Corporate Social Responsibility Contracting and Firm Innovation: International Evidence Albert Tsang* Schulich School of Business York University E-mail: [email protected] Kun Tracy Wang Research School of Accounting Australian National University E-mail: [email protected] Simeng Liu Research School of Accounting Australian National University E-mail: [email protected] Li Yu Research Institute of Economics and Management Southwestern University of Finance and Economics E-mail: [email protected] This version: December 2019 Abstract Shareholders have been showing growing interest in including sustainability performance criteria in executive compensation policies. In this study, we examine the relation between the inclusion of corporate social responsibility (CSR) criteria in executive compensation schemes (i.e., CSR contracting) and firm innovation in an international context. Using a large sample of firms from 30 countries, we find that firms with CSR contracting exhibit higher levels of innovation as measured by patents granted and citations received. Moreover, consistent with the argument that CSR contracting complements country-level institutional voids by incentivizing management to implement future-oriented initiatives, we show that CSR contracting has a stronger effect on firm innovation in countries with weaker stakeholder orientation or legal environments. Finally, our results suggest that firms’ CSR contracting and CSR performance have substitutive effects on firm innovation. Overall, this study sheds light on the effect that linking executive compensation to sustainability-oriented CSR criteria has on firm innovation in a global context, which has implications for business practitioners and researchers. Keywords: sustainability; executive compensation; innovation; patent; international ___________________________________________________________________________

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Corporate Social Responsibility Contracting and Firm Innovation:

International Evidence

Albert Tsang*

Schulich School of Business

York University

E-mail: [email protected]

Kun Tracy Wang

Research School of Accounting

Australian National University

E-mail: [email protected]

Simeng Liu

Research School of Accounting

Australian National University

E-mail: [email protected]

Li Yu

Research Institute of Economics and Management

Southwestern University of Finance and Economics

E-mail: [email protected]

This version: December 2019

Abstract

Shareholders have been showing growing interest in including sustainability performance

criteria in executive compensation policies. In this study, we examine the relation between the

inclusion of corporate social responsibility (CSR) criteria in executive compensation schemes

(i.e., CSR contracting) and firm innovation in an international context. Using a large sample of

firms from 30 countries, we find that firms with CSR contracting exhibit higher levels of

innovation as measured by patents granted and citations received. Moreover, consistent with

the argument that CSR contracting complements country-level institutional voids by

incentivizing management to implement future-oriented initiatives, we show that CSR

contracting has a stronger effect on firm innovation in countries with weaker stakeholder

orientation or legal environments. Finally, our results suggest that firms’ CSR contracting and

CSR performance have substitutive effects on firm innovation. Overall, this study sheds light

on the effect that linking executive compensation to sustainability-oriented CSR criteria has on

firm innovation in a global context, which has implications for business practitioners and

researchers.

Keywords: sustainability; executive compensation; innovation; patent; international

___________________________________________________________________________

2

1. Introduction

Innovation has long been recognized as a key driver of long-term organizational success and

national economic growth (e.g., Holmström 1989; Grossman & Helpman 1990; Hall et al. 2005; Gu

2005).1 In recent decades, innovation has become an even more important investment for firms due

to rapidly increasing competitive pressure in the domestic and global markets (e.g., Aghion et al.

2005; Aghion et al. 2014). However, although shareholders generally demand firms engage in

innovative activities to maximize firm value in the long term, managers, who usually face short-term

career pressures, tend to avoid future-oriented innovative activities because of their risky and long-

term nature (Narayanan 1985; Holmström 1989; Flammer & Bansal 2017). Anecdotal evidence

provides support to this argument. For example, Graham et al. (2005) find that 78% of their surveyed

executives would sacrifice future-oriented projects with positive net present value to meet their

financial performance targets in the short-turn. Therefore, how to alleviate this agency conflict and

motivate managers to undertake more future-oriented innovation activities is an important question

for both practitioners and researchers. The large body of academic research on innovation conducted

over the past decade also suggests there is an increasing need to understand the factors that drive and

determine innovation (He & Tian 2018).

To overcome the managerial short-termism that prevents managers from investing in projects

that have the potential to create long-term value, a growing number of firms have started to include

social and environmental (or corporate social responsibility, CSR) criteria, such as employee health

and safety, CO2 emissions/water pollution targets, and the inclusion of their securities in socially

responsible indices (e.g., the Dow Jones Sustainability Index, DJSI), in their executive compensation

contracts (Hong et al. 2016; Flammer et al. 2019).2 Generally, this practice is considered a means of

1 For example, studies show that innovation is important for improving firms’ long-term financial performance (e.g.,

Bloom & Van Reenen 2002; Gu 2005; Matolcsy & Wyatt 2008; Burrus et al. 2018), increasing firm value (e.g., Hall et

al. 2005), and developing firms’ competitive advantages (e.g., Porter 1992, 1998). 2 See Appendix A for a detailed example of CSR contracting. Anecdotal evidence suggests that CSR contracting has

become increasingly prevalent and that many companies view the incorporation of CSR criteria in executive

compensation as a good corporate governance practice (Flammer et al. 2019).

3

rewarding CEOs for implementing sustainability-oriented CSR initiatives. Consistent with the view

that CSR contracting mitigates corporate short-termism, Flammer et al. (2019) show that the adoption

of CSR contracting improves the CSR performance and value of firms.3

Although numerous studies have examined the effect of incorporating financial and stock

performance targets in executive compensation on managerial behavior such as firm innovation (e.g.,

Murphy & Gibbons 1992; Lerner & Wulf 2007; Baranchuk et al. 2014; Flammer & Bansal 2017;

Mao & Zhang 2017), very little is known about whether and how the integration of nonfinancial CSR

performance measures in executive compensation affects firm innovation. Moreover, compared to

the traditional long-term pay-for-financial-performance compensation schemes that tend to mix

forward-looking features with earnings or stock price targets, contracting on nonfinancial CSR

criteria tends to provide a less noisy and more explicit reflection of long-term strategies (Bushman

et al. 1996; Ittner et al. 1997; Dikolli & Vaysman 2006; Matĕjka et al. 2009). Thus, the primary

objective of this study is to empirically examine how the adoption of this emerging yet increasingly

popular compensation practice, which aims to link executive pay to nonfinancial CSR performance

(i.e., CSR contracting), affects firm innovation.

Despite the increasing trend in the use of CSR contracting in recent years, it remains unclear

whether and how CSR contracting affects firm innovation. Competing predictions can be drawn from

the research on the relationship between CSR and firm innovation. For instance, some studies

propose that an increased commitment to more responsible practices fosters corporate innovation by

reducing managerial short-termism stemming from the desire to achieve the short-term financial

goals demanded by more prominent stakeholders, such as customers and shareholders (e.g., Chen et

al. 2016a; Chen et al. 2016b; Flammer & Kacperczyk 2016; Flammer et al. 2019). However, other

studies suggest that a greater focus on a firm’s less direct stakeholders, such as the environment, local

3 This emerging compensation practice of including CSR-related criteria in executive compensation is commonly referred

to as “CSR contracting,” “CSR-based compensation,” and “pay for social and environmental performance” by

practitioners and academics (Flammer et al. 2019). In this study, we use these terms interchangeably.

4

community, and employees, hinders the firm’s ability to invest in firm innovations that have the

potential to maximize shareholder value (e.g., Manchiraju & Rajgopal 2017; Chen et al. 2018).

Moreover, although a number of studies have shown that country-level institutional

characteristics play an important role in firms’ CSR performance (Dhaliwal et al. 2012; Ioannou &

Serafeim 2012; Dhaliwal et al. 2014; El Ghoul et al. 2017; Marano et al. 2017; Liao et al. 2019),

which suggests that the effect of CSR contracting may vary across countries, to the best of our

knowledge, no studies have explored the heterogeneity in the consequences of CSR contracting

across countries. This gap is surprising given that firms in many countries have started to link

executive/employee remuneration to performance on social and environmental issues (Velte 2016;

Burchman & Sullivan 2017).4 Our study aims to fill this gap in the literature. Thus, as a second

research objective, we further examine whether and how the relation between CSR contracting and

firm innovation varies with country-level institutional characteristics related to stakeholder

orientation and the legal environment. Studies have shown that these two major country-level

institutional variables have significant effects on firms’ CSR performance (e.g., Dhaliwal et al. 2012;

Dhaliwal et al. 2014; Ioannou and Serafeim 2012).

