1 Copyright K.Cuthbertson and D.Nitzsche Lecture Futures Contracts This version 11/9/2001 Copyright K.Cuthbertson and D.Nitzsche

Copyright K.Cuthbertson and D.Nitzsche 1 Lecture Futures Contracts This version 11/9/2001 Copyright K.Cuthbertson and D.Nitzsche.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1Copyright K.Cuthbertson and D.Nitzsche

Lecture

Futures Contracts

This version 11/9/2001

Copyright K.Cuthbertson and D.Nitzsche

Copyright K.Cuthbertson and D.Nitzsche

2

Basic Concepts

Speculation

Pricing/Arbitrage

Hedging

Marking to Market (Margin Account)

Topics

Copyright K.Cuthbertson and D.Nitzsche

3

Investments:Spot and Derivative Markets,

K.Cuthbertson and D.Nitzsche

CHAPTER 19:CHAPTER 19:

Derivative Securities: An OverviewDerivative Securities: An Overview

CHAPTER 20:CHAPTER 20:

Futures MarketsFutures Markets

READING

Copyright K.Cuthbertson and D.Nitzsche

4

Basic Concepts

Copyright K.Cuthbertson and D.Nitzsche

5

Spot and Futures Markets

Futures contract is an agreement to buy or sell ‘something’ in the future at a price agreed today.

There is a spot/cash asset underlying the futures contract

(eg. can have a futures ‘written on’ live hogs/oil/stocks)

Let S = Spot/Cash price

S = price for delivery today(in cattle market)

Futures prices F are continuously quoted and change from second to second (and moves almost one-for-one with movements in S)

But it is the futures contract you are buying and selling not the underlying asset itself (e.g. they are traded on different exchanges - e.g. NYSE and CBOT)

Copyright K.Cuthbertson and D.Nitzsche

Futures Contract

Futures Price F0 =$100 on live hogs, quoted today (1st Jan) with Delivery Month in say September

Buy = Long Futures

~ agree a (legal) contract to buy the “underlying” (eg, 1-live hog) in the delivery month at F0 = $100 (IF the contract is held to maturity)

Sell = Short Futures

~ agree to sell the “underlying” (1-live hog) in the delivery month at , F0 =100 ( IF the short contract is held to maturity)

(You will be notified by the exchange a few days before the maturity date of the contract, that on your particular contract ‘delivery’ is going to take place

~ in order that you can have your hogs ready and ‘looking good’.

Copyright K.Cuthbertson and D.Nitzsche

No “payment” made today ( only a “deposit” to guarantee you will not “quit” on the deal - this is know as a “margin payment AND IS NOT THE FUTURES PRICE - see later).

This means that futures provide LEVERAGE, in that a speculator can enter into a futures contract whose value changes with that of the underlying stocks, but she does not have to spend any of her own money at t=0 !

The clearing house/futures exchange acts as an intermediary between buyers and sellers (and keeps a record of all transactions)

Futures Contract

Copyright K.Cuthbertson and D.Nitzsche

Why does F change between 1st Jan and 1st Feb ?

As we see later ‘arbitrageurs’ ensure that F changes as the price of hogs changes in the spot market S.

If S increases (falls) then F will increase (fall)

- almost $1 for $1 over short horizons (e.g. 1 - 3 months)

Analytically: Care must be taken to state whether your analysis involves holding the futures to maturity or “buying then selling “ prior to maturity

Copyright K.Cuthbertson and D.Nitzsche

9

Table 2 : Forward and Futures Contracts

FORWARDS

Private (non-marketable) contract between two parties

Delivery or cash settlement at expiry

Usually one delivery date

No cash paid until expiry

Negotiable choice of delivery dates, size of contract

FUTURES

Traded on an exchange

Contract is usually closed out prior to maturity

Range of delivery dates

Cash payments into (out of) margin account, daily

Standardised Contract

Copyright K.Cuthbertson and D.Nitzsche

10

FINANCIAL FUTURES MARKETS

Money market instruments:

3-mth Euro$ Deposits 90-day US T-bills 3-mth Sterling, DM,

deposits Bonds US T-bond, UK Gilt,

German Bund. Stock Indexes S&P 500, FTSE100 Currencies DM, Sterling, Yen, Mortgage pools (GNMA)

LIFFECBOT(IMM) CMEN.Y. Futures Exch.Phil. Exch.

