Copyright © 2014 Deloitte Tax LLP. All rights reserved. 1 APA Silicon Valley Chapter Meeting March 2014 Meeting Deloitte Tax LLP

Copyright © 2014 Deloitte Tax LLP. All rights reserved. 0 APA Silicon Valley Chapter Meeting March 2014 Meeting Deloitte Tax LLP.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2014 Deloitte Tax LLP. All rights reserved.1

APA Silicon Valley Chapter MeetingMarch 2014 Meeting

Deloitte Tax LLP

Copyright © 2014 Deloitte Tax LLP. All rights reserved.2

Agenda

• IRS Audit Landscape

• U.S. Payroll Deposit Rules & Equity Transactions

• Noncash Fringe Benefits

• Worker Classification & Settlement Program

• Mobile Workforce Taxation

• FICA Refunds – Quality Stores and April 15, 2014 Deadline

• DOMA

Copyright © 2014 Deloitte Tax LLP. All rights reserved.3

IRS Audit Landscape

Copyright © 2014 Deloitte Tax LLP. All rights reserved.4

Recent Audit Findings

• Separate Audit Teams: 12 month duration

• Multiple IDRs

• Equity Deposit Timing

• 1099 (Vendors, Ex-Spouses, Contractors, Foreign Contractors)

• Noncash Fringe Benefits

• Mobile Workforce Taxation (Global): Equity and FICA

• Exempt W-4s/39.6% withholding

Copyright © 2014 Deloitte Tax LLP. All rights reserved.5

U.S. payroll deposit rules

Copyright © 2014 Deloitte Tax LLP. All rights reserved.6

• Typically, the date the compensation becomes taxable, will trigger the employment tax liability. The deposit date for that liability, will be based on the employer’s payroll deposit filing status. – Monthly deposit schedule — deposit due by the 15th day of the following

month.

– Semi-weekly deposit schedule• If the payday falls on a Wednesday, Thursday, and/or Friday, then deposit taxes by

the following Wednesday.

• If the payday falls on a Saturday, Sunday, Monday and/or Tuesday, then deposit taxes by the following Friday

– Deposits are due on business days, if a due date falls on a Saturday, Sunday, or legal holiday, the deposit is considered timely if it is made on the following business day.

– There is a next day deposit requirement once the accrued payroll tax liability exceeds $100,000 (“one day deposit rule”)

What is the payroll deposit date?

Copyright © 2014 Deloitte Tax LLP. All rights reserved.7

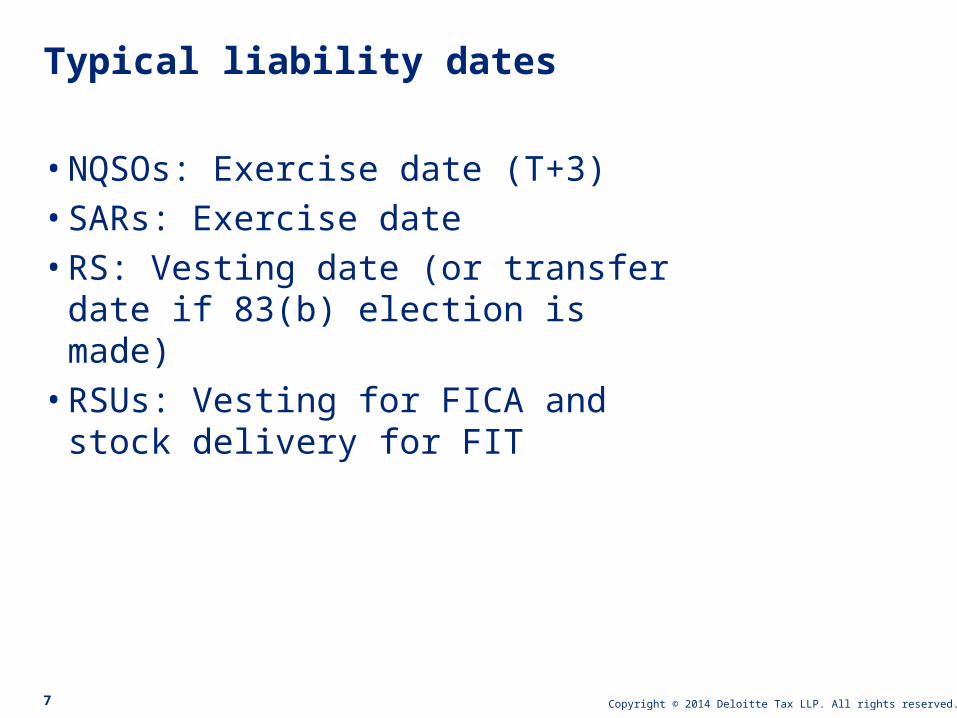

• NQSOs: Exercise date (T+3)• SARs: Exercise date• RS: Vesting date (or transfer date if 83(b)

election is made)• RSUs: Vesting for FICA and stock

delivery for FIT

Typical liability dates

Copyright © 2014 Deloitte Tax LLP. All rights reserved.8

• On March 14, 2003, a Memorandum was issued by the IRS to audit examiners to provide guidelines surrounding assessment of employment tax penalties for NQSOs.– “It has been argued that the shares (or the value of the shares) are not available to the

exerciser of the options until settlement date, and therefore no actual or constructive payment of wages takes place until that time.

