Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Agenda

Results HighlightsResults Highlights

Market and Business Review

Financial Review

O l k d lOutlook and Development Strategy

Appendix:pp

Corporate Profile

Historical Segment Results (Shipping Services)Historical Segment Results (Shipping Services)

2

Results HighlightsResults HighlightsResults HighlightsResults Highlights

Results Highlights

Achieving Profit Growth in Difficult TimesRevenue: HK$1,630 mn (‐22.4% YOY)

Profit before income tax (PBT): HK$905 mn (+55.4% YOY)Segment PBT in Shipping Services: HK$325 mn (+26.5% YOY)

Profit attributable to the equity holders of the Company:HK$844 mn (+71.8% YOY)HK$844 mn (+71.8% YOY)

If excluding deemed disposal gain and profit contribution from Sino‐Ocean Land, profit attributable to the equity holders would h e bee HK$244 ( 41 9% YOY)have been HK$244 mn (+41.9% YOY)

Basic earnings per share: HK$0.5625 (+69.5% YOY)

Proposed final DPS: 8.4 HK centsProposed final DPS: 8.4 HK centsTogether with interim DPS 1.0 HK cent, total DPS for the year: 9.4 HK cents (+ 27% YOY) *

4*Representing 36% dividend payout ratio in terms of recurrent operating profit.

Results Highlights

Expansion in Marine Fuel Supply and Trading Business

April 2009: Acquisition of 18% interest in Double Rich Limited

November 2009: Incorporation of Sinfeng Marine Services Pte. Ltd in SingaporeDouble Rich Limited in Singapore

COSCO Group

CHIMBUSCO*

50%

COSCO InternationalCOSCO International COSCO Petroleum**

COSCO (HK) Group 100%

82%

COSCO InternationalCOSCO International

D bl Ri h (HK) Sinfeng Marine Service (SGP)

100%18%

COSCO Petroleum

Double Rich (HK) Sinfeng Marine Service (SGP)

* China Marine Bunker (Petro China) Co., Ltd., a JV of COSCO Group and Petro China.** a fuel oil supply and trading company in Singapore, providing services to the fleet of COSCO Group, and the sole authorised

t ti ithi COSCO G d i t d t ti i t i f l il h d i ti iti

5

representative within COSCO Group designated to participate in fuel oil hedging activities.

Market & Business Market & Business

ReviewReview

Market Review(1) Newbuilding Ship Contracts & Price

40.3%37 4%

45.7%Global Total Contracts

DWT mn

182.6

276.8

173.717 2%

22.1%

31.8%

37.4%P.R. China Shipbuilder's Share

30.6

104.4 94.6

34.1

17.2%

3.5

30.6‐80%

2004 2005 2006 2007 2008 2009

Shipbuilding Price 6 8

H1 H2

Global Ship Orderbook by Shipbuilding Price(US$ mn)* 2002 2003 2004 2005 2006 2007 2008 2009

VLCC 63.5 77.0 110.0 120.0 129.0 146.0 150.0 101.0

Capesize 36.3 48.0 64.0 59.0 68.0 97.0 88.0 56.0

Global Ship Orderbook byBuilder Country*

China 38%, 187 mn DWTJapan

19%,94mn DWT

Source: Clarkson Research

Panamax 21.5 27.0 36.0 36.0 40.0 55.0 46.5 33.8

Handymax 19.0 24.0 30.0 30.5 36.5 48.0 42.0 30.5

* As at end of the year* As at Feb 2010

South Korea35%,171 mn DWT

7

Source: Clarkson Research As at end of the year. As at Feb 2010.

