opyright © 2007 Pearson Addison-Wesley. All rights reserved. Chapter 21 Multinational Tax Management

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. Chapter 21 Multinational Tax Management.

Apr 01, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

Chapter 21

Multinational Tax Management

PCL Questions

• What are the tax aspects need to be considered by MNE?

• What are types of taxes that are faced by the MNE?

• How can an MNE can manage their taxes?

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.1-2

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-3

Multinational Tax Management

• Tax planning for multinational operations is an extremely complex but vitally important aspect of international business.

• To plan effectively, MNEs must understand not only the intricacies of their own operations worldwide, but also the different structures and interpretations of tax liabilities across countries.

• The primary objective of multinational tax planning is the minimization of the firm’s worldwide tax burden.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-4

Multinational Tax Management

• Taxes have a major impact on corporate net income and cash flow through their influence on foreign investment decisions, financial structure, determination of the cost of capital, foreign exchange management, working capital management, and financial control.

• Management must not pursue the objective of minimizing the firm’s worldwide tax burden without full recognition that decision making within the firm must always be based on the economic fundamentals of the firm’s line of business.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-5

Tax Principles

• Tax morality:

– In many countries taxpayers, corporate or individual, do not voluntarily comply with the tax laws

– The MNE must decide whether to follow a practice of full disclosure to tax authorities or adopt the philosophy “When in Rome, do as the Romans do”

– Most MNEs follow the full disclosure practice

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-6

Tax Principles

• Tax neutrality:– When a government decides to levy a tax, it must

consider not only the potential revenue from the tax, or how effectively it can be collected, but also the effect the proposed tax can have on private economic behavior

– For example, the US government’s policy on taxation of foreign-source income has multiple objectives:

• Neutralizing tax incentives that favor or disfavor US private investment in developed countries

• Providing an incentive for US private investment in developing countries

• Improving the US BOP

• Raising revenue

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-7

Tax Principles

• One way to view neutrality is to require that the burden of taxation on each dollar, euro, pound, or yen of profit earned in home country operations by a MNE be equal to the burden of taxation on each currency equivalent of profit earned by the same firm in its foreign operations (domestic neutrality).

• A second way to view neutrality is to require that the tax burden on each foreign subsidiary of the firm be equal to the tax burden on its competitors in the am country (foreign neutrality).

• In theory, an equitable tax is one that imposes the same total tax burden on all taxpayers who are similarly situated and located in the same tax jurisdiction.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-8

Tax Principles

• Despite the fundamental objectives of national tax authorities, it is widely agreed that taxes do affect economic decisions made by MNEs.

• Tax treaties between nations and differential tax structures, rates, and practices all result in a less than level playing field for the MNEs competing on world markets.

• Nations typically structure their tax systems along one of two basic approaches:– The worldwide approach

– The territorial approach

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-9

Tax Principles

• The worldwide approach, also referred to as the residential or national approach, levies taxes on the income earned by firms that are incorporated in the host country, regardless of where the income was earned (domestically or abroad).

• A MNE earning income both at home and abroad would therefore find its worldwide income taxed by its home country tax authorities.– For example, a country like the US taxes the income earned by firms based in

the US regardless of whether the income earned by the firm is domestic or foreign in origin.

• The territorial approach, also termed the source approach, focuses on the income earned by the firms within the legal jurisdiction of the host country, not on the country of firm incorporation.

– Countries like Germany follow this approach and apply taxes equally to foreign or domestic firms on income earned within the country, but in principle not on income earned outside the country

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-10

Tax Principles

• The territorial approach, like the worldwide approach, results in a major gap in coverage if resident firms earn income outside the country but are not taxed by the country in which the profits are earned.

• If the worldwide approach to international taxation is followed to the letter, it would end the tax-deferral privilege for many MNEs.

• Foreign subsidiaries of MNEs pay host country corporate income taxes, but many parent countries defer claiming additional income taxes on that foreign source income until it is remitted to the parent firm.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-11

Tax Principles

• A network of bilateral tax treaties, many of which are modeled after one proposed by the Organization for Economic Cooperation and Development (OECD), provides a means of reducing double taxation.

• Tax treaties normally define whether taxes are to be imposed on income earned in one country by the nationals of another, and if so, how.

