1 Kelley School of Business, Indiana University, Bloomington, IN 47405. Email: [email protected] 2 Kelley School of Business, Indiana University, Bloomington, IN 47405. Email: [email protected] * This paper has benefitted from the response of seminar participants at Alabama, Humboldt, Frankfurt, Illinois, Indiana, INSEAD, Norwegian School of Management, Notre Dame, Penn State and Pittsburgh. Costless Versus Costly Signaling: Theory and Evidence from Share Repurchases * by Utpal Bhattacharya 1 and Amy Dittmar 2 JEL Classification: D80, G14, G30 Key Words: Cheap talk, costly signals, share repurchases First version: January 2001 This version: February 2003

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1 Kelley School of Business, Indiana University, Bloomington, IN 47405. Email: [email protected]

2 Kelley School of Business, Indiana University, Bloomington, IN 47405. Email: [email protected]

* This paper has benefitted from the response of seminar participants at Alabama, Humboldt, Frankfurt,Illinois, Indiana, INSEAD, Norwegian School of Management, Notre Dame, Penn State and Pittsburgh.

Costless Versus Costly Signaling:Theory and Evidence

from Share Repurchases*

by

Utpal Bhattacharya1

and

Amy Dittmar2

JEL Classification: D80, G14, G30Key Words: Cheap talk, costly signals, share repurchases

First version: January 2001This version: February 2003

COSTLESS VERSUS COSTLY SIGNALING:

THEORY AND EVIDENCE FROM SHARE REPURCHASES

Abstract

When does a good firm separate itself from a bad firm by “putting its money where its mouth is” and

when does it engage in cheap talk? We develop a simple model in this paper to find out which signaling

mechanism will be used under what circumstances in a capital market. We find, as one would expect, that

the good firm prefers cheap talk over costly signaling, because in the latter method, all of the cost of

separation is being borne by the firm. However, costless signaling can only be used by good firms who are

more undervalued and are more ignored. These restrictions exist because cheap talk will only attract attention

from speculators when scrutiny is likely to uncover more opportunities for trading profits that will cover the

costs of scrutiny. We then test the predictions of the model using a data set of open market share repurchases

that contains firms that employ costless signals (announce share repurchases, but do not repurchase) as well

as firms that employ costly signals (announce share repurchases, and repurchase). The evidence in favor of

the predictions of the model is surprisingly robust.

1

COSTLESS VERSUS COSTLY SIGNALING:

THEORY AND EVIDENCE FROM SHARE REPURCHASES

When does a good firm separate itself from a bad firm by “putting its money where its mouth is” and

when does it engage in cheap talk? Signaling theory predicts that a good firm can separate itself from a bad

firm by giving a costly signal to capital markets; the bad firm will not mimic because the signal is costlier for

the bad firm. A good firm can also separate itself by engaging in cheap talk to attract scrutiny; the bad firm

will not mimic because the bad firm does not gain from being discovered. This paper explores, both

theoretically and empirically, when do good firms use costly signals to separate and when they use costless

signals to separate.

The first contribution of this paper is to develop a simple theoretical model that gives a good firm the

choice between costless and costly signaling in a capital market. This allows us to make precise the

circumstances under which each signaling mechanism will be used. We obtain the following insights from

our theoretical model. The good firm always prefers costless signaling over costly signaling because, in the

latter method, all of the cost of separation is being borne by the firm; whereas, in the former method, all of

the cost of separation is being borne by a speculator who, after his attention has been attracted, finds it

optimal to expend search costs to find out more about the firm. The good firm is, thus, discovered. The bad

firm does not gain from being discovered, and so it does not attract attention. Separation by costless signals,

however, is effective only under very special circumstances in a stock market. This is because the speculator

will only undertake search if he hopes to discover substantial material non-public information about a firm

and then make substantial trading profits to cover the cost of scrutiny. As only good firms, i.e. only

undervalued firms, signal in equilibrium, substantial material non-public information can only be obtained

if the firm is deeply undervalued. Second, the discovery of substantial material non-public information about

a firm is useless if many other speculators discover the same information and compete away all trading

profits. In other words, if the size of informed trading increases, stock prices become more informative, and

so the value of the additional information that can be obtained from costly search diminishes. To summarize,

2

our theoretical model predicts costless signals are effective for more undervalued firms and for more ignored

firms. For other firms, this signaling mechanism will not work, and they have to put their money where their

mouths are – employ costly signals.

The second contribution of our paper is to take the above two testable implications of our theoretical

model to the data. To test our model, we need a signaling mechanism that allows a firm a choice between

a costly and a costless signal. Our data set consists of a sample of firms that have announced open market

share repurchases. This data set offers a unique opportunity to test the predictions of our theoretical model,

because we find that 46% of all firms that announce share repurchase programs do not purchase a single

share within the quarter of or the quarter following the announcement. As a matter of fact, 27% of firms that

announce, do not repurchase within four fiscal years of the announcement or prior to dropping out of

Compustat. Thus, if a repurchase announcement signals value, then these firms simply use the

announcement, which is virtually costless, to attract scrutiny from speculators and have their true value

discovered, whereas the rest of the firms repurchase their shares, which is costly, to signal their true value.

The differences between these two sets of firms should shed some light as to which type of firms use costless

signaling and which type of firms use costly signaling, enabling us to test the predictions of our model.

We test the predictions of our theoretical model using proxies for measuring the two variables of

interest. Our proxy for measuring our first variable of interest, undervaluation, is the amount of positive

information that comes out at the announcement or between the announcement date and the time the firm

reveals if it has used a costly or a costless signal. Since firms do not report stock repurchases until they file

their quarterly statements, the market may not know the type of signal until the close of the next fiscal quarter.

Thus, we assume that the signal corrects the undervaluation within t days after the announcement – where

we take t to be one day, one quarter or two quarters. A classical measure of the amount of undervaluation

is the abnormal returns from the announcement till date t, and this is what we use. Our primary proxy for

measuring our second variable of interest, ignorance, is the number of analyst following. We also use firm

size since the market is typically better informed about large versus small firms.

3

The following are our results from our empirical tests. We find that firms that announce share

repurchases and do not carry them out, have higher cumulative abnormal returns over the announcement

period, have fewer analysts following them, and are smaller than firms which announce share repurchases

and carry them out. These results indicate that firms that are more undervalued and are more ignored are

more likely to use a costless signal. These two pieces of evidence provide strong support for our model.

Our theoretical model liberally borrows insights from two strands of a vast signaling literature. The

first strand, the costly signaling literature, began with Spence (1973). He showed that if the cost of the signal

is higher for the bad type than it is for the good type, the bad type may not find it worthwhile to mimic, and

so the signal could be credible. Riley (1979) formalized the conditions under which such costly signaling

equilibria exist. Numerous papers giving examples of such costly signaling in capital markets followed. An

early paper was by Ross (1977), who showed how debt could be used as a costly signal to separate the good

from the bad. The second strand, the “cheap talk literature” which we call costless signaling in this paper,

began with Crawford and Sobel (1982). They showed that “cheap talk,” defined as a costless, non-binding,

and unverifiable message, could also be a credible signal. They modeled a two-player non-cooperative

information transmission game between a Sender and a Receiver. They demonstrated that the optimal

response of the Receiver after a signal is received may affect the utility of the Sender in a way that it may be

optimal for the Sender to tell the truth. In capital markets, an early paper was by Brennan and Hughes (1991),

who modeled how good firms doing costless stock splits could motivate brokers to provide favorable reports

about them.

In a recent paper, Austen-Smith and Banks (2000) have also allowed both costless and costly

signaling. The main difference between their model and ours is that they view the two types of signals as

complements in a general framework, whereas we model them as substitutes in the specific context of

signaling to capital markets. This means that the focus in Austen-Smith and Banks (2000) is on how costly

signals can improve cheap talk communication, whereas the focus in our model is on when costly signals have

to be used because costless signals will not work.

