CONSTRUCTION ACTIVITY IN EUROPE L’ACTIVITÉ DE LA CONSTRUCTION EN EUROPE DIE BAUTÄTIGKEIT IN EUROPA EDITION 2016 EUROPEAN CONSTRUCTION INDUSTRY FEDERATION

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CONSTRUCTION ACTIVITY IN EUROPEL’ACTIVITÉ DE LA CONSTRUCTION EN EUROPEDIE BAUTÄTIGKEIT IN EUROPA

EDITION 2016

EUROPEAN CONSTRUCTIONINDUSTRY FEDERATION

TOTAL CONSTRUCTION

€ 1,241BILLION

CONSTRUCTION WORKERS:

14.1 MILLION

3.2 MILLIONENTERPRISES

OF WHICH:95% ARE SME’S

WITH FEWER THAN 2093% WITH FEWER

THAN 10 OPERATIVES

30.9%OF INDUSTRIAL EMPLOYMENT

43.5%OF GROSS FIXED

CAPITAL FORMATION

ALL KEY FIGURES AS AT 2015 (EU 28)

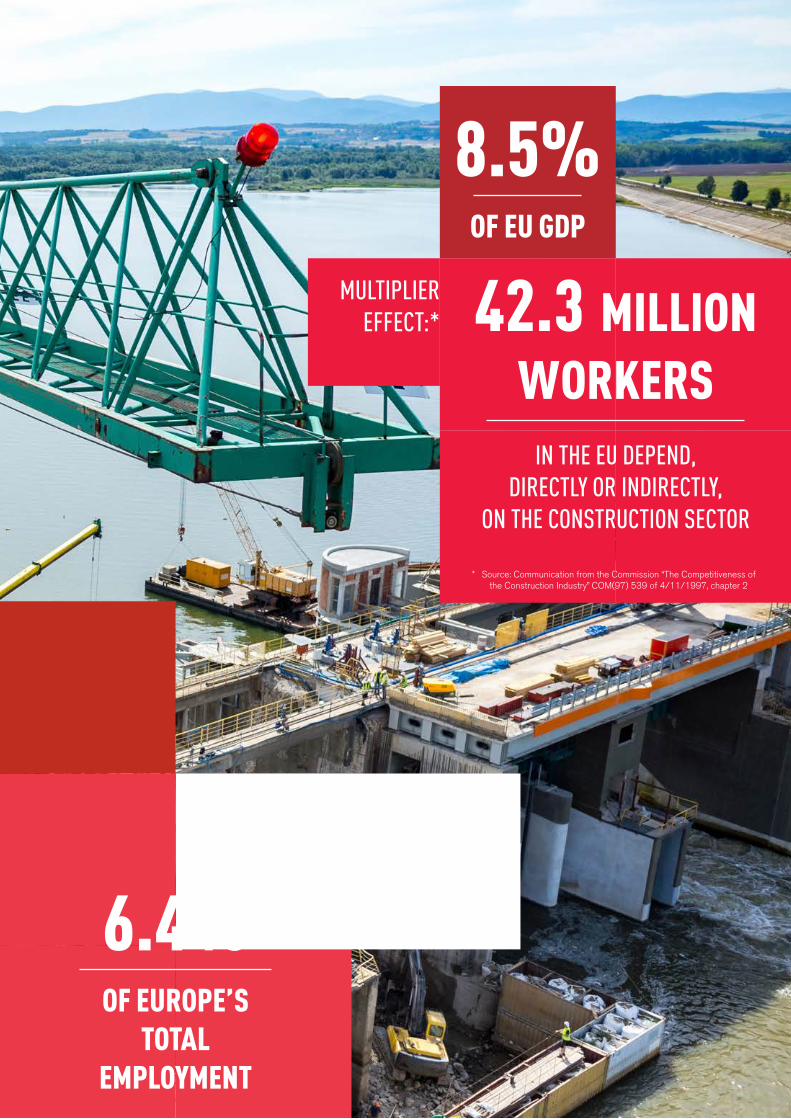

42.3 MILLIONWORKERS

IN THE EU DEPEND,

DIRECTLY OR INDIRECTLY, ON THE CONSTRUCTION SECTOR

6.4%OF EUROPE’S

TOTAL EMPLOYMENT

8.5%OF EU GDP

* Source: Communication from the Commission “The Competitiveness of the Construction Industry” COM(97) 539 of 4/11/1997, chapter 2

MULTIPLIER EFFECT:*

Created in 1905Legal personality under French law

26 countries (23 EU, Switzerland, Norway and Turkey)

29 National member federations representing firms:• of all sizes• of all building and civil engeneering specialties• practising all kind of working methods (whenever operationg as general contractors or as sub-contractors)

Associate members:EFFC European Federation of Foundation ContractorsEQAR European Quality Association for Recycling e.V.

Cooperation Agreement:

NFB National Federation of Builders (UK)

FIEC

Partnerships

Sectoral Social Dialogue

Social Partner in the European Sectoral Social Dialogue of the Construction Industry together with FETBB-EFBWW-EFBH (European Federation of Building and Woodworkers)http://ec.europa.eu/social/main.jsp?catId=480

EICCooperation with EIC (European International Contractors) for activities beyond Europe’s borderswww.eic-federation.eu

CICAThe European founding member of CICA (Confederation of International Contractors’ Associations)www.cica.net

ECFParticipant in the ECF (European Construction Forum)www.ecf.be

EHFMember of EHF (European Housing Forum)www.europeanhousingforum.eu

CENPartner Organisation of CEN (European Committee for Standardisation)www.cen.eu

ECCREDIMember of ECCREDI (European Council for Construction Research, Development and Innovation)www.eccredi.org

EENAssociate Member of the Enterprise Europe Network of the European Commissionhttp://een.ec.europa.eu/

WorldSkill EuropeAssociate Member of WorldSkills Europewww.euroskills.org

Campaigns & Portals

Renovate Europe Partner in the Renovate Europe Campaign www.renovate-europe.eu

Healthy Workplaces (OSHA)

Partner in the OSHA (European Agency for Health and Safety at Work) Campaign on “Healthy Worpkplaces for All Ages”www.healthy-workplaces.eu

BUILD UPPartner of BuiLD uP (The european Portal for energy efficiency in Buildings) www.buildup.eu

Projects

ProductInfoXPartner of Product InfoX www.productxchange.com/en/International/Partners/ProductinfoX/projectdescription/

Posting of workersFIEC-EFBWW website on “Posting of workers”www.posting-workers.eu

Construction for youth

FIEC-EFBWW website on “Construction for youth”www.construction-for-youth.eu

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

04

CONTENTS

EU

AT

BE

BG

CY

CZ

DE

DK

EE

ES

FI

FR

GR

HU

IE

IT

LT

NL

PL

PT

RO

SE

SI

UK

CH

NO

TR

Introduction 6

Total construction output by country 7

European Union 8

Austria 24

Belgium 26

Bulgaria 28

Cyprus 30

Czech Republic 32

Germany 34

Denmark 36

Estonia 38

Spain 40

Finland 42

France 44

Greece 46

Hungary 48

Ireland 50

Italy 52

Lithuania 54

The Netherlands 56

Poland 58

Portugal 60

Romania 62

Sweden 64

Slovenia 66

United Kingdom 68

Switzerland 70

Norway 72

Turkey 74

List of the experts 76

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

05

INTRODUCTION

It is a great pleasure for me to present this new edition (no. 59) of the annual FIEC Statistical Report.

The report provides an overview of recent developments and perspectives in the con-struction industry in the various EU Member States, as well as a series of indicators with figures both for each country and for the EU as a whole. The map shown opposite gives an overall view of the performance of construc-tion activity in the various European countries in 2015.

As regards the EU economy, 2015 was the first year since the beginning of the crisis in which all Member States reported an increase in their GDP, but substantial growth differenc-es persist between countries, reflecting both their structural features and their different cyclical positions. This was mainly supported by several positive factors such as the low oil prices, the Euro exchange rate and the very low interest rate and mortgage rates, which have stimulated exports and private consumption.

There are however some economic and polit-ical challenges for the EU, such as the devel-opment and the handling of the asylum-seek-ers issue and the outcome of the referendum in the United Kingdom, which are hindering a stronger recovery in the current year.

Within this framework as regards construc-tion activity the recovery observed in 2014 (+1.7%) continued and strengthened in 2015 (+2.4%). However, the above economic and political uncertainties within the EU and at international level will have an impact on the forecast for 2016 with construction activity expected to continue its recovery (+2.1%), but at a slower pace.

Despite the overall decline in the general gov-ernment deficit, several Member States still have to cope with the necessary budgetary consolidation measures which have been put in place and which continue to lead to some-times significant cuts in public investment.

FIEC never stopped reminding political deci-sion makers of the importance of investment, in particular the public one, as there cannot be any growth without investment and infrastructure. Significant support could still come from the Investment Plan for Europe (also known as the “Juncker Plan”), which is expected to mobilise investments of at least €315 billion over three years. It is therefore crucial to continue to mobilise our forces at all levels (EU, national, regional, local) , in or-der to ensure that projects which can benefit not only larger companies, but also SMEs, can be launched.

I would like to thank all the people in FIEC and from our Member Federations who have contributed to this report and I sincerely hope that its content will be useful and interesting for all readers.

Jean-Louis Marchand Chairman of the Economic and Legal Commission

C’est avec grand plaisir que je vous présente cette nouvelle édition (N° 59) du Rapport Statistique annuel de la FIEC.

Il dresse l’inventaire des récentes avancées et perspectives pour le secteur de la construction dans les différents États membres en Europe et fournit divers indicateurs chiffrés, tant pour chaque membre que pour l’Union Européenne dans son ensemble. Par ailleurs, la carte qui l’accompagne donne un aperçu global des performances de l’activité de construction dans les différents pays européens en 2015.

En ce qui concerne l’économie européenne, 2015 est la première année depuis le début de la crise au cours de laquelle l’intégralité des États membres a enregistré une augmentation du PIB. Néanmoins, il subsiste d’importants écarts de croissance entre les pays, qui témoignent de leurs caractéristiques structurelles et de leurs différents cycles. Différents facteurs positifs y ont contribué, comme la diminution du prix de l’essence, le cours de l’euro, ainsi que des taux d’intérêt et hypothé-caires très bas, qui ont stimulé les exportations et la consommation des ménages.

L’Union Européenne reste toutefois confrontée à certains défis, tant économiques que poli-tiques, telles que la gestion des demandeurs d’asile ou l’issue du referendum au Royaume-Uni, qui empêchent un redressement plus marqué au cours de l’actuel exercice.

Ainsi, en ce qui concerne l’activité de construc-tion, la reprise observée en 2014 (+1,7 %) a perduré et s’est même renforcée en 2015 (+2,4 %). Cependant, les incertitudes écono-miques et politiques susmentionnées au sein de l’UE et au niveau international auront une incidence sur les prévisions de 2016. En effet, l’activité de construction devrait poursuivre sa reprise (+2,1 %), mais à un rythme plus lent.

Malgré la diminution globale du déficit public, plusieurs États membres doivent encore faire face aux mesures de consolidation budgétaire requises qui ont été mises en place et qui sont à l’origine de coupes sombres dans l’investis-sement public.

La FIEC n’a eu de cesse de rappeler aux déci-deurs politiques l’importance de l’investissement, et plus particulièrement de l’investissement public, étant donné que l’investissement et l’in-frastructure sont des conditions essentielles à la croissance. Le Plan pour l’Europe (également appelé le « Plan Juncker ») pourrait encore jouer un rôle majeur, vu qu’il devrait mobiliser des investissements d’au moins 315 milliards d’euros au cours des trois prochaines années. Par conséquent, il est essentiel d’unir nos forces à tous les niveaux (européen, national, régional, local) pour veiller à mettre en place des projets qui seront à la fois bénéfiques aux plus grandes entreprises, et aux PME.

Je souhaiterais remercier toutes les personnes de la FIEC et de nos fédérations membres qui ont participé à ce rapport, et j’espère sincè-rement que tous ses lecteurs trouveront son contenu utile et intéressant.

