The Convergence to IFRS – Reasons, Implications, Applicability, and Concerns

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Convergence to IFRS – Reasons, Implications,

Applicability, and Concerns

Northampton Business School/ Prince Oduro/14420066 Page 2

Table of Contents

1. Introduction .............................................................................................. 3

2. International Financial Reporting Standards (IFRS) ................................... 3

2.1. History of IAS/ IFRS ....................................................................................................................... 3

3.0 Convergence to IFRS – Reasons/Advantages .......................................... 4

3.1. Greater Comparability .................................................................................................................. 4

3.2 Cheaper Capital in Public Market .................................................................................................. 4

3.3. Reduction in Cost of Capital ......................................................................................................... 4

3.4. Reduced Complexity in Auditing .................................................................................................. 5

3.5. Attraction of Foreign Direct Investment ...................................................................................... 5

3.6. Greater Flexibility for Governments ............................................................................................ 5

3.7. Promotion of Regional Economic Grouping. ................................................................................ 5

3.7. Other Reasons. ............................................................................................................................. 5

4.0 Current Adoption Rate – IAS/IFRS ........................................................... 5

4.1. Analysis of Extent of Adoption: .................................................................................................... 6

5.0 Why Some Countries Refused Adoption – IAS/IFRS ................................ 8

5.1. Protection of indigenous firms. .................................................................................................... 8

5.2. Perpetuation of Dictatorship........................................................................................................ 9

5.3. The Cost of Adoption and implementation. ................................................................................ 9

6.0 IFRS – Applicability and Concerns ........................................................... 9

Non- Listed SMEs: ..................................................................................................................... 9

Sub-Set IFRS: ............................................................................................................................. 9

Mechanistic Accounting: .......................................................................................................... 9

7.0 Conclusion: ............................................................................................. 9

8.0 Reference List: ....................................................................................... 10

Northampton Business School/ Prince Oduro/14420066 Page 3

1. Introduction

Since the emergence of Accounting in 1494 by the help of Luca Pacioli, the subject matter has continually evolved

and has become a prominent subject in the sphere of world business activities. Today, not many businesses and

nations can do without accounting. A lot of structures such GAAP, SSAP, IAS and IFRS have evolved at various

stages to guide the practice of accounting.

This report seeks to look in details “The convergence to IFRS – Reasons, implications, applicability, and

concerns” by demonstrating the following:

Why was there a need for converting from GAAP to IFRS.

The difference between the IAS and IFRS.

Application rate of IFRS by countries in the world focusing of full, partial and no application of

IFRS by jurisdiction basis and thy reasons.

The advantages and challenges faced in IAS/IFRS application.

And whether IAS/IFRS can be applied in all contexts.

2. International Financial Reporting Standards (IFRS) International Financial Reporting Standards (IFRS) is a set of accounting standards developed by an

independent, not-for-profit organization called the International Accounting Standards Board (IASB) to regulate the

practice of accounting and corporate reporting.

2.1. History of IAS/ IFRS

The evolving of accounting and Corporate reporting led to the development of Generally accepted accounting

principles (GAAP) which refers to the standard framework of guidelines for financial accounting used in any given

jurisdiction; generally known as accounting standards or standard accounting practice.

The GAAP led to:

The promulgation of various national accounting legislations to regulate the accounting profession in their

respective countries due to cultural differences.

Accounting rules which were different in various countries though they followed a set of accounting

standards established by accounting regulators to govern and regulate the accounting profession. E.g. the

UK had SSAP/FRS, USA had US GAAP, Canadian GAAP and Ghana had GNAS. Etc.

Differences resulting in lack of uniformity in financial statements prepared in different countries and such

failed to meet enhancing qualities of financial statements.

Translations of companies’ financial statements into other countries GAAP has resulted in huge losses.

Working in different countries as accounting professional or auditor was overly difficult due different

legislations and standard one is required to master. Etc.

