Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

5

Annual Report 2005-06 Statement from the Governor

The global economy continued to expandat a fairly robust rate of 4.9 per cent in 2005,after registering a growth rate of 5.3 per cent in2004, and is projected to expand by 5.1 per centin 2006 despite high and volatile oil prices. Theworld’s largest economy, the United Statesposted a reasonably healthy performance. Signsthat the recovery in the euro zone has beenstrengthening are evident. In the UK, wherelabour and product market reforms are relativelyadvanced, productivity growth has beenstronger. Japan's economic expansion remainssolidly on track. Economic activity in EmergingAsia remains buoyant. Nonetheless, persistentglobal imbalances and high oil prices representsome risks to global economic prospects.Globally, consumer price inflation has begun toedge up as excess capacity in product and labourmarkets has diminished, energy prices haverisen and started to feed through to other pricesand the restraining effect that globalisation hashad on inflation in recent years has faded. In amove to pre-empt any resurgence of inflationarypressures, central banks have started to hike uptheir interest rates.

Faced with the triple shocks stemmingfrom the erosion of trade preferences in thesugar and textile sectors and the surge in oilprices on the international market, Mauritiustoday has no choice but to embrace a strategy ofbold reforms that the authorities have alreadyembarked upon. The achievement of higher job-creating growth remains a central policychallenge for Mauritius in the years ahead. Tomake any significant dent in the unemploymentproblem, Mauritius needs to move to a highergrowth path of at least 6 per cent per annum.While developing new growth poles, there is aclear need to consolidate all the existing pillars ofthe economy. As part of the reforms aimed ataddressing issues relating to rigidities andmismatch of skills in the labour market, theGovernment has already announced its intentionto review current labour laws and regulationsand the setting up of a National Wages Council to

replace the current centralized wage settingmechanism. The new economic strategy of theGovernment also places emphasis on thedemocratization of the economy while focusingon new opportunities for small and mediumenterprises. Efforts at fiscal consolidation with aview to maintaining medium-term fiscalsustainability, the achievement of a stablemacroeconomic environment and socialconsensus are key ingredients for ensuring thesuccess of economic reforms.

Economic performance during fiscal year2005-06 was characterized by a real GDP growthof 3.5 per cent, an increase in the budget deficitas a proportion of GDP to 5.3 per cent from 5.0per cent in 2004-05, an increase in theunemployment rate to 9.6 per cent, a deficit onthe current account balance and overall balanceof payments as well as a drop in the level ofgross foreign exchange reserves of the centralbank. However, net international reservesincreased, reflecting essentially the rise in thenet foreign assets of banks. On the externalfront, the current account of the balance ofpayments posted a higher deficit, attributablemainly to the faster growth of imports relative toexports. Real GDP growth is estimated at 4.6 percent in 2006.

The inflation rate declined from 5.6 percent in 2004-05 to 5.1 per cent in 2005-06 butwas higher than the target of 4.0 per cent set bythe Bank of Mauritius at the beginning of thefiscal year. This departure from the target rate ofinflation was to a large extent attributable todomestic adjustments to higher energy pricesthat have prevailed on the international marketand higher administered prices in theconsumption basket. Higher rates of inflation inour major trading partners and the depreciationof the rupee have also contributed to theinflation rate during the period under review.

International oil prices have been on arising trend during the period under review andhave amplified the imbalances on the current

Statement from the Governor

Contents-2006 (pg1-10) 12/26/06 2:59 PM Page 5

Statement from the Governor Annual Report 2005-06

6

account of the balance of payments. Petroleumimports, which used to represent around 9 percent of our total imports during the recent past,accounted for nearly 15.8 per cent of the totalimport bill for 2005-06. For the secondconsecutive year, the current account and overallbalance of payments registered a deficit.

The current account of the balance ofpayments deteriorated significantly to record ahigher deficit of Rs10,356 million in 2005-06compared with Rs6,321 million registered in2004-05. The deficit on the current accountrepresented 5.3 per cent of GDP in 2005-06compared to a deficit equivalent to 3.5 per centof GDP in 2004-05. The deterioration largelyreflected the worsening in the merchandiseaccount, which was to a certain extent offset bythe combined surpluses on the services, incomeand current transfers accounts.

During the period under review, the Bankof Mauritius raised the Lombard Rate on twooccasions, by a total of 150 basis points, from10.00 per cent to 10.50 per cent on 5 August2005 and to 11.50 per cent on 7 December2005. Banks adjusted their deposits and lendingrates more or less in line with the changes in theLombard Rate. These increases were deemednecessary to counteract the build-up ofinflationary pressures in the economy, promotemonetary conditions conducive to the reductionof the inflation differential with our major tradingpartners, maintain the attractiveness of keyrupee-denominated financial instruments andcontain emerging demand pressures on theforeign exchange market.

Effective mid-December 2006, the Bank ofMauritius will be introducing a new operationalframework for the conduct of monetary policy. Inthis connexion, the Bank has already haddiscussions with the Heads of Treasury as well aswith the Chief Executives of banks. Under thenew operational framework, the Bank will usethe Repo Rate, instead of the Lombard Rate, asthe key policy rate to signal changes in thestance of monetary policy. The Bank willimplement its monetary policy by influencingshort-term money market rates via the key RepoRate. The Bank will signal shifts in its monetarypolicy stance through announced changes in itskey Repo Rate, which would also constitute the

price of a major source of funds to the bankingsystem. Banks are expected to adjust theirinterest rates on lending and deposits in the lightof the changes in the key Repo rate. In additionto repurchase transactions, monetary policyprocedures will also include the use of reserverequirements and a standing facility.

Prior to the promulgation of the BankingAct 2004, there were two categories of BankingLicences, namely a Category 1 Banking Licenceand a Category 2 Banking Licence. Moreover,annual licence fees were payable only by banksholding a Category 2 Banking Licence. Thesebanks were dealing solely in foreign currencies.The new Banking Act 2004 has eliminated theprevious distinction and banks operate under aSingle Banking Licence regime. The Banking Act2004 further provides that an annual licence feebe levied on all banks. Similarly, everyapplication for a Banking Licence or a CashDealer Licence will have to be accompanied bythe payment of an appropriate processing fee.

The Bank is actively involved in theimplementation of the Basel II Accord (theAccord) and intends to implement the Accord by2008. At the implementation date of the NewAccord, all banks will be required to maintaincapital buffers for credit, operational and marketrisk using, as a minimum, the standardisedframeworks set out in the Accord. It is to benoted that the Bank has had an advancedimplementation schedule regarding theoperational risk component of the Accord in thesense that banks were required to have soundpractices for the management and measurementof operational risk since February 2005. Indeed,banks are already maintaining capital foroperational risk using, as a minimum, thesimplest available option under the Basel IIframework namely the Basic Indicator Approach.Furthermore, the Bank has started compilingindustry data on operational losses and isenvisaging a similar framework for credit losses.Proposal papers have been issued to the industryon the scope of application for the Basel IIframework, the standardised approach for creditrisk and on the measurement and managementof market risk.

Following the Mauritius Islamic FinanceForum held in July 2005, a Steering Committee on

Contents-2006 (pg1-10) 12/26/06 2:59 PM Page 6

7

Annual Report 2005-06 Statement from the Governor

Islamic Financial Services was set up. TheCommittee, which is Chaired by the Bank andcomprising representatives from the Ministry ofFinance and Economic Development, Ministry ofArts and Culture, State Law Office, FinancialServices Commission and the Mauritius BankersAssociation, aims at studying the prospect of anIslamic Financial Services sector in Mauritius andaccordingly propose relevant amendments to thelaw for its promotion, regulation and supervision.The Committee has made significant progress andhas prepared a research paper on the matter. Itis currently endeavouring to obtain technicalassistance from the Islamic Development Bank,which has demonstrated a keen interest in theproject. It is expected that the provision ofIslamic financial services will soon become areality in Mauritius.

Regarding the financial performance of thecentral bank, it may be noted that the Bank ofMauritius realised a profit of Rs906.1 million forthe year ended June 2006, which was slightlylower than the level of Rs967.3 million recordedin the year ended June 2005, reflecting mainlylower interest income on foreign investments.Expenses, however, declined mainly due to lowercosts of servicing Bank of Mauritius Bills, whichwent down from Rs560.6 million in 2004-05 toRs342.8 million in 2005-06.

The establishment of the Mauritius CreditInformation Bureau (MCIB), as part of the Bank’sobjective to promote a sound financial system,has been another important development duringthe year under review. Eleven banks participate inthe MCIB. As from 1 December 2005, it becamemandatory for all banks to make the necessaryenquiry from the MCIB before appraising orrenewing any credit facility. The MCIB aims atfacilitating credit decision making for banks byproviding them with a summary of borrowers’overall indebtedness towards other participatinginstitutions. The MCIB will be a useful instrumentfor the participating banks to reduce the level ofnon-performing advances in their loan portfolios.

Banks in Mauritius are increasinglyengaging in cross-border banking transactions,and in this respect, the Bank of Mauritiusinitiated action with a view to adopting anInternational Bank Account Number (IBAN)format for Mauritius. Extensive consultations

were held with banks during 2005-06 and aconsensus was reached on the IBAN format,which was implemented by banks as from March2006. Banks were requested to issue an IBAN totheir clients as from 1 April 2006. The Bank ofMauritius has also made a request to theEuropean Committee for Banking Standards(ECBS) to register the IBAN format for Mauritius.The Bank has also initiated work on a ChequeTruncation System, which is an image-basedclearing system that will replace the physicalcheque flow with electronic information flowthroughout the clearing cycle and reduce delaysassociated with movements of cheques.