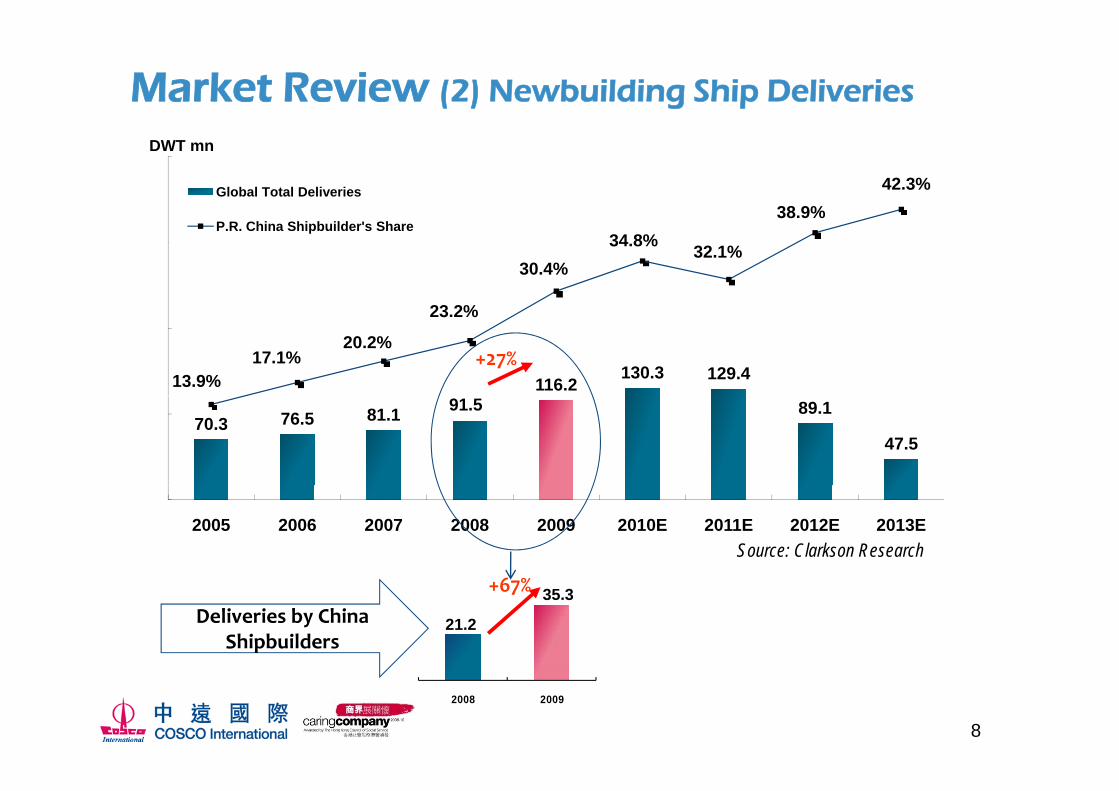

Market Review (2) Newbuilding Ship Deliveries

DWT mn

38.9%42.3%Global Total Deliveries

23 2%

30.4%34.8% 32.1%

38.9%P.R. China Shipbuilder's Share

116.2130.3 129.4 13.9%

17.1%20.2%

23.2%

+27%

70.3 76.5 81.1 91.5 89.1

47.5

Source: Clarkson Research2005 2006 2007 2008 2009 2010E 2011E 2012E 2013E

21.2

35.3+67%Deliveries by China

Shipbuilders

8

2008 2009

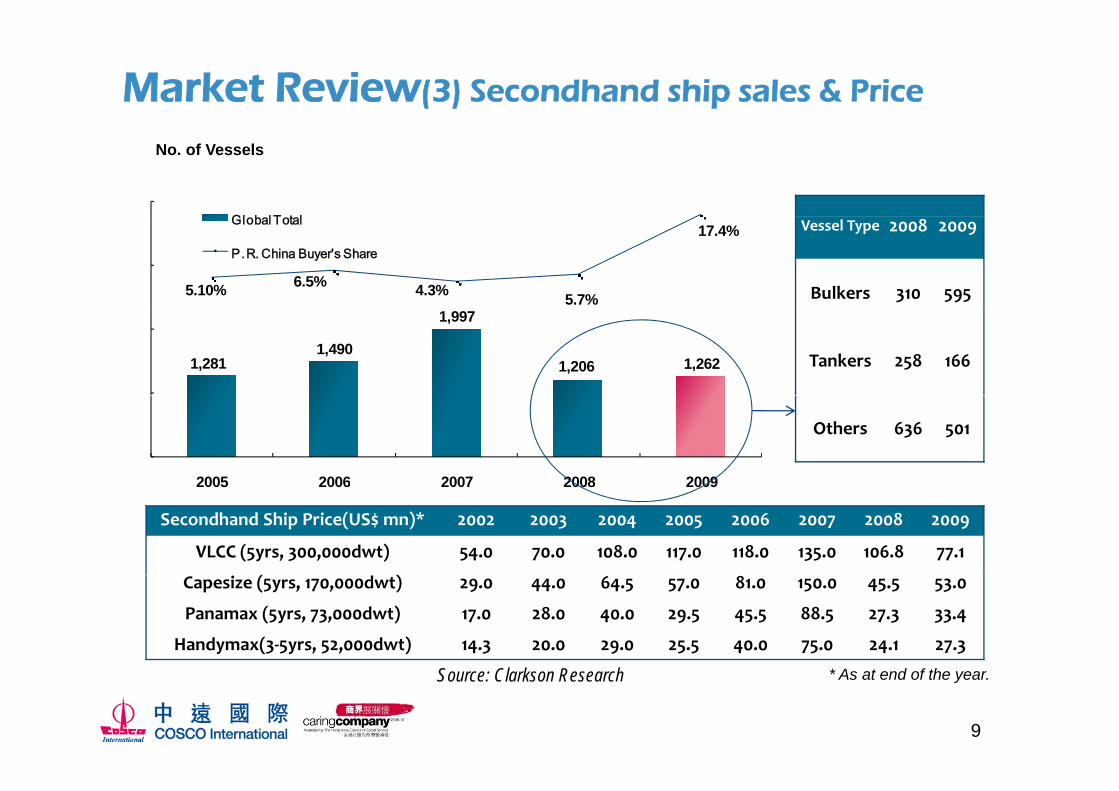

Market Review(3) Secondhand ship sales & Price

Gl b l T t l

No. of Vessels

5.10% 6.5% 4.3% 5.7%

17.4%Global Total

P.R. China Buyer's Share

Vessel Type 2008 2009

Bulkers 310 595

1,281 1,490

1,997

1,206 1,262 Tankers 258 166

2005 2006 2007 2008 2009

Others 636 501

Secondhand Ship Price(US$ mn)* 2002 2003 2004 2005 2006 2007 2008 2009

VLCC (5yrs, 300,000dwt) 54.0 70.0 108.0 117.0 118.0 135.0 106.8 77.1

( )

2005 2006 2007 2008 2009

Capesize (5yrs, 170,000dwt) 29.0 44.0 64.5 57.0 81.0 150.0 45.5 53.0

Panamax (5yrs, 73,000dwt) 17.0 28.0 40.0 29.5 45.5 88.5 27.3 33.4

Handymax(3‐5yrs, 52,000dwt) 14.3 20.0 29.0 25.5 40.0 75.0 24.1 27.3

9

Source: Clarkson Research * As at end of the year.

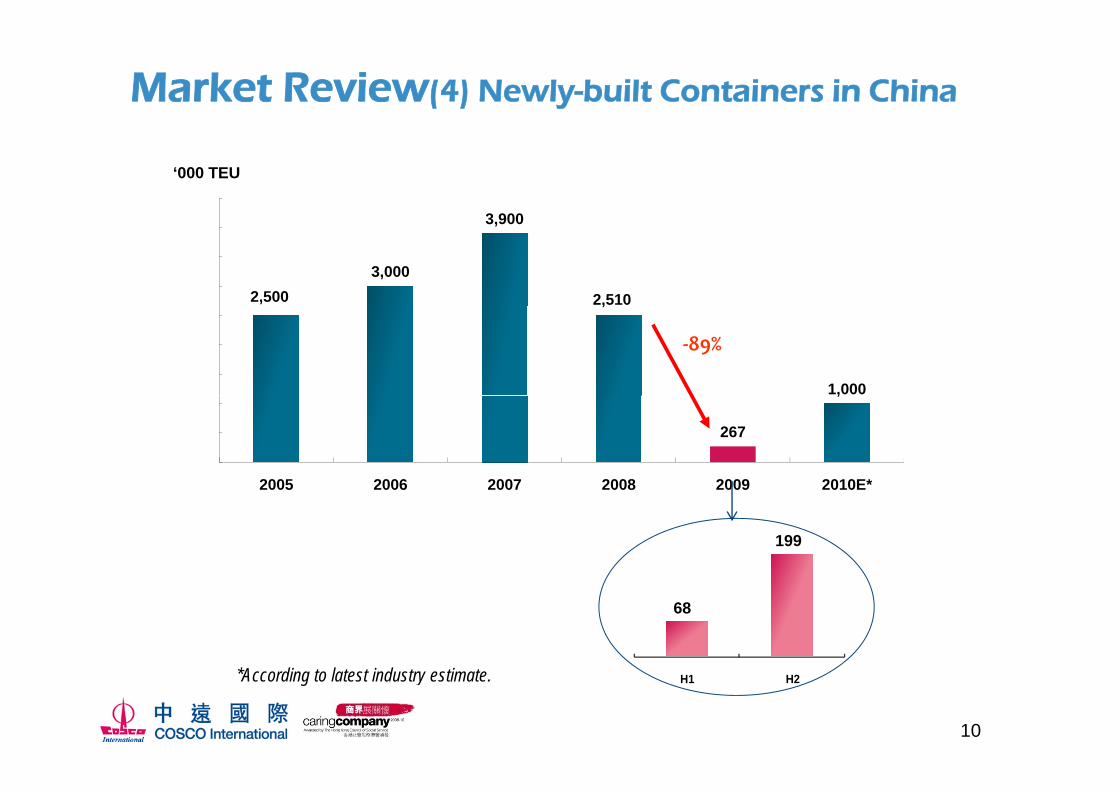

Market Review(4) Newly-built Containers in China

3 900

‘000 TEU

2,500 3,000

3,900

2,510 ,

1,000

‐89%

267

,

2005 2006 2007 2008 2009 2010E*2005 2006 2007 2008 2009 2010E

199

68

10

*According to latest industry estimate. H1 H2

Business Review - Shipping Services

Stable Earnings Growth in Core BusinessesStable Earnings Growth in Core Businesses

2009 Segment Revenue in Shipping Services: HK$ 1,110 mn (‐45.4% YOY)

2009 Segment PBT in Shipping Services : HK$ 325 mn (+26.5% YOY)2009 Segment PBT in Shipping Services : HK$ 325 mn ( 26.5% YOY)

2009 Segment Profit After Income Tax in Shipping Services : HK$ 279 mn (+25.6% YOY)

Production and Sale of Coatings: Impressive profit growth in Marine Coatings offsets profit Production and Sale of Coatings: Impressive profit growth in Marine Coatings offsets profit decline in Container Coatings, and there have seen signs of recovery in Container Coatings in 2009Q4.

