CORPORATE GOVERNANCE, INTERNAL AUDIT AND FINANCIAL PERFORMANCE IN PRIVATE COMMERCIAL BANKS IN ETHIOPIA BY FENET JIMA BEDASO 02/0118/1314653/E A RESEARCH REPORT SUBMITTED TO THE SCHOOL OF POSTGRADUATE STUDIES IN PARTIAL FULFILLMENT FOR THE REQUIREMENT OF THEAWARD OF A MASTER’S DEGREE OF BUSINESS ADMINISTRATIONIN ACCOUNTING AND FINANCE OF CAVENDISH UNIVERSITY, UGANDA November, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CORPORATE GOVERNANCE, INTERNAL AUDIT AND FINANCIAL

PERFORMANCE IN PRIVATE COMMERCIAL

BANKS IN ETHIOPIA

BY

FENET JIMA BEDASO

02/0118/1314653/E

A RESEARCH REPORT SUBMITTED TO THE SCHOOL OF POSTGRADUATE

STUDIES IN PARTIAL FULFILLMENT FOR THE REQUIREMENT OF

THEAWARD OF A MASTER’S DEGREE OF BUSINESS

ADMINISTRATIONIN ACCOUNTING AND

FINANCE OF CAVENDISH

UNIVERSITY, UGANDA

November, 2014

ii

DECLARATION

This research report is my original work and has not been presented for a degree or any other

academic award in any university or institution of higher learning.

Signed Date: November 10, 2014

Fenet Jima Bedaso

iii

APPROVAL

This is to certify that this research report has been submitted to the University Board of

examiners with our approval as University Supervisor.

Signed………………….................... Date …………………...........

Supervisor: Mr. Kyamabbade Edward

Department of Accounting and Finance

School of Business and Management

Cavendish University Uganda

iv

DEDICATION

I dedicate this piece of work to my beloved Parents for the overwhelming support and

encouragement that they have given me.

v

ACKNOWLEGMENT

My sincere gratitude goes to Almighty God for the gift of life that he gave me throughout my

life.

I would like to express heartfelt gratitude to my supervisor, Mr.Kyamabbade Edward for his

priceless time to supervise me during the research period. May the lord reward your effort.

Iam greatly indebted to my colleagues of ACJPS staff, the lecturers in the faculty of school of

postgraduate of Cavendish University Uganda and my fellow classmate for your support during

this journey.

Iam grateful to the staff of private commercial banks in Ethiopia who participated in the research

by sparing their precious time answering my questionnaires without your contribution this

research would not have been possible.

All authors whose material was used to compile this study, Google. Those who supported this

study in one way or another, I appreciate you all

I take this opportunity to thank my beloved family and friends for their love and encouragement

during my study

Lastly, Many more blessing to Ethiopian Fellow in Kampala who has made Positive contribution

during my study.

vi

LIST ACRONYMS

GAAP Generally Applied Accounting Practices

IA Internal Auditing

IAS International accounting Standards

IIA Institute of Internal Auditors

NBE National Bank of Ethiopia

NLB Net Liquid Balance

SPSS Statistical Package for Social Sciences

ROA Return on Asset

ROE Return on Equity

vii

DEFINITIONS OF KEY TERMS

Corporate Governance: is the system of rules, practices and processes by which a corporation

directed and controlled.

Financial Performance: is the measure of the extent to which objectives of an organization are

achieved in relation to defined standards and targets for each objective.

Internal Audit: is independent appraisal function established within an organization to examine

and evaluate its activities as a service to the organization.

viii

TABLE OF CONTENTS

DECLARATION .......................................................................................................................................... ii

APPROVAL ................................................................................................................................................ iii

DEDICATION ........................................................................................................................................... iiiv

ACKNOWLEDGEMENT ........................................................................................................................... iv

LIST ACRONYMS ...................................................................................................................................... v

DEFINITIONS OF KEY TERMS .............................................................................................................. vii

LIST OF TABLES ....................................................................................................................................... xi

LIST OF FIGURES .................................................................................................................................... xii

ABSTRACT ................................................................................................................................................xiii

CHAPTER ONE ........................................................................................................................................... 1

INTRODUCTION AND BACK GROUND TO THE STUDY ................................................................... 1

1.0 Introduction ............................................................................................................................................. 1

1.1 Background to the study ......................................................................................................................... 2

1.2 Problem Statement .................................................................................................................................. 3

1.3 Purpose of the Study ............................................................................................................................... 5

1.6 Scope of the Study .................................................................................................................................. 5

1.6.1 Geographical Scope ............................................................................................................................. 5

1.6.2 Content Scope ...................................................................................................................................... 6

1.6.3 Time Scope .......................................................................................................................................... 6

1.7 Significance of the study ......................................................................................................................... 6

1.8 Conceptual framework ............................................................................................................................ 7

CHAPTER TWO .......................................................................................................................................... 9

LITERATURE REVIEW ............................................................................................................................. 9

2.0 Introduction ……………………………………………………………………………………………………………………………………..9

2.1 The Relationship between Corporate governance and Financial Performance ....................................... 9

2.1.1 Corporate Governance ......................................................................................................................... 9

2.2. The Relationship between Internal Auditing and Financial Performance ........................................... 14

2.2.1 Internal Auditing ................................................................................................................................ 14

2.3 The Factor Structure of corporate governance, internal audit and Financial Performance ................... 17

2.4 Agency Theory…………………………………………………………………………………………………………………………………30

ix

2.5 Stewardship Theory………………………………………………………………………………………………………..……….……..31

CHAPTER THREE .................................................................................................................................... 21

METHODOLOGY ..................................................................................................................................... 21

3.0 Introduction ........................................................................................................................................... 21

3.1. Research design ................................................................................................................................... 21

3.2 Study population ................................................................................................................................... 21

3.3 Sample size ........................................................................................................................................... 21

3.4 Sampling technique ............................................................................................................................... 22

3.5 Data Source ........................................................................................................................................... 22

3.5.1 Primary data ....................................................................................................................................... 22

3.5.2 Secondary data ................................................................................................................................... 23

3.6 Data collection methods ........................................................................................................................ 23

3.6.1 Questionnaire ..................................................................................................................................... 23

3.7 Measurement of Variables .................................................................................................................... 23

3.8 Validity and Reliability of Research Instruments ................................................................................. 23

3.9 Data Processing and Data Analysis ...................................................................................................... 24

3.10 Limitation of the study ........................................................................................................................ 24

CHAPTER FOUR ....................................................................................................................................... 26

DATA PRESENTATION, ANALYSIS AND INTERPRETATION ........................................................ 26

4.0 Introduction ........................................................................................................................................... 26

4.1 Demographic Characteristics of Respondents ...................................................................................... 26

4.2 The Relationship between Corporate Governance and Financial Performance .................................... 28

4.3 The Relationship between Internal Audit and Financial Performance of Selected Private Commercial

Banks in Ethiopia ........................................................................................................................................ 29

4.4 The Factor Structure of corporate governance, Internal Audit, and Financial Performance ................ 30

CHAPTER FIVE ........................................................................................................................................ 34

DISCUSSION OF FINDINGS ................................................................................................................... 34

5.0 Introduction ........................................................................................................................................... 34

5.1 Demographic Profile of the Respondents ............................................................................................. 34

5.1.1 Gender ................................................................................................................................................ 34

5.1.2 Age ..................................................................................................................................................... 34

5.1.3 Educational Level .............................................................................................................................. 34

x

5.1.4 Work experience ................................................................................................................................ 34

5.2 Discussion of Major Findings ............................................................................................................... 35

5.2.1 The Relationship Between Corporate Governance and Financial Performance of Selected Private

Commercial Banks in Ethiopia ................................................................................................................... 35

5.2.2 The Relationship between Internal Audit and Financial Performance of Selected Private

Commercial Banks in Ethiopia ................................................................................................................... 35

5.2.3 Factor Structure of Corporate Governance, Internal Audit and Financial Performance .................... 35

5.2.3.1 Corporate Governance .................................................................................................................... 35

5.2.3.2 Internal audit ................................................................................................................................... 36

5.2.3.3 Financial Performance .................................................................................................................... 36

CHAPTER SIX ........................................................................................................................................... 38

CONCLUSION AND RECOMMENDATIONS ........................................................................................ 38

6.0 Introduction ........................................................................................................................................... 38

6.1 Conclusion ............................................................................................................................................ 38

5.2 Recommendations ................................................................................................................................. 38

6.2.1 The Relationship Between Corporate Governance and Financial Performance of Selected Private

Commercial Banks in Ethiopia ................................................................................................................... 38

6.2.2 The Relationship between Internal Audit and Financial Performance of Selected Private

Commercial Banks in Ethiopia ................................................................................................................... 39

6.2.3 The Factor Structure of Corporate Governance, Internal Audit and Financial Performance of

Selected Private Banks in Ethiopia………………………………………………………………………………………………………...48

6.3 Areas for Further Research ................................................................................................................... 39

References ................................................................................................................................................... 40

Appendix I: Research Instrument ............................................................................................................... 44

