Consumers’ quantitative inflation perceptions and expectations in the euro area: an evaluation (*) Gianluigi Ferrucci (ECB), Olivier Biau (EC), Heinz Dieden (ECB), Roberta Friz (EC), Staffan Linden (EC) Conference on Consumer Inflation Expectations Federal Reserve Bank of New York, 18-19 November (*) The views expressed in this presentation are those of the authors and do not necessarily reflect those of the European Central Bank, the Eurosystem or the European Commission.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Consumers’ quantitative inflation perceptions and expectations in the

euro area: an evaluation(*)

Gianluigi Ferrucci (ECB), Olivier Biau (EC),

Heinz Dieden (ECB), Roberta Friz (EC), Staffan Linden (EC)

Conference on Consumer Inflation Expectations

Federal Reserve Bank of New York, 18-19 November

(*) The views expressed in this presentation are those of the authors and do not necessarily reflect those of the European Central Bank, the Eurosystem or the European Commission.

Motivation of the study

Quantitative inflation expectations based on consumer surveys relatively little analysed in the euro area

This study assesses the information content of a dataset collected for research purposes by the European Commission

Aim is twofold• discuss the usefulness of the data• refine the monitoring of survey-based consumers’

inflation expectations in the euro area

Outline

Main features of the survey

Key results

Why do euro area consumers overestimate inflation?- role of outliers- data quality- design of the survey questionnaire

Conclusions and future research

The quantitative dataset

Quantitative information on consumers’ inflation expectations (and perceptions) in the euro area is provided by the European Commission

Quantitative survey is part of the “Joint EU Harmonised Programme of Business and Consumer Survey”

• Consistent methodology across countries• Reliability of the data

Dataset is experimental• no official release following each data collection;• dissemination of the data is limited

Main features of the experimental survey

• National samples, focus on the euro area (all countries except NL)

• In total ca. 23,000 randomly selected consumers take part in the survey every month (for the euro area)

• Monthly frequency starting in May 2003 (to June 2010)

The quantitative questions

Two questions asked whenever respondent perceives or expects changes in consumer prices (in qualitative questionnaire):

• By how many percent do you think that consumer prices have gone up/down over the past 12 months? They have increased by ...% / decreased by ...%.

• By how many percent do you expect consumer prices to go up/down in the next 12 months? They will increase by ...% / decrease by ...%.

