What the world thinks CONSUMER INSIGHTS PANEL FMCG from the outside in Survey Debate Report Consumers, Brands and Corporates Loyalty and trust at the centre of strategy

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

What the world thinks CONSUMER INSIGHTS PANEL FMCG from the outside in

Survey Debate Report

Consumers, Brands and Corporates Loyalty and trust at the centre of strategy

M

eet

the

Co

nsu

mer

Insi

gh

ts P

anel

1 | Consumer insights

Dr Dag Bennett Director of the Ehrenberg Centre for Research in Marketing

Director of the Ehrenberg Centre for Research in Marketing. Dag’s research focuses on branding, buying behaviour, and developing markets.

Liz Claydon UK Head of Consumer Markets, KPMG

Liz is a transaction services specialist, with particular experience in advising FMCG companies. She has advised on some of the largest cross border deals of recent years.

Scott Corfe Managing Economist, Centre for Economics and Business Research

Scott authors and coordinates Cebr’s award-winning thought leadership, public policy and strategic research.

Martin Deboo Consumer Goods Analyst, Jefferies International Ltd

Martin makes investment recommendations on major consumer goods fi rms. His 30yr career has spanned both the worlds of marketing and branding on the one hand, and strategy and fi nance on the other.

Jeremy Garlick Partner, Insight Traction

Jeremy advises FMCG companies on how to win with consumers, via category, channel and marketing strategies. Previously Jeremy led the insight teams at Sainsbury’s, Premier Foods and Waitrose, and worked in insight for PepsiCo.

Jim Grover Senior Consumer Markets Strategy Advisor at KPMG

Formerly Jim was the Strategy Director and a member of the Executive Committee at Diageo PLC.

Tim Kelly Senior Consumer Markets Advisor NBGI Private Equity

Previously Tim has held senior positions at Premier Foods, RHM, Constellation Brands, Diageo, Cola-Cola and Unilever.

Melanie Leech Director General, Food and Drinks Federation

The largest trade association in the UK representing food and drink manufacturers.

Gail Lumsden Head of Strategy and Planning, SABMiller

Gail joined SABMiller PLC in 2004 and is responsible for corporate strategy. Prior to this Gail held senior roles in strategy, fi nance and business development for Diageo/GrandMet.

Joe Petyan Executive Partner, JWT London

Joe has worked on domestic and international business in across FMCG, media, telecoms and fi nancial services and jointly leads the JWT London agency.

Louise Vacher Consulting Director, YouGov

Louise has worked in research for over 25 years, for major agencies in the UK and Australia as well as at Nestlé UK.

Keith Weed Chief Marketing & Communications Offi cer, Unilever

Keith is a member of the Unilever Executive Committee and holds other key external positions such as Chair of the Consumer Industry Board at the World Economic Forum, and Chair of the International Board of Business in the Community.

Consumer insights | 2

FOREWORD The Consumer Insights Panel is a forum of thought leaders with extensive FMCG experience that come together to discuss, debate and challenge ideas and customer insights on a quarterly basis.

The FMCG industry is always hungry for new ideas and insights to help manage the complexity of the world around it. Driven by the views of the consumer through bespoke surveys run by YouGov, our Panel applies new thinking to complex issues both current and emerging.

In this, the Panel’s inaugural debate, we looked at the relationship between consumers and brands in terms of loyalty and trust. As the debate shows, there is no one view but, there are a lot of ideas and new approaches. We believe that – by sharing our views, insights and experiences – we can help FMCG organisations create new strategies and take advantage of new opportunities in the marketplace. As such, we welcome you to the first edition of the Consumer Insights Panel debate report. On behalf of the Panel, we would like to thank YouGov and all of the respondents that participated in our survey.

To learn more about the Consumer Insights Panel, or to receive future debate reports, we encourage you to visit consumerinsightspanel.org

CONTENTS Executive Summary

The Nexus between trust and loyalty

The relationship between corporate brands and trust

How much does price really matter?