xi

LIST OF TABLES

Tables Pages

3.1 Sample size of the respondents 32

3.2 Reliability Analysis showing Cronbach‟s Alpha Coefficients for Reliability

of Instruments

34

4.1 Relationship between Corporate Governance and Financial Performance 39

4.2 Prediction of financial performance 39

4.3 Relationship between Internal Audit and Financial Performance 39

4.4 Prediction of Financial Performance 40

4.5 Factor Analysis of Corporate Governance 40

4.6 Factor Analysis for Internal Audit 41

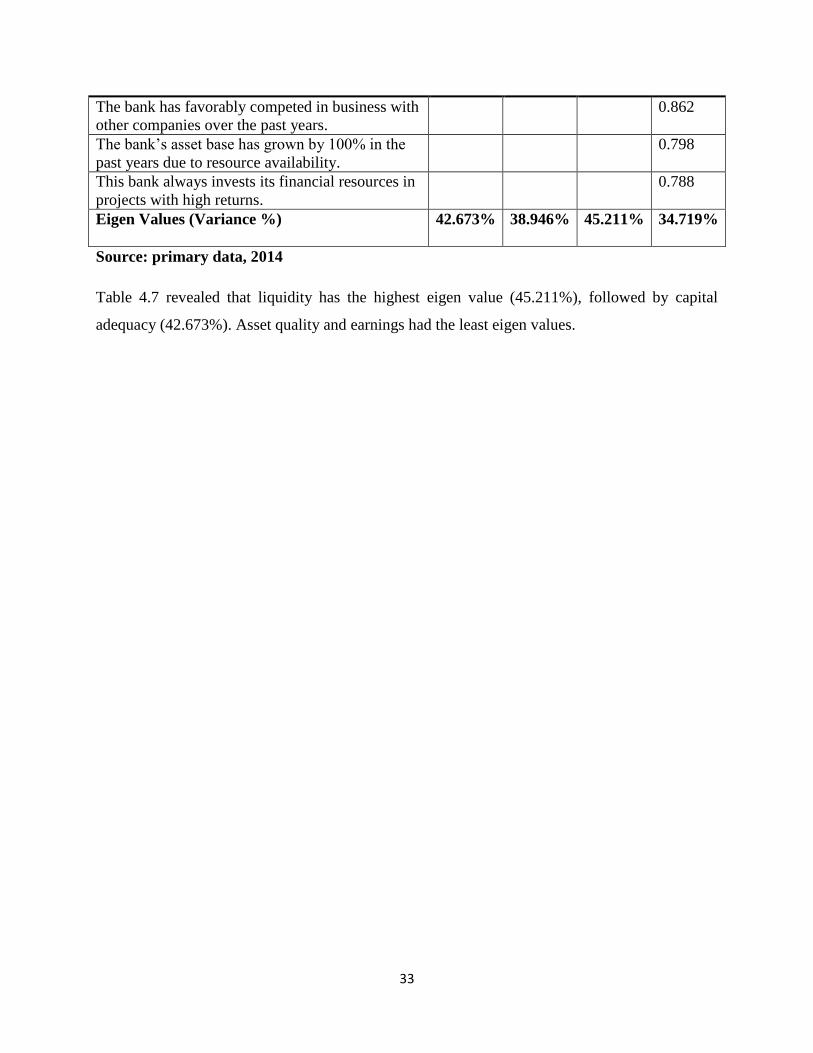

4.7 Factor Analysis of Financial Performance 42

xii

LIST OF FIGURES

Figures Pages

2.1 Conceptual framework 20

4.1 Gender of the Respondents 36

4.2 Age of the respondents 37

4.3 Highest Level of Education of the Respondents 37

4.4 Working experience of the respondents 38

xiii

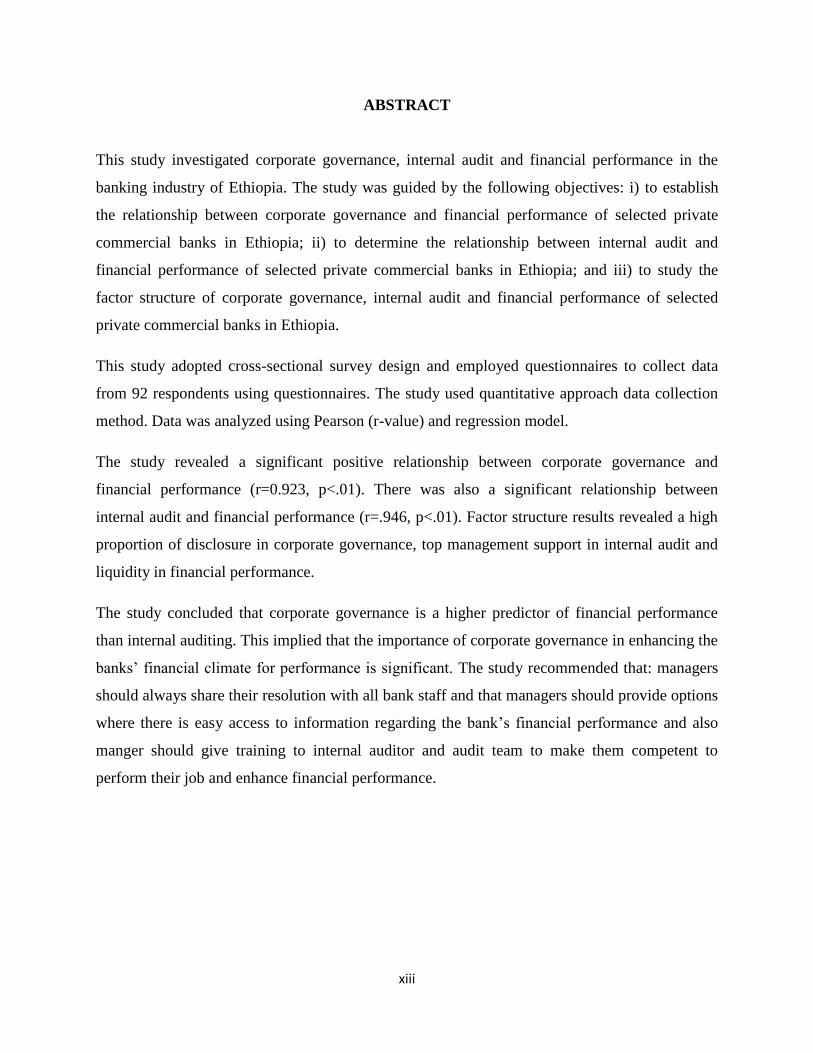

ABSTRACT

This study investigated corporate governance, internal audit and financial performance in the

banking industry of Ethiopia. The study was guided by the following objectives: i) to establish

the relationship between corporate governance and financial performance of selected private

commercial banks in Ethiopia; ii) to determine the relationship between internal audit and

financial performance of selected private commercial banks in Ethiopia; and iii) to study the

factor structure of corporate governance, internal audit and financial performance of selected

private commercial banks in Ethiopia.

This study adopted cross-sectional survey design and employed questionnaires to collect data

from 92 respondents using questionnaires. The study used quantitative approach data collection

method. Data was analyzed using Pearson (r-value) and regression model.

The study revealed a significant positive relationship between corporate governance and

financial performance (r=0.923, p<.01). There was also a significant relationship between

internal audit and financial performance (r=.946, p<.01). Factor structure results revealed a high

proportion of disclosure in corporate governance, top management support in internal audit and

liquidity in financial performance.

The study concluded that corporate governance is a higher predictor of financial performance

than internal auditing. This implied that the importance of corporate governance in enhancing the

banks‟ financial climate for performance is significant. The study recommended that: managers

should always share their resolution with all bank staff and that managers should provide options

where there is easy access to information regarding the bank‟s financial performance and also

manger should give training to internal auditor and audit team to make them competent to

perform their job and enhance financial performance.

CHAPTER ONE

INTRODUCTION AND BACK GROUND TO THE STUDY

1.0 Introduction

This chapter presents the introduction, background of the study, problem statement, purpose of

the study, general and specific objectives, research questions, scope of the study, significance of

the study and the conceptual frame work.

Currently, the banking sector in Ethiopia is fragile state. It is small, relatively undeveloped,

closed and characterized by a large share of state ownership. The state- owned commercial banks

account for nearly two-thirds of the banking sector assets. Such extensive state presence in the

banking sector coupled with total state ownership of land and telecommunications, as well as

majority government ownership in many sectors of the economy have serious ramifications for

private sector development in Ethiopia. The government continues to implement repressive

policies that negatively impact the performance of money and foreign exchange markets and

weaken private commercial banks. In addition to controlling interest rates on deposits, the

government interferes with the credit allocation decisions of private banks. Credit is often

rationed in favor of larger and more established businesses.

In fact, the World Bank‟s assessment demonstrates that state-owned enterprises have much

better access to credit than private businesses (World Bank, June 2009). The state-owned

Development Bank of Ethiopia only lends to support the government‟s industrial development

initiatives, selectively providing capital to firms in sectors the government wants to promote.

Moreover, the National Bank issued a directive on April 6, 2011 ordering private commercial

banks to buy government bonds worth 27 percent of the loan disbursements they have made

since July, 2010. This measure was set to earn 3 percent interest while the deposit rates set by the

National Bank stand at 5 percent (Ethiopian Bank, July, 2010).

Proclamation No. 84/1994 that allowed the private sector to engage in the banking business

marked the beginning of a new era in Ethiopian banking. Following this proclamation Ethiopia

witnessed a proliferation of domestic private banks. The industry comprises one state owned

development bank and 19 commercial banks, two of which are state-owned, including the

2

dominant Commercial Bank of Ethiopia (CBE), with assets accounting for approximately 70

percent of the industry‟s total holdings.2 The banking industry‟s nonperforming loan ratio is

commendably low, and profitability is good, but the dominance of public sector banking

certainly restricts financial intermediation and economic growth. It contrasts with regional and

international peer countries where banking industries have a much higher share of private sector

and foreign participation. This study will investigate the relationship between corporate

governance, internal auditing, and financial performance of commercial banks in Ethiopia.

1.1 Background to the study

Corporate governance refers to all issues related to ownership and control of corporate property,

the rights of shareholders and management, powers and responsibilities of the Board of

Directors, disclosure and transparency of corporate information, the protection of interests of

stakeholders that are not shareholders, enforcement of rights, etc (Fekadu, 2010). Corporate

governance systems depend upon a set of institutions such as laws, regulations, contract

enforcements and norms that create self-governing firms as the central element of a competitive

market economy (Fernando, 1997). These institutions ensure that the internal corporate

governance procedures adopted by firms are enforced and they render management responsible

to owners and other stakeholders. The definition of „corporate governance‟ is not provided under

the Ethiopian company law. For the purpose of this study, it is thus important to adopt a working

definition for corporate governance as a system of rules and institutions that determine the

control and direction of a company and that define relations among the company‟s primary

participants including board of directors, managers, shareholders and other stakeholders

(Fernando, 2006). This combines the narrow and broad definitions and it considers corporate

governance as a system of rules and institutions which determine the control and direction of a

company. It recognizes not only shareholders but also stakeholders that should be involved in the

governance of share companies.

Internal Audit is defined by the institute of internal auditors as “independent appraisal function

established within an organization to examine and evaluate its activities as a service to the

organization. According to Okezie (2004), the main objectives of internal auditing are “to assist

management in the effective discharge of their responsibilities by furnishing them with the

analysis, appraisal, recommendation and pertinent comments concerning the activities

3

reviewed”. Internal auditing (IA) serves as an important link in the business and financial

reporting processes of corporations and not-for-profit providers (Reynolds, 2000). Internal

auditors play a key role in monitoring a company‟s risk profile and identifying areas to improve

risk management (Goodwin-Stewart and Kent, 2006). The aim of internal auditing is to improve

organizational efficiency and effectiveness through constructive criticism. IA has four main

components: (1) verification of written records; (2) analysis of policy; (3) evaluation of the logic

and completeness of procedures, internal services and staffing to assure they are efficient and

appropriate for the organization‟s policies; and (4) reporting recommendations for improvements

to management (Eden and Moriah, 1996).This study investigated the internal audit practices in

selected private commercial banks in Ethiopia.

Financial performance is the measure of the extent to which objectives of an organization are

achieved in relation to defined standards and targets for each objective (Monaghan, 2000; Dess

and Shaw, 2001).According to (Adams and Buckle, 2003), financial performance is the level of

performance of a business over a specified period of time, expressed in terms of overall profits

and losses during that time. Evaluating the financial performance of a business allows decision-

makers to judge the results of business strategies and activities in objective monetary terms.

According to Panwala (2009), the ability of an organization to analyze its financial position is

essential for improving its competitive position in the marketplace. Through a careful analysis of

its financial performance, the organization can identify opportunities to improve performance of

the department, unit or organizational level. The financial performances of selected private

commercial Ethiopian banks were measured in terms of capital adequacy, asset quality, earnings,

and liquidity.

1.2 Problem Statement

Some scholarly works have been published recently on company law in general and corporate

governance in particular by Ethiopian academics. Minga (2008) observes that the status of

corporate governance in Ethiopia is disappointing and notes that “the Commercial Code of 1960

does not provide adequate legislative response to complex governance issues of the day, and the

new draft corporate law has not yet been finalized;” and he further states that “key international

conventions, codes and standards are not ratified or adequately incorporated in the

4

Proclamations” and that “the Decrees and Directives lack coherence and foresights, and at times

suffer from poor drafting (Minga, 2008).”

Fekadu (2010) underlines the growing separation between ownership and control in Ethiopia,

and he submits some empirical evidence in this regard. Relying on the data and literature on

corporate governance, he shows the deficiency of the Commercial Code in protecting the rights

of minority shareholders in the context of publicly held companies. The state owned commercial

banks has used tools such as low interest rates, currency appreciation, and targeted usage of

credit and foreign exchange to support public enterprises and drive economic growth. This

strategy has succeeded but led to the neglect of private sector development, a low national

savings rate, a loss of international competitiveness, and an increase in the trade deficit.

In regard to financial performance, the private commercial banks in Ethiopia are currently facing

challenges regarding their finances with most of them reported to have made financial losses in

the past two years (Ethiopia Banking Sector Review, 2012). According to the International

Monetary Fund (IMF) (2013) report, most commercials banks did not meet their 2011-2012

budget goals. The banks invested heavily in promoting new products but not much profit was

realized out of these efforts.

The report from IMF (2013) further revealed that out of the 14 private commercial banks in

Ethiopia, only 5 were able to make profit increment of at least 5.2% while the rest made profit

increment of less than 3.0% in their annual financial reports. Furthermore, a report from Access

Capital Research (2012) revealed that by the end of 2012, only 4 commercial banks in Ethiopia

had the ability to meet their long-term fixed expenses and accomplish expansion. This therefore

shows how poorly the private commercial banks have been performing for the past two years.

This sudden poor financial performance could be due to the repressive government policies that

the government is imposing on private commercial banks or because incompetent directors as

cited by (Minga, 2008)”. However this research attempted to further expound and investigate if

internal auditing and corporate governance are linked to the poor financial performance of the

private commercial banks in Ethiopia.

5

1.3 Purpose of the Study

The purpose of this study was to establish the relationship between corporate governance,

internal auditing, and financial performance of selected commercial banks in Ethiopia.

1.4 Objectives of the Study

i) To establish the relationship between corporate governance and financial performance of

selected private commercial banks in Ethiopia.

ii) To determine the relationship between internal audit and financial performance of

selected private commercial banks in Ethiopia.

iii) To study the factor structure of corporate governance, internal audit and financial

performance of selected private commercial banks in Ethiopia.

1.5 Research Questions

i) What is the relationship between Corporate Governance and financial performance of

selected private commercial banks in Ethiopia?

ii) What is the relationship between internal audit and financial performance of selected

private commercial banks in Ethiopia?

iii) What is the factor structure of corporate governance, internal auditing and financial

performance of selected private commercial banks in Ethiopia?