– There is generally only a three day delay between time of exercise and time of settlement resulting from such exercise. In fact, under 17 C.F.R. Sec. 240.15c6-1(a), the SEC generally established a maximum three day settlement period for broker- dealer trades. There is presently no specific published guidance relative to whether the date of exercise or date of settlement is the appropriate date for considering assertion of the penalty for failure to deposit employment taxes attributable to the exercise of nonqualified stock options.”

• Under this Field Directive, auditors “should not challenge the timeliness of deposits required under Treas. Reg. § 31.6302-1(c), if such deposits are made within one day of the settlement date, as long as such settlement date does not fall more than three days from date of exercise.”

Field audit memorandum

Copyright © 2014 Deloitte Tax LLP. All rights reserved.9

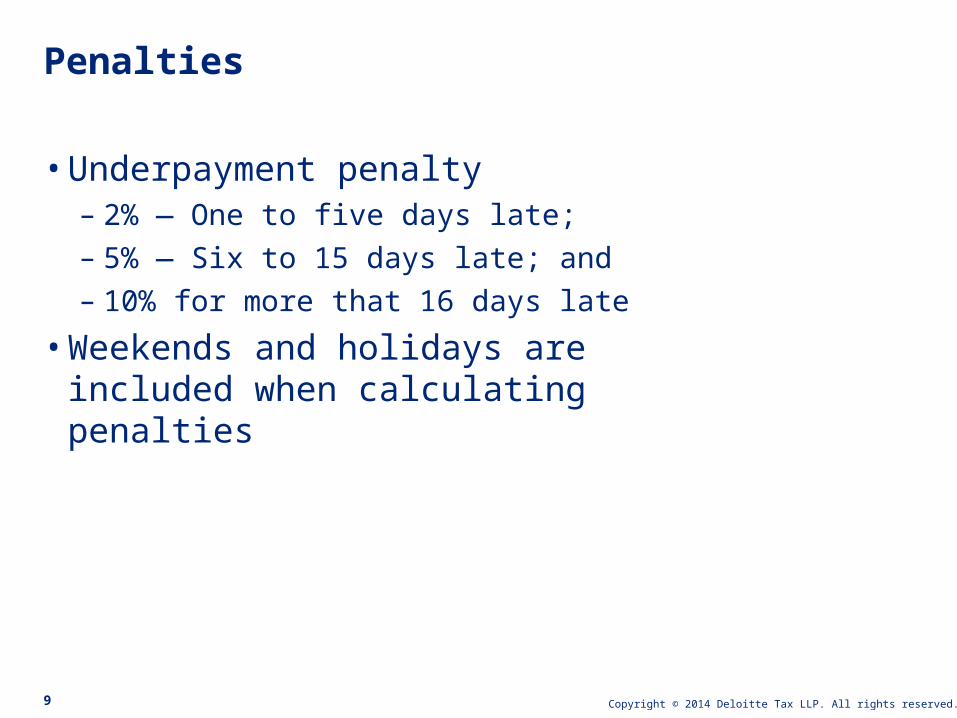

• Underpayment penalty– 2% — One to five days late;

– 5% — Six to 15 days late; and

– 10% for more that 16 days late

• Weekends and holidays are included when calculating penalties

Penalties

Copyright © 2014 Deloitte Tax LLP. All rights reserved.10

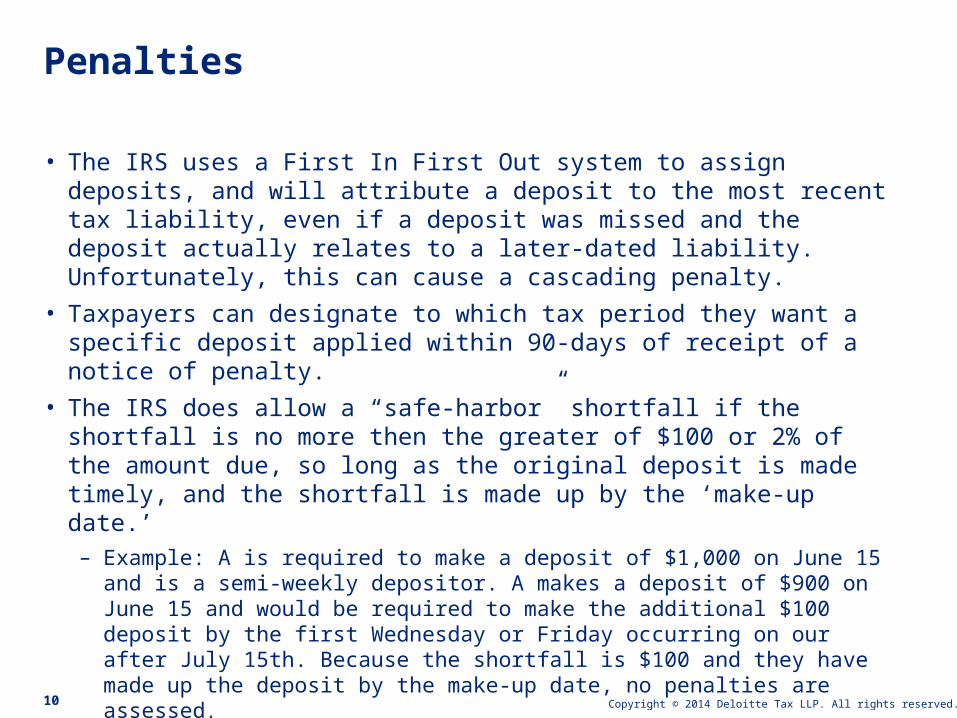

• The IRS uses a First In First Out system to assign deposits, and will attribute a deposit to the most recent tax liability, even if a deposit was missed and the deposit actually relates to a later-dated liability. Unfortunately, this can cause a cascading penalty.

