Corporate Presentation September - 2016 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Corporate Presentation September - 2016

1

2

3

4

Fullerton India Credit Company Ltd. [FICC] A step down subsidiary of Temasek Holdings

Fullerton Financial Holdings (FFH), the parent, was incorporated in January 2003 as a wholly owned subsidiary by Temasek Holdings (Private) Ltd

FFH has 9 operating financial services entities located across 8 countries serving 7 million customers

FFH’s vision is to develop unique business models that bring financial services closer to the underserved in emerging economies

DUBAI, UAE 19 Branches 234k Customers

PAKISTAN 171 Branches 488k Customers

INDIA 514 Branches 1,526k Customers

4 Provinces, Central CHINA 32 Branches 8.6k Customers

CHINA 77Branches 879k Customers

MYANMANR 12 Branches 44k Customers

CAMBODIA POST BANK 37 Branches 60k Customers

MALAYSIA 94 Branches

INDONESIA 1,901Branches

4

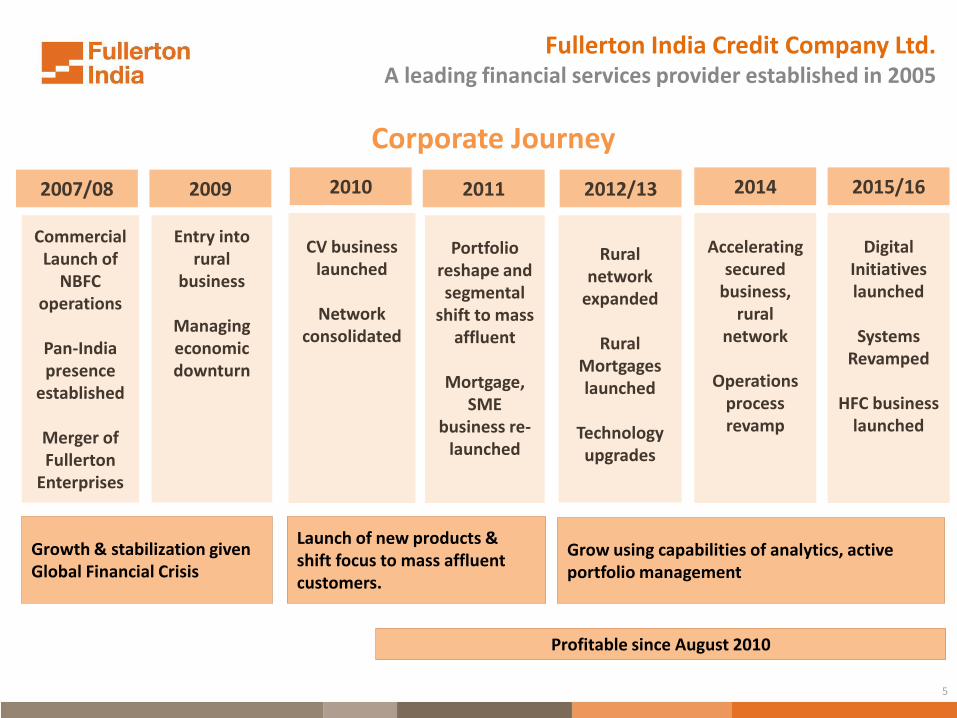

2007/08 2009 2010 2011

Commercial Launch of

NBFC operations

Pan-India presence

established

Merger of Fullerton

Enterprises

CV business launched

Network

consolidated

Portfolio reshape and segmental

shift to mass affluent

Mortgage,

SME business re-

launched

2012/13

Rural

network expanded

Rural

Mortgages launched

Technology upgrades

2014

Accelerating secured

business, rural

network

Operations process revamp

Corporate Journey

Launch of new products & shift focus to mass affluent customers.

Grow using capabilities of analytics, active portfolio management

Profitable since August 2010

Growth & stabilization given Global Financial Crisis

Fullerton India Credit Company Ltd. A leading financial services provider established in 2005