Singapore Int Exch.

Hong Kong

Tokyo\Osaka

Pacific St. Ex. (San F.)

Sydney Fut. Exch.

Copyright K.Cuthbertson and D.Nitzsche

Most contracts are “closed out” prior to the maturity/delivery date ( -see also “hedging”, later)

Note that if on 1st Jan you bought a Sept-futures contract at F0 then

you can “get out” of this contract before maturity simply by

selling this Sept-futures contract on say 1st Feb

at whatever price F1 is being quoted for the Sept-contract on 1st Feb. Then “nobody” delivers “anything” at maturity.

Futures Contract

Copyright K.Cuthbertson and D.Nitzsche

12

Who Uses Futures ?

Speculation with futures

Buy low, sell high - risky ( ‘naked/open’ position)

Hedging with futures

eg.In Jan, farmer wants to “lock in” sale price of his hogs which will be ‘fat’ by Sept

- In Jan he sells hog futures at F0=$100 with maturity date of Sept - if he holds contract to maturity he ‘delivers’ his hog in Sept and receives the $100 (for certain) - ie. even if hogs in (spot) cattle market are selling for $10 .

Arbitrage

Spot and futures prices are ‘linked’ by the actions of arbitrageurs and S and F move almost one-for-one - latter is useful for hedgers (see later)

Copyright K.Cuthbertson and D.Nitzsche

13

Table 2.4: Futures: Price QuotesCORN (CBT) 5,000 bu (cents per bu.)

(1) (2) (3) (4) (5) Lifetime Open

OpenHighLowSettleChange HighLow Interest

Sept 18212183

14179

14180

12- 2

14 265

12178

14 132,493

Dec 19412195 191

14192

14- 2 1/2 279 ½190 176,843

Mar 0120612206 ¾203 204

14- 2

14 279 ¾202 37,875

Source : Wall Street Journal Thursday 27th July 2000.

Copyright K.Cuthbertson and D.Nitzsche

14

Speculation With Futures

Copyright K.Cuthbertson and D.Nitzsche

15

Speculation With Futures

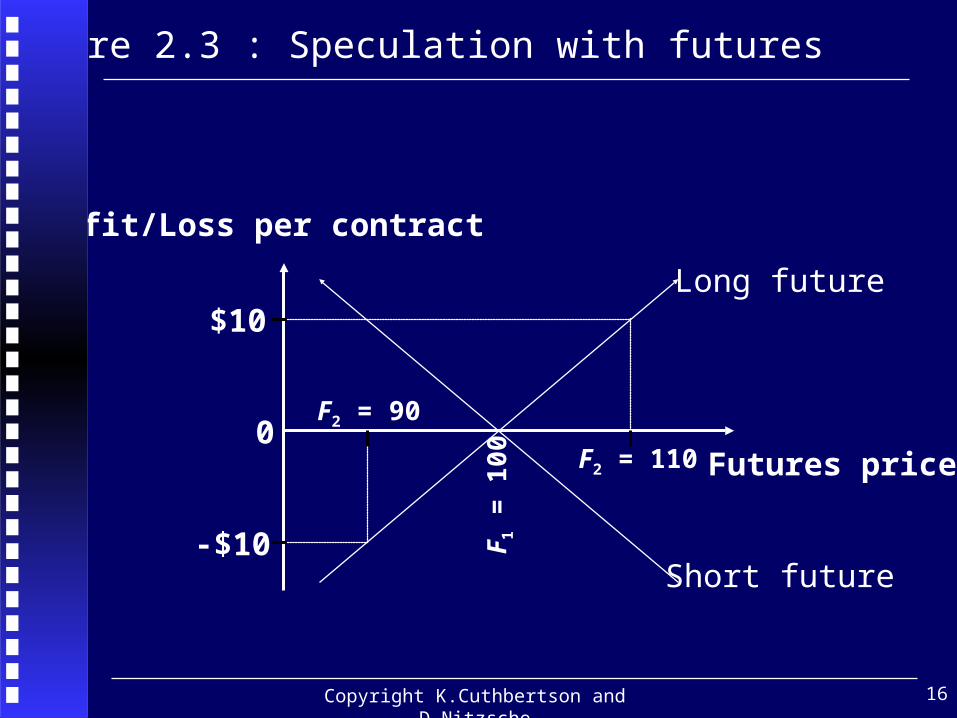

Purchase at F0 = 100

Hope to sell at higher price later F1 = 110

Close-out position before delivery date.