Jean-Louis Marchand Président de la Commission économique et juridique

Gerne präsentiere ich Ihnen die aktuelle Aus-gabe (Nr. 59) des jährlichen Statistikberichts der FIEC.

Der Bericht enthält einen Überblick über die jüngsten Entwicklungen und Perspektiven der Bauwirtschaft in den einzelnen EU-Mitgliedstaaten sowie eine Reihe von Indikatoren mit Zahlen auf Länder- und EU-Ebene. Die Karte auf der gegen-überliegenden Seite bietet eine Gesamtübersicht zur Performance der Bauwirtschaft in den einzelnen europäischen Ländern im Jahr 2015.

Im Hinblick auf die EU-Konjunktur war 2015 das erste Jahr seit Beginn der Krise, in dem alle Mitgliedstaaten einen Anstieg ihres BIP vermelde-ten. Allerdings bestehen weiterhin starke Wachs-tumsunterschiede zwischen den Ländern, was ihre strukturellen Merkmale sowie die unterschiedlichen Konjunkturlagen in den einzelnen Staaten widerspie-gelt. Dies wurde vorwiegend durch mehrere positive Faktoren gestützt – z. B. die niedrigen Ölpreise, den Euro-Wechselkurs und die sehr niedrigen Zinsen und Hypothekenzinsen –, durch die Exporte und der private Konsum angekurbelt wurden.

Es gibt jedoch einige wirtschaftliche und politische Herausforderungen für die EU wie beispielsweise die weitere Entwicklung und Bewältigung der Migra-tions-Problematik und der Ausgang des bevorste-henden Referendums im Vereinigten Königreich, die eine stärkere Erholung im laufenden Jahr bremsen.

Vor diesem Hintergrund setzte sich in der Bauwirt-schaft die Erholung aus dem Jahr 2014 (+1,7 %) im Jahr 2015 verstärkt fort (+2,4 %). Die bereits erwähnten wirtschaftlichen und politischen Unwäg-barkeiten innerhalb der EU und auf internationaler Ebene wirken sich jedoch auf die Prognose für 2016 aus. Die Bautätigkeit bleibt demnach weiterhin im Aufschwung (+2,1 %), jedoch in langsamerem Tempo.

Trotz der insgesamt sinkenden Staatsdefizite haben mehrere Mitgliedstaaten noch immer mit den ergriffenen notwendigen Maßnahmen zur Haushaltskonsolidierung zu kämpfen, die weiterhin teils signifikante Einschnitte bei den öffentlichen Investitionen zur Folge haben.

Die FIEC weist die politischen Entscheidungsträger stets auf die Bedeutung von Investitionen hin, insbe-sondere Investitionen der öffentlichen Hand, ohne die es keine Infrastrukturen und kein Wachstum geben kann. Eine erkennbare Unterstützung dessen könnte sich aus der Investitionsoffensive für Europa (auch bekannt als „Juncker-Plan“) ergeben. Es wird erwartet, dass diese über drei Jahre hinweg min-destens 315 Mrd. Euro an Investitionen „freisetzen“ wird. Daher ist es wichtig, dass wir auch zukünftig auf allen Ebenen (EU, national, regional, lokal) unsere Kräfte mobilisieren, um sicherzustellen, dass Projekte aufgelegt werden können, die nicht nur den größeren, sondern auch kleinen und mittleren Unternehmen zugutekommen.

Ich möchte mich bei allen Mitarbeitern in der FIEC und aus unseren Mitgliedsverbänden bedanken, die zu diesem Bericht beigetragen haben und hoffe aufrichtig, dass die Inhalte für alle Leser aufschluss-reich und nützlich sein werden.

Jean-Louis Marchand Vorsitzender Wirtschafts- und Rechtsausschuss

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

06

TOTAL CONSTRUCTION OUTPUT BY COUNTRY

NB:The text and data contained within the European report have been drawn up on the basis of the national reports supplied by the FIEC Member Federations.

EU2.4%

AT0.2%

BE1.3%

NL7.2%

LUNA

IE8.3%

BG-0.7%

RO10.0%

CH-2.8%

CYNA

TRNA

CZ-5.5%

PL5.9%

DE0.2%

DK1.7%

NO2.3%

SE10.0%

EE-7.5%

LT-5.2%

ES5.6%

UK8.5%

PT3.0%

FI-1.0%

FR-3.3%

HRNA

GR-15.1%

IT-1.3%

MTNA

SKNA

SI-7.3%

HUNA

NB:Le texte et les données du chapitre Union Européenne ont été élaborés sur la base des rapports nationaux envoyés par les fédérations membres de la FIEC.

NB:Der Text und die Zahlen des Kapitels „Europäische Union“ beruhen auf den von den FIEC-Mitgliedsverbänden zur Verfügung gestellten nationalen Berichten.

Variation of production in real terms on previous year (2015/2014)

Variation du volume de la production sur l’année précédente (2015/2014)

Reale Veränderungsrate im Vergleich zum Vorjahr (2015/2014)

Co-operation Agreement

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

07

EUROPEAN UNION

1. General economic overview

According to the latest eco-nomic forecast of the European Commission, a moderate recov-ery of the EU economy can be observed, but it is still facing heigthened risks. The recovery is mainly supported by several positive factors such as the low oil prices, the Euro exchange rate and the very low level of inter-est rates which have stimulated exports and private consumption. The level of investment remains however hampered by economic and policy uncertainty and, in some Member States, by a high level of public debt.

Further economic and political uncertainties are linked to the development and the handling of the asylum-seekers issue, to the outcome of the referendum in the United Kingdom next June, to the geo-political situation in the Middle-East and to the intensified downturn in emerging markets.

The data of the European Commission indicates an increase in the EU GDP of 1.9% for 2015, which should remain on the same level in 2016, whereas an increase of 2.0% is expected for 2017.

2015 was the first year since the beginning of the crisis in which all Member States reported an increase in their output, but substantial growth differences persist, reflecting both structural features and different cyclical positions. This has been mainly due to an overall improvement in private consumption, which is attributable to the fall in inflation and the slowly improving labour market conditions. However, such development is expected to lose some momentum due to the fore-cast increase in inflation (+1.6% in the EU in 2017).

1. Aperçu économique général

Selon les dernières prévisions économiques de la Commission européenne, une reprise modérée de l’économie européenne peut être observée, mais l’UE reste confrontée à des risques accentués. La reprise est essentiellement soutenue par plusieurs facteurs positifs, dont la faiblesse des prix du pétrole, le taux de change de l’euro ou le niveau très bas des taux d’intérêt, qui ont stimulé les exportations et la consommation privée. Les investissements restent cependant freinés par l’incertitude économique et politique et, dans certains États membres, par le niveau élevé de l’endettement public.

D’autres incertitudes économiques et politiques sont liées au développe-ment et à la gestion du problème des demandeurs d’asile, aux résultats du référendum organisé au Royaume-Uni en juin prochain, à la situation géopolitique au Moyen-Orient et à l’intensification de la récession sur les marchés émergents.

Les données de la Commission euro-péenne indiquent une augmentation du PIB de l’UE de 1,9 % pour 2015, qui devrait rester au même niveau en 2016, tandis qu’une hausse de 2 % est prévue pour 2017.

2015 a été la première année depuis le début de la crise où tous les États membres ont rapporté une croissance de leur PIB mais des différences majeures persistent en termes de croissance en raison de caractéristiques structurelles et de positions conjoncturelles différentes. Cela s’explique en grande partie par une amélioration globale de la consommation privée qui est impu-table à la baisse de l’inflation et à la lente amélioration des conditions sur le marché de l’emploi. Toutefois, cette évolution positive devrait quelque peu s’essouffler en raison des prévisions de remontée de l’inflation (+1,6 % dans l’UE en 2017).

1. Allgemeine Konjunkturlage

Laut der jüngsten Konjunkturprognose der Europäischen Kommission ist eine moderate Erholung der EU-Konjunktur zu beobachten. Dennoch ist sie weiter-hin einem erhöhten Risiko ausgesetzt. Die Erholung wird vorwiegend durch mehrere positive Faktoren gestützt wie die niedrigen Ölpreise, den Euro-Wechselkurs und das extrem niedrige Zinsniveau, wodurch Exporte und der private Konsum angekurbelt wurden. Investitionen werden jedoch weiterhin durch die wirtschaftlichen und politi-schen Unwägbarkeiten sowie in eini-gen Mitgliedstaaten durch eine hohe öffentliche Schuldenlast gebremst.

Weitere wirtschaftliche und politi-sche Unsicherheitsfaktoren sind die weitere Entwicklung und Bewältigung von Migrationspolitik, der Ausgang des Referendums im Vereinigten Königreich im Juni, die geopoliti-sche Lage im Nahen Osten sowie der deutliche Abschwung in den Wachstumsmärkten.

Die Daten der Europäischen Kommission ergeben für 2015 ein BIP-Wachstum von 1,9 % in der EU. Für 2016 wird eine ähnliche Steigerungsrate erwartet, während man für 2017 sogar von einer Erhöhung um 2,0 % ausgeht.

2015 war das erste Jahr seit Beginn der Krise, in dem alle Mitgliedstaaten einen Anstieg ihrer Wirtschaftsleistung vermeldeten. Allerdings bestehen wei-terhin starke Wachstumsunterschiede, was sich durch strukturelle Merkmale und unterschiedliche Konjunkturlagen in den einzelnen Staaten widerspie-gelt. Grund für das Wachstum ist hauptsächlich der insgesamt stärkere private Konsum, zurückzuführen auf die sinkende Inflation und die sich langsam verbessernde Lage am Arbeitsmarkt. Diese Entwicklung dürfte jedoch an Schwung verlieren, wenn die Inflationsrate, wie prognos-tiziert, wieder ansteigt (+1,6 % in der EU im Jahr 2017).

8

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

Sectors 2007 2008 2009 2010 2011 2012 2013 2014 2015a 2016b

1. Building 3.6 -0.9 -9.7 -0.5 2.6 -3.2 -1.6 2.4 2.1 2.3

1.1. Housebuilding 2.2 -3.7 -10.6 2.4 2.8 -2.4 -1.0 4.6 2.8 3.0

1.1.1. New -3.0 -10.5 -17.1 3.7 6.5 -4.9 -0.9 6.1 3.5 4.0

1.1.2. R&M 5.3 2.3 -3.3 1.6 1.7 0.4 -0.3 3.7 2.6 2.2

1.2. Non residential ** 5.6 2.4 -9.2 -5.7 1.6 -4.3 -2.3 1.1 -0.5 1.4

1.2.1. Private 6.3 2.4 -12.3 1.7 2.1 -3.0 -1.8 1.5 0.3 1.6

1.2.2. Public 2.8 2.8 1.4 -1.8 -0.7 -8.7 -3.5 3.5 -2.4 1.0

2. Civil Engineering 2.4 2.4 0.3 1.3 0.4 -5.8 -1.6 -0.8 6.2 1.8

(1 + 2) Total Construction * 3.5 -0.5 -8.1 -0.5 2.1 -3.6 -1.6 1.7 2.4 2.1

* without : CY, CZ, EE, HR, HU, IE, LU, LV, MT, PL, SK** incl. R&M

80

82

84

86

88

90

92

94

96

98

100

102

104

‘07

‘08

‘09

‘10

‘11

‘12

‘13

‘14

2015

a

2016

b

Housebuilding - Logement - Wohnungsgebau Non residential - Non résidentiel - Nichwohnbau Civil Engineering - Génie Civil - Tiefbau Total Construction - Bauwesen

2007 = 100

VARIATION OF PRODUCTION IN REAL TERMS ON PREVIOUS YEAR (%)

VARIATION DU VOLUME DE LA PRODUCTION SUR L’ANNÉE PRÉCÉDENTE (%)

REALE VERÄNDERUNGSRATE IM VERGLEICH ZUM VORJAHR (%)

INVESTMENT IN CONSTRUCTION INVESTISSEMENT DANS LA CONSTRUCTION INVESTITIONEN IN BAUWESEN

€ 14.605BILLION € 1.241 BILLION

GDP 2015 TOTAL CONSTRUCTIONOUTPUT 2015

9

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

As regards public investment, an improvement is expected mainly because of the continuous overall decline in the general government deficit, albeit at a slower pace than in recent years due to the fiscal expenditures associated with the arrival of asylum-seekers in some countries, as well as to fiscal policy measures adopted by some Member States to lower the tax wedge on labour.