• Taxpayers can designate to which tax period they want a specific deposit applied within 90-days of receipt of a notice of penalty.

• The IRS does allow a “safe-harbor” shortfall if the shortfall is no more then the greater of $100 or 2% of the amount due, so long as the original deposit is made timely, and the shortfall is made up by the ‘make-up date.’– Example: A is required to make a deposit of $1,000 on June 15 and is a semi-

weekly depositor. A makes a deposit of $900 on June 15 and would be required to make the additional $100 deposit by the first Wednesday or Friday occurring on our after July 15th. Because the shortfall is $100 and they have made up the deposit by the make-up date, no penalties are assessed.

Penalties

Copyright © 2014 Deloitte Tax LLP. All rights reserved.11

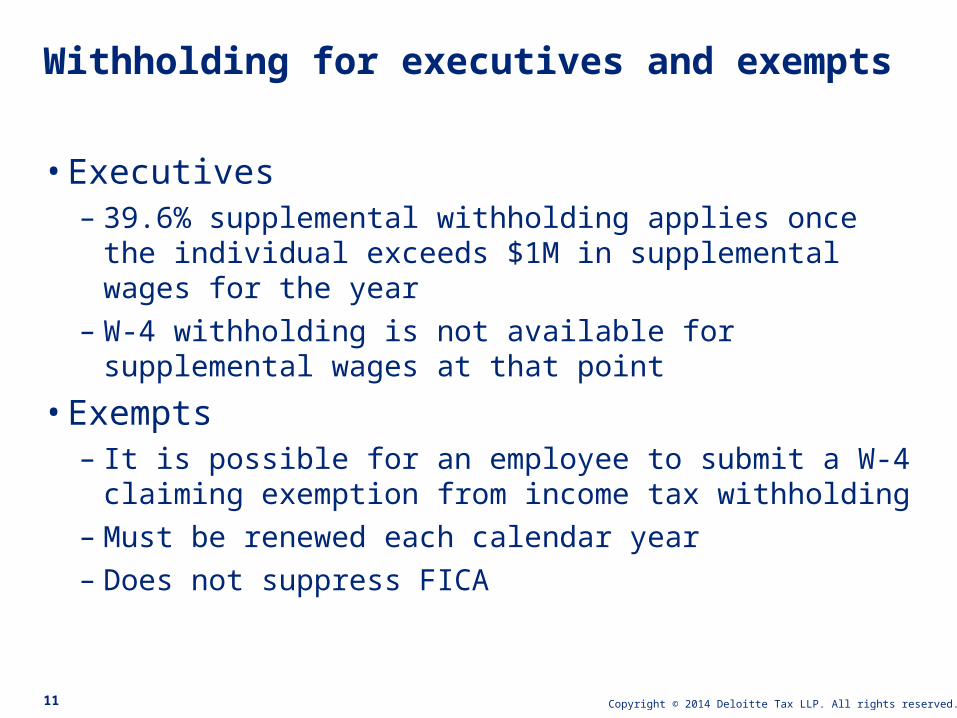

• Executives– 39.6% supplemental withholding applies once the individual

exceeds $1M in supplemental wages for the year

– W-4 withholding is not available for supplemental wages at that point

• Exempts– It is possible for an employee to submit a W-4 claiming

exemption from income tax withholding

– Must be renewed each calendar year

– Does not suppress FICA

Withholding for executives and exempts

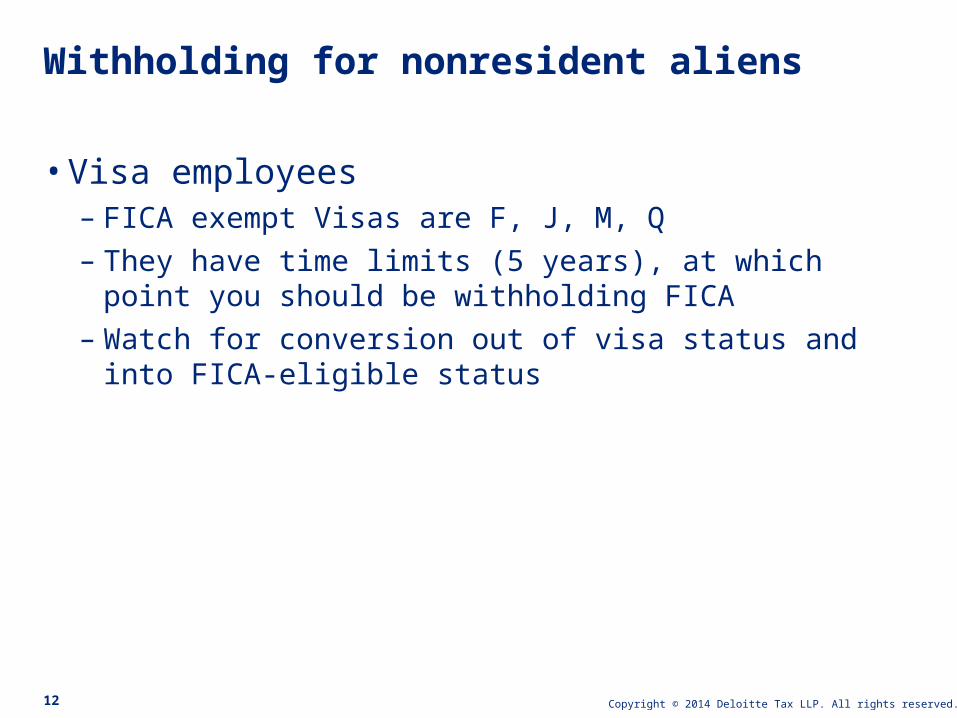

Copyright © 2014 Deloitte Tax LLP. All rights reserved.12

• Visa employees– FICA exempt Visas are F, J, M, Q

– They have time limits (5 years), at which point you should be withholding FICA

– Watch for conversion out of visa status and into FICA-eligible status

