INTRODUCTION Scope of Financial Management Finance is considered as the life blood of business organisation. Financial management is that managerial activity which is concerned with the planning and controlling of the firm’s financial resources. Financial management as an academic discipline has undergone fundamental changes as regards its scope and coverage. Here we follow two approaches to its scope and functions - that is Traditional and Modern. a. Traditional Approach The traditional concept of financial management was termed as corporate finance. This concept deals only with the procurement of funds by the corporate enterprises to meet their financial needs. This concept encompassed three interrelated aspects of raising finance from outside:- 1) Institutional arrangement of finance (IFCI, IDBI etc). 2) Raising of funds through issue of financial instruments (shares, debenture etc). 3) The legal relationship between the issuer and creditor. Main Limitations of Traditional Concept (Criticisms) 1) It is outsider looking in approach & insider looking out. 2) Focus only on financing problems of corporate enterprises. 3) Concentration only on episodic events & no treatment of working capital needs. 4) Focus was on long term financing. Modern Approach This concept covers acquisition, allocation and efficient utilisation of funds by business enterprises. Here apart from the issues involved in the external funds, the

Corporate Finance

Nov 29, 2015

introduction and detailed report on corporate finance.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTRODUCTION

Scope of Financial Management

Finance is considered as the life blood of business organisation. Financial

management is that managerial activity which is concerned with the planning and

controlling of the firm’s financial resources. Financial management as an academic

discipline has undergone fundamental changes as regards its scope and coverage. Here

we follow two approaches to its scope and functions - that is Traditional and Modern.

a. Traditional Approach The traditional concept of financial management was termed as corporate

finance. This concept deals only with the procurement of funds by the corporate

enterprises to meet their financial needs. This concept encompassed three interrelated

aspects of raising finance from outside:-

1) Institutional arrangement of finance (IFCI, IDBI etc).

2) Raising of funds through issue of financial instruments (shares, debenture etc).

3) The legal relationship between the issuer and creditor.

Main Limitations of Traditional Concept (Criticisms)

1) It is outsider looking in approach & insider looking out.

2) Focus only on financing problems of corporate enterprises.

3) Concentration only on episodic events & no treatment of working capital needs.

4) Focus was on long term financing.

Modern Approach

This concept covers acquisition, allocation and efficient utilisation of funds by

business enterprises. Here apart from the issues involved in the external funds, the

main concern is efficient and wise allocation of funds to various uses. It is viewed as

an integral part of overall management

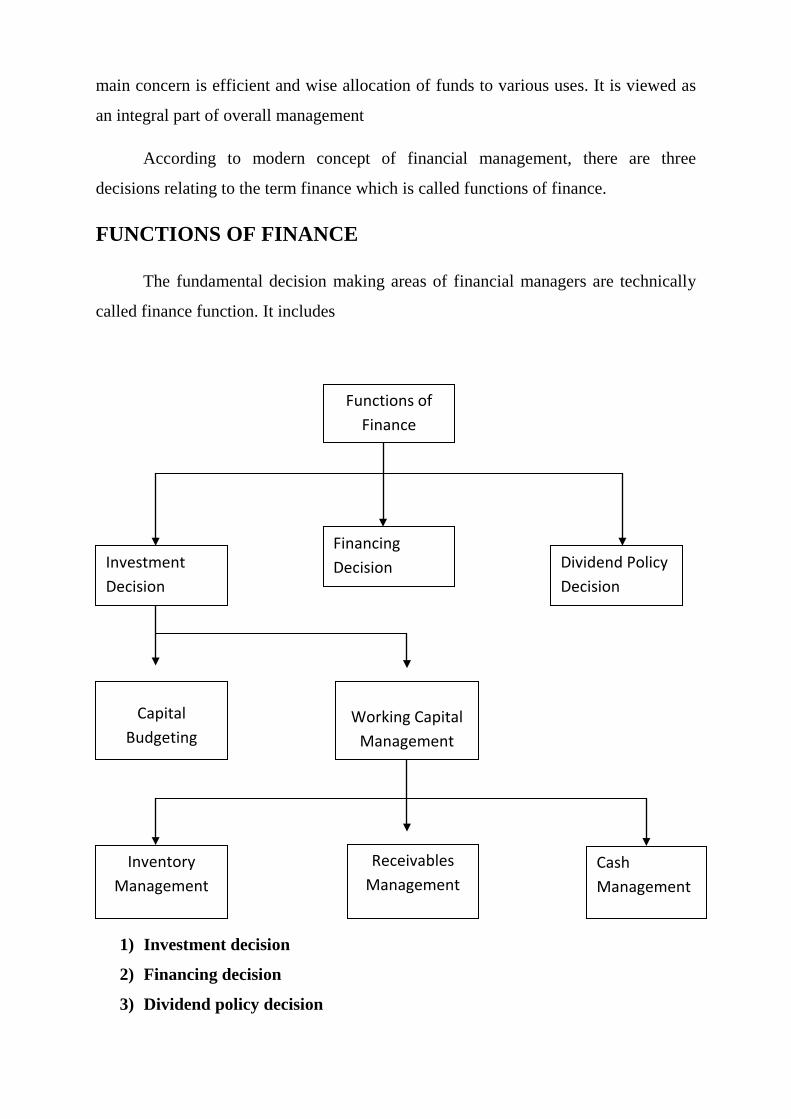

According to modern concept of financial management, there are three

decisions relating to the term finance which is called functions of finance.

FUNCTIONS OF FINANCE

The fundamental decision making areas of financial managers are technically

called finance function. It includes

1) Investment decision

2) Financing decision

3) Dividend policy decision

Capital Budgeting

Investment Decision

Working Capital Management

Inventory Management

Receivables Management

Cash Management

Dividend Policy Decision

Financing Decision

Functions of Finance

1. Investment decision: Decision relating to the investment in assets is called investment decision. Here

we take decision as to the amount of investment, type of assets for investment etc.

There are two types of assets needed by a concern.

1) Fixed assets

Fixed assets means assets required for the permanent use of the business.

Investment decision relating to the fixed assets is called capital budgeting decision.

It is also known as long term investment decision.

2) Current assets

Current assets are the assets needed for meeting the day to day requirement of

the firm. These assets provide liquidity to the firm. Investment decision relating to the

current assets is called working capital management decision. There are three

component of working capital management

1) Inventory management

2) Receivables management

3) Cash management

Liquidity Vs profitability- Liquidity means the capacity to meet the payables in time

or the capacity to convert an asset in to cash. Profitability means capacity to make

additional profit for the firm. Liquidity and profitability are negatively correlated.

While taking investment decision the financial manager has to consider the

trade off between profitability and liquidity. Investment in fixed assets shall provide

profitability to the firm but affects its liquidity position. On the other hand investments

in current assets bring liquidity to the firm but adversely affect its profit. So an

optimum investment decision should be one which must satisfy both profitability and

liquidity criteria.

2. Financing decision.

Here financial manger has to take a decision on the source of finance that shall

be used by the concern for meeting its requirements. Both equity and debt mode of

financing can be applied by the concern for raising finance. Determination of debt

equity mix (capital structure) for a firm is one of the main functions of financial

management. A capital structure gives maximum value to the firm is called optimum

capital structure. Designing of an optimum capital structure is the main objective of

this decision.

3. Dividend policy decision. Decision relating to the utilisation of surplus earnings is called dividend policy

decision. Earnings made by a firm can either be utilized as an internal source of

finance or for making payment of dividend among the share holders. Determination of

dividend pay out ratio is called dividend policy decision.

In dividend policy decision the financial manger has to decide whether to

declare dividend to share holders, if yes to what extent it should be done so. Dividend

payout ratio means the ratio of dividend to total earnings made by the concern.

Determination of dividend pay out ratio is the main decision to be taken by the

financial manger with respect to the dividend policy. This definitely depends on the

preference of shareholders and investment opportunities available with in the firm.

Objectives of Financial Management

There are two approaches towards the objectives of financial management i.e.

traditional approach and modern approach.

I) Traditional Approach (Profit Maximization)

According to this approach the objective of financial management is

maximization of profit.Profit is the test of economic efficiency of a business and

ensures maximum economic welfare. According to this approach actions that increase

profits should be undertaken and those that decrease profits are to be avoided. As the

business is profit making activity, a project which has higher profit profile should be

accepted for investment. But this approach suffers from the following limitations.

1) The term profit is ill defined. There are different concepts used for the term profit

i.e. earnings before interest and tax (EBIT), earnings after tax (EAT) etc. This

approach fails to recognize the form of profit (ie.ambiguity).

2) It didn’t take in to consider the timing of profit - that is time value of money.

Suppose the total pay off profiles of two different projects may be same, then both

of them are equally acceptable even if their pattern of flows is different. (I.e.

ignore timing of benefits).

3) No provision for certainty of benefits. As the future is uncertain, we have to

consider the certainty of occurrence of the profit before making a valuable

investment. (No importance to quality of benefits).

II) Modern Approach(Wealth Maximization)

In order to overcome the limitations of traditional approach the modern

approach of financial management were developed. According to this approach wealth

maximization is the main objective of financial management. The term wealth

indicates the value of investment of share holders. It is the difference between the

present value of cash inflows and present value of cash outflows or cost of investment.

It is also known as value maximization or Net Present Worth maximization.

Advantageous of Modern Approach

1) The term wealth is clearly defined.

2) Present value is computed by discounting the future cash inflows there by this

approach consider the time value or time adjusted value of money.

3) By selecting a suitable discount factor it also provides importance to the quality of

benefits. This is because the discount factor includes the premium for uncertainty

or risk also.

Time value of money

One of the main factors that will be considered for making investment is time

factor or time value of money. As the time passes the value of money will be

changing. This principle simply indicates Re 1 today is not equal to Re1 tomorrow.