Reflecting tight liquidity conditions in thedomestic foreign exchange market, the Bank ofMauritius sold a total amount of US$108.6million through intervention on the inter-bankforeign exchange market during the financialyear 2005-06. Continued vigilance isnevertheless necessary to ensure that ourinternational competitiveness is not eroded. Theexchange rate policy will continue to reflect themacroeconomic fundamentals of the country.

As part of its on-going dialogue withdomestic financial markets, the FinancialMarkets Committee, comprising the Heads ofTreasury from banks, has met regularly underthe Chairmanship of the Bank of Mauritius. TheFinancial Markets Committee acts as a forum fordiscussions on developments in the domesticmarkets and also on existing and future marketpractices and instruments.

It will be recalled that a BankingCommittee comprising the Chief Executives ofthe eleven domestic banks under myChairmanship was established in February 2001.This Committee acts as a consultative forum onbroad monetary and financial sector issues withthe overall objective of enhancing the efficientfunctioning of the banking system. Themembership of the Banking Committee has alsobeen extended to the Chief Executives of theformer Category 2 banks in line with the changeto a Single Banking Licence Regime, To date, theCommittee has met on twenty four occasions.

At the regional level, during the periodunder review, the Bank has participated in themeetings of the Committee of Central Bank

Contents-2006 (pg1-10) 12/26/06 2:59 PM Page 7

Governors in Common Market for Eastern andSouthern Africa (COMESA) and theCommittee of Central Bank Governors (CCBG)in Southern African Development Community(SADC).

The construction of the Bank’s NewHeadquarters Building is nearing completionand the Building will be officially inauguratedshortly.

Finally, I would like to express my deepappreciation for the commitment,encouragement and support of the Board ofDirectors and staff of the Bank, without whichthe objectives of the Bank would not havebeen attained.

Rameswurlall Basant Roi, G.C.S.K.

8 December 2006

Statement from the Governor Annual Report 2005-06

8

Contents-2006 (pg1-10) 12/26/06 2:59 PM Page 8

Annual Report 2005-06 Review of the Economy: 2005-06

11

Economic performance during fiscal year2005-06

1was characterized by a real GDP growth of

3.5 per cent, an increase in the budget deficit as aproportion of GDP to 5.3 per cent from 5.0 per centin 2004-05, an increase in the unemployment rateto 9.6 per cent, a deficit on the current accountbalance and overall balance of payments as well asa drop in the level of gross foreign exchangereserves of the central bank. However, netinternational reserves increased, reflectingessentially the rise in the net foreign assets ofbanks. On the external front, the current account ofthe balance of payments posted a higher deficit,attributable mainly to the faster growth of importsrelative to exports. Consumer price inflationdeclined from 5.6 per cent in 2004-05 to 5.1 percent in 2005-06. Net credit to Government from thebanking system expanded by 11.2 per cent. Broadmoney supply (M2) grew by 11.2 per cent duringthe period under review as a result of increases inboth domestic credit and net foreign assets ofbanks.

Gross Domestic Product (GDP) at basic pricesincreased by 6.5 per cent, from Rs152,420 millionin 2004 to Rs162,310 million in 2005. In realterms, the growth rate was 2.5 per cent in 2005,lower than the 4.7 per cent registered in 2004. Theagricultural sector contracted in 2005, mainly as aresult of a lower sugar output following adverseclimatic conditions. The economy is expected togrow by 4.6 per cent in 2006.

The agricultural sector declined by 5.3 percent in 2005, mainly on account of a fall of 9.2 percent in sugar output to 519,816 tonnes. The“Manufacturing” sector registered a negativegrowth of 5.5 per cent in 2005. The EPZ sectorcontracted further by 12.3 per cent in 2005, withexports totalling Rs29.0 billion compared to Rs32.0billion in 2004. It is forecast, however, that the EPZsector will register a growth of 1.5 per cent in 2006since the restructuring measures taken by severallarge firms will more than offset the impact of

increased competition stemming from low-cost andhigh-volume textile producing economies. EPZexports are estimated at around Rs33.0 billion in2006. The tourism sector grew by 5.6 per cent,with tourist arrivals increasing from 718,861 in2004 to 761,063 in 2005. Gross tourism earningswent up by 9.6 per cent, from Rs23,448 million in2004 to Rs25,704 million in 2005, compared to agrowth of 20.8 per cent in 2004. The constructionsector registered a contraction of 5.2 per cent in2005 as against a growth of 0.5 per cent in 2004.The “Financial Intermediation” sector grew by 7.0per cent in 2005 compared to 4.3 per cent in 2004.

In nominal terms, aggregate consumptionexpenditure increased by 14.2 per cent in 2005compared to 15.5 per cent in 2004. In real terms,it registered a growth of 7.1 per cent in 2005compared to 7.2 per cent in 2004. Gross NationalSavings (GNS) decreased, in nominal terms, by22.7 per cent in 2005. The savings rate, defined asthe ratio of GNS to GDP at market prices, fell from22.6 per cent in 2004 to 16.6 per cent in 2005, andis expected to decline further to 15.1 per cent in2006.

Gross Domestic Fixed Capital Formation(GDFCF), exclusive of the acquisition of aircraft,expanded by 4.3 per cent in nominal terms in 2005.In real terms, it declined by 2.1 per cent in 2005 asagainst an expansion of 4.8 per cent in 2004. Theratio of GDFCF to GDP at market prices droppedfrom 21.6 per cent in 2004 to 21.3 per cent in 2005,but is estimated to increase to 23.8 per cent in2006.

The population of the Republic of Mauritius,including Agalega and St Brandon, was estimated at1,248,592 as at 31 December 2005.

According to the “Continuous Multi-PurposeHousehold Survey” (CMPHS), the total labour forcestood at 559,100, with 358,500 males and 200,600females, in 2005. The number of foreign workersdeclined from 17,500 in 2004 to 16,600, or 5.1 per

1 Review of the Economy:2005-06

1 The fiscal year extends from 1 July to 30 June.

Chap 1-Review2006 12/26/06 3:00 PM Page 11

Review of the Economy: 2005-06 Annual Report 2005-06

12

cent, in 2005. The total number of persons inemployment, inclusive of foreign workers, stood at507,000, comprising 338,200 males and 168,800females in 2005. The unemployment rate reached9.6 per cent in 2005 from 8.5 per cent in 2004. Ona quarter-to-quarter basis, data released recentlypoint to an acceleration in the unemployment rateto 9.9 per cent in the second quarter of 2006 from9.3 per cent in the first quarter of 2006. However,it is forecast that the unemployment rate for 2006will decline to 9.4 per cent.

The rate of consumer price inflation declinedfrom 5.6 per cent in 2004-05 to 5.1 per cent in2005-06 but was higher than the target of 4.0 percent set by the Bank of Mauritius at the beginning ofthe fiscal year. This departure from the target rateof inflation was to a large extent attributable todomestic adjustments to higher energy prices thathave prevailed on the international market andhigher administered prices in the consumptionbasket. Higher rates of inflation in our major tradingpartners and the depreciation of the rupee havealso contributed to the inflation rate during theperiod under review.

International oil prices have been on a risingtrend during the period under review with adverseeffect on the current account of the balance ofpayments. Petroleum imports, which used torepresent around 9 per cent of our total importsduring the recent past, accounted for nearly 15.8per cent of the total import bill for 2005-06. Oilprices reached new record highs, with NYMEX WTI(New York Mercantile Exchange West TexasIntermediate benchmark crude oil) and IPE(International Petroleum Exchange) Brent futuresmoving from an average of US$48.8 and US$46.5 abarrel, respectively, in 2004-05 to an average ofUS$64.4 and US$63.2 a barrel, respectively, in2005-06. NYMEX WTI and IPE Brent peaked atUS$75.2 and US$74.7 a barrel, respectively, on 21April 2006. In Mauritius, as per therecommendation of the Certification Committee ofthe Automatic Price Mechanism (APM), the prices ofmogas and diesel oil were adjusted three timesduring 2005-06. Effective 3 October 2005, theprices of mogas and diesel oil were raised by 15 percent, from Rs25.25 per litre and Rs17.25 per litre,respectively, to Rs29.00 per litre and Rs19.80 perlitre, respectively. In January 2006, the governmentdecided to raise the maximum permissibleadjustment under the APM from 15 per cent to 20per cent and, effective 4 January 2006, the prices of

mogas and diesel oil were increased by 20 per centto Rs34.80 per litre and Rs23.75 per litre,respectively. At the following quarterly meeting ofthe Certification Committee of the APM, the price ofmogas was reduced by 10.1 per cent to Rs31.30 perlitre while the price of diesel oil was increased by 20per cent to Rs28.50 per litre, effective 3 April 2006.For the year 2005-06 as a whole, the prices ofmogas and diesel oil registered increases of 24.0per cent and 65.2 per cent, respectively.

During the period under review, the Bank ofMauritius raised the Lombard Rate on twooccasions, by a total of 150 basis points, from 10.00per cent to 10.50 per cent on 5 August 2005 and to11.50 per cent on 7 December 2005. Banksadjusted their deposits and lending rates more orless in line with the changes in the Lombard Rate.These increases were deemed necessary tocounteract the build-up of inflationary pressures inthe economy, promote monetary conditionsconducive to the reduction of the inflationdifferential with our major trading partners,maintain the attractiveness of key rupee-denominated financial instruments and containemerging demand pressures on the foreignexchange market. The prime lending rate of banksrose from 8.00 per cent to 9.50 per cent. Theirinterest rate on savings deposits increased from4.50 per cent to 6.00 per cent. The weightedaverage term deposits and weighted averagelending rates of banks rose from 6.42 per cent and10.89 per cent, respectively, at the end of June2005 to 7.35 per cent and 11.41 per cent,respectively, at the end of June 2006.