Higher labour market flexibility and moderate wage increases are expected to contribute positively to the development on the labour market and the unemployment rates are set to continue their gradual decline over the next two years but at a slower pace than last year : 11% in 2015, 10.5% in 2016 and 10.2% in 2017.

2. Overall construction activity

Within this framework the overall construction output in the EU in 2015 amounted to € 1.241 billion Euro, which represented 8.5% of the GDP.

The recovery observed in 2014 (+1.7%) continued and strength-ened in 2015 (+2.4%), thanks to a high level of activity in civil engineering (+6.2%) and in new housebuilding (+3.5%). However, the non-residential sector remained weak (-0.5%) both in its private (+0.3%) and in particular in the public (-2.4%) component.

Behind this overall picture the situations vary significantly from one country to the other. Increases in construction activity in 2015 were recorded in Ireland (+8.3%), where the positive trend that started in 2013 will be even further reinforced in 2016 (+16%), in the Netherlands (+7.2%), thanks to a strong level of activity in the new housebuild-ing sector, as in Sweden (+10%), in Poland (+5.9%), Portugal

En ce qui concerne les investissements publics, une amélioration est attendue principalement grâce à la diminution continue du déficit des administrations publiques, mais à un rythme moins sou-tenu qu’au cours des dernières années à cause des dépenses fiscales liées à l’arrivée des demandeurs d’asile dans certains pays ainsi que des mesures de politique fiscale adoptées par certains États membres pour alléger la charge fiscale sur le travail.

Une plus grande flexibilité du marché de l’emploi et des hausses salariales modé-rées devraient contribuer positivement au développement du marché de l’em-ploi et les taux de chômage devraient poursuivre leur baisse progressive au cours des deux prochaines années mais à un rythme moins soutenu que l’année passée : 11 % en 2015, 10,5 % en 2016 et 10,2 % en 2017.

2. Activité globale de construction

Dans ce contexte, la production de l’activité globale de construction dans l’UE s’est élevée en 2015 à 1.241 milliards €, ce qui représente 8,5% du PIB.

La reprise observée en 2014 (+1,7 %) s’est poursuivie et renfor-cée en 2015 (+2,4 %), grâce à un niveau d’activité élevé dans le génie civil (+6,2 %) et la construction résidentielle (+3,5 %). L’activité dans le secteur non résidentiel est par contre restée faible (-0,5 %), dans sa composante privée (+0,3 %) mais surtout dans sa composante publique (-2,4 %).

Derrière cette vision globale, les situations varient énormément d’un pays à l’autre. Une hausse de l’activité de la construction en 2015 a été observée en Irlande (+8,3 %), où la tendance positive qui s’est profilée en 2013 sera encore renforcée en 2016 (+16 %), aux Pays-Bas (+7,2 %), grâce à un niveau élevé d’activité dans le secteur de la construction rési-dentielle, ainsi qu’en Suède (+10 %), en Pologne (+5,9 %), au Portugal

Bei den öffentlichen Investitionen sind deutliche Verbesserungen zu erwar-ten, weil die Staatsdefizite insgesamt kontinuierlich sinken, wenn auch langsamer als in den vergangenen Jahren. Grund hierfür sind Ausgaben im Zusammenhang mit dem Zustrom von Asylsuchenden in einigen Ländern sowie die fiskalpolitischen Maßnahmen einiger Mitgliedstaaten zur Senkung der Abgabenlast bei Löhnen und Gehältern.

Größere Flexibilität am Arbeitsmarkt und moderate Lohnerhöhungen sollen einen positiven Beitrag zur Entwicklung am Arbeitsmarkt leisten. Die Arbeitslosenquoten werden im Laufe der kommenden zwei Jahre demnach weiterhin schrittweise sinken, jedoch weniger schnell als im vergangenen Jahr: 11 % in 2015, 10,5 % in 2016 und 10,2 % in 2017.

2. Entwicklung in der Bauwirtschaft

Vor diesem Hintergrund lag das Gesamtergebnis der Bauwirtschaft in der EU im Jahr 2015 bei 1.241 Mrd. Euro, ein Anteil von 8.5 % am BIP.

Die Erholung aus dem Jahr 2014 (+1,7 %) setzte sich im Jahr 2015 verstärkt fort (+2,4 %) , dank hoher Aktivität im Tiefbau (+6,2 %) und im Wohnungsneubau (+3,5 %) . Im Wirtschaftsbau blieb die Entwicklung mit -0,5 % jedoch schwach, sowohl im privaten (+0,3 %) als auch insbesondere im öffentlichen Bereich (-2,4 %) .

Im Ländervergleich zeichnen sich in Abgrenzung zur Gesamtlage zum Teil sehr unterschiedliche Bilder ab. Zuwächse bei der Bautätigkeit wurden 2015 verzeichnet in Irland (+8,3 %), wo der positive Trend 2013 einsetzte und 2016 noch stärker ausfallen wird (+16 %); in den Niederlanden (+7,2 %) dank der starken Entwicklung im Wohnungsneubau; wie auch in Schweden (+10 %); in Polen (+5,9 %); in Portugal (+3 %); in Rumänien (+10 %), wobei die Entwicklung in Rumänien vor allem

10

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

NB: The absolute value figures concerning the total volume of construction are given for guidance only and are provisional. The reason for this is that in the various countries these figures are not necessarily calculated on the same basis.

Country 2014(1) Constr. (2) Total economy (1)/(2)

United Kingdom 124.8 2,008 6.2%Germany 120.7 2,623 4.6%France 108.3 1,910 5.7%Italy 71.4 1,449 4.9%Spain 51.4 948 5.4%Poland 27.1 365 7.4%Netherlands 26.9 597 4.5%Sweden 23.0 381 6.0%Belgium 20.3 358 5.7%Austria 18.7 293 6.4%Finland 11.0 177 6.2%Romania 10.7 133 8.1%Denmark 10.3 225 4.6%Czech Republic 7.8 140 5.6%Portugal 6.8 152 4.5%Slovakia 5.7 69 8.3%Ireland 5.0 171 2.9%Greece 4.6 157 2.9%Hungary 3.8 88 4.3%Luxembourg 2.5 44 5.7%Lithuania 2.5 33 7.6%Croatia 1.8 36 5.0%Bulgaria 1.6 37 4.3%Latvia 1.4 21 6.7%Estonia 1.1 17 6.3%Slovenia 1.8 32 5.6%Cyprus 0.4 16 2.5%Malta 0.3 7 4.2%EU28 672 12,487 5.4%Switzerland 27.3 512 5.3%Norway 19.4 338 5.7%Turkey

Country 2015a(1) Constr. (2) GDP (1)/(2)

Germany 297 3,026 9.8%United Kingdom 163 2,577 6.3%France 160 2,160 7.4%Italy 129 1,636 7.9%Spain 101 1,081 9.3%Sweden 63 435 14.5%Netherlands 57 678 8.4%Poland 51 445 11.5%Belgium 42 410 10.2%Austria 33 338 9.8%Finland 29 206 14.1%Denmark 23 267 8.6%Czech Republic 17 162 10.5%Ireland 13 199 6.5%Portugal 11 179 6.1%Romania 9 155 5.8%Greece 8 176 4.5%Bulgaria 7 44 15.9%Hungary 7 109 6.4%Slovakia 6 78 7.7%Luxembourg 4 53 7.5%Lithuania 2 37 5.4%Croatia 2 44 4.5%Latvia 2 25 8.0%Estonia 2 20 10.0%Slovenia 2 39 5.1%Cyprus 1 17 2.9%Malta 1 9 5.6%EU28 1,241 14,605 8.5%Switzerland 58 582 10.0%Turkey 58 646 9.0%Norway 57 410 13.9%

GROSS VALUE ADDED - CONSTRUCTION / TOTAL ECONOMY

VALEUR AJOUTEE BRUTE - CONSTRUCTION / TOTAL ECONOMIE

BRUTTOWERTSCHÖPFUNG - BAUGEWERBE / GESAMTWIRTSCHAFT

CONSTRUCTION INVESTMENT/GDP INVESTISSEMENT CONSTRUCTION/PIB BAUINVESTITIONEN/BIP

Current prices in Bln. € %

Current prices in Bln. €

11

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

(+3%), Romania (+10%), the latter mainly supported by the civil engineering sector, and in Spain (+5.6%), the first increase since the beginning of the crisis in 2008. In the United Kingdom the sector also performed particularly well (+8.5%) driven by a remark-able increase in civil engineering (+34%).

In Austria (+0.2%) and Germany (+0.2%) the overall level of activ-ity remained more or less stable compared to the previous year, whilst several other countries recorded a negative trend. It is the case of Bulgaria (-0.7%), Estonia (-7.5%) and Greece (-15.1%), due to a decrease in civil engineering; Finland (-1%) and Italy (-1.3%), due to a drop in new housebuilding; France (-3.3%), due to a lack of public investment in particular in the non-residential sector; Lithuania (-5.2%) and Slovenia (-6.5%) where both new housebuilding and civil engineering declined.

The economic and political uncertainties within the EU and at the international level mentioned above are having an impact on the forecast for 2016 with a level of construction activity expected to continue its recovery (+2.1%), but at a slower pace. All the sub-sec-tors should show an increase, but with a strong slowdown for civil engineering (+1.8%) compared to 2015 (+6.2%). The main driver should remain the new house-building sector (+4.0) thanks to the low level of interest rates and of mortgage rates, as well as improvements expected on the labour market and rising real disposable income. However, the high levels of household debts in some Member States will continue to prevent a stronger increase in construction invest-ment in 2016.

(+3 %), en Roumanie (+10 %), où l’activité est principalement soutenue par le secteur du génie civil, et en Espagne (+5,6 %), qui connaît la première hausse depuis le début de la crise en 2008. Au Royaume-Uni, le secteur a aussi enregistré des résultats positifs (+8,5 %) soutenus par une remarquable progression du génie civil (+34 %).

En Autriche (+0,2 %) et en Allemagne (+0,2 %), le niveau d’activité global est resté plus ou moins stable par rapport à l’année précédente, tandis que plusieurs autres pays ont enregistré une évolution négative. C’est le cas de la Bulgarie (-0,7 %), de l’Estonie (-7,5 %) et de la Grèce (-15,1 %), en raison d’une baisse d’activité dans le génie civil ; de la Finlande (-1 %) et de l’Italie (-1,3 %), suite à un recul dans la construction résidentielle ; de la France (-3,3 %), à cause d’un manque d’inves-tissements publics, dans le secteur non résidentiel en particulier ; de la Lituanie (-5,2 %) et de la Slovénie (-6,5 %) où la construction résidentielle et le génie civil ont tous deux connu une baisse.

Les incertitudes économiques et politiques au sein de l’UE et à l’échelle internationale mentionnées plus haut ont eu un impact sur les prévisions pour 2016 qui indiquent que l’activité de la construction devrait poursuivre sa reprise (+2,1 %), mais à un rythme plus lent. Tous les sous-secteurs devraient enregistrer une progression, mais avec un fort ralentissement pour le génie civil (+1,8 %) par rapport à 2015 (+6,2 %). Le principal moteur de croissance devrait rester le secteur de la construction résidentielle (+4%) grâce au faible niveau des taux d’in-térêt et des taux hypothécaires ainsi qu’aux améliorations attendues sur le marché de l’emploi et à l’augmentation du revenu réel disponible. Toutefois, les niveaux d’endettement élevés des ménages dans certains États membres continueront à empêcher une augmen-tation plus forte des investissements en construction en 2016.

durch den Tiefbau getragen wurde; sowie in Spanien (+5,6 %), wo erstes Wachstum seit Beginn der Krise im Jahr 2008 verzeichnet wurde. Auch im Vereinigten Königreich entwickelte sich die Branche besonders gut (+8,5 %). Zurückzuführen war dies vor allem auf bemerkenswerte Zuwächse im Tiefbau (+34 %).

