Content Contributed by the Appraisal Database and Mentoring Services’ (ADAM) Around the Valuation World ™ in 90 Minutes Monthly Webzine

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Content Contributed by the Appraisal Database and Mentoring Services’ (ADAM)

Around the Valuation World™ in 90 Minutes Monthly Webzine

DISCLAIMER

All rights reserved. No part of this work covered by the copyrights herein may be reproduced or copied in any form or by any means—graphically, electronically, or mechanically, including photocopying, audio/video recording, or information storage and retrieval of any kind—without the express written permission of the CTI, NACVA, and the presenter.

The information contained in this presentation is only intended for general purposes.

It is designed to provide authoritative and accurate information about the subject covered. It is sold with the understanding that the copyright holder is not engaged in rendering legal, accounting, or other professional service or advice. If legal or other expert advice is required, the services of an appropriate professional person should be sought.

The material may not be applicable or suitable for the reader’s specific needs or circumstances. Readers/viewers may not use this information as a substitute for consultation with qualified professionals in the subject matter presented here.

Although information contained in this publication has been carefully compiled from sources believed to be reliable, the accuracy of the information is not guaranteed. It is neither intended nor should it be construed as either legal, accounting, and/or tax advice, nor as an opinion provided by the Consultants’ Training Institute (CTI), National Association of Certified Valuators and Analysts (NACVA), the Institute of Business Appraisers (IBA), the presenter, or the presenter’s firm.

The authors specifically disclaim any personal liability, loss, or risk incurred as a consequence of the use, either directly or indirectly, of any information or advice given in these materials. The instructor’s opinion may not reflect those of the CTI, NACVA, its policies, other instructors, or materials.

Each occurrence and the facts of each occurrence are different. Changes in facts and/or policy terms may result in conclusions different than those stated herein. It is not intended to reflect the opinions or positions of the authors and instructors in relation to any specific case, but rather to be illustrative for educational purposes. The user is cautioned that this course is not all inclusive.

© 2013—1997 NACVA • 5217 South State Street, Suite 400 • Salt Lake City, UT, 84107—ALL RIGHTS RESERVED.

The Consultants' Training Institute (CTI) is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted through its web site: learningmarket.org.

2© 2013 National Association of Certified Valuators and Analysts

3

Lorenzo CarverMS, MBA, CPA, CVA

IN 90 MINUTES™

Valuation of Privately‐Held‐Company Equity Securities Issued as Compensation;Accounting and Valuation Guide Final Revisions to the 2004 Guide Released In June 2013

Published by the American Institute of Certified Public Accountants

© 2013 National Association of Certified Valuators and Analysts

4

One trillion dollars in private company

value

© 2013 National Association of Certified Valuators and Analysts

5

General solicitation ban ended July 9th

2013

© 2013 National Association of Certified Valuators and Analysts

Improved differentiation PE/VC practices

More examples and specific recommendations

New section on secondary market transactions

6© 2013 National Association of Certified Valuators and Analysts

VC Typically have lots of company poised to rapidly grow new markets (revenue), but little or no earnings before interest, taxes, depreciation, and amortization (EBITDA)

PE funds typically have just a handful of companies, but almost all promise EBITDA growth

7© 2013 National Association of Certified Valuators and Analysts

8© 2013 National Association of Certified Valuators and Analysts

9

“Why is Dropbox worth more than four billion dollars?”

© 2013 National Association of Certified Valuators and Analysts

10

Where did Forbes really get “$4 Billion” From?

© 2013 National Association of Certified Valuators and Analysts

© 2013 National Association of Certified Valuators and Analysts 11

“Soon after, Dropbox raised $250 Million. Putting its value at over $4 billion. ”

$250 Million÷ X% (assumed % of company purchased-FDS)≈ $3.75 Billion Pre-money + $250MM ≈ $4.00 Billion Post-money value

© 2013 National Association of Certified Valuators and Analysts 12

Where did the Economist get “$4 Billion” From?

