Sector Update 06 April 2016 PP7004/02/2013(031762) Page 1 of 10 Consumer Neutral Showing Glimpses of Recovery ↔ By Soong Wei Siang l [email protected] We maintain our NEUTRAL call on the consumer sector. Although sentiment is still languishing at multiple-year low in the absence of strong catalysts or stimulants that could provide more certainty or clarity to the consumer, we think that it will not sink deeper as the sales growth in 4Q15 suggested that the gestation or transition period of one year post-GST implementation should be sufficient for the consumers to adapt or acclimatise to the new costing environment. Our Top Pick for the sector is DLADY (OP; RM56.40), as we believe it: (i) should continue to benefit from the subdued commodity trend, and (ii) is in a good position to increase its dividend pay-out by distributing special dividends to reward shareholders. Valuation is also undemanding as our TP implies FY16E PER of 22.6x which is on par with its 3-year mean while offering decent dividend yield of 4.7%. We also reiterate our NEUTRAL rating on the sin sector. We are bearish on the tobacco sector after the knee-jerk reaction of volume decline in the industry to the significant price increase led by massive excise duty hike but we believe the brewers will have a better time due to the far more modest excise duty hike while we expect more favourable product mix, innovative launching of new products and the push factor of Euro 2016 to drive the brewery sector. Our top pick of the sector is GAB (OP; RM16.36). We like its market-leading position in the local Malt Liquor Market (MLM), evidenced by its: (i) 3-year CAGR sales growth of 2.5% vs. competitor’s 1.6%, (ii) revenue share in Malaysia has strengthened to 61.3% in CY2015 from 57.9% in CY2013, and (iii) better earnings margin as compared to competitor (between 0.4ppt to 3.5ppt in operating margin over last 3 years), while the strategy of focusing on premium segment by embarking on aggressive marketing activities will help to sustain earnings growth. A start of an end? The round of results in 4QCY15 was inconclusive to the health of the consumer sector with 50% or 5 out of 10 stocks under or coverage reported disappointing results, including DLADY, OLDTOWN, AEON, AMWAY, and PARKSON. While almost all of the companies except OLDTOWN recorded YoY sales growth as compared to the same period last year, earnings were somehow dragged down by higher promotional or distribution expenses incurred in order to stimulate consumer sentiment or consolidate market position. As such, we believe that the sector has started to show glimpse of recovery, but we think that only a consistent growth trend will convince us in giving a firmer conclusion. A change in appetite. The KL Consumer Index (KLCSU) has performed up to par with the local benchmark index (KLCI) with YTD gain of 0.5% vis-à-vis 0.7% of the latter. While the recently concluded 4QCY15 results failed to send out a strong message on the clear direction of the sector, we believe investors were still wary and cautious of the weak consumer sentiment, resulting in flattish performance of KLCSU and only more consistent and stronger sets of results moving forward can bring clarity on whether a recovery is on the fast track. We also noticed that there was a switch in preference as blue-chip companies with larger market capitalisation are back on investors’ radar with names, including PPB, CARLSBG, DLADY, F&N, and GAB making YTD gains ranging from 6.2% to 17.4% while some profit-taking activities on the second-liners are observed, resulting in more modest performance by the companies with smaller market capitalization. Big price increase unlikely. The Anti-Profiteering Act, which was introduced to prevent traders from raising prices by taking advantage of GST implementation, will be expiring on June 2016 after an implementation period of 18 months. While businesses will regain the freedom and flexibility to adjust selling prices, we are not anticipating a big round of price increase in view of the all-time low consumer sentiment which induced higher sensitivity of consumer towards pricing and thus stronger consumerism. Secondly, we also expect the authorities to continue keeping a close watch on the prices, particularly key necessities items even after the expiry of the Act to ensure price stability. Besides, none of the companies under our coverage has openly indicated the intention to raise prices upon the expiry of the Act as most of them are cautious of the weak consumer sentiment and competitive business landscape. Sentiment has not sunk further? According to MIER (Malaysian Institute of Economic Research), the consumer sentiment deteriorated further after slumping to a 10-year low in 3Q15 with 4Q15 Consumer Sentiment Index dipping to 63.8 in 4Q15 from 70.2 in 3Q15. However, the picture was comparatively rosier according to Nielsen as its benchmark index inched up by 2 ppt to 80% in 4Q15. Nonetheless, as we have not spotted any strong indicators or clues to prove that the sentiment has recovered significantly, but we believe that the sentiment has gradually normalize post-GST implementation one year ago, although issues over the uncertainties in economy outlook and job security are still creating uneasiness in consumers. During 4Q15, 75% or 9 out of 12 companies under our coverage have recorded YoY growth in revenue (refer to table below). We think that the trend is healthy and supportive of our thesis that the consumer sentiment has not sunk further as price increases are unlikely the factor driving the revenue growth due to the Anti-Profiteering Act.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Sector Update

06 April 2016

PP7004/02/2013(031762) Page 1 of 10

Consumer Neutral Showing Glimpses of Recovery ↔

By Soong Wei Siang l [email protected]

We maintain our NEUTRAL call on the consumer sector. Although sentiment is still languishing at

multiple-year low in the absence of strong catalysts or stimulants that could provide more certainty or clarity

to the consumer, we think that it will not sink deeper as the sales growth in 4Q15 suggested that the

gestation or transition period of one year post-GST implementation should be sufficient for the consumers to

adapt or acclimatise to the new costing environment. Our Top Pick for the sector is DLADY (OP;

RM56.40), as we believe it: (i) should continue to benefit from the subdued commodity trend, and (ii) is in a

good position to increase its dividend pay-out by distributing special dividends to reward shareholders.

