Costing a Service Costing a Service Level Agreement Level Agreement Douglas Westwater Douglas Westwater 4 4 th th September 2008 September 2008 Welcome Welcome

Costing a Service Level Agreement Douglas Westwater 4 th September 2008 Welcome.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Costing a Service Level Costing a Service Level AgreementAgreement

Douglas WestwaterDouglas Westwater

44thth September 2008 September 2008

WelcomeWelcome

Welcome and Introductions

Course SummaryCourse Summary

Putting a price on the services that you deliver Putting a price on the services that you deliver can be very difficult. The session takes you can be very difficult. The session takes you through some of the key principles of costing through some of the key principles of costing your services, including:your services, including:

Full cost recovery - what does this mean and Full cost recovery - what does this mean and how can I calculate it for my organisation? how can I calculate it for my organisation?

Unit cost - how do I calculate the unit cost of Unit cost - how do I calculate the unit cost of my service? my service?

What is the best way to present our costs in What is the best way to present our costs in the SLA?the SLA?

Context : Service Level AgreementContext : Service Level Agreement

A A Service Level AgreementService Level Agreement ( (SLASLA) ) is a service contract where the level is a service contract where the level of service is formally defined. In of service is formally defined. In practice, the term practice, the term SLASLA is used to is used to refer to the contracted delivery time refer to the contracted delivery time (of the service) or performance (of the service) or performance

Everything is negotiatedEverything is negotiated

Service Level AgreementService Level Agreement

Definition of service to be deliveredDefinition of service to be delivered CostCost How is service measured, and outcomes How is service measured, and outcomes

analysed and monitoredanalysed and monitored Problem management (what systems do Problem management (what systems do

you have in place)you have in place) Customer (ie Midlothian Council, NHS etc) Customer (ie Midlothian Council, NHS etc)

responsibility – SLA is a 2 way processresponsibility – SLA is a 2 way process Warranties and insurancesWarranties and insurances Termination of contract - whyTermination of contract - why

Context of costingContext of costing

How fully you cost your recovery How fully you cost your recovery depends on depends on

How much you need this contractHow much you need this contract Your relationship with the purchaserYour relationship with the purchaser

Begging or sellingBegging or selling

Full Cost RecoveryFull Cost Recovery

Core Costs

CEO / Admin staff

Rent

etc

Project A

Project B

Project C

Profit margin and surplus£$$$$$

Break Even PointBreak Even PointBreak Even Point

Working out your priceWorking out your price

Assumptions;Assumptions; All costs are fixed or variableAll costs are fixed or variable Fixed costs remain constantFixed costs remain constant Variable costs vary in proportion to Variable costs vary in proportion to

activityactivity The only factor affecting costs and The only factor affecting costs and

revenue is activityrevenue is activity

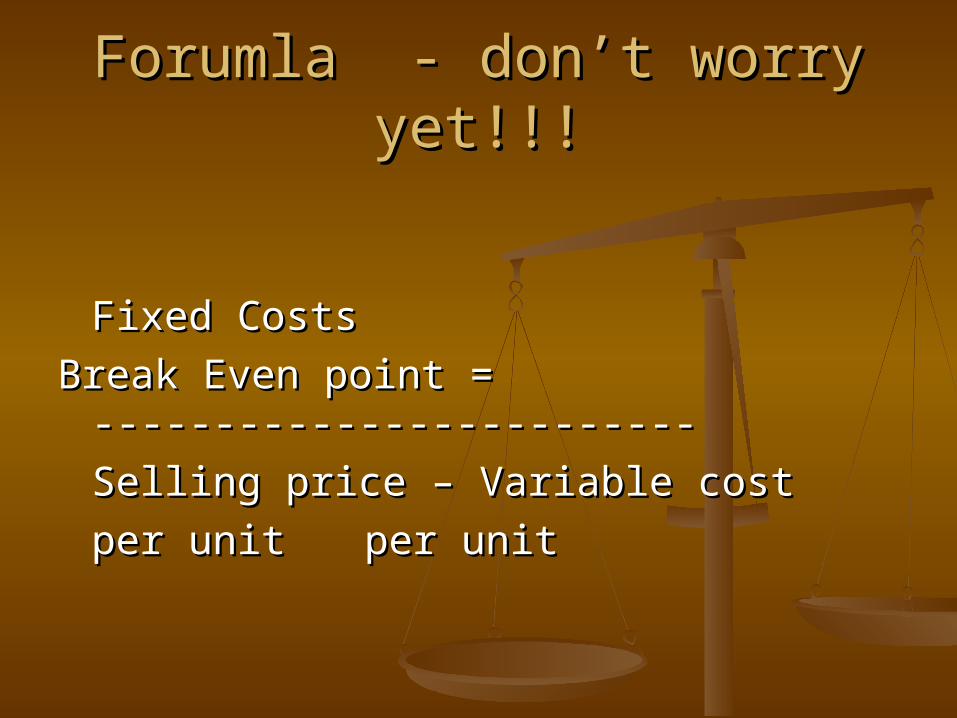

Forumla - don’t worry yet!!!Forumla - don’t worry yet!!!