Using a novel database on CSR contracting and a comprehensive sample of publicly listed

firms in 30 countries, we test these competing predictions on the relation between CSR contracting

and firm innovation. After controlling for year-, industry-, and country-fixed effects and a vector of

firm-, industry-, and country-level factors that have been shown to have potential effects on firm

innovation, we find a significantly positive relation between CSR contracting and firm innovation

measured by the patents granted and citations received. The results of additional tests using a

4 For example, evidence from the 2013 KPMG Survey of Corporate Responsibility Reporting

(https://assets.kpmg/content/dam/kpmg/pdf/2013/12/corporate-responsibility-reporting-survey-2013.pdf) suggests that

more than 10% of the world’s largest companies (G250) currently provide a clear explanation in their CSR reporting of

how remuneration is linked to CSR performance (see “Linking CSR performance with pay sends clear sustainability

signal,” available at https://www.theguardian.com/sustainable-business/linking-csr-pay-sustainability). In recent years,

increasing numbers of companies have begun to link executive pay to CSR performance (see, for example,

https://www.wsj.com/articles/more-companies-link-executive-pay-to-sustainability-targets-11561379745).

5

difference-in-differences (DID) model and focusing on first-time CSR contracting lend further

support to the positive effect of CSR contracting on firm innovation.

Our results are robust to an array of additional tests including tests accounting for the potential

large sample bias and the truncation bias of the innovation variables, and the use of alternative

innovation and CSR contracting measures. We also conduct additional tests to reduce the concern

that the positive relation between CSR contracting and innovation is driven by a change of CEO, the

effect of non-CSR-related compensation schemes, and heterogeneity in corporate governance

attributes across firms. Furthermore, we use multiple approaches to address endogeneity concerns

relating to unobserved firm characteristics, including the use of a propensity score matched sample

obtained by matching CSR contracting adopters with non-adopters to increase the comparability

between the two groups, controlling firm fixed effects to account for all time-invariant firm-specific

factors, and the use of a DID method to account for the temporal variation in innovation that is not

attributable to the adoption of CSR contracting. A Heckman-type correction is also performed using

a two-stage Heckman model to mitigate potential sample selection bias.

Having established a robust positive relation between CSR contracting and firm innovation,

we next explore whether and how this positive relation varies with country-level institutional

characteristics. Consistent with the argument that CSR contracting complements country-level

institutional voids by incentivizing management to implement sustainability-oriented initiatives, we

show that the effect of CSR contracting on firm innovation is stronger in countries with weaker

stakeholder orientation or legal environments. Finally, given that both CSR contracting and CSR

performance are likely to be positively related to firm innovation, in an additional test, we further

explore whether CSR contracting and CSR performance substitute or complement each other in terms

of their effect on firm innovation. Our results indicate that a firm’s CSR contracting and CSR

performance act as substitutes in terms of their effects on firm innovation.

6

Our study contributes to the literature in several ways. First, the literature on compensation

focuses on the effects of long-term financial and equity-based executive incentives in encouraging

innovation, in view that these types of compensation are likely to mitigate managerial myopia, and

thereby encourage managerial risk-taking and align managerial interests with the creation of long-

term shareholder value (e.g., Dechow & Sloan 1991; Murphy & Gibbons 1992; Holthausen et al.

1995; Lerner & Wulf 2007; Xue 2007; Francis et al. 2011; Sheikh 2012; Flammer & Bansal 2017;

Nguyen 2018).5 Our study adds to this growing body of literature on the relation between managerial

compensation schemes and firm innovation by examining the relation between the inclusion of

nonfinancial sustainability-oriented CSR criteria in executive compensation schemes and innovation.

Second, the literature on CSR generally indicates that improved CSR performance and

stakeholder engagement lead to enhanced firm innovation (e.g., Wagner 2010; Bocquet et al. 2013;

2017; Kim et al. 2014; Luo & Du 2015; Flammer & Kacperczyk 2016; Cook et al. 2019). However,

few studies have examined how to incentivize managers to implement sustainability-oriented CSR

initiatives by crafting appropriate executive compensation contracts that, in turn, affect firm

innovation. As such, our study contributes to the literature by showing that the inclusion of CSR

criteria and targets in executive compensation schemes provides an effective incentive to motivate

managers to invest in long-term value maximization activities, and in turn fosters firm innovation.6

Finally, the increasing awareness of the importance of CSR performance for firms and the

growing significance of CSR as a corporate investment have raised the fundamental question of

whether CSR enhances shareholder value. Although a substantial number of studies have examined

this question from different perspectives, the evidence is conflicting. For example, while a number

5 Other studies, such as Sauermann and Cohen (2010), Change et al. (2015), and Jia et al. (2016), have also examined the

roles that non-CEO executives’ incentive designs and lower-ranked employees play in encouraging firm innovation. 6 Related to our study, in a U.S. setting, Flammer et al. (2019) find that the adoption of CSR contracting is conducive to

environmentally friendly innovation, measured as the proportion of green patents relative to total patents generated by

the firm. Although their research focuses on green innovation using a sample of large U.S. firms, our study sheds light

on the role of CSR contracting in promoting the overall quantity and quality of innovation and more importantly

demonstrates the cross-national differences in CSR contracting in a global context.

7

of studies have found a positive relationship between CSR performance and firm financial

performance (e.g., Orlitzky et al. 2003; Deng et al. 2013; Ferrell et al. 2016), other studies have found

evidence supporting CSR as a potential agency cost that has the potential to undermine shareholder

value (e.g., Krüger 2015; Masulis & Reza 2015).

Motivated by these conflicting findings, studies have started to examine how contextual factors

affect the relationship between CSR and firm value. For instance, Dhaliwal et al. (2011) suggest that

an important contextual factor influencing the relation between CSR performance and the cost of

equity capital is the presence of voluntary CSR disclosure. That is, CSR reporting firms with superior

CSR performance are more likely to be associated with a significantly lower cost of equity capital.

Similarly, Tsang et al. (2019b) show that the issuance of integrated reporting (i.e., disclosures that

integrate financial and non-financial CSR information) moderates the relation between CSR

performance and firm value. Lins et al. (2017) find that the financial performance implications of

CSR performance can vary across time. Specifically, they show that CSR performance can generate

more value during financial crises (i.e., when the overall level of trust in corporations and markets is

low). Thus, our finding of a substitutive effect between CSR performance and CSR contracting

contributes to the debate by demonstrating the potential role that CSR contracting can play in the

relation between CSR performance and firm innovation.

Our study also has practical implications for business practitioners, such as controlling

shareholders and board of directors, in terms of how to design appropriate executive compensation

schemes to effectively motivate managers to engage in firm innovation and long-term value creation.

Our results highlight that CSR contracting, as an emerging corporate governance mechanism, can be

used to stimulate firm innovation, especially for firms with fewer future-oriented initiatives and firms

domiciled in countries with weaker stakeholder orientation or legal environments.

The remainder of this study is organized as follows. In Section 2, we develop two competing

hypotheses on the relation between CSR contracting and firm innovation. Section 3 describes the

8

research design, including the sample selection, model specification, and variable construction.

Section 4 presents the sample distribution, summary statistics, and empirical results of the hypothesis

tests and robustness checks. In Section 5, we perform additional tests to further explore the relation

of interest. Finally, Section 6 concludes the study.

2. Related Literature and Hypotheses Development

In recent years, there have been a number of significant environmental, regulatory, and social

developments in countries around the world. For example, publicly listed Indian firms are now

required to spend at least 2% of their net income on CSR (Manchiraju & Rajgopal 2017). Moreover,

countries such as China, Denmark, Malaysia, and South Africa have introduced regulations requiring

firms to conduct CSR reporting (Ioannou & Serafeim 2017). With the growing acceptance of

sustainability as an important driver of business value, many firms have started to integrate CSR

criteria in their executive compensation packages to ensure that the notion of sustainability is

effectively embedded with the organization (Forbes 2010; E&Y 2010; GreenBiz 2015).7 CSR-based

executive compensation generally links executive compensation to the performance of a wide range

of stakeholder-friendly initiatives. This compensation practice tends to focus on the interests of

different non-shareholder stakeholders, such as employees, customers, the community, and the

environment, by setting managerial targets to address their needs.8

7 For example, shareholder proposal No. 6 in the 2018 proxy ballot of United Parcel Service, Inc. (UPS) states,

“Shareholders request the Board Compensation Committee prepare a report assessing the feasibility of integrating

sustainability metrics into the performance measures of senior executives under the Company’s compensation incentive

plans.” This proposal is supported by the investors’ belief that “Linking executive compensation and sustainability would

help position UPS for sustainability leadership and drive improvement on challenges that our Company has defined as

material.” Available at http://www.investors.ups.com/node/25326/html. 8 For example, the Netherlands’ international energy enterprise Shell PLC links 20% of its executives’ annual bonuses

and 10% of their long-term incentive plans to sustainable development, especially in relation to carbon reduction (Royal

Dutch Shell Plc 2018). Similarly, the U.S multinational retail corporation Walmart Inc. links its executives’ annual

incentives with diversity/inclusion and ethics/compliance goals (Walmart Inc. 2019). Xcel Energy links its annual

incentive awards for executives to environmental (e.g., greenhouse gas reduction goals) and social metrics (e.g.,

employee safety) (Xcel Energy 2011).