Valuation is also undemanding as our TP implies FY16E PER of 22.6x which is on par with its 3 -year mean

while offering decent dividend yield of 4.7%. We also reiterate our NEUTRAL rating on the sin sector. We

are bearish on the tobacco sector after the knee-jerk reaction of volume decline in the industry to the

significant price increase led by massive excise duty hike but we believe the brewers will have a better time

due to the far more modest excise duty hike while we expect more favourable product mix, innovative

launching of new products and the push factor of Euro 2016 to drive the brewery sector. Our top pick of the

sector is GAB (OP; RM16.36). We like its market-leading position in the local Malt Liquor Market (MLM),

evidenced by its: (i) 3-year CAGR sales growth of 2.5% vs. competitor’s 1.6%, (ii) revenue share in Malaysia

has strengthened to 61.3% in CY2015 from 57.9% in CY2013, and (iii) bette r earnings margin as compared

to competitor (between 0.4ppt to 3.5ppt in operating margin over last 3 years), while the strategy of focusing

on premium segment by embarking on aggressive marketing activities will help to sustain earnings growth.

A start of an end? The round of results in 4QCY15 was inconclusive to the health of the

consumer sector with 50% or 5 out of 10 stocks under or coverage reported disappointing results, including DLADY, OLDTOWN, AEON, AMWAY, and PARKSON. While almost all of the companies except OLDTOWN recorded YoY sales growth as compared to the same period last year, earnings were somehow dragged down by higher promotional or distribution expenses incurred in order to stimulate consumer sentiment or consolidate market position. As such, we believe that the sector has started to show glimpse of recovery, but we think that only a consistent growth trend will convince us in giving a firmer conclusion.

A change in appetite. The KL Consumer Index (KLCSU) has performed up to par with the local

benchmark index (KLCI) with YTD gain of 0.5% vis-à-vis 0.7% of the latter. While the recently concluded 4QCY15 results failed to send out a strong message on the clear direction of the sector, we believe investors were still wary and cautious of the weak consumer sentiment, resulting in flattish performance of KLCSU and only more consistent and stronger sets of results moving forward can bring clarity on whether a recovery is on the fast track. We also noticed that there was a switch in preference as blue-chip companies with larger market capitalisation are back on investors’ radar with names, including PPB, CARLSBG, DLADY, F&N, and GAB making YTD gains ranging from 6.2% to 17.4% while some profit-taking activities on the second-liners are observed, resulting in more modest performance by the companies with smaller market capitalization.

Big price increase unlikely. The Anti-Profiteering Act, which was introduced to prevent traders from raising prices by taking

advantage of GST implementation, will be expiring on June 2016 after an implementation period of 18 months. While businesses will regain the freedom and flexibility to adjust selling prices, we are not anticipating a big round of price increase in view of the all-time low consumer sentiment which induced higher sensitivity of consumer towards pricing and thus stronger consumerism. Secondly, we also expect the authorities to continue keeping a close watch on the prices, particularly key necessities items even after the expiry of the Act to ensure price stability. Besides, none of the companies under our coverage has openly indicated the intention to raise prices upon the expiry of the Act as most of them are cautious of the weak consumer sentiment and competitive business landscape.

Sentiment has not sunk further? According to MIER (Malaysian Institute of Economic Research), the consumer sentiment

deteriorated further after slumping to a 10-year low in 3Q15 with 4Q15 Consumer Sentiment Index dipping to 63.8 in 4Q15 from 70.2 in 3Q15. However, the picture was comparatively rosier according to Nielsen as its benchmark index inched up by 2 ppt to 80% in 4Q15. Nonetheless, as we have not spotted any strong indicators or clues to prove that the sentiment has recovered significantly, but we believe that the sentiment has gradually normalize post-GST implementation one year ago, although issues over the uncertainties in economy outlook and job security are still creating uneasiness in consumers. During 4Q15, 75% or 9 out of 12 companies under our coverage have recorded YoY growth in revenue (refer to table below). We think that the trend is healthy and supportive of our thesis that the consumer sentiment has not sunk further as price increases are unlikely the factor driving the revenue growth due to the Anti-Profiteering Act.

