TERM PAPER A Corporate Governance Assessment and Evaluation on Traphaco Joint Stock Company LE HUNG ANH 1100002 COMPARATIVE CORPARATE GOVERNACE PROFESSOR CHARLES MADDOX NOVEMBER 30, 2014 TAN TAO UNIVERSITY

Corporate governance report

Jul 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TERM PAPER A Corporate Governance Assessment and Evaluation on Traphaco Joint Stock

Company

LE HUNG ANH

1100002

COMPARATIVE CORPARATE GOVERNACE

PROFESSOR CHARLES MADDOX

NOVEMBER 30, 2014

TAN TAO UNIVERSITY

2

Contents A. Executive Summary ...................................................................................... 4

B. Research Methodology ................................................................................. 5

I. Benchmarks .............................................................................................. 5

II. Structure and Assessment of Areas .......................................................... 5

III. Company Review ................................................................................... 11

IV. Data ......................................................................................................... 12

V. Weight of areas and categories ............................................................... 12

VI. Evaluation method .................................................................................. 12

VII. Scoring and Weighting score .............................................................. 13

VIII. Final company scores .......................................................................... 13

IX. Caveats ................................................................................................... 14

C. Specific Finding .......................................................................................... 15

D. Discussion and Conclusion ......................................................................... 38

I. Overall Performance ............................................................................... 38

II. Discussion............................................................................................... 39

1. The rights of shareholders ................................................................... 39

2. Equitable treatment of shareholders .................................................... 40

3. Role of stakeholders in corporate governance .................................... 40

4. Disclosure and transparency ............................................................... 41

5. The responsibilities of the board ......................................................... 42

III. Conclusion .............................................................................................. 42

E. Appendix ..................................................................................................... 44

3

Abbreviations

AGM Annual General Meeting of Shareholders

BOD Board of Directors

BOM Board of Management

CG Corporate Governance

HOSE Ho Chi Minh City Stock Exchange

OECD Organization for Economic Cooperation and Development

RPT Related Party Transaction

4

A. Executive Summary

This term paper is commissioned to evaluate the assessment and implementation of corporate

governance which examined on Traphaco Joint Stock Company, a Vietnamese

Pharmaceutical company. The research is intended to measure the level of applicable

corporate governance practice regarding to the strengths and weakness on company’s

corporate governance performance.

Methodologies for approaching and analyzing company issues are based on the instructions

of OECD Corporate Governance Principles which is emphasized on five key categories

including the rights of shareholders, equitable treatment of shareholders, role of stakeholders,

disclosure and transparency, and the responsibility of the board. The assessments to the

company structure of corporate governance are based on available and accessible information

and document on public such as company Annual report, notice, minutes, reports and

company website.

The overall result shows that Traphaco Joint Stock Company performs well on its corporate

governance perspectives with the total average score is 69.1%. Contributed to that, there are

four categories have above average score except the role of stakeholder category – which has

score under average. In particular, the company basically exercises effectively the rights of

shareholder and equitable treatment of shareholders for providing fair and appropriate to

shareholder rights and interests. Disclosure and transparency is on medium level with some

ambiguous issues. The remaining two categories, role of stakeholders and the responsibility

of the board, needed to be improved to meet the requirement on the Principles.

The research have found that Traphaco is on the right trace to improve and fulfill their

assessments on corporate governance benchmarks based on the OECD Principle guidelines.

For the effective achievements, the company should promote the role of Board of Director

and gain supports from regulators as well as its stakeholders, for a major driving force in

implementing good corporate governance practice.

The accessed data of this research mainly based on available information and documents

public on the company website and other reliable online sources. This may cause limitations

and possibilities of inaccurate on evaluated results.

5

B. Research Methodology

I. Benchmarks

OECD has been accomplished as a leading organization to promote good practice of

corporate government. The OECD Principles of Corporate Governance is accepted as an

international benchmark and wildly applied in both country level and company level. The

ultimate goal of the Principles is identify the strengths and weakness in corporate governance,

and propose orientations for improving and enhancing the performance of corporate

governance companies.

The effective framework of corporate governance under OECD methodology should be

included six principles1

Principle I: Ensuring the Basis for an Effective Corporate Governance Framework

Principle II: The Rights of Shareholders

Principle III: The Equitable Treatment of Shareholders

Principle IV: The Role of Stakeholders in Corporate Governance

Principle V: Disclosure and Transparency

Principle VI: The Responsibilities of the Board

Each principle would have more detail criteria for accessing and analyzing closer to company

aspects of corporate governance which is consistent with company regulatory and complying

with the Vietnamese law. Except the Principle I, which is considered for dealing with

“government and regulator issues”2, the remaining five principles are critical for the

evaluation of company in term of effectiveness and transparency.

II. Structure and Assessment of Areas

The research takes a review on five important areas of the OECD principles consisting of

rights of shareholders, equitable of treatment of shareholders, role of stakeholders, disclosure

and transparency, and responsibilities of the board. The approaches of each area will be

measured and evaluated by asking questions on specific issues, instructed by OECD criteria,

for assessing the company corporate governance based on the available public information of

the company. There have five parts and each part dealing with one principle containing

assessment questions:

Part 1: The Rights of Shareholders

1 Methodology for Assessing the Implementation of OECD Principles of Corporate Governance – OECD 2007.

2 Vietnam Corporate Governance Scorecard 2012, p.27.

6

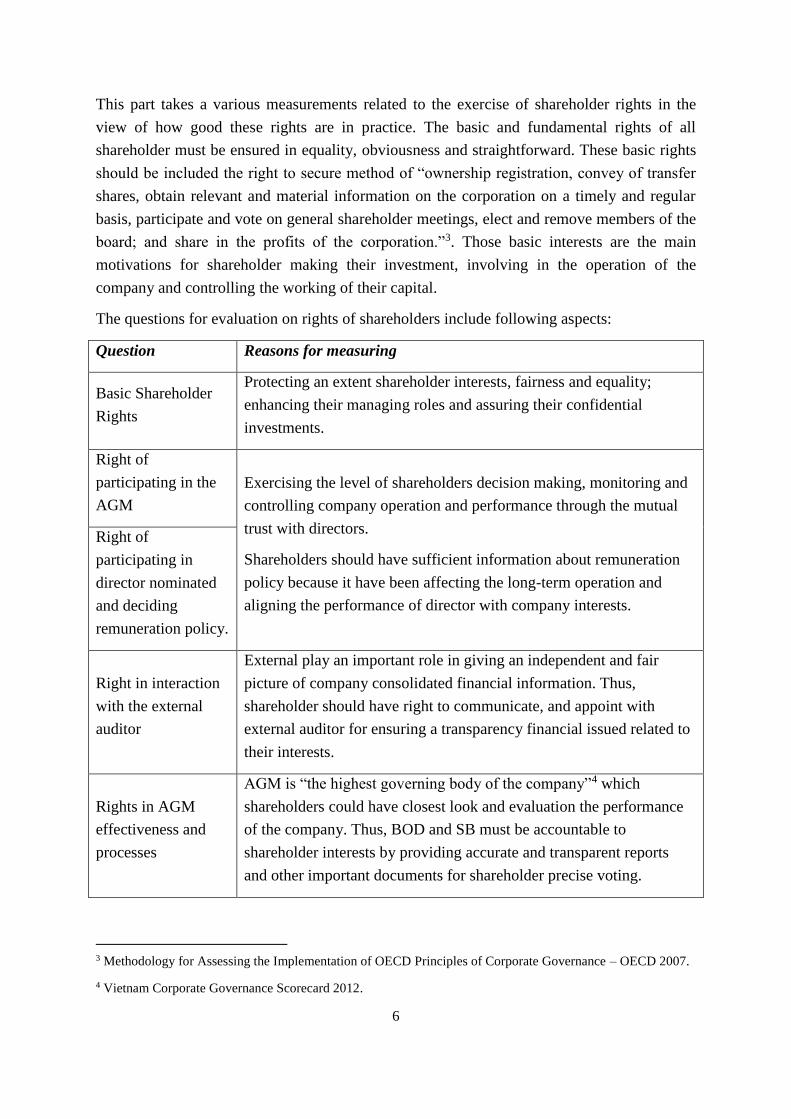

This part takes a various measurements related to the exercise of shareholder rights in the

view of how good these rights are in practice. The basic and fundamental rights of all

shareholder must be ensured in equality, obviousness and straightforward. These basic rights

should be included the right to secure method of “ownership registration, convey of transfer

shares, obtain relevant and material information on the corporation on a timely and regular

basis, participate and vote on general shareholder meetings, elect and remove members of the

board; and share in the profits of the corporation.”3. Those basic interests are the main

motivations for shareholder making their investment, involving in the operation of the

company and controlling the working of their capital.