Entry into rural

business

Managing economic downturn

2015/16

Digital Initiatives launched

Systems

Revamped

HFC business launched

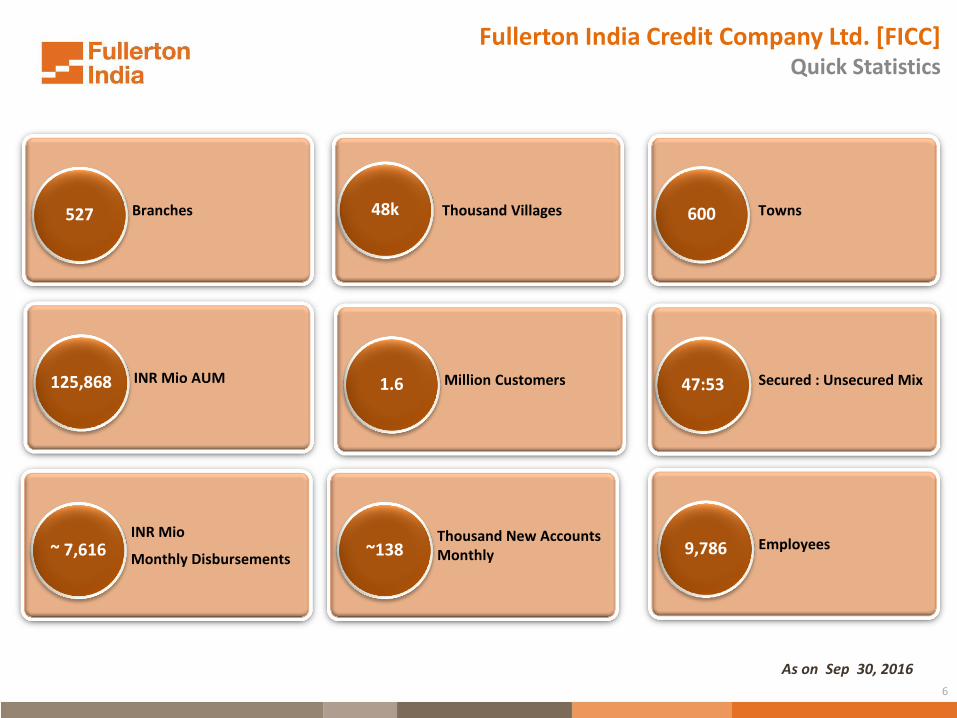

5

As on Sep 30, 2016

Branches 527 Thousand Villages Towns

INR Mio

Monthly Disbursements ~ 7,616

Thousand New Accounts Monthly ~138 Employees 9,786

INR Mio AUM 125,868 Million Customers 1.6 Secured : Unsecured Mix 47:53

48k

Fullerton India Credit Company Ltd. [FICC] Quick Statistics

6

600

Customers (In ‘000)

40

3

Branch Coverage by city population size

…with strong presence in under banked geographies

45% of branches in cities with <100K population

Deep experience in areas under the Regulator’s focus for furthering financial inclusion

42 94 107 401 1,003

4

13

2

1

Urban – 226 Branches

Rural – 301 Branches

22 States and 3 Union Territories 600Towns

48kVillages

Strong pan-India distribution network Over 527 Branches covering 22 States and 3 UT…

7

4

18 8

2

24

2 3

1 9

3 23

36

7

65

50

56

55

66

3

73

16

54 48

172

237

>5mio 1mio - 5mio 500k - 1mio 100k - 500k <100k

62

87

106 115

120 126

Mar 14 Mar 15 Dec 15 Mar 16 Jun 16 Sep 16

Retail Commercial Rural

Broad product range Customized to segment needs and aspirations

Personal Loans Commercial

Vehicle Finance Personal /

Group Loans

Business Loans Rural

Mortgages Mortgages

LAP Vehicle Loans

Pro

du

ct

Low 12- 24 M

Medium 24- 60 M

High > 60 M

Tenor

Co

mm

erc

ial

Ru

ral

Re

tail

SME

Aspiring Affluent

Mass Affluent Mortgages

Portfolio Composition

Cross sell – Life/ General Insurance

Commercial Rural Retail

Two- Wheeler, Personal /

Solidarity Loan Personal Loans

LAP, Commercial

Vehicles

Mortgages, CV Finance

Commercial Rural Retail

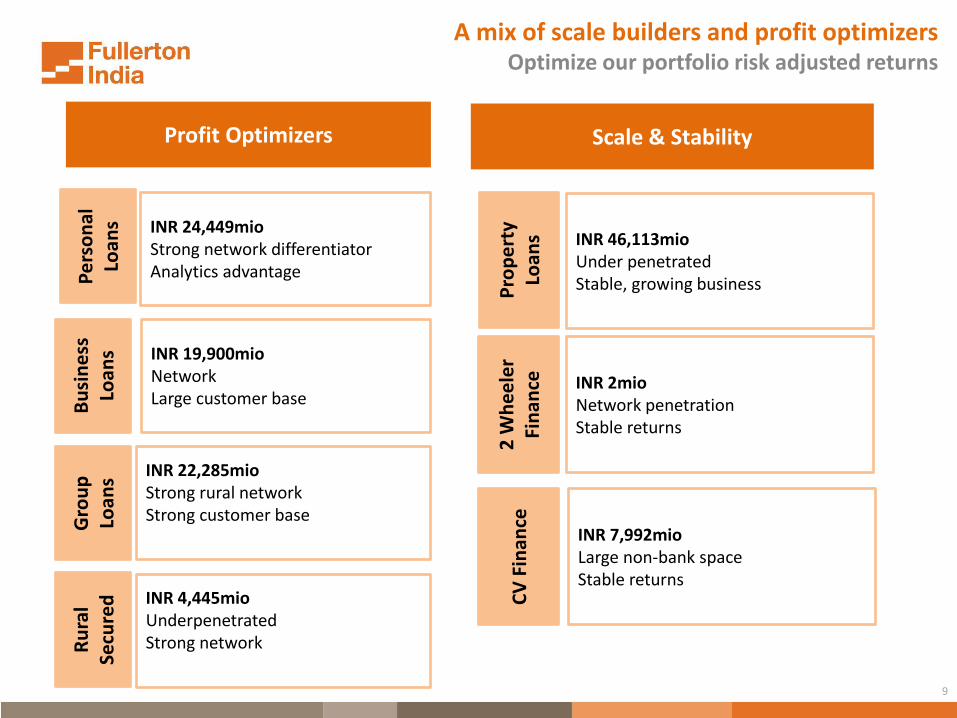

8

53%

23%

24%

77%

12% 11%

Profit Optimizers Scale & Stability

INR 24,449mio Strong network differentiator Analytics advantage P

ers

on

al

Loan

s

INR 22,285mio Strong rural network Strong customer base

Gro

up

Lo

ans

INR 46,113mio Under penetrated Stable, growing business P

rop

ert

y Lo

ans

INR 2mio Network penetration Stable returns

2 W

he

ele

r Fi

nan

ce

INR 4,445mio Underpenetrated Strong network

Ru

ral

Secu

red

INR 7,992mio Large non-bank space Stable returns

CV

Fin

ance

INR 19,900mio Network Large customer base B

usi

ne

ss

Loan

s

A mix of scale builders and profit optimizers Optimize our portfolio risk adjusted returns