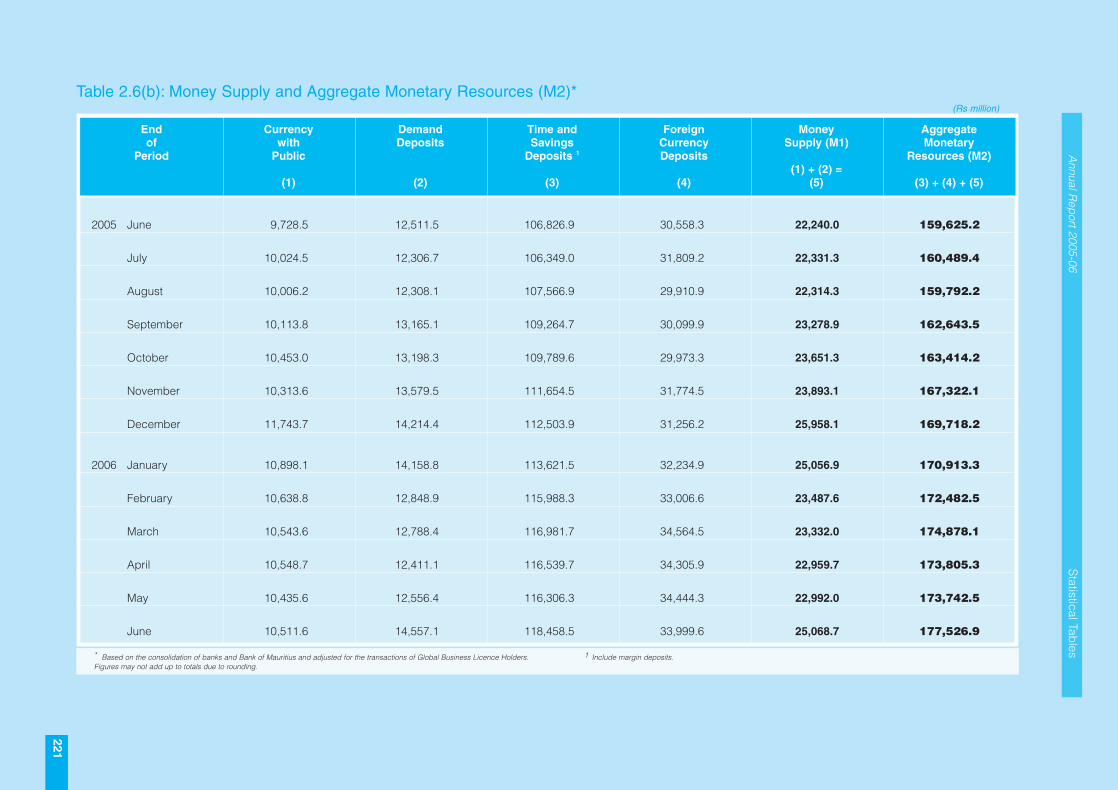

Aggregate monetary resources, that is,money supply M2, expanded by 11.2 per cent in2005-06, higher than the increase of 8.5 per cent in2004-05, on account of increases in both of itscomponents. Net foreign assets of the bankingsystem went up by 16.0 per cent, from Rs52,951million at the end of June 2005 to Rs61,435 millionat the end of June 2006, mainly on account of theincrease in the net foreign assets of banks.Domestic credit increased by 13.0 per cent in 2005-06, higher than the growth of 11.3 per cent in thepreceding year. The rise in domestic credit wasdriven by increases in both credit to the privatesector and net credit to Government. Credit to theprivate sector expanded by 13.7 per cent in 2005-06, compared to a growth of 9.6 per cent in 2004-05. Net credit to Government from thebanking system grew by 11.2 per cent in 2005-06

Chap 1-Review2006 12/26/06 3:00 PM Page 12

Annual Report 2005-06 Review of the Economy: 2005-06

13

compared to a rise of 15.7 per cent in 2004-05.

The budget deficit for 2005-06 was estimatedat Rs10,393 million, higher than the originalestimate of Rs9,546 million and the deficit ofRs9,025 million for 2004-05. As a percentage ofGDP at market prices, the budget deficit stood at5.3 per cent in 2005-06 as against 5.0 per cent in2004-05. The budget deficit for 2005-06 wasfinanced only from domestic sources. Domesticfinancing resulted mainly from the non-bank sectorand banks to the extent of Rs7,040 million andRs3,745 million, respectively. Financing from thecentral bank was also positive at Rs838 million. Netforeign financing was negative at Rs1,149 million in2005-06. At the end of June 2006, total public debtwas estimated at Rs113,477 million, representingan increase of 7.2 per cent on the end-June 2005level of Rs105,816 million. As a percentage of GDPat market prices, total public debt fell from 58.2 percent at the end of June 2005 to 57.9 per cent at theend of June 2006. The debt service ratio of thecountry increased from 6.5 per cent in 2004-05 to8.4 per cent in 2005-06.

Exchange rate movements during the periodunder review reflected the combined effects ofinternational trends and local market conditions.Between the 12-month period ended June 2005 andthe 12-month period ended June 2006, the rupee,on an average basis, depreciated by 5.5 per centagainst the US dollar, 2.7 per cent against the SouthAfrican rand, 1.4 per cent against the Poundsterling, 1.5 per cent against the Euro, butappreciated by 1.2 per cent against the Japaneseyen. Reflecting tight liquidity conditions in thedomestic foreign exchange market, the Bank ofMauritius sold a total amount of US$108.7 millionthrough intervention on the inter-bank foreignexchange market during 2005-06.

The current account of the balance ofpayments deteriorated significantly to record ahigher deficit of Rs10,356 million in 2005-06compared with Rs6,321 million registered in 2004-05. The deficit on the current accountrepresented 5.3 per cent of GDP in 2005-06compared to a deficit equivalent to 3.5 per cent ofGDP in 2004-05. The deterioration largely reflectedthe worsening in the merchandise account, whichwas to a certain extent offset by the combinedsurpluses on the services, income and currenttransfers accounts. Total exports (f.o.b.) increasedby 19.0 per cent to Rs68,849 million in 2005-06while total imports (f.o.b.) increased by 20.9 per

cent to Rs94,539 million. The capital and financialaccount, inclusive of reserve assets, recorded netinflows of Rs4,159 million in 2005-06 compared tonet inflows of Rs3,380 million in 2004-05.

Net international reserves of the country,comprising the net foreign assets of the bankingsystem, foreign assets of Government andMauritius’ Reserve position in the InternationalMonetary Fund (IMF), increased from Rs53,932million at the end of June 2005 to Rs61,974 million(US$2,004 million) at the end of June 2006. Netinternational reserves represented around 7.4months of imports at the end of June 2006compared to 7.7 months of imports at the end ofJune 2005.

The issue of Treasury/Bank of Mauritius Billswith a maturity of 728 days was discontinued inAugust 2005. With a view to lengthening thematurity profile of Government debt and offeringinvestors a wider variety of investmentinstruments, Treasury Notes with maturities of 2, 3and 4 years have been issued on a monthly basis asfrom the month of October 2005, in multiples ofRs100,000 with interest payable on a semi-annualbasis. With a view to avoiding the bunching ofpayment stemming mainly from 3-Year TreasuryNotes previously issued and with interest payable atmaturity in fiscal year 2007-08, holders of these 3-Year Treasury Notes were allowed in June 2006 toconvert part or the full amount of their holdings into2, 3 and 4-Year Treasury Notes with interestpayable on a semi-annual basis. The bulk of the 3-Year Treasury Notes with interest payable onmaturity was in fact converted into Treasury Notesof varying maturities with interest payable on asemi-annual basis.

The Banking Act 2004 has provided for theintegration of domestic and offshore bankingbusiness and eliminated the previous distinctionbetween former Category 1 (domestic) banks andformer Category 2 (offshore) banks. Both activitiesare covered under a single banking licence regime.Under the Bank of Mauritius Act 2004 and BankingAct 2004, the Bank is responsible for the regulationand supervision of banks, money-changers, foreignexchange dealers and the deposit-taking activity ofnon-bank financial institutions. The Bank devotessizeable resources to ensure the soundness andstability of financial institutions under its purview.In this context, the Bank has issued a series ofprudential guidelines to be observed by financialinstitutions and closely monitors their activities

Chap 1-Review2006 12/26/06 3:00 PM Page 13

Review of the Economy: 2005-06 Annual Report 2005-06

14

through on-site and off-site supervision. Inaddition to the sixteen guidelines already in force,the Bank issued an additional Guideline onOutsourcing by Financial Institutions during theyear. This Guideline was deemed necessaryfollowing a growing trend in outsourcing activitiesthat have given rise to new risks that have to becatered for. Another important development hasbeen the establishment of the Mauritius CreditInformation Bureau (MCIB) as part of the Bank’sobjective to promote a sound financial system.Eleven banks participate in the MCIB. As from 1December 2005, it became mandatory for all banksto make the necessary enquiry from the MCIBbefore appraising or renewing any credit facility.The MCIB aims at facilitating credit decision makingfor banks by providing them with a summary ofborrowers’ overall indebtedness towards otherparticipating institutions. The MCIB will be a usefulinstrument for the participating banks to reduce thelevel of non-performing advances in their loanportfolios.