The questions for evaluation on rights of shareholders include following aspects:

Question Reasons for measuring

Basic Shareholder

Rights

Protecting an extent shareholder interests, fairness and equality;

enhancing their managing roles and assuring their confidential

investments.

Right of

participating in the

AGM

Exercising the level of shareholders decision making, monitoring and

controlling company operation and performance through the mutual

trust with directors.

Shareholders should have sufficient information about remuneration

policy because it have been affecting the long-term operation and

aligning the performance of director with company interests.

Right of

participating in

director nominated

and deciding

remuneration policy.

Right in interaction

with the external

auditor

External play an important role in giving an independent and fair

picture of company consolidated financial information. Thus,

shareholder should have right to communicate, and appoint with

external auditor for ensuring a transparency financial issued related to

their interests.

Rights in AGM

effectiveness and

processes

AGM is “the highest governing body of the company”4 which

shareholders could have closest look and evaluation the performance

of the company. Thus, BOD and SB must be accountable to

shareholder interests by providing accurate and transparent reports

and other important documents for shareholder precise voting.

3 Methodology for Assessing the Implementation of OECD Principles of Corporate Governance – OECD 2007.

4 Vietnam Corporate Governance Scorecard 2012.

7

Part 2: The Equitable Treatment of Shareholders

A good corporate government practices “should ensure the equitable treatment of all

shareholders, including minority and foreign shareholders”5. The fundamental rights of all

shareholders should be respected and defined the guidelines to preserve effectively equitable

treatment of shareholder, as well as protected from infringed actions. This part includes

questions that investigate not only in how equitable treatment of shareholder is exercised, but

level of integrity of protection for shareholders from potential misappropriated actions of

boards, managers as well as majority shareholders. The categories of questions will cover

issues in equally treatment of share classes in following aspects:

Questions Reasons for measuring

Equitable treatment of

shareholders in share

rights and voting rights

With the same class of share, it should carry the same right.

Shareholders that hold those share must be treat equally for

obtaining information as well as decision making. This enhance

the fairness confidential of shareholder involving in company

decision making.

Application of

shareholder rights in

certain circumstances

Accompany with the policy on equitable treatment, the level of

practical application the rights in reality should be regularly

promoted, especially minority shareholders.

Company structure and

shareholder right of

redress from abusive

actions

Shareholders need to know about the company structure and the

level of alerting from abusive actions should be observed for

preventing and also, for appropriate compensations.

Equitable treatment of

shareholders at the AGM

It is important for shareholders exercising their right at the AGM

and all of them should be treated equitably in assessing AGM

procedures and approval of all issues related to the company

changes which are discussed.

An alert to conflicts of

interests, insider trading,

and self-dealing actions

There are always potential conflicts between BOD and

shareholders related to the interests of both sides. The policy on

this relationship should be disclosed and follow the Law. For the

good CG practices, those conflict issues should be well aware,

monitored and managed.

Related party

transactions

Related party transactions have generated profit or dividend to

shareholders. Thus, the information on this issues should be well

managed and fully provided to all shareholders.

5 Methodology for Assessing the Implementation of OECD Principles of Corporate Governance – OECD 2007.

8

Part 3: The Role of Stakeholders

The sustainable development of a company have been recognized as “the competitiveness

and ultimate success of a corporation is the result of team work that embodies contributions

from a range of different resource providers including investors, employees, creditors, and

suppliers. Therefore, in the long-term interest of a corporation foster wealthy-creating co-

operation among stakeholders.”6 The main characteristics of this part will take a disclosed

view and legal framework of the stakeholder related issues. The questions will briefly

describe the respectabilities of stakeholder right dealing with law or mutual agreement, an

effective compensation available dealing with violations, sufficient and reliable access to

information, directed communication and company’s obligation to broader community.

Question of evaluations:

Questions Reasons for measuring

The protection

and recognition

on stakeholder

interests.

The company must effectively enforce the legal right of stakeholders

stated in law and mutual agreement. Because stakeholders have strong

impacts on the company activities. By this, it will favorable the mutual

relationship between the company and their stakeholders. Moreover,

stakeholder mutual communication should be promoted for unifying

benefits in case of infringement happens.

Company

obligations and

employee

benefits

“The employees of a company are important stakeholder”7 who is the

critical motivation for the development and prosperousness. Thus,

benefits and protection from unethical issues for employees must be

aligned with long-term company policies, should be carefully evaluated.

Creditor rights Creditors deserve an important investor and their right should be

respected with the obligation of the company in paying their interests.

Benefits to the

environment and

the community

The good corporate governance practice is not only focusing on the

company development, but the being responsible for the social

sustainable development.

Part 4: Disclosure and Transparency

The international standard of OECD about disclosure and transparency require “the timely

and accurate disclosure on all material matters, including financial situation, performance,

6 OECD Principle of Corporate Governance, Annotation, Chapter IV, p.46, 2004.

7 Methodology for Assessing the Implementation of OECD Principles of Corporate Governance – OECD 2007.

9

ownership and governance of the company.”8 The strong disclosure and transparency policies

contributes to promote shareholder ability to monitor and exercise their ownership rights,

increase the company level of investor protection and attract new flow of capital as well as

maintaining confidence of market. The weak of transparency cause a totally counter-effect

such as a failure and bankruptcy in the perspective of complex and non-disclosure financial

statement and audit. It rises an important unethical issues for financial management and the

warning of catastrophic of mismanagement.

Based on those importance of the issues, the good corporate governance practices of a

company should be fairly investigated and disclosed for critical categories include in the

Annual report such as “financial and operating result, company objective, major share

ownership and voting rights, remuneration policy, issues regarding employees and other

stakeholders, related transaction party, governance structure and policies.”9 In addition,

disclosure and transparency related to independent audit, accountable external auditors,

timely and cost effective information should be well prepared and disclosed. This part

consists of questions that take measurements on above categories based on available

document publicly provided by the company.

Questions Reasons for measuring

Annual report

The Annual report is considered as a communication vehicle for

shareholders accessing to the performance of the company, specific in

financial statement, BOD and SB performance reports, dividend

policies and other necessary information. Those information gives the

shareholder access to “management’s capacity to respond successfully

to changes in the business environment and convince potential

investors of the benefits of investing in the company”10.The company

should provide a transparent and accurate Annual report for achieving

a good CG practice.

Disclosure on

related party-

transactions

The undisclosed on related party-transactions would cause a risk of

abusive actions which are harmful to the company performance and to

shareholders interests.

CG report

perspectives

The CG report should be provided as part of the Annual report.

Because it includes BOD and SB values and responsibilities, as well

as the company guideline and strategies. Based on the SG report,

shareholder could have accessed to the company performance,

8 The OECD Principles of Corporate Governance, 2004.

9 OECD Principles of Corporate Governance, Annotation, 2004.

10 Vietnam Corporate Governance Scorecard 2012, p.67.

10

objective achievements and consolidated financial statements.

External audit and

audit activities

disclosures

An external auditor is critical for independence, assurance and

credibility in providing a competent financial information to

shareholders and affecting the opinion of potential investors also.

Thus, there should be transparent in authorizing external auditor with

an approval from shareholders.

Information

disseminating

Level of mechanism for ensuring shareholder access to information of

the company. This is important for them to inspect and monitor the

ongoing operation of the company.

Part 5: The Responsibilities of the Board

The Board generally takes a responsibility for the whole operating of the company and be

accountable to the interests of company and its shareholders. The OECD principle for this

part recognized the responsibilities of the Board in “monitoring managerial performance and

achieving an adequate rate of return for shareholders, while preventing conflicts of interest

and balancing competing demands on the corporation.”11 The works of Board must be

effectively comply with law and regulations, as well as the Charter and other company’s

agreements.

Basically, Vietnamese companies have two tiers of Board consisting of BOD and SB. The

BOD takes a duty of ensuring fairness and equitability on shareholders, working on company

interests, protecting shareholder rights. Moreover, BOD is responsible for the operation and

performance of its business, for appointment, remuneration and discipline policies. Which is

all should be adherent to Company Charter and reported to the shareholder at the AGM.

On the other hand, SB is responsible for monitoring all financial oversights of the company

which are standardized by law and regulations. The SB also monitors the internal fulfillments

related to role of BOD and other management’s functions for reporting to shareholders.

In general, BOD and SB are not only act on company and shareholder interests, but on their

own interests. Thus, they are expected to take more responsibility on transparency of their

works. The questions for evaluation responsibility of board includes following aspects:

Questions Reasons for measuring

Board basic responsibilities Evaluating the effective role of board and discovering

comprehensiveness level of CG guidelines.

