Globalization of Natural Gas Markets Working Papers WP-GG-17 Corporate Strategies along the LNG Value Added Chain - An Empirical Analysis of the Determinants of Vertical Integration Sophia Rüster and Anne Neumann September, 2006 Chair of Energy Economics and German Institute for Public Sector Management Economic Research Dresden University of Technology

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Globalization of Natural Gas Markets Working Papers

WP-GG-17

Corporate Strategies along the LNG Value

Added Chain - An Empirical Analysis of the

Determinants of Vertical Integration

Sophia Rüster and Anne Neumann

September, 2006

Chair of Energy Economics and German Institute for Public Sector Management Economic Research Dresden University of Technology

II

Corporate Strategies along the LNG Value Added Chain

An Empirical Analysis of the Determinants of Vertical Integration

Sophia Ruester1 and Anne Neumann

Correspondent author: Sophia Rüster Dresden University of Technology Dpt. of Business and Economics Chair of Energy Economics and Public Sector Management D-01062 Dresden Germany Phone: +49-351-463-39769 Fax: +49-351-463-39763 Mail: [email protected] URL: www.ee2.biz

Abstract This study analyzes corporate strategies in the emerging global LNG market. In particular, we provide an empirical analysis of the determinants driving companies towards increasing vertical integration. Our hypothesis is that high transaction costs along the LNG value added chain induce a higher degree of vertical integration. This hypothesis is tested by implementing ordered response models. To explain determinants of vertical integration in the LNG industry we derive proxy variables by using explicit project data on 85 LNG (importing and exporting) projects worldwide. The transaction cost attributes asset specificity, uncertainty and frequency are measured. Additionally, we include industry and firm characteristics into the analysis. Our results show that players active in LNG export projects are characterized by a higher degree of vertical integration than those situated on the importing side of the value chain. The extent of investments in specific assets has a positive impact on the degree of vertical integration and the level of vertical integration has increased significantly with start up dates of projects since 2002. Private companies’ degree of vertical integration exceeds the degree of vertical integration of state-owned entities. Players tend to be more integrated with rising firm size and frequency of transactions in the LNG industry. We show that for value chains situated in the Atlantic Basin (in contrast to the Pacific Basin) the degree of vertical integration is higher. This is particularly the case for value chains connecting to European instead of North American import markets. Keywords: liquefied natural gas, vertical integration, LNG value chain, corporate strategies JEL-Codes: D23, L22, L95

1 This study is based on the Diploma Thesis of Ruester (2006). We thank Christian von Hirschhausen (Dresden University of Technology), Karsten Neuhoff (University of Cambridge), participants of a seminar at Groupe Réseaux Jean Monnet (University Paris Sud), participants of the 1st Enerday Workshop 2006 (Dresden University of Technology), participants of the ESNIE Summer School 2006 in Cargèse, and participants of the 29th IAEE International Conference held in Potsdam for helpful comments and suggestions. The usual disclaimer applies.