In Österreich (+0,2 %) und Deutschland (+0,2 %) stagnierte die Bautätigkeit insgesamt im Vergleich zum Vorjahr weitgehend, während mehrere andere Länder negative Entwicklungen verzeichne-ten. Dies war der Fall in Bulgarien (-0,7 %), Estland (-7,5 %) und Griechenland (-15,1 %), aufgrund eines Rückgangs im Tiefbau; in Finnland (-1 %) und Italien (-1,3 %), aufgrund von Rückgängen im Wohnungsneubau; in Frankreich (-3,3 %), aufgrund fehlender öffent-licher Investitionen vor allem im Wirtschaftsbau; in Litauen (-5,2 %) und Slowenien (-6,5 %), wo sich sowohl der Wohnungsneubau als auch der Tiefbau negativ entwickelten.

Die bereits erwähnten wirt-schaftlichen und politischen Unwägbarkeiten innerhalb der EU und auf internationaler Ebene wirken sich auf die Prognose für 2016 aus. Die Bautätigkeit bleibt demnach weiterhin im Aufschwung (+2,1 %), jedoch in langsame-rem Tempo. Alle Sektoren der Branche dürften zulegen, aller-dings mit einem stark gebremsten Wachstum im Tiefbau (+1,8 %) im Vergleich zu 2015 (+6,2 %). Der Wohnungsneubau (+4,0 %) dürfte weiterhin Hauptimpulsgeber sein, dank des niedrigen Zinsniveaus und niedriger Hypothekenzinsen sowie der erwarteten Verbesserungen am Arbeitsmarkt und des steigenden verfügbaren Realeinkommens. Die hohe Verschuldung der öffentlichen Haushalte in einigen Mitgliedstaaten wird jedoch 2016 einer stärkeren Ausweitung der Bauinvestitionen weiterhin im Wege stehen.

12

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

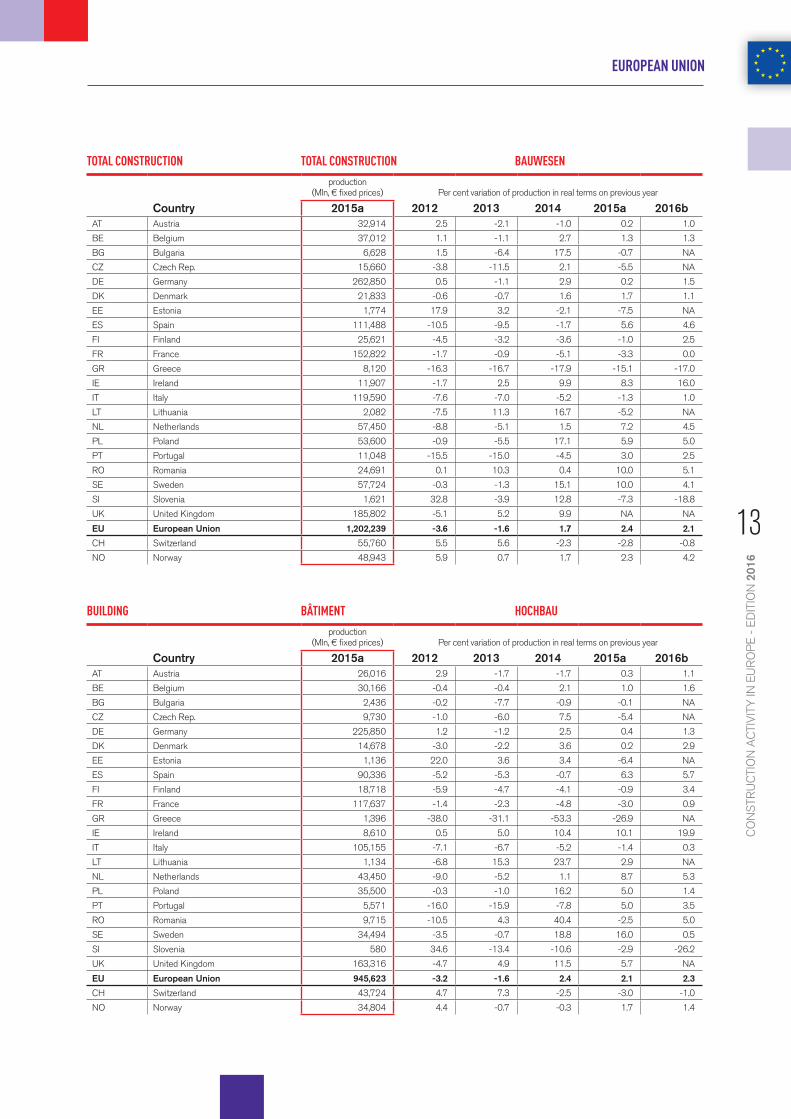

Country 2015a 2012 2013 2014 2015a 2016bAT Austria 32,914 2.5 -2.1 -1.0 0.2 1.0

BE Belgium 37,012 1.1 -1.1 2.7 1.3 1.3

BG Bulgaria 6,628 1.5 -6.4 17.5 -0.7 NA

CZ Czech Rep. 15,660 -3.8 -11.5 2.1 -5.5 NA

DE Germany 262,850 0.5 -1.1 2.9 0.2 1.5

DK Denmark 21,833 -0.6 -0.7 1.6 1.7 1.1

EE Estonia 1,774 17.9 3.2 -2.1 -7.5 NA

ES Spain 111,488 -10.5 -9.5 -1.7 5.6 4.6

FI Finland 25,621 -4.5 -3.2 -3.6 -1.0 2.5

FR France 152,822 -1.7 -0.9 -5.1 -3.3 0.0

GR Greece 8,120 -16.3 -16.7 -17.9 -15.1 -17.0

IE Ireland 11,907 -1.7 2.5 9.9 8.3 16.0

IT Italy 119,590 -7.6 -7.0 -5.2 -1.3 1.0

LT Lithuania 2,082 -7.5 11.3 16.7 -5.2 NA

NL Netherlands 57,450 -8.8 -5.1 1.5 7.2 4.5

PL Poland 53,600 -0.9 -5.5 17.1 5.9 5.0

PT Portugal 11,048 -15.5 -15.0 -4.5 3.0 2.5

RO Romania 24,691 0.1 10.3 0.4 10.0 5.1

SE Sweden 57,724 -0.3 -1.3 15.1 10.0 4.1

SI Slovenia 1,621 32.8 -3.9 12.8 -7.3 -18.8

UK United Kingdom 185,802 -5.1 5.2 9.9 NA NA

EU European Union 1,202,239 -3.6 -1.6 1.7 2.4 2.1

CH Switzerland 55,760 5.5 5.6 -2.3 -2.8 -0.8

NO Norway 48,943 5.9 0.7 1.7 2.3 4.2

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

Country 2015a 2012 2013 2014 2015a 2016bAT Austria 26,016 2.9 -1.7 -1.7 0.3 1.1

BE Belgium 30,166 -0.4 -0.4 2.1 1.0 1.6

BG Bulgaria 2,436 -0.2 -7.7 -0.9 -0.1 NA

CZ Czech Rep. 9,730 -1.0 -6.0 7.5 -5.4 NA

DE Germany 225,850 1.2 -1.2 2.5 0.4 1.3

DK Denmark 14,678 -3.0 -2.2 3.6 0.2 2.9

EE Estonia 1,136 22.0 3.6 3.4 -6.4 NA

ES Spain 90,336 -5.2 -5.3 -0.7 6.3 5.7

FI Finland 18,718 -5.9 -4.7 -4.1 -0.9 3.4

FR France 117,637 -1.4 -2.3 -4.8 -3.0 0.9

GR Greece 1,396 -38.0 -31.1 -53.3 -26.9 NA

IE Ireland 8,610 0.5 5.0 10.4 10.1 19.9

IT Italy 105,155 -7.1 -6.7 -5.2 -1.4 0.3

LT Lithuania 1,134 -6.8 15.3 23.7 2.9 NA

NL Netherlands 43,450 -9.0 -5.2 1.1 8.7 5.3

PL Poland 35,500 -0.3 -1.0 16.2 5.0 1.4

PT Portugal 5,571 -16.0 -15.9 -7.8 5.0 3.5

RO Romania 9,715 -10.5 4.3 40.4 -2.5 5.0

SE Sweden 34,494 -3.5 -0.7 18.8 16.0 0.5

SI Slovenia 580 34.6 -13.4 -10.6 -2.9 -26.2

UK United Kingdom 163,316 -4.7 4.9 11.5 5.7 NA

EU European Union 945,623 -3.2 -1.6 2.4 2.1 2.3

CH Switzerland 43,724 4.7 7.3 -2.5 -3.0 -1.0

NO Norway 34,804 4.4 -0.7 -0.3 1.7 1.4

TOTAL CONSTRUCTION TOTAL CONSTRUCTION BAUWESEN

BUILDING BÂTIMENT HOCHBAU

13

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

In a medium term perspective, the Investment Plan for Europe (also known as the “Juncker Plan”), which is expected to mobilise investments of at least €315 bil-lion over three years, until 2017, should show a positive impact on public and private investment and therefore also on construction activity over the next few years.

3. New housebuilding

The historically low level of inter-est and mortgage rates continue to support new housebuilding, although the increase observed in 2015 (+3.5%) was below the one of 2014 (+6.1%). It remains an important engine of the overall construction activity in several Member States and a further increase of 4.0% is expected for 2016.

In 2015 good levels of activity have been observed in Germany (+5.0%), where residential construction represents approxi-mately 60% of total construction output, in Ireland (+10.4%), due to projections of significant increases of population, in the Netherlands (+23%), amongst others because of a strong inflow of asylum seekers for whom dwellings are needed, in Poland (+6.6%), in Spain (+6.5%), where it compensated the slower growth of civil engineering and of public investment in general, in Sweden (+23.8%) and in the United Kingdom (+6.5%).

At the same time other coun-tries recorded a more or less unchanged level of activity, such as in Austria (-0.5%), Bulgaria (+0.1%) and Denmark (+0.6%), where an increase is expected for 2016 (+3.8%). Others had to face sometimes a strong decline which is the case of France (-3.9%) and Finland (-3.0%), but

Dans une perspective à moyen terme, le Plan d’investissement pour l’Eu-rope (aussi connu sous le nom de « Plan Juncker »), qui devrait mobiliser des investissements d’au moins 315 milliards € sur trois ans, jusqu’en 2017, devrait avoir un impact positif sur les investissements publics et privés et, dès lors aussi, sur l’activité de construc-tion au cours des prochaines années.

3. Construction résidentielle neuve

Le niveau historiquement bas des taux d’intérêt bancaires et hypo-thécaires continue de soutenir la construction résidentielle bien que la hausse observée en 2015 (+3,5 %) ait été inférieure à celle de 2014 (+6,1 %). Ce secteur reste néanmoins un moteur important de l’activité globale de construction dans plusieurs États membres et une nouvelle hausse de 4 % est attendue pour 2016.

En 2015, de bons niveaux d’activité ont été observés en Allemagne (+5 %), où la construction résiden-tielle représente près de 60 % de la production totale de la construction, en Irlande (+10,4 %), en raison de projections de hausses importantes de la population, aux Pays-Bas (+23 %), notamment à cause d’un afflux important de demandeurs d’asile qui auront besoin de loge-ments, en Pologne (+6,6 %), en Espagne (+6,5 %), où le secteur a compensé le ralentissement de la croissance du génie civil et des investissements publics en général, en Suède (+23,8 %) et au Royaume-Uni (+6,5 %).

Au même moment, d’autres pays ont enregistré un niveau d’activité plus ou moins inchangé ; c’est le cas de l’Au-triche (0,5 %), de la Bulgarie (+0,1 %) et du Danemark (+0,6 %), où une croissance est attendue pour 2016 (+3,8 %). D’autres pays ont parfois dû faire face à un net recul de l’activité : c’est le cas de la France (-3,9 %) et de

Mittelfristig sollte sich in den kommenden Jahren aus der Investitionsoffensive für Europa (auch bekannt als „Juncker-Plan“) eine positive Wirkung für öffentliche und private Investitionen und damit auch für die Bautätigkeit ergeben. Es wird erwartet, dass der Plan über drei Jahre hinweg mindestens 315 Mrd. Euro an Investitionen „freisetzen“ wird.