Ship Trading Agency Services & Marine Insurance Brokerage Services: Newbuild ship Ship Trading Agency Services & Marine Insurance Brokerage Services: Newbuild ship deliveries increased commission income in 2009H2.

Our efforts in exploring new markets, developing new products and targeting new customers in all business segments resulted in volume growth in 2009H2customers in all business segments resulted in volume growth in 2009H2.

Trading and Supply of Marine Fuel: The new business segment started to contribute profit.

11

Business Review - Shipping Services

1. Ship Trading Agency Services*

Revenue Operating Profit

+15 9%HK$ mn HK$ mn+15.9% ** +35.9%

83.3113.2

100131.1

152.0 150

5050

100

00

50

* COSCO International Ship Trading Co., Ltd, a wholly-owned subsidiary of the Company, provides exclusive agency services inshipbuilding and ship trading for the fleet of COSCO Group.** In which HK$ 105.3 mn or 69.2% was from controlling subsidiaries of COSCO Group.

2008 20092008 2009

12

Business Review - Shipping Services (cont’d)

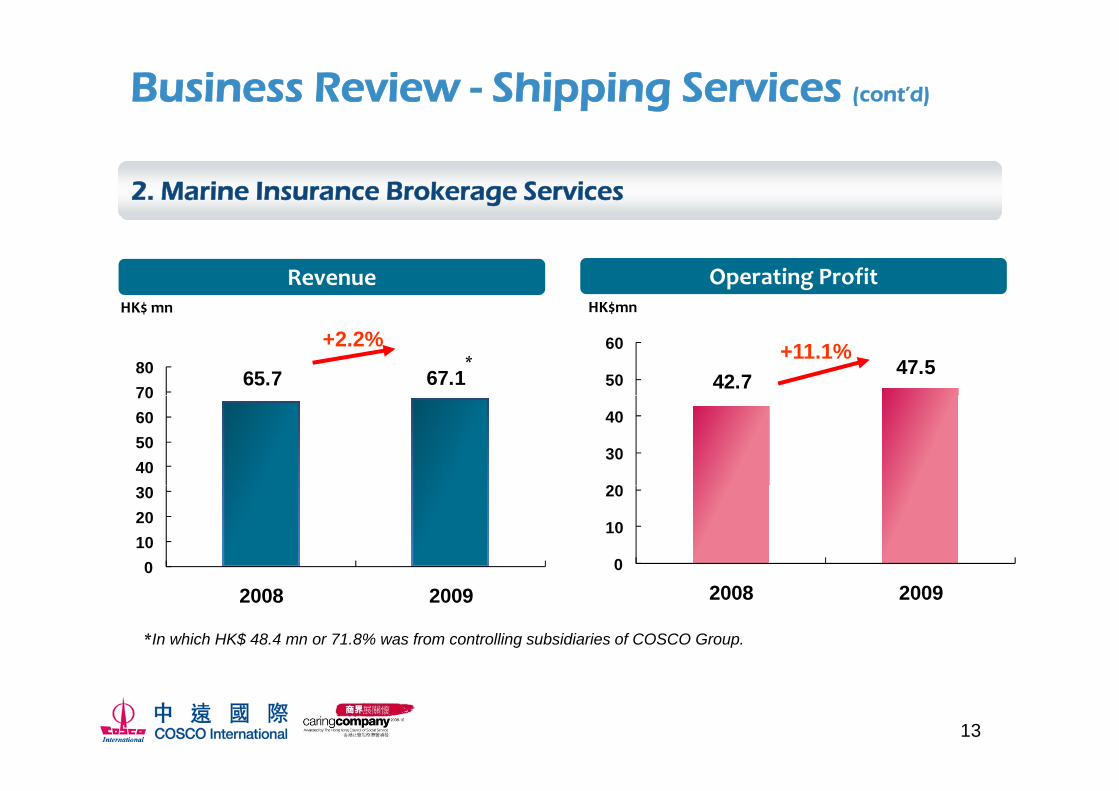

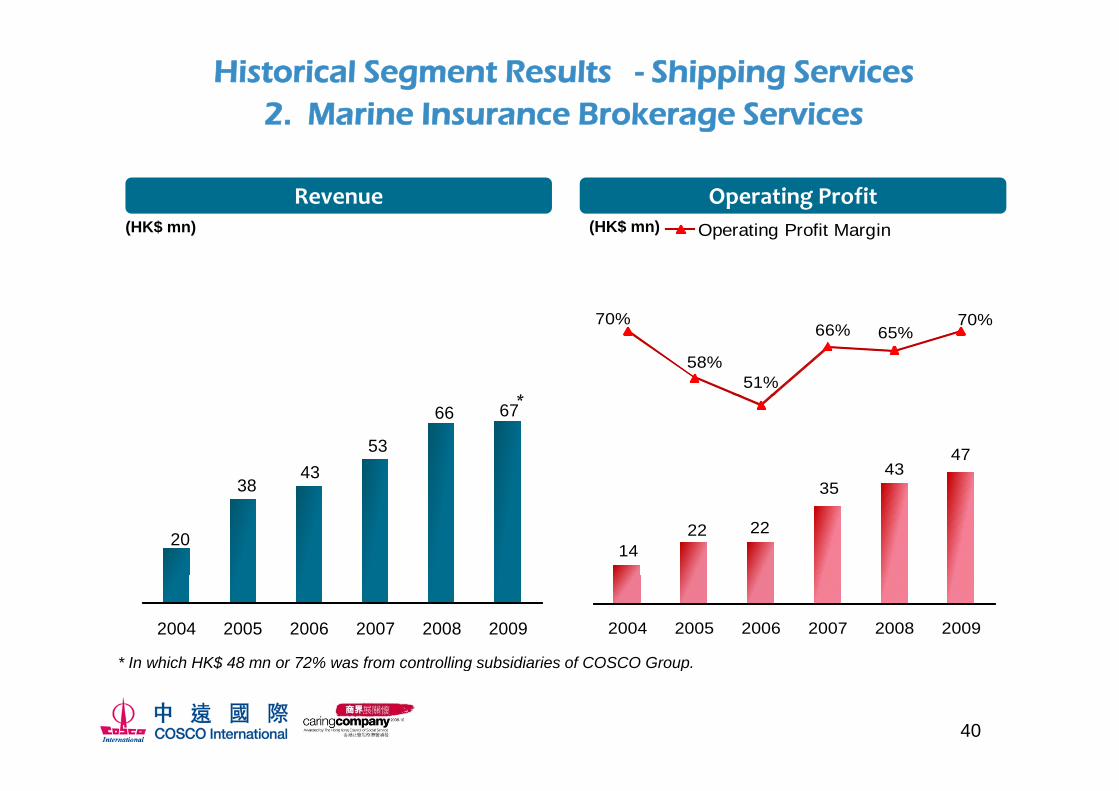

2. Marine Insurance Brokerage Services

HK$ mn HK$mn

Revenue Operating ProfitHK$ mn

+2.2%HK$mn

+11.1%*65.7 67.1

7080

42.747.5

50

60

40506070

20

30

40

0102030

0

10

20

*In which HK$ 48.4 mn or 71.8% was from controlling subsidiaries of COSCO Group.

