CORPORATE TRANSITION Advanced Options Strategy For Privately Held Business Presented by: ATI Capital Group, Inc.

CORPORATE TRANSITION Advanced Options Strategy For Privately Held Business Presented by: ATI Capital Group, Inc.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CORPORATE TRANSITIONAdvanced Options Strategy

For

Privately Held BusinessPresented by:

ATI Capital Group, Inc.

Capital Markets

– An Overview

Sales($millions)

5 150 500 1,000

Small Lower Middle Upper Large

Businesses M I d d l e M a r k e t Companies

2-3x 4-7x 8-9x 10-11x >12x

5.4MM 300,000 2,000

ATICG © 2001-2005 ATI Capital Group, Inc. 3

Potential Buyers

• A Corporation

• An Individual

• A Qualified Plan

ATICG © 2001-2005 ATI Capital Group, Inc. 4

Where to Get Stock in a Private Company

• From the Corporation that MAKES IT!

• From an Existing Shareholder

Employees Family Co-Owners Outside

[Retire] Outside [Continue] Public

Charitable Trusts

T R A N S F E R M O T I V E S

T R A N S F E R M E T H O D S

ESOPs Management

Buyouts/Ins Phantom Stock Stock Appre- ciation Rights

Charitable Remainder

Trusts Charitable

Lead Trusts

Outright Gifts SCINs Annuities GRATs FLPs IDGTs

Negotiated One-Step Private Auctions Two-Step Private

Auctions

Consolidate Roll-ups Buy and Build Recapitali- zations

Initial Public Offerings

Direct Public Offerings

Reverse Mergers

Going Private

INTERNAL TRANSFERS

EXTERNAL TRANSFERS

Buy/Sell Russian

Roulette Dutch

Auction Right of

First Refusal

T R A N S F E R C H A N N E L S

Business Transfer Spectrum

External Transfers

● These are typically the big liquidity events

● The market value world dominates here

● 3 Subworlds: Asset, Financial, and Synergy

● We don’t want to transfer in Asset market value (although most private companies will transfer in this Sub-world)

It’s a Recast World

Which level of earnings do you choose?

● Reported EBITDA

● Recast EBITDA

● Synergized recast EBITDA

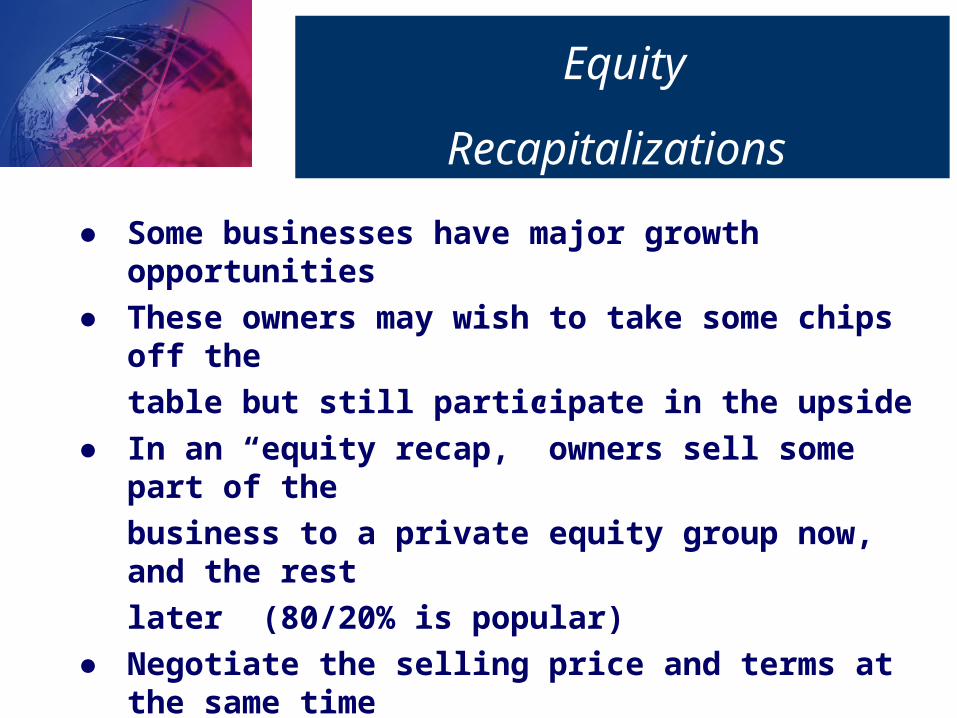

Equity

Recapitalizations

● Some businesses have major growth opportunities

● These owners may wish to take some chips off the

table but still participate in the upside

● In an “equity recap,” owners sell some part of the

business to a private equity group now, and the rest

later (80/20% is popular)

