Copyright © PERS 2018 2019-2021 Budget Presentation Ways and Means General Government Subcommittee Phase 1 – Day 4 Kevin Olineck Director

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

C o p y r i g h t © P E R S 2 0 1 8

2019-2021 Budget Presentation

Ways and Means General Government

SubcommitteePhase 1 – Day 4

Kevin OlineckDirector

C o p y r i g h t © P E R S 2 0 1 8

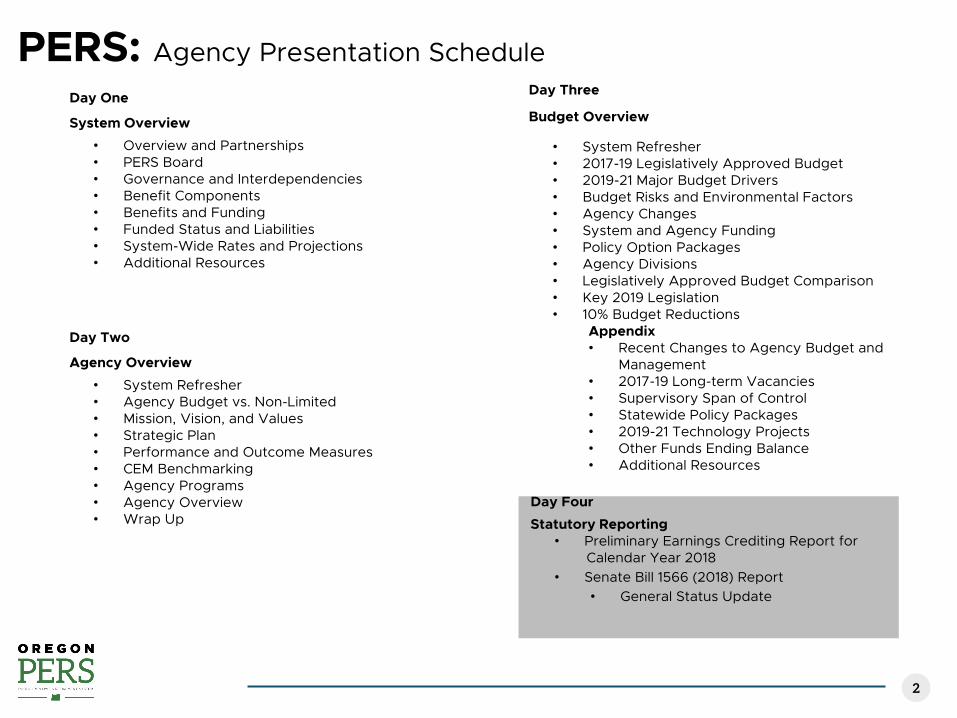

Day Two

Agency Overview

• System Refresher• Agency Budget vs. Non-Limited• Mission, Vision, and Values• Strategic Plan• Performance and Outcome Measures• CEM Benchmarking• Agency Programs• Agency Overview• Wrap Up

PERS: Agency Presentation ScheduleDay Three

Budget Overview

• System Refresher• 2017-19 Legislatively Approved Budget• 2019-21 Major Budget Drivers• Budget Risks and Environmental Factors• Agency Changes • System and Agency Funding• Policy Option Packages• Agency Divisions • Legislatively Approved Budget Comparison• Key 2019 Legislation• 10% Budget Reductions

Appendix• Recent Changes to Agency Budget and

Management• 2017-19 Long-term Vacancies• Supervisory Span of Control• Statewide Policy Packages• 2019-21 Technology Projects• Other Funds Ending Balance• Additional Resources

Day One

System Overview

• Overview and Partnerships• PERS Board• Governance and Interdependencies• Benefit Components• Benefits and Funding • Funded Status and Liabilities• System-Wide Rates and Projections• Additional Resources

Day Four

Statutory Reporting• Preliminary Earnings Crediting Report for

Calendar Year 2018• Senate Bill 1566 (2018) Report

• General Status Update

2

C o p y r i g h t © P E R S 2 0 1 8

PERS: Day Four

3

Statutory Reporting

C o p y r i g h t © P E R S 2 0 1 8

PERS: Preliminary Earnings Crediting and Required Reports

2018 Preliminary Earnings Crediting

ORS 238.670(5) directs the PERS Board to submit a preliminary earnings crediting report to the legislature at least 30 days prior to making any final allocation.

