Accounting of Brand Equity Jamnalal Bajaj Institute of Management Studies Management Accounting, MMS I, Batch of 2014 Prepared and Submitted By : (In order of the presentation) Rajiv Parwani (98) Vibhuti Mhatre (93) Priyanka Pardeshi Amit Mutha (94) Vivek Metkar (92) Preethi Parthasarathy (100) Neha Dave (95) Rohan Pai (96)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 1/16

Accounting of

Brand Equity

Jamnalal Bajaj Institute of

Management Studies

Management Accounting,

MMS I, Batch of 2014

Prepared and Submitted By :(In order of the presentation)

Rajiv Parwani (98)Vibhuti Mhatre (93)

Priyanka Pardeshi

Amit Mutha (94)

Vivek Metkar (92)

Preethi Parthasarathy (100)

Neha Dave (95)

Rohan Pai (96)

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 2/16

What is Brand Equity?

It is a brand's power derived from the goodwill and name recognition that it has earned over time,

which translates into higher sales volume and higher profit margins against competing brands.Mass

marketing campaigns can also help to create brand equity.

Positive Brand Equity

“A brand has positive customer-based brand equity when consumers react more favourably to a product

and the way it is marketed when the brand is identified than when it is not”. Positive brand equity is the

positive effect of the brand on the difference between the prices that the consumer accepts to pay

when the brand known compared to the value of the benefit received.

If the brand's equity is positive, the company can increase the likelihood that customers will buy its new

product by associating the new product with an existing, successful brand. For example, if Nestle

releases a new soup, it would likely keep it under the brand name of Maggie, rather than inventing a

new brand. The positive associations customers already have with Maggi would make the new product

more enticing than if the soup had an unfamiliar brand name.

Negative Brand Equity

If consumers are willing to pay more for a generic product than for a branded one, however, the brand is

said to have negative brand equity. This might happen if a company had a major product recall or

caused a widely publicized environmental disaster. Negative brand equity occurs when a company’s

brand actually has a negative impact on its business – meaning that the company would be better off

with no name at all. It happened in the Seventies when Tesco’s brand was so poorly perceived that

Imperial Tobacco decided not to acquire the retailer for fear of being associated with such a tarnished

and unpopular organisation. It happened again in the Nineties when Skoda discovered to its horror that

it could not get British consumers to buy its cars despite spending millions on advertising. Consumer

research later confirmed that two-thirds of its target market would literally not consider anything at any

price that carried the Skoda badge

Importance of Brand EquityIn the last quarter of the 20th century there was a dramatic shift in the understanding of the creation of

shareholder value. For most of the century, tangible assets were regarded as the main source of

business value. These included manufacturing assets, land and buildings or financial assets such as

receivables and investments. They would be valued at cost or outstanding value as shown in the balance

sheet. The market was aware of intangibles, but their specific value remained unclear and was not

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 3/16

specifically quantified. Even today, the evaluation of profitability and performance of businesses focuses

on indicators such as return on investment, assets or equity that exclude intangibles from the

denominator. Measures of price relatives (for example, price-to-book ratio) also exclude the value of

intangible assets as these are absent from accounting book values.

This does not mean that management failed to recognize the importance of intangibles. Brands,

technology, patents and employees were always at the heart of corporate success, but rarely explicitly

valued. Their value was subsumed in the overall asset value. Major brand owners like The Coca-Cola

Company, Procter & Gamble, Unilever and Nestlé were aware of the importance of their brands, as

indicated by their creation of brand managers, but on the stock market, investors focused their value

assessment on the exploitation of tangible assets. High brand equity offers numerous competitive advantages:

It can help buffer the impact of a sagging economy

It can reduce marketing costs due to increased brand awareness and loyalty

It offers more trade leverage in bargaining with distributors and retailers

Strong brand equity facilitates the launch of (new) brand extensions because your brand

already carries high credibility

Strong brand equity can help stave off price battles

Strong brand equity helps achieve larger margins because the consumer becomes less price conscious

and expenses go down through more cost effective marketing initiatives. This allows you to generate

revenue through increased sales and higher price margins, while at the same time continually

strengthening your brand’s competitive position by building the consumer’s positive perception of your

brand.

