Copyright © 2007 Prentice-Hall. All rights reserved The Master Budget and Responsibility Accounting Chapter 22

Copyright © 2007 Prentice-Hall. All rights reserved The Master Budget and Responsibility Accounting Chapter 22.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2007 Prentice-Hall. All rights reserved

The Master Budget and Responsibility AccountingThe Master Budget and

Responsibility Accounting

Chapter 22

Copyright © 2007 Prentice-Hall. All rights reserved

All of the following are key benefits of budgeting except:

1. provides a benchmark for evaluating performance

2. forces manager to plan for the future

3. ensures a positive cash flow

4. promotes coordination and communication within the organization

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: 3

Copyright © 2007 Prentice-Hall. All rights reserved

The operating budget includes all of the following except

1. Operating expense budget

2. Budgeted income statement

3. Sales budget

4. Capital expenditures budget

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: 4Although the capital expenditures budget is a part of the Master Budget, it is not part of the Operating Budget

Copyright © 2007 Prentice-Hall. All rights reserved

The preparation of the Master Budget begins with

1. Operating expense budget

2. Budgeted income statement

3. Sales budget

4. Capital expenditures budget

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: 3

Copyright © 2007 Prentice-Hall. All rights reserved

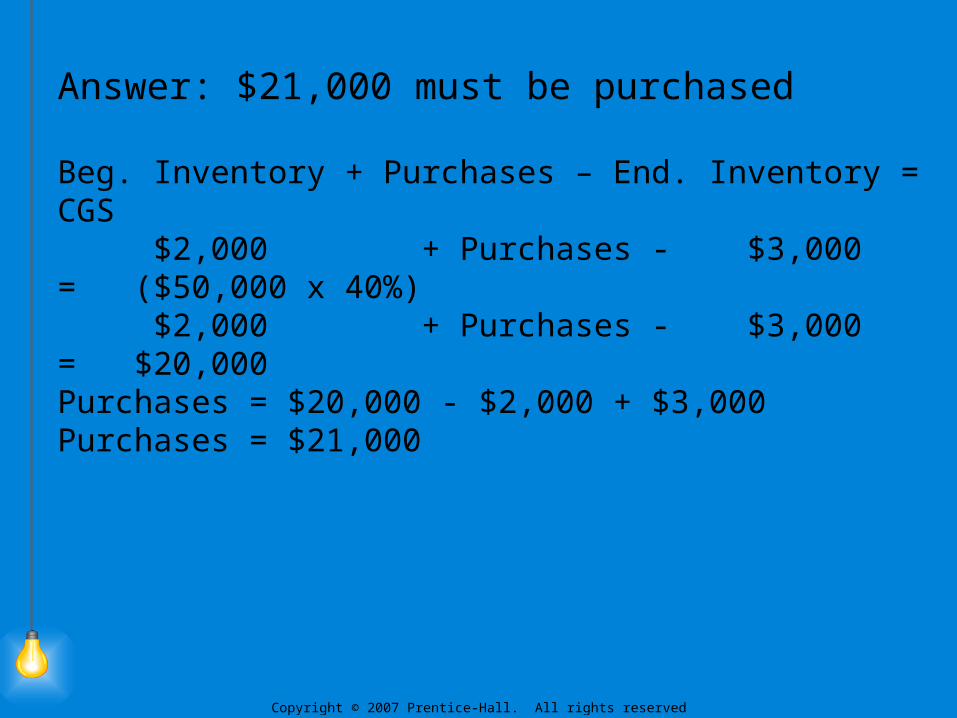

The purchasing department has gathered the following data:

Sales from sales budget $50,000

Beginning Inventory 2,000

Projected ending inventory 3,000

Cost of goods sold 40% of sales

How much inventory must be purchased?

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: $21,000 must be purchased

Beg. Inventory + Purchases – End. Inventory = CGS $2,000 + Purchases - $3,000 = ($50,000 x 40%) $2,000 + Purchases - $3,000 = $20,000Purchases = $20,000 - $2,000 + $3,000Purchases = $21,000

Copyright © 2007 Prentice-Hall. All rights reserved

The following have been projected in appropriate budgets: Sales for October: $50,000

Cost of goods sold: 60% of salesSales are expected to increase by 10% in November. What is the budgeted gross profit for November?

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: Budgeted sales for Nov.($50,000 x 110%) $55,000Less cost of goods sold ($55,000 x 60%) 33,000Budgeted gross profit for Nov. $22,000

Copyright © 2007 Prentice-Hall. All rights reserved

The following amounts have been projected:Sales from sales budget: $50,000Salaries: $10,000Commissions: 10% of salesRent: $1,000Miscellaneous expenses: 6% of salesWhat are the projected operating expenses?

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: Projected operating expenses = $19,000

Salaries $10,000Commissions 5,000Rent 1,000Miscellaneous 3,000 Total $19,000

Copyright © 2007 Prentice-Hall. All rights reserved

Which of the following would not be included in the cash budget?

