Contact via website: www.YourBestPlan.ne t Samuel J Alibrando Copyright 2004 Why Life Insurance The Most Elegant Financial Tool

Contact via website: Samuel J Alibrando Copyright 2004 Why Life Insurance The Most Elegant Financial Tool.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

Why Life Insurance

The Most Elegant Financial Tool

5 Minutes

• In the next 5 minutes, you will probably learn more about the concept and use of life insurance in ways you have not previously known or considered.

• Enjoy

Samuel J Alibrando www.YourBestPlan.net

American dollars are used as examples here but same principles apply in most countries

Laws may change or vary in some states or countries

Samuel J Alibrando www.YourBestPlan.net

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

As a Death Benefit

This is only the first reason,

but worth understanding

Samuel J Alibrando www.YourBestPlan.net

Insurance Is . . .

• Insurance of all kinds are designed to transfer an unbearable financial risk away from you to a company that will bear the risk for you.

Samuel J Alibrando www.YourBestPlan.net

The Chance of Dying• There is a percentage chance that you may

or may not – be in a car accident– lose your home to fire– spend time in a hospital– have no income for a duration

• Your chances of dying, however, is 100%

Samuel J Alibrando www.YourBestPlan.net

Why Don’t All Life Policies Pay?

• The ONLY way your life insurance policy will not pay is if you lose the policy for non-payment before dying

Samuel J Alibrando www.YourBestPlan.net

Do the Math

• Everyone dies, but most die in old age• Term insurance is a good investment ONLY

if you die young or soon after buying the policy

• Term insurance will end up costing you more than it pays at death if you keep it into your older years

Samuel J Alibrando www.YourBestPlan.net

Think About It

• Of what use is fire insurance if it covers you until you have a fire?

• How sensible is it to buy a death benefit that is too expensive to keep once you get close to the normal age most people die?