Senate Bill 1566(2018) Reporting

General status of the Employer Incentive Fund, School Districts Unfunded Liability Fund, and the Unfunded Actuarial Liability Resolution Program

4

C o p y r i g h t © P E R S 2 0 1 8

PERS: 2018 Preliminary Earnings Crediting

• February 1, 2019 the PERS Board submitted its preliminary earnings crediting report to the Joint Committee on Ways and Means.

• Report highlights:

• Beginning January 1, 2018, member IAP accounts were invested in Target Date Funds (TDF) based on year of birth. This is the first reporting of annual earnings crediting for each TDF

• Preliminary earnings crediting allocates approximately $83.5 million in 2018 (net of expenses and other adjustments) to member, employer and reserve accounts

• Final crediting will take place at the April 1, 2019 PERS Board meeting

• The Board was unable to credit earnings to the Contingency Reserve. This was due to the fact that the Contingency Account balance, before crediting, was $50 million

• The Board is strictly limited in crediting of funds to the Contingency Reserve; specifically, “…the board may not credit further amounts to the reserve account if the amounts in the reserve account exceed $50 million.” The current balance of the Contingency Reserve is $50 million, with $2.5 million earmarked for resolving employer insolvencies.

5

C o p y r i g h t © P E R S 2 0 1 8

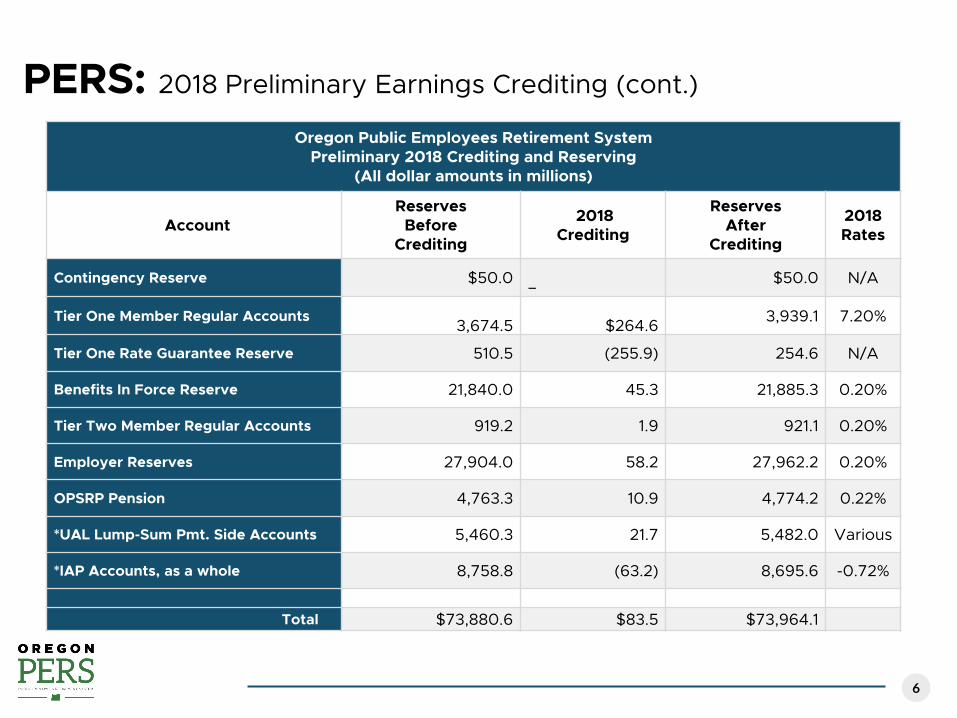

PERS: 2018 Preliminary Earnings Crediting (cont.)