1 Dittmar (2000) also finds that share repurchases deter takeovers by increasing share prices (see Bagwell (1991)). However, this methodis most commonly linked to self tender offers, not open market repurchases. The latter is the subject of our paper.

4

Our empirical tests also liberally borrow insights from a growing literature. We are not the first to

empirically examine stock repurchases as signals of firm value (see, for example, Asquith and Mullins (1986),

Comment and Jarrell (1991), Dann, Masulis and Mayers (1991), Hertzel and Jain (1991), Lee, Mikkelson and

Partch (1992), and Vermaelen (1981)). However, most of these investigations assume that the repurchase

is a costly signal, which may not be true in an open market stock repurchase program if the firm does not

repurchase stock. Additionally, signaling firm value is not the only reason firms repurchase stock. We use

control variables in our empirical tests to account for the other reasons that firms repurchase stocks, and

which the literature has documented. Dittmar (2000) surveys the hypotheses expounded in the literature to

explain why firms repurchase shares and finds that three other motives are important at different times in the

period 1977 to 1996. The three other motives are: one, share repurchases are an alternative means of

distributing cash to shareholders (see, for example, Brennan and Thakor (1990), and Lucas and McDonald

(1996)); two, share repurchases may be used to tilt leverage ratios towards a target leverage ratio (see, for

example, Bagwell and Shoven (1988), and Havakimian, Opler and Titman (2001)); and three, share

repurchases may be preferred to dividends when a firm has employee stock options outstanding because most

stock options are not dividend-protected and share repurchases allow the firm to distribute cash without

diluting the per-share value of the stock. This third motive is particularly important if managers hold a lot

of stock options (see, for example, Jolls (1996), Kahle (2001), Fenn and Liang (2001), and Weisbenner

(2001)).1

Finally, our theoretical and empirical analyses also address two puzzles in the repurchase literature:

one, why some firms announce open market share repurchases, but never repurchase any stock; and two, why

stock prices increase at the announcement of an open market repurchase program, even though the

announcement does not commit the firm to purchase any stock, and many firms do not. Our hypotheses for

these two puzzles, as formalized in our theoretical model and evidence provided in our empirical investigation

5

are: in some special cases, the mere announcement of an open market share repurchase attracts scrutiny from

speculators, who then discover the true value of the firm; and two, this causes stock prices to increase at the

announcement of an open market repurchase program, even though the announcement does not commit the

firm to purchase any stock.

Oded (2000), like us, also puzzles as to why the announcement of an open-market share repurchase

program, which involves no commitment, is regarded as good news by the market. Ikenberry and Vermaelen

(1996) argue that this may be because announcements are tantamount to creations of valuable options of

buying undervalued shares in the future, but Oded (2000) argues that, if this were the reason, all types of

firms would make such announcements. So, in equilibrium, such “cheap talk” cannot create value. He then

goes on to develop a three-period signaling model that delivers positive announcement returns. In our paper,

we contend that “cheap talk” can create value when it attracts the attention of speculators, who go on to

discover the true value of the firm. We then put our hypothesis to the test.

The plan of the rest of the paper is as follows. We introduce the model in Section I. In Section II

we analyze the choice between costless signaling and costly signaling. The testable implications are

formalized in Section III. The data is discussed in Section IV. Section V is devoted to the empirical tests of

the model. Section VI concludes.

I. Model

There are two types of firms, good firms and bad firms, and each are equally likely. The good firms

as well as the bad firms are equally likely to have good projects or bad projects. The bad projects of both the

good firms as well as the bad firms have a payoff of - :. The good project of the bad firm has a payoff of +:,

whereas the good project of the good firm is equally likely to have a payoff of +: or a payoff of +a:. Here

a > 1. This asymmetry ensures that “good news is uncertain, but bad news is certain” for the market, an

2 The reason we need the “good news is uncertain, but bad news is certain” assumption for a cheap talk equilibrium is that we need thesearch strategy of the trader to be state-contingent: search only the good firm that is attracting attention. The same critical assumption drives the resultsof the Bhattacharya and Krishnan (1999) paper. How valid is this assumption? Bhattacharya and Krishnan (1999) tested this. They obtained a sampleof 1259 firms, each of which had data for fifteen quarters of 5-day returns after an earnings announcement. They then computed, for each firm, themean and the skewness of cumulative abnormal returns (CAR) in this 5-day event window. The cross-sectional statistics of these firm-specific metricwere as follows. The mean of the mean was indistinguishable from zero; the skewness ranged from a high of 0.67 to a low of -0.71, with a mean of0.009. Thus, good news is more uncertain than bad.

6

assumption that is critical for delivering a cheap talk equilibrium.2

Who knows what and when? This is given in Figure 1 below.

______________________

Insert Figure 1 about here

______________________

A. At time t

At time t, the world comes to know that all firms will have access to a positive net present value

project at time t+4. The NPV of this project is ". The investment required to start this project at time t+4

is I, which, with some loss of generality, we normalize to - :. This ensures that, if the firm does not do a

costly signal, the project can be funded from payoffs in all states for all types of firms.

B. At time t+1

At time t+1, a firm is born. As mentioned before, this firm could be good or bad with equal

probability. The manager of the firm knows the type of her firm. She may decide to keep quiet or to signal

its value. Value could be signaled in one of two ways: signal costlessly by attracting scrutiny or do a costly

signal by spending money m. The manager will take the action that maximizes the expected price of her

firm’s share. In other words, there are current shareholders who employ the manager to maximize the

expected share price, with agency problems, if any, resolved by the optimal contract between shareholders

and the manager.

C. At time t+2

At time t+2, it becomes known to all market participants whether a firm has a good project or a bad

project, though it is not publicly known who this project belongs to, a good firm or a bad firm .

3 The Kyle (1985) model gives the same results in our binary framework. Krishnan (1992) uses a binary framework to show the equivalencebetween Glosten-Milgrom (1985) and Kyle (1985), given identical parametric assumptions.

7

D. At time t+3

At time t+3, after receiving the public signal at time t+2, and after observing the action of the firm

at time t+1 – which, recall, could be a costless signal or a costly signal or inaction – a risk-neutral trader can

acquire, at a cost c, additional private information about the firm. This additional private information is a

costly private signal he gets telling him exactly what the project payoff at t+4 will be. This information cost

could be interpreted as the time and money spent doing further investigations by consulting an in-house

expert or an outside expert. The information set of the trader will therefore consist of his observation of the

manager’s actions, a piece of public information, and the outcome of incremental costly information

acquisition if he does any search.

E. At time t+3.5

At time t+3.5, there is a market for shares of these firms. The details of this market are inspired by

the extensive form introduced in Glosten and Milgrom (1985).3 There is a risk-neutral market maker who

commits himself to offer a liquidity supply schedule. To be specific, he commits himself to offer share prices

that are conditioned on the manager’s action, the public information, and his observation of order flows. We

allow only three order flows: +q, +1 and -1. We exogenously restrict the size of the order flows, as did

Glosten-Milgrom (1985), to prevent infinite orders from risk-neutral traders. Share prices are set such that

the market maker’s conditional expected profit in this competitive market is zero. In other words, the share

price equals the conditional expected value of the firm, a conditioning that is done with respect to the market

maker’s information set. The market maker’s information set is his observation of the manager’s actions, the

public information, and his observation of order flow.

Order flows are noisy. They could be information-based or non-information based. The logic for

making this assumption on order flow noise is now standard (see, for example, Grossman and Stiglitz (1980)).

Without it, the informed trader’s order would fully reveal his private information, and thus there would be

4 It is standard in market micro structure models and noisy rational expectations models to introduce noise in the order flow in this way.In some models, the non information-based noise is modeled, whereas in other models, it is assumed to be coming from noise traders. In most models,the non information-based noise is symmetric: there are as many buy non information-based orders as there are sell non information-based orders.There is no conceptual reason for assuming symmetry. Allen and Gorton (1982) derive intriguing results on price manipulation when non information-based orders are asymmetric.