• It is easy to lose with term insurance

Samuel J Alibrando www.YourBestPlan.net

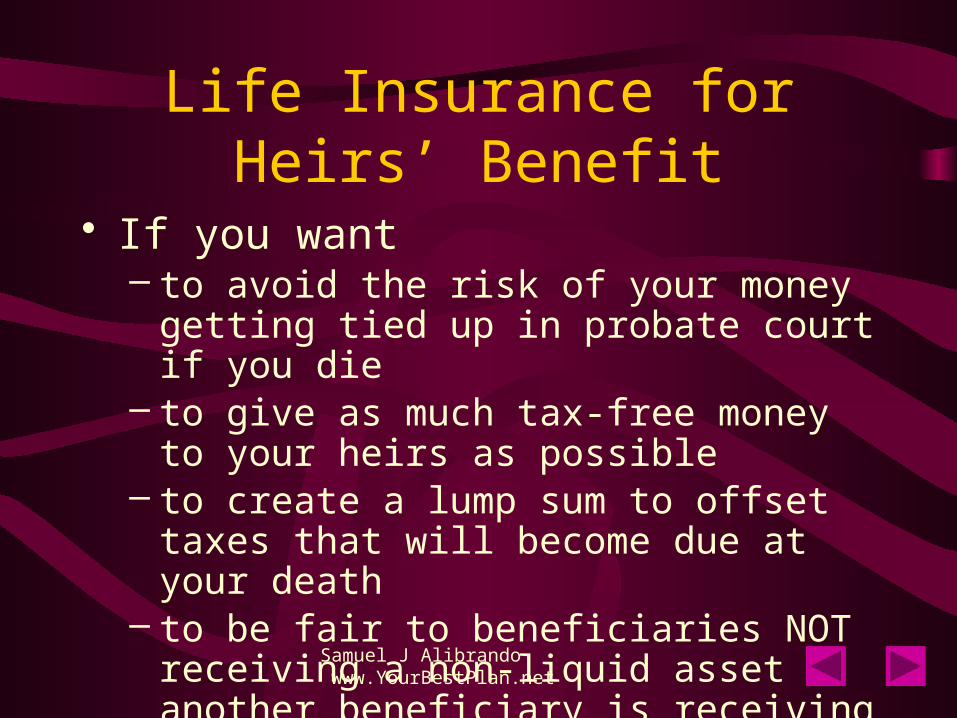

Life Insurance for Heirs’ Benefit

• If you want – to avoid the risk of your money getting tied up

in probate court if you die– to give as much tax-free money to your heirs as

possible– to create a lump sum to offset taxes that will

become due at your death– to be fair to beneficiaries NOT receiving a non-

liquid asset another beneficiary is receiving

Samuel J Alibrando www.YourBestPlan.net

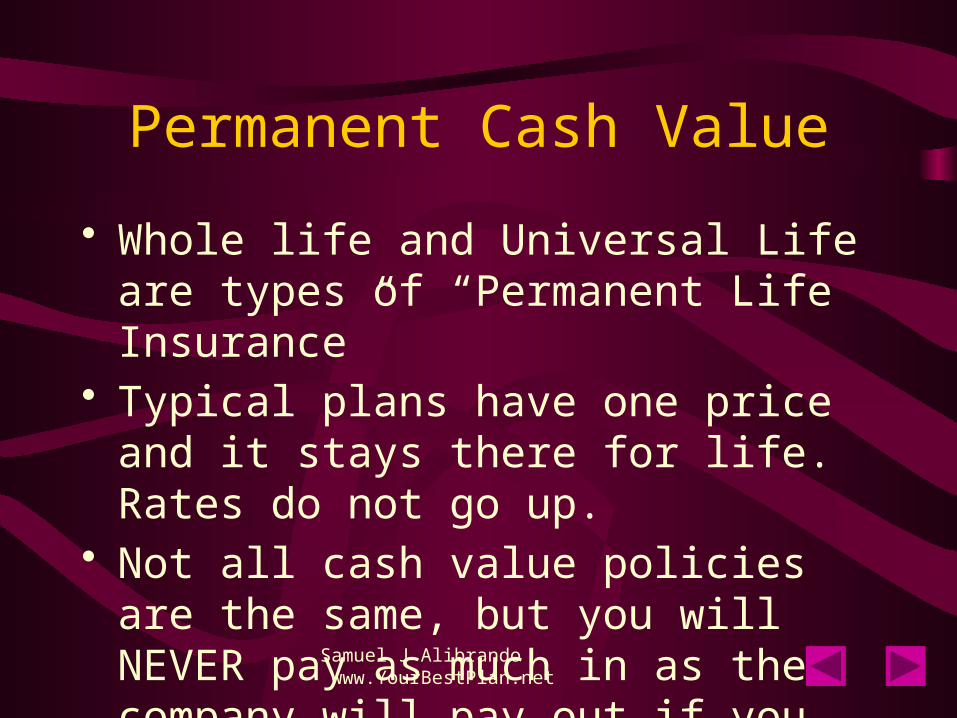

Permanent Cash Value

• Whole life and Universal Life are types of “Permanent Life Insurance”

• Typical plans have one price and it stays there for life. Rates do not go up.

• Not all cash value policies are the same, but you will NEVER pay as much in as the company will pay out if you don’t drop it

Samuel J Alibrando www.YourBestPlan.net

Summarize: Term vs. Permanent

• Since you will drop your term insurance in your older years let’s summarize:– Inexpensive Term insurance will pay a death