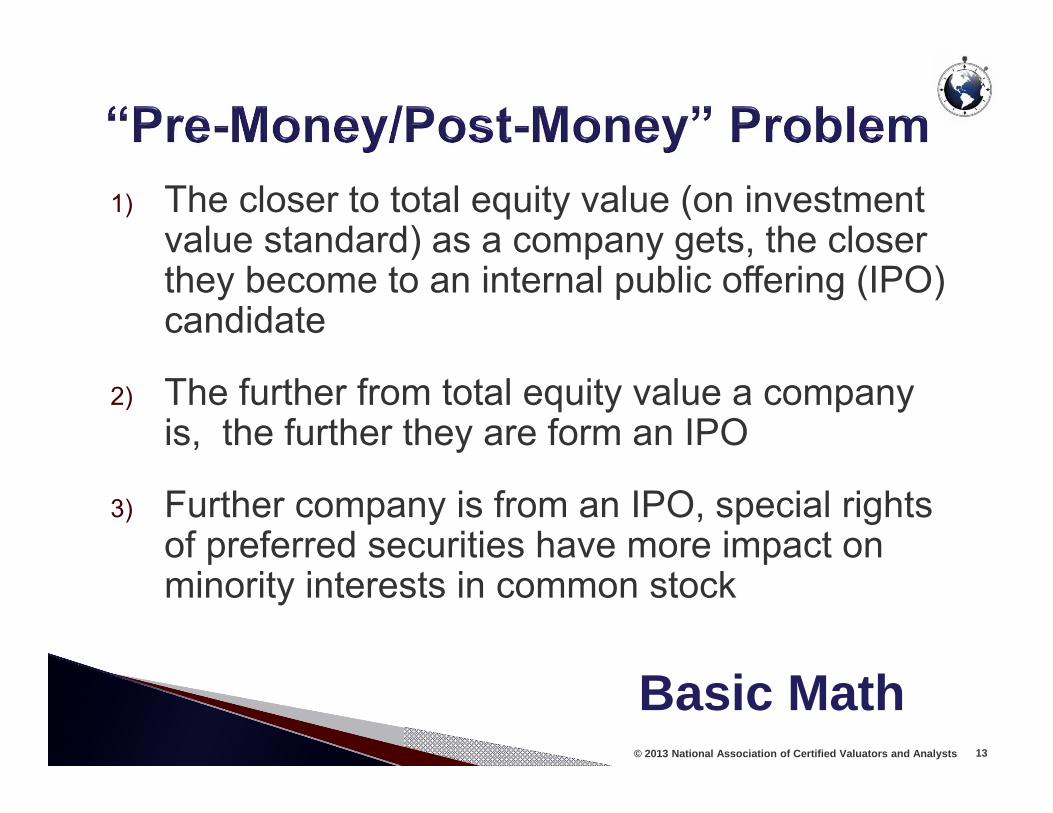

Basic Math

© 2013 National Association of Certified Valuators and Analysts 13

Basic Math

1) The closer to total equity value (on investment value standard) as a company gets, the closer they become to an internal public offering (IPO) candidate

2) The further from total equity value a company is, the further they are form an IPO

3) Further company is from an IPO, special rights of preferred securities have more impact on minority interests in common stock

© 2013 National Association of Certified Valuators and Analysts 14

More Involved Math

Use last round price as input

◦ This has already been done for years by valuators before the AICPA recommendation, and for decades by investors

“Back-solve” last round price to get total equity value indication

◦ Valuators have been doing this for a while, but most investors don’t believe in this methodology (and many finance teams don’t agree with it)

© 2013 National Association of Certified Valuators and Analysts 15

More Involved Math

Use last round price as input:◦ This has already been done for years by valuators

before the AICPA recommendation, and for decades by investors

“Back-solve” last round price to get total equity value indication:◦ Valuators have been doing this for a while, but most

investors don’t believe in this methodology (and many finance teams don’t agree with it)

