© MS Consultants, LLC 2013 © MS Consultants, LLC 2013 By David A. Fabian & Jeffrey D. HiaC MS Consultants, LLC Cost Segregation Studies, Depreciation Updates, and Final Tangible Property Regs

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

By David A. Fabian & Jeffrey D. HiaC MS Consultants, LLC

Cost Segregation Studies, Depreciation Updates, and Final Tangible Property Regs

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Today’s Topics

1. Cost SegregaEon 2. DepreciaEon Updates 3. Tangible Property Regs (TPR)

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

David A. Fabian Director, MS Consultants LLC

Office: 716-‐633-‐9840 Cell : 716-‐308-‐4868 Fax : 716-‐633-‐9469

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

David A. Fabian

• 25 years’ tax and accounting experience • Joined MS Consultants in 1999 • Personally involved in over 5,000 Cost

Segregation projects in more than 30 states • Presented on a variety of topics including

depreciation & cost segregation, energy modeling, repair vs. capitalization, & more

• Developed comprehensive in-house training and quality control programs

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Jeffrey D. Hiatt Heads the New England office

87 Lafayette Rd. Suite 11

Hampton Falls, NH 03844

Toll Free: 888.989.0054 Phone: 508.878.4846

Fax: 603.926.2811

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

MS Consultants, LLC

• We’re made up of tax, construcEon, and engineering professionals.

• Years of experience: – Cost SegregaEon Studies since 1996 – §179D cerEficaEons since 2006 – §45L cerEficaEon since 2008 – Repair vs. CapitalizaEon analyses since 2008

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Jeffrey D. Hiatt

• Has been affiliated with MS Consultants, LLC since 1999 • Helped MS Consultants become New England’s leading

provider of Cost Segregation Studies • Developed and fostered relationships with individual

clients, accounting firms and Societies. • Organized and run a practice helping Commercial

property owners reduce expenses on all types of commercial properties.

© MS Consultants, LLC 2012

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

MS Consultants, LLC

We have these folks…

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

MS Consultants, LLC

… and these folks…

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

MS Consultants, LLC

So that when it comes Eme to save money on your property or design and build projects you don’t look like this guy.

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013 Find us online – www.costsegs.com

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Today’s Topics

1. Cost Segrega-on Studies 2. DepreciaEon & Other Tax Topics 3. Tangible Property Regs (TPR)

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

What is a cost segregation study?

• IRS approved method to accelerate depreciaEon of specific assets

• Allocates a porEon of “39 and 27.5 year” property into 5, 7, and 15 year property

• IRS Tax codes §1245 and §1250

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

We perform cost segregation studies because…

Taxpayers under-depreciate their assets.

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Why?

• Rules are very complex • Properly segregaEng a property is a complex

process, requiring the right combinaEon of know-‐how: o Tax experEse and familiarity with prior tax liEgaEon o Engineering and construcEon knowledge

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

When’s the last -me you saved a client $213,315?

The Big Money Question

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Sample Study

Client purchases a building for $5,000,000 in 2006, and has taken depreciaEon over 39 years.

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

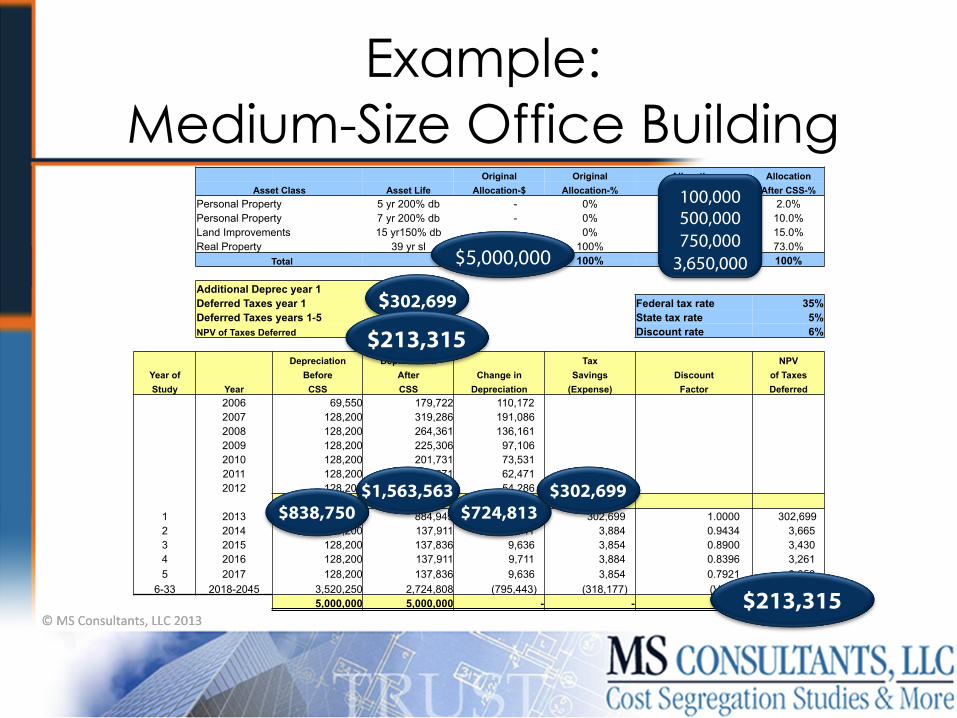

Example: Medium-Size Office Building

.

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Original Original Allocation Allocation Asset Class Asset Life Allocation-$ Allocation-% After CSS-$ After CSS-%

Personal Property 5 yr 200% db - 0% 100,000 2.0% Personal Property 7 yr 200% db - 0% 500,000 10.0% Land Improvements 15 yr150% db - 0% 750,000 15.0% Real Property 39 yr sl 5,000,000 100% 3,650,000 73.0%

Total 5,000,000 100% 5,000,000 100%

Additional Deprec year 1 756,749 Deferred Taxes year 1 302,699 Federal tax rate 35% Deferred Taxes years 1-5 318,177 State tax rate 5% NPV of Taxes Deferred 213,315 Discount rate 6%

Depreciation Depreciation Tax NPV Year of Before After Change in Savings Discount of Taxes Study Year CSS CSS Depreciation (Expense) Factor Deferred

2006 69,550 179,722 110,172 2007 128,200 319,286 191,086 2008 128,200 264,361 136,161 2009 128,200 225,306 97,106 2010 128,200 201,731 73,531 2011 128,200 190,671 62,471 2012 128,200 182,486 54,286 838,750 1,563,563 724,813 1 2013 128,200 884,949 756,749 302,699 1.0000 302,699 2 2014 128,200 137,911 9,711 3,884 0.9434 3,665 3 2015 128,200 137,836 9,636 3,854 0.8900 3,430 4 2016 128,200 137,911 9,711 3,884 0.8396 3,261 5 2017 128,200 137,836 9,636 3,854 0.7921 3,053

6-33 2018-2045 3,520,250 2,724,808 (795,443) (318,177) (Various) (102,794) 5,000,000 5,000,000 - - 213,315

Example: Medium-Size Office Building

.

100,000 500,000 750,000

3,650,000

$838,750 $1,563,563

$724,813 $302,699

$302,699 $213,315

$213,315

$5,000,000

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

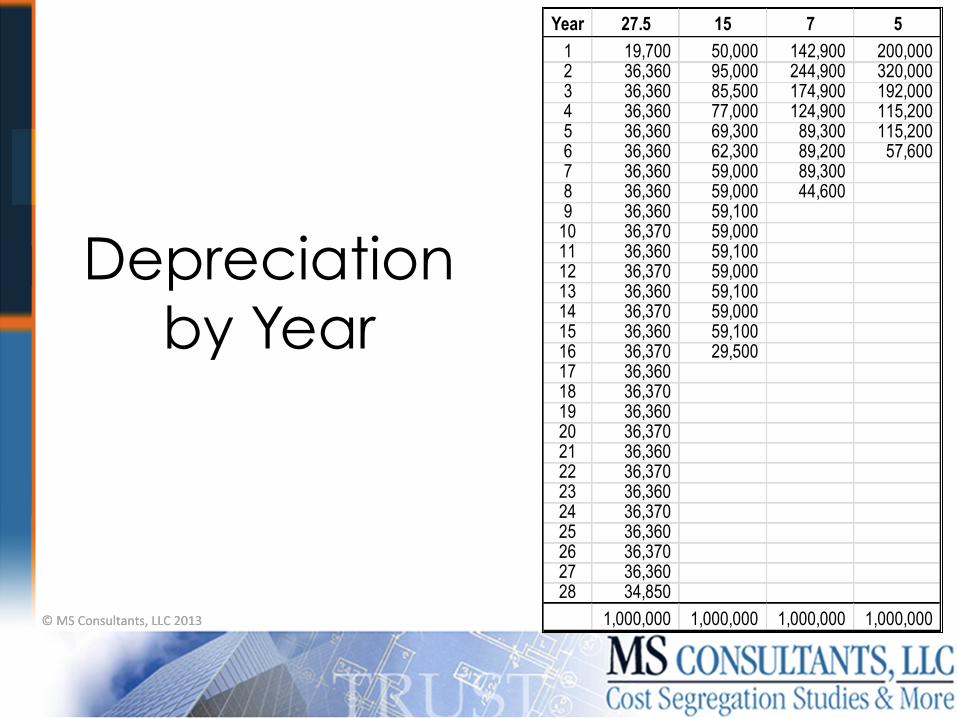

Depreciation by Year

Year 27.5 15 7 51 19,700 50,000 142,900 200,000 2 36,360 95,000 244,900 320,000 3 36,360 85,500 174,900 192,000 4 36,360 77,000 124,900 115,200 5 36,360 69,300 89,300 115,200 6 36,360 62,300 89,200 57,600 7 36,360 59,000 89,300 8 36,360 59,000 44,600 9 36,360 59,100

10 36,370 59,000 11 36,360 59,100 12 36,370 59,000 13 36,360 59,100 14 36,370 59,000 15 36,360 59,100 16 36,370 29,500 17 36,360 18 36,370 19 36,360 20 36,370 21 36,360 22 36,370 23 36,360 24 36,370 25 36,360 26 36,370 27 36,360 28 34,850

1,000,000 1,000,000 1,000,000 1,000,000

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Real Property: 27.5 or 39 Year (Structural Components)

• HVAC units • Ceramic Ele floors • Exterior doors • Windows • Interior plumbing • Siding • Concrete flatwork & foundaEons • Roof

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

HVAC Units

Ceramic Tile

Siding Concrete !atwork

& foundations

Exterior Doors & Windows

Roofs

Interior Plumbing

Where does the money come from?

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

15-year Property (Land Improvements)

• Removable site improvements • Certain Site uEliEes & drainage • Fencing & gates • RecreaEonal equipment • Signs & decoraEon • & More

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Where does the money come from?

Paving

Sidewalks, Steps and Curbing

Retaining Walls

Site Lighting

Trees, Landscaping and Irrigation

Grid Striping and Pavement Symbols

Flagpoles

Benches and other Outdoor equipment

15-year Property Land Improvements

& More

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Other 5- & 7-year Property (Personal Property)

• Specialty plumbing & electric • DecoraEve wall coverings • Carpet and other removable flooring • DecoraEve lighEng • Trim, cabinetry & millwork • Window treatments • & More

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Where does the money come from?

Decorative Trim

Decorative and accent lighting

Window Treatments

Decorative wood panels, wallpaper And other wallcoverings

Specialty electric and plumbing

Carpet and removable !ooring

5-year Property– Personal Property

& Much, Much More

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Where does the money come from? … a look inside our very own conference room

• Carpet • Wallpaper

• DecoraEve LighEng… • Audio/ Visual Electronics…

• Trim & Millwork

• … the wiring and hookups for all special equipment that you can’t see! • & More…

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

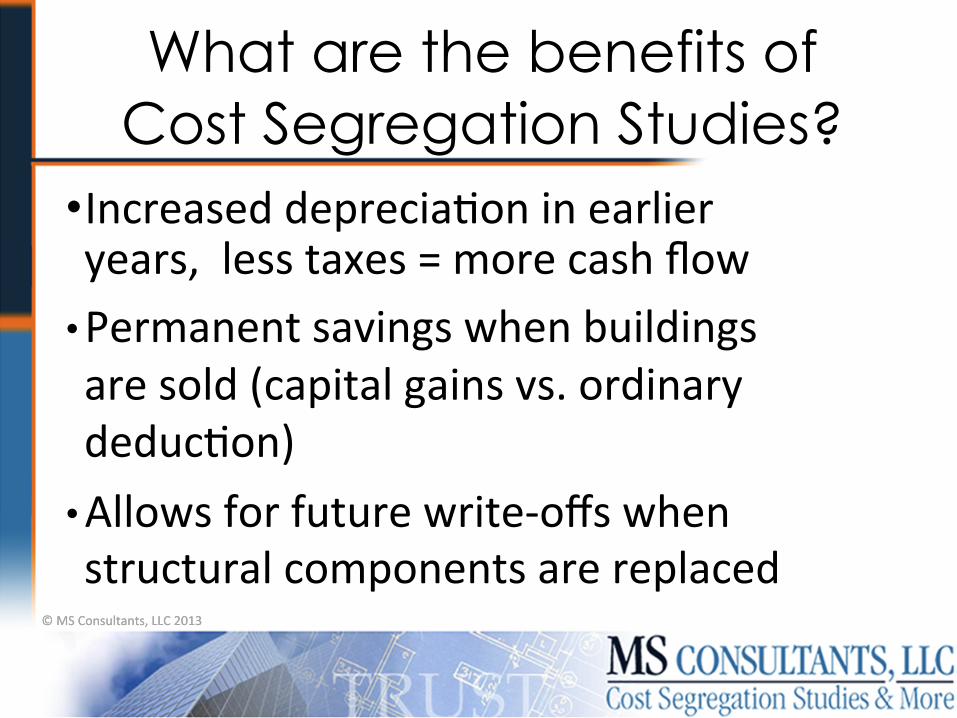

What are the benefits of Cost Segregation Studies?

• Increased depreciaEon in earlier years, less taxes = more cash flow

• Permanent savings when buildings are sold (capital gains vs. ordinary deducEon)

• Allows for future write-‐offs when structural components are replaced

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

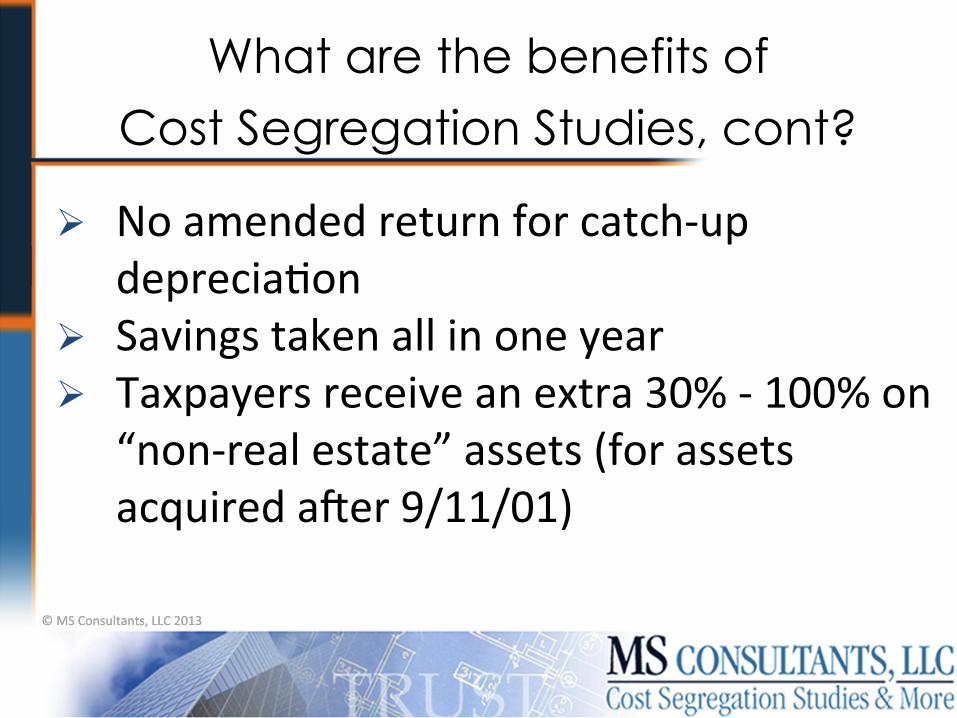

What are the benefits of

Cost Segregation Studies, cont?

Ø No amended return for catch-‐up depreciaEon

Ø Savings taken all in one year Ø Taxpayers receive an extra 30% -‐ 100% on

“non-‐real estate” assets (for assets acquired auer 9/11/01)

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

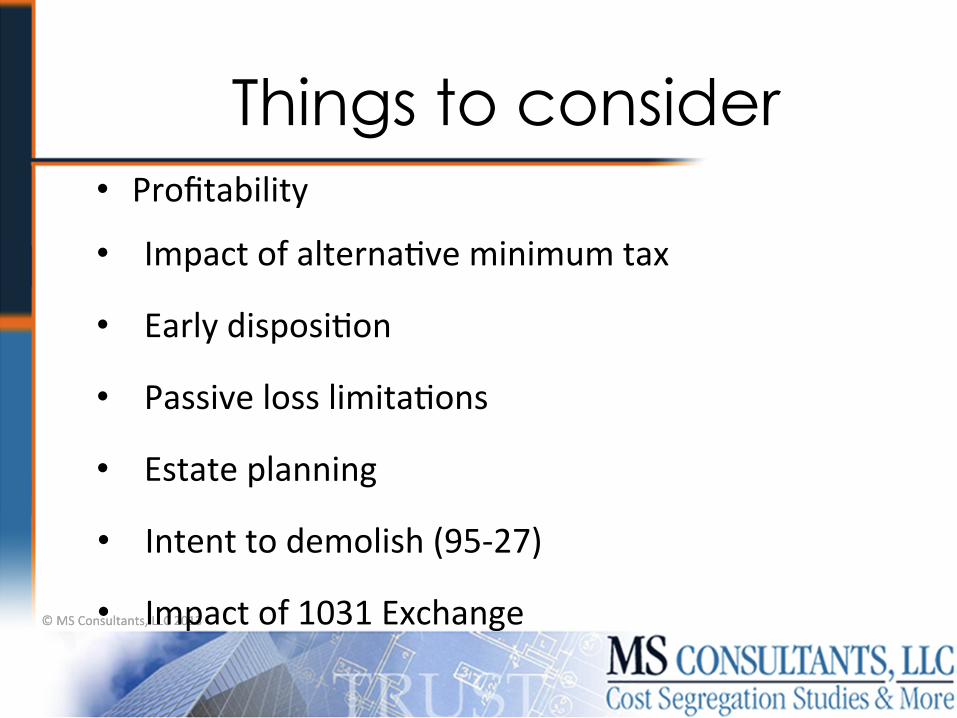

Things to consider • Profitability

• Impact of alternaEve minimum tax

• Early disposiEon

• Passive loss limitaEons

• Estate planning

• Intent to demolish (95-‐27)

• Impact of 1031 Exchange

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

How much can be reclassified?

Average

Ø Hotels

Ø Office buildings

Ø Apartments

Ø Medical office buildings

Ø Shopping plazas

Ø Manufacturing facilities

Ø Restaurants

20 – 30%

12 – 30%

20 – 35%

15 – 32%

20 – 38%

20 – 55%

15 – 40%

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

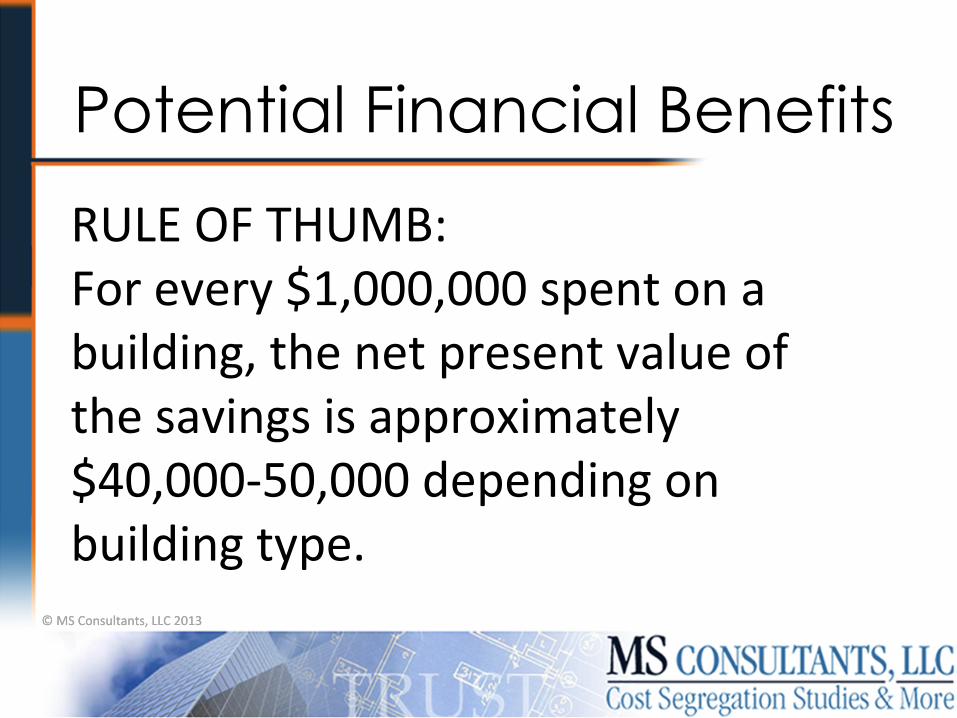

Potential Financial Benefits

RULE OF THUMB: For every $1,000,000 spent on a building, the net present value of the savings is approximately $40,000-‐50,000 depending on building type.