Evolution: Studies Involved

Initial research into the valuation of brands originated from two areas : marketing measurement of

brand equity, and the financial treatment of brands. The first was popularized by Keller (1993), and

included subsequent studies by Lassar et al (1995) on the measure of brand strength, by Park and

Srinivasan (1994) on evaluating the equity of brand extension, Kamakura and Russell (1993) on single-

source scanner panel data to estimate brand equity, and Aaker (1996) and Montameni and Shahrokhi

(1998) on the issue of valuing brand equity across local and global markets.

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 4/16

The financial treatment of brands has traditionally stemmed from the recognition of brands on the

balance sheet (Barwise et.al., 1989, Oldroyd, 1994, 1998), which presents problems to the accounting

profession due to the uncertainty of dealing with the future nature of the benefits associated with

brands, and hence the reliability of the information presented. Tollington (1989) has debated the

distinction between goodwill and intangible brand assets. Further studies investigated the impact on the

stock price of customer perceptions of perceived quality, a component of brand equity (Aaker and

Jacobson, 1994), and on the linkage between shareholder value and the financial value of a company's

brands (Kerin and Sethuraman, 1998).

Simon and Sullivan (1993) developed a technique for measuring brand equity, based on the financial

market estimates of profits attributable to brands. The co-dependency of the marketing and accounting

professions in providing joint assessments of the valuation of brands has been recognized by Calderon et

al (1997) and Cravens and Guilding (1999). They provide useful alternatives to the traditional marketing

perspectives of brands (Aaker, 1991; Kapferer, 1997; Keller, 1998; Aaker&Joachimsthaler, 2000).

The debate over the appropriate method of valuation continues in the literature (Perrier, 1997) and in

the commercial world. The commercial valuation of brands has been led by Inter-brand, a UK-based firm

specializing in valuing brands, Financial World, a magazine which has provided annual estimates of

brand equity since 1992, and Brand Finance Limited, a British consulting organization. These

organizations utilize formulae approaches, and highlight the importance of brand valuation in the

business environment.

Brands on the balance sheet:

The wave of brand acquisitions in the late 1980s resulted in large amounts of goodwill that most

accounting standards could not deal with in an economically sensible way. Transactions that sparked the

debate about accounting for goodwill on the balance sheet included Nestlé’s purchase of Rowntree,

United Biscuits’ acquisition and later divestiture of Keebler, Grand Metropolitan acquiring Pillsbury and

Danone buying Nabisco’s European businesses.

Accounting practice for so-called goodwill did not deal with the increasing importance of intangible

assets, with the result that companies were penalized for making what they believed to be value

enhancing acquisitions. They either had to suffer massive amortization charges on their profit and loss

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 5/16

accounts (income statements), or they had to write off the amount to reserves and in many cases ended

up with a lower asset base than before the acquisition.

In countries such as the UK, France, Australia and New Zealand it was, and still is, possible to recognize

the value of acquired brands as identifiable intangible assets and to put these on the balance sheet of

the acquiring company. This helped to resolve the problem of goodwill. Then the recognition of brands

as intangible assets made use of a grey area of accounting, at least in the UK and France, whereby

companies were not encouraged to include brands on the balance sheet but nor were they prevented

from doing so. In the mid-1980s, Reckitt & Colman, a UK-based company, put a value on its balance

sheet for the Airwick brand that it had recently bought; Grand Metropolitan did the same with the

Smirnoff brand, which it had acquired as part of Heublein. At the same time, some newspaper groups

put the value of their acquired mastheads on their balance sheets.

By the late 1980s, the recognition of the value of acquired brands on the balance sheet prompted a

similar recognition of internally generated brands as valuable financial assets within a company.