Consumer Sector Update Sector Update

06 April 2016

PP7004/02/2013(031762) Page 2 of 10

YoY growth (4QCY15)

F&B

Sin

Retail

MLM

DLADY 2.7%

BAT -12.2%

AEON 0.4%

AMWAY 16.7%

NESTLE 8.1%

CARLSBG* -14.6%

PADINI 3.0%

HAIO 29.9%

OLDTOWN -0.8%

GAB 0.7%

PARKSON* 38.6% QL 0.7%

*Malaysian sales only Source: Companies, Kenanga Research

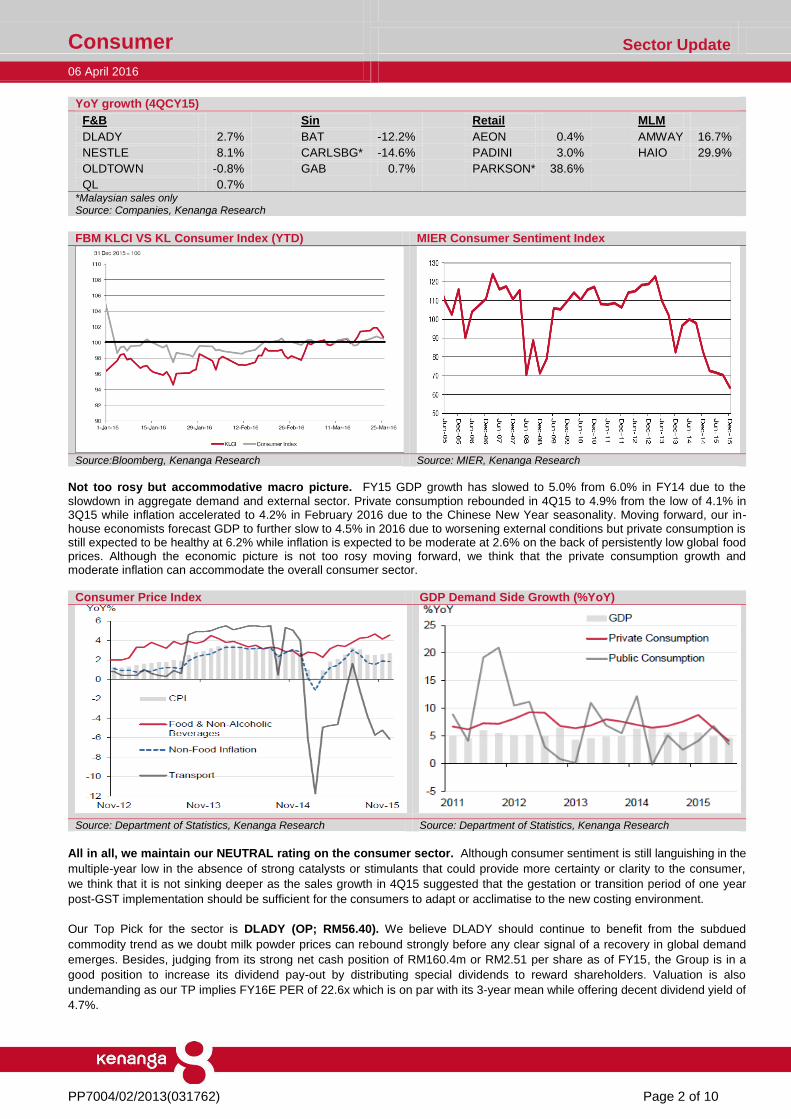

FBM KLCI VS KL Consumer Index (YTD) MIER Consumer Sentiment Index

Source:Bloomberg, Kenanga Research Source: MIER, Kenanga Research

Not too rosy but accommodative macro picture. FY15 GDP growth has slowed to 5.0% from 6.0% in FY14 due to the

slowdown in aggregate demand and external sector. Private consumption rebounded in 4Q15 to 4.9% from the low of 4.1% in 3Q15 while inflation accelerated to 4.2% in February 2016 due to the Chinese New Year seasonality. Moving forward, our in-house economists forecast GDP to further slow to 4.5% in 2016 due to worsening external conditions but private consumption is still expected to be healthy at 6.2% while inflation is expected to be moderate at 2.6% on the back of persistently low global food prices. Although the economic picture is not too rosy moving forward, we think that the private consumption growth and moderate inflation can accommodate the overall consumer sector.

Consumer Price Index GDP Demand Side Growth (%YoY)

Source: Department of Statistics, Kenanga Research Source: Department of Statistics, Kenanga Research

All in all, we maintain our NEUTRAL rating on the consumer sector. Although consumer sentiment is still languishing in the

multiple-year low in the absence of strong catalysts or stimulants that could provide more certainty or clarity to the consumer,

we think that it is not sinking deeper as the sales growth in 4Q15 suggested that the gestation or transition period of one year

post-GST implementation should be sufficient for the consumers to adapt or acclimatise to the new costing environment.