That is sum of money received today more than its value received after sometime.

There are two techniques for measuring the time influence on value of money.

1) Compounding

2) Discounting

Compounding

Compounding is the process of ascertaining the future value of a present sum of

investment. The Compound value of Re1 at a particular rate for a particular period is

called Compounding factor. This can be mathematically expresses as:-

Compounding factor = [1+r] n

Where r = rate of return from investment

n = number of years

e.g. if we invest Rs 1000 today shall be come Rs 1210 after two years at the rate of

10% compound interest

1000(1+0.1)2

=1210

Discounting or present value

Discounting is the process of ascertaining the present value of a future sum

which is gone to be received. It is the opposite of compounding and the present value

of Re1 after some time at a particular rate is called Discount factor or present value

factor.

1

Discounting factor PV = ------------

[1+r] n

E.g. the present value of Rs 1000 which will be received after two years shall be Rs

826 at10% discount rate.

1000. 1000

PV = --------------- = ---------- = Rs 826

(1+ 0.1)2

1.21

Reversible investments

Reversible investments mean the investments which can be reversed and

marketable. The real value of such investment shall always be equal to the present

value of the future income from it. This value is also called fundamental value

intrinsic value.

Financial forecasting

Financial forecastingmeans a systematic projection of the expected action of finance

through financial statement. The merits of the financial forecasting are

1) It can be used as a control device to fix the standards and evaluating the result

thereof.

2) It helps to explain the requirement of funds for the firm.

3) It helps to explain the proper requirement of the cash and their optimum

utilisation.

Tools of Financial Forecasting

I) Pro forma income statement

Pro forma income statement is a projection of income for a period of time in future

which is to furnish a fair and reasonable estimate of expected revenue, cost profit, tax,

dividend, etc. It is prepared around the estimate of the expected sales for the forecast

period. Forecasting of various items is done in the following way.

1) Sales on the basis of marketing research and economic survey.

2) Preparation of production schedule for estimating cost of production.

3) Cost goods sold on the basis of past sales.

4) Administrative and selling expenses estimated on suitable basis.

II) Pro. Forma Balance sheet

Preparation of proforma Balance sheet is based on

1) Net worth of the company

2) Comparison of projected assets with total source of funds

3) Liabilities based on the past indication.

4) The net investment in each component of assets of the company.

III) Cash budget

Cash budget is statement of plan which shows the expected receipt, payment

and payment of cash for a definite future period. It is prepared after the preparation of

all functional budgets. The main objectives of preparing cash budgets are

1) To see that adequate amount of cash are available for capital as well as

revenue expenditure.

2) To make an arrangement of cash in advance, if there is any expected shortage

of cash.

3) To see that the surplus amount of cash, if employed in any profitable

investment outside the business.

Advantageous of Cash Budget

1) It helps to identify the amount and the time of cash needed by the concern.

2) It informs how much additional cash is required during the peak period and the

possible ways to raising that cash.

3) Benefits through cash discount can be derived by making payments before due

date.

4) It expresses either the deficit or surplus of cash, so surplus cash can be

invested properly.

Methods of Preparing Cash Budget

1) Receipt and payment Method

2) The adjusted profit and loss method

3) Balance sheet method.

Adjusted net income method of cash forecasting

This method of forecasting seeks to estimate the firm’s need for cash at some

future date and indicates whether this need can be meet from initial source or not. In

this method with the opening balance of cash estimated cash receipts are added. Then

cash payments deducted from it in order to find out of the closing balance. This source

of cash balance may be met from business income, borrowings, sale of equity shares,

non cash charges such as amortization etc and payment of cash included capital

expenditure, increase in current assets, repayment of loan etc.

Principles of financial plan

1) Simplicity

2) Long term view

3) Optimum usage of resources

4) Fore right

5) Provide for contingencies

6) Flexible

7) Liquid

8) Economical

Functions of financial system

1) Provision of liquidity- Provide platform for conversion of monitory assets into

cash readily without loss.

2) Mobilizations of savings

3) Channelisation of funds to productive activity

4) Efficient utilization of funds

5) Diversified investment opportunities.

Causes of financial distress

1) Increased cost of production

2) Increase in inflation rate

3) Increase in general interest rate

4) Reduction of surplus.

Financial restructuring

Financial restructuring involved in significant reorientation, reorganization or

realignment of the assets and liabilities of the organisation through conscious

management action with the objective of significant improvement in the quality and

quantity of future cash inflows. The objective of this process also includes the increase

in the organization’s bargaining power and synergies.

ORGANISATION CHART FOR FINANCE FUNCTION

SPECIAL REPORT

&STUDIES

COST

FUNDS

BOARD OF DIRECTORS

CHAIRMAN/ MANAGING DIRECTOR

FINANCE MANAGER

TREASURER

CREDIT MANAGEMENT

PERSONAL & TRUST

MANAGEMENT

AUDITING

PLANNING & BUDGETING

PROFIT

ACCOUNTING

CONTROLLER

Module 2

Capital budgeting

Capital budgeting is the decision relating to the investment in fixed asset or

long term project of the business. Here the financial manager is evaluating the

expenditure decision which involves current out lay but is likely to produce benefits

over a period of time in future. The basic features of capital budgeting are

Key Features

1) Potentially large anticipated profit or benefit.

2) Relatively high degree of risk.

3) Relatively long time period between the initial outlay and the anticipated return.

While making this type of decision the manager has to consider the risk return trade

off.

Importance

1. Decides future destiny of the company.

2. It affects the company's future cost structure.

3. Once made, are not reversible without much financial loss.

4. It involves huge cost of investment.

Types of Capital Budgeting Decisions

• Accept-reject decisions

In this decision only one project are under consideration. That project yield rate of

return grater than certain required rate of return.

• Mutually exclusive project decisions

Here More than one similar project is under consideration and the management

wants to accept only one. The project which offers higher rate of return than that of

others in the group should be accepted.

• Capital rationing decision

Most of the firms have fixed capital budget with limited amount funds. A large

number of investment proposals compete for this limited fund. So the firm should

allocate funds to various projects in a manner that it maximizing long run return.

Stages of capital budgeting

1) Need realization.

2) Selection of program –well defined procedures.

3) Collection of data and evaluation.

4) Follow up action.

5) Cost – cost of investment, running and maintenance cost.

6) Benefit- cash inflows.

Principles of Capital budget

1) Budget should increase revenue(profitability)

2) Liquidity(less risky)

3) Flexibility

4) Economical( capacity to reduce cost)

5) Meaningful and viable.

Factors affecting capital investment

1) Cost of the new project.

2) Installation charge

3) Working capital

4) Proceeds from sale of assets

5) Tax effect (tax shall have an impact on the cash inflows from business. This is

because cash inflow means profit after tax plus depreciation.)

6) Investment allowances. This means special allowance given to the enterprise

under Income Tax Act on the cost of new machinery and equipments.

Capital budgeting techniques

Capital budgeting techniques are divided in to two categories

1) Traditional techniques

2) Modern techniques (Time adjusted technique or discount cash flow method.)

I) Traditional techniques

In the traditional method we take the absolute value of the earnings and no

importance is given to the time value of money and quality of benefits. In this

category two main techniques are applied.

1) Pay back period.

2) Average Rate of Return or Accounting Rate of Return (ARR).

1) Pay back period –

Pay back period represents the time period required for recouping the original

cost of investment. While taking it as a capital budgeting technique, we have to accept

the project which shall recoup the amount of investment with in the time period

specified for it. In case of mutually exclusive projects, a project with lower pay back

period should be selected.

If annual cash inflows during the project period are equal, we can apply the

following formula for ascertaining payback period.

Cost of investment

Pay back period = --------------------------------------------

Average annual cash inflows

Merits

1. It is simple and easy to apply.

2. It is a rough and ready method for dealing with risk.

3. It most suitable in the case of dynamic industries.

Demerits

1. No consideration for the time value of money.

2. Overlooks beyond the pay back period.

2) Average Rate of Return (ARR)

Average rate of return represents the rate of return that can be generated by the

project during the project period. It is symbolically represented as ARR - It is the rate

of average accounting profit to the average cost of investment over the life of the

project.

Average Annual profit

Average rate or return (ARR) = -------------------------------------

Average investment

Original cost of investment – salvage value

Average investment = ---------------------------------- ----------------+ salvage value 2

Acceptances criteria

In the case of project which offer the rate of return at least equal to the rate of

return expected shall be accepted. In the case of mutually exclusive projects a project

with higher ARR shall be selected

II) Modern Techniques (Time adjusted techniques)

This method is also known as discounted cash flow method. The main

advantage of this technique is that it considers the time value of money. Following are

the important time adjusted techniques.

1. Net Present Value

Net Present Value is the difference between the present value of cash inflows and

present value of cash outflows. For accepting a project the NPV should be at least

zero. In the case of mutually exclusive project, a project with higher NPV should be

selected.

2. Profitability Index (a relative measure)

It is the ratio of the present value of cash inflows and present value of cash

outflows. When the cost of investment of two projects are not equal, NPV may not be

used a capital budgeting evaluation tool. This is because two projects with different

cost of investment may provide you the same NPV. In such case for evaluating the

proposals we use another tool called benefit cost ratio.

Present value of cash inflows

Profitability Index(PI) = --------------------------------------------

Present value of cash outflows.

3. Internal Rate of Return(IRR)

IRR is the rate of return, at which the present value of cash inflows equal to the

present value of cash outflows. At this rate NPV shall be ‘0’ and Profitability

Index(PI) shall be ‘1’.

The use of IRR as a criterion to accept capital investment decision involves the

comparison of actual IRR with the required rate of return (cut off). If the IRR exceeds

the cut off rate the project shall be accepted.