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

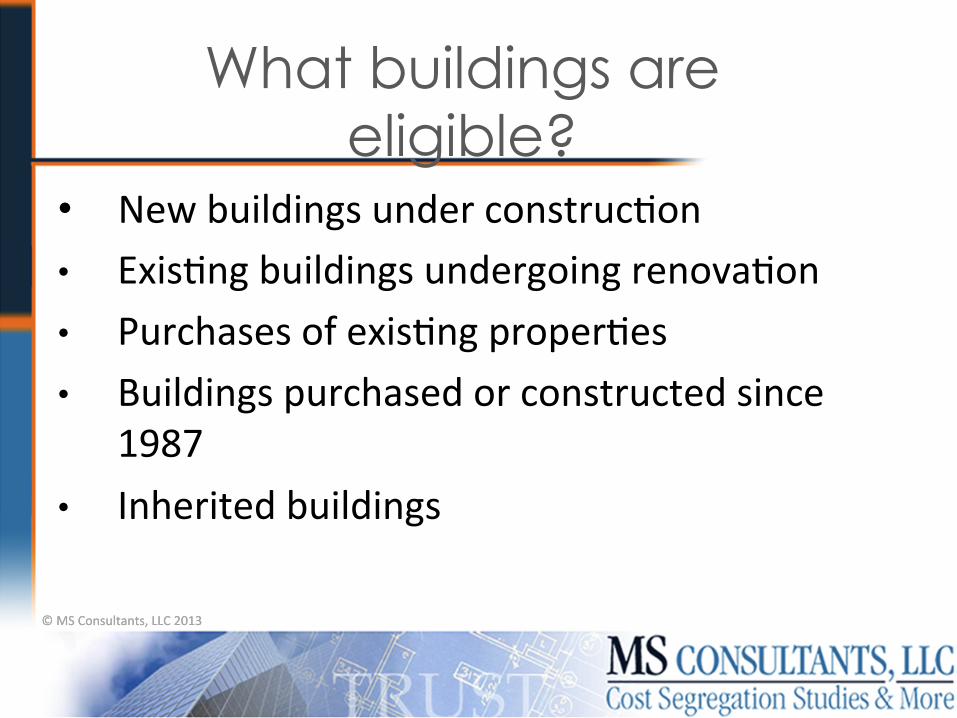

What buildings are eligible?

• New buildings under construcEon • ExisEng buildings undergoing renovaEon • Purchases of exisEng properEes • Buildings purchased or constructed since

1987 • Inherited buildings

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

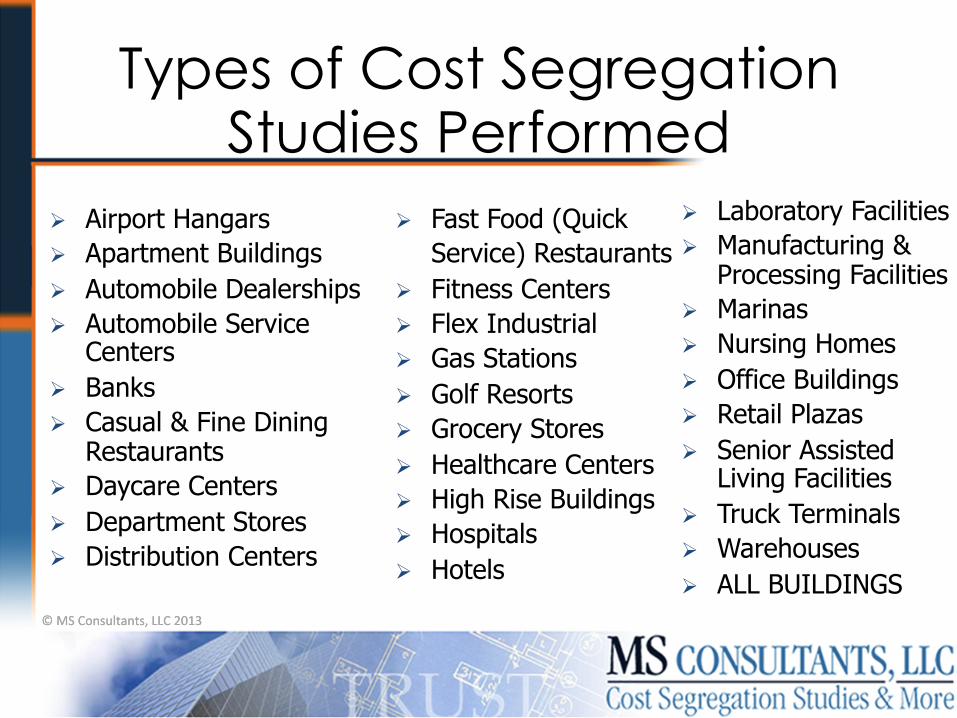

Types of Cost Segregation Studies Performed

Ø Airport Hangars Ø Apartment Buildings Ø Automobile Dealerships Ø Automobile Service

Centers Ø Banks Ø Casual & Fine Dining

Restaurants Ø Daycare Centers Ø Department Stores Ø Distribution Centers

Ø Fast Food (Quick Service) Restaurants

Ø Fitness Centers Ø Flex Industrial Ø Gas Stations Ø Golf Resorts Ø Grocery Stores Ø Healthcare Centers Ø High Rise Buildings Ø Hospitals Ø Hotels

Ø Laboratory Facilities Ø Manufacturing &

Processing Facilities Ø Marinas Ø Nursing Homes Ø Office Buildings Ø Retail Plazas Ø Senior Assisted

Living Facilities Ø Truck Terminals Ø Warehouses Ø ALL BUILDINGS

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Major Areas of Cost Allocation

Decora-ve Flooring

Decora-ve Non-‐structural wall coverings and trim

Window Treatments

Decora-ve Ceiling

Decora-ve Ligh-ng

Items not men-oned: Fire Protec-on Equipment,

Junc-on Boxes, Cabinets, Signs, Gas lines, Electrical Lines, Data Room Equipment, Power Panels, Conduit, Data Lines, HVAC System, Cable Trays, Improvements, etc…

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

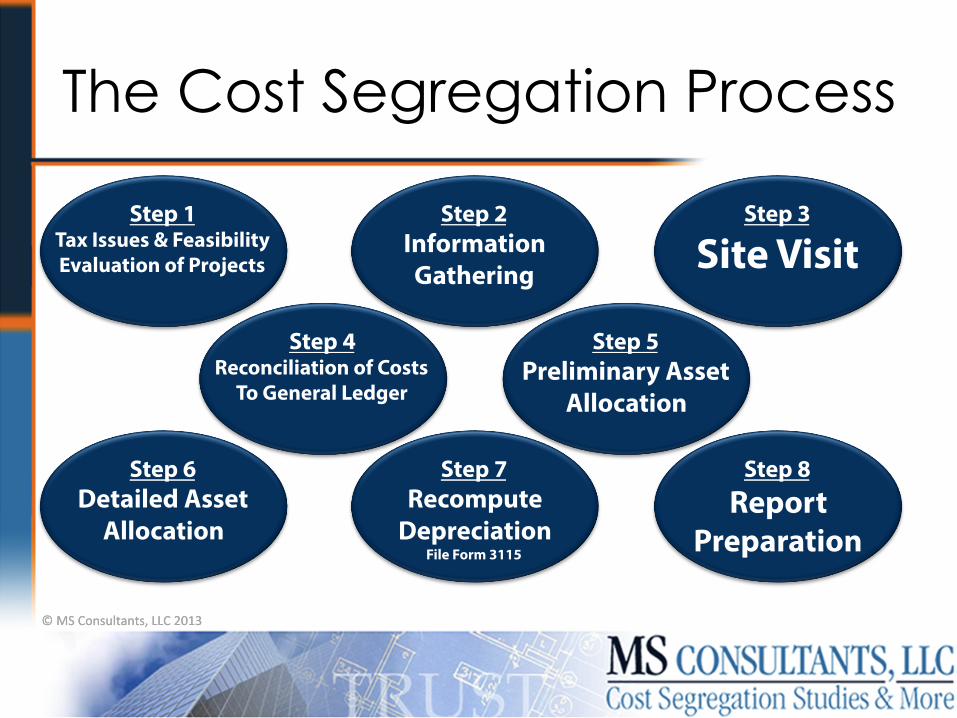

The Cost Segregation Process

Step 1 Tax Issues & Feasibility Evaluation of Projects

Step 2 Information Gathering

Step 3

Site Visit

Step 4 Reconciliation of Costs

To General Ledger

Step 5 Preliminary Asset

Allocation

Step 6 Detailed Asset

Allocation

Step 7 Recompute

Depreciation File Form 3115

Step 8 Report

Preparation

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Today’s Topics

1. Cost SegregaEon Studies 2. Deprecia-on & Other Tax Topics 3. Tangible Property Regs (TPR)

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

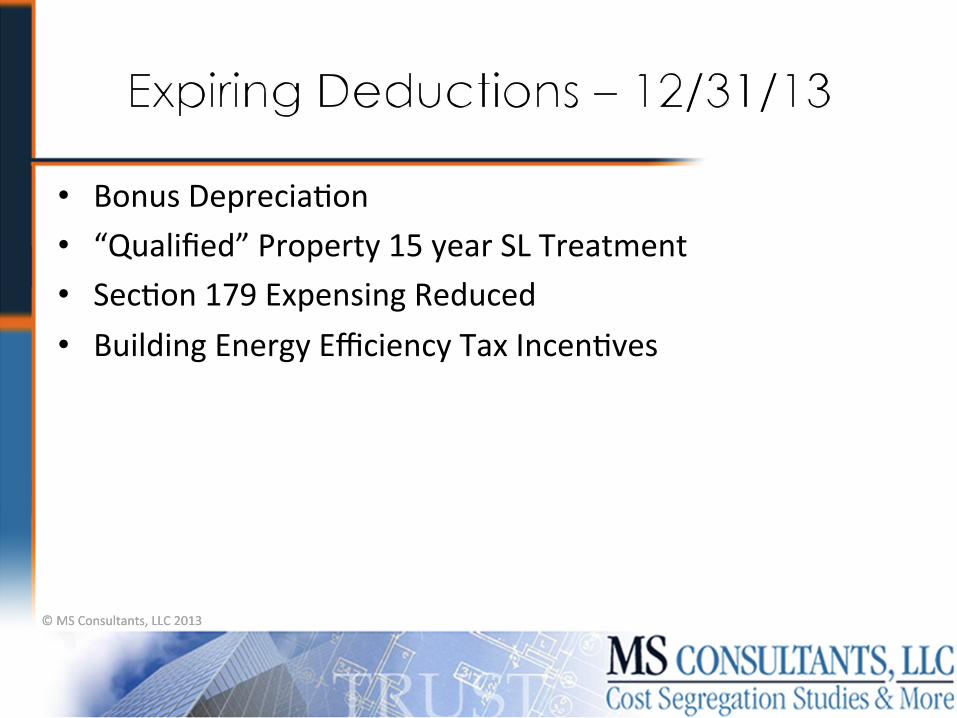

• Bonus DepreciaEon • “Qualified” Property 15 year SL Treatment • SecEon 179 Expensing Reduced • Building Energy Efficiency Tax IncenEves

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

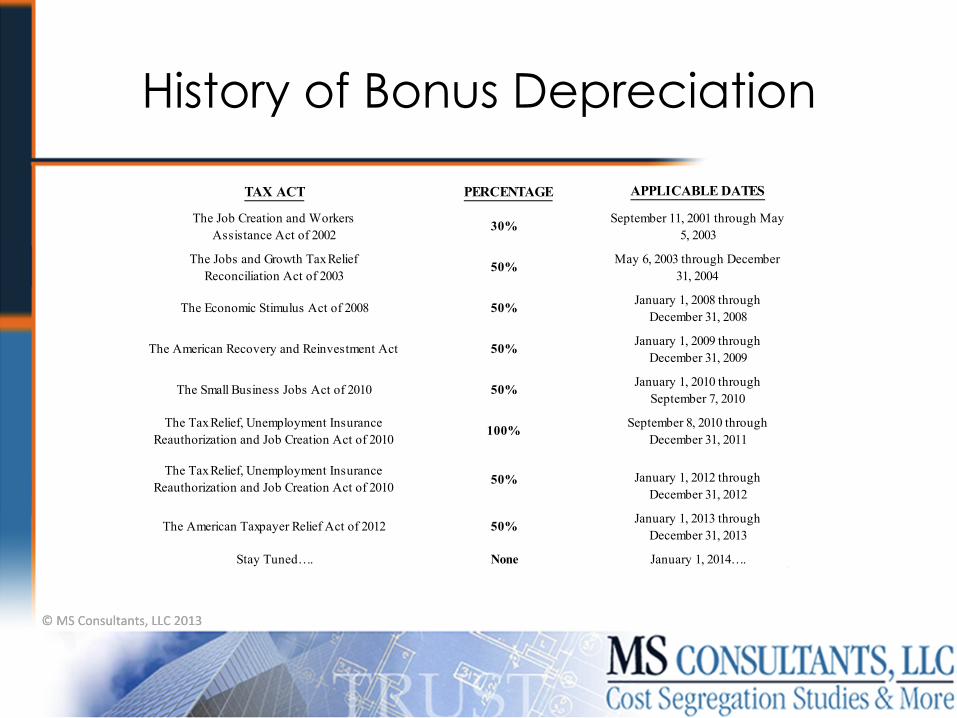

History of Bonus Depreciation

TAX ACT PERCENTAGE

The Job Creation and WorkersAssistance Act of 2002

30%

The Jobs and Growth Tax ReliefReconciliation Act of 2003

50%

The Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010

100%

The Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010 50%

The American Taxpayer Relief Act of 2012 50%

Stay Tuned…. None

September 8, 2010 through December 31, 2011

The Small Business Jobs Act of 2010 50% January 1, 2010 through September 7, 2010

The American Recovery and Reinvestment Act 50% January 1, 2009 through December 31, 2009

The Economic Stimulus Act of 2008 50% January 1, 2008 through December 31, 2008

May 6, 2003 through December 31, 2004

September 11, 2001 through May 5, 2003

January 1, 2013 through December 31, 2013

January 1, 2014….

January 1, 2012 through December 31, 2012

APPLICABLE DATES

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

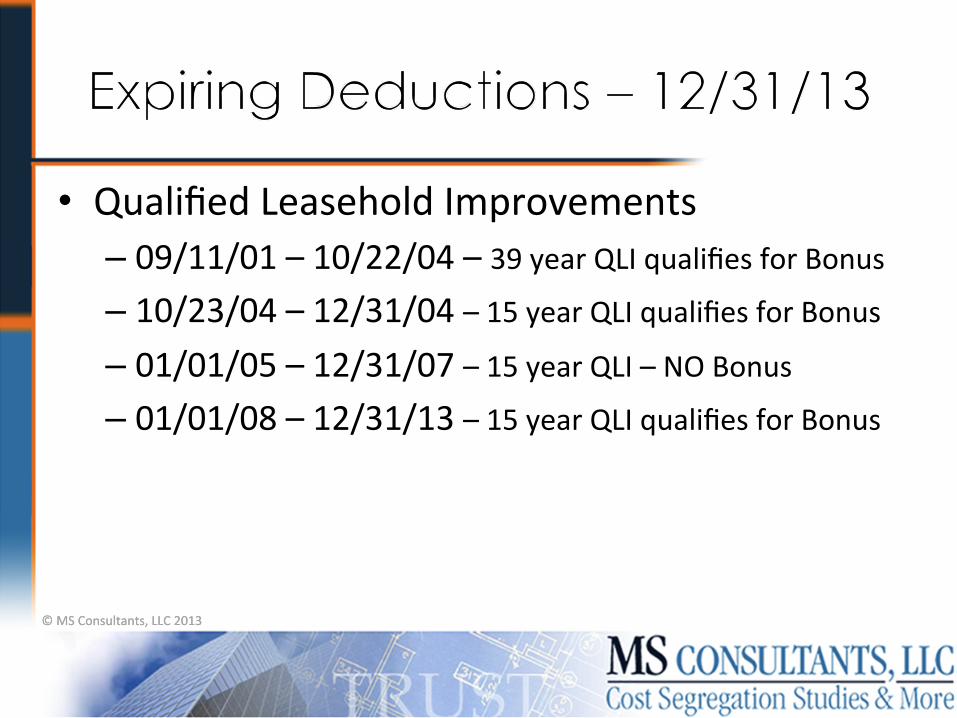

• Qualified Property – 15 year Straight Line Treatment – Qualified Leasehold Improvements (QLI) – Qualified Restaurant Property (QRP) – Qualified Retail Improvement Property (QRIP)

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

• Qualified Leasehold Improvements – 09/11/01 – 10/22/04 – 39 year QLI qualifies for Bonus – 10/23/04 – 12/31/04 – 15 year QLI qualifies for Bonus – 01/01/05 – 12/31/07 – 15 year QLI – NO Bonus – 01/01/08 – 12/31/13 – 15 year QLI qualifies for Bonus

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

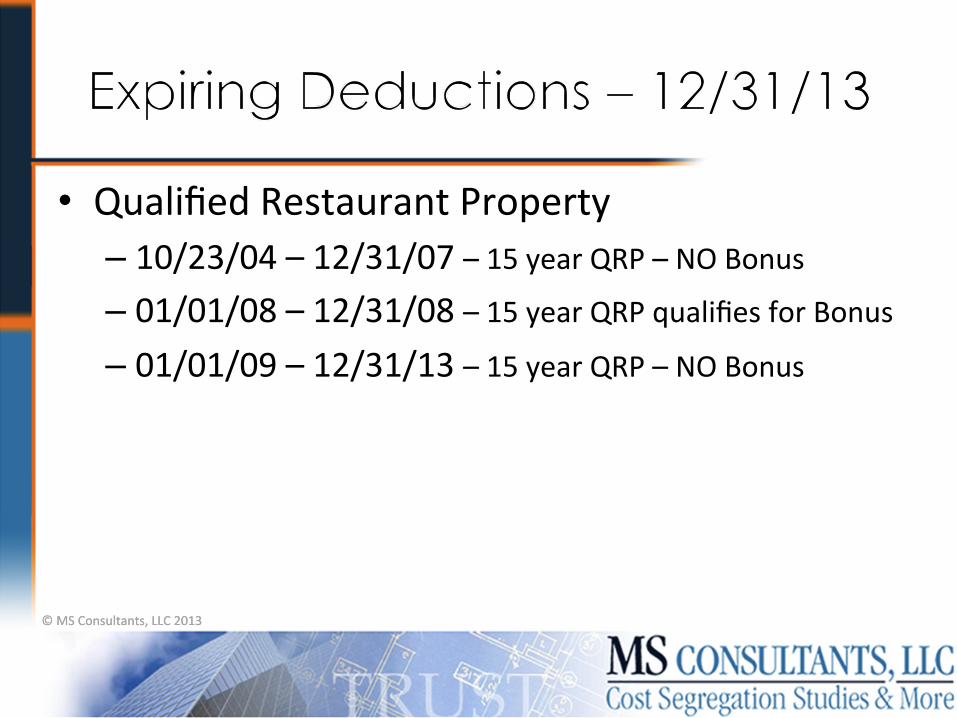

• Qualified Restaurant Property – 10/23/04 – 12/31/07 – 15 year QRP – NO Bonus – 01/01/08 – 12/31/08 – 15 year QRP qualifies for Bonus – 01/01/09 – 12/31/13 – 15 year QRP – NO Bonus

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

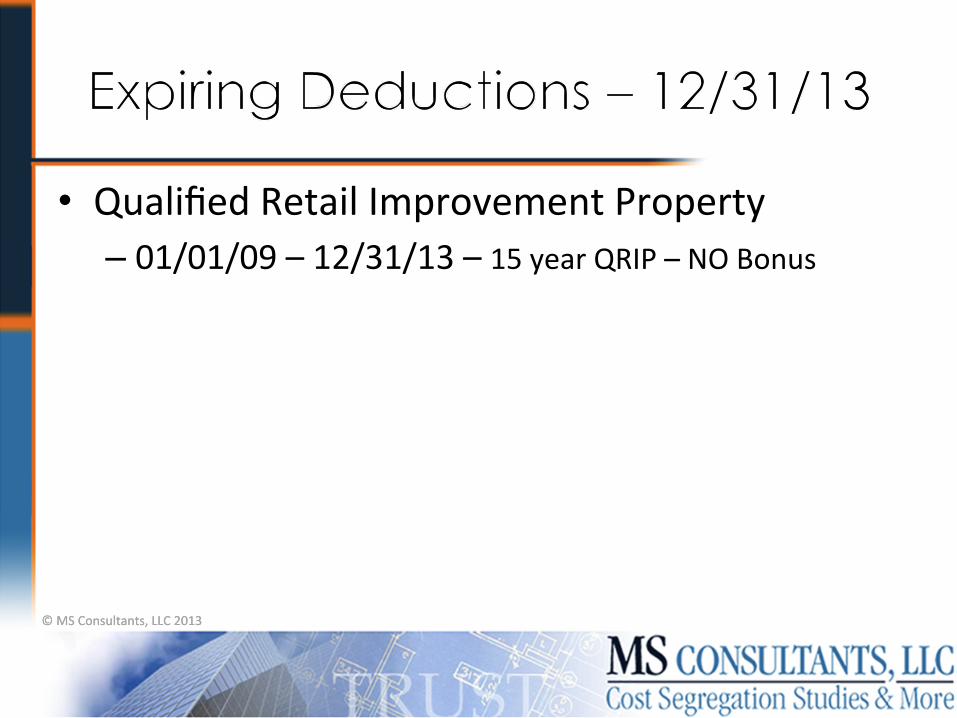

• Qualified Retail Improvement Property – 01/01/09 – 12/31/13 – 15 year QRIP – NO Bonus

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

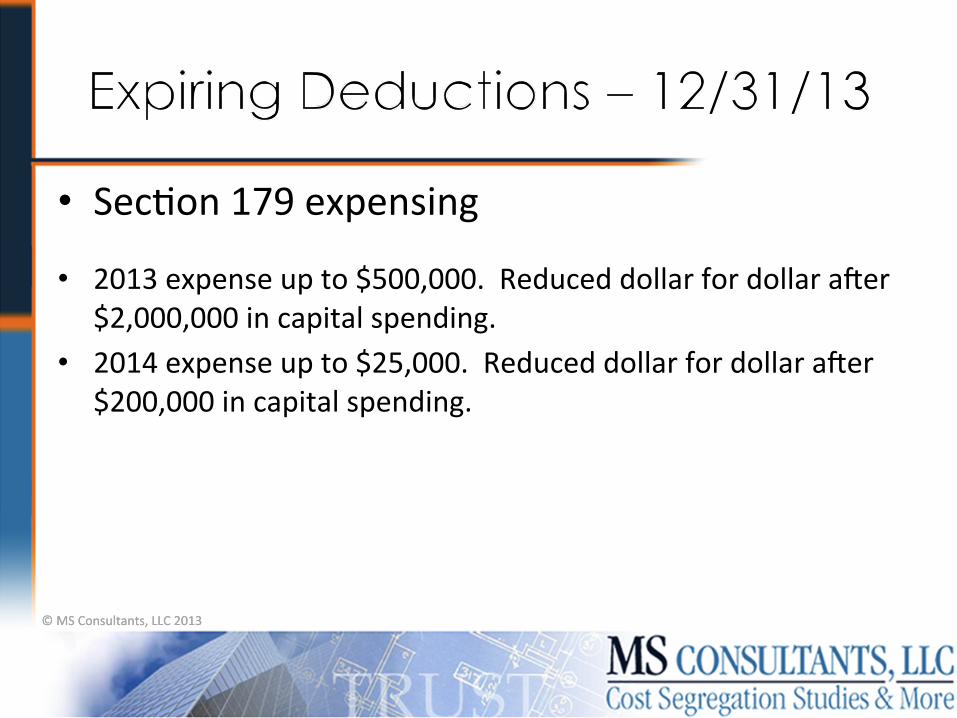

• SecEon 179 expensing • 2013 expense up to $500,000. Reduced dollar for dollar auer

$2,000,000 in capital spending. • 2014 expense up to $25,000. Reduced dollar for dollar auer

$200,000 in capital spending.