The impact of social media on trust

Our research

3 | Consumer insights

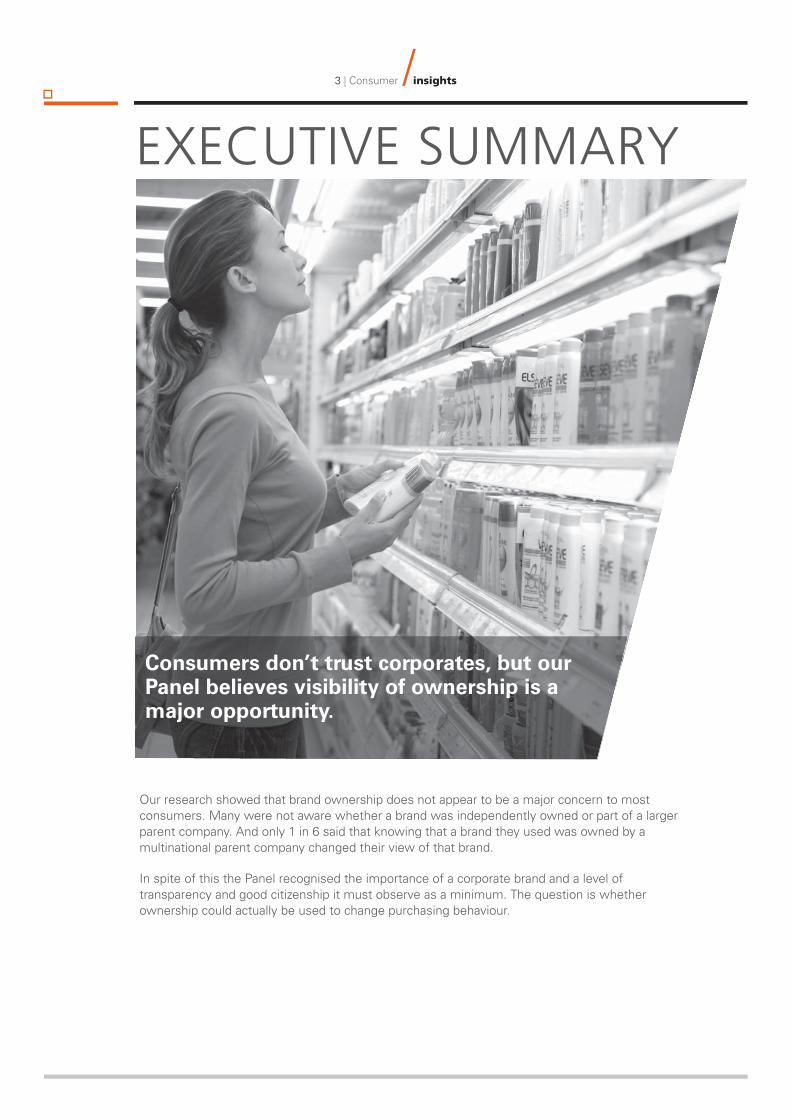

EXECUTIVE SUMMARY

Consumers don’t trust corporates, but our Panel believes visibility of ownership is a major opportunity.

Our research showed that brand ownership does not appear to be a major concern to most consumers. Many were not aware whether a brand was independently owned or part of a larger parent company. And only 1 in 6 said that knowing that a brand they used was owned by a multinational parent company changed their view of that brand.

In spite of this the Panel recognised the importance of a corporate brand and a level of transparency and good citizenship it must observe as a minimum. The question is whether ownership could actually be used to change purchasing behaviour.

Consumer insights | 4

The consumers we asked said that being open and transparent and paying the appropriate levels of tax, ranked well above fair-trade and environmental standards, in determining whether to trust a company. Our survey showed a high level of cynicism, around the latter…

66% believe companies are doing the bare minimum

66% don’t always believe what companies say they are doing

It raises the question as to whether FMCG players should actively be increasing visibility and consumer awareness of ethical corporate activity? There’s a real opportunity here, as the impact of corporate brands on consumers is not yet fully realised, and our Panel believes we’ll see an upsurge in corporate pursuit to harness this as a differentiator.

The jury is out on social media

Perhaps most at odds with the survey results were the panel’s opinions around social media. Whilst the research showed that…

28%

of respondents have started buying new brands as a result of discovering or learning about them via social media, and

31%

have changed their brands as a result of recommendations from friends on social media

… the panel believe that the jury is still out on whether all those ‘clicks’ and ‘likes’ translate to sales and suggest that ultimately they consider it just another tool in a marketer’s armoury.

We’re seeing marketing evolve from ‘push’, ‘tell’, ‘broadcast’ models to those that embrace consumer engagement. Consumers want to talk to each other and to interact with brands; not just be told. There is little doubt that this digital dialogue will continue to democratise brands and simultaneously level the playing fi eld for new smart and agile entrants, that can now establish and build brands through social media.

The world is getting louder in the digital age and, as the volume of information and choice increases at pace, overwhelmed consumers may just decide to cut through it all and revert to what they know best – established brands that they can trust. Relying on that outcome however is not an option. Listen, engage and respond is the new order. Our panel agreed that there is no industry more or less likely to experience the effect of brand democratisation, neither is there safety in size nor longevity in the marketplace.

5 | Consumer insights

TO

PIC1 THE NEXUS BETWEEN

TRUST AND LOYALTY

What is the relationship between loyalty and trust? Can brands win loyalty if they don’t have trust or is trust just a ‘nice to have’? We asked our Consumer Insights Panel how they defined the difference between loyalty and trust.