8

no incentive to collect costly information to trade. We will assume that the small orders, +1 and -1, are

information-based, whereas the large order, +q, is information-based with a probability B. This asymmetry

ensures that “good news is uncertain, but bad news is certain” for the market-maker as well, an assumption

that is critical for delivering a cheap talk equilibrium.4

At t+3.5, the risk-neutral trader gives an order flow to maximize his expected profits. This order

could be, as mentioned before, -1, +1, or +q.

F. At time t+4

At t+4, since the -: funding required for the positive net present value project comes from the payoffs

of the projects, and since the manager used up cash m for signaling (m equals zero for costless signaling or

if the manager keeps quiet) at time t+1, the manager may have a shortfall of cash for the funding. This

shortfall is

s = Max [(-:) - (Project payoff at time t+4 – m), 0] (1).

She will have to borrow this shortfall s; otherwise, the positive NPV project will not be financed. External

borrowing, as opposed to internal financing, is costly. Let the cost of borrowing the shortfall s be denoted

by b(s). We shall assume that b(0) =0, and that b is increasing in s.

The payoffs are revealed. Portfolios are consumed.

9

II. Equilibria

From the point of view of the manager of the good firm, it is apparent in our model that if she could,

she would like to separate her firm by attracting scrutiny rather than incurring the deadweight cost of a costly

signal. The reason this is true is because in the former case, the cost of separation is being borne by the

strategic trader, who may find it in his interest to expend search costs and differentiate these firms, whereas

in the latter case, the cost of separation is being borne entirely by the firm. It should be mentioned here that

this unambiguous preference for costless signals over costly signals is an artifact of our model; in more

general models, this result may not hold. The reason this result may not hold in more general models, as in

the model of Austen-Smith and Banks (2000), is because the Receiver of the signal can pass all of the costs

of search to the Sender. As these search costs are passed entirely to the noise traders in our model, this will

not happen here. This allows us to claim that the manager of the good firm will always like to separate by

attracting scrutiny, but if that is not possible, costly signaling is the last resort.

What are the special circumstances under which costless signaling is possible? We now explore this

question.

A. Separating by costless signaling

Assume that q> 2/(1-B) and c < 0.25(a-1):[q(1-B) -2]. Conjecture that at time t+1 only good firms

attract attention. If a firm has attracted attention at time t+1, and if the public information is “good project”

at time t+2, conjecture that the trader searches at time t+3. If his search reveals the project payoff to be +:

(+a:), conjecture that the trader gives an order +1 (+q) at time t+3.5. If a firm has attracted attention at time

t+1, and if the public information is “bad project” at time t+2, conjecture that the trader does not search, and

he gives an order of - 1 at time t+3.5. If a firm has not attracted attention at time t+1, and if the public

information is “bad project” (“good project”) at time t+2, conjecture that the trader does not search, and he

gives an order of - 1 (+1) at time t+3.5. Conjecture that the posted prices of the market maker, which are set

at time t+3.5, are P(firm has attracted attention, good project, +q) = " + 0.5:{(a+1)+(a-1)B} > " + :; P(firm

10

has attracted attention, good project, +1) = "+:, P(firm has attracted attention, good project, -1) = " - :;

P(firm has not attracted attention, good project) = " + : and P(bad project) = " - :. Finally, conjecture that

at time t+4, the positive NPV project of value +" is undertaken by all types of firms.

Will these conjectures hold in a subgame perfect equilibrium? To check, we work backwards.

Assume that we are at time t+3.5. The various possibilities of the market maker’s information set at t+3.5,

his posterior beliefs given this information set and his conjectures, and the resultant prices that he posts are

given in Table I below.

______________________

Insert Table I about here

______________________

Given the above posted prices of the market maker at t+3.5, we now examine the trader’s expected

profits for his various order flows under his possible information sets at t+3.5 in Table II below.

______________________

Insert Table II about here

______________________

As q> 2/(1-B) by assumption, 0.5 q:(a-1)(1-B) > :(a-1). Therefore, from Table II, our conjectures

on the trader’s order flow strategy is upheld. Specifically, if a firm has attracted attention at time t+1, and

if the public information is “good project” at time t+2, and if a traders’s search at t+3 reveals the project

payoff to be +: (+a:), the trader gives an order +1 (+q) at time t+3.5. If, on the other hand, a firm has

attracted attention at time t+1, and if the public information is “bad project” at time t+2, and if the trader does

not search at t+3, the trader gives an order of - 1 at time t+3.5. If a firm has not attracted attention at time t+1,

and if the public information is “bad project” (“good project”) at time t+2, and if the trader does not search

at t+3, the trader gives an order of - 1 (+1) at time t+3.5. Table I tells us that the conjectures on the market

maker’s posted prices are upheld as well. Specifically, P(firm has attracted attention, good project, +q) = "

+ 0.5:{(a+1)+(a-1)B} > " + :; P(firm has attracted attention, good project, +1) = " + :, P(firm has attracted

11

attention, good project, -1) = " - :; P(firm has not attracted attention, good project) = " + : and P(bad

project) = " - :.

Let us now go to time t+3, where the trader has to make a decision on whether to incur an additional

cost c to find out more about the firm. We need to show that the trader’s search strategy – to search only

when a firm has attracted attention at t+1 and the public information at t+2 is “good project” – is optimal.

It is clear from the market maker’s posted prices in Table I that share prices are fully-revealing in all

states except the state where a firm has attracted attention at t+1 and the public information at t+2 is “good

project.” We know from Grossman and Stiglitz (1980) that costly search is unprofitable under fully revealing

prices. This implies that the only state where search could be profitable is the state where a firm has attracted

attention at t+1 and the public information at t+2 is “good project.” If the trader searches in this state he is

equally likely to discover a: or :. From Table II, his optimal order flow would be, respectively, +q or +1,

and the consequent gross expected profits would be, respectively, 0.5 q:(a-1)(1-B) and 0. Therefore, the net

expected profits from search is

0.25q:(a-1)(1-B) - c (2).

If he does not search, and gives an order of +1, his net expected profit is going to be

1 [0.5(a:+"-(:+")) + 0.5(:+" -(:+"))] = 0.5:(a-1) (3).

If he does not search, and gives an order of +q, his net expected profit is going to be

q [0.5(a:+" -0.5:{(a+1)+(a-1)B}+" ) + 0.5(:+" -0.5:{(a+1)+(a-1)B} +" )] < 0 (4).

Therefore, search when the firm has attracted attention and the public information is “good project” is optimal

if (2) > (3). This gives us

c < 0.25(a-1):[q(1-B) -2] (5).

This was the assumption on the upper bound of c we had made earlier. As we had also assumed that

q> 2/(1-B) (6),

the right-hand side of inequality (5) is positive. Therefore, if inequalities (5) and (6) hold, the trader will only

search the firm that has separated by attracting scrutiny and the public information is “good news.” He will

12

not search the firm in any other case. His optimal orders will be as given before, and the market maker’s

prices will be posted as shown in Table I.

Let us now go to time t+1. To complete the proof, we have to show that, given these strategies of

the other agents in the future, their conjectures on the signaling behavior of the managers at time t+1 will be

upheld in equilibrium. Specifically, we need to check that the conjectures that only the good manager attracts

attention at t+1, and that both types of firms undertake a project of positive NPV +" at t+4, are upheld.