Leadership role of the chairman Measuring the level of effectiveness that the chairman

11 Methodology for Assessing the Implementation of OECD Principles of Corporate Governance – OECD 2007.

11

leads the other directors with integrity and trust. Because

the Chairman provides the effective leadership to all

board members and quality decision making as well as

ensuring the working of the whole operation. The

chairman is expected to be independent.

Skills, competences and

effectiveness of Board

Board is responsible for the best interest of the company

and its shareholders. Thus, competency and skill of Boar

should be well accomplished and disclosed to

shareholders.

Board effectiveness referring

information, meetings and

records

Level of transparent requirements in board meeting and

records should be well disclosed to their shareholders.

Because this disclosure will reveal the effectiveness of

the working of Board are responsibilities.

Board effectiveness referring to

company strategy, risk, and

oversight

Level of effectiveness of board in handling company

objectives and operations. Shareholder’s intension for

making an investment is how their investing will

generate interests. Thus, Board effectiveness referring to

company strategy, risk, and oversight is important for

shareholder decision and should be measured.

Auditing

The responsibility of auditing activities in providing

clear, effective, and reasonable reports on company

operating and functioning.

Supervisory Board role

SB assures that work of BOD must be comply with law

and regulation. SB also is responsible for inspecting and

evaluating of the financial reports, as well as managing

the external auditor.

III. Company Review

The research takes a view on the performance of Traphaco, a Vietnamese manufacturer and

distributor of pharmaceutical products, on its degree of corporate governance practice in

current circumstances. Traphaco Joint Stock Company was successfully conducted IPO in

2007 for attracting participating of shareholders. The company was listed on Ho Chi Minh

Stock Exchange (HOSE) in 2008, after being invested by Mekong Capital (a private equity

company based in Ho Chi Minh City).

12

Mekong capital works closely to the board of management for improving the company

corporate governance structure. Up to this point, the charter capital of Traphaco has been

increased to VND 246,764,330,000 after 10 issuances.

IV. Data

The assessment of this research consists of all available public information and documents

provided on the company website and other internet reliable sources. They are included:

Traphaco Annual Report, Company Charter, Minutes of Meeting, AGM Notices, AGM

documents, company website, and other reliable corporate governance sources.

V. Weight of areas and categories

Weighting practices are based on specific 78 questions divided into five part according to

OECD principle which have mentioned in structure part. In each part, every questions would

be evaluated by a comparison between the company’s reality CG issues and the standardized

of CG good practice in the Vietnamese Model charter and OECD Principle Corporate

Governance.

The weighting of scored areas regarding to five categories are summing to 100% as

following:

Category

Number

of

questions

Weight (%

of total

score)

Why it is needed

The rights of shareholders 17 20 The chosen of equality weight of score

to each five categories of corporate

governance factors would increase the

relative importance for each category

that needed to be emphasized.

Equitable treatment of

shareholders 16 15

Role of stakeholders in

corporate governance 7 5

Disclosure and transparency 19 25

The responsibilities of the

board 19 35

Total 78 100

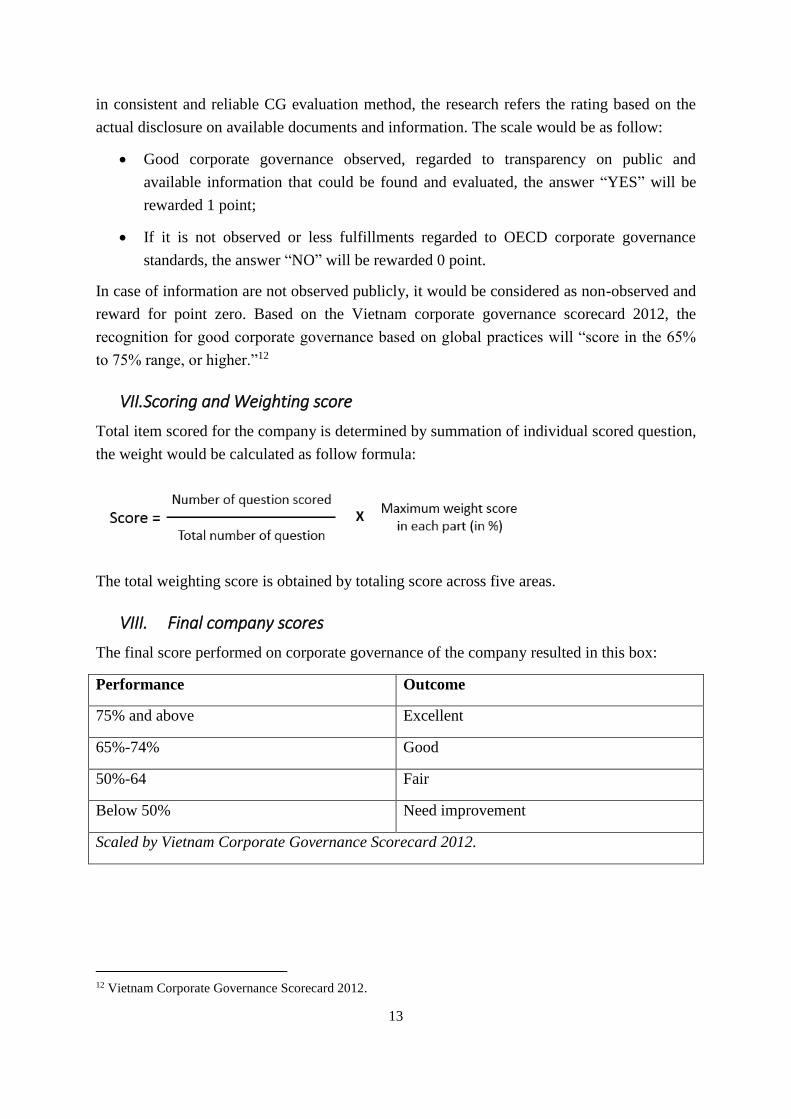

VI. Evaluation method

The quality of corporate governance should be recognized in three levels according to the

terminology of the OECD Principles Assessment Methodology. Because there is a limitation

13

in consistent and reliable CG evaluation method, the research refers the rating based on the

actual disclosure on available documents and information. The scale would be as follow:

Good corporate governance observed, regarded to transparency on public and

available information that could be found and evaluated, the answer “YES” will be

rewarded 1 point;

If it is not observed or less fulfillments regarded to OECD corporate governance

standards, the answer “NO” will be rewarded 0 point.

In case of information are not observed publicly, it would be considered as non-observed and

reward for point zero. Based on the Vietnam corporate governance scorecard 2012, the

recognition for good corporate governance based on global practices will “score in the 65%

to 75% range, or higher.”12

VII. Scoring and Weighting score

Total item scored for the company is determined by summation of individual scored question,

the weight would be calculated as follow formula:

The total weighting score is obtained by totaling score across five areas.

VIII. Final company scores

The final score performed on corporate governance of the company resulted in this box:

Performance Outcome

75% and above Excellent

65%-74% Good

50%-64 Fair

Below 50% Need improvement

Scaled by Vietnam Corporate Governance Scorecard 2012.

12 Vietnam Corporate Governance Scorecard 2012.

14

IX. Caveats

Firstly, the research is conducted on available public information and documents and it is

not expected to discover and predict the accurate level of corporate governance in reality.

Secondly, there are only corporate governance policies and practices which are standardized

by OECD principle are assessed in this research.

15

C. Specific Finding

This section includes the analysis on specific questions in order to examine which categories

are well implemented and which ones need to be improved.

Part 1: Rights of Shareholders (OECD Principle II)

No. Questions Answer Sources References

Basic Shareholder Rights

1 Does the company

offer an accurate

ownership on share

registration?

YES Company

Charter:

Article 6

Company charter, Article 6: Share

Certificate.

“Shareholders of the Company are

entitled to be granted a share

certificate or certificate on ownership

of shares (hereinafter referred to as

“share certificate”) corresponding to

their number of shares and types of

shares.”

2 Does the company

offer freely

transferring share

right?

YES Company

Charter,

Article

8/Article 11

The company offer the right for

shareholder freely transfer their share

comply with the Law.

Company charter, Article 8:

“All shares can be freely transferred,

unless otherwise provided by this

Charter and the Law. All shares

listed at the Stock Exchange/the

Securities Trading Center shall be

transferred under the Law on

securities and the securities

market, and the of the Stock

Exchange/the Securities Trading

Center.”