benefit if there is premature death– Permanent Life Insurance is a guaranteed

savings at any age

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

Treatment at Death

Disbursement of Funds

Samuel J Alibrando www.YourBestPlan.net

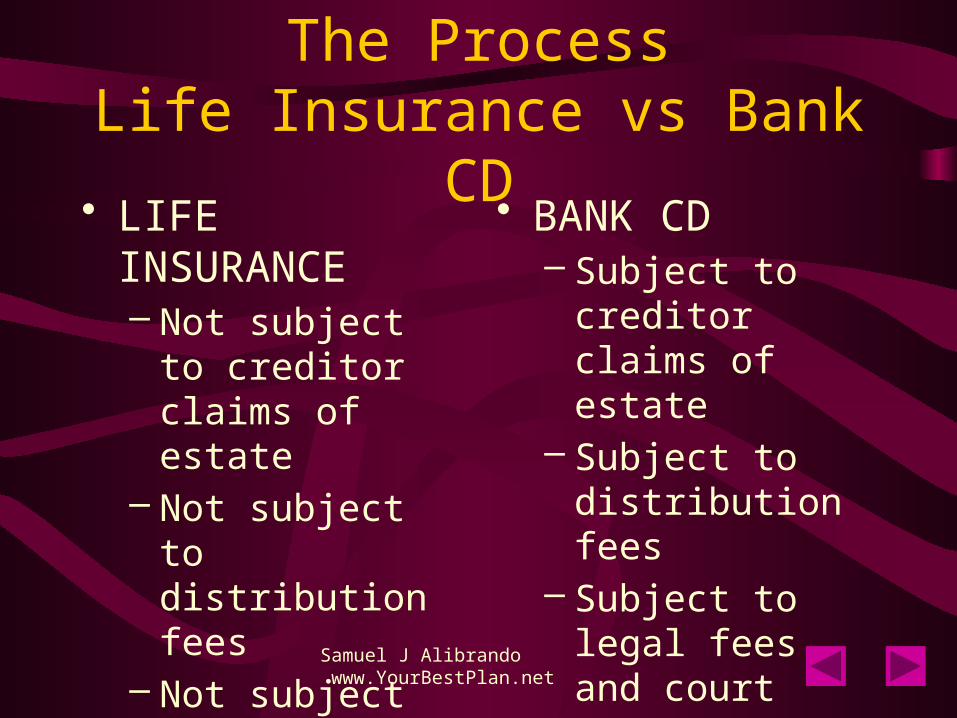

• The following comparisons assume all assets are owned by an individual not a trust

• Probate can tie up the distribution of proceeds for up to 2 years, however it can be less

Samuel J Alibrando www.YourBestPlan.net

The ProcessLife Insurance vs Bank CD

• LIFE INSURANCE– Not subject to

creditor claims of estate

– Not subject to distribution fees

– Not subject to legal fees

– Usually paid within 2 weeks of receiving death certificate

• BANK CD– Subject to creditor

claims of estate– Subject to

distribution fees– Subject to legal fees

and court costs– Usually paid within

2 years

Samuel J Alibrando www.YourBestPlan.net

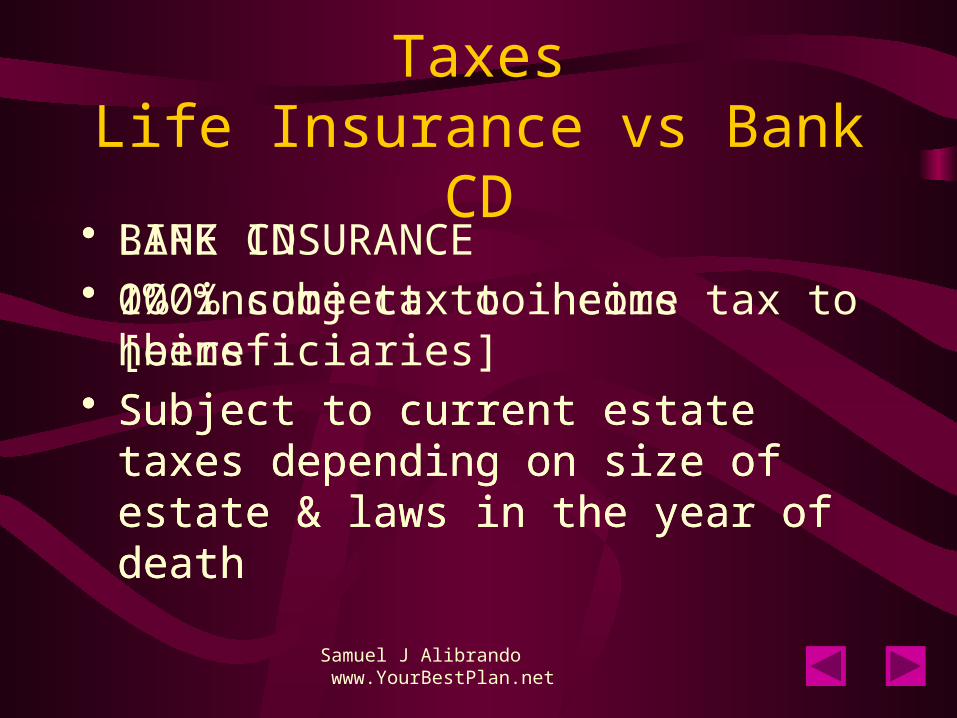

TaxesLife Insurance vs Bank CD

• LIFE INSURANCE• 0% income tax to heirs [beneficiaries]• Subject to current estate taxes depending on