III

Table of Contents

Abstract

Table of Contents

List of Figures

List of Tables

Abbreviations

Executive Summary

1 Introduction

2 The (Liquefied) Natural Gas Sector and Corporate Strategies

2.1 Liquefied Natural Gas Business – From Infant towards Maturing Industry

2.2 Natural Gas Importing Regions – A Focus on Liquefied Natural Gas

2.3 Changing Corporate Strategies – Integrated Companies, Tollers, and New Entrants

3 Transaction Costs: A Literature Survey

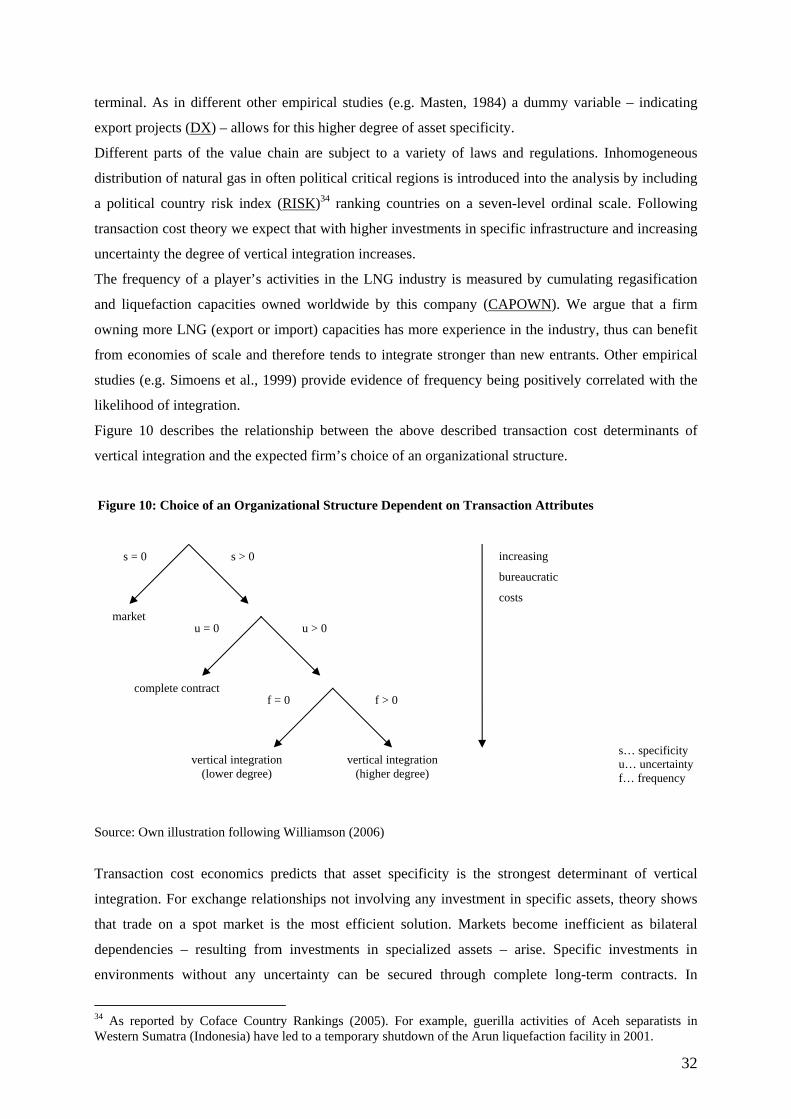

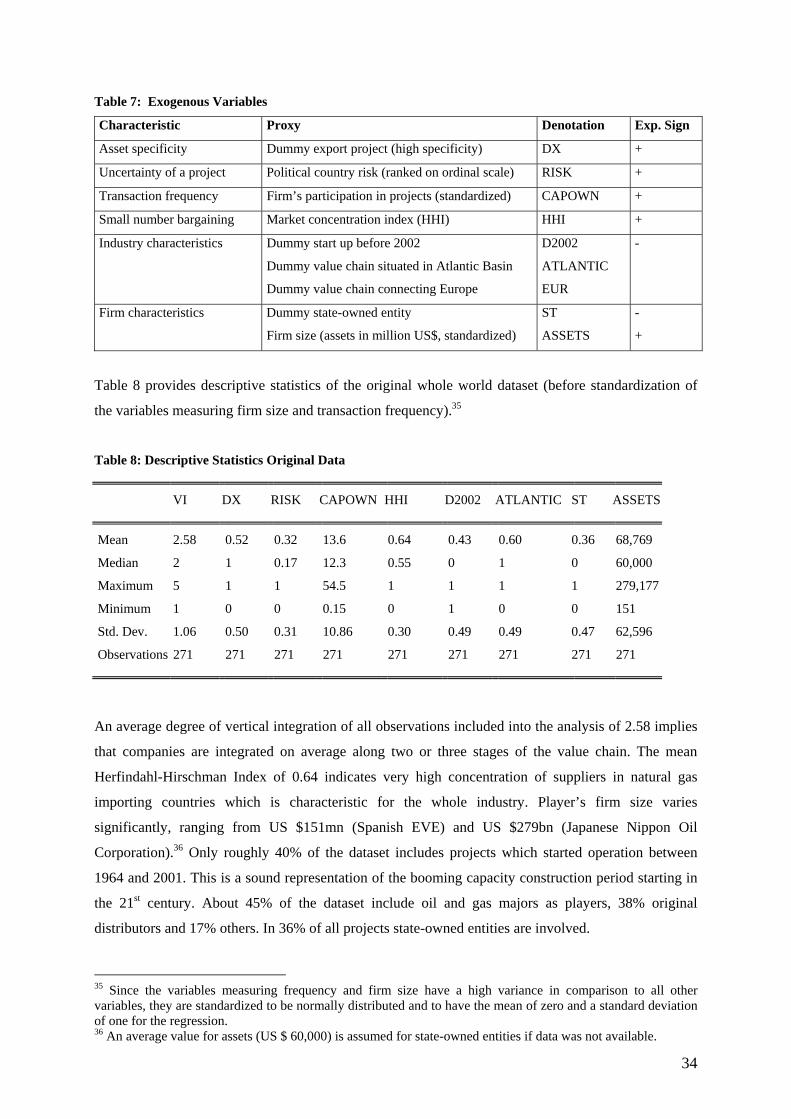

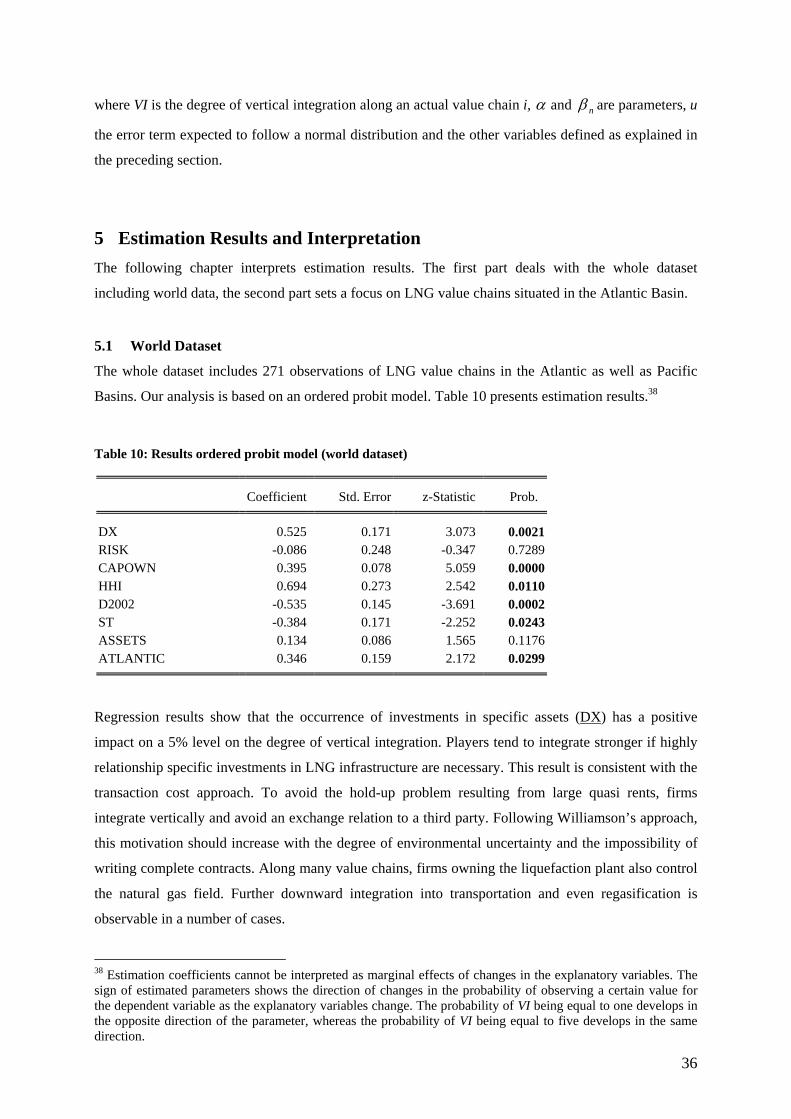

4 Data and Methodology

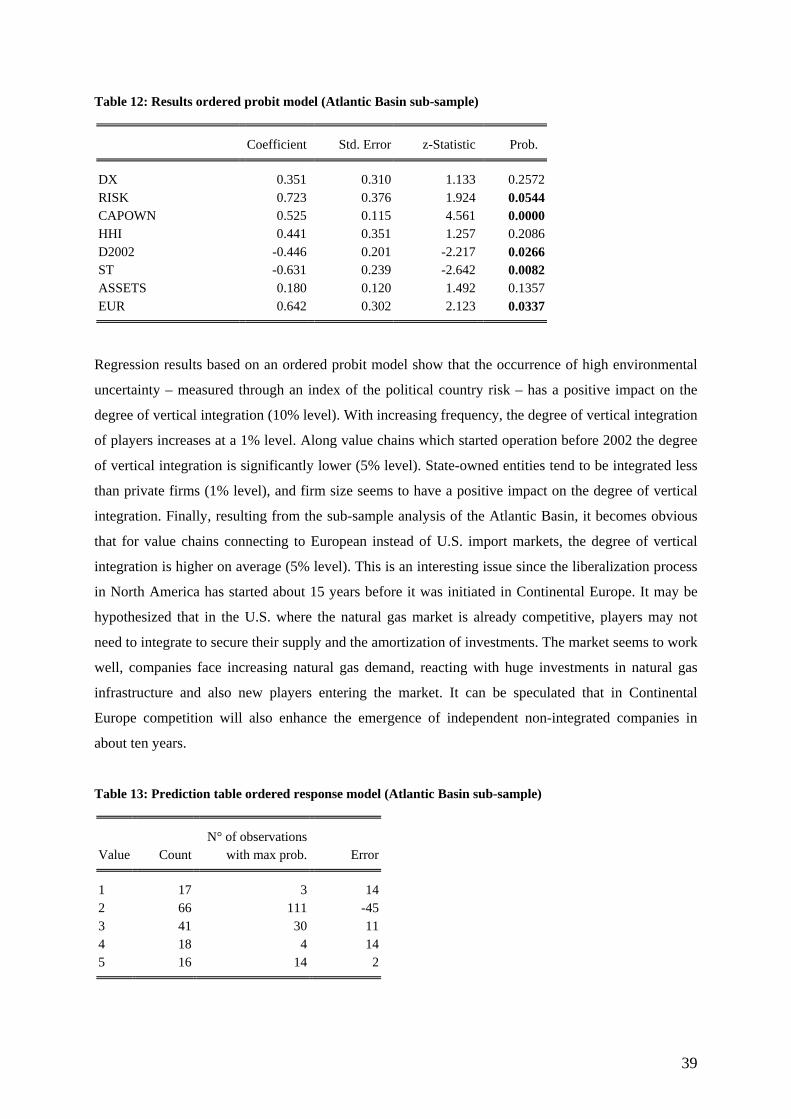

5 Estimation Results and Interpretation

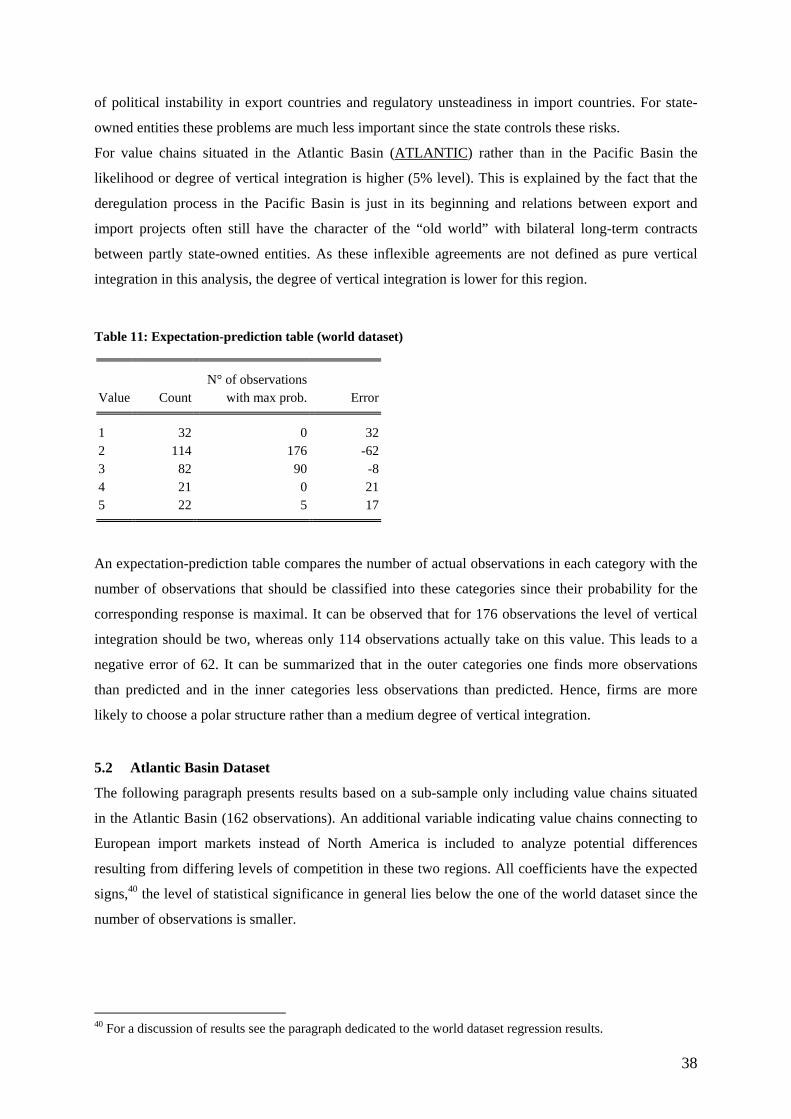

5.1 World Dataset

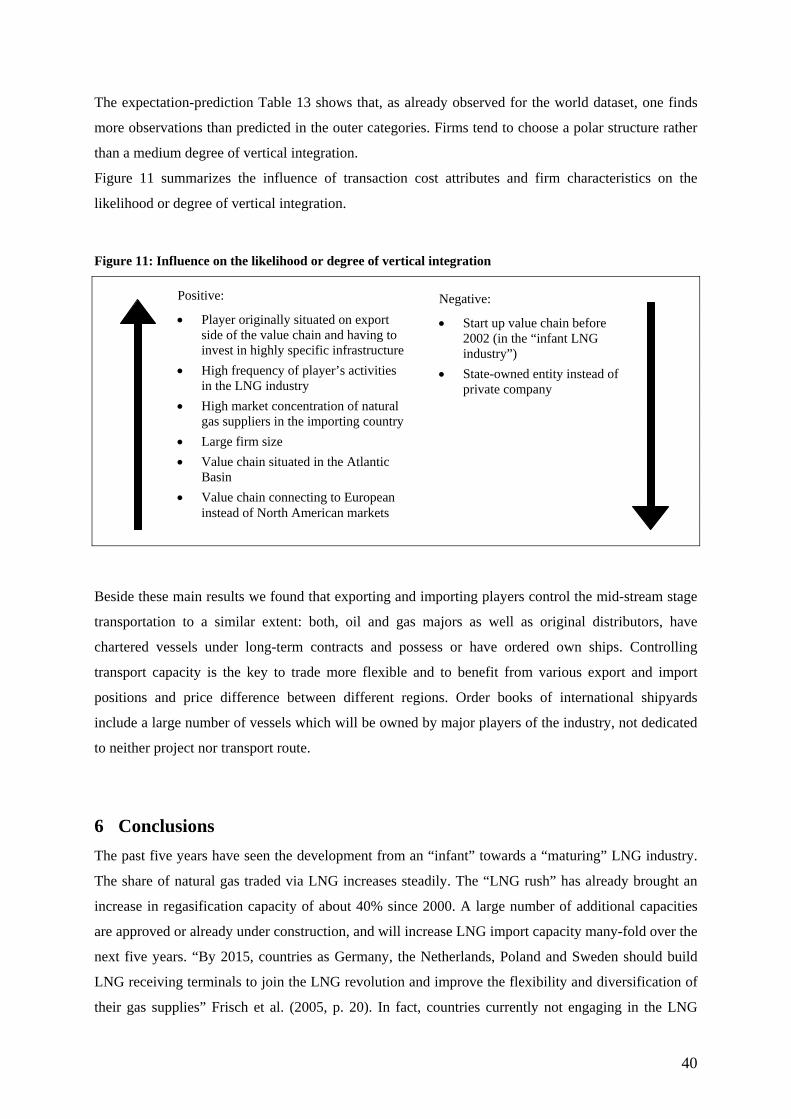

5.2 Atlantic Basin Dataset

6 Conclusions

References

Appendices

II

III

IV

IV

V

1

3

5

6

13

24

28

30

36

36

38

40

42

IV

List of Figures

Figure 1: The LNG value chain 6 Figure 2: Costs of gas, oil, and coal transportation 7 Figure 3: Capital costs for different LNG value chains 8 Figure 4: Average train capacities of new built liquefaction facilities 9 Figure 5: LNG vessel capacity development 9 Figure 6: Average costs per new built MTPA liquefaction capacity 10 Figure 7: Supply structure of different natural gas importing regions 14 Figure 8: Development of LNG import capacities worldwide until 2010 15 Figure 9: Country matrix measuring capacity development and LNG dependency 22 Figure 10: Choice of an Organizational Structure Dependent on Transaction Attributes 32 Figure 11: Influence on the likelihood or degree of vertical integration 40

List of Tables

Table 1: LNG imports by country 2005 14 Table 2: Existing U.S. LNG import terminals 16 Table 3: Existing European LNG import facilities 18 Table 4: European LNG import facilities (under construction or planned) 19 Table 5: Interpretation of the country matrix 23 Table 6: Global players' activities along the LNG value chain 25 Table 7: Exogenous Variables 34 Table 8: Descriptive Statistics Original Data 34 Table 9: Correlation Matrix Independent Variables 35 Table 10: Results ordered probit model (world dataset) 36 Table 11: Expectation-prediction table (world dataset) 38 Table 12: Results ordered probit model (Atlantic Basin sub-sample) 39 Table 13: Prediction table ordered response model (Atlantic Basin sub-sample) 39

V

Abbreviations

°C degree Celsius

°F degree Fahrenheit

bcf/d billion cubic feet per day

bcm billion cubic meter

bcm/a billion cubic meter per year

BG British Gas

bn billion

c.i.f. cost, insurance, freight

cm cubic meter

EDF Electricité de France

EIA Energy Information Administration

EU European Union

FERC Federal Energy Regulatory Commission

f.o.b. free on board

GDF Gaz de France

GDP gross domestic product

IEA International Energy Agency

IEEJ Institute of Energy Economics Japan

km kilometer

LNG liquefied natural gas

MARAD U.S. Maritime Administration

MBtu million British thermal units

MJ mega joule

MMscf/d million standard cubic feet per day

mn million

mtpa million tons per year

MWh mega Watt hour

n.a. not available

NBP National Balancing Point United Kingdom

OLS ordinary least squares

tba to be announced

TPA Third party access

UK United Kingdom

U.S. United States

1

Executive Summary Transportation of natural gas via LNG has been around for 40 years, but it is only now that it

increasingly gains in importance. According to IEA (2005b) natural gas demand will reach a share of

25% of total energy demand in 2030. This development is driven by several factors, ranging from

supply security to environmental concerns. In times of rising energy needs worldwide and expected

competition between demand regions – new (Asian) importers with strong economic growth enter the

stage – security of supply issues are on the political agenda.

The past five years have seen the development from an “infant” towards a “maturing” LNG industry.

Even if LNG technologies enabled transport over longer distances, shipping remained expensive and

markets therefore regional in nature in the “old world”. Most of the infrastructure along LNG value

chains remained under state control; trade was based on inflexible bilateral long-term contracts with

take-or-pay and destination clauses. Transport capacity was assigned to dedicated import and export

projects and routes. Fostered by increasing natural gas demand, investments in LNG infrastructure

grew rapidly during the 1990s. Today, LNG has turned from being an expensive and only regionally

traded fuel to a globally traded source of energy with rapidly diminishing cost. LNG plays an

increasing role in the energy supply of all major coastal countries such as the United States, the UK,

Spain, South Korea, India or China. The number of countries and companies participating in the

industry rises continuously. The Middle East, accounting for more than 40% of worldwide proven

natural gas reserves, will become the largest LNG exporting region and currently evolves to a swing

producer; deliveries to European as well as Asian markets are feasible without a significant difference

in (transportation) cost.

Changes in the institutional framework have moved the industry away from monopolistic structures

towards competition, thus stipulating fundamental changes in the organizational behavior of market

participants. Increasing competition, mirrored by functioning spot markets, a gain in contract

flexibility and increasing international trade, put traditional players (incumbents) under pressure.

Recent years have been characterized by integration and strategic partnerships becoming a common

corporate behavior in the industry. Global oil and natural gas producing companies as well as original

distributors heavily engage in all stages of the value chain of LNG production. Cornot-Gandolphe

(2005) and Iniss (2004) indicate that the coexistence of long- and short-term trading activities is

increasingly accompanied by vertical integration in the LNG industry. But we also observe a number

of new entrants into the market, currently mainly in North America, where the natural gas market is

characterized by functioning competition.

Based on a dataset constructed using detailed information about 85 LNG projects worldwide, we

analyze the determinants of vertical integration in the LNG industry under a transaction cost view. We

confirm our main hypothesis that increasing transaction costs lead to a higher degree of vertical

integration. Additionally, we show that the occurrence of investments in specific assets has a positive

impact on the degree of vertical integration. Players tend to integrate more strongly if highly

2

relationship specific investments in LNG infrastructure are required. Along many value chains, firms

owning the liquefaction plant also control the natural gas field. Further downward integration into

transportation and even regasification is observable in a number of cases. With increasing frequency

of transactions in the LNG industry players tend to be integrated to a higher extent. This results from

increasing experience on the one hand and the possibility to benefit from economies of scale on the

other hand. Furthermore, the higher the market concentration of natural gas suppliers in the importing

country, the higher transaction costs resulting from small number bargaining and the higher the

motivation to integrate downstream into distribution and marketing of natural gas to avoid these costs.

In addition, we show that a shift in corporate strategies has taken place. Vertical integration becomes

more common to secure supply in times of increasing demand worldwide and the amortization of

capital intensive specific investments. Estimation results show that with start up dates of value chains

from 2002 on, the degree of vertical integration has increased significantly.

We also can show that larger firms are more integrated. This is due to an increasing ability to finance

integration investing in infrastructure and human capital, potentially merging other companies,

organizing strategic partnerships and joint ventures. State-owned entities are less integrated than

private firms, typically controlling one to two stages of the value chain (exploration/production and

liquefaction or regasification and marketing).

Value chains situated in the Atlantic Basin, as compared to the Pacific Basin, display a higher degree

of vertical integration. The deregulation process in the Pacific Basin is just in its beginning and

relations between export and import projects still have the character of the “old world” with bilateral

long-term contracts between partly state-owned entities.

Finally, resulting from the sub-sample analysis of the Atlantic Basin, it becomes obvious that for value

chains connecting to European instead of U.S. import markets, the degree of vertical integration on

average is higher. This is an interesting issue since the liberalization process in North America has

started about 15 years before it was initiated in Continental Europe. It might be that in the U.S. where

the natural gas market is already competitive, players do not need to integrate to secure their supply

and the amortization of investments. The market seems to work well, companies face increasing

natural gas demand, reacting with large investments in natural gas infrastructure and also new players

entering the market. It can be speculated that in Continental Europe competition will also enhance the

emergence of independent non-integrated companies in the future.

3

1 Introduction This study analyzes corporate strategies in the emerging global liquefied natural gas market. In

particular, we provide an empirical study of the determinants pushing companies towards vertical

integration, a trend recently observed in a large number of cases (see Iniss, 2004, p. 12). The dataset

was developed using detailed information on 85 LNG projects – both export and import – worldwide.

We test the main hypothesis of increasing transaction costs along the LNG value chain inducing a

higher degree of vertical integration applying ordered probit estimation.

According to IEA (2005b, p. I.3) natural gas demand will increase more in absolute terms than that of

any other primary energy source and reach a share of 25% of total energy demand in 2030. This is

driven by several factors, ranging from supply security to environmental concerns. In times of raising

energy needs worldwide and expected competition between demanding regions – new (Asian)

importers with strong economic growth enter the stage – security of supply issues are on the political

agenda. Increasing the share of natural gas in the energy mix reduces oil dependency; importing the

fuel in the form of LNG via sea transport technically enables deliveries from numerous sources all

over the world. Countries dependent on natural gas imports diversify their portfolios of energy sources

as well as suppliers. Natural gas has the advantage of being a clean fuel due to its favorable hydrogen-

carbon ratio. Furthermore, with the development of the gas-fired combined cycle technology,

electricity generation with a thermal efficiency of about 60 percent can be achieved, whereas

traditional steam boilers feature efficiencies below 40 percent. For countries applying the Kyoto

Protocol, natural gas often becomes the fuel of choice.

Transporting natural gas via LNG has been around for 40 years, but it is only now that it increasingly

gains in importance. The first tanker shipment of LNG – an experimental vessel – took place from

Lake Charles in the U.S. to Canvey Island in the UK in 1958. Transport of natural gas via pipelines

remained the only option until 1964 when the UK was the first country receiving a commercial cargo

of LNG supplied by the Algerian Sonatrach. However, natural gas transportation is more capital

intense than oil or coal shipping since the fuel has a lower density and therefore a lower energy

content per volume unit. Prices between different geographic locations may differ substantially. Break

even of pipeline and LNG transport is achieved at about 3,000 km (Jensen, 2004, p. 7).

The past five years have seen the development from an “infant” towards a “maturing” LNG industry.

Even if LNG technologies enabled transport over longer distances, transport remained expensive and

markets therefore regional in nature in the old world. Most of the infrastructure along LNG value

chains remained under state control, private or foreign companies were hardly involved and markets

were not competitive. Inflexible bilateral long-term contracts with take-or-pay and destination clauses

between the LNG export project as seller and national energy companies as buyers secured

infrastructure investments on the one hand and security of supply on the other hand. These contracts

were signed before any investment took place. A crucial element, ship ownership, was traditionally

4

embedded in these contracts; with transportation capacity thus dedicated to special import and export

projects and routes.

Fostered by increasing natural gas demand, investments in LNG infrastructure grew rapidly during the

1990s. Liquefied natural gas has turned from being an expensive and only regionally traded fuel to a

globally traded source of energy with rapidly diminishing cost. Today, LNG plays an increasing role

in the energy supply of all major coastal countries such as the United States, the UK, Spain, South

Korea, India or China. The number of countries and companies participating in the industry rises

continuously. For a survey of the globalizing LNG market see Jensen (2004). Making large volumes

of natural gas accessible for importing regions, bulky investments in asset specific infrastructure along

the whole value chain remain a crucial issue. During the last five years 46 billion cubic meters (bcm)

of regasification capacity started operation worldwide (11.3% of today’s capacity), an additional 140

bcm are expected to come on stream until 2010. The Middle East, accounting for more than 40% of

worldwide proven natural gas reserves, will become the largest LNG exporting region and currently

evolves to a swing producer; deliveries to European as well as Asian markets are feasible without a

significant difference in (transportation) cost.

Changes in the institutional framework have moved the industry away from monopolistic structures

towards competition thus stipulating fundamental changes in the organizational behavior of market

participants. Increasing competition, mirrored by functioning spot markets, a gain in contract

flexibility and increasing international trade, put traditional players (incumbents) under pressure.

Recent years have been characterized by integration and strategic partnerships becoming a common

corporate behavior in the industry. Global oil and natural gas producing companies as well as original

distributors heavily engage in all stages of the value chain of LNG production. Export projects, a long

time dominated by state-owned entities, are increasingly developed by private oil and gas companies.

Former (European) monopolists of natural gas are facing their traditional markets challenged by the

intrusion of oil and gas majors integrating downstream into import markets. Vertical integration in

response to market deregulation features several drivers: upstream producers aiming to benefit from

downstream margins, ownership of transportation capacities to exploit arbitraging possibilities, and

distribution and power companies moving upstream to ensure margins and security of supply in times

of increasing demand worldwide. Several publications (e.g. Cornot-Gandolphe (2005), Iniss (2004))

focus on activities in LNG trade in the Atlantic Basin and indicate that coexistence of long- and short-

term trading activities is increasingly accompanied by vertical integration in the LNG industry. Nissen

(2006) describes the commercial model of LNG trade.

However, vertical integration, strategic partnerships and mergers lead to an industry in which a small

number of large and powerful players are active. Jensen (2004, p. 4) argues that in the developing

global LNG market “super majors” will play an important role. Vertical integration along the value

chain limits competition at the horizontal level thus counteracting liberalization efforts in downstream

markets.

5

A large number of empirical case studies examine firms’ motivation to choose alternative institutions

of governance and determinants of vertical integration in different industries, such as Monteverde and

Teece (1982), Masten (1984), and Klein (1988) focusing on make-or-buy decisions in the

manufacturing sector. The work of Joskow (1985), discussing coal fired power plants in the U.S.,

distinguishes between different situations leading to coal procurement on spot markets, based on long-

term contracts or through vertical integration. An in-depth overview on existing empirical work is

provided by Klein (2004). All mentioned case studies explain vertical integration by institutional

factors basically represented by proxy variables for transaction costs, industry- and firm characteristics

and other exogenous factors.

This study is placed in the continuation of this literature analyzing the determinants of vertical

integration in the LNG industry from the perspective of transaction cost economics. The main

hypothesis of increasing transaction costs along the LNG value chain (mainly due to increasing asset

specificity and uncertainty) leading to a higher degree of vertical integration is tested applying ordered

response models. The main findings are consistent with theory. It can be shown that investments in

specific infrastructure have a positive impact on the likelihood of vertical integration. The extent of

vertical integration has increased significantly with project start up dates later than 2002, which can

possibly be explained as firms’ response to changes in the institutional environment due to the

liberalization of natural gas markets. Furthermore, private companies’ degree of vertical integration

exceeds the one of state-owned entities. With rising firm size and frequency of transactions in the

LNG industry players tend to be more integrated, which is explained by the increasing capability of

financing integration and benefits from experience and economies of scale. Furthermore, we show that

for value chains situated in the Atlantic Basin (in contrast to the Pacific Basin) the degree of vertical

integration is higher. This is particularly the case for value chains connecting to European instead of

North American import markets.

The remainder of this study is organized as follows: Section 2 provides a technical overview on the

development of the LNG industry, discusses different characteristics of three main natural gas

importing regions worldwide, and analyzes actual corporate strategies. Section 3 summarizes the

theoretical framework. Section 4 describes the dataset and introduces the econometric methodology. In

Section 5 estimation results for the whole world dataset as well as a sub-sample focusing on Atlantic

Basin value chains are presented and interpreted before Section 6 concludes.