© 2013 National Association of Certified Valuators and Analysts 16

At AICPA Backsolve Other Preferred is Worth Less Than Series B

© 2013 National Association of Certified Valuators and Analysts 17

Current Method – All Equal @ Post Money

© 2013 National Association of Certified Valuators and Analysts 18

With Higher Volatility, Assumed OPM Gets Closer

© 2013 National Association of Certified Valuators and Analysts 19

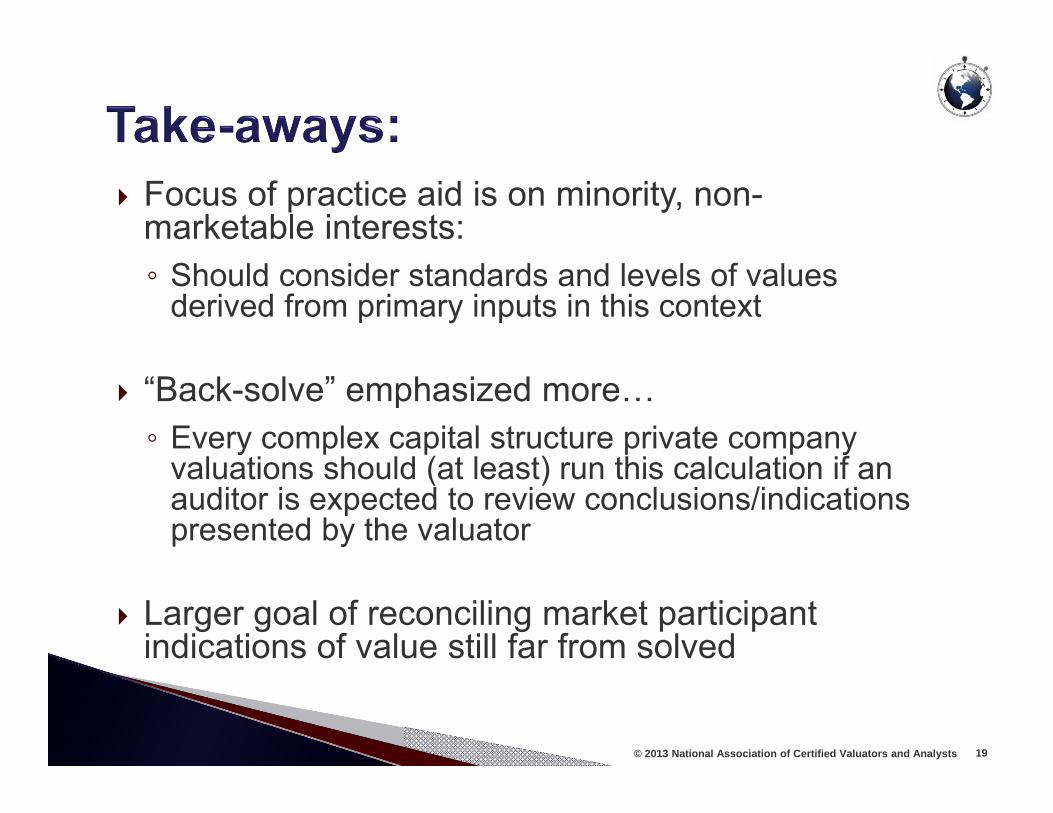

Focus of practice aid is on minority, non-marketable interests:◦ Should consider standards and levels of values

derived from primary inputs in this context

“Back-solve” emphasized more…◦ Every complex capital structure private company

valuations should (at least) run this calculation if an auditor is expected to review conclusions/indications presented by the valuator

Larger goal of reconciling market participant indications of value still far from solved

© 2013 National Association of Certified Valuators and Analysts 20

•Free Version: (of the draft aid – E&Y site)

•Paid Version: (final aid – AICPA site)

•Interactive Version of DropBox Example: (iTunes Appstore – CrunchMyCap –iPhone/iPad – Authored by Me - Free)

•NACVA Valuation Webinar Week

Related Documents