size of estate & laws in the year of death

• BANK CD• 100% subject to income tax to heirs• Subject to current estate taxes depending on

size of estate & laws in the year of death

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

As a Savings

Why life insurance is better than saving at a bank

Samuel J Alibrando www.YourBestPlan.net

The Jar

• If your goal was to give $250,000 to your spouse, children, or grandchildren and you began putting money in a jar, how long would it take to save that money?

• What if you needed some money, would you take it from the jar?

Samuel J Alibrando www.YourBestPlan.net

Do You Believe in Saving?

• How much have you saved ON YOUR OWN? – Do not count your 401k from work

• Do you pay your bills?– A monthly deduction to pay a bill can also be

your savings

Samuel J Alibrando www.YourBestPlan.net

Why You Should Pay the Life Insurance Bill

• If you drop your life insurance– You lose your locked in rate

• Your rates will be higher every year due to your age• There are first year fees you must pay all over again

– You may be too unhealthy to get life insurance again

– If you do not rollover the cash value into another life insurance, you lose the growth momentum and efficiency of the cash value

Samuel J Alibrando www.YourBestPlan.net

If you stop putting money into a savings in a bank, you lose nothing, it simply grows slower

But there is more to a life insurance policy than a bank will ever offer

Samuel J Alibrando www.YourBestPlan.net

The Rich Friend• A life insurance company makes an agreement

with you to reach your savings goal for $250,000 in your jar

• If you put it in their “jar” and you die before reaching your goal, they will pay the full $250,000 to whoever you want- GUARANTEED

• If you don’t drop the policy your goal is GUARANTEED no matter when you die

• But there’s more . . .

Samuel J Alibrando www.YourBestPlan.net

More Perks in Life Insurance

• The interest paid is NOT taxed as it is growing. • Your interest IS taxed in a bank, stock or mutual

fund • The interest paid on your savings portion is more

than the bank pays but takes longer to catch up and show itself– Life insurance charges– Early administration & underwriting fees

Samuel J Alibrando www.YourBestPlan.net

More Perks in Life Insurance• You can take money out of your life

insurance savings “jar” and call it a loan– No income tax – Pay interest on the “loan” tax deductible and

then the insurance company will pay interest on the amount borrowed as though it was never removed from the “jar”

– Your net loan may be 1% or zero because of this arrangement

Samuel J Alibrando www.YourBestPlan.net

Will the Bank do that?• Allow your money to grow with ZERO taxation

every year?• CREDIT interest on money that you have

borrowed?• Guarantee in writing loans for the future at a net

1% or less no matter what future loan rates become?

• Pass your savings goal to whomever you want even if you die before your goal is reached?

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

The Most Flexible for Unpredictability

With Future Uncertainty,

Options are Paramount

Samuel J Alibrando www.YourBestPlan.net

Financial Crisis Scenarios

• You become temporarily unemployed• You have a medical emergency• A family member has an emergency and

desperately needs a loan from you• Something happens to your house that is not

insured• Some other unforeseen emergency

Samuel J Alibrando www.YourBestPlan.net

You don’t want to drop your current insurance and have to reapply at an older rate after the crisis

Good news – with your life insuranceYou have OPTIONS

Samuel J Alibrando www.YourBestPlan.net

Options with Life Insurance

• You can arrange to pay less premium each month

• Or you can allow your cash values to pay 100% until the crisis is over

• Or you can borrow money out of your cash values– You may pay back – You may choose to not pay back

Samuel J Alibrando www.YourBestPlan.net

Reasons You May Want to Put More $ Into Your Life Insurance Cash Growth• After comparing other financial products,

you want to add to your life insurance cash growth

• You want money to grow tax free but available to use BEFORE you are age 60

• You don’t want limitations on how much you save in tax-deferred savings

• Paying a “bill” is the only way you can save• You have a creative idea on self-financing