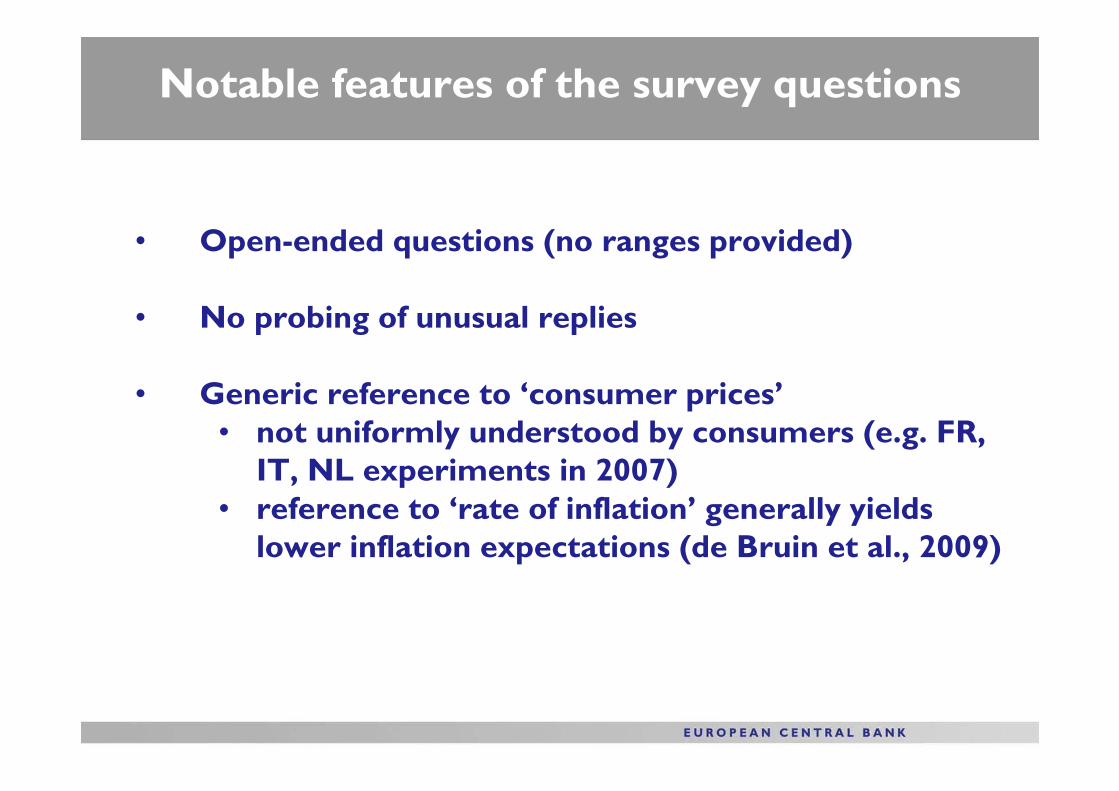

Notable features of the survey questions

• Open-ended questions (no ranges provided)

• No probing of unusual replies

• Generic reference to ‘consumer prices’• not uniformly understood by consumers (e.g. FR,

IT, NL experiments in 2007)• reference to ‘rate of inflation’ generally yields

lower inflation expectations (de Bruin et al., 2009)

(percent )

•Response rate of arund 75% for the euro area•But rather diverse picture cross countries

Source: European Commission.Note: as a percentage of respondents who believe that the inflation rate has changed or will change; average response rates

over the period May 2003 to June 2010.