3. Wohnungsneubau

Das historisch niedrige Niveau von Zinsen und Hypothekenzinsen erweist sich weiterhin als Stütze für den Wohnungsneubau, auch wenn dessen Wachstum 2015 mit +3,5 % schwächer ausfiel als 2014 (+6,1 %). Damit bleibt der Wohnungsneubau ein wichtiger Motor der Gesamtbautätigkeit in mehreren Mitgliedstaaten. Für 2016 wird ein weiteres Wachstum von 4,0 % prognostiziert.

2015 verzeichnete der Wohnungsneubau eine gute Entwicklung in Deutschland (+5,0 %), wo der Wohnungsbau rund 60 % der gesamten Bautätigkeit ausmacht; in Irland (+10,4 %), aufgrund von Prognosen für eine starke Zunahme der Bevölkerungszahl; in den Niederlanden (+23 %), unter anderem wegen des starken Zustroms von Asylsuchenden, für die Wohnraum benötigt wird; in Polen (+6,6 %); in Spanien (+6,5 %), wo der Wohnungsneubau das ver-langsamte Wachstum im Tiefbau und der öffentlichen Investitionen im Allgemeinen kompensierte; in Schweden (+23,8 %) und im Vereinigten Königreich (+6,5 %).

Zugleich stagnierte der Sektor in anderen Ländern mehr oder weniger, beispiels-weise in Österreich (-0,5 %), Bulgarien (+0,1 %) und Dänemark (+0,6 %), wo allerdings für 2016 eine Steigerung prog-nostiziert wird (+3,8 %) Andere Länder hatten mit einer teils stark rückläufigen Entwicklung im Wohnungsneubau zu kämpfen, so Frankreich (-3,9 %) und Finnland (-3,0 %), wobei jedoch

14

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

Country 2015a 2012 2013 2014 2015a 2016bAT Austria 15,404 3.9 -1.5 -1.4 -0.2 1.0

BE Belgium 16,936 -3.7 -1.7 6.7 3.0 -1.6

BG Bulgaria 830 -16.5 -4.3 -0.4 1.5 NA

CZ Czech Rep. 2,500 1.0 -13.2 7.2 -15.5 NA

DE Germany 157,750 3.4 -0.7 3.3 1.5 2.0

DK Denmark 8,961 -5.1 -2.9 3.7 0.6 3.1

EE Estonia NA 17.7 11.5 24.1 NA NA

ES Spain 56,255 -6.2 -5.6 -1.1 7.6 6.7

FI Finland 10,864 -3.6 -3.3 -5.6 1.8 4.4

FR France 71,565 -2.0 -2.4 -5.9 -1.8 3.0

GR Greece NA NA NA NA NA NA

IE Ireland 5,612 -8.7 -0.9 12.7 10.4 19.9

IT Italy 63,110 -4.4 -3.7 -4.1 -1.4 -0.1

LT Lithuania 354 17.3 13.2 50.2 36.5 NA

NL Netherlands 23,250 -11.6 -7.3 0.6 15.2 6.5

PL Poland 11,600 16.3 0.0 3.7 4.5 4.3

PT Portugal 2,611 -20.0 -18.0 -10.0 5.0 4.0

RO Romania 4,733 -2.5 -13.2 63.4 -2.5 5.0

SE Sweden 17,981 -11.8 0.9 19.8 16.7 7.6

SI Slovenia 160 37.8 -9.7 -10.4 -10.7 -28.4

UK United Kingdom 65,368 -1.7 7.4 20.2 3.6 NA

EU European Union 535,845 -2.4 -1.0 4.6 2.8 3.0

CH Switzerland 26,298 3.7 6.6 -1.9 -4.0 -1.0

NO Norway 15,972 6.5 2.8 -4.4 1.8 2.7

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

Country 2015a 2012 2013 2014 2015a 2016bAT Austria 10,628 4.5 -1.7 -1.5 -0.5 1.0

BE Belgium 7,192 -3.3 -1.6 11.9 3.0 -7.5

BG Bulgaria 672 -18.7 -5.9 -2.5 0.1 NA

CZ Czech Rep. 1,890 48.9 -12.5 -18.0 -6.0 NA

DE Germany 50,000 5.1 4.9 8.4 5.0 5.0

DK Denmark 1,930 -19.1 -11.1 -2.2 0.6 3.8

EE Estonia NA 19.1 4.5 63.3 NA NA

ES Spain 33,970 -7.5 -7.0 -1.5 6.5 6.5

FI Finland 4,454 -9.6 -9.6 -11.6 -3.0 5.0

FR France 31,135 -3.4 -3.5 -11.5 -3.9 5.5

GR Greece NA NA NA NA NA NA

IE Ireland 2,430 -6.1 2.3 28.0 13.3 37.7

IT Italy 19,837 -11.1 -13.4 -13.9 -6.0 -3.5

LT Lithuania 161 -1.3 41.2 47.7 -16.7 NA

NL Netherlands 10,500 -16.8 -12.3 -4.5 23.2 13.3

PL Poland 8,100 17.2 -1.3 2.7 6.6 4.9

PT Portugal 1,671 -23.4 -23.3 -19.9 3.4 2.4

RO Romania 2,905 -5.2 -24.7 75.5 -2.5 5.0

SE Sweden 9,566 -21.1 10.4 33.7 23.8 12.8

SI Slovenia 80 9.8 -19.8 -12.5 -10.7 -30.0

UK United Kingdom 35,954 -4.9 10.8 32.1 6.5 NA

EU European Union 233,077 -4.9 -0.9 6.1 3.5 4.0

CH Switzerland 19,250 3.9 6.3 -1.8 -3.1 -1.5

NO Norway 10,613 7.2 4.1 -7.8 1.2 3.3

HOUSEBUILDING LOGEMENT WOHNUNGSBAU

NEW HOUSEBUILDING LOGEMENT NEUF WOHNUNGSNEUBAU

15

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

in both countries the perspectives for 2016 are good (+5.5% in France and +5.0%), as well as in Italy (-6.0%), where the num-ber of construction permits has been steadily declining over the last decade, Lithuania (-16.7%), Romania (-2.5%) and Slovenia (-9.9%), amongst others because of the absence of long-term state housebuilding policy.

4. Rehabilitation and maintenance

Rehabilitation and maintenance activity maintained at a relatively stable development before and throughout the crisis, thereby playing an important cushioning effect for the entire construction sector. This trend is expected to continue in the near future. In 2015, R&M activities grew by 2.6%, reflecting growth in this segment in the majority of EU countries. A further increase of 2.2% is expected in 2016.

In 2015 this segment has developed positively in Belgium (+3.0%), Bulgaria (+8.2%), thanks to significant investments in energy efficiency works, Finland (+5.5%), thanks to public incentives, Germany (+5.0), Ireland (+8.3%), Netherlands (+9.4%), where it has been strongly supported by the low VAT rate for housing renovation which however will now expire and significantly slow down the activity in this segment in 2016 (+0.8), Portugal (+8.0%), Spain (+9.4%), supported by improving household income and confidence levels, and in Sweden (+11.6%), where the less favourable tax deduction scheme for renovation works that entered into force at the beginning of 2016 will slow down the growth (+0.7%).

In contrast, in 2015 R&M activi-ties declined in France and more sharply in Romania and Slovenia

la Finlande (-3 %), mais dans ces deux pays, les perspectives pour 2016 sont bonnes (+5,5 % en France et +5 %), ainsi que de l’Italie (-6 %), où le nombre de permis de bâtir n’a cessé de dimi-nuer au cours de la dernière décennie, la Lituanie (-16,7 %), la Roumanie (-2,5 %) et la Slovénie (-9,9 %), notam-ment à cause de l’absence de politique à long terme en matière de construc-tion résidentielle.

4. Réhabilitation et maintenance

L’activité de réhabilitation et de main-tenance a enregistré une évolution relativement stable avant et pendant la crise, jouant ainsi un rôle d’amortisseur important pour tout le secteur de la construction. Cette tendance devrait se poursuivre dans un avenir proche. En 2015, les activités de R&M ont augmenté de 2,6 %, ce qui reflète une progression de ce segment dans la majorité des pays de l’UE. Une aug-mentation supplémentaire de 2,2 % est prévue en 2016.

En 2015, ce segment a connu une évolution positive en Belgique (+3 %), en Bulgarie (+8,2 %), grâce à des investissements importants dans des travaux en matière d’efficacité énergé-tique, en Finlande (+5,5 %), grâce aux aides publiques, en Allemagne (+5), en Irlande (+8,3 %), aux Pays-Bas (+9,4 %), où l’activité a été fortement soutenue par le faible taux de TVA pour les rénovations de logements, lequel arrive toutefois à expiration et risque de ralentir considérablement l’activité dans ce segment en 2016 (+0,8 %), au Portugal (+8 %), en Espagne (+9,4 %), où l’activité est soutenue pour une amélioration des revenus des ménages et des niveaux de confiance, et en Suède (+11,6 %), où le système de déduction fiscale moins favorable pour les travaux de rénovation qui est entré en vigueur début 2016 devrait ralentir la croissance (+0,7 %).

Par contre, en 2015, les activités de R&M ont connu une baisse en France et une chute encore plus marquée en

die Aussichten für 2016 in beiden Ländern gut sind (+5,5 % in Frankreich und +5,0 % in Finnland); außerdem Italien (-6,0 %), wo die Zahl erteilter Baugenehmigungen im Laufe der vergangenen zehn Jahre kontinuier-lich gesunken ist; Litauen (-16,7 %), Rumänien (-2,5 %) und Slowenien (-9,9 %), unter anderem wegen einer fehlenden langfristig ausgerichteten staatlichen Wohnungsbaupolitik.

4. Modernisierung und Instandhaltung

Das Segment Modernisierung und Instandhaltung entwickelte sich vor und während der Krise relativ stabil und hatte damit eine erhebliche stützende Wirkung für die Bauwirtschaft insgesamt. Diese Entwicklung soll sich in naher Zukunft entsprechend fortsetzen. Im Jahr 2015 ist der Anteil des Modernisierungs- und Instandhaltungssegments um 2,6 % gestiegen, was ein Wachstum dieses Sektors in den meisten EU-Staaten widerspiegelt. Für 2016 wird ein zusätzli-ches Plus von 2,2 % erwartet.

2015 entwickelte sich das Segment positiv in Belgien (+3,0 %); Bulgarien (+8,2 %), dank umfassender Investitionen in Baumaßnahmen zur Förderung der Energieeffizienz; Finnland (+5,5 %), dank öffentli-cher Anreize; Deutschland (+5,0 %); Irland (+8,3 %); den Niederlanden (+9,4 %), wo der niedrige MwSt.-Satz für Renovierungsmaßnahmen im Bereich Wohnraum eine beflügelnde Wirkung zeigte (+0,8 %) (dieser läuft nun allerdings aus und dürfte das Wachstum in diesem Segment 2016 erheblich bremsen); Portugal (+8,0 %); Spanien (+9,4 %), getragen von stei-genden Einkommen und wachsendem Vertrauen der privaten Haushalte; und in Schweden (+11,6 %), wo allerdings die Anfang 2016 in Kraft getretene weniger günstige Steuerabzugsregelung für Renovierungsarbeiten das Wachstum künftig bremsen dürfte (+0,7 %).