2008 2009 2008 2009

13

Business Review – Shipping Services (cont’d)

3. Supply of Marine Equipment and Spare Parts

Revenue Operating Profit

+52.7%

HK$ mn HK$ mn

*-2.2%

455.2 445.1

400

500 32.6

40**

300

400

21.420

30

100

200

10

*In which HK$ 305.8 mn or 68.7% was from controlling subsidiaries of COSCO Group.

0

2008 20090

2008 2009

** I l di f i l i i i i HK$4 000 000 (2008 f i l l f HK$3 600 000)

14

** Including fair value gains on investment properties amounting to HK$4,000,000 (2008: fair value losses of HK$3,600,000) and reversal of provision for impairment of trade receivables, net of provision, of HK$855,000 (2008: provision for impairment

of trade receivables, net of reversal, of HK$5,451,000) upon collection of trade debts.

Business Review – Shipping Services (cont’d)

4. Production and Sale of Coatings (1) Container & IndustrialAnti corrosion Coatings by COSCO Kansai CompaniesAnti-corrosion Coatings by COSCO Kansai Companies

Revenue Operating Profit

HK$mnHK$ mn

1381.1 1,400 67.0 80

-80.0%-71.0%

800

1,000

1,200

4050 60 70

400.0

200

400

600

13.4 10 20 30 40

0

00

2008 2009

0

2008 2009

15

Business Review – Shipping Services (cont’d)

4. Production and Sale of Coatings (1) Container & IndustrialAnti corrosion Coatings by COSCO Kansai Companies (cont’d)Anti-corrosion Coatings by COSCO Kansai Companies (cont d)

Sales Volume ofContainer Coatings

Sales Volume of IndustrialAnti‐corrosion Coatings

51,034 50,000

TonnesTonnes

g

20,000

30,000

40,000 -92%

-30%10,091 7 087

12,000

16,000

3,835 10,000

20,000 7,087

4,000

8,000

0

2008 20090

2008 2009

16

Business Review – Shipping Services (cont’d)

4. Production and Sale of Coatings (2) Marine Coatings by Jotun COSCO

Sales Volume Operating ProfitHK$ mnTonnes

+29%

72,014 92,800

80,000

100,000

For ship repair and maintenance 23%For ship

*+29%

+139%

40,000

60,000

For shipnewbuilding **

23%

For ship

prepair and maintenance 33%

0

20,000

g73%For ship

newbuilding 61%

2008 2009*In which the volume for ship newbuilding increased by 54% YOY and for ship repair and maintenance decreased by 10%YOY.** Representing the supply of marine coatings for 9.55 mn DWTs newbuilding ship capacity.Note: As of Dec 31 2009 the total secured contract volume of the supply of marine coatings for ship newbuilding amounted

17

Note: As of Dec 31, 2009, the total secured contract volume of the supply of marine coatings for ship newbuilding amounted to 34 mn DWTs.

Business Review – Shipping Services (cont’d)

Market Leadership of Our Coating Businesses in China

1st

33%

ContainerCoatings

M&RMarine Coatings

25%28%

New-buildingMarine Coatings

33%25%28%

Jotun COSCO COSCO Kansai Companies

18Source: Company Statistic Data

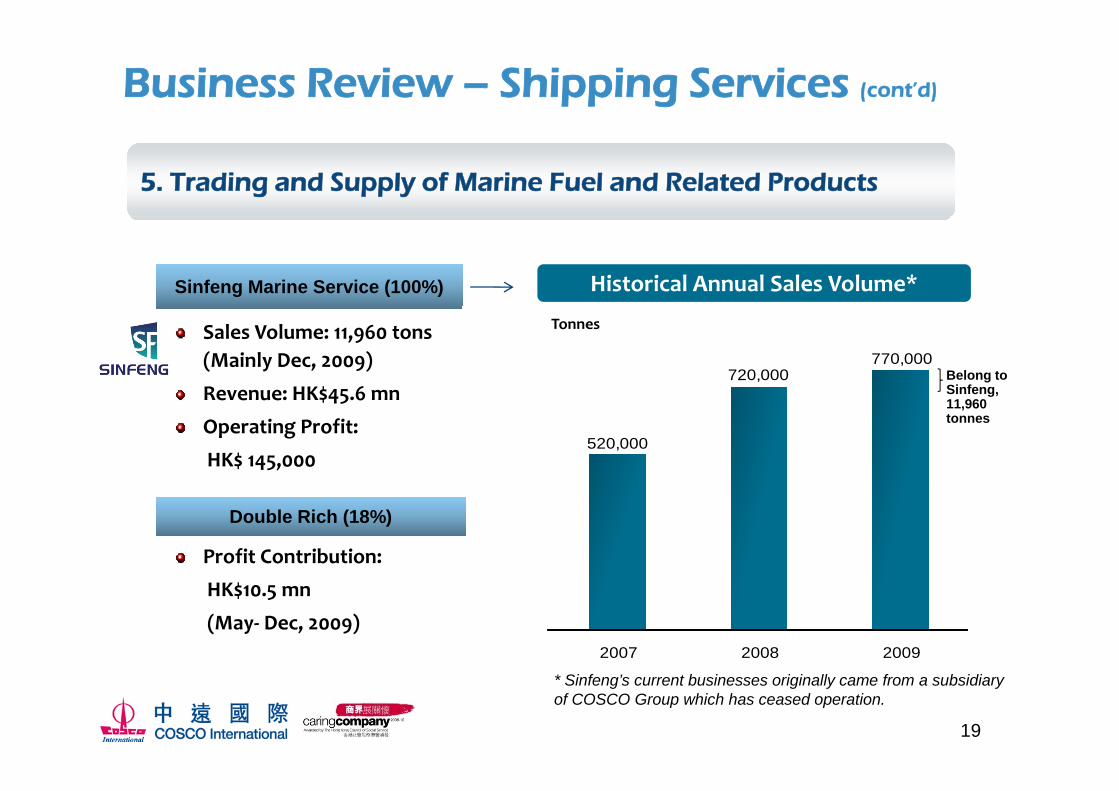

Business Review – Shipping Services (cont’d)

5. Trading and Supply of Marine Fuel and Related Products

Historical Annual Sales Volume*Sinfeng Marine Service (100%)

720,000770,000

Belong to Sinfeng,

Sales Volume: 11,960 tons (Mainly Dec, 2009)

Revenue: HK$45 6 mn

Tonnes

520,000

g,11,960 tonnes

Revenue: HK$45.6 mn

Operating Profit:

HK$ 145,000

Double Rich (18%)

Profit Contribution:

2007 2008 2009

HK$10.5 mn

(May‐ Dec, 2009)

19

* Sinfeng’s current businesses originally came from a subsidiary of COSCO Group which has ceased operation.