9

Board of Directors

Operating Committees

ALCO Operational Risk Forum Borrowing Committee Customer Service Forum

Balance Sheet management

Agrees on funds deployment

Controls liquidity interest rate risks

Establishes operational risk appetite Establishes framework for managing operational risk Monitors underlying risks and remediation actions

Approves borrowing arrangements Approves terms and conditions for borrowings Approves pre-payments

Monitors customer experience, improving service Enables system improvements, performance measures

Risk Oversight Committee Audit Committee Nomination & Remuneration Committee

CSR Committee

Oversees credit, market and operational risk Approves risk appetite and credit policies Monitors portfolio performance and approves mitigation actions

Oversees Internal controls framework Reviews the financial statements and financial reporting process Reviews scope, findings, reports, etc. of Internal and external audit

Oversees overall Human Capital mission and strategy. Oversees key appointments and compensation matters Reviews structure and composition of the Board and recommends for changes

Recommends CSR policy, budgets, projects, etc. Monitors implementation of the CSR activities

A Robust governance framework.. ..incorporates international good practice, reinforced with oversight

10

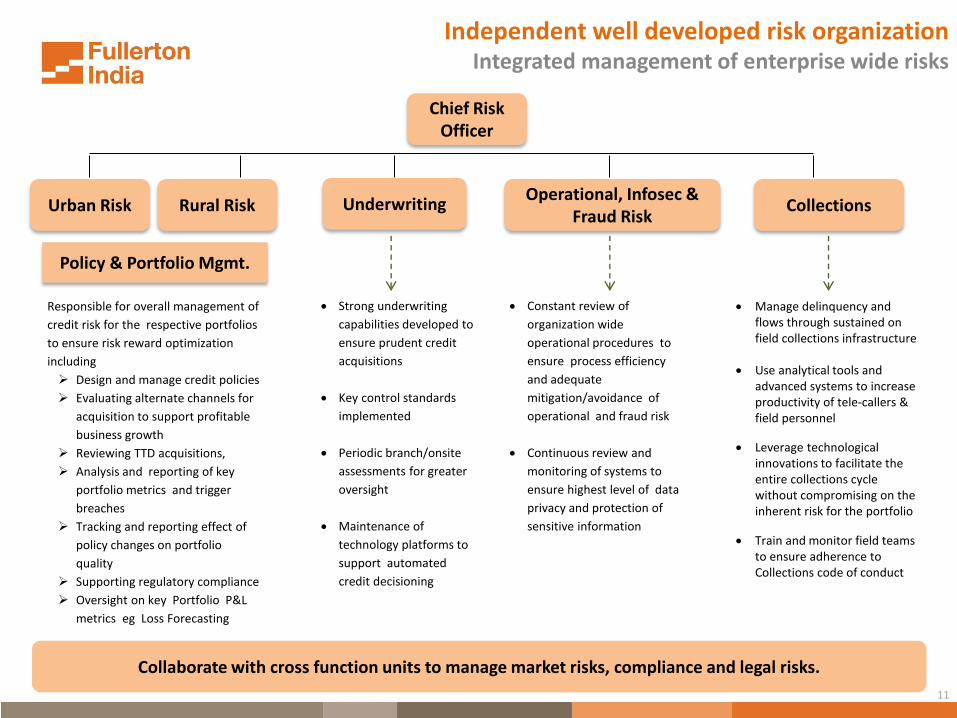

Independent well developed risk organization Integrated management of enterprise wide risks

11

11

Policy & Portfolio Mgmt.

Strong underwriting

capabilities developed to

ensure prudent credit

acquisitions

Key control standards

implemented

Periodic branch/onsite

assessments for greater

oversight

Maintenance of

technology platforms to

support automated

credit decisioning

Constant review of

organization wide

operational procedures to

ensure process efficiency

and adequate

mitigation/avoidance of

operational and fraud risk

Continuous review and

monitoring of systems to

ensure highest level of data

privacy and protection of

sensitive information

Manage delinquency and flows through sustained on field collections infrastructure

Use analytical tools and advanced systems to increase productivity of tele-callers & field personnel

Leverage technological innovations to facilitate the entire collections cycle without compromising on the inherent risk for the portfolio

Train and monitor field teams to ensure adherence to Collections code of conduct

Responsible for overall management of

credit risk for the respective portfolios

to ensure risk reward optimization

including

Design and manage credit policies

Evaluating alternate channels for

acquisition to support profitable

business growth

Reviewing TTD acquisitions,

Analysis and reporting of key

portfolio metrics and trigger

breaches

Tracking and reporting effect of

policy changes on portfolio

quality

Supporting regulatory compliance

Oversight on key Portfolio P&L

metrics eg Loss Forecasting

Chief Risk Officer

Operational, Infosec & Fraud Risk

Collections Rural Risk Urban Risk Underwriting

Collaborate with cross function units to manage market risks, compliance and legal risks.

