Corporate Financial Planning Directed by John R. Graham D. Richard Mead Jr. Family Professor of Finance Fuqua School of Business, Duke University Data from around the world are used in this report. Results are presented from a North American (US + Canada) perspective. To save space in the report, at times “US” is used as shorthand for “North America” because more than 90% of North American responses are from the US. A joint survey project between Duke University, CFO Magazine, and NYSE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Corporate Financial Planning

Directed by John R. GrahamD. Richard Mead Jr. Family Professor of Finance

Fuqua School of Business, Duke University

Data from around the world are used in this report. Results are presented from a North American (US + Canada) perspective. To save space in the report, at times “US” is used as shorthand for “North America” because more than 90% of North American responses are from the US.

A joint survey project between

Duke University, CFOMagazine, and NYSE

2

CFO Optimism Q1 20191

High vs. Low Revenue Projections2

Capital Structure3

Liquidity4

Page 3

Page 4

Page 6

Page 12

Corporate Financial Planning5

Investment, Hurdle Rates, Cost of Capital6

Key results CFO Survey7

Demographics, Survey Details8

Page 13

Page 17

Page 21

Page 22

-13%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

24%

More optimistic about

economic outlook, with 37%

more pessimistic

48%

More optimistic about

company’s financial

outlook, with 22% more

pessimistic

3

US CFO’s “growing more optimistic” minus “growing more pessimistic” (QoQ)

Percentage of optimists –- percentage of pessimists w.r.t. economy

CFO optimism Q1 2019

Economic optimism among CFOs

The charts below and to the right indicate that a higher proportion of US CFOs are growing pessimistic

about the US economy (37%), relative to those growing more optimistic (24%).

In a separate question not reflected in these charts, CFOs around the world rate their optimism about

the economic outlook for their own countries on a scale from 0 to 100. In Q1 2019, US CFOs rated their

optimism at 64, which is higher than the long-run average CFO Optimism Index of 60. While high by

historic standards, optimism has declined from 71 one year ago. The Optimism Index is slightly higher

in Latin America (65 out of 100) and in Asia (65). Optimism is lower in Europe (60) and in Africa (55).

4

Very bad scenario: There is a 1-in-10 chance that in 2019 revenue growth will be less than:

Best Guess: CFOs expect 2019 revenue growth will be:

Very good scenario: There is a 1-in-10 chance that in 2019 revenue growth will be greater than:

Percentage of CFOs expecting revenues to increase during 2019

Percentage of CFOs expecting revenues to decrease during 2019

2,4%

13,9%

21,6%

North America 85.5% 8.6%

2,4%

13,1%

23,4%

Europe 79.8% 12.8%

8,1%

35,8% 37,1%

Africa 90.9% 9.1%

5,9%

20,0%

32,2%

Asia 91% 6.6%

8,1%

24,1%

39,5%

Latin America 89.3% 5.1%

CFOs’ revenue growth outlook for 2019

85.5% of US financial executives expect company revenues to increase during 2019.

Approximately 9 out of 10 CFOs anticipate an increase in revenues in Africa, Asia, and

Latin America. Only 8 out of 10 of European CFOs expect revenue to increase.

In their ‘base case’, US CFOs expect revenue to increase by 13.9% in 2019. In their ‘very

bad’ planning scenarios, CFOs expect revenue growth of just 2.4%. In their ‘very good’

scenarios, revenue will grow by 21.6%.

Revenue Growth Estimates by Region; by Industry

-10

0

10

20

30

40

50

US Europe Asia Latam Africa Retail Finance Service Tech Manu Healthcare

REV

ENU

E G

RO

WTH

Good Scenario (top) Bad Scenario (bottom) Best Guess

The top of each line shows the “very good” revenue projection.

The bottom of each line shows the “very bad” revenue projection.

The dot on the line shows the “best guess” revenue estimate.