● Negotiate the selling price and terms at the same time

● The second sale in 5-6 years usually nets more to the

owner than the first sale

ATICG © 2001-2005 ATI Capital Group, Inc. 9

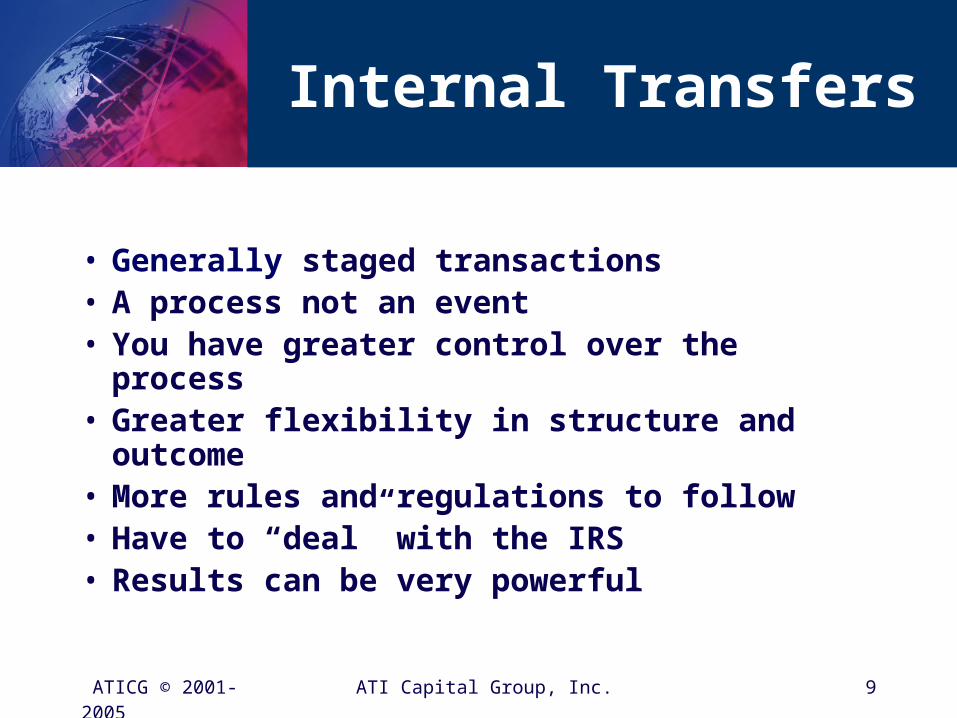

Internal Transfers

• Generally staged transactions• A process not an event• You have greater control over the process• Greater flexibility in structure and outcome• More rules and regulations to follow• Have to “deal” with the IRS• Results can be very powerful

ATICG © 2001-2005 ATI Capital Group, Inc. 10

What is an ESOP

• ESOP = Employee Stock Ownership Plan• An ESOP is a QUALIFIED PLAN under

the Employees’ Retirement Income Security Act of 1974 (ERISA)

• See Sections 401(a), 4975(e)(7), and 501(a) of the Internal Revenue Code of 1986, as amended, and Section 407(d)(6) of ERISA, 1974

ATICG © 2001-2005 ATI Capital Group, Inc. 11

Unique Features of ESOT

An ESOP trust “ESOT” has three very unique features:

1. ESOT must own “principally” stock in its sponsor company.

2. An ESOT is the ONLY qualified plan under ERISA allowed to BORROW MONEY!!

3. The trust can purchase the Company in “Stages” (multiple transactions).

ATICG © 2001-2005 ATI Capital Group, Inc. 12

Powerful Use #1: Exit Strategy

ESOP

$ Loan 2

Stock

$3

QRPsSec. 1042

QualifiedReplacementProperty= Stocks& Bonds

Div

’d $

$ 4

5

Collateral

No Tax onTransactionCompany

Deducts Princ.On Loan

Lender

The BasicTransaction

Corporation

1$ Loan

ATICG © 2001-2005 ATI Capital Group, Inc. 13

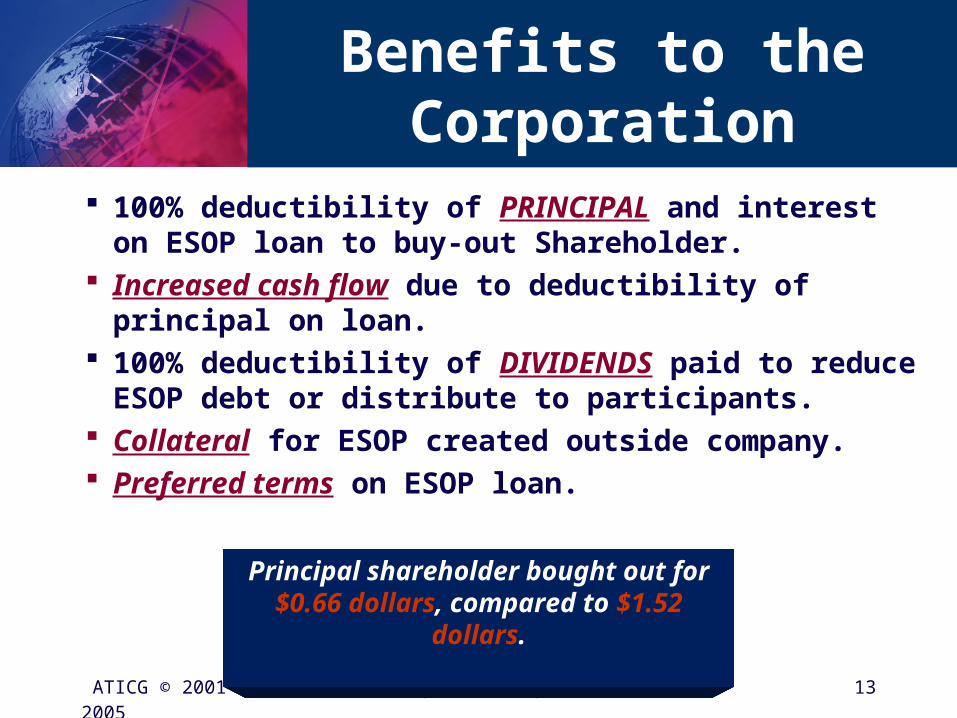

Benefits to the Corporation

100% deductibility of PRINCIPAL and interest on ESOP loan to buy-out Shareholder.

Increased cash flow due to deductibility of principal on loan.

100% deductibility of DIVIDENDS paid to reduce ESOP debt or distribute to participants.

Collateral for ESOP created outside company. Preferred terms on ESOP loan.

Principal shareholder bought out for $0.66 dollars, compared to $1.52 dollars.