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

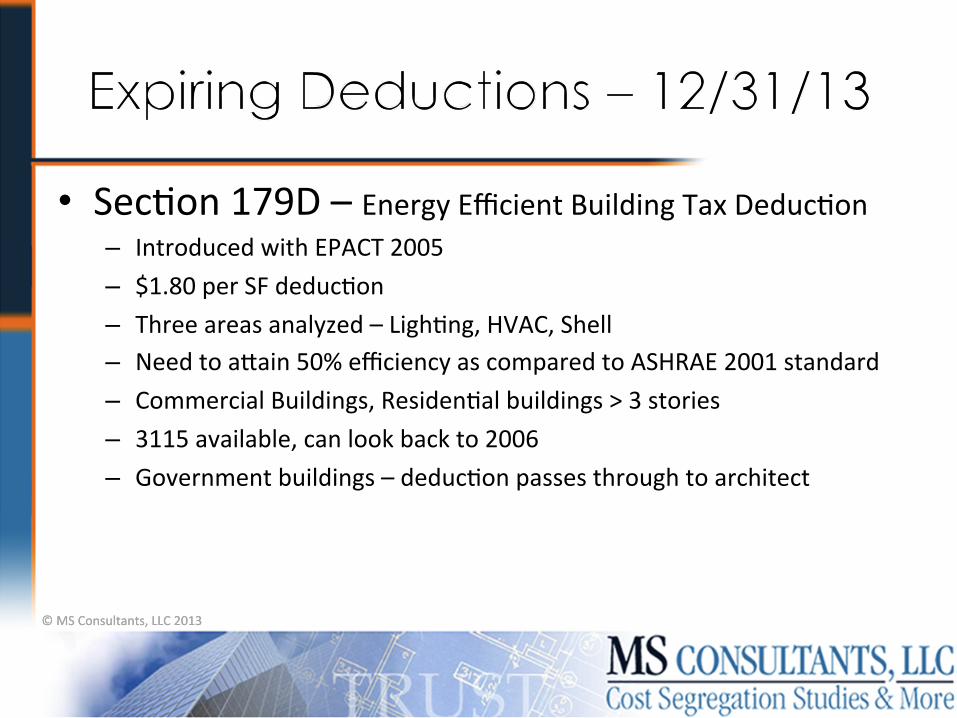

• SecEon 179D – Energy Efficient Building Tax DeducEon – Introduced with EPACT 2005 – $1.80 per SF deducEon – Three areas analyzed – LighEng, HVAC, Shell – Need to aCain 50% efficiency as compared to ASHRAE 2001 standard – Commercial Buildings, ResidenEal buildings > 3 stories – 3115 available, can look back to 2006 – Government buildings – deducEon passes through to architect

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

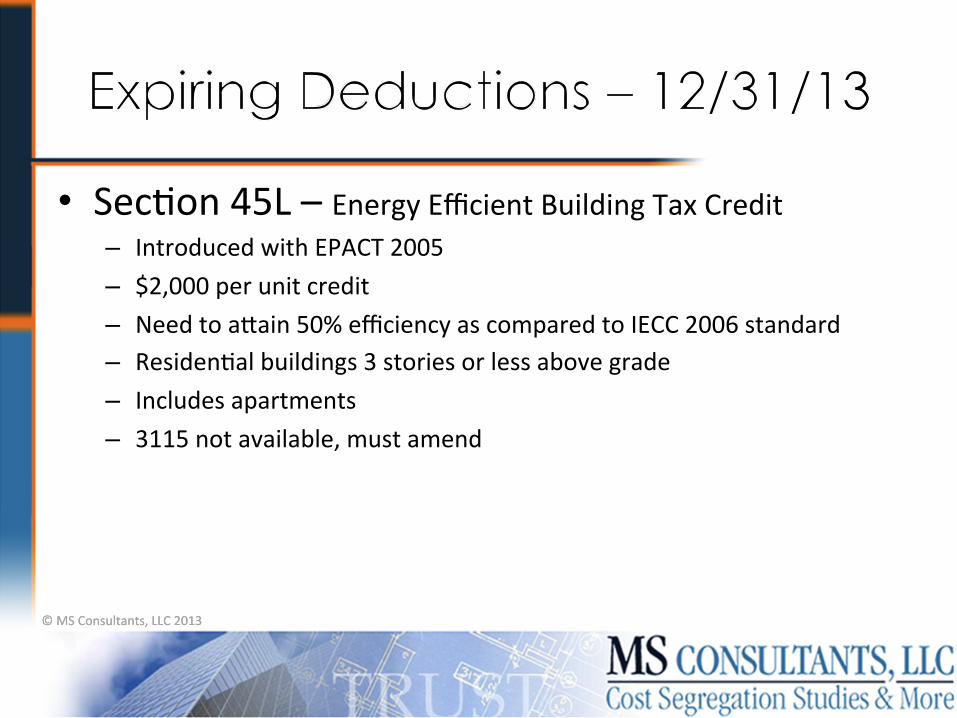

• SecEon 45L – Energy Efficient Building Tax Credit – Introduced with EPACT 2005 – $2,000 per unit credit – Need to aCain 50% efficiency as compared to IECC 2006 standard – ResidenEal buildings 3 stories or less above grade – Includes apartments – 3115 not available, must amend

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Today’s Topics

1. Cost SegregaEon Studies 2. DepreciaEon & Other Tax Topics 3. Tangible Property Regs (TPR)

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Tangible Property Regulations (TPR)

Repair vs. Capitalization

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

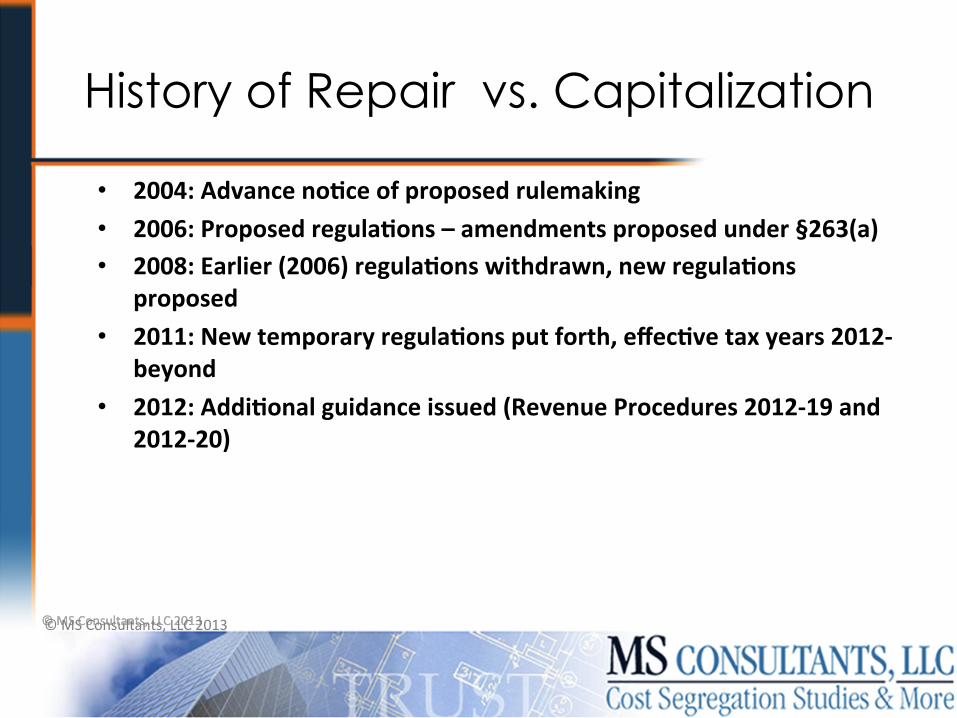

History of Repair vs. Capitalization

• 2004: Advance no-ce of proposed rulemaking • 2006: Proposed regula-ons – amendments proposed under §263(a) • 2008: Earlier (2006) regula-ons withdrawn, new regula-ons

proposed • 2011: New temporary regula-ons put forth, effec-ve tax years 2012-‐

beyond • 2012: Addi-onal guidance issued (Revenue Procedures 2012-‐19 and

2012-‐20)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

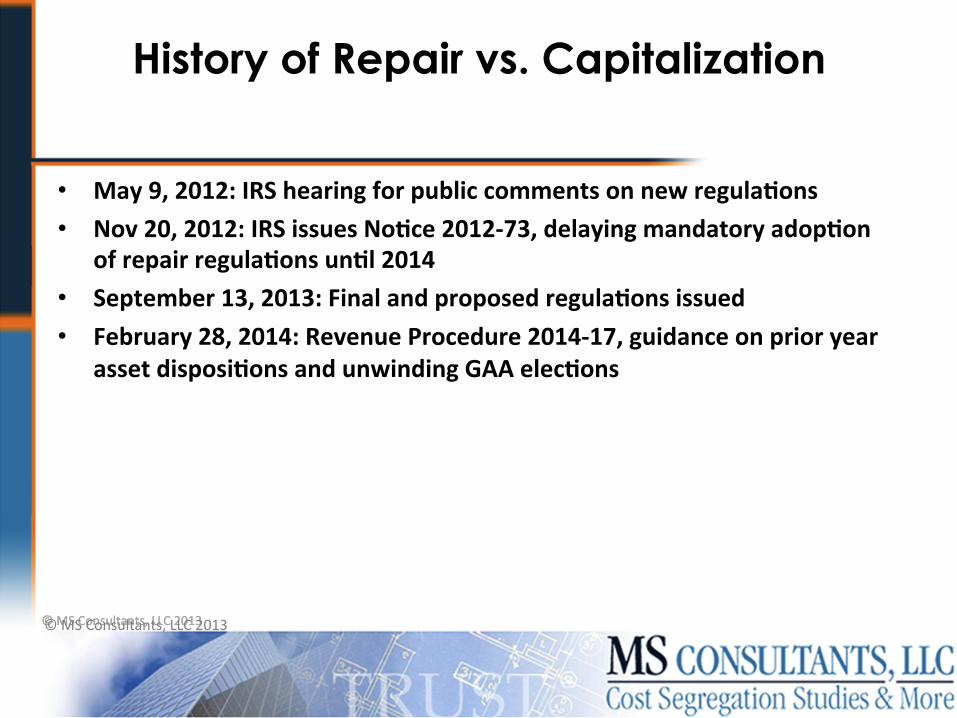

History of Repair vs. Capitalization

• May 9, 2012: IRS hearing for public comments on new regula-ons • Nov 20, 2012: IRS issues No-ce 2012-‐73, delaying mandatory adop-on

of repair regula-ons un-l 2014 • September 13, 2013: Final and proposed regula-ons issued • February 28, 2014: Revenue Procedure 2014-‐17, guidance on prior year

asset disposi-ons and unwinding GAA elec-ons

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

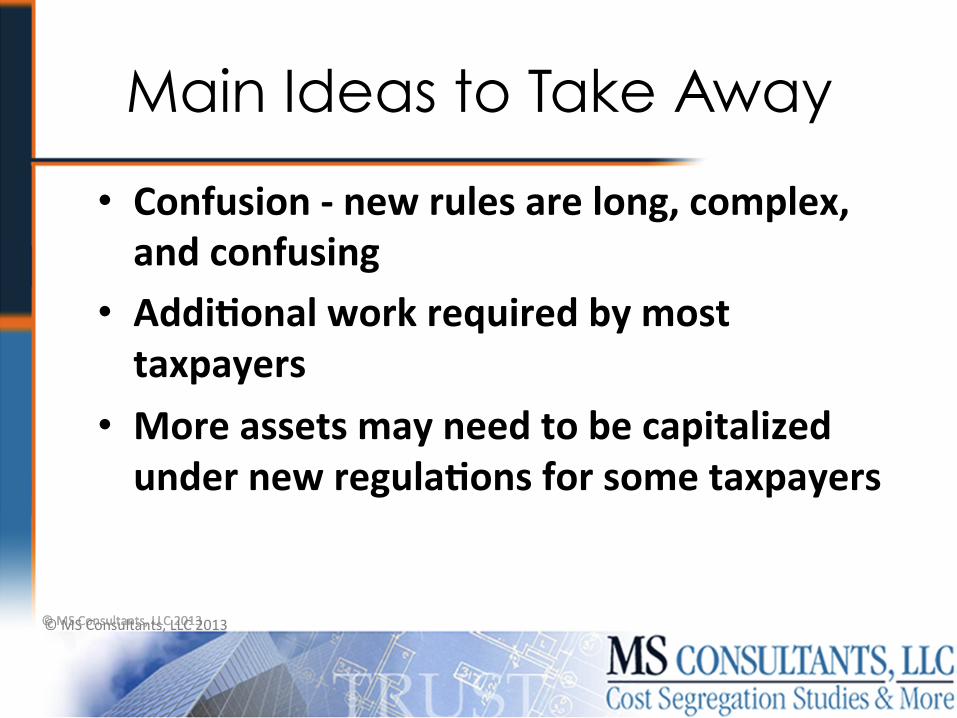

Main Ideas to Take Away

• Confusion -‐ new rules are long, complex, and confusing

• Addi-onal work required by most taxpayers

• More assets may need to be capitalized under new regula-ons for some taxpayers

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

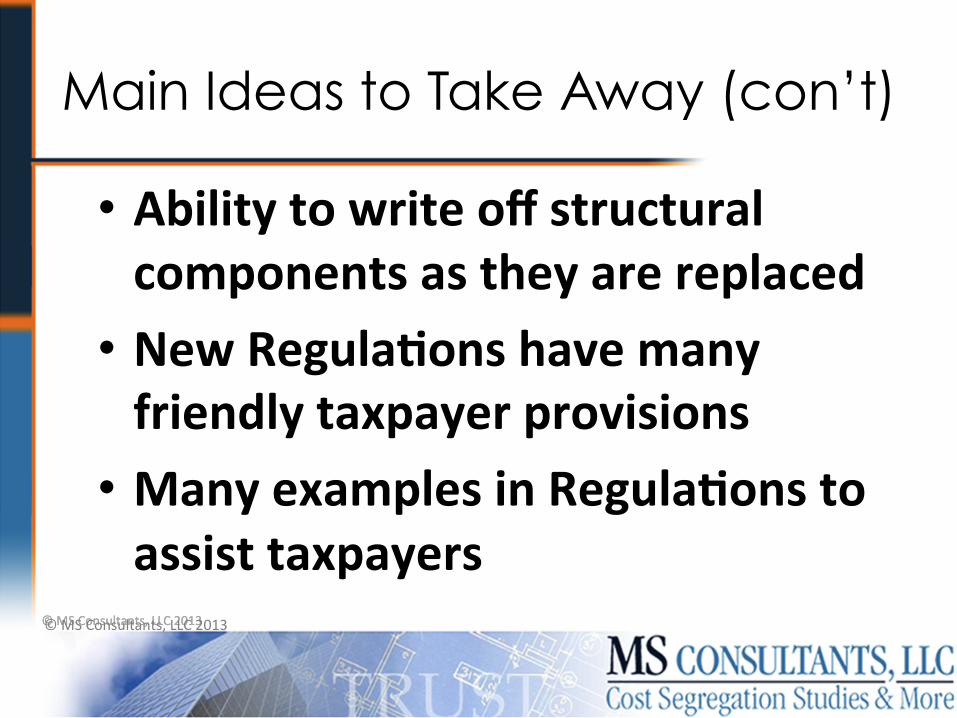

Main Ideas to Take Away (con’t)

• Ability to write off structural components as they are replaced

• New Regula-ons have many friendly taxpayer provisions

• Many examples in Regula-ons to assist taxpayers

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

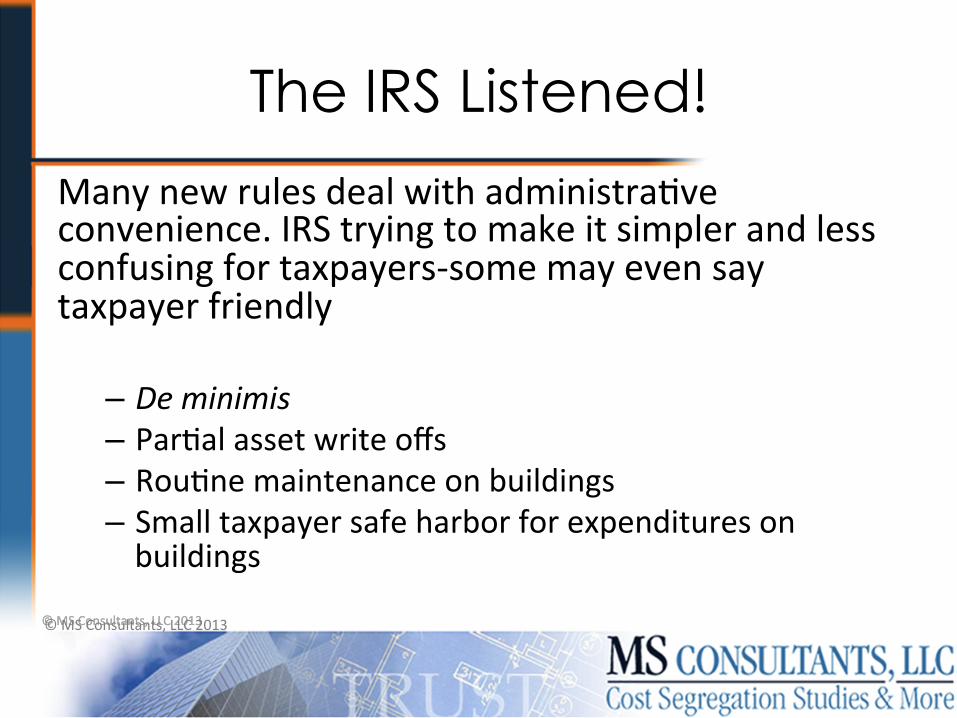

The IRS Listened!

Many new rules deal with administraEve convenience. IRS trying to make it simpler and less confusing for taxpayers-‐some may even say taxpayer friendly

– De minimis – ParEal asset write offs – RouEne maintenance on buildings – Small taxpayer safe harbor for expenditures on buildings

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Transition Rules

• TransiEon Rules – UElize temporary regulaEons for 2012 and 2013-‐Only do when favorable

– Adopt Final regs retroacEvely to 2012 and 2013 – Mandatory use for tax years beginning 1/1/2014 – Allows for amending returns and 3115 filings

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

There is work to be done…

– Form 3115 filings – Annual elecEons – WriCen capitalizaEon policy – Annual review of repair vs capitalizaEon items – New UOP classificaEons on depreciaEon schedules

– Billing opportuniEes? © MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Taxpayer Benefits

• Safe harbor elecEons and de minimis rules provide addiEonal write-‐off opportuniEes

• “Free” immediate tax deducEons for wriEng off improperly capitalized assets. Includes repair items and structural components

• Removing replaced assets off depreciaEon schedules will reduce depreciaEon recapture in the future.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

The Impact of Doing Nothing!

• Trapped double or triple assets on the depreciaEon schedules

• Future disallowed depreciaEon for – Incorrect asset classes – Incorrect bonus elecEons

• Clients will pay more taxes.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Common elections under the new rules

• De minimus Safe Harbor-‐annually • RouEne Maintenance Safe Harbor-‐annually • Small Business Safe Harbor-‐annually if applicable

• ParEal asset disposiEon-‐in year of replacement

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Common 3115 filings

• Fix bonus elecEon problems • Write-‐off prior improperly capitalized repairs • Write-‐off replaced structural components sEll being depreciated.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Repair vs. Capitalization

Let’s go back to the old rules.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

The Old Rules-What is Capitalized?

• You are required to capitalize expenditures that: • Materially increase the value of the property • SubstanEally prolong the useful life of the property or

• Adapt the property to a new or different use Excerpted from Reg. 1.263(a)-‐1(b)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

The Old Rules, con’t

“The cost of incidental repairs which neither materially add to the value of the property nor appreciably prolong its life, but keep it in an ordinarily efficient operaEng condiEon, may be deducted as an expense . . . Repairs in the nature of replacements, to the extent that they arrest deterioraEon and appreciably prolong the life of the property, shall . . . be capitalized and depreciated.”