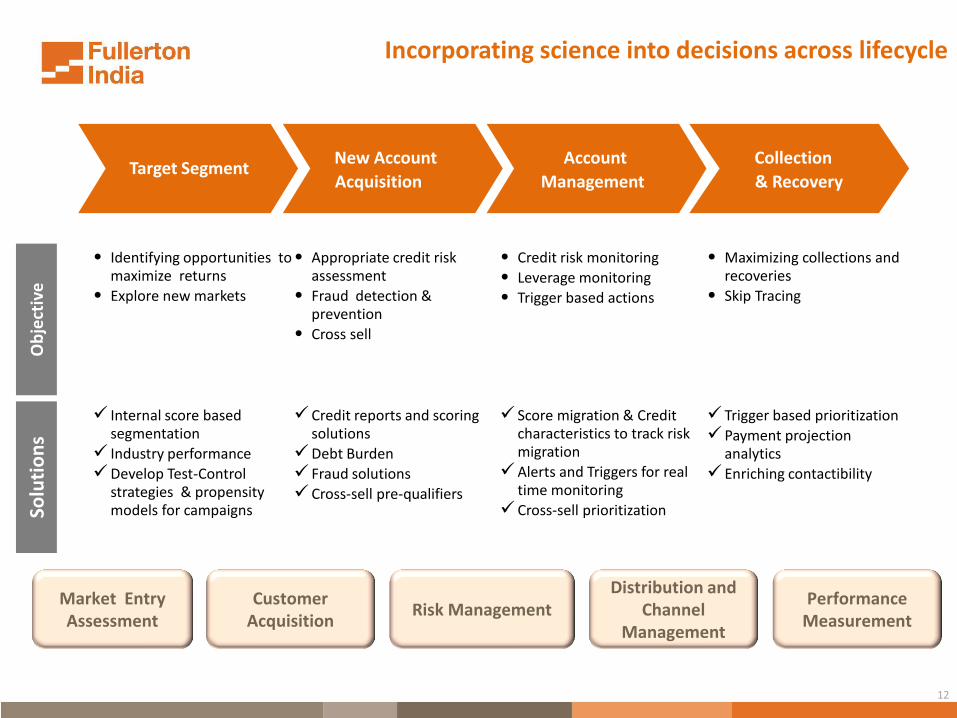

• Identifying opportunities to maximize returns

• Explore new markets

• Appropriate credit risk assessment

• Fraud detection & prevention

• Cross sell

• Credit risk monitoring

• Leverage monitoring

• Trigger based actions

• Maximizing collections and recoveries

• Skip Tracing

Target Segment New Account

Acquisition

Account

Management

Collection

& Recovery

Ob

ject

ive

So

luti

on

s

Internal score based segmentation

Industry performance

Develop Test-Control strategies & propensity models for campaigns

Credit reports and scoring solutions

Debt Burden

Fraud solutions

Cross-sell pre-qualifiers

Score migration & Credit characteristics to track risk migration

Alerts and Triggers for real time monitoring

Cross-sell prioritization

Trigger based prioritization

Payment projection analytics

Enriching contactibility

Incorporating science into decisions across lifecycle

Customer Acquisition

Market Entry Assessment

Performance Measurement

Distribution and Channel

Management Risk Management

12

Strong rural franchise Establishing leadership through delivery platform and product range

Catchment model enables customer intimacy and superior service quality

Comprehensive product suite serves customer growth and aspiration

Group Loans

General Enterprise Loans

Two wheeler loans

CV Loans

Loans against property

Mortgages

Insurance

Livelihood Micro-

enterprise, consumption

Consumption, Small business

Aspirational Needs

13

Strugglers < INR 200K

Next Billion INR 200K – 450K

Aspirers INR 450K – 1,100K

Affluent > INR 1,100K

Urban

Rural

Annual Household Income

FICC Niche

Source : Euro Monitor and BCG

Households

Foreign and Private Banks

Niche target segment covering 75 mio households Underserved segment not covered by large banks

Segment Profile FICC Offering

Urban Aspirers Educated with mid-sized businesses or stable jobs with high lifestyle aspirations

Personal Loans, Loan against Property, Business Loans, SME loans

Next Billion Basic education levels, small businesses or low paying jobs. Basic lifestyle

Personal Loans, Two wheeler Loans, Business Loans

FICC niche segment below the Foreign and Private banks

Caters to 75 mio HH’s – 50% is underserved

Microfinance 121 Mio ( 50%)

72 Mio (30%)

34 Mio (14%)

13 Mio (6%)

14

7

34 37

33

4

36

49

40

6

35

42 38

CPs Bank Loans Debentures Total

Mar 15 Mar 16 Sep 16

Well funded book… Providing strong liquidity from well diversified funding sources

15

Institutional Lenders Nos

Residual Maturity Months

Fund Profile INR mio

AA+ AA+ AAA

20

14

2

01

5

20

16

AA+ AA+ AAA

19

38

717

35

18

42

2

24

121

Mutual Funds Banks FIIs Insurance Pension Funds

Sep-15 Sep-16

54,153 54,156 52,957

35,899 41,839 47,089

11,250 5,500 7,450 5,070 5,603

4,735 107,122 107,604 113,396

Mar 16 Jun 16 Sep 16Bank Loans Bonds

Working Capital Commercial Papers

Direct Assignment /Securitisation

AA+ AA+ AAA

Well capitalized Ahead of current and proposed regulatory norms

• INR 5,000mio raised through Masala bond (Oct 2016) • Capital adequacy at 21.1% (Sep 2016) • Tier 1 Capital Adequacy at 15.8% (Sep 2016)

16

Capital Adequacy Percent

Shareholder’s Fund INR mio

17,521

20,122 21,149

21,889 22,793

Sep 15 Dec 15 Mar 16 Jun 16 Sep 16

15.7 15.5 16.1 16.2 15.8

19.5 20.2 21.9 21.9

21.1

Sep 15 Dec 15 Mar 16 Jun 16 Sep 16

Regulatory Minimum (15%)

Total

Tier 1

Regulatory Minimum (15%)

Total

Tier 1

Cumulative NPA Provisions (Percentage)

90DPD 120DPD 150DPD 270DPD 360DPD 540DPD 720DPD

Personal Loans 25 100

Mortgages/Loans against Property

15 25 50 70 100

Group Loans 25 100

Commercial Vehicle Loans 15 30 60 100

2Wheelers 25 100

• FICCL reports NPA at 90DPD as against RBI requirement of 150 DPD

• Standard Assets provision maintained at 40bps for Urban business and 1% for Rural business, against statutory requirement of 30bps.