1.6 Scope of the Study

1.6.1 Geographical Scope

This study was carried out in Ethiopia. This country is located in the Horn of Africa. It is

bordered by Eritrea to the north and northeast, Djibouti and Somalia to the east, Sudan and South

Sudan to the west, and Kenya to the south. Specifically the study will be carried out in Addis

Ababa-the capital of Ethiopia.

6

1.6.2 Content Scope

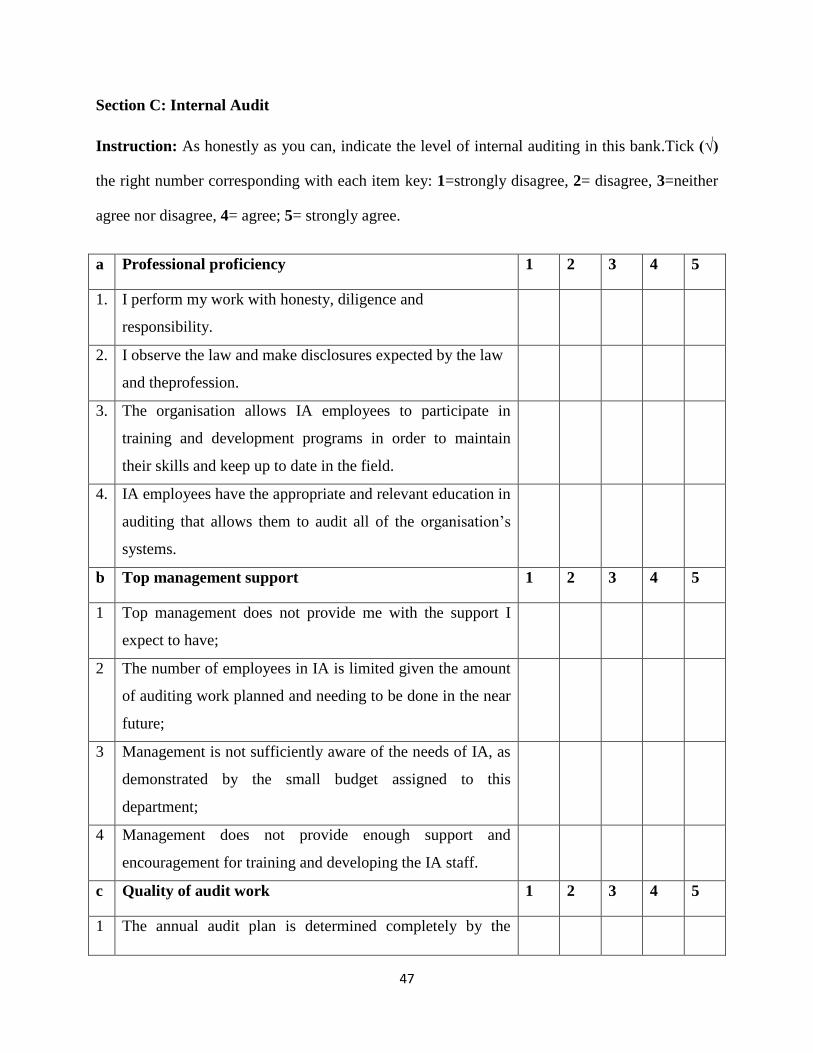

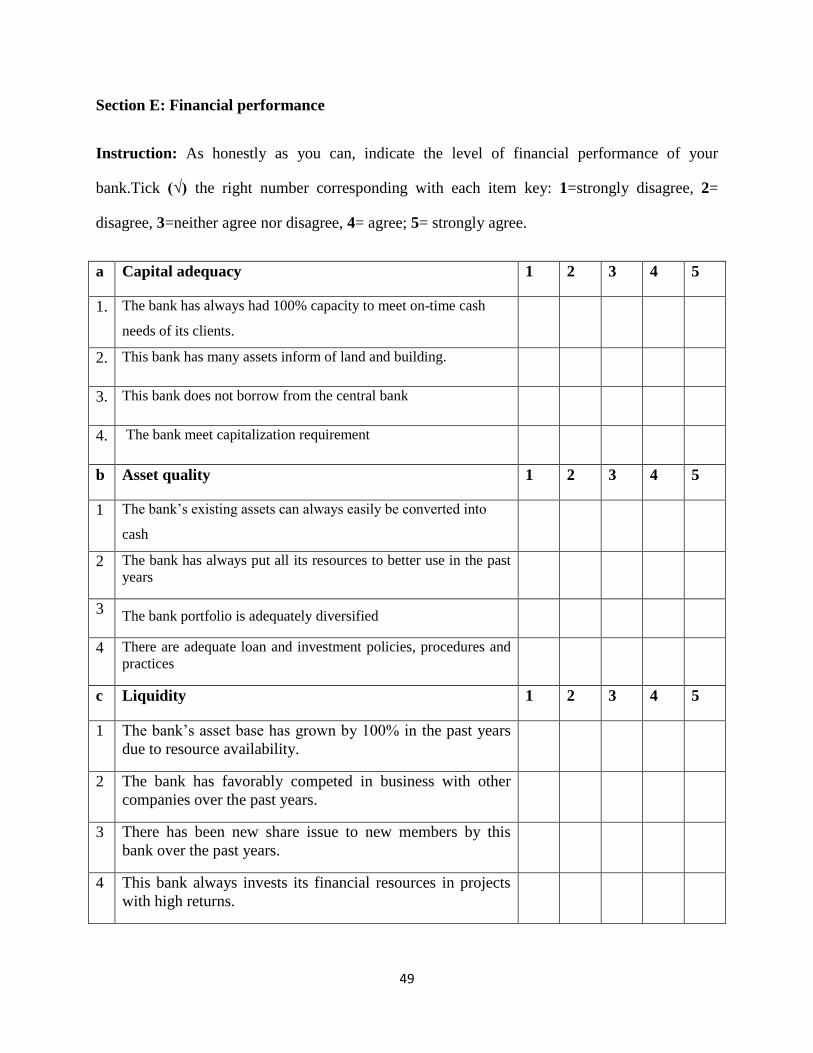

Corporate Governance was measured in terms of transparency, disclosure and trust. Internal

Audit was measured in terms of professional proficiency, management support, quality of audit

work and organizational independence. Financial performance was measured in terms of capital

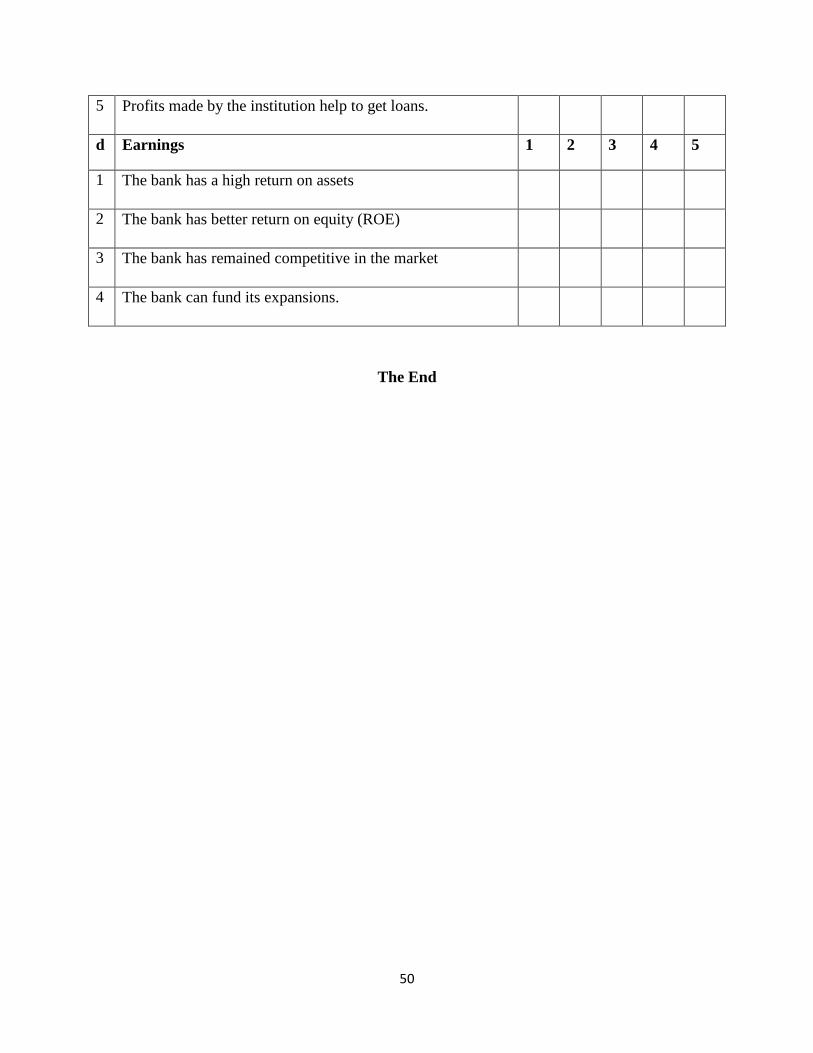

adequacy, asset quality, earnings and liquidity.

1.6.3 Time Scope

This study looked at the financial performance of the selected commercial banks for a period of 3

years, that is, from 2011-2013. The researcher investigated if the results in the financial

performance are influenced by corporate governance or internal auditing or both.

1.7 Significance of the study

i. It is hoped that the study findings will help commercial banks in formulating

appropriate internal auditing that will help in enhancing better financial performance.

ii. The study results will be useful to management, board of governors, and all stakeholders,

specifically they will use the findings from the study to redesign policies aimed at

improving on the levels of financial performance of their institutions.

iii. It is also assumed that the study findings will be an addition to the already existing

knowledge especially in the field of internal auditing, corporate governance and

financial performance of commercial banks in Ethiopia.

iv. Future researchers will use the findings of this study to carry out a related study.

7

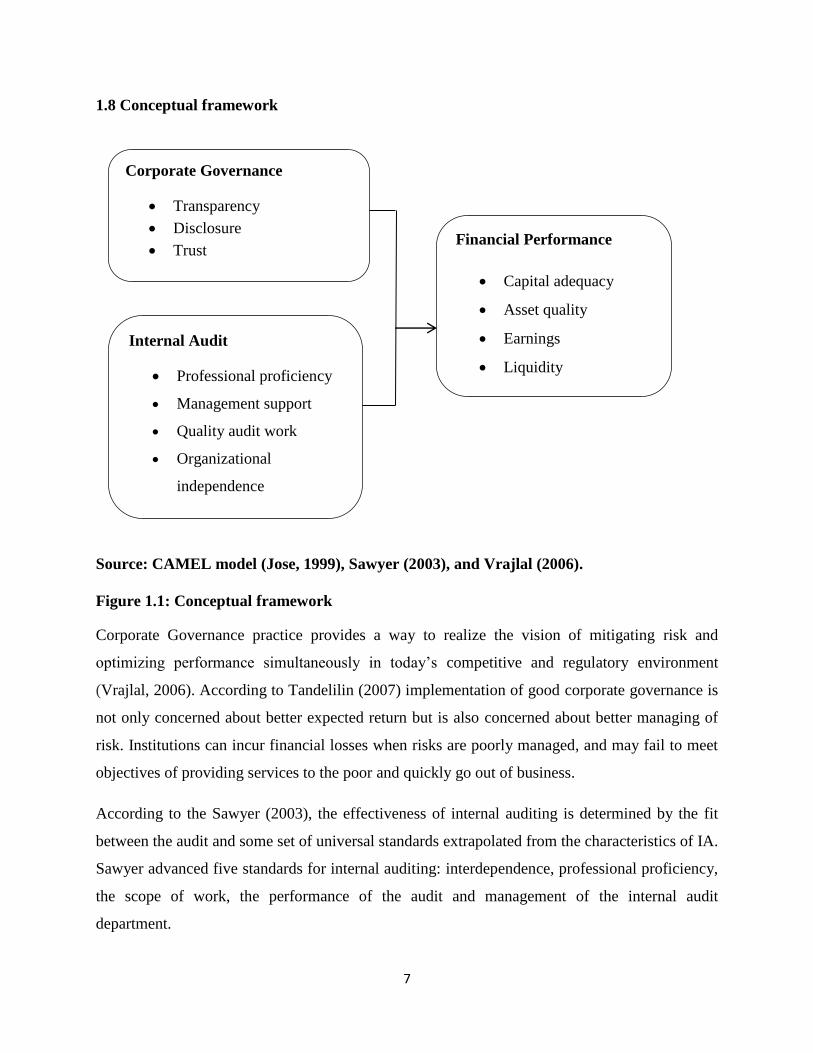

1.8 Conceptual framework

Source: CAMEL model (Jose, 1999), Sawyer (2003), and Vrajlal (2006).