9

Survey evidence further suggests that the practice of linking sustainability objectives to

executive compensation (i.e., the adoption of CSR contracting) has become a global trend. For

example, a survey of the constituents of the indices in 11 global markets, including the U.S., U.K.,

Australia, France, Germany, and the Netherlands, found that 42% of the companies studied provided

a link between sustainability and executive compensation (Glass Lewis 2010). Supporting the

growing prevalence of CSR contracting, our sample from a large number of countries shows that

while less than 5% of firms globally used explicit CSR contracting in 2004, the ratio increased to

more than 14% in 2015.

As a typical long-term investment activity, innovation can improve firms’ financial

performance and long-term firm value (Gu 2005; Hall et al. 2005; Matolcsy & Wyatt 2008). In this

section, we develop two competing hypotheses on the relation between the adoption of CSR

contracting and firm innovation. Agency theory suggests that managers tend to underinvest in

innovative activities in consideration of the long investment horizons and high failure rates of

innovation (Baysinger et al. 1991; Holmström 1989, 1999; Frederick et al. 2002; Ferreira et al. 2014).

Although shareholders care about firms’ long-term performance, managers tend to be more myopic

and focus excessively on short-term results because of their career concerns (Narayanan 1985; Stein

1989; Degeorge et al. 1999). Thus, the short-termism of managers could induce them to invest in

projects with short-term payoffs at the cost of valuable long-term projects such as innovative

activities, even if the latter are expected to yield higher returns (Stein 1989; Holmström 1999).

Research shows that CSR contracting mitigates managers’ short-termism and fosters long-term

orientation (Matĕjka et al. 2009; Flammer et al. 2019). Thus, the managers of firms that implement

this compensation practice are likely to divert their attention from short-term financial gain to longer-

term value creation, and are thereby likely to engage in more future-oriented investment projects

(Dikolli & Vaysman 2006; Matĕjka et al. 2009). In line with this, it is likely that firms that include

CSR criteria in their executive compensation schemes will place greater emphasis on sustainability-

10

oriented investments that are valuable to the shareholders over the long term and subsequently

undertake more future-oriented innovation activities.

Although in our study, we argue that CSR contracting incentivizes managers to increase their

investment in CSR performance, which in terms creates a positive externality on shareholders’ value

by fostering future-oriented innovation activities, it could be argued that improvements in CSR

performance have little impact on firms’ innovation. This argument is plausible especially given that

CSR activities are more likely to be associated with the interests of non-shareholder stakeholders

than shareholders. However, it is worth noting that greater effort to improve CSR performance can

also directly affect shareholders’ value through its direct effect on firms’ innovation outcomes. For

example, Ryou et al. (2019) suggest that CSR activity can be considered as a type of product

innovation (e.g., the creation of new socially responsible product features or categories) and process

innovation (e.g., the use of socially responsible production processes). 9 In a similar vein, Flammer

et al. (2019) show that the adoption of CSR contracting leads to increased green innovation.

Thus, to the extent that integrating CSR criteria in executive compensation can have a positive

effect in fostering executives’ long-term orientation, which is essential for innovation, we posit that

the adoption of CSR contracting likely fosters firms’ innovation success. Accordingly, we state our

first hypothesis formally as follows.

Hypothesis 1a. CSR contacting has a positive impact on firm innovation.

Alternatively, integrating CSR criteria in executive compensation may have a non-significant

or even a negative impact on firm innovation. First, CSR-based compensation may merely serve as

a symbolic component that has no substantial influence on managers’ behavior (Westphal & Zajac

1994; Zajac & Westphal 1995). For example, executive compensation mainly comprises a fixed

9 According to the Thomson Reuters ASSET4 database, “Product Innovation” is a major category for measuring firms’

CSR performance. Specifically, the product innovation category measures a firm’s commitment to and effectiveness in

supporting research and development on eco-efficient products, technologies, and services.

11

salary with contingent payments linked to the firm’s financial performance, and CSR contracting

may only represent a small proportion of the overall compensation and may be too trivial to influence

managers’ business decisions or effectively divert their attention toward long-term investments in

areas such as innovation. Moreover, executives who have a substantial influence over their boards

may take the initiative to use CSR contracting to enhance the legitimacy of their formal compensation

contracts and improve shareholders’ impressions of them and the firm (Tedeschi & Reiss 1981;

Schlenker 1980). In this case, the adoption of CSR contracting would be expected to have no effect

on firm innovation.

Second, even if CSR contracting contributes to enhanced stakeholder engagement, the role that

better stakeholder engagement plays in firm innovation is unclear. For example, it is possible that

enhanced stakeholder engagement entrenches the roles of executives and employees by increasing

their job security and reducing the likelihood of dismissal (Cespa & Cestone 2007), which in turn

would reduce their incentives for innovation. It is also possible that an improved relationship between

managers and employees would result in the managers and employees enjoying the “quiet life” with

reduced incentives for undertaking risky activities such as innovation (Bertrand & Mullainathan

2003).

Third, according to Friedman (1970), a firm’s commitment to its stakeholders may draw limited

and valuable resources away from activities that maximize profits and shareholder value. That is, a

greater focus on the firm’s nonfinancial CSR performance as a result of CSR contracting may divert

limited financial, human, and physical resources from innovation activities to CSR investment,

thereby reducing the firm’s innovation success. Supporting this view, studies have shown that greater

CSR investment and more CSR reporting requirements hinder firms’ profitability and shareholders’

value (Manchiraju & Rajgopal 2017; Chen et al. 2018).

Finally, Hubbard et al. (2017) show that investments in CSR initiatives can expose the CEOs

of firms with poor financial performance to a greater risk of dismissal. Although the long-term returns

12

on firms’ innovation investments are unlikely to be certain, it is more certain that the firms would

need to make substantial investments in innovation in the short term which may hinder firms’

financial performance. Thus, it is possible that managers may reduce their investments in innovation

to reduce their career concerns when they are required to place greater emphasis on CSR performance,

for instance, through the integration of CSR criteria in executive compensation schemes.

Taken together, these discussions suggest that CSR contracting may hinder firms’ innovation.

Accordingly, we state the alternative hypothesis formally as follows:

Hypothesis 1b. CSR contracting has a negative (or no) impact on firm innovation.

3. Research Design

3.1 Sample selection and data collection

We begin our sample selection by first obtaining information about firms’ executive

compensation policies and CSR performance from the Thomson Reuters ASSET4 database. Our

sample period starts from 2004 because this is the first year that ASSET4 provides global coverage

of executive compensation policy data on whether a firm includes CSR criteria in executive

performance evaluation. As research suggests that there is generally a lag (e.g., one to two years)

between the filing year and the actual grant year of patents (Hall et al. 2001; Fang et al., 2014; Zhong

2018), we end our CSR contracting sample in 2015 to ensure that the patent data are available in the

two-year leading period of each sample year. Next, we merge the compensation data from ASSET4

with the Worldscope database, which provides accounting and financial information on publicly

listed firms globally.

We further collect the patent and citation data for our innovation measures from the BvD Orbis

patent database.10 We then calculate the total number of patents filed and citations received by a

10 This database contains patent and citation information on about 115 million patent applications and around 300 million

firms around the world. Compared with other widely used patent databases, including the National Bureau of Economic

Research patent database and the Harvard Patent Network Database, this database provides more comprehensive

coverage of global firms over a longer period, thus enabling the construction of a larger sample.