Our Top Pick for the sector is DLADY (OP; RM56.40). We believe DLADY should continue to benefit from the subdued

commodity trend as we doubt milk powder prices can rebound strongly before any clear signal of a recovery in global demand

emerges. Besides, judging from its strong net cash position of RM160.4m or RM2.51 per share as of FY15, the Group is in a

good position to increase its dividend pay-out by distributing special dividends to reward shareholders. Valuation is also

undemanding as our TP implies FY16E PER of 22.6x which is on par with its 3-year mean while offering decent dividend yield of

4.7%.

Consumer Sector Update Sector Update

06 April 2016

PP7004/02/2013(031762) Page 3 of 10

Sin Sector

Duty hike for brewers, after all. As highlighted in our previous strategy report, the excise duty hike in brewery sector came to

pass as the duty was raised by 8%-10% (effective March 2016) after a hiatus of 10 years. We view the development neutrally as we believe the brewery companies will be able to pass through the additional costs arising from the higher duty. We also do not think the moderate resultant price increase will cause a significant dip in volume as beers or alcoholic drinks’ prices are less visible or standardized as opposed to cigarettes differing from sales channel and product type, and thus, volume sensitivity to the price changes is less inelastic as compared to the tobacco industry. However, we do not think that brewers are able to capitalize on the excise duty hike by increasing prices beyond the excise duty hike quantum in view of the Anti-Profiteering Act which is effective until 31st June 2016. The sustainability of earnings growth should come from the more favourable product mix towards the premium segment which will be driven by aggressive marketing activities and the innovation in new product launching. Pessimistic outlook on tobacco sector. On the flipside, the picture was bleaker for the tobacco sector as the price increase in

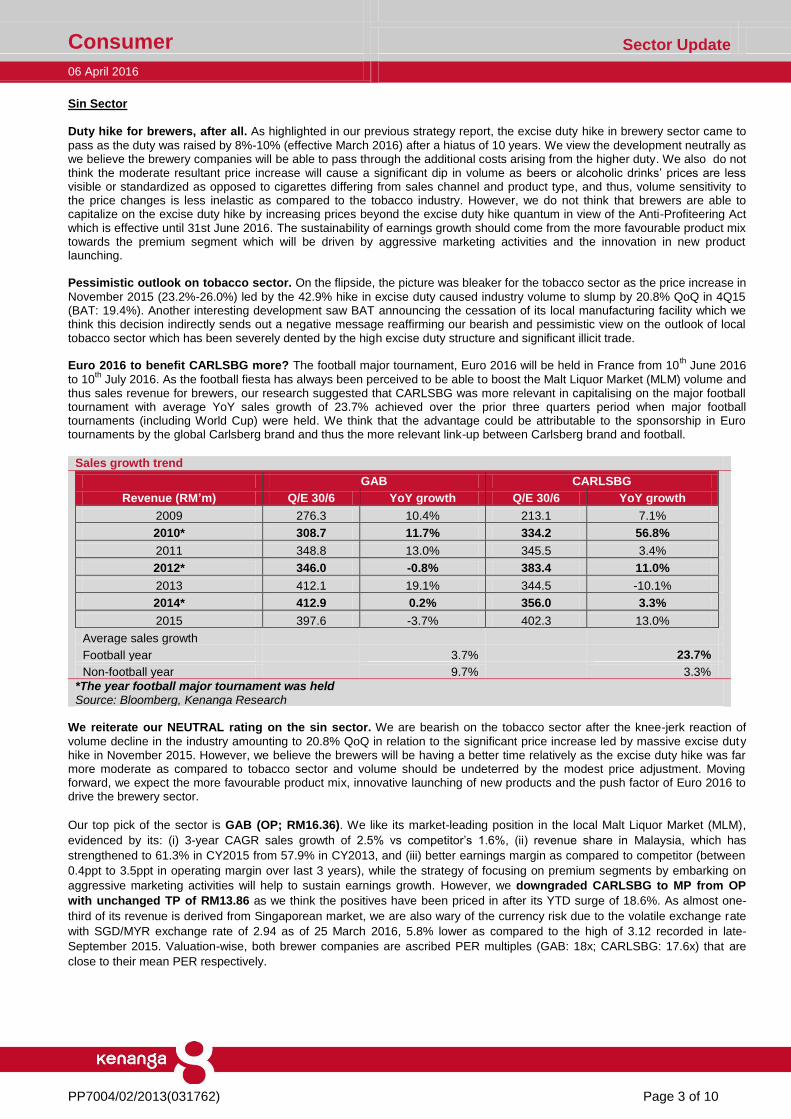

November 2015 (23.2%-26.0%) led by the 42.9% hike in excise duty caused industry volume to slump by 20.8% QoQ in 4Q15 (BAT: 19.4%). Another interesting development saw BAT announcing the cessation of its local manufacturing facility which we think this decision indirectly sends out a negative message reaffirming our bearish and pessimistic view on the outlook of local tobacco sector which has been severely dented by the high excise duty structure and significant illicit trade. Euro 2016 to benefit CARLSBG more? The football major tournament, Euro 2016 will be held in France from 10

th June 2016

to 10th

July 2016. As the football fiesta has always been perceived to be able to boost the Malt Liquor Market (MLM) volume and thus sales revenue for brewers, our research suggested that CARLSBG was more relevant in capitalising on the major football tournament with average YoY sales growth of 23.7% achieved over the prior three quarters period when major football tournaments (including World Cup) were held. We think that the advantage could be attributable to the sponsorship in Euro tournaments by the global Carlsberg brand and thus the more relevant link-up between Carlsberg brand and football.