North AmericanIndustries

5

Euro

pe. 7

4%

Euro

pe. 4

4%

Euro

pe. 1

3%

Euro

pe. 1

2%

Euro

pe. 1

2%

Euro

pe. 1

1%

Euro

pe. 8

%

Euro

pe. 6

%

Euro

pe. 1

%

Nort

h Am

eric

a. 3

3%

Nort

h Am

eric

a. 3

9%

Nort

h Am

eric

a. 12

%

Nort

h Am

eric

a. 8

%

Nort

h Am

eric

a. 10

%

Nort

h Am

eric

a. 10

%

Nort

h Am

eric

a. 2

%

Nort

h Am

eric

a. 6

%

Nort

h Am

eric

a. 6

%

Latin

Am

eric

a, 6

5%

Latin

Am

eric

a, 4

4%

Latin

Am

eric

a, 18

%

Latin

Am

eric

a, 10

%

Latin

Am

eric

a, 18

%

Latin

Am

eric

a, 19

%

Latin

Am

eric

a, 5

%

Latin

Am

eric

a, 10

%

Latin

Am

eric

a, 5

%

Asia

. 71%

Asia

. 37%

Asia

. 26%

Asia

. 21%

Asia

. 11%

Asia

. 13%

Asia

. 14%

Asia

. 13%

Asia

. 10%

Afri

ca. 5

4%

Afri

ca. 3

9%

Afri

ca. 2

3%

Afri

ca. 1

9%

Afri

ca. 2

3%

Afri

ca. 1

2%

Afri

ca. 1

5%

Afri

ca. 8

%

Afri

ca. 1

9%

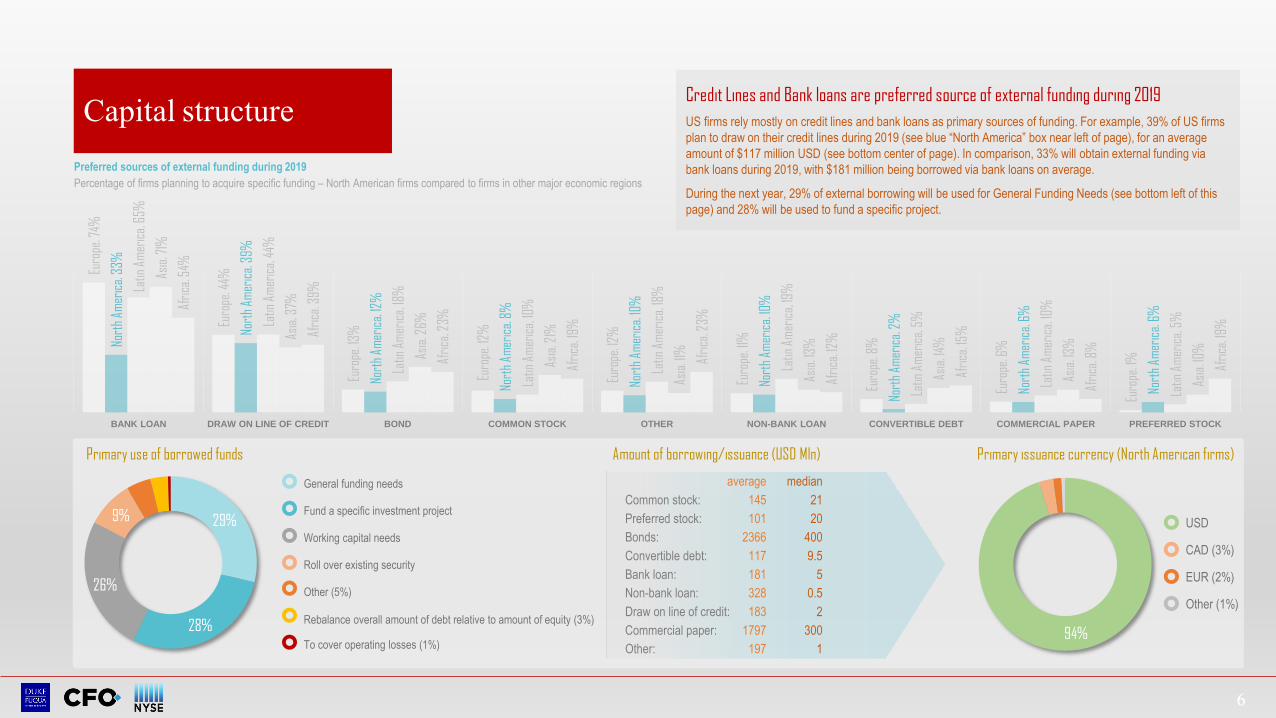

BANK LOAN DRAW ON LINE OF CREDIT BOND COMMON STOCK OTHER NON-BANK LOAN CONVERTIBLE DEBT COMMERCIAL PAPER PREFERRED STOCK

6

Preferred sources of external funding during 2019

Percentage of firms planning to acquire specific funding – North American firms compared to firms in other major economic regions