13

patent owner in a year. For the firm-year observations without patent or citation information, a value

of zero is assigned. Country-level data are collected from the World Bank’s official website

(https://www.worldbank.org). We exclude firm-years with missing data and remove countries with

less than 50 observations, leading to a final sample comprising 17,855 firm-year observations from

30 countries from 2004 to 2015.

3.2. Model specification

To examine whether and how the use of CSR contracting is associated with corporate

innovation, we estimate the following regression model:

INNOVATIONijt+1 = 0 + 1CSRContractingijt + 2CSRPerfijt + All Other

Controls + YearFE + IndustryFE + CountryFE + ijt (1)

where i indexes the firm, j indexes the country, and t indexes the fiscal year. We use one-year forward

innovation measures to account for the time needed to complete innovation projects.11 All standard

errors in the regressions are clustered at the firm level to account for possible correlations in the error

terms. Detailed definitions of the variables are provided in Appendix B.

In our study, corporate innovation is measured using output-oriented measures (i.e., patents

and citations) instead of input-oriented measures (i.e., R&D expenditure or R&D capital) in

consideration of the inconsistencies in accounting for R&D across countries. As our study is

conducted in an international context, the differences in accounting standards among countries could

lead to substantial inconsistent accounting treatments for R&D activities. For example, ASC 730 of

the U.S. GAAP mandates that all R&D spending be expensed as incurred except in several specific

cases (e.g., software development costs), whereas although IAS 38 of IFRS requires all research costs

to be expensed, part of the development cost should be capitalized when certain criteria are met

(Deloitte 2019; KPMG 2019). These inconsistencies in accounting standards indicate that the

11 For brevity, we report the results using one-year forward innovation measures. Using two-year forward innovation

measures does not change our inference.

14

differences in reported R&D expenditures do not necessarily represent the differences in innovative

efforts.12

We then construct two patent-based innovation measures following innovation literature (Hall

et al. 2005; Tian & Wang 2014; Flammer & Kacperczyk 2016; Francis et al. 2018). The first measure

is the patent count (PATENT), which is defined as the natural logarithm of one plus the number of

patents filed by a firm in a given year that are eventually granted. We use the patent application year

when calculating PATENT because compared to the grant year, the patent application year better

captures the actual timing of the patented innovation (Griliches et al. 1988; Hall et al. 2001).

Although a simple count of patents can capture the quantity of innovation, it does not differentiate

impactful breakthrough inventions from incremental technological discoveries (Sevilir & Tian 2012;

Nguyen 2018). In addition, according to Griliches et al. (1988), there is extreme skewness in the

distribution curve of patent value due to the existence of small numbers of highly valued and cited

patents. In view of the large variation in patent quality, we take the number of citations received by

patents as the second proxy, which reflects the technological and economic significance of the

patented innovation (Trajtenberg 1990; Hall et al. 2005). Thus, the second measure of innovation

output is the citation count (CITATION), which is defined as the natural logarithm of one plus the

number of citations received for all patents granted to a firm during a given year. For the above two

measures of innovation output, the transformation using the natural logarithm of the patent (citation)

count plus one can avoid the loss of observations with zero patents (citations) and alleviate the right-

skewness in the patent (citation) distribution.

The test variable of interest is CSR contracting (CSRContracting), which is constructed as an

indicator variable that equals 1 if CSR (or health and safety, or sustainability) performance targets

are included in the firm’s executive compensation contracts in that year and 0 otherwise. Thus, the

12 Supporting this argument, Koh and Reeb (2015) show that even firms that do not report R&D expenditures may still

engage in innovation and acquire patents.

15

coefficient of interest 1 captures the change in corporate innovation associated with the inclusion of

CSR-related criteria in executive compensation. Following the prediction of Hypothesis 1a (1b), we

expect that CSR contracting will have a positive (negative) association with corporate innovation.

Following the literature (e.g., Hall & Ziedonis 2001; Chen et al. 2016a; Flammer & Kacperczyk

2016; Francis et al. 2018; Zhong 2018; Flammer et al. 2019; Tsang et al. 2019a), we control for a set

of firm-, industry-, and country-level variables that may affect innovation output when examining

the relation between CSR contracting and corporate innovation. First, as studies have shown that

CSR performance has a positive impact on firm innovation (e.g., Bocquet et al. 2013; 2017; Luo &

Du 2015), we include in the model a firm-year’s overall CSR performance (CSRPerf), which is

defined as the average of the firm-year’s social and environmental performance scores based on the

data from ASSET4. The value of CSRPerf ranges between 0 and 100, with a higher value indicating

better CSR performance. Second, we control for the existence of long-term financial targets in

executive compensation (Comp_LongtermFin) because the literature (e.g., Murphy & Gibbons 1992;

Manso 2011) suggests that this executive compensation design plays an important role in fostering

corporate innovation by encouraging managers to focus on long-term value creation. Third, given

that R&D intensity is positively related to innovation output (e.g., Bradley et al. 2017), we include

R&D intensity (R&D) as a control, which is constructed as R&D expenditure scaled by total assets.

We control for capital intensity (i.e., the capital-labor ratio) (CapitalIntensity) because Hall and

Ziedonis (2001) have demonstrated that capital intensive firms tend to patent more aggressively to

avoid costly litigation and improve their negotiating position with other patent owners. Older firms

tend to generate more innovations as they have accumulated more experience in conducting

innovation activities compared to younger enterprises (Sørensen & Stuart 2000). Thus, we also

include firm age (Age) in the model. The literature shows that firm size, profitability, growth

opportunities, capital structure, and access to external financing could also impact firms’ engagement

in costly, risky, and long-term innovative projects (e.g., Kleinknecht 1989; Audretsch 1995; O’Brien

16

2003; Brown et al. 2009, 2013; Wies & Moorman 2015; Lyandres & Palazzo 2016). Correspondingly,

we control for an array of relevant corporate characteristics including firm size (Size), return on assets

(ROA), market-to-book ratio (MTB), sales growth (SalesGrowth), leverage ratio (Leverage), level of

cash holdings (CASH), and access to external financing (ExternalFinance). In addition, we control

the percentage of foreign sales (ForeignSales) because the literature suggests that exposure to foreign

markets has a positive effect on firm innovation (Alvarez & Robertson 2014). We also include the

percentage of closely held shares (InsiderOwnership) as research suggests it may influence

managerial incentives to innovate (e.g., Francis & Smith 1995; Choi et al. 2011).

Furthermore, at the industry level, Aghion et al. (2005) show that the relationship between

market competition and innovation takes an inverted-U shape, so we control for the degree of product

market competition using the Herfindahl-Hirschman index (HHI), which is calculated as the sum of

the squared market shares in the sales of a firm’s industry, with industries being classified based on

the three-digit SIC codes in each country. The squared term of the Herfindahl-Hirschman index (HHI2)

is also included to mitigate the possible non-linear relation between industry competition and

corporate innovation. At the country level, we control for GDP per capita (LNGDP) to capture the

aggregate technological sophistication at the country level (Furman et al. 2002). Finally, year-,

industry- and country-fixed effects (YearFE, IndustryFE, and CountryFE) are included to control for

variations in patenting and citation intensities over time, by industry, and across countries.

4. Empirical Results

4.1. Sample distribution

Panel A of Table 1 presents the sample distribution and summary statistics by country.13 There

are large variations in the number of observations, the percentage of CSR contracting adopters, and

13 As a large proportion of firm-year observations are not associated with a patent or citation, we also provide summary

statistics for the innovation output of firms that have at least one patent (i.e., the patent sample) or citation (i.e., the

citation sample).

17

innovation output across the 30 countries in our sample. As in many international studies, U.S. firms

comprise the largest proportion of the sample (34.11%). In our full sample, firm-years with the

presence of CSR contracting account for 15.84% of the sample. Australia has the highest percentage

of CSR contracting adopters (39.85%), followed by Norway (36.89%) and South Africa (35.45%).

The most innovative country in our sample is Japan, where firms have, on average, 219.44 patents

and 138.12 citations, followed by South Korea, Finland, Germany, and the U.S.

Panel B of Table 1 presents the sample distribution and summary statistics over time. Over the

sample period, the number of firms included in the sample shows a generally increasing trend, from

855 firms in 2004 to 2,523 firms in 2015, indicating the increasing coverage of ASSET4. The results

also indicate that firms increasingly adopt CSR contracting over the sample period, rising from 1.87%

of firms in 2004 to 32.29% in 2014, although the ratio drops slightly to 24.73% in 2015. The overall

rising trend also reflects the emerging practice of linking CSR criteria to executive incentive schemes

in recent years, which further highlights the need for research on CSR contracting.