Obtain Leverage (ie. initial margin is ‘low’)

Example:Leeson: Feb 95, Long 61,000 Nikkei-225 index futures (underlying value = $7bn). Nikkei fell and he lost money (lots of it) - he was supposed to be doing riskless ‘index arbitrage’ not speculating

Copyright K.Cuthbertson and D.Nitzsche

16

Figure 2.3 : Speculation with futures

Futures price

Profit/Loss per contract

$10

-$10

0

Long future

Short future

F2 = 110

F2 = 90

F1 =

100

Copyright K.Cuthbertson and D.Nitzsche

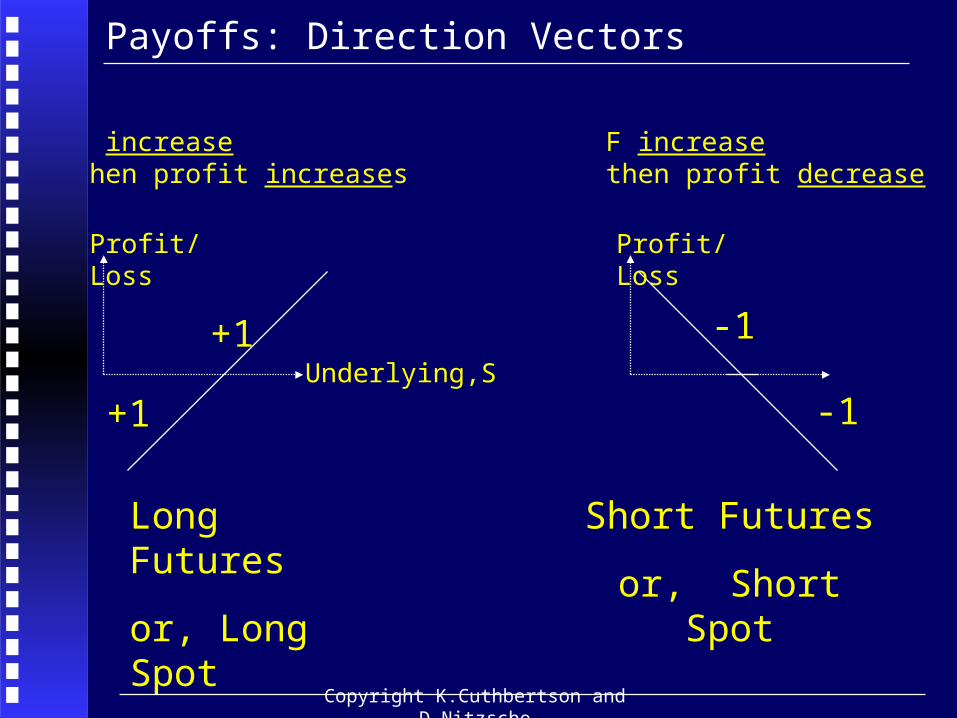

Payoffs: Direction Vectors

Long Futures

or, Long Spot

Short Futures

or, Short Spot

+1

-1

-1

+1

F increasethen profit increases

F increasethen profit decrease

Underlying,S

Profit/Loss Profit/Loss

Copyright K.Cuthbertson and D.Nitzsche

Pricing/Arbitrage

with

Futures

Copyright K.Cuthbertson and D.Nitzsche

Arbitrage at Maturity

At expiry (T) we must have FT = ST

otherwise riskless arbitrage profits could be made

EG. Suppose 1-day before maturity

FT = 100 > ST =98

Then buy ‘low’ at S=98 in ‘cattle market’ , and at same time sell one future contract at F = 100.

One day later ‘deliver’ the hog in the futures contract and collect F=$100 (at maturity).

This is (virtually) riskless.

Copyright K.Cuthbertson and D.Nitzsche

20

Figure 2.7 : Backwardation and Contango

Stock price, St

For simplicity we assume that the spot price remains constant. In practise, S and hence F will fluctuate as you approach T but with Ft > St if the market is in contango and Ft < St if the market is in backwardation.