The International Accounting Standards Committee (IASC) was established in mid-1973 with mandated of

developing new international standards, which would be accepted and implemented globally. The IASC lasted 27

years until March 2001, where IASC foundation, not for Profit Corporation incorporated in the USA and the parent

Northampton Business School/ Prince Oduro/14420066 Page 4

entity of International Accounting Standards Board (IASB) was restructured to become IASB.

A series of accounting standards, known as the International Accounting Standards, were released by the IASC

between 1973 and 2000, and were sequentially numbered. The series started with IAS 1, and concluded with the IAS

41, in December 2000. In April 2001, when IASB become operational, they agreed to adopt the set of standards that

were issued by the IASC, i.e. the IAS 1 to 41, but that any standards to be published after that would follow a series

known as the International Financial Reporting Standards (IFRS). Currently, the IASB is based in London.

3.0 Convergence to IFRS – Reasons/Advantages The formal objectives of the IASB, formulated in its mission statement are:

To develop, in the public interest, a single set of high quality, understandable and enforceable worldwide

accounting standards that required transparent and comparable information in general purpose financial

statements.

To co-operate with national accounting standard setters to achieve convergence in accounting standards

around the world.

The reasons for the above set objectives of IAS/IFRS are discussed below:

3.1. Greater Comparability

Investors, both individuals and corporates, would like to be able to compare the financial results of different

companies internationally, nationally wise as well as industry wise in making investment decisions. The single set of

financial reporting standard which harmonizes global accounting enable investors irrespective of where they are

understand the financial results if different companies in the world and compare performance of such companies to

arrive at investment decisions.

3.2 Cheaper Capital in Public Market

Companies which are IFRS compliant can obtain huge and cheaper public finance both locally and

internationally by listing on various Stock exchanges in the world such as London Stock exchange, Ghana

stock Exchange, New York Stock Exchange (NYSE), Tokyo Stock Exchange, Shanghai Stock Exchange etc. They

as well attract foreign investors. This is because IFRS application ensures proper scrutiny of companies’

financial results through auditing. This ensures that integrity of those financial results are maintained and

that they faithfully represent what they supposed to represent while reposing investor confidence in

financial reporting.

3.3. Reduction in Cost of Capital

Companies that access funding in different countries needed to translate their financial statements in compliance with

the GAAP requirements of those countries. This adds to the cost of raising such funding. Global IFRS harmonization

will mean that such companies can present the same financial statements in all major markets in anywhere in the

world without any conversion which in effect reduces the cost of capital.

Northampton Business School/ Prince Oduro/14420066 Page 5

3.4. Reduced Complexity in Auditing

Under the GAAP, auditing multinational companies was pretty complex as the auditor would have to be

familiar with the respective accounting framework and regulations of the countries in which subsidiaries are

located. It increased the burden on external audits which also resulted in high audit fees. The Convergence in

IFRS simplifies accounting and auditing of multinational companies as same accounting standards are applied

by both the parent company and its subsidiaries.

3.5. Attraction of Foreign Direct Investment

Application of various domestic GAAP somehow restricted foreign direct investments in many countries especially

in the developing world. Helping foreign companies to list in your country makes your domestic market busier, thus

encourages more investment. This could be achieved much easier if the country is IFRS compliant.

3.6. Greater Flexibility for Governments

Governments of various countries would save time and money if they could adopt IFRS and, if these were used

internally, governments of especially developing countries could attempt to control the activities of foreign

multinational companies in their own countries. These companies could not ‘hide’ behind foreign accounting

practices which are difficult to understand.

3.7. Promotion of Regional Economic Grouping.

Regional economic groups usually promote trade within a specific geographical region. The effectiveness of such

groups largely depends structures in place which building blocks and includes accounting framework. The adoption

of a common accounting practice such as IFRS aids cohesive and solid regional grouping. Currently, regional

groupings such as EU, ECOWAS, and the so forth have adopted IFRS.