Fixed CostsFixed Costs

Break Even point = -------------------------Break Even point = -------------------------

Selling price – Variable Selling price – Variable costcost

per unitper unit per unitper unit

Explanation – Don’t worry yet!!Explanation – Don’t worry yet!!

Sales revenue per unit less the Sales revenue per unit less the variable costs per unit equals a variable costs per unit equals a financial contribution to fixed costsfinancial contribution to fixed costs

Eventually a given number of Eventually a given number of contributions will cover the fixed contributions will cover the fixed costscosts

Each contribution per sale after this Each contribution per sale after this point is no longer required to cover point is no longer required to cover fixed costs and is therefore profitfixed costs and is therefore profit

ExampleExample

A social enterprise training org (MVA?) A social enterprise training org (MVA?) markets workshops openly. The markets workshops openly. The maximum number of participants is maximum number of participants is 20. Lesley wants to be able to offer 20. Lesley wants to be able to offer other social enterprises or vol orgs other social enterprises or vol orgs free or subsidised places. free or subsidised places.

Information we haveInformation we have

Commercial ChargeSelling price

£80 per place at each course

Fixed

Room Hire £250 Fixed

Facilitator £410 Fixed

Marketing and admin

£250 Fixed

Handouts £5 per place at each course

Variable

Lunch £5 per place at each course

Variable

SolutionSolutionFixed CostsFixed Costs

Break Even point = Break Even point = --------------------------------------------------Selling price – Variable costSelling price – Variable costper unitper unit per unitper unit

250 + 410 + 250 910250 + 410 + 250 910-------------------- ------------------------- -----80 – 1080 – 10 70 70

Break even point is 13 participants per course. Once Break even point is 13 participants per course. Once there are 13 paying places on the course all costs there are 13 paying places on the course all costs are covered.are covered.

Therefore 7 places can be free or subsidisedTherefore 7 places can be free or subsidised

Exercise 1Exercise 1

Commercial Charge £60,000 200 units x £300

MVA Hire £7500 Fixed

Freelancers £35,000 Variable 200 units x £175

John salary £20,000 Fixed

Stationary and admin

£2500 Variable

SolutionSolutionFixed Costs (divided where appropriate by 200 to get a per intervention costFixed Costs (divided where appropriate by 200 to get a per intervention cost

- same applies if yearly costs are used)- same applies if yearly costs are used)Break Even point = -------------------------Break Even point = -------------------------

Selling price – Variable costSelling price – Variable costper unitper unit per unitper unit

37.5 + 100 37.5 + 100 £137.50£137.50-------------------- -------------------- ----------

300 – 175 + 12.5300 – 175 + 12.5 £112.50£112.50

Break even point is 1.2 interventions. He needs to do 1.2 Break even point is 1.2 interventions. He needs to do 1.2 interventions to break even. This represents a loss. He therefore interventions to break even. This represents a loss. He therefore needs 1.2 x£300 = £360 per job to break even or 1.2 x 200 = 240 needs 1.2 x£300 = £360 per job to break even or 1.2 x 200 = 240 interventions to break even.interventions to break even.

0.2 is the loss each intervention. He makes an income of £125 each 0.2 is the loss each intervention. He makes an income of £125 each time. 125 x 0.2 = £25 loss x 200 interventions = yearly loss of time. 125 x 0.2 = £25 loss x 200 interventions = yearly loss of £5000 £5000

Fully costing your product or Fully costing your product or serviceservice

There is no right or wrong answer and it will be There is no right or wrong answer and it will be an estimate.an estimate.

1.1. Direct costs should be attributed to each Direct costs should be attributed to each activityactivity

2.2. Consistent and logical method to apportion Consistent and logical method to apportion remaining costs related to ‘Drivers’;remaining costs related to ‘Drivers’;

Space allocated to the projectSpace allocated to the project Numbers of beneficiariesNumbers of beneficiaries Numbers of employees involved (usually the Numbers of employees involved (usually the

largest cost)largest cost)

Allocating costsAllocating costs

Direct Premises ManagementOther

Project

costs

Individual Project costs

with apportioned overheads

Though no precise answer ALL costs must be allocated

One solution?One solution?