Reg. 1.162 -‐4

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

“Some items are clearly capital and other items are clearly expense, but between the two extremes a point is approached at which it is difficult to determine whether the expenditure is

capital or expense”

-‐ Libby & Blouin, LTD., 4 BTA 910 (1926)

The Old rules

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

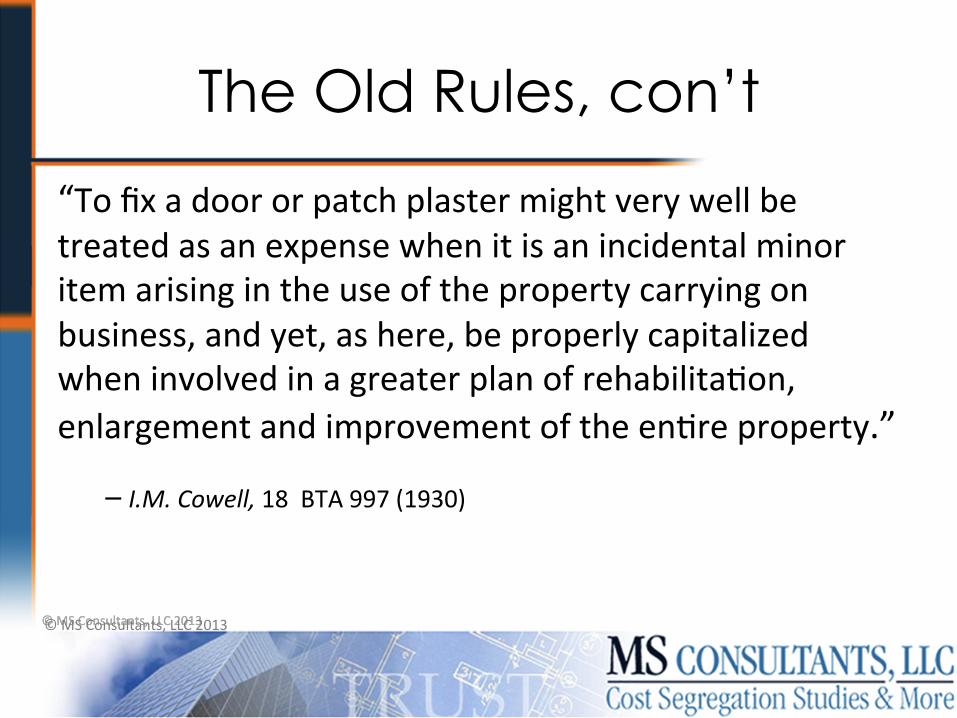

The Old Rules, con’t

“To fix a door or patch plaster might very well be treated as an expense when it is an incidental minor item arising in the use of the property carrying on business, and yet, as here, be properly capitalized when involved in a greater plan of rehabilitaEon, enlargement and improvement of the enEre property.”

– I.M. Cowell, 18 BTA 997 (1930)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

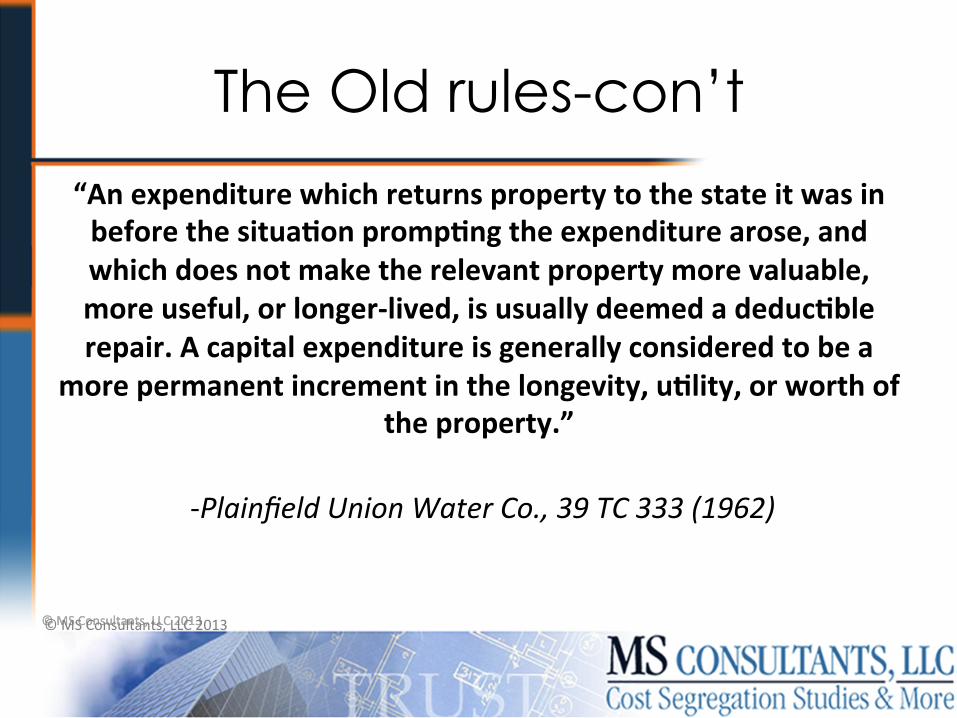

The Old rules-con’t

“An expenditure which returns property to the state it was in before the situa-on promp-ng the expenditure arose, and which does not make the relevant property more valuable, more useful, or longer-‐lived, is usually deemed a deduc-ble repair. A capital expenditure is generally considered to be a

more permanent increment in the longevity, u-lity, or worth of the property.”

-‐Plainfield Union Water Co., 39 TC 333 (1962)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

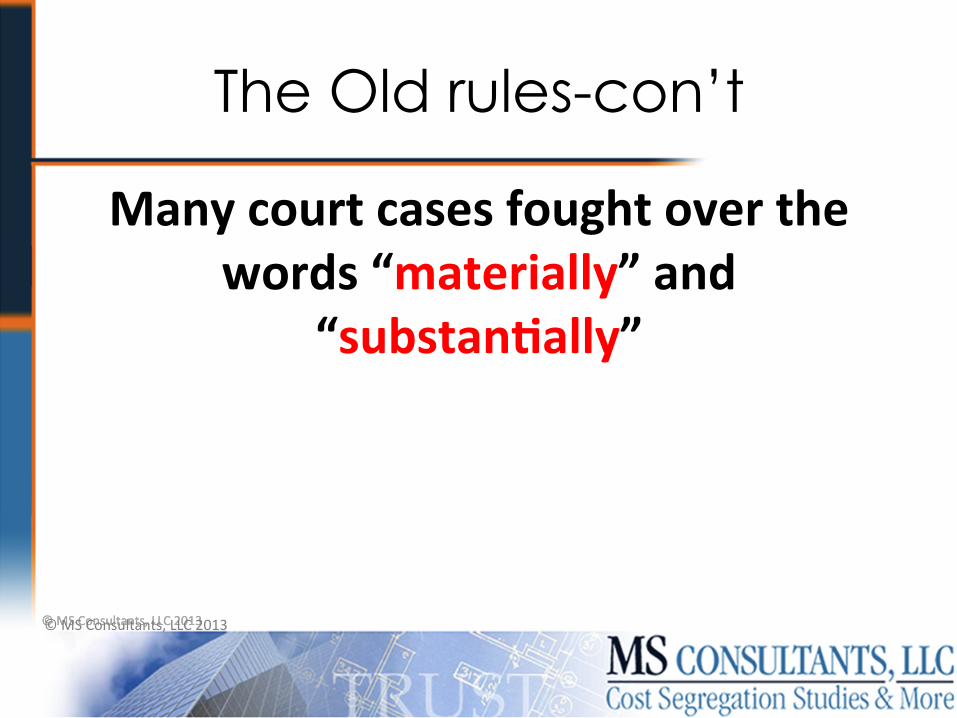

The Old rules-con’t

Many court cases fought over the words “materially” and

“substan-ally”

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

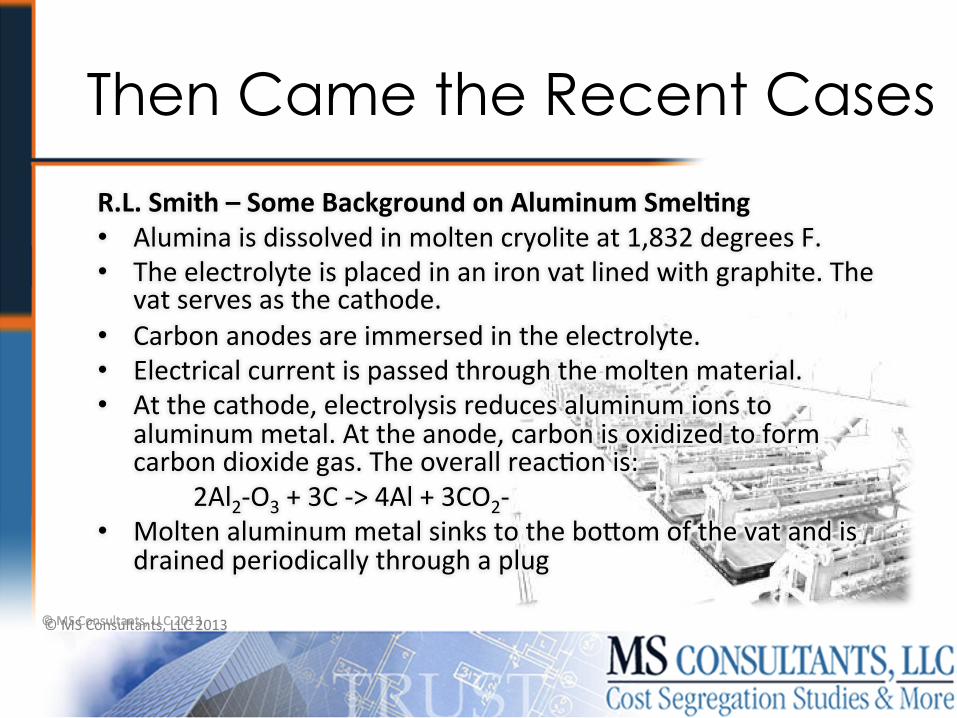

Then Came the Recent Cases

R.L. Smith – Some Background on Aluminum Smel-ng • Alumina is dissolved in molten cryolite at 1,832 degrees F. • The electrolyte is placed in an iron vat lined with graphite. The

vat serves as the cathode. • Carbon anodes are immersed in the electrolyte. • Electrical current is passed through the molten material. • At the cathode, electrolysis reduces aluminum ions to

aluminum metal. At the anode, carbon is oxidized to form carbon dioxide gas. The overall reacEon is:

2Al2-‐O3 + 3C -‐> 4Al + 3CO2-‐ • Molten aluminum metal sinks to the boCom of the vat and is

drained periodically through a plug

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

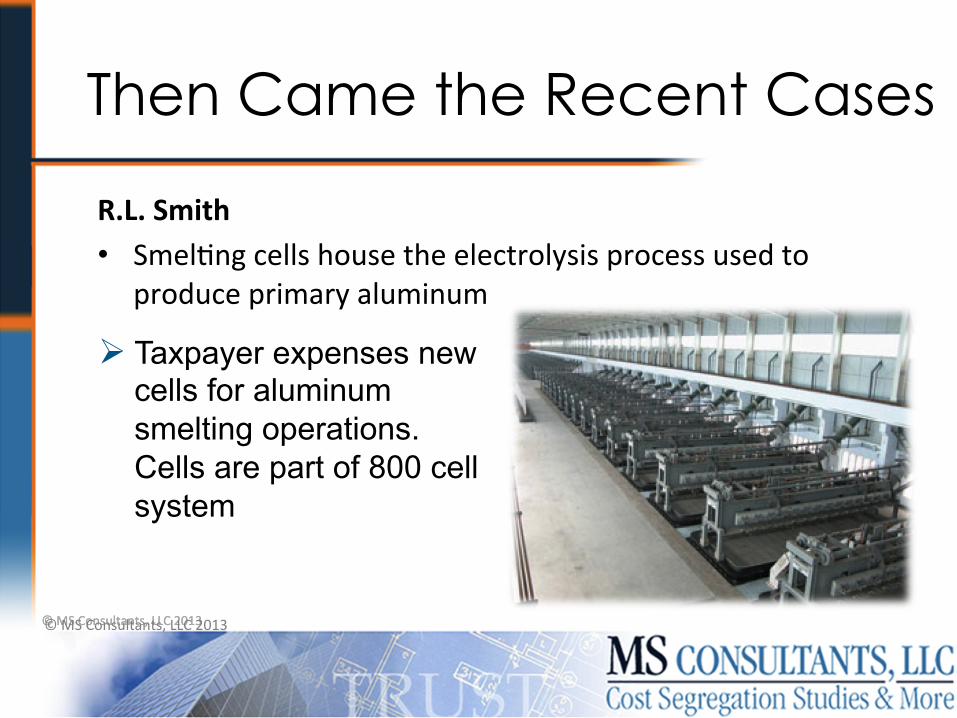

Then Came the Recent Cases

R.L. Smith • SmelEng cells house the electrolysis process used to

produce primary aluminum

Ø Taxpayer expenses new cells for aluminum smelting operations. Cells are part of 800 cell system

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Recent Court Cases, con’t

R.L. Smith

• IRS wins -‐ each cell is unit of property • Taxpayer argued that each cell was part of a larger system

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

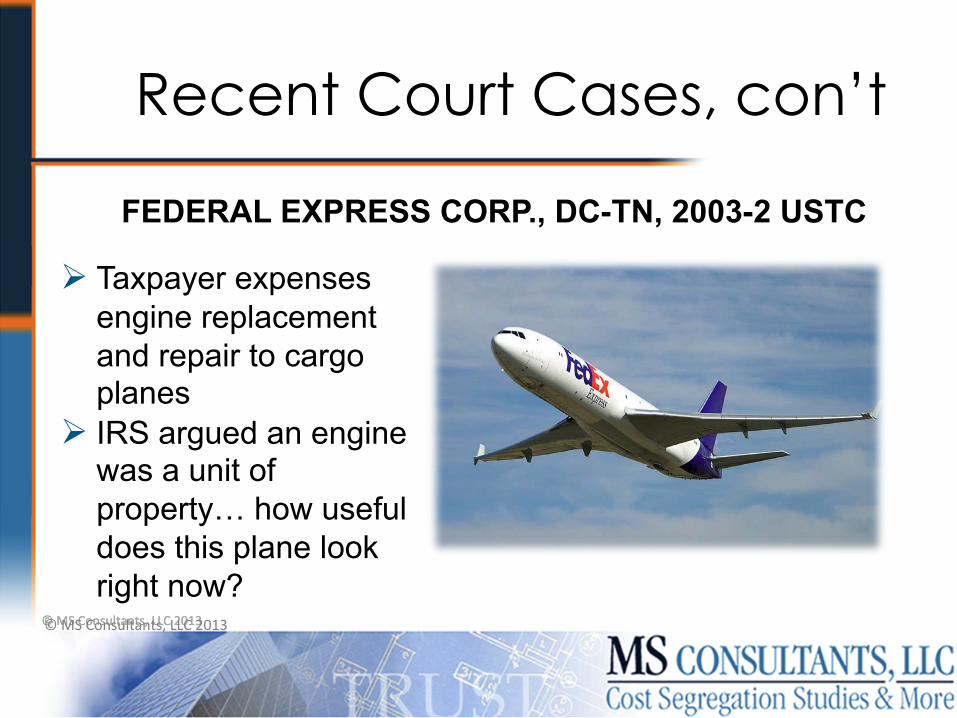

Ø IRS argued an engine was a unit of property… how useful does this plane look right now?

FEDERAL EXPRESS CORP., DC-TN, 2003-2 USTC

Recent Court Cases, con’t

Ø Taxpayer expenses

engine replacement and repair to cargo planes

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

FEDERAL EXPRESS CORP., DC-TN, 2003-2 USTC

Recent Court Cases, con’t

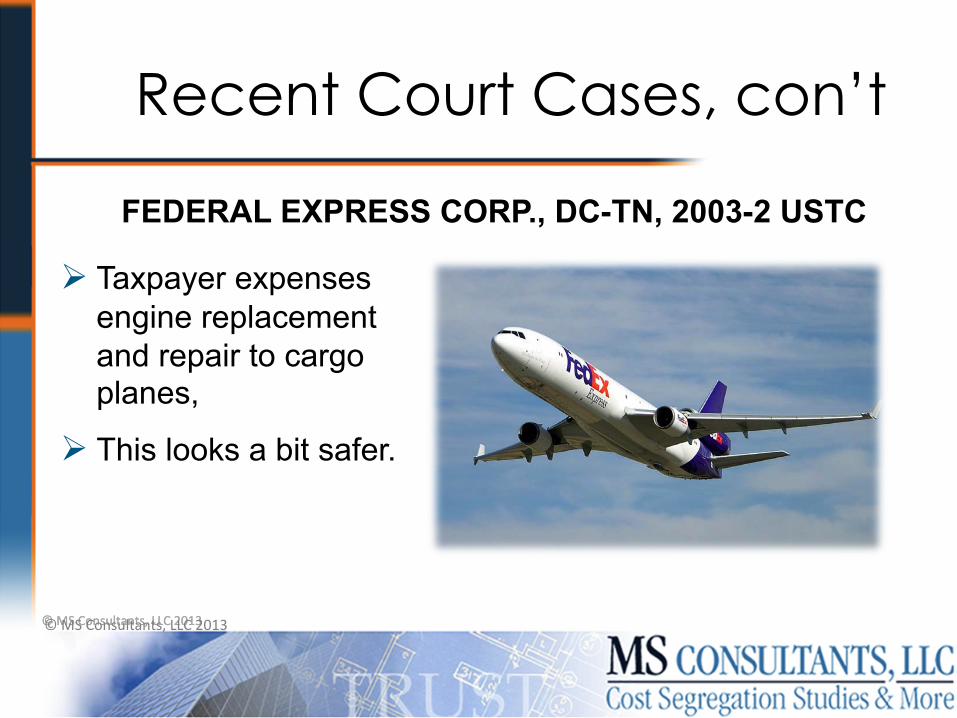

Ø Taxpayer expenses

engine replacement and repair to cargo planes,

Ø This looks a bit safer.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Recent Court Cases, con’t

FEDERAL EXPRESS CORP., DC-TN, 2003-2 USTC

Ø Taxpayer wins – plane is unit of property Ø IRS argued that engines were unit of

property

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

The New Regulations

• The standards for applying §263(a), as set forth in the regulaEons, case law, and administraEve guidance, are difficult to discern and apply in pracEce and have led to considerable controversy for taxpayers or so says the AICPA.

• EffecEve for tax years beginning in 2014 – taxpayers must comply.

• To comply with the new rules – many taxpayers will need to file Form 3115 “Change in AccounEng Method” or make annual elecEons.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

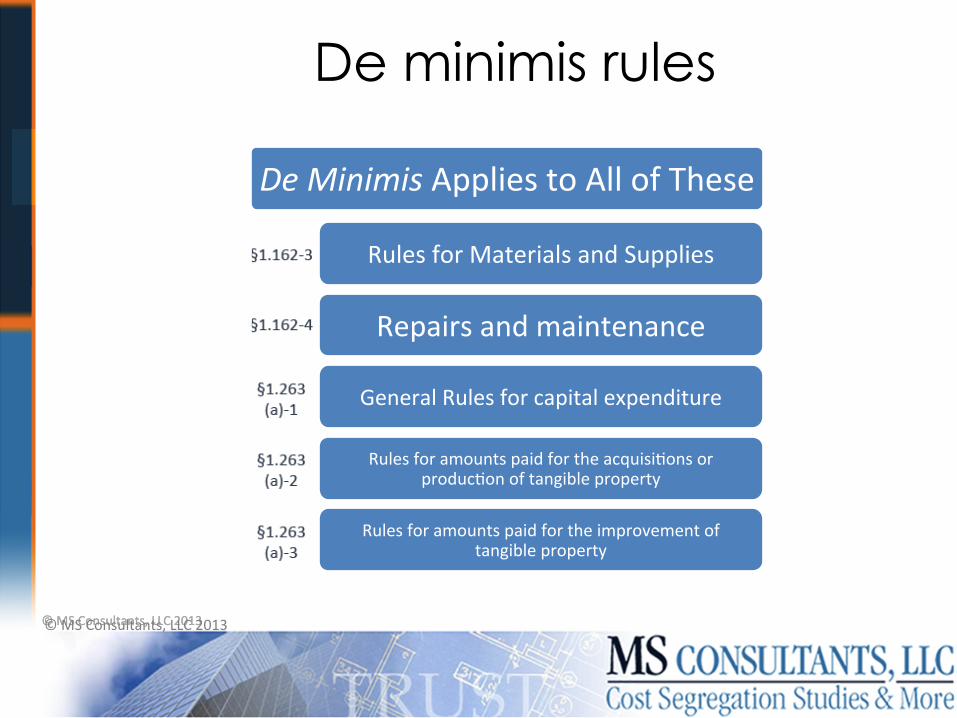

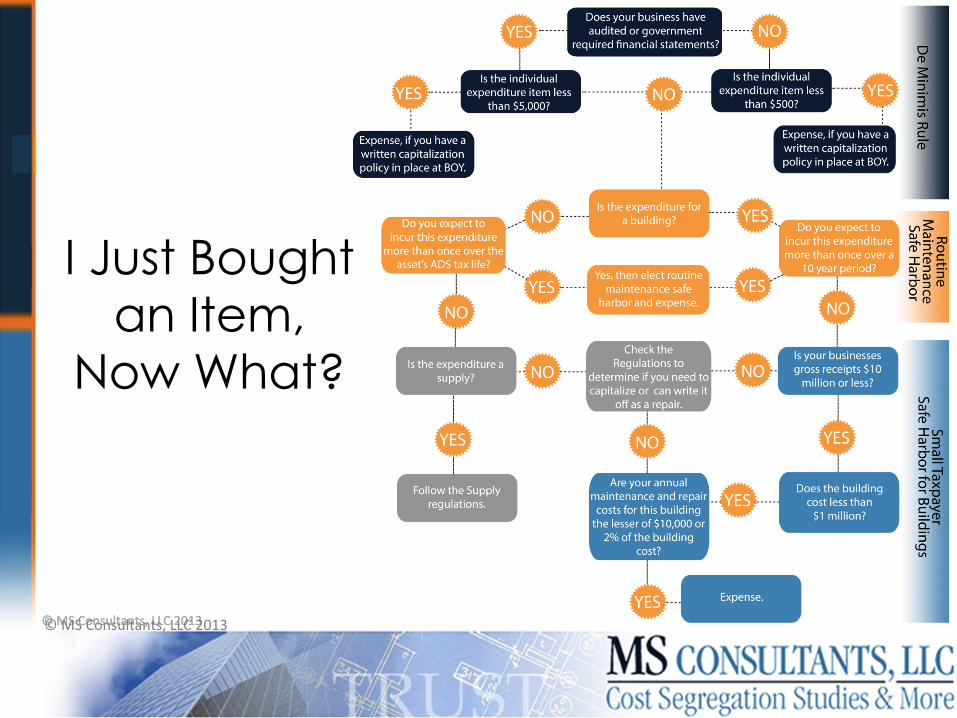

De Minimis Applies to All of These

Rules for Materials and Supplies

Repairs and maintenance

General Rules for capital expenditure

Rules for amounts paid for the acquisiEons or producEon of tangible property

Rules for amounts paid for the improvement of tangible property

De minimis rules

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

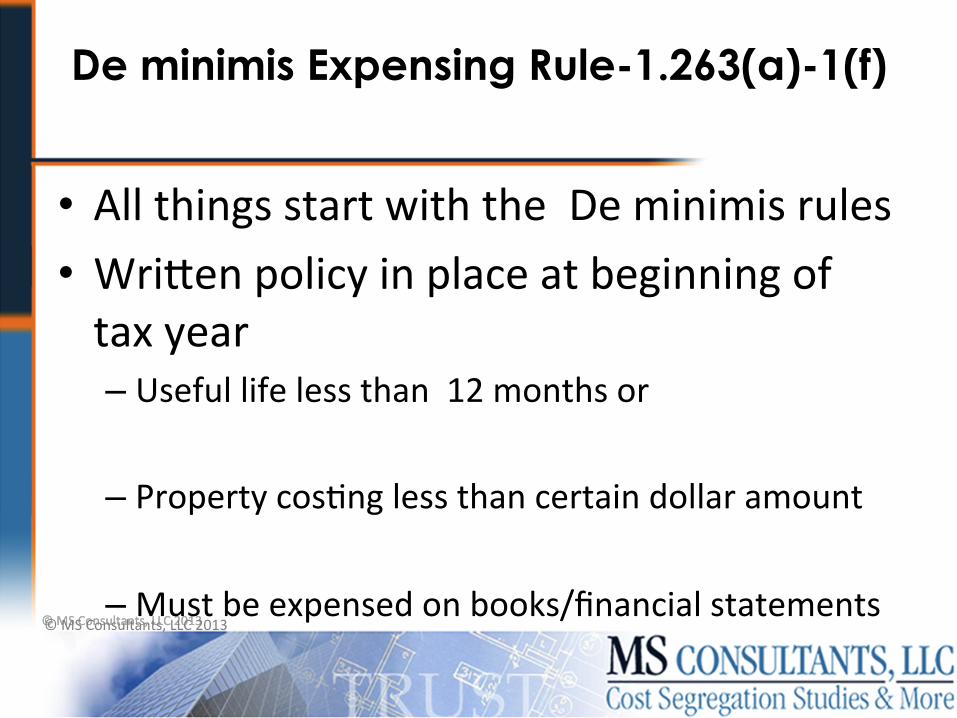

De minimis Expensing Rule-1.263(a)-1(f)