Company charter, Article 11, item

2c:

“To freely transfer the paid-up

shares in accordance with the

provisions of this Charter and the

applicable Law.”

16

2 Does the company

effectively and

seriously provide

voting right, and

right to timely

information?

YES Company

Charter,

Article 11,

items 2a,

2e.

Voting right and right to information

are provided on company charter.

Article 11, item 2a: “Holders of

ordinary shares have the right to

attend the General Meeting of

Shareholders and exercise the right

of voting in person or through a

Proxy.”

Article 11, item 2e: “inspect

information related to Shareholders

in the list of Shareholders who are

fully qualified to participate in the

General Meeting of Shareholders and

request the correction of inaccurate

information.”

3 Do shareholders

have the right in

nominating or

dismissing member

of BOD and SB?

YES Company

Charter,

Article 11

and

Article 24

The right of nominating member of

board is mentioned in company

charter. Article 11, item 3a:

“A Shareholder or a group of

Shareholders holding more than

5% of total ordinary shares for six

consecutive months or more shall

have the right to nominate members

of the Board of Management or the

Inspection Committee.”

Company charter, article 24, item

2:

“The Shareholders holding more

than 5% of voting shares for a

consecutive period of six months or

more have the right to add up the

voting rights of each one together for

nominating candidates to the Board

of Management. A Shareholder or a

group of the Shareholder holding

more than 5% to below 10% of

17

voting shares for a consecutive

period of six months or more shall

have the right to nominate one

member; from 10% to below 30%

shall have the right to nominate

two members; from 30% to below

50% shall have the right to nominate

three members; from 50% to below

65% shall have the right to nominate

four members and from 65% or more

shall have the right to nominate full

of members.”

4 Does the company

pay interim and

dividend an

equitable and timely

schedule?

YES Company

Charter,

Article

11/Resoluti

on of BOD

on interim

and

dividend.

The dividend policy stated in the

Company Charter. Article 11, item

2b:

“Holders of ordinary shares have

right to receive dividends.”

The company have timely interim

and dividend announced on the

website on regular “Resolution of

BOD on interim and dividend.”

5 Do shareholders

have the right to

“approve major

corporate

transactions

(mergers,

acquisitions,

divestments and / or

takeovers)?”13

YES Company

Charter,

Article 20,

item 2.

The article 20, item 2 in the Charter

states that “the purchase

transactions affected by the

Company or its branches valued at

50% or more of the total value of

assets of the Company and its

branches recorded in the latest

audited accounting books shall be

approved by at least 75% of the

total voting shares of the

Shareholders eligible to vote who

attend the General Meeting of

Shareholders in person or through

the Proxy.”

13 Vietnam Corporate Governance Scorecard 2012

18

Right of participating in the AGM

6 Does the company

provide an effective

AGM shareholder

notice (notice

sufficiently includes

date, location,

discussed issues?

YES Company

Charter,

Article 17

Company

website

The AGM notice must be provided

on timely manner which is stated in

the company Charter, Article 17,

item 2 that requires date, location, an

agenda for the meeting.

The item 3 of this article requires

that: “The notice of the General

Meeting of Shareholders must

include the meeting’s agenda and

information relating to matters to

be discussed and voted on at the

General Meeting of

Shareholders……”

In addition, the company website

also provide timely the “Invitation

letter of the annual general assembly

of shareholders.” Thus, there is full

information about the AGM that

could easily be found.

7 Are there

opportunities for

shareholders ask

questions at the

AGM allowed on the

agenda?

YES Guidelines

and

Working

Agenda on

the AGM.

The company have clearly stated an

instruction procedure for

shareholders to discuss at the AGM

effectively in the “Guidelines and

Working Agenda on the AGM.”

8 Do shareholders

have opportunities to

place a matter or

proposal at the

AGM?

YES Company

Charter,

Article 17

The shareholders have right to rise

issues, matter or proposal at the

AGM which is stated in Article 17,

item 4 - Convention of the General

Meeting of Shareholders, agenda

and notice of the meeting.

It states that: “A Shareholder or

groups of Shareholders as stipulated

by Article 11.3 of this Charter have

the right to propose matters for

19

the agenda of the General

Meeting of Shareholders.”

9 Are there evidence

of the attendance of

Chairman, BOD,

Head of SB, and

CEO?

YES Company

Charter,

Article 19,

item 4.

Minute of

the Annual

General

Meeting

2014.

The attendance of Chairman, BOD,

Head of SB, CEO is not compulsory

as stated in company charter, Article

19, item 4.

However, it is evident that there are a

full attendance of those position

which is mentioned in the “Minute of

the Annual General Meeting 2014.”

Right of participating in director nominated

10 Are there sufficient

information (from

notice and company

website) about

potential nominated

directors for

shareholders to

evaluate?

YES Annual

Report

Decision on

nominating

additional

director.

There is sufficient information

related to profile and qualifications

of the potential nominated directors

provided in the BOD report, part of

the Annual Report (page 32). There

is a “Decision on nominating

additional director” public on the

website for announce voting results.

11 Do shareholders

effectively have

opportunities to

receive information,

make their view, and

vote on

remuneration policy?

NO Annual

Report

Company

Charter

The amount of Board remuneration

are disclosed on the Annual report

2013 (Consolidated financial

statement, page 104). However,

there are no additional information

find on public about the detail

information on remuneration for

appropriateness to shareholders.

Right interaction with the external auditor

12 Were there

evidences of the

attendance of

external auditor at

AGM for evaluating

company audit

NO Annual

Report

There is no evident information

related to the attendance of external

auditor at the AGM available on the

website or in other company public

documents. There is only an

independent report of external

20

issues? auditor mentioned in the Annual

Report 2013 (page 73), reported by

Deloitte Vietnam limited. Thus, this

leads to poor interaction between

shareholders and external auditor.

13 Did the company

fully provided

independent

information about

appointment of

external audit to

shareholder?

NO The information on external auditor

is rarely provided on official

document on the website with full

profile.

14 Did the shareholder

have opportunities in

selecting and

appointing external

auditor for the

company?

NO Minutes on

AGM 2014

Generally, the selecting of the

external auditor is authorized for

BOD and shareholder will voting for

appointing the external auditor. The

voting result are disclose on the

Minutes on AGM.

Rights in AGM effectiveness and processes

15 Does BOD and SB

provide a full and

comprehensive

report to AGM on

their performance?

YES Annual

Report

The report on the performance of

BOD and SB are found in the

Annual Report 2013 (page 26 – 44).

The report are generally detail, clear

and comprehensive related to

business performance, financial

situations, company objective and

recommendations.

16 “Does the company

provide explicit

information in the

AGM notice for

voting in absentia

and proxy voting?”14

YES Company

website

Notice on

AGM 2014.

Company

Charter,

Based on the Company Charter,

stated in Article 15, item 1, the

shareholder could “Authorized

Representative(s) to exercise their

rights of shareholders in

accordance with the Law.”

The Notice on AGM that is public on

14 Vietnam Corporate Governance Scorecard 2012.

21

Article 15. the website contain information and

procedure for absentia and proxy

voting.

17 Does the company

provide a full and

necessary

explanation (in

AGM meeting

minutes or website)

about each agenda

items approved by

shareholders?

YES Company

website

Minutes on

AGM .

Company

Charter,

Article 22.

Based on the Company Charter,

Article 15 stated that it is

requirement for the company to

provide sufficient and timely minute

with “true evidence of works which

have been conducted at the General

Meeting of Shareholders.”

The minutes on AGM posted on the

website includes agenda items that

fix with issues discussed in notice

and Annual report 2013.

Part 2: The Equitable Treatment of Shareholders (OECD Principle III)

No. Questions Answer Source References

Equitable treatment of shareholders in share rights and voting rights

1 Are there evidence

that the same class of

share carrying the

same right?

YES Traphco

Regulation

on

Corporate

Governance

The company provides shareholder

the same right on the same class of

share that they hold and it is stated

on Chapter 2, Article 3, item 5 in

the “Traphco Regulation on

Corporate Governance 2014.”

2 Does the company

feature one vote for

one share policy?

YES Guidelines

and

Working

Agenda on

the AGM

The policy of “one vote on one

share” is stated in the “Guidelines

and Working Agenda on the AGM.”

The section II, item 3 provides

shareholders one vote for each share

owned.

Application of shareholder rights in certain circumstances

3 Are there evidence

that minority

shareholders are

effectively

NO The public documents for assuring

the minority shareholder right is

limited.

22

protected?

4 Do minority

shareholders have

impacts on board

decisions or other

company key issues?

