Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved. 16-1 CHAPTER 16 Changes in the Macroeconomy and Changes in Macroeconomic Policy

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved. 16-1 CHAPTER 16 Changes in the Macroeconomy and Changes in Macroeconomic Policy.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-1

CHAPTER 16

Changes in the Macroeconomy and Changes in Macroeconomic Policy

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-2

Questions• How has the structure of the economy

changed over the course of the past century?

• How has the business cycle changed over the last century?

• How has economic policy changed over the past century?

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-3

Questions• What are future prospects for

successful management of the business cycle?

• Why does unemployment in Europe remain so high?

• Why does growth in Japan remain so low?

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-4

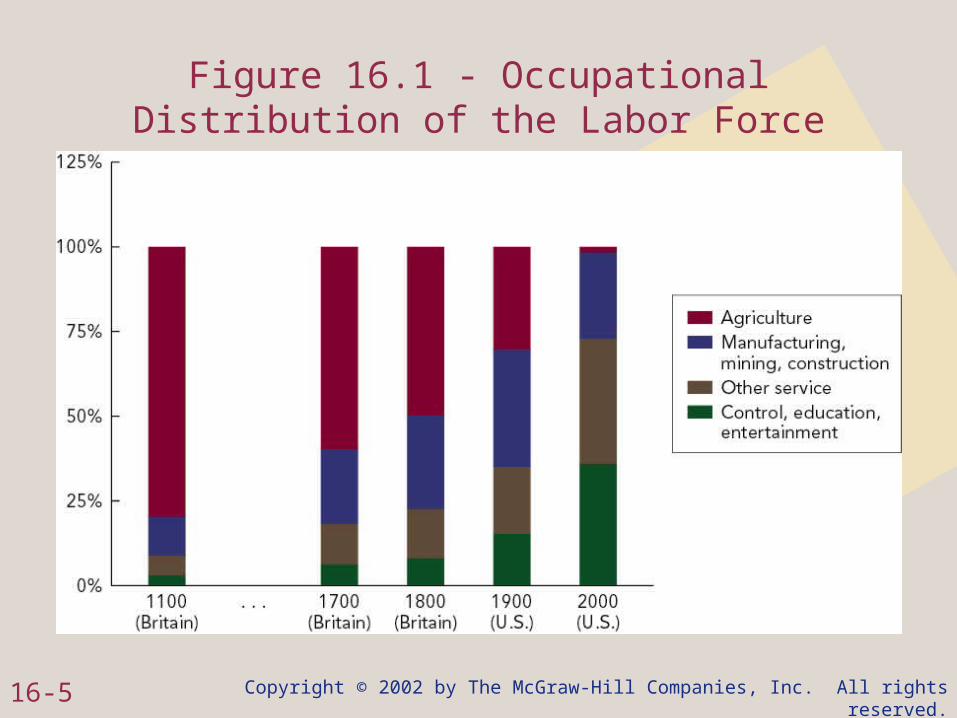

Changes in the Macroeconomy• Over the past century, the structure of

modern industrial economies has changed– significant decline in the share of the

labor force engaged in agriculture– decline in the proportion of the labor

force involved in mining, manufacturing, and construction

– rise in service-sector employment

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-5

Figure 16.1 - Occupational Distribution of the Labor Force

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-6

Changes in the Macroeconomy– growth of the government’s social

insurance programs and progressive tax system• automatic stabilizers

– broader financial system• allows households to smooth consumption

spending• lowers the marginal propensity to consume and

the multiplier

– the creation of the deposit insurance system• reduces the number of financial panics