Content

6

Oregon Public Employees Retirement SystemPreliminary 2018 Crediting and Reserving

(All dollar amounts in millions)

AccountReserves

BeforeCrediting

2018Crediting

ReservesAfter

Crediting

2018Rates

Contingency Reserve $50.0 – $50.0 N/A

Tier One Member Regular Accounts3,674.5 $264.6 3,939.1 7.20%

Tier One Rate Guarantee Reserve 510.5 (255.9) 254.6 N/A

Benefits In Force Reserve 21,840.0 45.3 21,885.3 0.20%

Tier Two Member Regular Accounts 919.2 1.9 921.1 0.20%

Employer Reserves 27,904.0 58.2 27,962.2 0.20%

OPSRP Pension 4,763.3 10.9 4,774.2 0.22%

*UAL Lump-Sum Pmt. Side Accounts 5,460.3 21.7 5,482.0 Various

*IAP Accounts, as a whole 8,758.8 (63.2) 8,695.6 -0.72%

Total $73,880.6 $83.5 $73,964.1

C o p y r i g h t © P E R S 2 0 1 8

PERS: 2018 Preliminary Earnings Crediting (cont.)

7

Cont.Reserve

Tier 1 Mem.Reg. Accts

Tier 1 RateGuaranteeReserve

Benefits InForce

Reserve

Tier TwoMemberRegular

Accounts

EmployerReserves

OPSRPPension

*UALLump-SumPmt. SideAccounts

*IAPAccounts,as a whole

Balance Before Crediting $50 $3,675 $511 $21,840 $919 $27,904 $4,763 $5,460 $8,759Balance After Crediting $50 $3,939 $255 $21,885 $921 $27,962 $4,774 $5,482 $8,696 2018 Crediting $- $265 $(256) $45 $2 $58 $11 $22 $(63)

$(300)

$(200)

$(100)

$-

$100

$200

$300

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

2018 Preliminary Crediting(in Millions)

C o p y r i g h t © P E R S 2 0 1 8

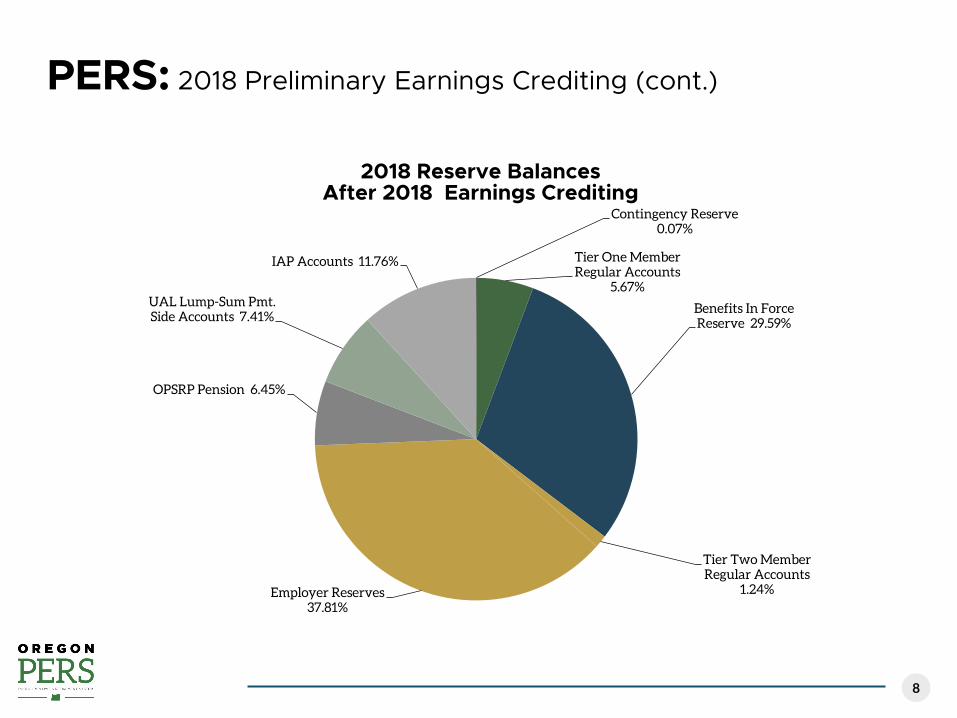

PERS: 2018 Preliminary Earnings Crediting (cont.)