17

Conservative provisioning policy Industry leading

Secured

Sub standard: NPA Up to 18 Months

10%

Doubtful, 1: NPA 18 – 30 Months

20%

Doubtful, 2: NPA 30 – 54 Months

30%

Doubtful, 3: NPA Greater than 54 Months

50% R

BI

No

rms

Unsecured

NPA Up to 18 Months 10%

NPA Up to 18 Months 100%

Mobility

Customer Service

Analytics

Fully Integrated Front to Back

Customer Acquisition , Servicing and Collections using Tablets

Collections using Android tablets and Bluetooth Printers

Use of advanced analytical tools for customer behaviour modelling

Use of alternate data analytics using social media for faster underwriting and decisioning

Self Service Portal for enquires and service requests

Contact Center with Interactive Voice Response (IVR)

Online Origination through internet platform

Online interface with Bureau, Service Providers and Aggregators

Backend automation from Origination to Disbursement and Collections

Technology enabled Customer Service & Operations

18

Infosec

Independent professional team managing Infosec

Penetration testing, 3 tier Firewalls, VPN for access and protection

Fully redundant disaster recovery site with Platinum support

Mobile Device containerisation

Depth of management experience Bankers with deep domain experience and multinational orientation

Business & Franchise Development

Integrated Risk Management

Capital and Financial

Management

Infrastructure & Resources

Management

• Extensive local experience in Product development and Distribution in large branch networks in Rural & Urban India.

• Subject matter expertise in Retail Lending and Housing Finance

• MNC Banking and International Markets exposure

• Strong appreciation of Risk Management

• In depth experience in Risk Management in Consumer businesses in MNC Banks and in large Indian NBFC including Housing Finance

• Specialised teams focused on Risk Policy, Underwriting, Operational Risk , Collections, and Legal management

• Develops Risk and Business Analytics scorecards and integrates with Digital opportunities with business strategy

• Strong experience in Global Markets in leading MNC Banks

• Rapidly growing relationships with large Indian & MNC Banks and FIs

• Strong Financial Control experience in MNCs

• Specialised teams dedicated for FP&A, Accounting, Taxation and Company Secretarial

• Strong orientation in compliance and controls

• Strong international experience HR management in large MNC retail Financial experience

• Strong Operations capability with six sigma Process Reengineering expertise

• Advanced technology deployment and change management skills

Combined senior team experience

200+ years

200+ years

150+ years

150+ years

19

Our Strategic Themes

1

Build balanced & resilient book

Continued focus on stable secured, differentiated products, expanded suite

2

Leverage footprint strength

3

Focus on scale and efficiency

Disciplined cost management, consistent productivity gains, focus on scale

4

Deliver through cycle returns

5

Stable, diversified funding

Continue to extend funding base, expand retail, QFIs, DFIs and Insurance

Leverage deep market knowledge, depth of presence and large customer base

Risk appetite, predictive models measure stress performance, rather than current

20

INR mio Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17 QoQ% YoY%

Net Revenue 3,253 3,415 3,652 3,800 4,151 9.3 27.6

Expenses 1,731 1,710 1,878 1,927 1,952 1.3 12.8

Working Profit 1,522 1,705 1,774 1,873 2,199 17.4 44.5

Net Credit Losses* 426 577 643 708 829 17.1 94.5

Pre Tax Profit 1,096 1,128 1,131 1,165 1,370 17.6 25.0

Disbursals 21,711 21,377 26,403 21,253 24,445 15.0 12.6

Customer Assets (AUM) 98,914 105,857 115,082 119,804 125,868 5.1 27.2

Secured Assets (%) 47.7 48.6 48.6 47.9 46.5 (1.3) (1.1)

Shareholder Funds 17,521 20,122 21,149 21,889 22,793 4.1 30.1

Capital Adequacy (%) 19.5 20.2 21.9 21.9 21.1 (0.8) 1.6

Branches (#) 445 445 488 514 527 13.0 82.0

* Net Credit Loss includes Provision for Standard Assets.

Financial Performance Significant performance improvement

21

Net NPA

Improved cost to income (%) RoA (%) RoE (%)

*Loss Coverage = Operating Profit/Credit Losses

Key performance indicators Improved efficiencies and returns; strong credit performance

22

Loss coverage* Credit losses (%)

4.7% 4.5% 4.4% 4.2%4.7%

Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17

25.9%

23.9%

22.0%21.6%

24.2%

Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17

53.2%

50.1%

51.4%50.7%

47.0%

Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17

1.9%

2.3% 2.4% 2.5%2.7%

Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17

3.6 3.4

4.0

3.1

2.4

Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17

1.5% 1.5%

1.3%

1.7% 1.7%

Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17

Jeevika-Vocational Training

No of Programs 340

Impact 7024 Households

Krishi Mitra-Organic Farming

No of Programs 80

Impact 600 Farmers

Health Care Services

Impact 31,106 Patients

No of Programs 356

23

Save The Eye

No of VCC 11

22,221 Patients Impact

Pashu Vikas-Cattle Care Camp

No of Programs 20

Impact 7516 Households

CSR Projects & Impact in H1 FY17

Employee led CSR program for livelihood advancement and women empowerment

Income enhancing vocational training programs for urban and rural women, in fashion designing and beauty & hair care