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-7

Changes in the Macroeconomy– improvements in labor productivity are

now the result of improvements in the efficiency of labor (rather than capital deepening)• innovations in materials production, materials

handling, and organization

– research and development is now a key component of investment

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-8

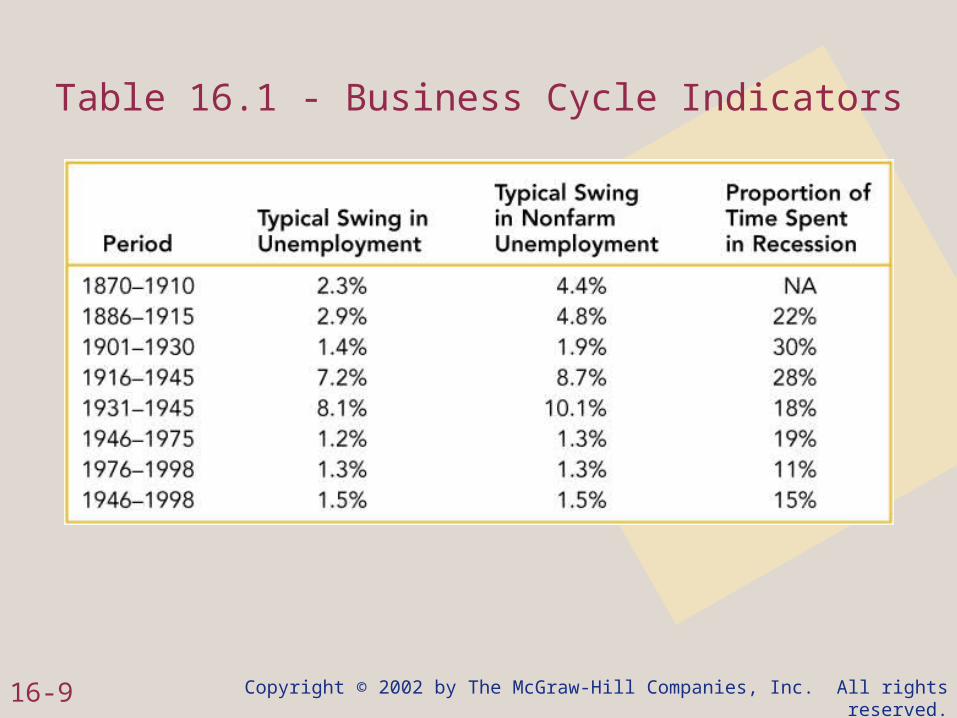

Changes in the Macroeconomy• Even with these changes, the U.S.

economy’s business cycle has continued– there are some signs that fluctuations in

unemployment have become smaller in recent years

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-9

Table 16.1 - Business Cycle Indicators

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-10

Future Changes• Consumption

– liquidity constraints will continue to decline• the marginal propensity to consume and the