In terms of innovation output, our data show a significant decrease in the average number of

patents a firm applies for and is granted each year over the last several years of the sample period.

This decline could be due to the significant time lag between a patent application and the granting of

the patent (Hall et al. 2001; Fang et al. 2014), as we only observe the information on a patent after it

has been granted. Thus, it is likely that some patents applied for in the last few years of the sample

period may have still been under review and not been granted, and hence are not included in the

database and our sample. Citation data are subject to a similar truncation bias because patents granted

in later years tend to have fewer citations than those granted in the early years of the sample period.

In our robustness tests, we use truncation-adjusted patent and citation counts to address the concerns

relating to the truncation bias in our patent and citation data.

Table 1, Panel C reports the sample distribution and summary statistics across industry sectors.

The three industries with the highest proportions of CSR contracting are the extractive (29.91%),

18

mining/construction (26.12%), and chemicals (20.19%) industries, all of which are among the

world’s most polluting industries according to a report prepared by Pure Earth and Green Cross

(2016), two international non-profit organizations. This suggests that CSR contracting is more

prevalent in less eco-friendly industries, perhaps because these industries seek to reduce their

environmental impact and obtain a social license to operate. In contrast, the industry with the lowest

proportion of CSR contracting is the miscellaneous manufacturing sector (3.71%). The three most

innovative industries are electrical equipment manufacturing, transportation equipment

manufacturing, and computers, which is consistent with the intuition that the firms in these industries

perceive innovative technologies and products as an important means of securing competitive

advantage. In contrast, firms in the retail industries tend to be less innovative.

[Table 1 here]

4.2. Summary statistics

Table 2 provides the descriptive statistics for all variables used in the main regression analyses.

All variables are winsorized at the 1st and 99th percentile to reduce the potential impact of outliers.

In the full sample, firms on average have 43 patents and 45 citations.14 The distribution of the patents

and citations shows a high degree of right-skewness, with the median being much smaller than the

corresponding mean, which suggests that a very small portion of observations have substantially

higher patent quantity and quality, which is consistent with prior studies (e.g., Griliches et al. 1988;

Zhong 2018). Therefore, we follow the literature and use the log transformation of the patent and

citation data in our regression analysis to correct the skewness of these variables. The mean of

CSRContracting is 0.158, indicating that 15.8% of the firm-year observations in the sample include

CSR-related criteria in their executive compensation schemes.

[Table 2 here]

14 The average patent and citation counts in the sample are larger than those reported by Francis et al. (2018), another

international study on innovation, mainly because we include firms from Japan and South Korea in our sample. The firms

in these countries generate significantly higher numbers of patents and receive more citations than firms in other countries.

19

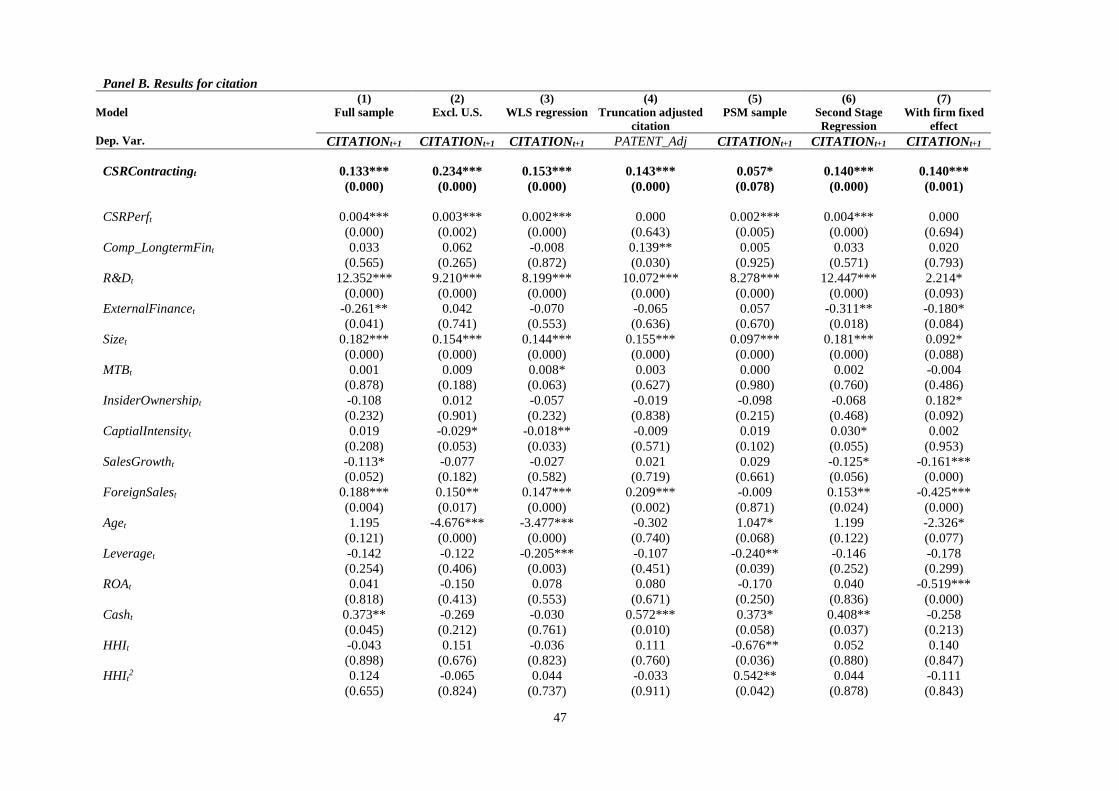

4.3. Main results

The main regression results of testing the competing hypotheses on the association between

CSR contracting and firm innovation are presented in Panels A (for the patent model) and B (for the

citation model) of Table 3. We find a significantly positive relation between CSRContracting and

firms’ patent counts (β = 0.106, p < 0.01 in Panel A, Column 1) and citation counts (β = 0.133, p <

0.001 in Panel B, Column 1), which provides support for Hypothesis 1a that the adoption of CSR

contracting has a positive effect on firm innovation. From an economic perspective, these results

indicate that controlling for other factors, linking executive compensation to CSR targets increases

the numbers of patents and citations by 10.6% and 13.3% on average, respectively. The signs of the

coefficients on the control variables are generally consistent with our predictions and consistent with

the innovation literature (e.g., Sørensen & Stuart 2000; Hall & Ziedonis 2001; Furman et al. 2002;

Brown et al. 2009; Lyandres & Palazzo 2016).

[Table 3 here]

4.4. Mitigating large sample bias

As shown in Panel A of Table 1, our sample is dominated by U.S. firms, which account for

about 34% of the sample. The large presence of firms from a single country gives rise to concerns

about large sample bias. To address this concern, we perform a robustness check by excluding U.S.

firms from the sample and rerunning the main regression. The regression results are presented in

Column 2 of Panels A and B of Table 3. Consistent with the main results, the coefficients on

CSRContracting remain positive and significant (β = 0.163, p < 0.001 for the patent model; β = 0.234,

p < 0.001 for the citation model). Furthermore, to assess whether heterogeneity in the number of

firm-years across countries affects our results, we apply a weighted least squares (WLS) model in

which the weight is the inverse of the number of observations per country. Column 3 of Table 3

reports the results of the WLS regressions for PATENT and CITATION. The coefficients on

CSRContracting are 0.154 (p < 0.001) and 0.153 (p < 0.001) for the patent and citation models,

20

respectively, which are statistically and economically similar to our main results. In summary, these

robustness tests demonstrate that our finding of a positive relation between CSR contracting and

innovation is not driven by countries with a larger presence in the sample, and is a phenomenon that

is applicable to firms in all of the sample countries.

4.5. Addressing truncation bias

The truncation bias in the patent counts arises from the significant time lag between a patent

application and the granting of the patent (Hall 2001; Fang et al. 2014). Although PATENT measures

the number of patents applied for by a firm in a given year that are eventually granted, some of the

patents applied for in the later years of the sample period may still have been under review, and

therefore not included in the BvD database. This truncation problem leads to underreported patent

counts toward the end of the sample period. Following Hall et al. (2001, 2005), we use adjustment

factors to address the truncation bias in the patent dataset and compute the truncation-adjusted patent

counts.15 Similar to the patent counts, the citation counts are also subject to a truncation problem

because firms can accumulate more citations over time. Thus, we make a similar adjustment to the

citation counts. Column 4 of Table 3 reports the results using the truncation-adjusted patent and

citation data. Our inference of a positive relation between CSR contracting and innovation remains

unchanged after accounting for truncation bias.