Sales growth trend

GAB CARLSBG

Revenue (RM’m) Q/E 30/6 YoY growth Q/E 30/6 YoY growth

2009 276.3 10.4% 213.1 7.1%

2010* 308.7 11.7% 334.2 56.8%

2011 348.8 13.0% 345.5 3.4%

2012* 346.0 -0.8% 383.4 11.0%

2013 412.1 19.1% 344.5 -10.1%

2014* 412.9 0.2% 356.0 3.3%

2015 397.6 -3.7% 402.3 13.0%

Average sales growth Football year

3.7%

23.7%

Non-football year

9.7%

3.3%

*The year football major tournament was held Source: Bloomberg, Kenanga Research

We reiterate our NEUTRAL rating on the sin sector. We are bearish on the tobacco sector after the knee-jerk reaction of

volume decline in the industry amounting to 20.8% QoQ in relation to the significant price increase led by massive excise duty hike in November 2015. However, we believe the brewers will be having a better time relatively as the excise duty hike was far more moderate as compared to tobacco sector and volume should be undeterred by the modest price adjustment. Moving forward, we expect the more favourable product mix, innovative launching of new products and the push factor of Euro 2016 to drive the brewery sector.

Our top pick of the sector is GAB (OP; RM16.36). We like its market-leading position in the local Malt Liquor Market (MLM),

evidenced by its: (i) 3-year CAGR sales growth of 2.5% vs competitor’s 1.6%, (ii) revenue share in Malaysia, which has

strengthened to 61.3% in CY2015 from 57.9% in CY2013, and (iii) better earnings margin as compared to competitor (between

0.4ppt to 3.5ppt in operating margin over last 3 years), while the strategy of focusing on premium segments by embarking on

aggressive marketing activities will help to sustain earnings growth. However, we downgraded CARLSBG to MP from OP

with unchanged TP of RM13.86 as we think the positives have been priced in after its YTD surge of 18.6%. As almost one-

third of its revenue is derived from Singaporean market, we are also wary of the currency risk due to the volatile exchange rate

with SGD/MYR exchange rate of 2.94 as of 25 March 2016, 5.8% lower as compared to the high of 3.12 recorded in late-

September 2015. Valuation-wise, both brewer companies are ascribed PER multiples (GAB: 18x; CARLSBG: 17.6x) that are

close to their mean PER respectively.

Consumer Sector Update

06 April 2016

PP7004/02/2013(031762) Page 4 of 10

Valuation & Justification For Calls

Consumer Retail / MLM Consumer F&B Consumer SIN

Recent results

Retail continued to be the most vulnerable sub-sector to the weak consumer sentiment as 50% of 3 out of 6 stocks under our coverage (AEON, AMWAY, PARKSON) reported weaker-than-expected results. Elsewhere, ZHULIAN and HAIO reported earnings within expectations while PADINI reported better-than-expected earnings.

A mixed quarter for the F&B players as two companies under our coverage reported earnings within expectations (NESTLE and QL), while the remaining two (DLADY, OLDTOWN) reported disappointing numbers due to higher distribution and taxation expenses, respectively.

Cheers for the breweries as both companies (CARLSBG and GAB) reported earnings above expectations while BAT results was within expectations after the earnings cut post excise duty hike in November 2015.

Comments/

Major upgrade or downgrade

Consumer sentiment is believed to be still weak in the absence of stimulants and clarity on the uncertainty on economy outlook.

Sales growth on sequential basis should be supported by the Chinese New Year festivities in 1Q16 before the real testament on the recovery from GST implementation can be witnessed in 2Q16 which marks a year after the implementation back in 2Q15.

Volume growth is expected to be under pressure due to the weak consumer sentiment on the back of uncertainty over the economy outlook. Thus, new innovative product launches are important to drive the consumer sentiments and buying appetite.

More A&P or brand building initiatives are expected in coming quarters as the F&B company leverage on the savings from lower raw material prices to reinvest into marketing activities in order to stimulate the consumer sentiments as well as consolidating or gaining market share from competitors.

Outlook for the tobacco sector remains bearish following the massive price increase led by the excise duty hike in November 2015. Volume growth will be under the threat of resurgence in illicit trade following the price increase.

Excise duty was raised after absent for 10 years but impact should be neutral as brewer are able to pass through the additional cost but further capitalization is unlikely in view of the weak sentiments.

Catalysts

Seasonality factors, school holidays and festivities to drive up sales.

More aggressive promotional and marketing activities in conjunction with festivities to boost sales as well as to clear stocks.

Sooner-than-expected recovery in consumer sentiment

Lower raw material prices to lift earnings margins.