3.7. Other Reasons.

Other popular reasons for convergence to IFRS may include the following:

Wide source of fund to companies overseas while permitting smaller companies to access funding locally

and hopefully at cheaper cost.

A more straight forward appraisal of foreign entities for take-overs and mergers.

Enable transfer of accounting staff across national borders easier as same accounting standards are used

everywhere.

Preparation of group accounts would be easier due to application of same accounting standard.

Easy Computation of tax liability of investors, including multinational who receives income from overseas.

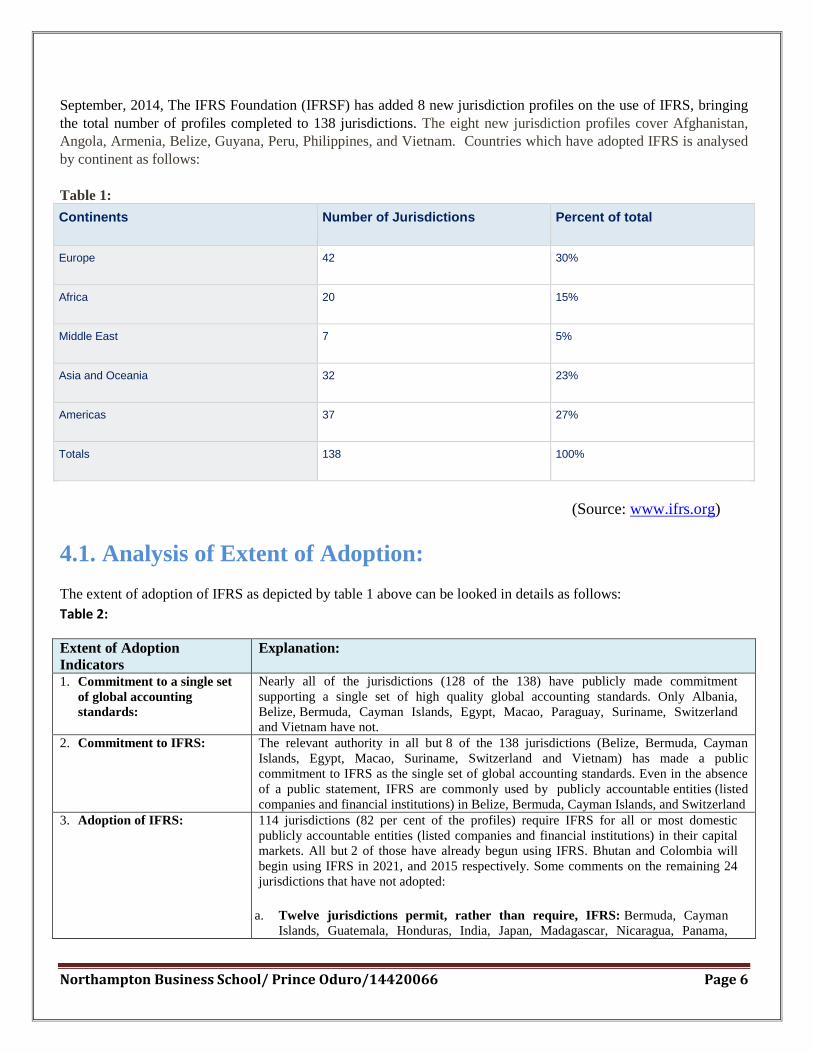

4.0 Current Adoption Rate – IAS/IFRS The IFRS Foundation has put mechanism in place to track the adoption of IFRS by various jurisdictions. A profile is

maintained for each country and various regional groups of the extent of adoption of IFRS by such regions. As at 25th

Northampton Business School/ Prince Oduro/14420066 Page 6

September, 2014, The IFRS Foundation (IFRSF) has added 8 new jurisdiction profiles on the use of IFRS, bringing

the total number of profiles completed to 138 jurisdictions. The eight new jurisdiction profiles cover Afghanistan,