Figure 1.1: Conceptual framework

Corporate Governance practice provides a way to realize the vision of mitigating risk and

optimizing performance simultaneously in today‟s competitive and regulatory environment

(Vrajlal, 2006). According to Tandelilin (2007) implementation of good corporate governance is

not only concerned about better expected return but is also concerned about better managing of

risk. Institutions can incur financial losses when risks are poorly managed, and may fail to meet

objectives of providing services to the poor and quickly go out of business.

According to the Sawyer (2003), the effectiveness of internal auditing is determined by the fit

between the audit and some set of universal standards extrapolated from the characteristics of IA.

Sawyer advanced five standards for internal auditing: interdependence, professional proficiency,

the scope of work, the performance of the audit and management of the internal audit

department.

Corporate Governance

Transparency

Disclosure

Trust

Internal Audit

Professional proficiency

Management support

Quality audit work

Organizational

independence

Financial Performance

Capital adequacy

Asset quality

Earnings

Liquidity

8

Some useful measures of financial performance which is the alternative term as financial

soundness are coined into what is referred to as CAMEL model (Jose, 1999). The acronym

"CAMEL" refers to the five components of a bank's condition that are assessed: Capital

adequacy, Asset quality, Management, Earnings, and Liquidity. A sixth component, a bank's

Sensitivity to market risk was added in 1997; hence the acronym was changed to CAMELS.

9

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

This chapter presents a review of the literature on the topic of corporate governance, internal

audit and financial performance from previous studies and the gap to be closed by this study. The

chapter is organized as to determine the relationship between variables that is internal audit,

corporate governance and financial performance, a review of theories in relation to internal

auditing and corporate governance, and a review of the empirical studies.

2.1 The Relationship between Corporate governance and Financial Performance

2.1.1 Corporate Governance

Corporate governance is about building credibility, ensuring transparency and accountability as

well as maintaining an effective channel of information disclosure that would foster good

corporate performance. It is also about how to build trust and sustain confidence among the

various interest groups that make up an organisations. Indeed the outcome of a survey by

Mckinsey in collaboration with the World Bank in June 2000 attested to the strong link between

corporate governance and stakeholder confidence (Mark, 2000).

Given that a study has already been carried out on the extent to which board composition affects

team processes (orientation communication feedbacks, coordination, leadership and monitoring),

board effectiveness and performance of the selected financial institutions in Ethiopia (Mihiret,

2002), the researcher picked three basic tenets of Corporate Governance; Transparency,

Disclosure and Trust in relation to commercial bank financial performance in Ethiopia, these

tenets fall under the accounting field. The constructs/tenets are reviewed in the following

sections.

Transparency: Transparency is integral to corporate governance, higher transparency reduces the

information asymmetry between a firm‟s management and financial stakeholder‟s (equity and

bondholders), mitigating the agency problem in corporate governance (Sandeep et al, 2002). The

concept of Bank transparency is broad in scope; it refers to the quality and quantity of public

information on a bank‟s risk profile and to the timing of its disclosure, including the banks past

and current decisions and actions as well as its plans for the future. The transparency of the

10

banking sector as a whole also includes public information on bank regulations and on safety net

operations of the central bank (Rosengren, 1998).Weak transparency makes banks‟ asset risks

opaque. Stock market participants including professional analysists such as Moody‟s encounter

difficulties in measuring banks credit worthiness and risk exposures (Rosengren, 2000). Ball

(2001) argues that timely incorporation of economic losses in the published financial statements

(that is, conservatism) increases the effectiveness of corporate governance, compensation

systems, and debt agreements in motivating and monitoring managers. For instance, improved

governance can manifest in a reduction of the private benefits that managers can extract from the

company or in a reduction of the legal and auditing costs that shareholders must bear to prevent

managerial opportunism.

Disclosure: Given the recent corporate scandals (US Based; Enron, WorldCom… (Heidi and

Marleen (2003) Greenland Bank Ltd, ICB. (Japheth (2001) restoring public trust is at the top of

the agenda of today‟s business leaders. Greater information provision (disclosure) on the

company‟s capital and control structures – can be an important means to achieve this goal. High

quality and relevant information is crucial for exercise of governance powers. Full Disclosure

seeks to avoid financial statements fraud (Beasley et al, 2000). Prior studies have concentrated

on disclosure of items such as management earnings forecasts (Johnson et al, 2001) or interim

earnings (Leftwich and Zimmerman 1981), or have examined a very general disclosure index of

financial and/or non - financial items (Chow and Wong –Borren, 1987). The CIFAR Index (i.e. a

disclosure index created by the Center for Intentional Financial Analysis and Research (CIFAR)

rates annual reports on the inclusion or omission of about 90 (rather traditional and mandatory

financial) items from the following categories; general information, income statements, balance

sheet, funds flow statement, accounting standards, stock data and special items (Laporta et al,

1998).

Trust: Trust means many things. Everyone knows intuitively what it is to trust; yet articulating a

precise definition is not a simple matter (Wayne & Megan 2002). Trust is difficult to define

because it is so complex, in fact, Hosmer (1995) has observed. “ There appears to be widespread

agreement on the importance of trust in human conduct, but unfortunately there also appears to

be an equally widespread lack of agreement on a suitable definition of the construct”.Trust is a

multifaceted construct, which may have different bases and phases depending on the context; it

11

is also a dynamic construct that can change over the course of arelationship (Wayne and Megan,

2002).There are at least five facets of trust that can be gleaned from the literature on trust (998;

Tschannen-Moran & Hoy 2001). Benevolence, reliability competence, honesty and openness are

all elements of trust (Wayne & Megan 2002).

Benevolence perhaps the most common facet of trust is a sense of benevolence -confidence that

one‟s wellbeing or something one cares about will be protected and notharmed by the trusted

party (Mishra 1996).

Reliability at its most basic level trust has to do with predictability that is, consistency of

behaviour and knowing what to expect from others (Hosmer1995). In and of itself, however,

predictability is insufficient for trust. We can expect a person to be invariably late, consistently

malicious, inauthentic, or dishonest when our well-being is diminished or damaged in a

predictable way, expectations may be met, but the sense in which we trust the other person or

group is weak.

Competence: Good intentions are not always enough when a person is dependent on another but

some level of skill is involved in fulfilling an expectation an individual who means well may

nonetheless not be trusted (Mishra, 1996).

Competence: is the ability to perform as expected and according to standards appropriate to task

at hand, many organizational tasks rely on competence. Honesty is the person‟s character,

integrity and authenticity. Rotter (1967) defined trust as “the expectancy that the word, promise,

verbal or written statement of another individual or group can be relied upon”. Statements are

truthful when they confirm to “what really happened “from that perspective and when

commitments made about future actions are kept. A correspondence between a person‟s

statements and deeds demonstrates integrity.

Openness: Openness is the extent to which relevant information is shared; it is process by which

individuals make themselves vulnerable to others. The information shared maybe strictly about

organizational matters or it may be personal information, but it is agiving of oneself (Mishra,

1996) such openness signals reciprocal trust a confidence that neither the information nor the

individual will be exploited and recipients can feel the same confidence in return. Individuals

12

who are unwilling to extend trust through openness end up isolated (Kramer, Brewer & Hanna,

1996).

Transparency, disclosure and trust, which constitute the integral part of corporate governance,

can provide pressure for improved financial performance. Financial performance, present and

prospective is a benchmark for investment. The Mckinsey Quarterly surveys suggest that

institutional investors will pay as much as 28% more for the shares of well governed companies

in emerging markets (Mark, 2000). According to the corporate governance survey 2002, carried

out by the Kuala Lumpur stock exchange and accounting firm Price Water House Coopers

(PWC), the majority of investors in Malaysia are prepared to pay 20% premium for companies

with superior corporate governance practices.

2.1.2 Financial performance

Financial soundness is a situation where depositor‟s funds are safe in a stable banking system.

The financial soundness of a financial institution may be strong or unsatisfactory varying from

one bank to another (BOU, 2002). External factors such as deregulation; lack of information

among bank customers; homogeneity of the bank business, connections among banks do cause

bank failure. Some useful measures of financial performance which is the alternative term as

financial soundness are coined into what is referred to as CAMEL. The acronym "CAMEL"

refers to the five components of a bank's condition: Capital adequacy, Asset quality,

Management, Earnings, and Liquidity.

Capital Adequacy: This ultimately determines how well financial institutions can cope with

shocks to their balance sheets. The bank monitors the adequacy of its capital using ratios

established by The Bank for International Settlements. Capital adequacy in commercial banks is

measured in relation to the relative risk weights assigned to the different category of assets held

both on and off the balance sheet items (Bank of Ethiopia, 2002).

Asset Quality: The solvency of financial institutions typically is at risk when their assets become

impaired, so it is important to monitor indicators of the quality of their assets interms of

overexposure to specific risks trends in non- performing loans, and the health and profitability of

bank borrowers especially the corporate sector. Credit risk is in herentin lending, which is the

major banking business. It arises when a borrower defaults on the loan repayment agreement. A

13

financial institution whose borrowers default on their repayments may face cash flow problems,

which eventually affect its liquidity position. Ultimately, this negatively impacts on the

profitability and capital through extra specific provisions for bad debts (Bank of Ethiopia, 2002).

Earnings: The continued viability of a bank depends on its ability to earn an adequate return on

its assets and capital. Good earnings performance enables a bank to fund its expansion, remain

competitive in the market and replenish and /or increase its capital (Bank of Ethiopia, 2002). A

number of authors have argued that, banks that must survive need: Higher Return on Assets

(ROA)., better return on net worth/Equity (ROE),sound capital base i.e. the Capital Adequacy

Ratio (CAR), adoption of corporate governance ensuring transparency to stakeholders that is

equity holders, regulators and the public.

Liquidity: Initially solvent financial institutions may be driven toward closure by poor

management of short-term liquidity. Indicators should cover funding sources and capture large

maturity mismatches. An unmatched position potentially enhances profitability but also increases

the risk of losses (The Ethiopia Banker, 2001). The “M” represents Management, given that this

paper is hinged on financial performance, the management component in not considered in the

measure.

Many empirical studies have documented a positive and significant relationship between

corporate governance and firm performance(Chen et al. 2008; Chalhoub 2009; Sueyoshi et al.

2010; Mehdi 2007; Brown and Caylor 2009).Other than these empirical works, surveys have

been conducted by various organisations to evaluate the relationship between the two issues:

corporate governance and financial performance. A study performed by Credit Lyonnais

Securities Asia (CLSA) in 2002 indicates the existence of the positive link between good

governance and indicators of financial performance on almost500 developing economy

companies. In a prior study conducted in 2001, CLSA generated an index for 495 firms from 25

emerging markets to find out their corporate governance rankings. This report demonstrated that

firms that rank high in this index display better operating and market performance.

A study by Sekhar (2012) examined the impact of corporate governance variables on firms‟

financial performance. Influence of corporate governance variables such as CEO duality,

Chairman of Audit Committee, Proportion of Non-executive Directors, Concentrated Ownership

14

structure, Institutional Investors, Gearing Ratio on firms‟ financial performance“ Return on

Assets” was researched using the firms traded in Bahrain Bourse. The study found that corporate

governance variables do influence firms‟ performance. CEO duality, proportion of non-executive

directors and leverage has negative influence and board member as chair of audit committee,

proportion of institutional ownership has positive influence on firms‟ financial performance.

DR.Guruswamy (2008) carried a study on the relationship between the core principles of

corporate governance and financial performance in commercial banks of Ethiopia. The findings

indicated that Corporate Governance predicts 34.5 % of the variance in the general financial

performance of Commercial banks in Ethiopia. However the significant contributors to financial

performance include openness and reliability. Openness and Reliability are measures of trust. On

the other hand credit risk as a measure of disclosure had a negative relationship with financial

performance. It is obvious that trust has a significant impact on financial performance; given that

transparency and disclosure boosts the trustworthiness of commercial banks.