Withholding for nonresident aliens

Copyright © 2014 Deloitte Tax LLP. All rights reserved.13

Non-cash fringe benefits

Copyright © 2014 Deloitte Tax LLP. All rights reserved.14

• These items represent areas of IRS concern– Awards and prizes – Wellness programs

• Gift cards

• iPod, iPad, raffle prizes

– Award trips• “President’s club, diamond club, century club”

• Spousal accompaniment

– Sports Tickets• Occasional tickets are considered di minimus

– Company cafeteria• Subsidy is OK; free is not

Non-cash fringe benefits

Copyright © 2014 Deloitte Tax LLP. All rights reserved.15

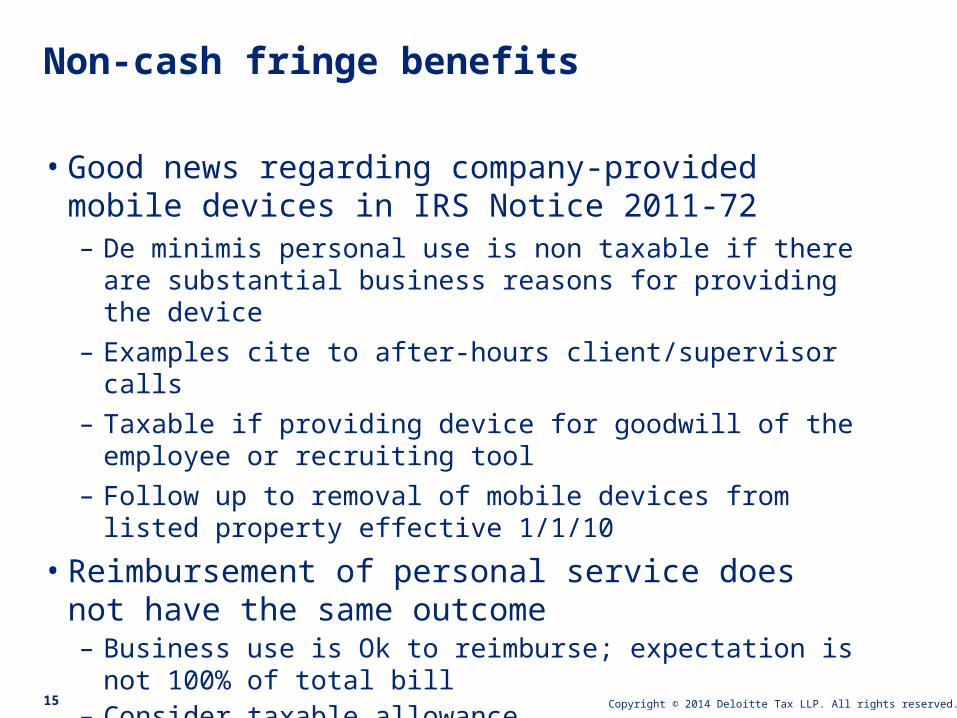

• Good news regarding company-provided mobile devices in IRS Notice 2011-72– De minimis personal use is non taxable if there are substantial

business reasons for providing the device

– Examples cite to after-hours client/supervisor calls

– Taxable if providing device for goodwill of the employee or recruiting tool

– Follow up to removal of mobile devices from listed property effective 1/1/10

• Reimbursement of personal service does not have the same outcome– Business use is Ok to reimburse; expectation is not 100% of

total bill– Consider taxable allowance

Non-cash fringe benefits

Copyright © 2014 Deloitte Tax LLP. All rights reserved.16

Employee Loans

Copyright © 2014 Deloitte Tax LLP. All rights reserved.17

• Court found that “loan” agreements were actually salary advances, taxable upon receipt.

• No fixed schedule of repayment.