4.6. Addressing additional endogeneity concerns

In this section, we address potential endogeneity concerns arising from omitted variables by

using the PSM approach and controlling for firm-fixed effects.

15 First, we estimate the application-grant lag distribution (Ws) for the first-half of the sample period from 2005 to 2010.

This is calculated as the percentage of patents applied for in a given year that are granted in s years. Then, truncation-

adjusted patent numbers are computed for the sample years from 2011 to 2015 by applying the adjustment factors to the

raw patent numbers. More specifically, the truncation-adjusted patent counts are Padj = 𝑃𝑟𝑎𝑤

∑ 𝑊𝑠2016−𝑡𝑠=0

, where Praw is the raw

(unadjusted) number of patent applications at year t and 2011=<t<=2016.

21

4.6.1. Propensity-score matched sample

A potential endogeneity concern is that firms that adopt CSR contracting may exhibit

fundamentally different characteristics compared to non-adopters, and these characteristics may

affect both the adoption of CSR contracting and innovation, and lead to a spurious correlation

between CSR contracting and firm innovation. For example, larger firms and more profitable firms

may be more likely to adopt CSR contracting and may also be more innovative. To address the

concern that controlling for the potential confounding factors in our main regression model may not

fully address the comparability of CSR contracting adopters and non-adopters, we use the PSM

approach to match CSR contracting adopters (the treatment group) with non-adopters (control group)

using one-to-one nearest neighbor propensity score matching without replacement. The matching is

based on firm size, industry, year, and country. To increase the comparability of the treatment and

control groups, we further require a caliper (the value for the maximum distance of the controls) of

0.01 for the matching. This matching process yields a matched sample of 4,748 firm years, consisting

of 2,374 firm years for CSR contracting adopters and 2,374 firm years for non-adopters.16 Column 5

of Panels A and B of Table 3 present the results using the PSM sample. The results demonstrate that

our inference remains unchanged.

4.6.2. Controlling for firm-fixed effects

We also include firm fixed effects in the regressions to capture time-invariant unobservable

firm characteristics. In particular, if the unobservable firm characteristics that are correlated with

both CSR contracting and innovation are constant over time, controlling for firm fixed effects will

help alleviate the omitted variable concern. The results of the regressions that include firm fixed

effects are reported in Column 6 in Panels A and B of Table 3. The coefficients on CSRContracting

16 Appendix C reports the summary statistics for the treatment and control groups and the differences in the means of the

two groups. Compared to non-adopters, CSR contracting adopters have significantly larger PATENT and CITATION

values, which is consistent with our main results based on the full sample. In addition, CSR contracting adopters do not

exhibit significant differences from non-adopters in terms of most of the control variables used in the regression model.

22

remain significantly positive (β = 0.087, p < 0.001 for the patent model, and β = 0.140, p < 0.001 for

the citation model).

4.7. Addressing the potential sample selection bias

As all of our sample firms are covered by the ASSET4 database, a potential concern is that our

results may be subject to sample selection bias if the decision on whether to include a firm in the

database is not random. To address this concern, we follow the literature (e.g., El Ghoul et al. 2017)

and perform a Heckman-type correction using a two-stage Heckman model. We merge the sample

from ASSET4 with the Worldscope data and distinguish firms covered in ASSET4 from those not

covered by generating an indicator variable ASSET4 Sample, which equals 1 if an observation is

covered in ASSET4, and 0 otherwise. In the first stage regression, we estimate a probit model by

regressing the dependent variable, ASSET4 Sample, on a set of explanatory variables that may have

affected the decision of ASSET4 on whether to cover a firm in that year. Using this model, we obtain

the inverse Mills ratio (Mills). In the second stage, we add Mills to Equation (1) to control for sample

selection bias.17 The second stage results presented in Column 7 of Table 3 show that the coefficients

on CSRContracting remain statistically and economically similar to our main results.

4.8. Alternative measures of innovation

In addition to using innovation output measures based on the patent and citation counts, we use

innovation efficiency and patent value as alternative innovation measures. First, following the

innovation literature (Lanjouw & Schankerman 2004; Becker-Blease 2011; Hirshleifer et al. 2013;

Zhong 2018), we use innovation efficiency (PATENT_Efficiency and CITATION_Efficiency) as our

first alternative innovation measure. We define PATENT_Efficiency (CITATION_Efficiency) as the

number of patents (citations) granted in a year divided by R&D capital (RDC), where RDC is

computed as R&Dt + 0.8R&Dt-1 + 0.6R&Dt-2 + 0.4R&Dt-3 + 0.2R&Dt-4 (Hirshleifer et al. 2013;

17 The results of the first stage regression are reported in Appendix D.

23

Zhong 2018).18 The results using PATENT_Efficiency and CITATION_Efficiency as the dependent

variables are presented in Columns 1 and 2 of Table 4.19 The second alternative measure of firm

innovation is PATENT_Value, which represents the economic value of innovation outcomes.

Following Kogan et al. (2017), the measure is calculated as the change in the market value of a firm

(adjusted by the average market return during the same measurement window) in the three-day

window following the patent grant announcement. Overall, our additional tests using the alternative

innovation measures show that CSR contracting helps increase the innovation efficiency and

economic value of innovation outputs.

[Table 4 here]

4.9. Additional robustness tests

4.9.1 Alternative measure of CSR contracting using data from Sustainalytics

In the previous tests, we used CSR contracting data from ASSET4. We now test the robustness

of our findings using CSR contracting data from an alternative database. Specifically,

CSRContracting_Alt is an indicator variable that equals 1 if a firm’s executive compensation is

explicitly tied to environmental, social, and corporate governance (ESG) performance targets based

on data from Sustainalytics, and 0 otherwise. We also take into account the more general corporate

governance practice of simply setting ESG performance targets that are not explicitly linked to

executive compensation, ExecutivePerf_ESGtarget.20 The results are presented in Table 5.21 The

coefficients on CSRContracting_Alt in both panels are significantly positive and quantitatively

18 RDC is calculated using five-year cumulative R&D expenses with the assumption of an annual depreciation rate of 20%

(Chan et al. 2001; Lev et al. 2005). Missing R&D expenditures are set as 0 for the calculation of RDC. 19 The control variable R&D is removed from this regression due to the mechanical relation between innovation efficiency

(scaled by R&D investment) and R&D. The results remain quantitatively and statistically similar when we include R&D

as a control in the regressions. 20 Sustainalytics provides worldwide ESG data on firms’ policies, programs, and preparedness for ESG risk management.

CSRContracting_Alt and ExecutivePerf_ESGtarget are constructed based on Sustainalytics’ data item “G.2.6, which

provides an assessment of whether a part of executive remuneration is explicitly linked to sustainability performance

targets, such as health and safety targets, environmental targets, etc.,” and “G.2.5, which provides an assessment of

whether there is explicit responsibility at the board level for ESG issues and/or whether there are committees dealing

with ESG issues and how they are linked to the company board.” 21 The sample size in this table is reduced significantly to 4,411 firm-years because the Sustainalytics database starts from

2009 and covers a much smaller sample of international firms than ASSET4.

24

similar to those on CSRContracting in Table 3. Notably, the coefficients on

ExecutivePerf_ESGtarget are insignificant, indicating that simply setting ESG targets without

explicitly linking executives’ remuneration to the targets does not appear to enhance innovation. This

finding again, lends support to the importance of explicitly linking CSR performance targets in

executive compensation policies in motivating managers’ behavior change.

4.9.2. Pre- and post-CSR contracting analysis using a difference-in-differences model

We also use a DID method to compare the changes in innovation between firms with CSR

contracting and those without. Following studies examining the effect of the staggered adoption of

laws and regulations (e.g., Bourveau et al. 2018; Tsang et al. 2019a), we use a staggered DID design.