Habitual purchasing behaviour can be seen to translate to a form of brand loyalty. Most consumers tend to buy within a range of brands and we’d argue that it is, in fact, quite unusual for anyone to buy the same item time and time again. Brand loyalty can be considered behavioural. It can be created by providing a winning proposition to consumers and success can be measured and quantifi ed. Brand owners that build advocacy models to track this are unlikely to be singularly chasing the Holy Grail of a consumer that always and only buys their brand, but rather competing like mad at the moment when a consumer is choosing from within their established repertoire.

Signifi cantly, a third of the respondents who took part in our research said they used to stick to a specifi c brand or set of brands, but over the last few years they have tended to choose brands based on factors such as price.

We have seen consumer loyalty decline during a price-sensitive recession, and increased variety, accessibility, comparability, and transparency through digitalisation means that it continues to decrease.

The marketplace is increasingly characterised by unpredictability, diminishing product differentiation and heightened competitive pressure, which means that loyalty is all the more important for brand owners.

If brand loyalty is understood as habitual, even transactional, behaviour that is created by brand owners persuading us to buy more, then where does trust come in? Our Panel describes trust as an emotional connection, which is created over the long term by establishing a relationship that is stronger than any discount. To put it simply, trust relates to consumer identifi cation with brand values – not to be confused with value; we’re talking trust related to principles and ideals.

Consumer insights | 6

Trust doesn’t necessarily buy you loyalty, but lack of trust can destroy it! Liz Claydon

According to our research, there doesn’t seem to be a strong relationship between the extent to which consumers trust brands and the extent to which they are loyal to them.

The personal care category received the lowest scoring for trust, but the highest levels of brand loyalty

Conversely...

The household goods category saw the highest rating of trust, but lowest level of brand loyalty

The above results exemplify two factors at play: there doesn’t seem to be a strong relationship between loyalty and trust, and it varies cross category.

Let’s consider the latter for a moment, and look at the loyalty/trust relationship across other sectors. Banking is characterised by low levels of trust but high levels of loyalty, largely due to apathy and the diffi culty of switching. The reverse is perhaps true of airlines: ‘I trust Ryanair to fl y planes safely, but I have no loyalty to them’. Our Panel debated whether trust and loyalty become more intertwined at higher-end categories or if, in fact, you can turn any product into a highly emotional/aspirational category. The consensus was that the more a category is commoditised, the more difficult it is to build emotional connections with customers that drive trust, but it’s nevertheless the aim and is more important than ever.

You can’t do anything to engender brand loyalty, but you can try to build trust. Jeremy Garlick

Building on this statement the Panel distinguished between the type of loyalty currently tracked by the industry – that which is reliant on repeat purchasing behaviour and measured as penetration to demonstrate market share – and a more enduring loyalty that is born of trust. To put it another way, loyalty without trust is simply apathetic purchasing behaviour. So, to achieve the loyalty that matters, should brands be concentrating on generating trust?

I think trust is becoming a more important issue, but not at a brand level, at a corporate level. The role of the corporate brand is coming of age… Keith Weed

PANEL MEMBER’S THOUGHTS...

“It’s an inconvenient truth that you can’t target loyalty. You can only target penetration. Loyalty and penetration are just correlated. If you’re looking for growth, it has to be about penetration first.”

Martin Deboo

“There’s not a whole lot you can do about loyalty except to make the brand bigger, then your loyalty goes up. It’s not the other way round. “

Dr Dag Bennett

“I feel that the more a category is commoditised, the more difficult it is to build those emotional connections with customers that drive trust.” Jim Grover

7 | Consumer insights T

OP

IC 2 THE RELATIONSHIP BETWEEN CORPORATE BRANDS AND TRUST

With many corporate brands starting to strut their stuff to consumers, observers are wondering how much value a strong corporate brand provides to the individual brands. We asked our Consumer Insights Panel whether they saw benefi ts in building up a corporate brand.

The Panel recognised that good corporate citizenship and a level of transparency is the minimum standard that corporates need to observe these days. The question is whether it actually causes positive dispositions and changes purchasing behaviours.

The FMCG industry and its investors are, of course, highly focused on social and environmental sustainability programmes, but are consumers aware of all the good work that is being done? Would they pay a premium to know this integrity sits behind the brands that they buy? And would adding this dimension to individual brand values increase levels of trust across a portfolio of products?

It’s the difference between a product to buy and an idea to buy into. Joe Petyan

Our research showed that while consumers have a greater propensity to trust long established British and independently owned companies, brand ownership does not appear to be a major concern to most. The consumers we surveyed were often not aware whether a brand is independently owned or part of a larger parent company. And only 1 in 6 said that knowing that a brand they used was owned by a multinational parent company changed their view of that brand.

In some markets and categories, there is a cultural and social dynamic at play where consumers perceive big brands from corporate behemoths to be less relevant to them. Gail Lumsden

Consumer insights | 8

There’s actually an argument to be made that bigger brands in other sectors are in trouble. They risk losing their personal connection with the consumer and that will impact upon their brand loyalty. The same could be said for pinning all of your individual brands up under a big corporate banner. A catastrophic failure in one brand or category could spill over into non-related categories that carry the same corporate brand.