• All things start with the De minimis rules • WriCen policy in place at beginning of tax year – Useful life less than 12 months or

– Property cosEng less than certain dollar amount

– Must be expensed on books/financial statements © MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

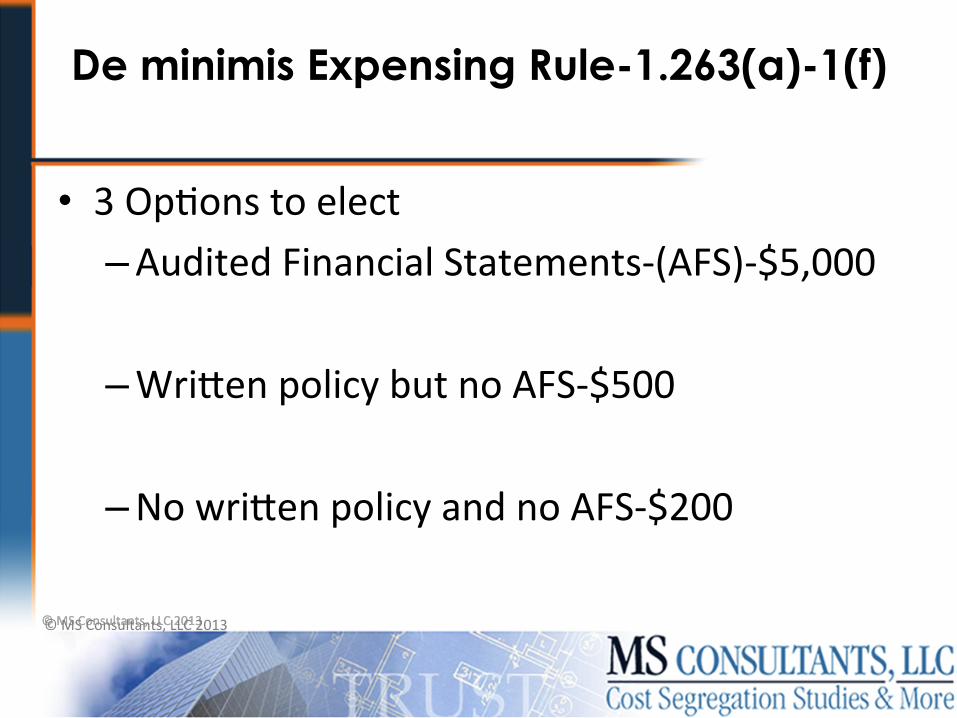

De minimis Expensing Rule-1.263(a)-1(f)

• 3 OpEons to elect – Audited Financial Statements-‐(AFS)-‐$5,000

– WriCen policy but no AFS-‐$500

– No wriCen policy and no AFS-‐$200

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

De minimis Expensing Rule-1.263(a)-1(f)

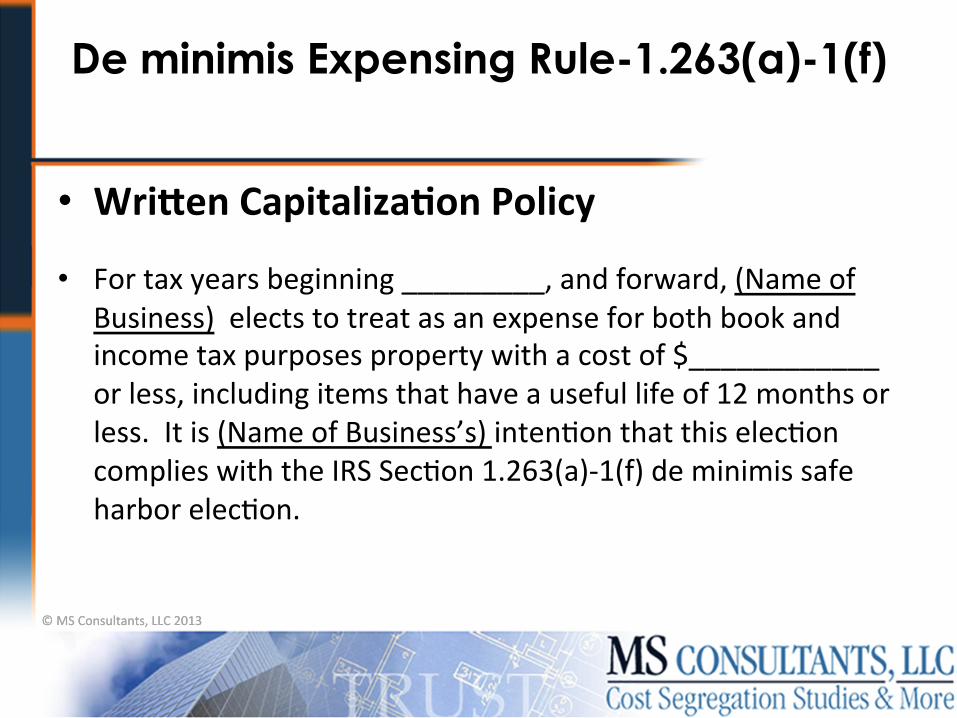

• Wriken Capitaliza-on Policy

• For tax years beginning _________, and forward, (Name of Business) elects to treat as an expense for both book and income tax purposes property with a cost of $____________ or less, including items that have a useful life of 12 months or less. It is (Name of Business’s) intenEon that this elecEon complies with the IRS SecEon 1.263(a)-‐1(f) de minimis safe harbor elecEon.

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

De minimis Expensing Rule-1.263(a)-1(f)

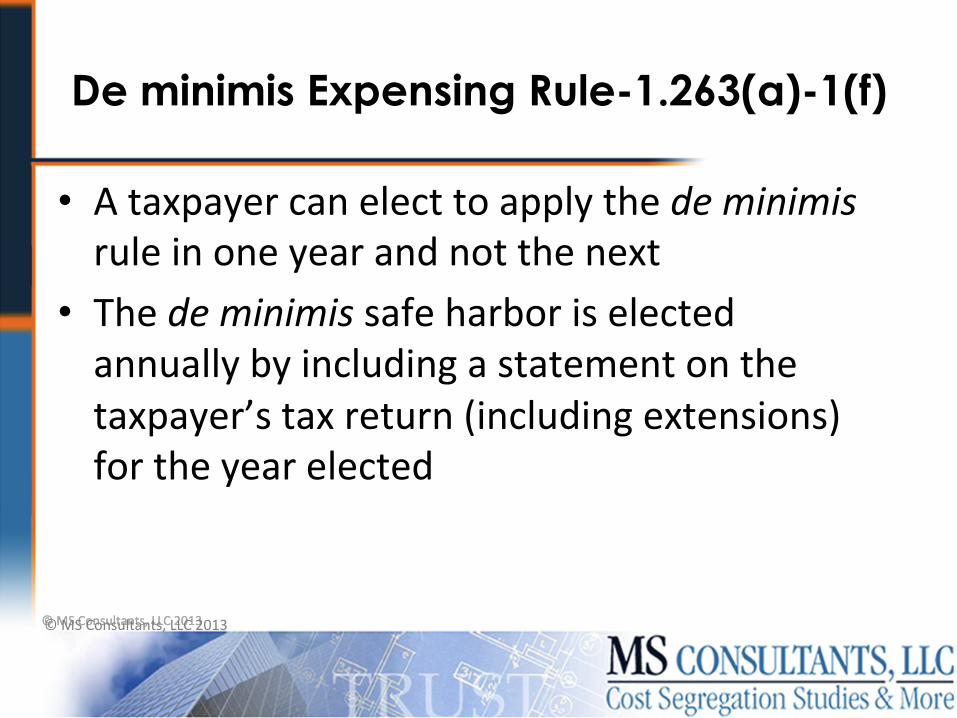

• A taxpayer can elect to apply the de minimis rule in one year and not the next

• The de minimis safe harbor is elected annually by including a statement on the taxpayer’s tax return (including extensions) for the year elected

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

De minimis Expensing Rule-1.263(a)-1(f)

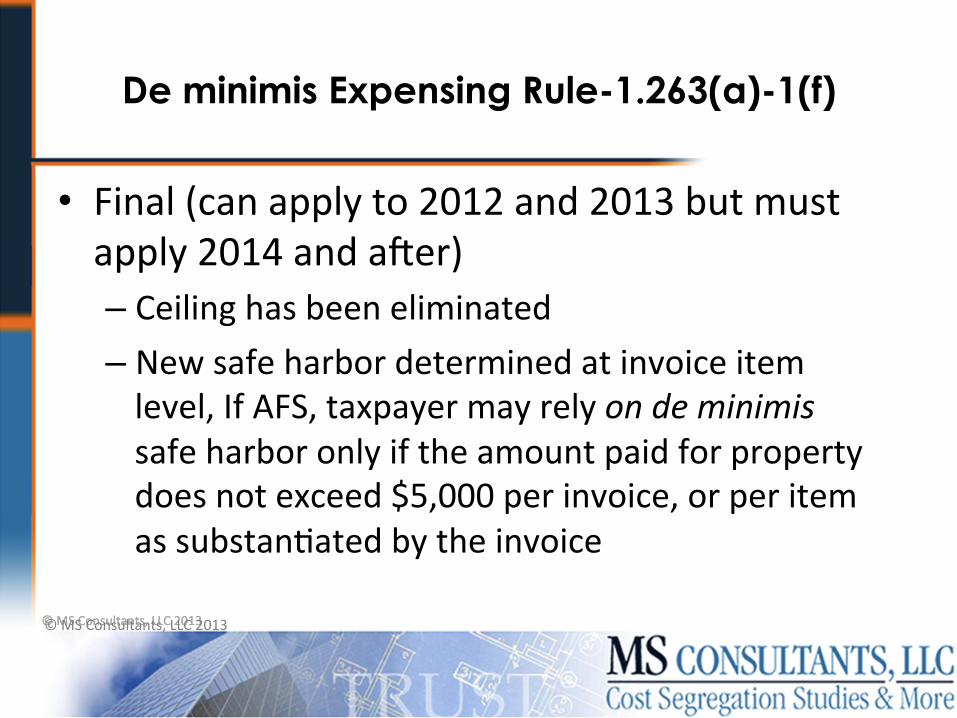

• Final (can apply to 2012 and 2013 but must apply 2014 and auer) – Ceiling has been eliminated – New safe harbor determined at invoice item level, If AFS, taxpayer may rely on de minimis safe harbor only if the amount paid for property does not exceed $5,000 per invoice, or per item as substanEated by the invoice

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

De minimis Expensing Rule-1.263(a)-1(f)

• The de minimis safe harbor does not preclude a taxpayer from reaching an agreement with the IRS that the IRS examining agents will not review certain items-‐same as Temporary regs

• Must apply same treatment to books and tax return

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

De minimis Expensing Rule-1.263(a)-1(f)

• A taxpayer is not required to include in the cost of the property the addiEonal costs if these costs are not included on the same invoice as the tangible property

• However, a taxpayer elecEng the de minimis must include in the cost of the property all addiEonal costs (for example, delivery fees, installaEon services, or similar costs) of acquiring or producing the property if these costs are included on the same invoice with the tangible property

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

De minimis Expensing Rule-1.263(a)-1(f)

• If an invoice includes amounts paid for mulEple tangible properEes and the invoice includes addiEonal invoice costs related to the mulEple properEes, then the taxpayer must allocate the addiEonal invoice costs to each property using a reasonable method

• The de minimis safe harbor must be applied to all eligible M & S (other than rotable, temporary, and standby emergency spare parts subject to the elecEon to capitalize or to rotable and temporary spare parts subject to the opEonal method of accounEng for such parts) if the taxpayer elects the de minimis safe harbor

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

De minimis Expensing Rule-1.263(a)-1(f)

• Taxpayers that do not elect the de minimis safe harbor must treat amounts paid for materials and supplies in accordance with Reg. §1.162-‐3

• Taxpayers subject to 263A can not avoid those provisions by using the de minimis

• Safe harbor does not apply to inventory, land, items it capitalizes, and the opEonal method of rotable parts

• Safe harbor is deducted as ordinary and necessary expense and no recapture on sale

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

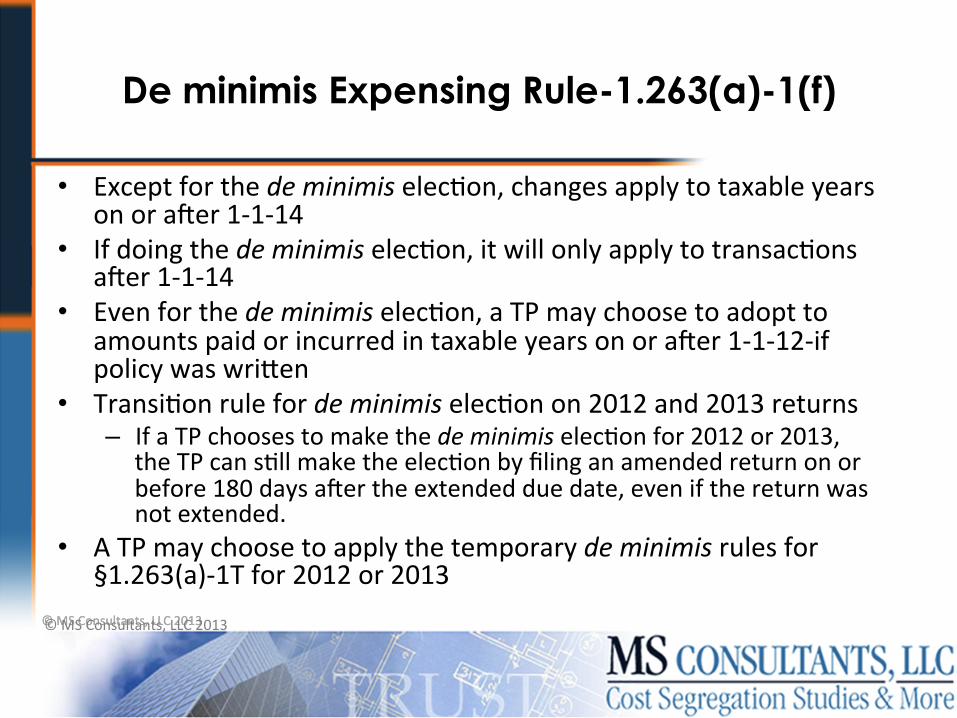

De minimis Expensing Rule-1.263(a)-1(f)

• Except for the de minimis elecEon, changes apply to taxable years on or auer 1-‐1-‐14

• If doing the de minimis elecEon, it will only apply to transacEons auer 1-‐1-‐14

• Even for the de minimis elecEon, a TP may choose to adopt to amounts paid or incurred in taxable years on or auer 1-‐1-‐12-‐if policy was wriCen

• TransiEon rule for de minimis elecEon on 2012 and 2013 returns – If a TP chooses to make the de minimis elecEon for 2012 or 2013,

the TP can sEll make the elecEon by filing an amended return on or before 180 days auer the extended due date, even if the return was not extended.

• A TP may choose to apply the temporary de minimis rules for §1.263(a)-‐1T for 2012 or 2013

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

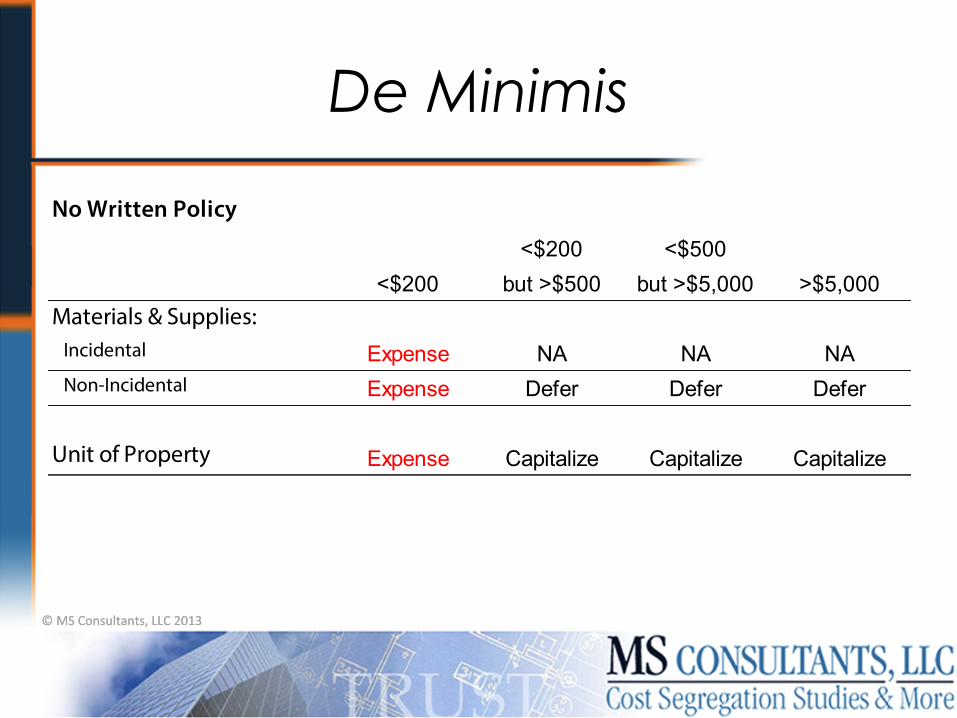

De Minimis

No Written Policy

<$200 <$500<$200 but >$500 but >$5,000 >$5,000

Materials & Supplies: Incidental Expense NA NA NA Non-Incidental Expense Defer Defer Defer

Unit of Property Expense Capitalize Capitalize Capitalize

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

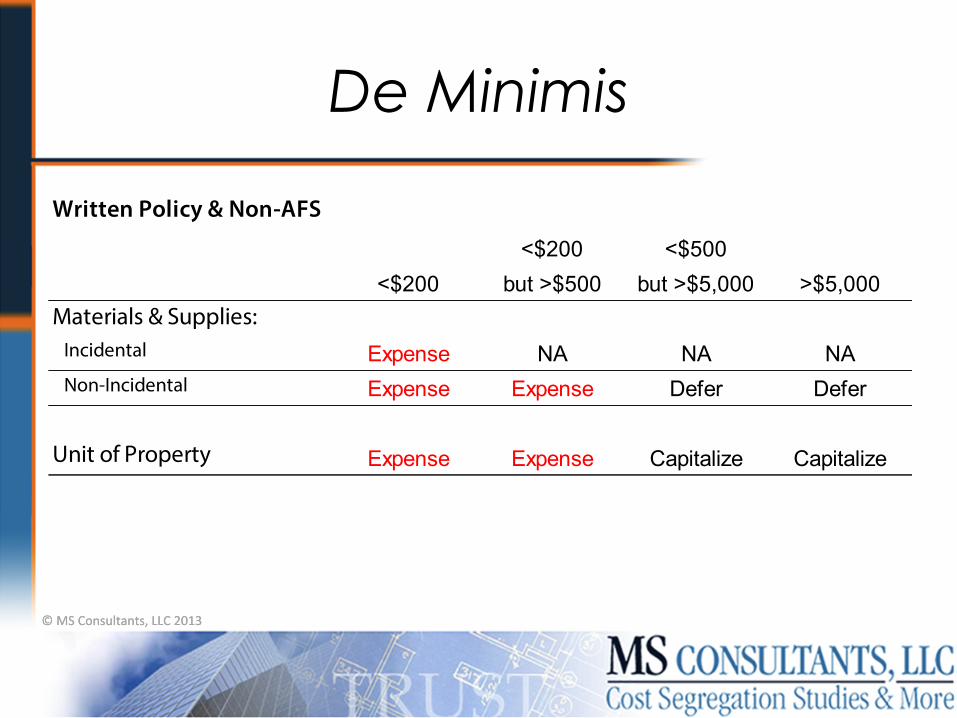

De Minimis

Written Policy & Non-AFS

<$200 <$500<$200 but >$500 but >$5,000 >$5,000

Materials & Supplies: Incidental Expense NA NA NA Non-Incidental Expense Expense Defer Defer