Angola, Armenia, Belize, Guyana, Peru, Philippines, and Vietnam. Countries which have adopted IFRS is analysed

by continent as follows:

Table 1:

Continents Number of Jurisdictions Percent of total

Europe 42 30%

Africa 20 15%

Middle East 7 5%

Asia and Oceania 32 23%

Americas 37 27%

Totals 138 100%

(Source: www.ifrs.org)

4.1. Analysis of Extent of Adoption:

The extent of adoption of IFRS as depicted by table 1 above can be looked in details as follows:

Table 2:

Extent of Adoption

Indicators

Explanation:

1. Commitment to a single set

of global accounting

standards:

Nearly all of the jurisdictions (128 of the 138) have publicly made commitment

supporting a single set of high quality global accounting standards. Only Albania,

Belize, Bermuda, Cayman Islands, Egypt, Macao, Paraguay, Suriname, Switzerland

and Vietnam have not.

2. Commitment to IFRS: The relevant authority in all but 8 of the 138 jurisdictions (Belize, Bermuda, Cayman

Islands, Egypt, Macao, Suriname, Switzerland and Vietnam) has made a public

commitment to IFRS as the single set of global accounting standards. Even in the absence

of a public statement, IFRS are commonly used by publicly accountable entities (listed

companies and financial institutions) in Belize, Bermuda, Cayman Islands, and Switzerland

3. Adoption of IFRS: 114 jurisdictions (82 per cent of the profiles) require IFRS for all or most domestic

publicly accountable entities (listed companies and financial institutions) in their capital

markets. All but 2 of those have already begun using IFRS. Bhutan and Colombia will

begin using IFRS in 2021, and 2015 respectively. Some comments on the remaining 24

jurisdictions that have not adopted:

a. Twelve jurisdictions permit, rather than require, IFRS: Bermuda, Cayman

Islands, Guatemala, Honduras, India, Japan, Madagascar, Nicaragua, Panama,

Northampton Business School/ Prince Oduro/14420066 Page 7

Paraguay, Suriname, Switzerland;

b. Two jurisdictions require IFRS for financial institutions but not listed

companies: Saudi Arabia, Uzbekistan;

c. One jurisdiction is in process of adopting IFRS in full: Thailand;

d. One jurisdiction is in process of converging its national standards substantially

(but not entirely) with IFRS: Indonesia; and

e. Eight jurisdictions use national or regional standards: Bolivia, China, Egypt,

Guinea-Bissau, Macao, Niger, United States, and Vietnam.

4. Scope of use of IFRS: 5. The 114 jurisdictions that require IFRS for all or most domestic publicly accountable

entities include 7 that have no stock exchange but that require IFRS for all financial

institutions (Afghanistan, Angola, Belize, Brunei, Kosovo, Lesotho, Yemen). Of the

107 jurisdictions that do have stock exchanges, 6 do not require IFRS for listed

financial institutions (Argentina, El Salvador, Israel, Mexico, Peru, Uruguay) though

they do require IFRS for other listed companies. All of the others require IFRS for all

listed companies. Around 60 per cent of the 114 jurisdictions that require IFRS for all

or most domestic publicly traded companies also require IFRS for some domestic

companies whose securities are not publicly traded, generally financial institutions and

large unlisted companies. Over 90 per cent of the 114 jurisdictions that require IFRS for

all or most domestic publicly traded companies also require or permit IFRS for all or

most non-publicly traded companies.

6. Few modifications: 7. The 138 countries made very few changes to IFRS, which were generally regarded as

temporary steps in the jurisdiction’s plans to adopt IFRS. For example, the EU itself

describes its IAS 39 ‘carve-out’ as ‘temporary’, and the ‘carve-out’ has been applied by

fewer than two dozen banks out of the 8,000 IFRS companies whose securities trade on

a regulated market in Europe. Several modifications related to IASB agenda projects

that are now completed, including loan loss provisioning, use of the equity method to

account for subsidiaries in separate company financial statements, and bearer

agricultural assets. Jurisdictions have already begun eliminating those

modifications. Several other modifications relate to projects currently on

the IASB's agenda, including accounting for rate-regulated activities. A few

jurisdictions deferred the effective dates of some Standards, particularly IFRSs 10, 11

and 12 and IFRIC 15, though many of those deferrals have now ended.