In balance there are other, less obvious, factors to consider. Keith Weed explained one proof point for Unilever: since it really started to focus on the corporate brand it has gone from being a top twenty employer for marketers to currently being number two, right behind Google.

Attracting the best talent improves our capabilities, transparency and ultimately brand value. Keith Weed

There are also different regional attitudes to take into account. In the developing markets at least, multinational brands seem to enjoy greater trust than most local brands and are often more trusted than the government itself.

Our research on this topic was carried out in the UK and the results around standards of behaviour that might contribute to trust in a company or brand speaks volumes.

20% of respondents said they don’t consider brand values in their purchasing decisions at all

66% believe companies are doing the bare minimum

66% don’t always believe what companies say they are doing

It’s clear there is a general level of cynicism amongst consumers about large organisations, and that consumers tend to place more trust in individual brands than in parent companies. Recent media coverage of organisations exploiting tax loopholes or not providing transparent information about the way they do business has plainly had an impact [see results page 15].

It is also evident that the public’s knowledge of brand ownership is patchy, and over half the respondents would like more clarity about who owns which brands. It would seem that it’s not just a question of transparency – which has become a buzzword of the digital age – but also about actively increasing visibility and consumer awareness of ethical corporate activity. There’s a real opportunity here, as the impact of corporate brands on consumers is not yet fully realised, and our Panel believes we’ll see an upsurge in corporate pursuit to harness this as a differentiator.

The consumers we surveyed were split with regards to how they thought companies should finance social and economic sustainability programmes. Just over half thought companies should put these aspects before profi t, while one-third believed it was acceptable to increase prices to enable investment in these areas. What is clear, however, is that consumers largely base their trust on factors that directly affect them, specifi cally fair pricing and quality.

PANEL MEMBER’S THOUGHTS...

“You can no longer treat branding and social impact as separate.” Gail Lumsden

“The big FMCG players need to prove to consumers that they are not merely paying lip service to their corporate responsibility programmes.”

Liz Claydon

9 | Consumer insights T

OP

IC 3 HOW MUCH DOES PRICE REALLY MATTER?

For some consumers price is everything. Clearly, price impacts purchase decisions, but what impact does it have on brand loyalty and trust? We asked our Consumer Insights Panel whether price should be the top consideration for brands going forward.

I’d argue that it isn’t really about price but rather about value. When the value equation goes wrong, the pricing goes askew. But I think from a business perspective we lazily think of it all as price. Jim Grover

There is an equation that we all use, where we compute price as a value for what we can afford, what we want to spend and even how we feel that day. We make these trade-offs on a constant basis and it’s up to the brand marketers to convince us it’s worth paying the premium. Joe Petyan

Consumer insights | 10

Brands play an important role in establishing the value equation by communicating the product proposition to consumers. Brands simplify our lives, you know what you’re going to get and they give you reliable quality, day in, day out.

People, on average, spend twelve seconds in the laundry aisle buying a laundry product. The reason people are able to spend just twelve seconds is because branding simplifies it. The brand story is here to stay. Keith Weed

The fact that price has become more important to consumers has signifi cantly raised the bar for brand marketers. Pricing is part of the marketer’s tool kit, and whilst using lower prices and promotional pricing to grow sales might be attractive in the short term, it’s not the way to build a sustainable business.

Some brands hurt themselves with what almost amounts to an addiction to promotions. Yes, they provide a hit in sales, but it’s very short-term and ultimately it can impact the perceived value of the brand. Our Panel believes that most brand owners aren’t even exploring the question of what promotions do to brand loyalty.