Unit of Property Expense Expense Capitalize Capitalize

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

De Minimis

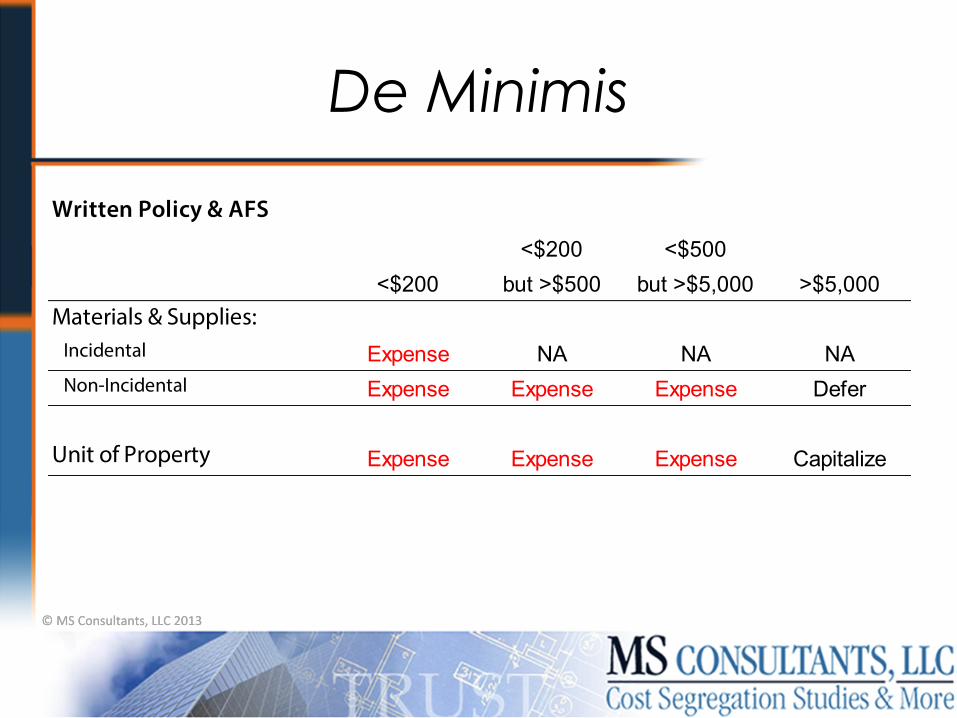

Written Policy & AFS

<$200 <$500<$200 but >$500 but >$5,000 >$5,000

Materials & Supplies: Incidental Expense NA NA NA Non-Incidental Expense Expense Expense Defer

Unit of Property Expense Expense Expense Capitalize

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

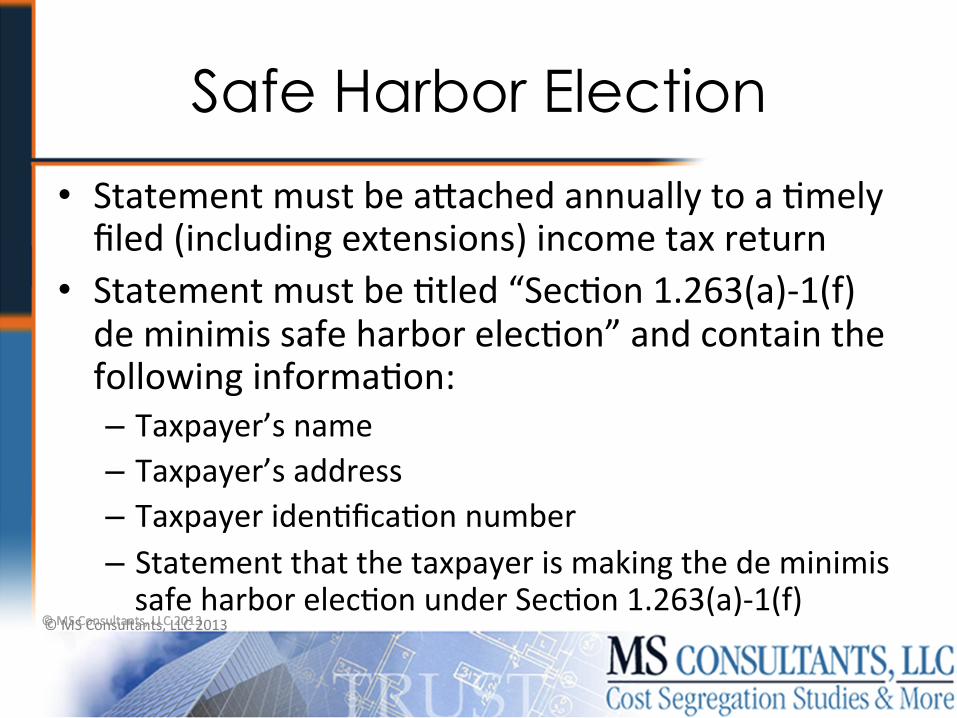

Safe Harbor Election

• Statement must be aCached annually to a Emely filed (including extensions) income tax return

• Statement must be Etled “SecEon 1.263(a)-‐1(f) de minimis safe harbor elecEon” and contain the following informaEon: – Taxpayer’s name – Taxpayer’s address – Taxpayer idenEficaEon number – Statement that the taxpayer is making the de minimis safe harbor elecEon under SecEon 1.263(a)-‐1(f)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

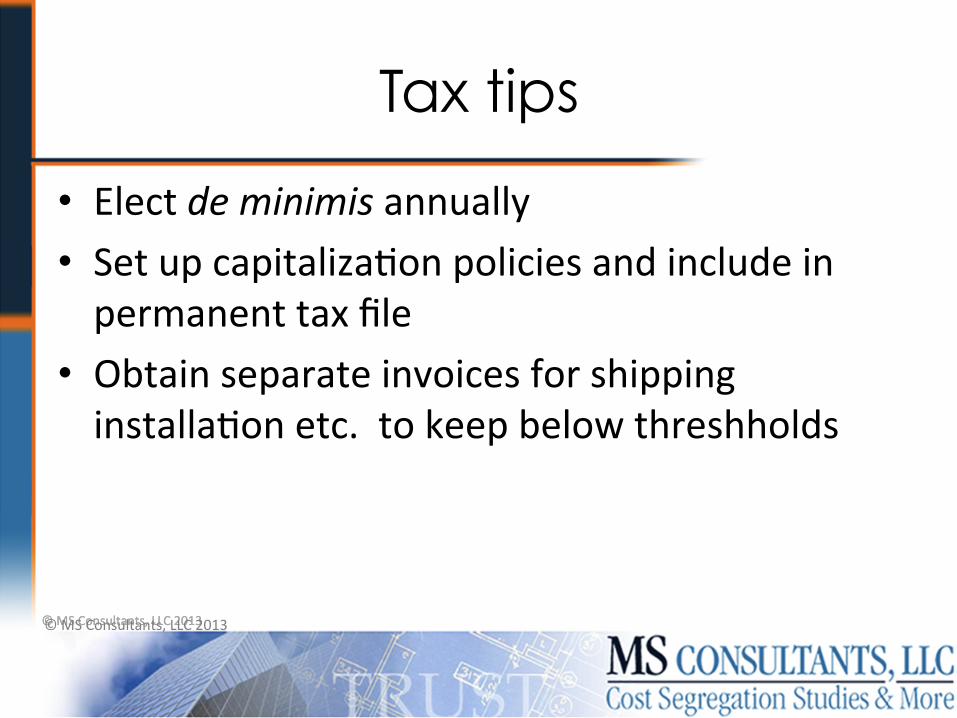

Tax tips

• Elect de minimis annually • Set up capitalizaEon policies and include in permanent tax file

• Obtain separate invoices for shipping installaEon etc. to keep below threshholds

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

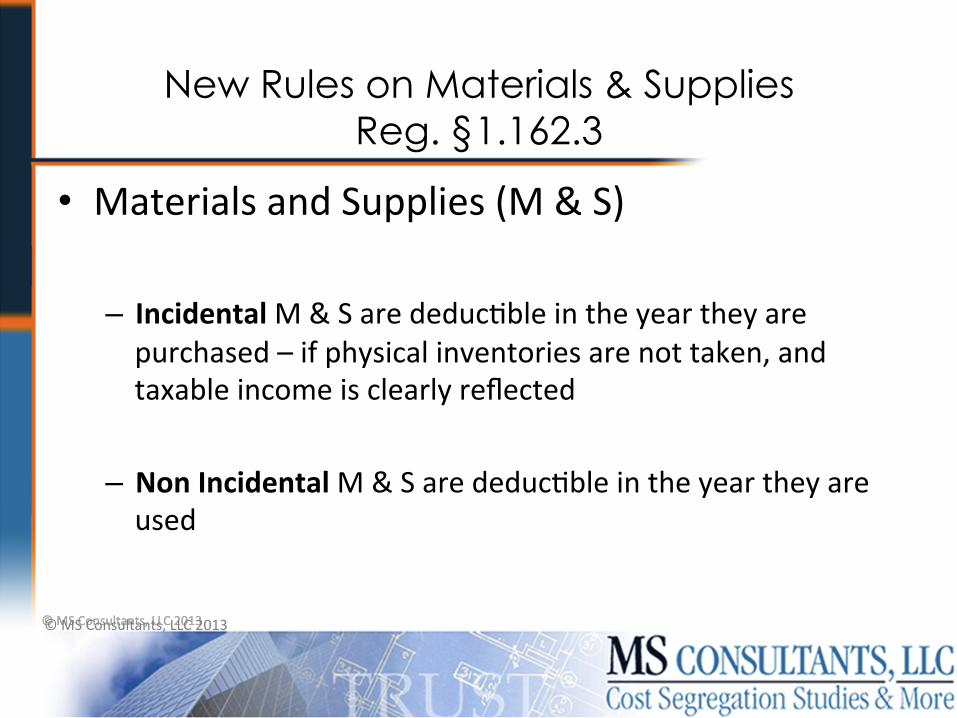

New Rules on Materials & Supplies Reg. §1.162.3

• Materials and Supplies (M & S)

– Incidental M & S are deducEble in the year they are purchased – if physical inventories are not taken, and taxable income is clearly reflected

– Non Incidental M & S are deducEble in the year they are used

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

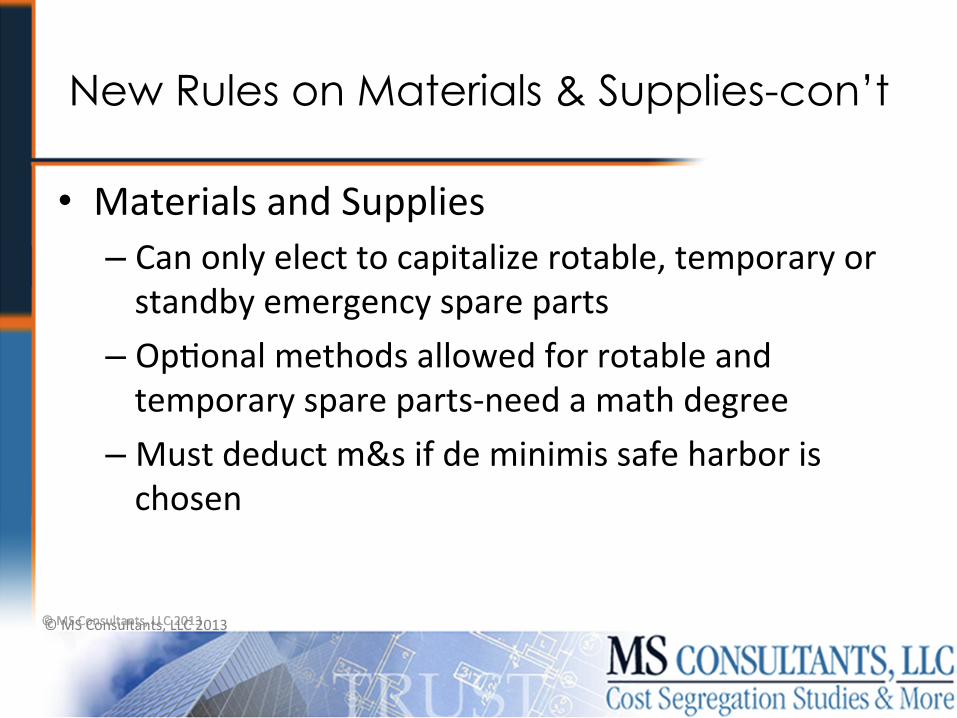

New Rules on Materials & Supplies-con’t

• Materials and Supplies – Can only elect to capitalize rotable, temporary or standby emergency spare parts

– OpEonal methods allowed for rotable and temporary spare parts-‐need a math degree

– Must deduct m&s if de minimis safe harbor is chosen

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Materials and Supplies Reg. §1.162-3

• If a taxpayer chooses to make the elecEon to capitalize and depreciate certain M & S for its tax year 2013, the taxpayer can sEll make the elecEon by filing an amended return on or before 180 days auer the extended due date, even if the return was not extended

• A taxpayer may choose to apply the temporary M & S rules for §1.162-‐3T for 2013

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Material & Supplies-example

• TP purchases a number of small individual items to rent to customers and maintains a supply of these items on hand

• In year one, TP purchases a large quanEty of items, all cosEng less than $300 each

• In year two, TP begins using the rental items in its business

• The rental items are M & S • The amounts paid in year one are deducEble in year

two

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Tax Tip

• You can only deduct non-‐incidental M&S when purchased if de minimus elecEon is made. Otherwise, deducEon is taken when M&S is used.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property (UOP)

• Building and its structural components are a single UOP

– The regulaEons define the building structure as the building (as defined in §1.48-‐1(e)(1)) and its structural components (as defined in §1.48-‐1(e)(2)) other than the components specifically enumerated as building systems.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property (UOP)

• UOP for buildings. In general, each building and its structural components is a UOP — “the building” and the improvement standards are applied at the building & building system level.

• Amounts are treated as paid for an improvement to a building if they improve: (1) the building structure; or (2) any designated building system.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

• This new term consists of the following nine structural components. Each of them (including their sub-‐components) is a building system that is separate from the building structure, and to which the improvement rules must be separately applied:

At the end of the day you end up with • Building structure: roof, walls, floors, windows, doors, etc.

and • 9 Building Systems

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property (UOP)

HVAC SYSTEM HeaEng VenElaEon & Air CondiEoning

PLUMBING SYSTEM Interior & exterior, incl. water, storm & sewer

ELECTRICAL SYSTEM Interior & exterior, incl. fixtures, wiring & distribuEon

ESCALATORS

FIRE PROTECTION SYSTEM Including sprinklers & alarms

SECURITY SYSTEM For protecEon of building & occupants

ELEVATORS

GAS DISTRIBUTION SYSTEM Interior & exterior

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

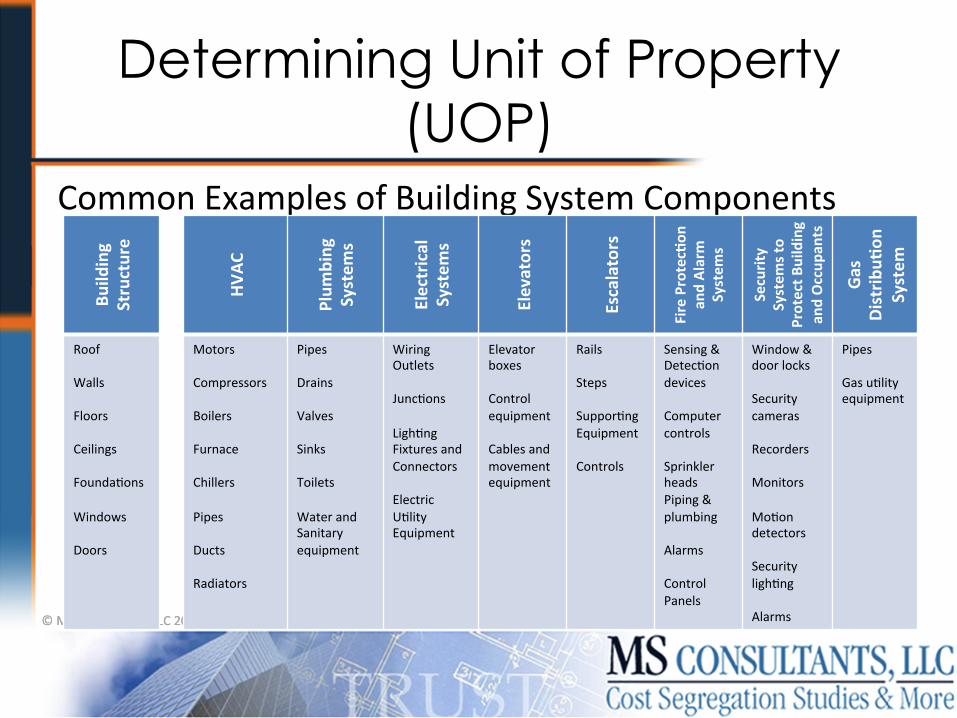

Determining Unit of Property(UOP)

Common Examples of Building System Components

Build

ing

Structure

HVAC

Plum

bing

System

s

Electrical

System

s

Elevators

Escalators

Fire Protec-on

an

d Alarm

System

s

Security

System

s to

Protect B

uilding

and Occup

ants

Gas

Distrib

u-on

System

Roof Walls Floors Ceilings FoundaEons Windows Doors

Motors Compressors Boilers Furnace Chillers Pipes Ducts Radiators

Pipes Drains Valves Sinks Toilets Water and Sanitary equipment

Wiring Outlets JuncEons LighEng Fixtures and Connectors Electric UElity Equipment

Elevator boxes Control equipment Cables and movement equipment

Rails Steps SupporEng Equipment Controls

Sensing & DetecEon devices Computer controls Sprinkler heads Piping & plumbing Alarms Control Panels

Window & door locks Security cameras Recorders Monitors MoEon detectors Security lighEng Alarms

Pipes Gas uElity equipment

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

• Example: Replacement of major component or substanEal structural part; elevator. – Taxpayer owns a $10M building that is used to operate its business,

and pays $50,000 to repair an elevator in the building. If the amount paid results in a restoraEon of the building structure or any building system, the taxpayer must treat the amount as an improvement to the building. The elevator is a building system and is valued at $200,000.

• Result = Costs are CAPITALIZED (the elevator system is the unit of property.)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

• Example: Not replacement of major component or substanEal structural part; plumbing system. – Taxpayer owns a building in which it conducts a retail business. The retail

building has three floors. The retail building has men's and women's restrooms on two of the three floors. X only pays an amount to replace three of the twenty sinks located in the various restrooms because these sinks had cracked. The three replaced sinks, by themselves, do not comprise a large porEon of the physical structure of the plumbing system nor do they perform a discrete and criEcal funcEon in the operaEon of the plumbing system.

• Result = Costs are EXPENSED (the sinks do not consEtute a major component or substanEal structural part of the building system)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

• UOP for leased property. Each building and its structural components(Landlord or Lessor) or the porEon of the building subject to a lease and the structural components associated with the leased space(Lessee or Tenant)

• Improvement standards are applied at the leased porEon of the building and building systems subject to the lease.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

UOP in Leased Buildings • Lessor incurs cost for tenant improvements

– The costs are included in UOP of the building

• Lessee incurs costs for tenant improvements – The costs are the UOP of the leased space, not of the enEre building.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

• Example: – Tenant wants a new HVAC unit and leases 10% of the space. There

are 12 HVAC units on the building. • If tenant pays, tenant must capitalize • If landlord pays, costs can be expensed • Note: This could impact common area maintenance charges(CAM)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

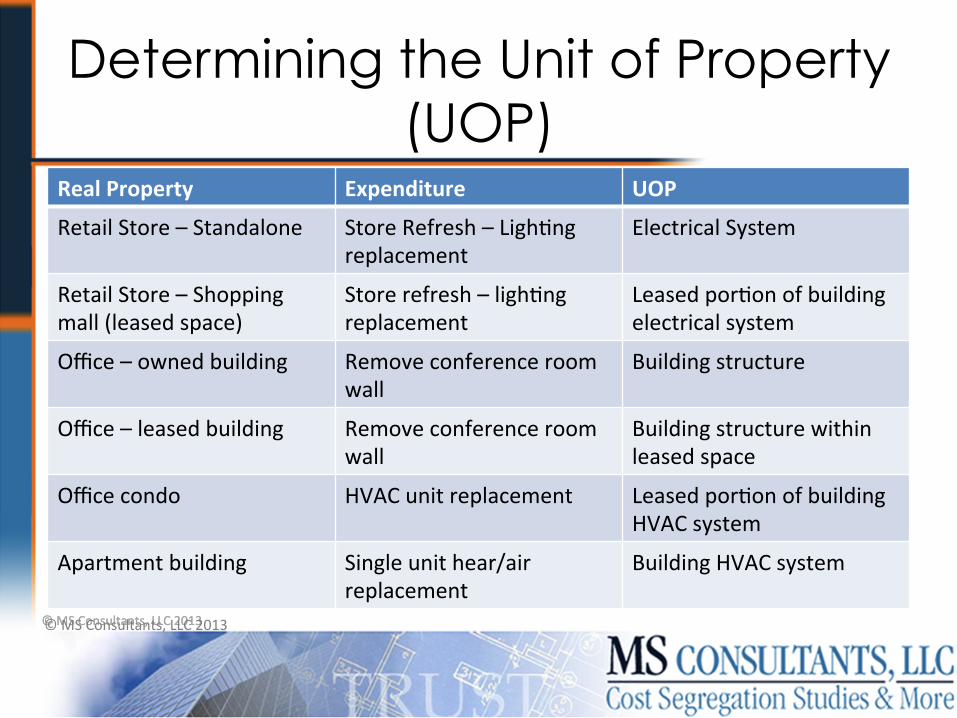

Determining the Unit of Property(UOP)

Real Property Expenditure UOP

Retail Store – Standalone Store Refresh – LighEng replacement

Electrical System

Retail Store – Shopping mall (leased space)

Store refresh – lighEng replacement

Leased porEon of building electrical system

Office – owned building Remove conference room wall

Building structure

Office – leased building Remove conference room wall

Building structure within leased space

Office condo HVAC unit replacement Leased porEon of building HVAC system

Apartment building Single unit hear/air replacement

Building HVAC system

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

• UOP for assets other than buildings. In general, for real or personal property that isn't classified as a building by the temp regs. all the components that are funcEonally interdependent comprise a single UOP. Components of property are funcEonally interdependent if the placing in service of one component by the taxpayer is dependent on the placing in service of the other component by the taxpayer.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

• UOP for Plant property.— FuncEonal interdependence test is used to determine UOP

• Discreet and major funcEon standard must be applied. • Each machine is typically treated as it own UOP • Applies to manufacturing, power generaEon, distribuEon and

warehousing

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Determining the Unit of Property(UOP)

• UOP for personal property.— FuncEonal interdependence test is used to determine UOP.