Business Review – General Trading & Property Investment

General Trading Property Investment

COSCO International Trading Co., Ltd ( %) t di f h lt d th

General Trading Property Investment

Sino‐Ocean Land Holdings Limited (100%)– trading of asphalt and other products

2009 Segment Revenue: HK$ 515.4

(16.85%) profit contribution:HK$354.5 mn (+11.1% YOY)

Net Deemed Disposal Gains: HK$ mn

2009 Segment Operating Profit: HK$ 4.0 mn

245.3 mn, mainly due to the issue of new shares by Sino‐Ocean Land

2009 Segment Revenue: HK$ 5.0 2009 Segment PBT: HK$ 0.7 mn mn (‐92.6% YOY)

2009 Segment Operating Profit: HK$ 36.1 mn (‐33.8% YOY)

2009 Segment PBT: HK$ 636.1 mn (+67.7YOY)

20

Revenue

Gross Profit

Profit Margin

EBITDA

Operating Profit

Financial ReviewFinancial ReviewFinancial ReviewFinancial Review

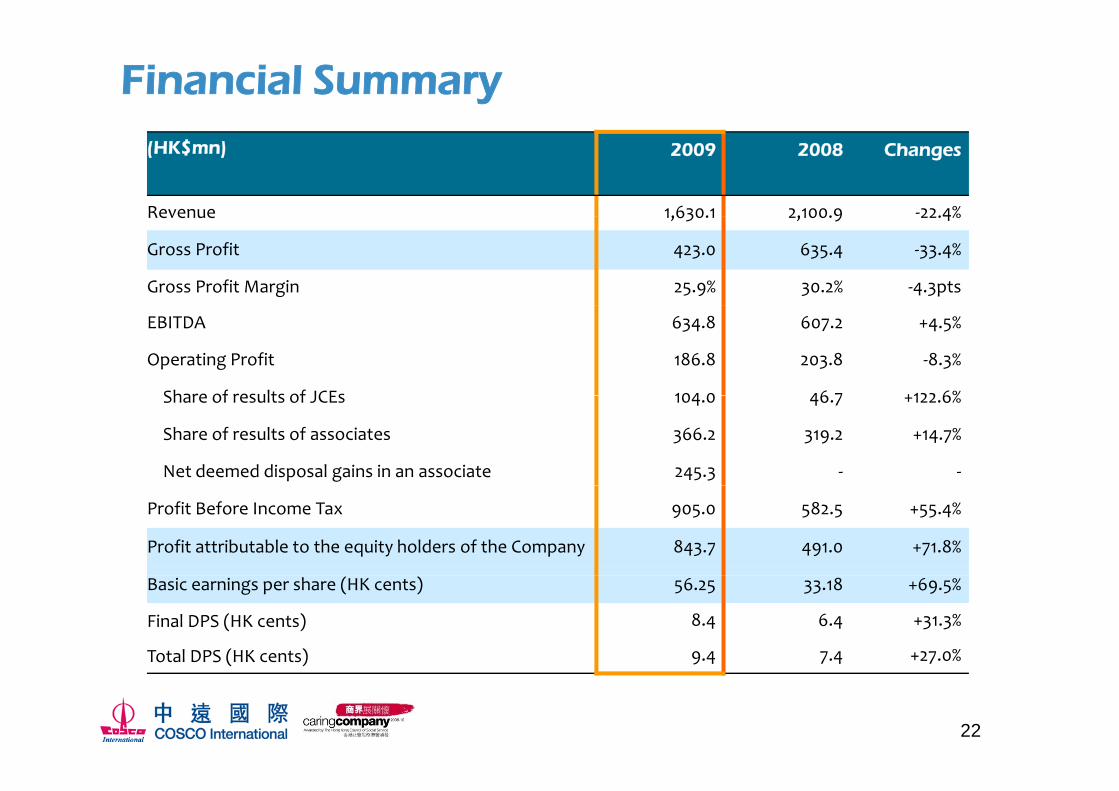

Financial Summary(HK$mn) 2009 2008 Changes

Revenue 1,630.1 2,100.9 ‐22.4%Revenue 1,630.1 2,100.9 22.4%

Gross Profit 423.0 635.4 ‐33.4%

Gross Profit Margin 25.9% 30.2% ‐4.3pts

EBITDA 634.8 607.2 +4.5%

Operating Profit 186.8 203.8 ‐8.3%

Share of results of JCEs 104 0 46 7 +122 6%Share of results of JCEs 104.0 46.7 +122.6%

Share of results of associates 366.2 319.2 +14.7%

Net deemed disposal gains in an associate 245.3 ‐ ‐

Profit Before Income Tax 905.0 582.5 +55.4%

Profit attributable to the equity holders of the Company 843.7 491.0 +71.8%

Basic earnings per share (HK cents) 56.25 33.18 +69.5%

Final DPS (HK cents) 8.4 6.4 +31.3%

Total DPS (HK cents) 9.4 7.4 +27.0%

22

( )