NO Company

Charter

Annual

Report

The Company charter, Article 11

“Right of Shareholders”, item 3

stated that “A Shareholder or a group

of Shareholders holding more than

5% of total ordinary shares for six

consecutive months or more” have

right on key issues of the company.

There is no room for minority

shareholder right in making decision.

The Annual Reports are also not well

stated the on equitability for small

holding share investors.

5 Does the requirement

on re-nominated and

re-elected director

timely exercise?

YES Company

Charter

The re-nominated and re-elected of

BOD are required in the time interval

of five years and unlimited time of

re-nomination as stated in the

Company Charter, Article 24, item

1 “ the members of the Board of

Management may be re-elected for

an unlimited number of terms.”

6 Does the company

effectively enable

cross border voting

rights?

NO Foreign or cross investors voting

rights are not possibly observed and

not well facilitated. Firstly, the

documents are rarely found in

English versions as well as not being

public on the website. For instance,

the latest uploaded English material

on Annual Meeting is still up to the

year 2009. Secondly, the related

material English on company issues

are not available in timely manner

compare to the best practice within

20 days. The English materials are

only translated only for special

purposes and hard to find on public.

Company structure and shareholder right of redress from abusive actions

23

7 Does the company

availably provide a

clear and transparent

description of

company structure?

YES Annual

Report

The company provide a clear and

transparent description of company

structure, with detail explanation in

inter-relationship, director’s profiles,

organization chart and function of

each responsible department. All

those information are revealed in the

Annual Report (page 54-61).

8 Are there no

evidence of structure

that potentially may

violate minority

shareholder rights?

NO Company

website

Annual

Report

Although the structure of the

organization is described in the

Annual Report, it may not fully

comprehensive to all shareholder,

especially minority shareholders. It

will imply a possibility of infringe

their right. The structure is also not

posted on company website which

limited the access to all shareholders.

9 Does the company

provide and ensure

effective redress

policy for

shareholders in case

of complaining or

violating their rights?

YES Company

Charter

Company Charter, Article 34, item 2

“Compensation.”

It is stated that “The Company shall

pay compensation to persons who

were, are being and shall possibly be

in danger of becoming an involved

party in cases of complaint, lawsuit

or prosecution, which were, are

being or shall possibly be

conducted regardless of whether

these are civil or administrative

cases…” The company assure the

available redress if there are any

infringements for shareholders as

stated in this Article.

Equitable treatment of shareholders at the AGM

10 Are there evidences

provided that

shareholders

effectively

YES Minute of

AGM

Guidelines

and

There is evident that the company

inform shareholders about

fundamental changes by posted

“Announcement” on the company

24

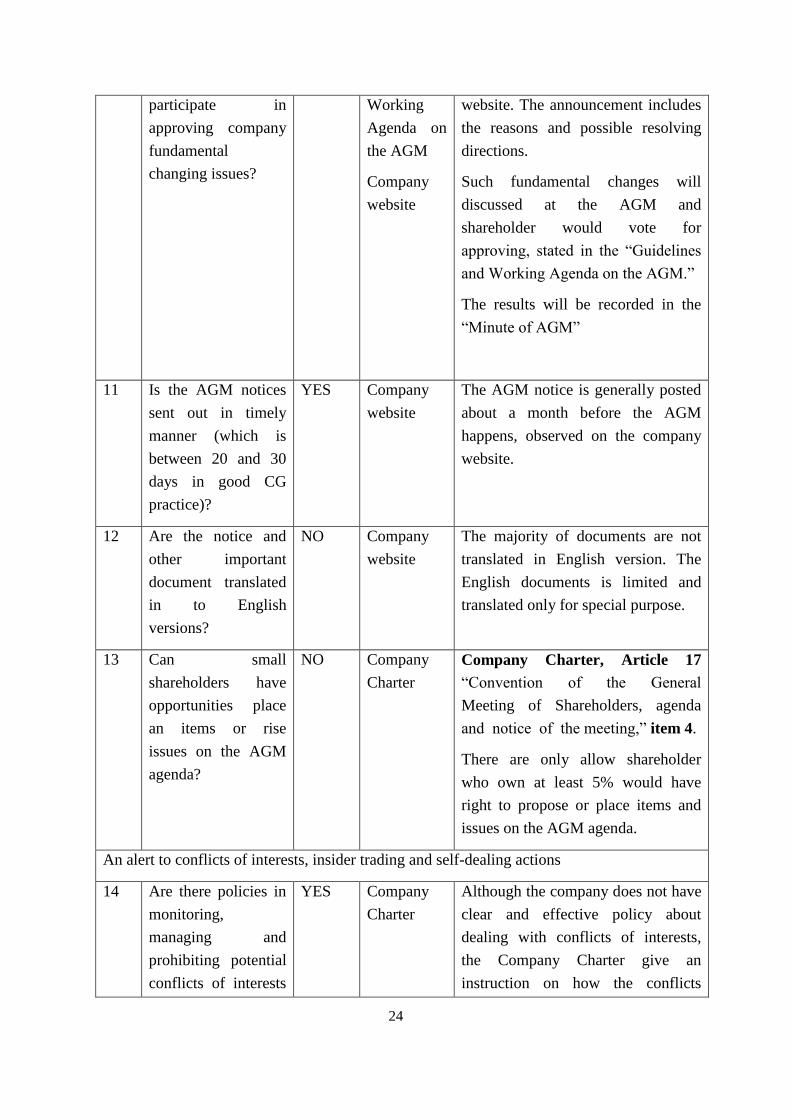

participate in

approving company

fundamental

changing issues?

Working

Agenda on

the AGM

Company

website

website. The announcement includes

the reasons and possible resolving

directions.

Such fundamental changes will

discussed at the AGM and

shareholder would vote for

approving, stated in the “Guidelines

and Working Agenda on the AGM.”

The results will be recorded in the

“Minute of AGM”

11 Is the AGM notices

sent out in timely

manner (which is

between 20 and 30

days in good CG

practice)?

YES Company

website

The AGM notice is generally posted

about a month before the AGM

happens, observed on the company

website.

12 Are the notice and

other important

document translated

in to English

versions?

NO Company

website

The majority of documents are not

translated in English version. The

English documents is limited and

translated only for special purpose.

13 Can small

shareholders have

opportunities place

an items or rise

issues on the AGM

agenda?

NO Company

Charter

Company Charter, Article 17

“Convention of the General

Meeting of Shareholders, agenda

and notice of the meeting,” item 4.

There are only allow shareholder

who own at least 5% would have

right to propose or place items and

issues on the AGM agenda.

An alert to conflicts of interests, insider trading and self-dealing actions

14 Are there policies in

monitoring,

managing and

prohibiting potential

conflicts of interests

YES Company

Charter

Although the company does not have

clear and effective policy about

dealing with conflicts of interests,

the Company Charter give an

instruction on how the conflicts

25

of management,

directors, and

shareholders?

could be solved. (Article 53

“Settlement of Internal Disputes”,

item 1, item 2, and item 3.

15 Does the company

provide effective

restrictions on

insider trading and

self-dealing

according to the

laws?

YES Company

Charter

The purpose of insider trading and

self-dealing actions are intended for

interests. Thus, the restriction and

avoidance for conflicts on those

issues is important for the sustainable

development of the company. The

concept of restrictions are stated in

Article 33“The duty of Honest and

avoidance of conflicts of interests”,

Related party transactions

16 Does company

policy require the

disclosure on the

related party

transactions?

YES Annual

Report

The related party transactions are

fully provide on the Annual report,

“The consolidated financial

statements, section 28, Related Party

Transaction and Balance.”

Part 3: The Role of Stakeholders

No. Questions Answer Source Reference

The protection and recognition on stakeholder interests

1 Are there full

recognition of

company obligation

to their stakeholders

(including in law and

mutual agreement)?

YES Annual

Report

The Annual Report is reflects all

aspects related to the company

obligations to their key stakeholders:

employees, customer, and

shareholders. The Annual Report has

separate section for accessing to

stakeholders:

- “Employees connectedness

through mutual alignments.”

- “Customer connectedness

through product quality.”

- Shareholder connectedness

26

through growing values.”

2 Does the company

provide effective

policies for

protecting/enforcing

stakeholder legal

right from violation

and obtaining

reasonable redress?

NO Annual

report

Company

Charter

There are not evident documents

publicly for specific company

policies for enforcing stakeholder

legal right from violation and

obtaining reasonable compensations.

3 Are there evidence

of clear and effective

communication

procedure among

stakeholders?

NO The company have no evidence for

the motivation of stakeholder

effective communication.

Company obligations and employee benefits

4 Does the company

provide effective

benefits as well as

explicit disclosures

on the health, safety,

and welfare policy

for its employees?