Seasonality, school holidays and festivities to drive up demand for F&B products.

Better efforts from the authorities in tackling illicit cigarettes and contraband beers.

Seasonality and festivities to boost beers demand.

Risks

Lower margin in relation to the higher-than-expected A&P costs.

Worse-than-expected deterioration in consumer sentiment.

Further weakening of the MYR.

Higher-than-expected import costs in relation to the unfavorable forex.

Higher-than-expected raw material prices.

Excise duty hike, higher input cost and operating costs

Stronger presence of illegal market.

Valuation basis

Between -1SD to +0.5SD over 3-5 years mean P/E. Between -1.0SD to +1.5SD over 3-5 years average P/E Between -1.5SD to mean over 3-5 years average P/E

Dividend Yield Offering average yield of 3.9%, MLM offers decent yield of 4.7%-4.8% while PADINI is offering highest yield of 5.9%.

Average yield at 3.4% ranging from 1.1% (QL) to 4.7% (DLADY). Offering decent yield of 5.2%-7.1%, one of the attractive points of sin stocks.

Source: Kenanga Research

Consumer Sector Update

06 April 2016

PP7004/02/2013(031762) Page 5 of 10

Valuation & Justification For Calls (Part 1 of 2)

Company

New TP

(RM) New Calls

Previous valuation basis

New Valuation Basis

TP Revision

(%) Calls

Action Comments

Retail Sector

AEON 2.22 UP

20x FY17 PER (in-line with its 5-year average Fwd PER)

20x FY17 PER (in-line with its 5-year average Fwd PER)

0.0% Maintain

Maintain CALL and TP.

Retail segment continues to be affected by the spillover of poor consumer sentiment in 2015, which could have been discouraged by the reduction in discretionary spending and disposable income arising from the prevailing weakness in the Ringgit and implementation of GST. We are hopeful that the overall market environment will improve but remain cautious that the poor consumer sentiment will pro-long much further into FY16.

AMWAY 9.16 MP

19x FY16 PER (which implies -1SD 3-year mean average)

19x FY16 PER (which implies -1SD 3-year mean average)

0.0% Maintain

Maintain CALL and TP.

AMWAY will continue to drive sales by encouraging its distributors with sales incentive as well as embarking on more marketing and sales activities to counter the weak consumer sentiment which will incur higher product costs and marketing expenses. Despite near-term weakness, we expect earnings to recover in FY16 as we foresee better consumer sentiment by FY16 and being further supported by its strong brand image and marketing activities to drive sales. Dividend yield of >4.5% can support the share price.

HAI-O 2.22 UP

12.9x FY17 PER (5-year mean average)

12.9x FY17 PER (5-year mean average)

0.0% Maintain

Maintain CALL and TP.

The revenue growth momentum is picking up thanks to members recruitment and incentive reward program. However, the Group expects the weak consumer and business sentiment to persist in the near term, which is in line with our cautious view. Overall, we still maintain our negative stance despite the improving MLM division’s performance in view of the pedestrian earnings growth forecasted for the next two years (4.0% and 7.3%) and the risk in the wholesale and retail divisions.

PADINI 2.21 MP

13x FY17 PER (+0.5SD over 5-year average Fwd PER)

13x FY17 PER (+0.5SD over 5-year average Fwd PER)

0.0% Maintain

Maintain CALL and TP.

Appears to be least affected by the decline in consumer sentiment during 2015, given the management’s strong direction and brand strategy to maintain market share. With management’s target for at least 10 new stores to be opened by end-FY16, Padini will be well positioned to ride on the up-wave with the advantage of a wider store presence when macroeconomic headwinds simmer down and consumer sentiment recovers.

PARKSON 0.82 MP SOP Valuation SOP Valuation 0.0% Maintain

Maintain CALL and TP.

Looking ahead, we expect Parkson to continue facing a tough operating environment on the back of weak consumer sentiment due to the economic slowdown, particularly in the China market, which contributes to the crux of its earnings. Coupled with the intense competition from online shopping and oversupply of retail space, we believe it would take a longer period of time for Parkson to reverse its declining trend in SSSG.

Source: Kenanga Research

Consumer Sector Update

06 April 2016

PP7004/02/2013(031762) Page 6 of 10

Valuation & Justification For Calls (Part 2 of 2)

Company New TP

(RM) New Calls

Previous valuation basis

New Valuation Basis

TP Revision

(%) Calls

Action Comments

F& B Sector

DLADY 56.40 OP 22.6x FY16 PER (implies 3-year mean)

22.6x FY16 PER (implies 3-year mean)

0.0% Maintain

Maintain Call and TP It should continue to benefit from the subdued commodity trend as we doubt milk powder prices can rebound strongly before any strong signal of a recovery in global demand emerges. Besides, judging from its strong net cash position of RM160.4m or RM2.51 per share as of FY15, the Group is in a good position to increase its dividend pay-out by distributing special dividends to reward shareholders. Valuation is also undemanding as our TP implies FY16E PER of 22.6x which is on par with its 3-year mean while offering decent dividend yield of 4.7%.