• Tax treaties are bilateral, with the two signatories specifying what rates are applicable to which types of income between themselves alone.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-12

Tax Principles

• Taxes are classified on the basis of whether they are applied directly to income, called direct taxes, or to some other measurable performance characteristic of the firm, called indirect taxes.

• Some categories include:– Income tax

– Withholding tax

– Value-added tax

– Other national taxes

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-13

Tax Principles

• To prevent double taxation on the same income, most countries grant a foreign tax credit for income taxes paid to the host country.

• A tax credit is a direct reduction of taxes that would otherwise be due and payable.

• If there were no credits for foreign taxes paid, sequential taxation by the host government and then by the home government would result in a very high cumulative tax rate.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-14

Transfer Pricing

• The pricing of goods, services, and technology transferred to a foreign subsidiary from an affiliated company, called transfer pricing, is the first and foremost method of transferring funds out of a foreign subsidiary.

• These costs enter directly into the cost-of-goods-sold component of the subsidiary’s income statement.

• This problem is particularly sensitive for MNEs.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-15

Transfer Pricing

• Fund Positioning Effect

– A parent company wishing to transfer funds out of a particular country can charge higher prices on goods sold to its subsidiary in that country, to the degree that government regulations allow.

– A foreign subsidiary can be financed by the reverse technique, a lowering of transfer prices.

– A major consideration in setting a transfer price is the income tax effect.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-16

Transfer Pricing

• Methods of Determining Transfer Prices

– IRS regulations provide three methods to establish arm’s length prices:

• Comparable uncontrolled prices

• Resale prices

• Cost-plus calculations

– In some cases, combinations of these three methods are used.

• Other Considerations for Transfer Pricing

– Managerial incentives and evaluation

– Effect on joint-venture partners

– Flexibility of host governments to transfer pricing strategies utilized

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-17

US Taxation of Foreign Source Income

• The amount of foreign tax allowed as a credit depends on five tax parameters:– Foreign corporate income tax rate

– Domestic corporate income tax rate

– Foreign corporate dividend withholding tax rate for nonresidents (per the applicable bilateral tax treaty)

– Proportion of ownership held by the domestic corporation in the foreign firm

– Proportion of net income distributed (payout rate)

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-18

US Taxation of Foreign Source Income

• For example, if a US based MNE receives income from a foreign country that imposes higher corporate income taxes than the US (or combined income and withholding tax), total creditable taxes will exceed US taxes on that foreign income.

• The result is excess foreign tax credits.

• The proper management of global taxes is not simple, and combines three different components:– Foreign tax credit limitations

– Tax credit carry-forward/carry-back

– Foreign tax averaging

• See Exhibit 21.6

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-19

US Taxation of Foreign Source Income

• A MNE normally has a choice whether to organize a foreign subsidiary as a branch of the parent or as a local corporation.

• Both tax and nontax consequences must be considered.

• Nontax factors include the locus of legal liability, public image in the host country, managerial incentive considerations, and local legal and political requirements.

• A major tax consideration is whether the foreign subsidiary is expected to run at a loss for several years after start-up.

• A second tax consideration is the net tax burden after paying withholding taxes on dividends.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-20

US Taxation of Foreign Source Income

• Over the years, the US has introduced into US tax laws special incentives dealing with international operations.

• To benefit from these incentives, a firm may have to form separate corporations for qualifying and nonqualifying activities.

• The most important US special corporation is a foreign sales corporation (FSC).

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-21

US Taxation of Foreign Source Income

• Over the years, the US has introduced into US tax laws special incentives dealing with international operations.

• To benefit from these incentives, a firm may have to form separate corporations for qualifying and nonqualifying activities.

• The most important US special corporation is a foreign sales corporation (FSC).

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-22

US Taxation of Foreign Source Income

• A business carried on to a substantial extent in a U.S. possession can be carried on by a separate U.S. corporation, which, if it meets the requirements for a possessions corporation, is not subject to U.S. tax on income earned outside the United States unless the income is received in the United States.