29%

28%

26%

9% Fund a specific investment project

General funding needs

Working capital needs

Roll over existing security

Other (5%)

Rebalance overall amount of debt relative to amount of equity (3%)

To cover operating losses (1%)

Primary use of borrowed funds

average median

Common stock: 145 21

Preferred stock: 101 20

Bonds: 2366 400

Convertible debt: 117 9.5

Bank loan: 181 5

Non-bank loan: 328 0.5

Draw on line of credit: 183 2

Commercial paper: 1797 300

Other: 197 1

Amount of borrowing/issuance (USD Mln)

CAD (3%)

USD

EUR (2%)

Other (1%)

94%

Primary issuance currency (North American firms)

Credit Lines and Bank loans are preferred source of external funding during 2019

US firms rely mostly on credit lines and bank loans as primary sources of funding. For example, 39% of US firms

plan to draw on their credit lines during 2019 (see blue “North America” box near left of page), for an average

amount of $117 million USD (see bottom center of page). In comparison, 33% will obtain external funding via

bank loans during 2019, with $181 million being borrowed via bank loans on average.

During the next year, 29% of external borrowing will be used for General Funding Needs (see bottom left of this

page) and 28% will be used to fund a specific project.

Capital structure

How Do US Firms Measure Leverage (their “Debt Ratio”)? Nearly 45% of US firms say that Debt/EBITDA is their primary measure of leverage, and approximately two-thirds say Debt/EBITDA is one of their top 3 measures of leverage (see bottom row).

0% 10% 20% 30% 40% 50% 60% 70%

Debt/EBITDA

Credit Rating

Interest Coverage

Debt/Asset

Debt/Value

Liability/Asset

Debt/Equity

Top 1

Top 2

Top 3

7

Do US Companies Have a “Target” Debt Ratio?

Strict Target/Range16%

Somewhat Tight Target/Range

30%

Flexible Target/Range27%

No Target/Range28%

8

Upper/Lower Limit Acceptable Debt Ratios (Debt/EBITDA)

The typical US firm currently has Debt/EBITDA = 3.4. CFOs say their firms would take action if the ratio increased to 4.1 or higher, and move Debt/EBITDA back into an acceptable range within 1.6 years.

We set a upper limit

Yes No

We set a lower limit

Yes No

We set a timetable to bring down debt ratio

Yes No

Average Upper Limit:

4.1

Average years to reduce debt ratio to accept. range

1.6 years

Average Lower Limit:

1.9

We set a timetable to bring up debt ratio

Yes No

Average years to increase debt

ratio

0.9 years

Current Debt/EBITDA

3.4

9

We set a upper limit

Yes No

We set a lower limit

Yes No

We set a timetable to bring down debt ratio

Yes No

Average Upper Limit:

40.3%

Average years to reduce debt ratio to accept. range

1.5 years

Average Lower Limit:

18.1%

We set a timetable to bring up debt ratio

Yes No

Average years to increase debt

ratio

1.2 years

Current Debt/Asset

26%

Upper/Lower Limit Acceptable Debt Ratios (Debt/Assets)The typical US firm currently has Debt/Assets = 26%.

CFOs say their firms would take action if Debt/Assets rose to 40.3%.

10

Which Factors Affect How Much Debt Firms Use?

11

85% of CFOs say that preserving financial flexibility is an important or very important consideration as they decide how much debt to use. Flexibility is the most popular answer, as reflected in the dark and medium dark blue bars in the bottom row. Credit ratings are the second most popular debt factor.

