

$16.80 Current Ratio 2.78

StockOmeterSeven Group Holdings

Ltd

Intrinsic Value

71

NO GOOD

NOT BAD

BUY

GOOD

DEEPVALUE

71

Unconventional View: We agree with Macquarie. This was a cracking result. Profit was up by more than 80% on the back of a recovering mining industry which helped boost earnings from its Westrac business which supplies earthmoving equipment parts. Shares were up as much as 17% and hit record highs. NPAT came in at $159.8m and was a beat on Macquarie’s forecasts. CEO Ryan Stokes said “The continued strength of the mining production cycle with greater utilisation of fleets has supported parts growth and component demand at WesTrac.” Last year SVW sold its Chinese mining machinery division WesTrac China to Chinese firm Lei Shing Hong Machinery for A$540m. It distributes Caterpillar earthmoving, mining and construction equipment throughout eastern China and Taiwan. The deal allowed SVW to focus on supplying an infrastructure boom in the east coast Australian states, which the company expects to peak by 2021. In September last year, SVW bought the 53.3% of Coates Hire it did not own. Also in that month, Seven’s oil and gas play, Beach Energy, acquired Lattice Energy. Some saying the Beach’s acquisition of Lattice was transformational and provides exposure to the east coast gas market and diversification across multiple basins. We think SVW’s move to take control of Coates Hire and up its exposure to the east coast gas through Beach are positive drivers for future growth. Sure it has increased its debt position to $2bn, but that’s ok. Its mining equipment and gas business are booming. Media is lagging. Seven Group went one step further and upgraded its 2018 forecast for EBITDA to be 15% above its comparable result last year. We think this is a positive sign of things to come. It was a strong result with a positive outlook. It’s a sign of things to come. On the chart, SVW is in a solid uptrend formation and is making higher highs. Those wanting to buy could wait for a pullback. Other than that, SVW looks attractive.

