CONTENTS 1. Notice 2. Directors’ Report 3. Report on Corporate Governance 4. BASEL Disclosures 5. Auditor’s Report 6. Balance Sheet 7. Profit & Loss Account 8. Schedules 9. Principal Accounting Policies 10. Notes on Accounts

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

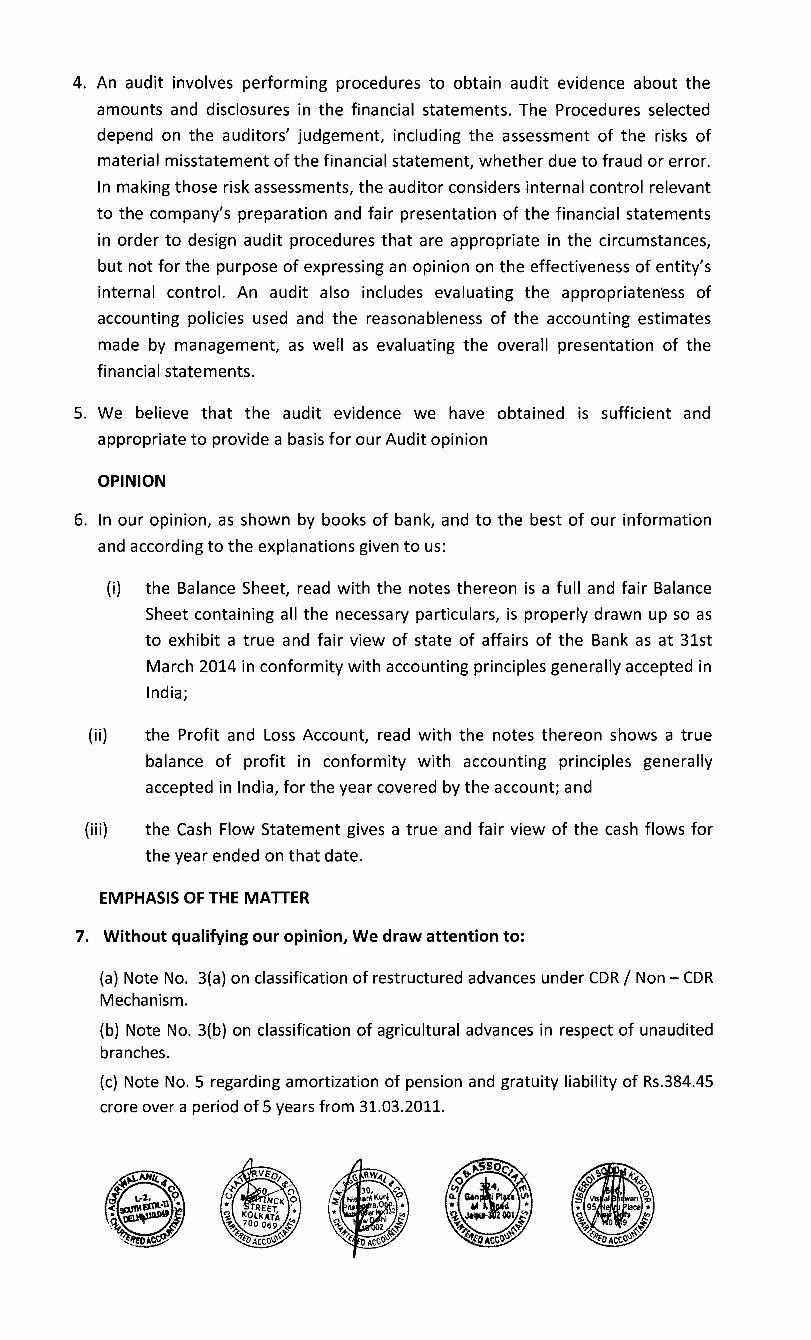

CONTENTS

1. Notice

2. Directors’ Report

3. Report on Corporate Governance

4. BASEL Disclosures

5. Auditor’s Report

6. Balance Sheet

7. Profit & Loss Account

8. Schedules

9. Principal Accounting Policies

10. Notes on Accounts

NOTICE OF AGM AND BOOK CLOSURE

NOTICE is hereby given that the Fifty-third

Annual General Meeting of the Shareholders of

State Bank of Bikaner and Jaipur will be held

in the Maharana Pratap Auditorium, Bharatiya

Vidya Bhavan, K. M. Munshi Marg, Opp.

O.T.S., Jaipur - 302015 on Monday, the 2nd

June, 2014 at 11.30 a.m. (Indian Standard

Time) instead of Wednesday, the 28th May,

2014 at 12.00 noon, as notified earlier, to

discuss and adopt the Balance Sheet and Profit

& Loss Account of the Bank, the report of the

Board of Directors on the working and

activities of the Bank and the Auditors' Report

on the Balance Sheet and Accounts for the

period 1st April, 2013 to 31st March, 2014.

The register of shareholders of the Bank shall

remain closed from Monday, the 26th May,

2014 to Sunday, the 1st June, 2014 (both

days inclusive) instead of from Wednesday,

the 21st May, 2014 to Tuesday, the 27th May,

2014, for the purpose of Annual General

Meeting for the year ended 31st March, 2014.

एतद्दद्दवाया सचूना दी जाती है कि स्टेट फैंि ऑप फीिानेय एण्ड जमऩयु िे अशंधायिों िी 5 3वीं वार्षिि साधायण सबा, भहायाणा प्रताऩ ऑडडटोरयमभ, बायतीम र्वद्दमा बवन, िे.एभ.भुशंी भार्ि, ओ.टी.एस. िे साभने, जमऩयु भें, ऩवूि ननधािरयत नतथथ फधुवाय ददनांि 28 भई, 2014 िो दोऩहय 12 फजे िे स्थान ऩय, सोमवार दिनाांक 2 जून, 2014 को प्रात:11.30 बजे (बायतीम भानि सभम) आमोजजत िी जामेर्ी, जजसभें 1 अप्रेर 2013 से 31 भाचि, 2014 ति िी अवथध िे तरुन-ऩत्र एव ंराब औय हानन खाता, इसी अवथध भें फैंि िे िामिियण एव ंकिमािराऩों ऩय ननदेशि भण्डर िे प्रनतवेदन तथा तरुन-ऩत्र व रेखों िे सम्फन्ध भें सऩंयीऺिों िे प्रनतवेदन ऩय र्वचाय िय ऩारयत किमा जामेर्ा।

फैंि िे अशंधायिों िा यजजस्टय फधुवाय, ददनांि 21 भई, 2014 से भरं्रवाय, ददनांि 27 भई, 2014 ति, िे स्थान ऩय सोमवार, दिनाांक 26 मई, 2014 से रवववार, दिनाांक 1 जून, 2014 तक (दोनो ददन मभरािय), 31 भाचि, 2014 िो सभाप्त वषि िी वार्षिि साधायण सबा हेत ुफन्द यहेर्ा।

1

REPORT OF THE BOARD OF DIRECTORS TO THE STATE BANK OF INDIA,

THE RESERVE BANK OF INDIA AND THE GOVERNMENT OF INDIA IN

TERMS OF SECTION 43(1) OF THE STATE BANK OF INDIA (SUBSIDIARY

BANKS) ACT 1959.

PERIOD COVERED BY REPORT: 1ST

APRIL 2013 TO 31ST

MARCH 2014.

The Board of Directors of State Bank of Bikaner and Jaipur have pleasure in presenting

this Annual Report together with the audited Balance Sheet and Profit and Loss Account

of the Bank for the year ended 31st March 2014.

MANAGEMENT DISCUSSION AND ANALYSIS

ECONOMIC SCENARIO

Global Economy:

The financial year 2013-14 has been a challenging year for the global economy put

together. Although the global economic turmoil, which shook US in 2008-09 and slowly

spread into Europe has not yet subsided completely, the recovery signals are very much

visible. While the sub-prime impact has gone off-screen in US, the European slowdown

is also slowly pulling through. Global growth is projected to be slightly higher, at around

3.7 percent in 2014 and rising to 3.9 percent in 2015. However, downward revisions to

growth forecasts in some economies highlight continued fragilities, and downside risks

do still remain.

Growth in United States is expected to be 2.8% in 2014, up from 1.9% in 2013. The Euro

area is turning the corner from recession to recovery and is projected to improve to 1

percent in 2014 and further strengthen to 1.4% in 2015.

The overall growth in emerging market and developing economies is expected to increase

to 5.1% in 2014 and to 5.4% in 2015. Growth in China which rebounded strongly in the

second half of 2013, largely due to acceleration in investment, is expected to be

temporary and may moderate slightly to around 7.5% in 2014-15.

In most of the emerging markets and developing economies, while domestic weaknesses

do remain a concern, stronger external demand from advanced economies has, to some

extent, lifted growth. While some economies may have room for monetary policy

support, output is close to potential in others, suggesting that growth declines partly

reflect structural factors or a cyclical cooling and that the main policy approach for

raising growth must be to push ahead with structural reform.

Indian Economy:

On the domestic front, the economy has continued to register below 5% growth mark

successively for five quarters in a row with 4.7% in GDP in the third quarter of 2013-14.

The growth in the second and third quarter of FY 2013-14 was also due to better

agriculture numbers. The negative growth under manufacturing continued to exert

2

pressure on the overall GDP numbers. The index of industrial production for most part of

the year remained under strain, thereby dampening the growth prospects. As such the

indicators do not point towards any sustained revival in the industry and services sector.

However, there were signs of relief on the inflation front. The WPI started easing towards

the end of the FY 2013-14 with easing observed in the CPI numbers as well which also

helped the interest rates to ease a little. As against the RBI‟s glide path of inflation (CPI)

touching 8% by Jan‟15, the CPI inflation eased to 8.1% in February. However, with the

hardening of prices, the inflation may again rise, albeit not as much as previous year.

Exports, which picked up to double digit growth from July to Oct 2013 on falling rupee

value, slowed to 3.67% in Feb‟14 due to slowdown in demand in partner countries and

softening of prices of exports of petroleum products and gems and jewellery.

RBI, in its first bi-monthly review of 2014-15, has estimated GDP growth in the range of

5 to 6%, with downward risks to the central estimate of 5.5%. The end of the financial

year saw Sensex touching new highs on the back of huge FII inflows in the country.

Banking Industry:

The Banking Industry growth points toward the growth pattern of the economy as well.

As against the projected aggregate deposit and non-food credit growth of 14% and 15%

respectively, the banking industry, as at 21st Mar‟14, registered a growth of 14.6% and

14.3% respectively. While the deposit growth surpassed the RBI‟s projections, the credit

growth projections could not be achieved which reflect the low credit off-take and

eventually the falling investments in the economy. The asset quality concerns continued

to build up, because of the overall trade and demand slowdown. The increase in the

benchmark interest rates towards the second half of the year alongwith other liquidity

tightening measures targeted to bring inflation under control had their own impact on the

corporate credit pick-up, which already was suffering from the demand slowdown. The

interest rates, however, seem to have peaked and may see some easing, owing to the fall

in the inflation levels. The performance of the banking industry may also improve in the

coming quarters due to an expected revival in country‟s economic and industrial growth,

which may also help in controlling the NPAs and a decline in fresh slippages.