multiplier will grow even smaller over time

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-11

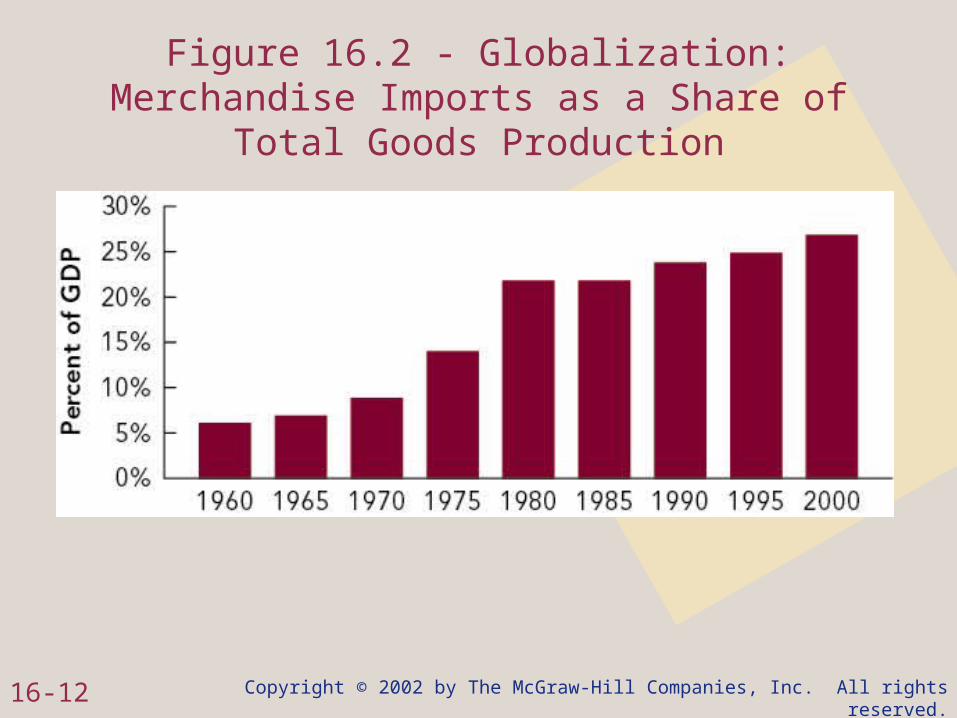

Future Changes• Globalization

– international trade will continue to expand• increased trade will further lower the multiplier• the domestic economy will be less vulnerable to

domestic shocks but more vulnerable to foreign shocks

– there will also be an increase in the magnitude of international financial flows• potential source of financial crisis and

macroeconomic volatility

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-12

Figure 16.2 - Globalization: Merchandise Imports as a Share of Total Goods Production

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-13

Future Changes• Monetary Policy

– the increase in financial flexibility will make it somewhat more difficult to conduct monetary policy

– as more and more different kinds of financial assets are traded, the supply of Treasury bills will have less of an effect on interest rates

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-14

Future Changes• Inventories

– improvements in information technology will improve businesses’ ability to control their inventories• mismatches between production and demand

have been a principal source of fluctuations in employment and output throughout history

• better information technology will reduce this component of macroeconomic instability

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-15

Estimating Long-Run Changes in Cyclical Volatility• To assess changes in the size of the

overall business cycle, we can compare the cyclical behavior of real GDP and unemployment over the century– good quality data exists only for the post-

World War II period– a consistent division of the past century

into recessions and expansions shows little difference in the size of recession

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-16

Figure 16.3 - The Great Depression Relative to Other Business Cycles: U.S. Unemployment

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-17

Estimating Long-Run Changes in Cyclical Volatility• Two conclusions can be drawn about

the changing cyclical variability of the American economy– the business cycle during the interwar

period was extraordinarily large• there were three major contractions during this

period including the Great Depression– the post-World War II business cycle,

measured relative to the size of the economy, has been a little smaller than back before World War I

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-18

Figure 16.4 - Real GDP Relative to Potential Output during the Great Depression

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-19

How Economic Policy Has Worked

• The fall in the multiplier, the creation of automatic stabilizers, and the increasing power of central banks have allowed monetary policy to offset many of the kinds of shocks that generated pre-Depression business cycles– the post-World War II economy has had

fewer small recessions caused by shocks to the IS and LM curves

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-20

How Economic Policy Has Not Worked

• Economic policy has caused recessions as well– the Federal Reserve has engineered a

recession (or has accepted the risk of a recession) in order to curb inflation at least four times since World War II

– the post-World War II boom-and-bust business cycle has been driven by policies that have allowed rises in inflation, followed by policies to fight it

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-21

How Economic Policy Has Not Worked

• Why have policy makers found themselves repeatedly driven to risk recession in order to fight inflation?– in the late 1940s, the Federal Reserve kept

interest rates low to reduce the cost of the national debt

– in the 1960s and 1970s, inflation was allowed to accelerate for a number of possible reasons• memory of the Great Depression• mistaken economic theories• political business cycle considerations

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-22

The Great Depression• The speed and magnitude of the

economy’s collapse during the first stages of the Great Depression was unprecedented– from 1929 to 1933, real GDP fell by almost

40 percent– by 1932, real investment spending was

less than one-ninth of what it had been in 1929

– by 1933, unemployment had reached 25 percent

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-23

Figure 16.5 - Movement along the IS Curve: The Great Contraction, 1929-1932

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-24

The Great Depression• Investment and real GDP fell so

quickly because of an extraordinary rise in real interest rates– real interest rates increased from 4 to

nearly 13 percent from 1929 to 1931– after 1932, investment spending

remained low even though real interest rates returned to more normal values• businesses put off expanding their capacity

• baseline investment (I0) fell

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-25

The Great Depression

• The cause of high real interest rates was rapid deflation– falling production, employment, and

demand led to steep declines in prices

• But there must have been an initial shock to cause the start of the downward spiral that was the Great Depression