Response rates to quantitative questions

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

1 0 0

A T B E D E E L E S F I F R I E I T L U P T SI C Y M T SK E A

I n f l a t i o n p e r c e p t i o n I n f l a t i o n e x p e c t a t i o n

Main findings

- Overestimation

- Dispersion across countries

- Demographics

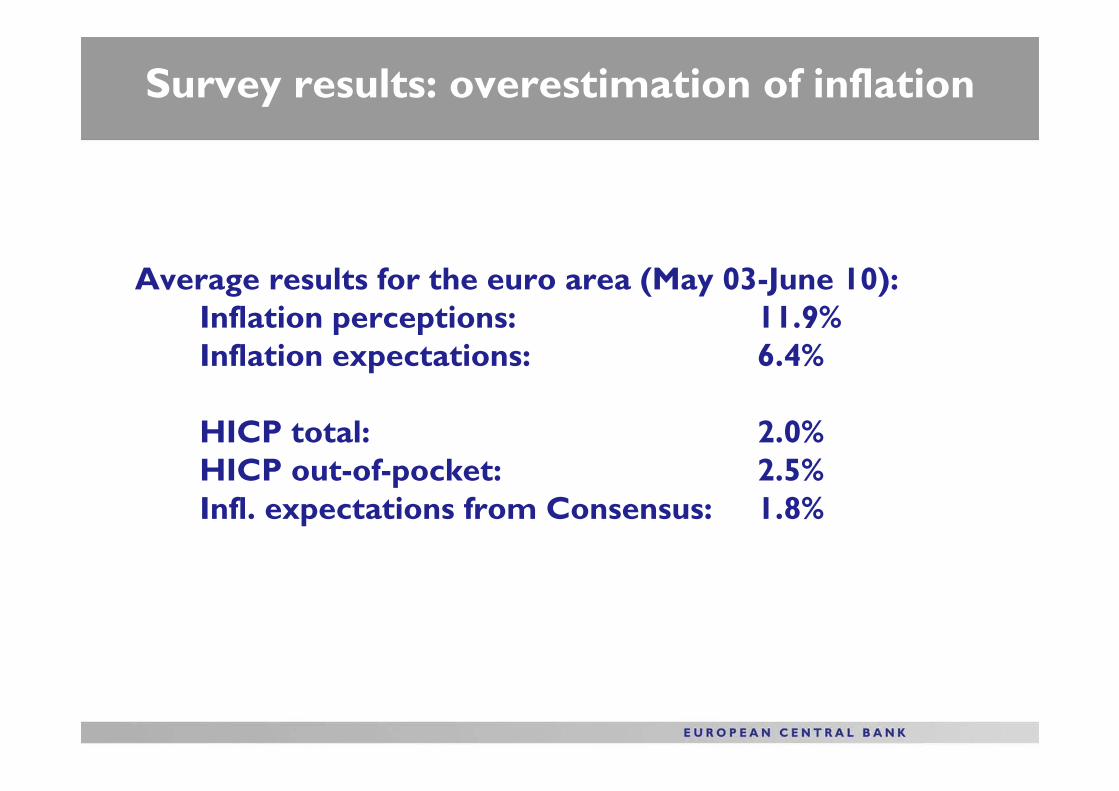

Survey results: overestimation of inflation

Average results for the euro area (May 03-June 10):Inflation perceptions: 11.9%Inflation expectations: 6.4%

HICP total: 2.0%HICP out-of-pocket: 2.5%Infl. expectations from Consensus: 1.8%

(annual percentage changes)

Sources: European Commission and Eurostat.Note: last observation: June 2010.

Evolution of households’ inflation estimates

-2

0

2

4

6

8

10

12

14

16

18

20

2003 2004 2005 2006 2007 2008 2009 2010

inflation perceptions

inflation expectations

HICP inflation

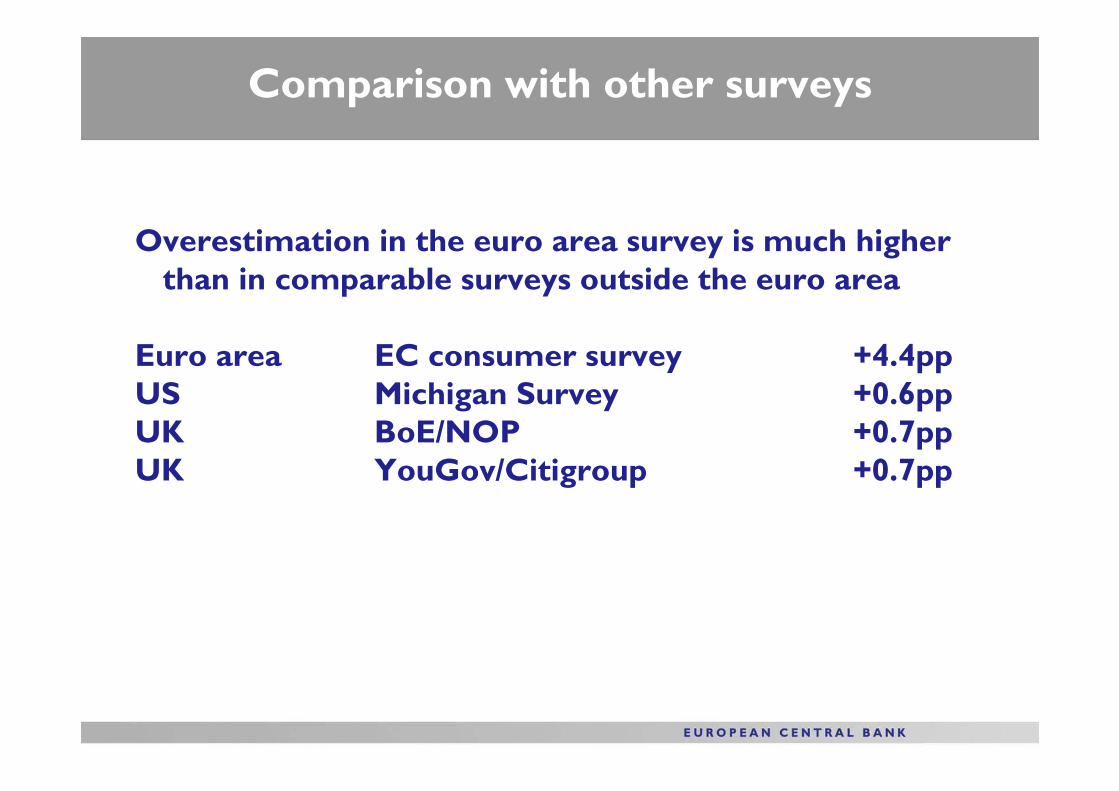

Comparison with other surveys

Overestimation in the euro area survey is much higher than in comparable surveys outside the euro area