0% 20% 40% 60% 80% 100%

Maintaining financial flexibility

Our credit rating (as assigned by rating agencies)

The level of interest rates

The volatility of our earnings and cash flows

Insufficient internal funds

The debt levels of other firms in our industry

The transaction costs and fees for issuing debt

Equity undervaluation/overvaluation

The amount collateral against which we can borrow

The tax advantage of interest deductibility

5=Very Important 4=Important 3=Moderate Importance

Asia average median

Current: Cash-to-Total Assets ratio: 20.55% 15%

Current: Long-term borrowing interest rate: 6.03% 6%

Year-end forecast: Long term borrowing interest rate: 6.35% 6%

12

Latin America average median

Current: Cash-to-Total Assets ratio: 18.38% 10%

Current: Long-term borrowing interest rate: 7.99% 7.45%

Year-end forecast: Long term borrowing interest rate: 7.58% 7%

Europe average median

Current: Cash-to-Total Assets ratio: 13.69% 10%

Current: Long-term borrowing interest rate: 2.83% 2%

Year-end forecast: Long term borrowing interest rate: 2.63% 2%

North America average median

Current: Cash-to-Total Assets ratio: 17.04% 10%

Current: Long-term borrowing interest rate: 4.84% 4.45%

Year-end forecast: Long term borrowing interest rate: 5.19% 5%

Africa average median

Current: Cash-to-Total Assets ratio: 32.88% 20.50%

Current: Long-term borrowing interest rate: 12.02% 10.25%

Year-end forecast: Long term borrowing interest rate: 12.30% 10.88%

Some (7%)

A little (10%)

Moderate (33%)

Sufficient (26%)

A lot (22%)

48%

of CFOs say firm has

(sufficient to a lot) financial

flexibility

11%

22%

30%

37%

42%

58%

62%

Preserve unused line of credit capacity

Ability to avoid financial distress during economic downturns

Ability to quickly pursue attractive investment opportunities

Access to long-term debt markets

Access to short-term funding (e.g. commercial paper, short-term debt)

Maintain large cash balance

Access to equity marketEur

opea

n C

FO

s st

ate

mos

t im

port

ant

aspe

cts

of m

aint

aini

ng fi

nanc

ial f

lexi

bilit

yFinancial flexibility and the cost of debt

As indicated on the previous slide, preserving financial flexibility is a key

objective of US companies. In explaining the primary goals of preserving

financial flexibility, the chart on the far right indicates that 62% of firms

say that they want to avoid distress should a downturn occur, and 58%

indicate they want to be able to quickly pursue investments. As to their

current situation, 48% of companies say they currently have ‘sufficient’ or

‘a lot’ of financial flexibility.

In the charts below, North American firms believe their cost of long-term

debt will increase from an average rate of 4.84% currently to 5.19% at

year-end 2019.

Corporate financial planning

13

% of firms that perform

scenario analysis

% of firms that do not

perform scenario analysis

23%

77%

Do you perform scenario analysis when making plans for the

overall company (e,g, your 5-year plan). How many scenarios?

Economic indicators that CFOs consider to be most important in affecting the

performance of their own firms (% that rank factor in the Top 3)

4%

12%

13%

18%

19%

20%

20%

29%

31%

38%

47%GDP growth (country level)

Consumer spending

Commodity prices

Interest rates

GDP growth (global)

Other (e.g. spending on defense,

natural disasters, price wars, etc.)

International trade (tariffs)

Infrastructure spending

Currency exchange rates

Defense spending

Inflation

Scenario analysis and corporate

performanceThe circle chart to the left shows that 77% of companies

conduct scenario analysis. Among these firms, the mean

number of scenarios considered is 3 when planning for

their overall company.

The green shape in the pentagon at the bottom of the

page shows that companies tilt towards considering

downside scenarios more so than upside scenarios. In

particular, 66% of companies consider downside

scenarios and 20% consider extreme downside. In

comparison, only 59% consider upside and 4% consider

extreme upside scenarios.

The chart at the far left summarizes the importance of

various economic variables in determining whether a firm

experiences downside or upside outcomes in their actual

performance. 47% of companies indicate that country

GDP growth is one of the “Top 3” economic indicators to

determine their company’s actual performance, and 38%

indicate consumer spending is similarly important.

3

the average number of

scenarios being considered in

the company planning cycle

Downside

Base caseUpside

Extreme upside

Extreme downside

20%66%

88%59%

4%

Scenarios receiving most of the company’s attention in

scenario planning

Downside, Base Case, and Upside Scenario Planning

14

-10

-5

0

5

10

15

20

25

30

Extreme Downside Downside Base Upside Extreme Upside

Revenue Growth Profit Margin Capex Growth Cash

For each of 5 scenarios, what will revenue growth, profits, capital spending, and cash holdings be during 2019?