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-26

Figure 16.6 - Real and NominalInterest Rates and the Inflation Rate

in the Great Depression

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-27

The Great Depression• Economists have proposed many

candidates for the shock that triggered the Great Depression– the stock market crash of 1929– the availability of consumer credit in the

1920s that led to a boom in consumption spending and then came to a natural end

– recognition of excessive residential investment that led to a decline in baseline investment

– an increase in interest rates in 1928

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-28

The Great Depression• Economists have reached a consensus

that sufficiently aggressive monetary policy could have stemmed the deflation and thus ended the Great Depression much earlier– massive federal deficits funded by printing

money coupled with aggressive open market purchases could have produced inflation• real interest rates would not have risen and

investment spending would have been less affected

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-29

The Great Depression• In addition to reducing real GDP

through higher real interest rates, deflation also redistributes wealth from debtors to creditors– businesses that are heavily in debt find

that they cannot pay and go bankrupt– financial institutions that have loaned to

these business find that their loans are worthless and go bankrupt as well• more than one-third of U.S. banks failed

during the first years of the Great Depression

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-30

Stabilization• If we divide the post-World War II era

into two periods with the breakpoint chosen at the end of the Volcker disinflation in the early 1980s, the pre-1984 years show much more business cycle volatility than do the post-1984 years– there have not been many shocks or any

truly large shocks to the economy– maybe lessons have truly been learned

from the 1960s and 1970s

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-31

High European Unemployment

• Unemployment rates in western Europe at the end of the 1990s are close to those achieved in the U.S. during the Great Depression– until the end of the 1970s, the

unemployment rate in western Europe had been lower than that in the U.S.

– after the 1970s, western European unemployment rose during recessions, but did not fall during expansions

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-32

Figure 16.7 - European Unemployment

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-33

High European Unemployment

• In the U.S., it is possible to explain the comovements of unemployment and inflation from 1960 to 2000 using the standard Phillips curve– movements in the expected rate of

inflation reflect changes in the economic policy environment

– movements in the natural rate of unemployment are relatively small and can be linked to plausible factors

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-34

High European Unemployment

• In western Europe, the accelerationist Phillips curve never fit the historical experience very well– each policy episode from 1970 on

seemed to shift the Phillips curve further out and to further raise the natural rate of unemployment

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-35

High European Unemployment

• The dominant view expressed in Europe in the early 1990s was that high European unemployment was the result of labor market rigidities– this would mean that high unemployment

is an equilibrium, because it is not caused by a deficiency of aggregate demand

• But the rigidities in the European labor market were stronger in the 1960s – the unemployment rate was lower

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-36

High European Unemployment

• Many economists see the western European situation as reversible– have central bankers and governments

shift to a more expansionary monetary policy• as demand rises, people will find the natural