Banks are required to maintain a minimumcapital adequacy ratio of 10.0 per cent. As at end-June 2006, the whole banking sector reported riskweighted capital adequacy ratios, which were wellabove the prescribed minimum of 10.0 per cent.The overall risk weighted capital adequacy ratio forcredit risk maintained by banks went up from 16.0per cent as at end-June 2005 to 17.0 per cent as atend-June 2006. During 2005-06, the bankingsector registered a strong financial performance.The aggregate pre-tax profits of banks for the yearunder review went up by Rs1,542 million, or 24.4per cent, from Rs6,312 million in 2004-05 toRs7,854 million in 2005-06. The growth in profitswas mainly driven by higher revenue derived frominterest and non-interest income as well as a lowercharge for bad and doubtful debts.

The Bank of Mauritius has adopted aparticipative approach to Basel II implementationand eight Working Groups, comprisingrepresentatives of the Bank of Mauritius as well asbanks, have been set up to look into issues relatingto Scope of Application, Credit Risk (foundation),Market Risk, Credit Risk (Advanced), OperationalRisk, External Credit Assessment Institutions(ECAI), Eligible Capital and Market Discipline. Thetarget date for the implementation of Basel II hasbeen tentatively set at early 2008.

Regarding its financial performance, it may be

noted that the Bank of Mauritius realised a profit ofRs906.1 million for the year ended June 2006,which was slightly lower than the level of Rs967.3million recorded in the year ended June 2005,reflecting mainly lower interest income on foreigninvestments. Expenses, however, declined mainlydue to lower costs of servicing Bank of MauritiusBills, which went down from Rs560.6 million in2004-05 to Rs342.8 million in 2005-06.

As banks in Mauritius are increasinglyengaging in cross-border banking transactions, theBank of Mauritius initiated action with a view toadopting an International Bank Account Number(IBAN) format for Mauritius. Extensiveconsultations were held with banks during 2005-06and a consensus was reached on the IBAN format,which was implemented by banks as from March2006. Banks were requested to issue an IBAN totheir clients as from 1 April 2006. The Bank ofMauritius has made a request to the EuropeanCommittee for Banking Standards (ECBS) toregister the IBAN format for Mauritius and hasalready forwarded to the ECBS the informationcalled for. The Bank has also initiated work on aCheque Truncation System, which is an image-based clearing system that will replace the physicalcheque flow with electronic information flowthroughout the clearing cycle and reduce delaysassociated with movements of cheques.

Faced with the triple shocks stemming fromthe erosion of trade preferences in the sugar andtextile sectors and the surge in oil prices on theinternational market, Mauritius today has no choicebut to embrace a strategy of bold reforms that theauthorities have already embarked upon. Theachievement of higher job-creating growth remainsa central policy challenge for Mauritius in the yearsahead. To make any significant dent in theunemployment problem, Mauritius needs to moveto a higher growth path of at least 6 per cent perannum. While developing new growth poles, thereis a clear need to consolidate all the existing pillarsof the economy. As part of the reforms aimed ataddressing issues relating to rigidities andmismatch of skills in the labour market, theGovernment has already announced its intention toreview current labour laws and regulations and setup a National Wages Council to replace the currentcentralized wage setting mechanism. Theimplementation of the National Wages Council willallow enterprises to put in place a flexible andcompetitive wage system which would be more

Chap 1-Review2006 12/26/06 3:00 PM Page 14

Annual Report 2005-06 Review of the Economy: 2005-06

15

responsive to the changing business environmentand with a clear focus on cost reduction as well asenhanced productivity and competitiveness. Thenew economic strategy of the Government alsoplaces emphasis on the democratization of theeconomy while focusing on new opportunities forsmall and medium enterprises. Efforts at fiscalconsolidation with a view to maintaining medium-term fiscal sustainability, the achievement of astable macroeconomic environment and socialconsensus are key ingredients for ensuring thesuccess of economic reforms.

The foregoing economic and financialdevelopments during the year 2005-06 arereviewed in greater detail in the following chaptersof the report.

Chap 1-Review2006 12/26/06 3:00 PM Page 15

National Income and Production Annual Report 2005-06

16

Output

Gross Domestic Product (GDP) at basic priceswent up by 6.5 per cent, in nominal terms, fromRs152,420 million in 2004 to Rs162,310 million in2005. In real terms, the economy grew by 2.5 percent in 2005, down from 4.7 per cent in 2004.Exclusive of sugar, the growth rate of the economyworked out to 3.0 per cent compared to 4.6 per centin 2004. The drop in the real growth rate of theeconomy in 2005 is largely explained by thenegative growth rates in the agricultural, EPZ andconstruction sectors. There was also a decelerationin the real growth rate of the ‘Wholesale and retailtrade’, ‘Transport, storage and communications’,‘Electricity, gas and water’ and ‘Real estate, rentingand business activities’ sectors. In contrast, the‘Hotels and restaurants’ and ‘Financialintermediation’ sectors recorded higher real growthrates than in 2004.

GDP at market prices increased by 5.6 percent, from Rs175,592 million in 2004 to Rs185,487million in 2005. Taxes on products amounted toRs23,177 million, slightly up on the 2004 figure.Gross National Income (GNI) at market pricesreached Rs185,251 million, up by 5.7 per cent, fromRs175,202 million in 2004. GNI per capita at marketprices went up by 4.9 per cent, from Rs142,017 in2004 to Rs148,971 in 2005. Per capita GDP atmarket prices increased by 4.8 per cent, fromRs142,333 in 2004 to Rs149,160 in 2005.

Table I.1 shows the main national accountingaggregates and ratios for the years 2003 through2006. Chart I.1 shows per capita GNI at marketprices and real growth rate of GDP for the years1998 through 2005.

Income

Compensation of Employees

Compensation of employees, which includeswages and salaries and employer socialcontributions, grew by 6.7 per cent, from Rs63,790million in 2004 to Rs68,064 million in 2005. As apercentage of GDP at basic prices, compensation of

employees was 41.9 per cent in 2005, unchangedfrom 2004.

Net Taxes on Production and Imports

Taxes (net of subsidies) on production andimports increased by 0.7 per cent, from Rs24,733million in 2004 to Rs24,900 million in 2005. Taxes onproducts went up by 1.2 per cent, from Rs23,785million to Rs24,060 million, over the same period.

Gross Operating Surplus

Gross operating surplus, which is the excess ofgross output over the sum of intermediateconsumption, compensation of employees and nettaxes on production and imports, increased by 6.3per cent, from Rs87,069 million in 2004 to Rs92,524million in 2005.

Transactions with Non-residents

Net primary income from the rest of the worldwent up by Rs154 million, from a negative figure ofRs390 million in 2004 to a negative figure of Rs236million in 2005. Net transfer from the rest of theworld went up by 30.9 per cent, from Rs1,374million in 2004 to Rs1,798 million in 2005.

Gross National Disposable Income

Gross National Disposable Income (GNDI) wentup, in nominal terms, by 5.9 per cent, fromRs176,576 million in 2004 to Rs187,049 million in2005, compared to a growth of 11.7 per cent in 2004.

Gross National Savings

Gross National Savings (GNS), which is thatpart of GNDI that is not spent on consumption, fellby 22.7 per cent, from Rs39,713 million in 2004 toRs30,713 million in 2005. The ratio of GNS to GDP atmarket prices declined from 22.6 per cent in 2004 to16.6 per cent in 2005.

Expenditure on GDP

Final Consumption Expenditure

Aggregate final consumption expenditure ofhouseholds and General Government went up by14.2 per cent, from Rs136,863 million in 2004 toRs156,336 million in 2005. In real terms, it grew by

I. NATIONAL INCOME ANDPRODUCTION

CHAP I-NY2006 12/26/06 3:18 PM Page 16

17

Annual Report 2005-06 National Income and Production

a lower rate of 7.1 per cent in 2005 compared to 7.2per cent in 2004. Household consumptionexpenditure expanded, in real terms, by 7.3 per centin 2005 compared to 7.8 per cent in 2004. Generalgovernment consumption expenditure registered areal growth rate of 6.1 per cent in 2005 compared to4.6 per cent in 2004. As a percentage of GDP atmarket prices, aggregate final consumptionexpenditure went up from 77.9 per cent in 2004 to84.3 per cent in 2005. Household final consumptionexpenditure as a percentage of GDP at market pricesrose from 63.6 per cent in 2004 to 69.5 per cent in2005. General government final consumptionexpenditure to GDP at market prices increased from14.3 per cent in 2004 to 14.8 per cent in 2005.

Gross Domestic Fixed Capital Formation(GDFCF)

Investment went up by 4.0 per cent, fromRs38,003 million in 2004 to Rs39,524 million in2005. In real terms, it declined by 2.4 per cent in

2005 after registering a real growth rate of 2.2 percent in 2004. As a percentage of GDP at marketprices, the Resource Balance (defined as Savingsminus Investment) fell from a negative figure of 2.4per cent in 2004 to a negative figure of 6.0 per centin 2005. Gross Domestic Fixed Capital Formation,exclusive of the purchase of aircraft, contracted, inreal terms, by 2.1 per cent in 2005 as against agrowth of 4.8 per cent in 2004. The ratio of GDFCFto GDP at market prices went down from 21.6 percent in 2004 to 21.3 per cent in 2005.

Investment by the private sector increased by5.4 per cent, from Rs26,345 million in 2004 toRs27,767 million in 2005. In real terms, however,private sector GDFCF registered a decline of 1.1 percent in 2005 after a high growth of 16.3 per cent in2004. The negative growth in private sector GDFCFis mostly explained by a contraction in theconstruction of houses and lower investment inhotels and in machinery and equipment in the EPZsector compared to 2004.