PV (cash inflow) at LR - PV (cash outflow)

IRR = LR + ---------------------------------- ------------------------------------*r

Difference between cash inflows at two discount levels

LR = Lower discount rate

r = difference in discount rate

Merits

1) Consider the time value of money.

2) Comparison between projects requiring different capital investments is

possible.

3) Consider directly the amount of expenses and revenues over the project life.

Demerits

1) Difficult in application.

2) Based on the presumption that cash inflow can be invested at the discounting

rate in the new project which doesn’t always right

ModifiedInternal Rate of Return (MIRR)

MIRR or Terminal internal rate of return (TIRR) is developed for overcoming

the limitation of IRR. MIRR is the compound rate of return that applied when the

initial outlay accumulation to the terminal value. This criterion is currently used in

advanced nations.

In this criterion it is assumed that each of future cash inflows is immediately

reinvested in another project at a certain rate of return. In other words net cash inflows

outlays are compounded foreword rather than discounting backward as followed in the

net present value (NPV).

The present value of compounded reinvested cash inflows are computed which

is called terminal value. IRR is that discount rate at which the terminal value of the

project equal to present value of cost of investments.

In IRR we consider only one aspect of time value of money that is discounting,

where as in MIRR we adjust the time value of the money in cash inflows through both

discounting and compounding processes.

Cost of capital

In simple words cost of capital means the price paid for obtaining and using

capital. In capital budgeting decision when we use IRR as an appraisal tool we

compare the IRR with the cost of capital there by it provides a yard stick to measure

the worth of investment proposal. It is also known as cut off rate, target rate, hurdle

rate, or minimum rate of return.

In operational terms the cost of capital refers to the discount rate that would be

used in determining the present value of estimated future cash proceeds and eventually

deciding whether the project is worth to undertake or not. In this sense it can be

defined as the minimum rate of return that the firm must earn on its investment for

making the market vale of the firm remain unchanged.

The capital structure of the company composed of several elements like

preference shares, equity shares, debentures etc. The cost capital of each source or

component is called specific cost of capital (cost of equity, cost of preference, cost of

debt etc). When these specific costs are combine together then it is called overall cost

of capital or weighted average cost of capital or composite cost of capital (Overall cost

of capital is the weighted average of specific cost of capital).

Weighted Average Cost of Capital (Traditional view)

Optimum capital structure is assumed that at a point where WACC is

minimum. Till the optimum level reaches, a firm can rise its debt component to

minimize WACC and for increasing returns to the shareholders. After this level any

further increase in debt increases risk to the equity shareholders thereby the overall

cost of capital start rising.

Computation of Cost of Capital

I) Cost of Debt

Computation of cost of debt is comparatively easy. Cost of debt is the cost of

fund raises through the issue of debentures or arrangement of loans from financial

institutions.

Cost of perpetual debt

There are two approaches

1) Before Tax

I

Cost of debt (Kd) = ------------

SV

2) After Tax I

Cost of debt (Kd) = ------------ (1-t)

SV

Sv = sale price of bond or debenture

I = annual interest payment

t = tax rate

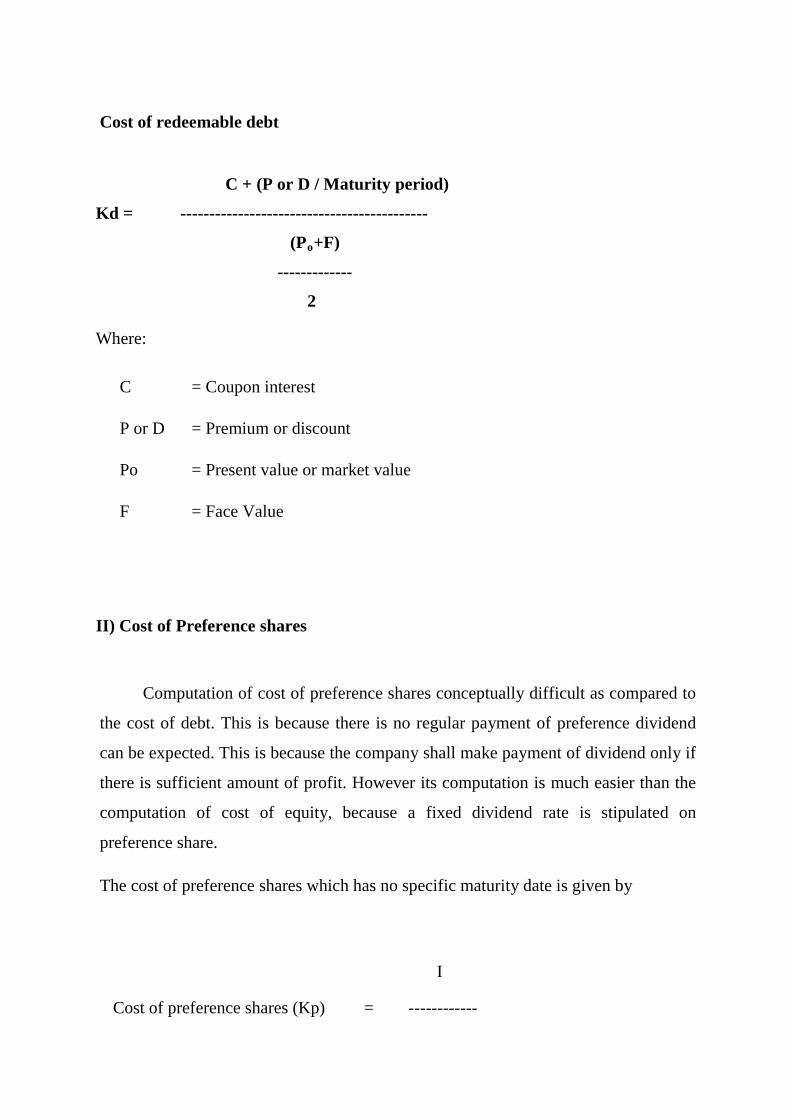

Cost of redeemable debt

C + (P or D / Maturity period)

Kd = -------------------------------------------

(Po+F)

-------------

2

Where:

C = Coupon interest

P or D = Premium or discount

Po = Present value or market value

F = Face Value

II) Cost of Preference shares

Computation of cost of preference shares conceptually difficult as compared to

the cost of debt. This is because there is no regular payment of preference dividend

can be expected. This is because the company shall make payment of dividend only if

there is sufficient amount of profit. However its computation is much easier than the

computation of cost of equity, because a fixed dividend rate is stipulated on

preference share.

The cost of preference shares which has no specific maturity date is given by

I

Cost of preference shares (Kp) = ------------

SV

Redeemable preference shares

PD+ (P or D / Maturity period)

Kp = -------------------------------------

(Po+F)

---------

2

PD = Pref.dividend.

P or D = Premium or discount

Po = Present value or Mkt. value

F = Face Value

III) Cost of Equity shares

Cost of equity capital, conceptually specializing the most difficult and

controversial to measure the cost. It is denoted by the symbol Ke. It can be defined as

minimum rate of return that a firm must earn on the equity financed portion of an

investment project in order to leave the unchanged market price of the shares. There

are two approaches employed to compute the cost of equity capital. They are

1) Dividend approach

According to this approach cost equity is the discount rate that equates the

present value of all expected future dividend per share with the net proceeds the sale

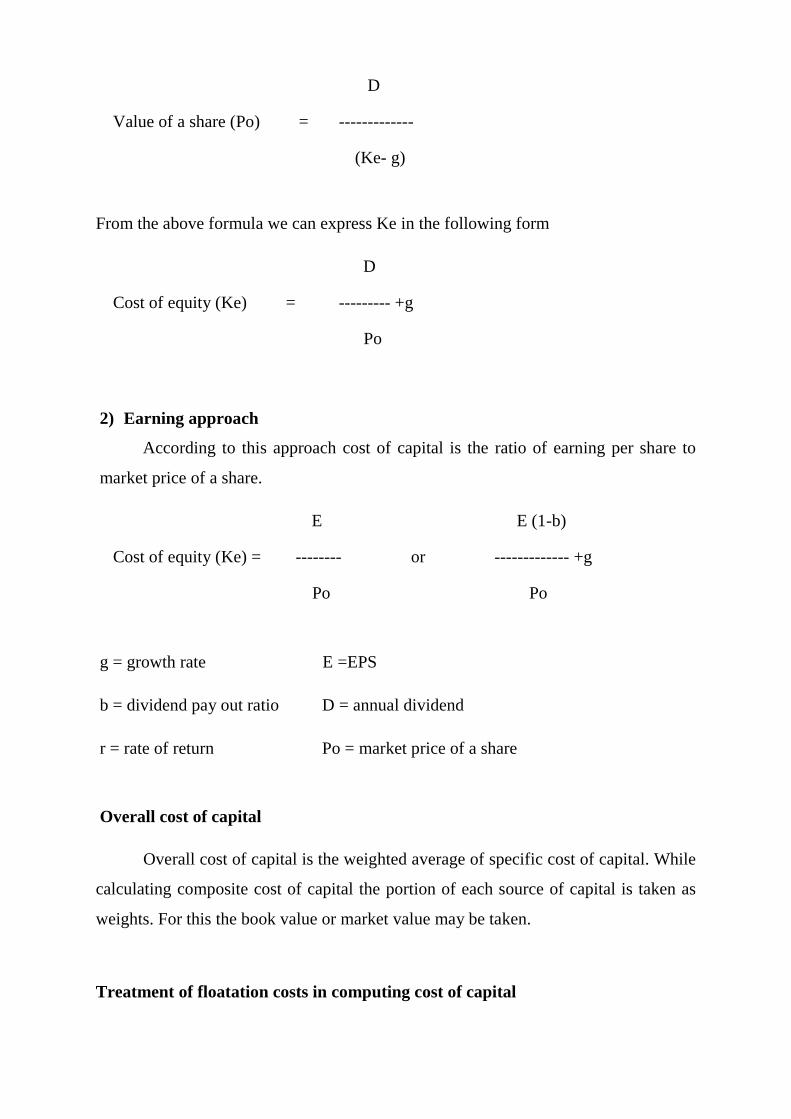

of share (market price). According to this approach the value a share

D

Value of a share (Po) = -------------

(Ke- g)

From the above formula we can express Ke in the following form

D

Cost of equity (Ke) = --------- +g

Po

2) Earning approach

According to this approach cost of capital is the ratio of earning per share to

market price of a share.