15

Company growth

In the chart to the right, North American companies say that on average, 17%

of current revenues are generated by new products (i.e., products that did not

exist 4 years ago). This percentage is lower than the impact of new products

on revenues in the rest of the world.

In an indication that business executives are very optimistic about their own

firms’ prospects relative to peer firms, 50% of North American companies say

their own firm will outperform their peers, and only 6% say they will

underperform their peers. Similarly, more than half of CFOs in other parts of

the world expect to outperform their peers.

6%

43%50%

NORTH AMERICA

4%

40%

55%

EUROPE

6% 27%

67%

LATIN AMERICA

5%16%

79%

AFRICA

6%

43%51%

ASIA

Compared to other firms in the industry, company growth over the next three years will be slower

Compared to other firms in the industry, company growth over the next three years will be the same

Compared to other firms in the industry, company growth over the next three years will be faster

New product development% of current sales revenue coming from new products (that did not exist 4 years ago)

Europe North America Latin America Africa Asia

23% 17% 22% 24% 30%

16

58%

of US CFOs expect the firm

to increase hiring of full

time employees, while 11%expect to downsize the labor

force

92%

of US CFOs expect the firm

to increase wages and

salaries during 2019, while

3% expects to reduce pay

levels

Hiring, wages, and corporate investment

In the chart immediately to the left, employment growth at North American

firms is expected to stay moderately strong over the next 12 months (2%),

down somewhat from expectations 6 or 12 months ago. Other parts of the

world expect 1% to 2% employment growth. The chart on the far upper

left indicates that 58% of North American firms expect to increase their

number of fulltime employees (versus 11% that expect to reduce

workforce).

The chart in the middle indicates that North American firms expect wages

to grow by 3% over the next 12 months, lower than the 4% to 6% growth

expected in Africa, Asia, and Latin America. Wage growth will be smallest

in Europe.

The chart at the bottom shows a rebound in capital spending growth, with

US companies expecting capital expenditures (CAPEX) to increase by 5%

over the next 12 months.

62%

of US CFOs plan to

increase capital spending

during 2019, while 16%expects to reduce CAPEX

5,00%

-5%

0%

5%

10%

15%

Mar 2018 Jun 2018 Sept 2018 Dec 2018 Mar 2019

United States

Europe

Asia

Latin America

Africa

2,00%

0%

2%

4%

6%

Mar 2018 Jun 2018 Sept 2018 Dec 2018 Mar 2019

3,00%

0%

2%

4%

6%

8%

10%

Mar 2018 Jun 2018 Sept 2018 Dec 2018 Mar 2019

Full-time employment growth rate

Growth in wages/salaries

Capital Spending growth rate

Hurdle Rate Versus the Cost of CapitalUS companies on average require a hurdle rate of 14%, meaning that an investment must earn at least 14% to be pursued. By comparison, the weighted average cost of capital (WACC) averages 9.6% in the US. The right part of the chart lists the reasons that firms provide to explain why they require a hurdle rate 4% to 5% higher than their WACC.

0% 10% 20% 30% 40% 50%

So that we choose only the best available projects

So that we choose projects that are profitable

To account for riskiness of the projects being evaluated

So that we choose projects that pay back the initial investmentquickly

To provide a margin of error in calculations and assumptions

To provide a buffer in case the project underperforms

To limit the number of projects that are approved – because we facefunding constraints

To limit the number of projects that are approved – because ofscarcity of managerial time / expertiseAverage WACC

9.6

Average Hurdle

Rate

14.0

Percentage of CFOs who list a given explanation among their “Top 4” explanations

17

9,6

12,410,92

12,25

14,4514 13,7512,69

15,79

21,56

0

5

10

15

20

25

US Europe Asia Latin America Africa

WACC Hurdle Rate

Hurdle Rate Versus the Cost of Capital, by Region

18

How Frequently Do You Change Hurdle Rates?

Over the past 10 years, 45% of US companies did not change their hurdle rate (by at least 1 percentage point), and 60% changed their hurdle rate zero or one times.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

US Europe Asia Latam Africa

0 1 2 3 4 5 6+ times

19

How Flexible are Investment Plans?The two shaded regions at the top of the leftmost bar indicate that 35% of US firms say that the start date of their largest capital spending project (CapX) is flexible or very flexible. European investment start dates and speed of completion are less flexible than in the US.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

US Europe Asia LatinAmerica

Africa US Europe Asia LatinAmerica

Africa

Very flexible

Flexible

Somewhat flexible

Somewhat inflexible

Inflexible

Very inflexible

How flexible is the start date of your largest CapX project?