Cattle care camps for enhancing existing livelihoods Integrated Livestock Development centres (ILD) for holistic cattle

care development program targeted at cattle breed improvement, 20 ILD centres are operational in 3 states i.e. Madhya Pradesh, Maharashtra & Karnataka

Eye check up camps for primary screening and cataract surgeries at the near by partner hospital

10-Vision Care Center (VCC) for primary screening and 1-mobile vision care van

Promotion of organic and homestead farming enhancing adoption of environment friendly practices

Primary health care services through mobile medical clinics and 24X7 call center for medical emergencies, operational in 3 locations Hubli, Jaipur, and Hoshangabad .1 Mobile Health Care Van providing primary health care services in Gujarat. Nutritional Mid-Day meals in 18 Gov schools in Uttar Pradesh, Rajasthan and Karnataka.

Jyoti – Eye Screening Camp

Krishi Mitra- Organic Farming program

Gurukul- Skill Development for Youth

Niramaya- Health Check-up Camp

Eye care through Mobile Vision Care Van in Godhra

CSR Moments in H1 FY17

Jeevika- Vocational Training Camp

24

Shantanu Mitra CEO and MD since August 2011

Joined FFH in 2010 as Head of Consumer Risk Management for consumer markets across all operational entities in various countries including India. Before the current role, he was the Deputy CEO of the Company. Over three decades of experience in financial services, with about 20 years at Standard Chartered and Citibank where he had stints in Singapore, Thailand and India. A Chartered Accountant with the Institute of Chartered Accountants, England and Wales.

Gan Chee Yen Chairman of the Company since November 2011. CEO and Board member of Fullerton Financial Holdings Pte Ltd, Singapore (FFH), and Board Commissioner of Bank Danamon. Previously Co-Chief Investment Officer and Senior Managing Director, Special Projects at Temasek International. With Temasek since 2003, first as CFO and subsequently in various senior management roles. Has served on several boards including Neptune Orient Line. Is a member of the Institute of Certified Public Accountants of Singapore.

Rajeev Kakar

Non - Executive Director Head of Consumer Banking at FFH. Executive Director and founder CEO of Dunia Finance LLC, a Dubai-based JV partnered by Fullerton Financial Holdings. Has over 20 years of experience in financial services. Served Citibank in a variety of Consumer Banking roles internationally. Is a Bachelor of Technology & Mechanical Engineering from the Indian Institute of Technology Delhi, and MBA from Indian Institute of Management, Ahmedabad.

Board of Directors

25

Kenneth Ho Tat Meng

Renu Challu Independent Director Ms. Renu Challu is a seasoned banker with decades of experience in Commercial and Investment Banking. She was with the State Bank of India (SBI) for more than 38 years serving in variety of positions. Some of the positions held at SBI include President & COO at SBI Capital Markets, MD & CEO at SBI DFHI, MD of State Bank of Hyderabad and Deputy MD, Corporate Strategy and New Business Development. She is on the Board of many other companies and is a partner in 5th Bridge Data Technologies LLP.

Independent Director

Ms. Pillai, a 1972 batch IAS officer held a number of senior positions in the Government of India and the State Government of Kerala for 40 years. She handled the Industry and Finance portfolios for nearly twenty years. In the Centre, she worked in the Ministries of Industry, Corporate Affairs, Labour and Employment .She contributed notably to reforms in Industrial and Foreign Direct Investment policies as also in formulating the National Skill Development Policy. In Kerala, as Principal Secretary Finance she worked to achieve enhanced developed outcomes, coupled with efficient fiscal management. Earlier as CMD, Kerala Finance Corporation she dealt with project financing to SMEs. Her last assignment was as Member Secretary (in the rank of Minister of State), Planning Commission, Government of India. She is currently Director on the Boards of Jubilant Life Sciences and International Travel House Ltd.

Sudha Pillai

Non - Executive Director Mr. Kenneth Ho carries more than two decades of Consumer and Commercial Banking experience. He is a graduate in Economics from Flinders University of South Australia and a Master of Business Administration holder from University Putra Malaysia. Currently, he is the Senor Vice President, Consumer Banking for Fullerton Financial Holdings (International) Pte Ltd. Previously he was in Citibank for 10 years covering the roles of Regional Director, Consumer Secured Lending of Citibank Asia Pacific regional office and in Citibank Singapore Ptd Ltd as Head of Autobusiness and Citibusiness (Commercial Banking). Prior to joining Citibank, he also had substantial exposure in EON Bank Berhad, Malaysia, including managing the entire Auto Loans business (national) and covering numerous roles in Branch Banking as well.

Board of Directors

26

Milan Robert Shuster Independent Director Dr. Shuster, is a professional with decades of experience in the banking sector. He is currently Chairman of the Audit Committee at Bank Danamon Indonesia. He served at Asian Development Bank, ING Bank, National Bank of Canada, Nippon Credit Bank in various capacities. After working as the President and CEO of P. T. Bank PDFCI, he served Bank Danamon Indonesia in various capacities. He became its president and CEO and later its Independent Commissioner. He has also served many other entities in Directorial and advisory capacities. He holds Ph.D. in International Economics and Law from University of Oxford. He also holds Master of Law from London School of Economics and Bachelor of Business Administration from Ivey Business School.