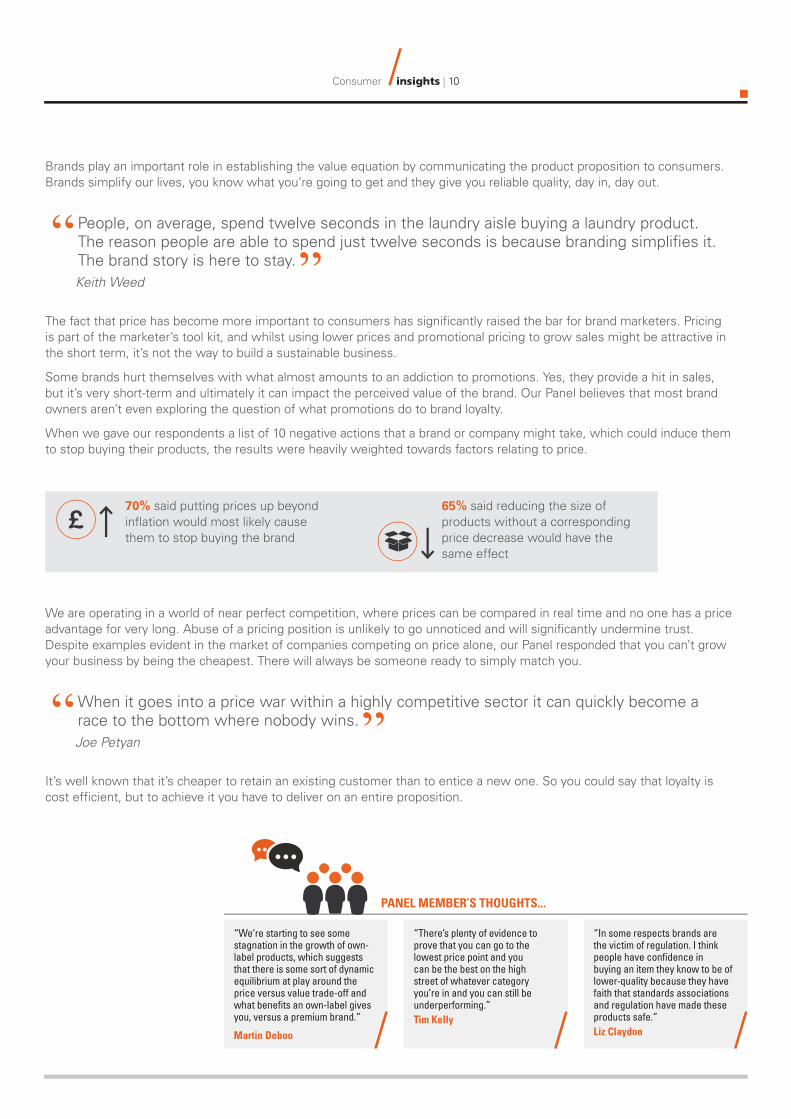

When we gave our respondents a list of 10 negative actions that a brand or company might take, which could induce them to stop buying their products, the results were heavily weighted towards factors relating to price.

70% said putting prices up beyond infl ation would most likely cause them to stop buying the brand

65% said reducing the size of products without a corresponding price decrease would have the same effect

We are operating in a world of near perfect competition, where prices can be compared in real time and no one has a price advantage for very long. Abuse of a pricing position is unlikely to go unnoticed and will signifi cantly undermine trust. Despite examples evident in the market of companies competing on price alone, our Panel responded that you can’t grow your business by being the cheapest. There will always be someone ready to simply match you.

When it goes into a price war within a highly competitive sector it can quickly become a race to the bottom where nobody wins. Joe Petyan

It’s well known that it’s cheaper to retain an existing customer than to entice a new one. So you could say that loyalty is cost effi cient, but to achieve it you have to deliver on an entire proposition.

PANEL MEMBER’S THOUGHTS...

“We’re starting to see some stagnation in the growth of own-label products, which suggests that there is some sort of dynamic equilibrium at play around the price versus value trade-off and what benefits an own-label gives you, versus a premium brand.”

Martin Deboo

“There’s plenty of evidence to prove that you can go to the lowest price point and you can be the best on the high street of whatever category you’re in and you can still be underperforming.” Tim Kelly

“In some respects brands are the victim of regulation. I think people have confi dence in buying an item they know to be of lower-quality because they have faith that standards associations and regulation have made these products safe.” Liz Claydon

11 | Consumer insights

TO

PIC 4

THE IMPACT OF SOCIAL MEDIA ON TRUST

Will social media replace traditional advertising or is it simply a tool for complaint handling and resolution? We asked our Consumer Insights Panel what role they thought social media should play in the marketing mix of the future.

None of us likes to admit we can be infl uenced by brands but we’re often happy to admit that we took our friends’ advice. Word of mouth has always been very powerful, but the impact of social media is more than simply moving the traditional ‘pub chat’ online and into forums. Consumers are starting to feel more confi dent about their point of view – whether they are right or wrong – and that drives advocacy. This is backed up by our research, which showed that user-generated content is three times as likely to be trusted as content from brands.

28% of respondents have started buying new brands as a result of discovering or learning about them via social media

25% have changed their brands as a result of recommendations from friends on social media

Controversially, Dr Dag Bennett argued that his research showed social media activity didn’t necessarily translate into purchasing.

We’ve looked at whether people buy the brands they like and found that there’s a very small connection, around 1%. Liking is a click – it’s easy and it rarely translates into committing to a purchase. Yes, there’s a lot of engagement but in terms of the effect it has on purchasing behaviour, I think the jury is still out. Dr Dag Bennett

There’s no doubt that there’s a difference between meaningful engagement and just engagement. The world is getting louder and we’re all on a steep learning curve to understand how to fi lter out what is and isn’t relevant to our lives.

Consumer insights | 12

We should also distinguish between the short-term transitory interaction that’s there one minute and gone the next – such as a tweet – and a long-term interaction with a brand that you come into contact with and are exposed to in varying ways. Dr Dag Bennett

Of course, certain media choices are used to fulfi l certain roles and social media can’t naturally fulfi l all of those roles. The UK consumers we asked actually said they trusted social channels less, in comparison to other advertisement channels.