Euro area EC consumer survey +4.4ppUS Michigan Survey +0.6ppUK BoE/NOP +0.7ppUK YouGov/Citigroup +0.7pp

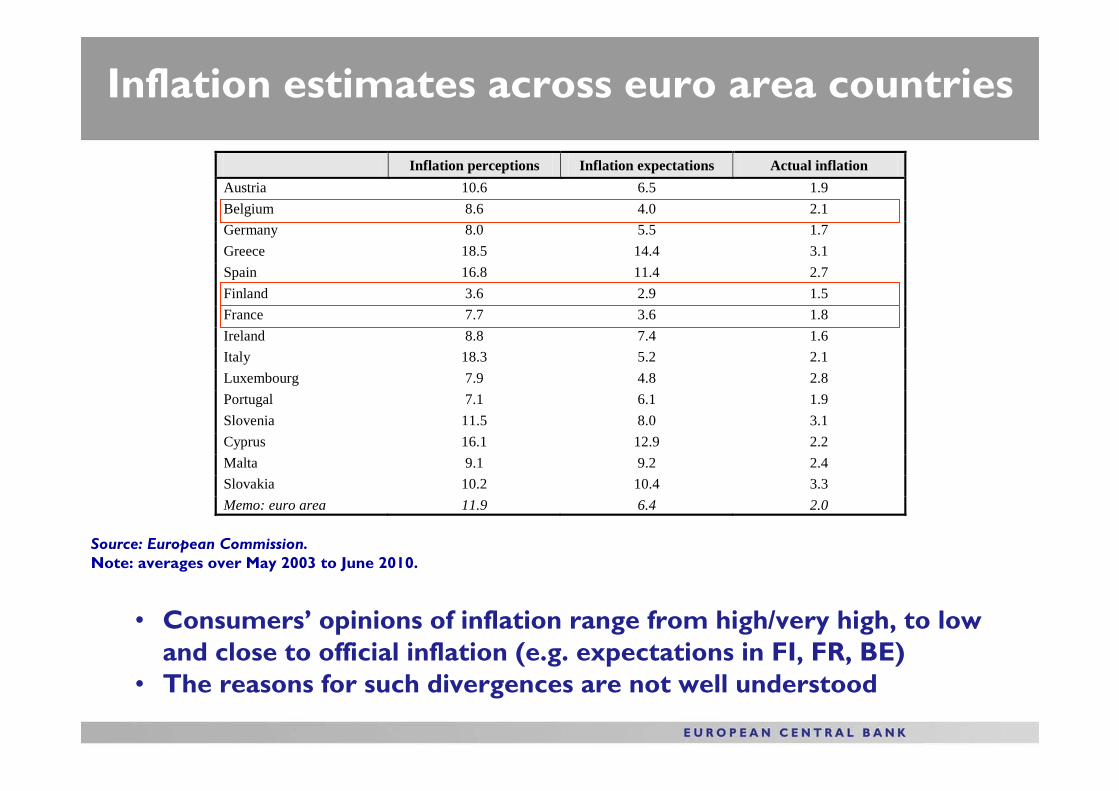

Inflation estimates across euro area countries

• Consumers’ opinions of inflation range from high/very high, to low and close to official inflation (e.g. expectations in FI, FR, BE)

• The reasons for such divergences are not well understood

Source: European Commission.Note: averages over May 2003 to June 2010.

Inflation perceptions Inflation expectations Actual inflation Austria 10.6 6.5 1.9 Belgium 8.6 4.0 2.1 Germany 8.0 5.5 1.7 Greece 18.5 14.4 3.1 Spain 16.8 11.4 2.7 Finland 3.6 2.9 1.5 France 7.7 3.6 1.8 Ireland 8.8 7.4 1.6 Italy 18.3 5.2 2.1 Luxembourg 7.9 4.8 2.8 Portugal 7.1 6.1 1.9 Slovenia 11.5 8.0 3.1 Cyprus 16.1 12.9 2.2 Malta 9.1 9.2 2.4 Slovakia 10.2 10.4 3.3 Memo: euro area 11.9 6.4 2.0