In 1988, Rank Hovis McDougall (RHM), a leading UK food conglomerate, played heavily on the power of

its brands to successfully defend a hostile takeover bid by Goodman Fiel der Wattie (GFW). RHM’s

defence strategy involved carrying out an exercise that demonstrated the value of RHM’s brand

portfolio. This was the first independent brand valuation establishing that it was possible to value

brands not only when they had been acquired, but also when they had been created by the company

itself. After successfully fending off the GFWbid, RHM included in its 1988 financial accounts the value of both the internally generated and acquired brands under intangible assets on the balance sheet.

In 1989, the London Stock Exchange endorsed the concept of brand valuation as used by RHM by

allowing the inclusion of intangible assets in the class tests for shareholder approvals during takeovers.

This proved to be the impetus for a wave of major branded-goods companies to recognize the value of

brands as intangible assets on their balance sheets. In the UK, these included Cadbury Schweppes,

Grand Metropolitan (when it acquired Pillsbury for $5 billion), Guinness, Ladbrokes (when it acquired

Hilton) and United Biscuits (including the Smith’s brand).

Today, many companies including LVMH, L’Oréal, Gucci, Prada and PPR have recognized acquired brands

on their balance sheet. Some companies have used the balance-sheet recognition of their brands as an

investor-relations tool by providing historic brand values and using brand value as a financial

performance indicator. In terms of accounting standards, the UK, Australia and New Zealand have been

leading the way by allowing acquired brands to appear on the balance sheet and providing detailed

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 6/16

guidelines on how to deal with acquired goodwill. In 1999, the UK Accounting Standards Board

introduced FRS 10and 11 on the treatment of acquired goodwill on the balance sheet. The International

Accounting Standards Board followed suit with IAS 38.

And in spring 2002, the US Accounting Standards Board introduced FASB 141 and 142, abandoning

pooling accounting and laying out detailed rules about recognizing acquired goodwill on the balance

sheet. There are indications that most accounting standards, including international and UK standards,

will eventually convert to the US model. This is because most international companies that wish to raise

funds in the US capital markets or have operations in the United States will be required to adhere to US

Generally Accepted Accounting Principles (GAAP).

The principal stipulations of all these accounting standards are that acquired goodwill needs to be

capitalized on the balance sheet and amortized according to its useful life. However, intangible assets

such as brands that can claim infinite life do not have to be subjected to amortization. Instead,companies need to perform annual impairment tests. If the value is the same or higher than the initial

valuation, the asset value on the balance sheet remains the same. If the impairment value is lower, the

asset needs to be written down to the lower value. Recommended valuation methods are discounted

cash flow (DCF) and market value approaches. The valuations need to be performed on the business unit

(or subsidiary) that generates the revenues and profit.

The accounting treatment of goodwill upon acquisition is an important step in improving the financial

reporting of intangibles such as brands. It is still insufficient, as only acquired goodwill is recognized and

the detail of the reporting is reduced to a minor footnote in the accounts. This leads to the distortion

that the McDonald’s brand does not appear on the company’s balance sheet, even though it is

estimated to account for about 70 per cent of the firm’s stock market value, yet the Burger King brand is

recognized on the balance sheet. There is also still a problem with the quality of brand valuations for

balance-sheet recognition. Although some companies use a brand-specific valuation approach, others

use less sophisticated valuation techniques that often produce questionable values. The debate about

bringing financial reporting more in line with the reality of long-term corporate value is likely to

continue, but if there is greater consistency in brand-valuation approaches and greater reporting of

brand values, corporate asset values will become much more transparent.

Brand Valuation Methods:

A number of methods have been proposed to define the value posted in the balance sheet when a

brand is part of the assets of an acquired company, or any other instance when this valuation is needed.

They can be positioned on a two-dimensional mapping.

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 7/16

The horizontal axis refers to time (but do we base the analysis on the past, the present or the future?).