E E (1-b)

Cost of equity (Ke) = -------- or ------------- +g

Po Po

g = growth rate E =EPS

b = dividend pay out ratio D = annual dividend

r = rate of return Po = market price of a share

Overall cost of capital

Overall cost of capital is the weighted average of specific cost of capital. While

calculating composite cost of capital the portion of each source of capital is taken as

weights. For this the book value or market value may be taken.

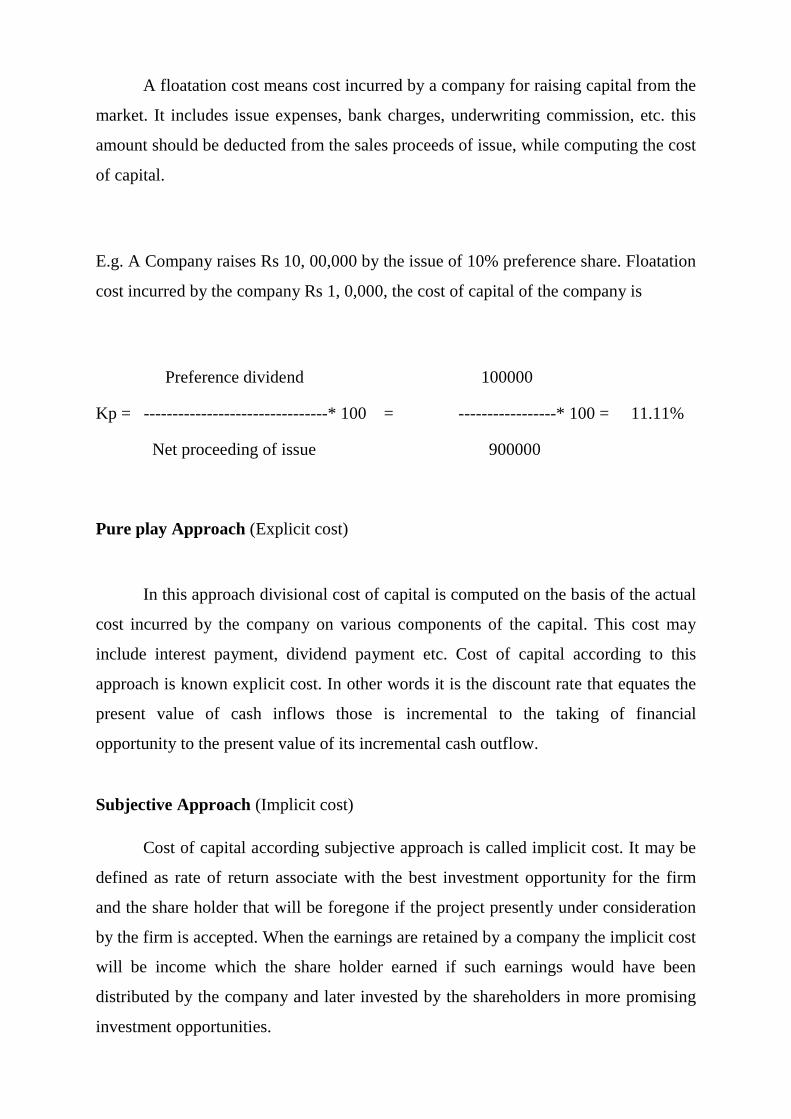

Treatment of floatation costs in computing cost of capital

A floatation cost means cost incurred by a company for raising capital from the

market. It includes issue expenses, bank charges, underwriting commission, etc. this

amount should be deducted from the sales proceeds of issue, while computing the cost

of capital.

E.g. A Company raises Rs 10, 00,000 by the issue of 10% preference share. Floatation

cost incurred by the company Rs 1, 0,000, the cost of capital of the company is

Preference dividend 100000

Kp = --------------------------------* 100 = -----------------* 100 = 11.11%

Net proceeding of issue 900000

Pure play Approach (Explicit cost)

In this approach divisional cost of capital is computed on the basis of the actual

cost incurred by the company on various components of the capital. This cost may

include interest payment, dividend payment etc. Cost of capital according to this

approach is known explicit cost. In other words it is the discount rate that equates the

present value of cash inflows those is incremental to the taking of financial

opportunity to the present value of its incremental cash outflow.

Subjective Approach (Implicit cost)

Cost of capital according subjective approach is called implicit cost. It may be

defined as rate of return associate with the best investment opportunity for the firm

and the share holder that will be foregone if the project presently under consideration

by the firm is accepted. When the earnings are retained by a company the implicit cost

will be income which the share holder earned if such earnings would have been

distributed by the company and later invested by the shareholders in more promising

investment opportunities.

So pure play approach followed when funds are raised and subjective approach

follows whenever funds are used by the firm.

Principle or guidelines relates to estimation of incremental cash flows

Cash flows must be measured in incremental terms. In estimating the

incremental cash flows the following guidelines must be kept in mind

1) Consider all incremental effect

2) In addition to the direct cash inflow of the project, all its incidental effect on the

rest of the firm must be considered.

3) Ignore sunk cost – Sunk cost means the past cost which cannot be recovered and is

not relevant for new investment decision. This is supported to the famous phrase

“buy gone are buy gone.

4) Include opportunity cost- The opportunity cost of a resource is the present value of

net cash inflows that it can be derived it, if it were put it to its best alternatives.

Such opportunity cost should charge to the proposal project.

5) Allocations of overhead cost to project- Cost which is indirectly related to a

project is referred to as its overhead cost. It includes item like administrative

expenses, managerial salary, legal expense etc. Accounts normally allocate this

cost to various projects on some suitable basis. So a portion of overhead cost of the

firm is usually allocated to the proposed project also.

CAPITAL ASSET PRICING MODEL

The Capital Asset pricing model was developed in 1960 by 3 researchers,

William Sharpe, John Lintner and Jan Mossin independently. As a result this model is

also known as Sharp - Lintner-Mossin model.

The CAPM is really an extension of the port folio theory of Markowitz. The

portfolio theory is really a description of how rational investors should build efficient

portfolios and select the optimal port folio. The CAPM derives the relationship

between the expected return and risk of individual securities and that of portfolios in

the capital market if everyone behaved in the way as portfolio theory suggested.

CAPM gives the nature of the relation between the expected return and the systematic

risk of a security and pricing of assets.

Assumptions of CAPM

1. The investor’s objective is to maximize the utility of terminal wealth, not to

maximize wealth.

2. Investors make choices on the basis of risk and return.

3. Investors have homogeneous expectations of risk and return.

4. Investors have identical time horizon.

5. Information is freely and simultaneously available to investors.

6. The investor can lend or borrow any amount of funds desired at a rate of interest

equal to the rate for risk less securities.

7. There are no taxes, transaction cost, restrictions on short rates, or other market

imperfections.

8. Total asset quantity is fixed and all assets are marketable.

CAPM states that the unsystematic risk of a portfolio can be diversified through

proper construction of portfolio. Even if we construct a portfolio comprises of all

available securities in the market, still there is a risk element which we call systematic

risk. Since such risk can not be diversified through portfolio construction, the real risk

that is met by the investor while making his portfolio investment is systematic risk. So

we have to compare only the market risk and return of a portfolio instead of total risk,

while making an investment.

According to CAPM the expected return of a portfolio is equal to –

E (Rp) = Rf + β (Rm-Rf)

Where E (Rp) = Expected return of the portfolio.

Rf = Risk free rate of return.

β = Market risk co-efficient

Rm= Return on market portfolio

So return of every portfolio consists of two components- Risk free rate of return

and market risk premium. Risk free rate of return is the return offered on Govt.

securities and market risk premium is closely related to the degree of sensitivity

shown by the portfolio towards the market trend. Higher value of beta indicates larger

sensitivity, so larger the market risk and higher will be the market risk premium.

Lower value of beta is the indicator of lower market risk and lower premium for it.

Capital Market Line (CML)

Capital market line is the graph line which indicates the relationship between the total

risk and return of all efficient portfolios in the portfolio opportunity set. It represents

the risk – return relationship in portfolio of securities explained by the Markowitz

model. This line indicates the risk-return relationship of only efficient portfolios but

not inefficient portfolios and individual securities. The mathematical form of risk

return relationship established by CML is:

Rp= Rf+ (Rm-Rf)σp/σm

Security Market Line (SML)

Security market line is the graph line which indicates the relationship between

the market risk and return of all portfolios those an investor can construct. It

represents the risk – return relationship in portfolio of securities explained by the

CAPM. This line indicates the risk-return relationship of all portfolios (whether

efficient or not) and also individual securities. The algebraic form of this line is :-

Rp = Rf+ β (Rm-Rf)

ARBITRAGE PRICING THEORY (APT Theory)

This theory was developed by Stephen Ross. This theory explains the nature of

equilibrium in the asset pricing in a lesser complicated manner. With fewer

assumptions compared to CAPM.