rate of unemployment is falling• the decline in the natural rate will create

further increases in demand and further declines in the natural rate

– begin reducing and eliminating labor-market rigidities

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-37

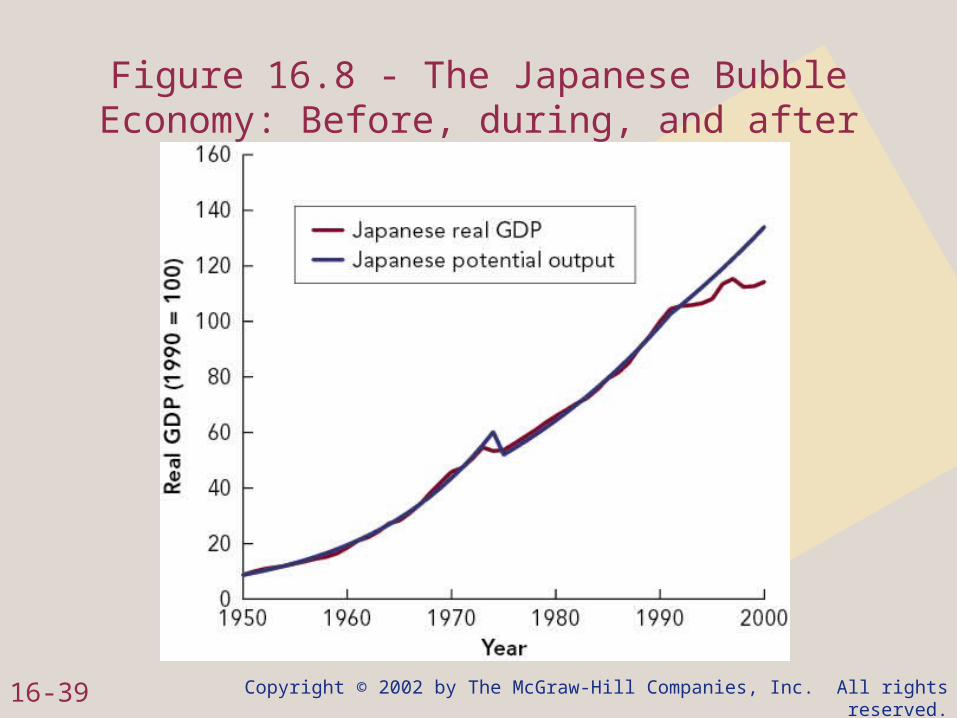

Japanese Stagnation• The Japanese stock market and real

estate market rose far and fast in the 1980s

• Eventually, the market turned and both the real estate and stock markets collapsed– many businesses and banks were

bankrupted– no one was willing to lend money

• investment spending was depressed

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-38

Japanese Stagnation• The Japanese economy has fallen into

a decade of economic stagnation– growth has been almost zero– unemployment has risen to high levels– the IS curve has shifted far left– even extremely low nominal interest

rates have not been enough to boost investment and aggregate demand

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-39

Figure 16.8 - The Japanese Bubble Economy: Before, during, and after

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-40

Japanese Stagnation• What should policy makers do?

– have the government run a substantial deficit

– have the central bank push the interest rate it charges close to zero

– deliberately try to engineer moderate inflation• makes the alternative to investment spending

more risky

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-41

Moral Hazard• In a financial crisis, the flow of funds

through financial markets will slow to a trickle and the IS curve will shift far and fast to the left– the government needs to close down and

liquidate those organizations that are fundamentally bankrupt

– the government needs to lend money to organizations that would be solvent if production and demand were at normal levels

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-42

Moral Hazard• Government support is necessary to

prevent a deep meltdown of the entire financial system

• But government assistance must be offered on terms unpleasant enough and expensive enough that no one wishes to get in a situation in which they need to draw on it– they need to prevent moral hazard

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-43

The Ultimate Lesson• In many ways, it seems to be very

hard to learn the lessons of history• The future of economic policy seems

likely to be similar to the past– gross mistakes will be made– historical analogies will be misapplied– economists and other observers will find

major policy mistakes made by governments and central banks to be inexcusable (after the fact)

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-44

Chapter Summary• The structure of the economy has

undergone mammoth changes over the past century, yet these changes appear to have had relatively little impact on the size of the business cycle

• Stabilization policy as we know it was impossible a hundred years ago– it is performed routinely and aggressively

since

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-45

Chapter Summary• Since World War II, stabilization policy

has had some successes and failures– its principal failure has been that it has

generated policy-induced recessions to fight inflation• these policy-reduced recessions have kept

policy from successfully stabilizing the economy to a greater degree

• In the past two decades, stabilization policy in the U.S. has been very successful

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-46

Chapter Summary• Certainly from the U.S. perspective

there is every reason to be optimistic about the future of macroeconomic policy and of the macroeconomy

• From a European perspective, there is less reason to be optimistic– European governments and central banks

have not learned how to deal with their high levels of unemployment

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-47

Chapter Summary• From a Japanese perspective, there is

less reason to be optimistic– the Japanese government has not learned

how to deal with its financial meltdown

Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.16-48

Chapter Summary• Even from a U.S. perspective, it seems

hard to learn the lesson that good economic policy during an economic crisis is not a matter of clinging to one principle, but of balancing off the conflicting requirements of several valid principles

Related Documents