RAJASTHAN ECONOMY

Rajasthan is one of the emerging states in the Indian eco-system. Rajasthan economy

though primarily agricultural and pastoral, is rising fast on the industrial map of the

country. As an investment destination, Rajasthan ranks 3rd among all states in terms of

investment proposals. Multinationals are looking at Rajasthan as a potential investment

destination. The NCR areas of Rajasthan are now buzzing with automobile and

manufacturing companies creating forward linkages to spur growth of small business

units in the region. Rajasthan is pre-eminent in quarrying and mining in India. The state

3

is the second largest source of cement. It is rich in salt deposits, copper and zinc.

Rajasthan is going to be benefitted by the proposed Delhi Mumbai freight corridor in a

big way. The proposed oil refinery at Barmer, which has been formally inaugurated on

22nd

Sep‟13, and discovery of huge copper resource in Alwar district will add to the

state‟s prospects of becoming new industrial investment hub. The Oil discovery in

Rajasthan by Cairn India has already brought Rajasthan on the world map of Oil and Gas

exploration.

Textile is another segment which, besides other industries, contributes a lot to Rajasthan

as well as Indian economy. The textile sector contributes about 4% to GDP of the

country.

Endowed with natural beauty and a great history, tourism is flourishing in Rajasthan with

places like Jaipur, Udaipur, Jodhpur & Jaisalmer always buzzing with tourists. The

healthy and growing tourism industry has been the source of growth of the local

handicrafts and jewellary industry. Tourism provides a big boost to the economy of

Rajasthan.

DEVELOPMENTS IN THE FINANCIAL SECTOR

The year 2013-14 has been a period of increased burden of stressed assets for PSBs with

total growth of 39% in Gross NPAs upto Dec‟13 and 51% growth in Net NPAs.

Growth slowdown, persistent inflation and the twin deficit risks, that were increasing

rapidly in 2012-13, gave some respite in the current fiscal with CAD expected to be less

than 2% of GDP, GDP expected to be growing at 5.5% in last quarter of the current fiscal

and a control on inflation. Export growth in FY 2013-14 surged high and imports saw a

negative growth, owing to a declining rupee and measures to curb unproductive imports.

This has given way to CAD to be contained within the budgetary level.

Monetary Policy:

With inflation at current levels still considered to be sticky if the food and fuel prices

were to be removed, the RBI Governor, in the First Bi-monthly Monetary Policy

statement for 2014-15, has as a cautious stance, maintained status quo in the rates.

Some of the important key monetary policy features are:

The GDP growth estimate is expected to be in the range of 5 to 6%, with downside

risks.

Banks have been asked not to levy penal charges for non-maintenance of minimum

balances in saving deposit, both operative as well as inoperative accounts.

The recommendations of the Expert Committee to Revise and Strengthen the

Monetary Policy Framework (Chairman: Dr. Urjit R. Patel) have been implemented,

including adoption of the new CPI (combined) as the key measure of inflation, explicit

recognition of the glide path for disinflation and transition to a bi-monthly monetary

policy cycle,

4

As the liquidity coverage ratio (LCR) stipulated by the Basel Committee becomes a

standard with effect from January 1, 2015, it is proposed to issue guidelines relating to

Basel III LCR and Liquidity Risk Monitoring tools by end-May 2014.

Following industry-wide concerns about asset quality and the consequential impact on

the performance/profitability of banks, the Reserve Bank has further extended the

transitional period for full implementation of Basel III Capital Regulations in India

from as on March 31, 2018 to as on March 31, 2019.

Interim Budget:

This being an election year, the Government had presented the interim budget for the FY

2014-15. The Budget has estimated a GDP growth of 4.9% for the FY 2013-14. The

fiscal deficit for 2013-14 is projected to be contained at 4.6% while fiscal Deficit in

2014-15 is estimated at 4.1%, which will be below the target set by new Fiscal

Consolidation Path and Revenue Deficit is estimated at 3.0%. Foreign exchange reserve

to grow by USD 15 billion in this Financial Year.

The savings rate and investment rate of the economy is estimated at 30.1% and 34.8%

respectively in 2012-13. To boost investment, the Government has set up a Cabinet

Committee on investment and Project Monitoring Group. By end of January 2014,

Projects numbering 296 with an estimated project cost of `660,000 crore had been

cleared.

Gross market borrowing for 2014-15 is kept at `5.97 trillion with net borrowings at `4.57

trillion. The plan is to buy back/switch bonds of `500 billion in 2014-15, Debt repayment

in 2014-15 is seen at `1.397 trillion and Interest payments are seen rising to `4.27 trillion

in 2014-15 from a revised estimate of `3.8 trillion for the current fiscal year. The plan

expenditure for 2014-15 is kept at `5.55 trillion, the same level as the previous fiscal

year, while non plan spending is estimated at about `12.08 trillion. The Government

would be providing `112 billion of capital infusion in state runs banks in 2014-15.

CORPORATE OPERATIONS

BUSINESS PERFORMANCE

The overall business of the Bank (deposits plus gross advances) reached a level of

`139207 crore as at end-March 2014 as against `130590 crore as at end-March 2013,

recording a growth of `8617 crore (6.60%). The total deposit increased by `1759 crore

(2.44%) to reach a level of `73875 crore while advances increased by `6858 crore

(11.73%) to reach a level of `65332 crore by end-March 2014. The cost of deposits of the

Bank decreased from 7.13% in 2012-13 to 7.04% in 2013-14, while yield on advances

decrease from 11.64% to 11.27%.

5

TREASURY AND INVESTMENTS

The year opened with softening of yields in bonds with 10 year benchmark sovereign

bond yield easing between 7.25% to 7.90% during the period April 2013 to mid July

2013, giving opportunity to dealers to book good profit. However, the second half of July

2013 and the rest of the year saw yields spiralling upwards, on a series of monetary

tightening steps initiated by the RBI to contain the fall of ` against the U.S. $. The 10

year benchmark yield touched a high of 9.48% during the year, before closing at 8.80%

on March 28, 2014. The Bank booked arbitrage profit whenever there arose an

opportunity due to difference in domestic and forex interest rates.

The stock market remained largely in the green territory during the first quarter, as a

result of various reform measures taken by the government and continued FII inflows.

During the second quarter, the market plunged due to several liquidity tightening

measures taken by RBI to strengthen the weakening ` against the U.S. $. The negative

sentiment accentuated further due to lower GDP growth, falling IIP and high inflation. In

the latter half of the year, the market showed strength and towards the end of the year

rallied to its level of an all time high on account of strengthening `, falling inflation and

pre election sentiments. During the year, Bank participated in Initial Public Offers/Offer

for Sale of companies with proven record/sound fundamentals and also undertook trading

in the secondary market to maximize returns.

The Bank‟s gross investments were `21287 crore as on 31st March 2014 as against

`20163 crore in the previous year while net investments (after netting repo and provision

for depreciation amounts) stood at ` 17750 crore as aginast `20146 crore in the previous

year. Profit for the year 2013-14 was `138.63 crore as against a profit of `75.55 crore for

the year 2012-13 thereby registering an increase of 83.49%. The yield on investments,

excluding profits, improved from 7.64% in 2012-13 to 7.83% in 2013-14. The yield on

investment including profit improved from 8.04% to 8.53% during the same period.

FINANCIAL HIGHLIGHTS

NET INTEREST INCOME

The Bank's total interest income increased from `7498.19 crore during 2012-13 to

`8168.56 crore during 2013-14, recording a growth of 8.94%. Interest expenditure

6

increased by 8.36% to `5344.78 crore, as against `4932.38 crore in the previous year.

The net interest income recorded a growth of 10.05% to `2823.78 crore, as against

`2565.81 crore in 2012-13. The net interest margin remained same at the last years level

of 3.62%.

NON-INTEREST INCOME

The non-interest income of the Bank has increased by 20.66% from `726.28 crore in

2012-13 to `876.34 crore during 2013-14. The increase during the year as compared to

the last year is mainly on account of increase in profit on sale of Investment by `63.08

and recovery in Written-off accounts by `38.57 crore.

OPERATING EXPENSES

The operating expenses recorded a growth of 26.99% from `1579.22 crore in 2012-13 to

`2005.46 crore during 2013-14. Of this, employee costs increased by 31.20% to

`1295.64 crore, while total other operating expenditure increased by 19.96% to `709.82

crore.

PROFIT

During 2013-14, the operating profit decreased to `1694.66 crore, (by -1.06%) as against

`1712.87 crore in the previous year. The net profit recorded a growth of 0.20% from

`730.24 crore in 2012-13 to `731.69 crore in 2013-14.

DIVIDEND

During the year 2013-14, the Bank declared an Interim Dividend of 143% i.e. `14.30 per

equity share (face value of share `10/- per share). Record date for ascertainment of

entitlement of shareholders for Interim Dividend was 31st March, 2014. Interim Dividend

may be treated as final dividend.

KEY FINANCIAL INDICATORS

The Return on Assets of the Bank stood at 0.87% during 2013-14 as against 0.96% in the

previous year. The return on equity decreased to 13.66% as against 15.33% in the

previous year. The earnings per share increased from `104.32 in 2012-13 to `104.53 in

2013-14, while the book value per share improved from `678.74 in 2012-13 to `765.13