ATICG © 2001-2005 ATI Capital Group, Inc. 14

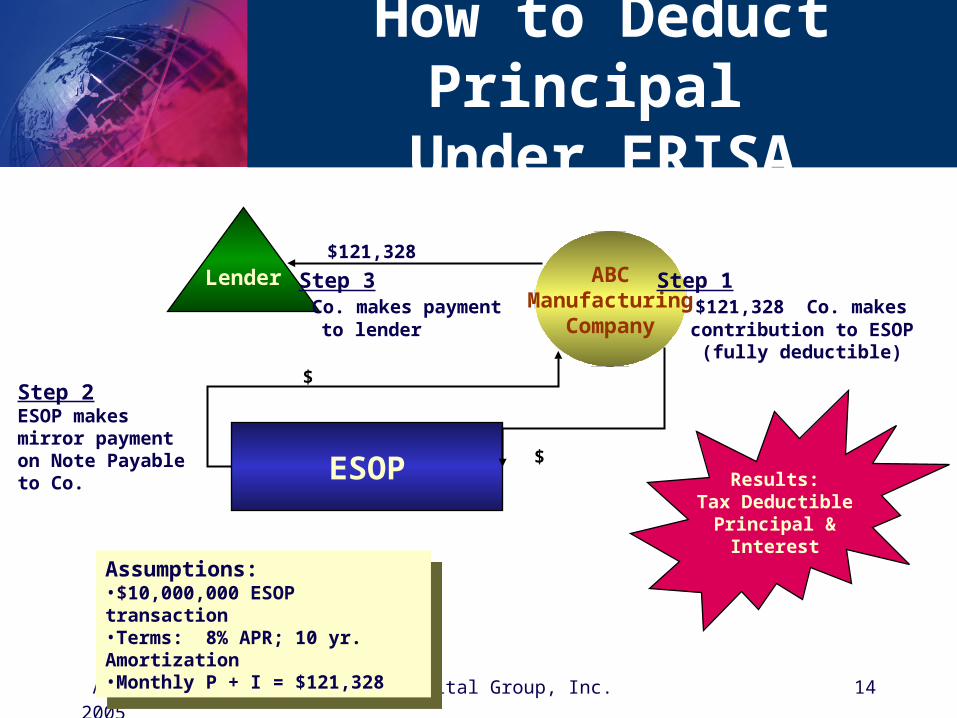

How to Deduct Principal Under ERISA

Results:Tax Deductible

Principal &Interest

Assumptions:•$10,000,000 ESOP transaction•Terms: 8% APR; 10 yr. Amortization•Monthly P + I = $121,328

Assumptions:•$10,000,000 ESOP transaction•Terms: 8% APR; 10 yr. Amortization•Monthly P + I = $121,328

Lender Step 3 Co. makes payment to lender

$121,328

Step 2 ESOP makes mirror payment on Note Payable to Co.

$

ESOP

ABCManufacturing

Company

Step 1 $121,328 Co. makes contribution to ESOP (fully deductible)

$

ATICG © 2001-2005 ATI Capital Group, Inc. 15

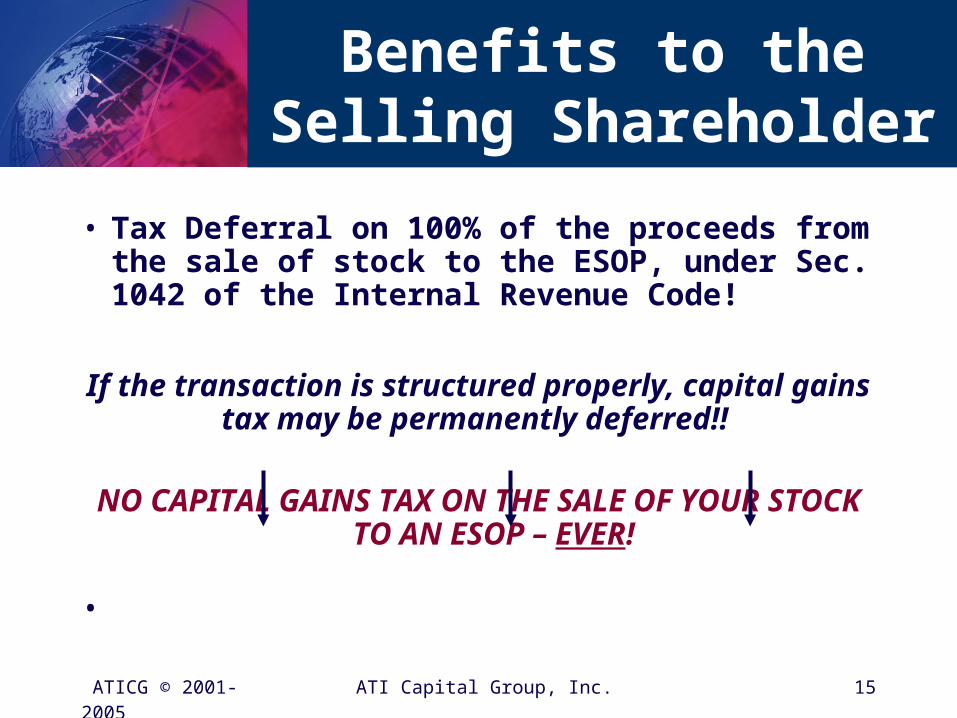

Benefits to the Selling Shareholder

• Tax Deferral on 100% of the proceeds from the sale of stock to the ESOP, under Sec. 1042 of the Internal Revenue Code!

If the transaction is structured properly, capital gains tax may be permanently deferred!!

NO CAPITAL GAINS TAX ON THE SALE OF YOUR STOCK TO AN ESOP – EVER!

•

ATICG © 2001-2005 ATI Capital Group, Inc. 16

Powerful USE #2: Purchase of Capital Goods

Lender

Corporation

ESOP

CapitalGoods

1$ Loan

$ Loan 2 Stoc

k

3

4

5

The BasicTransaction

Collateral

Capital GoodsPurchased WithPre-Tax Dollars =INCREASED CASH FLOW

$ C

ash

$ Cash

Cap. Goods

CAUTION:Dilution!!