YES Annual

Report

The benefits of employees are fully

provided in the Annual Report

(“Labor Policy for Employees”

section) in such main aspects:

compensation, training, healthcare,

and safety.

5 Does the company

have policy to

protect stakeholder

form illegal or

unethical issues?

NO The company have no available

document of policy on protecting

stakeholder form illegal or unethical

issues. It could not be found on

public.

6 Does the company

ensure the

enforcement of

creditor’s right?

NO Annual

Report

Although the company provide

financial report with detail in the

Annual Report, the actual rights of

creditors are not fully mentioned.

Annual report year 2013

Benefits to the environment and the community

7 Do company policies

and information

mention the

YES Annual

Report

Company

The responsibilities to the

environment and the community are

the long-term company objective

27

environment and the

community?

website mentioned in “Traphaco and Social

Responsibilities” section, page 108.

Traphaco – The way of Green Health

Part 4: Disclosure and Transparency

No. Questions Answer Source Reference

Annual report

1 Does the company

provide a full, clear

and comprehensive

financial

performance of the

company which

disclosed timely

manner on the

Annual report?

YES Annual

Report

A financial information is fully given

by the report of BOD, report of SD

and report of BOM.

- Report of BOD: page 27-28

- SB report: page 41

Other sections: Consolidated Balance

Sheet, Consolidated Income

Statement, Consolidated Cash Flow

Statement, and Notes to the

consolidated financial

Statements.

“Annual Report year 2013.”

2 “Do the CEO and

Chief Accountant

certify the annual

financial statements,

audited and

unaudited?”15

YES Annual

report

There is certifying of the General

Director on the consolidated cash

flow statement.

“BOARD OF DIRECTORS’

STATEMENT OF

RESPONSIBILITY”, Annual

Report year 2013, page 71

3 Are there evidence

that the company

used an

NO Annual

Report

Based on the “INDEPENDENT

AUDITORS’ REPORT” performed

by Deloitte Vietnam Company

15 Vietnam Corporate Governance Scorecard 2012.

28

internationally

accepted accounting

standards?

Limited, the company accounting

standard is “accordance with

Vietnamese accounting standards,

accounting regime for enterprises

and legal regulations relating to

financial reporting.”

4 Does the company

provide a full and

clear picture of

company operation,

including

commercial and non-

commercial

objectives?

YES Annual

Report

The commercial objectives are

clearly and effectively provided in

the “Report of Board of Director”

which are specific in targets, new

financial investments, and new

projects.

The objectives on non-commercial

activities is also mentioned including

investment in human resources,

training programs, and building the

company culture “Traphaco – The

way of Green Health.”

Annual Report year 2013 (page 34-

36).

5 Are the ownership

data related to

shareholding of

BOD, SB, senior

management and

major shareholders

clearly disclosed?

YES Annual

Report

The ownership BOD, SB, senior

management and major shareholders

are well disclosed on the “2014

Shareholder Information.” This

section include detail data about

number of shareholders, number of

shares, par value and percentage of

ownership. Annual Report year 2013

(page 63)

6 Are the board

member experiences

and qualifications

disclosed in the

Annual report?

YES Annual

Report

The profile of board members are

well described with detail and

comprehensiveness related to

qualifications, knowledge and

experiences. Annual Report year

2013 (page 58-61).

7 “Does the Annual

Report disclose

YES Annual

Report

The attendance of individual

directors are provided in the “Report

29

BOD / SB meeting

attendance of

individual

directors?”16

of by Supervisory Board.” Annual

report (page 41).

8 Does the

independent director

effectively

identified?

NO Annual

Report,

Resolutions

of Traphaco

Annual

Shareholder

s Meeting,

held on 29

March 2013

The independent director is not

identified in the Annual Report 2013

and even on the Resolutions of

Traphaco Annual Shareholders

Meeting, held on 29 March 2013.

It is obvious that the company does

not have independent director.

9 Does board

remuneration

information and

policy being

disclosed in the

Annual report?

NO Annual

Report

The remuneration (in data) is

available in the report on

consolidated financial statement.

However, there is not observed

remuneration policy for explaining

how the remuneration is built or

taken from. Annual Report year

2013.

10 Does the dividend

policy are disclosed

on the Annual

report?

YES Annual

Report

The dividend policy is stated in the

Annual Report (page 108). Specific

policy statement “Pay dividends to

shareholders or allocate to retained

earnings for developments in each

period depending on the resolutions

of the annual shareholders meeting

(the dividend payout ratio is 20% of

chartered capital).”

11 Does the company

fully explain and

manage foreseeable

business risk factors

YES The risk management strategy is well

managed by the company. The detail

information related to foreseeable

business risk factors mentioned in

16 Vietnam Corporate Governance Scorecard 2012

30

in the Annual report? the Annual Report, with specific and

comprehensiveness (page 36-39).

Disclosure on related party-transactions

12 Does the company

provide a timely,

comprehensive and

public disclosure

information of

related-party

transactions?

YES Annual

Report

The information on related-party

transactions is fully provided on the

consolidated financial statement,

section 28. The information includes

name of related party, sale and

capital distribution and specific

dividend to shareholder for each

transaction. Annual Report (page

103-104).

CG report perspectives

13 Is the CG report

perspectives

recognized with

quality evaluation?

NO Annual

Report

The CG report is not fully mentioned

in the Annual report, the section for

CG report is not provided. There are

only parts of the CG report are

disclose throughout the Annual

report and are not well described in

comparison with the OECD standard.

External audit and audit activities disclosures

14 Does the company’s

financial statement

being audited by

external auditor?

YES Annual

Report

Resolution

of Traphaco

AGM

The company financial statement is

audited from external auditor, the

Deloitte Vietnam Limited Company,

Annual report year 2013 (page 73).

Resolution of Traphaco AGM,

Article 5. It states that the AGM

have been approved in selecting the

Deloitte Vietnam Limited Company

as their external auditor.

15 Are there documents

that require a

selection of

independent external

auditor?

YES Company

Charter

The company Charter, Article 47,

item 1, item 3. It states that the

company must appoint an

independent auditor company “that

lawfully operates in Vietnam and is

accepted by the State Securities

31

Commission for auditing the listed

companies shall be designated to

audit the Company for the

subsequent fiscal year.”

16 Does external

auditor evaluation

and recommendation

on company

financial statement

disclosed?

YES Annual

report

The “Independent Auditor’s Report”

is included on the Annual report,

which show the auditor evaluation

and recommendation on company

financial statement. Annual Report

(page 73).

17 Are there evidence

that the external

independent Auditor

attend the AGM and

express their opinion

on company

financial issues

NO Resolution

of Traphaco

AGM

Minute of

AGM

Annual

Report

There are no observed sections in

those documents for evidence of the

attendance of independent auditor.

Information disseminating

18 Does the company

website provide

comprehensive,

accessible, and

updated

information?

YES Company

website

The company website generally

provide all key documents related to

the AGM, financial information and

others.

19 “Does the company

provide easy public

access to and contact

details for the

Investor Relations

person or unit?”17

YES Situation on

Corporate

Governance

The company disclose the listed of

contact detail of their shareholder on

the company site, which is part of the

“Situation on Corporate Governance

the first six months of year 2014”.

However, the List is only full access

for internal shareholder and it is

partly uncovered when being public

on the website.

17 Vietnam Corporate Governance Scorecard 2012.

32

Part 5: The Responsibilities of the Board

No. Questions Answer Source Reference

Board basic responsibilities

1 Are the roles of BOD

explicitly stated?

YES Company

Charter

Company charter, Article 32:

Fiduciary duties of members of the

Board of Management, the General

Director and Managers.

It is stated that “Members of the

Board of Management, the General

Director and the Managers shall be

entrusted with the responsibility to

perform their tasks, including tasks

performed in their capacity as

members of sub-committees of the

Board of Management in an honest

manner and by modes that they deem

are in the best interests of the

Company….”

2 “Does company CG

guidance disclose the

material transactions

that must be approved

by the board?”18

YES Company

Charter

The company Charter, Article 25:

Rights and duties of the Board of

Management.

Based on the Article, the Board have

duties to approve the material

transactions.

Leadership role of the chairman

3 Does the company

clearly state the role of

the chairman in the

CG guideline?

YES Company

Charter

The role of the chairman is stated

that “The Chairman of the Board

of Management shall have to

convene and preside over the

General Meeting of Shareholders and

meetings of the Board of

Management , and at the same time

shall have other rights and duties

prescribed in this Charter and the

18 Vietnam Corporate Governance Scorecard 2012.

33

Law on Enterprises.” Company

Charter, Article 26: Chairman and

Vice Chairman of the Board of

Management.