A. Aggregates (Rs million)

1. GDP at basic prices 137,588 152,420 162,310 178,353

Annual Real Growth Rate (Per cent) +4.4 +4.7 +2.5 +4.6

2. GDP at market prices 157,394 175,592 185,487 203,337

3. GNI at market prices 156,561 175,202 185,251 204,837

4. Per Capita GNI at market prices (Rupees) 128,004 142,017 148,971 163,479

5. Aggregate Consumption Expenditure 118,452 136,863 156,336 176,187

6. Compensation of Employees 58,675 63,790 68,064 73,390

7. Gross Domestic Fixed Capital Formation 35,554 38,003 39,524 48,376

8. Gross Capital Formation 36,922 42,894 40,216 47,610

9. Gross Domestic Savings 38,942 38,729 29,151 27,150

10. Resource Balance ( 9 - 8 ) 2,020 -4,165 -11,065 -20,460

11. Gross National Disposable Income 158,032 176,576 187,049 206,930

B. Ratios: As a Percentage of GDP at market prices

1. Gross Domestic Savings 24.7 22.1 15.7 13.4

2. Aggregate Consumption Expenditure 75.3 77.9 84.3 86.7

3. Gross Domestic Fixed Capital Formation 22.6 21.6 21.3 23.8

4. Resource Balance 1.3 -2.4 -6.0 -10.1

C. Ratio: As a Percentage of GDP at basic prices

1. Compensation of Employees 42.6 41.9 41.9 41.1

Table I.1: Main National Accounting Aggregates and Ratios: 2003 - 2006

2003 1 2004 1 2005 1 2006 2

1 Revised estimates. 2 Forecast. Figures are based on the 2002 Census of Economic Activities. Source: Central Statistics Office, Government of Mauritius.

CHAP I-NY2006 12/26/06 3:18 PM Page 17

National Income and Production Annual Report 2005-06

18

Public sector investment increased by 0.8 percent, in nominal terms, from Rs11,658 million in2004 to Rs11,757 million in 2005. In real terms,public sector GDFCF registered a lower contractionof 5.4 per cent in 2005 compared to the negativegrowth of 19.8 per cent in 2004. That decline isessentially attributable to lower investment in publichousing and health infrastructure and cyber towers,offset by higher investment in public sewerageworks and machinery and equipment by someparastatal bodies. The share of private sector GDFCFin total GDFCF increased to 70.3 per cent in 2005from 69.3 per cent in 2004 while the share of publicsector investment went down to 29.7 per cent in2005 from 30.7 per cent in 2004.

A breakdown of GDFCF by type of capitalgoods shows that, in real terms, investment in‘Building and construction work’ declined by 6.2 percent in 2005 compared to a contraction of 0.3 percent in 2004. Capital formation in ‘ResidentialBuilding’ went down, in real terms, by 10.5 per centin 2005 compared to a decline of 2.3 per cent in2004. Investment in the non-residential sub-sectorcontracted by 12.1 per cent in 2005 after growing by20.1 per cent in 2004. Investment in ‘Otherconstruction work’ expanded, in real terms, by 13.0per cent in 2005 as against a negative growth of24.2 per cent in 2004. Real growth of GDFCF in‘Machinery and equipment’ stood at 3.4 per cent in2005, down from 6.2 per cent in 2004. Exclusive of

aircraft, investment in ‘Machinery and equipment’grew, in real terms, by 4.1 per cent in 2005compared to 13.4 per cent in 2004. Investment in‘Passenger car’ decreased by 14.1 per cent in 2005after growing by 39.5 per cent in 2004. Investmentin ‘Other transport equipment’, excluding aircraft,expanded by 9.2 per cent in 2005 as against adecline of 16.3 per cent in 2004. Investment in‘Other machinery and equipment’ increased by 7.8per cent in 2005 compared to 14.0 per cent in 2004.

An analysis of investment by industrial useshows that investment activities in several sectorswere adversely affected in 2005. Investment in‘Manufacturing’ contracted by 1.7 per cent in 2005,with investment in the EPZ declining by 10.0 percent. Investment in ‘Hotels and restaurants’registered a real negative growth of 24.6 per cent in2005 after growing significantly by 52.2 per cent in2004. Investment in the ‘Health and social work’sector declined by 26.3 per cent in 2005 as againsta growth of 15.2 per cent in 2004. Capital formationin the ‘Real estate, renting and business activities’and ‘Construction’ sectors contracted by 11.5 percent and 12.2 per cent, respectively, in 2005 aftergrowing by 0.6 per cent and 19.5 per cent,respectively, in 2004.

In contrast, investment in the ‘Agriculture,hunting, forestry and fishing’ sector expanded, inreal terms, by 42.9 per cent in 2005 compared to

A. Building and Construction Work +12.9 -0.3 -6.2

Residential Building +4.6 -2.3 -10.5

Non-residential Building +7.6 +20.1 -12.1

Other Construction Work +34.5 -24.2 +13.0

B. Machinery and Equipment +6.5 +6.2 +3.4

Machinery and Equipment (excluding aircraft & marine vessel) +1.1 +13.4 +4.1

Passenger Car +12.2 +39.5 -14.1

Other Transport Equipment +66.5 -40.3 +2.0

Other Transport Equipment (excluding aircraft & marine vessel) +32.3 -16.3 +9.2

Other Machinery and Equipment -5.2 +14.0 +7.8

GDFCF +10.3 +2.2 -2.4

GDFCF (excluding aircraft & marine vessel) +8.1 +4.8 -2.1

Table I.2: Real Growth Rates of GDFCF by Type of Capital Goods: 2003 - 2005

2003 1 2004 1 2005 1

(Per cent)

1 Revised estimates.Source: Central Statistics Office, Government of Mauritius.

CHAP I-NY2006 12/26/06 3:18 PM Page 18

19

Annual Report 2005-06 National Income and Production

1. Agriculture, Hunting, Forestry and Fishing +10.8 +33.8 +42.9

2. Mining and Quarrying - +150.8 -100.0

3. Manufacturing -11.9 +26.5 -1.7

of which: EPZ -6.1 +71.6 -10.0

4. Electricity, Gas and Water +19.7 -4.8 +45.8

5. Construction +323.6 +19.5 -12.2

6. Wholesale and Retail Trade; Repair of Motor Vehicles,

Motor Cycles, Personal and Household Goods -3.7 -3.7 +3.6

of which: Wholesale and Retail Trade -4.1 -4.3 +4.0

7. Hotels and Restaurants -20.2 +52.2 -24.6

8. Transport, Storage and Communication +24.5 -30.3 +5.3

9. Financial Intermediation -18.0 +15.8 +32.6

10. Real Estate, Renting, and Business Activities +16.7 +0.6 -11.5

Owner occupied dwellings +4.6 -2.3 -10.5

Other +128.3 +13.2 -15.4

11. Public Administration and Defence; Compulsory Social Security +24.4 +9.5 -26.0

12. Education +14.3 -10.6 +6.1

13. Health and Social Work -7.6 +15.2 -26.3

14. Other Services +77.1 -34.6 +25.8

Gross Domestic Fixed Capital Formation +10.3 +2.2 -2.4

2003 1 2004 1 2005 1

1 Revised estimates.Source: Central Statistics Office, Government of Mauritius.

1998 1999 2000 2001 2002 2003 2004 200516

18

20

22

24

26

28

30

Chart I.2: Ratios of GDFCF and GNS to GDP at Market Prices:1998 - 2005

Source: Central Statistics Office, Government of Mauritius.

Per cent

GDFCF to GDP Ratio

GNS to GDP Ratio

1998 1999 2000 2001 2002 2003 2004 2005

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

0

1

2

3

4

5

6

7

8

9

10

Per capita GNI Growth Rate

Chart I.1: Per capita GNI and Growth Rate: 1998 - 2005

Source: Central Statistics Office, Government of Mauritius.

Per capita GNI (Rs) Real Growth Rate of GDP (%)

Table I.3: Real Growth Rates of GDFCF by Industrial Use: 2003 - 2005(Per cent)

CHAP I-NY2006 12/26/06 3:18 PM Page 19

National Income and Production Annual Report 2005-06

20

33.8 per cent in 2004. GDFCF in the ‘Education’sector expanded, in real terms, by 6.1 per cent in2005 following a contraction of 10.6 per cent in theprevious year. Investment in ‘Financialintermediation’ increased, in real terms, by 32.6 percent in 2005. Capital formation in the ‘Electricity,gas and water supply’ and ‘Transport, storage andcommunications’ sectors went up by 45.8 per centand 5.3 per cent, respectively, in 2005. As apercentage of total GDFCF, investment in‘Manufacturing’, ‘Hotels and restaurants’, ‘Transport,storage and communications’ and ‘Real estate,

renting and business activities’ stood at 14.1 per

cent, 10.6 per cent, 11.5 per cent and 24.1 per cent,

respectively, in 2005.

Changes in Inventories

Inventories, which include the value of the

physical change in inventories of raw materials,

work in progress and finished goods held by

producers, fell to Rs692 million in 2005 from

Rs4,891 million in 2004.

1. Value Added at current basic prices (Rs million) 8,727 9,663 9,624

of which: Sugarcane 4,508 5,094 5,046

2. Annual Real Growth Rate (Per cent) +1.9 +6.0 -5.3

3. Share of Agriculture in GDP at basic prices (Per cent) 6.4 6.3 5.9

4. Investment at current prices (Rs million) 953 1,328 2,025

5. Share of Investment in Agriculture in total GDFCF (Per cent) 2.7 3.5 5.1

6. Sugar Exports (Rs million) 8,775 9,631 10,536

7. Agricultural Exports other than Sugar (Rs million) 185 290 273

8. Share of Agricultural Exports in total Domestic Exports (Per cent) 21.3 22.7 25.7

Table I.4: Main Aggregates of the Agricultural Sector: 2003-2005

2003 1 2004 1 2005 2

Chart I.3: Investment by Sector in 2005

Agriculture5%

Manufacturing14%

Electricity, Gas and Water

7%

Construction2%

Wholesaleand Retail

Trade7%

Real Estate, Rentingand Business Services

24%

Hotels andRestaurants

11%

Governmentand Others

16%

Source: Central Statistics Office, Government of Mauritius.