At time t+1, if the manager of the good firm is expected to separate herself by attracting scrutiny and

she does, the price of her firm at t+3.5 will be (-:+") half the time, (+:+") a quarter of the time, and

0.5:{(a+1)+(a-1)B} +" a quarter of the time. So the expected price of this expected price maximizing good

manager, if she attracts attention, is going to be 0.125:(a+(a-1)B) + " > ". If the manager of the bad firm

is expected to keep quiet and she does, the price of her firm at t+3.5 will be (-:+") half the time and (+:+")

half the time. So the expected price of this expected price maximizing bad manager, if she keeps quiet, is

going to be ". If the manager of the good firm is expected to attract attention, but she decides to keep quiet,

she will not invite search from the trader if she gets a “good project.” The trader will give an order of +1

here, which will beget a price of (+:+"). So the price of her firm at t+3.5 will be (-:+") half the time and

(+:+") half the time, giving her an expected share price of of +". This is less than the expected share price

she would get if she attracted attention. So she would separate herself by attracting attention. However, if

the manager of the bad firm, who is expected to keep quiet but she does not, will invite search from the trader

if she gets a “good project.” The search will reveal a payoff of +: to the trader, who will give an order of

+1, which will beget a price of (+:+"). So the price of her firm at t+3.5 will be (-:+") half the time and

(+:+") half the time. So the expected price of this expected price maximizing bad manager, if she decides

to attract attention, is going to be ". This is the same expected share price she would obtain if she kept quiet.

Assuming an epsilon fixed cost of attracting scrutiny, the bad manager will prefer to keep quiet.

PROPOSITION 1: If the cost of search is below an upper bound, and there is an epsilon fixed cost

of attracting scrutiny, we obtain a costless signaling equilibrium. In this equilibrium, the good type will

13

separate by attracting scrutiny, and will be discovered to be good. The bad type will keep quiet, and no one

will investigate it.

If the cost of search is greater than the upper bound, that is inequality (5) is violated, there will not

be any search. If there is no search, traders will not be able to induce separation. Under this situation, the

good firm will have no recourse other than to resort to costly signaling to separate itself. We now consider

this equilibrium.

B. Separating by costly signaling

Our model on costly signaling follows the classic structure laid out by Spence (1973). The good firm

separates itself by spending money m, whereas the bad firm does not do anything. At time t+4, the positive

NPV project of value +" is undertaken by all types of firms. Suppose these are the conjectures of the market.

We will now show that these conjectures will be upheld in a separating equilibrium.

Assume that financing is not needed only when the project payoff is a:. Later we will give the

condition on exogenous parameter values that will guarantee this assumption. If the bad firm stays true, does

not spend cash m at t+1, and is regarded as a bad firm, its value, is

" + 0.5(:) + 0.5(-:) = " (7).

If the good firm stays true, spends cash m at t+1, and is regarded as a good firm, its value, is

" + 0.5(-:) + 0.5(0.5(:) + 0.5(a:)) - 0.75b(m) = " + 0.25:(a-1) - 0.75b(m) (8).

If the bad firm deviates by spending cash m at t+1, and is perceived as a good firm, its value, is

" + 0.25:(a-1) - b(m) (9).

If the good firm deviates by not spending cash m at t+1, and is perceived as a bad firm, its value, is

" (10).

Solve for m that makes (7) = (9). It will solve

b(m*) = 0.25:(a-1) (11).

It is easy to see that if m* solves (11), (8) > (10). As the good type will not like to spend more money

than is needed to separate, it will spend just m*. The bad type will be indifferent. Finally, to ensure that

5 In this paper, repurchasing stock is costly because this leads to a cash shortfall, which in turn leads to costly external financing. The extantliterature has modeled this cost in different ways. In Brennan and Thakor (1990), for example, share repurchase are costly because they redistributewealth from uninformed shareholders to informed shareholders. Our results depend on share repurchases being costly; they do not depend on whythey are costly.

14

financing is not needed only in the best state, when the payoff is a:, our exogenous parameters have to satisfy

the following condition: : - (-:) = 2: < m*, i.e.,

: < 0.5m* = 0.5 b-1 {0.25:(a-1)} (12)

PROPOSITION 2: If c is above a lower bound, we have a costly signaling equilibrium. In this

equilibrium, the good type will separate by spending money m*. The bad type will not spend any money.

Note that in the above model demonstrating costly signaling, in the interest of consistency, we

retained the critical assumption that drives the costless signaling result: “good news is uncertain, but bad news

is certain.” This asymmetry is not needed for our costly signaling result. The only critical assumption needed

for the costly signaling result is that good firms have a lower probability of a cash shortfall than bad firms

at t+4. This ensures that if bad firms try to mimic the good firm, they will have to undertake costly

refinancing more often.5

III. Testable Implications

Our theoretical model tells us that the good firm prefers costless signaling over costly signaling

because, in the former method, all of the cost of separation is being borne by the speculator who, after his

attention has been attracted, finds it optimal to expend search costs to find out more about the firm. The good

firm is discovered. The bad firm does not gain from being discovered; so it does not attract attention.

Speculators will only undertake search if they hope to discover substantial material non-public

information about a firm and then make substantial trading profits to cover the cost of scrutiny. As only good

firms, i.e. undervalued firms, signal, substantial material non-public information can only be obtained if the

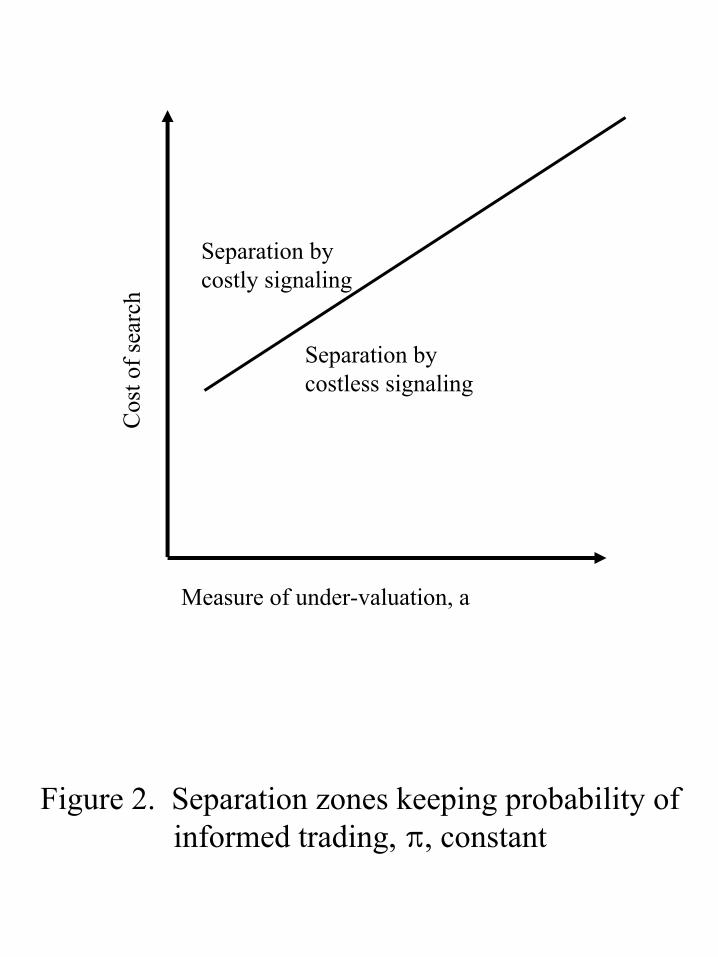

firm is deeply undervalued. The parameter a distinguishes the good firm from the bad firm. If a is 1, both

firms are equivalent. As a increases, their difference increases, and, if the firms are pooled, the higher is the

undervaluation of the good firm. Note that the upper bound of c – given in (5) – for which costless signaling

6 The mass of informed traders, B, is exogenous in our model. It could be argued that the mass of informed traders is endogenous, andit should depend on the cost of search. We claim that this is not going to make any difference to the comparative statics. The reason is the following.If the only barrier to becoming a speculator is the cost of gathering information, the number of speculators in equilibrium will be such that if anadditional speculator entered, he will lose money. Now suppose there is a shock in firm value which leads to a temporary disequilibrium. Theadditional speculator can now, perhaps, make short-term profits. He will make more short-term profits in the firm which had fewer speculators to beginwith because there is less competition. Such firms will, therefore, attract the marginal speculator more.

15

works increases as a increases. This is depicted in Figure 2.