2 The (Liquefied) Natural Gas Sector and Corporate Strategies This section describes the (liquefied) natural gas sector and corporate strategies. It points out varying

characteristics of different natural gas importing regions worldwide: the competitive U.S. market,

European countries currently liberalizing the industry, and Asian markets which are strongly

6

dependent on LNG imports and where liberalization is slow. Evolving corporate strategies resulting

from changing industry structures are discussed.

2.1 Liquefied Natural Gas Business – From Infant towards a Maturing Industry

The following paragraphs describe the LNG value chain, focusing on technical issues, cost structure

and economic improvements; and discus changes in this (currently enormously expanding) industry.

2.1.1 Liquefied natural gas value chain

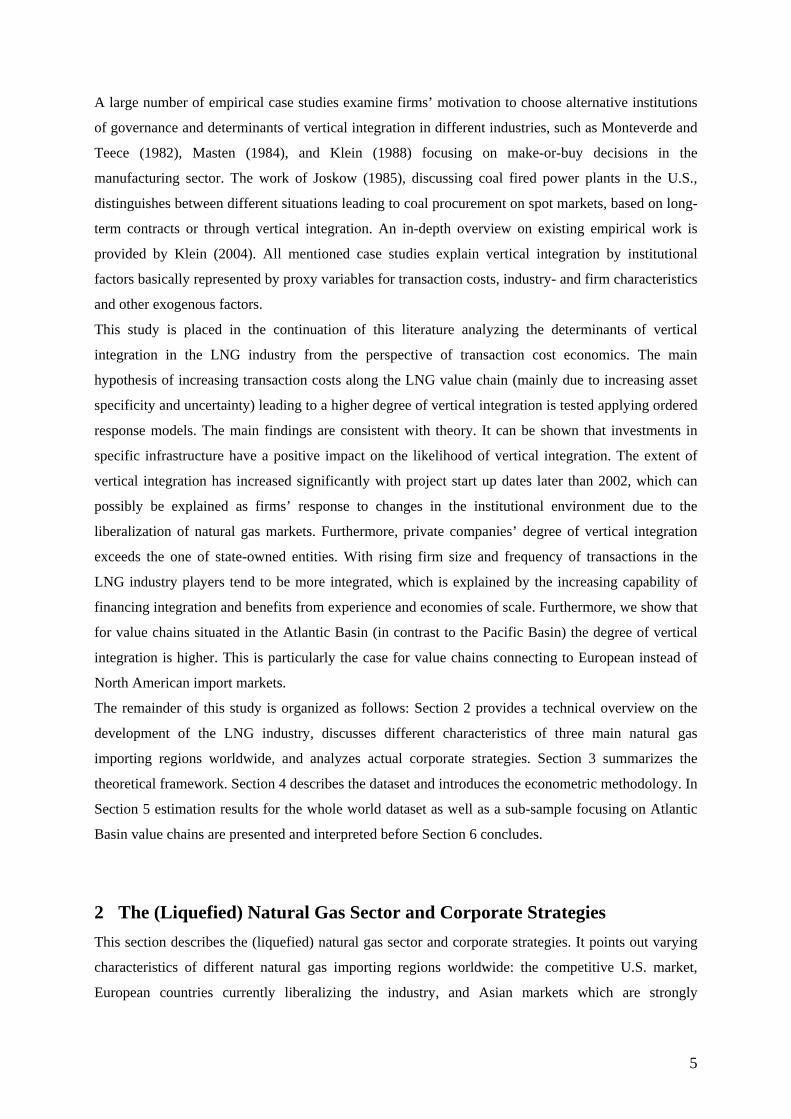

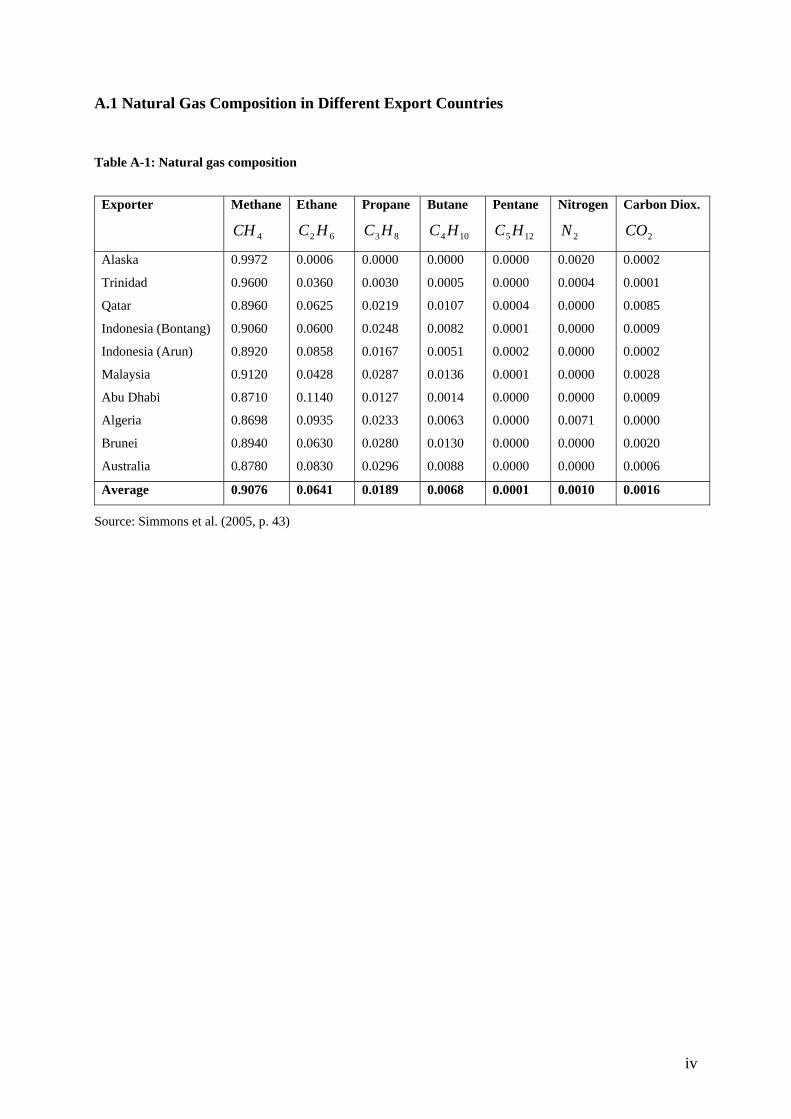

LNG is an odorless, colorless, non-corrosive, and non-toxic cryogenic liquid. It consists to around 90

percent of methane (e.g. Abu Dhabi 87.1%, Alaska 99.72%, see Appendix 1). Figure 1 depicts the

LNG value chain consisting of five stages, from field development in export regions over liquefaction,

transportation, and regasification to sales and marketing of natural gas in the importing country.2

Figure 1: The LNG value chain

Following exploration and production from onshore or offshore fields (stage 1), natural gas is

transported per pipelines to the liquefaction facility,3 where it has to be pre-treated. Natural gas liquids

and all components that would freeze under cryogenic temperatures (propane, butane, ethane, carbon

dioxide, and water) have to be removed. Under atmospheric pressure using a cooling process, the gas

is cooled down to 111K (-161°C or -259°F), thus becoming liquid and shrinking to about 1/600th of its

original volume (stage 2).4 This process takes place in a unit called “train”; a liquefaction plant in

general consists of several parallel trains whose capacity is determined and limited by the size of

available compressors. Liquefied natural gas is loaded into specially constructed vessels, containing

complex cooling and insulation systems which are essential to keep the gas liquid. Today, two types of

tankers are common, Moss design (spherical tanks) and Membrane design (tanks in the form of the

cargo). Typical size of a ship is about 138,000 cm; larger designs up to 250,000 cm are currently under 2 Other authors define the LNG value chain as consisting only of three stages; exploration and production are seen as part of the liquefaction project, sales and marketing are eliminated (see e.g. IEEJ, 2003, p. 8). 3 Pipelines from the field to a liquefaction plant are considered as part of the “liquefaction project”, so are storage tanks, loading equipment and other operational facilities. 4 Among different methods to liquefy natural gas, today, the LNG market is dominated by two technologies. For Air Products’ Pre-Cooled Mixed Refrigerant Process (82% of all existing terminals, see Simmons, 2006, p. 45) propane is used for pre-cooling. A process using a mixture of nitrogen, methane, ethane and propane realizes liquefaction. A self-built cryogenic heat exchanger is employed. Philipps developed the Optimized Cascade Process (13%) in which natural gas passes through a cascade of three cooling processes using propane, ethylene and methane as refrigerants. A simple aluminum plate fin component serves as heat exchanger. A technology still new on the market is the one Linde and Statoil developed for the Snovhit terminal in Norway using a cascade process, with a mixture of refrigerants liquefying the gas in every stage.

Exploration & Production

Liquefaction Transport Sales Regasification

7

investigation. LNG is shipped to its destination country (stage 3); the gas vaporizing during transport

is used to fuel the ship. At import terminals, LNG is converted to its original state of aggregation

through a heating process (stage 4). Storage tanks are used to enable a more continuous flow into the

pipeline grid and to cover peak demand.5 Finally, after pressure regulation, natural gas is fed into the

national pipeline grid and sold (stage 5) to marketers, distributors or directly to power producers and

large industrial consumers. In some instances, LNG is transported in its liquid state by truck to single

consumers (e.g. from the U.S. to Mexico).

Natural gas transportation is much more expensive than oil or coal shipping since the fuel has a lower

density and therefore a lower energy content per volume unit. Prices between different geographic

locations may differ substantially. Whereas gas pipelines benefit strongly from economies of scale,

LNG projects require large fixed investments specific infrastructure. For shorter distances pipelines

are more economic, for longer distances LNG is economically feasible. The following figure

illustrates the development of costs of natural gas, oil and coal transportation with raising distances

between exporter and importer.

Figure 2: Costs of gas, oil, and coal transportation

Source: Jensen (2004, p. 7)

Investment costs within the five stages vary significantly, with the largest share induced by the

liquefaction project. The typical structure described by EIA (2003, p. 42) is exploration and

production accounting for 15-20% of the total costs of the LNG value chain; liquefaction for 30-45%;

5 Whereas liquefaction facilities usually run at full capacity, what is necessary to amortize these capital intensive investments, regasification plants often do not so, they may also serve as strategic supply sources to cover seasonal demand spikes. For example, in cold winter periods, different countries like Spain and South Korea purchase extra cargoes above volumes contracted in long-term agreements on a spot basis.

8

shipping for 10-30%; and regasification and distribution finally for 15-25%. Concrete values depend

on different driving factors like the distance between exporting and importing region, employed

technologies, or traded volumes.

Figure 3 compares detailed cost structures for value chains from different exporting countries to

importers in the Atlantic and Pacific Basin. It shows that transportation costs vary strongly with the

distance and have a significant influence on the price of LNG; this is in contrast to oil or coal trade,

where transportation expenses have only a marginal influence on the price. Exploration and production

costs are very similar for all examples. Regasification and distribution have the lowest impact on total

capital costs of an LNG value chain.6

Figure 3: Capital costs for different LNG value chains

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

T rinidad to U.S.(brown-field)

Indonesia toJapan (green-

field)

Nigeria to U.S.(green-field)

Qatar to U.S.(brown-field)

Bolivia to U.S.(green-field)

CA

PEX

in m

illio

n U

SD

E&P Liquefaction T ransport Regasification & Distribution

Source: Jensen (2003, p. 3)

2.1.2 Economics along the LNG value chain

During the last years, significant cost reductions along all stages of the value chain were realized.

Whereas in 1990 investment costs per mtpa liquefaction capacity were about US $500, in 2002 this

amount decreased to US $200 (EIA, 2003, p. 42). Over-design was reduced and benefits from large

economies of scale in liquefaction due to the shift from steam-driven to gas-turbine-driven

compressors and increasing size of gas turbines were realized. The first liquefaction trains had a

capacity of 1.1 mtpa (Arzew in Algeria), today trains with a capacity of around 4 mtpa are common,

and even the construction of units with 7.8 mtpa is planned. Economies of scale of two 4 mtpa trains

reduce liquefaction cost of an 8 mtpa green-field project with four 2 mtpa units by nearly 30%; a

6 Assumptions (Jensen, 2004, p. 6): two 3.3 mtpa liquefaction trains, a field investment of US $3.85 per annual MBtu, pipelines between fields and liquefaction facility are part of the „liquefaction project“. For the last value chain with deliveries from Bolivia to the U.S., liquefaction cost are significantly higher than for other projects, because a pipeline from Bolivia through Chile or Peru to the Pacific coast – treated as part of the liquefaction facility – would have to be constructed.

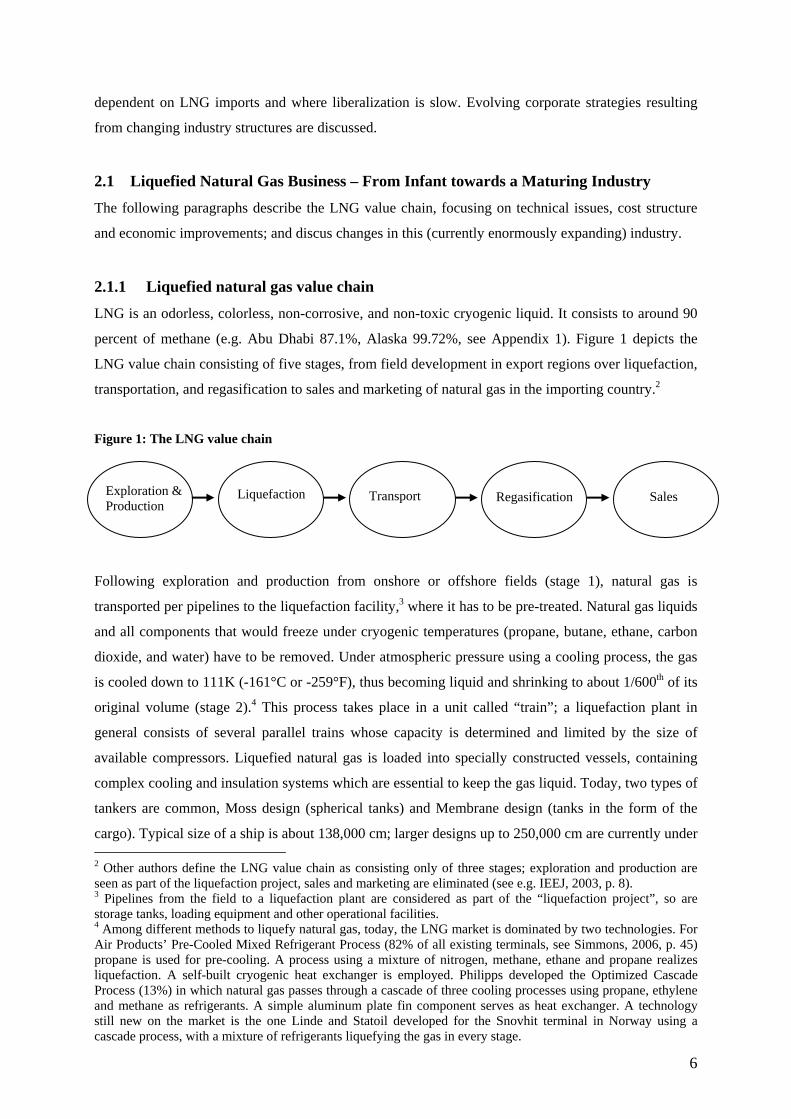

9

further increase to one 7.5 mtpa unit leads to an additional cost reduction by another 20% (Jensen,

2003, p. 31). Figure 4 shows average liquefaction train capacities which came on stream since 1964

and which are expected to start operation until 2010. The figure emphasizes the trend of increasing

train size.

Figure 4: Average train capacities of new built liquefaction facilities

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

1964

1070

1974

1978

1982

1984

1989

1993

1995

1998

2000

2003

2005

2007

2009

mtp

a

Source: Own illustration based on publicly available sources

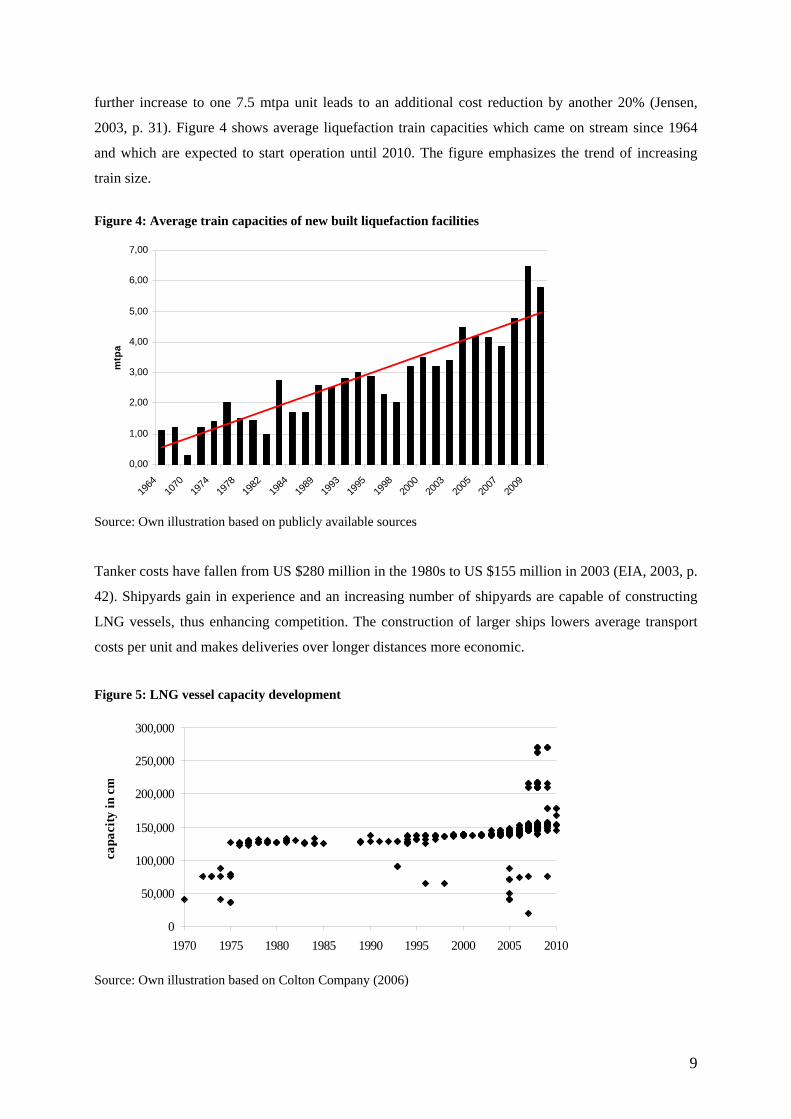

Tanker costs have fallen from US $280 million in the 1980s to US $155 million in 2003 (EIA, 2003, p.