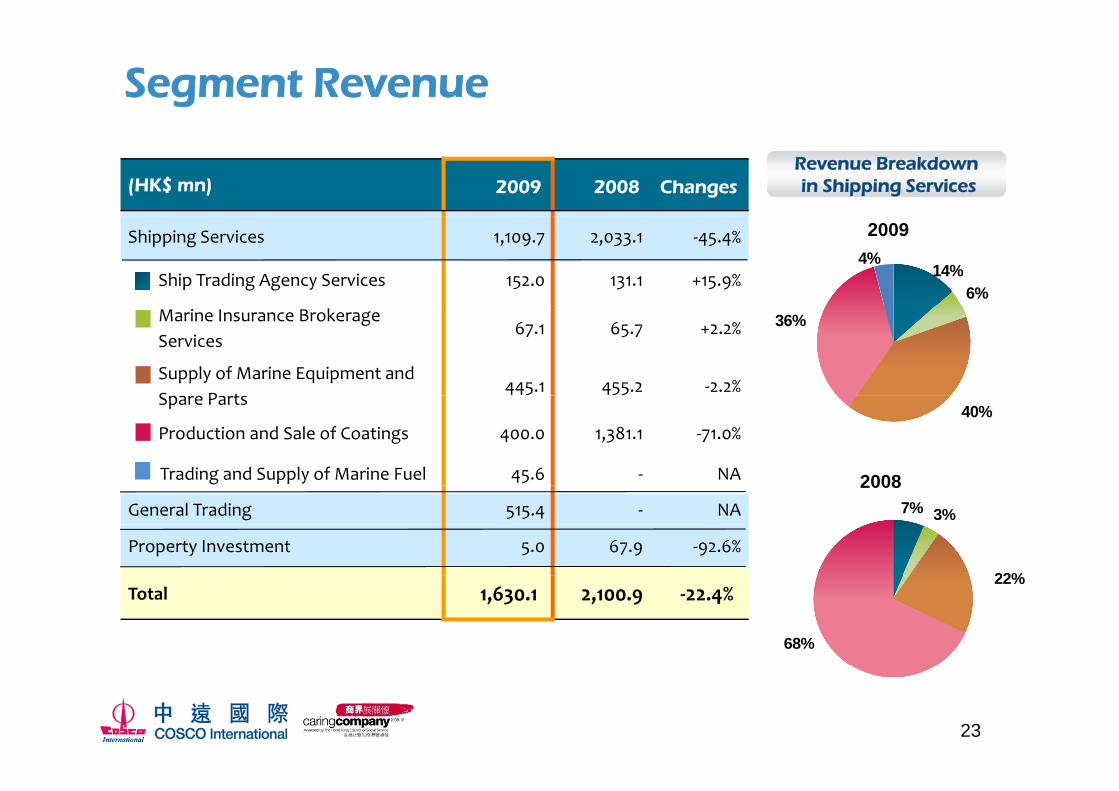

Segment Revenue

Revenue Breakdownin Shipping Services(HK$ mn) 2009 2008 Changes

Shipping Services 1,109.7 2,033.1 ‐45.4%

Ship Trading Agency Services 152.0 131.1 +15.9%

2009

14%6%

4%

Marine Insurance Brokerage Services

67.1 65.7 +2.2%

Supply of Marine Equipment andS P t

445.1 455.2 ‐2.2%

36%

Spare Parts

Production and Sale of Coatings 400.0 1,381.1 ‐71.0%

Trading and Supply of Marine Fuel 45.6 ‐ NA 2008

40%

General Trading 515.4 ‐ NA

Property Investment 5.0 67.9 ‐92.6%

20087% 3%

22%Total 1,630.1 2,100.9 ‐22.4%

22%

68%

23

Segment Profit Before Income Tax

(HK$ mn) 2009 2008 ChangesPBT Breakdown

in Shipping Services

36%

35%

3%Shipping Services 324.7 256.7 +26.5%

Ship Trading Agency Services 116.2 89.3 +30.1%

2009

Marine Insurance Brokerage Services

47.7 43.7 +9.3%

Supply of Marine Equipment andS P t

37.1 25.6 +45.4%15%

11%

Spare Parts

Production and Sale of Coatings 113.1 98.2 +15.2%

Trading and Supply of Marine Fuel 10.7 ‐ NA 2008

35%38%General Trading 0.7 ‐ NA

Property Investment 636.1 379.3 +67.7%

17%10%

Total 905.0 582.5 +55.4%

24

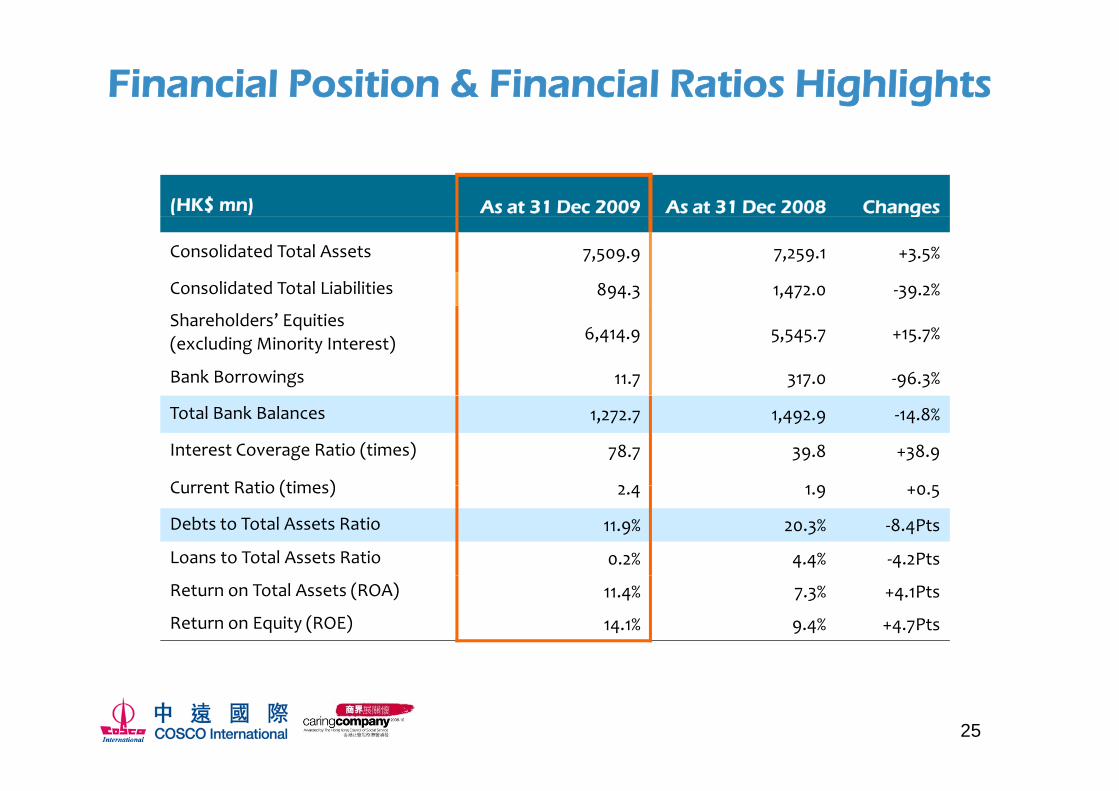

Financial Position & Financial Ratios Highlights

(HK$ mn) As at 31 Dec 2009 As at 31 Dec 2008 Changesg

Consolidated Total Assets 7,509.9 7,259.1 +3.5%

Consolidated Total Liabilities 894.3 1,472.0 ‐39.2%

Shareholders’ Equities(excluding Minority Interest) 6,414.9 5,545.7 +15.7%

Bank Borrowings 11.7 317.0 ‐96.3%

Total Bank Balances 1,272.7 1,492.9 ‐14.8%

Interest Coverage Ratio (times) 78.7 39.8 +38.9

Current Ratio (times) 2 4 1 9 0 5Current Ratio (times) 2.4 1.9 +0.5

Debts to Total Assets Ratio 11.9% 20.3% ‐8.4Pts

Loans to Total Assets Ratio 0.2% 4.4% ‐4.2Pts

Return on Total Assets (ROA) 11.4% 7.3% +4.1Pts

Return on Equity (ROE) 14.1% 9.4% +4.7Pts

25

Summary Cash Flow

(HK$ mn) 2009 2008

Cash & Cash Equivalents – Beginning 1,309.1 967.0q g g ,3 9 9 7

Cash Inflow (outflow)

Generated from operating activities 335 4 408 0Generated from operating activities 335.4 408.0

(Used in)/Generated from investing activities (52.3) 34.3

(Used in)/Generated from financing activities (398.7) (111.9)( )/ o g (39 7) ( 9)