Assumptions

1. Investors have homogeneous expectations.

2. They are risk averse and utility maxi misers.

3. Perfect competition prevails in the market and there is no transaction cost.

According to Stephen Ross return of the securities are influenced a number of macro

economic factors. The factors are

a) Inflation

b) Interest Rate

c) GDP, etc

Here the investor has no need to hold market portfolio and they indulge in

arbitrage process, moving the price upwards if securities are held long and driving

down the prices of securities if held in short position till the elimination of arbitrage

possibilities. An arbitrage portfolio is constructed with out any additional financial

commitment. The main concept behind the application of this model is that the factors

those have impact on a group of securities may not affect another group of securities.

As a result as far as the arbitrage process is possible investor can maximise his return

through constantly revised portfolio.

Risk

Risk means the chance of loss. Normally the term risk is different from the

term uncertainty. Usually we can find the probability of losing something and we call

that chance or that probability is risk. But in the case of a certainty nothing can be

predicted, so no probability computation is possible. But in security analysis we use

both the term risk and uncertainty inter changeably. Here risk means the uncertainty

surrounding the future stream of return and repayment of capital. If an investment’s

returns are fairly stable, it is considered to be a low risk investment. But when the

return from an investment is fluctuating widely then it is called risky investment. The

risk and return are positively correlated. Higher the risk higher will be the return and

lower the risk lower will be the return. When we expect a return from a risky

investment the risk should be much higher than that of a low risk investment.

Elements of risk

The elements of risk may be broadly classified into two groups.

1. Systematic Risk - This type of risks are external to a company and effect a large

no. of securities simultaneously. These risks are mostly uncontrollable in nature. Risk

produced by external factors is known as systematic risk.

2. Unsystematic Risk - There are certain factors which are internal to the company

and affect only that company. The risks due to these factors are called unsystematic

risk. These risks are controllable in nature. By building an efficient portfolio we can

diversify these risks. So

Total risk = systematic risk + unsystematic risk (specific risk)

Types of systematic risk

Systematic risk is mainly divided into three,

Interest Rate Risk

Interest rate risk is a systematic risk that particularly affects debt securities like

bonds and debentures. It is the devaluation in bond prices due to the increase in the

market interest rate. When the market rate of interest move up the interest rate offered

by a bond investment then that bond investment will be lose its value. That loss is

called interest rate risk. It also affects equity shares. When the market interest rate

increases, the debt instruments become more attractive. Then the investors shall

dispose their shareholdings and utilize the proceeds for making investment in debt

instruments. This action will cause decline in the value of stocks.

Market Rate Risk

Market risk is the increased variability of the investor return due to the

alternating movements of the share markets. A general decline in share price is

referred to as bearish trend. Due to these variations in stock market movement the

investors return will also be varied. The fluctuations in investor return due to these

alternative market movements is called market risk. The reasons for these market

fluctuations may be changes in the social economic and political conditions, changes

in the investor’s attitude and expectations etc.

Purchasing Power Risk

Purchasing power risk refers to variations in investor returns due to increase in

inflation rate. This risk will affect entire investment securities in the economy.

Moreover the hike in the inflation rate shall reduce the value of all assets including

securities.

The two important causes of inflation are increase in the cost of production and

increase in demand for goods. When demand is increasing but supply cannot be

increased the price of the goods increases. The inflation due to this excess demand is

called demand pull inflation. Similarly when the cost of production increases the price

will be increased which lead to inflation and this inflation is called cost push inflation.

Both of these inflations shall affect the purchasing power of currency there by the

value of all investment in an economy.

Types of unsystematic risk (specific risk)

There are mainly two types of unsystematic risk.

Business Risk

Business risk means a risk due to the poor operating conditions faced by a

company. When a company’s operating conditions become worse etc. the operating

cost will be increased which in turn bring into a reduction in its operating income.

Since this risk element is associated with the securities of only poor performing

companies, we can avoid it through portfolio diversification. So this risk is a part of

diversifiable risk. (Simply we can say unsystematic risk means risk due to the poor

operating efficiency and business performance of a company.) . As this risk element is

associated with the securities of only poor performing companies, we can avoid it

through portfolio diversification. So this risk is a part of diversifiable risk.

Financial Risk

Financial risk is the second part of a unsystematic risk. It is the risk arises due

to the use of the debt in total capital structure of a firm. When there is a debt

component in the capital structure of a company, there may be variability in the

returns available to the equity share holders.

If the companies rate of return higher than the interest rate payable on the debt,

earning per share would increase. If the rate of return is lower than the interest rate

earning per share would be decreased because interest is a compulsory payment.

The increase or decrease in earning per share due to the presence of debt capital

in the total capital structure of a company is referred to as financial risk. This risk is

also an avoidable risk because a company is free to finance its activity without

resulting to debut.

MODULE 3

The 2nd important decision taken by financial manager is financing decision.

This decision relates to the source from which the firm has raised necessary finance

for meeting its requirements. There two terms connected with this decision.

1) Capital structure

2) Financial structure

Capital structure

Capital structure means the ratio between different forms of long-term capital or funds

of the firm such as equity capital, preference capital, reserve & surplus, debentures

etc. It relates only to the long term solvency position of the firm. Decision relating to

capital structure is very important for a firm. This is because capital structure is

significant to the maximization of corporate wealth of the firm.

Financial structure

It refers to the way the firm’s assets are financed. It includes both long-term

and short-term (internal and external) source of funds. But capital structure relates to

the long term source of funds only.

Optimum capital structure

It is that Capital structure or debt equity mix which gives the maximum value

to the firm in the market. Use of debt in the capital structure of the firm shall increase

EPS as the interest on debt is tax deductible which leads to increase in share price. At

the same time it causes financial risk to the firm. Optimum capital structure strikes a

balance between the risks and return and thus examines the price of the share.

Factors determining the capital structure

• Trading on equity

The benefit or advantageous due to equity share holders on account of the use

of debt content in total capital structure is called trading on equity. In other wards

when the leverage is favorable, then it is called trading on equity.

• Retaining control

The capital structure of a company is also influenced the promoter’s objective

of retaining their control in the firm. Some promoters want to raise funds from the

public without losing their effective control in business. If the promoter wishes to

retain control, they may raise larger part of the capital from debt source i.e. non

equity source.

• Period of finance

If the funds are required for short period it is better to raise capital by the issue

of short term debt securities or arrange loans from bank. On the other hand, if the

requirement is for along period equity is beneficial.

• Cost of financing

Cost of financing is a very important factor for determining the capital structure

of the company. The generally accepted principle is that the company must incur the

minimum possible cost in interest, dividend, etc. In this contest, one must born in

mind that debenture is the cheapest source of capital. This is because rate of interest is

fixed and can be deducted from profit for tax purposes. Other factors include -

• Nature of the company

• Elasticity of capital structure

• Legal requirements

• Risk.

• Income.

• Tax consideration.

• Cost of capital.

• Investor’s attitude.

• Timing.

• Profitability

• Growth rate.

• Govt. policy.

• Marketability.

• Company size.

• Financing purpose.

Theories of Capital structure

There are mainly five theories explaining the capital structure, cost of capital

and value of firm.

• Net income approach.

• Net operating income approach.

• Modigliani and Miller approach.

• Traditional approach (Weighted average cost of capital)

• Pecking order theory.

● Net Income(NI) Approach (Durand David)

This approach is suggested by Durand David. According to this approach,

Capital structure of a company is relevant in valuation of the firm. A change in the

capital structure causes a corresponding change in overall cost of capital as well as the

total value of firm.

Here market Value of firm (V) = S+B

S (Market Value of equity) = Earnings available to equity sharer holders (NI)

----------------------------------------------------------

Capitalisation rate [cost of equity (Ke)]

B (Market Value of debt) = V-S

Argument -Higher debt component in the capital structure results in decline in the

overall cost of capital which in turn increases EPS and value of the firm.

Assumptions

a. No corporate taxes.

b. No change in risk perception

c. Cost of debt < cost of equity

● Net Operating Income (NOI) Approach (Durand David) This approach is also suggested by Durand David. According to this approach

market value of firm is not at all affected by capital structure changes i.e. Value of the

firm is independent of capital structure. The market capitalizes the total value of the

firm and so the debt equity shall not affect its overall cost of capital. Market value of

the firm depends on EBIT and is fully independent of the financing mix.

According to this approach market value of firm =

Net operating income (EBIT)

-----------------------------------------

Total capitalisation rate (Kc)

Value of equity = Value of firm - Value of debt

Assumptions

a. No corporate taxes.

b. Cost of debt is also constant.

c. Kc remains constant and Ke increases with increase in debt.

● Modigliani and Miller approach

Cost of capital is independent of capital structure and so there is no optimum

value. MM proposition supports the NOI approach relating to independence of the

cost of capital from the valuation of the firm at any level of debt equity ratio. The

significance of their hypothesis lies in the fact that it provides behavioural justification

for constant overall cost of capital.

Prepositions

1. Market valueof firm is independent of its capital structure, changing the gearing

ratio cannot have any effect on company’s annual cash inflow.

2. Rate of return expected by shareholders increases linearly as the debt equity ratio

increases.

3. Cut off rate for new investment will always be average cost of capital and is

independent of financing decision.

Assumptions

1. Free buy & sale.

2. Perfect and efficient market.

3. Kd<Ke

4. Interest rates are equal.

5. No transaction cost, personal taxes and corporate income taxes.

6. Homogeneous risk classes.

7. Investors are rational. i.e. they have same expectation of firm’s net operating

income(EBIT)

8. No retained earnings. i.e. dividend pay out ratio is 100%

The basic preposition among MM approach is that the total value of the firm

must be constant irrespective of the debt equity ratio. Similarly, cost of capital as well

as market price of shares must be the same regardless of the financing mix.