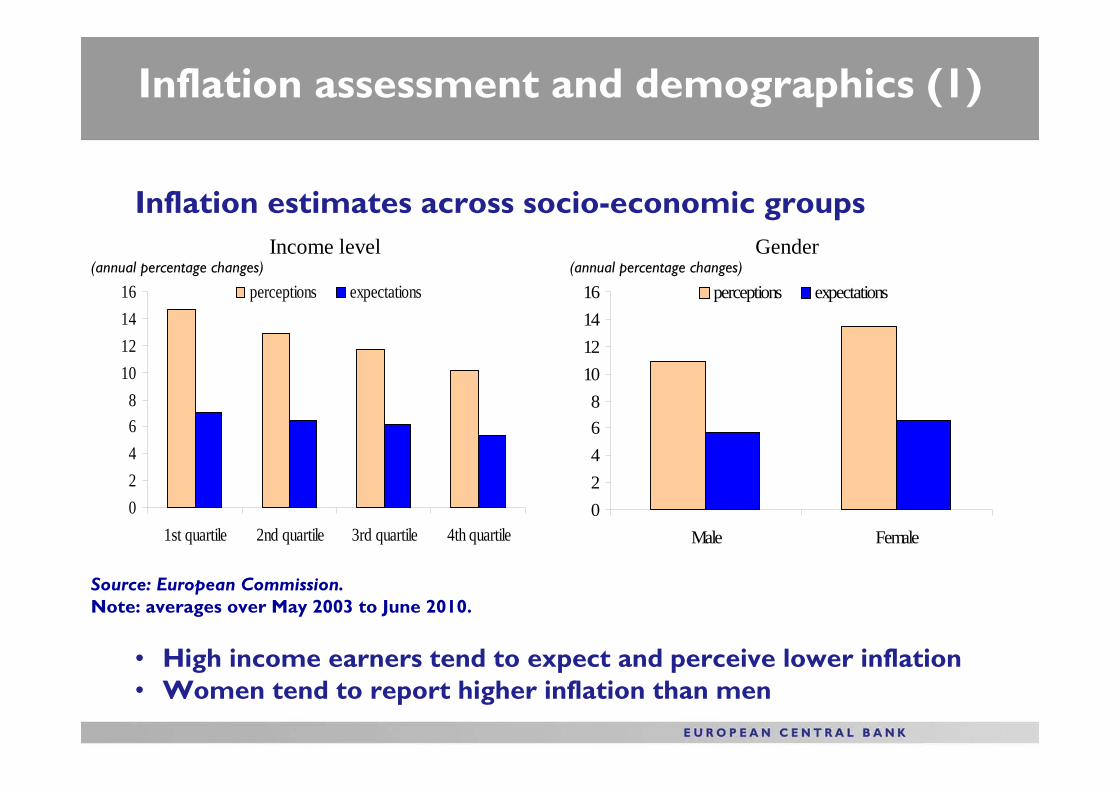

Inflation assessment and demographics (1)

Inflation estimates across socio-economic groups

• High income earners tend to expect and perceive lower inflation• Women tend to report higher inflation than men

Source: European Commission.Note: averages over May 2003 to June 2010.

Income level

02468

10121416

1st quartile 2nd quartile 3rd quartile 4th quartile

perceptions expectations

Gender

02468

10121416

Male Female

perceptions expectations

(annual percentage changes) (annual percentage changes)