42). Shipyards gain in experience and an increasing number of shipyards are capable of constructing

LNG vessels, thus enhancing competition. The construction of larger ships lowers average transport

costs per unit and makes deliveries over longer distances more economic.

Figure 5: LNG vessel capacity development

0

50,000

100,000

150,000

200,000

250,000

300,000

1970 1975 1980 1985 1990 1995 2000 2005 2010

capa

city

in c

m

Source: Own illustration based on Colton Company (2006)

10

Figure 5 shows that following ten years of smaller vessels with a capacity of 50,000 to 75,000 cm,

about 30 years ships of 130,000 to 140,000 cm have become common. Currently, large vessels with a

capacity of 210,000 to 250,000 cm are under investigation. A mixture of large-scale, mid-scale as well

as very small-scale ships will be employed for future LNG trade.7

On the importing side of the value chain, economies of scale especially due to larger but fewer storage

tanks could be achieved. Furthermore, for liquefaction as well as regasification projects the

construction of brown-field units (expansions of already existing liquefaction or regasification plants)

is much expensive than green-field facilities. In addition, construction costs are minimized using a

competitive bidding process to choose the less expensive EPC (engineering, procurement,

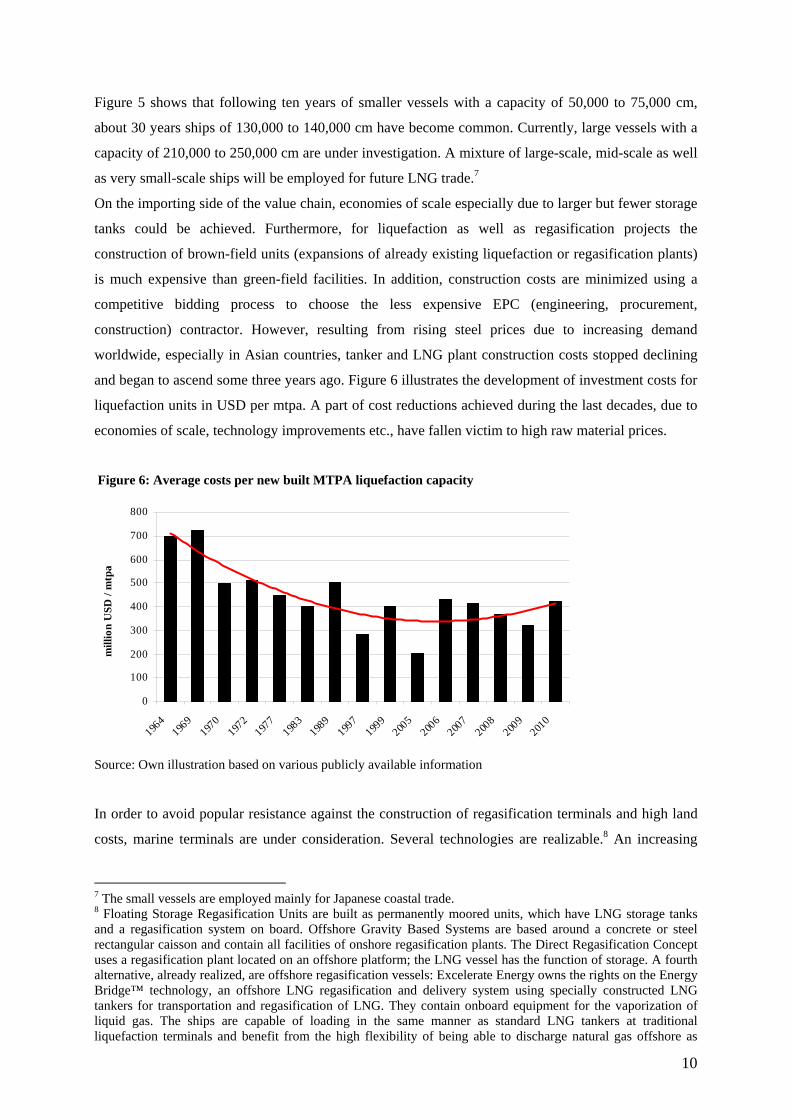

construction) contractor. However, resulting from rising steel prices due to increasing demand

worldwide, especially in Asian countries, tanker and LNG plant construction costs stopped declining

and began to ascend some three years ago. Figure 6 illustrates the development of investment costs for

liquefaction units in USD per mtpa. A part of cost reductions achieved during the last decades, due to

economies of scale, technology improvements etc., have fallen victim to high raw material prices.

Figure 6: Average costs per new built MTPA liquefaction capacity

0

100

200

300

400

500

600

700

800

1964

1969

1970

1972

1977

1983

1989

1997

1999

2005

2006

2007

2008

2009

2010

mill

ion

USD

/ m

tpa

Source: Own illustration based on various publicly available information

In order to avoid popular resistance against the construction of regasification terminals and high land

costs, marine terminals are under consideration. Several technologies are realizable.8 An increasing

7 The small vessels are employed mainly for Japanese coastal trade. 8 Floating Storage Regasification Units are built as permanently moored units, which have LNG storage tanks and a regasification system on board. Offshore Gravity Based Systems are based around a concrete or steel rectangular caisson and contain all facilities of onshore regasification plants. The Direct Regasification Concept uses a regasification plant located on an offshore platform; the LNG vessel has the function of storage. A fourth alternative, already realized, are offshore regasification vessels: Excelerate Energy owns the rights on the Energy Bridge™ technology, an offshore LNG regasification and delivery system using specially constructed LNG tankers for transportation and regasification of LNG. They contain onboard equipment for the vaporization of liquid gas. The ships are capable of loading in the same manner as standard LNG tankers at traditional liquefaction terminals and benefit from the high flexibility of being able to discharge natural gas offshore as

11

development of offshore natural gas fields has also led to a discussion about floating liquefaction

platforms on the upstream side of the value chain. These have the advantage of avoiding long distance

pipelines connecting offshore fields with onshore gas processing and liquefaction plants.9

2.1.3 From infant towards a maturing LNG industry

Since the last decade of the 20th century, substantial structural changes are under way in the LNG

industry. Traded volumes increase rapidly, new players – countries as well as companies – enter the

stage and market conditions are modified due to ongoing liberalization processes. The following

paragraph describes the infant and the currently developing maturity LNG industry. Jensen (2004, p.

49) refers to the “traditional risk-averse, contract dependent model” and the “free market, trading

model”, terms summarizing the characteristics of these two periods very well.

In the old world – or as we call it “infant LNG industry” – three major (liquefied) natural gas trading

regions existed: the market around Canada and the U.S. in North America, deliveries from North

Africa and Russia to Europe, and Pacific Basin trade. Even if trade over longer distances was

technically feasible, sea transport remained expensive and markets therefore regional in nature. The

traditional situation was characterized by inflexible long-term contracts with a duration of about 20 to

25 years. These contracts were rigid sales-and-purchase agreements, typically containing a destination

clause preventing buyers from re-selling imported gas to third parties, high take-or-pay provisions

(around 90% of the contracted volume (IEA, 1998, p. 83)), and price escalating clauses. Sellers had

the guarantee of an efficient use of their capital intensive liquefaction facilities, but flexible deliveries

were hardly possible.10 Ship ownership generally was embedded in these bilateral contracts. Ships

were dedicated to certain routes for the whole contract duration and the LNG typically traded ex ship

(c.i.f. agreements) with the supplier being responsible for transportation. Along these well defined

value chains investments were front-end loaded, revenue generation could not start before every

element was completed.

Since the mid 1990s changes are under way in world natural gas markets, a “maturing LNG industry”

has started to develop. Fostered by increasing natural gas demand, investments in LNG infrastructure

grew rapidly. Exporting and importing countries expanded their capacities; more and more countries

entered the industry.11 As described above, significant cost reductions along the whole value chain

were realized, the distance over which economic deliveries are possible is rising.

vapor, but also onshore as liquid at conventional LNG receiving terminals. The first offshore terminal using this technology, Excelerate’s Gulf Gateway, is operating since March 2005. 9 Shell proposed such a terminal for the Sunrise project in Australia. 10 One exemption realizing a number of flexible cargoes are Pacific Basin exporters; Korea’s Kogas purchased some cargos additional to its existing long-term contracts to cover seasonal peak demand (e.g. from Qatar). 11 Four green-field export projects (22 mtpa) and seven expansions (32.4 mtpa) were realized since 1999, an additional 49 mtpa liquefaction capacity is under construction. Eight green-field regasification projects (30 mtpa) and three expansions (14 mtpa) were realized, an additional 54.4 mtpa are under construction. A large number of LNG projects are proposed. New countries like China are expected to enter the industry.

12

Deregulation of natural gas sectors is a driving factor for changing corporate behavior in the natural

gas business. During the 1980s, the U.S. was the first country which deregulated its natural gas

industry to enhance competition; Canada and the UK followed soon. In these countries, competition is

well advanced. Natural gas spot markets develop; the fuel is traded at several hubs. Europe followed

about 15 years later with the Gas Directive 98/30/EC, repealed in 2003 by 2003/55/EC. As a result of

liberalization, margins of LNG production move downstream (see Ellis et al., 1999, p. 298).

Inflexible contracts can not survive in competitive import markets. Hence, contracts become more

flexible, even if long-term contracts remain part of the risk management in LNG infrastructure

investments. All suppliers to the European Union have to eliminate destination clauses (Jensen, 2004,

p. 22). Contract duration as well as Take-or-Pay-provisions decrease (Neumann and Hirschhausen,

2006). More volumes today are traded free on board, rather than ex ship, to be more flexible in the

choice of the destination country.12 An increasing amount of LNG is traded under short-term contracts

outside the scope of existing long-term contracts. They are particularly important to cover higher

demand of countries with many gas-fired power plants during cold winter months. Spain, the U.S. and

South Korea are main destinations for actual spot deliveries. Spot cargoes in 1992 represented about

1.3% of whole LNG trade, in 2005 spot trade accounted for 11%. Futures trade evolves in competitive

markets (IEA, 1998, p. 28) as part of the risk management. In some cases (e.g. NLNG 4&5/Nigeria;

Qalhat 3/Oman) the construction of LNG plants even starts before all capacity is contracted.

Players active in the LNG industry respond to this changing market environment. Global oil producing

companies heavily engage in production, liquefaction, transport, and also regasification of LNG.

Private oil and gas companies joined the long-established state-owned entities in export projects. In

import markets former (European) monopolists of natural gas are facing their traditional markets at

stake by the intrusion of those oil and gas majors, integrating downstream to benefit from marginal

rents in the natural gas industry. On the other side, traditional downstream players integrate upstream,

control transport capacities and even get access to liquefaction plants and natural gas reserves in order

to minimize risks and secure their supply. Independent power producers investing in gas-fired power

plants evolve becoming potential new buyers of LNG.

Nissen (2004) describes the evolving “commercial LNG model” where players control capacities in all

stages along the value chain, participating in different export projects, owning undedicated transport

capacity and controlling multiple import facility access. Thus, they are able to use these capacities

flexible and benefit from arbitrage. There exists a number of liquefaction plants – so called “tolling

facilities” (e.g. ELNG in Egypt/Idku or SEGAS in Egypt/Damietta) – only selling the service of

liquefaction, storage and loading. In that case natural gas producers rather than export projects become

the seller. On the importing side, the U.S. company Cheniere Energy plans to construct four

regasification plants that sell the service of regasification to LNG importers.

12 Tokyo Gas and Tepco in Japan have renegotiated a Malaysian contract to provide for a portion of the volume to be supplied f.o.b. rather than ex ship.

13

A number of vessels are not dedicated to special routes anymore; different players – for example the

British Gas Group – order own uncommitted ships. At the end of 2005, 27 vessels were operating

without any dedication and nine vessels were ordered by private oil and gas majors (CERA, 2006, p.

2). A second-hand market for vessels has emerged since the 1990s.13

Oil-linkage of natural gas prices is currently heavily debated since oil-linked prices are a poor

indicator of the value of gas in a gas-to-gas competitive market. In Japan for example, during the

1970s, when the first LNG long-term contracts were signed, oil accounted for 73% of power

generation. Therefore, Japanese natural gas prices traditionally are linked to the Japanese Customs

Clearing price (IEEJ, 2005, p. 26). Today, less than 10% of the electricity is generated with oil as fuel.

Therefore, a gas market indicator would be more suitable, like it is in the U.S. for certain contracts the

Henry Hub price. But in many cases oil-price-linkage remains because the contracting parties do not

find any better alternative.

A world market for LNG is developing. The Middle East evolves to a swing producer from where

deliveries to European as well as Asian markets are possible without a significant (transport) cost

difference. Jensen (2003, p. 10) states that “for a business that was for a long time sufficiently

fragmented geographically that the concept of a world gas market was unthinkable, LNG is now

seeing the first elements of interregional gas price competition.” A number of cargoes have already

been re-routed to higher value markets. Inflexible long-term contracts and short-term agreements will

co-exist. Following Jensen (2003, p. 10) it is argued that the “ultimate shape of the LNG system will

be a synthesis of the traditional (thesis) and the new (antithesis).”

2.2 Natural Gas Importing Regions – A Focus on Liquefied Natural Gas

Varying pre-conditions and development of LNG trade in the Atlantic and the Pacific Basins continue

to affect import volumes, pricing systems, and contract terms. This chapter provides an overview on

the three major natural gas importing regions worldwide.

2.2.1 Overview

During the 1980s and early 1990s, in the Atlantic Basin indigenous natural gas supplies and imports

via pipeline were sufficient to cover demand; therefore, LNG capacities grew relatively slowly. Still

today, LNG has to compete with domestic supplies and pipeline imports. In contrast, natural gas

importing countries in the Pacific Basin like Japan, South Korea or Taiwan do not have large (or even

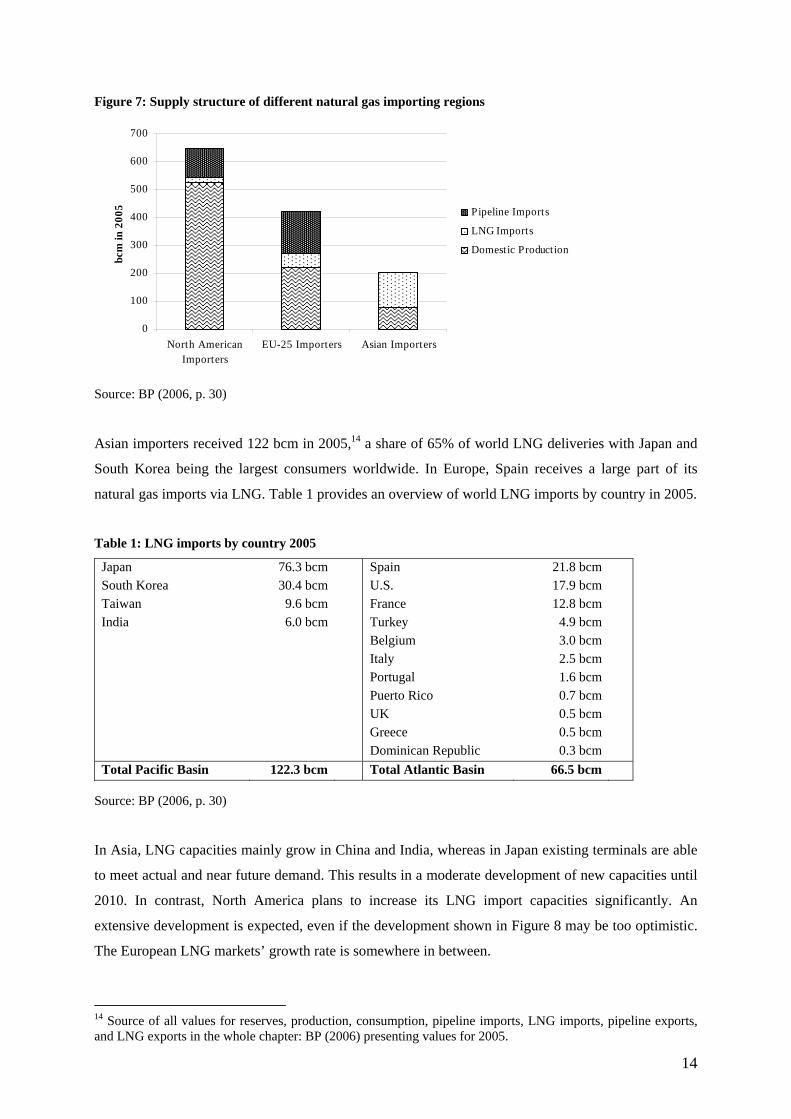

no) domestic supply and no pipeline sources and strongly depend on LNG imports. Figure 7 depicts

structural differences of natural gas supply situations in the three LNG importing regions North

America, Europe and Asia.