_________________

Insert Figure 2 here

_________________

Figure 2 gives us the first testable implication of our model. Everything else equal, especially

holding the cost of search equal, more is the undervaluation of the good firm, greater is the likelihood of the

good firm separating itself by a costless signal rather than a costly signal.

The discovery of substantial material non-public information about a firm is useless if many other

speculators discover the same information and compete away all trading profits. In other words, if the size

of informed trading increases, stock prices become more informative, and so the value of the additional

information that can be obtained from costly search diminishes. To put it another way, more is the informed

trading, less is the benefit from search. The parameter B is a measure of the magnitude of informed trading.

If B increases, informed trading increases, and if B equals 1, all prices are fully revealing, and there is no

incentive to collect costly information. Note that the upper bound of c – given in (5) – for which costless

signaling works decreases as B increases. This is depicted in Figure 3.

_________________

Insert Figure 3 here

_________________

Figure 3 gives us the second testable implication of our model. Everything else equal, especially

holding the cost of search equal, more is the level of informed trading, less is the likelihood of the good firm

separating itself by a costless signal rather than a costly signal.6

7 Note that we do not claim that announcement of open market share repurchases is the only costless signal available to firms. Our claimis simply that announcement of open market share repurchases is that rare corporate signal that could be either costly or costless, depending onwhether the firm repurchases its own shares or it does not.

16

IV. Sample and Data

It is essential to the tests of the implications of our model that the firm has a choice of using a costless

signal, which means that it has the freedom not to carry through an announced transaction. It is equally

essential that some firms actually make this choice of not carrying through an announced transaction. The

announcement of open market stock repurchases meets both of these requirements. When the board of

directors approves an open market stock repurchase program, the firm typically announces the program to

the public. They do this because, if they do not, the repurchase may be a violation of the safe harbor

provisions under the stock price manipulation provisions of the Securities and Exchange Commission.

According to Stephens, Jagannathan and Weisbach (2000), there is little evidence of firms repurchasing stock

without first announcing the program. However, once the firm announces the repurchase program, it is not

obligated to repurchase stock. Further, as will be shown in Table III, a significant proportion of firms

announcing a stock repurchase never actually repurchase stock. This means that these firms signal with the

announcement, but never incur the cost of the signal. Thus, open market stock repurchase announcements

provide a unique opportunity to test the choice between costless and costly signals, and to investigate why

some firms announce a share repurchase program and never repurchase any stock, whereas other firms

announce and repurchase. 7

The initial sample consists of all firms announcing an open market stock repurchase between 1985

and 1995 as listed on Securities Data Corporation’s Mergers and Acquisitions database. We exclude

announcements in the last quarter of 1987, because the magnitude of the number of announcements suggests

that these announcements may differ from typical repurchase programs. Netter and Mitchell (1989) show

that twice as many repurchases were announced in this quarter than the prior three quarters of 1987. We do

not consider repurchase announcements subsequent to 1995 because we wish to examine if the firm

8This measure is the same as that used in Dittmar (2000) and Grullon and Michaely (2002).

17

repurchases stock for four fiscal years following the announcement. We limit our analysis to the first

repurchase announcement by each firm during the sample period. This is because these subsequent

announcements result in overlapping event windows when we consider the actual repurchases for the years

following the repurchase. Additionally, the information content of subsequent announcements may differ

from that of the initial announcement. We further require that the firms are listed on Compustat in the quarter

of the announcement. This results in a sample of 2297 firm repurchase announcements.

To determine if a firm repurchases stock, we use the Compustat data item Purchase of Stock. As

discussed in Stephens and Weisbach (1998), these data overstate stock repurchases because they include: 1)

conversions of class A, class B, and special stock into common stock; 2) conversions of preferred stock into

common stock; 3) purchases of treasury stock; 4) retirement or redemption of common stock; 5) retirement

of preferred stock; and 6) retirement or redemption of redeemable preferred stock.8. In this paper, we are only

interested in item 3, the purchase of treasury stock. We therefore adjust stock repurchases by reducing

Purchase of Stock by any decrease in preferred stock that occurs. This removes items 2, 5, and 6. The

resulting number may still be overstated by the amount of class A, class B, and special stock converted into

common stock, and the amount of retired common stock. However, most firms have only a single class of

stock and the retirement of stock is much less frequent than stock repurchases. Additionally, we measure if

the firm repurchases stock, not the amount of the repurchase; thus, these errors should have little impact on

our results.

Data on the number of analysts following the stock are from IBES. The market capitalization and

accounting data are from Compustat. The daily and quarterly stock returns are from CRSP. All explanatory

variables, except returns, are measured as of the fiscal year end prior to the year of the repurchase

announcement.

Panel A of Table III shows that of the 2,297 firms that announce repurchase programs between 1985

18

and 1995, the majority (1,248 firms) make their first repurchases within the quarter of or the quarter following

the announcement. This finding is consistent with the findings in Cook, Krigman, and Leach (2002), who

show that the length of the average repurchase program is 116 days for NASDAQ firms and 195 days for

NYSE firms. Panel B of Table III dissects what happens to the rest 1049 firms that do not make their first

repurchase within the quarter of or the quarter following the announcement. A surprising 409 firms (18%

of total sample) do not repurchase stock in any of the four years following the announcement. Additionally,

218 (9% of total sample) firms drop off of Compustat without repurchasing stock. Thus, 27% of the firms

in our sample appear to never repurchase any stock.

The previous statistics show that a significant 18% of the firms announcing a stock repurchase do not

repurchase stock in the four fiscal years following the announcement. This percentage is surprising in light

of the evidence in Stephens and Weisbach (1998). Stephens and Weisbach (1998) show that 10% of the firms

announcing a repurchase program purchase less than 5% of their stock. Our results differ from Stephens and

Weisbach (1998) for two reasons. First, Stephens and Weisbach (1998) look at Wall Street Journal

Announcements; we use all announcements on Security Data Corporation, which relies on several news

sources to track announcements, and is likely to include smaller firms. Second, our sample period is later

than the sample period used in Stephens and Weisbach (1998), who look at the 1981 to 1990 period. Fewer

announcing firms repurchase their stock in the later years of our sample. Panel C of Table III illustrates the

percentage of firms repurchasing stock by the year of the announcement. In 1985 and 1986, only 8% and 9%

of the firms did not repurchase stock in the four fiscal years after an announcement. It is likely that in the

period prior to 1985, the percentage of firms announcing but not repurchasing stock was even lower, since

the type of repurchase and types of firms repurchasing differ prior to 1984 (Dittmar (2000) and Grullon and

Michaely (2002)). In the later years of our sample, the number of non-repurchasers increased. In 1991, for

instance, the percentage of firms announcing but not repurchasing stock in the next four fiscal years peaked

at 27%.

9 If the announcement occurs in the last 2 trading days of the quarter, the quarter of the announcement is defined as the following quarter.

19

V. Empirical Tests

Our theoretical model relies on investors being able to determine if a firm uses a costless or a costly

signal. Thus, in the context of stock repurchases, it is important that investors know if the firm repurchased

stock. Unfortunately, in the U.S., firms do not disclose repurchases until their quarterly statements. We

therefore define a repurchaser (non-repurchaser) as a firm that has announced an open market share

repurchase and has repurchased (has not repurchased) in the quarter of or following the announcement. We

examine two quarters because the announcement may occur late in the first quarter and we need to allow

sufficient time for the firm to repurchase stock.9 Robustness checks with different time windows are

conducted in Table VII. The results do not change.

Our theoretical model predicts that a firm will chose a costless signal if the signal attracts scrutiny;

otherwise, the firm must put its money where its mouth is, and provide a costly signal. The signal will attract

scrutiny if the benefit to search is high. This is true for deeply undervalued firms, because the potential

capital gains to be realized from discovering large undervaluations and trading on that information is high.

Thus, our theoretical model predicts that more undervalued firms use a costless signal (announce share

repurchases without actually repurchasing) for separating, whereas less undervalued firms, where the benefits

to search are low, will use a costly signal (announce share repurchases and actually repurchase) for separating.