Hingegen verzeichnete das Segment im Jahr 2015 Rückgänge in Frankreich sowie – in wesentlich schärferem

16

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

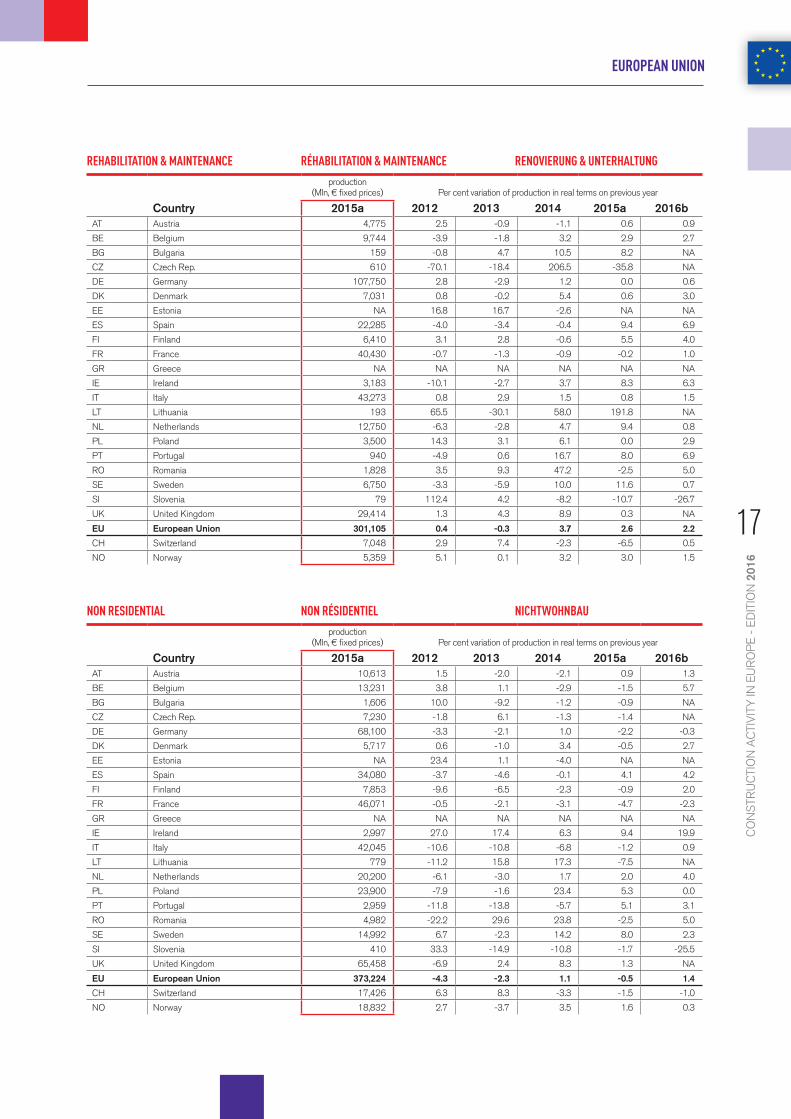

Country 2015a 2012 2013 2014 2015a 2016bAT Austria 4,775 2.5 -0.9 -1.1 0.6 0.9

BE Belgium 9,744 -3.9 -1.8 3.2 2.9 2.7

BG Bulgaria 159 -0.8 4.7 10.5 8.2 NA

CZ Czech Rep. 610 -70.1 -18.4 206.5 -35.8 NA

DE Germany 107,750 2.8 -2.9 1.2 0.0 0.6

DK Denmark 7,031 0.8 -0.2 5.4 0.6 3.0

EE Estonia NA 16.8 16.7 -2.6 NA NA

ES Spain 22,285 -4.0 -3.4 -0.4 9.4 6.9

FI Finland 6,410 3.1 2.8 -0.6 5.5 4.0

FR France 40,430 -0.7 -1.3 -0.9 -0.2 1.0

GR Greece NA NA NA NA NA NA

IE Ireland 3,183 -10.1 -2.7 3.7 8.3 6.3

IT Italy 43,273 0.8 2.9 1.5 0.8 1.5

LT Lithuania 193 65.5 -30.1 58.0 191.8 NA

NL Netherlands 12,750 -6.3 -2.8 4.7 9.4 0.8

PL Poland 3,500 14.3 3.1 6.1 0.0 2.9

PT Portugal 940 -4.9 0.6 16.7 8.0 6.9

RO Romania 1,828 3.5 9.3 47.2 -2.5 5.0

SE Sweden 6,750 -3.3 -5.9 10.0 11.6 0.7

SI Slovenia 79 112.4 4.2 -8.2 -10.7 -26.7

UK United Kingdom 29,414 1.3 4.3 8.9 0.3 NA

EU European Union 301,105 0.4 -0.3 3.7 2.6 2.2

CH Switzerland 7,048 2.9 7.4 -2.3 -6.5 0.5

NO Norway 5,359 5.1 0.1 3.2 3.0 1.5

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

Country 2015a 2012 2013 2014 2015a 2016bAT Austria 10,613 1.5 -2.0 -2.1 0.9 1.3

BE Belgium 13,231 3.8 1.1 -2.9 -1.5 5.7

BG Bulgaria 1,606 10.0 -9.2 -1.2 -0.9 NA

CZ Czech Rep. 7,230 -1.8 6.1 -1.3 -1.4 NA

DE Germany 68,100 -3.3 -2.1 1.0 -2.2 -0.3

DK Denmark 5,717 0.6 -1.0 3.4 -0.5 2.7

EE Estonia NA 23.4 1.1 -4.0 NA NA

ES Spain 34,080 -3.7 -4.6 -0.1 4.1 4.2

FI Finland 7,853 -9.6 -6.5 -2.3 -0.9 2.0

FR France 46,071 -0.5 -2.1 -3.1 -4.7 -2.3

GR Greece NA NA NA NA NA NA

IE Ireland 2,997 27.0 17.4 6.3 9.4 19.9

IT Italy 42,045 -10.6 -10.8 -6.8 -1.2 0.9

LT Lithuania 779 -11.2 15.8 17.3 -7.5 NA

NL Netherlands 20,200 -6.1 -3.0 1.7 2.0 4.0

PL Poland 23,900 -7.9 -1.6 23.4 5.3 0.0

PT Portugal 2,959 -11.8 -13.8 -5.7 5.1 3.1

RO Romania 4,982 -22.2 29.6 23.8 -2.5 5.0

SE Sweden 14,992 6.7 -2.3 14.2 8.0 2.3

SI Slovenia 410 33.3 -14.9 -10.8 -1.7 -25.5

UK United Kingdom 65,458 -6.9 2.4 8.3 1.3 NA

EU European Union 373,224 -4.3 -2.3 1.1 -0.5 1.4

CH Switzerland 17,426 6.3 8.3 -3.3 -1.5 -1.0

NO Norway 18,832 2.7 -3.7 3.5 1.6 0.3

REHABILITATION & MAINTENANCE RÉHABILITATION & MAINTENANCE RENOVIERUNG & UNTERHALTUNG

NON RESIDENTIAL NON RÉSIDENTIEL NICHTWOHNBAU

17

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

(respectively -0.2%, -2.5% and -9.9%). In France such devel-opment occurred despite a new tax credit for energy renovation and an attractive VAT reduced rate (5.5%) for renovation works, but can be explained by the low energy prices.

5. Non-residential buildings

Contrary to all the other sub-sec-tors, the non-residential sector was the only one to show a nega-tive trend in 2015 (-0.5%), mainly because of the decrease of its public component (-2.4%), due to the low level of public investment in several Member States. The overall situation is expected to improve slightly in 2016 (+1.4%) despite the fact that investors remain hesitant with regards to external risks (oil price decline, economic development in China and in other emerging econo-mies, ongoing turbulence in the Euro-zone).

The situation is however quite contrasted amongst the various EU countries.

In 2015 the sector performed well in Ireland (+9.4%), Portugal (+5.1%), Spain (+4.1%) and in Sweden (+8.0%), pulled by the pri-vate component, which in the case of Sweden reached a double-digit growth of 10.9%, mainly thanks to increasing investment in the industrial sector.

In several other Member States a sometimes significant decline was recorded in the public segment. It is the case of France (-6.5%), Germany (-2.7%), Lithuania (-20.3%) and the United Kingdom (-4.3%),

Roumanie et en Slovénie (respecti-vement -0,2 %, -2,5 % et -9,9 %). En France, cette évolution s’est produite malgré un nouveau crédit d’impôt pour la rénovation énergétique et un taux de TVA réduit attractif (5,5 %) pour les travaux de rénovation, mais elle peut s’expliquer par la faiblesse des prix de l’énergie.

5. Construction non-résidentielle

Contrairement à tous les autres sous-secteurs, la construction non résidentielle a été le seul segment à enregistrer une tendance négative en 2015 (-0,5 %), surtout à cause de la baisse de sa composante publique (-2,4 %) qui est due au faible niveau d’investissements publics dans plusieurs États membres. La situation globale devrait s’améliorer légèrement en 2016 (+1,4 %) malgré le fait que les investisseurs restent circonspects face aux risques externes (baisse des prix du pétrole, développement éco-nomique en Chine et dans d’autres économies divergentes, turbulences actuelles dans la zone euro).

La situation est toutefois relative-ment contrastée parmi les différents pays de l’UE.

En 2015, le secteur a réalisé de bons résultats en Irlande (+9,4 %), au Portugal (+5,1 %), en Espagne (+4,1 %) et en Suède (+8 %), où il a été entraîné par la composante privée qui, dans le cas de la Suède, a atteint une croissance à deux chiffres de 10,9 %, surtout grâce à la progression des inves-tissements dans le secteur industriel.

Dans plusieurs autres États membres, une baisse parfois impor-tante a été enregistrée dans le seg-ment public. C’est le cas de la France (-6,5 %), de l’Allemagne (-2,7 %), de la Lituanie (-20,3 %) et du Royaume-Uni (-4,3 %).

Ausmaß – Rumänien und Slowenien (jeweils -0,2 %, -2,5 % und -9,9 %). Die Entwicklung in Frankreich ergab sich trotz neuer steuerlicher Anreize für Energieeffizienzmaßnahmen und eines attraktiven reduzierten MwSt.-Satzes (5,5 %) für Renovierungsarbeiten, was sich auch durch niedrige Energiepreise erklären lässt.

5. Nichtwohnungsbau

Im Gegensatz zu allen anderen Sektoren entwickelte sich der Wirtschaftsbau 2015 insge-samt negativ (-0,5 %), vor allem wegen der negativen Entwicklung im öffentlichen Bereich (-2,4 %) aufgrund des niedrigen Niveaus öffentlicher Investitionen in mehre-ren Mitgliedstaaten. Die Gesamtlage soll sich laut Prognose 2016 leicht verbessern (+1,4 %), auch wenn Investoren wegen externer Risiken (Ölpreisverfall, Konjunkturentwickung in China und anderen aufstreben-den Volkswirtschaften, andauernde Turbulenzen in der Eurozone) zurück-haltend bleiben.

Allerdings präsentiert sich die Lage in den einzelnen EU-Staaten sehr unterschiedlich.

2015 lief es für den Sektor gut in Irland (+9,4 %), Portugal (+5,1 %), Spanien (+4,1 %) und Schweden (+8,0 %), beflügelt durch den pri-vaten Bereich, in dem im Falle von Schweden zweistellige Zuwächse zu verzeichnen waren (+10,9 %), vor allem dank zunehmender Investitionen in der Industrie.

In mehreren anderen Mitgliedstaaten verzeichnete das öffentliche Segment ein teils erhebliches Minus. Dies gilt für Frankreich (-6,5 %), Deutschland (-2,7 %), Litauen (-20,3 %) und das Vereinigte Königreich (-4,3 %).

