Copyright © 2008 Pearson Education Canada 5-1 Chapter 5 Life Insurance

Copyright © 2008 Pearson Education Canada 5-1 Chapter 5 Life Insurance.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2008 Pearson Education Canada5-1

Chapter 5

Life Insurance

Copyright © 2008 Pearson Education Canada 5-2

Purpose of Life Insurance Protect dependent’s income

stream Provide liquidity for estate

Copyright © 2008 Pearson Education Canada 5-3

Life Insurance Proceeds Can Be Used to

Provide education or income for children Pay off the mortgage or other debts Provide retirement income Make estate or tax payments Provide survivor benefits Establish endowment funds for children

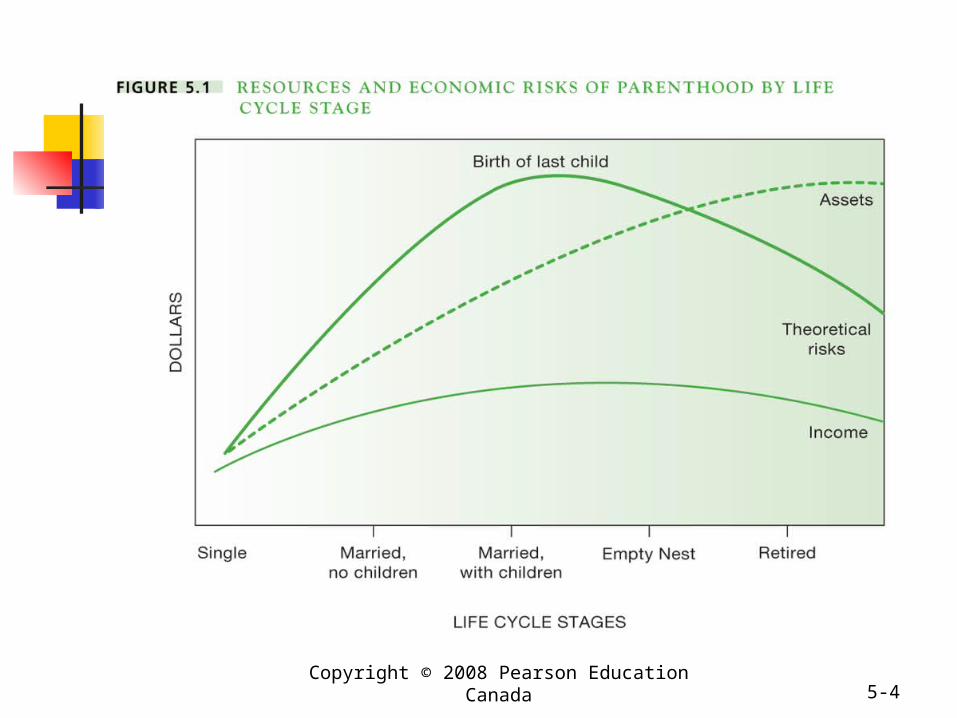

Copyright © 2008 Pearson Education Canada 5-4

Copyright © 2008 Pearson Education Canada 5-5

Basic Concepts of Life Insurance

Copyright © 2008 Pearson Education Canada 5-6

Policy Agreement or contract Between

Insured person and insurance company

States which risks the life insurance company has agreed to assume

Copyright © 2008 Pearson Education Canada 5-7

Face Amount Amount of agreed payout

At time of death

Copyright © 2008 Pearson Education Canada 5-8

Beneficiary Person named in the policy

To receive the death benefit

Copyright © 2008 Pearson Education Canada 5-9

Premiums Regular payments by the insured

To the insurance company

Copyright © 2008 Pearson Education Canada 5-10

Insurable Interest Relationship between

Insured and event insured against Essential for all insurance

Insure your own life Insure life of another person

Spouse, child, grandchild, employee Or any person on whom insured may

be wholly or partially dependent

Copyright © 2008 Pearson Education Canada 5-11

Three Basic Principles of Life Insurance

1. Pooling risk2. The pure cost of insurance3. The level premium

Copyright © 2008 Pearson Education Canada 5-12

1. Pooling Risk Pooling small contributions of

many people Compensate a few experiencing a

loss Based on mortality tables

Copyright © 2008 Pearson Education Canada 5-13

2. The Pure Cost of Life Insurance Follows mortality curve More expensive

With age For males

Copyright © 2008 Pearson Education Canada 5-14

Mortality Rate Deaths per thousand of population Rises with age Higher for males General state of health Hazardous activities