T

Forward price in contango : F > S

Forward price in backwardation : F < S

0

At T, ST = FT

Copyright K.Cuthbertson and D.Nitzsche

21

Arbitrage (at t<T): Pricing a Futures Contract

‘Cash and Carry’ Arbitrage

Stock price, S = $100 Safe rate r = 4% p.a.

Quoted Futures Price F = $102 (for delivery in 3m )

Strategy Today

Sell futures contract at $102 (receive nothing today)

Borrow $100, buy stock ( = synthetic future)

Use no “own funds”

3-Months Time ( T = 1/4 )

Loan Outstanding = $100( 1 + 0.04 / 4) = $101

Deliver stock and receipt from f.c. = $102

Riskless profit = $1

Copyright K.Cuthbertson and D.Nitzsche

22

Borrow and purchase stock today isequivalent to having the stock in 3-mnths

= SYNTHETIC FUTURE

( Note: No “own funds” used to create the “synthetic” ) Cost of synthetic future, SF = S ( 1 + r.T ) = $101

Arbitrage ensures quoted futures price equals SF

F = S ( 1 + r .T ) = $101

Futures Price = Spot price + cost of carry

“Cost of Carry” = S rT = $1

Arbitrage (at t<T): Pricing a Futures Contract

Copyright K.Cuthbertson and D.Nitzsche

23

Hedging with Futures

Copyright K.Cuthbertson and D.Nitzsche

24

Hedging with Futures

Arbitrageurs ensure F and S are nearly perfectly positively correlated and move $1 for $1.

F = S ( 1 + r .T ) = S (1.01)

so approx:

(F1 - F0) = (S1 - S0) ie. ‘dollar for dollar’

Copyright K.Cuthbertson and D.Nitzsche

25

Hedging with Futures

F and S are positively correlated To Hedge: Create a negative correlation If you are long spot( ie. own 1-share) then short the

futures contract ( on the share) to offset the risk in spot/cash market

1) Hope that the loss in the cash/spot market is (partly) offset by gain on the futures (‘dollar for dollar’)

or,

2) Final Value = Cash Market Value + gain on futures, “locks in” a known “price”

Copyright K.Cuthbertson and D.Nitzsche

Hedge = Long Underlying + Short Futures

Long Underlying

Stock +

Short Futures

Hedge=0

0

+1

+1

-1

-1

Copyright K.Cuthbertson and D.Nitzsche

27

Own (long) 1-share Spot price S0= $100

Fear price fall over next 3-mths

3-month futures contract has current price, F0 = $101

AIMS:

1) To offset some of the loss in S by profit on F or,

2) To “lock in” a “final value” of F0 = $101

Assume: F and S are perfectly (positively) correlated

Strategy: ‘Long’ share + ‘short’ one futures contract

Simple Hedging

Copyright K.Cuthbertson and D.Nitzsche

28

Simple Hedging (S0 = $100, F0 = $101)

1) Loss in spot market offset by gain on the futures

3 MONTHS LATER(Spot Price has fallen)

Spot Price S1 = $90 Futures Price F1 = $90

Note that we have assumed the contract is closed out just before maturity so that S1 = F1

Gain on Futures = (101 - 90) = ( F0 - F1) = $11

Loss on the spot = (100 - 90) = (S0 - S1 ) = $10

Net Profit = ( F0 - F1 ) - ( S0 - S1 ) = 11 - 10 = $1

Note that you cannot guarantee that the hedge will give a net profit of zero, only that the net profit in the hedge will be less uncertain

than simply holding the stocks (ie. here a loss of $10).

Copyright K.Cuthbertson and D.Nitzsche

29

Simple Hedging (S0 = $100, F0 = $101)

2) Can we “lock in” a price of F0 = 101 ?