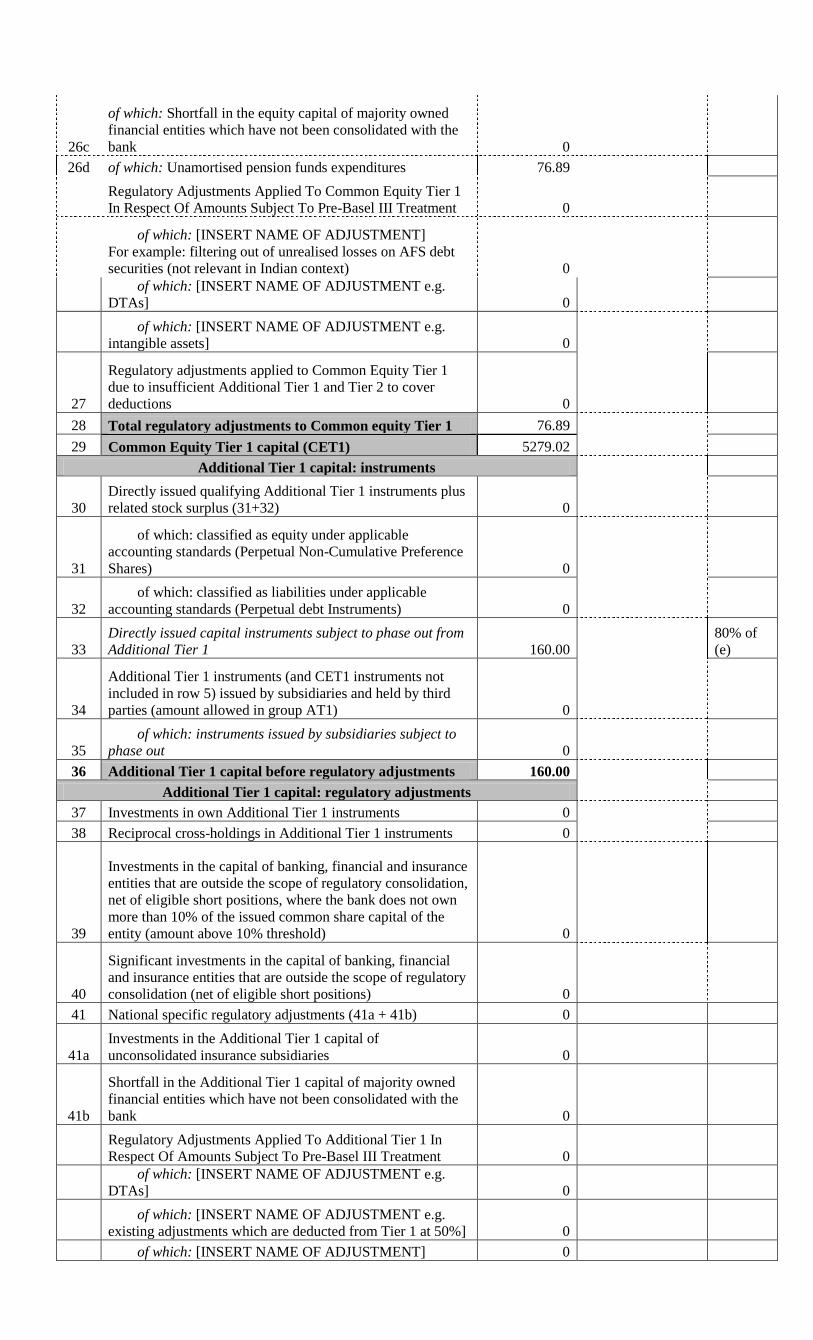

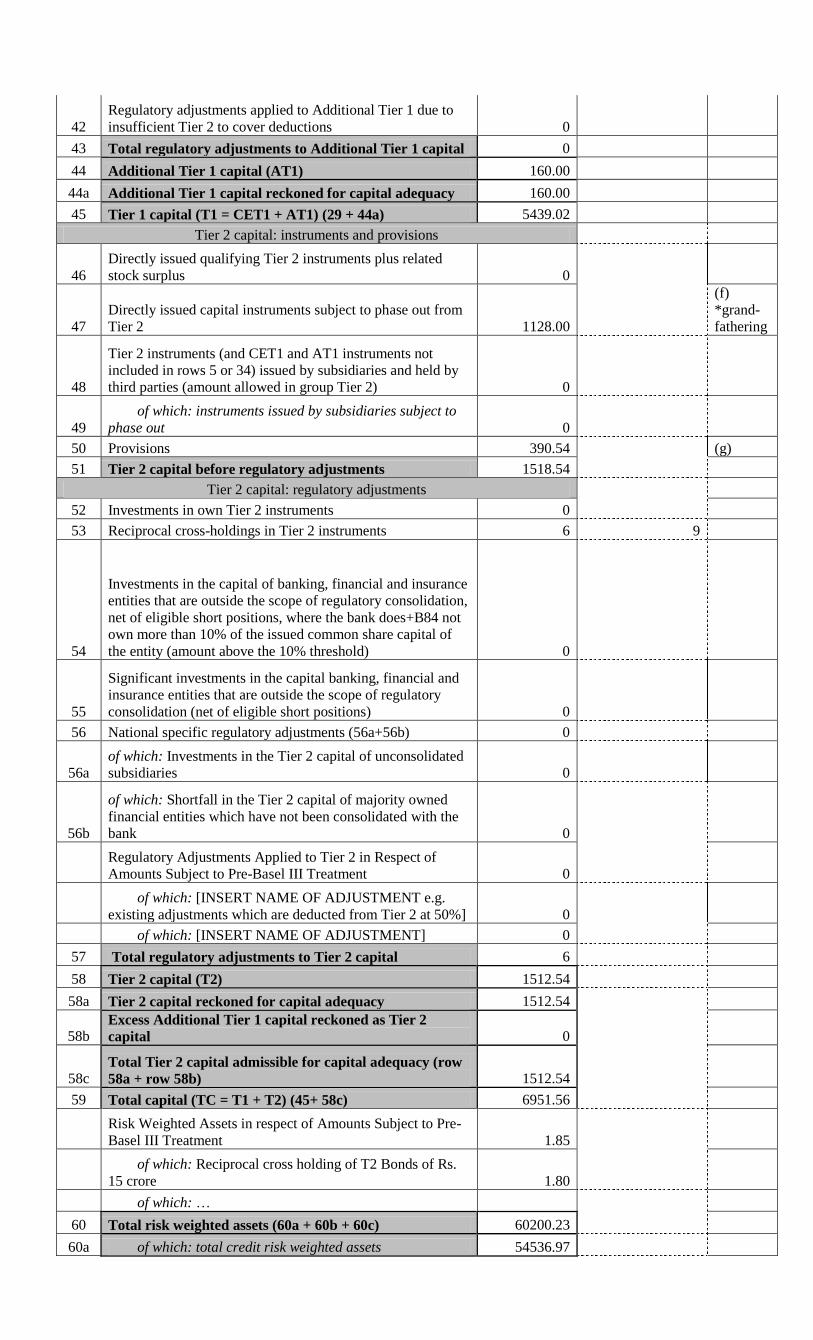

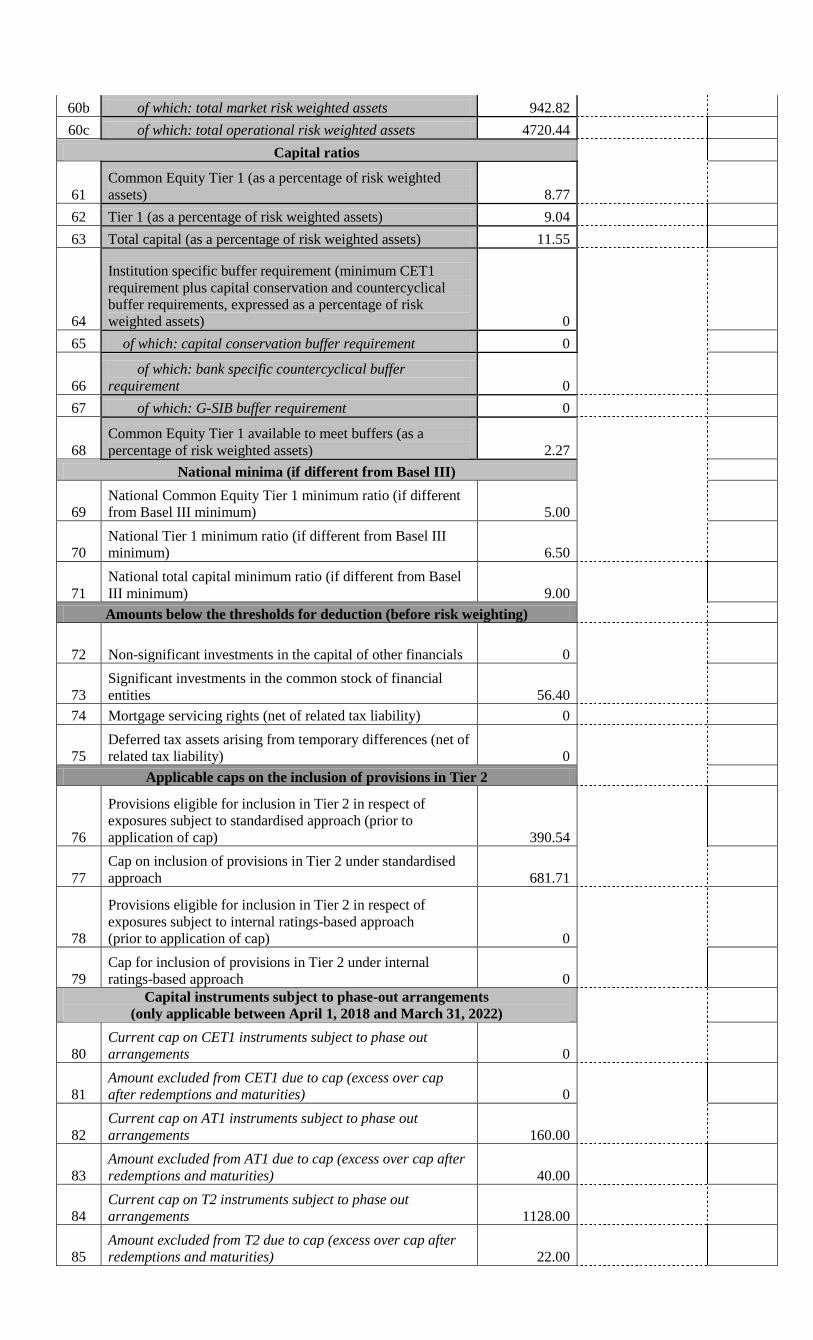

in 2013-14. As at end-March 2014, the capital adequacy ratio of the Bank stood at

11.71% and 11.55% as per Basel II and III norms respectively, as against 12.16% as per

Basel II norms respectively, as at end-March 2013. This was well above the RBI

benchmark of 9%. Due to rise in NPAs on account of continued stress faced by the

industrial sector coupled with agriculture NPAs, the Bank's Gross NPA ratio and Net

NPA ratio increased from 3.62% and 2.27% respectively as at end-March 2013 to 4.18%

and 2.76% respectively, as at end-March 2014. The average business per employee

7

increased to `977 lakh in 2013-14, as against `900 lakh in the previous year. The net

profit per employee decreased to `5.62 lakh in 2013-14, compared to `5.91 lakh during

2012-13. The average business per branch increased to `116.52 crore during 2013-14, as

against `112.42 crore in the previous year.

CREDIT MANAGEMENT

The overall credit demand remained muted during the FY 2013-14, with GDP growth in

sub 5 % range due to overall slowdown in the economy leading to a lower level of

investment activity. However, the Bank continued to focus on qualitative credit growth

and faster credit delivery. Total advances of the Bank grew by 11.72% during 2013-14,

as against growth of 16.98% during 2012-13.

The Bank‟s Commercial & Institutional (C&I) segment advances (other than food credit)

during the FY 2013-14 grew by 9.40% with an increase of ` 3099.00 crore over FY

2012-13, whereas non C&I segment comprising personal, small & micro enterprises and

agricultural advances grew by ` 2907.42 crore (11.50%).

Against the backdrop of stress in the various segments of the industry, the impetus of

financing remained mainly towards top rated PSUs and other sectors such as Real Estate

(RH), textiles and NBFCs etc.

In view of the prevailing competitive and stretched market scenario, closer interaction

and regular meetings by the Top Management with high value customers were held at

major centers in the country which resulted in booking several good advances.

PERSONAL BANKING

Deposits under Personal Segment grew from `41,905 Cr as on 31st March 2013 to

`46,726 Cr as on 31st March 2014, thus recording a growth of 11.50%.

Acquisition of new customers

Acquisition of new customers was the prime focus of the Bank during the year to

augment its retail deposit base. We could open 24.97 lakh new savings Bank

accounts during the year which accounts 23.46% of the base level. The resources

mobilized in the savings bank portfolio was `3,617 Crores, which helped the Bank to

improve its CASA deposits.

55% of the new accounts are opened by either students or youth which reflect the

penetration to the younger age groups of the population.

Nearly 73% of the total deposit in the newly opened accounts are contributed by youth

and Middle aged customers ranging from 20 years to 60 years which shows the

effective linkage to salaried/ Income earning segments of the society.