2.2. The Relationship between Internal Auditing and Financial Performance

2.2.1 Internal Auditing

Internal auditing is an independent, objective assurance and consulting activity designed to add

value and improve an organization's operations. It helps an organization accomplish its

objectives by bringing a systematic, disciplined approach to evaluate and improve the

effectiveness of risk management, control, and governance processes (IIA, 2002). Internal

auditing is a catalyst for improving an organization's governance, risk management and

management controls by providing insight and recommendations based on analyses and

assessments of data and business processes. With commitment to integrity and accountability,

internal auditing provides value to governing bodies and senior management as an objective

source of independent advice (Sawyer, 2003).

According to Brown (2008), internal auditing is the examination, monitoring and analysis of

activities related to a company's operation, including its business structure, employee behavior

and information systems. An internal audit is designed to review what a company is doing in

15

order to identify potential threats to the organization's health and profitability, and to make

suggestions for mitigating the risk associated with those threats in order to minimize costs.

Internal auditing may also involve conducting proactive fraud audits to identify potentially

fraudulent acts; participating in fraud investigations under the direction of fraud investigation

professionals, and conducting post investigation fraud audits to identify control breakdowns and

establish financial loss (Frigo, 2002).

Professional proficiency: Appropriate staffing of an internal audit department and good

management of that staff are keys to the effective operation of an internal audit. An audit

requires a professional staff that collectively has the necessary education, training, experience

and professional qualifications to conduct the full range of audits required by its mandate (Al-

Twaijry, Brierley and Gwillian 2003). Auditors must comply with minimum continuing

education requirements and professional standards published by their relevant professional

organisations and the IIA (2008). Bou-Raad (2000) argued that auditors must have a high level

of education in order to be considered a human resource. The diversity of skills required,

according to Bou-Raad, represents a major challenge to professional bodies, tertiary institutions

and management.

Management support: The management literature offers ample evidence for the key role of top

management support in the success of almost all programs and processes within an organisation.

Fernandez and Rainey (2006) argued, based on a thorough literature review, that top

management support and commitment to change play a crucial role in organisational renewal, as

senior managers can mobilise the critical mass needed to follow through on efforts launched by

one or two visionary thinkers. Given this, it is not surprising that management acceptance of, and

support for, the internal audit function has long been seen as critical to the success of that

function (Sawyer, 2003). Several recent studies have demonstrated that support for internal

auditing by top management is an important determinant of its effectiveness (Jill 1998; Schwartz,

Dunfee and Kline 2005). Funding, of course, is an important measure of such support: IA

departments must have the resources needed to hire the right number of high-quality staff, to

keep up-to-date in training and development, to acquire and maintain physical resources like

computers, and so on.

16

Quality audit work: Standards for audits and audit-related services are published by the IIA

(2008) and include attribute, performance and implementation standards. In general, formal

auditing standards recognize that internal auditors also provide services regarding information

other than financial reports. They require auditors to carry out their role objectively and in

compliance with accepted criteria for professional practice, such that internal audit activity will

evaluate and contribute to the improvement of risk management, control and governance using a

systematic and disciplined approach. This is important not only for compliance with legal

requirements, but because the scope of an auditor‟s duties could involve the evaluation of areas

in which a high level of judgment is involved, and audit reports may have a direct impact on the

decisions or the course of action adopted by management (Bou-Raad 2000). It can thus be argued

that greater quality of IA work – understood in terms of compliance with formal standards, as

well as a high level of efficiency in the audit‟s planning and execution – will improve the audit‟s

effectiveness.

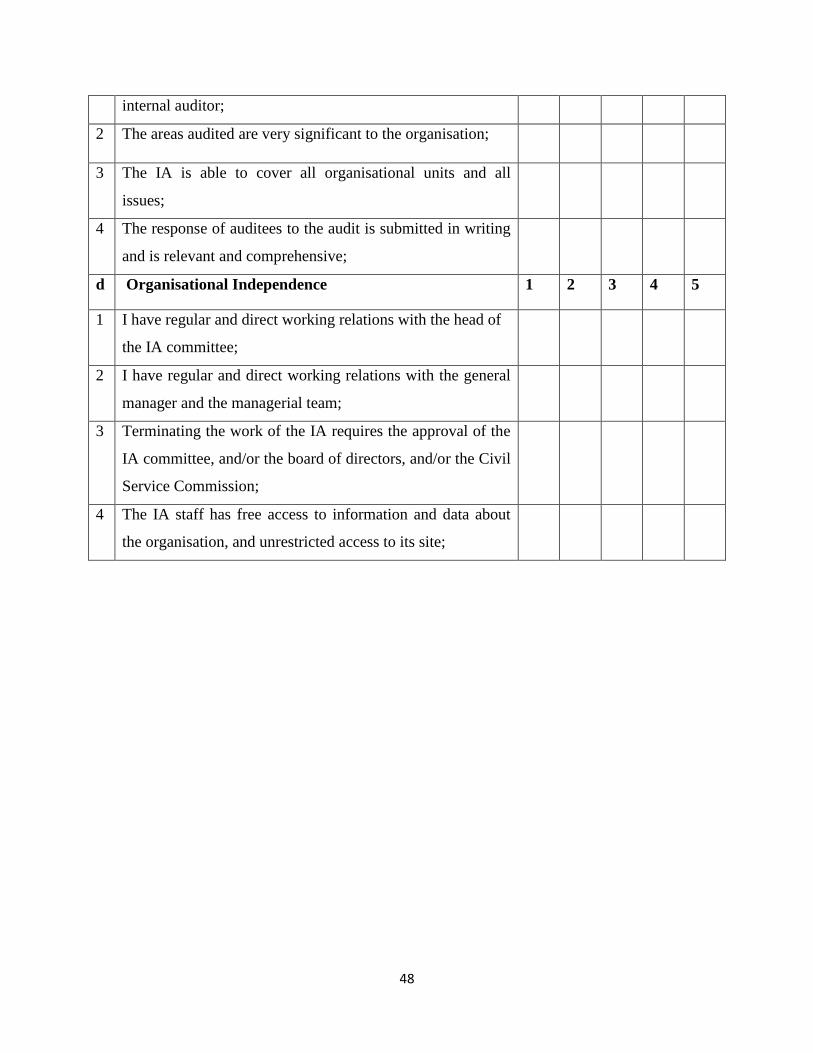

Organizational independence: The role of IA in organisations is complex. Van Peursem

(2004) identifies strong potential for confusion in the relationship between internal auditors and

management: internal auditors are expected to aid managers in doing their jobs, and at the same

time to independently evaluate management‟s effectiveness. Internal auditors are charged with

upholding the best interests of their employer, but they may be reluctant to counter management,

regardless of the consequences. Bou-Raad (2000) argued that the strength of an IA department

must be assessed with respect to the level of independence it enjoys from management and from

operating responsibilities. The IIA, the American Institute of Certified Public Accountants

(AICPA) and others have likewise identified organizational independence as crucial to the

viability of the internal audit function (Brown 2009). Auditors should be sufficiently independent

from those they are required to audit that they can both conduct their work without interference,

and – equally important – be seen to do so. Coupled with objectivity, organizational

independence contributes to the accuracy of the auditors‟ work and gives employers confidence

that they can rely on the results and the report.

A study by Nahom (2012) in Ethiopia on Internal audit function and financial performance of a

public organization established a relationship between internal audit function and financial

performance with control environment, risk assessment, control activities, information and

17

communication, monitoring and advisory services having a great impact on the financial

performance of the government enterprise. The study recommended that internal control

procedures and policies should be regularly revised at least annually and it should be ensured

that the results are communicated to the implementers.

2.3 The Factor Structure of corporate governance, internal audit and Financial

Performance

Corporate Governance has come to mean many things. Traditionally and at a fundamental level,

the concept refers to corporate decision making and control, particularly the structure of the

board and its working procedures Hermes, (2004). Jenifer, (2002) defines Corporate Governance

as a set of interlocking rules by which corporations, shareholders and management govern their

behavior. In each country, this is a combination of a legal system that sets some common

standards of governance and systems of behavior determined by firms themselves. This study

factored corporate governance in terms of transparency, disclosure and trust.

Internal auditing helps an organization accomplish its objectives by bringing a systematic,

disciplined approach to evaluate and improve the effectiveness of risk management, control and

governance processes (IIA, 2012). This study factored internal auditing using professional

proficiency, top management support, quality of audit work, organizational independence.

Financial performance is the level of performance of a business over a specified period of time,

expressed in terms of overall profits and losses during that time. In this study financial

performance was factored in terms of capital adequacy, asset quality, earnings and liquidity.

2.4 Agency Theory

Meckling and Jensen (1976) define agency relationship as a contract under which one or more

person(s) (the principal) engages another person (agent) to perform some service on their behalf

which involves delegating some decision making authority to the agent. Watts and Zimmerman

(1986) argues that agency theory in its purest form also assumes that individuals will take into

account all available information, rationally and instantly, to make decisions. Assumptions of an

efficient market can be relaxed to explain the importance of accounting practices and contracting

services. In an imperfect market where principals cannot know everything at any one point in

18

time, emphasizes the need to incur Fama (1980) proposes that separation of security ownership

and control can be

explained as an efficient form of economic organization within the “set of contracts” perspective.

He set aside the typical presumption that a corporation has owners in any meaningful sense and

the concept of the entrepreneur for the purposes of the large modern corporation. Instead the two

functions attributed to the entrepreneur, management and risk bearing were treated as naturally

separate factors within the set of contracts called a firm. He proposes that the firm is disciplined

by competition from other firms which forces the evolution of devices for efficiently monitoring

the performance of the entire team and of its individual members. In addition individual

participants in the firm and in particular its manager face both the disciplined and opportunity

provided by the markets for their services both within and outside of the firm.

Sheret and Kent (1983) and Watts (1988) suggest that internal auditing is a bonding cost borne

by agents to satisfy the principal‟s demand for accountability made by external participants

especially shareholders. The cost of internal auditing can be judged to be monitoring cost which

is incurred by the principals to protect their economic interests. Agency theory contends that

internal auditing like other intervention mechanism like financial reporting and external auditing

helps to maintain cost efficient contracting between owners and managers.

Adam (1994) uses agency theory to mark the internal audit department as an important

monitoring body that enables management to evaluate possible information asymmetry between

principal and agent. He assumes that management sees internal audit as a mechanism to

supervise external auditors and control costs. Further he questions why some companies have

internal audit while others don‟t and he assumes that more complex organizations are more

likely to have it than the less complex. It is assumed that the more information asymmetry the

greater the need for monitoring to reduce this information asymmetry resulting in a larger

internal audit function. In a large internal audit function there will be more staff representing a

more diverse range of skills and competences that will be able to reduce a greater range of

information asymmetry problems. Further the scope of the internal audit function covered would

be greater in a larger function than a small function. It is further assumed that a larger internal

audit function has a broader scope of work and is able to cover more areas where information

19

asymmetry exists. Carcello, Hermanson and Raghunandan (2005) asserts that this separation is

considered as the basic principle behind the demand for corporate governance which forms the

growing importance of internal audit monitoring role in contemporary corporate governance.

From the foregoing it is apparent that agency theory can help explain the existence of internal

audit, the nature of internal audit function and the particular approach adopted by internal

auditors to their work.

2.5 Stewardship Theory

Stewardship theory has its roots from psychology and sociology and is defined by Davis,

Schoorman and Donaldson (1997) as “a steward protects and maximizes shareholders wealth

through firm performance, because by so doing, the steward‟s utility functions are maximized”.

In this perspective, stewards are company executives and managers working for the shareholders,

protects and make profits for the shareholders. Unlike agency theory, stewardship theory stresses

not on the perspective of individualism (Donaldson and Davis, 1991), but rather on the role of

top management being as stewards, integrating their goals as part of the organization. The

stewardship perspective suggests that stewards are satisfied and motivated when organizational

success is attained.

Agyris (1973) argues that while agency theory looks at an employee or people as an economic

being, which suppresses an individual‟s own aspirations, on the other hard Donaldson and Davis

(1991) argues that stewardship theory recognizes the importance of structures that empower the

steward and offers maximum autonomy built on trust. It stresses on the position of employees or

executives to act more autonomously so that the shareholders‟ returns are maximized. Indeed,

Fama (1980) contend that executives and directors are also managing their careers in order to be

seen as effective stewards of their organization, whilst, Shleifer and Vishny (1997) claims that

managers return finance to investors to establish a good reputation so that that can re-enter the

market for future finance.