Specifically, we create the variable POST_CSRContracting, which is an indicator variable that equals

1 for the year in which a firm adopts CSR contracting and any year after, and 0 otherwise. For the

control firms, we randomly assign a CSR contracting adoption year when defining

POST_CSRContracting. The results using the DID method with the inclusion of year and firm fixed

effects are reported in Column 2 of Panels A and B of Table 5. The coefficients on

POST_CSRContracting are 0.062 (p = 0.019) for the patent model and 0.133 (p = 0.008) for the

citation model, both of which are positive and statistically significant.22

4.9.3. Alternative measurement window for innovation

To investigate whether the findings are robust to the choice of measurement window, we

restrict the sample to a [t-3, t+3] window (with t denoting the year in which a firm adopts CSR

contracting) for measuring the patent outputs and rerun the regression. To be included in the test

sample, a firm is required to be observable during the pre- and post-CSR contracting periods. This

additional requirement helps mitigate the potential influence of the differences in firm composition

and sample years during the pre- and post-adoption periods on our findings. As presented in Column

22 By focusing on the cross-temporal differences in innovation between the treatment and control groups before and after

the adoption of CSR contracting, the DID method controls for the unobservable cross-temporal trends in firm innovation

and eliminates the influence of temporal variation in innovation that is not caused by the adoption of CSR contracting,

and thereby helps to address issues relating to unobserved heterogeneity and endogeneity (Bertrand et al. 2004).

25

3 of Panels A and B of Table 5, the coefficients on CSRContracting remain significantly positive (β

= 0.081, p < 0.001 and β = 0.101, p = 0.005 for the patent model and citation model, respectively).

4.10. Addressing possible alternative explanations

4.10.1. CEO changes

A remaining concern is that our results may be explained by factors such as top executive

turnover, which is also likely to influence corporate innovation strategies and outputs. To ensure our

findings are not driven by CEO changes, we exclude all firm-years for firms that experienced a CEO

change during the sample period. As reported in Column 4 of Panels A and B of Table 5, the

coefficients on CSRContracting remain significantly positive and quantitatively similar to the main

results (β = 0.091, p < 0.05 for the patent model and β = 0.184, p = 0.001 for the citation model).

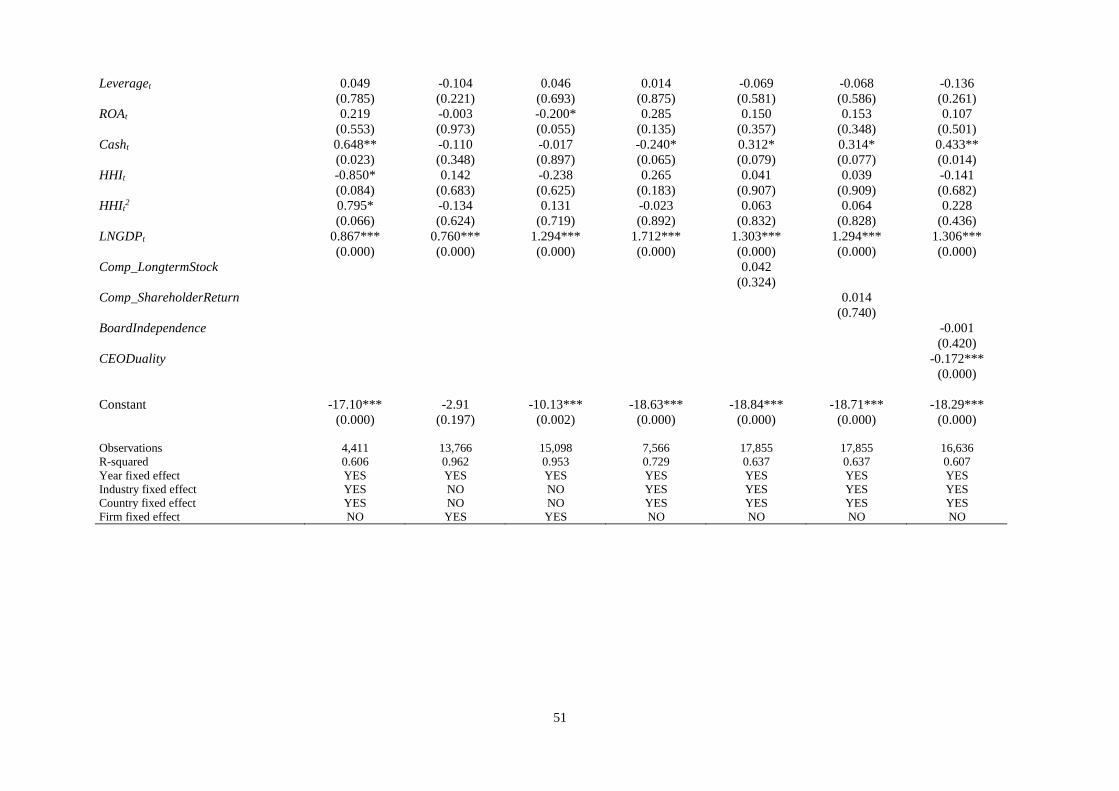

4.10.2. Other compensation incentives

Studies have suggested that the long-term equity-based components of executive compensation,

such as restricted stocks and stock options, can motivate innovation by alleviating managerial myopia

and directing managers’ attention toward longer-term value creation (e.g., Lerner & Wulf 2007;

Flammer & Bansal 2017; Nguyen 2018). Thus, we include Comp_LongtermStock in our model,

which is an indicator variable measuring whether a firm has recently distributed long-term equity

incentives to its executives. The results are reported in Column 5 of Table 5. In addition, studies have

shown that managerial compensation based on stock performance targets rather than accounting

earnings has a positive impact on innovation (e.g., Murphy & Gibbons 1992). Accordingly, we

include an additional variable for stock performance-oriented compensation

(Comp_ShareholderReturn), which is an indicator variable that equals 1 if an executive

compensation scheme is linked to total shareholder returns in that year, and 0 otherwise. We continue

to find that our inferences are unchanged.

26

4.10.3. Corporate governance attributes

Good corporate governance practices presumably mitigate agency conflicts, improve

transparency, and optimize the allocation of investment capital, which in turn may enhance the

adoption of CSR contracting and engagement in firm innovation (Fauver et al. 2017; Zhong 2018).

Therefore, following Chen et al. (2016a), we add two corporate governance factors to our model:

board independence (BoardIndependence) and CEO duality (CEODuality). 23 The results are

reported in Column 7 of Table 5. Our inferences are unchanged after the addition of the two corporate

governance variables.

[Table 5 here]

5. Additional Analysis

5.1. Country-level institutions and CSR contracting

Rodriguez et al. (2006) argue that the strategic implications of CSR are influenced by cross-

country differences in the institutions that regulate market activity, such as business, labor, and social

agencies. Thus, in this section, we investigate the possible role of country-level institutional

characteristics on the association between CSR contracting and innovation.

5.1.1. National stakeholder orientation

National stakeholder orientation refers to a society’s overall expectations for CSR performance,

which are shaped by the country’s institutional, legal, and cultural characteristics (Williams &

Aguilera 2008; Dhaliwal et al. 2012; Cheung et al. 2018). In general, countries that are more

stakeholder-oriented have relatively more stringent labor rights legislation and laws on CSR

disclosure, and higher public awareness of CSR issues. Thus, national stakeholder orientation may

either substitute or complement the relation between CSR contracting and innovation. For example,

23 A board with greater independence or without CEO duality is widely regarded as having good corporate governance.

BoardIndependence is calculated as the proportion of independent directors on the board in a given year. CEODuality is

an indicator variable that equals 1 if the CEO also serves as the chairperson of the board, and 0 otherwise.

27

given the lower level of CSR activities of firms in countries with lower stakeholder orientation, the

use of CSR contracting to improve firms’ CSR performance may have relatively little effect in

fostering managers’ future-oriented activities, including those related to innovation. In contrast, by

developing close connections with stakeholders who are able to provide resources and support for

innovative activities, CSR contracting may help fill the gaps in the institutional, legal, and social

environments in less stakeholder-oriented countries. This suggests that CSR contracting has a more

positive effect on innovation.

Using the median of STAKE for the countries included in our sample as a cut-off point, we split

the sample into two subsamples: firms in countries with strong stakeholder orientation (6,627

observations) and firms in countries with weak national stakeholder orientation (9,158

observations).24 The results for the two subsamples are presented in Table 6. The coefficients on

CSRContracting are significantly positive for countries with weak stakeholder orientation (β = 0.142,

p < 0.05 in Column 2 for the patent model; β = 0.112, p < 0.05 in Column 4 for the citation model),

and insignificant albeit positive for countries with high stakeholder orientation. These results support

our conjecture that the positive effect of CSR contracting on firm innovation is more pronounced in

less stakeholder-oriented countries.