13 Vessels have a life time of about 40 years, the typical long-term contract has a duration of about 20 years. Marathon/ConocoPhilipps renegotiated in 1994 the contract between U.S. and Japan. They increased volumes and decided to employ new larger tankers. Hence, both original tankers were idled and purchased by BG.

14

Figure 7: Supply structure of different natural gas importing regions

0

100

200

300

400

500

600

700

North AmericanImporters

EU-25 Importers Asian Importers

bcm

in 2

005 Pipeline Imports

LNG Imports

Domestic Production

Source: BP (2006, p. 30)

Asian importers received 122 bcm in 2005,14 a share of 65% of world LNG deliveries with Japan and

South Korea being the largest consumers worldwide. In Europe, Spain receives a large part of its

natural gas imports via LNG. Table 1 provides an overview of world LNG imports by country in 2005.

Table 1: LNG imports by country 2005

Japan South Korea Taiwan India

76.3 bcm 30.4 bcm

9.6 bcm 6.0 bcm

Spain U.S. France Turkey Belgium Italy Portugal Puerto Rico UK Greece Dominican Republic

21.8 bcm 17.9 bcm 12.8 bcm

4.9 bcm 3.0 bcm 2.5 bcm 1.6 bcm 0.7 bcm 0.5 bcm 0.5 bcm 0.3 bcm

Total Pacific Basin 122.3 bcm Total Atlantic Basin 66.5 bcm Source: BP (2006, p. 30)

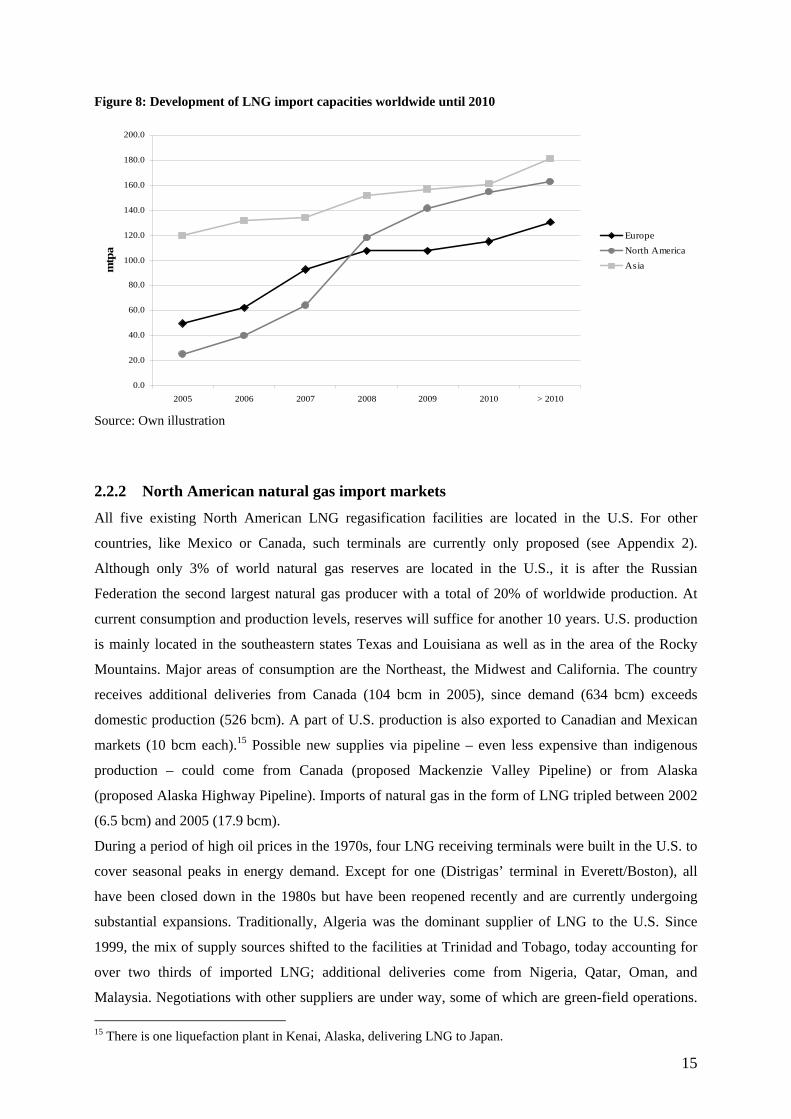

In Asia, LNG capacities mainly grow in China and India, whereas in Japan existing terminals are able

to meet actual and near future demand. This results in a moderate development of new capacities until

2010. In contrast, North America plans to increase its LNG import capacities significantly. An

extensive development is expected, even if the development shown in Figure 8 may be too optimistic.

The European LNG markets’ growth rate is somewhere in between.

14 Source of all values for reserves, production, consumption, pipeline imports, LNG imports, pipeline exports, and LNG exports in the whole chapter: BP (2006) presenting values for 2005.

15

Figure 8: Development of LNG import capacities worldwide until 2010

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

2005 2006 2007 2008 2009 2010 > 2010

mtp

a

EuropeNorth AmericaAsia

Source: Own illustration

2.2.2 North American natural gas import markets

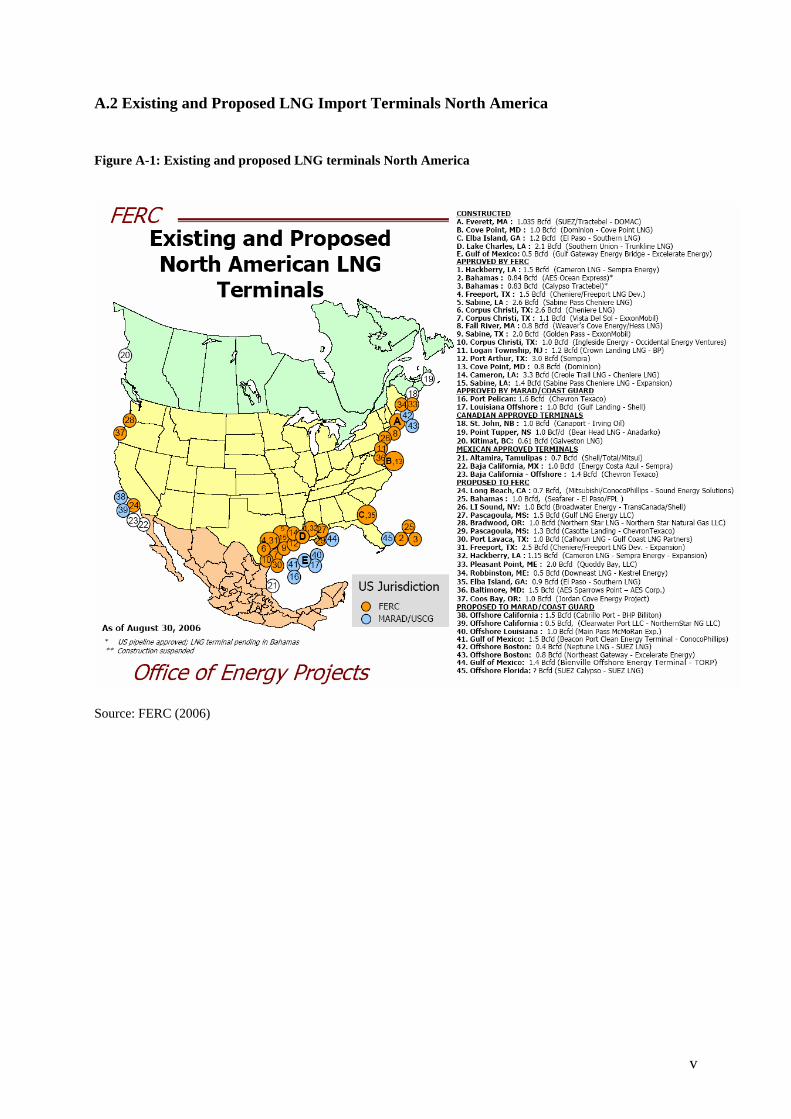

All five existing North American LNG regasification facilities are located in the U.S. For other

countries, like Mexico or Canada, such terminals are currently only proposed (see Appendix 2).

Although only 3% of world natural gas reserves are located in the U.S., it is after the Russian

Federation the second largest natural gas producer with a total of 20% of worldwide production. At

current consumption and production levels, reserves will suffice for another 10 years. U.S. production

is mainly located in the southeastern states Texas and Louisiana as well as in the area of the Rocky

Mountains. Major areas of consumption are the Northeast, the Midwest and California. The country

receives additional deliveries from Canada (104 bcm in 2005), since demand (634 bcm) exceeds

domestic production (526 bcm). A part of U.S. production is also exported to Canadian and Mexican

markets (10 bcm each).15 Possible new supplies via pipeline – even less expensive than indigenous

production – could come from Canada (proposed Mackenzie Valley Pipeline) or from Alaska

(proposed Alaska Highway Pipeline). Imports of natural gas in the form of LNG tripled between 2002

(6.5 bcm) and 2005 (17.9 bcm).

During a period of high oil prices in the 1970s, four LNG receiving terminals were built in the U.S. to

cover seasonal peaks in energy demand. Except for one (Distrigas’ terminal in Everett/Boston), all

have been closed down in the 1980s but have been reopened recently and are currently undergoing

substantial expansions. Traditionally, Algeria was the dominant supplier of LNG to the U.S. Since

1999, the mix of supply sources shifted to the facilities at Trinidad and Tobago, today accounting for

over two thirds of imported LNG; additional deliveries come from Nigeria, Qatar, Oman, and

Malaysia. Negotiations with other suppliers are under way, some of which are green-field operations. 15 There is one liquefaction plant in Kenai, Alaska, delivering LNG to Japan.

16

LNG imports have risen steadily even though capacity utilization with 55% is still modest (Simmons

et al., 2005, p. 21). There is a general consensus that LNG imports will continue to increase. Domestic

production as well as imports from other sources (e.g. Canadian pipeline gas) are declining. The first

newly build terminal started operation in 2005 with the delivery of a first cargo from Malaysia.

Excelerate’s “Gulf Gateway Energy Bridge” is located about 116 miles offshore the Louisiana coast.16

Natural gas is transported via the Sea Robin Pipe and the Blue Water Pipe and comes ashore on the

Louisiana coast near Henry Hub. Table 2 provides an overview on technical data of existing LNG

import terminals and planned expansions.

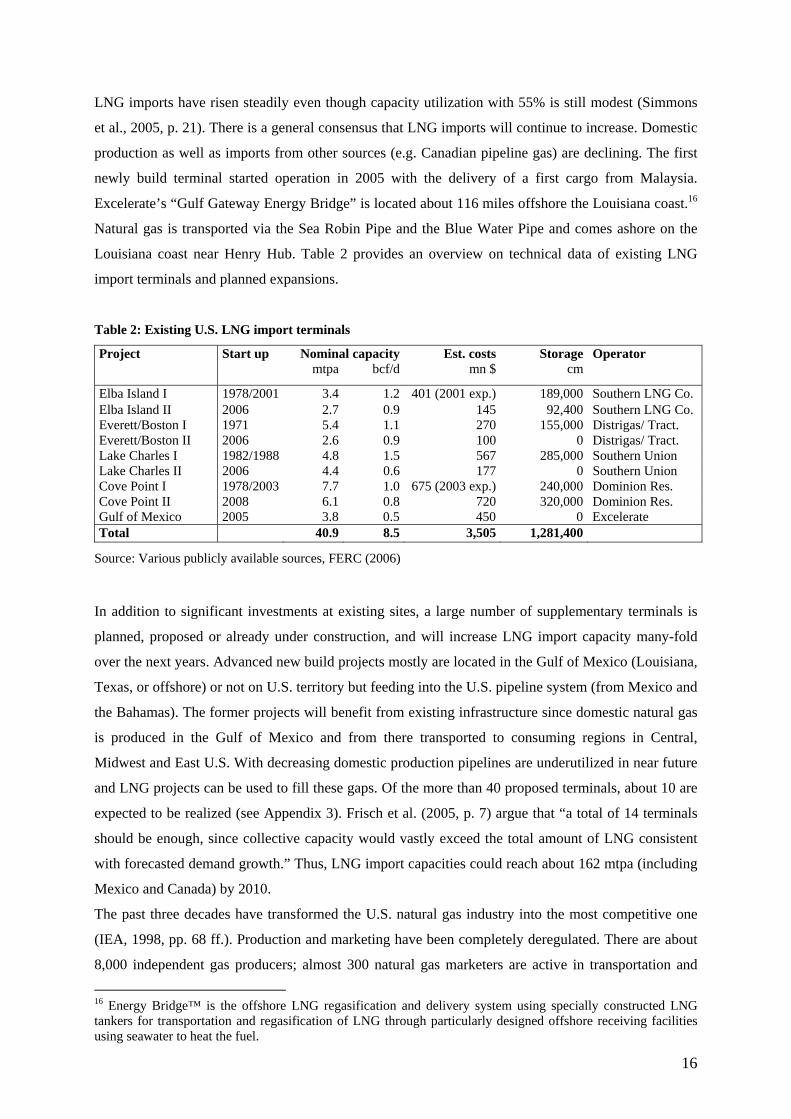

Table 2: Existing U.S. LNG import terminals

Project Start up Nominal capacity Est. costs Storage Operator mtpa bcf/d mn $ cm

Elba Island I 1978/2001 3.4 1.2 401 (2001 exp.) 189,000 Southern LNG Co. Elba Island II 2006 2.7 0.9 145 92,400 Southern LNG Co. Everett/Boston I 1971 5.4 1.1 270 155,000 Distrigas/ Tract. Everett/Boston II 2006 2.6 0.9 100 0 Distrigas/ Tract. Lake Charles I 1982/1988 4.8 1.5 567 285,000 Southern Union Lake Charles II 2006 4.4 0.6 177 0 Southern Union Cove Point I 1978/2003 7.7 1.0 675 (2003 exp.) 240,000 Dominion Res. Cove Point II 2008 6.1 0.8 720 320,000 Dominion Res. Gulf of Mexico 2005 3.8 0.5 450 0 Excelerate Total 40.9 8.5 3,505 1,281,400

Source: Various publicly available sources, FERC (2006) In addition to significant investments at existing sites, a large number of supplementary terminals is

planned, proposed or already under construction, and will increase LNG import capacity many-fold

over the next years. Advanced new build projects mostly are located in the Gulf of Mexico (Louisiana,

Texas, or offshore) or not on U.S. territory but feeding into the U.S. pipeline system (from Mexico and

the Bahamas). The former projects will benefit from existing infrastructure since domestic natural gas

is produced in the Gulf of Mexico and from there transported to consuming regions in Central,

Midwest and East U.S. With decreasing domestic production pipelines are underutilized in near future

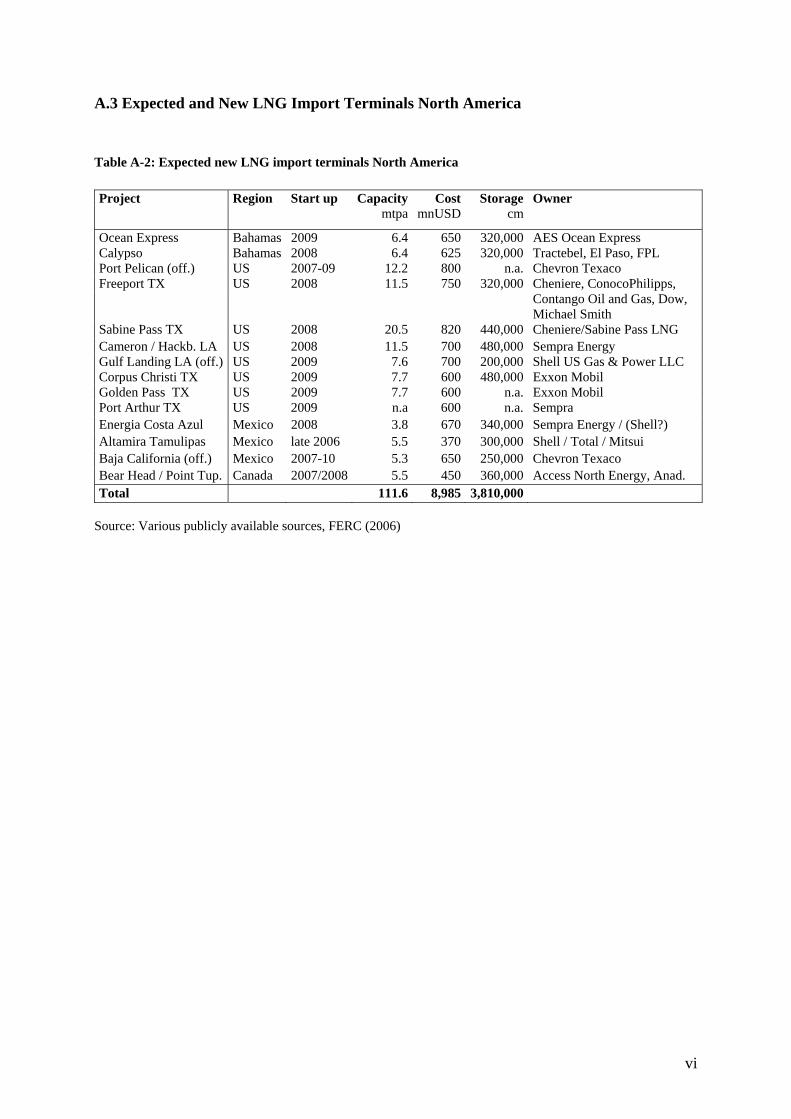

and LNG projects can be used to fill these gaps. Of the more than 40 proposed terminals, about 10 are

expected to be realized (see Appendix 3). Frisch et al. (2005, p. 7) argue that “a total of 14 terminals

should be enough, since collective capacity would vastly exceed the total amount of LNG consistent

with forecasted demand growth.” Thus, LNG import capacities could reach about 162 mtpa (including

Mexico and Canada) by 2010.