Davis et al. (1997) and Tosi et al. (2003) notes that the involvement-oriented, participative

management philosophy espoused by the stewardship theory automatically reduces the need for

20

strict internal control mechanisms to curb governance challenges and agency costs, part of which

is the involvement of internal audit in an organization.

Meckling and Jensen (1994) further states the cost incurred to curb agency problems (reducing

information asymmetries and accompanying moral hazards) is less when owners directly

participate in the management of the firm as there is a natural alignment of owner managers‟

interest with growth opportunities and risk. This alignment reduces their incentive to be

opportunistic and hence owner managed firms have little to guard against the governance

challenges.

It follows from the above that stewardship theory unlike agency theory is a complete contrast

and doesn‟t emphasize on the need to incur monitoring or agency cost which includes

establishing an internal audit function. Nevertheless Donaldson and Davis (1991) further notes

that returns are improved by having both of these theories combined rather than separated which

implies that management must strike a balance.

21

CHAPTER THREE

METHODOLOGY

3.0 Introduction

This chapter presents the research design and methodology that was used. They are presented

under the following major sub headings: research design, study population, sample size and

sample design, data source, measurement of variables, validity and reliability of research

instrument, data process and analysis and limitations.

3.1. Research design

The research design was cross sectional survey design and the researcher used quantitative

approaches. Quantitative approach was largely used in the research because of necessity to arrive

at conclusions about the relationships of the study.

3.2 Study population

The study population comprised of a total of 92 participants selected from seven private

commercial banks scattered in Addis Ababa city. The researcher was basically interested in the

General Manager, Finance Manager, Shareholders, Accountant and Internal Auditors of those

banks as respondents. These respondents were preferred because they are well informed of the

subject under study.

3.3 Sample size

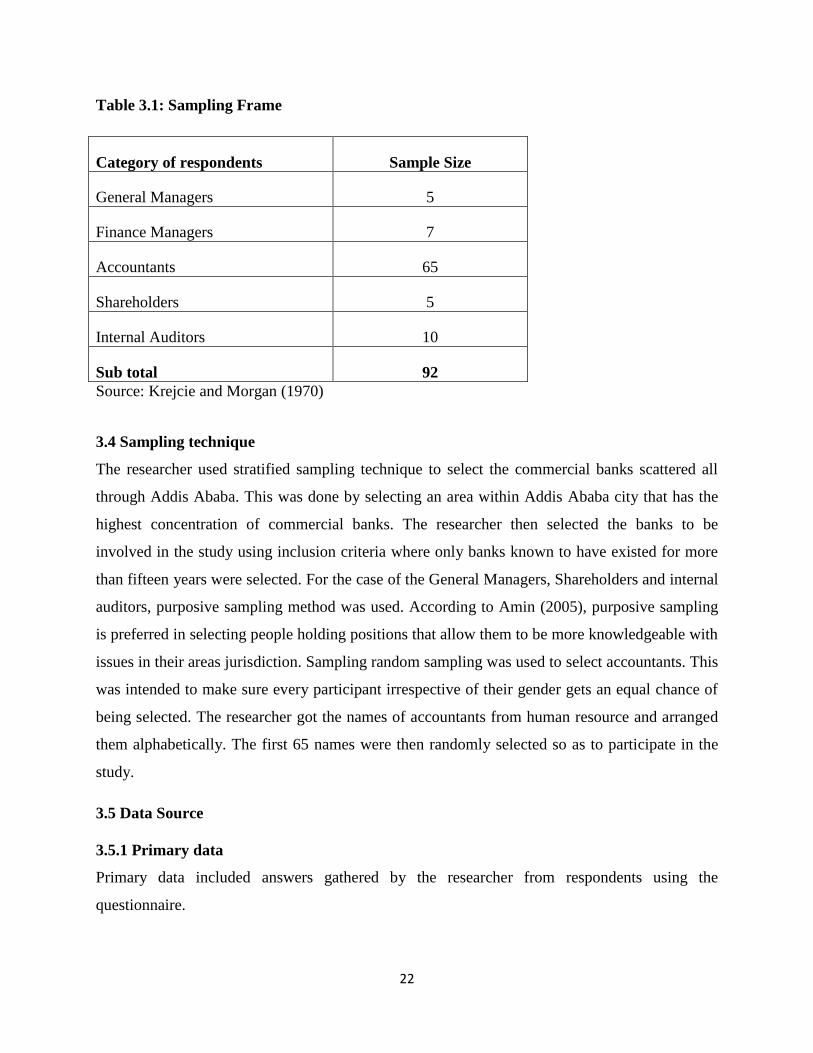

This study use Krejcie and Morgan (1970) table guide for sample determination of the target

population. The population and sample distributions of this study are presented in table 3.1.

22

Table 3.1: Sampling Frame

Category of respondents Sample Size

General Managers 5

Finance Managers 7

Accountants 65

Shareholders 5

Internal Auditors 10

Sub total 92

Source: Krejcie and Morgan (1970)

3.4 Sampling technique

The researcher used stratified sampling technique to select the commercial banks scattered all

through Addis Ababa. This was done by selecting an area within Addis Ababa city that has the

highest concentration of commercial banks. The researcher then selected the banks to be

involved in the study using inclusion criteria where only banks known to have existed for more

than fifteen years were selected. For the case of the General Managers, Shareholders and internal

auditors, purposive sampling method was used. According to Amin (2005), purposive sampling

is preferred in selecting people holding positions that allow them to be more knowledgeable with

issues in their areas jurisdiction. Sampling random sampling was used to select accountants. This

was intended to make sure every participant irrespective of their gender gets an equal chance of

being selected. The researcher got the names of accountants from human resource and arranged

them alphabetically. The first 65 names were then randomly selected so as to participate in the

study.

3.5 Data Source

3.5.1 Primary data

Primary data included answers gathered by the researcher from respondents using the

questionnaire.

23

3.5.2 Secondary data

Secondary data were obtained from the available financial reports, journals, newspapers and

research magazines. On the other hand, Internet and libraries were also utilized as a significant

source of secondary data.

3.6 Data collection methods

3.6.1 Questionnaire

The study used a self-administered questionnaire and semi structured instruments to collect data

from the employees. Questionnaires on Corporate governance, internal auditing and financial

performance will be distributed to the selected respondents to collect their opinions on the

subject. The 5 Likert scale grading 1=strongly disagree and 5=strongly agree were adopted for

this study due to its suitability in measuring perceptions, attitudes, values and behaviors that

relate to corporate governance, internal auditing and financial performance.

3.7 Measurement of Variables

Corporate governance was measured using a structured questionnaire based on a 5-point Likert

scale (Vrajlal, 2006), where 1=strongly agree, 2=agree, 3=disagree, 4= strongly disagree and

5=don‟t know.

Internal audit was measured using a structured questionnaire based on a 5-point Likert scale

(Sawyer, 2003), where 1=strongly agree, 2=agree, 3=disagree, 4= strongly disagree and 5=don‟t

know.

Financial performance was measured using (Jose, 1999). This was measured on a 5-point

Likert Scale, where 1=strongly agree, 2=agree, 3=disagree, 4= strongly disagree and 5=don‟t

know.

3.8 Validity and Reliability of Research Instruments

The validity of the instruments was ascertained by involving experts and non-experts in the

school of post graduate studies. The questionnaires were distributed to various management

scholars (supervisors) to read through and offer their opinion so as to establish face validity. The

errors that were found were adjusted accordingly to ensure that the data collected are valid.

24

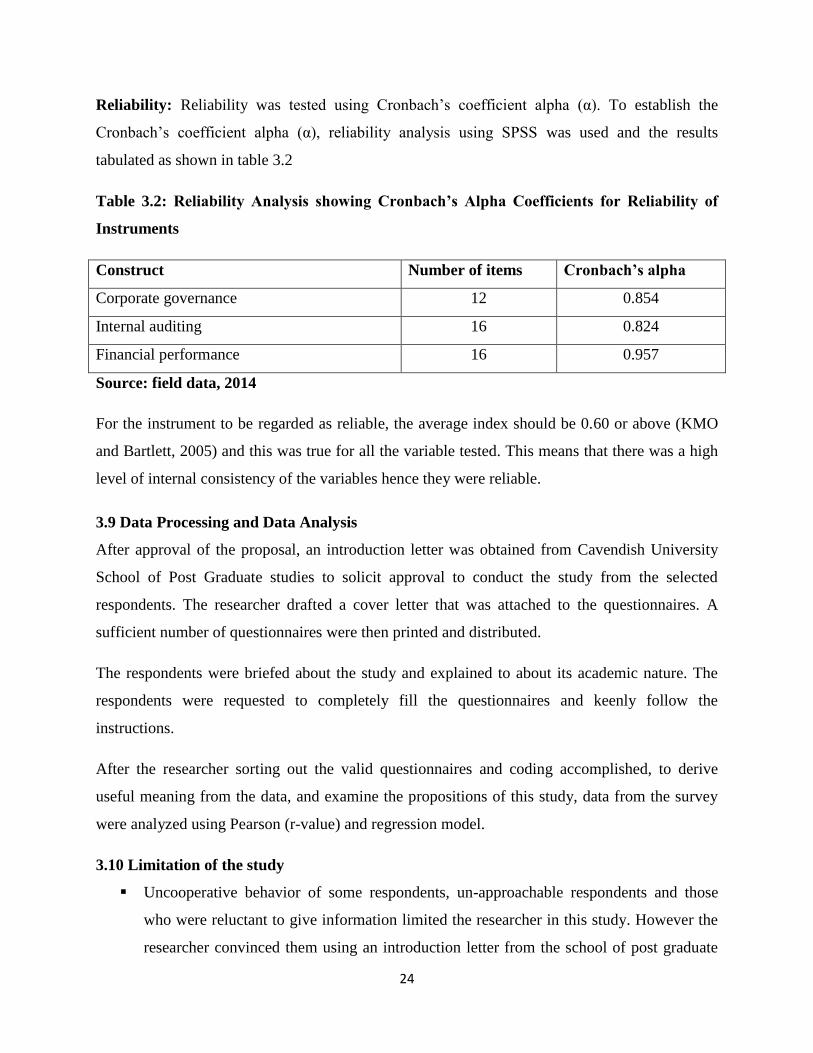

Reliability: Reliability was tested using Cronbach‟s coefficient alpha (α). To establish the

Cronbach‟s coefficient alpha (α), reliability analysis using SPSS was used and the results

tabulated as shown in table 3.2

Table 3.2: Reliability Analysis showing Cronbach’s Alpha Coefficients for Reliability of

Instruments

Construct Number of items Cronbach’s alpha

Corporate governance 12 0.854

Internal auditing 16 0.824

Financial performance 16 0.957

Source: field data, 2014

For the instrument to be regarded as reliable, the average index should be 0.60 or above (KMO

and Bartlett, 2005) and this was true for all the variable tested. This means that there was a high

level of internal consistency of the variables hence they were reliable.

3.9 Data Processing and Data Analysis

After approval of the proposal, an introduction letter was obtained from Cavendish University

School of Post Graduate studies to solicit approval to conduct the study from the selected

respondents. The researcher drafted a cover letter that was attached to the questionnaires. A

sufficient number of questionnaires were then printed and distributed.

The respondents were briefed about the study and explained to about its academic nature. The

respondents were requested to completely fill the questionnaires and keenly follow the

instructions.

After the researcher sorting out the valid questionnaires and coding accomplished, to derive

useful meaning from the data, and examine the propositions of this study, data from the survey

were analyzed using Pearson (r-value) and regression model.

3.10 Limitation of the study

Uncooperative behavior of some respondents, un-approachable respondents and those

who were reluctant to give information limited the researcher in this study. However the

researcher convinced them using an introduction letter from the school of post graduate

25

and research of Cavendish University explaining to them that the work is for academic

purposes only.

The researcher was also limited by privacy to information by administrators because of

organizational policy regarding information disbursement. The researcher had to select

other commercial banks there were willing to provide relevant information in regard to

the study.

The researcher was limited by extraneous variables such as honesty of the respondents

where some of them did not say the truth. The researcher provided the respondents with

an informed consent sheet for them to consent that they would provide relevant

information with utmost honesty.

26

CHAPTER FOUR

DATA PRESENTATION, ANALYSIS AND INTERPRETATION

4.0 Introduction

This chapter presents the results of data analysis and findings compiled from the field. The

findings are presented in line with the study objectives.