Vermaelen (1981), Dann (1981), Comment and Jarell (1991) and Grullon (2000) show that firms

announcing stock repurchases are undervalued, and that the announcement is a signal of their undervaluation.

Obviously, some firms are more undervalued than others. We measure undervaluation as the abnormal return

over the announcement period using three windows. The first window is the three days surrounding the

announcement, t-1 to t+1. We measure the cumulative abnormal return over this window using a market

model, the CRSP value-weighted market return, and a comparison period of –200 to –50 trading days. There

are two problems with a three day window: first, it may take more than three days to resolve the

10 Ikenberry, Lakonishok, and Vermaelen (1995) show that these narrow windows may not be sufficient to measure the full extent ofundervaluation. They provide evidence that repurchasing firms outperform non-repurchasing firms in the three years following the announcement.However, because our theoretical model relies entirely on investors interpreting one particular signal, we find it prudent to curtail the influence ofconfounding events by using a shorter window.

11 Several of the variables investigated are not available for all sample firms.

20

undervaluation and, second, as share repurchases are not disclosed immediately, shareholders will not be able

to distinguish between costly and costless signals. Our second measure of undervaluation is the buy and hold

abnormal return over the quarter of the announcement. We calculate the abnormal returns by subtracting out

the expected return, calculated using the CRSP value-weighted market return over the quarter and the firm

beta calculated over the 1985 to 1995 sample period. Finally, as the primary definition of a repurchaser (non-

repurchaser) in our paper is a firm that has announced an open market share repurchase and has repurchased

(has not repurchased) in the quarter of or following the announcement, our third measure of undervaluation

is the buy and hold abnormal return over these two quarters. The abnormal returns over these two quarters

are computed in the same way we computed abnormal returns over one quarter.10

Our theoretical model also predicts that the benefit to search is high when the ignorance in the market

about the firm is high. Thus, our theoretical model predicts that more ignored firms use a costless signal

(announce share repurchases without actually repurchasing) for separating, whereas less ignored firms, where

the benefits to search are low, will use a costly signal (announce share repurchases and actually repurchase)

for separating. In this paper, we use the number of analysts and two measures of firm size, the natural log

of the market capitalization and the natural log of assets, as measures for the lack of market ignorance about

a firm.

A. Summary Firm Characteristics of the Two Sub-Samples

Table IV presents summary statistics and tests for differences between the repurchasing and non-

repurchasing firms using t-tests for unequal, unpaired samples and Wilcoxon Rank-sum tests.11

Panel A describes our measures of ignorance; it depicts the number of analysts and firm size of the

repurchasing and non-repurchasing firms in the year prior to the repurchase announcement. Unfortunately,

21

IBES only follows 1,405 of the 2,297 sample firms. Thus, we assume that any firm not covered by IBES

has no analyst following. Though this assumption is not perfect, it is likely that firms not on IBES have

significantly less analyst following. To check the impact of this assumption, we repeat all the analysis

presented in this paper using only those firms that IBES covers. The results are unchanged. The mean

(median) repurchasing firm has 5.74 (2) analysts following it in the year before the announcement. The mean

(median) non-repurchasing firm has 3.39 (1) analysts following it in the year before the announcement. The

difference between the repurchasing and non-repurchasing firms’ mean and median number of analysts is

statistically significant. Thus, non-repurchasing firms are more ignored.

It could be argued that any analyst following will improve information and, thus, the proper metric

is a dummy variable if the firm has at least one analyst following it. Based on this dichotomous variable, the

repurchasing firms are more followed: 38% of repurchasing firms have no analyst following, whereas 50%

of the non-repurchasers have no analyst following. We repeat all the analysis presented in this paper using

this alternative measure. The results are unchanged. These statistics support the implications of the

theoretical model: firms that announce but do not repurchase are the ignored firms. Consistent with this

interpretation, repurchasing firms are also significantly larger than non-repurchasing firms, as measured by

the natural log of market capitalization or total assets.

Panel B of Table IV shows our measures of undervaluation. The three-day abnormal returns for

repurchasers and non-repurchasers are not significantly different. However, the one and the two quarter

abnormal mean or median returns for non-repurchasing firms are significantly higher than those for

repurchasing firms. This indicates that firms using stock repurchases as a costless rather than a costly signal

are more undervalued than those using a costly signal. Specifically, the median two quarter abnormal return

is six percent for the non-repurchasing firms and one percent for the repurchasing firms. Both sub-samples’

median abnormal returns are significantly greater than zero.

Our theoretical model focuses only on the signaling motive for repurchasing stock. However, there

are several other reasons why firms may repurchase stock. We control for these motives. Summary statistics

22

of these control variables are presented in Panel C of Table IV. One of the dominant motives firms

repurchase stock is to distribute excess cashflow. We measure the firm’s cashflow as its operating income

before depreciation divided by total assets in the fiscal year prior to the announcement; its cash balances as

the amount of cash and marketable securities divided by assets in the fiscal year prior to the announcement;

one measure of growth opportunity as the market value of equity plus the book value of debt divided by the

book value of assets; and another measure of growth opportunity as the ratio of research and development

expenses to sales in the fiscal year prior to the announcement. Research and development expense is assumed

to be zero for any firm with missing data. Panel C shows that repurchasing firms have significantly higher

cash flow. However, the difference between the sub-samples’ cash balances and growth opportunities is

inconclusive. Table IV also shows that the average repurchasing firm has a higher dividend payout ratio

(common dividends paid divided by operating income before depreciation), but the difference is not

significant. As stock repurchases absorb equity and therefore increase the firm’s leverage ratio, the firm may

use a stock repurchase to achieve its target debt ratio (Bagwell and Shoven (1988) and Havakimian, Opler

and Titman (2001)). We measure the leverage ratio as total debt net of cash balances divided by assets in the

fiscal year prior to the announcement. Table IV shows that the leverage ratios of repurchasing firms are

significantly lower than those of non-repurchasing firms. Also, since employee stock options are typically

not dividend protected, firms with a high level of stock options outstanding may prefer repurchases to

dividends since repurchases do not dilute the per share value of the firm (Jolls (1996), Kahle (2001), Fenn

and Liang (2001), and Weisbenner (2001)). Similar to Dittmar (2000), we measure the number of stock

options outstanding as the percentage of common shares reserved for stock options in the fiscal year prior to

the announcement, as reported in Compustat. Table IV shows that the mean percentage reserved is not

significantly different across the two samples.

We also control for the percentage of shares sought in the repurchase. This item is from the

repurchase announcement, and is reported by Security Data Corporation, but it is not available for all firms.

Not surprisingly, as we observe in Table IV, repurchasing firms announce that they are planning to repurchase

23

a greater percentage of stock than non-repurchasing firms.

B. Logit Analysis

To more formally test the implications of our theoretical model, we estimate a logit model in which

the dependent variable is one if the firm repurchases stock in the quarter of or following the repurchase

announcement, and zero otherwise, conditional upon the firm announcing a stock repurchase. We investigate

the impact that the number of informed traders (proxied by the number of analysts following and firm size)

and undervaluation (proxied by abnormal returns over the announcement period) have on the probability of

repurchasing, given that a firm announces a stock repurchase.

We present the results in Panel A of Table V. Columns one through three of Panel A provide

univariate analysis indicating that the firm is more likely to use a costless signal if the firm is more ignored.

An increase in analyst following or size significantly increases the probability a firm will repurchase stock.

In columns five and six, we provide univariate analysis indicating that the firm is more likely to use a costless

signal if the firm is more undervalued. An increase in undervaluation, as measured by either a one quarter

or a two quarter abnormal return following the announcement of a share repurchase program, significantly

increases the probability a firm will not repurchase stock. The three-day abnormal return shown in column

four, however, does not indicate a difference in the undervaluation of the sub-samples. All results continue

to hold in the bi-variate analysis presented in columns seven through nine. These results indicate that firms

put their money where their mouths are and repurchase, when there are more analysts following them and

when they are less undervalued.