The operational justification for MM hypothesis is the arbitrage process. The

term arbitrage refers to an act of buying security in one market at lower price and

selling another market at high price. As a result equilibrium is restored in the market

price of security in different market.

MM illustrates arbitrage process with reference to valuation in terms of two

firms which are exactly similar in all respect except leverage. Such homogeneous

firms are according to MM perfect substitutes. The total value of homogeneous firms

which differ only in respect of leverage cannot be different because of the operation of

arbitrage. The investors of firm whose value is higher sell their shares and buy the

shares of the firm whose value is lower. Then the investors will be able to earn same

return at lower investment with the same perceived risk. Simultaneous buy and sell of

securities continue till the market price of two identical firms become identical. Thus

the presence of debt component in the capital structure of the firm shall not have any

effects in the market value.

Arbitrage process

It is the process of buying a security from a market where it has lower price and

sell it in the other market where it fetches higher price. It is speculation activity. The

person who is engaged in this process is called Arbitrager.

● Traditional Approach(Weighted average cost of capital).

It is the combination of Net incomeApproach (NI) and Net operating

incomeApproach (NOI). It supports Net incomeApproach is that up to a particular

point the capital structure affects the cost of capital and its valuation. Optimum capital

structure is assumed that at a point where WACC is minimum. Till the optimum level

reaches, a firm can rise its debt component to minimize WACC and for increasing

returns to the shareholders. After this level any further increase in debt increases risk

to the equity shareholders thereby the overall cost of capital start rising.

● Pecking Order Theory (Donaldson)

• Dividend policy is sticky.

• Firms prefer internal to external financing.

• If firms require external financing, they will issue the safest security i.e. “debt”

• As the firms seeks more external financing, it will work down the pecking

order of securities from safe to risky debt and finally to equity as a last resort.

Business finance

It is the activity concerns with planning, rising, controlling and administrating

the funds used in the process. It involves planning and raising as well as effective

utilisation of funds of the business.

Financial planning

1) Estimating the amount capital to be raised.

2) Source from which is raised.

3) Designing the financial policies

Basis of capitalisation

Capitalisation is the sum of the par values the stock and outstanding. This term is used

only in respect of companies. There are two recognized theories of capitalisation.

1) Cost Theory

2) Earning Theory

Cost Theory

According to this theory the total amount of capitalisation of a new company is

arrived at by adding up the cost of fixed assets, working capital, preliminary expenses.

Earning Theory

According to this theory the true value of an enterprise depends on it earning

capacity. The worth of a company is not measured by the capital raised, but by the

profit generated by employing the capital.

Leverage

Leverage refers to means of accomplishing power for gaining an advantage. It

is the employment of fixed assets or funds for which a firm has to meet fixed costs or

fixed rate of interest obligation irrespective of the debt equity mix. Leverage is three

types

1) Financial Leverage

2) Operating leverage

3) Combosite leverage

● Financial Leverage The ability of a firm to use fixed financial charges (interest bearing securities)

to magnify the effect of change in Earning before Interest and Tax (EBIT) on Earning

per share (EPS).it is the process of using fixed cost of funds for increasing the return

to the share holders.

Earning before Interest and Tax (EBIT)

Financial Leverage (FL) = --------------------------------------------------------

Earning before Tax (EBT)

%change in EPS

Degree of Financial Leverage DFL = --------------------------- >1

%change in EBIT

1 2 3

Eqty. 50 25 12.5

15%Debt -- 25 37.5

----------- ------------ ----------

project cost 50 50 50

------ ------- --------

-Net cash flow @24% 12 12 12

Less interest on debt -- 3.75 5.625

----- -------- ---------

12 8.25 6.375

Return on eqty(Dd/Eqty 24% 33% 51%

Return on debt nil 15% 15%

WACC

( Kex% eqty+Kdx%debt) 24% 24% 24%

Value of firm 50 50 50

● Operating leverage

The ability of a firm to use fixed operating charges to magnify the effect of

change in sales on its Earning before Interest and Tax (EBIT). In this situation

percentage change in profit on account of increase in sales shall be higher than

percentage change in sales volume.

Contribution

Operating Leverage O L = ------------------

EBIT

%change in EBIT

Degree of Operating Leverage DOL = --------------------------- >1

%change in sales

● Composite leverage (combined leverage)

The combination of financial leverageand operating leverage is called

combined leverage. The risk associated with the combined leverage is known as total

risk.

Degree of combined Leverage DCL = DFL*DOL

%change in EPS %change in EBIT

Degree of Composite Leverage DCL = ------------------------- * ----------------------

%change in EBIT %change in sales

%change in EPS

i.e. DCL = -------------------------

%change in sales

Point of indifference

It refers to that EBIT level at which earning per share remains same

irrespective of the debt equity mix. At this level cost of debt and cost of equity shall

remain same. Point of indifference find out from following equation.

(x- I1)(1-T)-PD = (x-I2) (1-T)-PD

----------------------- -------------------------

S1 S2

x = Point of indifference

I1 = interest rate under plan 1

I2 = interest rate under plan 2

T = Tax rate

S1 = no of equity shares in plan 1

S2 = no of equity shares in plan 2

PD= preference dividend

Dividend policy

The 3rd function of finance is called dividend policy decision. Dividend is the

portion of divisible profit (net earnings) of the company. It is the portion of the profit

distributed among the share holders as a return of their investment.

In dividend policy decision the financial manger has to decide whether to

declare dividend to share holders, if yes to what extent it should be done so. Dividend

payout ratio means the ratio of dividend to total earnings made by the concern.

Determination of dividend pay out ratio is the main decision to be taken by the

financial manger with respect to the dividend policy. This definitely depends on the

preference of shareholders and investment opportunities available with in the firm.

The dividend policy of firm may have direct impact of the value of firm or

market value of the share. If the company declare dividend, the share holder receive

an income for their commitment. So the market value of the firm is increased. The

dividend policy i.e. determination of the dividend payout ratio which gives maximum

value to the share of the firm is called optimum dividend policy.

Importance

A major decision of FM is the dividend decision. This is because it is believed

that there is relationship between dividend policy and market value of equity shares.

So a firm should design a dividend policy which shall give maximum value to the

business.

Basic terms used

1. Dividend pay out ratio: Ratio of dividend to total earnings made by the concern.

2. Retained earnings: Earnings retained in the business for future expansion and

development (also known as ploughing back of profit).

3. Bonus issue: Issue of shares to existing shareholders on free of cost as a part of

capitalisation of reserves. No change in the par value of shares.

4 Stock splits: Conversion of shares of larger denomination in to shares of smaller

denomination.

5. Cash dividend: Dividend in the form of cash.

6. Bond dividend: Dividend in the form of bond. Purpose is postponement of

immediate payment of dividend in cash.

7. Scrip dividend: Dividend in the form of shares of other companies.

8. Property dividend: Dividend in the form of assets other than cash.

9. Stock dividend: Dividend in the form of shares.

Determinants of Dividend Policy

Determinants of Dividend Policy are classified into two factors, that is external Factors

and internal Factors

1) External Factors

1) State of Economy

2) Capital Market

3) Legal restrictions

4) Contractual restrictions

5) Tax policy

2) Internal Factors

1) Investor preference

2) Financial needs of company

3) Nature of earnings

4) Desire of control

5) Liquidity position.

Procedure aspects of dividend

1) Board of resolution- Board of directors should in formal meeting resolve to pay the

dividend.

2) Share holders approval- Share holders should approve the dividend plan in A.G.M.

3) Record date- Dividend is payable to share holders whose name appear in the

register of members as on the record date.

4) Dividend payment- Once dividend declaration has been made dividend warrant

must be paid within 30 days of its date of declaration. After the expiry of 42 days

unpaid dividend must be transferred to special account maintained in a scheduled

bank.

Types of Dividend Polices

1) Stable dividend pay out Ratio

2) Stable dividend or steadily changing dividends

3) Pure residual dividend approach

4) Fixed dividend pay out ratio

5) Smoothed residual dividend approach (Total earnings less equity finance required

to supports investment).

6) Generous dividend policy

7) Erratic dividend policy

1) Stable dividend pay out Ratio- According to this policy the percentage of earning

paid out as divided remain constant. Such a policy is really adopted by a business

firm.

2) Stable dividend or steadily changing dividends- As per this policy the rupee

level of dividend remain stable or gradually increase or decrease. The following

reasons are the firm to follow a policy of stable dividend or gradually rising

dividend.

a) Many individuals depend on dividend income to meet a portion of their living

expenses. So if dividend falls too cheaply, they may force to sell the shares.

b) Institutional investors often view a record of steady dividend payment as a highly

desirable future.

c) Dividend decision can be regarded as an important means by which the

management looking for information about the prospects of firm. An increase in

dividend indicates improved earning prospects.

3) Pure residual dividend approach- According to this approach amount is highly

fluctuating year by year. In this approach the earnings in excess of equity support

required for financially investment in a year shall be paid out as dividend.

4) Fixed dividend pay out ratio- In this approach the firm follows the same

procedure of Stable dividend pay out ratio.

5) Smoothed residual dividend approach (Total earnings less equity finance

required to supports investment).- Under this approach the level of dividend is so

set that in the long run total dividend paid is equal to the total earnings less equity

finance required to support investment.

6) Generous dividend policy- In this approach the dividend gives on the basis of

profit of company.

7) Erratic dividend policy- In this approach there is no fixed dividend policy and

company gives dividend in accordance with the direction of management.

Dividend Models (Theories)

There are different opinions relating to the relevance of dividend policy in

determining the value of the firm. Some experts are arguing that dividend policy is

very relevant in deciding the value of the firm and some others stand for the

irrelevance of dividend policy in the valuation of firm.