How flexible is the speed at which you complete this largest CapX project?

20

21

Key Results CFO SurveyUS, Europe, Latin America, Africa and Asia

EUROPE UNITED STATES LATIN AMERICA AFRICA ASIA

Economic sentiment

CFOs More optimistic 26.2% 24.1% 65.8% 50.0% 47.4%

CFOs Less optimistic 38.3% 36.8% 13.1% 35.7% 29.6%

No change 35.5% 39.1% 21.0% 14.3% 23.0%

Own country optimism level 59.5 64.6 65.4 54.8 64.9

Employment – full-time 1.8% 4.6% 5.4% 4.9% 3.0%

Inflation (own-firm products) n/a n/a n/a n/a n/a

Financial outlook own company

CFOs More optimistic 42.4% 48.3% 68.4% 66.7% 60.7%

CFOs Less optimistic 25.1% 36.8% 23.9% 31.0% 19.3%

No change 32.5% 39.1% 17.8% 2.4% 20.0%

Own company optimism level 67.5 70.4 70.8 63.8 69.6

Revenue growth 3.5% 6.3% 12.5% 9.8% 10.4%

Earnings growth n/a n/a n/a n/a n/a

Business spending

Capital spending 8.5% 8.2% 10.0% 16.4% 11.0%

Technology spending n/a n/a n/a n/a n/a

R&D spending n/a n/a n/a n/a n/a

Advertising and marketing spending n/a n/a n/a n/a n/a

Wages and Salaries 2.9% 5.1% 5.5% 5.7% 6.1%

Health Care Costs n/a n/a n/a n/a n/a

NOTE: this special edition survey did not cover all of the standard survey questions we usually ask each quarter (see www.cfosurvey.org for past results). Key results indicated by n/a were omitted from the special edition survey.

CFO Survey – Industry Breakdown, North America

Manufacturing21%

Banking/Finance/Insurance/Real Estate

18%

Services, Consulting13%

Technology[Software/Hardware/Biotech]

12%

Retail/Wholesale9%

Healthcare/Pharmaceutical9%

Energy7%

Communication/Media4%

Mining/Construction3%

Transportation & Public Utilities

2%

Agriculture, Forestry, & Fishing

1%Public Administration

1%

22

CFO Survey North America

The Global Business Outlook is conducted every quarter jointly by Duke University and CFO Magazine. The

NYSE also patterned on the 2019 Q1 special project. The logos of many global partners appear below.

This Special Survey Edition – Corporate Financial Planning

The Special Survey Edition of CFO Survey aims to document best practices in corporate financial planning and

capital allocation around the globe. The goal is to understand how companies make financial planning decisions

dynamically; that is, how companies adapt and adjust to economic conditions that are constantly changing.

Therefore, another Special Edition will conducted one year from now (Q1 2020).

Note on methodology

The figures quoted in this report are taken from the Global Business Outlook CFO survey for the first quarter of 2019.

The survey concluded March 7, 2019 in most regions. Every quarter, CFOs in Europe, the US, Latin America, Asia, and

Africa are polled about their economic expectations. Current quarterly records go back more than 21 years. The latest

survey generated responses from nearly 1,500 CFOs, including 469 from North America, 145 from Asia, 261 from

Europe, 590 from Latin America and 42 from Africa.

The Global Business Outlook covers a wide range of companies (public and private, small and large, many industries,

etc.). The responses are representative of the population of CFOs that are surveyed. Among the industries represented

in the survey are retail/wholesale, mining/construction, manufacturing, transportation/energy, communications/media,

technology, service/consulting and banking/finance/insurance.

The average growth rates reported are weighted by revenues or number of employees. For example, one $5 billion

company affects on average as much as 10 $500-million firms would. Revenue-weighted mean growth rates are

provided for earnings, revenues, capital spending, technology spending and prices of products. Employee-weighted

mean growth rates are used for health care costs, productivity, number of employees and outsourced employment.

Unless noted, the numbers are for all companies, including private companies.

23

About the Global Business OutlookThe Special Corporate Financial Planning Survey

Related Documents