The above analysis indicates that ignorance and undervaluation have a statistically significant impact

on the probability a firm chooses a costly over a costless signal. However, the coefficients of a logit model

are not the partial derivatives of the probabilities with respect to the independent variable, and thus must be

transformed to predict the effect of a change in one of the independent variables on the probability. To

evaluate the economic significance of these variables, we calculate the derivative with respect to each

independent variable, holding all variables constant at their mean. We use the coefficients from column nine

24

in Panel A, Table V, to calculate the impact of each variable. We then multiply the derivatives by the

standard deviation of the independent variable to determine the effect a one standard deviation change in the

independent variable has on the probability. The results show that analyst following and undervaluation have

an economically, as well as a statistically, significant effect on the probability a firm chooses a costly over

a costless signal. Specifically, a one standard deviation decrease in the two quarter abnormal return results

in a 10% increase in the probability a firm repurchases stock, i.e. uses a costly verus a costless signal. A one

standard deviation increase in the number of analysts results in a 7% increase in the probability of a stock

repurchase. These derivatives indicate that a change in the firm’s undervaluation or degree of informed

trading will have a significant impact on the probability of a costly versus a costless signal.

In Panel B of Table V, we further examine the impact of ignorance and undervaluation on the choice

between a costly and a costless signal using a stock repurchase announcement, while controlling for variables

that measure alternative reasons firms may repurchase stock. The results continue to strongly support the

implications of our model. The results presented in Panel B of Table V also show that cashflow, growth

opportunities, and leverage significantly impact the probability of a repurchase given that a firm announces

a repurchase program. Of these effects, cashflow has the greatest economic impact with a one standard

deviation change in cash flow resulting in a 24 percent increase in the probability a firm repurchases stock.

Thus, signaling value is not the only significant influence on a firms decision to repurchase stock. However,

the results supporting our model are robust to including these other control variables.

As explained above, our theoretical model predicts that firms are more likely to announce and not

repurchase – use a costless signal – if they are more undervalued. Further, our model shows that only

undervalued firms will signal value with an announcement; bad firms will not find it advantageous to mimic

good firms. However, since signaling is not the only motive to repurchase. In actuality, a firm may

announce a stock repurchase even if they are not undervalued. Thus, our model applies only to the subset

of undervalued firms announcing a stock repurchase. We focus on this subset in Table VI. We restrict our

sample to only those firms that have an abnormal return greater than zero, because these are the firms that

25

are likely to signal undervaluation. The results are striking. Consistent with the results presented in Panels

A and B of Table V, the coefficients on the one and two quarter returns show that firms are more likely to

not repurchase (use a costless signal) if they are more undervalued. However, unlike the previous results, this

holds true even for the more strict measure of undervaluation – the three-day abnormal returns. The

coefficient on analyst following has the same sign as in Table V, and it remains statistically significant. The

economic significance of the measures in the analysis presented in Table VI is similar to that from using the

full sample that is presented in Table V.

Though the primary definition of a repurchaser (non-repurchaser) in our paper is a firm that has

announced an open market share repurchase and has repurchased (has not repurchased) in the quarter of or

following the announcement, we conduct several robustness checks using different time windows for

repurchasing. In Table VII, we present results for three different time windows: the quarter of the

announcement, the fiscal year of the announcement, and four fiscal years after the announcement. The

advantage of using short windows are two: first, investors need to know soon whether the signal is costly or

costless and, second, not many other changes in firm characteristics nor many other news occur in short time

windows. The advantage of using long windows is that firms typically announce a two to three year

repurchasing program, and we should give firms this time to implement their repurchasing programs.

In column one of Table VII, we examine the quarter of the announcement. In this test, we measure

undervaluation using the one quarter abnormal return so that our horizon for repurchases and the resolution

of undervaluation concur. The results are similar to those using two quarters. The results examining longer

windows are presented in columns two through five of Table VII. In this analysis, we present results using

the one quarter abnormal return variable; however, the results are similar using the two quarter abnormal

return variable. A problem that arises in using these longer windows is that many of the firm characteristics

used to control for alternative reasons a firm may repurchase stock may change in this longer time window.

Thus, in columns three and five, but not in columns two and four, we include all control variables for the

subsequent years. When the repurchase horizon is one year, we include the control variables for the year of

26

the repurchase announcement. When the repurchase horizon also includes the three years following the

repurchase announcement, we include the variables at the end of these years, as well. The results continue

to support the predictions of our theoretical model. The economic significance of undervaluation and analyst

following is slightly less, but this is not surprising given the longer horizon. For instance, using the

coefficients in column five, a one standard deviation increase in abnormal returns (number of analysts)

decreases (increases) the probability a firm repurchases stock by 7% (5%). Thus, the variables of interest

continue to be economically important factors regardless of the repurchase horizon.

In a related paper, Ikenberry, Lakonishok, and Vermaelen (2000)examine the long run stock returns

following open market share repurchase announcements for Canadian firms. An advantage of using Canadian

firms is that, unlike U.S. firms, they have to report their monthly stock repurchases. The authors find similar

long-run returns to those reported in the U.S. Additionally, they show that firms buy more stock when returns

are lower. This evidence is consistent with our findings in that we show that firms are more likely to

repurchase stock when their announcement returns are low. The difference in our paper and their paper is

that one, we focus on the announcement period and use the abnormal return in that period to measure the

degree of undervaluation; two, we do not examine the amount of stock a firm repurchases but rather if they

repurchase any stock or not, because we are interested in determining if the repurchase announcement is a

costly or a costless signal; and three, for most of our analysis, we limit our examination period to only two

quarters because we need the firm to communicate soon to investors the type of signal they use.

Alternatively, Ikenberry, Lakonishok and Vermaelen (2000) examine much longer windows for repurchases

and returns in order to determine if firms repurchase stock after periods of stock price declines. Thus, they

investigate the market timing hypothesis, while we investigate the choice of signals. Though the results in

the two papers are consistent, we explore different issues.

The paper most similar to our empirical analysis is Stephens and Weisbach (1998). In this paper, the

authors document the percentage of stock repurchased and investigate why some firms repurchase more stock

than others. Our analysis differs from theirs in three ways. First, their question of interest differs from ours.

27

Their question of interest is what determines the amount of stock a firm repurchases. We are interested in

testing the dichotomous choice between costly and costless signaling. Second, because our question of

interest differs, so do our testing methods. Stephens and Weisbach (1998) estimate a tobit model to

investigate both the choice to repurchase and the percentage repurchased ,whereas we use a logit model to

focus on the difference in firms that announce and repurchase, and those that announce and never repurchase

any stock. Third, we examine and control for several motives for repurchasing that are not relevant to their

study. Thus, the results presented here cannot be inferred from their work.

VI. Concluding Remarks

This paper focuses on the two signaling mechanisms that can be used by a good type to separate itself

from the bad type: costless signaling and costly signaling. Under costless signaling, a good type can separate

itself from a bad type by attracting scrutiny; the bad type will not mimic because the bad type will not gain

from being discovered. Under costly signaling, a good type can separate itself from a bad type by giving a

costly signal; the bad type will not mimic because the signal is costlier for the bad type.

We develop a simple model that gives the good type the choice of signaling method. We set this

model in the context of an undervalued firm signaling its value to the capital market. Costless signaling

involves attracting scrutiny from speculators. Costly signaling involves spending money. We show that

under this capital market environment, the undervalued firm will always prefer the costless signaling method

to the costly signaling method. The intuition is that under the former method, the cost required for separating

is borne by the speculator, whereas under the latter method, the cost required for separating is borne by the

undervalued firm.