• To qualify as a possessions corporation, a corporation must but a domestic U.S. corporation, have at least 80% of its gross income derived from within a U.S. possession and at least 75% of its gross income derived from the active conduct of a trade or business in a U.S. possession.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-23

US Taxation of Foreign Source Income

• The primary tax issues facing a US-based MNE are:– Domestic-source income and foreign-source income

are separated

– Foreign-source income is separated into active and passive categories

– If the remittance of active income from one subsidiary results in an excess foreign tax credit, and the remittance from a second subsidiary results in a foreign tax deficit, the credit may be applied to the deficit if the incomes are of the same “basket” under US tax law

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-24

Exhibit 21.7

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-25

Exhibit 21.8

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-26

Tax-Haven Subsidiaries and International Offshore Financial Centers

• Many MNEs have foreign subsidiaries that act as tax havens for corporate funds awaiting reinvestment or repatriation.

• Tax-haven subsidiaries, categorically referred to as international offshore financial centers, are partially a result of tax-deferral features on earned foreign income allowed by some of the parent countries.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-27

Tax-Haven Subsidiaries and International Offshore Financial Centers• Tax-haven subsidiaries are typically established in a

country that can meet the following requirements:– A low tax on foreign investment or sales income earned by

resident corporations and a low dividend withholding tax on dividends paid to the parent firm

– A stable currency to permit easy conversion of funds into and out of the local currency

– The facilities to support financial services activity

– A stable government that encourages the establishment of foreign-owned financial and service facilities within its borders

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-28

Exhibit 21.9 International Offshore Financial Centers

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

Chapter 22

Working Capital Management

• What does working capital mean for an MNE?

• Why does working capital need to be managed?

• How can an MNE run its working capital management?

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-30

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-31

Working Capital Management in the MNE

• Working capital management in a multinational enterprise requires managing current assets (cash balances, accounts receivable, and inventory) and current liabilities (accounts payable and short-term debt) when faced with political, foreign exchange, tax, and liquidity constraints.

• The overall goal is to reduce funds tied up in working capital while simultaneously providing sufficient funding and liquidity for the conduct of global business.

• Working capital management should enhance return on assets and return on equity and should also improve efficiency ratios and other performance measures.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-32

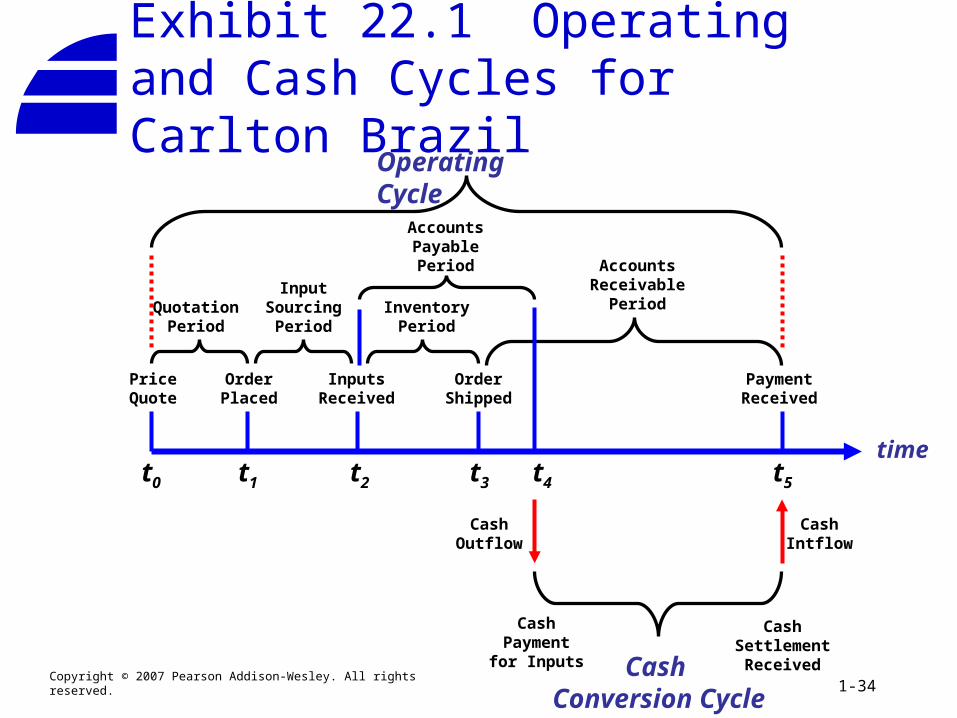

Working Capital Management

• The operating cycle of a business generates funding needs, cash inflows and outflows (the cash conversion cycle) and foreign exchange rate and credit risks.

