Copyright (c) 2006 McGraw-Hill Ryerson Limited

Copyright (c) 2006 McGraw-Hill Ryerson Limited. Chapter 4: Learning Objectives Characteristics of Financial Market Instruments: Money Market Instruments.

Dec 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright (c) 2006 McGraw-Hill Ryerson Limited

Copyright (c) 2006 McGraw-Hill Ryerson Limited

Chapter 4:Learning Objectives

Characteristics of Financial Market Instruments: Money Market Instruments Capital Market Instruments

Financial Innovations

Money Market Instruments

Short-term, low risk financial instruments Bankers' Acceptance Certificates of Deposit (CDs) Commercial Paper Treasury Bills (T-bills)

Copyright (c) 2006 McGraw-Hill Ryerson Limited

Copyright (c) 2006 McGraw-Hill Ryerson Limited

Copyright (c) 2006 McGraw-Hill Ryerson Limited

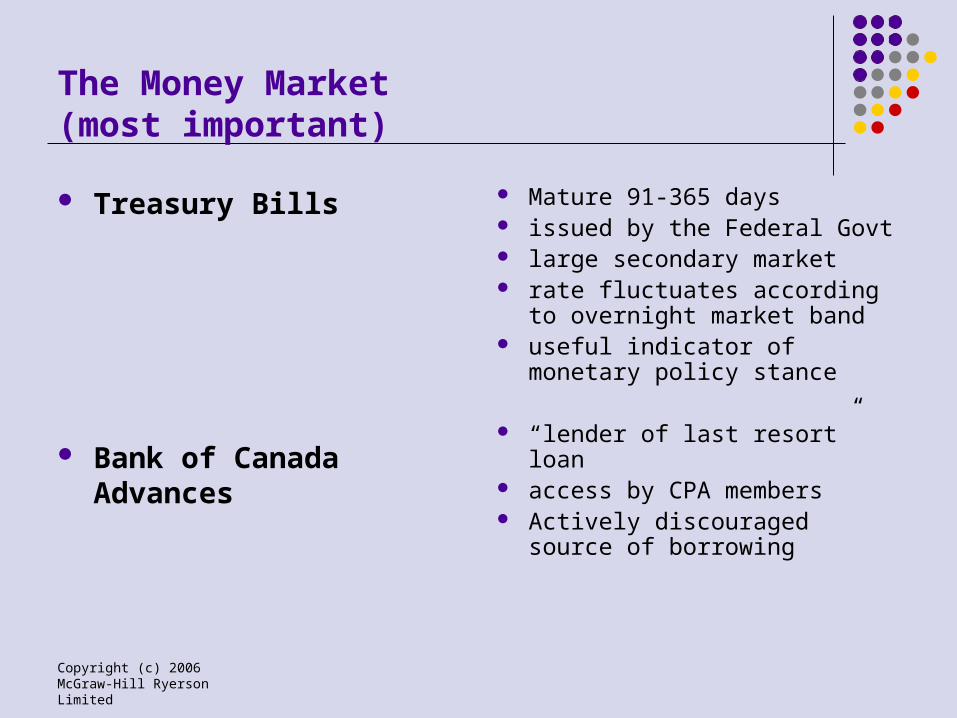

The Money Market (most important)

Treasury Bills

Bank of Canada Advances

Mature 91-365 days issued by the Federal Govt large secondary market rate fluctuates according