Costless signaling is shown to work only under special circumstances. This is because the ability to

attract scrutiny from speculators depends on whether there are enough incentives for these speculators to

scrutinize the firm. In a capital market, the incentives of speculators to scrutinize a firm is the trading profits

they obtain from discovering material non-public information about the firm. This means, and the model

28

formally shows, that costless signaling will only work if the benefits to search are high. These benefits of

search are high if the firm is deeply undervalued and it is deeply ignored, which increases the potential trading

profit of a speculator.

We then take our testable implications to a sample of firms announcing open market share

repurchases. This is a unique data set to test our theoretical model because a significant proportion of firms

that announce that they will repurchase their shares do not do it. Presuming that this subset is using costless

signaling, we investigate the characteristics of this subset. Compared to the firms who actually repurchase,

we find that this subset is more undervalued (as measured by abnormal returns over the announcement) and

is more ignored (as measured by analyst following and firm size). These two pieces of evidence strongly

support the predictions of our theoretical model.

Our results also address two questions in the repurchase literature: one, why do some firms announce

a stock repurchase but never repurchase any stock; and two, why does the stock price react positively to the

announcement of an open market stock repurchase program when it is not a commitment, and many firms

never repurchase any stock. Our response is that the second question answers the first: firms announce but

do not repurchase because the signal works, i.e,. the stock price increases. The stock price increases because

the announcement attracts scrutiny. This signals undervaluation because only undervalued firms will benefit

from scrutiny, and so will choose to attract scrutiny. More is the undervaluation, or more ignored is the firm,

more will be the scrutiny, because more will be the trading profits to be made from discovering material non-

public information about the firm. So, cheap talk is likely to work when the firm is more ignored and is more

undervalued.

i

REFERENCES

Allen, F. And G. Gorton, 1992, Stock price manipulation, market microstructure and asymmetric information,

European Economic Review 36, 624-630.

Asquith, P. and D. Mullins, 1986, Signaling with dividends, stock repurchases, and equity issues, Financial

Management 15, 27-44.

Austen-Smith, D. and J. Banks, 2000, Cheap talk and burned money, Journal of Economic Theory 91, 1-16.

Bagwell, L., 1991, Share repurchase and takeover deterrence, RAND Journal of Economics 22, 72-88.

Bagwell, L. and J. Shoven, 1989, Cash distribution to shareholders, Journal of Economic Perspectives 3, 129-

140.

Bhattacharya, U. and M. Krishnan, 1999, To believe or not to believe, Journal of Financial Markets 2, 69-98.

Brennan, M. and P. Hughes, 1991, Stock prices and the supply of information, Journal of Finance 46, 1665-

1691.

Brennan, M. and A. Thakor, 1990, Shareholder preferences and dividend policy, Journal of Finance 45, 992-

1017.

Comment, R. and G. Jarrell, 1991, The relative signaling power of dutch-auction and fixed-price self-tender

offers and open-market share repurchases, Journal of Finance 46, 1243-1271.

Cook, D., L. Krigman and C. Leach, 2002, On the timing and execution of open market stock repurchases,

Review of Financial Studies forthcoming.

Crawford, V.P. and J. Sobel, 1982, Strategic information transmission, Econometrica 50, 1431-1451.

Dann, L. 1981, Common stock repurchases: An analysis of returns to bondholders and stockholders, Journal

of Financial Economics 9, 113-138.

Dann, L., R. Masulis and D. Mayers, 1991, Repurchase tender offers and earnings information, Journal of

Accounting and Economics 14, 217-251.

Dittmar, A., 2000, Why do firms repurchase stock, Journal of Business 73, 331-355.

Fenn, G. and N. Liang, 2001 Good news and bad news about share repurchases, Journal of Financial

ii

Economics 60, 45-72

Glosten, L., and P. Milgrom, 1985, Bid, ask and transactions prices in a specialist model with

heterogeneously informed traders, Journal of Financial Economics 14, 71-100.

Grossman, S., and J. Stiglitz,1980, On the impossibility of informationally efficient markets, American

Economic Review, 70, 393-408.

Grullon, G., and R. Michaely, 2002, Dividends, share repurchaes, and the substitution hypothesis, Journal

of Finance 57, 1649-1684.

Grullon, G., 2000, The information content of share repurchase programs, working paper, Rice University.

Havakimian, A., T. Opler, and S. Titman, 2001, The debt-equity choice: An analysis of issuing firms, Journal

of Financial and Quantitative Analysis, forthcoming.

Hertzel, M. and P. Jain, 1991, Earnings and risk changes around stock repurchase tender offers, Journal

of Accounting and Economics 14, 253-274.

Ikenberry, D. and T. Vermaelen, 1996, The option to repurchase stock, Financial Management 25, 9-24.

Ikenberry, D., J. Lakonishok and T. Vermaelen, 1995, Market under-reaction to open market share

repurchases, Journal of Financial Economics 39, 181-208.

Ikenberry, D., J. Lakonishok, and T. Vermaelen, 2000, Stock repurchases in Canada: Performance and

strategic trading, Journal of Finance 55, 2373-2397.

Jolls, C., 1996, The role of compensation in explaining the stock-repurchase puzzle, working paper, Harvard

Law School.

Kahle, K., 2001, When a buyback isn’t a buyback: Open market repurchases and employee options,

Journal of Financial Economics, forthcoming.

Krishnan, M., 1992, On the equivalence between Kyle (1985) and Glosten-Milgrom (1985), Economics

Letters 40, 333-338.

Kyle, A.S., 1985, Continuous auctions and insider trading, Econometrica 53, 1315-1336.

Lee, D., W. Mikkelson and M. Partch, 1992, Managers’ trading around stock repurchases, Journal of Finance

iii

47, 147-1961.

Lucas, D. and R. McDonald, 1996, Shareholder heterogeneity, adverse selection, and payout policy, working

paper, Northwestern University.

Netter, J. and Mitchell, M., 1989, Stock-repurchase announcements and insider transactions after the October

1987 stock market crash, Financial Management 18, 84-96.

Oded, J., 2000, Why do firms announce open market repurchase programs? working paper, Carnegie Mellon

University.

Riley, J., 1979, Informational equilibrium, Econometrica 47, 331-360.

Ross, S., 1977, The determination of financial structure: The incentive signaling approach, Bell Journal of

Economics 8, 23-40.

Spence, M., 1973, Job market signaling, Quarterly Journal of Economics 87, 296-332.

Stephens, C. and Weisbach, M., 1998, Actual share reacquisitions in open-market repurchase programs,

Journal of Finance 53, 313-334.

Stephens, C., M. Jagannathan, and M. Weisbach, 2000, Financial flexibility and the choice between dividends

and stock repurchases, working paper, University of Missouri at Columbia.

Vermaelen, T., 1981, Common stock repurchases and market signaling: an empirical study, Journal of

Financial Economics 9, 139-183.

Weisbenner, Scott J., 2001, Corporate share repurchases in the 1990s: What role do stock options play?,

working paper, Univeristy of Illinois.

iv

Table IPosted Prices of the Market Maker

Market maker’sinformation at time t+3.5

Market maker’s posterior beliefs at timet+3.5

Market maker’s postedprices at t+3.5

Firm has attractedattention at time t+1;

good project at t+2; orderflow is +q at t+3.5

Probability B that the order is from traderwho has observed a:; Prob (1-B) that theorder is non information-based about a

good firm with expected value 0.5(:+a:)Project with NPV equal to + " will be

undertaken at t+4

" + B {a:} + (1-B) {0.5(:+a:)}

= " +0.5:{(a+1)+(a-1)B}

Firm has attractedattention at time t+1;

good project at t+2; orderflow is +1 at t+3.5

The order is from trader who has observed:

Project with NPV equal to + " will beundertaken at t+4

" + :

Firm has attractedattention at time t+1;

good project at t+2; orderflow is -1 at t+3.5

An out-of-equilibrium order flowProject with NPV equal to + " will be

undertaken at t+4

" - :

Firm has attractedattention at time t+1; bad

project at t+2

Bad project of value -:Project with NPV equal to + " will be

undertaken at t+4

" - :