3 MONTHS LATER(Spot Price has fallen)

Spot Price S1 = $90 Futures Price F1 = $90

Spot asset is worth S1 = 90 and we close out futures position

Profit on Futures = (101 - 90) = F0 - F1 = $11

Final Value = Final Value of stocks + profit from futures

= 90 + 11 = (S1) + F0 - F1 = $101

Hence we have locked in a final value of F0 = 101

Copyright K.Cuthbertson and D.Nitzsche

30

Simple Hedging (S0 = $100, F0 = $101)

Some Algebra:

Final Value = S1 + (F0 - F1 ) = $101

= (S1 - F1 ) + F0

= b1 + F0

where “Final basis” = b1 = S1 - F1

Note: At maturity of the futures contract the basis is zero (since S1 = F1 . In general, when the contract is closed out prior to maturity b1 = S1 - F1 may not be zero. This is called BASIS RISK. However b1 will usually be “small in relation to F0.

Source of basis risk is changes in r : F = S (1+r.T)

Copyright K.Cuthbertson and D.Nitzsche

31

Even though you close out the contract, you still “ lock in” a price which is close to the initial futures (delivery) price of F0 = 101.

But why not just take delivery at F0 = 101 ?

Easiest to see if you are a farmer in New Orleans who wants to sell his” live hogs” in 3-months time when they have been fattened up.

If he delivers them in the futures contract he will have to send the hogs to Chicago (the delivery point). This is expensive, so instead he sells them in the local cattle market in New Orleans for S1 =90

But he also makes $11 cash profit on the futures, giving an effective price of $101, which EQUALS the F-price had he taken delivery

Why does the hedger close out before maturity ?

Copyright K.Cuthbertson and D.Nitzsche

32

MARKING TO MARKET

Copyright K.Cuthbertson and D.Nitzsche

Marking To Market: Contract Specification

One contract is for z = $100,000 of the underlying asset (eg. US T-Bond Future).

F= price per $100 nominal

Let “1-tick” = change in F of 1 unit (eg. 98.0 to 99.0 )

Tick Value (set by the CBOT) = $1000 (= 1.0 /100) x $100,000

Initial Margin = $5000 Maintenance Margin=$4,000

If balance in margin account falls below $4,000 at market close, then it must be made up to $5,000 by the next morning.

Buy one contract at F0 = 98 (noon, day-1) [ Value = $98,000]

Close out contract at F3 = 98.5 (after 3-days)

Copyright K.Cuthbertson and D.Nitzsche

Day Settlement(Price)

Mark toMarket

MarginPayment

Balance

1. 94,000(94.0) -4000 5000 $1000

2. 93,500(93.5) -500 4000 $4500

3. 98,500(98.5) +5000 $9500

Tick value (=1unit) = $1,000

Initial margin = $5000, (Maintenance margin = $4000)

Buy at F0 = 98 (noon, day-1)

TEXT BOOK:

Total Profit = (F3 - F0) 1,000 = (98.5 - 98) $1,000 = +$500

Marking To Market

Copyright K.Cuthbertson and D.Nitzsche

35

Buy at F0 = 98 (noon, day-1)

End of Day-1, contract is worth F1 = 94.0

Change on the day = - 4 x $1000 = -$4000

New balance = $5,000 - $4,000 = $1000

Balance is below maintenance margin, hence must pay in 4,000 to make opening balance on day-2 = £5,000 (ie. the initial margin)

End of Day-2, contract is worth F2 = 93.5 (ie. Lost 500)

Closing balance = 5,000 - 500 = 4,500 (above, maintenance margin)

End of Day-3, contract is worth F2 = 98.5 (ie. +5 ticks)

Closing balance = 4,000+5000 = $9,500 (send cheque)

Total Profit using Margin Account

Final balance received = $9,500

less what you paid in $5,000+$4000 = $9,000

So final profit = + $500

Marking To Market: Day-by-Day

Copyright K.Cuthbertson and D.Nitzsche

36

Futures contract is like a forward contract that is closed out every day and your daily cash gains/losses are noted by the Clearing House (CH). Then you enter a new forward contract at the beginning of the next day at the new futures price. Any cash gain/loss alters the balance in your margin account, daily.

The initial margin of $5000 is equivalent to 5 ticks. If the market falls less than 5 ticks in a day, the “long” (and the Clearing House) can always honour the contract. Trading halts are sometimes used to prevent a fall of more than 5 ticks in one day, so that margin payments can take place before the next days trading.

This is why futures contract involve no credit(default) risk

Marking To Market

Copyright K.Cuthbertson and D.Nitzsche

37

SLIDES END HERE

Related Documents