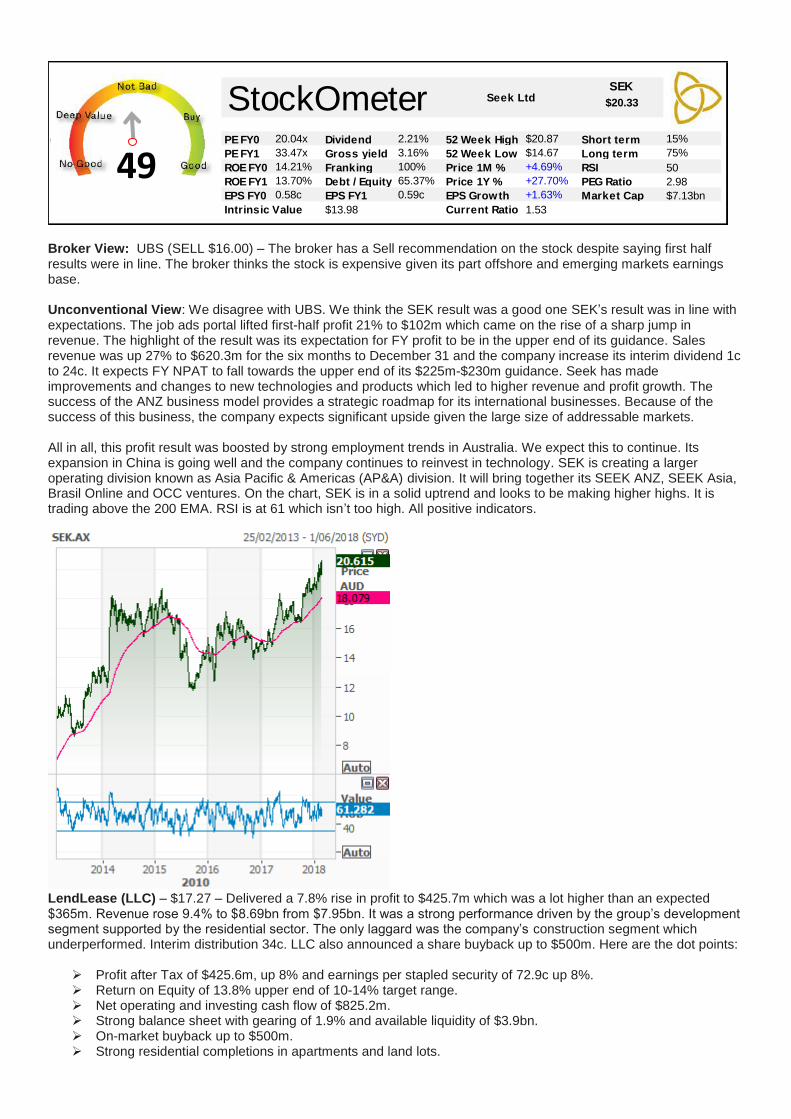

SEEK (SEK) – $20.61 – Is a market leading website for job advertisements. The company runs an online employment classifieds platform providing in 12 countries with three main business divisions: SEEK Employment, SEEK Learning and SEEK International. It entails a strong portfolio of employment, education and volunteer businesses which span across Australia, New Zealand, China, South East Asia, Brazil, Mexico, Africa and Bangladesh. SEK receives over 450 million visits to its sites every month and has over 4 million job opportunities available at any given time and relationships with over 150m candidates. This week SEK delivered its profit result. Here at the dot points:

SEEK Limited (“SEEK”) announced its results for 6 months ended 31 December 2017 Reported Revenue of A$620.3m (pcp: A$487.9m) Reported EBITDA of A$221.2 (pcp: A$170.3m) Underlying NPAT (excl significant items & Early Stage Ventures) of A$114.0m (pcp: A$113.6m) Reported NPAT of A$102.0m (pcp: A$84.1m) SEEK said “It is pleased to deliver strong financial results alongside aggressive reinvestment. In our largest

businesses we are seeing investment translate directly into growth in our operating metrics and financial results.”

Positive guidance provided - Upgraded EBITDA guidance and confirmed NPAT guidance at upper end of previous range. H118 dividend of 24 cents, growth of 4% compared to pcp.

Broker View: UBS (SELL $16.00) – The broker has a Sell recommendation on the stock despite saying first half results were in line. The broker thinks the stock is expensive given its part offshore and emerging markets earnings base. Unconventional View: We disagree with UBS. We think the SEK result was a good one SEK’s result was in line with expectations. The job ads portal lifted first-half profit 21% to $102m which came on the rise of a sharp jump in revenue. The highlight of the result was its expectation for FY profit to be in the upper end of its guidance. Sales revenue was up 27% to $620.3m for the six months to December 31 and the company increase its interim dividend 1c to 24c. It expects FY NPAT to fall towards the upper end of its $225m-$230m guidance. Seek has made improvements and changes to new technologies and products which led to higher revenue and profit growth. The success of the ANZ business model provides a strategic roadmap for its international businesses. Because of the success of this business, the company expects significant upside given the large size of addressable markets. All in all, this profit result was boosted by strong employment trends in Australia. We expect this to continue. Its expansion in China is going well and the company continues to reinvest in technology. SEK is creating a larger operating division known as Asia Pacific & Americas (AP&A) division. It will bring together its SEEK ANZ, SEEK Asia, Brasil Online and OCC ventures. On the chart, SEK is in a solid uptrend and looks to be making higher highs. It is trading above the 200 EMA. RSI is at 61 which isn’t too high. All positive indicators.