Scuba diving Hang gliding

Copyright © 2008 Pearson Education Canada 5-15

Copyright © 2008 Pearson Education Canada 5-16

Mortality Cost

Death ofy ProbabilitBenefitDeath

Copyright © 2008 Pearson Education Canada 5-17

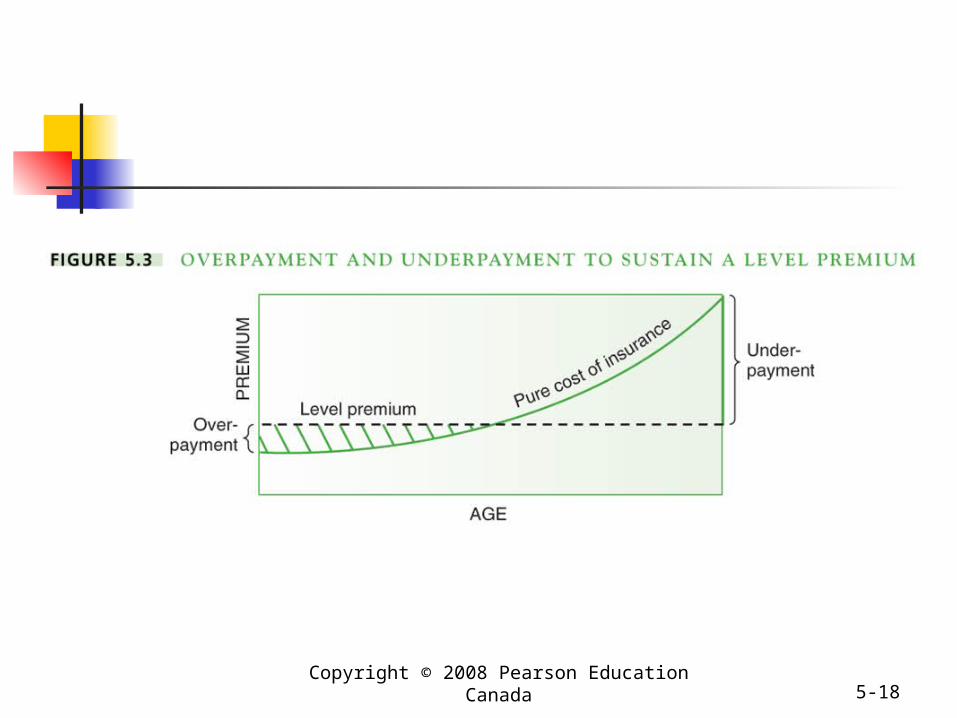

3. The Level Premium Constant premium over the life of

the policy Causes overpayment at beginning

of the policy And underpayment at end

Gives rise to policy reserves

Copyright © 2008 Pearson Education Canada 5-18

Copyright © 2008 Pearson Education Canada 5-19

Policy Reserves Also called cash surrender value Overpayment of premium in early

years Level premium > pure cost of insurance

Refundable If policy cancelled If coverage reduced

Not a saving feature!

Copyright © 2008 Pearson Education Canada 5-20

Factors Affecting Cost of Life Insurance Mortality rate Loading charges

Administrative costs, commissions, dividends

Frequency of premium payments Annual payments cheaper than monthly

How premiums are calculated Participating policies Non-participating policies

Copyright © 2008 Pearson Education Canada 5-21

Participating Policies Premiums generally higher Policy-holder gets refund

If premiums are too high Refund called a dividend Refund not taxable

Copyright © 2008 Pearson Education Canada 5-22

Refund, Dividend, Depends Upon Company’s efficiency Return on investment Amount paid in claims Policy cancellations

Copyright © 2008 Pearson Education Canada 5-23

Non-participating Policies Premiums cannot be increased No dividends

Copyright © 2008 Pearson Education Canada 5-24

Types of Life Insurance Term life Whole life Combination

Copyright © 2008 Pearson Education Canada 5-25

Term Life Insurance Term life insurance Decreasing term life insurance Group life insurance Credit life insurance