• There was a reasonable prospect of repayment only in exceptional circumstances.

• Only had to repay loan if they broke their contractual promise to remain employed.

• Not required to pay interest over the term of the agreement, and not required to repay anything if they continue working.

• Did not conduct a financial investigation or credit check.

The Vancouver Clinic vs. US

Copyright © 2014 Deloitte Tax LLP. All rights reserved.18

• Unconditional promise to repay

• Whether the parties actually intended for the advance to be repaid at the time it was made.

• Expectation of both parties at the time the agreement was entered into was that the employee would work the full term of the agreement.

The Vancouver Clinic vs. US

Copyright © 2014 Deloitte Tax LLP. All rights reserved.19

Worker classification (employee v. contractor)

Copyright © 2014 Deloitte Tax LLP. All rights reserved.20

•Project workers are not employees

•Temporary workers are not employees

•Former executives returning as “consultants” are independent contractors

Common misconceptions of worker classification

Copyright © 2014 Deloitte Tax LLP. All rights reserved.21

IRS 2006 audit manual on worker classification

• Created 3 categories of evidence:• Behavioral control• Financial control• Relationship of the parties

Copyright © 2014 Deloitte Tax LLP. All rights reserved.22

Worker classification “Red flags”

• Former employees• Form 1099 & Form W-2• Form 1099 – Multiple years• Industry focus• Leads

‒ IRS internal database‒ Contractor originated‒ State info sharing

Copyright © 2013 Deloitte Development LLC. All rights reserved.23 Footer

• A new program that allows employers to resolve past worker classification issues at a reduced cost by voluntarily reclassifying their workers

• Available to businesses, tax-exempt organizations and government entities that currently erroneously treat their workers as independent contractors, and would like to correctly treat them as employees in the future

Voluntary worker classification settlement program

Copyright © 2013 Deloitte Development LLC. All rights reserved.24 Footer

• To be eligible, an applicant must:– Consistently have treated the workers in the past as nonemployees

– Have filed all required Forms 1099 for the workers for the previous three years

– Not currently be under audit by the IRS, and not currently be under audit by the DOL or a state agency concerning the classification of these workers

Eligibility for Voluntary Program

Copyright © 2013 Deloitte Development LLC. All rights reserved.25 Footer

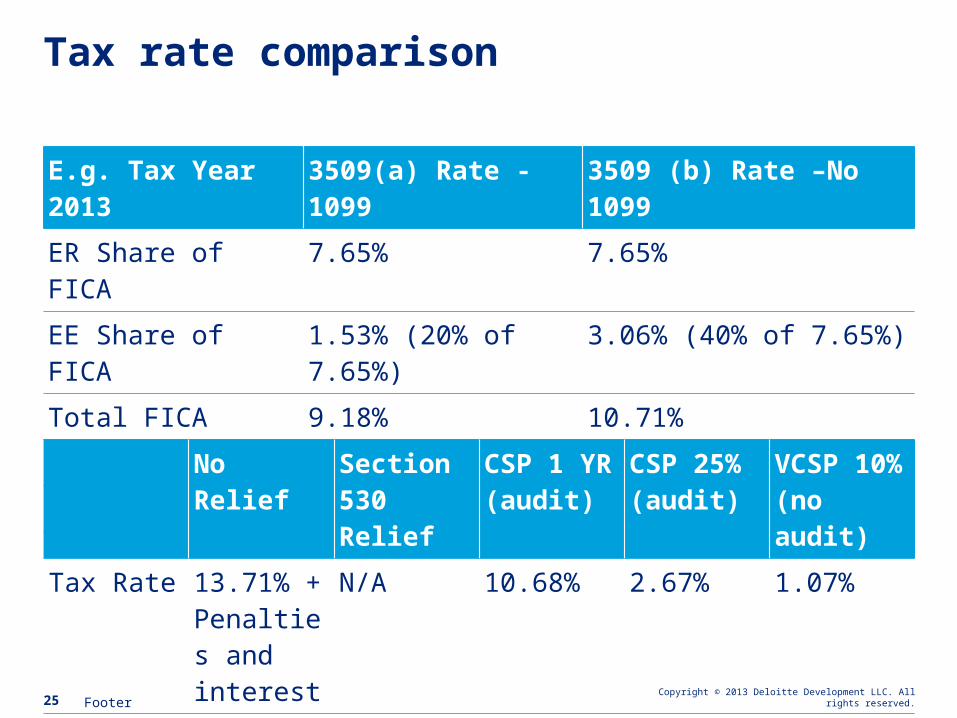

E.g. Tax Year 2013 3509(a) Rate -1099 3509 (b) Rate –No 1099

ER Share of FICA 7.65% 7.65%

EE Share of FICA 1.53% (20% of 7.65%) 3.06% (40% of 7.65%)

Total FICA 9.18% 10.71%

ITW 1.50% 3.00%

Total 10.68% 13.71%

Tax rate comparison

No Relief Section 530 Relief

CSP 1 YR (audit)

CSP 25% (audit)

VCSP 10% (no audit)

Tax Rate 13.71% + Penalties and interest

N/A 10.68% 2.67% 1.07%

Copyright © 2014 Deloitte Tax LLP. All rights reserved.26

Mobile Workforce Taxation

Copyright © 2014 Deloitte Tax LLP. All rights reserved.27

• Many states have not established a de minimus reporting threshold, which creates administrative challenges to achieving full compliance.