ATICG © 2001-2005 ATI Capital Group, Inc. 17

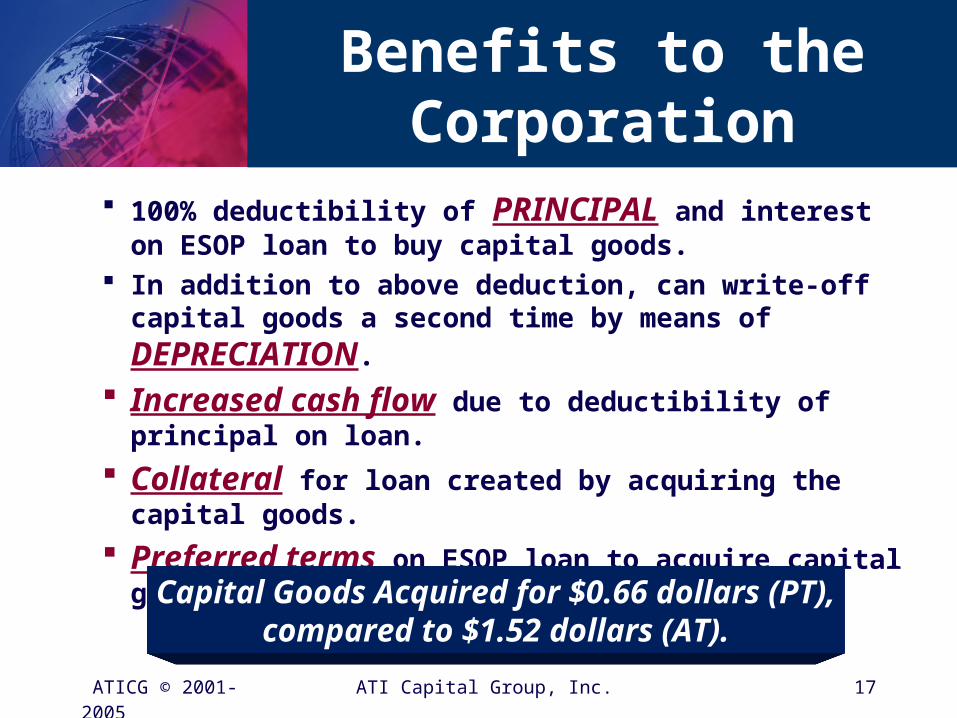

Benefits to the Corporation

100% deductibility of PRINCIPAL and interest on ESOP loan to buy capital goods.

In addition to above deduction, can write-off capital goods a

second time by means of DEPRECIATION.

Increased cash flow due to deductibility of principal on loan.

Collateral for loan created by acquiring the capital goods.

Preferred terms on ESOP loan to acquire capital goods.

Capital Goods Acquired for $0.66 dollars (PT),compared to $1.52 dollars (AT).

Consolidation Math Game

Sales($millions)

5 150 500 1,000

2-3x 4-7x 8-9x 10-11x >12x

Small Lower Middle Upper Large

Businesses M I d d l e M a r k e t Companies

The Rules of this Game

● Identify your market segment

● You have a platform company

● Determine which competitors are not adding value

● Go after all of them at once

● Use the Head-’n-Shoulders approach

● The toughest part is integrating the operations

● Don’t fall in love with the result

ATICG © 2001-2005 ATI Capital Group, Inc. 20

Powerful USE #3: Purchase of a Target Company

Lender

Corporation

ESOP

TargetCompany

1$ Loan

$ Loan 2 Stoc

k

3

4

5

The BasicTransaction

Collateral

Target CompanyPurchased WithPre-Tax Dollars =INCREASED RETURN ON INV.

$ C

ash

$ Cash

Ownership

CAUTION:Dilution!!

ATICG © 2001-2005 ATI Capital Group, Inc. 21

Benefits to the Corporation

100% deductibility of PRINCIPAL and interest on ESOP loan to buy Target Company.

Increased cash flow due to deductibility of principal on loan.

Collateral for loan created by acquiring the Target Company.

Preferred terms on ESOP loan to acquire Target Company.

Target Company Acquired for $0.66 dollars (PT),compared to $1.52 dollars (AT).

The Rules of this Game

● Identify your market segment

● You have a platform company

● Determine which competitors are not adding value

● Go after them one at time

● Take advantage of the tax savings

● Use the Head-’n-Shoulders approach

● The toughest part is integrating the operations

● Stop when you have had enough & achieve the rest through internal growth

Related Documents