Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall. Account for stock dividends 1 1

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall. Account for stock dividends 1 1 1.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Account for stock dividends

1

11

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

A distribution of a corporation’s own stockAffects only stockholders’ equity accounts

No effect on total stockholders’ equityNo effect on assets or liabilities

Stockholders receive proportionate sharesExample–10% stock dividend; every stockholder receives 10% of shares distributed

Total number of shares issued and outstanding increasesOwnership percentages remain the same

2

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Conserve cashContinue dividends without using cash

Reduce market price per shareShare supply increases; market price decreasesLess expensive; more attractive investment

Reward investorsShareholders receive something of value

3

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Same three dates for a stock dividendDeclaration date; record date; distribution date

Small stock dividendDistribution is less than 20 to 25% of issued sharesDebit Retained earnings for market value of shares to be distributedCredit Common stock for the par value of the stock andCredit Paid-in capital for excess of par—common

4

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

LargeDistribution is greater than 20% to 25% of issued sharesDebit Retained earnings for par or stated value of sharesCredit Common stock for par or stated value of sharesRare

5

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Equity after 5% Common Stock Dividend

Equity after 50% Common Stock Dividend

6

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Compare and contrast the accounting for cash dividends and stock dividends.

1.In the space provided, insert either “Cash dividends,” “Stock dividends,” or “Both cash dividends and stock dividends” to complete each of the following statements:

a. ________________decrease Retained earnings.

b. ________________ has(have) no effect on a liability.

7

Both cash dividends and stock dividends

Stock dividends

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

(Continued)

c. ________________ increase Paid-in capital by the same amount that they decrease Retained earnings.

d. ________________ decrease both total assets and total stockholders’ equity, resulting in a decrease in the size of the company.

8

Stock dividends

Cash dividends

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Yummy, Inc., had 310,000 shares of $1 par common stock issued and outstanding as of December 1, 2012. The company is authorized to issue 1,400,000 common shares. On December 15, 2012, Yummy declared and distributed a 5% stock dividend when the market value for Yummy’s common stock was $3.

Requirements:1. Journalize the stock dividend.2. How many shares of common stock are outstanding after the dividend?

9

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

1. Journalize the stock dividend.

2. How many shares of common stock are outstanding after the dividend?

10

Journal EntryDATE ACCOUNTS DEBIT CREDIT

Dec 15 Retained earnings 46,500

Common stock 15,500

Paid in capital in excess of par-

common

31,000

310,000 +15,500 = 325,500

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Account for stock splits

11

22

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

A stock split:Cuts par value per shareIncreases the number of shares of stock issued and outstandingLeaves all account balances and total stockholders’ equity unchanged

Balances in the accounts are unchangedRecord in a memorandum entry–a journal entry without debits and credits

12

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Before split

13

After split

Authorized shares should be

40,000,000

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Stock dividends and stock splits have similarities and differences

14

EventCommon

stock

Paid-in capital in

excess of par

Retained earnings

Total stockholders

’ equity

Cash dividend

No effect No effect Decrease Decrease

Stock dividend

Increase Increase Decrease No effect

Stock split No effect No effect No effect No effect

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Decorator Plus Imports recently reported the following stockholders’ equity (adapted except par value per share):

Suppose Decorator Plus split its common stock 2 for 1 in order to decrease the market price per share of its stock. The company’s stock was trading at $20 per share immediately before the split.