Net increase (decrease) in cash and cash equivalents (115.6) 330.4

Exchange difference 1.0 11.7

Cash & Cash Equivalents‐ End 1,194.5 1,309.1

26

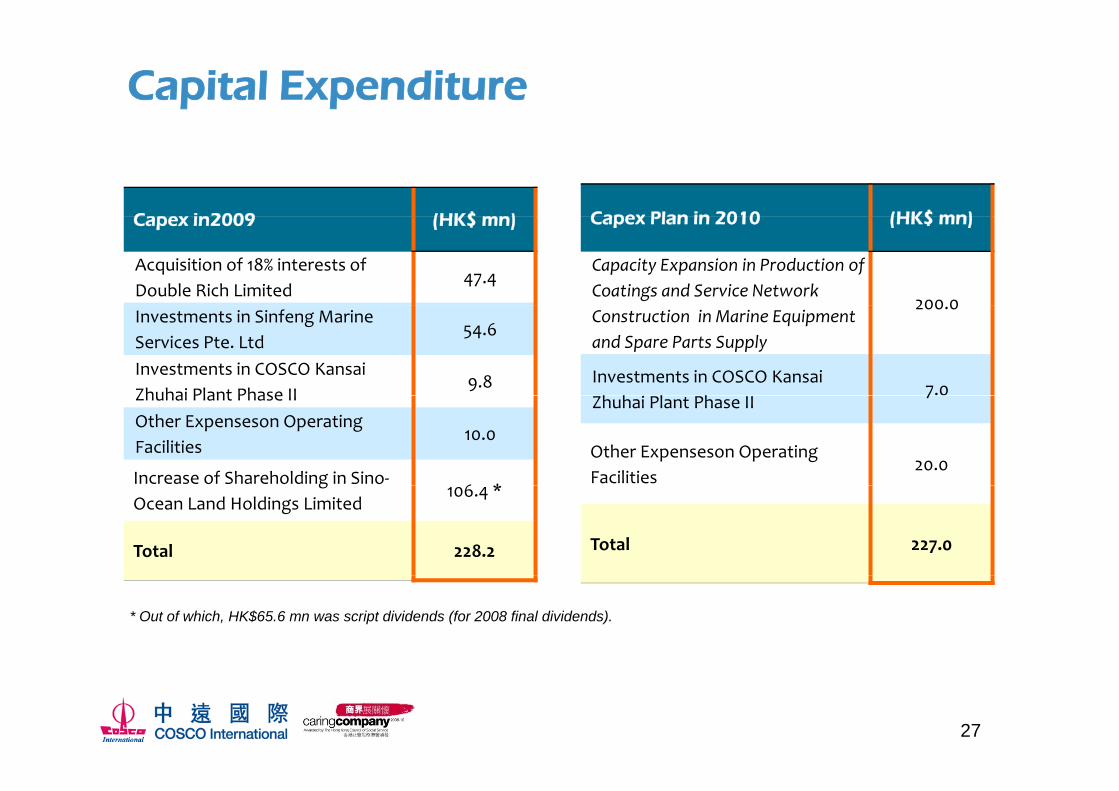

Capital Expenditure

C i 2009 (HK$ ) Capex Plan in 2010 (HK$ mn)Capex in2009 (HK$ mn)

Acquisition of 18% interests ofDouble Rich Limited

47.4

Capex Plan in 2010 (HK$ mn)

Capacity Expansion in Production of Coatings and Service Network

200 0Investments in Sinfeng Marine Services Pte. Ltd

54.6

Investments in COSCO Kansai Zhuhai Plant Phase II

9.8

Construction in Marine Equipment and Spare Parts Supply

200.0

Investments in COSCO Kansai h h l h

7.0Zhuhai Plant Phase IIOther Expenseson Operating Facilities

10.0

Increase of Shareholding in Sino‐6 *

Zhuhai Plant Phase II7

Other Expenseson Operating Facilities

20.0g

Ocean Land Holdings Limited106.4 *

Total 228.2 Total 227.0

* Out of which, HK$65.6 mn was script dividends (for 2008 final dividends).

27

Outlook and Outlook and Development StrategyDevelopment Strategy

Outlook in 2010 –Ship Trading Agency Services

Total number of new build deliveries in

Positive Negative

Total number of newbuild orders 2010 will be stable compared with that in 2009 according to latest schedule*.

Secondhand ship sale and new build l ill ti t b ti

Total number of newbuild orders will continue to decrease because of comparatively small number of new order contracts.

China COSCO 2010 2011 2012 2013 Total

resale will continue to be active.

Orderbook** 2010 2011 2012 2013 TotalNo. of

VesselsDWT000’

No. ofVessels

DWT000’

No. ofVessels

DWT000’

No. ofVessels

DWT000’

No. ofVessels

DWT000’

Bulkers - VLOC 4 1,190 8 2,381

Bulkers - Capesize 2 410 6 1,230 10 1,994p , ,

Bulkers - Panamax 9 879 3 345 15 1,452

Bulkers - Handymax 4 228 2 114 11 627

Bulkers - Total 19 2,707 9 1,575 2 114 44 6,454No. of TEU No. of TEU No. of TEU No. of TEU No. of TEUNo. of

VesselsTEU000’

No. ofVessels

TEU000’

No. ofVessels

TEU000’

No. ofVessels

TEU000’

No. ofVessels

TEU000’

Container Vessels 4 20.4 7 29.75 16 95.3 5 66.75 36 232.6

*Commission income on new vessels is recognized upon delivery of the newl d t d f b t 78% f th f hi t di

29

vessels and accounted for about 78% of the revenue of ship trading agency segment in 2009.

** Source: China COSCO 2009 Interim Results Announcement

Outlook in 2010 –Marine Insurance Brokerage Services & Supply of Marine Equipment and Spare Parts

NegativeP iti

Services & Supply of Marine Equipment and Spare Parts

Increase in newbuilding deliveries i ill b i d d t

Negative

Commission income in marine insurance brokerage is difficult

Positive

in 2010 will bring new demand to marine insurance.

New investors in shipping are our potential customers in both

insurance brokerage is difficult to increase as the second‐hand ship prices are still in a very low level.

potential customers in both marine insurance brokerage and marine equipment and spare parts supply (More than 200 second‐h d l h d b

Container shipping companies will continue to stringently cut ship repairing and maintenance costhand vessels were purchased by

Chinese buyers in 2009).

Requirement on marine environmental protection will

cost.

Younger fleet age could reduce the total volume of marine equipment and spare parts environmental protection will

bring demand to marine equipment supply.

equipment and spare parts supply.

30

Outlook in 2010 – Production and Sale of Coatings

Positive Negative

ContainerContainerCoatingsCoatings

Container shipping volume recovery and restocking of containers will lead to container coating demand recovery , esp. after 2010Q1.

Overcapacity is still problem as the total newly‐built volume of containers in China in 2010 is expected to be 1,000,000 TEU (267,000TEU in 2009 and 2 51 mn TEU in 2008 )*

Industrial Industrial Industrial Industrial

gg y , p Q and 2.51 mn TEU in 2008 ) .

China’s stimulus package will continue to increase the coating demand in the industries such as new energy steel

Market competition will continue to be fierce, as part of the container coating capacity will be used in the Industrial Industrial

AntiAnti‐‐corrosion corrosion CoatingsCoatings

Industrial Industrial AntiAnti‐‐

corrosion corrosion CoatingsCoatings

industries such as new energy, steel framework and steel machinery manufacture.Recovery in global trade will start to increase the coating demand in the

f t f t il d t f ilit

coating capacity will be used in the production of industrial coatings.

Marine Marine

manufacture of trailers and port facility.

The huge demand for newbuilding coatings in 2010 is predictable due to the huge number of scheduled new ship deliveries

Prices of the two major raw materials for production ‐ petrochemicalproducts and metal will increase, which will squeeze the profit margin

CoatingsCoatingsdeliveries.The demand for M&R (maintenance and repair) coatings could start to increase YOY.

which will squeeze the profit margin of newbuilding coatings.

31*According to latest industry statistics and estimate.