18

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

Country 2015a 2012 2013 2014 2015a 2016bAT Austria NA NA NA NA NA NA

BE Belgium 8,622 3.8 1.1 -2.9 -1.5 5.7

BG Bulgaria 1,595 10.0 -9.2 -1.7 -0.9 NA

CZ Czech Rep. 4,080 17.0 -28.1 3.8 13.6 NA

DE Germany 57,150 -0.8 -2.4 1.7 -2.2 -0.4

DK Denmark 2,552 -12.9 -3.0 0.1 -5.6 0.8

EE Estonia NA NA NA NA NA NA

ES Spain 27,483 -0.4 0.1 0.9 4.9 7.3

FI Finland 4,995 -10.9 -14.6 -3.0 -1.5 2.5

FR France 24,345 -0.8 -2.0 -2.6 -3.0 -1.6

GR Greece NA NA NA NA NA NA

IE Ireland 1,561 82.1 28.7 4.8 10.7 26.9

IT Italy 33,567 -10.6 -11.2 -7.3 -1.2 -0.4

LT Lithuania 599 0.2 13.0 20.7 -2.8 NA

NL Netherlands NA NA NA NA NA NA

PL Poland NA NA NA NA NA NA

PT Portugal 1,849 -13.0 -13.0 -2.0 7.0 4.0

RO Romania 3,841 -21.1 29.5 2.6 -2.5 5.0

SE Sweden 10,238 7.8 -2.6 13.5 10.9 2.5

SI Slovenia NA NA NA NA NA NA

UK United Kingdom 47,896 -3.3 4.1 10.3 3.6 NA

EU European Union 230,372 -3.0 -1.8 1.5 0.3 1.6

CH Switzerland 10,770 5.9 12.3 -3.3 -1.5 -1.0

NO Norway 12,022 3.0 -5.1 3.1 -2.5 -0.7

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

Country 2015a 2012 2013 2014 2015a 2016bAT Austria NA NA NA NA NA NA

BE Belgium 4,609 3.8 1.1 -2.9 -1.5 5.7

BG Bulgaria 11 0.0 -25.0 266.7 0.0 NA

CZ Czech Rep. 3,150 -27.5 81.3 -5.8 -15.8 NA

DE Germany 10,950 -14.0 -0.9 -2.9 -2.7 0.5

DK Denmark 3,165 18.6 0.9 6.6 4.1 4.1

EE Estonia NA NA NA NA NA NA

ES Spain 6,598 -12.5 -19.1 -3.6 0.8 -8.8

FI Finland 2,858 -6.1 4.7 3.0 3.5 1.0

FR France 21,727 -0.2 -2.3 -3.7 -6.5 -3.1

GR Greece NA NA NA NA NA NA

IE Ireland 1,436 -0.3 7.1 7.9 8.1 12.3

IT Italy 8,478 -10.6 -9.3 -5.1 -1.3 6.0

LT Lithuania 180 -32.1 23.6 8.9 -20.3 NA

NL Netherlands NA NA NA NA NA NA

PL Poland NA NA NA NA NA NA

PT Portugal 1,110 -10.0 -15.0 -11.0 2.0 1.5

RO Romania 1,141 -34.7 31.2 309.1 -2.5 5.0

SE Sweden 4,754 4.6 -1.6 15.5 2.2 2.0

SI Slovenia NA NA NA NA NA NA

UK United Kingdom 17,562 -14.1 -1.2 3.6 -4.3 NA

EU European Union 87,729 -8.7 -3.5 3.5 -2.4 1.0

CH Switzerland 6,655 6.8 2.5 -3.3 -1.5 -1.0

NO Norway 6,810 1.9 -0.6 4.2 9.7 2.0

NON RESIDENTIAL PRIVATE NON RÉSIDENTIEL PRIVÉ NICHTWOHNBAU PRIVAT

NON RESIDENTIAL PUBLIC NON RÉSIDENTIEL PUBLIC NICHTWOHNBAU ÖFFENTLICH

19

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

Denmark and Finland, where the private segment declined by 5.6% and 1.5% respectively, and the public one increased respec-tively by 4.1% and 3.5%, are two exceptions to the main trends.

6. Civil engineering

Contrary to what was fore-casted in our previous report, civil engineering activity in 2015 increased with a surprisingly high growth rate of 6.2%, which can be explained in large part by the boom recorded in the United Kingdom (+34%) and Romania (+20%), for the latter thanks to a higher volume of financial resources allocated to invest-ments and a greater volume of European funds allocated to sec-torial programmes, in particular in roads and railway infrastructure.

Civil engineering activity also increased in several other countries, but to a lesser extent, such as in Belgium (+3%), where changes in the invest-ment cycle of local authorities is probably approaching a peak ahead of the forthcoming local elections in 2018, in Denmark (+5.1%), mainly thanks to large projects, especially in trans-port infrastructure, in Ireland (+4%), where the “Capital Plan” provides significant funding for investment in education facili-ties, as well as in health infra-structure, in energy efficiency and renewable energy pro-grammes and in flood mitigation initiatives, in the Netherlands (+2.8%), despite the lowered contribution of the central government and the transfer of several tasks (healthcare, labour market) to municipalities, in Spain (+3%), where the elec-toral cycle and the loosening of the fiscal consolidation process

Le Danemark et la Finlande, où le segment privé a baissé respective-ment de 5,6 % et 1,5 % et le seg-ment public a augmenté de 4,1 % et 3,5 %, sont deux exceptions aux principales tendances observées.

6. Génie civil

Contrairement aux prévisions annon-cées dans notre précédent rapport, l’activité du génie civil en 2015 a connu un taux de croissance étonnam-ment élevé de 6,2 %, ce qui peut en grande partie s’expliquer par l’expan-sion enregistrée au Royaume-Uni (+34 %) et en Roumanie (+20 %). Dans ce dernier cas, la progression est imputable à l’allocation de ressources financières accrues aux investisse-ments et à un volume plus important de fonds européens alloués aux programmes sectoriels, en particulier dans les infrastructures routières et ferroviaires.

L’activité du génie civil a aussi aug-menté dans plusieurs autres pays, mais dans une moindre mesure, comme en Belgique (+3 %), où des changements dans le cycle d’in-vestissement des autorités locales atteignent probablement leur apogée en vue des prochaines élections régionales en 2018, au Danemark (+5,1 %), surtout grâce à de gros projets, principalement dans les infrastructures de transport, en Irlande (+4 %), où le « Capital Plan » propose un financement conséquent pour des investissements dans des établisse-ments d’enseignement ainsi que dans des infrastructures de santé, dans des programmes d’efficacité énergétique et d’énergie renouvelable ainsi que des initiatives pour la prévention des inondations, aux Pays-Bas (+2,8 %), malgré la baisse de la contribution du gouvernement central et le transfert de plusieurs compétences (soins de santé, marché de l’emploi) aux municipalités, en Espagne (+3 %), où le cycle électoral et l’assouplissement du processus de consolidation fiscale

Dänemark und Finnland bilden eine Ausnahme zum allgemeinen Trend. Hier erzielte der öffentliche Bereich Zuwächse von 4,1 % bzw. 3,5 %, wohingegen im privaten Bereich ein Rückgang von 5,6 % bzw. 1,5 % zu Buche schlug.

6. Tiefbau

Gegenläufig zur unserer Prognose im letzten Bericht wuchs die Tiefbautätigkeit im Jahr 2015 mit einer Wachstumsrate von +6,2 % überraschend stark. Zurückzuführen ist dies in weiten Teilen auf den Boom im Vereinigten Königreich (+34 %) und in Rumänien (+20 %), in letzterem Fall dank vermehr-ter finanzieller Ressourcen für Investitionen und eines beträchtli-chen Volumens von EU-Mitteln für Tiefbaumaßnahmen, insbesondere auf dem Gebiet der Straßen- und Eisenbahninfrastruktur.

Auch in einigen anderen Ländern wuchs die Tiefbautätigkeit, aller-dings in geringerem Umfang, zum Beispiel in Belgien (+3 %), wo Veränderungen im Investitionszyklus der lokalen Behörden im Vorfeld der Kommunalwahlen im Jahr 2018 einen baldigen Höhepunkt nahelegen; in Dänemark (+5,1 %), vor allem dank großer Projekte insbesondere für die Verkehrsinfrastruktur; in Irland (+ 4 %), wo der „Capital Plan“ umfassende, vorwiegend staat-liche, Mittel für Investitionen in Bildungseinrichtungen, Programme für mehr Energieeffizienz bzw. zu erneuerbaren Energien und Hochwasserschutzmaßnahmen vorsieht; in den Niederlanden (+2,8 %), trotz des reduzierten Beitrags der Zentralregierung und der Verlagerung mehrerer Aufgabenbereiche (Gesundheit, Arbeitsmarkt) an die Städte und Gemeinden; in Spanien (+3 %), wo sich der Finanzierungsrahmen aufgrund der Wahlen und der Lockerung des finanzpolitischen

20

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

production (Mln, € fixed prices) Per cent variation of production in real terms on previous year

Country 2015a 2012 2013 2014 2015a 2016bAT Austria 6,897 1.0 -3.9 1.5 0.0 0.6

BE Belgium 6,846 8.0 -4.4 5.4 3.0 0.0

BG Bulgaria 4,192 2.8 -5.4 31.6 -1.1 NA

CZ Czech Rep. 5,930 -7.2 -18.3 -5.7 -5.7 NA

DE Germany 37,000 -3.5 -0.3 5.2 -1.2 2.7

DK Denmark 7,155 4.9 2.2 -2.4 5.1 -2.7

EE Estonia 638 12.2 2.6 -10.2 -9.4 NA

ES Spain 21,153 -24.0 -23.0 -5.5 3.0 0.0

FI Finland 6,903 -0.2 1.4 -2.2 -1.0 0.0

FR France 35,185 -2.6 3.8 -6.0 -4.5 -3.0

GR Greece 6,724 12.8 -5.9 1.3 -12.1 NA

IE Ireland 3,297 -6.3 -3.0 8.9 4.0 5.8

IT Italy 14,435 -10.6 -9.3 -5.1 -1.3 6.0

LT Lithuania 949 -8.1 8.0 10.4 -13.4 NA

NL Netherlands 14,000 -8.1 -4.7 2.4 2.8 2.1

PL Poland 18,100 -1.8 -13.5 19.1 7.7 12.2

PT Portugal 5,478 -15.0 -14.0 -1.0 1.0 1.5

RO Romania 14,976 8.1 11.6 -18.2 20.0 5.2

SE Sweden 8,213 11.7 -3.3 8.5 0.7 -0.6

SI Slovenia 1,048 31.0 5.1 30.4 -9.0 -15.2

UK United Kingdom 22,486 -7.9 7.2 -2.4 34.0 NA

EU European Union 241,606 -5.8 -1.6 -0.8 6.2 1.8

CH Switzerland 12,037 8.5 0.0 -1.7 -2.0 0.0

NO Norway 14,139 10.3 4.5 7.0 3.7 11.3

Thousand units Variation on previous year

Country 2015a (x1000) 2013 (%) 2014 (%) 2015a (%) 2016b (%)AT Austria 264 -0.4 0.3 -0.5 1.3BE Belgium 274 -1.0 -1.6 -0.7 -1.6BG Bulgaria 183 -3.8 -0.6 2.8 3.8CY Cyprus 25 -26.7 -14.8 -0.9 NACZ Czech Rep. 415 -9.2 -2.3 9.8 1.2DE Germany 2,431 0.7 0.6 -0.5 0.8DK Denmark 175 -0.5 1.5 4.8 1.3EE Estonia 42 1.4 -1.1 NA NAES Spain 1,074 -11.4 -3.5 8.1 4.5FI Finland 186 -1.3 -2.1 -0.2 2.2FR France 1,763 -1.1 -1.9 -2.3 -1.0GR Greece 145 -19.2 -6.6 -4.3 NAHR Croatia 93 -6.4 -3.3 NA NAHU Hungary 272 0.9 5.2 NA NAIE Ireland 127 0.4 12.6 8.5 NAIT Italy 1,488 -8.6 -4.4 0.3 NALT Lithuania 105 10.9 0.0 6.0 NALU Luxembourg 40 NA NA NA NALV Latvia 64 NA NA NA NAMT Malta 9 NA NA NA NANL Netherlands 452 -5.7 -3.5 -2.4 4.0PL Poland 1,140 -5.5 -0.9 0.5 0.9PT Portugal 276 -19.3 -4.4 0.1 0.9RO Romania 417 3.0 4.0 7.2 3.2SE Sweden 308 -0.5 0.0 -0.9 1.2SI Slovenia 54 -9.7 -0.4 0.6 -9.1SK Slovakia 223 NA NA NA NAUK United Kingdom 2,110 -0.5 2.9 0.5 NAEU28 European Union 14,155 -3.9 -0.8 0.9 NACH Switzerland 327 1.1 0.5 -0.3 -1.0NO Norway 206 1.5 1.5 3.0 2.0TR TR - Turkey 1,914 4.3 7.3 0.1 1.9

CIVIL ENGINEERING GÉNIE CIVIL TIEFBAU

TOTAL EMPLOYMENT IN CONSTRUCTION* EMPLOI TOTAL DANS LA CONSTRUCTION* GESAMTBESCHÄFTIGUNG IM BAUWESEN*

* NACE Section F

21

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

brought an improvement in the financial framework but which should nevertheless show a stagnation or a slight fall in 2016, and in Poland (+7.7%), where a special focus is given to investments co-financed by the EU.