• CapitalizaEon depends on facts and circumstances

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Tax tips

• Set up assets on depreciaEon schedules to comply with new UOP’s – Easier to idenEfy and write-‐off assets as they are replaced

– Gives basis in determining whether new expenditure should be capitalized

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

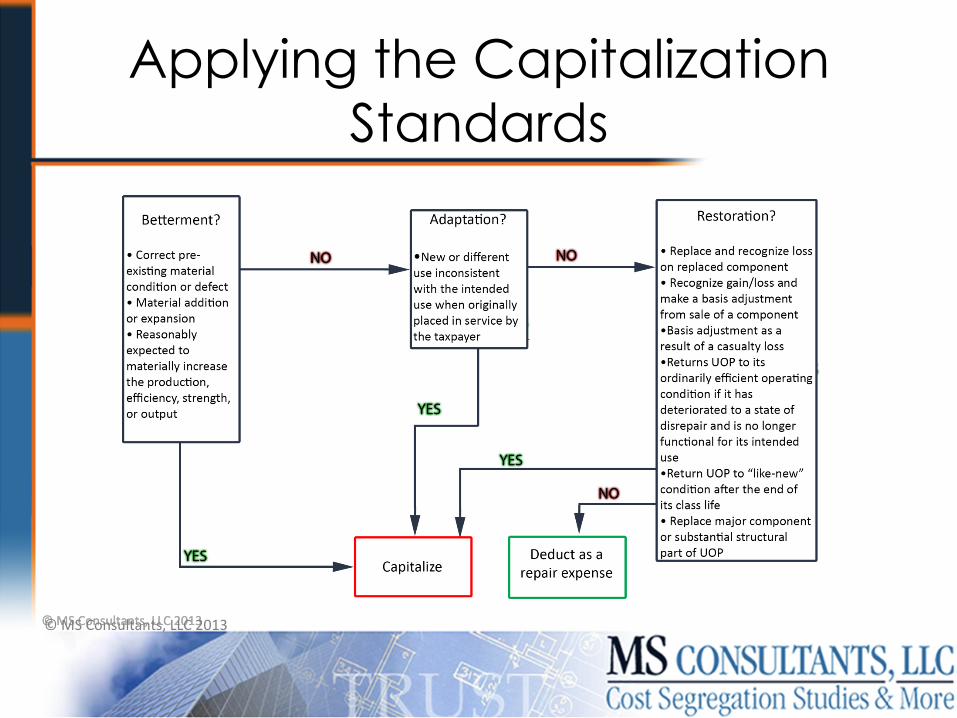

Applying the Capitalization standards: Reg. §1.263(a)-3

• BETTERMENT of the Unit of Property. Does it increase value? 19 examples in regs.

• ADAPTS the Unit of Property to a new or different use. Does it change use?

• RESTORATION of the Unit of Property. Does it increase life? 26 examples in regs.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

Old rules verse the new rules • OLD

• Materially increase the value of the property • Substan-ally prolong the useful life of the property or • Adapt the property to a new or different use

• New – BeCerment of unit of property – Adapt the property to new or different use – RestoraEon of unit of property

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

BETTERMENT of the Unit of Property • 1-‐ Ameliorate a material condiEon or defect that existed

prior to the acquisiEon of the property or arose during the producEon of the property;

• 2-‐ Material addiEon to the unit of property (including the physical enlargement, expansion, or extension);

• 3-‐ Material increase in the capacity, producEvity, efficiency, strength, or quality of the unit of property or its output

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

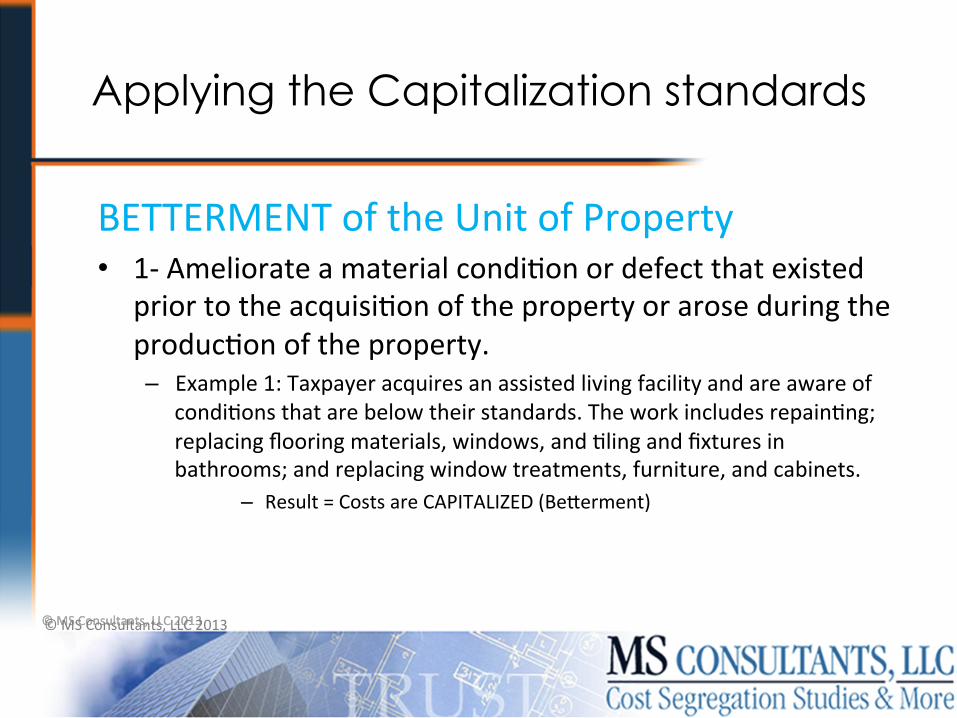

Applying the Capitalization standards

BETTERMENT of the Unit of Property • 1-‐ Ameliorate a material condiEon or defect that existed

prior to the acquisiEon of the property or arose during the producEon of the property. – Example 1: Taxpayer acquires an assisted living facility and are aware of

condiEons that are below their standards. The work includes repainEng; replacing flooring materials, windows, and Eling and fixtures in bathrooms; and replacing window treatments, furniture, and cabinets.

– Result = Costs are CAPITALIZED (BeCerment)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

BETTERMENT of the Unit of Property • 1-‐ Ameliorate a material condiEon or defect that existed

prior to the acquisiEon of the property or arose during the producEon of the property. – Example 2: Tapayer bought a store that had previously been used as a gas

staEon, located on land that had contained underground gasoline storage tanks. At the Eme of purchase, taxpayer did not know that the tanks had leaked, causing soil contaminaEon. In 2012, taxpayer discovered the contaminaEon and incurred costs to remediate the soil

• Result = Costs are CAPITALIZED (The remediaEon costs result in a beCerment of the land, because the costs ameliorate a material condiEon or defect that existed prior to the taxpayer’s purchase of the land. Because there is a beCerment, there is an improvement, and therefore is a capitalized cost.)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

BETTERMENT of the Unit of Property-‐con’t • 2-‐ Material addiEon to the unit of property (including the physical enlargement, expansion, or extension); – Example 1: Taxpayer owns a 100,000 SF manufacturing building that needed to extend the producEon area for their growing business. They construct a 30,000 SF addiEon.

– Result = Costs are CAPITALIZED (BeCerment)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

BETTERMENT of the Unit of Property-‐con’t • 2-‐ Material addiEon to the unit of property (including the physical enlargement, expansion, or extension); – Example 2: Taxpayer owns a factory building with limited office area, they extend the office into the exisEng storage area by cleaning, painEng, and replacing ceiling and floor Ele.

– Result = Costs are EXPENSED (not a BeCerment)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

BETTERMENT of the Unit of Property-‐con’t • 2-‐ Material addiEon to the unit of property (including the physical enlargement, expansion, or extension); – Example 3: What if the taxpayer adds a 3,000 square foot addiEon to the exisEng 100,000 square foot building?

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

BETTERMENT of the Unit of Property-‐con’t • 3-‐ Material increase in the capacity, producEvity, efficiency, strength, or quality of the unit of property or its output – Example 1: Taxpayer owns a factory building with a storage area on the 2nd floor, they replace columns and girder supports to permit greater weight capacity in the area for new products.

– Result = Costs are CAPITALIZED (BeCerment)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

BETTERMENT of the Unit of Property-‐con’t • 3-‐ Material increase in the capacity, producEvity, efficiency, strength, or quality of the unit of property or its output – Example 2: Taxpayer owns an office building with a 1st floor drop ceiling, they decide to remove this and repaint the original ceiling.

– Result = Costs are EXPENSED (not a BeCerment)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

RESTORATION of the Unit of Property • A taxpayer must capitalize amounts paid to restore a unit of property, including amounts paid in making good the exhausEon for which an allowance is or has been made.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

RESTORATION of the Unit of Property-‐cont • 1. Replacement of a component of a UOP and the taxpayer

has properly deducted a loss for that component; • 2. Replacement of a component of a UOP and the taxpayer

has properly taken into account the adjusted basis of the component in realizing gain or loss resulEng from the sale or exchange of the component;

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

RESTORATION of the Unit of Property-‐cont • 3. Repair of damage to a UOP for which the taxpayer has

properly taken into account the basis adjustment as a result of a casualty loss under Sec. 165 or relaEng to and event described in Sec. 165;-‐different from old casualty rules

• 4. Returns the UOP to its ordinarily efficient operaEng condiEon if the property has deteriorated to a state of disrepair and was no longer funcEonal for its intended use;

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

RESTORATION of the Unit of Property-‐cont • 5. Results in the rebuilding of the UOP to a like-‐new condiEon auer the end of its asset class life;

• 6. Replacement of a major component or a substanEal structural part of the UOP;

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Remodeling Expenditures –Part of the Restoration Standard

• Goodbye, Plan of RehabilitaEon Doctrine – The regulaEons obsolete the plan of rehabilitaEon doctrine to the extent the court created doctrine provided different standards for determining whether an otherwise deducEble cost must be capitalized as part of an improvement.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Remodeling Expenditures-con’t

• Building Refresh – “cosmeEc changes” to the Structural Component -‐ Repair

– Example: Taxpayer owns a retail store and periodically changes the layout/appearance to keep the store modern and aCracEve to customers. The work is not undertaken for the purpose of repairing damaged property but rather to renew the appearance of the property.

– Result = Costs are EXPENSED (not a BeCerment)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Remodeling Expenditures-con’t

• Building Refresh, Limited Improvement – the above, plus new bathroom fixtures – Capitalize Bathrooms (Plumbing), Other costs can be deducted as an expense

– Example: Taxpayer owns retail store and periodically changes the layout/appearance to keep the store modern and aCracEve to customers. Taxpayer also removes and replaces fixtures along with wall and floor Ele within the restroom faciliEes.

Result = – Refresh costs are EXPENSED (not a BeCerment) – Plumbing costs are CAPITALIZED (Structural/Building system)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Remodeling Expenditures-con’t

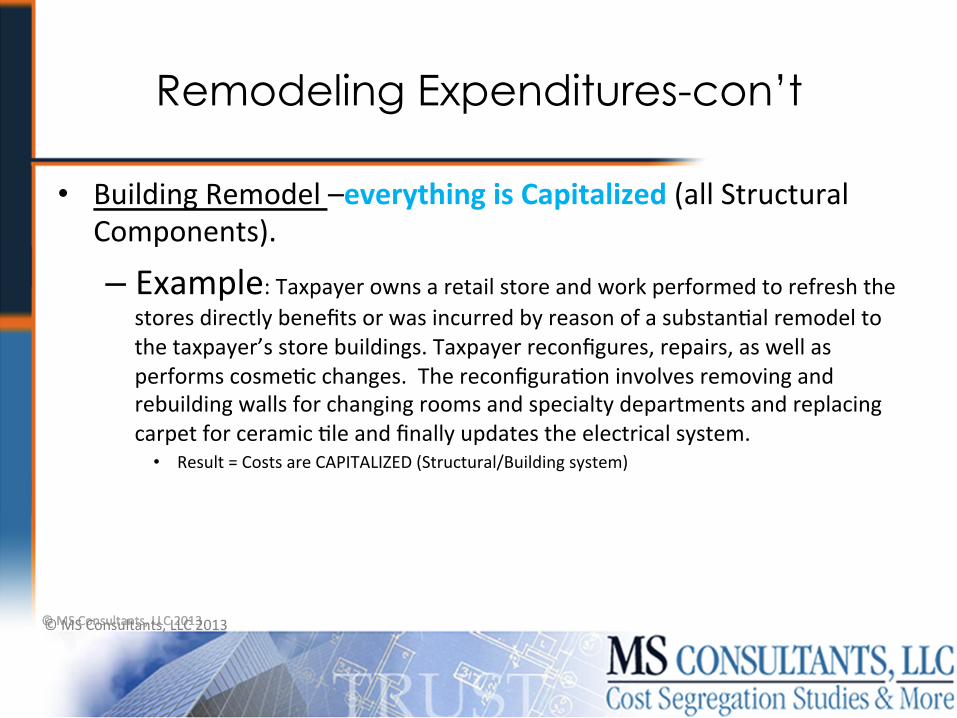

• Building Remodel –everything is Capitalized (all Structural Components).

– Example: Taxpayer owns a retail store and work performed to refresh the stores directly benefits or was incurred by reason of a substanEal remodel to the taxpayer’s store buildings. Taxpayer reconfigures, repairs, as well as performs cosmeEc changes. The reconfiguraEon involves removing and rebuilding walls for changing rooms and specialty departments and replacing carpet for ceramic Ele and finally updates the electrical system.

• Result = Costs are CAPITALIZED (Structural/Building system)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

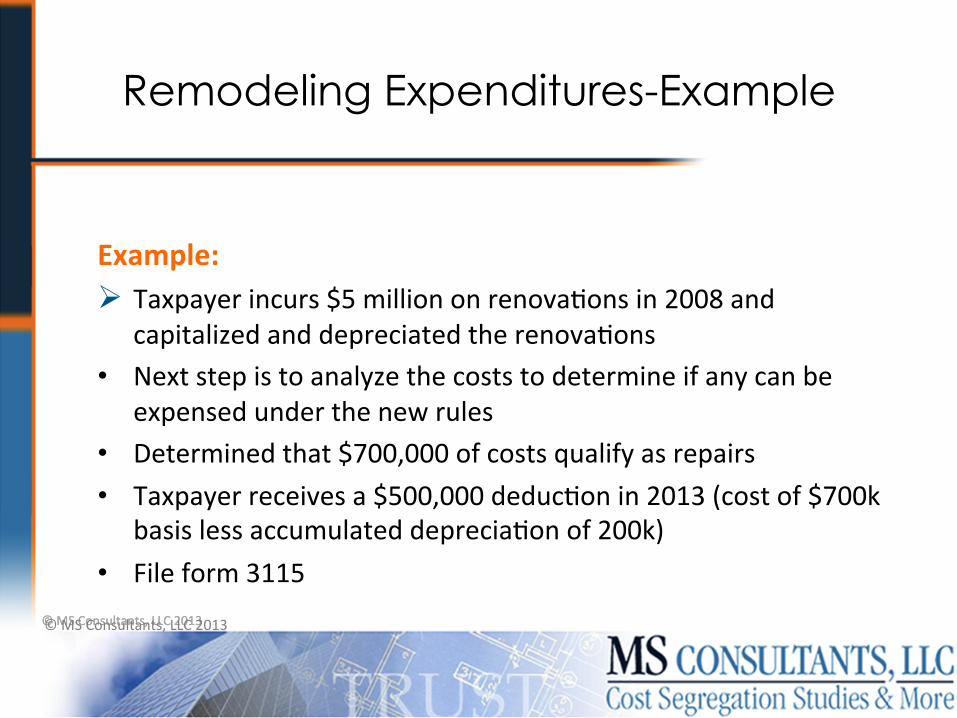

Remodeling Expenditures-Example

Example: Ø Taxpayer incurs $5 million on renovaEons in 2008 and

capitalized and depreciated the renovaEons • Next step is to analyze the costs to determine if any can be

expensed under the new rules • Determined that $700,000 of costs qualify as repairs • Taxpayer receives a $500,000 deducEon in 2013 (cost of $700k

basis less accumulated depreciaEon of 200k) • File form 3115

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

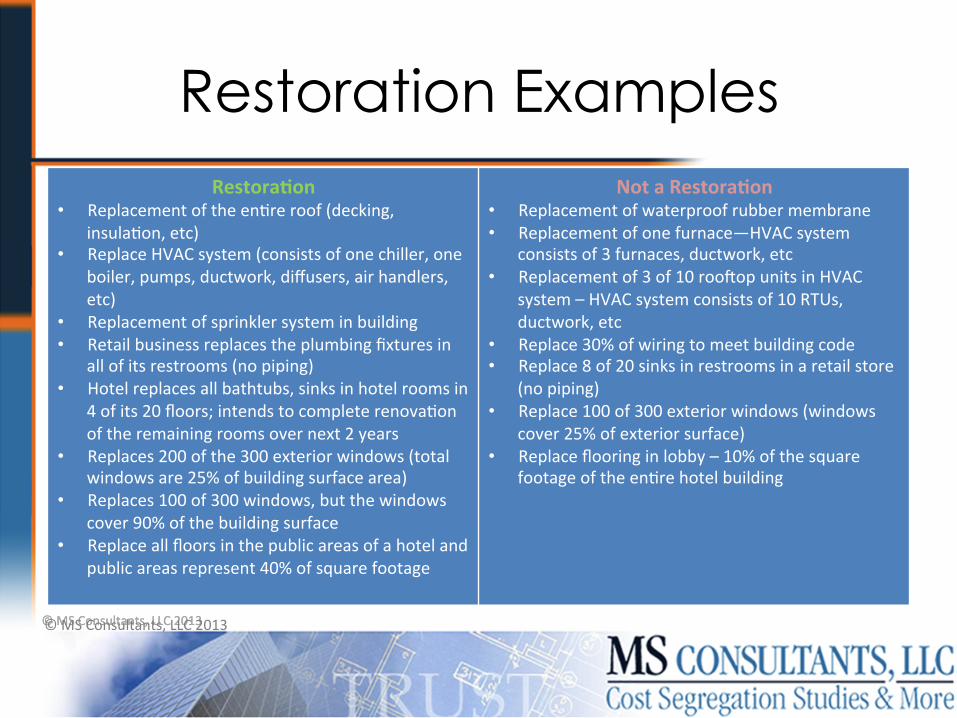

Restoration Examples Restora-on

• Replacement of the enEre roof (decking, insulaEon, etc)

• Replace HVAC system (consists of one chiller, one boiler, pumps, ductwork, diffusers, air handlers, etc)

• Replacement of sprinkler system in building • Retail business replaces the plumbing fixtures in

all of its restrooms (no piping) • Hotel replaces all bathtubs, sinks in hotel rooms in

4 of its 20 floors; intends to complete renovaEon of the remaining rooms over next 2 years

• Replaces 200 of the 300 exterior windows (total windows are 25% of building surface area)

• Replaces 100 of 300 windows, but the windows cover 90% of the building surface

• Replace all floors in the public areas of a hotel and public areas represent 40% of square footage

Not a Restora-on • Replacement of waterproof rubber membrane • Replacement of one furnace—HVAC system

consists of 3 furnaces, ductwork, etc • Replacement of 3 of 10 roouop units in HVAC

system – HVAC system consists of 10 RTUs, ductwork, etc

• Replace 30% of wiring to meet building code • Replace 8 of 20 sinks in restrooms in a retail store

(no piping) • Replace 100 of 300 exterior windows (windows

cover 25% of exterior surface) • Replace flooring in lobby – 10% of the square

footage of the enEre hotel building

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

Adapts the property to a new or different use:

• Same as the old rules • Change a manufacturing area to a retail store

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

Adapts the property to a new or different use • Example 1 -‐ New or different use:

– Taxpayer is a manufacturer and owns a manufacturing building that it has used for manufacturing since 2000. In the current year, the taxpayer pays an amount to convert its manufacturing building into a showroom for its business which involves removing and replacing various structural components to provide a beCer layout for the showroom and its offices. The amount paid to convert the manufacturing facility into a showroom adapts the building structure to a new or different use because the conversion is not consistent with their intended ordinary use of the building structure at the Eme it was placed in service.

• Result = Costs are CAPITALIZED (adaptaEon of the building structure as an amount that improves the building)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization standards

Adapts the property to a new or different use • Example 2 – Not a new or different use:

– Taxpayer owns a building consisEng of twenty retail spaces. The space was designed to be reconfigured; that is, adjoining spaces could be combined into one space. One of the tenants expands its occupancy to include two adjoining retail spaces. To facilitate the new lease, the taxpayer pays an amount to remove the walls between the three retail spaces. The amount paid to convert three retail spaces into one larger space for an exisEng tenant does not adapt the building structure to a new or different use because the combinaEon of retail spaces is consistent with the intended, ordinary use of the building structure.

• Result = Costs are EXPENSED (amount paid by the taxpayer to remove the walls does not improve the building)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Applying the Capitalization Standards

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

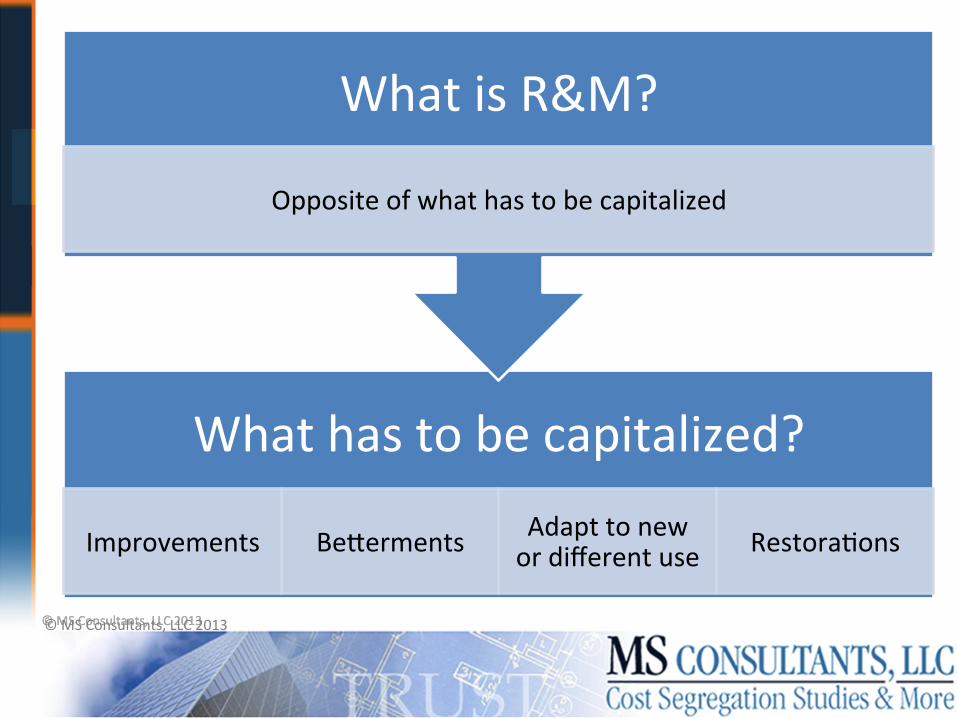

What has to be capitalized?