Strategies in 2010

Actively seek development opportunities including newinvestment or M&A in core businessinvestment or M&A in core business

Explore new value‐added services to increase profit driversl g l h ialong value chain

Maintain close relationship with key customers and be well‐prepared to capture market recovery

Increase customer base by targeting new Chinese investorsin shipping

Expand service network for better geographical presenceg g

Increase synergies between different business units

32

Thank you!IR Team ContactMs. Yang Ling Mr. Wilson LoTel: 852 2809 7810 Tel: 852 2809 7800E il l@ i tl E il l @ i tlEmail: [email protected] Email: [email protected]

33

Corporate ProfileCorporate ProfileAppendixAppendix

Corporate ProfileCorporate ProfileHistorical Segment Results Historical Segment Results

(Shipping Services)(Shipping Services)(Shipping Services)(Shipping Services)

Corporate Profile - Corporate Structure

COSCO GroupCOSCO Group

100%

CoreBusiness

Shipping Services

COSCO International Ship TradingCOSCO International Ship TradingCo., Ltd (100%)Co., Ltd (100%)

Ship TradingAgency Services

59.9%

COSCO (HK) Group LtdCOSCO (HK) Group Ltd COSCO (HK) Insurance Brokers Ltd.COSCO (HK) Insurance Brokers Ltd.(100%)(100%)Shenzhen COSCO Insurance Brokers Shenzhen COSCO Insurance Brokers Limited (55%)Limited (55%)

Marine InsuranceBrokerage Services

Agency Services

COSCO International*(Stock Code:00517)COSCO International*(Stock Code:00517)

Supply of Marine Equipment & Spare Parts

YuantongYuantongMarine Service Co. Limited Marine Service Co. Limited (100%) (100%)

COSCO Kansai Paint & Chemicals COSCO Kansai Paint & Chemicals (Tianjin) Co., Ltd. (63.07%)(Tianjin) Co., Ltd. (63.07%)COSCO Kansai Paint & Chemicals COSCO Kansai Paint & Chemicals

Production and Sale of C t i d I d t i l

COSCO International is a HK‐based shipping services

COSCO Kansai Paint & Chemicals COSCO Kansai Paint & Chemicals (Shanghai) Co., Ltd. (63.07%)(Shanghai) Co., Ltd. (63.07%)

JotunJotun COSCO Marine Coatings (HK) COSCO Marine Coatings (HK) Limited Limited (50%)(50%)

COSCO Kansai Paint & Chemicals COSCO Kansai Paint & Chemicals ((ZhuhaiZhuhai) Co., Ltd. (64.71%)) Co., Ltd. (64.71%)

Production and Sale of Marine Coatings

Container and IndustrialAnti‐corrosion Coatings

pp gprovider, offering diversified and specialized shipping related services or products to customers such as shipping

Limited Limited (50%)(50%)

SinfengSinfengMarine Services Marine Services Pte.Pte. Ltd. (100Ltd. (100%%) )

g

Double Rich Limited (18Double Rich Limited (18%%) )

Trading and Supply of Marine Fuel and Related Productspp g

companies, ship yards, container manufacturers, etc.

Property Investment

COSCO International Trading Co., Ltd COSCO International Trading Co., Ltd ((100100%)%)

SinoSino‐‐Ocean Land Holdings LimitedOcean Land Holdings Limited (3377.HK)(3377.HK)(16.85% or 949,937,399 shares)(16.85% or 949,937,399 shares)

General Trading

35*As of 31Dec 2009, the total number of issued shares is 1,510,697,429.

Corporate Profile - Business Network

Long Beach Beijing Zhuhai 1 10

NORTH AMERICA ASIA

Ship Trading Agency Services

Marine Insurance Brokerage Services

Supply of Marine Equipment and Spare Parts

Production and Sale of Container and Industrial Anti-corrosion Coatings

Production and Sale of Marine Coatings

New York

Rotterdam

Tianjin

Dalian

Qingdao

Shanghai

Fuzhou

Hong Kong

& Shenzhen

Malaysia

Singapore

2

3

4

5

6

78

11

12

13EUROPE

36

Trading and Supply of Marine Fuel and Related Products Guangzhou 9

Corporate Profile - Development Strategy

Development of To focus on the sustainable development of core business – shipping services, in order to achieve steady organic

p p gy

Current Businessesshipping services, in order to achieve steady organic

growth by exploring new markets, developing new products and targeting new customers.

To strengthen synergies among business segments inSynergies among Segments

To strengthen synergies among business segments in shipping services so as to realize maximization of overall results.

Development ofNew Businesses

To take proactive approach to identify new investment opportunities with the aim to expand the scale of core business – shipping services.pp g

Under the full support of COSCO Group and COSCO HK, COSCOInternational aims to be a specialized and leading shipping servicesp g pp gprovider by providing customers with diversified shipping relatedservices and products on the backup of a steadily growing Chinashipping services industry.

37

Historical Segment Results - Shipping Services

(HK$ mn)

38

Historical Segment Results - Shipping Services 1. Ship Trading Agency Services1. Ship Trading Agency Services

(HK$ mn) (HK$ mn)

Revenue Operating Profit

74%Operating Profit Margin

131

152

(HK$ mn)

*

(HK$ mn)

113

56%59%

64% 65%

74%Operating Profit Margin

83

56%49%

54 54 53

74

32

47

30 3226

30

2004 2005 2006 2007 2008 2009 2004 2005 2006 2007 2008 2009

39

* In which HK$ 105 mn or 69% was from controlling subsidiaries of COSCO Group.

Historical Segment Results - Shipping Services 2. Marine Insurance Brokerage Servicesg

Revenue Operating Profit(HK$ mn) (HK$ mn) Operating Profit Margin

*

70%

58%51%

66% 65%70%

3843

53

66 67*

3543

47

20

38

22 22

35

14

2004 2005 2006 2007 2008 2009

* In which HK$ 48 mn or 72% was from controlling subsidiaries of COSCO Group

2004 2005 2006 2007 2008 2009

40

In which HK$ 48 mn or 72% was from controlling subsidiaries of COSCO Group.

Historical Segment Results – Shipping Services 3. Supply of Marine Equipment and Spare Parts

(HK$ mn) (HK$ mn)

Revenue Operating Profit

Operating Profit Margin

350 351

455 445( $ )

* ( $ )

9%8%

312351

3122

28 21

33

7%

5%

7%

22 21

2004 2005 2006 2007 2008 20092004 2005 2006 2007 2008 2009

* In which HK$ 306 mn or 69% was from controlling subsidiaries of COSCO Group.

41

Historical Segment Results – Shipping Services 4. Production & Sale of Coatings (1) Container Coatings &

Industrial Anti-corrosion Coatings*

Revenue Operating Profit

1 228

1,580

1,381

(HK$ mn) (HK$ mn)Operating Profit Margin

894 903

1,228 9%8%

7%

400**

98 103

6780

5%5%

3%400 42

13

* By COSCO Kansai Companies (63.07%-64.71% owned subsidiaries).** In which HK$ 48 mn or 12% was from controlling subsidiaries and associated companies of COSCO Group.

2004 2005 2006 2007 2008 2009 2004 2005 2006 2007 2008 2009

42

Historical Segment Results – Shipping Services 4. Production & Sale of Coatings (2) Marine Coatings*g ( ) g

Sales Volume Operating Profit

23892,800

(Tonnes) (RMB mn)

72,014

10042,688

25

58 22,54828,920

9

2004 2005 2006 2007 2008 20092004 2005 2006 2007 2008 2009

43

* By Jotun COSCO (a 50% owned JCE).

Disclaimer

This presentation contains certain forward‐looking statements with respect to thefinancial condition, results of operations and business of COSCO International and, pcertain plans and prospects of the management of COSCO International.

Such forward‐looking statements involve known and unknown risks, uncertaintiesand other factors which may cause the actual result or performance of COSCOInternational to be materially different from any future results or performanceexpressed or implied by such forward looking statements. Such forward‐ lookingstatements are based on numerous assumptions regarding COSCO International’spresent and future business strategies and the political and economic environmentin which COSCO International will operate in the future.

The representations, analysis and advice made by COSCO International in thispresentation shall not be construed as recommendations for buying or sellingshares of COSCO International COSCO International shall not be responsible forshares of COSCO International. COSCO International shall not be responsible forany action or non‐action made according to the contents of this presentation.

44

Related Documents