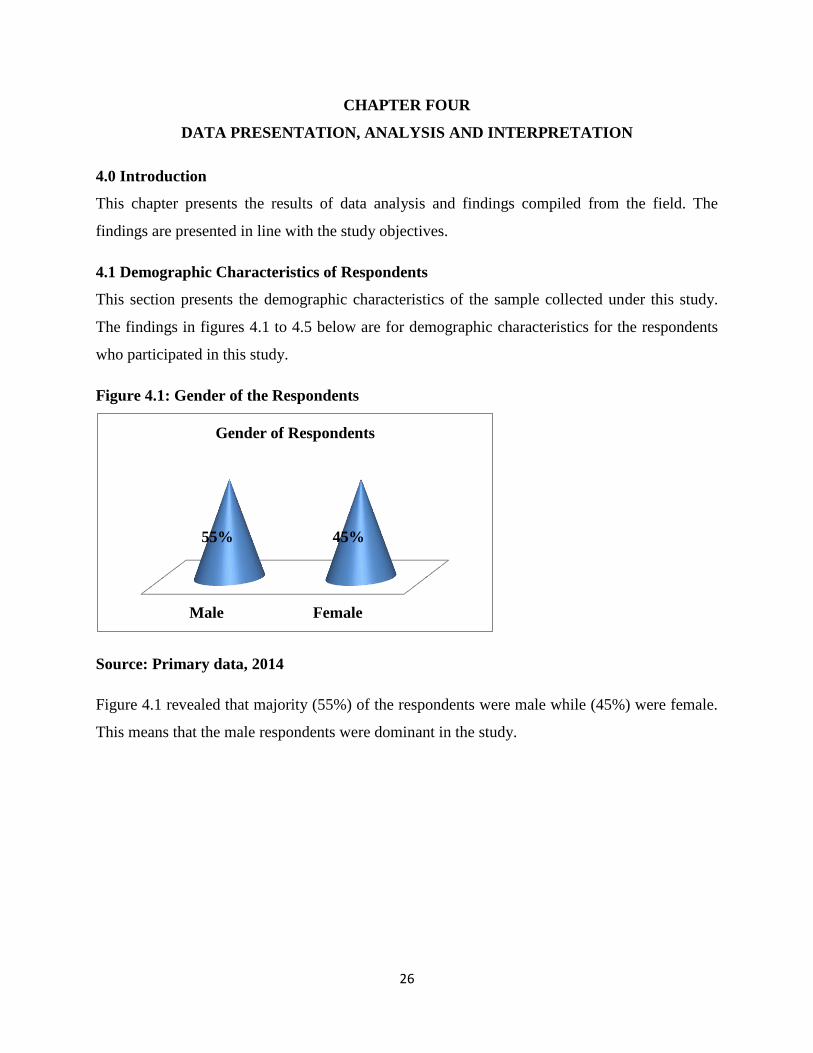

4.1 Demographic Characteristics of Respondents

This section presents the demographic characteristics of the sample collected under this study.

The findings in figures 4.1 to 4.5 below are for demographic characteristics for the respondents

who participated in this study.

Figure 4.1: Gender of the Respondents

Source: Primary data, 2014

Figure 4.1 revealed that majority (55%) of the respondents were male while (45%) were female.

This means that the male respondents were dominant in the study.

Male Female

55% 45%

Gender of Respondents

27

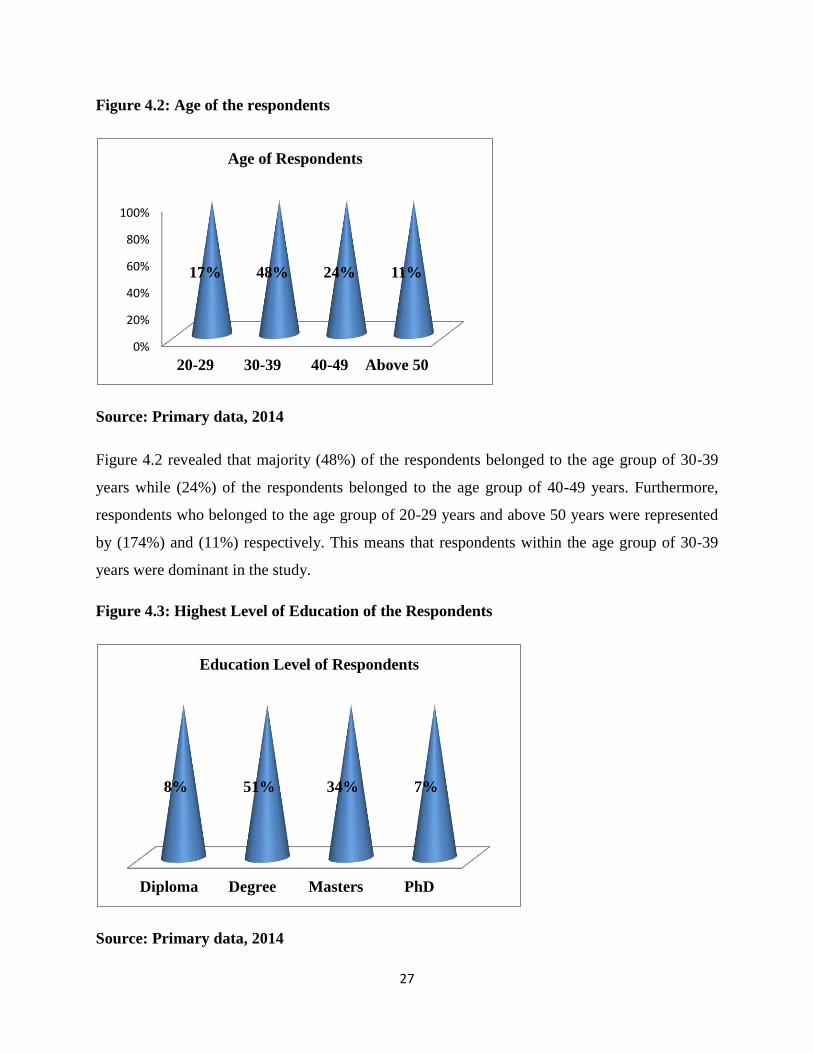

Figure 4.2: Age of the respondents

Source: Primary data, 2014

Figure 4.2 revealed that majority (48%) of the respondents belonged to the age group of 30-39

years while (24%) of the respondents belonged to the age group of 40-49 years. Furthermore,

respondents who belonged to the age group of 20-29 years and above 50 years were represented

by (174%) and (11%) respectively. This means that respondents within the age group of 30-39

years were dominant in the study.

Figure 4.3: Highest Level of Education of the Respondents

Source: Primary data, 2014

0%

20%

40%

60%

80%

100%

20-29 30-39 40-49 Above 50

17% 48% 24% 11%

Age of Respondents

Diploma Degree Masters PhD

8% 51% 34% 7%

Education Level of Respondents

28

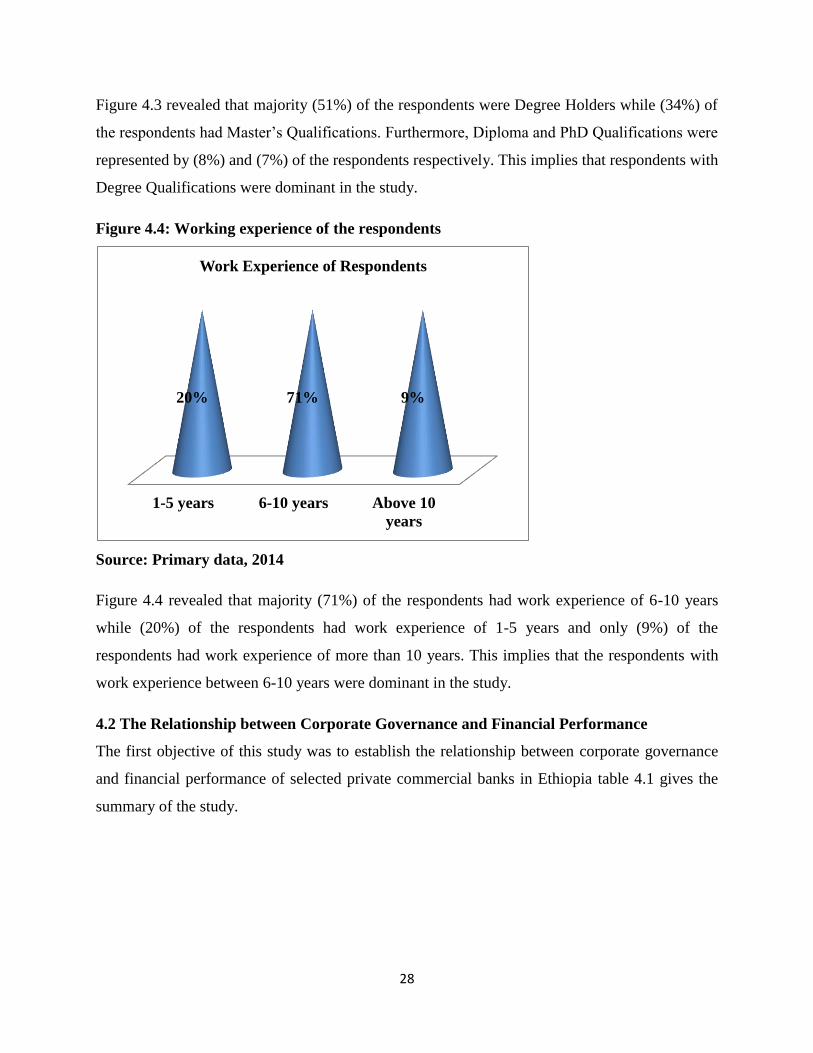

Figure 4.3 revealed that majority (51%) of the respondents were Degree Holders while (34%) of

the respondents had Master‟s Qualifications. Furthermore, Diploma and PhD Qualifications were

represented by (8%) and (7%) of the respondents respectively. This implies that respondents with

Degree Qualifications were dominant in the study.

Figure 4.4: Working experience of the respondents

Source: Primary data, 2014

Figure 4.4 revealed that majority (71%) of the respondents had work experience of 6-10 years

while (20%) of the respondents had work experience of 1-5 years and only (9%) of the

respondents had work experience of more than 10 years. This implies that the respondents with

work experience between 6-10 years were dominant in the study.

4.2 The Relationship between Corporate Governance and Financial Performance

The first objective of this study was to establish the relationship between corporate governance

and financial performance of selected private commercial banks in Ethiopia table 4.1 gives the

summary of the study.

1-5 years 6-10 years Above 10

years

20% 71% 9%

Work Experience of Respondents

29

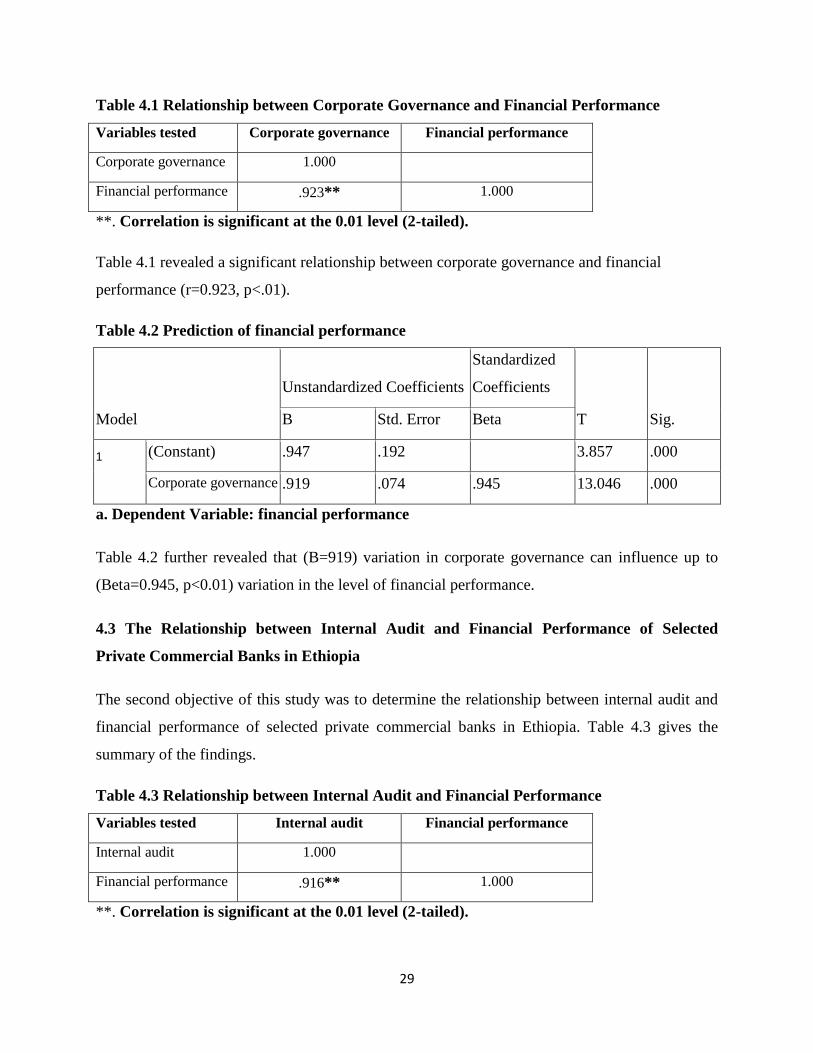

Table 4.1 Relationship between Corporate Governance and Financial Performance

Variables tested Corporate governance Financial performance

Corporate governance 1.000

Financial performance .923** 1.000

**. Correlation is significant at the 0.01 level (2-tailed).

Table 4.1 revealed a significant relationship between corporate governance and financial

performance (r=0.923, p<.01).