Improvements BeCerments Adapt to new or different use RestoraEons

What is R&M?

Opposite of what has to be capitalized

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

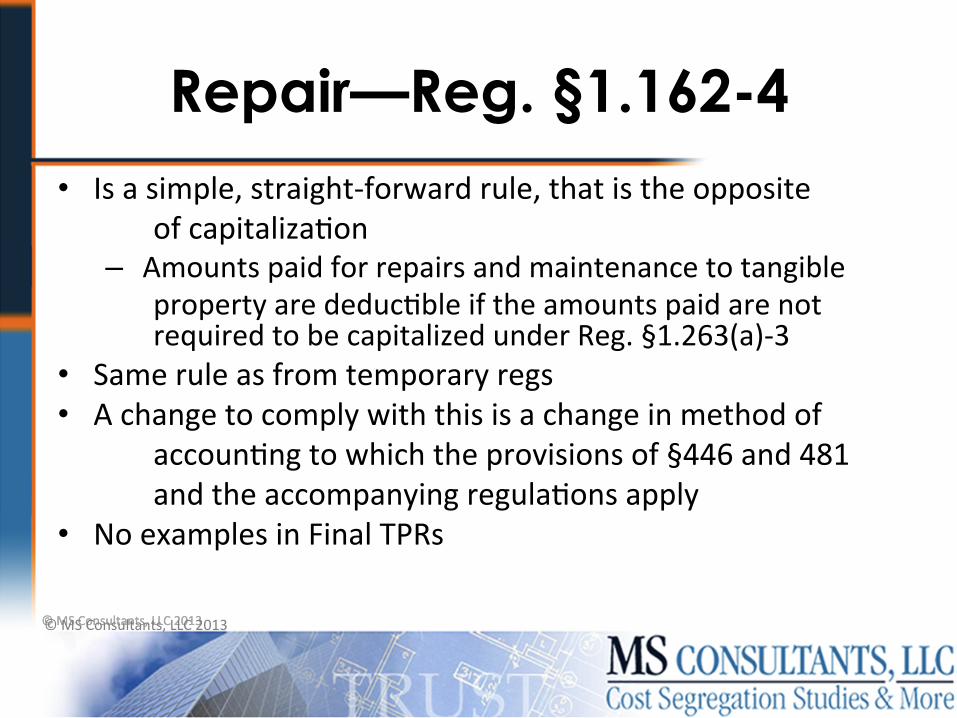

Repair—Reg. §1.162-4 • Is a simple, straight-‐forward rule, that is the opposite

of capitalizaEon – Amounts paid for repairs and maintenance to tangible

property are deducEble if the amounts paid are not required to be capitalized under Reg. §1.263(a)-‐3

• Same rule as from temporary regs • A change to comply with this is a change in method of

accounEng to which the provisions of §446 and 481 and the accompanying regulaEons apply

• No examples in Final TPRs

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

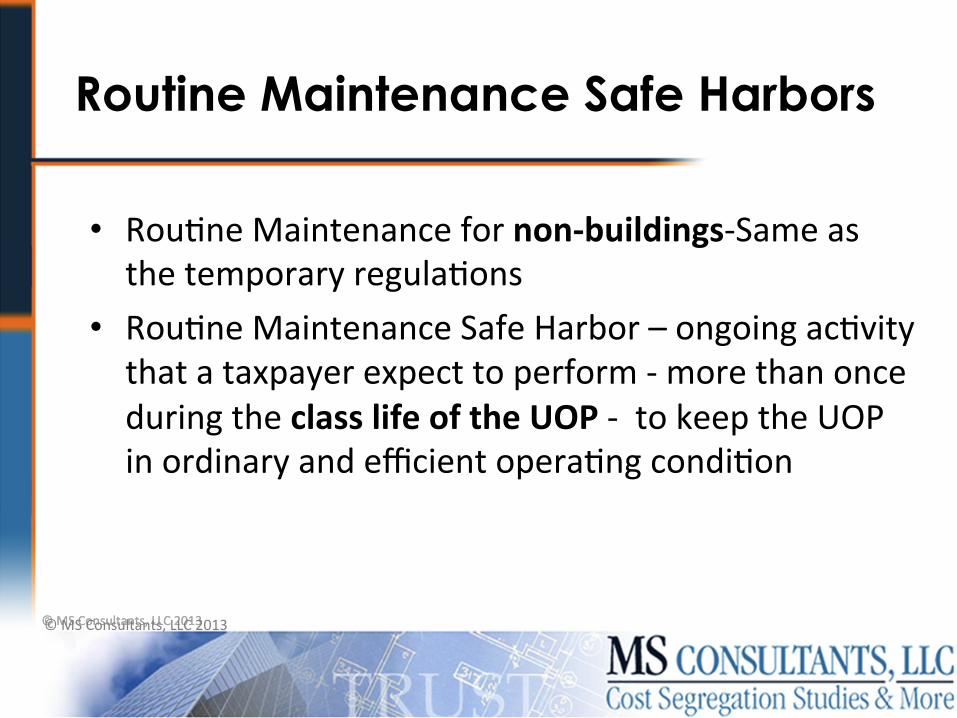

Routine Maintenance Safe Harbors

• RouEne Maintenance for non-‐buildings-‐Same as the temporary regulaEons

• RouEne Maintenance Safe Harbor – ongoing acEvity that a taxpayer expect to perform -‐ more than once during the class life of the UOP -‐ to keep the UOP in ordinary and efficient operaEng condiEon

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

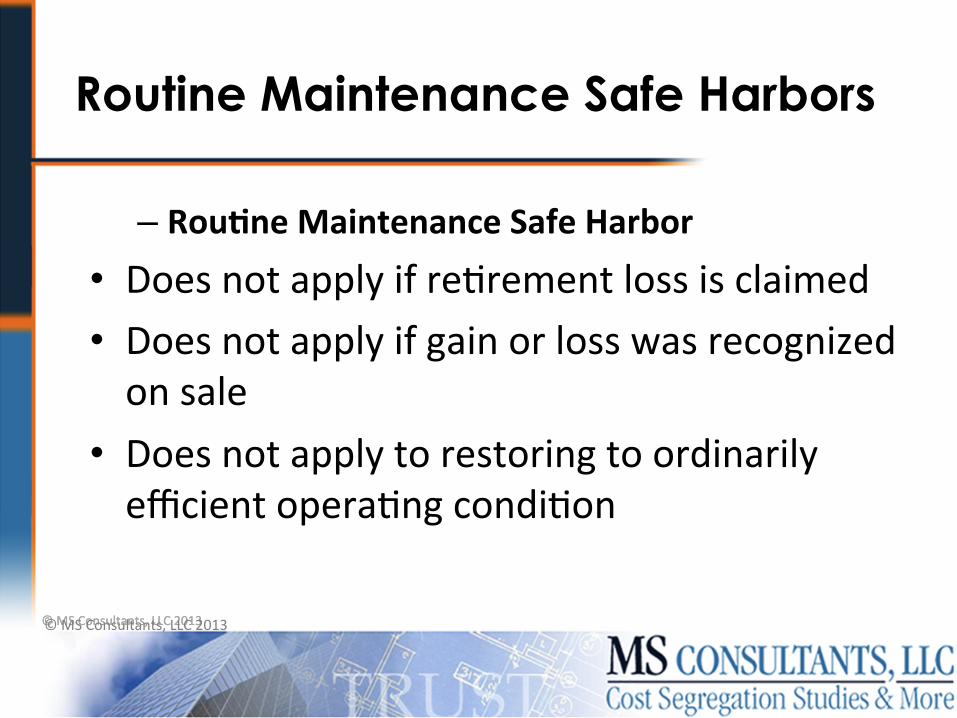

Routine Maintenance Safe Harbors

– Rou-ne Maintenance Safe Harbor • Does not apply if reErement loss is claimed • Does not apply if gain or loss was recognized on sale

• Does not apply to restoring to ordinarily efficient operaEng condiEon

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Routine Maintenance Safe Harbor

• RouEne Maintenance Safe Harbor – Example: Taxpayer acquires an agricultural machine with an ADS

class life of 10 years for its farming operaEons. The manufacturer of the machine recommends scheduled maintenance every three years, which includes the cleaning, oiling, inspecEng, and replacement of minor items such as bearings and seals. The taxpayer performs the maintenance 3 Emes in 10 years.Rev. Proc. 87-‐56, Table B-‐1 states that this assets falls under Asset Class 01.1, Agriculture with a MACRS life of 7 years and an ADS life of 10 years.

• Result = Costs are EXPENSED

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Routine Maintenance Safe Harbors

Rou-ne Maintenance Safe Harbor for buildings • Same general rules as other tangible personal property

• RouEne maintenance more than once over a 10 year period.

• An example would be brick repoinEng every 5 years. © MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Routine Maintenance Safe Harbors

NEW-‐Small Taxpayer Safe Harbor • Average 3 years gross receipts less than $10,000,000 • It is an elecEon not to capitalize R&M or improvements • Unadujsted basis cannot exceed 1,000,000 for building-‐

excludes land and land improvements if broken out. • Can be used for leased property • Total amount expended cannot exceed the lesser of

– 2% of unadjusted basis of the building or – $10,000

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Routine Maintenance Safe Harbors

• Taxpayer with average 3 year receipts of $6,000,000.

• Building 1-‐unadjusted basis is $1,200,000-‐Safe harbor doesn’t apply

• Building 2-‐unadjusted basis is $700,000-‐Safe harbor applies-‐

• Building 2-‐can deduct lesser of $10,000 or $14,000($700,000 x 2%)

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Tax tips

• Elect rouEne safe harbor elecEon annually • Review depreciaEon schedules to see if prior year assets were improperly capitalized. Fix by filing form 3115.

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

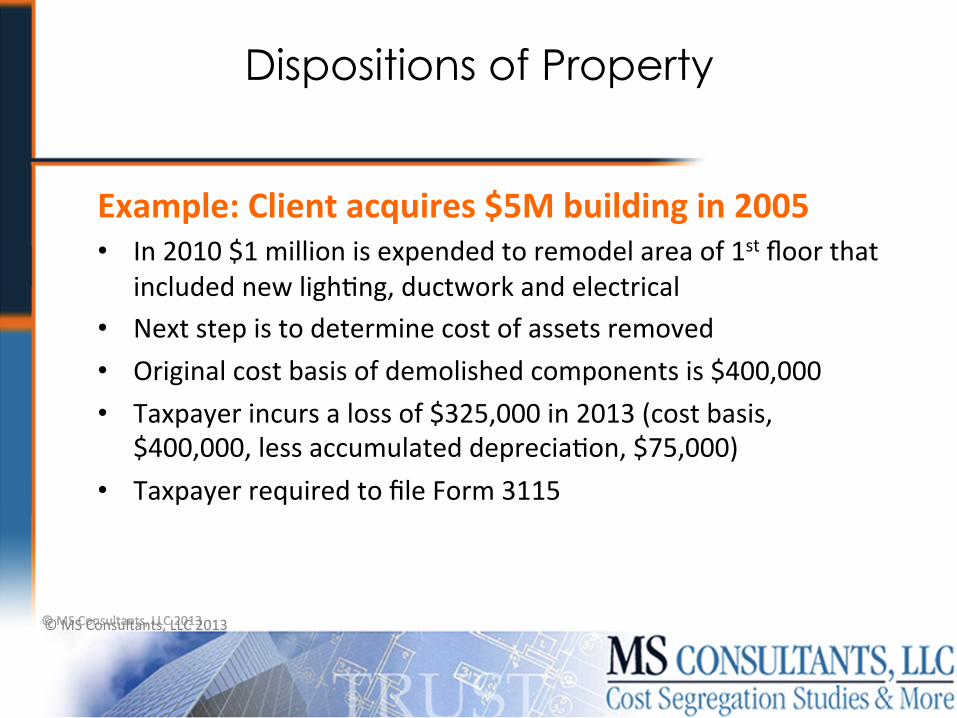

Dispositions of Property

• Revenue Procedure 2014-‐17 • Late ParEal DisposiEon ElecEon • IRS is now allowing this elecEon to be used for current and prior periods, beginning in 2013

• HOWEVER – Only available for tax years beginning in 2012 and 2013!

• ElecEon must be made now!

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Dispositions of Property

• Taxpayer may elect to write-‐off replaced assets • ElecEon is made in the year the asset is replaced • If elected, removal costs can be wriCen off. • If no elecEon is made removal costs are capitalized. • If no elecEon is made, taxpayer can never go back and write-‐off structural component. Choose it or lose it

• ElecEon rules the same as other elecEons in the final regs

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Dispositions of Property

• Taxpayer may file form 3115 for prior years. • Simplified rules for wriEng off old assets

– Specific idenEficaEon-‐I,e cost seg – CPI computaEon – Replacement cost of parEal disposiEon as a percentage of replacement cost

• GAA elecEon is no longer necessary or a good thing for buildings. (unwind old GAA elecEons using Rev Proc 2014-‐17)

• ElecEon rules the same as other elecEons in the final regs

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Dispositions of Property

Example: Client acquires $5M building in 2005 • In 2010 $1 million is expended to remodel area of 1st floor that

included new lighEng, ductwork and electrical • Next step is to determine cost of assets removed • Original cost basis of demolished components is $400,000 • Taxpayer incurs a loss of $325,000 in 2013 (cost basis,

$400,000, less accumulated depreciaEon, $75,000) • Taxpayer required to file Form 3115

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

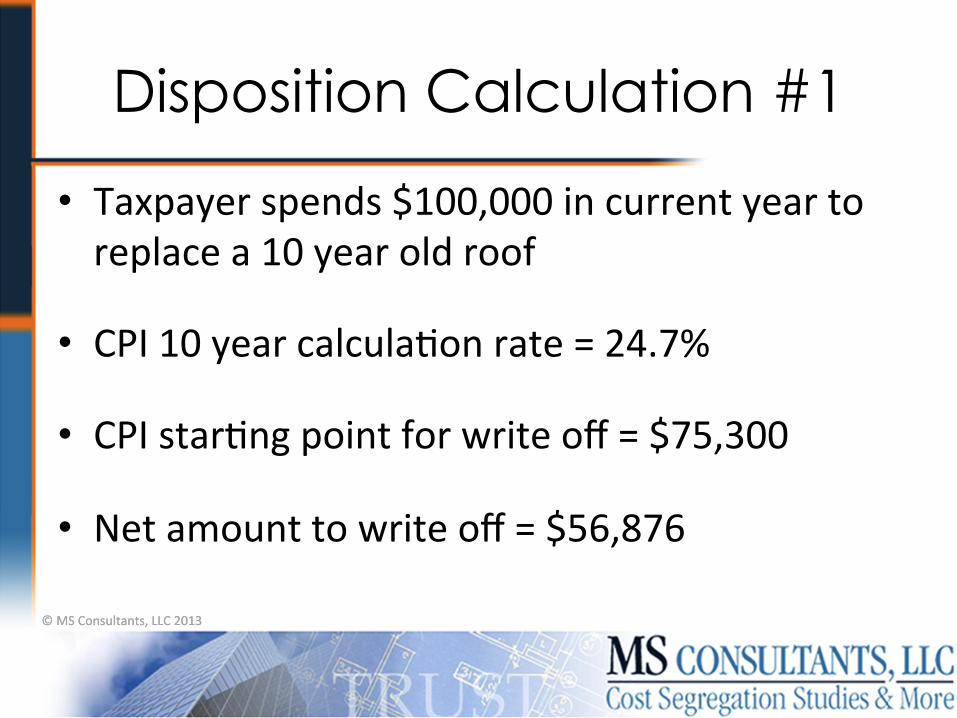

Disposition Calculation #1

• Taxpayer spends $100,000 in current year to replace a 10 year old roof

• CPI 10 year calculaEon rate = 24.7%

• CPI starEng point for write off = $75,300

• Net amount to write off = $56,876

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

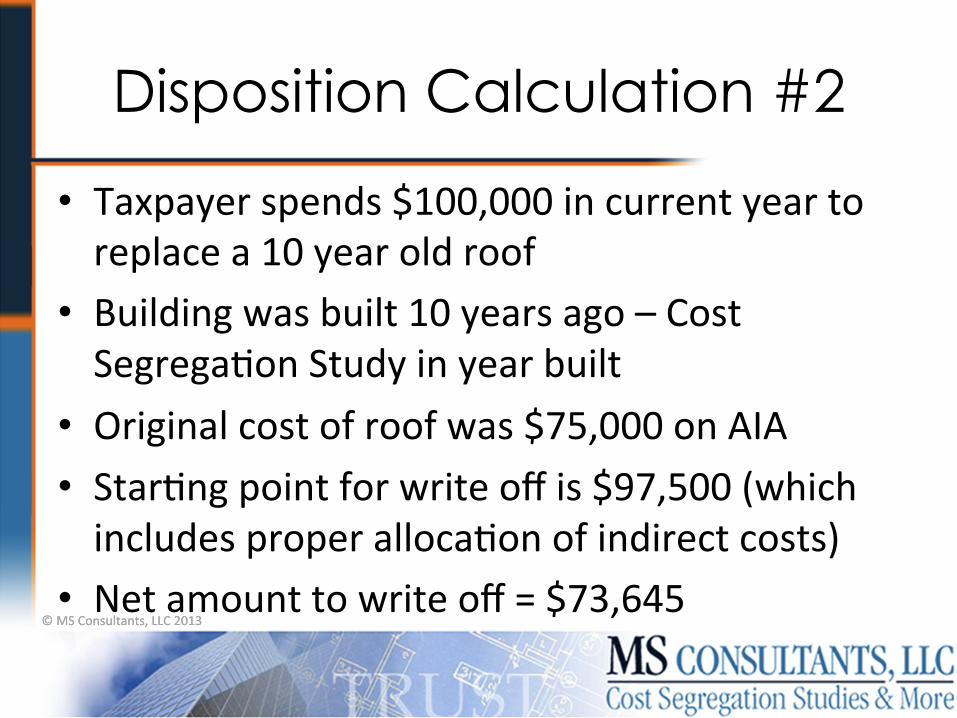

Disposition Calculation #2

• Taxpayer spends $100,000 in current year to replace a 10 year old roof

• Building was built 10 years ago – Cost SegregaEon Study in year built

• Original cost of roof was $75,000 on AIA • StarEng point for write off is $97,500 (which includes proper allocaEon of indirect costs)

• Net amount to write off = $73,645

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

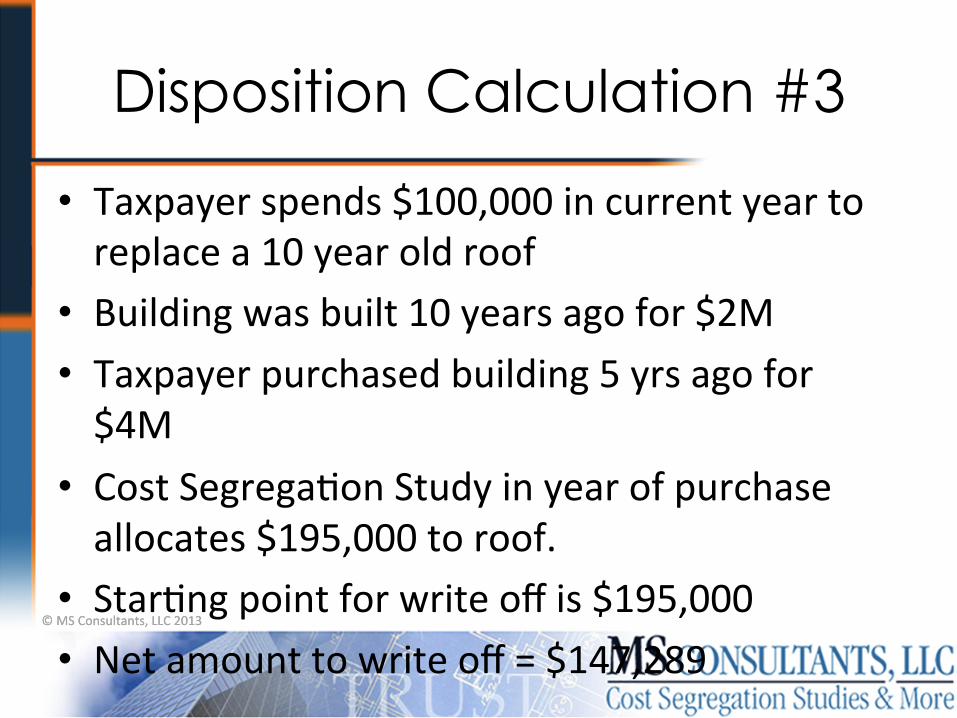

Disposition Calculation #3

• Taxpayer spends $100,000 in current year to replace a 10 year old roof

• Building was built 10 years ago for $2M • Taxpayer purchased building 5 yrs ago for $4M

• Cost SegregaEon Study in year of purchase allocates $195,000 to roof.

• StarEng point for write off is $195,000 • Net amount to write off = $147,289

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

To Capitalize, or Not to Capitalize: That is the Question

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

To Capitalize, or Not to Capitalize: That is the Question

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

I Just Bought an Item,

Now What?

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

What the IRS wanted to accomplish when the began rewriting the regs in 2004

“The Service and the Treasury Department want to provide clear, consistent and administraEve

rules that will reduce the uncertainty and controversy in this area . . .”

Did the IRS accomplish their goal?

© MS Consultants, LLC 2013

© MS Consultants, LLC 2013 © MS Consultants, LLC 2013

Thank you for listening. Any further quesEons, contact:

David A. Fabian

Director, MS Consultants LLC

Office: 716-‐633-‐9840 Cell : 716-‐308-‐4868 Fax : 716-‐633-‐9469

Related Documents