There are two schools of thought regarding the impact of dividend on valuation of

the firm.

1. Relevance approach.

a. Walter’s model b. Gordon’s model

2. Irrelevance approach.

Modigliani -Miller Approach (MM Model).

1. Relevance approach.

In this approach dividend is very relevant in valuation of the firm.

A. Walter’s model

According to Walter the dividend policy of the firm has relevance in

determining the value of the firm. Different firm should have different dividend policy

for maximizing its value in the market. Walter has derived the firm in three groups for

discussing about the impact of their dividend policy on the value of the firm.

1 Growth firm (r > k)

If the rate of the return on the investment by a firm is higher than the rate of

return expected by the share holders (i.e. cost of capital), the firm is said to be at

growth stage. In case of such firms for maximizing its value the firm should not

distribute its dividend and the entire earnings should be reinvested in its business for

financing its profitable ventures.

According to him the optimal dividend policy for a growth firm is zero

dividend payout ratios. This process of retained earnings can maximise the value of

the firm and wealth to the share holders.

2 Declining firm (r< k)

If the rate of the return on the investment by a firm is lower than the rate of

return expected by the share holders (i.e. cost of capital), the firm is said to be at

decline stage. Such firm should distribute its entire earnings as dividend among the

share holders for maximizing its value and the earnings should not be reinvested in its

business.

3 Normal firm(r = k)

In the case of normal firm the rate of return and the cost of capital shall be

same. According to Walters there is no optimum divided policy for a normal firm. So

the dividend pay out ratio in no way affects the value of firm.

Assumptions

a. All financing done through retained earnings.

b. No change in business risk (r and K are constant)

c. There is no change in key variables i.e. E & D.

d. The firm has perpetual life.

Mathematical model is –

D + R/Ke (E – D)

P = -----------------------

Ke

Preposition

a. When r< k (declining firm) – Cent percent dividend payout ratio.

b. When r > k (Growing firm) – Zero percent dividend payment.

c. When r = k (Normal firm) – No optimal dividend policy.

Criticisms

a. Applicable only to all-equity firms.

b. Unrealistic assumption of ‘r’ is constant.

c. Ignores the effect of risk on value of the firm by taking the assumption of k is

constant.

B. Gordon’s model

According to Gordon the dividend policy of the firm has relevance in

determining the value of the firm. Different firm should have different dividend policy

for maximizing its value in the market. Gordon has derived the firm in three groups

for discussing about the impact of their dividend policy on the value of the firm.

1 Growth firm (same as above)

2 Declining firm (same as above)

3 Normal firms

In the case of a normal firm there is an optimum dividend policy. The normal

firm should distribute its earning as dividend among the share holders for maximizing

its value. This is because people prefer current return to future return.

As the value of the Re1 today is more than that of Re1 tomorrow. For

satisfying the share holder, the firm should declare dividend.

Mathematical model is –

D E (1-b)

V = -----------+g or P = ---------------

K Ke - br

V = value of the firm

K= cost of capital

g = growth rate

D = Dividend

Assumptions

a. All financing done through retained earnings.

b. No change in business risk (r and K are constant)

c. Retention ratio once decided upon is constant .Then growth rate (g=br is also

constant)

d. Ke>br

e. The firm has perpetual life.

Preposition

a. When r< k (declining firm) – Cent percent dividend payout ratio.

b. When r > k (Growing firm) – Zero percent dividend payment.

c. When r = k (Normal firm) –Cent percent dividend payment is the optimal

dividend policy. This is because present value of current income is more than

that of the future income.

Criticisms

a. Applicable only to all-equity firms.

b. Unrealistic assumption of r is constant.

c. Ignores the effect of risk on value of the firm by taking the assumption of k is

constant.

Irrelevance approach

Dividend policy of a firm is only a part of its financial decision and has no

impact on the value of a firm.

Modigliani -Miller Approach (MM Model)

MM Modelis called dividend irrelevance model. This model says that dividend

policy of the firm is not at all affecting the value of the firm. It is strictly a financing

decision whether dividends are paid out of profit or earnings are retained will depend

on the available investment opportunities. It implies that when a firm has sufficient

investment opportunity it shall retain the earnings to finance them. If acceptable

investment opportunities are inadequate the implication is that the earnings would be

distributed to the share holders.

The most comprehensive argument in support of the irrelevance dividend is provided

by the MM Hypothesis. MM maintain dividend has no effect on the share price of the

firm and is of no consequence. According to MM the efficiency of firm to make

earnings is the main factor giving to the value of the firm.

Assumptions

1. Perfect capital market

2. No taxes

3. No change in the required rate of return (ke)

4. There is perfect certainty as to future investment and profit of the firm.

Suppose a firm has investment opportunity give its investment decision it has two

alternatives.

1. It can retain its earnings to finance the investment programme.

2. Distribute the earnings to the share holders as dividend and raise an equal amount

externally through the sale of new shares for the purpose. If the firm select second

alternative there is said to be arbitrage process. In that action payment of dividend

associated with raising of funds from other means of financing

Crux of argument

When dividend is paid to the share holders, the market price of the share will

increase. But if the company has any additional investment opportunity, the company

has to issue additional block of shares which will cause a decline in the terminal value

of the share. What is gained by the investors as a result of increased dividend will be

neutralized completely by the reduction in the terminal value of shares. So the market

price before and after the payment of dividend would be identical. So the investors

would be indifferent between dividend and retention of earnings. Since the share

holders are indifferent the wealth would not be affected by current and future dividend

decision of the firm. It would depend upon the expected future earnings.

Limitations of MM theory

1) Impact on tax

2) Floatation cost

3) Transaction and agency cost

MODULE -4

INTRODUCTION

Finance is the lifeblood of a business enterprise. This is because in the modern

money oriented economy, finance is one of the basic foundations of all kinds of

activities. The modern thinking is, financial management accords a far greater

importance to decision-making and policy. Today, financial managers do not perform

the passive role of scorekeepers of financial data and information and arranging funds

whenever directed to do so. Rather they occupy key position in top management areas

and play a dynamic role in solving complex management problems. It has rightly been

said that business needs money to make more money. Hence efficient should be the

management of its finance.

Working capital management is the functional area of finance that covers all

current accounts of the firm. It deals with the problems that arise in attempting to

manage the current assets, current liabilities and inadequacy of working capital

implies idle funds, which earn no profit for the business.

Working capital in general practice refers to the excess of current assets over

current liabilities. Working capital policies of a firm have a great effect on its

profitability, liquidity and structural health of the organization.

MEANING.

Working capital is the excess of current assets over current liabilities. Current

assets are those assets which can be converted into cash within an accounting year

without disrupting the operations of the firm and it includes cash, marketable

securities, accounts receivables and inventory. Current liabilities are those claims of

‘outsiders’, which are to be expected to mature for payment within an accounting year

and include creditors, bill payable, bank overdraft and outstanding expenses. Working

capital refers to that part of the firm’s capital, which is required for financing current

assets. Funds, thus, invested in current assets keep revolving and are being constantly

converted into cash and these cash flows out again in exchange for other current

assets. Hence it is also known as revolving or circulating capital.

DEFINITION

According to Gene Stenberg, Working capital is “the current asset of a

company that are changed in the ordinary course of business from one firm to another,

as for example, cash to inventory, inventory to receivables, receivables to cash”.

Hoagland defined working capital as “descriptive of that capital which is not fixed”.

CONCEPTS OF WORKING CAPITAL

Basically there are two concepts of Working capital:

Balance sheet concept and

Operating cycles or circular flow concept.

BALANCE SHEET CONCEPT

There are two interpretations of working capital under the balance sheet

concept. They are

Gross working capital concept

Net working capital concept

Gross working capital concept

Gross working capital concept refers to firm’s investment in current assets such

as marketable securities, bills receivables etc. Gross working capital focuses attention

on the efficient management of individual current assets in the day-to-day operations

of the business.

Net working capital concept.

Net working capital refers to the difference between current assets and current

liabilities. Net working capital can be positive or negative. When current assets exceed

current liabilities, the net working capital becomes positive. When current liabilities

exceed current assets the net working capital becomes negative. Long-term view of

working capital, it is essential to concentrate on the net concept of working capital,

because long-term funds are to be arranged for financing net working capital. Thus

working capital can be defined as the excess of current assets over current liabilities.