Table 4.2 Prediction of financial performance

Model

Unstandardized Coefficients

Standardized

Coefficients

T Sig. B Std. Error Beta

1 (Constant) .947 .192 3.857 .000

Corporate governance .919 .074 .945 13.046 .000

a. Dependent Variable: financial performance

Table 4.2 further revealed that (B=919) variation in corporate governance can influence up to

(Beta=0.945, p<0.01) variation in the level of financial performance.

4.3 The Relationship between Internal Audit and Financial Performance of Selected

Private Commercial Banks in Ethiopia

The second objective of this study was to determine the relationship between internal audit and

financial performance of selected private commercial banks in Ethiopia. Table 4.3 gives the

summary of the findings.

Table 4.3 Relationship between Internal Audit and Financial Performance

Variables tested Internal audit Financial performance

Internal audit 1.000

Financial performance .916** 1.000

**. Correlation is significant at the 0.01 level (2-tailed).

30

Table 4.3 revealed a significant relationship between internal audit and financial performance

(r=.916, p<.01).

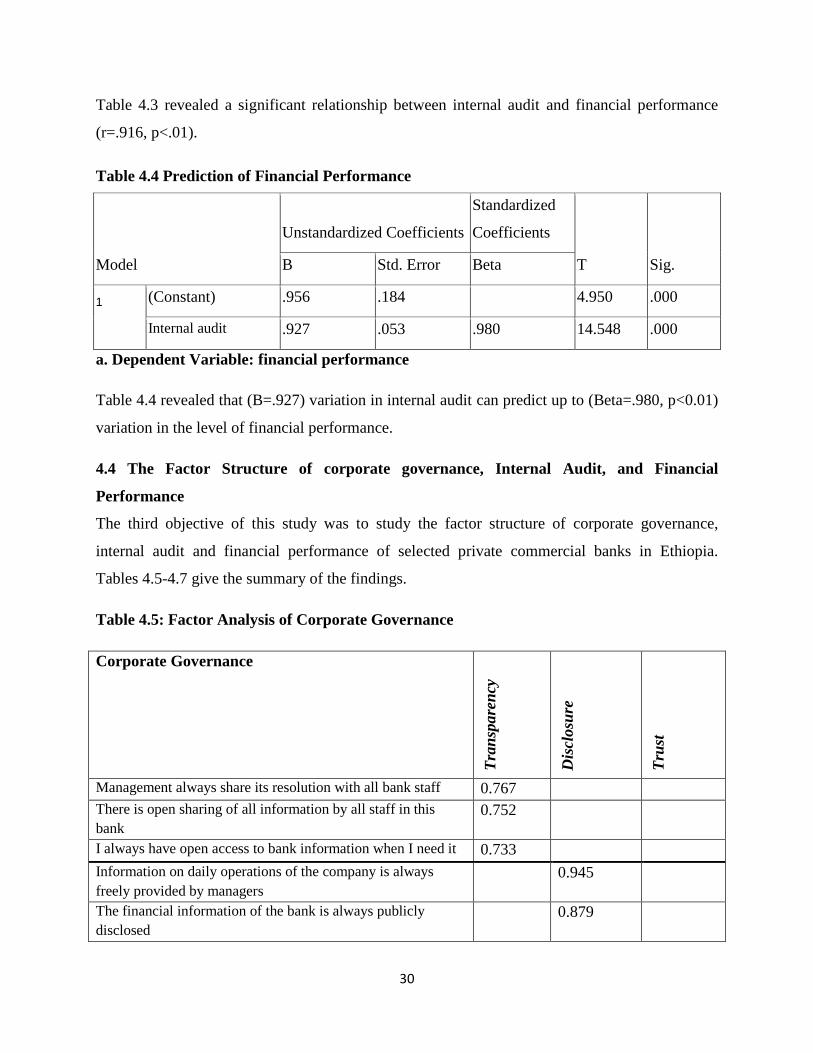

Table 4.4 Prediction of Financial Performance

Model

Unstandardized Coefficients

Standardized

Coefficients

T Sig. B Std. Error Beta

1 (Constant) .956 .184 4.950 .000

Internal audit .927 .053 .980 14.548 .000

a. Dependent Variable: financial performance

Table 4.4 revealed that (B=.927) variation in internal audit can predict up to (Beta=.980, p<0.01)

variation in the level of financial performance.

4.4 The Factor Structure of corporate governance, Internal Audit, and Financial

Performance

The third objective of this study was to study the factor structure of corporate governance,

internal audit and financial performance of selected private commercial banks in Ethiopia.

Tables 4.5-4.7 give the summary of the findings.

Table 4.5: Factor Analysis of Corporate Governance

Corporate Governance

Tra

nsp

are

ncy

Dis

closu

re

Tru

st

Management always share its resolution with all bank staff 0.767

There is open sharing of all information by all staff in this

bank 0.752

I always have open access to bank information when I need it 0.733

Information on daily operations of the company is always

freely provided by managers

0.945

The financial information of the bank is always publicly

disclosed 0.879

31

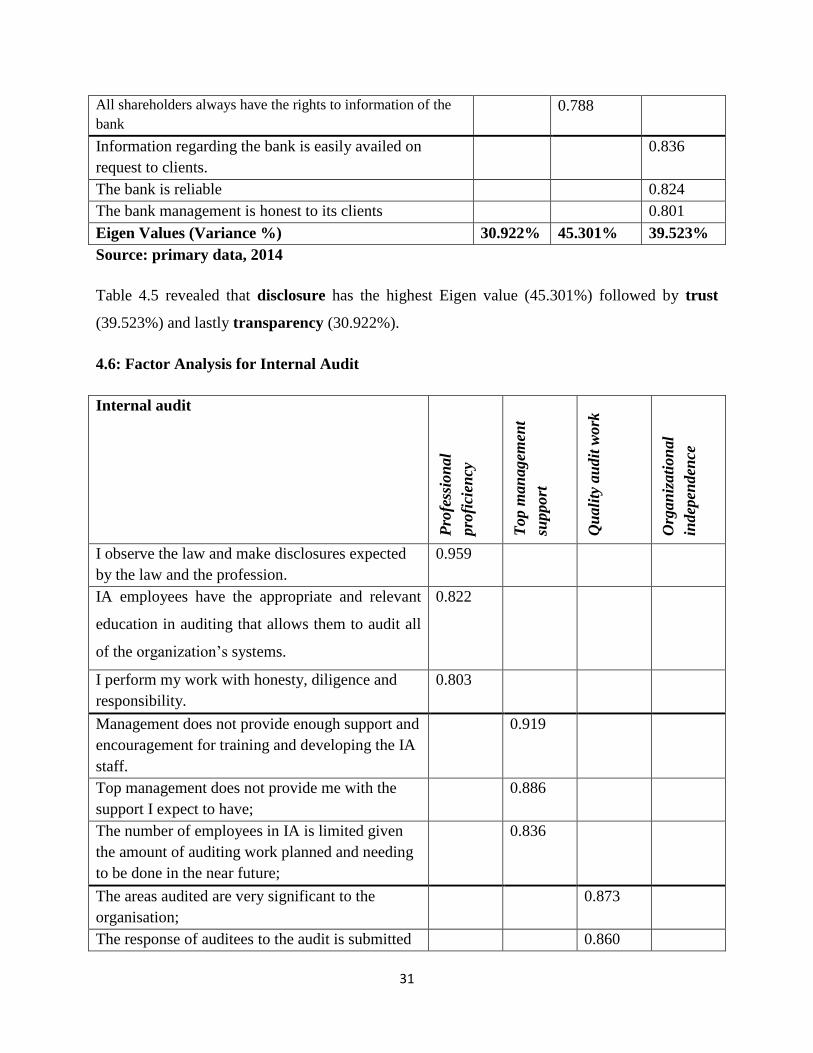

All shareholders always have the rights to information of the

bank 0.788

Information regarding the bank is easily availed on

request to clients.

0.836

The bank is reliable 0.824

The bank management is honest to its clients 0.801

Eigen Values (Variance %) 30.922% 45.301% 39.523%

Source: primary data, 2014

Table 4.5 revealed that disclosure has the highest Eigen value (45.301%) followed by trust

(39.523%) and lastly transparency (30.922%).

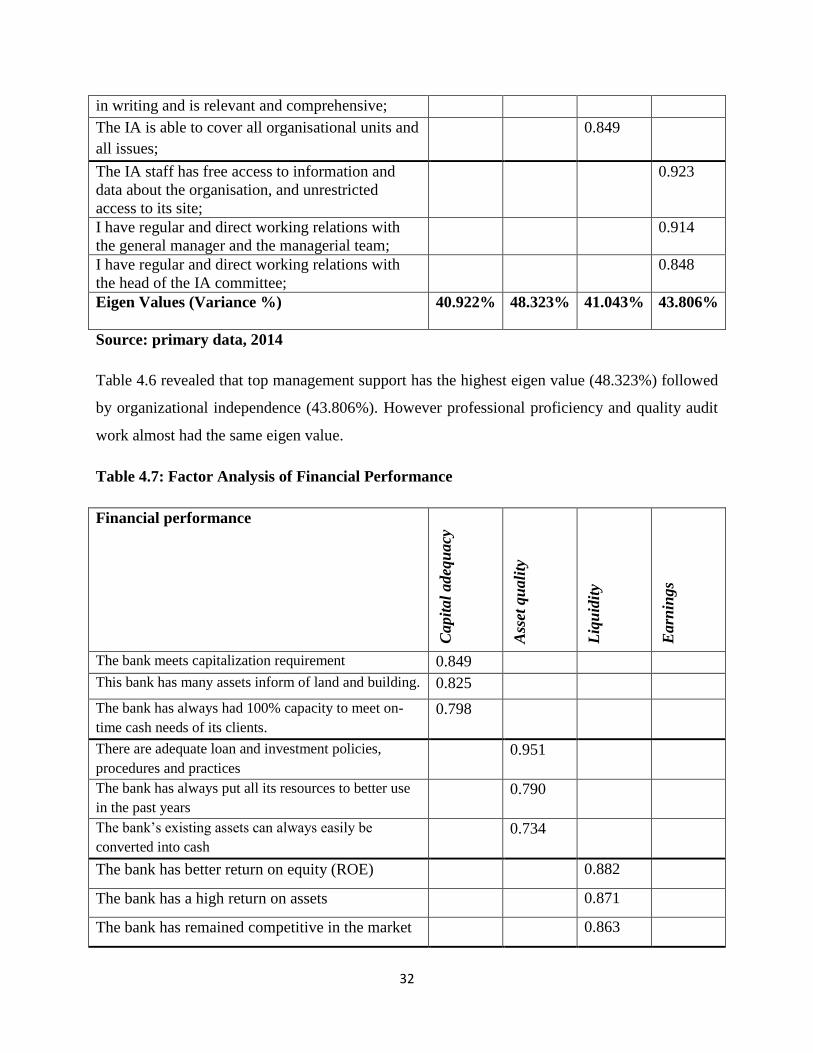

4.6: Factor Analysis for Internal Audit

Internal audit

Pro

fess

ion

al

pro

fici

ency

Top m

an

agem

ent

support

Qu

ali

ty a

udit

work

Org

an

izati

on

al

indep

enden

ce