(Source: www.ifrs.org)

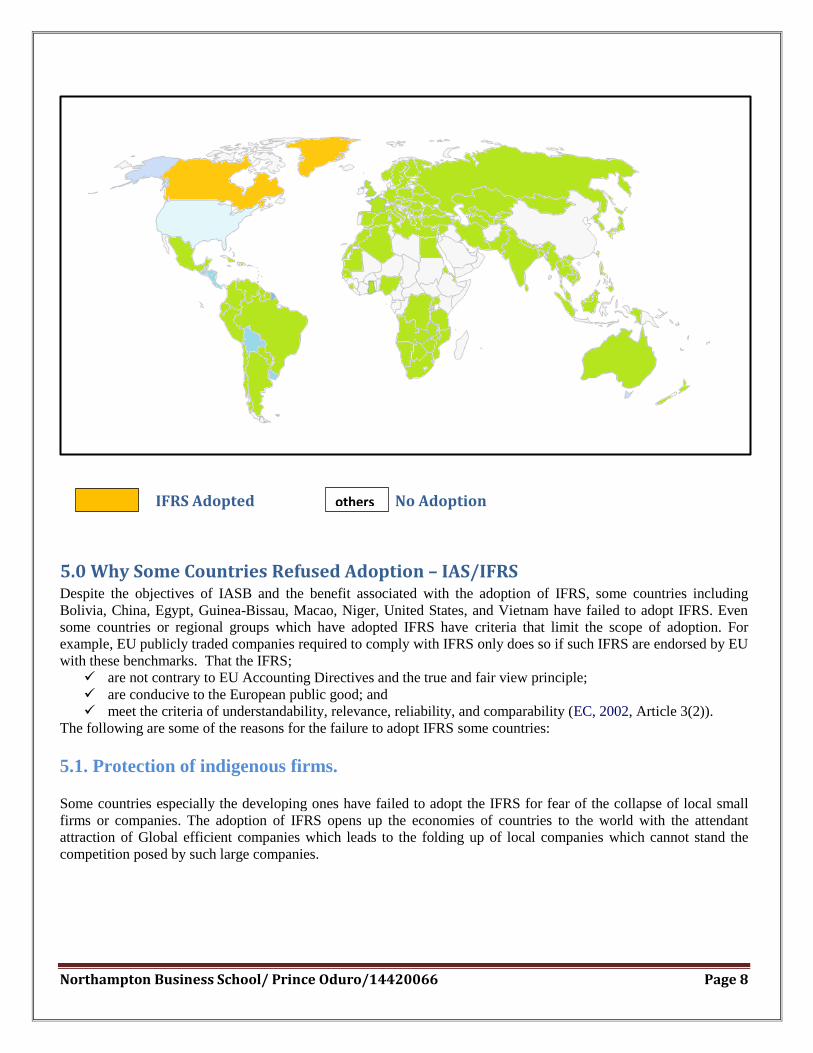

Overall, out of 196 countries in the world, 138 have adopted IFRS either fully or partial as their national accounting

standard. Over view of adoption is depicted by the map below:

Diagram – Map 1:

Geographical representation of IFRS Adoption:

Northampton Business School/ Prince Oduro/14420066 Page 8

IFRS Adopted No Adoption

5.0 Why Some Countries Refused Adoption – IAS/IFRS Despite the objectives of IASB and the benefit associated with the adoption of IFRS, some countries including

Bolivia, China, Egypt, Guinea-Bissau, Macao, Niger, United States, and Vietnam have failed to adopt IFRS. Even

some countries or regional groups which have adopted IFRS have criteria that limit the scope of adoption. For

example, EU publicly traded companies required to comply with IFRS only does so if such IFRS are endorsed by EU

with these benchmarks. That the IFRS;

are not contrary to EU Accounting Directives and the true and fair view principle;

are conducive to the European public good; and

meet the criteria of understandability, relevance, reliability, and comparability (EC, 2002, Article 3(2)).