8

Mahalakhpati Campaign

To encourage the habit of regular monthly savings among customers, we have made

our recurring deposit scheme popular through a special campaign called Mahalakhpati

RD Campaign. The campaign was focused on the opening of high value recurring deposit

with a maturity value of `10 lakh and above. We could mobilize 27,397 new Millionaire

Recurring Deposit accounts during the two months of the campaign. We could open

70,084 Recurring Deposit accounts during the year.

SBBJ Vaibhav & SBBJ Dhanshakti

We could mobilize `1,190 Cr in a specially designed term deposit/product called SBBJ

Vaibhav launched during the year. SBBJ Dhanshakti another deposit product for short

term deposit has mobilized `104.74 Crores during the year.

Personal Finance

The Personal finance portfolio has crossed a landmark of `10,000 Cr during the

financial year 2013-14. The Bank continued to be active in catering the credit

requirements of P segment customers mainly by way of Home Loans, Car Loans,

Education Loans and Personal Loans. The advances under the personal segment rose to a

level of `10,295 Cr as at Mar 2014 from `9,131 Cr as at the end of March 2013.

During the year under review 7,631 home loans aggregating to `816 Crore were

granted, taking the outstanding home loan level to `3,768

Crores as on 31.03.2014. Similarly 14,507 Car Loans aggregating `648 Cr were

granted during the same period taking outstanding car loan level to `1,452 Cr as on

31.03.2014. We could disburse 37,741 Personal loans aggregating `1,116 Cr during

the same period.

As in the previous years, the Bank contributed to support the younger generation to

pursue higher studies by extending Education Loan. To support the efforts of

Government of India to boost the sentiments of retail/consumer durable segments,

Bank has introduced a new scheme for financing of Consumer Durables during the

year. The other retail segment products like Max Gain Scheme, Rent Plus and Home

Cash have been revamped during the year to make them more customer/market

friendly.

PRIORITY SECTOR LENDING(PSL)

Priority Sector Lending is the major thrust area of the Bank's operations. As at the end of

March, 2014, the Bank's priority sector advances increased to a level of `23662 crore as

compared to `20807 Crore in the previous year i.e. growth of 13.72% over March 2013.

The PSL constituted 40.73% of the Adjusted Net Bank Credit, against the RBI

benchmark of 40%. However, Priority Sector Lending in Rajasthan stood higher at

66.40% of Rajasthan's ANBC.

9

AGRICULTURE

Lending to agriculture remains one of the major thrust areas of the Bank. The outstanding

level of agriculture advance increased from `9188 crore as at the end of March 2013 to

`10982 crore as at the end of March 2014, a growth of 19.52%. Our Bank‟s total direct

agriculture lending is 99.35% of total Agriculture advances amounting to `10911 crore, and

has registered a growth of ` 2658.90 crore during the Financial Year under review. The

flow of credit to agriculture stood at ` 7644 crore against the annual target of `3500 crore

during the current financial year. Agriculture advance constituted 18.90% of the Adjusted

Net Bank Credit (ANBC), against RBI benchmark of 18%. In the State of Rajasthan, it is

even higher at 37.2% of ANBC for Rajasthan State.

The Bank has issued 109933 Kisan Credit Cards (KCCs) with sanctioned limits of `2302

crore during the financial year 2013-14. The total number of KCC stood at 600317 as at end

of March 2014.

FINANCIAL INCLUSION (FI)

In the first phase our Bank was allocated 829 villages with population above 2000.

Accordingly 794 USBs (Ultra Small Branches) were established using PoS technology

and BCs/BCAs were engaged covering 823 villages and in the remaining 6 villages Brick

and Mortar branches were opened. In the second phase of FI (2013-16) our Bank has

been allocated 7588 villages with population below 2000 in 1878 Gram Panchayats

which are to be covered by engaging BCs and / or opening of branches by 31.03.2016.

During the current Financial Year i.e. 2013-14 we have been allocated target to cover

1067 villages and we have covered 1070 villages by 31.03.2014.

The KIOSK Banking Software developed by M/s TCS Ltd. and provided by SBI has

been rolled out in our Bank. Our Bank has entered into agreement with M/s CSC E-

Governance Services India Limited on 07.01.2013 and with M/s. FIA Technology

Services Pvt. Ltd. (a Corpoprate BC) on 20.11.2013 for providing the BC service. M/s

CMS Computers Ltd. which is a Service Centre Agency (SCA) of M/s. CSC e-

Governance Services India Ltd. has been allotted 19 districts in Rajasthan for engaging

CSCs as BCAs in the Gram Panchayats allocated to our Bank. Pali and Barmer districts

have been allotted to M/s FIA Technology Services Pvt. Ltd. for engaging their BCAs. In

the remaining 12 districts our existing Corporate BCs namely Lupin Human Welfare &

Research Foundation Samiti / P2P Microfinance and Allied Services or Individual BCs

will continue to provide banking services.

Aadhaar Seeding and mapping on NPCI Portal: Our Bank has successfully

implemented Aadhaar based payment system (APBS/NACH) through National Payment

Corporation of India (NPCI) gateway. Seeding of Aadhaar Number in CBS account is

10

under progress. We have seeded 625759 accounts with Aadhaar of which 616746

Aadhaars have been uploaded on NPCI Portal.

Direct Benefit Transfer:

DBT has been rolled out in 121 districts across the country of which 6 districts are in the

State of Rajasthan and SBBJ is Lead Bank in two DBT districts i.e. Udaipur and Pali. In

both the districts banks have opened accounts of all the befeciaries as per the list received

from District Authorities.

MICRO, SMALL AND MEDIUM ENTERPRISES (MSMEs)

The Micro, Small and Medium enterprises (MSME), is crucial to the Indian Economy.

There are 3 crore enterprises in various industries, employing approx 7 crore persons.

Together, these account for 45% of the industrial output and 40% of the exports. This

sector is contributing approx.11% per annum to India‟s GDP and is critical for the over

all GDP growth. RBI has also emphasized to adopt suitable strategies for higher lending

to MSMEs. Accordingly, our Bank has also given high priority to this area.

We have arranged MSME customers meet at Jaipur, Alwar, Bhiwadi, Udaipur.

Chittorgarh & Bikaner centres. We have also sensitized our operating officials by way of

training & seminar etc.

The Bank has assisted 21156 new MSME units during the year 2013-14. In order to boost

MSME advances, the Bank has modified its existing MSE loan schemes to make them

most competitive.

The Bank has continued its thrust to provide collateral free loans to MSMEs under the

credit guarantee scheme of CGTMSE. During the year (April 13 to March, 14), Bank

provided new collateral free loans under Credit Guarantee Scheme of CGTMSE to MSE

units amounting to `119.11 crore, taking the CGTMSE cover accounts (cumulative) at

`405.40 Crore as at the end of March 2014.

LOANS TO WOMEN BENEFICIARIES:

The Bank finance as on 31st March, 2014 to women beneficiary has increased to

`3181.21 Crore in 212925 accounts against `2732.87 crore in 204680 accounts as on

March 2013, registering a growth of ` 448.34 crore. This constitutes 5.48 % of ANBC

against the Bench Mark of 5 %.

ASSISTANCE TO MINORITY COMMUNITIES, WEAKER SECTIONS AND

SCHEDULED CASTES / SCHEDULED TRIBES

As at end March 2014, assistance to minority communities stood at `2960.73 crore

spread over 101591 accounts.

Financing to weaker sections stood at `10998.90 crore benefiting 1014090 persons as at

the end of March, 2014. The assistance to weaker sections as a percentage of Adjusted

11

Net Bank Credit is 18.93% as at end March, 2014. This is well above the benchmark of

10% prescribed by RBI.

The outstanding assistance towards Scheduled Castes (SCs)/Scheduled Tribes (STs)

stood at `3070.27 crore in 258602 accounts under priority sector as on 31st March, 2014.

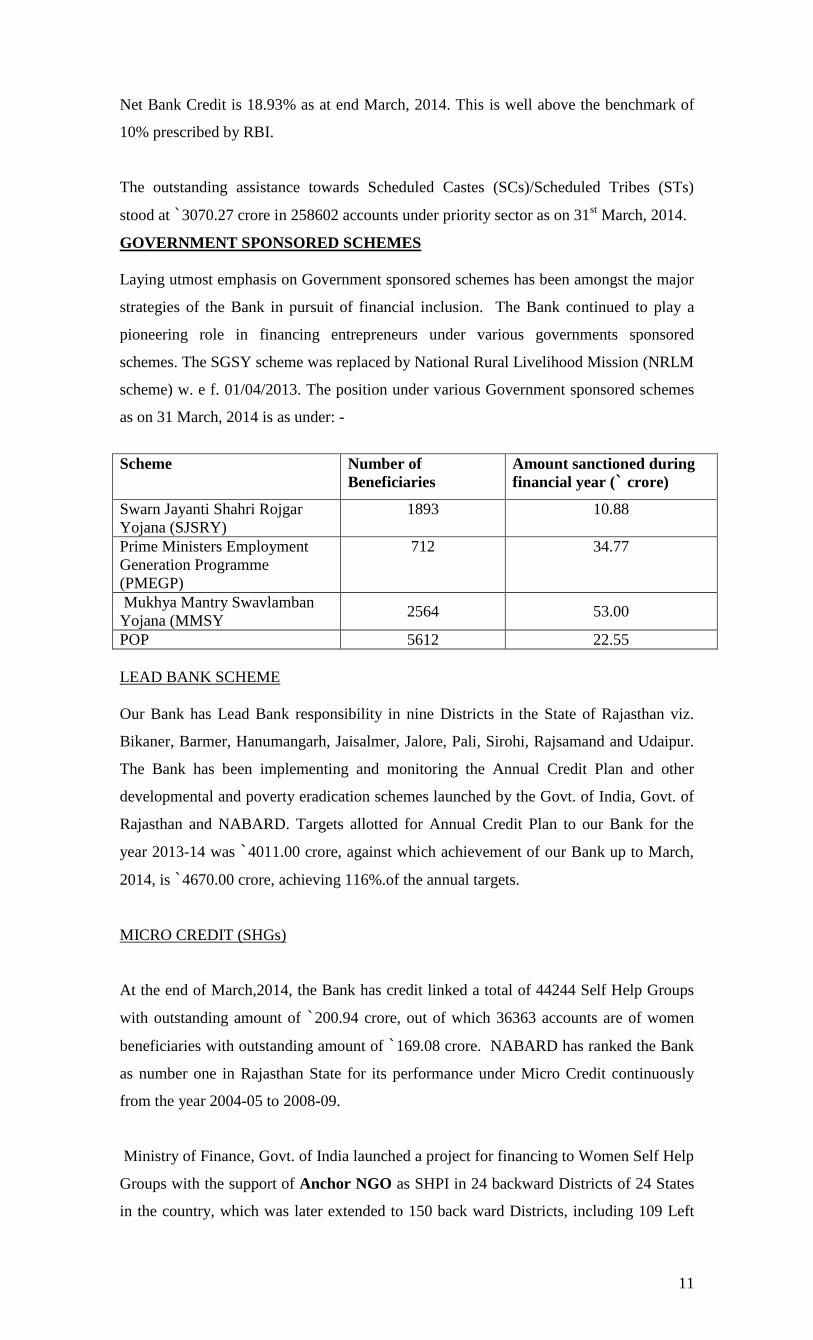

GOVERNMENT SPONSORED SCHEMES

Laying utmost emphasis on Government sponsored schemes has been amongst the major

strategies of the Bank in pursuit of financial inclusion. The Bank continued to play a

pioneering role in financing entrepreneurs under various governments sponsored

schemes. The SGSY scheme was replaced by National Rural Livelihood Mission (NRLM

scheme) w. e f. 01/04/2013. The position under various Government sponsored schemes

as on 31 March, 2014 is as under: -

Scheme Number of

Beneficiaries

Amount sanctioned during

financial year (` crore)

Swarn Jayanti Shahri Rojgar

Yojana (SJSRY)

1893 10.88

Prime Ministers Employment

Generation Programme

(PMEGP)

712 34.77

Mukhya Mantry Swavlamban

Yojana (MMSY 2564 53.00

POP 5612 22.55

LEAD BANK SCHEME

Our Bank has Lead Bank responsibility in nine Districts in the State of Rajasthan viz.