Transport, Storageand Communication

11%

FinancialIntermediation

3%

1 Revised estimates. 2 Provisional. Source: Central Statistics Office, Government of Mauritius.

1998 1999 2000 2001 2002 2003 2004 2005-40

-30

-20

-10

0

10

20

30

40

50

60

Chart I.4: Growth Rates of Public and Private Investment: 1998 - 2005

Source: Central Statistics Office, Government of Mauritius.

Per cent

Private Investment

Public Investment

CHAP I-NY2006 12/26/06 3:18 PM Page 20

21

Annual Report 2005-06 National Income and Production

Imports and Exports of Goods and Services

In nominal terms, imports of goods andservices went up by 23.4 per cent, from Rs99,024million in 2004 to Rs122,156 million in 2005,reflecting mainly increased activities of the Freeportand the rise in the import bill of petroleum products.In real terms, imports of goods and services grew by6.4 per cent, up from 2.8 per cent in 2004.

In nominal terms, exports of goods and serviceswent up by 17.1 per cent, from Rs94,859 million in2004 to Rs111,091 million in 2005, reflecting againthe increase in Freeport activities, which was partlyoffset by a decline in EPZ exports. In real terms,exports of goods and services grew by 11.7 per cent incontrast to a fall of 0.3 per cent in 2004.

Tables I.2 and I.3 show the real growth rates ofGDFCF by type of capital goods and by industrial use,respectively, for the years 2003 through 2005. ChartI.2 depicts the movements in the ratios of GDFCFand Gross National Savings (GNS) to GDP at marketprices for the years 1998 through 2005. Chart I.3shows investment by sector in 2005 and Chart I.4depicts the growth rates of public and privateinvestment for the years 1998 through 2005.

Agriculture

The agricultural sector was adversely affectedby unfavourable weather conditions prevailing in2005. In real terms, it contracted by 5.3 per cent in2005 as against a growth of 6.0 per cent in 2004.The sugar sector registered a negative real growthrate of 9.2 per cent in 2005 in contrast to a growth

Opening Stock (1 July) 25,890 39,029 30,702 40,119

Opening ISA Special Stock 0 0 0 0

Production 539,264 530,920 574,029 511,628

Available supplies 595,3671

607,3662

643,7743

593,6074

Exports: 515,036 534,911 564,020 521,210

United Kingdom 446,262 466,563 479,331 469,812

Other European Union 60,484 40,686 55,770 33,048

United States 1,852 2,681 21,983 7,041

Canada 143 186 386 165

Other 6,295 24,795 6,550 11,144

Domestic Consumption 40,745 40,778 39,597 39,638

Surplus/(Loss) in Storage 556 973 38 255

Closing Stock (30 June) 39,029 30,702 40,119 32,505

Closing ISA Special Stock 0 0 0 0

Table I.5: Sugar Production and Exports: 2002-03 - 2005-06

2002-03 2003-04 2004-05 2005-06

(Tonnes Tel Quel)

Chart I.5: Sectoral Distribution of GDP at Basic Prices in 2005

Agriculture6%

Manufacturing20%

Electricity, Gas and

Water2%

Construction5%

Wholesale andRetail Trade

12%

Real Estate, Rentingand Business Services

10%

Hotels andRestaurants

8%

Governmentand Others

14%

Source: Central Statistics Office, Government of Mauritius.

Transport, Storageand Communication

13%

FinancialIntermediation

10%

1 Includes 30,213 tonnes of imported sugar. 2 Includes 37,417 tonnes of imported sugar.3 Includes 39,043 tonnes of imported sugar. 4 Includes 41,860 tonnes of imported sugar.Note: The above figures refer to fiscal years, which extend from July to June, and not to crop years, which extend from June to May. Source: Mauritius Sugar News Bulletin, Mauritius Chamber of Agriculture.

CHAP I-NY2006 12/26/06 3:18 PM Page 21

National Income and Production Annual Report 2005-06

22

of 6.5 per cent in 2004. The non-sugar agriculturalsector declined by 1.0 per cent in 2005 as against agrowth of 5.4 per cent in 2004.

Table I.4 shows the main aggregates of theagricultural sector for the years 2003 through 2005.Chart I.5 shows the sectoral distribution of GDP atbasic prices in 2005.

Sugar

The adverse climatic conditions prevailingduring the months of March, April and May, theexcessive rainfall during September and the dryweather during the last months of 2005 affectedsugar cane production. Sugar output fell by 9.2 percent in 2005 and value added by the sugar sectoraccounted for approximately 52 per cent of totalvalue added by the agricultural sector. Sugarproduction stood at 519,816 tonnes in 2005compared to 572,316 tonnes in 2004. The totalsugarcane area harvested decreased to 68,351

hectares in 2005 from 69,698 hectares in 2004. Theaverage yield of sugarcane per hectare fell from75.76 tonnes in 2004 to 72.92 tonnes in 2005. Therate of extraction of sugar dropped from 10.85 percent in 2004 to 10.44 per cent in 2005.

Table I.5 shows sugar production and exportsfor the years 2002-03 through 2005-06.

Sugar production for fiscal year 2005-06attained 511,628 tonnes compared to 574,029tonnes for fiscal year 2004-05. For 2005-06, exportsand imports of sugar reached 521,210 tonnes and41,860 tonnes, respectively, compared to 564,020tonnes and 39,043 tonnes, respectively, for 2004-05. Around 96 per cent of total sugar exports, thatis, 502,860 tonnes, were directed to the EuropeanUnion under the Sugar Protocol. Domesticconsumption increased from 39,597 tonnes in 2004-05 to 39,638 tonnes in 2005-06.

In spite of a lower export volume, exportproceeds of cane sugar increased from Rs9,631

1. Number of Enterprises (as at December) 506 501 506

2. Value Added at current basic prices (Rs million) 13,171 13,134 12,100

3. Annual Real Growth Rate (Per cent) -6.0 -6.8 -12.3

4. Share of EPZ in total GDP at basic prices (Per cent) 9.6 8.6 7.5

5. Investment at current prices (Rs million) 1,418 2,508 2,391

6. Share of EPZ Investment in total GDFCF (Per cent) 4.0 6.6 6.0

7. Exports (f.o.b.) (Rs million) 31,444 32,046 28,954

8. Imports (c.i.f.) (Rs million) 15,579 17,195 15,518

9. Net Exports (Rs million) 15,865 14,851 13,436

Table I.7: Main Aggregates of the EPZ : 2003 - 2005

2003 1 2004 1 2005 2

1 Revised estimates. 2 Provisional.Source: Central Statistics Office, Government of Mauritius.

1. Value Added at current basic prices (Rs million) 29,581 31,799 32,040

2. Annual Real Growth Rate (Per cent) +0.0 +0.3 -5.5

3. Share of Value Added in GDP at basic prices (Per cent) 21.5 20.8 19.7

4. Investment at current prices (Rs million) 4,109 5,346 5,554

5. Share of Investment in total GDFCF (Per cent) 11.6 14.1 14.1

Table I.6: Main Aggregates of the Manufacturing Sector: 2003 - 2005

2003 1 2004 1 2005 1

1 Revised estimates.Source: Central Statistics Office, Government of Mauritius.

CHAP I-NY2006 12/26/06 3:18 PM Page 22

23

Annual Report 2005-06 National Income and Production

million in 2004 to Rs10,536 million in 2005. Theshare of sugar exports in total domestic exports rosefrom 22.1 per cent in 2004 to 25.0 per cent in 2005.Export receipts from cane molasses declined fromRs190 million in 2004 to Rs173 million in 2005.

Non-Sugar Agricultural Sector

The non-sugar agricultural sector declined by1.0 per cent in 2005 as against a growth of 5.4 percent in 2004. In nominal terms, however, valueadded by this sector increased from Rs4,569 millionin 2004 to Rs4,578 million in 2005. Its share in theagricultural sector rose from 47.3 per cent in 2004to 47.6 per cent in 2005.

The total area under foodcrop productiondropped from 7,553 hectares in 2004 to 6,971hectares in 2005, with foodcrop production fallingfrom 111,633 tonnes to 99,738 tonnes over thesame period as a result of unfavourable climaticconditions prevailing in 2005. The production of teafell from 7,229 tonnes in 2004 to 6,798 tonnes in2005 while tobacco production went down from 357tonnes in 2004 to 296 tonnes in 2005.

Manufacturing

The manufacturing sector, which comprisessugar milling, EPZ and ‘other manufacturing’,contracted, in real terms, by 5.5 per cent in 2005 asagainst a growth of 0.3 per cent in 2004. Themanufacturing sector accounted for 19.7 per cent oftotal value added in the economy in 2005. The EPZsub-sector registered a negative growth of 12.3 percent in 2005 after a contraction of 6.8 per cent in2004 due to the end of the textile trade quotas inJanuary 2005 in addition to the fierce competitionwith low-cost textile-producing countries. Total outputof the EPZ was Rs32.0 billion compared to Rs34.0billion in 2004. The sugar milling sub-sector declinedby 9.2 per cent in 2005 in contrast to a growth of 6.5per cent in 2004. The non-sugar milling and non-EPZsub-sectors registered zero growth in 2005 comparedto the 6.0 per cent growth in 2004.

Table I.6 shows the main aggregates of themanufacturing sector for the years 2003 through2005.