to overnight market band useful indicator of

monetary policy stance

“lender of last resort” loan access by CPA members Actively discouraged

source of borrowing

Copyright (c) 2006 McGraw-Hill Ryerson Limited

Bank of Canada Advances

0

1000

2000

3000

4000

198519871989 19911993199519971999 20012003

3469.0

868.0

798.0

484.9

312.0

471.0

1174.0

224.0

131.0

447.0

545.0 554.0

363.0

656.0

560.9

952.0

647.0

535.0

383.0

10.0

Mill

ions

of d

olla

rs

3469

868 798

485312

471

1174

224

131

447545554

363656

561

952

647535

383

10

Copyright (c) 2006 McGraw-Hill Ryerson Limited

The Operating Band for the Overnight Market

OvernightMarket Rates

Bank Rate

Rate on +ve balances =Bank rate less 0.50%

OPERATING BAND

BOC target rate = mid-pointof range

Overdraft Surplus

ON*=(BRt+Rtsb)/2

Copyright (c) 2006 McGraw-Hill Ryerson Limited

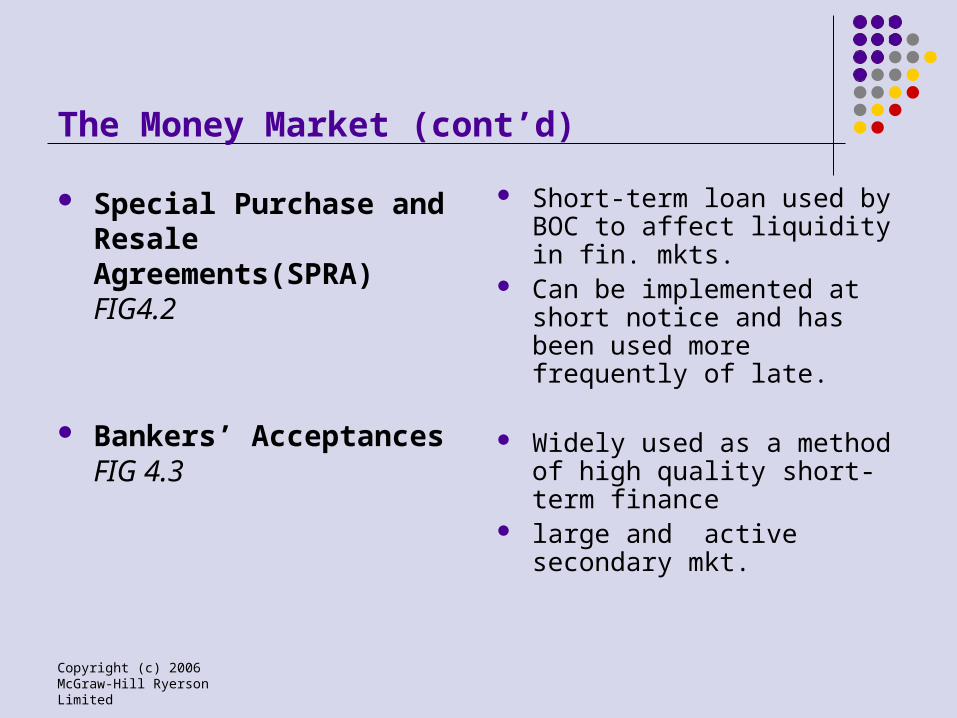

The Money Market (cont’d)

Special Purchase and Resale Agreements(SPRA) FIG4.2

Bankers’ Acceptances FIG 4.3

Short-term loan used by BOC to affect liquidity in fin. mkts.

Can be implemented at short notice and has been used more frequently of late.

Widely used as a method of high quality short-term finance

large and active secondary mkt.

Copyright (c) 2006 McGraw-Hill Ryerson Limited

Financing Through an SPRA

Investment Dealer Bank of Canada

Bank

SPRA T-bill Bank deposit

Call loan

BOC Dep.

Assets Liabilities

Call loan

Copyright (c) 2006 McGraw-Hill Ryerson Limited

Financing via a Banker’s Acceptance

Importer Exporter

BANKS

Investment Dealers

Investors

Letter of creditissued

Secondary Market

Rediscounting

“Stamped”

Copyright (c) 2006 McGraw-Hill Ryerson Limited

The Money Market (cont’d)

Interbank deposits

Eurocurrency instruments

growth reflects globalization and importance of interbank transactions

useful as a cash management tool

offshore financial market in several centers (London UK most important)

highly liquid, low tax and transactions costs

useful guide for int’l int rate developments

Copyright (c) 2006 McGraw-Hill Ryerson Limited

The Money Market [cont’d]

The Large Value Transfer System (LVTS) Assists in the operations of the clearing

system Attempting to reduce systemic risk Not, strictly speaking, an instrument Created by the CPA (Canadian payments

Association]

Copyright (c) 2006 McGraw-Hill Ryerson Limited

The Money Market (cont’d)

Special Purchase and Resale Agreements (SPRA) FIG4.2 (cont’d)

If participant i’s LVTS is LVTSi while participant j’s LVTS balance are LVTSj then we would expect:

LVTSi + LVTSj = 0

Copyright (c) 2006 McGraw-Hill Ryerson Limited

The Capital Market & Derivatives(most important)