Bikaner, Barmer, Hanumangarh, Jaisalmer, Jalore, Pali, Sirohi, Rajsamand and Udaipur.

The Bank has been implementing and monitoring the Annual Credit Plan and other

developmental and poverty eradication schemes launched by the Govt. of India, Govt. of

Rajasthan and NABARD. Targets allotted for Annual Credit Plan to our Bank for the

year 2013-14 was `4011.00 crore, against which achievement of our Bank up to March,

2014, is `4670.00 crore, achieving 116%.of the annual targets.

MICRO CREDIT (SHGs)

At the end of March,2014, the Bank has credit linked a total of 44244 Self Help Groups

with outstanding amount of `200.94 crore, out of which 36363 accounts are of women

beneficiaries with outstanding amount of `169.08 crore. NABARD has ranked the Bank

as number one in Rajasthan State for its performance under Micro Credit continuously

from the year 2004-05 to 2008-09.

Ministry of Finance, Govt. of India launched a project for financing to Women Self Help

Groups with the support of Anchor NGO as SHPI in 24 backward Districts of 24 States

in the country, which was later extended to 150 back ward Districts, including 109 Left

12

Wing Extremism (LWE) districts. In Rajasthan, Barmer (our lead district), Banswara,

Dungarpur and Jhalawar districts have been selected for this purpose.

The progress in this regard is directly reviewed by Department of Financial Services,

Ministry of Finance, Govt. of India. Bank branches and NGO has been identified and

Anchor NGO, CECOEDECON has surveyed and mapped the area in Barmer District. In

Barmer District, NGO has Linked 931 SHGs by SB Linkage and 521 SHGs by Credit

Linkage during the year against the targets of 1000 up to March, 2014.

RURAL SELF EMPLOYMENT TRAINING INSTITUTES (RSETI)

In order to impart job- oriented skills to rural unemployed youth, the Bank has set-up

eight RSETIs at Bikaner, Hanumangarh, Barmer Jaisalmer, Jalore, Pali, Sirohi and

Nathdwara (Distt. Rajsamand).

By the end of March, 2014, 33702 candidates have been imparted training for various

local demand jobs in these institutions and by imparting skill trainings, 4270 candidates

have been engaged in various jobs and 15340 candidates have started their own ventures.

8935 persons have been credit linked amounting to ` 4734.45 lakh. Rating process was

introduced by MoRD, New Delhi through State Project Co-coordinator of RSETIs in the

year ending March 2013. All our RSETIs secured AA+/AB rating. Our Managing

Director and Directors of four RSETIs namely Bikaner, Barmer, Hanumangarh and

Jaisalmer were honored in the felicitation function organized by MoRD, GoI on Rseti

Diwas at Vigyan Bhawan, MoRD, Delhi on 21/11/2013.

FINANCIAL LITERACY AND CREDIT COUNSELLING CENTRES (FLCC)

During the year 2010-11, in order to educate farmers and other people in rural / urban

areas with regard to various financial products, Bank schemes and services available

from the formal financial sector, the Bank had set up 9 Financial Literacy and Credit

Counseling Centres (FLCC) in all nine lead Districts in Rajasthan. These FLCCs are

providing awareness service, free of charge. Up to 31/03/2014, 111598 persons have

been counseled by these centres out of which 23605 persons have been linked with

Banks.

A campaign was launched to arrange five awareness camps per month in nearby villages

by FLCC Counsellors, which still continues and is very beneficial to rural people. In

addition to its campaign was also run through wall paintings, brochures and pamphlets.

The FLCC Counsellors also organize awareness camps in minority concentrated blocks,

in their Districts.

13

REGIONAL RURAL BANK

The Marudhara Gramin Bank (MGB) sponsored by SBBJ with its Head office at Jodhpur

has a net work of 501 branches spread over in 12 districts of Rajasthan state namely Pali,

Jalore, Sirohi, Sriganganagar, Bikaner, Hanumangarh, Jaisalmer, Barmer, Jodhpur,

Nagaur, Jaipur & Dausa. SBBJ continues to provide managerial support and financial

assistance by way of refinance etc. to MGB. All branches of MGB are on CBS platform

and provide Electronic Fund Transfer facility. MGB has a deposit of ` 5143.57 Crore and

advance of ` 3792.89 Crore as on 31.03.2014. MGB recorded Gross profit of ` 80.60

Crore & net profit of `55.50 Crore.

GOVERNMENT BUSINESS

The Bank conducts Government Business on behalf of State/Central Government

departments through 494 authorized branches. Income Tax, Central Excise, Service Tax,

Value added tax etc. are collected through physical challans and also through the

electronic mode. The Bank has established a Centralized Pension Processing Centre

(CPPC) which calculates as well as credits pension to the accounts of pensioners across

all the branches. We also have an Online Treasury Branch for online payment of Salary

of Rajasthan Govt. employees on behalf of the State Govt. Presently our Online

Treasury Branch is processing 9 lakh State Govt. transactions received through 18000

digitally signed files in a month. During 2013-14, commission income from Government

business was ` 132 crore.

INTERNATIONAL BANKING

The Bank provides Foreign Exchange related services to exporters/ importers, other

resident and non-resident customers through a network of 68 Authorized Category "B",

184 Category „C‟ branches and 4 Trade Finance Central Processing Centres(TFCPC).

Bank's forex dealing room at Mumbai and all the authorized category „B‟ branches are

equipped with infrastructure of latest technology for real-time communication and are

connected through SWIFT network with more than 750 offices of foreign banks

throughout the world. The Bank maintains 21 NOSTRO accounts in all major currencies

and non-account correspondent banking relationship with all major banking groups in the

world. To facilitate NRI customers for inward remittances, there is online remittance

facility and tie-ups with 5 Gulf based Exchange Houses.

The Bank also undertakes proprietary Forex trading to increase profit by taking

advantage of market movements. Our Merchant forex turnover stood at `31678 crore in

the FY 2013-14 as against `26717 crore of last financial year, representing an increase of

` 4961 crore (18.57 %) during the year.

Our NRI deposits stood at `1384 crore at the end of March 2014 against the base of

`1249 crore in March 2013, registering a growth of `135 crore ( 10.80%). Our export

14

credit stood at `2740 crore at the end of March 2014 as against `2334 crore of March

2013, recording a growth of `406crore (17.39%) during the financial year.

The Bank chairs the local chapter of Foreign Exchange Dealers' Association of India

(FEDAI). The Bank is an active member of FEDAI, International Chamber of Commerce

(ICC) and Clearing Corporation of India Limited (CCIL).

INDUSTRIAL REHABILITATION

Rehabilitation / restructuring of potentially viable industrial unit remains an important

thrust area of the bank. For this purpose, the bank has its own Industrial Rehabilitation

Policy containing detailed guidelines for undertaking rehabilitation / revival package and

the same is updated from time to time. Whenever units are found non viable or not

responding to the rehabilitation / restructuring package, focus is shifted to recovery of

Bank's dues through legal recourse such as action under SARFAESI / compromise

settlement / assignment of debt / through courts/ Debt Recovery Tribunals (DRT).

As at end of 31st March 2014, the Bank had 23 large sick /weak units on its books with

aggregate outstanding of `405.39 crores. There are 42 Corporate Debt Restructuring

cases with aggregate exposure of `2091.00 crores and 24 BIFR cases with exposure of

`498.19 crores. The Bank has been acting as BIFR's Operating Agency in 4 cases. During

the year under review, 38 accounts with aggregate exposure of `1770.09 crores have

been restructured under CDR mechanism as warranted basically by the tight economic

scenario. Sustained efforts are undertaken by the Bank in restructuring the accounts and

post sanction close monitoring and follow up have resulted in retaining most of the

restructured assets as Standard Assets.

NPA MANAGEMENT

The Bank continues with its multipronged strategy of controlling Non-Performing Assets

(NPAs) through intensive monitoring of large value accounts, close follow-up with

DRT/BIFR, restructuring of viable accounts and effectively utilizing the remedies

available under the SARFAESI and RODA Acts. GMs, DGMs and AGMs posted at

Head Office have been assigned the role of mentors of Zones / Regions and Branches to

provide support and monitor the NPA level. Due emphasis has been given to follow-up

with the Court and filing of Execution Petitions. During the year, large numbers of

“Recovery Camps”, Bank Adalats and Lok Adalats were organized for NPA recovery,

the results of which were quite encouraging. Recovery camps are being held in every

village, every week. The progress in NPA / AUC recovery is being discussed / reviewed

by the Management Committee by conducting Video- conferencing with all the Zones

and DGM headed branches. The “Loan Tracking Center” monitors / tracks the irregular

standard accounts from Head Office level. Pre-emptive measures such as restructuring

etc. are also taken, as per RBI guidelines. By adopting the above measures and utilizing

the provision of SARFAESI Act effectively, Bank also received a number of acceptable

15

compromise proposals which resulted in good recovery in NPA. There has been an

addition of `2123.54 crore in NPA during 2013-14. However, there has been recovery /

up-gradation to the tune of Rs1110.77 crore. At the end of March 2014, gross NPA ratio

of the Bank Stood at 4.18% and Net NPA ratio stood at 2.76%.

Loan Tracking

The Bank had set up the Loan Tracking Centre (LTC), a Centralized Outbound Call

Centre at Jaipur in June 2011, for follow-up of Personal and SME Segment Loan

accounts in IRAC4, IRAC3, IRAC2 and IRAC1 categories to avoid slippages of account

into a hardcore NPA. Subsequently in July 2012, the LTC started following up AGR

accounts also. The Call Executives at the LTC make calls to the borrowers, where contact

details are available in CBS, in a sustained manner to recover the overdue amount and

upgrade accounts in co-ordination with Branches / CPCs.

Improvement done during the current year:

(a) LTC has been set up at all the 8 Zonal offices of the Bank.

(b) Auto-Dialer system has been installed at Head Office LTC, whereby the

telephone / mobile numbers of borrowers are dialed by the Auto-dialer system and

our staff communicates with the borrower using a Head Phone attached with the

PC.

(c) With the setting up of zonal LTCs, all the NPA borrowers of the Bank are

contacted at least once during every 2 months.