NESTLE 76.20 MP

27x FY16 PER (implies +0.5SD over 5-years historical PER)

27x FY16 PER (implies +0.5SD over 5-years historical PER)

0.0% Maintain

Maintain Call and TP Moving forward, we foresee the subdued trend of commodity price to continue in view of the lackluster global economy outlook and thus expecting the Group to continue to benefit from that trend. We also anticipate the Group to be committed in marketing and promotional activities in order to stimulate the fragile sentiment and encourage consumer spending.

OLDTOWN 1.72 OP

14.1x FY17 PER (above -1 SD over 3-year mean PER)

14.1x FY17 PER (above -1 SD over 3-year mean PER)

0.0% Maintain

Maintain Call and TP Café Chain division seen improvement in both sales and PBT for the second consecutive quarters, which we believe is the results from the effective marketing activities while Manufacturing of Beverage division continued to grow steadily due to the defensive nature of its FMCG products despite weak sentiment. Recently announced plan to utilize its cash to look for M&A opportunity and potnetial distributing special dividend might provide excitement to the stock.

QL 4.16 UP

23x FY17 PER (implies +1.5SD over 5-year mean PER)

23x FY17 PER (implies +1.5SD over 5-year mean PER)

0.0% Maintain

Maintain Call and TP Earnings growth is expected to be healthy at 10.6% and 8.9% over the next two years underpinned by the defensive nature of its staple food products which are less vulnerable to the weak consumer sentiment. Although we like the company for its proven earnings track record and resilient nature, we think that the valuation (above +1.5 SD over 5-year mean) appears lofty.

Sin Sector

BAT 57.78 MP

17.4x PER FY16E (implies -1.5SD over 5-year mean average)

17.4x PER FY16E (implies -1.5SD over 5-year mean average

0.0% Maintain

Maintain Call and TP Looking forward, volume growth is expected to be soft following the latest round of price increase which encourages down trading to illicit cigarettes. Meanwhile, another round of price increase is unlikely upon the expiry of Anti-Profiteering Act in June 2016 in view of the fragile sentiment and threat of illicit trades. Thus, we think that market share gain is more relevant for the Group to sustain its earnings growth momentum through innovative new product launches and successful marketing campaigns. Recently,it announced the plan to shut down its local production facility which indirectly send out a negative message reaffirming our bearish and pessimistic view on the outlook of local tobacco sector

CARLSBG 13.86 MP 17.6x FY16 PER

(3-year mean average)

17.6x FY16 PER (3-year mean

average) 0.0% Downgrade

Downgrade Call but Maintain TP. Positives have been priced in after YTD surge of 18.6%. As almost one-third of its revenue is derived from Singaporean market, we are also wary of the currency risk due to the volatile exchange rate with SGD/MYR exchange rate of 2.94 as of 25/3/2016 5.8% lower as compared to the high of 3.12 recorded in late-September 2015.

GAB 16.36 OP 18x FY16 PER (below 5-year

mean average)

18x FY16 PER (below 5-year

mean average) 0.0% Maintain

Maintain Call and TP. We like its market-leading position in the local Malt Liquor Market (MLM), evidenced by its: (i) 3-year CAGR sales growth of 2.5% vs competitor’s 1.6%, (ii) revenue share in Malaysia which has strengthened to 61.3% in CY2015 from 57.9% in CY2013, and (iii) better earnings margin as compared to competitor (between 0.4ppt to 3.5ppt in operating margin over last 3 years), while the strategy of focusing on premium segment by embarking on aggressive marketing activities will help to sustain earnings growth.

Source: Kenanga Research

Consumer Sector Update

06 April 2016

PP7004/02/2013(031762) Page 7 of 10

Consumer stocks PER Bands

AEON AMWAY

Source: Bloomberg, Kenanga Research

HAIO PADINI

Source: Bloomberg, Kenanga Research

PARKSON

Source: Bloomberg, Kenanga Research

DLADY NESTLE

Source: Bloomberg, Kenanga Research

Consumer Sector Update Sector Update

06 April 2016

PP7004/02/2013(031762) Page 8 of 10

OLDTOWN QL

Source: Bloomberg, Kenanga Research

BAT CARLSBG

Source: Bloomberg, Kenanga Research

GAB

Source: Bloomberg, Kenanga Research

Consumer Sector Update

06 April 2016

PP7004/02/2013(031762) Page 9 of 10

Peer Comparison

NAME Price Mkt Cap PER (x) Est. Div. Yld.