8

Contingency Reserve 0.07%

Tier One Member Regular Accounts

5.67%

Benefits In Force Reserve 29.59%

Tier Two Member Regular Accounts

1.24%Employer Reserves 37.81%

OPSRP Pension 6.45%

UAL Lump-Sum Pmt. Side Accounts 7.41%

IAP Accounts 11.76%

2018 Reserve BalancesAfter 2018 Earnings Crediting

C o p y r i g h t © P E R S 2 0 1 8

PERS: 2018 Preliminary Earnings Crediting (cont.)

9

Oregon Public Employees Retirement SystemPreliminary IAP TDF Earnings

(All dollar amounts in thousands)

Target Date FundReserves

BeforeCrediting

2018Crediting

ReservesAfter

Crediting

2018Rates

RET Fund (Born 1952 or before) $370,324.9 (2,870.8) $367,454.1 -0.77%

2020 Fund (1953-1957) 955,906.3 1,958.8 957,865.1 0.20%

2025 Fund (1958-1962) 1,457,058.4 (10,107.6) 1,446,950.8 -0.69%

2030 Fund (1963-1967) 1,563,190.9 (12,344.6) 1,550,846.3 -0.78%

2035 Fund (1968-1972) 1,606,194.6 (3,594.6) 1,602,600.0 -0.22%

2040 Fund (1973-1977) 1,304,221.8 (5,380.4) 1,298,841.4 -0.41%

2045 Fund (1978-1982) 913,972.8 (18,547.3) 895,425.5 -2.02%

2050 Fund (1983-1987) 436,609.8 (9,015.9) 427,593.9 -2.06%

2055 Fund (1988-1992) 132,624.1 (2,877.2) 129,746.9 -2.16%

2060 Fund (Born 1993 or after) 18,680.8 (409.3) 18,271.5 -2.19%

Total $8,758,784.4 -$63,188.9 $8,695,595.5

C o p y r i g h t © P E R S 2 0 1 8

PERS: Senate Bill 1566(2018) Report

Senate Bill 1566:

• In response to recommendations from the Governor’s PERS Unfunded Actuarial Liability Task Force, which met in 2017, Senate Bill 1566 was approved in 2018

Senate Bill 1566 establishes:

• The Employer Incentive Fund (EIF) which provides up to a 25% match for employers who make a qualifying lump-sum payment to a side account

• The School Districts Unfunded Liability Fund (SDULF) which is a pooled side account that will provide employer rate relief to public school districts, charter schools, and education service districts

• The Unfunded Actuarial Liability Resolution Program which provides information and resources to assist employers as they develop plans to improve their funded status and projected rate changes

Senate Bill 1566 requires reporting:

• Senate Bill 1566 requires PERS to provide an update on the status of the Employer Incentive Fund, the School Districts Unfunded Liability Fund, and the Unfunded Actuarial Liability Resolution Program, as of January 2019