• The funding needs generated by the operating cycle of the firm constitute working capital.

• The cash conversion cycle, a subcomponent of the operating cycle (working capital cycle), is that period of time extending between cash outflow for purchased inputs and materials and cash inflow from cash settlement.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-33

Working Capital Management

• The operating and cash conversion cycles for Carlton Brazil is illustrated in the following exhibit.

• This is decomposed into five different periods (each with business, accounting, and potential cash flow implications):– Quotation period

– Input sourcing period

– Inventory period

– Accounts payable period

– Accounts receivable period

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-34

time

Operating Cycle

Cash Conversion Cycle

PriceQuote

OrderPlaced

OrderShipped

PaymentReceived

InputsReceived

AccountsReceivable

PeriodQuotationPeriod

InputSourcing

Period

AccountsPayablePeriod

t0 t1 t2 t3 t4 t5

InventoryPeriod

CashPayment

for Inputs

CashSettlementReceived

CashOutflow

CashIntflow

Exhibit 22.1 Operating and Cash Cycles for Carlton Brazil

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-35

Working Capital Management

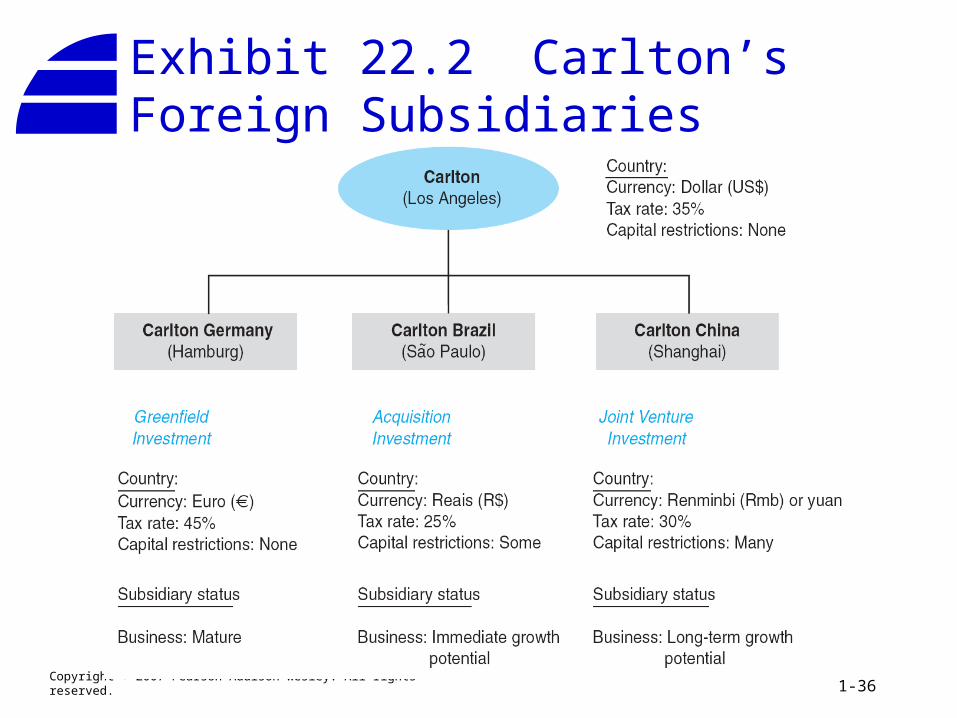

• Carlton’s three foreign subsidiaries each present a unique set of concerns.

• In practice, Carlton’s senior management in the parent company (corporate) will first determine its strategic objectives regarding the business developments in each subsidiary, and then design a financial management plan for the repositioning of profits, cash flows, and capital for each subsidiary.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-36

Exhibit 22.2 Carlton’s Foreign Subsidiaries

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-37

Restraints on Repositioning Funds

• Fund flows between units of a domestic business are generally unimpeded, but that is not the case in a multinational business.

• A firm operating globally faces a variety of political, tax, foreign exchange, and liquidity considerations that limit its ability to move funds easily and without cost from one country or currency to another.

• These constraints are the reason that multinational financial managers must plan ahead for repositioning funds within an MNE.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-38

Constraints on Repositioning Funds• Political constraints can block the transfer of

funds either overtly or covertly.

• Tax constraints arise because of the complex and possibly contradictory tax structures of various national governments through whose jurisdictions funds might pass.