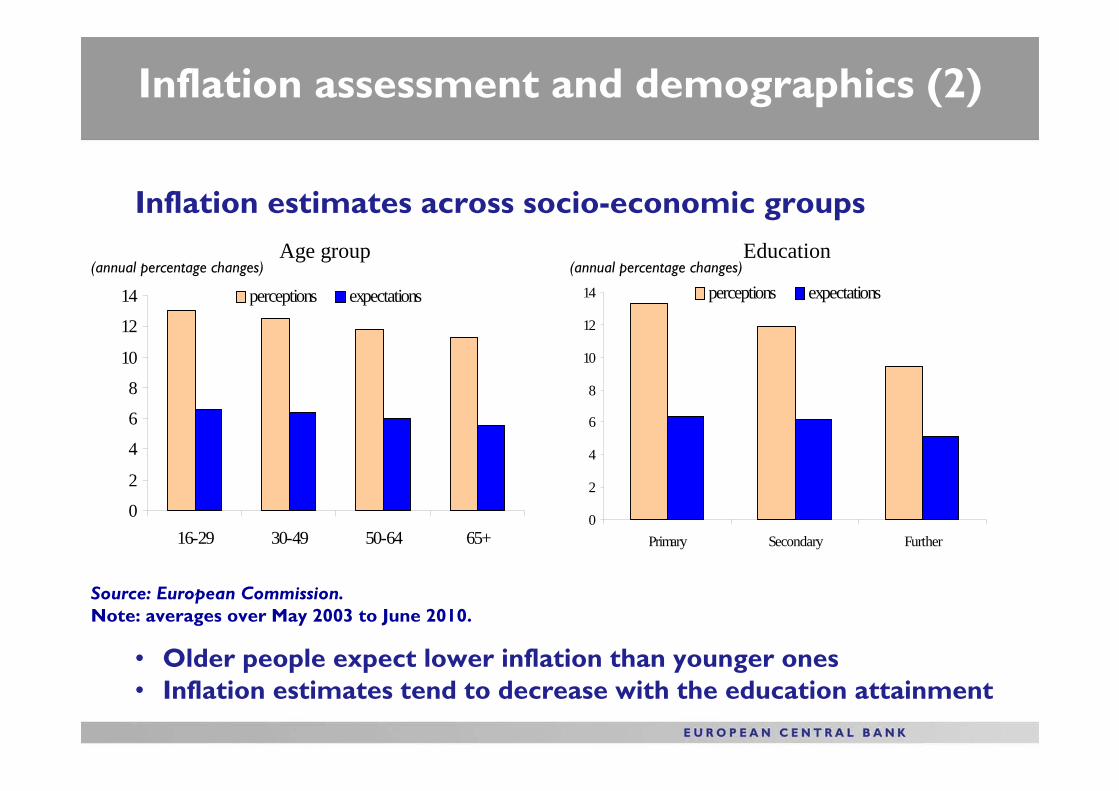

Inflation assessment and demographics (2)

Inflation estimates across socio-economic groups

• Older people expect lower inflation than younger ones• Inflation estimates tend to decrease with the education attainment

Source: European Commission.Note: averages over May 2003 to June 2010.

Age group

0

2

4

6

8

10

12

14

16-29 30-49 50-64 65+

perceptions expectations

Education

0

2

4

6

8

10

12

14

Primary Secondary Further

perceptions expectations

(annual percentage changes) (annual percentage changes)

Reasons for overestimation

Possible impact of:- Outliers- Data quality- Survey design

Reasons for overestimation: outliers?

Wide range of replies

For example:minimum expected rate of inflation: -200%maximum expected rate of inflation: 800%