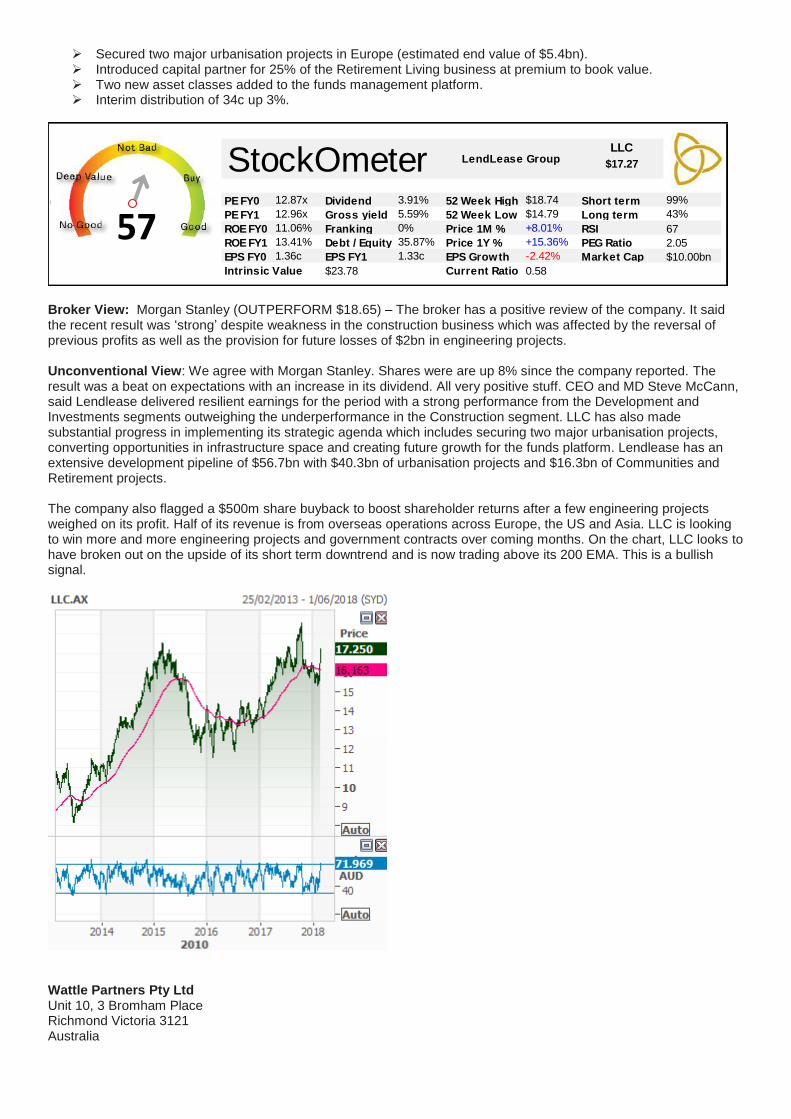

LendLease (LLC) – $17.27 – Delivered a 7.8% rise in profit to $425.7m which was a lot higher than an expected $365m. Revenue rose 9.4% to $8.69bn from $7.95bn. It was a strong performance driven by the group’s development segment supported by the residential sector. The only laggard was the company’s construction segment which underperformed. Interim distribution 34c. LLC also announced a share buyback up to $500m. Here are the dot points:

Profit after Tax of $425.6m, up 8% and earnings per stapled security of 72.9c up 8%. Return on Equity of 13.8% upper end of 10-14% target range. Net operating and investing cash flow of $825.2m. Strong balance sheet with gearing of 1.9% and available liquidity of $3.9bn. On-market buyback up to $500m. Strong residential completions in apartments and land lots.

SEK

$20.33

PE FY0 20.04x Dividend 2.21% 52 Week High $20.87 Short term 15%

PE FY1 33.47x Gross yield 3.16% 52 Week Low $14.67 Long term 75%

ROE FY0 14.21% Franking 100% Price 1M % +4.69% RSI 50

ROE FY1 13.70% Debt / Equity 65.37% Price 1Y % +27.70% PEG Ratio 2.98

EPS FY0 0.58c EPS FY1 0.59c EPS Growth +1.63% Market Cap $7.13bn

$13.98 Current Ratio 1.53

StockOmeter Seek Ltd

Intrinsic Value

49

NO GOOD

NOT BAD

BUY

GOOD

DEEPVALUE

49

Secured two major urbanisation projects in Europe (estimated end value of $5.4bn). Introduced capital partner for 25% of the Retirement Living business at premium to book value. Two new asset classes added to the funds management platform. Interim distribution of 34c up 3%.