This axis discriminates between valuations based on historical costs (those that helped build the brand),

valuations based on present earnings, on market price, and those which rely on a business plan: that is

to say, a forecast. The vertical axis is a real/virtual dimension. Some analysts rely on hard facts (historical

accounts are facts, as well as present earnings).

The brand valuation methods can be broadly classified into 3 types

• Cost based

• Income based

• Market based

Cost Based Methods:

The cost approach measures the value of a brand based on the costs invested in building it, or

duplicating or replacing it. The premise is that a prudent investor would not pay more for a brand than

the cost to replace or reproduce it. The actual amount invested encompasses all expenses to build andsupport it up to the valuation date. Replacement costs include those to create, at current prices, a

similar brand of equivalent utility. Duplication costs represent the expenses needed to recreate an

identical brand, adjusted for any potential losses of awareness and strength.

When adopting the cost approach, a comparison must be performed between past expenditures and

awareness of the brand generated by them. It should not be automatically assumed that there is a link

between money spent and value created. The cost approach is often based on retrospective data and

does not consider a company’s future earnings potential. It may be used when other valuation

approaches cannot be implemented and there is no other reliable data. It is sometimes used to

ascertain the consistency and reasonableness of values obtained through other approaches.

Creation costs method: this brand valuation methodology estimates the amount that has beeninvested in creating the brand. In this all the assets are taken at a current value and summed to

arrive at a value. This includes tangible assets, intangible assets, investments and stocks.

Replacement value method: this brand valuation method estimates the investment required to

build a brand with a similar market position and share.

Even assuming that historical cost data of the brand is available and/or the replacement cost can be

estimated with a reasonable degree of reliability and confidence, these approaches are generally

inappropriate. The reason is that cost is not relevant for determining the value of a brand, which, is

derived from future economic benefits. There is no direct correlation between expenditure on an asset

and its value. Probably one of the few occasions where cost can be a relevant benchmark is one where

the brand has been recently acquired.

Income Based Methods:

In general this involves estimating the expected after-tax cash flows attributable to the brand over its

remaining useful economic life, and present valuing them at an appropriate discount rate. The cash

flows (or another measure of brand earnings) used shall be those reasonably attributable to the brand.

Various methods are available to determine the cash flows to be calculated after tax.

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 8/16

• Valuation by royalty method: This is often chosen to determine the cash flow generated by a

brand. It measures the present value of expected future royalty payments, assuming that the

brand is not owned but licensed. The royalty rate selected shall be determined after an in-depth

analysis of available data from licensing arrangements for comparable brands and an

appropriate split of brand earnings between licensor and licensee. It should be as close aspossible to those for brands with the same characteristics and size.

• Valuation by Earnings Multiple method: The cash profit is multiplied by what is known as

earnings multiple which in turn is estimated on the basis of various attributes of Brand such as

Leadership, Stability, Market position, Internationality, Support and Protection

Out of the above two approaches, the earnings multiple approach is easy to use, but it is not based on strong

conceptual underpinning. Generally DCF approach is considered as the conceptually superior method of

Brand Valuation.

Market based Method:

A measure of value may be based on what other purchasers have paid for reasonably similar assets. The

market approach should result in an estimate of the price reasonably expected to be realized if the

brand were to be sold. Data on the prices paid for reasonably comparable brands shall be collected and

adjustments made for differences between them and the subject brand. For selected comparables,

multiples are calculated on the basis of their acquisition price and then applied to the aggregates of the

subject.

When applying this approach, comparables should have similar characteristics to the subject, such as

brand strength, goods or services, economic and legal situation, as well as a transaction reasonably closein time to the valuation date. The valuator shall take into account the fact that the actual prices

negotiated by independent parties in transactions may reflect strategic values and synergies that cannot

be realized by the present owner. The number of transactions relating to brands as isolated assets is

very small. In addition, when the data is known, the characteristics of the subject may differ significantly

from those of the few examples of brands sold.