The following are some of the reasons for the failure to adopt IFRS some countries:

5.1. Protection of indigenous firms.

Some countries especially the developing ones have failed to adopt the IFRS for fear of the collapse of local small

firms or companies. The adoption of IFRS opens up the economies of countries to the world with the attendant

attraction of Global efficient companies which leads to the folding up of local companies which cannot stand the

competition posed by such large companies.

others

Northampton Business School/ Prince Oduro/14420066 Page 9

5.2. Perpetuation of Dictatorship.

Countries with autocratic governance system normally will refuse globally accepted frameworks like the IFRS which

will open up the governance of those countries to the world and subsequently could lead to the collapse of such

governance system.

5.3. The Cost of Adoption and implementation.

The process of implementing IFRS is costly, complex and burdensome. Most companies implement IFRS for more

than consolidation purposes. Countries will have to spend huge financial resources in education and training of

professionals for the roll out of IFRS. These serve as impediment in the adoption process. E.g. The estimated total

cost of transition to IFRS is over $8 billion and one off transition costs for small and medium sized companies

will average $420,000, in USA which is material amount for a single company.

6.0 IFRS – Applicability and Concerns Aside the above reasons cited as bases of non-adoption of IFRS, the following concerns are worth noting:

Non- Listed SMEs: some concerns in respect of IFRS applicability is if SMEs are not publicly trading on

any stock exchange, why should such companies own by individuals go through the stress and cost intensive

exercise of adopting IFRS and not their local GAAP. This has led to lack of full adoption of IFRS in UK for

example where Non-listed private companies use Financial Reporting Standards (FRS) and public entities

apply IFRS. This fails to achieve IASB objective of single set financial standards for all.

Sub-Set IFRS: IASB itself in attempt to address the above concern has ended up creating a sub-set

financial reporting standard called the IFRS for SMEs which requires adoption by all countries with its

associated burden. Again, the single set of high quality, understandable and enforceable worldwide

accounting standards objective is under threat.

Mechanistic Accounting: IASB is an entity with staff who bringing new standards now and then while

changing the existing ones. Accountants and Auditors have to constantly be abreast IFRS applications and

new developments; this is making the practice of accounting too mechanical.

7.0 Conclusion: Under this report:

“The convergence to IFRS – Reasons, implications, applicability, and concerns” has been looked in details by

demonstrating the following:

Why was there a need for converting from GAAP to IFRS.

The difference between the IAS and IFRS.

Application rate of IFRS by countries in the world focusing of full, partial and no application of

IFRS by jurisdiction basis and thy reasons.

The advantages and challenges faced in IAS/IFRS application.

And whether IAS/IFRS can be applied in all contexts.

Northampton Business School/ Prince Oduro/14420066 Page 10

Over all, it is concluded that whiles the adoption of IFRS has far reaching positive benefits, it is indicative that it’s

not applicable under all circumstance. Again, countries which fails to adopt IFRS now over time may be forced to

adopt it due exclusion.

8.0 Reference List:

Book Reference:

International Financial Reporting Standards, London (2012). Part A Edition. IFRS Foundation Publications

Department

Augustine A, Student Guide to IFRS, Ghana (2007), 1st Edition. Koes Publications Ltd

Internet References:

http://www.ifrs.org/Use-around-the-world/Pages/Analysis-of-the-IFRS-jurisdictional-profiles.aspx

(Accessed on: 11th October, 2014)

http://research-methodology.net/advantages-and-disadvantages-of-ifrs-compared-to-gaap/

(Accessed on: 6th October, 2014)

Related Documents