10

C o p y r i g h t © P E R S 2 0 1 8

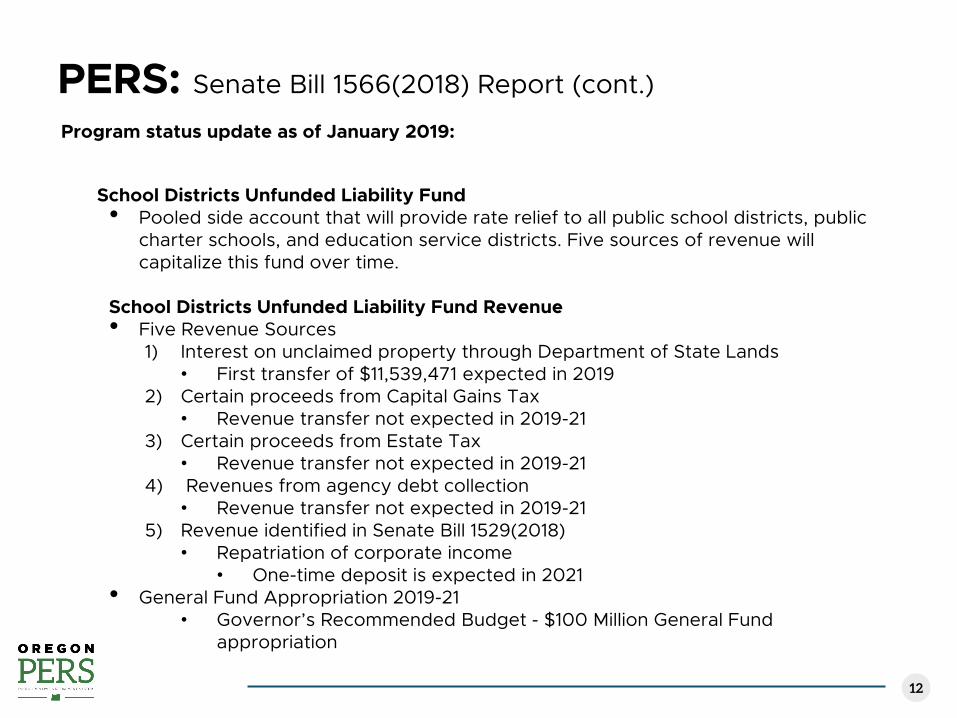

PERS: Senate Bill 1566(2018) Report (cont.)Senate Bill 1566 Report Covers:

• Program status update

Program status update as of January 2019:

Employer Incentive Fund• 25% match for employers who make a qualifying lump-sum payment to a side

account• Applications cannot be accepted for matching funds until the fund has sufficient

revenue

Employer Incentive Fund Revenue• Revenue sources are directed by Senate Bill 1529(2018) • The sole source of revenue - repatriation of corporate income• One-time revenues are expected after July 1, 2021

• Funds will not be available in EIF in 2019 • Section (2)(c)(A) of SB 1566 requires the application process to close by

December 31, 2019 • PERS cannot accept applications before the required application close date.

• PERS has requested Senate Bill 75(2019) to, among other changes, allow the Board to approve EIF applications as long as EIF moneys are projected to be available.

11

C o p y r i g h t © P E R S 2 0 1 8

PERS: Senate Bill 1566(2018) Report (cont.)

Program status update as of January 2019:

School Districts Unfunded Liability Fund • Pooled side account that will provide rate relief to all public school districts, public

charter schools, and education service districts. Five sources of revenue will capitalize this fund over time.

School Districts Unfunded Liability Fund Revenue• Five Revenue Sources

1) Interest on unclaimed property through Department of State Lands• First transfer of $11,539,471 expected in 2019

2) Certain proceeds from Capital Gains Tax • Revenue transfer not expected in 2019-21

3) Certain proceeds from Estate Tax• Revenue transfer not expected in 2019-21

4) Revenues from agency debt collection• Revenue transfer not expected in 2019-21

5) Revenue identified in Senate Bill 1529(2018)• Repatriation of corporate income

• One-time deposit is expected in 2021• General Fund Appropriation 2019-21

• Governor’s Recommended Budget - $100 Million General Fund appropriation

12

C o p y r i g h t © P E R S 2 0 1 8

PERS: Senate Bill 1566(2018) Report (cont.)

School Districts Unfunded Liability Fund Revenue (cont.)

• Revenue in the SDULF will be applied as an employer rate offset for all members of the School Districts Pool

• At this time, a 1% rate offset requires a fund balance of approximately $435 Million

• PERS does not anticipate applying a rate offset to the SDULF this biennium

Unfunded Actuarial Liability Resolution Program• PERS surveyed employers to determine what tools or resources they need in the

Unfunded Actuarial Liability Resolution Program.

• Resources and information are on the Internet including the Employer Rate Projection Tool

• Other resources are under development

Summary

• Uncertainty surrounding revenue streams for the EIF and the SDULF create challenges in planning for the amount and timing of rate relief. Administrative processes are in place, or have been outlined and are ready for deployment as soon as revenue is available to ensure rate relief at the earliest possible opportunity.

Senate Bill 75(2019)

• PERS requested introduction of housekeeping legislation so the agency may facilitate distribution of funds and ensure employer rate relief at the earliest opportunity.

13

C o p y r i g h t © P E R S 2 0 1 8

Kevin OlineckPERS Director

2019www.oregon.gov/pers

Thank You

Related Documents