Samuel J Alibrando www.YourBestPlan.net

Creating Your Own Financing

• More people are using the tax-favorable treatment of life insurance cash growth to finance large purchases through their own life insurance

• By-passing the expense of finance companies, life insurance owners pay back their own loans into the policy thereby INCREASING the cash growth

Samuel J Alibrando www.YourBestPlan.net

Creating Your Own Financing

• If your business borrows from your life insurance, the interest paid into the policy on the loan is tax-deductible

• The additional money saved from going to finance companies is back in your pocket but is also getting interest

• While saving thousands on finance charges, life insurance owners are enhancing their own portfolios safely and without paying taxes on growth

Samuel J Alibrando www.YourBestPlan.net

Be Good to Your Policy

• If you are good to your policy by keeping it well-funded, your policy will be good to you– At a later age you may elect to STOP making

payments and allow cash value to cover your payments for the rest of your life

– You can elect to purchase a Paid Up policy for any amount your cash value can buy and never pay premiums again

Samuel J Alibrando www.YourBestPlan.net

Get Regular Income from Your Life Insurance

• In addition to stopping your payments– You may elect to receive monthly payments to

supplement your social security– You can elect to annuitize your cash value for

lifetime benefits– You can rollover all or part of your cash into a

different plan without paying any taxes on the rollover

Samuel J Alibrando www.YourBestPlan.net

Never Pay Income Taxes

• If you have invested $80,000 into your life insurance policy and you have $200,000 in cash value, you can withdraw $80,000 tax free

• The remaining $120,000 is taxable UNLESS you “borrow” the money out

• Your “loan” is deducted from your death benefit AFTER you die and you never pay income taxes on it because it was a loan & it was “paid back”

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

Permanent Insurance

The flexible options we just discussed are not possible with term

insurance

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

More Settlement Options

Genuine Options

Many do not know

Samuel J Alibrando www.YourBestPlan.net

Critical Illness• Many new life insurance policies allow for

a good percentage of your death benefit to be payable to you while you are alive, if you are in a critical health situation

• This amount is usually more than your cash value

• Portion of death benefit can also be paid for terminal illness

• Would a bank or other investment do this?

Samuel J Alibrando www.YourBestPlan.net

Tax Treatment on Critical Illness

• Terminally Ill– Payments are NOT taxable as income if life expectancy 24 months

or less

• Chronic Illness– Non-taxable payments may not exceed actual costs or $175/day– Must lack 2 necessary functions of daily living

Samuel J Alibrando www.YourBestPlan.net

Life Settlement Option

• A Life Settlement is the sale of an existing life insurance policy to a third party company for a lump sum of cash that is more than the cash surrender value.

• A life insurance policy is property, like a car, house, stocks and bonds that can be legally sold in accordance with applicable laws.

• Through a Life Settlement company, a policy owner can realize value today from an asset before death, even without a critical illness in lieu of the death benefit.

Samuel J Alibrando www.YourBestPlan.net

Life Settlement Companies• There are a growing number of well financed

companies that offer to buy your life insurance policy for a percentage of the face amount– Often this is if you are in your 70’s and the amount is

$250,000 or more. $100,000 is acceptable with some companies.

– You have an illness that is life threatening. This is attractive when life settlement companies offer more than your cash value or any amount the life insurance company is willing to pay.

– This is valuable when cash now is more important than the death benefit

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

Is There a Conclusion

Simple Reasoning

Samuel J Alibrando www.YourBestPlan.net

Compared to Banks & Most Investments

• Better tax treatment• Better liquidity• Better interest• Better guarantees• Better flexibility• More options• A Death Benefit far exceeding your cost

Samuel J Alibrando www.YourBestPlan.net

A Bill that Pays You Back

• Procrastination is your greatest enemy– Every month you delay

• Less money in• Less time to grow• Higher & higher life insurance age rate permanently• Greater risk of health issues [un-insurability or rate

up]

Contact via website: www.YourBestPlan.net

Samuel J Alibrando Copyright 2004

Are You Insurable?

Let the company pay,

at no risk to you,

to find out

Waiver

• Everything discussed here exists and possibly all in one policy but all policies and all life insurance companies do not offer everything discussed here.

• Ask for assistance by emailing: [email protected]

Samuel J Alibrando www.YourBestPlan.net

Related Documents