15

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

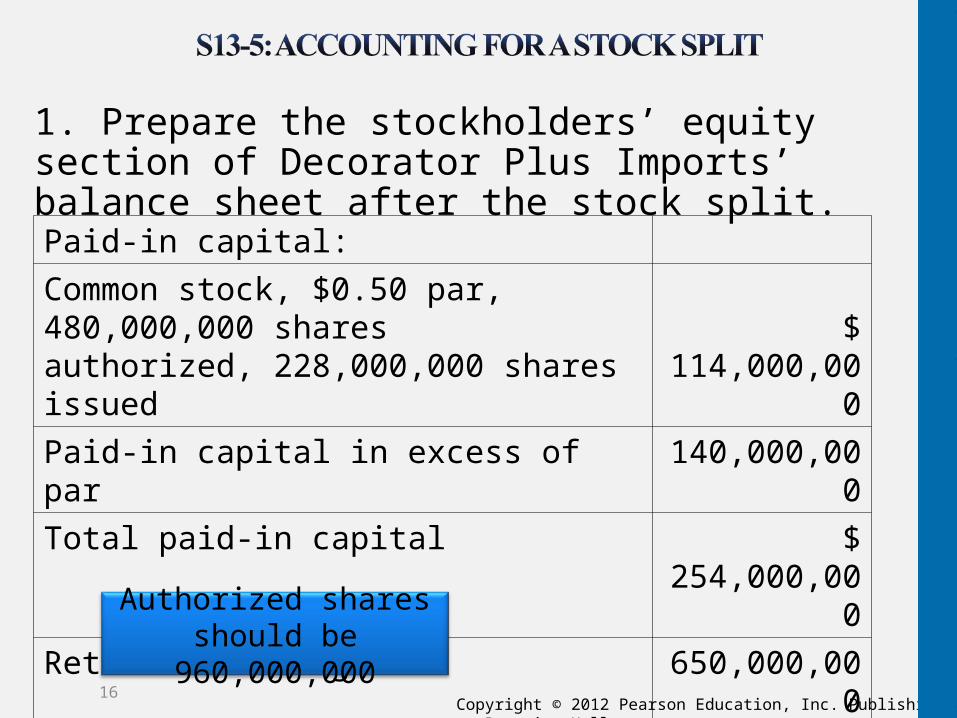

1. Prepare the stockholders’ equity section of Decorator Plus Imports’ balance sheet after the stock split.

16

Paid-in capital:

Common stock, $0.50 par, 480,000,000 sharesauthorized, 228,000,000 shares issued $ 114,000,000

Paid-in capital in excess of par 140,000,000

Total paid-in capital $ 254,000,000

Retained earnings 650,000,000

Total stockholders’ equity $ 904,000,000

Authorized shares should be

960,000,000

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

2. Were the account balances changed or unchanged after the stock split?

17

Paid-in capital:

Common stock, $0.50 par, 480,000,000 sharesauthorized, 228,000,000 shares issued $ 114,000,000