The past three decades have transformed the U.S. natural gas industry into the most competitive one

(IEA, 1998, pp. 68 ff.). Production and marketing have been completely deregulated. There are about

8,000 independent gas producers; almost 300 natural gas marketers are active in transportation and

16 Energy Bridge™ is the offshore LNG regasification and delivery system using specially constructed LNG tankers for transportation and regasification of LNG through particularly designed offshore receiving facilities using seawater to heat the fuel.

17

sales. Significant restructuring of the industry started in the 1970s, with the Natural Gas Policy Act

removing wellhead ceiling prices in 1978. Based on a number of FERC Orders transportation and

asset services were unbundled and open access was introduced.17 Traditionally, LNG terminals were

considered to be part of the transportation system, and thus subject to an open-access service under

Section 7c of the Natural Gas Act. Since the “Hackberry Decision” in 2002 LNG import facilities are

treated as “supply sources” rather than part of the transportation grid, open access no longer has to be

provided.

2.2.3 European natural gas import markets

European countries18 control only about three percent of world natural gas reserves. Consumption with

423 bcm (in 2005) exceeds own production (206 bcm) more than twice. Hence, import dependency is

very strong and is expected to increase further due to increasing primary energy demand,

environmental concerns and growing power production based on natural gas as fuel (IEA, 2006).

The network of high-pressure interstate pipelines carries gas from supply areas, situated mainly in the

North Sea, Eurasia, and North Africa. Main foreign deliveries come from Russia (151.3 bcm in 2005),

Algeria (38.1 bcm), Libya (4.5 bcm) and Iran (4.3 bcm). Indigenous production takes place in Norway

(79.5 bcm), the Netherlands (46.8 bcm), and the UK (9.7 bcm), with the last slowly developing from a

net exporter to a net importer as declining reserves face increasing demand since 2000. Domestic

production covers a part of demand in Austria, Belgium, Denmark, France, and Germany. Different

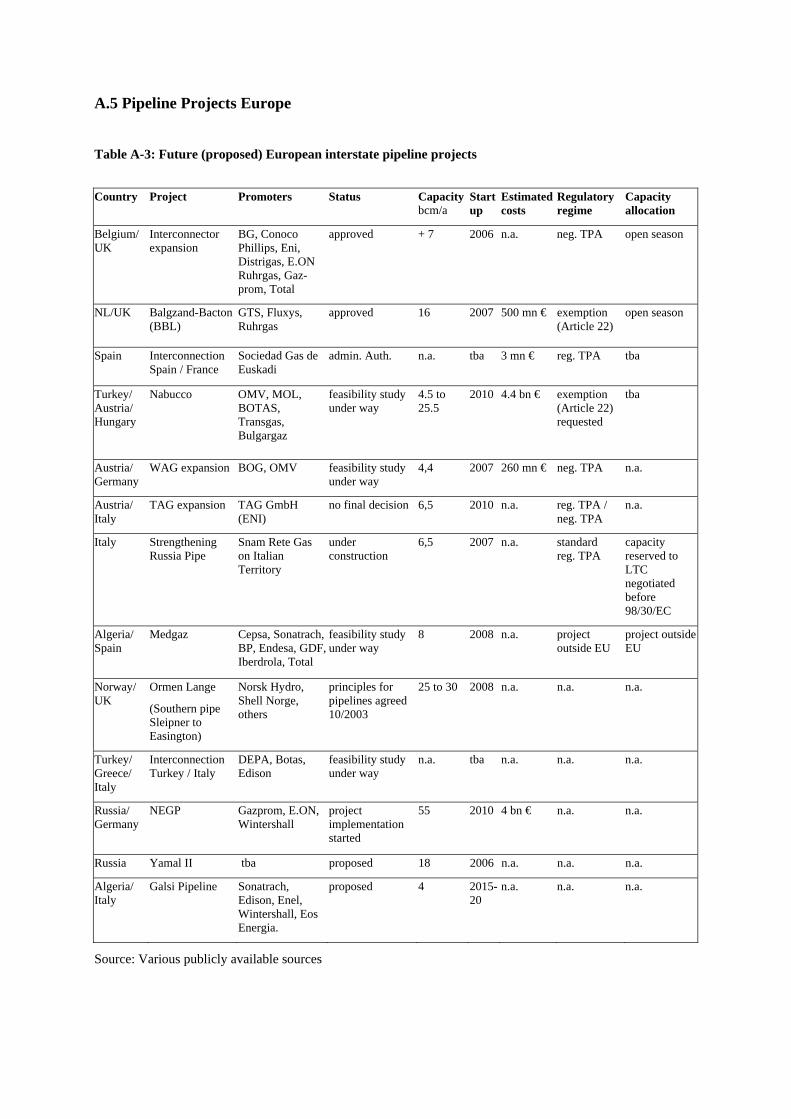

major interstate pipeline projects have been completed during the last decade.19 A certain number of

projects are proposed (see Appendix 5). These would enable further supplies from producing regions

for example in Norway (Orman Lange to UK), Russia (NEGP to Germany) or Turkey (Nabucco to

Austria). The degree of sponsors’ diversity increases, incumbent transmission system operators are

accompanied by international oil and gas majors, private gas producers as well as power companies.

Liquefied natural gas plays an important role to meet European energy demand. In 2005, nearly 12%

of the natural gas coming from foreign producers was imported in the form of LNG. Today, 12 LNG

regasification facilities with a total nominal capacity of about 50 mtpa are operational and able to send

69.3 billion cubic meters per year (bcm/a) of natural gas into national pipeline grids. Europe receives

LNG imports from Algeria (with deliveries of 6.6 bcm in 2004), Nigeria (4.8 bcm), and Qatar (3.9

bcm), followed by the states of Oman, Libya, the United Arab Emirate and Malaysia. Future supplies

will also include deliveries from Egypt (to France and Italy) and other exporting countries in the

Atlantic Basin and the region of the Middle East. The following table provides an overview on

existing terminals, corresponding technical data, and estimated project costs.

17 Order 380 (1984), Order 436 (1985), Order 636 (1992), Order 637 (2000) 18 Europe refers to the EU-25. 19 E.g. the Interconnector (UK/Belgium), the BBL Pipeline (Netherlands/UK), the Greenstream (Libya/Italy) or the Euskadour Natural Gas Pipeline (Spain to France).

18

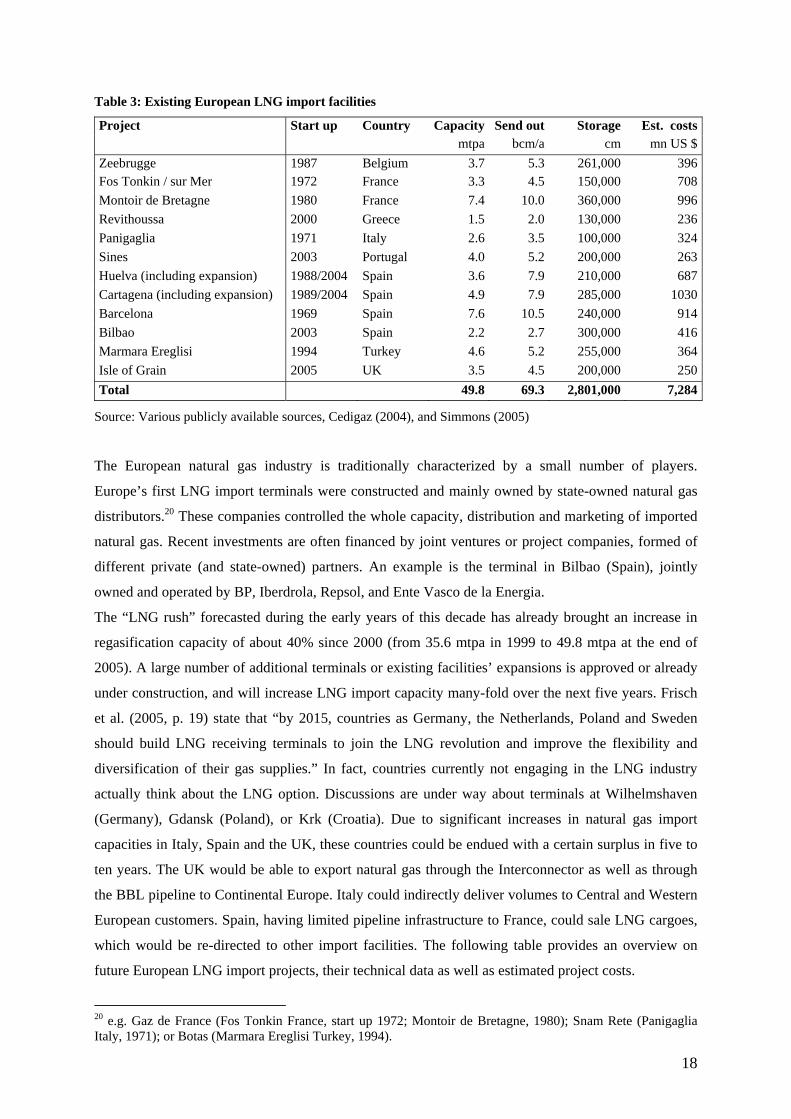

Table 3: Existing European LNG import facilities

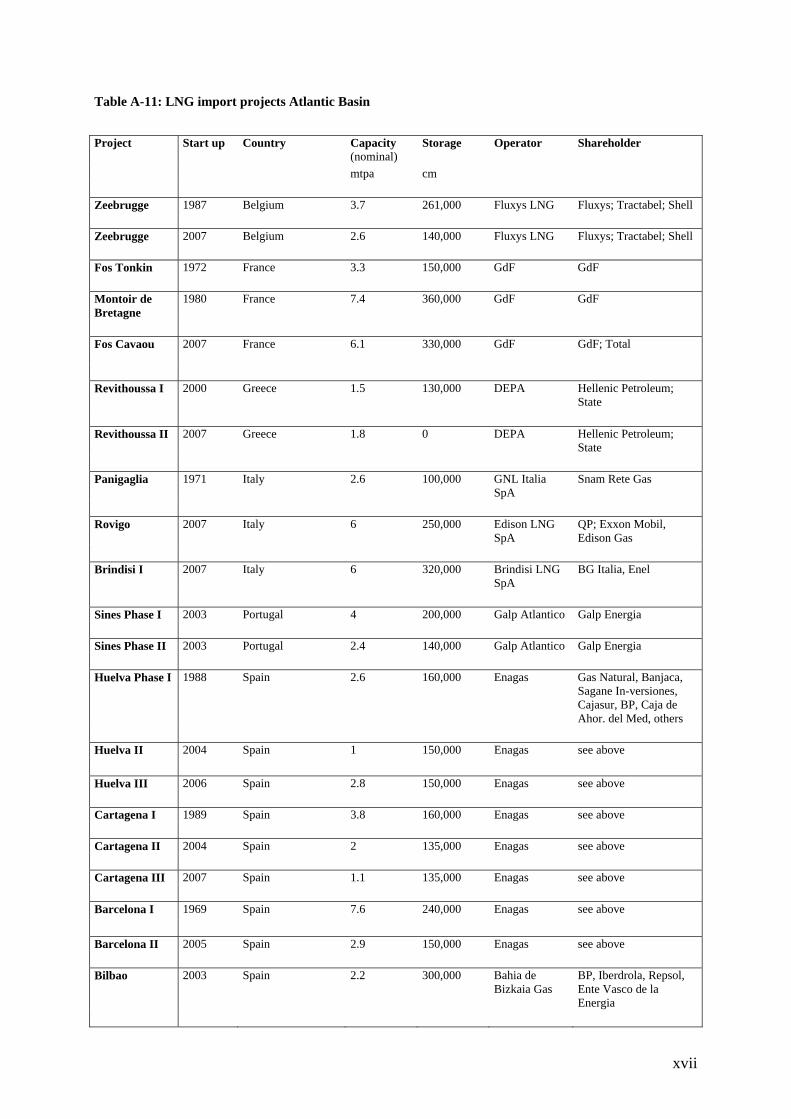

Project Start up Country Capacity Send out Storage Est. costs mtpa bcm/a cm mn US $Zeebrugge 1987 Belgium 3.7 5.3 261,000 396Fos Tonkin / sur Mer 1972 France 3.3 4.5 150,000 708Montoir de Bretagne 1980 France 7.4 10.0 360,000 996Revithoussa 2000 Greece 1.5 2.0 130,000 236Panigaglia 1971 Italy 2.6 3.5 100,000 324Sines 2003 Portugal 4.0 5.2 200,000 263Huelva (including expansion) 1988/2004 Spain 3.6 7.9 210,000 687Cartagena (including expansion) 1989/2004 Spain 4.9 7.9 285,000 1030Barcelona 1969 Spain 7.6 10.5 240,000 914Bilbao 2003 Spain 2.2 2.7 300,000 416Marmara Ereglisi 1994 Turkey 4.6 5.2 255,000 364Isle of Grain 2005 UK 3.5 4.5 200,000 250Total 49.8 69.3 2,801,000 7,284

Source: Various publicly available sources, Cedigaz (2004), and Simmons (2005)

The European natural gas industry is traditionally characterized by a small number of players.

Europe’s first LNG import terminals were constructed and mainly owned by state-owned natural gas

distributors.20 These companies controlled the whole capacity, distribution and marketing of imported

natural gas. Recent investments are often financed by joint ventures or project companies, formed of

different private (and state-owned) partners. An example is the terminal in Bilbao (Spain), jointly

owned and operated by BP, Iberdrola, Repsol, and Ente Vasco de la Energia.

The “LNG rush” forecasted during the early years of this decade has already brought an increase in

regasification capacity of about 40% since 2000 (from 35.6 mtpa in 1999 to 49.8 mtpa at the end of

2005). A large number of additional terminals or existing facilities’ expansions is approved or already

under construction, and will increase LNG import capacity many-fold over the next five years. Frisch

et al. (2005, p. 19) state that “by 2015, countries as Germany, the Netherlands, Poland and Sweden

should build LNG receiving terminals to join the LNG revolution and improve the flexibility and

diversification of their gas supplies.” In fact, countries currently not engaging in the LNG industry

actually think about the LNG option. Discussions are under way about terminals at Wilhelmshaven

(Germany), Gdansk (Poland), or Krk (Croatia). Due to significant increases in natural gas import

capacities in Italy, Spain and the UK, these countries could be endued with a certain surplus in five to

ten years. The UK would be able to export natural gas through the Interconnector as well as through

the BBL pipeline to Continental Europe. Italy could indirectly deliver volumes to Central and Western

European customers. Spain, having limited pipeline infrastructure to France, could sale LNG cargoes,

which would be re-directed to other import facilities. The following table provides an overview on

future European LNG import projects, their technical data as well as estimated project costs.

20 e.g. Gaz de France (Fos Tonkin France, start up 1972; Montoir de Bretagne, 1980); Snam Rete (Panigaglia Italy, 1971); or Botas (Marmara Ereglisi Turkey, 1994).