EPZ exports fell by 9.6 per cent, from Rs32,046million in 2004 to Rs28,954 million in 2005, as againstan increase of 1.9 per cent in 2004. EPZ imports alsodeclined by 9.8 per cent, from Rs17,195 million in

2004 to Rs15,518,million in 2005, in contrast to a riseof 10.4 per cent in 2004. Net EPZ exports went downby 9.5 per cent, from Rs14,851 million in 2004 toRs13,436 million in 2005.

In 2005, the main EPZ markets remained theUnited Kingdom, France and United States, whichrepresented 31.8 per cent, 20.9 per cent and 17.7per cent, respectively, of all EPZ export markets. Themain countries of origin of EPZ imports in 2005 wereIndia, China and France, with shares of 13.3 percent, 13.0 per cent and 12.4 per cent, respectively.EPZ imports from European countries increased by3.7 per cent, while those from Asian and Africancountries fell by 20.0 per cent and 14.0 per cent,respectively, in 2005.

Employment in the EPZ sector declined furtherby 1,091, or 1.6 per cent, from 68,022 as atDecember 2004 to 66,931 as at December 2005.This downward trend was the result of furtherclosures and downsizing of firms in the wake of theelimination of textile trade quotas and the fiercecompetition with low-cost textile-producingeconomies.

Table I.7 shows some major aggregates of theEPZ for the years 2003 through 2005.

1998 1999 2000 2001 2002 2003 2004 2005

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

0

5,000

10,000

15,000

20,000

25,000

30,000

Tourist Arrivals Tourism Receipts

Chart I.6: Tourist Arrivals and Tourism Receipts: 1998 - 2005

Source: Central Statistics Office, Government of Mauritius.

Tourist Arrivals Tourism Receipts(Rs million)

CHAP I-NY2006 12/26/06 3:18 PM Page 23

National Income and Production Annual Report 2005-06

24

Tourism

The tourism sector registered a real growth of5.6 per cent in 2005 compared to 2.4 per cent in2004. Gross tourism receipts went up by 9.6 percent, from Rs23,448 million in 2004 to Rs25,704million in 2005, compared to a growth of 20.8 percent in 2004. Tourist arrivals increased from718,861 in 2004 to 761,063 in 2005. Total touristnights increased from 7,119,000 in 2004 to7,498,000 in 2005. Around 90.9 per cent of foreignvisitors came to Mauritius on holiday in 2005 whilesome 3.2 per cent came for business purposes.

Chart I.6 shows tourist arrivals and tourismreceipts for the years 1998 through 2005.

Tourist arrivals from Europe increased by 5.4per cent, from 477,041 in 2004 to 502,715 in 2005,up from 2.5 per cent in 2004. In 2005, tourists fromEuropean countries represented almost two thirdsof total tourist arrivals. Tourist arrivals from France,United Kingdom, Germany and Italy went up by 4.8per cent, 3.0 per cent, 7.1 per cent and 5.3 percent, respectively, in 2005. Tourist arrivals from theAfrican region rose by 5.4 per cent, from 175,649 in2004 to 185,208 in 2005, compared to 0.7 per centin 2004. The number of tourists from Asia, Americaand Australia increased by 8.6 per cent, 5.2 per centand 18.6 per cent, respectively, in 2005. Touristarrivals from Reunion Island and the Republic ofSouth Africa rose by 2.6 per cent and 11.1 per cent,respectively, in 2005.

There were 99 hotels in operation at the endof December 2005 with the number of rooms andbed places standing at 10,497 and 21,072,respectively, compared to 10,640 and 21,355,respectively, at the end of December 2004. Theaverage room occupancy rate for all hotels and thatfor “large” hotels remained unchanged at 63 percent and 66 per cent, respectively, in 2005.

Direct employment in the tourism sectorincreased by 12.2 per cent, from 22,613 at the endof March 2004 to 25,377 at the end of March 2005,compared to 3.4 per cent in 2004.

Financial Intermediation

The ‘Financial intermediation’ sector, whichincludes insurance and banking services, expandedby 7.0 per cent in 2005, up from 4.3 per cent in2004. The ‘Insurance’ sub-sector grew by 5.0 per

cent in 2005, unchanged from 2004. Other financialintermediation activities registered a growth of 7.8per cent in 2005, up from 4.0 per cent in 2004,reflecting the growth of 19.4 per cent by offshorebanks, 2.3 per cent by commercial banks, and 10.2per cent by other financial institutions.

Real Estate, Renting and BusinessActivities

The ‘Real estate, renting and businessactivities’ sector, which comprises owner occupieddwellings, renting of machinery and operator,computer activities and other business activities,grew by 6.5 per cent in 2005 compared to 6.7 percent in 2004. The ‘Owner occupied dwellings’ sub-sector expanded by 4.8 per cent in 2005, lower thanthe 5.3 per cent in 2004, while activities other than‘Owner occupied dwellings’ increased by 8.1 percent in 2005 compared to 8.0 per cent in 2004.

Other Sectors

Value added in the ‘Electricity, gas and water’sector increased, in real terms, by 3.8 per cent in2005 compared to 4.0 per cent in 2004. The‘Construction’ sector declined by 5.2 per cent in 2005as against a growth of 0.5 per cent in 2004,reflecting the contraction of 6.2 per cent ininvestment in building and other construction work.The ‘Transport, storage and communications’ sectorexpanded by 7.8 per cent in 2005 compared to 8.3per cent in 2004. The growth rate of ‘Wholesale andretail trade’ decelerated from 5.7 per cent in 2004 to5.2 per cent in 2005, reflecting the fall in the growthof distributive trade from 5.5 per cent in 2004 to 5.0per cent in 2005. The ‘Public administration anddefence and compulsory social security’ sector grewby 5.3 per cent in 2005, higher than the 4.3 per centin 2004. The ‘Education’ sector recorded a growth of6.1 per cent in 2005 compared to 6.4 per cent in2004. The ‘Health and social work’ sector expandedby 6.5 per cent in 2005 compared to 7.4 per cent in2004, while ‘Other services’ grew by 7.9 per cent in2005 compared to 7.6 per cent in 2004.

Growth Outlook

The strong upturn of the world economyduring the past three years - notwithstanding thevolatility in financial and commodity markets and

CHAP I-NY2006 12/26/06 3:18 PM Page 24

25

Annual Report 2005-06 National Income and Production

the risks of inflation, posed mainly by the surge inthe price of oil but so far held back by the benefits ofglobalization - points to a favourable externaleconomic environment for the export sectors of thedomestic economy. However, it is the loss of tradepreferences for our two main exports, textiles andsugar, which poses the greatest challenge for theeconomy in the short to medium term and which hasno doubt seriously hit these industries. The sugarindustry, hit by a 36 per cent cut over the next fouryears in the price of sugar exported to the EuropeanUnion, is facing an impending contraction and is setfor a transformation in the medium to long term,with a process of diversification within the sectorunder way. From a macroeconomic managementstandpoint, the surge in oil prices has increased therisks of inflation and the high level of public debt,mainly domestic, continues to be an impediment.

The economy is projected to grow by 4.6 percent in 2006. Exclusive of the sugar sector, thegrowth rate works out to 5.0 per cent. The tourismand financial services sectors are expected to growby 4.8 per cent and 6.7 per cent, respectively, in2006. The agricultural sector, which fell by 5.3 percent in 2005, is expected to post a smallercontraction of 0.5 per cent in 2006. The textilessector is believed to be nearing the end of itsrestructuring and contraction phase and the EPZsector, comprising essentially the textiles andgarments industry, is expected to expand by 1.5 percent in 2006, after a decline of 12.3 per cent in 2005,the first post-preferential market access year.Aggregate consumption expenditure is projected togo up, in real terms, by 5.3 per cent. The savingsrate is forecast to decrease to 15.1 per cent and theratio of GDFCF to GDP at market prices is expected torise to 23.8 per cent.

The government has come up with arestructuring plan for the sugar sector, which will costRs24.5 billion over a period of ten years, but this willyield results at best only in the medium term. Theauthorities are encouraging the production of refined(higher value added) sugar and the use of sideproducts for the production of electricity and ethanolwhile, to reduce costs, they are putting in place aprogram to combine plantations into larger, moreefficient units and to support investment in irrigation.The government is seeking funding for the programfrom various sources, as contributions from the fundset up by the European Union to support countriesaffected by the reform of its sugar regime are likelyto be relatively small. The government has presented

a Multi-Annual Adaptation Strategy – Action Plan2006-15 to the European Union to seek increasedfinancial support for the restructuring of the industry.The plan highlights actions to reduce cost, increaserevenue, optimise use of by-products and alleviatedebt burdens. The aim is to transform the industryinto a cane cluster which includes different types ofsugar, bagasse for electricity generation, andmolasses for production of ethanol and value addedspirits.

As regards the manufacturing sector,restructuring plans for the textiles sector include thestrengthening of operations through improvedbusiness planning and market development andfinancial restructuring, the move to higher-endproducts and, in the context of bilateral tradenegotiations with certain emerging market economies,access for Mauritian textile products to certain high-end segments of their markets. The integration of theEPZ and non-EPZ sectors will be accelerated. Customsduty will be eliminated on all inputs for themanufacturing sector as a whole. This measure isexpected to facilitate outsourcing and the integrationof EPZ firms with enterprises serving the domesticeconomy. The use of the National Equity Fund will bereviewed. Half of the Rs500 million available in theFund will be accessed to provide equity and quasi-equity to assist re-engineering of firms under flexibleterms. The remaining Rs250 million will be used to setup a Second Equity Fund with a minimum fifty percentparticipation of the private sector. This source of fundwill give enterprises that are reengineering improvedease of access to some Rs750 million of finance. Thereis no limit on private sector participation in the SecondEquity Fund in view of leaving the door open for raisingmore funds. To encourage the development of thefinancial market and to facilitate the mobilization ofprivate financing for restructuring, Equity Funds willremain exempt from tax.