Trust in channels as information sources

Consumer bodies, eg Which? 23% 51% Web sites where customers can give their opinion

or review products, eg Mumsnet, blogs etc 18% 39%

TV advertising 6% 25%

Social media - posts and “likes” by my friends 7% 25%

Social media - company/ brand pages 4% 16%

I think if we ran this research in China – or almost anywhere in the developing world, where mobile penetration is high – you’d probably see very high levels of trust in social media, particularly versus TV, which is often state owned.

Louise Vacher

Digital plainly offers a scale that can facilitate global exposure. On top of which, user generated content, recommendations, and ‘likes’ from friends are a clear preference over company or brand pages. But our panel suggests that ultimately it’s just another tool in a marketer’s armoury, and traditional advertising remains highly effective. We are however seeing marketing evolve from ‘push’, ‘tell’, ‘broadcast’ models to those that embrace consumer engagement. Consumers want to talk to each other and to interact with brands; not just be told. This new world of dialogue and democratisation of brands through digital, means that the old principals of honesty and openness are more important than ever before.

As a marketing tool however, social media means that there’s no such thing as a predictable audience size. The way information and content spreads in this medium is rarely linear, rather it’s exponential, and so is its impact. As well as potential loss of control, a real watch-out for established brand owners is how social media lowers the barrier of entry to new players. Digital reduces the cost of establishing and then sustaining a brand. Now innovative, smart, agile young companies can reach mass markets and create a brand more quickly than ever before. In this way digital activity ultimately increases choice and therefore competition, which in turn heightens the fi ght for consumer loyalty.

The world is getting louder in the digital age and, as the volume of information and choice increases at pace, overwhelmed consumers may just decide to cut through it all and revert to what they know best – established brands that they can trust. In this way, big brands really could win out by simplifying our lives. Relying on that outcome however is not an option. Listen, engage and respond is the new order. Our panel agreed that there is no industry more or less likely to experience the effect of brand democratisation, neither is there safety in size nor longevity in the marketplace.

PANEL MEMBER’S THOUGHTS...

“It’s worth noting that none of the three shortlisted brands for the marketing society’s Marketing on a Shoestring award are social media campaigns. They’ve all used broadcast media and they are young brands in their infancy.” Joe Petyan

“Brands cannot just push campaigns onto social media and assert their power, they need to be thoughtful, personalise, respond to feedback, even learn how to co-create.” Tim Kelly

13 | Consumer insights

THE RESEARCH

What factors were considered most important when determining the level of trust in a company?

Fair pricing 23% 51%

Providing high quality products 18% 39%

Being open and transparent 15% 37%

Paying appropriate levels of tax 6% 25%

Listening and responding to customers 7% 25%

Treating suppliers fairly 4% 18%

Treating employees fairly 2% 17%

Support local suppliers 4% 16%

Helping improve consumers’ lives 5% 15%

Leadership behaving ethically 6% 15%

Minimising environmental impact 4% 15%

Controlling pay levels of top executives 3% 12% In top 3

Providing consumers with information/consumer education 2% 9% Most important

Philanthropy /charity support 1% 2%

Acting in a less environmentally friendly way to save money was found to have less impact on brand choice, than other aspects:

63% 62% 63% 61%

including exploiting treating employees management paying top tax loopholes unfairly behaving executives apparent

unethically excessive rates of pay/bonuses

What actions are most likely to cause a consumer to stop buying a brand?

said putting prices said reducing the size up beyond inflation of products without