Copyright © 2008 Pearson Education Canada 5-26

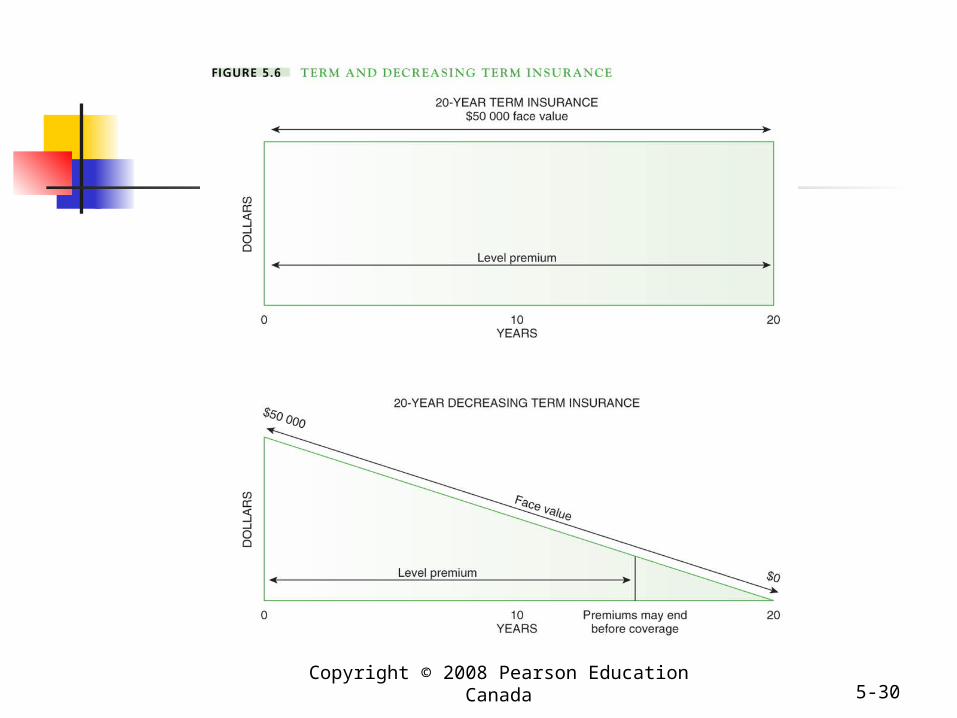

Term Life Insurance Constant face value Constant premium during term

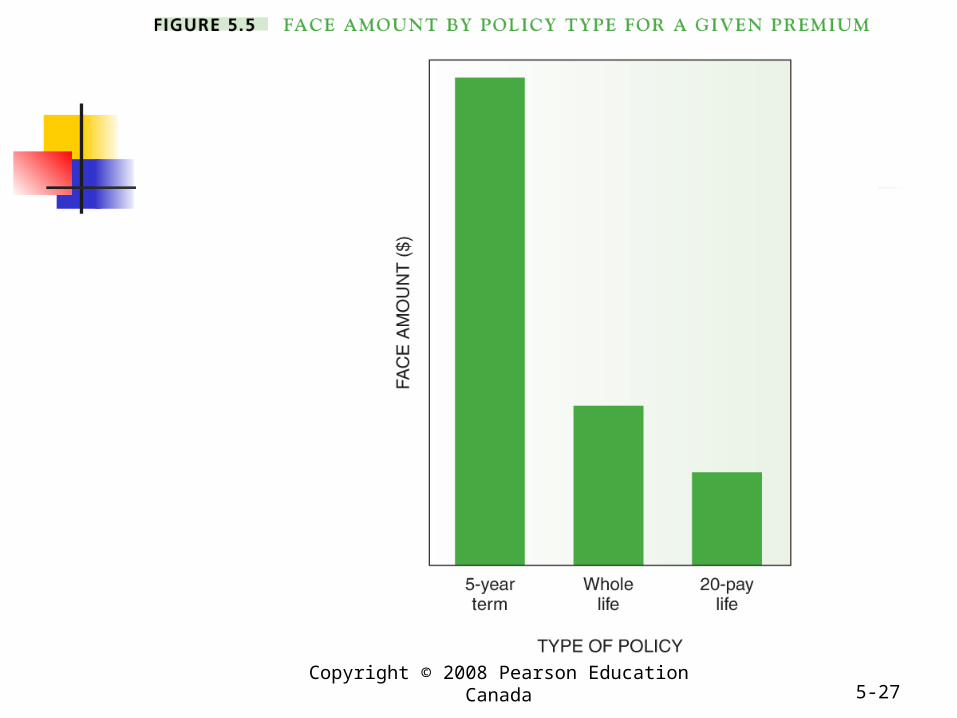

Premium increases upon renewal No cash surrender value Most face value per dollar premium

Specified risk Not 100% probability

Definite time Not life

Copyright © 2008 Pearson Education Canada 5-27

Copyright © 2008 Pearson Education Canada 5-28

Decreasing Term Life Insurance Variation of term insurance Decreasing face value

Falls to zero at end of term Constant premium Income protection for young families

Maximum coverage when children young Reduced coverage when children older

Copyright © 2008 Pearson Education Canada 5-29

Decreasing Term Life Insurance May be used as mortgage

insurance To pay off mortgage balance No legal obligation to pay off

mortgage

Copyright © 2008 Pearson Education Canada 5-30

Copyright © 2008 Pearson Education Canada 5-31

Group Life Insurance A variation of term insurance Bought by employers Paid for by workers/employer Usually one-year renewable term Terminates with employment

Possible option to convert to individual policy Premiums lower

Especially for older employees

Related Documents