Apparently the methodology sounds simple, attractive, and objective. But the methodology is frequently

impractical due to lack of market information. Arm’s length transactions involving similar brands in

similar industries are infrequent, given the uniqueness of individual brands. In addition, for transactions

that are comparable, it is likely that market and financial information concerning the asset will not bepublicly available. However this method can be used as a counter check.

How to Calculate Brand Value

To capture the complex value creation of a brand, take the following five steps:

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 9/16

1. Market segmentation: Brands influence customer choice, but the influence varies depending on the

market in which the brand operates. Split the brand’s markets into non-overlapping and homogeneous

groups of consumers according to applicable criteria such as product or service, distribution channels,

consumption patterns, purchase sophistication, geography, existing and new customers, and so on. The

brand is valued in each segment and the sum of the segment valuations constitutes the total value of

the brand.

2. Financial analysis: Identify and forecast revenues and earnings from intangibles generated by the

brand for each of the distinct segments determined in Step 1. Intangible earnings are defined as brand

revenue less operating costs, applicable taxes and a charge for the capital employed. The concept is

similar to the notion of economic profit.

3. Demand analysis: Assess the role that the brand plays in driving demand for products and services in

the markets in which it operates, and deter- mine what proportion of intangible earnings is attributable

to the brand measured by an indicator referred to as the “role of branding index.” This is done by first

identifying the various drivers of demand for the branded business, then determining the degree to

which each driver is directly influenced by the brand. The role of branding index represents the

percentage of intangible earnings that are generated by the brand. Brand earnings are calculated by

multiplying the role of branding index by intangible earnings.

4. Competitive benchmarking: Determine the competitive strengths and weaknesses of the brand to

derive the specific brand discount rate that reflects the risk profile of its expected future earnings (this is

measured by an indicator referred to as the “brand strength score”). This comprises extensive

competitive benchmarking and a structured evaluation of the brand’s market, stability, leadership

position, growth trend, support, geographic footprint and legal protectability.

5. Brand value calculation: Brand value is the net present value (NPV) of the forecast brand earnings,

discounted by the brand discount rate.

The NPV calculation comprises both the forecast period and the period beyond, reflecting the ability of

brands to continue generating future earnings. An example of a hypothetical valuation of a brand in one

market segment is shown in Table. This calculation is useful for brand value modeling in a wide range of

situations, such as:

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 10/16

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 11/16

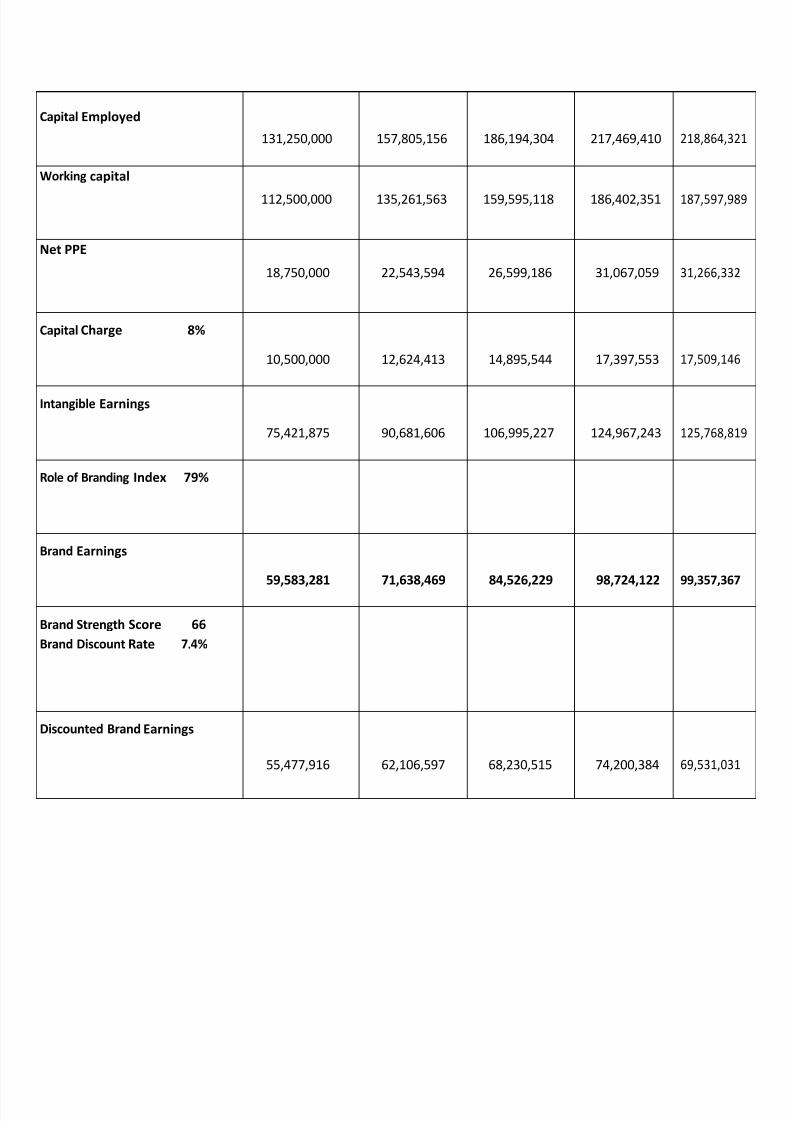

Branded Revenues

375,000,000 450,871,875 531,983,725 621,341,172 625,326,63

Cost of sales

150,000,000 180,348,750 212,793,490 248,536,469 250,130,65

Gross margin

225,000,000 270,523,125 319,190,235 372,804,703 375,195,97

Marketing costs

67,500,000 81,156,938 95,757,071 111,841,411 112,558,79

Depreciation

2,812,500 3,381,539 3,989,878 4,660,059 4,689,950

Other overheads

18,750,000 22,543,594 26,599,186 31,067,059 31,266,332

Central cost allocation

3,750,000 4,508,719 5,319,837 6,213,412 6,253,266

EBITA (Earnings Before

Interest, Tax and

Amortization)132,187,500 158,932,336 187,524,263 219,022,763 220,427,63

Applicable taxes 35%

46,265,625 55,626,318 65,633,492 76,657,967 77,149,673

NOPAT (Net Operating

Profit After Tax) 85,921,875 103,306,018 121,890,771 142,364,796 143,277,96

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 12/16

Capital Employed

131,250,000 157,805,156 186,194,304 217,469,410 218,864,32

Working capital

112,500,000 135,261,563 159,595,118 186,402,351 187,597,98

Net PPE

18,750,000 22,543,594 26,599,186 31,067,059 31,266,332

Capital Charge 8%

10,500,000 12,624,413 14,895,544 17,397,553 17,509,146

Intangible Earnings

75,421,875 90,681,606 106,995,227 124,967,243 125,768,81

Role of Branding Index 79%

Brand Earnings

59,583,281 71,638,469 84,526,229 98,724,122 99,357,367

Brand Strength Score 66

Brand Discount Rate 7.4%

Discounted Brand Earnings

55,477,916 62,106,597 68,230,515 74,200,384 69,531,031

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 13/16

NPV (Net Present Value) of

Discounted Brand

Earnings (Years1 –5)

329,546,442

Long-term growth rate 2.5%

NPV of Terminal

Brand Value (beyond Year 5)1,454,475,639

BRAND VALUE

1,784,022,082

Applications of Brand Valuation

Strategic Brand Management:

It helps in the purpose of analysis; which fosters economic value of brands. Analysis helps to

know how well the brand is established in the market, what is the customer acceptance of the

brand. Brand Valuation helps in knowing the strategies that need to be implemented in order to

increase brand presence or brand recall.