4 Are there evidences

that the chairman is a

non-executive and

independent director?

NO It is not observed that the chairman

of the company is as a non-executive

and independent director.

Skills, competences and effectiveness of Board

5 “Does company

information and

director information

clearly state/disclose

the number of board

seats each director

holds?”19

YES Annual

report

Company

Charter

The company charter, Article 24:

The number and office term of

members of the Board of

Management.

The disclosure on information

related to number of board seats each

director are mentioned in the Annual

report, where full descriptions are

provides on this issue.

6 How many of BOD

are independent

directors?

NO Annual

Report

The information on the Annual

Report does not show the number of

independent directors. It would be

concluded that the company does not

have the present of “independent

directors.”

7 Does the company

have induction policy

and orientation

programs for new

appointment

directors?

NO Company

website

Annual

Report

There are not evident documents

fulfilling the aspects of induction

policy and orientation programs for

new appointment directors available

on the website or mentioned in the

Annual Report.

8 Does the company

have encouraging

policy for BOD and

NO There are no available information

on an encouraging policy for BOD

and SB taking an annual self-

19 Vietnam Corporate Governance Scorecard 2012

34

SB taking an annual

self-assessment

evaluation?

assessment evaluation.

Board effectiveness referring information, meetings and records

9 Are there evidence

that BOD and SB have

a regular meeting

schedule?

YES Annual

Report

There are observed information that

there a regular meeting schedule of

BOD and SB.

Report of the Board of Director,

there is a report that “The Board of

Directors maintained a meeting

schedule of once a month and held

extra-ordinary meetings when issues

arose. Members of the Board are

assigned with clear accountabilities.”

On SB reports: “The Supervisory

Board participated in all regular and

extraordinary meetings of the Board

of Directors to get updated on

Traphaco’s business performance.”

Annual report year 2013, (page 31

and page 42)

10 “Are there

mechanisms in place

to ensure board

members receive

adequate notification

of the board meeting

for all BOD / SB

meetings?”20

YES Company

Charter

The adequate notification of the

board meeting for all BOD / SB

meetings is mechanism the Company

Charter, stated in Article 27, item 7:

Meeting notices and agenda.

11 Are there the

requirement of 2/3 on

quorum for board

decisions?

NO Company

Charter

The company applied voting on

majority, that is “the approval of

the majority of the present

members of the Board of

Management (more than 50%).”

20 Vietnam Corporate Governance Scorecard 2012.

35

Company Charter, Article 27, item

11.

12 Do all meeting

minutes and

resolutions in every

meeting being

recorded for

disclosure purpose?

YES Company

website

Annual

report

Company Charter, Article 27, item

14. It requires that all decisions on

the meeting should be regularly

written and recorded.

The SB report show mentioned that

“all minutes and resolutions in every

meeting are well disclosed and

complied with regulations.”

Annual report year 2013, page 42.

Board effectiveness referring to company strategy, risk, and oversight

13 “Is there evidence that

the BOD receives

regular management

reports on the

company activities

and its financial

position?”21

YES Annual

Report

The BOD have received the regular

reports for proving the role of

controlling and managing the

company. Report of BOD on the

Annual Report is totally based on

those regular management reports on

the company activities and its

financial position.

Annual report year 2013, “Report

of Board of Director.

14 “Is there evidence the

BOD is responsible

for the strategy and

business plans of the

company?”22

YES Annual

Report

Company

Charter

The BOD has responsibility of report

all issues that related to the operation

and the prospects of the company.

Thus, the BOD is responsible for the

strategy and business plans of the

company.

Annual Report, page 28-31.

Moreover, it is stated in the company

21 Vietnam Corporate Governance Scorecard 2012.

22 Vietnam Corporate Governance Scorecard 2012.

36

Charter that BOD have responsibility

to the Company’s business

activities and its affairs.

Article 25: Rights and duties of the

Board of Management, item 3.

15 “Are the BOD/SB be

responsible for and

oversee the risk

management system

of the company?”23

YES Annual

report

It is stated that “With the intention to

manage risk effectively, the Board of

Directors issued the decision

numbered 45/QĐ-HĐQT dated 01

August 2013 to authorize the

formation of the Risk Management

Department.”

Annual report year 2013, page 36.

Auditing

16 “Does the company

report on the activities

of internal audit in its

Annual Report and /

or SB Report?”24

YES Annual

Report

The Internal audit report is available

on the SB report. The function of

internal audit is also well informed

through the report including such

issues “business activities, financial

health, risk management and the

assessment and coordination among

Board team and shareholders.

Annual report year 2013, page 40-

43.

Supervisory Board role

17 “Does the SB report

include discussion of

the SB supervision of

operational and

financial condition of

the company;

performance of BOD,

YES Annual

report

Basically, the SB report provides a

detail and comprehensive contents

related to discussion of the SB

supervision of operational and

financial condition of the company;

performance of BOD, BOM and

executive officers.

23 Vietnam Corporate Governance Scorecard 2012.

24 Vietnam Corporate Governance Scorecard 2012.

37

BOM and executive

officers?”25

Annual Report year 2013, page 40-

43.

18 “Does the SB Report

include reference to

the SB’s performance,

issues discussed and

decisions taken?”26

NO Annual

Report

Although the SB report take an

assessment to SB’s performance,

issues discussed and decisions taken,

it does not include effective

references. This lead to an

ambiguousness on some aspects of

the SB report.

19 “Does the SB report

on its evaluation of

the coordination

between the SB,

BOD, BOM and

shareholders?”27

YES Annual

Report

It is mentioned in section

“Assessment of Coordination

between Supervisory Board with the

Board of Director, Management

Team and Shareholders.”

Annual Report year 2013, page 43.

25 Vietnam Corporate Governance Scorecard 2012.

26 Vietnam Corporate Governance Scorecard 2012.

27 Vietnam Corporate Governance Scorecard 2012.

38

D. Discussion and Conclusion

I. Overall Performance

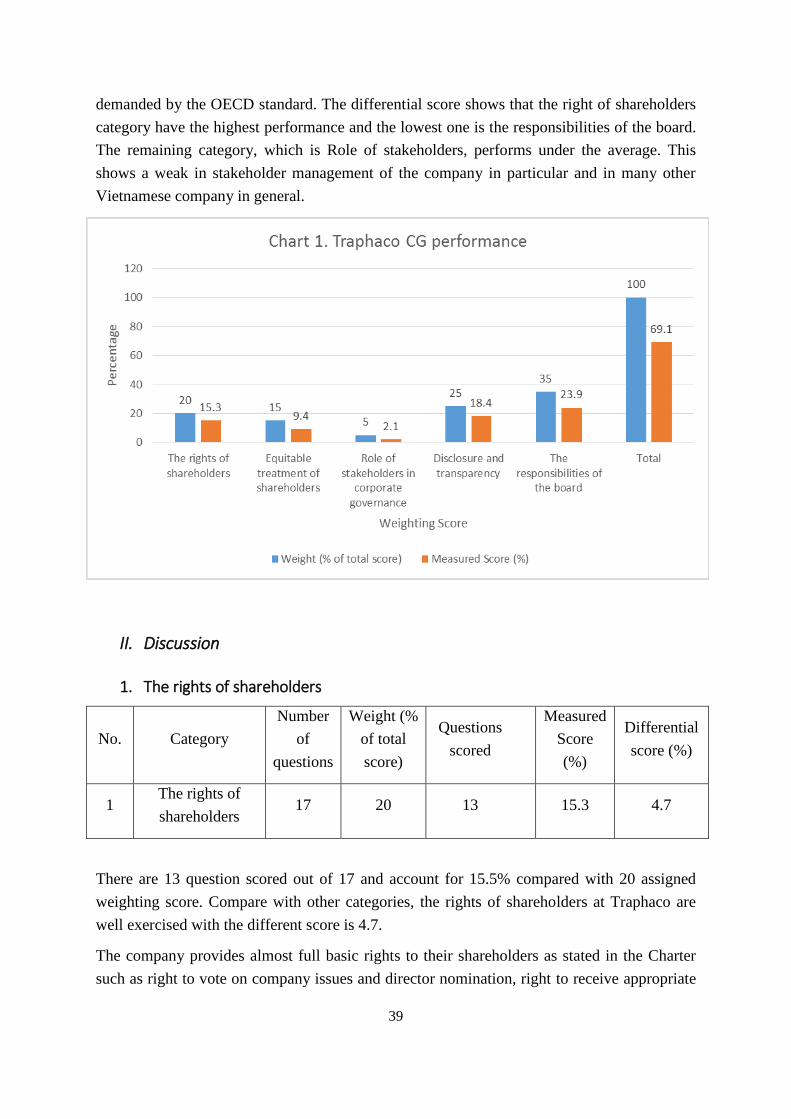

The table below shows overall average corporate governance of the Traphaco Joint Stock

Company is 69.1%, which is considered a good CG performance based on the OECD

standard. It is observed and evaluated from all available information collected from the public

data of the Traphaco’s company.