would most likely to 70%cause them to stop

a corresponding price 65% decrease would have

buying brand the same effect

Consumer insights | 14

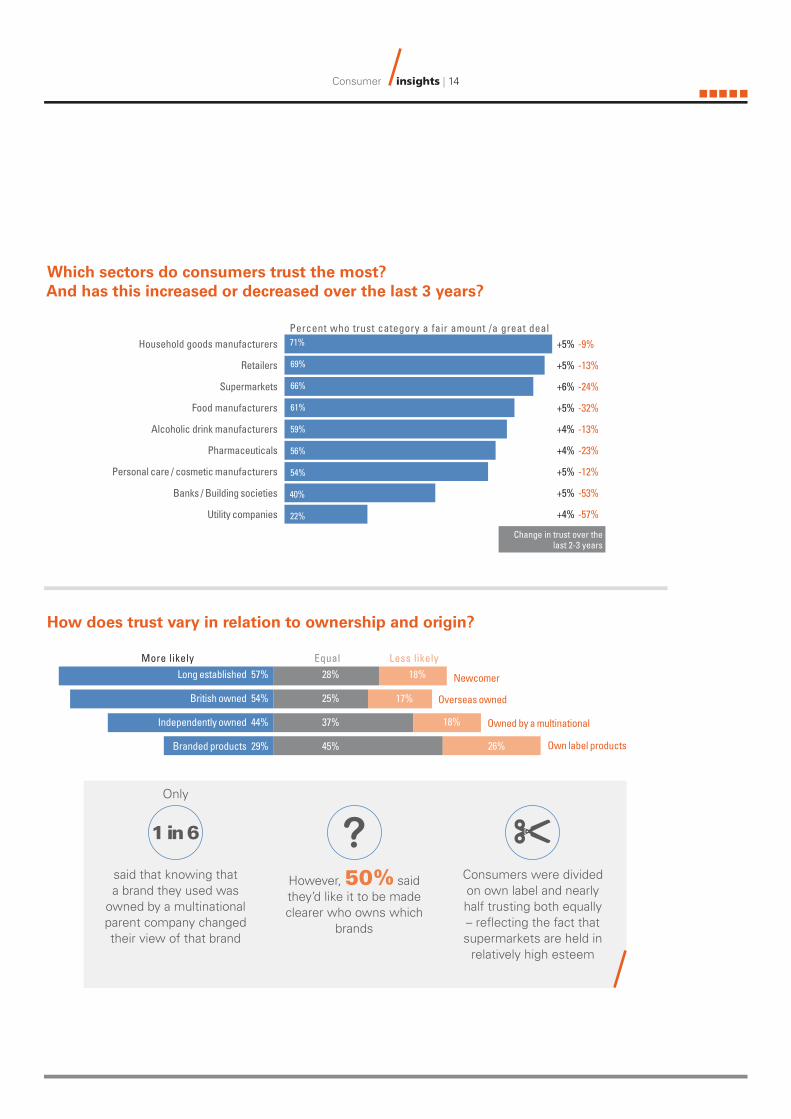

Which sectors do consumers trust the most? And has this increased or decreased over the last 3 years?

Household goods manufacturers Percent who trust category a fair amount /a great deal 71% +5% -9%

Retailers 69% +5% -13%

Supermarkets 66% +6% -24%

Food manufacturers 61% +5% -32%

Alcoholic drink manufacturers 59% +4% -13%

Pharmaceuticals 56% +4% -23%

Personal care / cosmetic manufacturers 54% +5% -12%

Banks / Building societies 40% +5% -53%

Utility companies 22% +4% -57%

Change in trust over the last 2-3 years

How does trust vary in relation to ownership and origin?

More likely Equal Less likelyLong established 57% 28% 18% Newcomer

British owned 54% 25% 17% Overseas owned

Independently owned 44% 37% 18% Owned by a multinational

Branded products 29% 45% 26% Own label products

Only

1 in 6

said that knowing that a brand they used was

owned by a multinational parent company changed their view of that brand

However, 50% said they’d like it to be made clearer who owns which

brands

Consumers were divided on own label and nearly half trusting both equally – refl ecting the fact that supermarkets are held in

relatively high esteem

15 | Consumer insights

What role does brand trust play in purchasing decision?

1/3

said that trust in a company is not

important

2/3

believe companies are doing the bare

minimum

2/3

don’t always believe what

companies say they are doing

1/3

of respondents said they used to stick to a specific brand

or set of brands, but now chose what

brands to buy based on other factors,

such as price

How does trust vary in relation to ownership and origin?

Personal care & beauty products 9% 38% 36% 17%

Household goods 7% 35% 39% 19%

Alcohol 8% 32% 37% 23%

Packaged food & soft drinks 6% 33% 41% 21%

The single biggest factor in my choice of product

A major factor in my choice of product

Something I consider but not a major factor

I don’t consider this at all

On average 20% of respondents said that they don’t consider brand values in their purchasing decisions at all