Admin space is 20% of rental (£6000)*. Rest Admin space is 20% of rental (£6000)*. Rest is a direct costs for the café. Rental costs is a direct costs for the café. Rental costs according to space occupied is 80% café according to space occupied is 80% café (£4800) and 20% outreach (£1200)(£4800) and 20% outreach (£1200)

Admin salary costs is £51,000* apportioned Admin salary costs is £51,000* apportioned by number of employees. Café is 15% by number of employees. Café is 15% (£7650) and outreach programme is 85% (£7650) and outreach programme is 85% (£43,350)(£43,350)

*Full overhead therefore is £57,000*Full overhead therefore is £57,000

Apportionment Apportionment

Café - £12,450Café - £12,450Outreach - £44,550 Outreach - £44,550

Total allocated is £57,000Total allocated is £57,000

To allocate by employee only would be To allocate by employee only would be Café Café £57,000 x 15% = £8550£57,000 x 15% = £8550OutreachOutreach £57,000 x 85% = £48,450£57,000 x 85% = £48,450

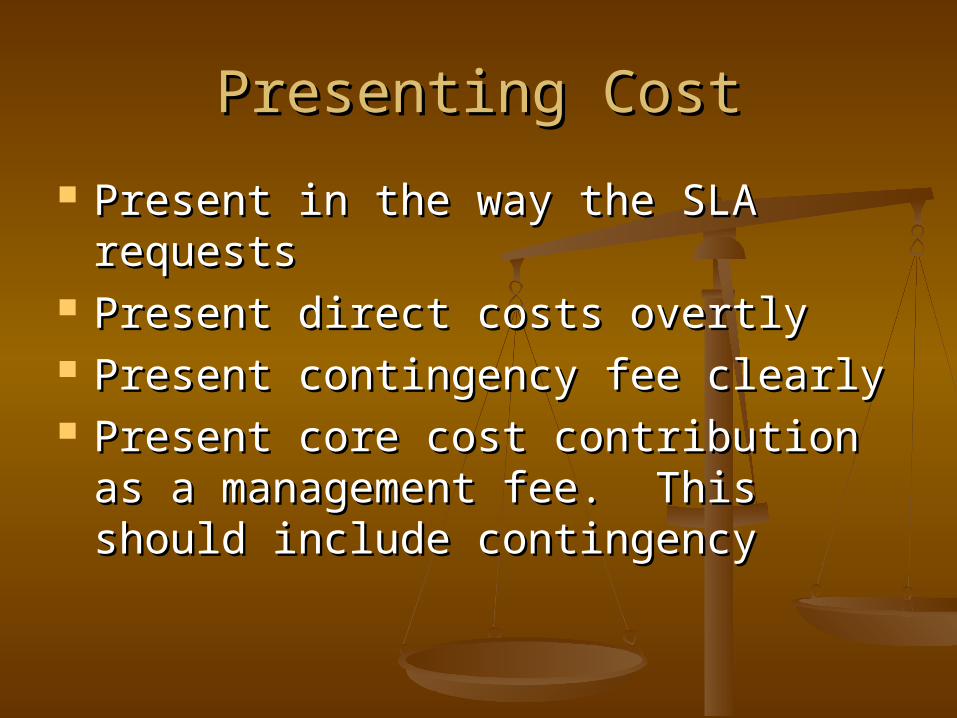

Presenting CostPresenting Cost

Present in the way the SLA requestsPresent in the way the SLA requests Present direct costs overtlyPresent direct costs overtly Present contingency fee clearlyPresent contingency fee clearly Present core cost contribution as a Present core cost contribution as a

management fee. This should management fee. This should include contingencyinclude contingency

ResourcesResources

http://www.philanthropycapital.org/tohttp://www.philanthropycapital.org/tools_for_charities/available_tools/full_cols_for_charities/available_tools/full_cost_recovery.aspxost_recovery.aspx

http://www.fullcostrecovery.org.uk/mhttp://www.fullcostrecovery.org.uk/main/index.php?content=homeain/index.php?content=home

http://www.biglotteryfund.org.uk/full_http://www.biglotteryfund.org.uk/full_cost_recoverycost_recovery

http://www.scotland.gov.uk/Publicatihttp://www.scotland.gov.uk/Publications/2007/02/14110906/0ons/2007/02/14110906/0

Related Documents