• Many states define the employer withholding obligations as an approximation of what the employee is anticipated to owe in taxes.

• Standard deductions and/or personal exemptions may provide a de minimus limit for determining when a tax filing obligation arises.

What are the concerns with domestic travel?U.S. Domestic business travelers

Copyright © 2014 Deloitte Tax LLP. All rights reserved.28

U.S. Domestic business travelers (cont.)

California Connecticut

Very aggressive regarding non-resident wage withholding and tax remittances

No De Minimis threshold

De Minimis threshold14 days

Illinois New York

No De Minimis threshold

De Minimis threshold14 days

December 2, 2009 CT issued Announcement 2009(9) requiring employer wage reporting and tax withholding for non-residents working 14 or more days in CT throughout the year

Has quite ‘favorable’ non-resident guidelines — Especially if firm is not located anywhere in IL

Uses an informal calendar year de minimis threshold for state tax withholding for a non-resident working in New York as reported in its state Field Audit Guidelines issued July 1, 2004 and TSB-M-12(5)I issued on July 5, 2012

Copyright © 2014 Deloitte Tax LLP. All rights reserved.29

• Jane resides and normally works in Ohio and travels to New York on business for more than 15 days during a year. New York has a higher individual state tax rate than Ohio.

Ohio state resident traveling to New YorkExample: State to state

Without multi-jurisdictional reporting With multi-jurisdictional reporting

Employee obligation

Employer obligation Employee obligation Employer obligation

Resident state Ohio File Ohio resident income tax return and taxes paid by employee

Report all wages and withhold income taxes from employee and remit income taxes only to Ohio

File Ohio resident income tax return with taxes paid by employee less credit for NY tax payments

Report all wages and withhold income taxes from employee and remit Ohio-sourced income taxes to Ohio

Non-resident working state (Not tax protected)

New York N/A N/A File New York non-resident income tax return with incremental NY taxes paid by employee

Report all wages, and withhold increased NY-sourced income taxes from employee, and remit applicable income taxes to New York

Non-resident working state (Tax protected)

New York N/A N/A File New York non-resident income tax return by employee with incremental taxes paid by firm

Report all wages and remit applicable New York sourced grossed up income taxes to New York

Copyright © 2014 Deloitte Tax LLP. All rights reserved.30

Non-resident Travelers to Canada

Reg. 105/Transfer Pricing

(Corporate)

PE/Services PE

(Corporate)

Reg 102/ Waivers

(HR-Payroll)

Copyright © 2014 Deloitte Tax LLP. All rights reserved.31

Current State – Regulation 102 Rules

• The Canadian tax rules (Regulation 102) stipulate that every employer paying non-resident employees working in Canada should withhold Canadian income tax at source on the Canadian source earnings.

• Withholding obligation applies to non-resident employers, with no threshold.

• Generally non resident or their Canadian subsidiaries will operate shadow payroll to meet the obligations.

• Withholding obligation applies even if the employee is ultimately exempt from Canadian tax under a Tax Treaty, unless a waiver is applied for.

Copyright © 2014 Deloitte Tax LLP. All rights reserved.32

Current State – Regulation 102 RULES

The current waiver process is done on an employee-by-employee basis:

• The R102 - J waiver is a joint employee/employer application used when the employee’s total Canadian remuneration is less than $10,000 for the US residents or $5,000 for residents of other treaty countries.

• The R102 - R waiver is an employee only application used when the employee is expected to earn more than $10,000 when a US resident (or $5,000 when a resident of another treaty country), but the income is exempt under other treaty conditions (i.e. remuneration not borne by a PE the NR employer has in Canada).

Copyright © 2014 Deloitte Tax LLP. All rights reserved.33

Current State – Enforcement of Rules

Employer Considerations:

• CRA is increasingly aggressive in assessing tax withholdings in all situations, unless a waiver has not been obtained.

• The employer must prepare a T4 slip and T4 Summary to report the Canadian source compensation and tax withheld at source.

• CRA requires the non-resident employer to register and open payroll accounts to facilitate the waiver application process.

• The employer can be held liable to pay the taxes that should have been withheld from the NR employees.

• Penalties of 10% (or 20% for certain situations) can apply on tax amounts not withheld, plus interest.

Copyright © 2014 Deloitte Tax LLP. All rights reserved.34

Current State – Enforcement of Rules

Employee Considerations:

• The NR employee is required to obtain either a Canadian SIN or ITN (Individual Tax Number) for reporting purposes (e.g. T4 slip).

• If the employee is treaty exempt but no waiver was filed, they must file a NIL personal tax return to be refunded the taxes withheld.

• CRA is not allowing any withholding taxes be refunded back to the Company directly. All refunds must be made in the name of the employee. This can be a problem if the tax was originally funded by the employer.

• The R102-R waiver can’t be filed retroactively. It must be submitted at least 30 days prior to the employee beginning work in Canada. The R102-J waiver can however be approved retroactively up to 60 days prior to the date a complete waiver application is received.