Consumer insights | 16

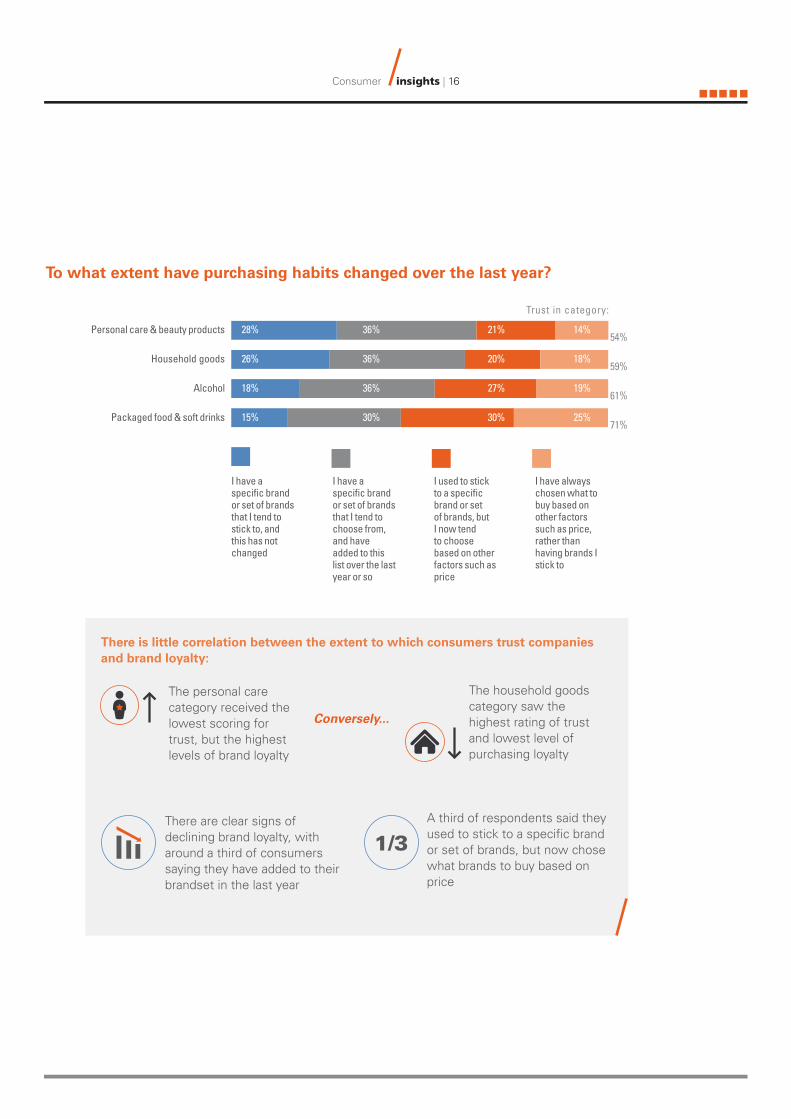

To what extent have purchasing habits changed over the last year?

1/3

Trust in category:

Personal care & beauty products 28% 36% 21% 14%54%

Household goods 26% 36% 20% 18%59%

Alcohol 18% 36% 27% 19%61%

Packaged food & soft drinks 15% 30% 30% 25%71%

I have a specifi c brand or set of brands

that I tend to stick to, and

this has not changed

I have a specifi c brand or set of brands

that I tend to choose from,

and have added to this list over the last year or so

I used to stick to a specifi c brand or set

of brands, but I now tend

to choose based on other factors such as price

I have always chosen what to

buy based on other factors such as price, rather than

having brands I stick to

There is little correlation between the extent to which consumers trust companies and brand loyalty:

The personal care category received the lowest scoring for trust, but the highest levels of brand loyalty

Conversely...

The household goods category saw the highest rating of trust and lowest level of purchasing loyalty

There are clear signs of declining brand loyalty, with around a third of consumers saying they have added to their brandset in the last year

A third of respondents said they used to stick to a specific brand or set of brands, but now chose what brands to buy based on price

Which media sources are considered the most trustworthy?

17 | Consumer insights

Consumer bodies, eg Which? 23% 51%

Web sites where customers can give their opinion or review products, eg Mumsnet, blogs etc

TV documentaries 15%

39%

37%

TV advertising 6% 25%

Social media - posts and “likes” by my friends 7% 25%

Manufacturer or brand websites 4% 18%

Print advertising (newspapers /magazines) 2% 17%

Social media - company/ brand pages 4% 16%

Billboard advertising 5% 15%

How much have recommendations made by friends via social media influenced the brands you buy ?

28%

have started buying new brands as a

result of discovering or learning about them via social media

25%

have changed their brands as a result of recommendations from friends on social media.

18%

Consumer insights | 18

ABOUT THE RESEARCH The survey refl ects the responses of 2,079 UK adults and was conducted between the 10th and 15th of April 2014. Respondents were fairly evenly split along gender lines (48% male versus 52% female). Twenty-nine percent were between the ages of 18 and 34, 35% were between the ages of 35 and 54, and the remainder were 55 years of age or older.

YouGov is the authoritative measure of public opinion and consumer behaviour. It is YouGov’s ambition to supply a live stream of continuous, accurate data and insights into what people are thinking and doing all over the world, all of the time, so that companies, governments and institutions can better serve the people that sustain them.

The Demographic breakdown

Gender

48% 52%

Age

18-24 25-34 35-44 45-54 55+ 12% 17% 16% 19% 36%

Regions

Scotland

8%

Northern Ireland

3% North

24%

Midlands

16%

East

9%

Wales

5%

12%22% London South

Base participants 2,079

consumerinsightspanel.org

The Consumer Insights Panel is a not-for-profit, independent body of industry specialists, formed to provide an authoritative and trusted view on what is happening in the FMCG sector. None of the opinions expressed in this forum or this publication represent advice and the views reflect those of the participants and not necessarily their organisations or the Panel as a whole.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

Oliver for KPMG | OM018666A | July 2014 | Printed on recycled material.

Related Documents