1. Cash payments to suppliers

2. Depreciation expense

3. Cash receipts from customers

4. Cash payments for 1 year’s insurance in advance

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: 2 Depreciation is a noncash expense.

Copyright © 2007 Prentice-Hall. All rights reserved

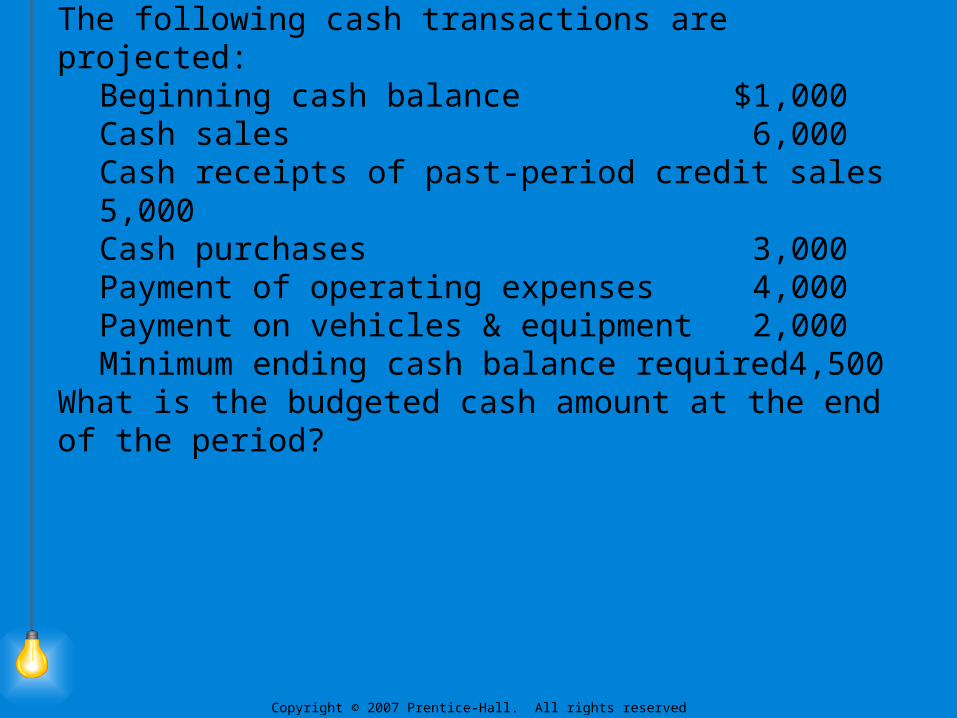

The following cash transactions are projected:Beginning cash balance $1,000Cash sales 6,000Cash receipts of past-period credit sales 5,000Cash purchases 3,000Payment of operating expenses 4,000Payment on vehicles & equipment 2,000Minimum ending cash balance required 4,500

What is the budgeted cash amount at the end of the period?

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: $3,000

Beginning cash balance $1,000Cash sales 6,000Cash receipts of past-period credit sales 5,000

Subtotal $12,000Cash purchases ($3,000)Payment of operating expenses (4,000)Payment on vehicles & equipment (2,000) (9,000)

Budgeted ending cash balance $3,000

Copyright © 2007 Prentice-Hall. All rights reserved

Bertrand Co. budgets the following credit sales: January, $4,000; February, $2,000; March, $6,000. Prior experience shows that payment for credit sales is received as follows: 10% in the month of sale, 70% in the first month after sale, 10% in the second month after the sale, and 10% uncollectible. How much cash does Bertrand expect to collect in March as a result of credit sales?

Copyright © 2007 Prentice-Hall. All rights reserved

Answer:$2,400 Collections from Jan. sales ($4,000 x 10%) $400Collections from Feb. sales ($2,000 x 70%) 1,400Collections from Mar. sales ($6,000 x 10%) 600 Total $2,400

Copyright © 2007 Prentice-Hall. All rights reserved

In which responsibility center is the manager responsible for the center’s expenses?

1. Cost center

2. Revenue center

3. Profit center

4. Investment center

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: 1

Copyright © 2007 Prentice-Hall. All rights reserved

The practice of directed executive attention to important deviations from budgeted amounts is called management by:

1. Objectives

2. Exception

3. Intimidation

4. Data analysis

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: 2

Copyright © 2007 Prentice-Hall. All rights reserved

Famous Co. compiled the following information at the end of the period:

Budgeted ActualSales $10,000 $8,000

Cost of goods sold 6,000 4,400Operating expenses 2,000 1,500

What amount of variance does the performance report for the period show? [Indicate whether the variance is positive/(negative)]

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: +$100

Budgeted net income $2,000Actual net income 2,100Positive variance $100

Copyright © 2007 Prentice-Hall. All rights reserved

Responsibility accounting reports at various levels are used to

1. Make managers at all levels accountable

2. Identify coordination weaknesses

3. Decide which manager gets fired at the end of each period.

4. Inform the public about the company’s ability to manage resources.

Copyright © 2007 Prentice-Hall. All rights reserved

Answer: 1

Copyright © 2007 Prentice-Hall. All rights reserved

Related Documents