Historical ROE

P/BV Net Profit (RMm) 1Y Fwd Growth

2Y Fwd Growth

Target Price

Rating

(RM) (RMm) Historical 1Y Fwd

2Y FWd

(x) Historical 1Y Fwd

2Y FWd

(%) (%) (RM)

Consumer - Retail

AEON CO (M) BHD 2.66 3,734.6 28.0 24.2 24.0 1.5% 7.4% 2.05 133.4 154.8 155.5 16.0% 0.5% 2.22 Underperform

AMWAY (MALAYSIA) HLDGS BHD 9.50 1,561.7 24.4 19.7 18.2 4.7% 29.3% 7.60 63.9 79.2 84.7 23.9% 6.9% 9.16 Market Perform

HAI-O ENTERPRISE BHD 2.50 483.3 16.2 15.6 14.5 4.8% 13.1% 1.89 30.1 31.3 33.7 4.0% 7.7% 2.22 Underperform

PADINI HOLDINGS BERHAD 2.02 1,329.0 16.6 12.7 11.8 5.9% 26.3% 3.28 80.2 104.2 112.9 29.9% 8.3% 2.24 Market Perform

PARKSON HOLDINGS BHD 0.90 955.5 12.2 36.0 17.3 2.8% -2.0% 0.37 80.7 27.0 56.4 -66.5% 108.9% 0.82 Underperform

Consumer - F&B

DUTCH LADY 51.00 3,264.0 23.2 20.4 19.4 4.7% 89.7% 20.73 141.0 159.7 168.3 13.3% 5.4% 56.40 Outperform

NESTLE (M) 75.00 17,587.5 29.8 26.7 25.3 3.6% 79.5% 24.83 590.7 659.3 695.5 11.6% 5.5% 76.20 Market Perform

OLDTOWN BHD 1.51 681.7 13.4 14.0 12.7 4.0% 15.5% 2.07 51.0 48.6 53.7 -4.8% 10.6% 1.72 Outperform

QL RESOURCES BHD 4.30 5,366.5 28.7 25.9 23.8 1.1% 13.6% 3.76 187.5 207.4 225.7 10.6% 8.8% 4.16 Underperform

Consumer - Sin

BRITISH AMERICAN TOBACCO BHD 55.10 15,732.7 17.3 16.6 16.6 5.9% 170.0% 28.85 910.1 946.0 948.0 4.0% 0.2% 57.78 Market Perform

CARLSBERG BREWERY MALAYSIA B 13.88 4,269.8 18.7 17.7 16.7 5.2% 66.7% 12.46 228.5 241.8 256.4 5.8% 6.0% 13.86 Market Perform

GUINNESS ANCHOR BHD 14.00 4,229.4 19.7 16.8 15.4 7.1% 65.1% 11.20 214.2 251.7 274.6 17.5% 9.1% 16.36 Outperform

Source: Bloomberg, Kenanga Research

C

Consumer Sector Update Sector Update

06 April 2016

PP7004/02/2013(031762) Page 10 of 10

Stock Ratings are defined as follows: Stock Recommendations

OUTPERFORM : A particular stock’s Expected Total Return is MORE than 10% (an approximation to the 5-year annualised Total Return of FBMKLCI of 10.2%). MARKET PERFORM : A particular stock’s Expected Total Return is WITHIN the range of 3% to 10%. UNDERPERFORM : A particular stock’s Expected Total Return is LESS than 3% (an approximation to the 12-month Fixed Deposit Rate of 3.15% as a proxy to Risk-Free Rate). Sector Recommendations***

OVERWEIGHT : A particular sector’s Expected Total Return is MORE than 10% (an approximation to the 5-year annualised Total Return of FBMKLCI of 10.2%). NEUTRAL : A particular sector’s Expected Total Return is WITHIN the range of 3% to 10%. UNDERWEIGHT : A particular sector’s Expected Total Return is LESS than 3% (an approximation to the

12-month Fixed Deposit Rate of 3.15% as a proxy to Risk-Free Rate). ***Sector recommendations are defined based on market capitalisation weighted average expected total return for stocks under our coverage.

This document has been prepared for general circulation based on information obtained from sources believed to be reliable but we do not make any representations as to its accuracy or completeness. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may read this document. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees. Kenanga Investment Bank Berhad accepts no liability whatsoever for any direct or consequential loss arising from any use of this document or any solicitations of an offer to buy or sell any securities. Kenanga Investment Bank Berhad and its associates, their directors, and/or employees may have positions in, and may effect transactions in securities mentioned herein from time to time in the open market or otherwise, and may receive brokerage fees or act as principal or agent in dealings with respect to these companies.

Published and printed by: KENANGA INVESTMENT BANK BERHAD (15678-H) 8th Floor, Kenanga International, Jalan Sultan Ismail, 50250 Kuala Lumpur, Malaysia Chan Ken Yew Telephone: (603) 2166 6822 Facsimile: (603) 2166 6823 Website: www.kenanga.com.my Head of Research

Related Documents

![[Unchanged] Opportunity amid adversity - I3investorcdn1.i3investor.com/my/files/dfgs88n/2016/01/07/1483882668... · Opportunity amid adversity Adapt ... for corporate exercises ...](https://static.cupdf.com/doc/110x72/5b0a24417f8b9abe5d8dc293/unchanged-opportunity-amid-adversity-i3investorcdn1-amid-adversity-adapt-.jpg)