Paid-in capital in excess of par 140,000,000

Total paid-in capital $ 254,000,000

Retained earnings 650,000,000

Total stockholders’ equity $ 904,000,000

Unchanged

Unchanged

Unchanged

Unchanged

Authorized shares should be 960,000,000

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Account for treasury stock

18

33

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

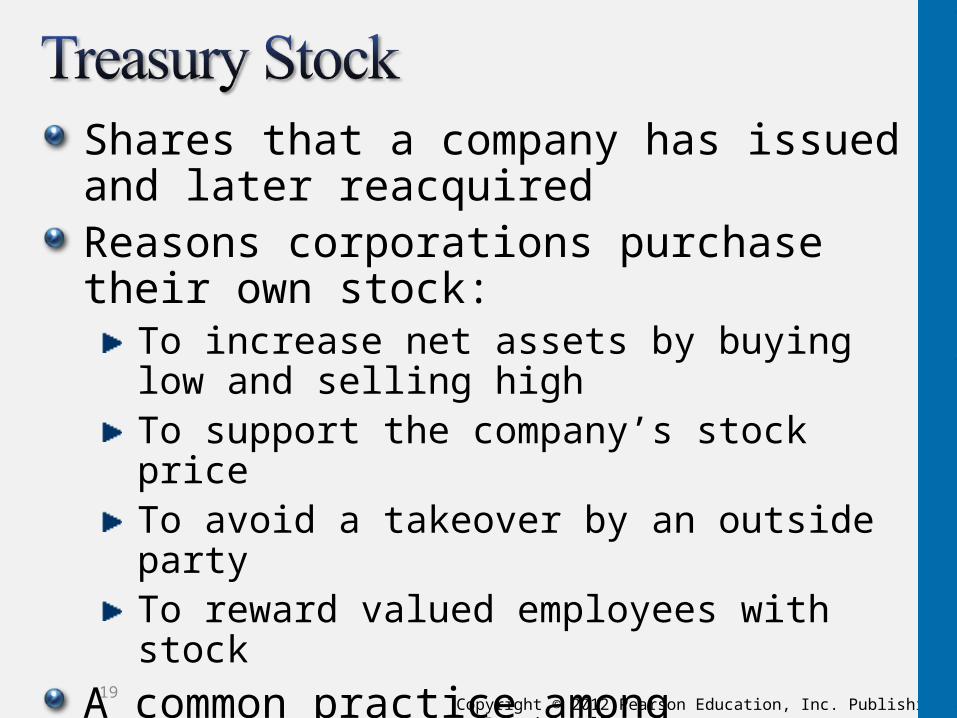

Shares that a company has issued and later reacquiredReasons corporations purchase their own stock:

To increase net assets by buying low and selling highTo support the company’s stock priceTo avoid a takeover by an outside partyTo reward valued employees with stock

A common practice among corporations

19

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Contra equity accountDebit balance

Recorded at cost (not par)Reported beneath Retained earnings on the balance sheet

Reduction to total stockholders’ equity

Decreases outstanding sharesNot eligible for dividendsNot eligible to vote

20

Issued stock – Treasury stock = Outstanding stock

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

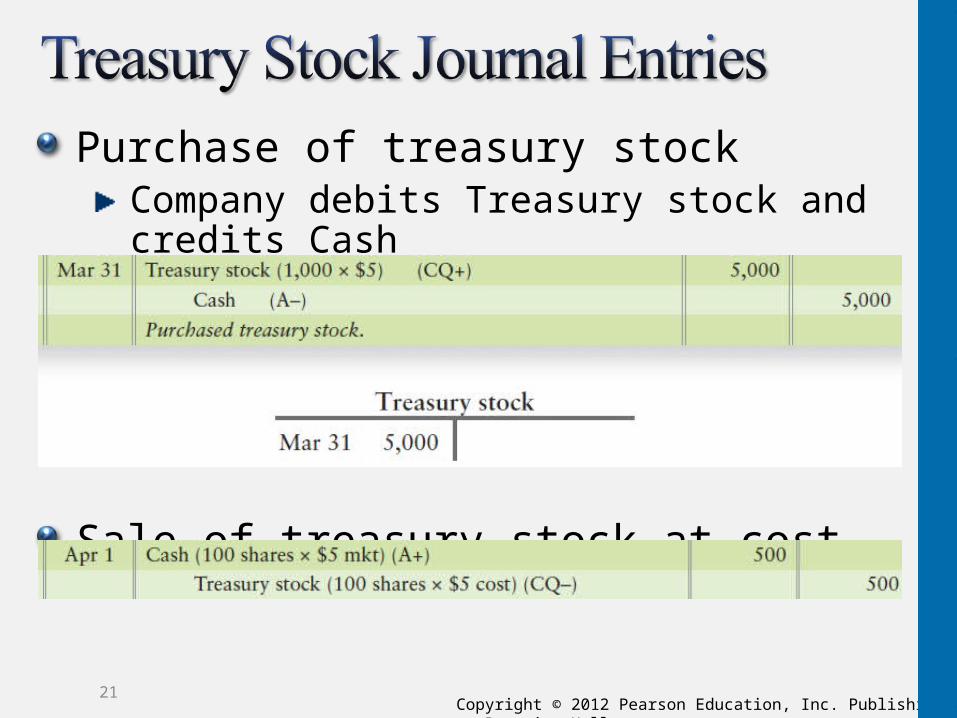

Purchase of treasury stockCompany debits Treasury stock and credits Cash

Sale of treasury stock at cost

21

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Sale of treasury stock above costDifference is credited to Paid-in capital from treasury stock transactions

Sale of treasury stock below costDifference is debited to Paid-in Capital from treasury stock transactions, if availableOtherwise debit Retained earnings