The tourism sector has been doing very well,contributing significantly to growth in recent yearsand there is much scope for expansion. The industryhas relied on up-market tourism for this rapidgrowth. The authorities are now putting in place astrategy to rapidly expand the sector to more thandouble its present capacity. The objective is toattract two million tourists by the year 2015. Overthe next ten years, the private sector is expected toinvest in the equivalent of 25,000 rooms that willgenerate direct employment for about 50,000people and indirect employment for about twice thatfigure. Air access is being liberalized so as to

CHAP I-NY2006 12/26/06 3:18 PM Page 25

National Income and Production Annual Report 2005-06

26

expand capacity on existing routes and establishnew air-links in order to tap new markets. In themedium term, the sector will include shopping andconference activities. The Integrated Resort Scheme(IRS) for the construction and sale of luxury villaswith attached amenities looks very promising asshown by the number and scale of projectsapproved and awaiting approval.

Alongside the tourism industry, otherindustries that could help put the economy back onthe path of high and job-creating growth in the shortto medium term are the financial services sector, theInformation and Communication Technology (ICT)sector, and the seafood sector. Prospects for theexpansion of the offshore financial sector also existprovided efforts are made to enhance theattractiveness of the sector, such as establishingbilateral tax agreements with emerging economiesand also ensuring that the required human resourcedevelopment takes place. The ICT sector, whichfocuses on business process outsourcing, softwaredevelopment and call centres, is expected toexperience a steady expansion. To unlock thepotential of the ICT sector to create well paid jobs,government is formulating a National ICT StrategicPlan to spell out its strategy to transform Mauritiusinto a Cyber Island. The sector may not contributesignificantly to growth directly but indirectly byproviding a boost to productivity generally in theeconomy.

Potential for growth also exists in thedevelopment of Mauritius into a regional platform forthe storage, processing and distribution of seafoodand for the repair and maintenance of fishingvessels. While the sector is a relatively new one, thescale and range of projects for which interest isbeing shown point to a huge potential for the sector.

Mauritius has the potential to become a duty-free shopping centre for the Indian Ocean Region.The elimination of customs duties and therationalization of the incentive regime together withthe movement to a low tax platform set the stage forthe development of this sector. The free entry ofhigh net worth IRS owners, investors, skilledprofessionals and retirees and the family and friendslikely to visit them offers a large pool of demand forhigh end shopping. On the supply side, the freeing ofaccess to land for investment purposes andimprovements in the framework for doing business,facilitates the setting up by flagship commercialoperators of a base in Mauritius.

The Empowerment Program is expected toplay an important role in fostering small andmedium-sized enterprises, which would contributesignificantly to growth in the future. The objective isto unlock opportunities for the unemployed, forthose recycled from their jobs, for women, for youngpeople entering the labour force and for small andmedium entrepreneurs. The Programme will alsofacilitate the transition from sugar, textiles and otheractivities hit by shocks, into higher value addedactivities with better paying jobs. It will have a lifespan of 5 years. An item has been created in the2006-07 capital budget for the EmpowermentProgramme with a project value of Rs5 billion, withRs750 million for the next financial year to kick offthe Programme. The Empowerment Programme willundertake seven critical activities, including theprovision of land for social housing and for smallentrepreneurs; setting up a workfare programmeemphasizing training and reskilling and specialprogrammes for unemployed women; the creationof tourist villages; providing assistance foroutsourcing; and supporting the development ofnew entrepreneurs and SMEs. Finance will beprovided in the form of equity participation throughan Empowerment Fund that will become operationalin July 2006. The Empowerment Fund will provideequity of Rs300,000 to Rs3 million.

Government is also investing heavily ineducation infrastructure and in the educationsystem to enhance training and address the skillsneeds of the economy.

CHAP I-NY2006 12/26/06 3:18 PM Page 26

Annual Report 2005-06 Labour Market and Price Developments

27

The decline of the textiles and garmentsindustry and the restructuring of the sugar industryhave exacerbated the unemployment problem inrecent years, the vast majority of the unemployedbeing unskilled and low-skill workers. The loss oftrade preferences in the textiles and sugar industriescoupled with the challenges of globalisation havebrought on a sense of urgency in the restructuring ofthe economy. The labour market is one area that haslong been resistant to reform. The government isnow pushing ahead with labour market reforms inorder to boost competitiveness and help job creation.

The government has announced a revision of labourlaws that would give firms more flexibility in hiringand firing workers. It has also announced the settingup of a National Wages Council for the determinationof wages, replacing the current centralized wage-settlement mechanism by a two tier system thatwould both take into consideration the overallperformance of the economy and provide for firm-level bargaining to take into account firm/sector-specific productivity and performance.

Wage Developments

Average Monthly Earnings

According to the Survey on Employment andEarnings in “Large” establishments carried out by

II. LABOUR MARKET ANDPRICE DEVELOPMENTS

1. Agriculture, Forestry and Fishing 9,334 9,825 10,019 2.0 -2.8

of which: Sugarcane 8,580 9,054 9,202 1.6 -3.1

2. Mining and Quarrying 5,496 5,588 5,744 2.8 -2.0

3. Manufacturing 7,299 7,798 8,202 5.2 0.3

of which: Sugar 11,257 11,284 12,468 10.5 5.3

EPZ products 6,196 6,646 7,006 5.4 0.5

4. Electricity, Gas and Water 18,456 19,457 22,056 13.4 8.1

5. Construction 11,465 12,042 13,047 8.3 3.3

6. Wholesale & Retail Trade; Repair of Motor Vehicles, 12,032 12,772 13,547 6.1 1.1Motorcycles, Personal and Household Goods

of which: Wholesale & Retail Trade 12,044 12,776 13,500 5.7 0.7

7. Hotels and Restaurants 8,947 9,881 10,560 6.9 1.9

8. Transport, Storage and Communication 15,189 15,982 16,664 4.3 -0.6

9. Financial Intermediation 20,225 21,478 22,692 5.7 0.7

of which: Insurance 17,357 19,293 19,536 1.3 -3.5

10. Real Estate, Renting and Business Activities 12,003 12,822 13,447 4.9 0.0

11. Public Administration and Defence; Compulsory Social Security 13,960 15,056 14,529 -3.5 -8.0

12. Education 13,993 15,096 16,216 7.4 2.4

13. Health and Social Work 15,134 16,628 17,283 3.9 -0.9

14. Other Services 10,846 11,427 12,298 7.6 2.6

Total 11,103 12,061 12,625 4.7 -0.2

Table II.1: Average Monthly Earnings1 in Large Establishments

Industrial Group Mar-04 2

Mar-052

Mar-06 3

% Nominal % ChangeChange Adjustedbetween for Increase Mar-05 in Price

and Mar-06 Level(Rs) (Rs) (Rs)

1 Earnings of daily, hourly and piece rate workers have been converted to a monthly basis. 2 Revised. 3 Provisional.Source: Central Statistics Office, Government of Mauritius.

CHAP.II-LABOUR 2006 12/26/06 3:21 PM Page 27

Labour Market and Price Developments Annual Report 2005-06

28

the Central Statistics Office (CSO), the averagemonthly earnings for all industrial groups increasedfrom Rs12,061 to Rs12,625, or 4.7 per cent,between March 2005 and March 2006 compared to8.6 per cent between March 2004 and March 2005.Adjusted for the twelve-month running inflationrate, the average monthly earnings for all industrialgroups registered a marginal contraction of 0.2 percent between March 2005 and March 2006 asagainst a growth of 3.3 per cent rise between March2004 and March 2005.

An analysis by industrial group shows thataverage monthly earnings grew in the range of 1.3per cent to 13.4 per cent between March 2005 andMarch 2006. The highest increase in averagemonthly earnings occurred in “Electricity, Gas andWater” (13.4 per cent) followed by “Construction”(8.3 per cent), “Other Services” (7.6 per cent) and“Education” (7.4 per cent). Average monthlyearnings in the “Public Administration and Defence;Compulsory Social Security” sector registered acontraction of 3.5 per cent between March 2005 andMarch 2006. The remaining sectors recordedincreases in average earnings in the range of 1.3 percent to 6.9 per cent.

Table II.1 shows the average monthlyearnings in large establishments by industrial groupover the period March 2004 through March 2006.

Compensation of Employees

Compensation of employees went up, innominal terms, from Rs63,790 million in 2004 toRs68,064 million in 2005, or by 6.7 per cent,compared to an increase of 8.7 per cent in 2004.Compensation of employees as a percentage of GDPat basic prices remained unchanged at 41.9 per centin 2005. Compensation of employees in the GeneralGovernment sector, which accounts for around 26per cent of total compensation, grew, in nominalterms, by 7.0 per cent in 2005 compared to 12.9 percent in 2004, while for the rest of the economy, itincreased by 6.3 per cent in 2005 compared to 7.3per cent in 2004.

Cost of Living Compensation

During the fiscal year 2005-06, a cost of livingcompensation of 5.0 per cent was awarded toemployees receiving a monthly salary of up toRs2,700 and Rs135 to those earning aboveRs2,700. This wage increase is estimated to costthe public sector an amount of Rs590 million andthe private sector a total of Rs855 million.Following an appeal by the Deputy Prime Minister,Minister of Finance and Economic Development,some companies that are financially profitable andoperating in economic sectors such as the financialand hotel sectors were prepared to award their

1. Agriculture and Fishing 7.1 4.9

2. Manufacturing, Mining and Quarrying 6.0 5.5

3. Electricity and Water 5.4 6.2

4. Construction 2.7 7.1