• Foreign exchange transaction costs are incurred when one currency is exchanged for another.

• Liquidity needs are often driven by individual locations (difficult to conduct worldwide cash handling).

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-39

Conduits for Moving Funds by Unbundling Them• Multinational firms often unbundle their transfer

of funds into separate flows for specific purposes.

• Host countries are then more likely to perceive that a portion of what might otherwise be called remittance of profits constitutes and essential purchase of specific benefits that command worldwide values and benefit the host country.

• Unbundling allows a multinational firm to recover funds from subsidiaries without piquing host country sensitivities over large dividend drains.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-40

Exhibit 22.3 Potential Conduits for Moving Funds from Subsidiary to Parent

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-41

International Dividend Remittances

• Payment of dividends is the classic method by which firms transfer profit back to owners, be those owners individual shareholders or parent corporations.

• International dividend policy now incorporates tax considerations, political risk, and foreign exchange risk, as well as a return for business guidance and technology.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-42

Working Capital Management

• If Carlton Brazil’s business continues to expand, it will continually add to inventories and accounts payable (A/P) in order to fill increased sales in the form of accounts receivable (A/R).

• These components make up net working capital (NWC):

NWC = (A/R + inventory) – (A/P)

1-43

Net Working Capital (NWC) is the net investment required of the firmto support on-going sales. NWC components typically grow as the

firm buys inputs, produces product, and sells finished goods.

Assets Liabilities & Net Worth

Cash

Accounts receivable (A/R)

Inventory

Current assets

Accounts payable (A/P)

Short-term debt

Current liabilities

NWC = ( A/R + Inventory ) - A/P

Note that NWC is not the same as Current assets & Current liabilities.

Carlton Brazil’s Balance Sheet

Exhibit 22.4 Carlton Brazil’s Net Working Capital Requirements

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-44

Working Capital Management

• The previous exhibit illustrates one of the key managerial decisions for any subsidiary:

– Should A/P be paid off early, taking discounts offered by suppliers?

– The alternate form of financing for NWC balances is short-term debt

• In our example, Cascade Mexico’s CFO must decide which is the lower cost (short-term Mexican peso borrowings or the effective annual interest cost of supplier financing – cost of carry).

• Clearly, there are issues such as access to local currency debt, or various intra-company financing alternatives that complicate the decision.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-45

Working Capital Management

• A common method of benchmarking financial management practice is to calculate the NWC of the firm on a “days sales” basis.

• An analysis of this metric in a global context shows that US firms have a typical days sales of 29, while the European group has a days sales of 75.

• Clearly, European-based (technology firms in this example) are carrying a significantly higher level of net working capital in their financial structures.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-46

Working Capital Management

• The MNE itself poses some unique challenges in the management of working capital.

• Many multinationals manufacture goods in a few specific countries and then ship the intermediate products to other facilities globally for completion and distribution.

• The payables, receivables, and inventory levels of the various units are a combination of intra-firm and inter-firm.

• The varying business practices observed globally regarding payment terms – both days and discounts – create severe mismatches in some cases.

1-47

A/PA/RInventory

Carlton USABalance Sheet

A/PA/RInventory

Carlton BrazilBalance Sheet

A/P

Local-sourcing: 60 days

Intra-firm:30 days 30 days60 days

Cash inflows to Carlton Brazil arise from local market sales.These cash flows are used to repay both intra-firm payables

(to Carlton USA) and local suppliers.

Brazilian Business PracticesPayment terms in Brazil are longer than those typical of the United States. Carlton Brazil must offer 60-day terms to local customers to be competitive with other firms in the local market.

United States Business PracticesPayment terms used by Carlton USA are typical of the United States, 30 days. Carlton USA’s local customers will expect to be paid in 30 days. Carlton USA may consider extending longer terms to Brazil to reduce the squeeze.

Result: Carlton Brazil is squeezed in terms of cash flow. It receives inflows in 60 days but must pay Carlton USA in 30 days.

Exhibit 22.6 Carlton’s Multinational Working Capital Sequence

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-48

Working Capital Management

• A firm’s operating cash inflow is derived primarily from the collection of accounts receivable.

• Multinational accounts receivable are created by two separate types of transactions:

– Sales to related subsidiaries

– Sales to independent or unrelated buyers

• Management of accounts receivable form independent customers requires two types of decisions:

– What currency should the transaction be denominated?