[Table 6 here]

5.1.2. National law enforcement

Next, we examine the role of country-level law enforcement on the relation between CSR

contracting and firm innovation. Flammer and Kacperczyk (2016) demonstrate that the legal

enforcement of statutes that consider the needs of nonfinancial stakeholders has a positive effect on

firm innovation, as the enforcement can protect the interests of stakeholders, foster their longer-term

24 The data on national stakeholder orientation are obtained from Dhaliwal et al. (2012), who develop a measure of

country-level stakeholder orientation (STAKE) that incorporates four dimensions of national stakeholder engagement: (1)

the stringency of a country’s legal environment in protecting labor rights and benefits; (2) the degree of a country’s

mandatory requirements for CSR disclosure; (3) a country’s public awareness of CSR issues; and (4) the country-level

attitudes of corporate executives to CSR engagement.

28

horizons, and strengthen their tolerance for risks associated with firm innovation. However, in

countries with weak legal enforcement, stakeholders tend to be less protected against adverse events

by formal legal institutions, and in turn have a shorter-term orientation and less tolerance of

uncertainty. Hence, the stakeholders are less willing to accept or engage in risky innovation initiatives.

In this condition, the voluntary adoption of CSR contracting may act as a substitute for law

enforcement in terms of protecting stakeholders’ interests by increasing management’s commitment

to CSR and stakeholders. Thus, we expect CSR contracting to have a stronger effect on innovation

in countries with weaker enforcement of legal institutions. Alternatively, in countries with a strong

legal environment, CSR contracting may play an even more important role in fostering corporate

innovation activities because presumably corporate innovation outputs (e.g., property right) can be

better protected in countries with more stringent legal environment.

To test our conjecture, we partition the sample into two subsamples, namely firms in countries

with strong law enforcement and firms in countries with weak law enforcement, using the median of

Rule of law for the countries included in our sample.25 The results are reported in Table 7. The

coefficients on CSRContracting are significantly positive only for the subsample of countries with

weak law enforcement (β = 0.137, p < 0.01 in Column 2 for the patent model and β = 0.210, p <

0.001 in Column 4 for the citation model). These results are consistent with our prediction that the

association between CSR contracting and firm innovation is amplified in countries with weak law

enforcement.

[Table 7 here]

5.2. CSR contracting, CSR performance, and firm innovation

Given that CSR contracting and CSR performance are both likely to have a positive relation

with firm innovation, in an additional test, we further explore whether CSR contracting and CSR

25 Following La Porta et al. (1998), we use the country-level rule of law (Rule of law) as a proxy for the overall

enforcement ability of a country’s legal system. We obtain the Rule of law data from the World Bank. Specifically, this

variable measures the extent to which agents can trust that a country’s legislation will be enforced, especially in regard

to contracts, the protection of property rights, and the authority of the police and courts.

29

performance substitute or complement each other in terms of their effects on firm innovation. Thus,

we further examine the interactive role of CSR contracting and CSR performance in innovation by

interacting the CSR contracting and CSR performance variables. In terms of the CSR performance

measures, in addition to the overall CSR performance score (CSRPerf), which we introduced as a

control in the earlier tests, we include five new variables measuring employee-related CSR

performance,26 as research shows that positive employee treatment enhances firm innovation by

promoting a learning climate and facilitating the exchange and absorption of knowledge and ideas

(Lau & Ngo 2004; Sung & Choi 2014; Mao & Weathers 2019). The results after including the

interaction terms between CSRContracting and the CSR performance measures are presented in

Table 8. The coefficients on both CSRContracting and CSRPerf are significantly positive in all

columns, indicating that CSR contracting and good CSR performance are beneficial to firm

innovation. Furthermore, all of the interaction terms are negatively and significantly related to firm

innovation, which suggests that CSR contracting can substitute for CSR performance in terms of its

effect on firm innovation.

[Table 8 here]

5.3. Mandatory CSR reporting requirements

A possible alternative explanation of the observed positive effect of CSR contracting on

innovation is that firms tend to signal their innovation success through CSR contracting. To partially

address this concern, we take advantage of the country-level CSR reporting regulations as an

exogenous shock and examine their impact on the relation between CSR contracting and innovation

because studies suggest that mandatory CSR or CSR reporting requirements substantially increase

firms’ commitment to CSR (e.g., Manchiraju & Rajgopal 2017; Chen et al. 2018). According to

Ioannou and Serafeim (2017), during our sample period, CSR disclosure was mandated by law in

26 Specifically, the five measures of employee-related CSR performance include the overall CSR performance associated

with employees’ wellbeing (EMPperf) and its four dimensions: (1) employment quality (EMP_EQ); (2) workforce health

and safety (EMP_HS); (3) training and development (EMP_TD); and (4) diversity and opportunity (EMP_DO). See

Appendix B for more detailed variable definitions.

30

five countries, namely China, Denmark, India, Malaysia, and South Africa. Thus, we introduce

POST_CSRRMandate, which is an indicator variable that equals 1 for the year of the adoption of

mandatory CSR reporting and any year after, and 0 otherwise. We then add POST_CSRRMandate

and its interaction with CSRContracting to our innovation model using a staggered DID design that

includes firm fixed effects. 27 Our untabulated results show that the main effects of

POST_CSRRMandate and CSRContracting are significantly positive, while the interaction term

CSRContracting × POST_CSRRMandate is significantly negative. These results indicate that

mandatory CSR disclosure requirements increase firm innovation, and attenuate the positive relation

between CSR contracting and firm innovation, which is consistent with our results showing that CSR

contracting is substitutive for country-level CSR orientation and firm-level CSR performance in

enhancing firm innovation.

6. Conclusion

With the growing awareness of the relationship between the nonfinancial performance and

long-term financial performance of firms, shareholders and researchers have shown increasing

interest in the inclusion of CSR performance requirements in firms’ executive compensation policies.

Although the inclusion of equity compensation and stock performance targets in executive

compensation schemes has been shown to be effective in motivating firm innovation (e.g., Murphy

& Gibbons 1992; Lerner & Wulf 2007; Flammer & Bansal 2017), we have limited understanding of

whether the inclusion of nonfinancial CSR criteria in executive compensation policies plays a similar

role.

In this study, based on a comprehensive sample of firms from 30 countries, we find robust

evidence showing that the inclusion of CSR criteria in executive compensation policies has a positive

27 We exclude firms that are from CSR reporting mandated countries but have no pre-mandate firm-years from our sample

to ensure better comparison.

31

effect on firm innovation. We further explore whether and how country-level institutional

characteristics moderate the relation between CSR contracting and firm innovation. We find that

CSR contracting has a stronger effect on firm innovation in countries with weaker stakeholder

orientation or legal enforcement. This finding is consistent with the notion that CSR contracting plays

an important role in filling these institutional voids by incentivizing management to commit to future-

oriented investment, which in turn fosters better firm innovation. Finally, we present evidence

suggesting that while CSR contracting and CSR performance appear to be positively related to firm

innovation, they substitute each other in terms of their effects on firm innovation.

Our study contributes to the literature on the relation between executive compensation and firm

innovation by shedding light on the role of CSR-based compensation in incentivizing future-oriented

investments in areas such as innovation. The findings of our study also have a number of practical

implications. For example, our findings suggest that boards can improve the innovation outcomes of

their firms by introducing CSR-based executive compensation, especially for firms domiciled in

countries with weak stakeholder orientation or legal environments.

32

REFERENCES

Aghion, P., N. Bloom, R. Blundell, R. Griffith, and P. Howitt. 2005. Competition and innovation: An inverted-

U relationship. The Quarterly Journal of Economics 120 (2): 701–728.

Aghion, P., S. Bechtold, L. Cassar, and H. Herz. 2014. The casual effects of competition on innovation:

Experimental evidence. NBER Working Paper. https://www.nber.org/papers/w19987

Alvarez, R., and R. Robertson. 2004. Exposure to foreign markets and plant-level innovation: Evidence from

Chile and Mexico. The Journal of International Trade and Economic Development 13 (1): 57–87.

Audretsch, D. B. 1995. Firm profitability, growth, and innovation. Review of Industrial Organization 10 (5):

579–588.

Baranchuk, N., R. Kieschnick, and R. Moussawi. 2014. Motivating innovation in newly public firms. Journal