Risk Management Structure of the Bank

The Bank has an independent Risk Management Framework in place. At the apex level,

there is a Risk Management Committee of the Board (RMCB), which oversees the

policies and strategies for Risk Management in the Bank. Credit Risk Management

Committee (CRMC), Asset Liability Management Committee (ALCO), Market Risk

Management Committee (MRMC) and Operational Risk Management Committee

(ORMC) provide support to RMCB. These sub-committees are required to place all

critical issues/ development in their respective areas before the RMCB. The Bank has

Credit, Market and Operational Risks Management Policies for identification,

measurement and management of major risks. These policies are reviewed and updated

from time to time, keeping in view the dynamic business environment. Integrated Risk

Management Department (IRMD) at the Head Office, functions under a Dy. General

Manager. The IRMD acts as the nodal centre for coordination with other departments/

operating units engaged in managing risk in their respective business areas.

16

Capital Framework

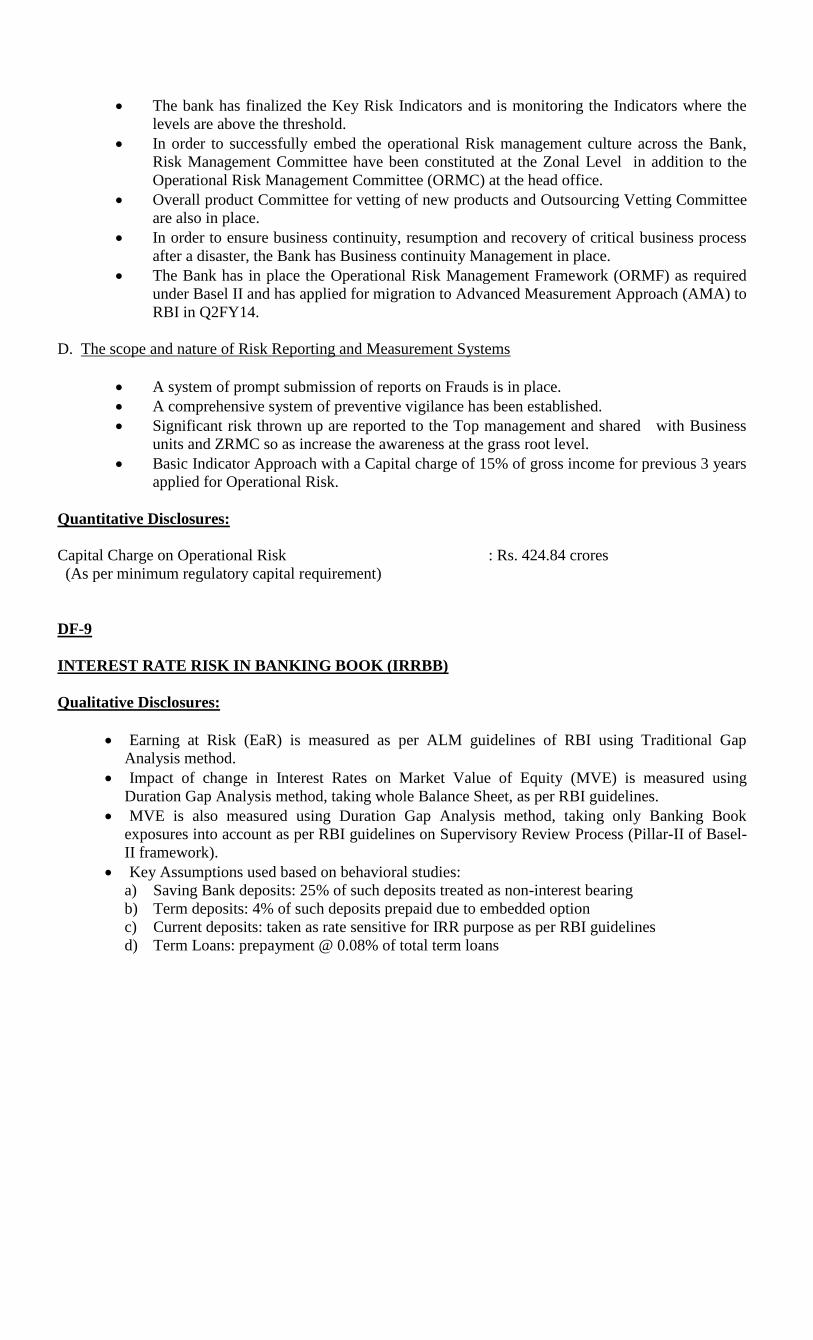

BASEL II : Under Pillar-I of the New Capital Adequacy Framework (NCAF) guidelines

issued by Reserve Bank of India, the Bank is computing Capital to Risk Weighted Assets

Ratio (CRAR) using Standardised Approach for Credit Risk, Standardised Duration

Approach for Market Risk and Basic Indicator Approach for Operational Risk. Under

Pillar-II of NCAF, the Bank has assessed capital requirement for 2013-14 for other risks

in its Internal Capital Adequacy Assessment Process (ICAAP) document, a copy of

which has been submitted to RBI. Basel-II Disclosures have been made by the Bank in

the Annual Report as also on Bank's website as part of the Pillar-III guidelines of NCAF.

BASEL III : In order to improve the quality of capital and address the liquidity risk

issues, Basel III Capital Regulation has been implemented in phases in India w.e.f.

01.04.2013. Accordingly, the Bank is computing Capital to Risk Weighted Assets Ratio

(CRAR) as per Pillar-I of Basel III Framework. With a view to improve market discipline

under Pillar 3 of Basel III framework and to improve transparency of capital base, Basel-

III Disclosures have been made by the Bank in the Annual Report as also on Bank's

website.

Credit Risk

Credit Risk management remains a major task for Bank and receives prime attention.

Control and monitoring of credit risk is dealt with as per the Loan Policy and Credit Risk

Management, Credit Risk Mitigation & Collateral Management Policy of the Bank

approved by the Board. These policies cover methodologies for measuring, monitoring

and control of credit risk. In order to control the magnitude of credit risk, prudential

norms on benchmark, financing ratios, single borrower or borrower-group exposure,

industry specific and sector-specific exposure, exposure to sensitive sectors, hurdle rate

for taking a fresh exposure etc. have been set up. Credit appraisal systems and a clearly

defined delegation of powers form an integral part of the Bank's Loan Policy.

Market Risk

To monitor market risks and treasury operations, mid-offices (domestic & forex) are

functional at IRMD. Scenario Analysis on market risk covering events such as decline in

stock markets, rise in bond yields and foreign exchange rate movements are conducted

regularly as per the Stress Testing Policy of the Bank to assess resilience of Investment

portfolio.

17

Operational Risk

One of the major tools for managing operational risk is to put in place a well established

internal control system, which includes segregation of duties, clear management reporting

lines and adequate operating procedures. Most of the operational risk events are

associated with weak links in internal control systems or laxity in complying with the

existing internal control procedures. The Bank has suitable systems and procedures for

managing and control of operational risks.

Preparation for Advanced Approaches of Basel-II

Bank plans to move over to advanced approaches of Basel-II guidelines for Credit,

Market & Operational Risks in a phased manner. Letter of Intents (LOI) for all the three

Risks have been submitted to Reserve Bank of India for this purpose. On receipt of

approval from Reserve Bank of India, Internal Rating Based (IRB) Approach for Credit

Risk, Internal Models Approach (IMA) for Market Risk and Advanced Measurement

Approach (AMA) for Operational Risk will be followed under advanced approaches.

This will not only help the Bank to maintain Economic Capital, but will also strengthen

the risk monitoring framework and control aspects.

Data Cleansing

Augmentation of capital is not only costly but its availability is also scarce. Hence, efforts

are being made for optimum utilisation of the existing capital. Bank aims at conservation

of capital by improving data quality. Cleansing of data will lead to accurate computation

of the Risk Weighted Assets of the Bank and is likely to reduce requirement of additional

capital.

Asset Liability Management

A comprehensive Asset Liability Management (ALM) System is in place for effective

management of Liquidity Risk and Interest Rate Risk. These Risks are assessed and

monitored through Structural Liquidity Reports and Traditional Gap Analysis

respectively. The structural liquidity report is being prepared and reviewed on a daily

basis as per RBI guidelines. Both these risks on Foreign Assets & Liabilities are being

monitored through Maturity & Positions (MAP) and Sensitivity to Interest Rate (SIR)

statements. The monitoring of liquidity on a dynamic basis, over a time horizon spanning

1-90 days, is in place. Duration Gap Analysis is also used to manage interest rate risk for

the entire balance sheet.

18

The Asset Liability Management Policy, coupled with Investment Policy of the Bank

specify various prudential limits for management of Liquidity and Interest Rate Risks.

The Bank is regularly monitoring these limits. A comprehensive Contingency Funding

Plan and a system of daily monitoring of inflows & outflows of deposits are in place for

managing Liquidity on a day-to-day basis. Calculation of Value at Risk (VaR) on Foreign

Exchange Forward Positions and Stress Testing on Liquidity, Interest rate and Foreign

Exchange Open & Forwards Positions is also undertaken regularly.

INTERNAL CONTROL, INSPECTION AND AUDIT

The Bank has in place a well established independent audit system and structure to ensure

adequate internal control for safe and sound operations. Internal Audit is carried out

under Risk Focused Internal Audit (RFIA) as envisaged under Risk Based Supervision of

RBI with focus on assessment of risk and internal control mechanism.

The branches have been categorised into three groups as per risk perception and are

subject to varying degrees of audit. During FY 2013-14, 738 Branches and 50

Centres/Processing Centres (under Business Process Re-engineering (BPR) initiatives)

have been subjected to Internal Audit. No branch of the Bank remained overdue for audit

as on 31.12.2013.

As at the end of March, 2014, 99.90% of the Bank's branches were rated "Well

Controlled" and "Adequately Controlled ".

Concurrent Audit

106 branches and 35 Centres/ Processing Centres (under BPR initiatives) covering

66.31% of advances and 40.70% of deposits as on 31.03.2013, besides 13 Head Office

Departments have been placed under Concurrent Audit.

Information System (IS) Audit

Information System Audit Cell is in place to conduct IS audit of major IT establishments

including Core Banking Project , Zonal Computer Centres, etc. in accordance with RBI

directives and Bank's IT Security Policy.

RECONCILIATION OF INTER-OFFICE TRANSACTIONS

As per the RBI guidelines, all the entries need to be reconciled within a period of six

months from the date of their origin. By the end of March 2014, the bank has reconciled

inter-branch debit transactions originated up to 28.02.2014 i.e. well before the time limit

prescribed. The Bank shall aim at reconciling all entries within two months of their

origin.

19

INFORMATION TECHNOLOGY

1. CORE BANKING SOLUTION (CBS)

All our branches are running successfully on Core Banking Solution. We were able to

provide better customer satisfaction and services by providing many Value Added

Services like; multi functional ATMs, Internet Banking, Mobile Banking, flexi deposit

scheme, multi city cheque facility, instant credit of local and outstation cheques, etc. For

all type of Debit/Credit transactions in CBS, SMS alert is sent to customers, where

mobile number is registered with the Bank.