There are 4 major implications of strategic brand management:

1) Making decisions on business investments: Brand valuation helps to decide how much one

should invest in a brand, in a way it also helps to decide whether or not to go for co-

branding. For example, Nike the market leader in sports category, very closely followed by

Reebok and Adidas, collaborated with Apple to launch the Nike+ shoes, this increased their

brand value tremendously

2) Making decision on licensing the brand to a subsidiary: When a brand is licensed to a

subsidiary, the subsidiary becomes responsible for management of that brand. So before

doing so, proper evaluation of the subsidiary is necessary. Brand evaluation can help to

know how the subsidiary is performing over the years and how well it is managing its own

brands3) Measuring the return on brand investments: It helps to know the return-on-investment in a

brand. What was the brand value before investment and what is the brand value after

investment

4) Awarding and promoting the employees: Depending upon the growth in brand value,

responsible employees for the growth can be awarded to keep them motivated

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 14/16

Financial Transactions : Brand valuation helps in transactions with external partners

There are 3 major implications of Financial Transactions are:

1) Assessing fair transfer prices for the use of brands in subsidiaries

2) Determining a price for brand assets in mergers, acquisitions or sale of company

3) Capitalizing brand assets on the balance sheet according to accounting standards

Benefits of Brand Valuation:

Budget allocation decision making: Depending on how much value does a brand have in the

market, budget can be allocated according for the marketing activities of that brand.

Use of brand values supports a better way to hold managers accountable for their actions: If two

managers are working on two different projects, there should be a common platform on the

basis of which these two managers can be evaluated. Now, based on the value that each

manager has added to his brand, one manger can be evaluated against other, thus brand

valuation forms the common platform. Brand value is a meaningful metric that provides marketers and accountants with a common

focus in brand planning.

Case Study: Value of a brand name

Our case: We are going to compare and find out the value of the brand name of ‘Coca Cola’. For this, we

will compare the Value of firm/ Sales ratio of a generic cola company and that of Coca Cola. The model

being used to find out the value has been proposed by Aswath Damodaran who is

a Professor of Finance at the Stern School of Business at New York University (Kerschner Family Chair in

Finance Education), where he teaches corporate finance and equity valuation.

Value of a brand: Traditional valuation fails to consider the value of brand names and other intangibles.

One of the benefits of having a well-known and respected brand name is that firms can charge higher

prices for the same products, leading to higher profit margins and hence to higher price-sales ratios and

firm value. The larger the price premium that a firm can charge, the greater is the value of the brand

name. In general, the value of a brand name can be written as:

Value of brand name = {(V/S)b-(V/S)g}* Sales

(V/S)b = Value of Firm/Sales ratio with the benefit of the brand name

(V/S)g = Value of Firm/Sales ratio of the firm with the generic product

Formula:

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 15/16

Where:

P: Value of firm

g: expected growth rate

r: cost of capital

n: no of years

Consider the Value/Sales ratio of Coca Cola. The company had the following characteristics:

• After-tax Operating Margin =18.56% Sales/BV of Capital = 1.67

• Return on Capital = 1.67* 18.56% = 31.02%

• Reinvestment Rate= 65.00% in high growth; 20% in stable growth;

• Expected Growth = 31.02% * 0.65 =20.16%

• Length of High Growth Period = 10 years

• Cost of Equity =12.33% E/(D+E) = 97.65%

• After-tax Cost of Debt = 4.16%

• D/(D+E) 2.35%

• Cost of Capital= 12.33% (.9765)+4.16% (.0235) = 12.13%

Substituting these values in the formula, we get Value to firm/ Sales ratio as 6.10.

The values for Coca-Cola and generic cola brand are as follows:

7/27/2019 Cost Accounting_Brand Equity Calculations

http://slidepdf.com/reader/full/cost-accountingbrand-equity-calculations 16/16

Value of Coke’s brand name:

Value of Coke’s Brand Name = (6.10 - 0.69) ($18,868 million) = $102 billion

Value of Coke as a company = 6.10 ($ 18,868 million) = $ 115 billion

Approximately 88.69% of the value of the company can be traced to brand name value

Related Documents