Copyright © 2014 Deloitte Tax LLP. All rights reserved.35

Administrative Relief - Conferences

If an employee is working in Canada immediately before or after the conference, only the days (maximum of 10) spent at the conference will be exempted.

Employee still required to obtain a waiver of the withholding tax for the work days spent before or after.

The relief will not be allowed in circumstances the CRA considers to be abusive. For example the relief will not apply where an employee participates in numerous conferences in a year.

The relief appears to be of somewhat limited application

Copyright © 2014 Deloitte Tax LLP. All rights reserved.36

FICA Refunds – Quality Stores

Copyright © 2014 Deloitte Tax LLP. All rights reserved.37

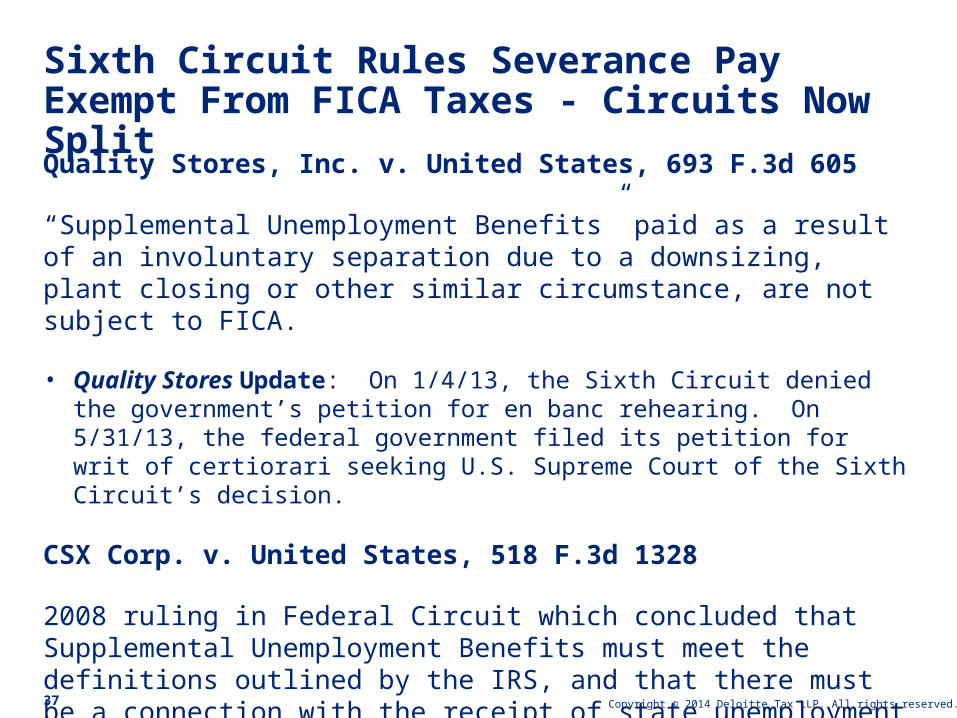

Quality Stores, Inc. v. United States, 693 F.3d 605

“Supplemental Unemployment Benefits” paid as a result of an involuntary separation due to a downsizing, plant closing or other similar circumstance, are not subject to FICA.

• Quality Stores Update: On 1/4/13, the Sixth Circuit denied the government’s petition for en banc rehearing. On 5/31/13, the federal government filed its petition for writ of certiorari seeking U.S. Supreme Court of the Sixth Circuit’s decision.

CSX Corp. v. United States, 518 F.3d 1328

2008 ruling in Federal Circuit which concluded that Supplemental Unemployment Benefits must meet the definitions outlined by the IRS, and that there must be a connection with the receipt of state unemployment benefits.