…but the number of such extreme replies is small

Digit preference e.g. 0%, 2%, 5%, 10%, 20%

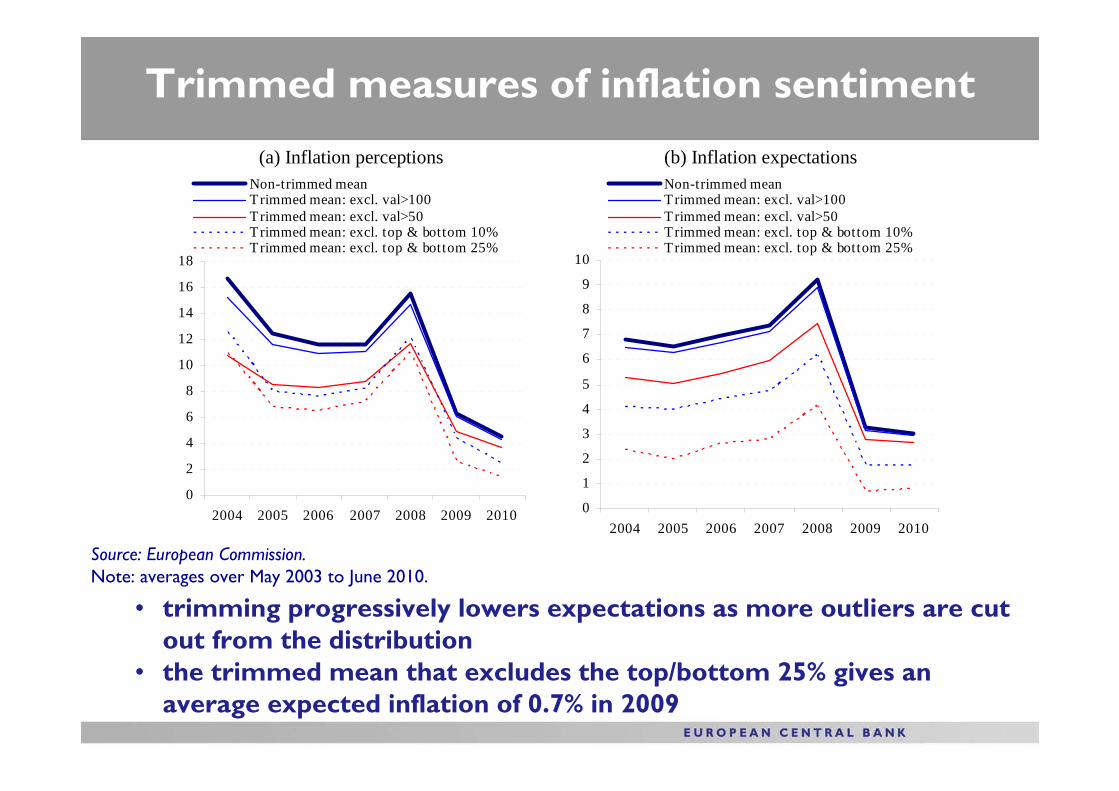

Trimmed measures of inflation sentiment

• trimming progressively lowers expectations as more outliers are cut out from the distribution

• the trimmed mean that excludes the top/bottom 25% gives an average expected inflation of 0.7% in 2009

Source: European Commission.Note: averages over May 2003 to June 2010.

(a) Inflation perceptions

0

2

4

6

8

10

12

14

16

18

2004 2005 2006 2007 2008 2009 2010

Non-trimmed meanTrimmed mean: excl. val>100Trimmed mean: excl. val>50Trimmed mean: excl. top & bottom 10%Trimmed mean: excl. top & bottom 25%

(b) Inflation expectations

0

1

2

3

4

5

6

7

8

9

10

2004 2005 2006 2007 2008 2009 2010

Non-trimmed meanTrimmed mean: excl. val>100Trimmed mean: excl. val>50Trimmed mean: excl. top & bottom 10%Trimmed mean: excl. top & bottom 25%

Controlling for outliers: the median

Median of consumers’ inflation assessment in the euro area

• The median as a summary statistic that is less sensitive to outliers• Owing to the prevalence of round digits, median tends to exhibit

discrete jumps

Source: European Commission.

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2004 2005 2006 2007 2008 2009 2010

median perceptionsmedian expectationsHICP inflation

Reasons for overestimation: data quality?

Possible measurement and data quality issues:“data entry” errorsin the validation processes in the data collection

Question misunderstood?Concept “annual percentage change” unknown?

CheckData entry and validation processes Methods for outlier correction, e.g. “probing question”

Reasons for overestimation: survey design?

Michigan survey in the US probes unusual replies

BoE/NOP and YouGov/Citigroup surveys for the UK provide brackets of responses

Reasons for overestimation: survey design?