Govt of Canada bonds

Large secondary market principal source of debt

finance across the term structure

Copyright (c) 2006 McGraw-Hill Ryerson Limited

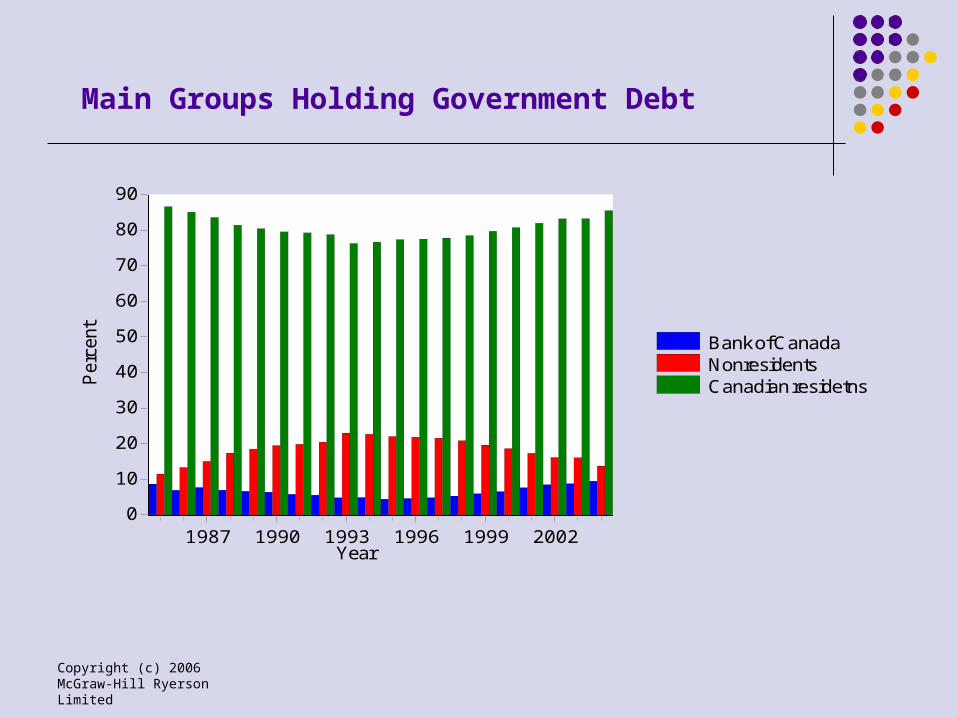

Main Groups Holding Government Debt

0

10

20

30

40

50

60

70

80

90

1987 1990 1993 1996 1999 2002

Bank of CanadaNonresidentsCanadian residetnsP

erce

nt

Year

Copyright (c) 2006 McGraw-Hill Ryerson Limited

The Capital Market & Derivatives(most important)

Govt of Canada bonds

Stocks

Large secondary market principal source of debt

finance across the term structure

newly issued and large secondary market

private source of debt

Copyright (c) 2006 McGraw-Hill Ryerson Limited

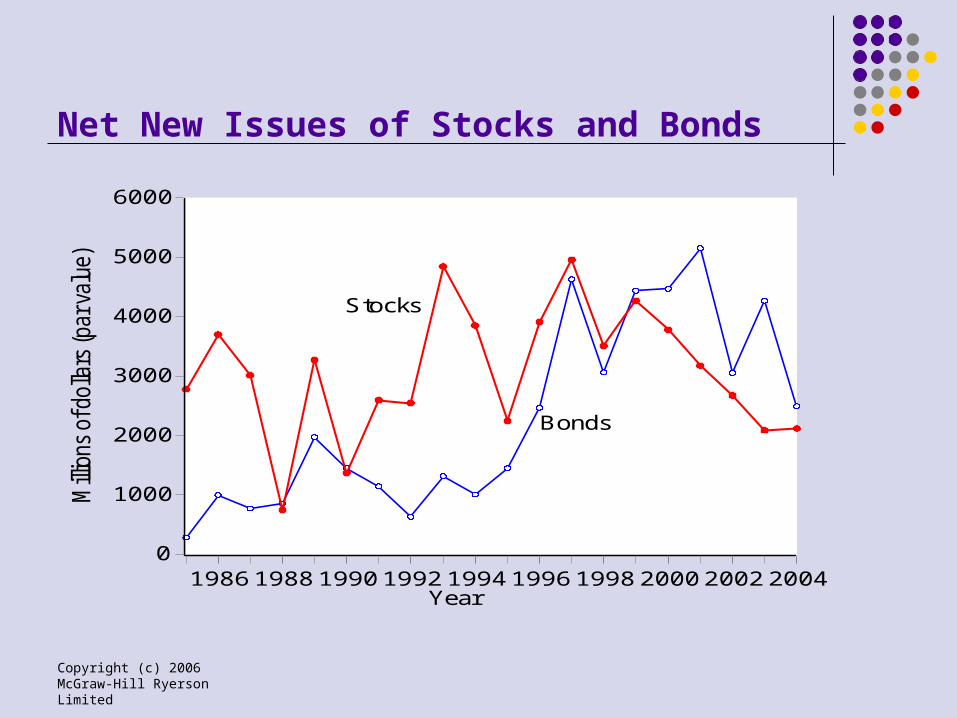

Net New Issues of Stocks and Bonds

0

1000

2000

3000

4000

5000

6000

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Millio

ns

of d

olla

rs (par va

lue)

Year

Stocks

Bonds

Copyright (c) 2006 McGraw-Hill Ryerson Limited

The Capital Market & Derivatives(most important)

Govt of Canada bonds

Stocks

Derivatives

large secondary market principal source of debt

finance across the term structure

newly issued and large secondary market

private source of debt

large variety can be a source of reduced

or increased risk

Copyright (c) 2006 McGraw-Hill Ryerson Limited

Summary

Financial Markets can be subdivided into the Money and Capital Markets

Money Market instruments are short-term in nature Capital Market instruments are long-term in nature The principal Money market instruments are T-bills,

Bank of Canada Advances, SPRAs, Banker’s Acceptances, interbank deposits and the Eurocurrency market

The principal capital market instruments are Govt bonds, stocks and derivative products

Related Documents