19

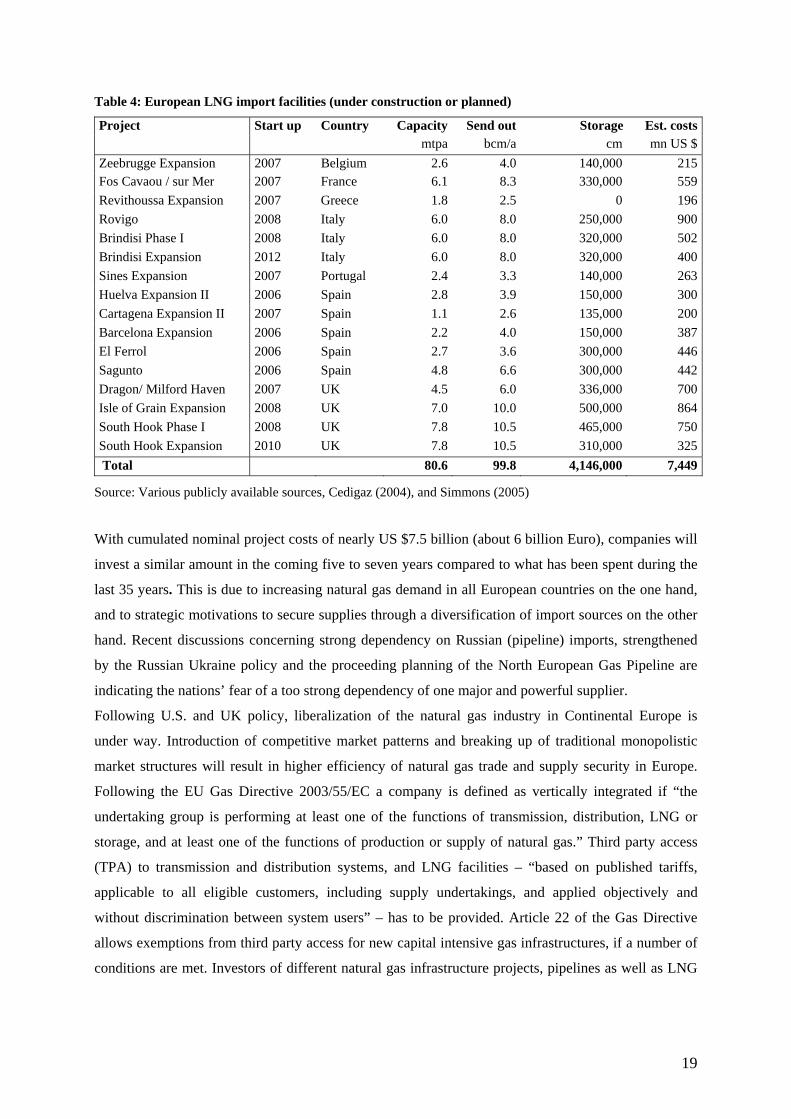

Table 4: European LNG import facilities (under construction or planned)

Project Start up Country Capacity Send out Storage Est. costs mtpa bcm/a cm mn US $Zeebrugge Expansion 2007 Belgium 2.6 4.0 140,000 215Fos Cavaou / sur Mer 2007 France 6.1 8.3 330,000 559Revithoussa Expansion 2007 Greece 1.8 2.5 0 196Rovigo 2008 Italy 6.0 8.0 250,000 900Brindisi Phase I 2008 Italy 6.0 8.0 320,000 502Brindisi Expansion 2012 Italy 6.0 8.0 320,000 400Sines Expansion 2007 Portugal 2.4 3.3 140,000 263Huelva Expansion II 2006 Spain 2.8 3.9 150,000 300Cartagena Expansion II 2007 Spain 1.1 2.6 135,000 200Barcelona Expansion 2006 Spain 2.2 4.0 150,000 387El Ferrol 2006 Spain 2.7 3.6 300,000 446Sagunto 2006 Spain 4.8 6.6 300,000 442Dragon/ Milford Haven 2007 UK 4.5 6.0 336,000 700Isle of Grain Expansion 2008 UK 7.0 10.0 500,000 864South Hook Phase I 2008 UK 7.8 10.5 465,000 750South Hook Expansion 2010 UK 7.8 10.5 310,000 325 Total 80.6 99.8 4,146,000 7,449

Source: Various publicly available sources, Cedigaz (2004), and Simmons (2005)

With cumulated nominal project costs of nearly US $7.5 billion (about 6 billion Euro), companies will

invest a similar amount in the coming five to seven years compared to what has been spent during the

last 35 years. This is due to increasing natural gas demand in all European countries on the one hand,

and to strategic motivations to secure supplies through a diversification of import sources on the other

hand. Recent discussions concerning strong dependency on Russian (pipeline) imports, strengthened

by the Russian Ukraine policy and the proceeding planning of the North European Gas Pipeline are

indicating the nations’ fear of a too strong dependency of one major and powerful supplier.

Following U.S. and UK policy, liberalization of the natural gas industry in Continental Europe is

under way. Introduction of competitive market patterns and breaking up of traditional monopolistic

market structures will result in higher efficiency of natural gas trade and supply security in Europe.

Following the EU Gas Directive 2003/55/EC a company is defined as vertically integrated if “the

undertaking group is performing at least one of the functions of transmission, distribution, LNG or

storage, and at least one of the functions of production or supply of natural gas.” Third party access

(TPA) to transmission and distribution systems, and LNG facilities – “based on published tariffs,

applicable to all eligible customers, including supply undertakings, and applied objectively and

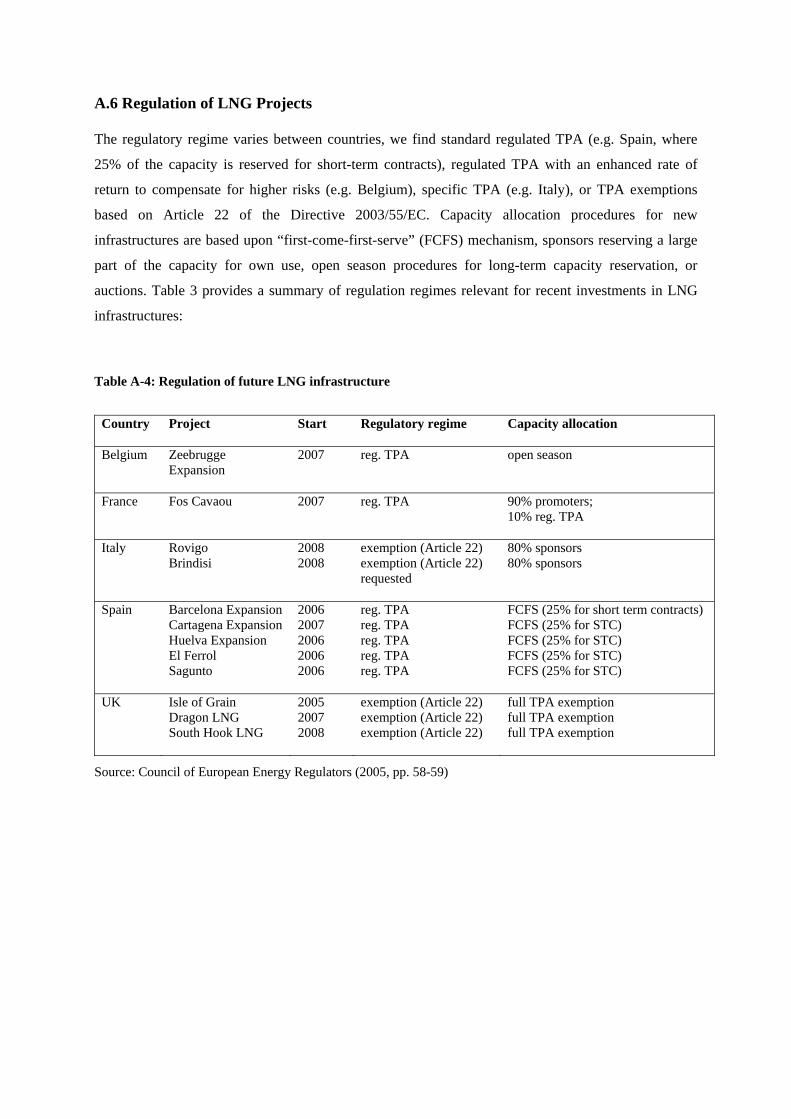

without discrimination between system users” – has to be provided. Article 22 of the Gas Directive

allows exemptions from third party access for new capital intensive gas infrastructures, if a number of

conditions are met. Investors of different natural gas infrastructure projects, pipelines as well as LNG

20

import facilities, have extensively made use of this article.21 National regulatory authorities decide

upon regulation methods applied to transmission, distribution, third-party access, and LNG facilities

resulting in varying regulatory regimes between countries.22 Former European monopolists, active in

pipeline operation as well as distribution and marketing of natural gas, have formed independent

transport utilities to meet the obligations resulting from the EU Gas Directive 2003/55/EC and

implemented national laws. Unbundling of competitive and monopolistic elements of the value-added

chain has been realized. However, there are mainly incumbents participating in the industry. Appendix

7 provides an overview on main owners and operators of European national transmission pipelines.

2.2.4 Asian natural gas import markets

The major form of primary energy used in Asian countries is coal, especially in China and India,

which are strongly dependent on domestic cheap coal for power production. Even though the share of

coal in the energy mix of China decreased since the mid 1990s, nominal values are expected to

continue to rise. Increasing the diversification of energy sources as well as diminishing green-house

gas emissions to meet Kyoto protocol obligations are main drivers for an increase of natural gas’ share

in the energy mix. During the 1980s, Asian economies grew rapidly. The currency crisis, starting 1997

in Thailand, determined a temporary stagnation in economic growth resulting also in decreasing

energy consumption. However, the countries picked up very quickly and today are the regions which

show the highest growth rates in primary energy as well as natural gas demand. Currently, a

liberalization process of natural gas and electric power industries is introduced in Japan, South Korea

and Taiwan. Trading environment changes substantially.

Main natural gas importing countries in the Asia-Pacific region are Japan, South Korea, and India.

China and the Philippines are likely to follow soon. Only 1.7% of worldwide reserves are located

within China and India, whereas other countries house none at all. The gap between domestic

production of 80 bcm and consumption of 190 bcm in 2005 reveals the strong import dependency of

the whole region. A characteristic issue influencing natural gas supply policy is that until today, no

major foreign source is connected with these countries via pipeline. A summary of existing and

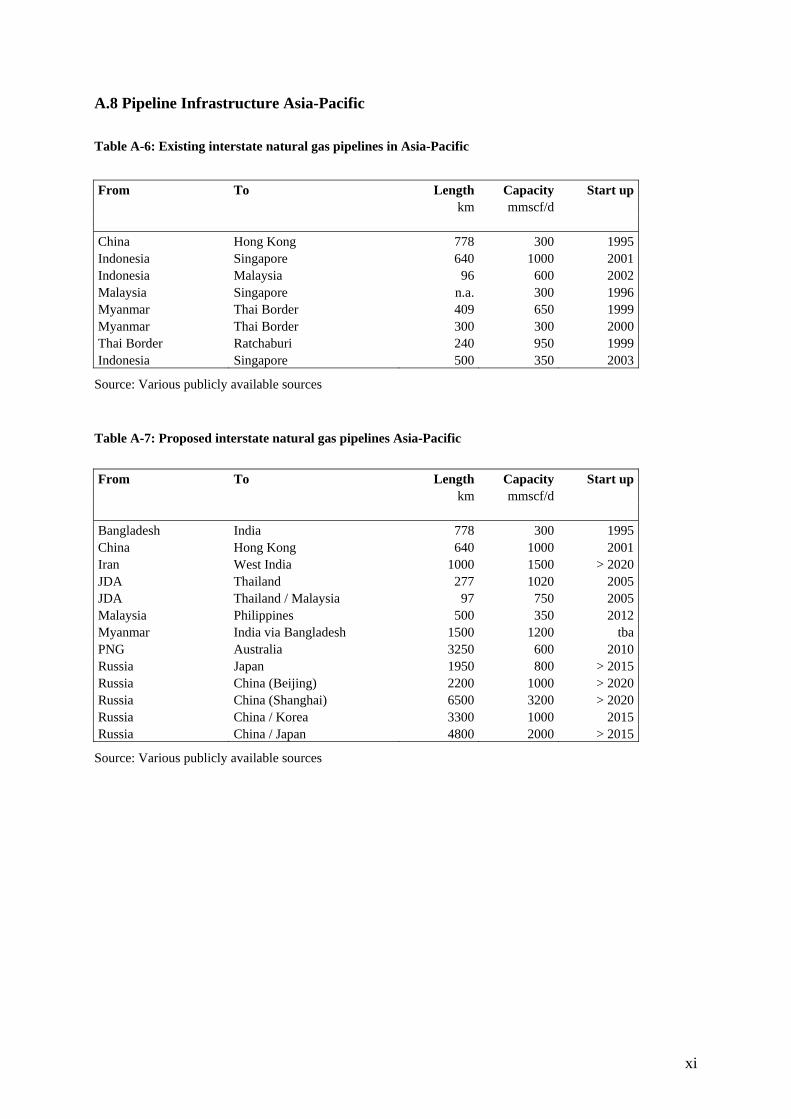

proposed interstate pipelines can be found in Appendix 8. In the next decade, pipeline deliveries could

come from Russia. Discussions are under way to connect Japan, China, and South Korea with the

Sakhalin fields and Eastern Siberia.23 Today, imports are delivered in the form of LNG from Australia,

Indonesia, Malaysia and the area of the Middle East. From these terminals pipelines deliver regasified

natural gas to power plants, industrial users and main consuming regions which are mainly situated in 21 E.g. the BBL Interconnector between Balgzand (Netherlands) and Bacton (UK), Isle of Grain LNG terminal (UK), Milford Haven LNG terminals (UK), Rovigo LNG terminal (Italy), Brindisi LNG terminal (Italy). 22 We find standard regulated TPA (e.g. Spain), regulated TPA with an enhanced rate of return to compensate for higher risks (e.g. Belgium), specific TPA (e.g. Italy), or exemptions based on Article 22 (see Appendix 6). 23 China has an agreement with Russia to proceed with natural gas development in East Siberia; the supplier wants Japan and South Korea to be involved to reduce project risk. Concerning Sakhalin 1, the Russian oil and gas project which is strongly supported by the Japanese government, Japanese utilities decided in 2002 to realize the Sakhalin 2 LNG project and to postpone the potential pipeline to the post 2010 period.

21

coastal areas. No long pipeline connections have to be built, hence, the natural gas system is more a

collection of smaller “islands” of consumption than a real network.

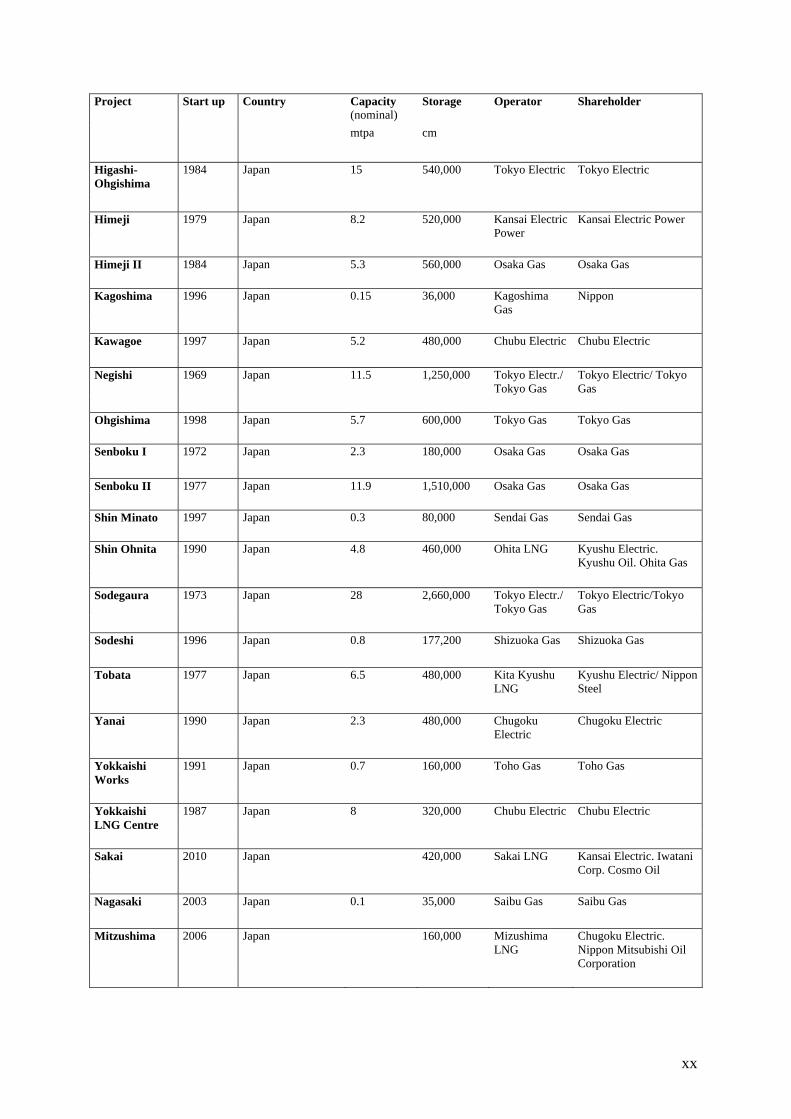

Japan receives more than 40 percent of worldwide LNG deliveries (76.3 bcm in 2005) and thus forms

the largest importing country. It started LNG imports with its first terminal Negishi in 1969 receiving

deliveries from Alaska. Today, 23 terminals are operating with a total capacity of 77 mtpa. Three new

plants are planned. Since the early 1990s, Japan’s energy policy follows the “3Es”: “economic

efficiency”, “environmental protection”, and “energy security” (see IEEJ, 2004, p. 1). The ongoing

liberalization process, based on the Gas and Electric Utility Laws (introduced in 1995, further

amended in 1999/2000) encourages significant market changes. City-gas companies launch into

supply to large consumers; foreign firms, traders and large industrial users move towards electricity

retailing; natural gas distributors start activities in power production (Tokyo Gas, Osaka Gas); power

producers in gas sales (e.g. Tohoku Electric Power or Kansai Electric Power).