22

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Sale of treasury stock below cost Paid-in capital from treasury stock transactions is insufficient to cover shortfallDebit Retained earnings for the difference

23

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Reported beneath Retained earnings as a reduction

24

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

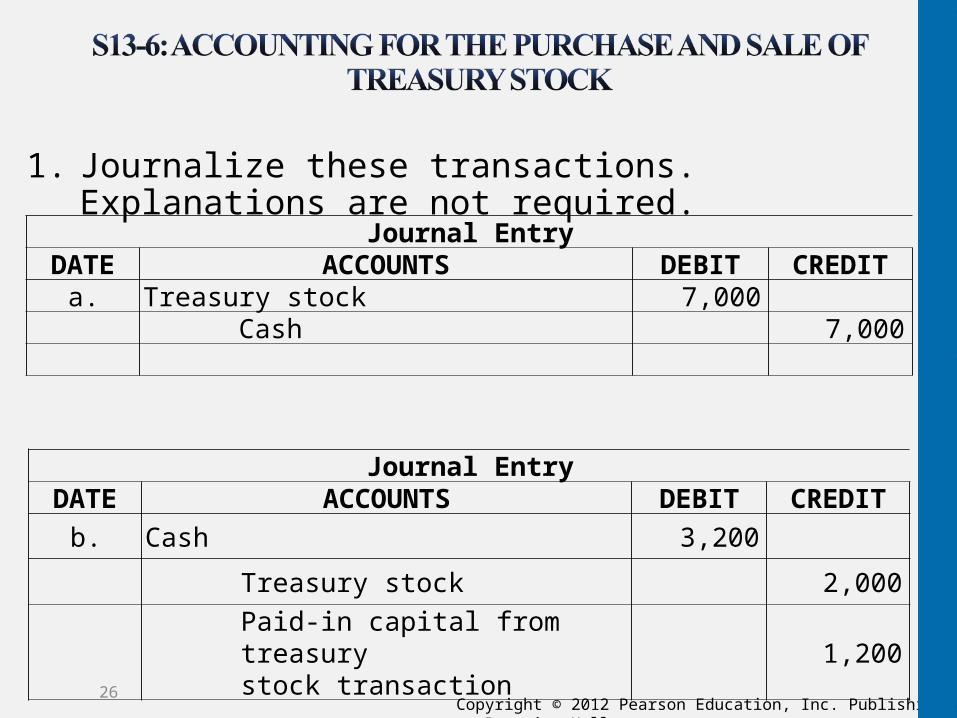

Discount Center Furniture, Inc., completed the following treasury stock transactions:a.Purchased 1,400 shares of the company’s $1 par common stock as treasury stock, paying cash of $5 per share. b.Sold 400 shares of the treasury stock for cash of $8 per share.

RequirementsJournalize these transactions. Explanations are not required.

Show how Discount Center will report treasury stock on its December 31, 2012 balance sheet after completing the two transactions. In reporting the treasury stock, report only on the Treasury stock account.

25

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

1. Journalize these transactions. Explanations are not required.

26

Journal EntryDATE ACCOUNTS DEBIT CREDIT

a. Treasury stock 7,000Cash 7,000

Journal EntryDATE ACCOUNTS DEBIT CREDIT

b. Cash 3,200

Treasury stock 2,000

Paid-in capital from treasurystock transaction

1,200

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

2. Show how Discount Center will report treasury stock on its December 31, 2012 balance sheet after completing the two transactions. In reporting the treasury stock, report only on the Treasury stock account.

27

Stockholders’ equity

Treasury stock 1,000 shares at cost 5,000

Related Documents

![Dividends and _dividend_policy_powerpoint_presentation[1]](https://static.cupdf.com/doc/110x72/5549020cb4c9058d368b45f6/dividends-and-dividendpolicypowerpointpresentation1.jpg)

![Optionnel - Demographic Dividends[1].Kobe.2005](https://static.cupdf.com/doc/110x72/577cd37e1a28ab9e789716f0/optionnel-demographic-dividends1kobe2005.jpg)