Premod Thomas

Independent Director

Mr. Thomas is currently the Chief Executive Officer and Executive Director of Capital Insights Pte Ltd, a management and strategy consulting company focused on the financial technology and healthcare sectors. He is also the Head of Corporate Strategy of Clifford Capital Pte Ltd, a company providing financing solutions in the infrastructure and offshore marine sectors and an Independent Director and Member of the Audit and Risk Committee of Mapletree Commercial Trust Management Ltd, Singapore. Before establishing Capital Insights Pte Ltd, he was the Chief Financial Officer and Executive Director of Singapore-listed GuocoLeisure Ltd. This was preceded by a career in Finance and Banking with Temasek Holding Ltd, Standard Chartered Bank and Bank of America. In addition, Mr. Thomas is a member of the Singapore Institute of Directors. Mr. Thomas holds an MBA from the Indian Institute of Management, Ahmedabad (PGDM) and a Bachelor of Commerce degree from Loyola College, Madras.

Board of Directors

27

Anand Natarajan Head - Strategy and Business Execution Anand is the Head of Strategy and Business Execution for Fullerton India. In this role, he is responsible for the overall corporate strategy of the company and its subsidiaries covering Risk, Operations, Technology, Analytics and Digital Initiatives. Anand is a Chartered Accountant and Cost Accountant, with an MBA from the Henley Business School. He joined Fullerton India in Jan 2016 from ANZ Bank, Indonesia, where he served as Chief Operating Officer, responsible for retail, institutional, branch and credit operations, technology and infrastructure, contact centre and service, procurement and property management and enterprise-wide operational risk management. Previously, Anand was the Chief Operating Officer for Fullerton India with responsibilities of Treasury, Finance and Operations. Anand has held various leadership positions in his 23 years with Standard Chartered Bank, where he served as Head of Global Markets Operations India, Head Securities Services South Asia, Chief Operating Officer Consumer Banking, Head Country /BPO Operations and Regional Credit Officer Middle East, Pakistan and Africa and as the Chief Risk Officer for Consumer Banking, India and South Asia.

Leadership Team

Rakesh Makkar Head - Business & Marketing

Rakesh spearheads Fullerton India's Urban and Rural business, in addition to heading the Marketing & CSR functions. He has over two decades of valuable experience including new business and brand launches while developing dynamic sales teams, product and distribution networks. Prior to joining Fullerton India, Rakesh was the Chief Distribution Officer and Management Committee member at DHFL. His earlier stints include Future Money as Chief Executive Officer, Citigroup and as a consultant for a Vietnamese Bank on consumer finance. Rakesh is a qualified national rank holder Chartered Accountant and an MBA.

28

Leadership Team

Swaminathan Subramanian Head - Human Resource

Swaminathan is an engineer from Jadavpur University, Kolkata and an MBA from XLRI. He joined Fullerton India in May 2013 to lead the Human Capital and Training function. Swami has over 18 years of HR experience across Asia, Africa & Middle East markets. He has held various leadership positions including Head of HR for Retail Banking, Barclays- Africa and Head of Compensation & Benefits, Standard Chartered Bank, South Asia and more recently as HR lead for Corporate & Investment Banking Operations & Technology with JP Morgan Chase, India.

29

Ajay Pareek Head - Sales & Product, Urban Business

Ajay is a Chartered Accountant with over 18 years' experience in audit & financial services. Starting his career with A. F. Fergusons & Co, he moved to CitiFinancial as part of the start-up team to launch their retail finance business in India. At Citi Financial he handled the risk and operations functions for 3 years and later took over as a Regional Business Head. After 8 years at Citi Financial, he joined Fullerton India in 2005 as part of the start-up team. Ajay is now Head - Sales and Distribution for the Retail Business and oversees distribution of the company's key products of Personal Loans, two-wheeler & used car loans and mortgages.

Ravindra comes with over 18 years of work experience in Risk Management and Business function. He has been with Fullerton India since September 2011 and during his stint, headed Credit Policy & Underwriting for Commercial & Rural Business, Collections, Fraud Risk, Operational Risk, Legal and Compliance. He also led the Mortgage and SME business vertical before being appointed as Chief Operating Officer for Fullerton India. Ravindra is now Chief Executive Officer for Fullerton India Home Finance Company Limited. Prior to joining Fullerton India, Ravindra was heading Collections & Fraud Control for South Asia in Standard Chartered Bank and was also the Collections Head for HDFC Bank Ltd. He has held regional positions at ABN Amro Bank and Bank of America at the beginning of his career.

Ravindra Rao Chief Executive Officer - Grihashakti (Fullerton India Home Finance Company Limited)

Leadership Team

Deepak is an Electrical Engineer with a Masters in Management from Jamnalal Bajaj Institute, Mumbai. In his work experience of 20 years he has handled diverse roles including Quality Assurance, Sales and Distribution, Debt Collections, Operational Risk and Audit. After successful stints at Cable Corporation, HCL Infosystems and Citibank he joined Fullerton India in 2007 as Head – Retail Collections. Deepak manages Internal Audit at Fullerton India.

Deepak Patkar Head - Internal Audit

30

Pankaj has an overall experience of 18+ years in various capacities across finance and allied functions. He is the Chief Financial Officer, Company Secretary and Chief Compliance Officer for Fullerton India Credit Company Limited. In addition, he holds the position of Chief Financial Officer of Fullerton India Home Finance Company Limited. At Fullerton, he is responsible for corporate planning, accounting, finance, taxation, compliance and corporate governance functions. Prior to joining Fullerton in Sep 2007, Pankaj was associated with COLT Telecom (“COLT”), an affiliate of Fidelity international, as the Financial Controller-cum-Company Secretary. He has also been associated with GE Commercial Financial and Motherson Sumi Systems Limited in various capacities. Pankaj is a Chartered Accountant, Company Secretary and Cost Accountant from India and Certified Public Accountant from the State of Colorado, the USA.