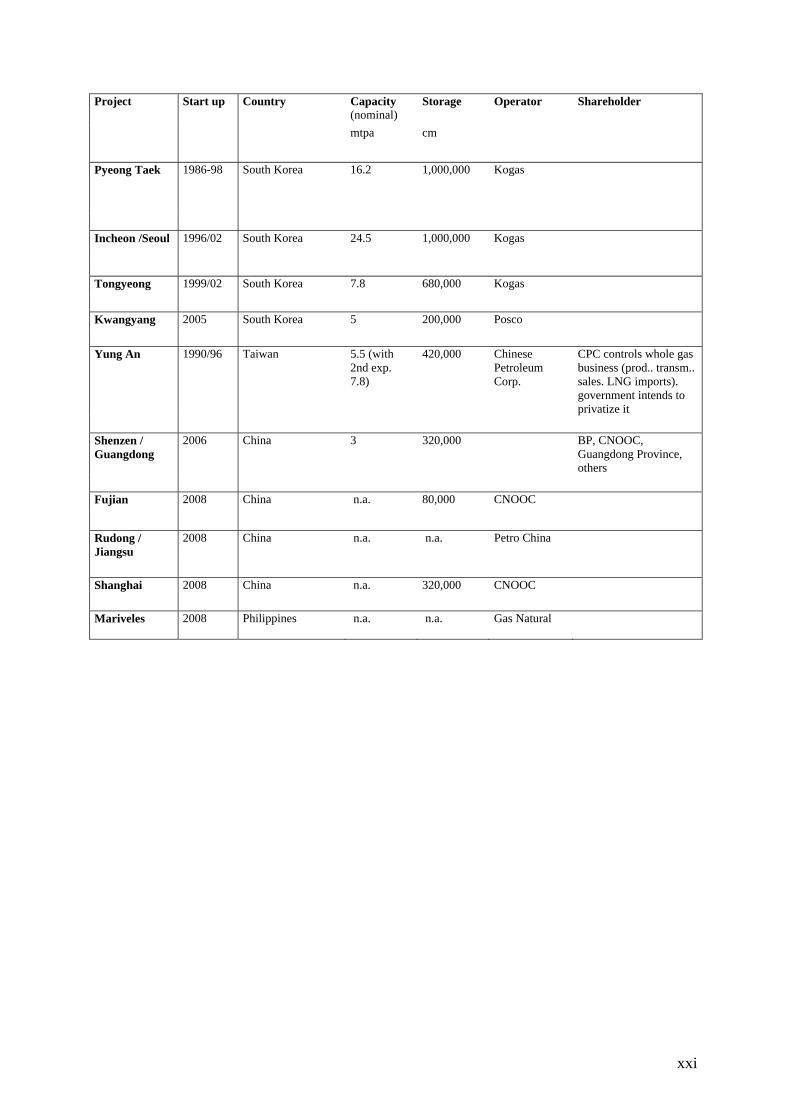

South Korea joined the industry in 1986 with currently four operating terminals (in total 30 mtpa) and

today representing the second largest LNG importer (30.4 bcm in 2004). Regasified LNG today is

delivered not only to industrial but also to private end-consumers. Gas-fired power plants are used to

cover seasonal peaks in cold winter periods; hence, natural gas demand is highly volatile. Deliveries

under short-term agreements as well as spot cargoes therefore play an important role. The government

plans to unbundle both state-owned monopolies Kepco (electricity generation) and Kogas (natural gas

wholesaler), to privatize certain assets like a number of power plants, and to introduce open access to

pipelines as well as LNG terminals.

Potential suppliers to India, already importing LNG, and China, entering soon, are concerned about the

countries’ ability to pay for LNG in hard currency. The economic level of these countries is much

lower than those of Japan, South Korea, and Taiwan when entering LNG business.24 India plans about

10 new LNG facilities, mainly in combination with power production, situated at the West coast since

electricity generation in the East is based on cheap domestic coal. Currently subsidized electricity

tariffs may lead to a situation in which customers are unable to pay the price for purchased quantities.

China is constructing a terminal at Guangdong, which is expected to come on stream in 2006. Three

additional facilities are proposed. An interesting issue is that the supply contract has another structure

than traditional Asian contracts. Oil linkage has been reduced from 85 to only 30%; hence, decreasing

price volatility is expected. Natural gas is mainly used for power production and industrial consumers.

The Chinese Petroleum Corporation is furthermore responsible for LNG imports and wholesale natural

gas supplies in Taiwan. Taipower, the state-owned power producer, is the major LNG customer.

Asian LNG prices are less competitive than European since Asia strongly depends on deliveries in the

form of LNG and importers are willing to pay the “Asian Risk Premium” (IEEJ, 2004, p. 3) of about

US 1$/MBtu. Japanese contracts are linked to crude oil prices (Japanese Customs Clearing price).

24 GDP per capita China and India (in 1990 price): < $1,000 whereas for existing Asian importers: $3,000-10,000

22

India has fixed prices without any linkage to other fuels, which are subsidized by the state. For LNG

import prices see Appendix 9.

2.2.5 Country matrix LNG strategies

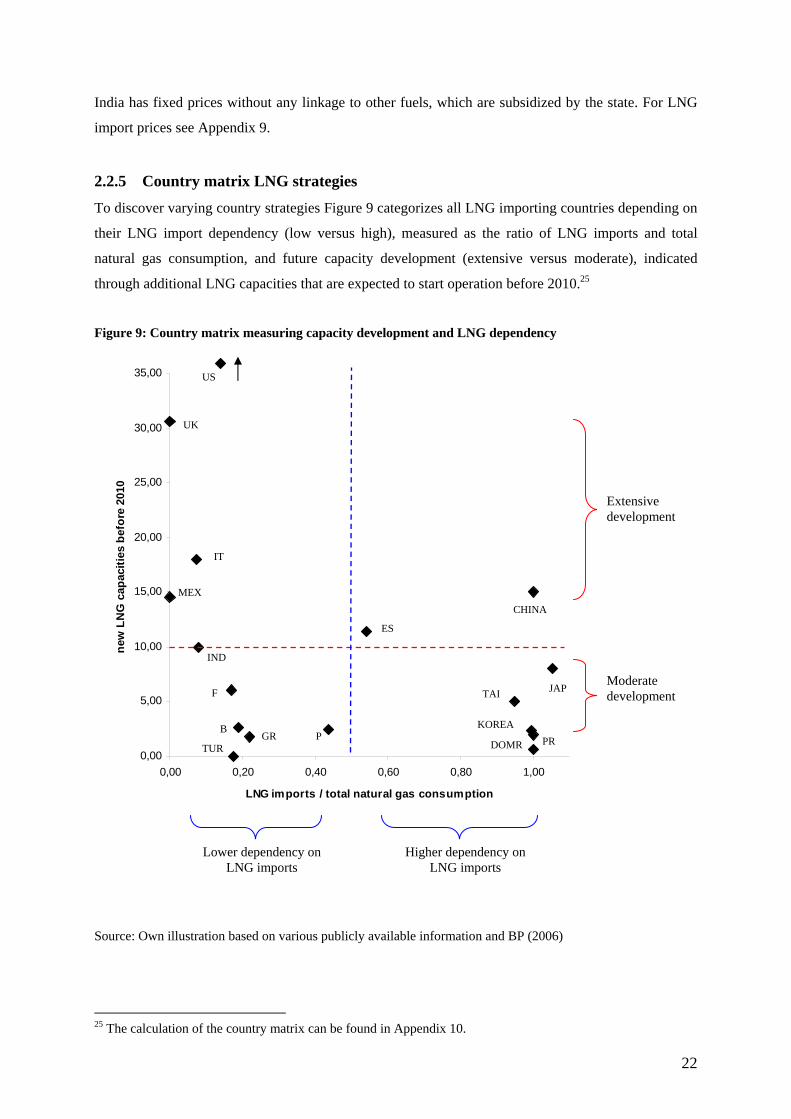

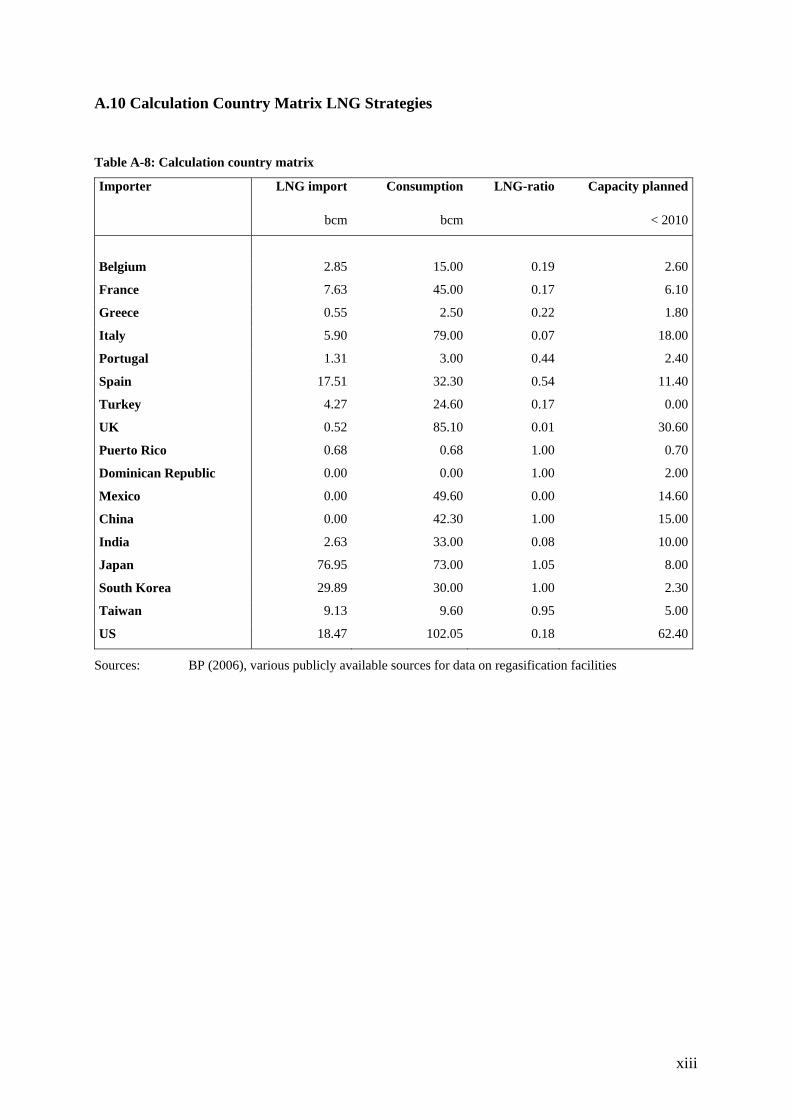

To discover varying country strategies Figure 9 categorizes all LNG importing countries depending on

their LNG import dependency (low versus high), measured as the ratio of LNG imports and total

natural gas consumption, and future capacity development (extensive versus moderate), indicated

through additional LNG capacities that are expected to start operation before 2010.25

Figure 9: Country matrix measuring capacity development and LNG dependency

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

0,00 0,20 0,40 0,60 0,80 1,00

LNG imports / total natural gas consumption

new

LN

G c

apac

ities

bef

ore

2010

Source: Own illustration based on various publicly available information and BP (2006)

25 The calculation of the country matrix can be found in Appendix 10.

Extensive development

Moderate development

Lower dependency on LNG imports

Higher dependency on LNG imports

B

F

GR

IT

P

ES

TUR

UK

PR

MEX

US

CHINA

IND

JAP

KOREA

DOMR

TAI

23

Table 5: Interpretation of the country matrix

Lower dependency on LNG import Higher dependency on LNG imports

Extensive capacity development

Italy, UK, U.S., Mexico

Diversification of supply sources

Domestic production may decline (especially UK, U.S.)

Exports of the imported LNG planned, function of transit countries (except U.S.)

Spain, China

High potential

Dependency will continue to increase, if suppliers remain the same, but it can be expected that the (natural) LNG dependency will be met with diversifica-tion of supply sources.

Moderate capacity development

Belgium, France, Greece, Portugal, Turkey, India

Saturated market or potential not recognized

This category also includes countries like Germany, Poland or Croatia discussing potential LNG receiving terminals

Puerto Rico, Dominican Republic, Japan, Taiwan, South Korea

Saturated market

Increase in LNG capacities only to an extent to meet demand increase

Source: Own illustration

Four country types can be distinguished following a categorization on LNG dependency and future

capacity development.

• Firstly, there are countries (like Italy, UK, or the U.S.) that have access to pipeline natural gas

and/or domestic production. Hence, LNG import dependency is relatively low. Although, they

plan huge investments in additional regasification capacities. Such a strategy can have

different motivations. Through a policy of diversification, energy supply security is increased.

Furthermore, different countries’ natural gas production declines (e.g. UK). To cover demand,

new supplies are necessary. Some of those countries also plan exports of surplus volumes to

third countries. An example is Italy, which may serve as a transit country to mid- and western

European consuming regions.

• Secondly, there are countries that have diversified natural gas supply sources but do not plan

to invest in significant additional capacity (e.g. Belgium, France). Markets may be saturated.

Besides, a functioning interstate trade of natural gas can substitute own LNG import terminals,

countries may benefit from capacity increases and a diversification of supply sources in

neighboring areas. All countries not involved in the LNG business yet (like Germany or

Poland) do also fall under this category.

• Thirdly, different countries being strongly dependent on LNG imports do not plan to invest in

a large number of new plants (e.g. Japan). The LNG industry is well developed; natural gas is

often employed as fuel for power generation. Existing regasification plants are able to meet

actual demand. Expansions only serve to meet natural demand increase.

• And finally, different countries, strongly dependent on LNG imports and heavily investing in

LNG infrastructure (e.g. China) with a high future potential can be identified. They do not

24

have access to major natural gas resources via pipeline and only limited domestic production.

Significant expansions in LNG import capacities are mainly required to meet increasing

demand (above world average). Natural gas serves mainly as fuel for power production.

2.3 Changing Corporate Strategies – Integrated Companies, Tollers, and New

Entrants

In times of a changing institutional environment in the natural gas sector and a rapidly increasing

industry, one observes global players active in the LNG industry following a strategy of vertical

integration along the whole value chain. In fact, this is only one part of the observed development,

whereas another part is the emergence of new non-integrated players in North American markets. In

Japan, power producers enter the LNG industry to secure their supply. Jensen (2003, p. 36) states that

“the synthesis of traditional LNG practices and a theoretical competitive market may well not yield in

the same industry structure in all regions, nor is it likely to produce one corporate model that can be

successful for all companies.” The following paragraph describes different corporate strategies and

presents case studies of (non-) integrated companies and new entrants.

2.3.1 Vertically integrated companies

Traditional long-term contracts did not require vertical integration in the sense of capacity ownership.

However, with ongoing liberalization and increasing demand worldwide global oil producing

companies heavily engage in production, liquefaction, transport, and also downstream regasification

and marketing of LNG. Private oil and gas companies join long-established state-owned entities in

exporting countries securing low cost sources and connecting the fuel to high value markets,

integrating downstream to benefit from marginal rents in the natural gas industry. In contrast,

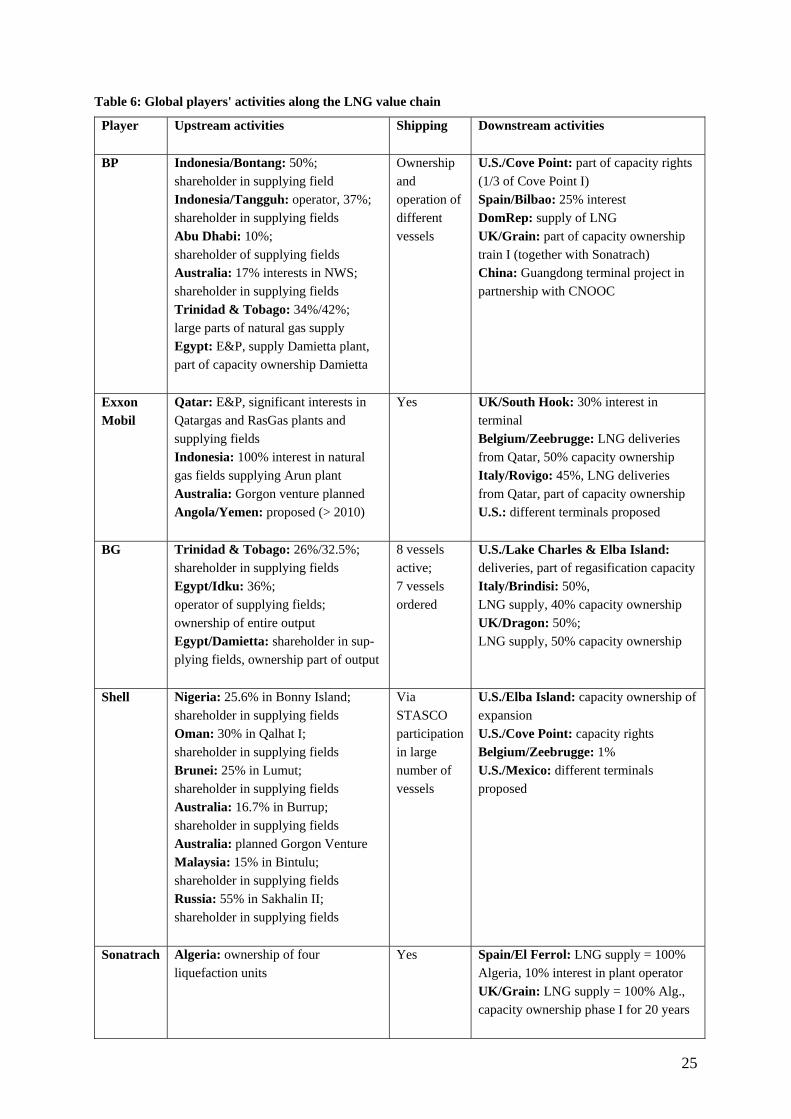

traditional downstream players integrate upstream, control transport capacities and secure access to