No. Category

Number

of

questions

Weight

(% of

total

score)

Questions

scored

Measured

Score (%)

Differential

score (%)

(Weight

score –

measured

score)

1 The rights of

shareholders 17 20 13 15.3 4.7

2

Equitable

treatment of

shareholders

16 15 11 9.4 5.6

3

Role of

stakeholders in

corporate

governance

7 5 3 2.1 2.9

4 Disclosure and

transparency 19 25 14 18.4 6.6

5

The

responsibilities

of the board

19 35 13 23.9 11.1

6 Total 78 100 53 69.1 30.9

The chart on Traphaco CG performance (chart 1) shows the comparison of initial weighting

score and the performance of the company. Based on that, the four categories includes Right

of Shareholder, Equitable treatment of Shareholder, Disclosure and Transparency, and the

Responsibility of Board perform above average (compare with weight of total score). It

indicates that the company application of SG regulatory framework is close to good practice

39

demanded by the OECD standard. The differential score shows that the right of shareholders

category have the highest performance and the lowest one is the responsibilities of the board.

The remaining category, which is Role of stakeholders, performs under the average. This

shows a weak in stakeholder management of the company in particular and in many other

Vietnamese company in general.

II. Discussion

1. The rights of shareholders

No. Category

Number

of

questions

Weight (%

of total

score)

Questions

scored

Measured

Score

(%)

Differential

score (%)

1 The rights of

shareholders 17 20 13 15.3 4.7

There are 13 question scored out of 17 and account for 15.5% compared with 20 assigned

weighting score. Compare with other categories, the rights of shareholders at Traphaco are

well exercised with the different score is 4.7.

The company provides almost full basic rights to their shareholders as stated in the Charter

such as right to vote on company issues and director nomination, right to receive appropriate

40

and timely dividend and right to obtain information related to the operation of the company.

It is evident that shareholders are effective and convenient in participating the AGM with

clear, comprehensive and timely notice. The effectiveness and process of the AGM is assured

with a clear agenda for shareholder’s involvement in rising issues or proposals, the full

report, minutes and resolutions of the AGM are also fully provided on the company website.

Regarding areas for improvement, the company fails to provide accurate information on

remuneration policy as well as not promote the external auditor appointment right to

shareholders.

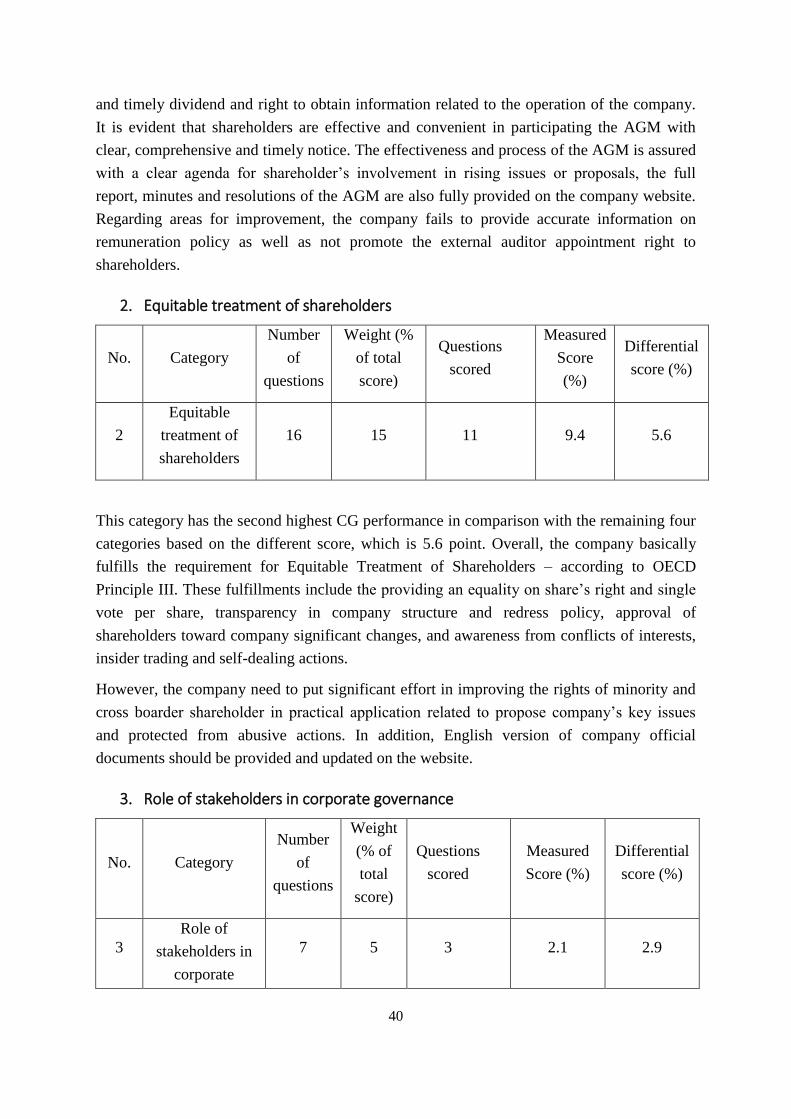

2. Equitable treatment of shareholders

No. Category

Number

of

questions

Weight (%

of total

score)

Questions

scored

Measured

Score

(%)

Differential

score (%)

2

Equitable

treatment of

shareholders

16 15 11 9.4 5.6

This category has the second highest CG performance in comparison with the remaining four

categories based on the different score, which is 5.6 point. Overall, the company basically

fulfills the requirement for Equitable Treatment of Shareholders – according to OECD

Principle III. These fulfillments include the providing an equality on share’s right and single

vote per share, transparency in company structure and redress policy, approval of

shareholders toward company significant changes, and awareness from conflicts of interests,

insider trading and self-dealing actions.

However, the company need to put significant effort in improving the rights of minority and

cross boarder shareholder in practical application related to propose company’s key issues

and protected from abusive actions. In addition, English version of company official

documents should be provided and updated on the website.

3. Role of stakeholders in corporate governance

No. Category

Number

of

questions

Weight

(% of

total

score)

Questions

scored

Measured

Score (%)

Differential

score (%)

3

Role of

stakeholders in

corporate

7 5 3 2.1 2.9

41

governance

The company have performed poorly (below average with 2.1% compare with 5%) in

promoting roles of stakeholder relating to corporate governance perspective. Strengthening in

protecting and enforcing stakeholder legal right from violation, illegal or unethical issues,

obtaining reasonable redress are strongly suggested for the company. Besides that,

communication and relationship amongst stakeholders as well as enforcement of creditor’s

right needed for improvement. Regarding on good practices, the company has shown

obligations to their stakeholders (including in law and mutual agreement) and disclosures on

the health, safety, and welfare policy for its employees which are observed in the Annual

report.

4. Disclosure and transparency

No. Category

Number

of

questions

Weight

(% of

total

score)

Questions

scored

Measured

Score (%)

Differential

score (%)

4 Disclosure and

transparency 19 25 14 18.4 6.6

Based on this finding, there is two-third of the questions assuring for disclosure and

transparency which account for 18.4 percentage. In comparison with the requirements on

“Circular No. 52/2012/TT-BTC”28, the company provides full and basic disclosure on the

Annual report related to such issues business operation, reports of BOD, BOM and SB,

financial statement reports, and senior management team profile/background. In addition,

information on related party-transactions is also provided with detail and comprehensive

manner. Information dissemination is well managed with variety of corporate governance

documents uploaded on the website and available for downloading.

In contrast with these good practices, the company still have areas for improvement. There

are not have an identify of independent director or an explanation of specific director to be

independent. Remuneration and benefits of board are not disclosed or descriptive in the

Annual report and the attendance of external independent Auditor at the AGM is not

observed.

28 Circular No. 52/2012/TT-BTC dated April 05, 2012 of the Ministry of Finance guiding the disclosure of

information on securities market.

42

5. The responsibilities of the board

No. Category

Number

of

questions

Weight

(% of

total

score)

Questions

scored

Measured

Score (%)

Differential

score (%)

5

The

responsibilities

of the board

19 35 13 23.9 11.1