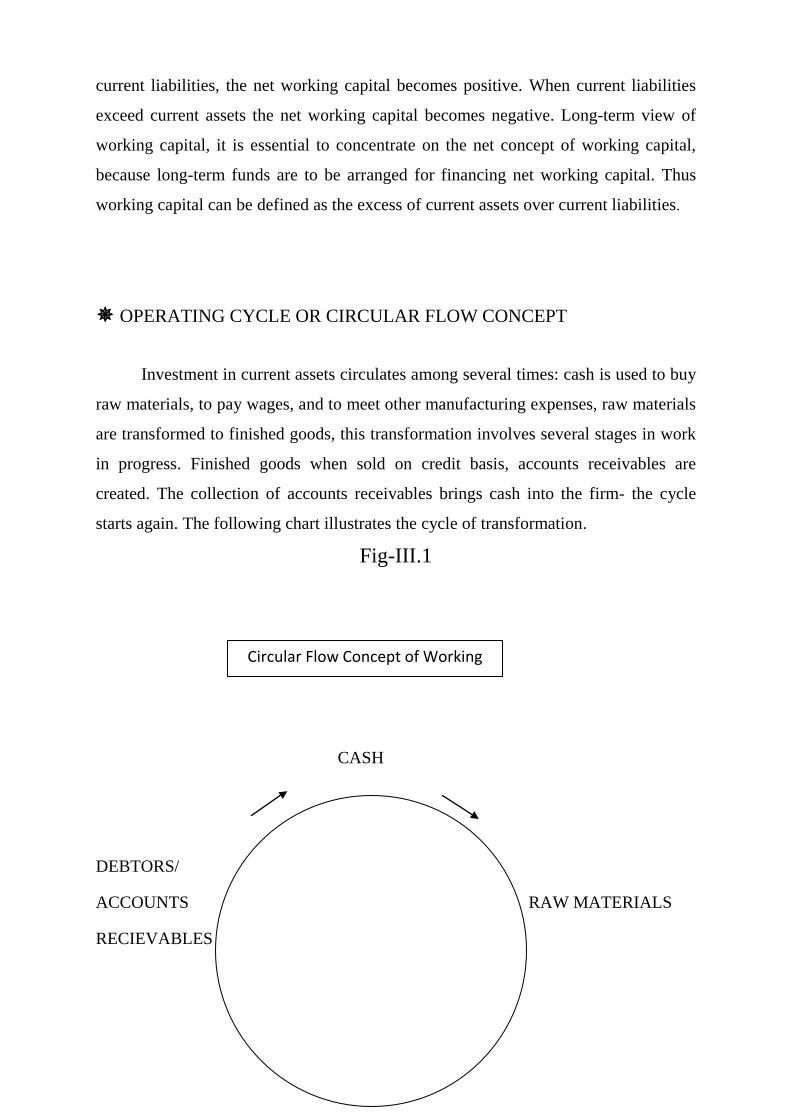

OPERATING CYCLE OR CIRCULAR FLOW CONCEPT

Investment in current assets circulates among several times: cash is used to buy

raw materials, to pay wages, and to meet other manufacturing expenses, raw materials

are transformed to finished goods, this transformation involves several stages in work

in progress. Finished goods when sold on credit basis, accounts receivables are

created. The collection of accounts receivables brings cash into the firm- the cycle

starts again. The following chart illustrates the cycle of transformation.

Fig-III.1

CASH

DEBTORS/

ACCOUNTS RAW MATERIALS

RECIEVABLES

Circular Flow Concept of Working

SALES OF WORK IN PROGRESS

FINISHED

GOODS

FINISHED

GOODS

KINDS OF WORKING CAPITAL

The changes in current assets in short and long terms have led to

classifications of working capital into two components:

Permanent or Fixed Working Capital:

Permanent or fixed working capital is the minimum amount, which is required

to ensure effective utilization of fixed facilities and for maintaining the circulations of

current assets. This minimum level of current assets is called permanent or fixed

capital as this part of capital is permanently blocked in current assets. As the business

grows, the requirements of permanent working capital also increase due to the increase in

current assets.

Temporary or Variable Working Capital

Temporary or variable working capital is the amount of working capital which

is required to meet the seasonal demands. The fluctuation in current assets may be

increase or decrease and are generally cyclical in nature. Additional current assets are

required at different times during the operating year.

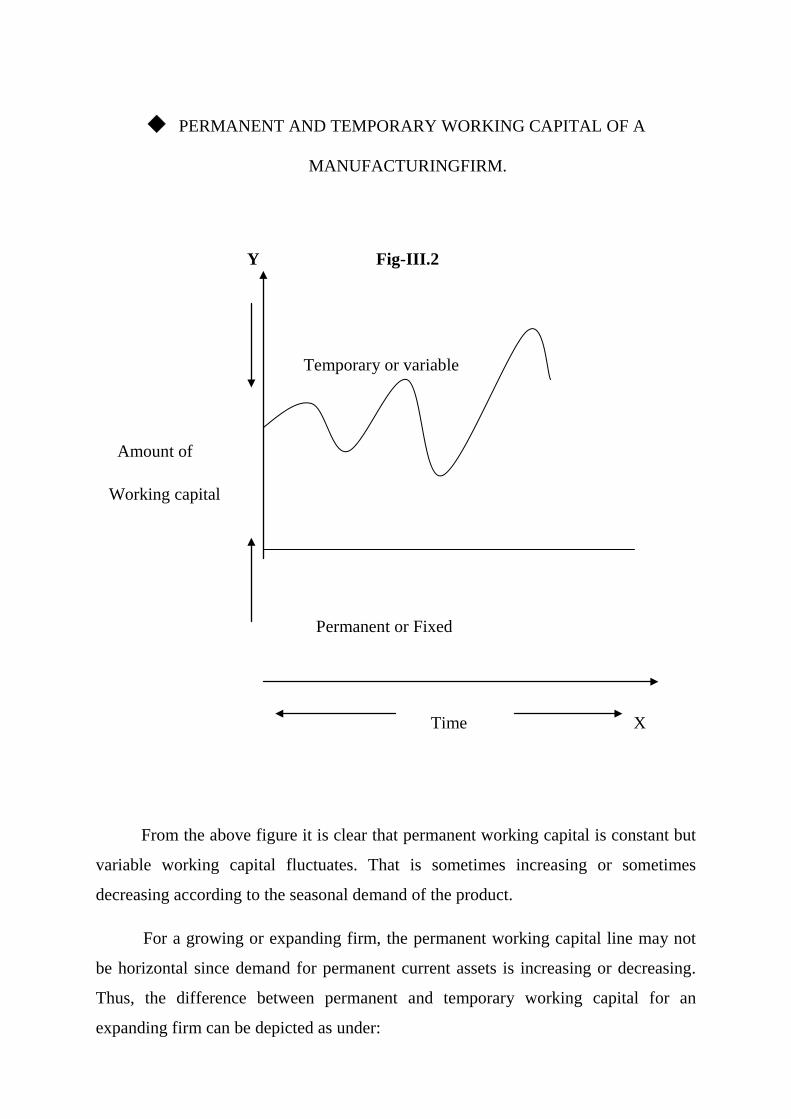

PERMANENT AND TEMPORARY WORKING CAPITAL OF A

MANUFACTURINGFIRM.

Y Fig-III.2

Temporary or variable

Amount of

Working capital

Permanent or Fixed

Time X

From the above figure it is clear that permanent working capital is constant but

variable working capital fluctuates. That is sometimes increasing or sometimes

decreasing according to the seasonal demand of the product.

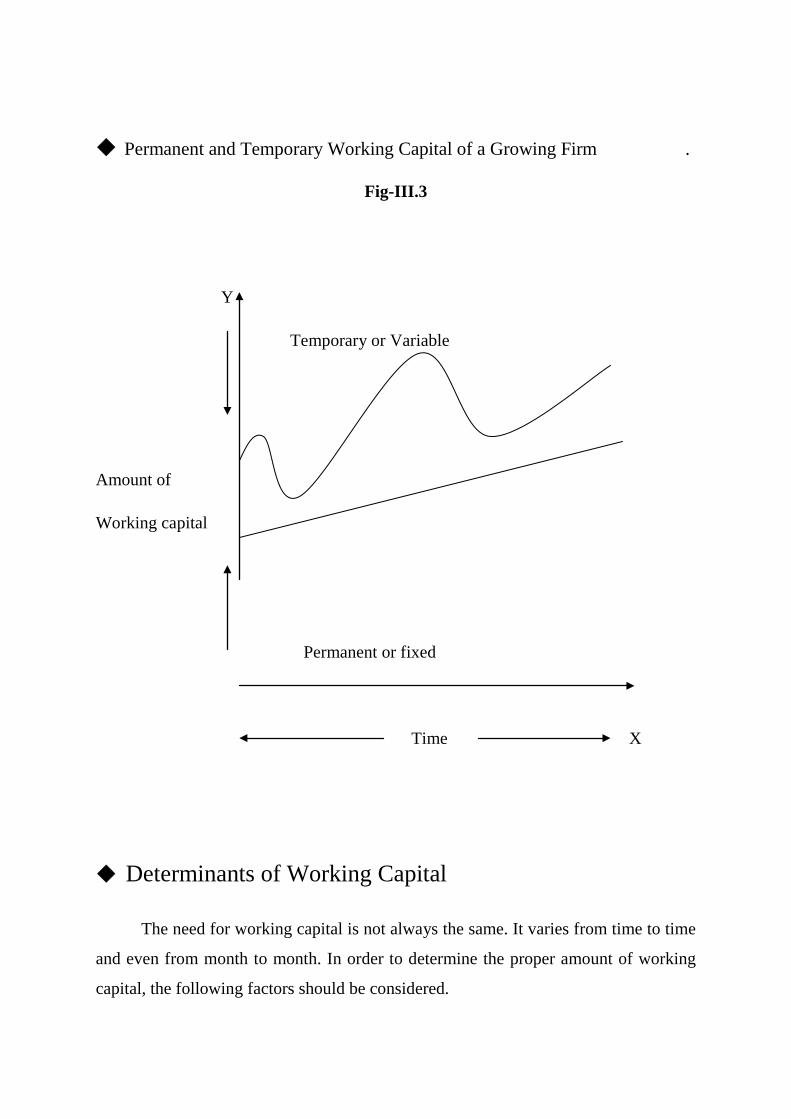

For a growing or expanding firm, the permanent working capital line may not

be horizontal since demand for permanent current assets is increasing or decreasing.

Thus, the difference between permanent and temporary working capital for an

expanding firm can be depicted as under:

Permanent and Temporary Working Capital of a Growing Firm .

Fig-III.3

Y

Temporary or Variable

Amount of

Working capital

Permanent or fixed

Time X

Determinants of Working Capital

The need for working capital is not always the same. It varies from time to time

and even from month to month. In order to determine the proper amount of working

capital, the following factors should be considered.

Nature of business- Trading concerns requires more working capital and public

utility concerns requires less working capital.

Size of the business unit- Larger firm larger will be the working capital and vice

versa.