2. ELECTRONIC PAYMENT SYSTEMS: RTGS, NEFT & SBGRPT

Real Time Gross Settlement (RTGS) is an instant payment and settlement system and

National Electronic Fund Transfer (NEFT) is a scheme for inter-bank funds transfer

operated by the RBI. All branches of our bank are RTGS & NEFT enabled. Our

customers can make their inter-bank remittances in a faster and secured manner at very

nominal cost. SB Group Payment (SBGRPT) functionality for electronic funds transfer

within State Bank Group is also available for customer.

3. AUTOMATED TELLER MACHINES (ATMs)

The Bank has installed 467 new networked ATMs and replaced 123 ATMs during the

year to take the tally of ATMs to 1554. All the ATMs are connected to the network of

State Bank Group ATMs, there by enabling more than 62.50 lakh card holders of the

Bank to have free of cost access to over 45000 ATMs of the State Bank Group all over

the country.

4. INTERNET BANKING

All our branches are enabled to offer Internet Banking facility to our retail as well as

corporate customers. Looking to the rapid increase in the usage of Internet banking

worldwide, the Bank has introduced several new features during the year. Apart from

own account and third party transfer within bank, our customers can transfer funds to

other banks in online mode. TDS enquiry for Term Deposits from the comfort of their

homes or offices, opening / closing of e - TDR / e - STDR / e - Recurring Deposit (RD)

account, facility to view the details of Income - Tax Statement (26 -AS) and viewing of

Pension Slip is available. Retail Internet Banking facility for visually challenged persons

has also been made available. For Corporate customers, a new facility 'SB - Collect', for

on line collection of funds has been provided.

Online payment of direct and indirect taxes e.g. Income Tax, Service Tax, Excise Duty,

Customs Duty of Central Government, VAT/CST of Rajasthan State Government and

Maharashtra State Government, EGRAS facility for online collection of all Tax and non

Tax revenue of Rajasthan Government. Facility of online payment of Professional Tax of

20

Maharashtra State Govt. has also been provided. Facility of online application for IPOs

using ASBA (Application Supported with Blocked Amount) facility where investor

customer continues to earn interest during the application process is available to internet

banking users.

Facility of online booking of Railway / Air Tickets has been widely accepted. Electronic

payment of railway freight (E-Freight) is gaining popularity. We have integrated number

of Aggregators to our online system to provide the payment facility of wide range of

merchants, e-commerce services and utility bills to our Internet Banking users.

Bank has taken steps to increase awareness about Internet banking among staff as well as

customers through seminars and awareness meets. To popularize online payment of taxes

a facility of "Zero Balance Internet Current Account" has been introduced.

5. MOBILE BANKING & IMMEDIATE PAYMENT SERVICES (IMPS)

Mobile Banking facility was introduced in the year of 2009, for our customers having a

Savings / Current Account. The product is named "State Bank Freedom. Presently, there

is upper ceiling of `50000/- for fund transfer and for purchase of goods / services per day

with in overall calendar month limit of `2,50,000/-. In order to make the registration

process more robust and to eliminate the threat of frauds/ phishing attempts, our Bank

enabled registrations over ATM/CBS, only if the mobile number entered matches with

the mobile number already available in the customer‟s CIF in CBS.

"Immediate Payment Service" (IMPS) P2P (Person-to-Person), was launched in our bank

in the year of 2012 for enabling our customers to use mobile instruments as a channel for

remitting funds 24 x7 using MMID (Mobile Money Identifier) & Mobile Number.

During 2013-14, two more services P2A (Person-to-Account) & P2M (Person-to-

Merchant) has been enabled in our Bank to make fund transfer using Account No. & IFS

code and to make various utility payments at shops and commercial establishments, ticket

booking though IRCTC website etc., The upper ceiling for remittance or payment of bills

is same as in Mobile Banking facility.

6. Green Channel Counter

Bank has implemented “Green Channel Counter” facility at various branches viz., all

districts Head Quarters in Rajasthan, branches situated at Delhi NCR, Mumbai,

Bangalore and Ahmedabad, other identified Urban, Semi-Urban and Rural branches.

It is a paperless, eco-friendly and easy facility for the customers to be carried out through

ATM cum Debit Card using a Transaction Processing Device (TPD) placed at the Single

Window Operator‟s (SWO) terminal connected to CBS terminal of the SWO. Presently

this facility is available at 506 branches with 2 such counters minimum at each branch.

21

7. Prepaid Cards

The Rupee Pre-paid Card (eZPay Card) has been launched, particularly for salaried

persons and students for pocket money and scholarship payments, who undertake only

one or two transactions in a month and maintain account for the purpose. The Rupee Pre-

paid Card (eZPay Card) is equally useful for the Corporate, who have to make various

payments to their staff and vendors. The cards can be reloaded and can be used in any

ATM or with any POS merchant, any number of times during their validity period.

8. Bunch Note Acceptor (BNA)

BNA machines are installed at Banks‟ 2 branches. It is a full-functional freestanding

lobby machine installed in the Branches Banking Hall. The BNA machine is capable of

accepting `49,900/- cash in bundles and receipt is given to the customer and cash is

immediately credited to the customer on real time basis.

9. Cash Deposit Machine (CDM)

The Bank has planned to install CDM at various High Cash Receipt branches providing

24/7 availability with round the clock security in onsite ATM kiosk. The CDM machine

is operable through ATM-cum-Debit card and is capable of accepting cash up-to `

49,900/-. Receipt of the deposit transaction is given to the customer and cash is

immediately credited to customer‟s account on real time basis.

10. Self Service Kiosk (SSK)

75 Self Service Kiosks (SSKs) have been installed at various branches of our Bank.

Customers can perform financial and non-financial transactions such as passbook

printing, fund transfer etc. using State Bank ATM-cum-Debit Cards at these SSKs. The

SSK solution has user friendly touch screen based customer interface.

11. Adoption of advanced IT infrastructure products for internal housekeeping at

the branches/offices:

i. Biometric Authentication of CBS users

For improved security in Core Banking Solutions, the Bank has rolled out Biometric

Authentication Solution (BAS) at branches/offices for the front end tellers using CBS.

The solution is used as a second factor for authentication of CBS tellers, the primary

mode being the CBS password combination.

ii. ACTIVE DIRECTORY SERVICES (ADS )

For enhanced security Bank has implemented Active Directory Services within State

Bank Connect Network in all the branches/offices. Active Directory (AD) provides

centralized administration of network and security. It authenticates and authorizes all

users and computers in a Windows domain, assigning and enforcing security policies for

all computers and facilitates installing or updating software centrally.

22

iii. SB-Connect:

At present all 1100 branches/offices are connected through State Bank Connect. A

technology shift from „Point to Point‟ to MPLS has been initiated by Bank to ensure

seamless best path connectivity at all the branches with availability of redundant circuits

at all times. Wifi / Wimax / 3G and 4G modes of connectivity is also under consideration

at the Group level after ensuring information security clearance of these products in our

Bank.

iv. Online Voucher Viewing and Verification Module(OVVVM)

OVVVM has been implemented in the Bank at all branches/offices (other than single

officer branches). Same day transactions can be verified by the supervisors after posting

of the transactions in CBS. With the viewing / verifying of transactions online on the

same day, any fraud / malpractices can come to notice on near real-time basis and adverse

position can be avoided to the extent possible.

12. MGNREGA e-Payment

Government of Rajasthan has designated our Bank as the Nodal Bank for MGNREGA e-

Payments in the State of Rajasthan. MGNREGA e-Payment system has been

implemented for centralized payment of NREGA wages and other expenditures directly

to the beneficiaries' accounts. The project has been smoothly handling transactions of

about 2 to 2.5 lakh per month.

13. SMS UNHAPPY

The "Project SMS Unhappy" was launched by the Bank with the objective to provide a

simple and economical way to the customers to represent their grievances. This has

reduced complaint resolution time drastically, to below 48 hours, thereby enhancing the

customer satisfaction level and creating a loyal customer pool.

14. INSTANT LOAN SANCTION

Bank is providing the facility of online instant sanction of Housing Loan and Car loan to

the customers under the head "Home Loan in 20 minutes" and "Car Loan in 10 minutes"

respectively on Bank's website http: //www.sbbjbank.com/.

Customer gets sanction letter instantly on submitting completely filled application form

on Bank's website if he fulfills the eligibility criteria.

15. ONLINE LOAN APPLICATION TRACKING SOFTWARE

Bank has introduced a web based application for Online Tracking of Loan application for

customer and status of their application can be viewed by customer on internet

through our Bank's website.

16. INFORMATION SYSTEM (IS) SECURITY

23

With the efforts of the Bank to popularize IT enabled services, the threats and risks to our

IT assets have increased manifold. To control these threats and risks our Bank has a

formulated comprehensive IT and Information Systems (IS) Security Policy that

addresses all these concerns including maintenance of customers' confidentiality, security

and integrity of data. State Bank's data centre where our CBS data base resides (both at

the Primary and Disaster Recovery Site) has already acquired the accreditation from the

international standard for Information Security Management Systems ISO/IEC: 27001:

2005. All the Banking applications have built-in security features like access control, data

encryption and transmission through secured channels as per requirement of the

application. The threat of virus and worms is minimized by having a centralized anti-

virus solution.

Adequate Firewalls and Intrusion Detection Systems are in place so as to prevent

unauthorized access to the network. The Disaster Recovery Plan (DRP) and Business

Continuity Plan (BCP) for all branches are in place.

KNOW YOUR CUSTOMER/ANTI MONEY LAUNDERING /COMBATING

OF FINANCING OF TERRORISM MEASURES

Bank follows Reserve Bank of India/ Government of India guidelines on Know Your

Customer/ Anti Money Laundering / Combating Financing of Terrorism. Prescribed

documents relating to the identity and address are obtained from customers while opening

their accounts.

With the objective of Universal Financial Inclusion, Bank facilitates opening of 'Small

Account' by migrant labourers, street hawkers and other poorer sections of the society,

with limited KYC documents.

To facilitate inclusion of lower strata of society to mainstream banking, Basic Saving

Bank Deposit Account (BSBA) for the customer having prescribed KYC documents has

been introduced. BSBA shall not have the requirement of minimum balance. At the same

time the entire range of services available to a normal saving bank account is extended to

this product.

In order to identify and examine suspicious transactions, the Bank has installed the

AMLOCK software besides setting up an ANTI Money Laundering Cell at the Head

Office. The customers' accounts have been allocated different risk categories and alerts

are generated once any transaction exceeds a predefined threshold limit. These alerts help

in identification of suspicious transactions, which are further reported to Financial

Intelligence Unit, Government of India, in appropriate cases".

DEMAT SERVICES

Our Bank is providing Depository Participant Services with National Securities

Depository Limited (NSDL) to our customers, wherein they can hold their securities as

24

electronic book entries and transfer securities without actually handling physical scripts.

Customers can also obtain loans against Demat shares. SBBJ is registered with NSDL as

a Depository Participant.

Customer Service:

Customer Service is a top priority for the Bank. We are in a service industry and our

success to a very large extent depends on the satisfaction level of our customers. The

environment we operate in is increasingly becoming intensely competitive.

The meetings of the Customer Service Committee of the Board and Standing Committee

on Customer Service were convened at regular intervals to review the position of

customer service rendered. Similar Committees are also functioning at Branches, Zonal

and Head Offices, which helps in continuous improvement in service standards.