– What should be the terms of payment?

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-49

Working Capital Management

• Operations in inflationary, devaluation-prone economies sometimes force management to modify its normal approach to inventory management.

• In some cases, management may choose to maintain inventory and reorder levels far in excess of what would be called for in an economic order-quantity model.

• It is important to anticipate:

– Devaluation

– Price freezes

– The implications of various forms of free-trade zones

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-50

Working Capital Management

• A free-trade zone combines the old idea of duty-free ports with legislation that reduces or eliminates customs duties to retailers or manufacturers who structure their operations to benefit from the technique.

• Income taxes may also be reduced for operations in a free-trade zone.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-51

International Cash Management

• International cash management is the set of activities determining the levels of cash balances held throughout the MNE (cash management) and the facilitation of its movement cross-border (settlements and processing).

• These activities are typically handled by the international treasury of the MNE.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-52

International Cash Management

• The level of cash maintained by an individual subsidiary is determined independent of the working capital management decisions we have discussed.

• Cash balances, including marketable securities, are held partly to enable normal day-to-day cash disbursements and partly to protect against unanticipated variations from budgeted cash flows.

• These two motives are called the transaction motive and the precautionary motive.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-53

International Cash Management

• Cash disbursed for operations is replenished from two sources:– Internal working capital turnover

– External sourcing, traditionally short-term borrowing

• Efficient cash management aims to reduce cash tied up unnecessarily in the system, without diminishing profit or increasing risk, so as to increase the rate of return on invested assets.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-54

International Cash Management

• Multinational business increases the complexity of making payments and settling cash flows between related and unrelated firms.

• Over time a number of techniques and services have evolved that simplify and reduce the costs of making these cross-border payments.

• Four such techniques include:– Wire transfers

– Cash pooling

– Payment netting

– Electronic fund transfers

1-55

Carlton USA

Carlton Brazil Carlton China

Carlton Germany

$5,000

$4,000

$4,000

$3,000

$2,000

$1,000

$5,000

$3,000

$3,000

$2,000

$6,000

$5,000

Prior to netting, the four sister affiliates of Carlton companies have numerousintra-firm payments between them. Each payment results in transfer charges.

Exhibit 22.8 Multilateral Matrix Before Netting (thousands of US dollars)

1-56

Carlton USA

Carlton Brazil Carlton China

Carlton Germany

After netting, the four sister Carlton companies have only threenet payments to make among themselves to settle all intra-firm obligations

Pays $1,000Pays $3,000Pays $1,000

Exhibit 22.9 Multilateral Matrix After Netting (thousands of US dollars)

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-57

Financing Working Capital

• All firms need to finance working capital.

• The normal sources of funds for financing short-term working capital are accounts payable to suppliers and loans against bank credit lines.

• In some countries, such as the United States, borrowing is done by the firm issuing notes payable to banks and other creditors.

• In many other countries, short term borrowing is done on an “overdraft” basis.

• In all cases, permanent working capital requirements, as opposed to seasonal needs, are at least partially financed with long-term debt and equity.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-58

Financing Working Capital

• Some MNEs have found that their financial resources and needs are either too large or too sophisticated for the financial services available in may locations where they operate.

• One solution to this has been the establishment of an in-house or internal bank within the firm.

• Such an in-house bank is not a separate corporation; rather, it is a set of functions performed by the existing treasury department.

• The following exhibit, illustrates how the in-house bank of Cascade Pharmaceuticals, Inc., could work.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-59

Financing Working Capital

• Carlton Brazil sells all its receivables to the in-house bank as they arise, reducing some of the domestic working capital needs.

• Additional working capital needs are supplied by the in-house bank directly to Carlton Brazil.

• Because the in-house bank is part of the same company, the interest rates it charges may be significantly lower than what Carlton Brazil could obtain on its own.

• In addition to providing financing benefits, in-house banks allow for more effective currency risk management.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved. 1-60

Financing Working Capital

• MNEs depend on their commercial banks to handle most of the trade financing needs, such as letters of credit, and to provide advice on government support, country risk assessment, introductions to foreign firms and banks, and general financing availability.

• The main points of bank contacts are correspondent banks, representative offices, branch banks, subsidiaries, and affiliates.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

The End

Related Documents