At the same time the sector declined or stagnated in several countries, mainly because of cuts in public investment. It is the case of Estonia (-9.4%), France (-4.5%), which has been deeply affected by successive expected factors (municipal post-elections and departmental elections) and extraordinary measures (a signif-icant drop in State grants to local governments), Finland (-1%), where the lack of long-term planning is the greatest source of uncertainty, Greece (-12.1%), where the sector is expected to decline further due to cuts in public spending and delays in EU funding of new infrastructure projects, Italy (-1.3%), where an increase of 6% is expected in 2016 thanks to some measures contained in the Italian 2016 Budget Law which should remove several economic and financial obstacles that prevented the carrying out of public works in Italy over the last years, Lithuania (-13.4%) and Slovenia (-8.2%), where a further reduction of already extremely low investment activity in national road network reconstruction is expected.

The unexpected positive develop-ments of 2015 will not continue in 2016 and a smaller overall increase of 1.8% is forecasted.

ont amélioré le contexte financier mais où l’activité devrait quand même enregistrer une stagnation ou une légère baisse en 2016, et en Pologne (+7,7 %), où une attention spécifique est accordée aux investissements cofinancés par l’UE.

En même temps, le secteur a connu un déclin ou une stagnation dans plu-sieurs pays, surtout à cause de coupes dans les investissements publics. C’est le cas de l’Estonie (-9,4 %), de la France (-4,5 %), qui a été profondé-ment touchée par plusieurs facteurs successifs attendus (post-élections municipales et élections départemen-tales) et des mesures extraordinaires (une baisse importante des subven-tions de l’État aux gouvernements locaux), de la Finlande (-1 %), où le manque de planification à long terme constitue la plus grande source d’incertitude, de la Grèce (-12,1 %), où le secteur devrait poursuivre son déclin à cause de coupes dans les dépenses publiques et des retards dans le finan-cement européen de nouveaux projets d’infrastructure, de l’Italie (-1,3 %), où une croissance de 6 % est attendue en 2016 grâce à certaines mesures adoptées dans la loi italienne sur le budget 2016 qui devrait supprimer plusieurs obstacles économiques et financiers qui empêchaient la réalisa-tion de travaux publics dans le pays au cours de ces dernières années, de la Lituanie (-13,4 %) et de la Slovénie (-8,2 %), où il faut s’attendre à une nouvelle baisse du niveau déjà très bas des investissements dans la recons-truction du réseau routier national.

Les développements positifs inatten-dus de 2015 ne se poursuivront pas en 2016, et une croissance globale plus faible de 1,8 % est prévue.

Konsolidierungsprozesses verbessert hat, wo jedoch für 2016 dennoch eine stagnierende oder leicht rückläufige Entwicklung zu erwarten ist; und in Polen (+ 7,7 %), wo ein besonderer Schwerpunkt auf von der EU kofinanzierten Investitionen liegt.

Zugleich stagnierte der Sektor in meh-reren Ländern oder verzeichnete ein Minus, vorwiegend wegen Einschnitten bei öffentlichen Investitionen. Dies war der Fall in Estland (-9,4 %); Frankreich (-4,5 %), aufgrund von starken Beeinträchtigungen durch aufeinan-der folgende absehbare Ereignisse (Nachwahlen auf kommunaler Ebene und Wahlen auf Departement-Ebene) und außergewöhnliche Maßnahmen (erhebliche Einschnitte bei Regierungsmitteln auf kommuna-ler Ebene ); Finnland (-1 %), wo der Mangel an langfristiger Planung den größten Unsicherheitsfaktor darstellt; Griechenland (-12,1 %), wo der Tiefbau den Erwartungen zufolge weitere Rückgänge verzeichnen wird aufgrund von Einschnitten bei den öffentlichen Ausgaben und Verzögerungen bei der Bereitstellung von EU-Mitteln für neue Infrastrukturprojekte; Italien (-1,3 %), wo 2016 ein Wachstum von 6 % erwartet wird dank bestimmter Maßnahmen aus dem italienischen Haushaltsgesetz für 2016, die dafür sorgen sollen, dass die seit Jahren bestehenden wirtschaftli-chen und finanziellen Hürden für die Ausführung öffentlicher Arbeiten in Italien fallen; Litauen (-13,4 %) und Slowenien (-8,2 %), wo eine wei-tere Reduzierung der bereits extrem niedrigen Investitionstätigkeit für die Sanierung des nationalen Straßennetzes erwartet wird.

Die unerwartet positiven Entwicklungen im Jahr 2015 werden sich 2016 nicht fortsetzen, sodass insgesamt ein geringeres Gesamtwachstum von 1,8 % prognos-tiziert wird.

22

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

EUROPEAN UNION

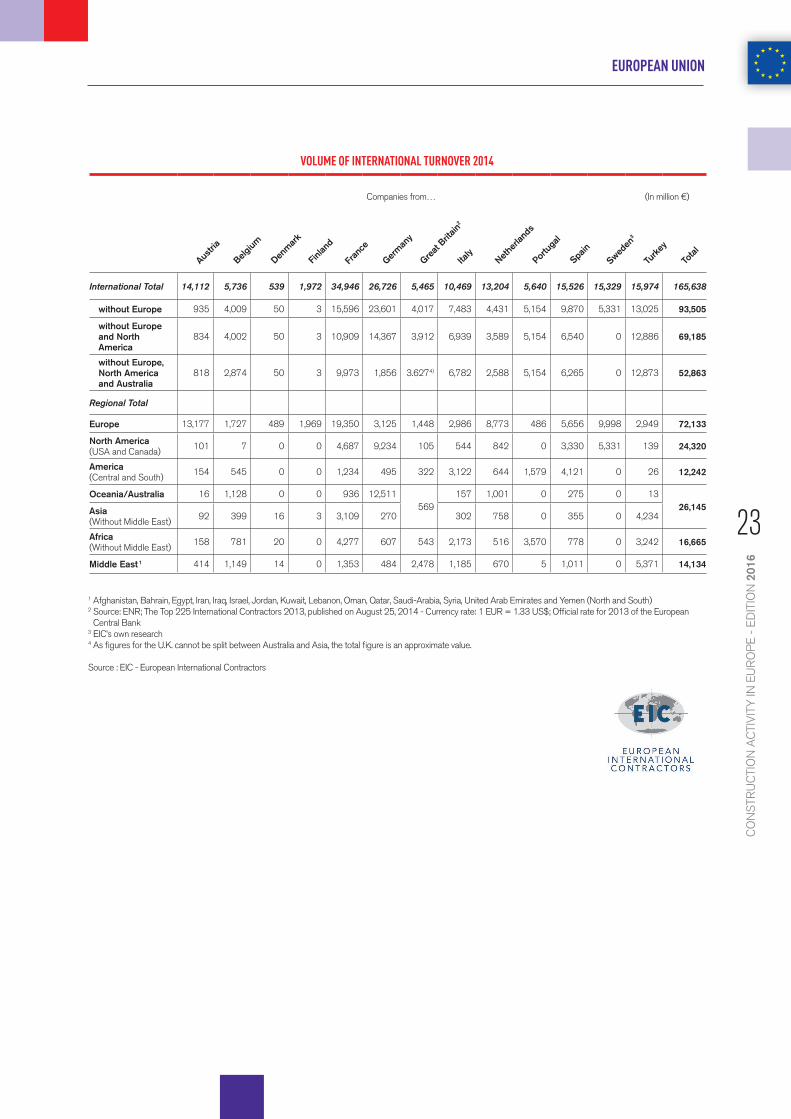

Companies from… (In million €)

International Total 14,112 5,736 539 1,972 34,946 26,726 5,465 10,469 13,204 5,640 15,526 15,329 15,974 165,638

without Europe 935 4,009 50 3 15,596 23,601 4,017 7,483 4,431 5,154 9,870 5,331 13,025 93,505

without Europe and North America

834 4,002 50 3 10,909 14,367 3,912 6,939 3,589 5,154 6,540 0 12,886 69,185

without Europe, North America and Australia

818 2,874 50 3 9,973 1,856 3.6274) 6,782 2,588 5,154 6,265 0 12,873 52,863

Regional Total

Europe 13,177 1,727 489 1,969 19,350 3,125 1,448 2,986 8,773 486 5,656 9,998 2,949 72,133

North America (USA and Canada)

101 7 0 0 4,687 9,234 105 544 842 0 3,330 5,331 139 24,320

America (Central and South)

154 545 0 0 1,234 495 322 3,122 644 1,579 4,121 0 26 12,242

Oceania/Australia 16 1,128 0 0 936 12,511 569

157 1,001 0 275 0 13 26,145 Asia

(Without Middle East)92 399 16 3 3,109 270 302 758 0 355 0 4,234

Africa (Without Middle East)

158 781 20 0 4,277 607 543 2,173 516 3,570 778 0 3,242 16,665

Middle East 1 414 1,149 14 0 1,353 484 2,478 1,185 670 5 1,011 0 5,371 14,134

VOLUME OF INTERNATIONAL TURNOVER 2014

1 Afghanistan, Bahrain, Egypt, Iran, Iraq, Israel, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi-Arabia, Syria, United Arab Emirates and Yemen (North and South)2 Source: ENR; The Top 225 International Contractors 2013, published on August 25, 2014 - Currency rate: 1 EUR = 1.33 US$; Official rate for 2013 of the European

Central Bank3 EIC’s own research4 As figures for the U.K. cannot be split between Australia and Asia, the total figure is an approximate value.

Source : EIC - European International Contractors

Austri

a

Belgium

Denm

ark

Finlan

d

Fran

ce

Germ

any

Great

Britain

2

Italy

Nethe

rland

s

Portu

gal

Spain

Sweden

3

Turk

ey

Total

23

CO

NS

TRU

CTI

ON

AC

TIV

ITY

IN E

UR

OP

E -

ED

ITIO

N 2

016

1. Overall construction activity

The Austrian economy is picking up pace, but only very slowly. According to the September forecast of the Austrian Institute of Economic Research (WIFO), Austrian GDP (real) will grow by 0.7% in 2015 and 1.4% in 2016. In particular, foreign trade remains weaker than expected and is unable to serve as a catalyst for the recovery of the Austrian economy.The consequences of the weak recovery are most visible in the labour market. Despite a steadily increasing employment rate - it has been growing for 5 consecutive years - the unem-ployment rates are increasing as well.The overall weak economic performance has had a direct impact on the Austrian construction industry. Following the remarkably strong decline (-2.1%) in real construction investment in 2013, 2014 also resulted in a decline (-1.0%). The construction sector, despite good weather conditions in H1 2014, slipped into a negative result for the annual total, emphasising the cur-rent weakness. Even if the negative trend, according to the forecast, slowed down in the year 2015 (+ 0.2%), the currently available data do not envisage prospects for an early recovery.Total construction will be close to stagnation in 2015. In the forecasting period an average growth of slightly above 1% is expected, which rather stems from building construction than from civil engineering.

2. Housebuilding

The residential construction market is improving marginally from year to year, nevertheless 2015 will be the third year in a row with a decline in housing output, even if it is close to stag-nation. In the coming years a small growth is expected, which will mainly stem from new con-struction of flats and multi-storey buildings. In 2017 and 2018 the market will be bouyed by the recently announced stimulus package for housing, which should fulfil future housing needs especially in urban areas, above all in Vienna. Total housing construction is therefore ex-pected to grow slightly above 1% from 2016 onwards.

3. Non-residential construction

New non-residential construction performed less well than expected in 2014. Starting from a lower volume combined with an improving economic framework, non-residential construction is expected to recover again in 2015. Major office projects which will be completed in 2015, helping this market segment. In the public sector projects in the area of health care are also contributing to growth in 2015 while in the coming years growth will mainly result from further investments in the area of industrial buildings.Total non-residential construction is expected to grow by close to 1% in 2015 with an increas-ing trend to 2.2% towards 2018.

4. Civil engineering