The Bank is a member of the Banking Codes and Standards Board of India (BCSBI) and

has voluntarily adopted a 'Code of Bank's Commitment to Customers,' which sets a

framework for setting a minimum standard of banking services to be provided by the

banks. An awareness camp for BCSBI code was organised at Jaipur on 19 November

2013 in coordination with BCSBI.

Customer Grievances Redressal Mechanism:

The Bank has put in place a multi pronged grievances redressal mechanism to suit varied

customer requirements. An aggrieved customer can either make a written complaint at

branch / regional / zonal / head office of the Bank or make an online submission in the

form provided on the Bank's website / through e-mail against acknowledgement.

DISCLOSURE OF COMPLAINTS/UNIMPLEMENTED AWARD OF BANKING

OMBUDSMENT :-

In terms of RBI circular DBOD.No.Leg BC.60/09.07.005/2006-07 dated 22.02.2007, the

information in respect of customer complaints and awards passed by the Banking

Ombudsment is given in the Table below :-

A. Customer Complaints

(a) No. of Complaints pending at the beginning of the year 71

(b) No. of Complaints received during the year(*) 6470

(c) No. of Complaints redressed during the year(*) 6434

(d) No. of Complaints pending at the end of the year 107

(*) Excluding 1499 Complaints found non maintainable.

B. Awards passed by the Banking Ombudsman (BO)

(a) No. of unimplemented Awards at the beginning of the year 01

(b) No. of Awards passed by the Banking Ombudsman during the year 17**

(c) No. of Awards implemented during the year 12

(d) No. of unimplemented Awards at the end of the year(in 2 cases Appeal

has been made before Appellate Authority and in 1 case matter in

under process)

03

25

** In 3 cases, under 1st case BO Delhi has re-examined the case and cancelled the award

against the Bank. In 2nd

case complainant not accepted the award and in another one

appeal allowed and award passed by BO is set aside by the Appellate Authority.

ATM COMPLAINTS

To monitor the ATM failed transactions related customer complaints received at the

branches, ATM Complaints Reconciliation Cell has been established at Head Office.

Reserve Bank of India has prescribed that all ATM related complaints be resolved within

7 working days. For faster resolution /redressal of complaints, an online ATM Complaint

Management System (ATMCMS) has been developed and implemented. During the year

2013-14, the Bank has received 20567 ATM failed transactions related complaints, out of

which 20477 complaints were resolved. No home bank complaint (where customer and

ATM both belong to our bank) is pending for more than 7 working days. Number of

complaints pending for more than 7 days where claim is pending with other banks is 3.

THE RIGHT TO INFORMATION (RTI)

The Right to Information (RTI) Department was constituted at the Bank's Head Office in

December, 2010 for better coordination and effective implementation of the Right to

information Act, 2005 . The Department has since then been instrumental in ensuring that

information sought for under the various RTI applications received by them is dispensed

with efficiently and effectively in a time bound manner as per the provisions of the RTI

Act, 2005 and that the appeals too, if received, are redressed timely, while also

complying with the directives of the Hon'ble Central Information Commission (CIC) in

this regard.

During financial year 2013-14, the RTI Department received 1553 applications under the

RTI Act, 2005, out of which 1532 applications were disposed off. 21 applications were

awaiting disposal as on 31st March, 2014, and these were all pending for less than 30

days.

Besides, the Department also received 73 appeals under the RTI Act, 2005 during

financial 2013-14, out of which 71 appeals were disposed off. 2 appeals were awaiting

disposal as on 31st March, 2014, and these also were pending for less than 30 days.

BUSINESS PROCESS RE-ENGINEERING

Business Process Re-engineering (BPR) Initiatives stabilized further during 2013-14 and

their coverage extended to more branches. Bank operates 12 city-centric loan CPCs, viz.

Retail Assets Central Processing Centre (RACPC)/ Small & Medium Enterprises City

Credit Centre (SMECCC)/ Retail Assets and Small & Medium Enterprises City Credit

Cell (RASMECCC) having end-state at 11 centres with 275 branches linked to them.

Coverage of Rural Central Processing Centre (RCPC) increased to 374 branches at 19

26

centres. 22 Relationship Managers-Medium Enterprises (Hub Model) and 1 Relationship

Managers-Small Enterprises are working at 14 major business centres.

Non loan CPCs/ initiatives, viz. Liability Central Processing Centre (LCPC), Trade

Finance Central Processing Centre (TFCPC), Currency Administration Cell (CAC),

Central Pension Processing Cell (CPPC), Clearing CPC (CCPC), Multi Product Sales

Team (MPST), Relationship Manager-Personal Banking (RMPB) have helped in further

improvement in customer service. The coverage of various non loan CPCs / initiatives as

on 31.03.2014 vis-à-vis 31.03.2013 was as under:

CPC / Initiative Branches Covered

31.03.2013 31.03.2014

LCPC 996 1097

TFCPC 122 124

CAC / SCAB 155 180

Clg. CPC 224 250

CPPC 844 909

Branch Re-design 185 196

During Financial Year 2013-14, following developments took place to make CPCs /

initiatives more effective and to optimize gains:

In Branch Cash Handling (IBCH) has been rolled out w.e.f. 15.06.2013.

RASMECCC at Bhiwadi centre started functioning w.e.f. 31.01.2014.

CAC at Delhi centre started functioning w.e.f. 26.02.2014.

Shifting of back office activities to loan CPCs, implementation of revised roles for branch

functionaries and better ambience in branches has not only improved the Bank‟s image

but also helped the linked branches to focus more on customer service and marketing for

business.

Currency Management Department

Being the Bank having the highest market share in Rajasthan, RBI has designated 199

branches as Currency Chest branches in the state and 15 branches in other parts of the

country. All of our Currency Chest branches are undertaking the following activities in an

efficient manner:-

1. Circulation of New Currency Notes among Public.

2. Distribution of Coins to the Public.

3. Exchange of torn/damaged/soiled/mutilated notes.

4. Providing of linkage facilities to branches of other banks which are linked to them.

5. Our 9 branches are providing facilities of Note Exchange and coin distribution on 3rd

Sunday of every month and 6 branches are providing facilities of Note Exchange and

coin distribution on 3rd

Sunday of alternate month.

27

CROSS SELLING

The Bank continues to market life and non-life insurance, mutual fund and credit card

products in order to augment its non interest income. For the purpose, the Bank has in

place tie up arrangements with SBI Life Insurance Co. Ltd., SBI General Insurance Co.

Ltd., SBI Fund Management Pvt. Ltd. and SBI Cards and Payments Services Pvt. Ltd.

Various campaigns were launched for marketing of these products, and the bank earned a

total income of ` 20.03 crore from cross selling activities.

COMMUNITY SERVICES BANKING

As a responsible Corporate Citizen, the Bank undertakes community based social

activities such as tree plantation, free health check up & blood donation camps,

establishing of water huts and water coolers, sponsoring prizes / kit for sports

competitions, honouring meritorious students etc. During the year 2013-14, the Bank

donated ` 1.00 crore for Uttarakhand Chief Minister‟s Relief Fund and `25 lakh for

Odisha Chief Minister‟s Relief Fund to assist in relief measures to people affected by

Natural Calamity. Bank also provided 5 ambulance, one each to Maheshwari Hospital &

Research Centre Trust Jaisalmer, Ram Niwas Dham Trust Shahpura Bhilwara, Sant

Sukhdev Shah Memorial Religious & Charitable Trust Alwar, L.K.C. Shri Jagdamba

Andh Vidhyalaya Samiti Sriganganagar, People Welfare Society Sikar and one Antim

Darshanika Vahini (Mortury Van) to Jagriti Jaipur.

Other activities or financial assistance by our Bank are listed as under :-

- Water purifiers and ceiling fans by every branch of the bank to its nearby

School which had scarcity of funds.

- Provided Medical equipments to Manav Sewa Sangh Jaipur, which

providing free treatment of Bone Marrow Transplantation to Thalassemia

affected children of poor family.

- Financial assistance to Society for Rational Development Jodhpur for free

education to poor children in rural areas.

- Computer, Projector, Laptop, Printer and T.T. Table to Udayan Care

Jaipur, an NGO which shelters, educate and rehabilitates,

orphaned/abandoned children.

- Computer & Projecter to I Create Jaipur, an NGO which organizes

training programmes and vocational training for youth and women.

- Provided furniture to Vimukti Sansthan helping slum area girls with free

education and vocational training .

- Donated Generator to RamaKrishana Mission, Khetri for running various

welfare activities like health support programmes (free eye surgery) and

providing nutritious food for poor children and their mothers.

28

- Branches of the Bank Continues to adopt one girl child each from a poor

family with an objective of providing financial assistance for pursuing

their studies in Government /Municipal Schools

- Distributed 200 folding sticks to poor blinds at Blind & Humanity Welfare

Centre, Mumbai.

- Provided Roti Making Machine to Manav Sewa Samiti Udaipur, serving

poor people by way of providing free meals to attendants of patients at

Hospitals.

- Provided Vela Ventilator (Life Saving Equipment) to Sheth D.C.Shroff

Ashaktashram Hospital, Surat which is charity based hospital.

Bank shall remain dedicated to respond to the needs of the less fortunate and under-

privileged members of the society and will also do its bit for a clean environment.

BRANCH EXPANSION

During 2013-14, the Bank opened 113 new fully computerized branches which includes

34 branches in unbanked rural centres in Tier V and VI. 25 branches were inaugurated

online from the Head Office on 27.02.2014.

As on 31.03.2014, the total number of branches of the Bank stood at 1148, the category

wise distribution thereof being as under:

Rural Semi Urban Urban Metro Total

416 308 214 210 1148

The Bank continued to maintain its dominant presence amongst all other banks in the

State of Rajasthan with a network of 932 branches as on 31.03.2014, with 699 branches

being located in rural and semi urban areas .

The Bank continues to play a pivotal role in the socio-economic development, alleviation

of poverty and resultant overall uplift of the masses in the State .

HUMAN RESOURCES DEVELOPMENT

The Bank‟s staff strength as on 31.03.2014 is 13359 employees, with the following break

up: -

AS ON 31.03.2014 OUT OF WHICH

STAFF

CADRE

SC ST GENERAL TOTAL WOMEN MINORITY

OFFICERS 1058 489 3837 5384 695 368

CLERKS 936 584 3744 5264 918 317

SUB-STAFF 318 219 1418 1955 125 67

SAFAI

KARAMCHARI

591 19 146 756 234 6

29

TOTAL 2903 1311 9145 13359 1972 758

Out of the Bank‟s total staff strength as on 31.03.2014, 2903 (21.73%) belong to SC and

1311 ( 9.81%) to ST categories which is well above required percentage . SC/ST cell to

safeguard interests of SC/ST employees is also well in place. Reservation policy is

implemented in our Bank as per Government guidelines.

Necessary complement of staff has been made available for working in new frontiers like

core banking solution, tele-banking, internet banking, ATMs, credit / debit cards,

marketing, cross selling, business process re-engineering etc. The Bank has been

according high priority to training and sensitization of staff members to respond to the

customers‟ expectations and deliver modern banking facilities in the technology-driven

environment."

.

Human Resource is the most important constituent and quintessence of an organization