Sixth Circuit Rules Severance Pay Exempt From FICA Taxes - Circuits Now Split

Copyright © 2014 Deloitte Tax LLP. All rights reserved.38

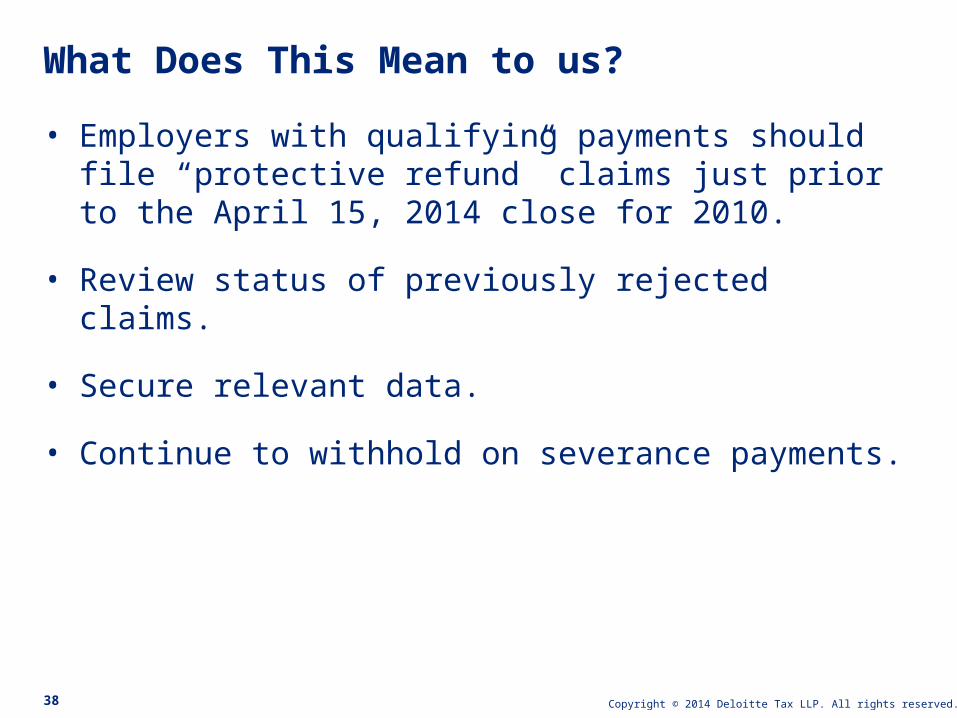

• Employers with qualifying payments should file “protective refund” claims just prior to the April 15, 2014 close for 2010.

• Review status of previously rejected claims.

• Secure relevant data.

• Continue to withhold on severance payments.

What Does This Mean to us?

Copyright © 2014 Deloitte Tax LLP. All rights reserved.39

DOMA

Copyright © 2014 Deloitte Tax LLP. All rights reserved.40

• IRS clarified that for federal purposes, a same-sex marriage valid in a U.S. state, District of Columbia, U.S. territory, or a foreign country will be recognized for U.S. federal tax purposes.

• Applies regardless of current state of residence.

• Applies to all federal tax provisions where marriage is a factor.

• Amended tax returns may be filed for open statute of limitations year(s)—generally 2010 and later.

DOMA impact: Rev. Rul. 2013-17

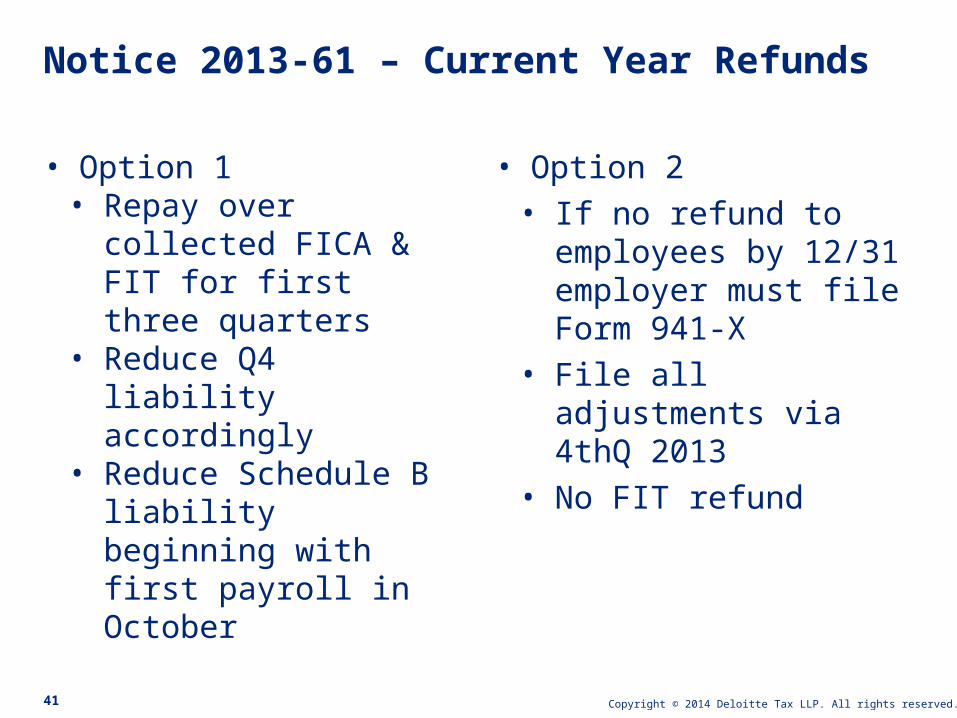

Copyright © 2014 Deloitte Tax LLP. All rights reserved.41

• Option 1• Repay over collected

FICA & FIT for first three quarters

• Reduce Q4 liability accordingly

• Reduce Schedule B liability beginning with first payroll in October

Notice 2013-61 – Current Year Refunds

• Option 2• If no refund to

employees by 12/31 employer must file Form 941-X

• File all adjustments via 4thQ 2013

• No FIT refund

Copyright © 2014 Deloitte Tax LLP. All rights reserved.42

• File Form 941-X for the 4thQ of each open year

• Write “WINDSOR” on the top of Page 1

• Correct applicable Social Security and Medicare wages/tax

• No refund of FIT

• W-2c’s are required

Notice 2013-61 - Prior Year Refund

Copyright © 2014 Deloitte Tax LLP. All rights reserved.43

Questions?

Copyright © 2014 Deloitte Tax LLP. All rights reserved.44

Jason RussellDirectorDeloitte Tax LLP+1 [email protected]

Contact information

Copyright © 2014 Deloitte Tax LLP. All rights reserved.45

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

Copyright © 2014 Deloitte Tax LLP. All rights reserved.46

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2013 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu Limited

Related Documents