Pankaj Malik Chief Financial Officer

Arvind Sampath Head - Treasury

Bikramjit Ganguly Head - Analytics & Information Management

31

Arvind is Head of Treasury at Fullerton India Credit Company Ltd. He is responsible for all liabilities strategy, surplus management and investor relationships. He has scaled up the Treasury over the last 3.5 years, de-risked liabilities, enhanced relationships and upsized financing. Across size and complexity, the Treasury has concluded several projects initiatives and raised the profile with the market. Arvind began his career with ICICI Securities, where he was instrumental in setting up the ‘interest rate derivatives’ desk. He then moved to Standard Chartered Bank in the bond trading desk before moving to a pan dealing-room Chief Operating Officer role. Arvind has over two decades of experience in financial markets, across a Primary Dealer, a Foreign Bank and a Non-Banking Financial Company; He is also a frequent media speaker and presenter of views on financial markets.

Bikramjit has an overall experience of 13+ years in various capacities across analytics and allied functions. He is currently the Head of Digital Initiatives and Analytics & Information Management for Fullerton India Credit Company Limited. At Fullerton, he is responsible for leading the company’s digital strategy and execution as well as the risk and business analytics functions. Prior to joining Fullerton in Mar 2012, Bikramjit was associated with Standard Chartered Bank, heading the regional credit risk analytics unit of South Asia. He has also been associated with Fair Isaac (“FICO”) in various capacities and has extensive experience of driving analytics driven strategies for major financial organizations across Asia, Middle East, Latin America, Europe and Africa. Bikramjit is a Masters in Statistics from the Indian Statistical Institute.

Leadership Team

Contact Fullerton India Credit Company Ltd. Floor 6, B Wing, Supreme IT Park, Powai, Mumbai 400 076 INDIA Phone: +91 22 6749 1234

www.fullertonindia.com 32

Your Preferred

Financial Partner

33

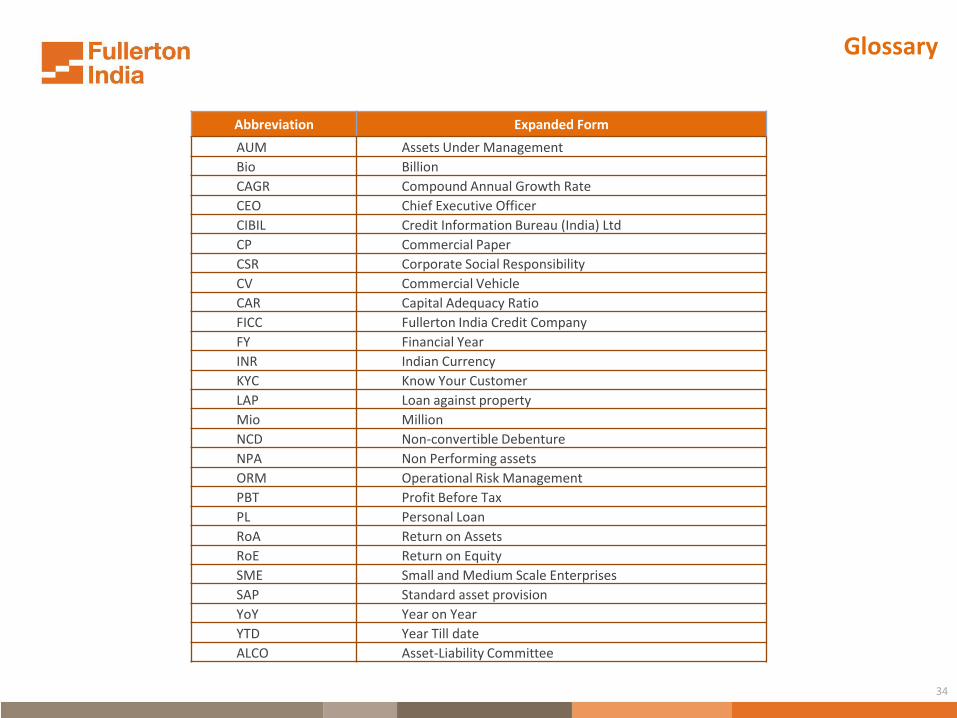

Abbreviation Expanded Form

AUM Assets Under Management

Bio Billion

CAGR Compound Annual Growth Rate

CEO Chief Executive Officer

CIBIL Credit Information Bureau (India) Ltd

CP Commercial Paper

CSR Corporate Social Responsibility

CV Commercial Vehicle

CAR Capital Adequacy Ratio

FICC Fullerton India Credit Company

FY Financial Year

INR Indian Currency

KYC Know Your Customer

LAP Loan against property

Mio Million

NCD Non-convertible Debenture

NPA Non Performing assets

ORM Operational Risk Management

PBT Profit Before Tax

PL Personal Loan

RoA Return on Assets

RoE Return on Equity

SME Small and Medium Scale Enterprises

SAP Standard asset provision

YoY Year on Year

YTD Year Till date

ALCO Asset-Liability Committee

34

Glossary

Related Documents

![Hopeman Primary School Hopeman - Home Page350307]Termly… · Web viewP.E (after break) P.E (after registration) Library. Homework collected. Mrs Fullerton. Mrs Fullerton. Mrs Fullerton.](https://static.cupdf.com/doc/110x72/5f8af41e97bc433e5b7476e5/hopeman-primary-school-hopeman-home-350307termly-web-view-pe-after-break.jpg)