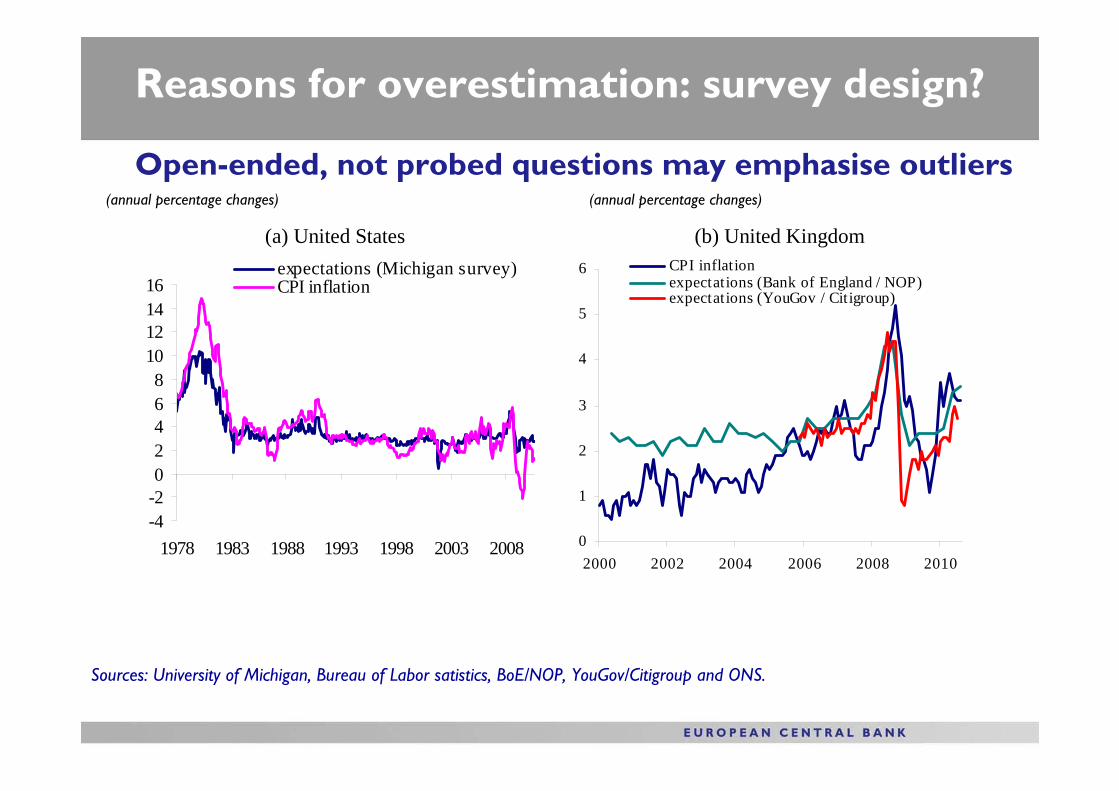

Open-ended, not probed questions may emphasise outliers

(a) United States

-4-202468

10121416

1978 1983 1988 1993 1998 2003 2008

expectations (Michigan survey)CPI inflation

(b) United Kingdom

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010

CPI inflationexpectations (Bank of England / NOP)expectations (YouGov / Citigroup)

Sources: University of Michigan, Bureau of Labor satistics, BoE/NOP, YouGov/Citigroup and ONS.

(annual percentage changes) (annual percentage changes)

Reasons for overestimation: survey design?

UK consumers’ estimates of inflation expectations

• UK as a natural experiment to test the effect of ranges of reply• Expectations tend to track actual inflation closely when consumers

select their replies from given ranges

Sources: European Commission, BoE/NOP and ONS.

0

2

4

6

8

1 0

1 2

1 4

2 0 0 0 2 0 0 2 2 0 0 4 2 0 0 6 2 0 0 8 2 0 1 0

C P I i n f l a t i o ne x p e c t a t i o n s ( B a n k o f E n g l a n d / N O P )e x p e c t a t i o n s ( E C C o n s u m e r S u r v e y )

Conclusions

Tentative evidence that overestimation of inflation by euro area consumers is affected by the survey design (no probing question) and heterogeneous interpretation of survey question

Outliers play a more modest role

Euro area consumers hold very different opinions of inflation depending on their income, age, education and gender

Wide dispersion of responses across countries

Future research

• Trial ‘probing question’ (as in the US survey)

• Ranges of responses (as in the UK surveys) might reduce the overestimation, but do they add a different bias?

• Refer to ‘rate of inflation’ (as opposed to ‘prices in general’; see van der Klaauw et al, 2008)

• Investigate why answers are closer to the official inflation rate in some countries than in others

• Monitor inflation expectations in the medium term (2 to 5 years ahead)

Related Documents